Embed Size (px)

Citation preview

Recent Developments and Outlook for the Mexican Economy

April 19, 2016

Credit Suisse, 2016 Macro Conference

Outline

Recent Developments and Outlook for the Mexican Economy

2

Final Remarks3

Inflation and Monetary Policy1

2Recent Developments and Outlook for the Mexican Economy

3

In line with its constitutional mandate, the monetary policy conducted by Banco de Méxicoaims at procuring the stability of the national currency’s purchasing power, at the lowest costto society in terms of economic activity.

Thus, an environment of low and stable inflation in Mexico has been achieved:

In 2015 headline inflation closed at 2.13 percent.

Banco de México expects inflation to close 2016 around the 3 percent permanent target.

During 2016 inflation rebounded due to transitory factors, staying at levels below 3 percent.

Recent Developments and Outlook for the Mexican Economy

To achieve this, the monetary policy conducted by Banco de México has been fundamental.Banco de México has set its monetary policy rate to achieve its permanent target.

1

2

3

4

5

6

7

8

9

10

11

12

13

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

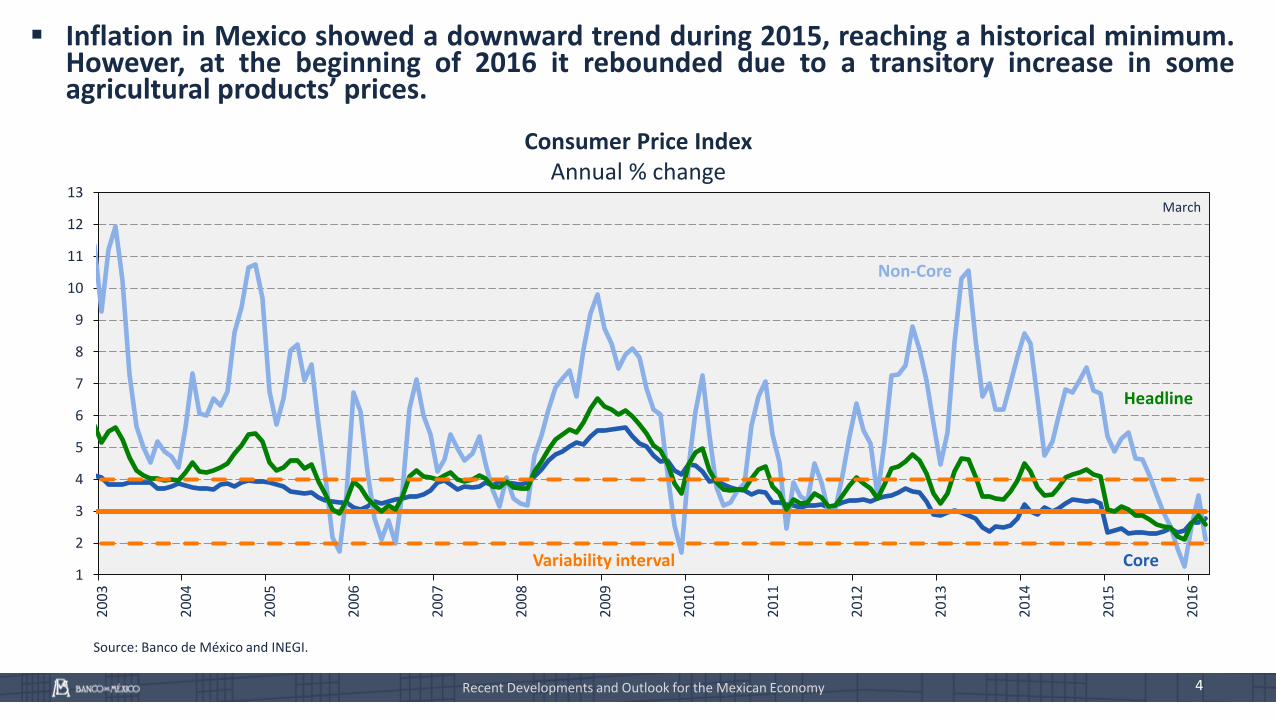

Inflation in Mexico showed a downward trend during 2015, reaching a historical minimum.However, at the beginning of 2016 it rebounded due to a transitory increase in someagricultural products’ prices.

Consumer Price IndexAnnual % change

Source: Banco de México and INEGI.

Headline

CoreVariability interval

Non-Core

4

March

Recent Developments and Outlook for the Mexican Economy

5

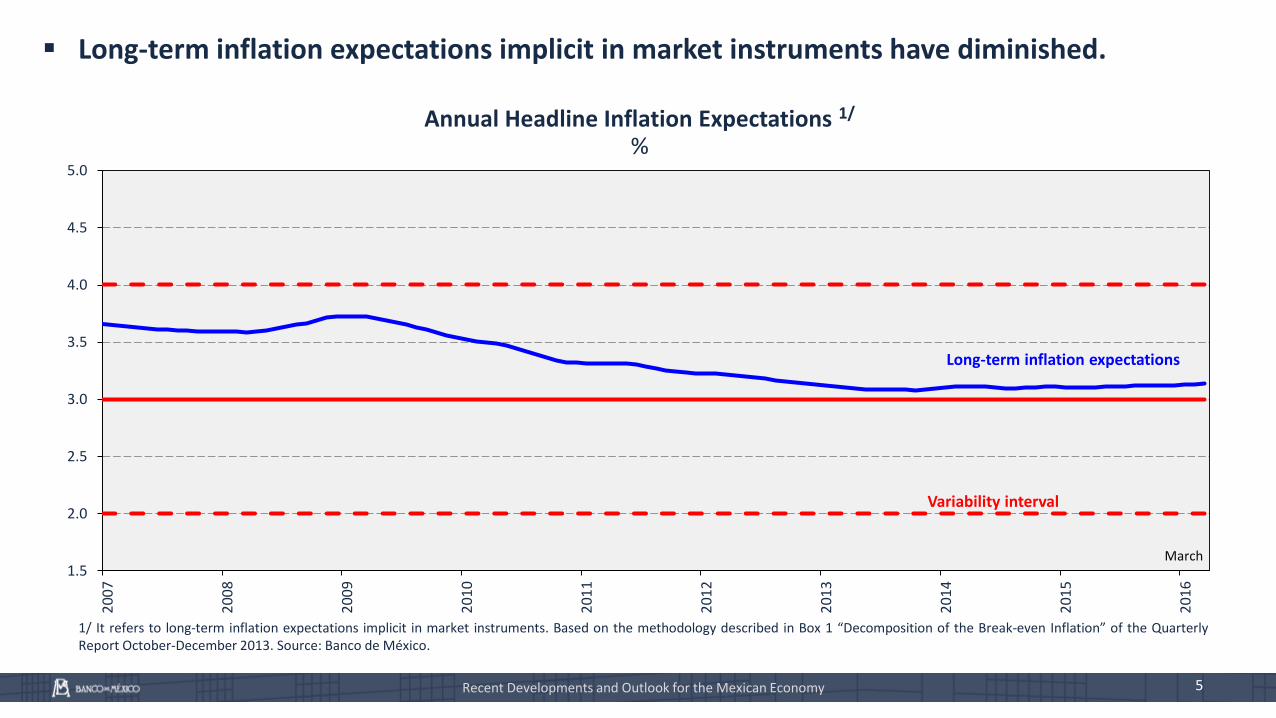

Long-term inflation expectations implicit in market instruments have diminished.

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Annual Headline Inflation Expectations 1/

%

1/ It refers to long-term inflation expectations implicit in market instruments. Based on the methodology described in Box 1 “Decomposition of the Break-even Inflation” of the QuarterlyReport October-December 2013. Source: Banco de México.

