Embed Size (px)

Citation preview

REAL ESTATE TAXATION BUSINESS INCOME

FEW IMPORTANT ISUES

Friday

1st February 2013

Hotel J.W.Mariott

IMC & BCAS

Pradip Kapasi & Co. 1

SYNOPSIS Judicial view on Project Completion Method

Relevance of PCM in present times

Tax Accounting Standards

Road Ahead for PCM

Matching concept of Accounting

Finance cost and Treatment in taxation

Few real estate related developments

Development Agreements

Joint Development Agreements – Status & taxation

Character of income

Conversion and Introduction and Dissolution

Redevelopment

Applicability of s. 50C

Real Estate Investments Trust, Venture Capital Fund &Co.

Tax Incentives - s. 10(23FB), 10(47), 35AD and 80IAB2

YEAR OF TAXATION FOR DEVELOPER Bilahari Investment, 299 ITR 1 (SC)

Case of a chit fund

CCM (Project Completion)acceptable in tax laws

Possible for integrated scheme > 12 months

Objective assessment of income of contract

Revenue neutral

New AS not invoked

Method accepted in past

Onus on AO for change in method

Possible to invoke new AS – para 21

Realest Builders Pvt. Ltd. 307 ITR 202(SC)

Pradip Kapasi & Co. 3

RELEVANCE OF PCM IN TAXATION

Accountancy and ICAI - Current status AS 7 Revised 1.04.2003

EAC, The CA Vol.52 pg.232

Exposure Draft AS I – The CA Vol. 54 April, 2005,

Guidance Note 23, 55 The CA, 1764 June 06

Revised Guidance Note, 60 The CA, pg. 1436, March,12

IFRS on Real estate & Investment properties

Material aspects of Guidance Note

IFRS Effect

New S. 145

Tax Accounting Standards , 349 ITR 87(st.)

Pradip Kapasi & Co. 4

TAX ACCOUNTING STANDARDS-TAS

Modification in AS 7 and AS 9

Service transaction only on % of Completion basis

Postpone only for price escalation and export incentives

For recognition of rev. outcome need not be measurable

Contract cost be actually incurred for allowance

No deduction for future losses unless incurred

Recognition of retention money to be recognised

Reversal of rev.only on compliance of s. 36(1)(vii)

Preconstruction income taxable

Recognition only on completion of 25% of work

Pradip Kapasi & Co. 5

ROAD AHEAD IN TAXATION

Prudent and Better view Method for taxation

Time for recognition

Stage for recognition

TAS

Post 1.04.2003 and revised AS 7 Avadhesh Builders, 37 SOT 122 (Mum)

Prestige Estates Projects Ltd., 129 TTJ 680 (Bang)

Pradip Kapasi & Co. 6

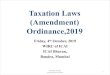

MATCHING CONCEPT OF ACCOUNTANCY

Matching concept Expenditure to match income recognised

Judicial acceptance Calcutta Co. Ltd. 37 ITR 1(SC)

Rajgir Builders, 70 ITD 226 (Mum)

Taparia Tools, 260 ITR 102 (Bom.)

Pradip Kapasi & Co. 7

Section 36(1)(iii)

Analysis Lokhandwala Construction, 260 ITR 579(Bom)

Wallstreet Constructions, 101 ITD 156 (Mum)(SB)

Panchvati Developers, 115 TTJ 139(Mum)

Mangal Tirth Estate Developers(Mad), ITAT India

Thakkar Developers, 115 TTJ 841(Pune)

Effect of Revised AS-7 & New s.145

AS 16 and Borrowing costs

Industry practices

Pradip Kapasi & Co. 8

FINANCE COST & TREATMENT

FEW RELATED DEVELOPMENTS

Advance receipts and stage of certainty National Builders, 137 ITD 277(Ahd.)

Time for applying AS7 Lurgi India,114 ITD 1(Delhi)

TDR proceeds and Project Completion method Pushpa Construction Co., 44A –BCAJ 59(Mum.)

Taxation of retention money- year of receipt

Chandragir Construction Co., 147 TTJ 249 (TM )

Pradip Kapasi & Co. 9

FEW RELATED DEVELOPMENTS

Time sharing arrangements Club Mahindra (Chennai) (SB)

Explanation to s. 37(1) Mehta Enterprises, 135 Taxman 293(Ker.)

