Embed Size (px)

Citation preview

i

Part 3: Exporting of Organic Producefrom Gisborne District

RECENT DEVELOPMENTS INORGANIC FOOD PRODUCTION

IN NEW ZEALAND:

BRAD COOMBES

HUGH CAMPBELL

JOHN FAIRWEATHER

Studies in Rural SustainabilityResearch Report No. 4

Department of Anthropology,University of Otago

May 1998

ii

Published byDepartment of Anthropology,University of Otago,P.O. Box 56,Dunedin, New Zealand.1998

Phone 03 479 8751. Fax 03 479 9095.Email: [email protected]

ISBN 0-9582015-0-1

Studies in Rural SustainabilityResearch reports1. Recent Developments in Organic Food Production in

New Zealand: Part 1, Organic food exporting inCanterbury. H. Campbell 1996

2. Recent Developments in Organic Food Production inNew Zealand: Part 2, Kiwifruit in the Bay of Plenty.H. Campbell, J. Fairweather & D. Steven 1997

3. Men and Women as Stakeholders in the Initiationand Implementation of Sustainable Farm Practices:Organic Farming in Canterbury. R. Liepins & H.Campbell 1997

iii

ContentsAcknowledgements ................................................ ivAuthors ..................................................................... ivExecutive Summary ................................................. v

Chapter 1. Introduction ........................................... 11.1 Research objectives ............................................. 11.2 Site selection: the choice of GisborneDistrict ......................................................................... 21.3 Research Process .................................................. 3

Chapter 2. Contexts for horticulturalproduction in Gisborne District ............................ 42.1 Physical features .................................................. 42.2 Social and cultural features ............................... 52.3 Restructuring of agriculture andhorticulture ................................................................. 6

Chapter 3. Initial development of organichorticulture in Gisborne District .......................... 83.1 The structural position of Heinz-Wattie Ltd. in the early 1990s .................................. 83.2 The HWL strategy for convertingsweet corn growers to organic production ......... 103.3 The development of organic methodsfor sweet corn production ..................................... 153.4 The relationship between local and exportorganic industries .................................................... 18

Chapter 4. Emerging issues .................................. 204.1 Complementary and competing firms:the impact of an increasing range ofcompanies involved in organic exporting ........... 204.2 Grower concerns relating to Gisborne’sorganic industry ...................................................... 264.3 Emergent organic industries in GisborneDistrict ....................................................................... 324.4 Impediments to the expansion of organicproduction in Gisborne District ............................ 37