March

Variability interval

Recent Developments and Outlook for the Mexican Economy

Long-term inflation expectations

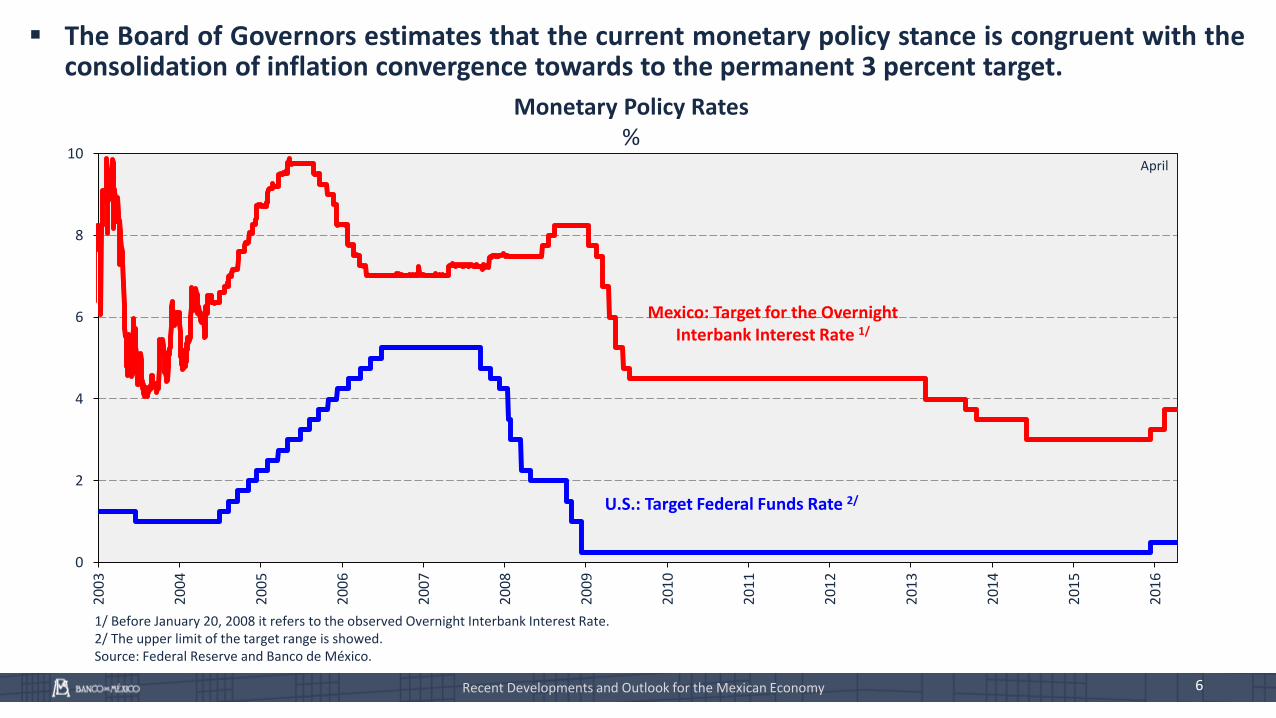

The Board of Governors estimates that the current monetary policy stance is congruent with theconsolidation of inflation convergence towards to the permanent 3 percent target.

Monetary Policy Rates%

1/ Before January 20, 2008 it refers to the observed Overnight Interbank Interest Rate.2/ The upper limit of the target range is showed.Source: Federal Reserve and Banco de México.

0

2

4

6

8

10

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

U.S.: Target Federal Funds Rate 2/

Mexico: Target for the Overnight Interbank Interest Rate 1/

April

6Recent Developments and Outlook for the Mexican Economy

Outline

Recent Developments and Outlook for the Mexican Economy

2

Final Remarks3

Inflation and Monetary Policy1

7Recent Developments and Outlook for the Mexican Economy

60

70

80

90

100

110

120

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Recent Developments and Outlook for the Mexican Economy 8

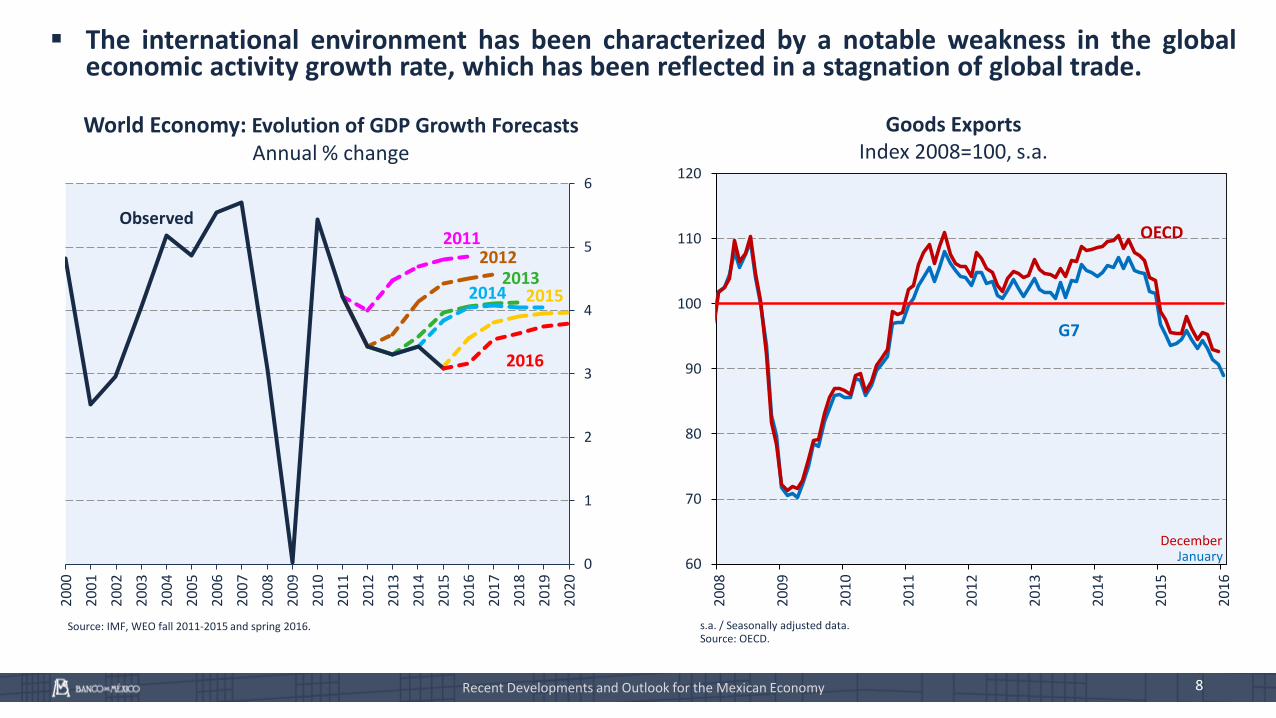

The international environment has been characterized by a notable weakness in the globaleconomic activity growth rate, which has been reflected in a stagnation of global trade.

World Economy: Evolution of GDP Growth ForecastsAnnual % change

Goods ExportsIndex 2008=100, s.a.

Source: IMF, WEO fall 2011-2015 and spring 2016. s.a. / Seasonally adjusted data.Source: OECD.

