Embed Size (px)

Citation preview

Realizing The Knowledge-Based Economy Through a Comprehensive Policy

Environment

Karel PienaarCEO MTN South Africa

Copyright 2008 © Mobile Telephone Networks. All rights reserved.

Contents

1. Africa is poised to reap the rewards of the Knowledge Economy.

2. What can a knowledge-based economy deliver for Africa?3. Broadband investment is the foundation to enable a

Knowledge Economy.4. The Knowledge Economy Index – Where is Africa today?5. Mobile communications remains the key driver for organic

growth in African ICT markets.6. Mobile industry partnering with governments to bring the

benefits of the African continent’s ICT development goals.7. Competition engineering through licensing does not work.8. Conclusion and recommendations.

2

Copyright 2008 © Mobile Telephone Networks. All rights reserved.

3

The trends suggest that Africa is poised to reap the rewards of the Knowledge Economy

Trend 1: A larger, younger and more affluent population

Trend 2: Africa’s urbanising population

Trend 3: Africa is leapfrogging through technology

Trend 4: Africa’s commodity wealth

Trend 5: Africa’s expansion of its financial sector

Afr

ican

Gro

wth

Driven by key trends

Source: Freemantle, SBSA

Copyright 2008 © Mobile Telephone Networks. All rights reserved.

4

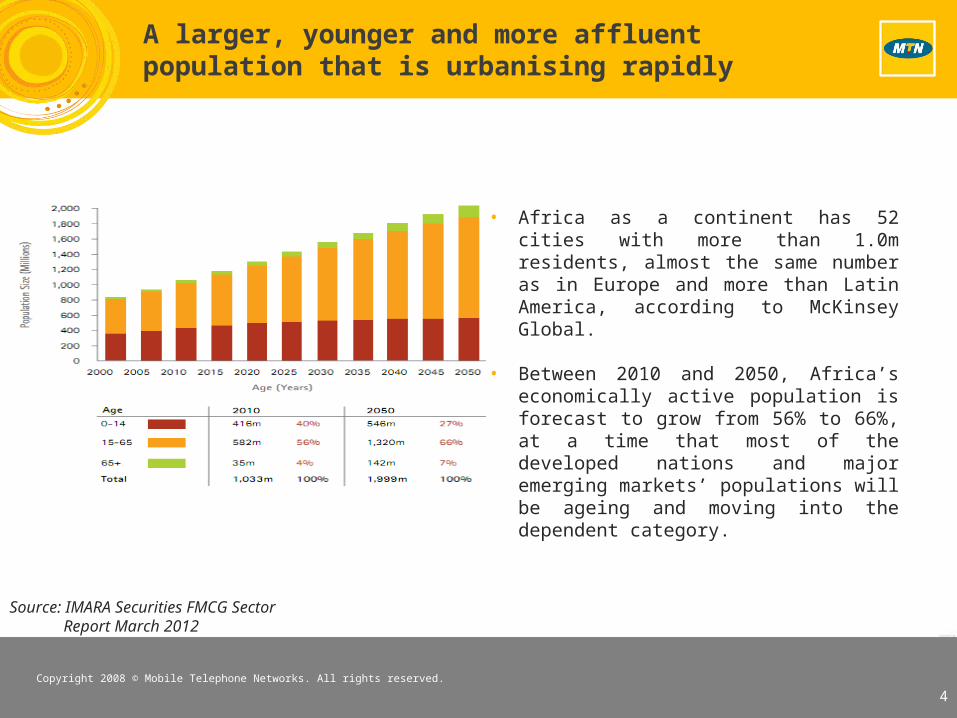

A larger, younger and more affluent population that is urbanising rapidly

Afr

ican

Gro

wth

Source: IMARA Securities FMCG Sector Report March 2012

• Africa as a continent has 52 cities with more than 1.0m residents, almost the same number as in Europe and more than Latin America, according to McKinsey Global.

• Between 2010 and 2050, Africa’s economically active population is forecast to grow from 56% to 66%, at a time that most of the developed nations and major emerging markets’ populations will be ageing and moving into the dependent category.

Copyright 2008 © Mobile Telephone Networks. All rights reserved.

5

Africa’s commodity wealth is further enhanced by becoming a player in the world’s energy markets

Africa’s share of world commodities

Copper production growth, 2006 − 2010

Proved oil reserves as at 2011, bn barrels

Africa had 9.5% of world’s crude oil and

8% of the world’s natural gas reserves at

the end of 2011

Source: SBSA, Africa Macro Insight & Strategy

Copyright 2008 © Mobile Telephone Networks. All rights reserved.