Mamta Enterprises, 266 ITR 356(Karn.)

322 ITR 421(Karn.) , 219 Taxation 1(Delhi)

Change from PCM/WIP to CCM Satish H. Patel, 93 TTJ 458 (Pune)

Audit Gopalkishan Builders, 92TTJ 215(Luck.)

Pilot Construction Pvt. Ltd, 44-B, BCAJ 422 (Mum.)

Pradip Kapasi & Co. 10

DEVELOPMENT AGREEMENTS

Typical agreement

Permission – License – Power – Consideration - Sharing

No transfer u/s 2(47) 26 TTD 477 (Del), 70 ITD 9 (Mum),

80 ITD 58 (Cal), 272 ITR 264 (Del)

Transfer – Chatrabhuj Dwarkadas, 260 ITR 491 (Bom)

Date of substantial compliance and possession not relevant

Objectives of s. 2(47(v) and (vi)

Disguised sale - Date of contract relevant

Pradip Kapasi & Co. 11

Pradip Kapasi & Co. 12

DEVELOPMENT AGREEMENTS

Findings in Chaturbhuj Dwarkadas’ case Arrangement conferring privileges of ownership

Passing or transferring complete control

Substantial performance - a non relevant

Payment and permission not relevant factors

Limited POA is significant even an agreement to grant is sufficient

Irrevocable license relevant

Actual possession and irrevocable license not relevant

Disguised agreement for sale

Year of execution of contract is year of transfer

Objective behind introduction of clause(v) of s. 2(47)

Guideline for Income tax Department

DA is not a transfer under general law

Pradip Kapasi & Co. 13

DEVELOPMENT AGREEMENTS

Ingredients of part performance u/s 53A Agreement for transfer of an immovable property

Written instrument for a consideration

Possession – Willingness to perform

Reconsideration of decision

Privileges of o’ship & Passing of comp. control Is ‘License’ a ‘possession’

Future possession and satisfaction u/s. 2(47)(v)

Difference - Agreement for sale & Dev. Agreement

Grant of POA – Limited or general

Subsequent non performance

Finality of subsequent decisions

POSSIBLE ALTERNATIVES

Conversion and contract, 213 CTR 241(Del)

Piecemeal transfer

Partial retention

Pending approvals,13 SOT 82(Mum.)

Willingness to perform, 14 SOT 32(Mum.), 65 DTR 250(Hyd.)

Possession deferred, Pending approvals 14 SOT 63(Mum) , Aug.08 I T Review 32 (Bom.)

12 DTR 1(Delhi), 114 TTJ 246(Bang), 60 DTR 403(Karn.)

Written agreement 301 ITR 124(Mad.), 135 ITD 441(Delhi)

On taking steps for development, 52 SOT 521(Hyd.)

On grant of POA , 131 ITD 71(Agra)(TM)

Pradip Kapasi & Co. 14

JOINT VENTURES TAXATION

Status- AOP or not

Van Ord , 248 ITR 399(AAR)

Geo Consult GmbH, 304 ITR 283(AAR)

Linde AG, 349 ITR 172(AAR)

Alstom, 349 ITR 292(AAR)

Arm’s Length

Landowner and Builder

Mahesh Nemichand Ganeshwade, 73 DTR 1(Pune)

Vijay Productions (P) Ltd., 134 ITD 19(Chennai)

Developer and Builder

Pradip Kapasi & Co. 15

Pradip Kapasi & Co. 16

CONVERSION OF CAPITAL ASSET - S. 45(2) – I

Year of computation of capital gains Law applicable * Rate of tax * 50C value

Set-off of losses * On conversion * Others

End year for Indexation , 55DTR 5(Karn.)

Time for reinvestment Circular No. 560 (18.05.1990) & No. 791( 02.06.2000)

Need for existence of business ‘Of a business carried on ‘

Jeahngir T. Nagree, 23 SOT 512(Mum)

Need for documentation Kamalkant Kasliwal, 97 TTJ 427(Jp.)

Pradip Kapasi & Co. 17

CONVERSION OF CAPITAL ASSET - S. 45(2) II

Event of ‘transfer’ Agreement for flat sale,

Crest Hotels, 75 TTJ 771(Mum)

Power of Attorney,

Wipro Ltd. 34 DTR 493 (Bang.)

Development Agreement

R. Gopinath(HUF), 133 TTJ 595(Chennai)

Triloksingh P.Rajpal, 91 TTJ 322(Mum.)