G7

January

OECD

December

0

1

2

3

4

5

6

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

2015

Observed

20132014

20122011

2016

15

30

45

60

75

90

105

120

135

150

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

Mexican Oil Mix

WTI

Futures 1/

9

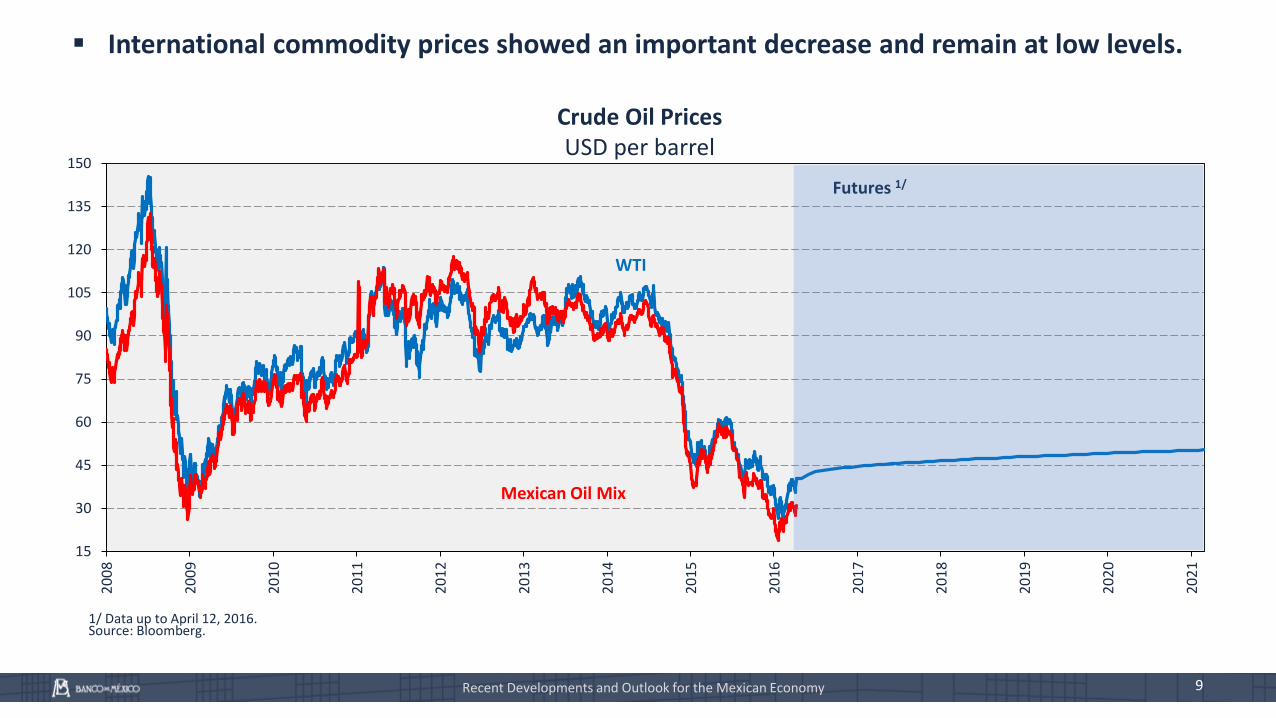

International commodity prices showed an important decrease and remain at low levels.

Crude Oil PricesUSD per barrel

1/ Data up to April 12, 2016.Source: Bloomberg.

Recent Developments and Outlook for the Mexican Economy

-20

-15

-10

-5

0

5

10

15

20

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Mexico

U.S.

2.7

1.9

0.5

0.1

1.9

1.1

3.0

3.8

-0.9

4.6

5.0

2.1

0.6

3.9

2.0

1.4

2.0

2.4

2.4

2.4

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

I 201

2

III 2

012

I 201

3

III 2

013

I 201

4

III 2

014

I 201

5

III 2

015

I 201

6

III 2

016

Recent Developments and Outlook for the Mexican Economy 10

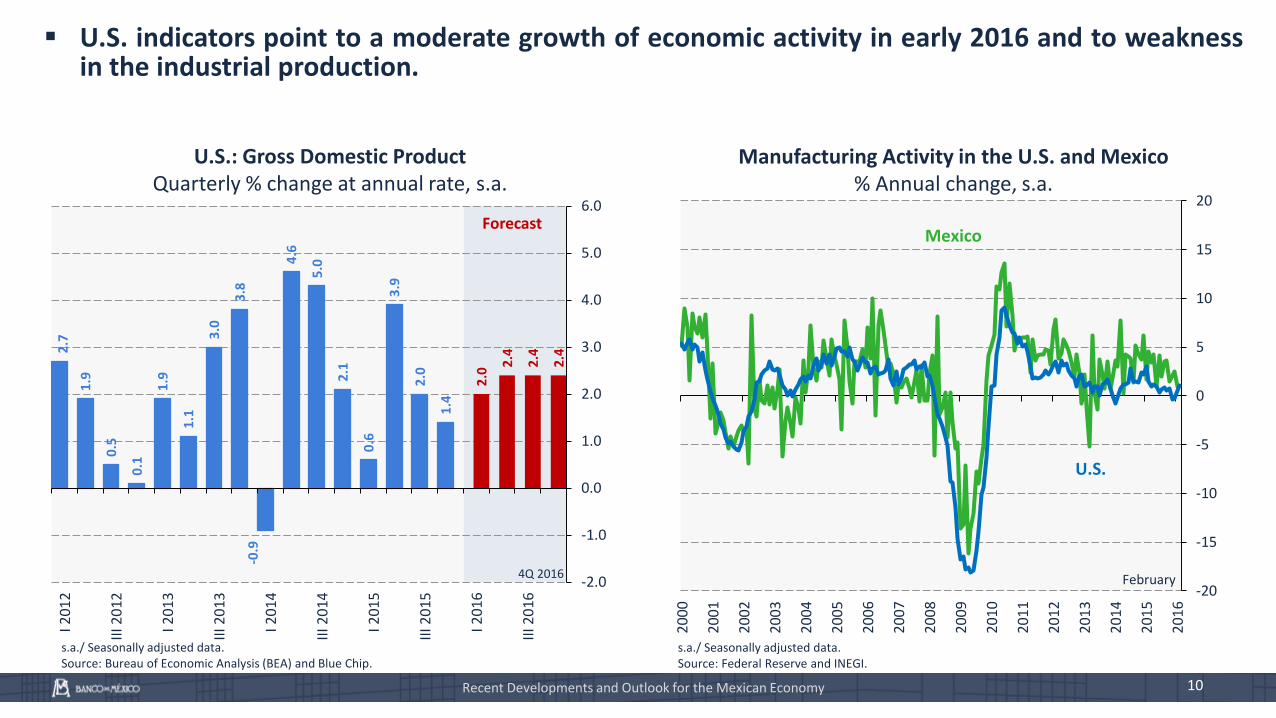

U.S. indicators point to a moderate growth of economic activity in early 2016 and to weaknessin the industrial production.

U.S.: Gross Domestic ProductQuarterly % change at annual rate, s.a.

Manufacturing Activity in the U.S. and Mexico % Annual change, s.a.

s.a./ Seasonally adjusted data.Source: Bureau of Economic Analysis (BEA) and Blue Chip.

s.a./ Seasonally adjusted data.Source: Federal Reserve and INEGI.