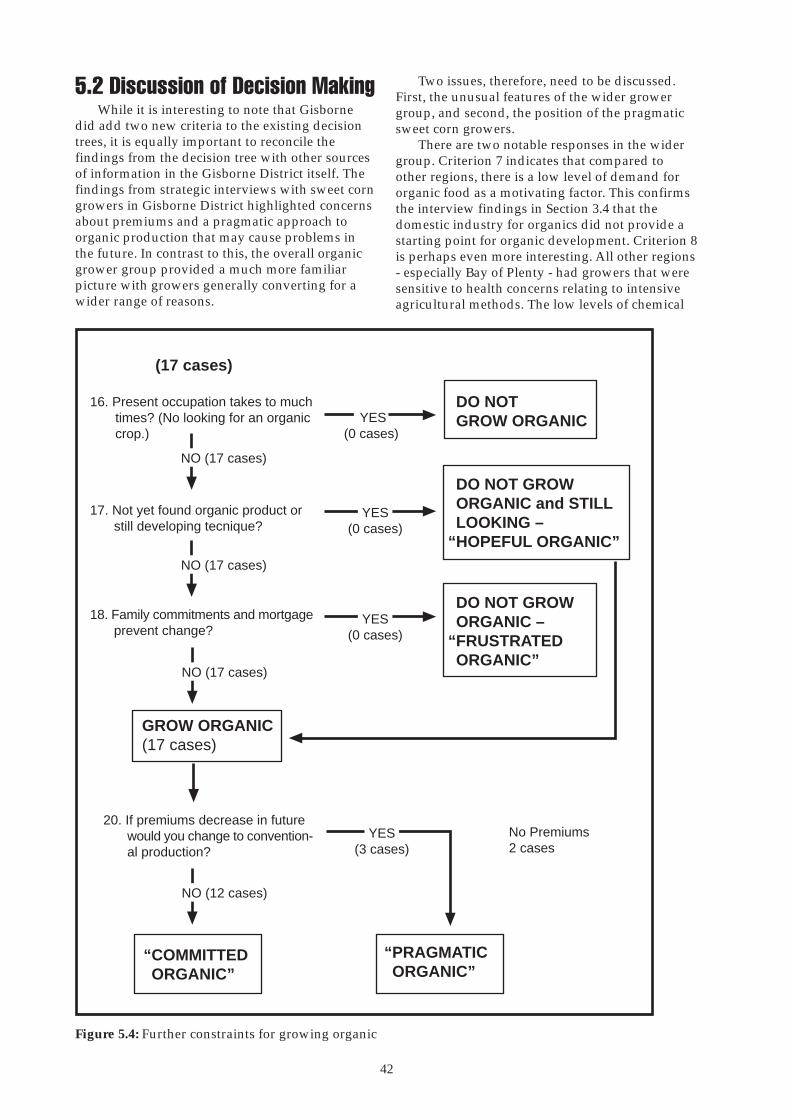

Chapter 5. Grower decision making inGisborne District .................................................... 395.1 Existing Decision Tree Applied toGisborne District ...................................................... 395.2 Discussion of Decision Making ....................... 42

Chapter 6. Conclusion: the evolution ofGisborne’s organic industry ................................. 446.1 Key issues specific to Gisborne ....................... 446.2 Wider issues relevant to the organicindustry in New Zealand ....................................... 45

References ................................................................ 47

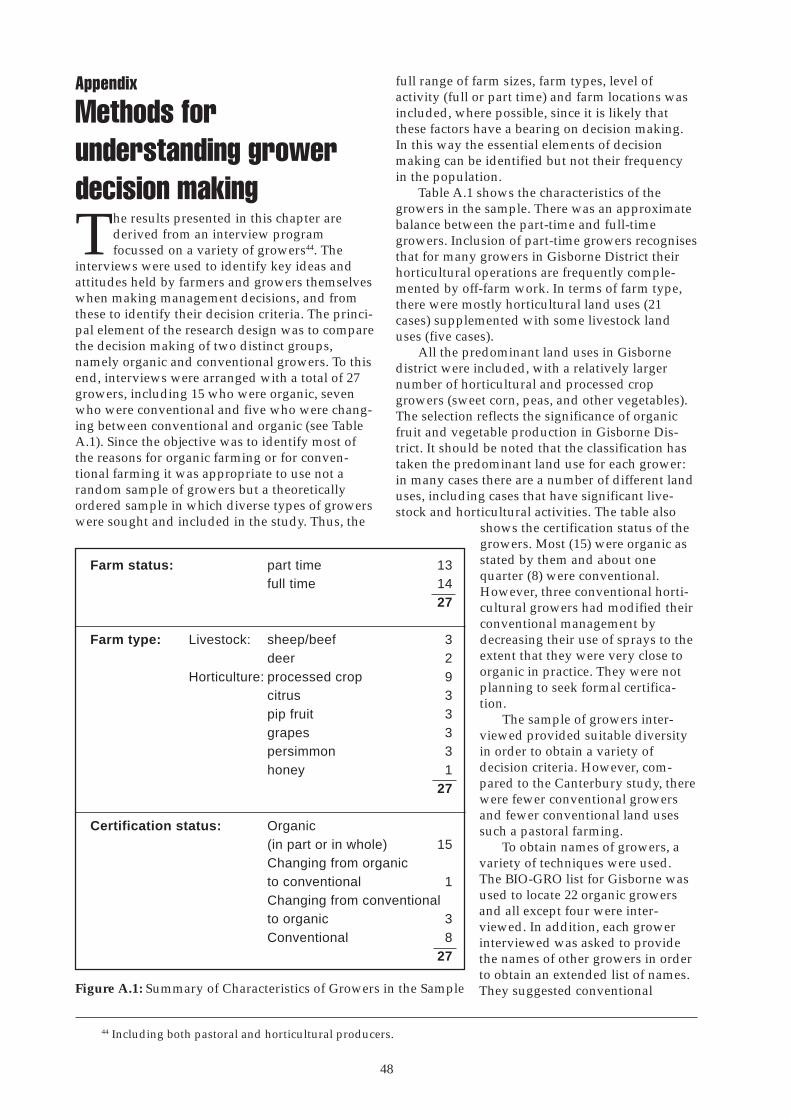

Appendix: Methods for understandinggrower decision making ....................................... 48