Introduction in firm or Joint Venture

Nayanaben R. Desai, 124 ITD 387(Ahd.)

Piece meal transfer

Ajay Kumar Shah Jagati, 55ITD 348(Del), 215 CTR 346

Cost of acquiring stock Shirinbai Kooka’ a good law – Book value or FMV

S. 50C Applicability

Pradip Kapasi & Co. 18

INTRODUCTION OF CAPITAL ASSETS s. 45(3) -I

Capital contribution or ‘otherwise’ Payment in kind

Stock-in-trade DLF Universal Ltd.’s case, 123 ITD 1 (Del)(SB) - Analysis

Value recorded in books of account Dharamshi B. Shah, 32 DTR 106 (Ahd) – Revaluation

Applicability of s. 50C, s. 50, s. 56(2)(viia) & s. 92C

Carlton Hotels (P) Ltd. 122 TTJ 515(Luck.) (para 24, 25)

Canora Resources Ltd., 313 ITR 5(AAR)

Pradip Kapasi & Co. 19

INTRODUCTION OF CAPITAL ASSETS s. 45(3) -I I

COA for firm or AOP Where s. 50C applied

Where s. 56(2)(viia) applied – s.49(4)

Where none applied

Cost where stock introduced at a higher value

Period of holding for firm or AOP

Pradip Kapasi & Co. 20

DISTRIBUTION ON DISSOLUTION – s.45(4)

Change in constitution Gurnath Talkies, 226 CTR 474 (Karn)

Kunnankulam Mills Board, 257 ITR 544 (Ker.)

Meaning of ‘or otherwise’ Retirement, A.N. Naik, 265 ITR 346(Bom.)

Withdrawal

Applicability of s.50 & s. 50C & 50B & s.56(2)(vii) Kumbagha Tourist Home, 233 CTR 599 (Kerala)

Malukhan & Party, 84TTJ 31(Jd.) – deduction of cost

AOP or firm – ‘chargeable to tax as income of the firm or AOP’

Kothari Vora Associates, 57 ITD 171 (Pune)

P. N. Devigirikar, 61 ITD 376 (Pune)

Pradip Kapasi & Co. 21

UNCONVENTIONAL MODES

Liquidation and s. 46 , 49 and 55

Company and Shareholders

Society take over

Lease

Membership of society

Slum – Cluster – Parking - Others

22

INCOME FROM HP v. BUSINESS Composite arrangements

Shambhu Inv. Pvt. Ltd., 263 ITR 143 (SC)

Business Service Centres/Shopping malls Royal Business Centre Pvt. Ltd. 39-B BCAJ 24(Mum)

PFH Mall & Retail Management Ltd.112 TTJ 523(Kol)

Marwar Textiles (Agency) Pvt. Ltd., 22 SOT 493(Mum)

Service Apartments

Premises – F & F – Services, 206 CTR 421(All.)

Letting of premises held as stock-in-trade

Period of lease & s. 27, 111 ITD 203(Delhi)

Stamp duty , Regn, Brokerage, Aug.2008 BCAJ 449-M

With security and pesticides Rasiklal & Co. 123 TTJ 279(Mum)

INCOME FROM HP V.BUSINESS

Income from leasing of IT Park

IT Park Ltd, 49 SOT 491 (Bang.)

Narayan Market Complex, 51 SOT 387 (Cuttack)

Income from hospital business

Kenton Leisure Services P. Ltd 135 ITD 10 (Coch.)

Pradip Kapasi & Co. 23

Pradip Kapasi & Co. 24

BUSINESS V. CAPITAL GAINS

Plotting and Infrastructure development

Nature of income

P.M.Mohammed Mira Khan, 73 ITR 735(SC)

Shashikumar Agarwala, 195 ITR 767(All)

Premji Gopalbhai, 113 ITR 785(Guj)

R.V. Gupta, 177 CTR 101(Del.)

G.Venkataswamy Naidu & Co. 35 ITR 594(SC)

Year of accrual

Madanlal Ahuja, 136 ITR 649(All)

Ashaland Corpn,133 ITR 55(Guj)

Estate Investment, 121 ITR 580(Bom)

S. 50C SOME DEVELOPMENTS -I

Scope Tenancy

Kishori S. Gaitonde, 41-B, BCAJ 5321 (Mum)

Tejinder Singh, itatonline.org (Kol.)