4Q 2016 February

Forecast

Recent Developments and Outlook for the Mexican Economy 11

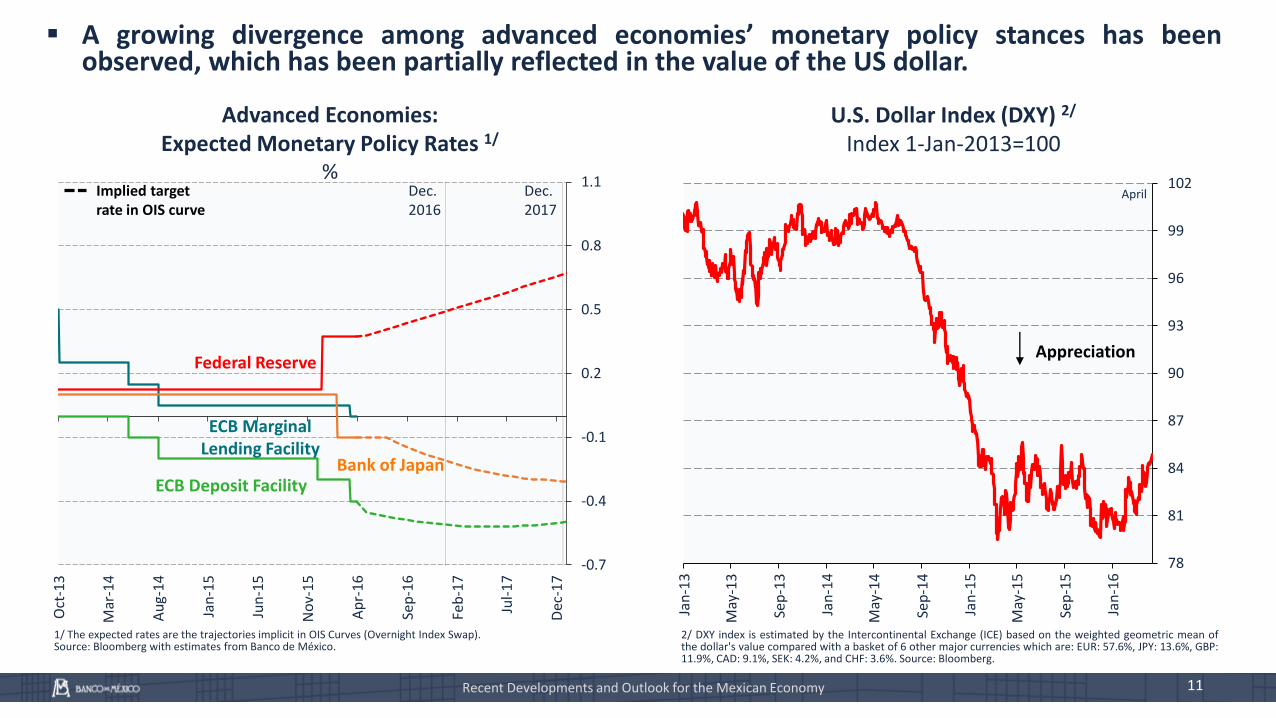

A growing divergence among advanced economies’ monetary policy stances has beenobserved, which has been partially reflected in the value of the US dollar.

-0.7

-0.4

-0.1

0.2

0.5

0.8

1.1

Oct

-13

Mar

-14

Au

g-1

4

Jan

-15

Jun

-15

No

v-1

5

Ap

r-1

6

Sep

-16

Feb

-17

Jul-

17

Dec

-17

Advanced Economies: Expected Monetary Policy Rates 1/

%

U.S. Dollar Index (DXY) 2/

Index 1-Jan-2013=100

1/ The expected rates are the trajectories implicit in OIS Curves (Overnight Index Swap).Source: Bloomberg with estimates from Banco de México.

2/ DXY index is estimated by the Intercontinental Exchange (ICE) based on the weighted geometric mean ofthe dollar's value compared with a basket of 6 other major currencies which are: EUR: 57.6%, JPY: 13.6%, GBP:11.9%, CAD: 9.1%, SEK: 4.2%, and CHF: 3.6%. Source: Bloomberg.

78

81

84

87

90

93

96

99

102

Jan

-13

May

-13

Sep

-13

Jan

-14

May

-14

Sep

-14

Jan

-15

May

-15

Sep

-15

Jan

-16

April

Appreciation

Dec. 2016

Dec. 2017

Implied target rate in OIS curve

Federal Reserve

ECB Deposit Facility

ECB Marginal Lending Facility

Bank of Japan

Recent Developments and Outlook for the Mexican Economy 12

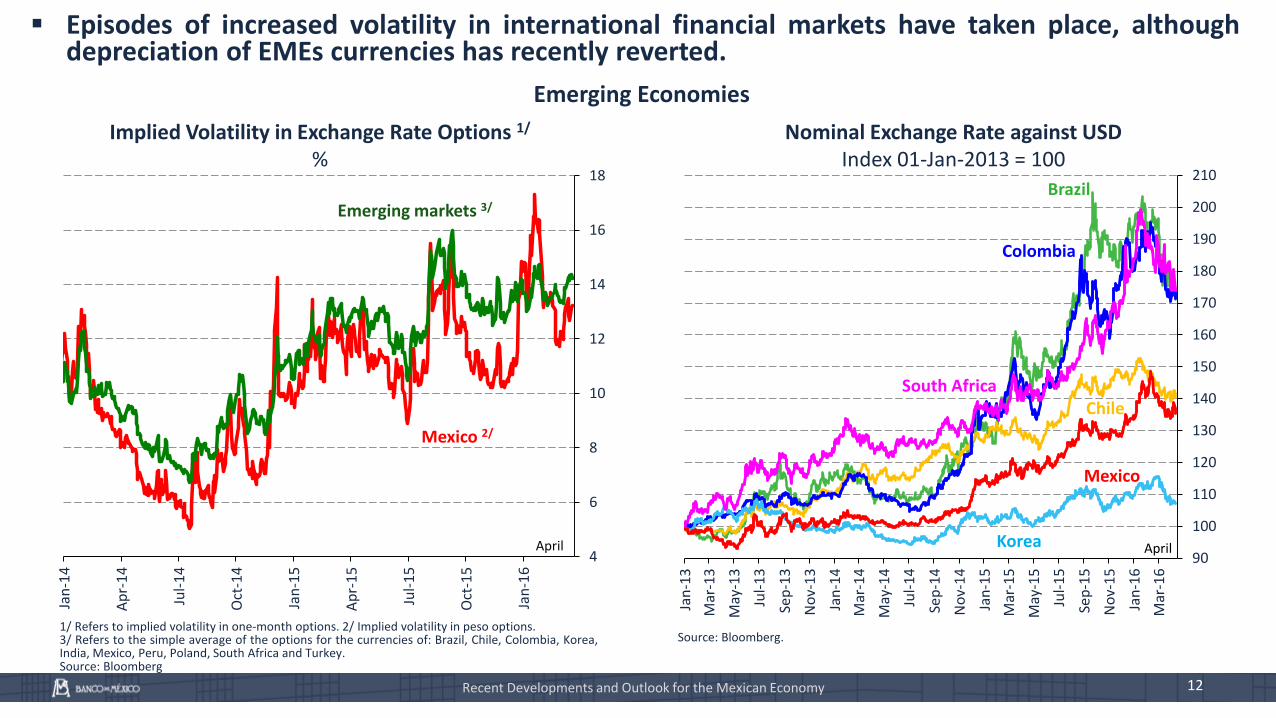

Episodes of increased volatility in international financial markets have taken place, althoughdepreciation of EMEs currencies has recently reverted.

Emerging Economies

4

6

8

10

12

14

16

18

Jan

-14

Ap

r-1

4

Jul-

14

Oct

-14

Jan

-15

Ap

r-1

5

Jul-

15

Oct

-15

Jan

-16

Implied Volatility in Exchange Rate Options 1/

%

1/ Refers to implied volatility in one-month options. 2/ Implied volatility in peso options.3/ Refers to the simple average of the options for the currencies of: Brazil, Chile, Colombia, Korea,India, Mexico, Peru, Poland, South Africa and Turkey.Source: Bloomberg

Emerging markets 3/

Mexico 2/

April90

100

110

120

130

140

150

160

170

180

190

200

210

Jan

-13

Mar

-13

May

-13

Jul-

13

Sep

-13

No

v-1

3

Jan

-14

Mar

-14

May

-14

Jul-

14

Sep

-14

No

v-1

4

Jan

-15

Mar

-15

May

-15

Jul-

15

Sep

-15

No

v-1

5

Jan

-16

Mar

-16

Nominal Exchange Rate against USDIndex 01-Jan-2013 = 100

Source: Bloomberg.