6

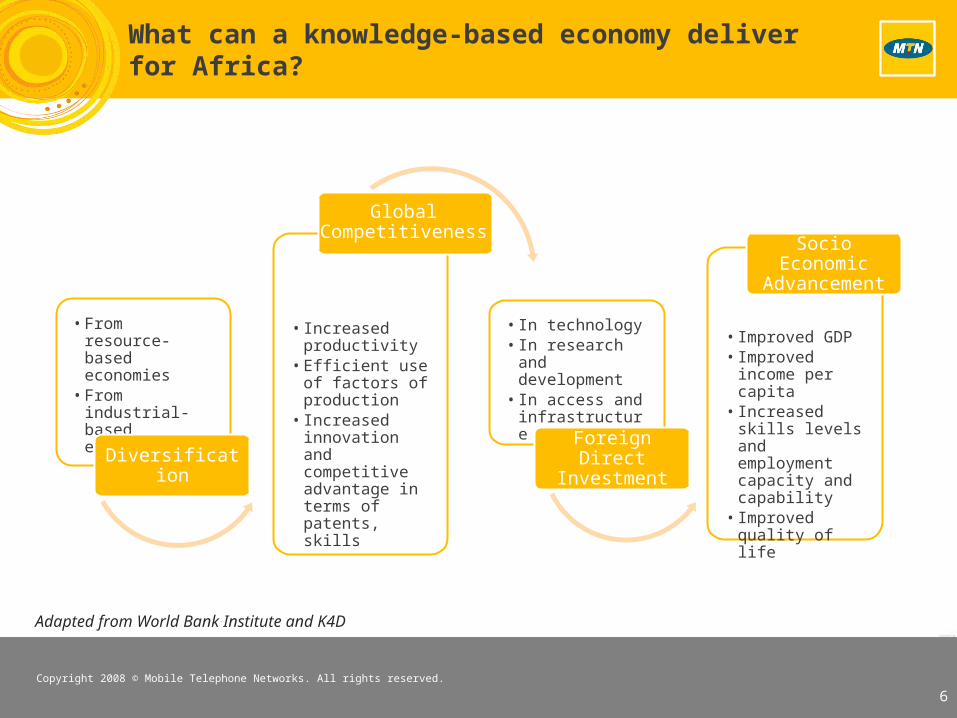

What can a knowledge-based economy deliver for Africa?

• From resource-based economies

• From industrial-based economies

Diversification

• Increased productivity

• Efficient use of factors of production

• Increased innovation and competitive advantage in terms of patents, skills

Global Competitiveness

• In technology• In research and

development• In access and

infrastructure

Foreign Direct Investment

• Improved GDP• Improved

income per capita

• Increased skills levels and employment capacity and capability

• Improved quality of life

Socio Economic

Advancement

Adapted from World Bank Institute and K4D

Copyright 2008 © Mobile Telephone Networks. All rights reserved.