iv

Acknowledgements

This report forms part of the findings of aFoundation for Research Science andTechnology (Public Good Science Fund)

funded programme entitled ‘Optimum Develop-ment of Certified Organic Horticulture in NewZealand’. The authors would like to gratefullyacknowledge the importance of this funding in thesuccess of this research programme.

We would also like to acknowledge the contri-bution of Heinz-Wattie Ltd. for their cooperationwith our research activities. In particular, wewould like to acknowledge our debt to StuartDavis and Bruce Snowdon who contributed aconsiderable amount of time in assisting with thepreparation of a final draft of this report, andGrant MacDonald who provided assistance inconducting fieldwork in Gisborne. We would alsolike to thank the many growers and other industryparticipants who cooperated with our researchactivities.

Finally, we would like to thank Martin Fisherfor his usual excellent standard of formatting andpresentation of the final report.

While acknowledging the contribution ofthese individuals and organisations, the finalcontent of the report remains, as always, theresponsibility of the authors.

AuthorsDr Brad Coombes was a Junior Research

Fellow on the PGSF programme ‘Optimum Devel-opment of Certified Organic Horticulture in NewZealand’. His Ph.D thesis in Geography examinedissues of rural economic development on the EastCoast and Catlins Coast. His current publicationsprovide a critical examination of the politicaleconomy of sustainable development. Dr HughCampbell is based in the Department of Anthro-pology, Otago University, and is the leader of thePGSF funded research programme. He has ongo-ing research interests in the development ofalternative agriculture and low-input systems offood production. Dr John Fairweather is a SeniorResearch Sociologist at the Agribusiness andEconomics Research Unit, Lincoln University. Heis involved in a wide range of research activitiesinvestigating social and economic change in ruralNew Zealand.

v

Executive Summary

Despite an almost non-existent base prior to1990, Gisborne District has experienced avery rapid uptake of organic production.

The key growth area has been organic sweet cornproduction fostered by Heinz-Wattie Ltd. Thevast majority of organic products - by volume andvalue - are destined for export markets.

The rapid uptake of organics in GisborneDistrict has been influenced by the following localfactors:

• Local sweet corn growers display a distinctivelyautonomous psyche towards organics (whichmay be related to the relative economic andspatial isolation of the district as well as a rangeof social problems which has reduced percep-tual barriers to new economic forms);

• Broader agricultural restructuring in the Districthas seen increased land areas devoted tohorticultural production and a move from bulk-commodity to niche production.

Heinz-Wattie Ltd. (HWL) have been prominentin developing organic exporting. The followingfactors are of significance:

• Organic sweet corn was essential to the market-ing strategy of HWL in Japan, and GisborneDistrict provided the most likely source of thisproduct;

• HWL has been the only significant organisationengaging in technology transfer with newlyconverted organic growers;

• In the last two seasons, some HWL sweet corngrowers have employed a full organic rotationin high value export crops using sweet corn,peas, and squash as well as green-manure cropsgrown over the winter. This rotation, onceestablished, represents an important develop-ment in the context of the entire New Zealandorganic industry where broadacre rotations ofhigh value organic crops have - to date - proveddifficult to establish.

The longer-term survival of organic produc-tion in Gisborne – which now appears to berelatively assured – is dependent on local diversifi-cation in terms of organic crops and fosteringsynergies among a variety of organic processingfirms. Diversification has had the followingeffects:

• It has provided the elements for a successfulrotation in organic crops;

• It created useful synergies between organicprocessors/exporters - as evidenced by coop-eration between squash exporters and HWL;

• It has led to an increasing range of purchasers oforganic products which has reassured manyconventional growers considering conversionto organic production;

• It has, however, led to the potential for competi-tion between purchasers of organic products,especially sweet corn. This raises seriousquestions about the current structure of tech-nology transfer and skills development amongorganic growers. It also has undermined someof the trust in the generally successful relation-ship established between HWL and some of itsearly organic growers.