Korea

Chile

Colombia

South Africa

Brazil

Mexico

April

13

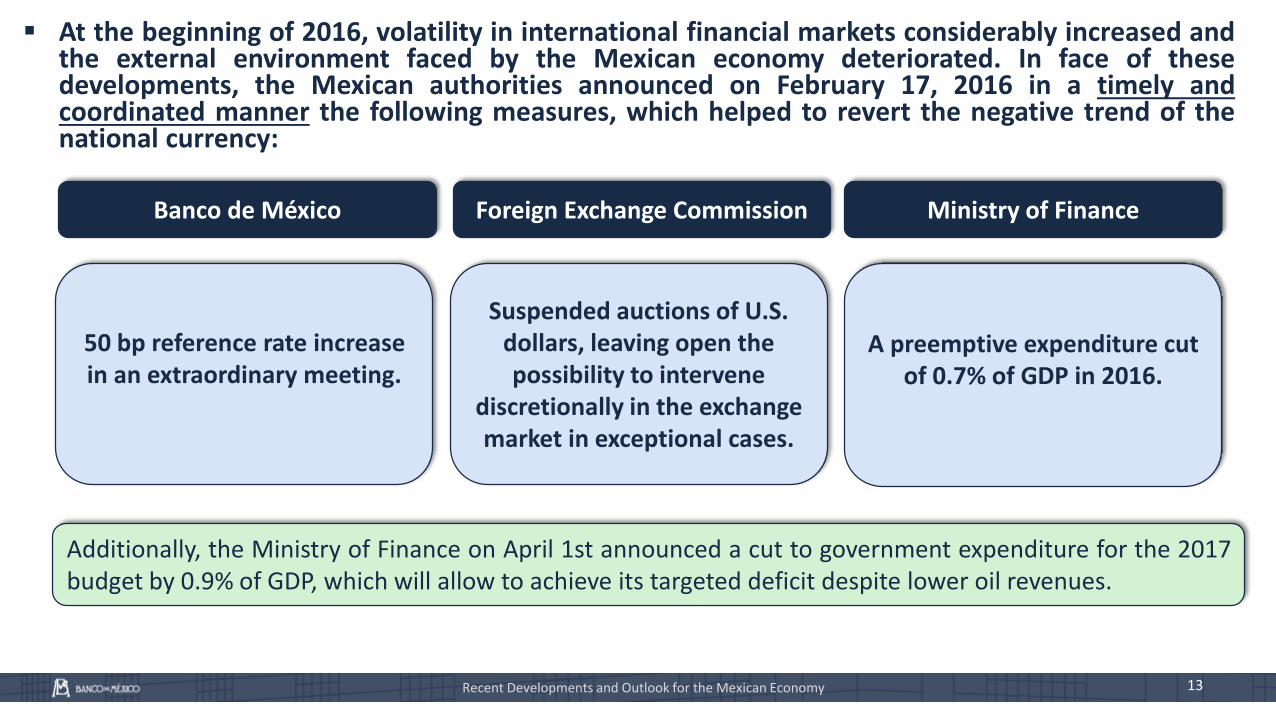

At the beginning of 2016, volatility in international financial markets considerably increased andthe external environment faced by the Mexican economy deteriorated. In face of thesedevelopments, the Mexican authorities announced on February 17, 2016 in a timely andcoordinated manner the following measures, which helped to revert the negative trend of thenational currency:

Recent Developments and Outlook for the Mexican Economy

Banco de México

50 bp reference rate increase in an extraordinary meeting.

Foreign Exchange Commission

Suspended auctions of U.S. dollars, leaving open the possibility to intervene

discretionally in the exchange market in exceptional cases.

A preemptive expenditure cut of 0.7% of GDP in 2016.

Ministry of Finance

Additionally, the Ministry of Finance on April 1st announced a cut to government expenditure for the 2017budget by 0.9% of GDP, which will allow to achieve its targeted deficit despite lower oil revenues.

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

-300

-200

-100

0

100

200

300

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

32

.3 34

.5 35

.6

32

.8

31

.5

29

.8

29

.1

33

.2

36

.2

36

.2 37

.5

37

.7 40

.4 43

.2

47

.6

48

.6

48

.3

47

.9

47

.5

47

.1

46

.80

10

20

30

40

50

60

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

14

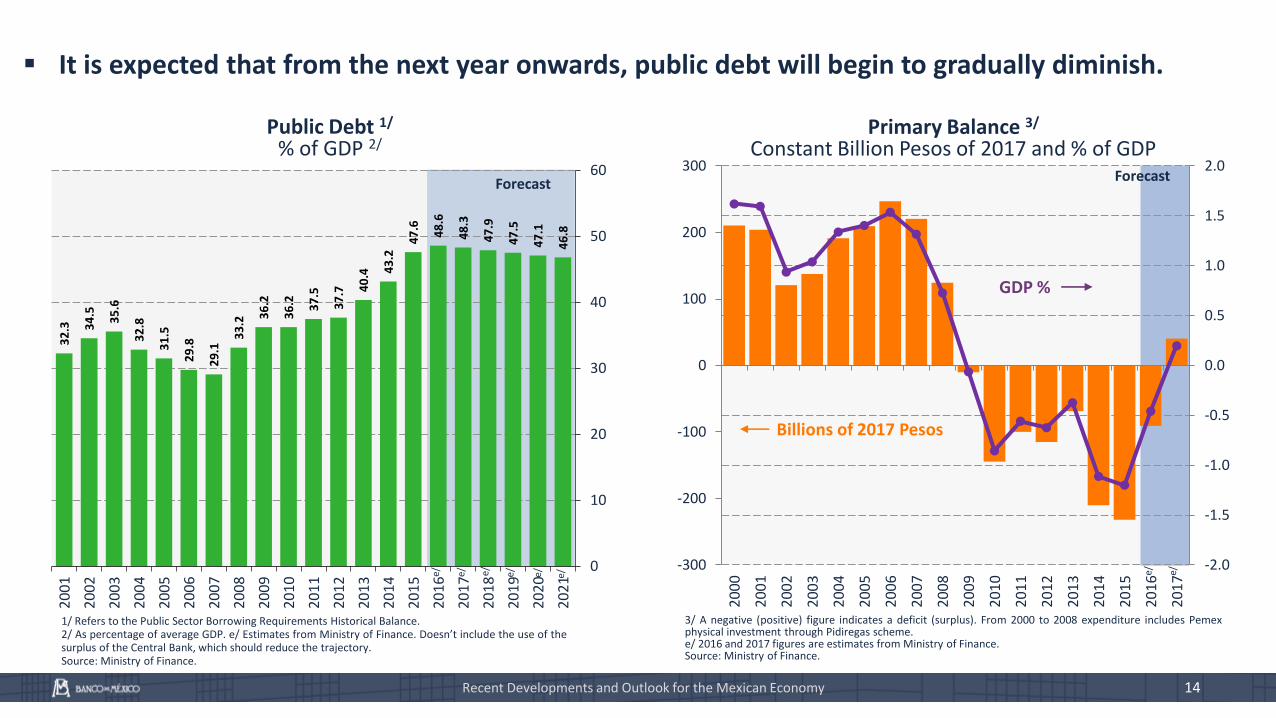

Public Debt 1/

% of GDP 2/Primary Balance 3/

Constant Billion Pesos of 2017 and % of GDP

1/ Refers to the Public Sector Borrowing Requirements Historical Balance.2/ As percentage of average GDP. e/ Estimates from Ministry of Finance. Doesn’t include the use of thesurplus of the Central Bank, which should reduce the trajectory.Source: Ministry of Finance.