7

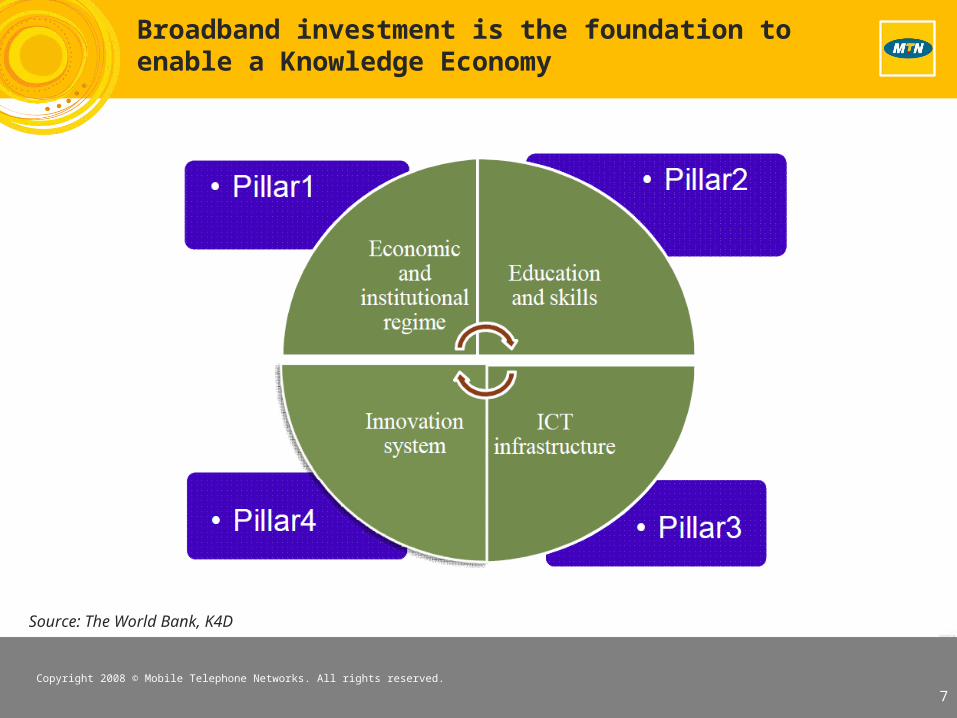

Broadband investment is the foundation to enable a Knowledge Economy

Source: The World Bank, K4D

Copyright 2008 © Mobile Telephone Networks. All rights reserved.

8

Broadband Internet users and traffic – How do we light up the

African continent?

Copyright 2008 © Mobile Telephone Networks. All rights reserved.

9

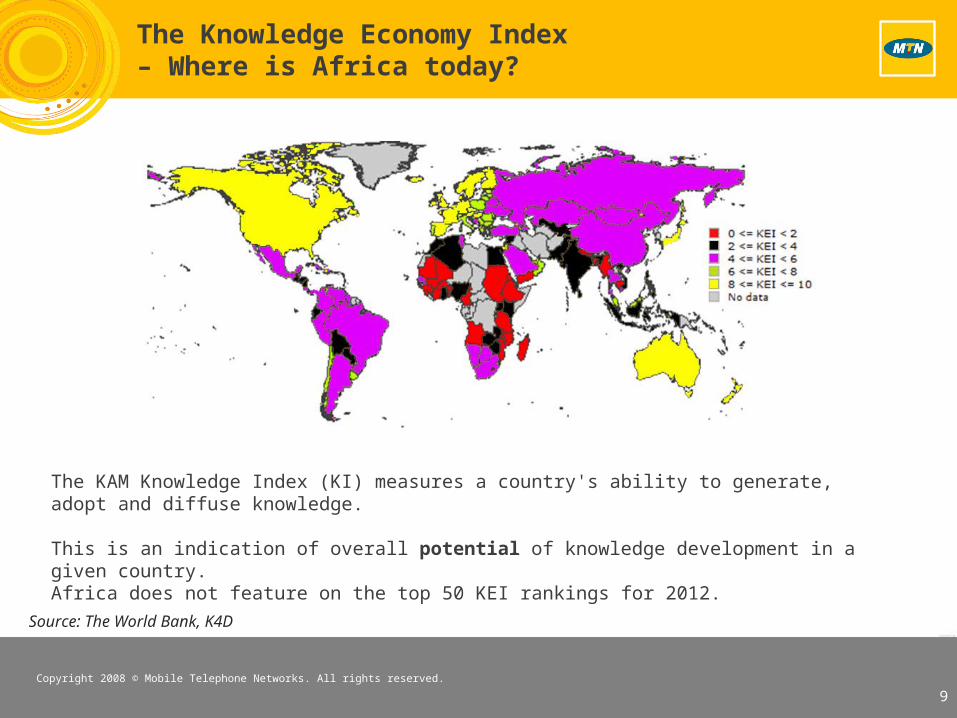

The Knowledge Economy Index – Where is Africa today?

The KAM Knowledge Index (KI) measures a country's ability to generate, adopt and diffuse knowledge.

This is an indication of overall potential of knowledge development in a given country.Africa does not feature on the top 50 KEI rankings for 2012.

Source: The World Bank, K4D

Copyright 2008 © Mobile Telephone Networks. All rights reserved.