Lease Atul G.Puranik, 132 ITD 499(Mum)

Development rights Arif Akhtar Hussain, 140 TTJ 413(Mm)

Chiranjivlal Khanna, 132 ITD 474(Mum)

Stock –in – trade Thiruvengadam Inv., 320 ITR 346 (Mad)

Purchasers Chandni Bhuchar , 323 ITR 510 (P&H)

Right in a flat Yasin Mussa Godi, 18 ITR 253 (Ahd.)(TM )

25Pradip Kapasi & Co.

S. 50C SOME DEVELOPMENTS -II

Chapter XXC & Conveyance Neville D Nooranha, 115 TTJ 390(Kol)

Agreement and conveyance Mr. Sivaparvathi, 129 TTJ 463 (Visakha)

S. 50C and s. 50 Panchiram Nahata, 127 TTJ 128 (Kol)

Mrs. Munira S. Bootwala, ITA No. 7468/M/07 for A.Y.04-05 dt. 01.05.09

United Marine Academy, 130 ITD 113 (SB) (Mum.)

S.54F and s. 50C Gouli Mahadevappa, 128 ITD 503 (Bang.)

Prakash Karnavat, 49 SOT 160 (Jaipur)(Trib.)

Gyan Chand Batra, 133 TTJ 482 (Jp.)

Mohammed Shoib, 29 DTR 306 (Luck.)

26

Pradip Kapasi & Co. 27

REDEVELOPMENT

Redevelopment of Ownership premises in society

Redevelopment of Tenanted premises

Permanent Alternative Accommodation Tenancy

Wagle Process Studio, June, 2003 AIFTP Journal 18

Milan A. Patel, ITA No.2167/M/02 dt.27.12.2002

Tenancy to ownership

J.C.Chandiok, 69 ITD 75(Del),G.D. Thirani, 70 ITD 148(Cal.)

Ownership

Subsequent transfer

Dr. Modi, 218 ITR 1(Karn), Dr. Irani, 234 ITR 850(Bom).

Temporary Alternative Accommodation

Monetary compensation

Corpus Fund

Pradip Kapasi & Co. 28

CAPITAL EXPENDITURE –s. 35AD

Deduction for capital expenditure

Weight @ 150%

Year of expenditure

Business

Affordable Housing

Slum Redevelopment

Star Hotel

Hospital with 100 Beds

Warehousing for Agricultural Produce & Sugar

Cold Chain facility

ICD & CFS

Pradip Kapasi & Co. 29

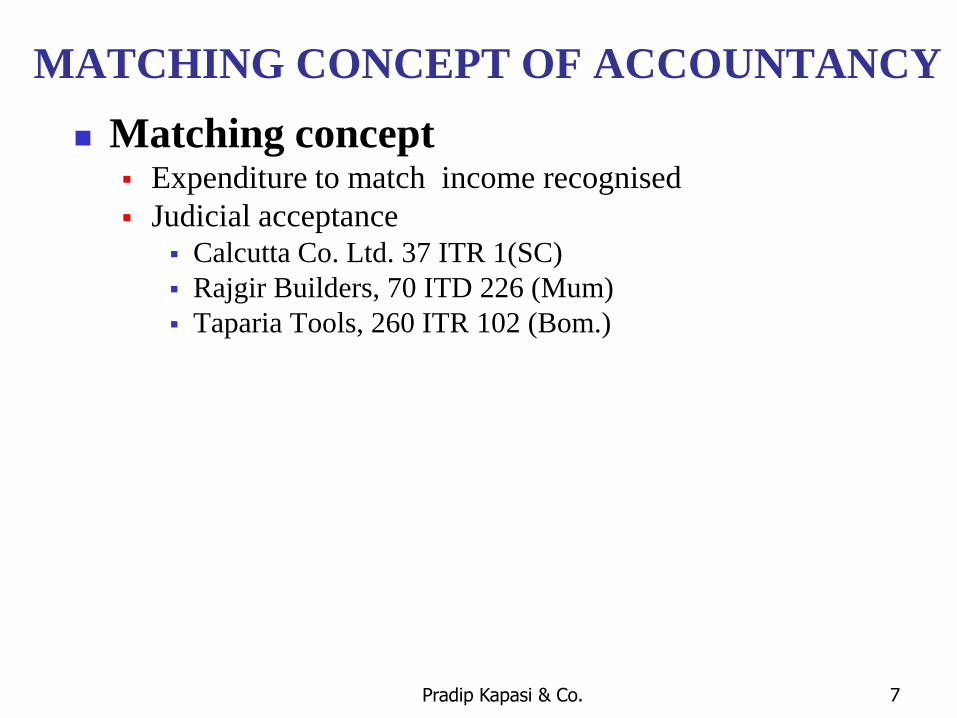

VENTURE CAPITAL – s 10(24FB)