3/ A negative (positive) figure indicates a deficit (surplus). From 2000 to 2008 expenditure includes Pemexphysical investment through Pidiregas scheme.e/ 2016 and 2017 figures are estimates from Ministry of Finance.Source: Ministry of Finance.

Forecast Forecast

e/e/ e/ e/ e/ e/ e/e/

Billions of 2017 Pesos

GDP %

Recent Developments and Outlook for the Mexican Economy

It is expected that from the next year onwards, public debt will begin to gradually diminish.

15

Domestic Environment:

Moderate economic growth.

• The output gap has remained negative and it is expected to be gradually closed inthe foreseeable future due to structural reforms.

Banco de México has remained particularly vigilant to the external environment, given thatin the domestic front no signs of aggregate demand pressures on prices have been observed.

Recent Developments and Outlook for the Mexican Economy

• Inflation expectations remain anchored.

• The labor market is gradually recovering.

16

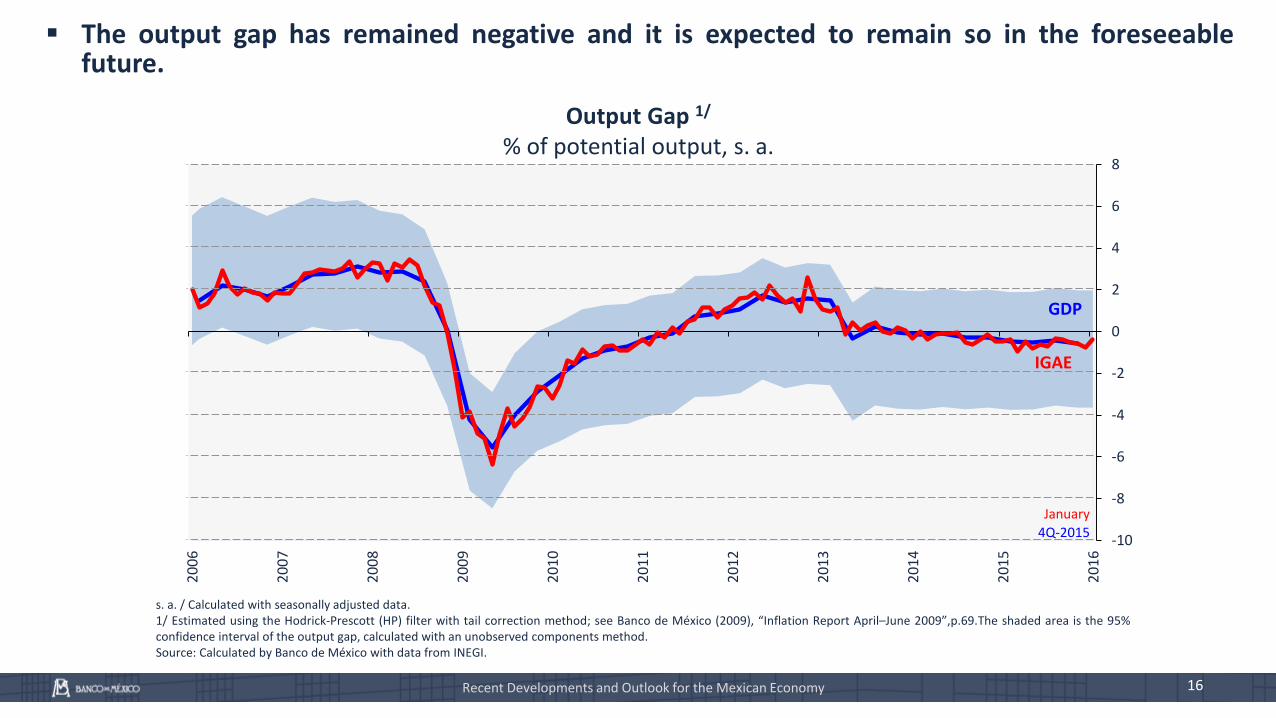

The output gap has remained negative and it is expected to remain so in the foreseeablefuture.

-10

-8

-6

-4

-2

0

2

4

6

8

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

GDP

IGAE

January

4Q-2015

s. a. / Calculated with seasonally adjusted data.1/ Estimated using the Hodrick-Prescott (HP) filter with tail correction method; see Banco de México (2009), “Inflation Report April–June 2009”,p.69.The shaded area is the 95%confidence interval of the output gap, calculated with an unobserved components method.Source: Calculated by Banco de México with data from INEGI.

Output Gap 1/

% of potential output, s. a.

Recent Developments and Outlook for the Mexican Economy

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

7

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

17

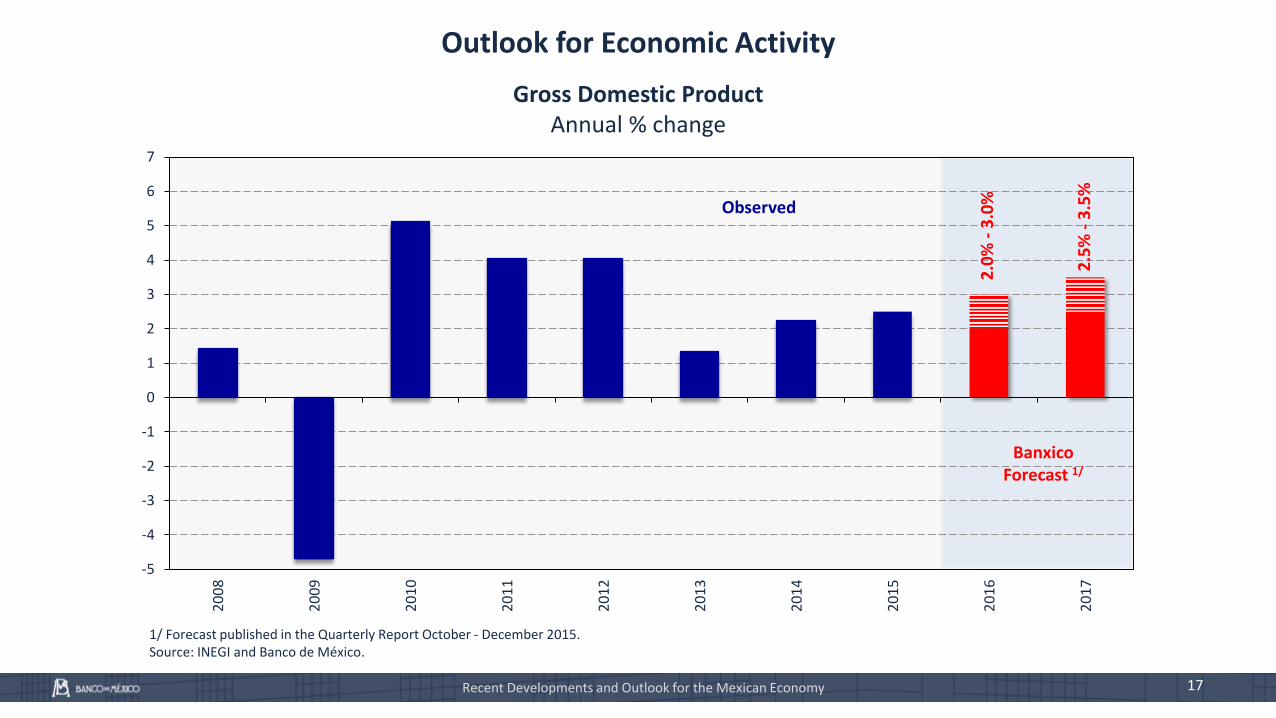

Outlook for Economic Activity

Gross Domestic ProductAnnual % change

1/ Forecast published in the Quarterly Report October - December 2015.Source: INEGI and Banco de México.