• Further to this, there is also an emerging compe-tition over what constitutes a legitimate organiccertification process. Gisborne District is onesite where firm-specific standards for ‘organic’production are being developed and inspectedby MAF Qual. This has the potential to under-mine some significant and beneficial aspects ofthe current structure of organic certification asprovided by BIO-GRO NZ.

A distinctive feature of land-use in GisborneDistrict is the amount of land in multiple-owner-ship and managed by Maori resource incorpora-tions/trusts. Despite considerable attention oflocal Maori to organic production, few suchincorporations/trusts have become involved inorganic production:

• Several Maori properties appear suited toorganic production: local Maori perceiveorganics as suited to the communal ownershipof land and many properties have had lowlevels of applied agrichemicals, so they couldbe quickly moved through the BIO-GRO NZcertification procedures;

• However, key structural impediments to Maoridevelopment, especially the issues of leasing,and raising development capital for, communalland will need to be resolved for future devel-opment of organic production in the region.

The most significant factor in determining thecharacteristics of organic production in Gisbornehas been its terra nullius status in terms of organicproduction at the start of the decade:

• Unlike other regions, Gisborne District did nothave significant levels of debate and interactionbetween long-term organic producers andnewly converted export growers;

• This is reflected in a more ‘pragmatic’ approachto organic production by many new growers inGisborne District compared to other regions;

• Such pragmatism is indicated by the heighteneddegree to which some sweet corn growers wereattracted to organic production by premiumsand have stayed in organic production prima-

vi

rily to achieve these premiums. While the sameGrow Organics With Watties promotionalmaterial was used in both Canterbury andGisborne, some Gisborne growers took some-what different messages from this material thantheir counterparts in Canterbury;

• Furthermore, some highly pragmatic sweet corngrowers will, in the next few years, probablycome into conflict with the BIO-GRO inspector-ate over issues of soil fertility and fallowing;

• All the study regions had newly convertedgrowers who were initially only interested inpremiums but then experienced a ‘progressiveconversion’ to the wider aims of the organicmovement. However, in Gisborne District, theextent of ‘progressive conversion’ seems sloweramong some prominent sweet corn growers, asituation that is exacerbated by their disinterestin the local organisation for organic producers.

Five challenges will need to be faced in thefuture, if the high rate of organic development inGisborne District is to be maintained.

1) Skills and technology transfer: a significantneed for a local grower organisation commited todeveloping skills and knowledge among growers.All firms engaged in organic exporting should beinvesting in technology transfer, while the stateshould also be a provider of research and educa-tion in organic production.

2) Synergies not competition: synergisticdevelopment with companies cooperating toservice different elements of a full organic rotationis clearly more suitable to organic production thanoutright competition. Again, grower pragmatismand the commitment to maintaining premiums isleading some growers to seek to strengthen theirposition vis-a-vis processors by encouragingcompetition for single crops within their overallrotation rather than finding strength throughdeveloping a full rotation.

3) Resolution of leasing and overcomingbarriers to Maori development: current strategiesfor incorporating Maori land into organic develop-ment have emphasised leasing arrangements.These are undesirable in the long term as a form oforganic production and can only be viewedfavourably as a ‘stepping stone’ to independentorganic production by Maori incorporations.

4) Soil fertility and encouragement of ‘pro-gressive conversion’ of pragmatic sweet corngrowers: some growers will have difficulty main-taining their organic status unless they adopt aless pragmatic attitude to production and begin toaddress issues of long-term soil fertility.

5) Maintenance of integrity of organic stand-ards: as a region which lacks any long termorganic history, Gisborne is potentially susceptibleto activities which might undermine or ‘waterdown’ established notions of what constitutesorganic production. MAF Regulatory Authorityneeds to give clear direction to exporting compa-nies by recognising a national standard for organicproduction.

1

Chapter 1

Introduction

This report is the third in a series of four casestudies on the evolution of organic produc-tion in key regional areas of New Zealand.