10

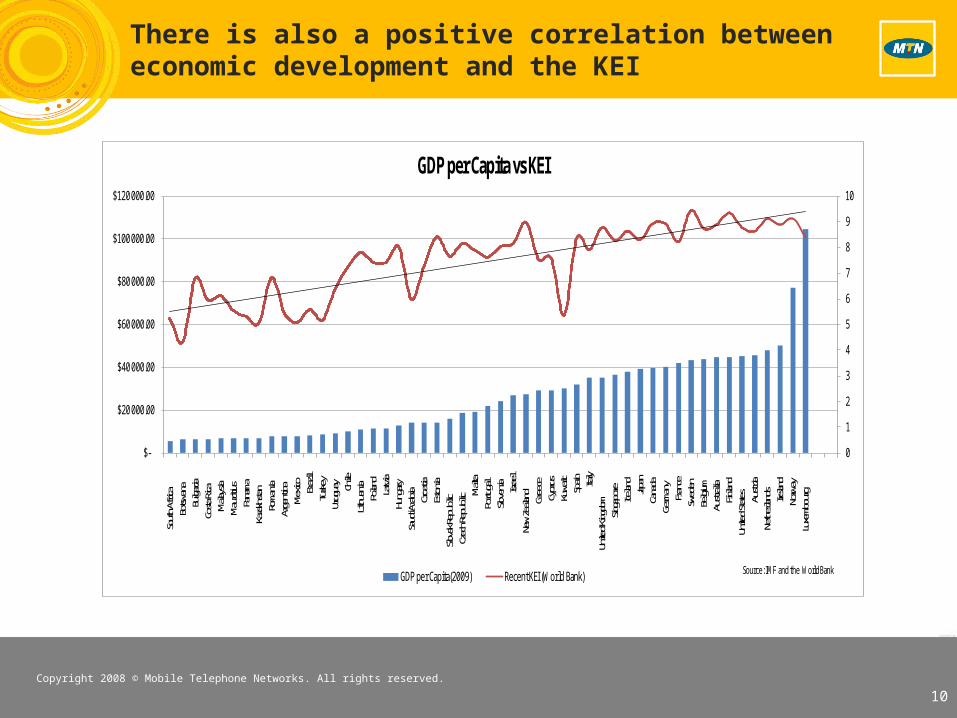

There is also a positive correlation between economic development and the KEI

0

1

2

3

4

5

6

7

8

9

10

$-

$20 000.00

$40 000.00

$60 000.00

$80 000.00

$100 000.00

$120 000.00

South

Afric

aBo

tswan

aBu

lgaria

Costa

Rica

Malay

siaMa

uritiu

sPa

nama

Kazak

hstan

Roma

niaAr

genti

naMe

xico

Brazil

Turke

yUr

ugua

y Chile

Lithu

ania

Polan

dLat

viaHu

ngary

Saudi

Arab

iaCro

atia

Eston

iaSlo

vak Re

publi

cCze

ch Re

publi

c Malta

Portu

galSlo

venia Isr

ael

New Z

ealan

dGr

eece

Cypru

sKu

wait

Spain Ita

lyUn

ited K

ingdo

mSin

gapore Icelan

dJap

anCa

nada

Germ

any

Franc

eSw

eden

Belgiu

mAu

stralia

Finlan

dUn

ited S

tates Au

stria

Nethe

rland

sIre

land

Norw

ayLu

xemb

ourg

GDP per Capita vs KEI

GDP per Capita(2009) Recent KEI (World Bank) Source: IMF and the World Bank

Copyright 2008 © Mobile Telephone Networks. All rights reserved.