Banxico Forecast 1/

2.0

% -

3.0

%

2.5

% -

3.5

%

Observed

Recent Developments and Outlook for the Mexican Economy

18

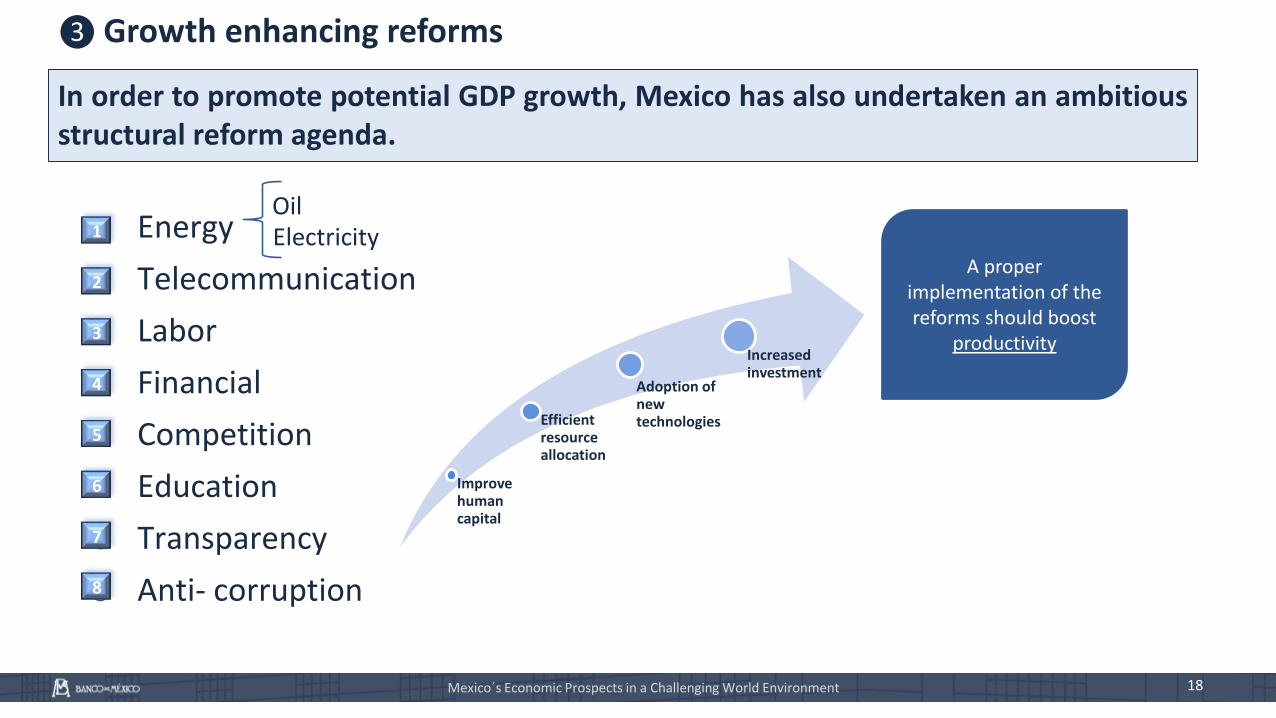

❸ Growth enhancing reforms

In order to promote potential GDP growth, Mexico has also undertaken an ambitiousstructural reform agenda.

o Energy

o Telecommunication

o Labor

o Financial

o Competition

o Education

o Transparency

o Anti- corruption

A proper implementation of the reforms should boost

productivity

Improvehuman capital

Efficientresourceallocation

Adoption of new technologies

Increasedinvestment

OilElectricity1

2

3

4

5

6

7

8

Mexico´s Economic Prospects in a Challenging World Environment

-50

0

50

100

150

200

250

300

19

78

19

81

19

84

19

87

19

90

19

93

19

96

19

99

20

02

20

05

20

08

20

11

20

14

19

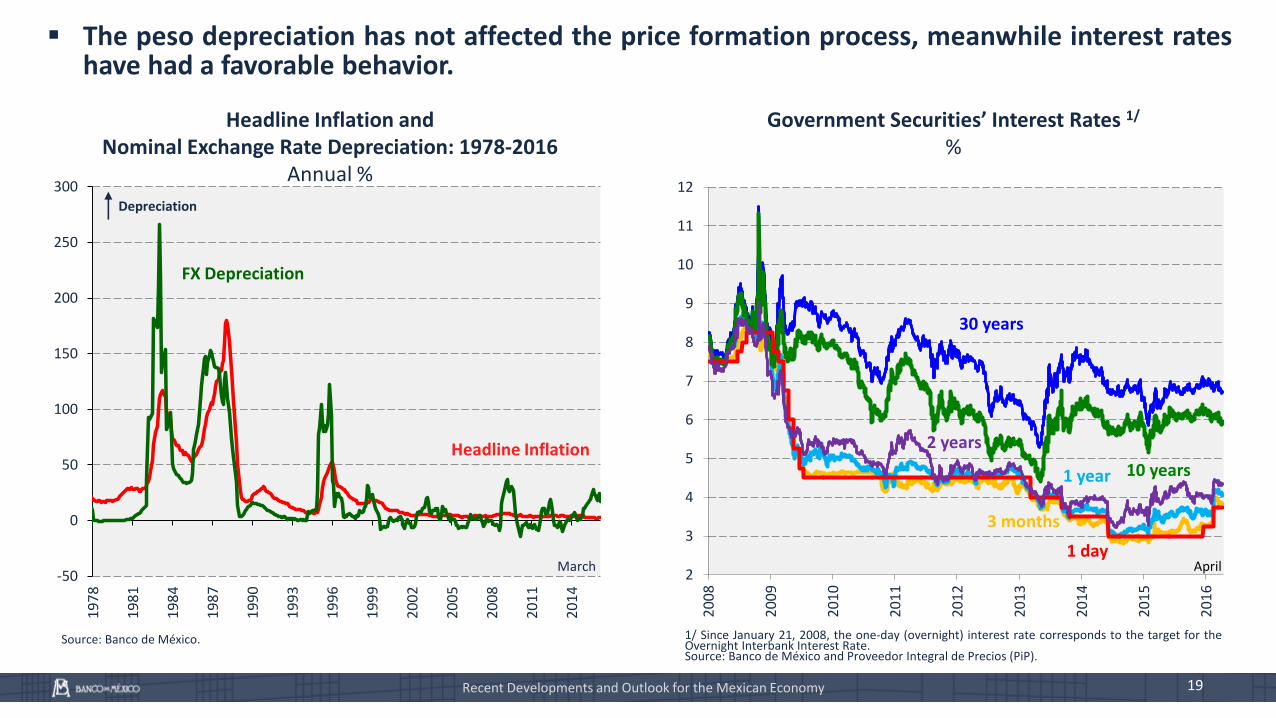

The peso depreciation has not affected the price formation process, meanwhile interest rateshave had a favorable behavior.

Government Securities’ Interest Rates 1/

%

1/ Since January 21, 2008, the one-day (overnight) interest rate corresponds to the target for theOvernight Interbank Interest Rate.Source: Banco de México and Proveedor Integral de Precios (PiP).

Recent Developments and Outlook for the Mexican Economy

Headline Inflation and Nominal Exchange Rate Depreciation: 1978-2016

Annual %

Source: Banco de México.