The other three case studies are Canterbury(Campbell 1996), Bay of Plenty (Campbell et al.1997) and Nelson (to be completed in mid 1998).The four reports are the main outputs for theresearch program ‘Optimum Development ofCertified Organic Horticulture in New Zealand’,funded by the Public Good Science Fund. Thecurrent report presents the findings of researchinto the development of organic production inGisborne District1 (see Figure 1.1). Although thesefindings are significant and stand in their ownright as suitable for individual publication, somecomparisons are made in the text between theevolution of organics in Gisborne and the develop-ment of organics in Canterbury and Bay of Plenty.This mainly involves comparisons betweenGisborne and Canterbury, because organic cropsand an individual company – Heinz-Wattie Ltd.2 –have been prominent in both areas. This enablesthe Gisborne case study to be more fully under-stood. Nevertheless, extensive comparisons arenot made in this report: they have been set asidefor a future publication to be completed after theNelson report.

1.1 Research objectivesSince 1990, organic production has increased

markedly in New Zealand, with a considerablechange in emphasis in terms of the target con-sumer. During the 1970s and 1980s, productionwas largely in the informal sector – with a focuson self-provision and bartering – or in semi-commercial sectors, with local growers supplyinglocal buyers or cooperatives. The domestic marketconsumed almost all organic produce. Organicproduction was part of a philosophical stance: adirect critique of intensive methods of food pro-duction which had emerged after WWII. Theorganic movement sought to retain the historicalnecessity for food production to cooperate withnatural systems as the basis for sustainability. BIO-GRO NZ – the organisation which formed in 1983as an umbrella group for the various actors withinthe organic agriculture movement – has become

the certifying agency of choice in recent times.However, the 1990s have seen a considerablechange which, through the establishment of aburgeoning export industry for organic food, hasattracted a number of new organic growers. It hasalso challenged the established organic agriculturemovement in terms of its philosophical orienta-tion and infrastructural ability to certify the largenumbers of new producers.

In the Canterbury and Bay of Plenty studies, itwas found that many growers who formerlyproduced under conventional systems convertedto organic production for a variety of reasons, allrelating to the increasing number of contradic-tions arising in their conventional productionsystems. The four most prominent reasons were:health concerns attributed to high agrichemicaluse; the attraction of premiums for organic versusconventional products; concerns over high pro-duction costs of chemical usage; and concern overthe long-term viability and sustainability ofconventional systems and products. Many in theorganic agriculture movement have also changedtheir orientation towards the commercial potentialof the industry and are now interested in makingorganics both commercially viable and a success-ful export industry. Others saw such changes asunacceptable or too costly for small growers anddisassociated themselves from BIO-GRO NZ.

There are many potential issues of interestwhich emanate from this growing commercialisa-tion and export-orientation of organic productionin New Zealand:

• What are the impediments which preventconventional growers from converting toorganic production?

• What regional and sectoral differences exist inthe growing New Zealand organics industry?

• Will suitable methods, structures for certifica-tion and technology evolve which allow for thesuccessful commercialisation of organics yetwill also maintain appropriate organic stand-ards?

• Which companies are becoming involved inorganic production, for what reasons and howdo they incorporate organics within theirproduction, distribution and marketing divi-sions?

• What direction is the structure of the organicindustry presently taking and what is an

1 At various points in the text the phrase ‘East Coast’ is also used. More specifically, the study areaencapsulates the Poverty Bay/Waipaoa flats, on which is Gisborne City itself, and the horticultural land nearWhangara and Tolaga Bay. The Maori term ‘Tairawhiti’ covers a similar area to the Gisborne District. Also notethat Gisborne District is one of the few unitary authorities in New Zealand. Hence, there is no Regional Council ofwhich Gisborne District is a part.

2 Henceforth, HWL. During much of the period under discussion this company was called Wattie FrozenFoods Ltd., which was absorbed as an operating division of the Heinz group in 1992. This division ceased to havean independent name when Heinz-Wattie Ltd. was restructured in 1996. To avoid confusion over the changingname of the division, reference will only be made to Heinz-Wattie Ltd for the entire period.

2

appropriate industry structure that could fosterorganic production?