11

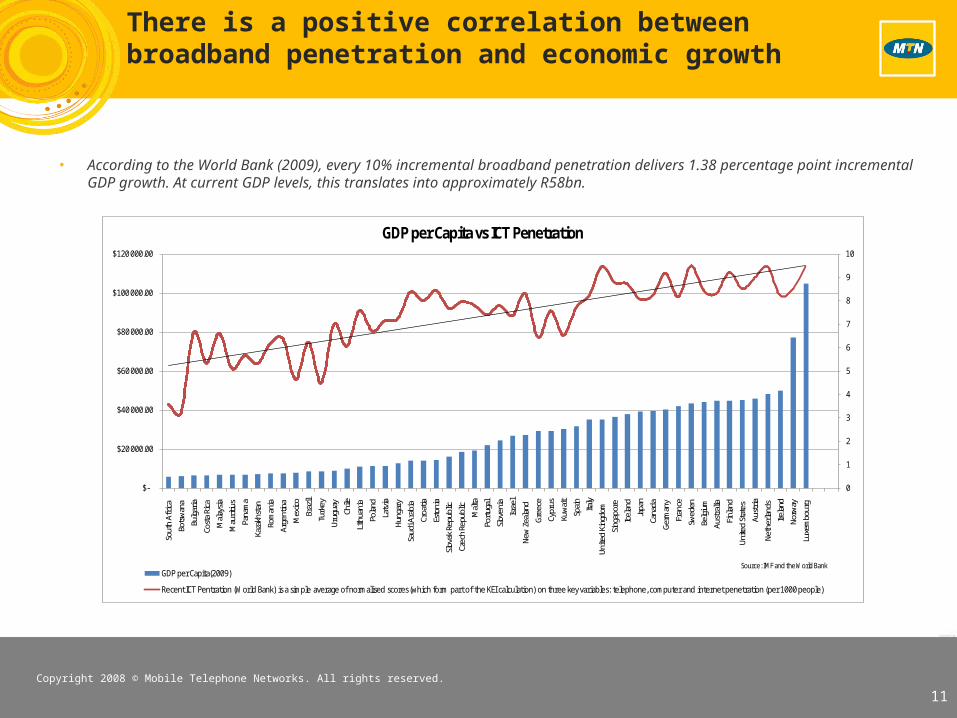

There is a positive correlation between broadband penetration and economic growth

0

1

2

3

4

5

6

7

8

9

10

$-

$20 000.00

$40 000.00

$60 000.00

$80 000.00

$100 000.00

$120 000.00

Sout

h Af

rica

Bots

wan

aBu

lgar

iaCo

sta

Rica

Mal

aysia

Mau

ritius

Pana

ma

Kaza

khst

anRo

man

iaAr

genti

naM

exic

oBr

azil

Turk

eyUr

ugua

yCh

ileLi

thua

nia

Pola

ndLa

tvia

Hung

ary

Saud

i Ara

bia

Croa

tiaEs

toni

aSl

ovak

Rep

ublic

Czec

h Re

publ

icM

alta

Port

ugal

Slov

enia

Israe

lNe

w Z

eala

ndGr

eece

Cypr

usKu

wai

tSp

ain

Italy

Unite

d Ki

ngdo

mSi

ngap

ore

Icel

and

Japa

nCa

nada

Germ

any

Fran

ceSw

eden

Belg

ium

Aust

ralia

Finl

and

Unite

d St

ates

Aust

riaNe

ther

land

sIre

land

Norw

ayLu

xem

bour

g

GDP per Capita vs ICT Penetration

GDP per Capita(2009)

Recent ICT Pentration (World Bank) is a simple average of normalised scores (which form part of the KEI calculation) on three key variables: telephone, computer and internet penetration (per 1000 people)

Source: IMF and the World Bank

• According to the World Bank (2009), every 10% incremental broadband penetration delivers 1.38 percentage point incremental GDP growth. At current GDP levels, this translates into approximately R58bn.

Copyright 2008 © Mobile Telephone Networks. All rights reserved.

12

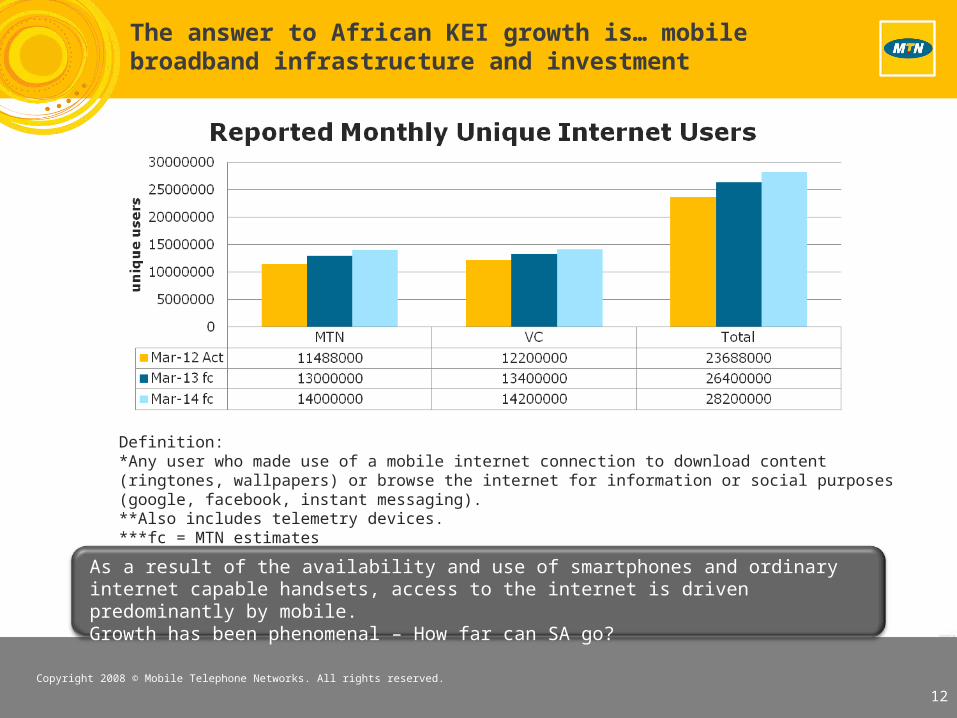

The answer to African KEI growth is… mobile broadband infrastructure and investment

As a result of the availability and use of smartphones and ordinary internet capable handsets, access to the internet is driven predominantly by mobile. Growth has been phenomenal – How far can SA go?