March

Headline Inflation

FX Depreciation

Depreciation

2

3

4

5

6

7

8

9

10

11

12

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

1 day

10 years

30 years

1 year

3 months

2 years

April

20

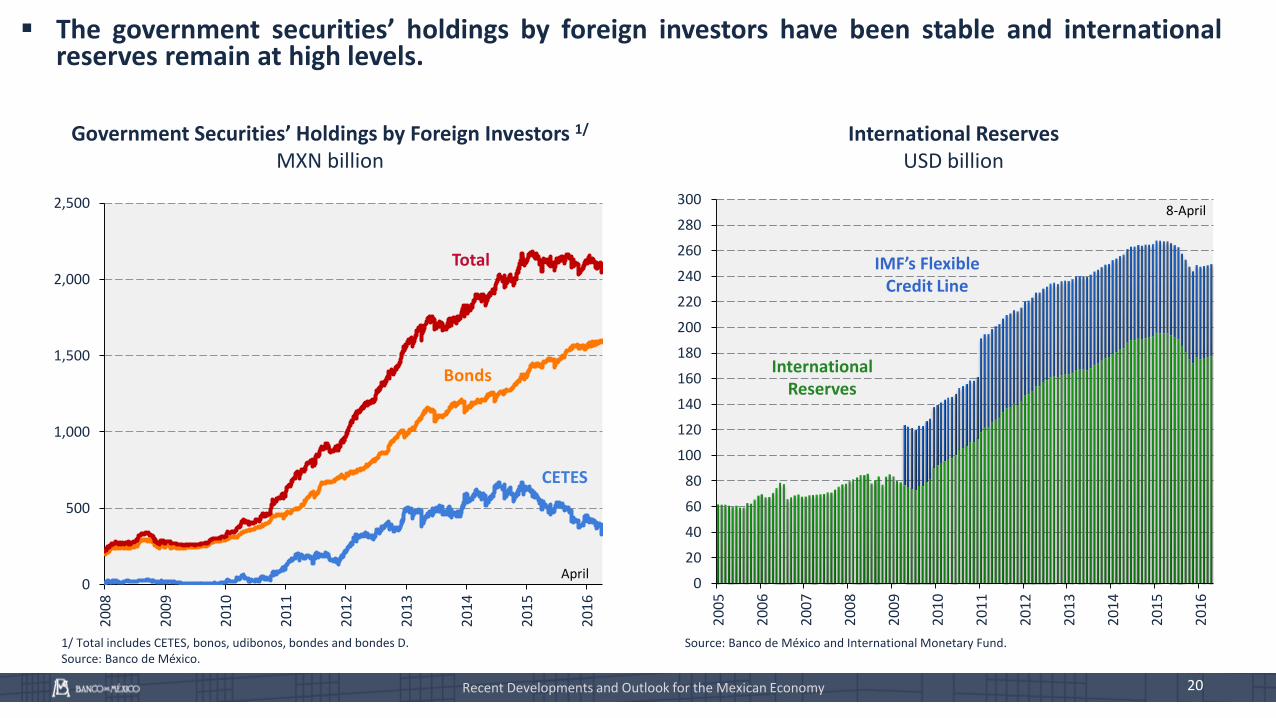

Government Securities’ Holdings by Foreign Investors 1/

MXN billionInternational Reserves

USD billion

1/ Total includes CETES, bonos, udibonos, bondes and bondes D.Source: Banco de México.

Source: Banco de México and International Monetary Fund.

The government securities’ holdings by foreign investors have been stable and internationalreserves remain at high levels.

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

0

500

1,000

1,500

2,000

2,500

Mill

ares

April

Total

0

20

40

60

80

100

120

140

160

180

200

220

240

260

280

300

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Recent Developments and Outlook for the Mexican Economy

8-April

International Reserves

IMF’s Flexible Credit Line

Bonds

CETES

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

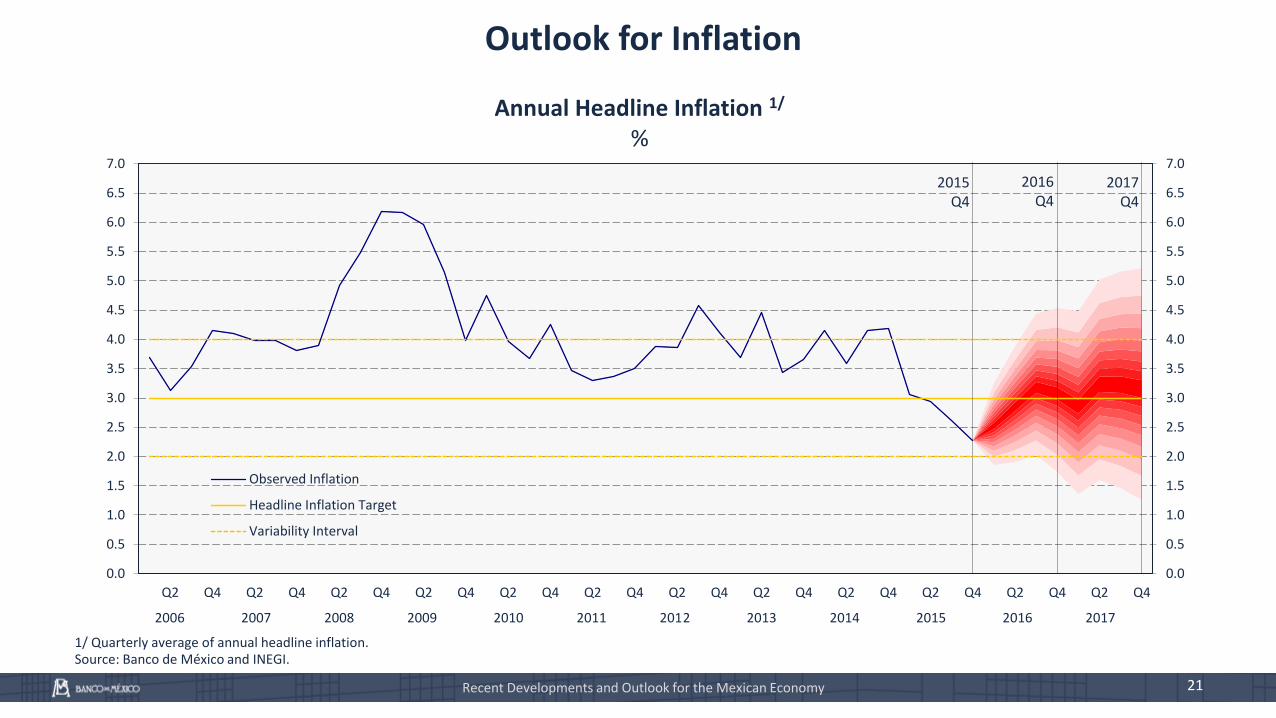

Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4

Observed Inflation

Headline Inflation Target

Variability Interval

21

Annual Headline Inflation 1/

%

1/ Quarterly average of annual headline inflation.Source: Banco de México and INEGI.

2015 Q4

2017 Q4

2016 Q4

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Outlook for Inflation

Recent Developments and Outlook for the Mexican Economy

Outline

Recent Developments and Outlook for the Mexican Economy

2

Final Remarks3

Inflation and Monetary Policy1

22Recent Developments and Outlook for the Mexican Economy

23

Final Remarks

Looking forward, Banco de México’s Board of Governors will remain alert to the performance of allinflation determinants and its expectations for the medium and long term, especially:

The exchange rate and its possible pass-through onto consumer prices.

The monetary stance of Mexico relative to the U.S.

The evolution of the output gap.

→ All of the above, in order to be able to take measures in a flexible manner and whenever conditionsdemand it, so as to consolidate the efficient convergence of inflation to the 3 percent target.

Recent Developments and Outlook for the Mexican Economy