Deduction for capital expenditure

Weight @ 150%

Year of expenditure

Business

Affordable Housing

Slum Redevelopment

Star Hotel

Hospital with 100 Beds

Warehousing for Agricultural Produce & Sugar

Cold Chain facility

ICD & CFS

Pradip Kapasi & Co. 30

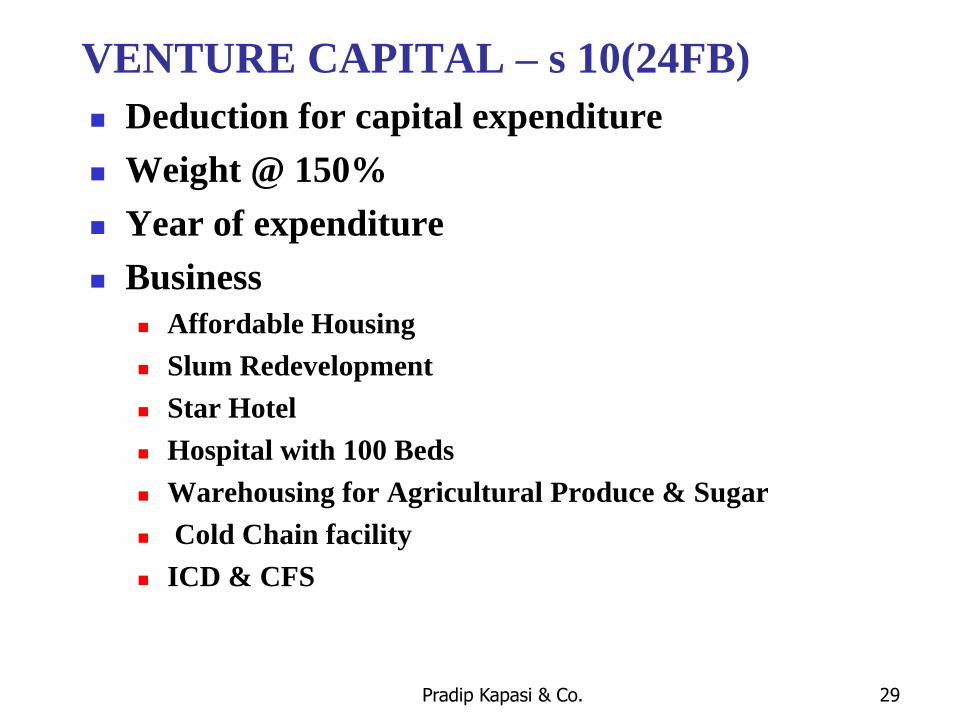

INFRASTRUCTURE DEBT FUND –s. 10(47)

Infrastructure Debt Fund

Investment in Infrastructure

Exemption for Income

Rule 2F

Prescribed Guidelines

Notified by Central Government

Pradip Kapasi & Co. 31

SPECIAL ECONOMIC ZONE –s. 80 IAB

Development of SEZ

Deduction @ 100% for Income

10 consecutive years out of 15 years block

Compliance of prescribed conditions

Pradip Kapasi & Co. 32

HOTEL AT WORLD HERITAGE SITE –s. 80ID

Hotel located in specified district

World Heitage Site

Construction and commencement by 31.03.2013

Deduction for Income @ 100% for 5 years

Compliance of prescribed connditions

Pradip Kapasi & Co. 33

R E INVESTMENTS TRUSTS & FUNDS

Pooling SPVs

Domestic & Offshore

Offshore

FDI and PN 2

Structure selection

Tax efficient offshore jurisdiction

Character of income & DTC

Domestic

VCU , VCC & VCF

PMS

Pass through vehicle

S. 160 to s.167B

THANK YOU

&

GOOD LUCK

Pradip Kapasi & Co. 34