Definition:*Any user who made use of a mobile internet connection to download content (ringtones, wallpapers) or browse the internet for information or social purposes (google, facebook, instant messaging). **Also includes telemetry devices.***fc = MTN estimates

Copyright 2008 © Mobile Telephone Networks. All rights reserved.

13

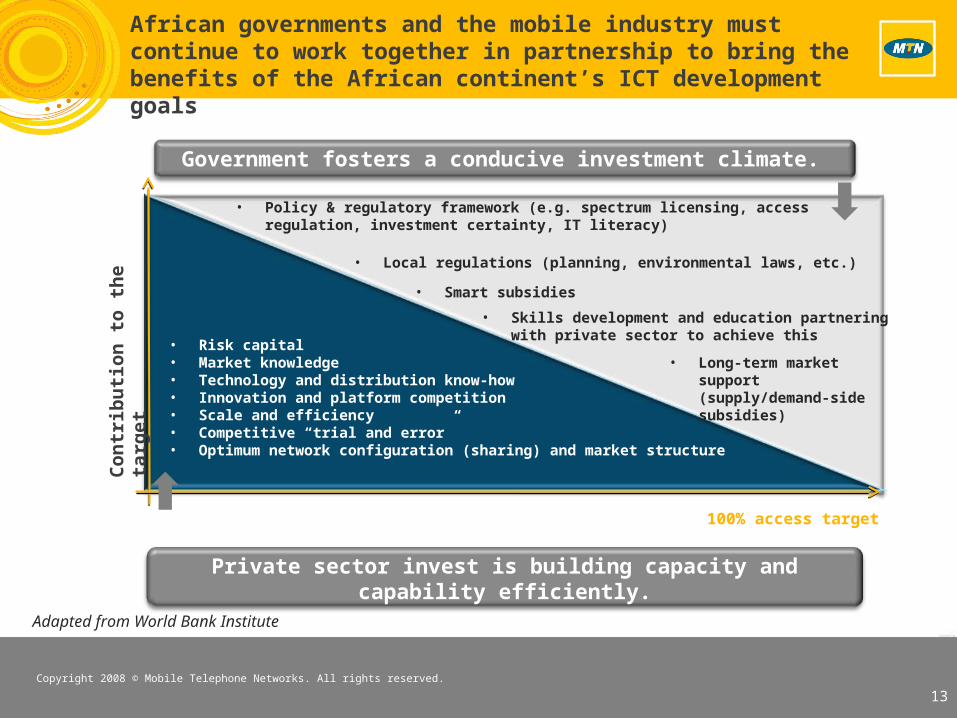

African governments and the mobile industry must continue to work together in partnership to bring the benefits of the African continent’s ICT development goals

Private sector invest is building capacity and capability efficiently.

• Risk capital• Market knowledge • Technology and distribution know-how• Innovation and platform competition• Scale and efficiency • Competitive “trial and error”• Optimum network configuration (sharing) and market structure

100% access target

• Local regulations (planning, environmental laws, etc.)

Con

trib

uti

on

to t

he t

arg

et

• Smart subsidies

• Long-term market support (supply/demand-side subsidies)

• Policy & regulatory framework (e.g. spectrum licensing, access regulation, investment certainty, IT literacy)

Government fosters a conducive investment climate.

• Skills development and education partnering with private sector to achieve this

Adapted from World Bank Institute

Copyright 2008 © Mobile Telephone Networks. All rights reserved.

14

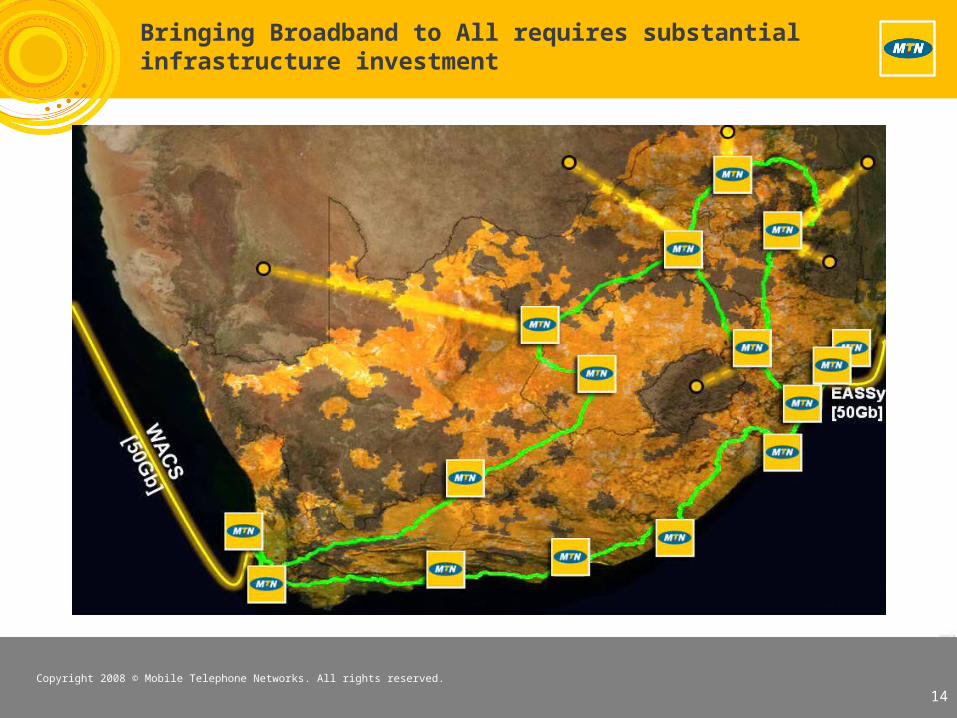

Bringing Broadband to All requires substantial infrastructure investment

Private sector invest is building capacity and capability efficiently.

• Risk capital• Market knowledge • Technology and distribution know-how• Innovation and platform competition• Scale and efficiency • Competitive “trial and error”• Optimum network configuration (sharing) and market structure

Copyright 2008 © Mobile Telephone Networks. All rights reserved.

15

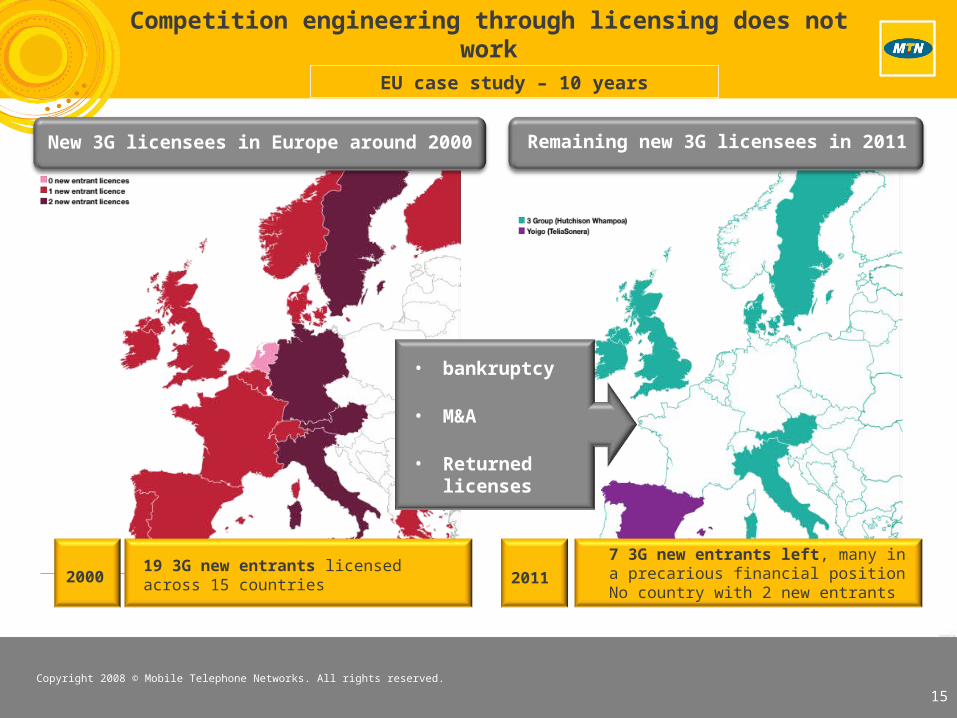

Competition engineering through licensing does not work

Private sector invest is building capacity and capability efficiently.

2000 19 3G new entrants licensed across 15 countries 2011

7 3G new entrants left, many in a precarious financial position No country with 2 new entrants

Remaining new 3G licensees in 2011

• bankruptcy

• M&A

• Returned licenses

New 3G licensees in Europe around 2000

EU case study – 10 years

Copyright 2008 © Mobile Telephone Networks. All rights reserved.

16

Use the USO funds but USO needs to be “smarter”

Private sector invest is building capacity and capability efficiently.

• Poor global track record of USO funds:• No fund has been capable of

distributing more than 2% of sector revenue.

• Government can play a significant role in releasing funds to subsidise roll-out of fibre in rural areas through SOEs where commercial incentive is lacking.

• Learn from past South African experience, e.g. UALs.

Performance of 15 developing countries USFs.

Source:Intelecon

Copyright 2008 © Mobile Telephone Networks. All rights reserved.

17

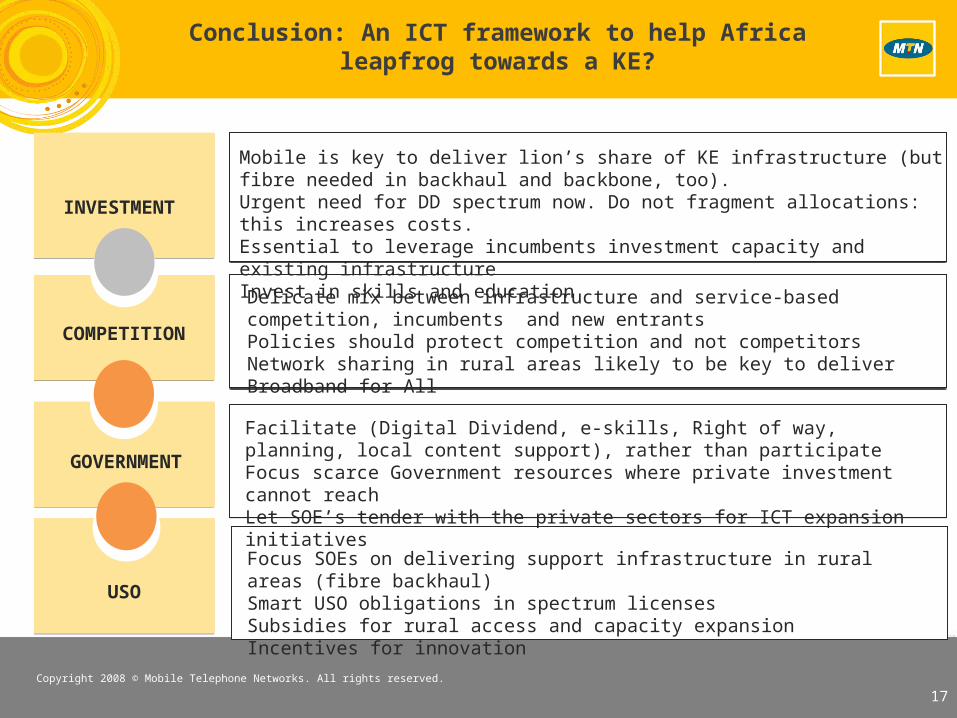

Conclusion: An ICT framework to help Africa leapfrog towards a KE?

Mobile is key to deliver lion’s share of KE infrastructure (but fibre needed in backhaul and backbone, too).Urgent need for DD spectrum now. Do not fragment allocations: this increases costs.Essential to leverage incumbents investment capacity and existing infrastructure Invest in skills and education

Delicate mix between infrastructure and service-based competition, incumbents and new entrantsPolicies should protect competition and not competitorsNetwork sharing in rural areas likely to be key to deliver Broadband for All

Facilitate (Digital Dividend, e-skills, Right of way, planning, local content support), rather than participateFocus scarce Government resources where private investment cannot reach Let SOE’s tender with the private sectors for ICT expansion initiatives

INVESTMENT

COMPETITION

GOVERNMENT

USO

Focus SOEs on delivering support infrastructure in rural areas (fibre backhaul)Smart USO obligations in spectrum licensesSubsidies for rural access and capacity expansionIncentives for innovation

Copyright 2008 © Mobile Telephone Networks. All rights reserved.

Thank you

18