• Can the export/commercial and domestic/philosophical components of the organicindustry evolve in parallel without the formerdominating the latter?

These are just a few of the issues which formthe research objectives of the present series ofreports. More detail on these objectives can beobtained from Report No. 1 (Campbell 1996).

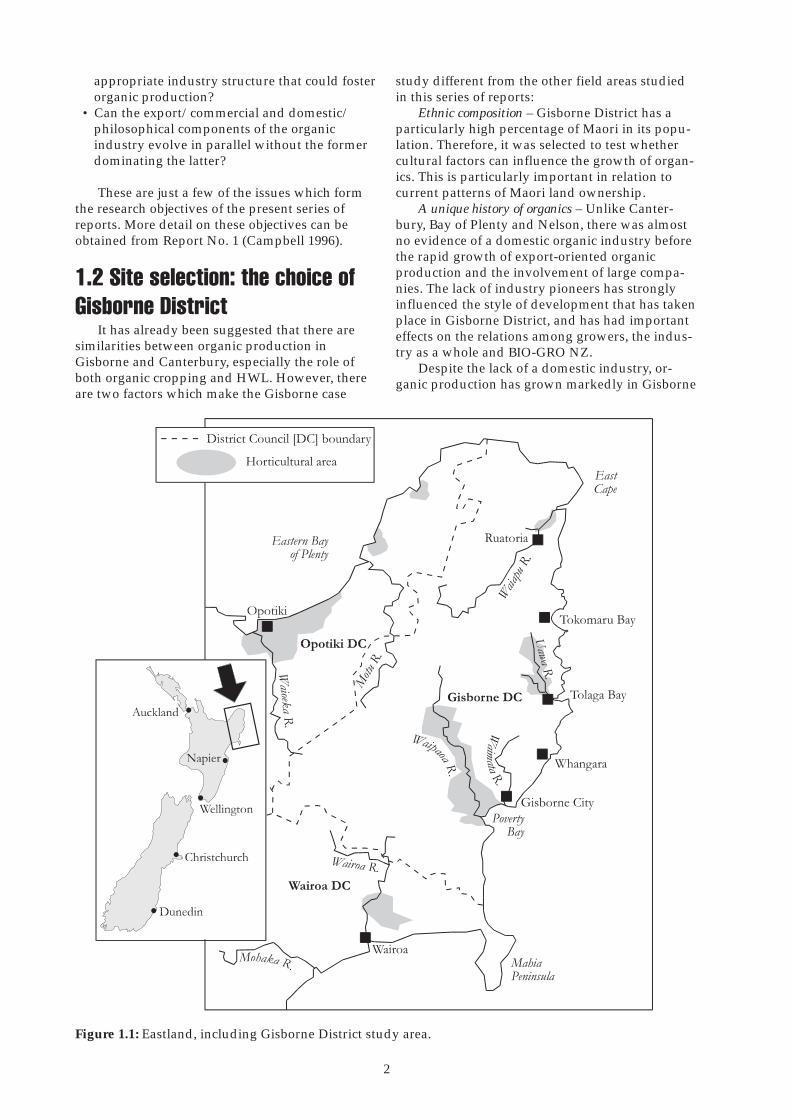

1.2 Site selection: the choice ofGisborne District

It has already been suggested that there aresimilarities between organic production inGisborne and Canterbury, especially the role ofboth organic cropping and HWL. However, thereare two factors which make the Gisborne case

study different from the other field areas studiedin this series of reports:

Ethnic composition – Gisborne District has aparticularly high percentage of Maori in its popu-lation. Therefore, it was selected to test whethercultural factors can influence the growth of organ-ics. This is particularly important in relation tocurrent patterns of Maori land ownership.

A unique history of organics – Unlike Canter-bury, Bay of Plenty and Nelson, there was almostno evidence of a domestic organic industry beforethe rapid growth of export-oriented organicproduction and the involvement of large compa-nies. The lack of industry pioneers has stronglyinfluenced the style of development that has takenplace in Gisborne District, and has had importanteffects on the relations among growers, the indus-try as a whole and BIO-GRO NZ.

Despite the lack of a domestic industry, or-ganic production has grown markedly in Gisborne

Figure 1.1: Eastland, including Gisborne District study area.

3

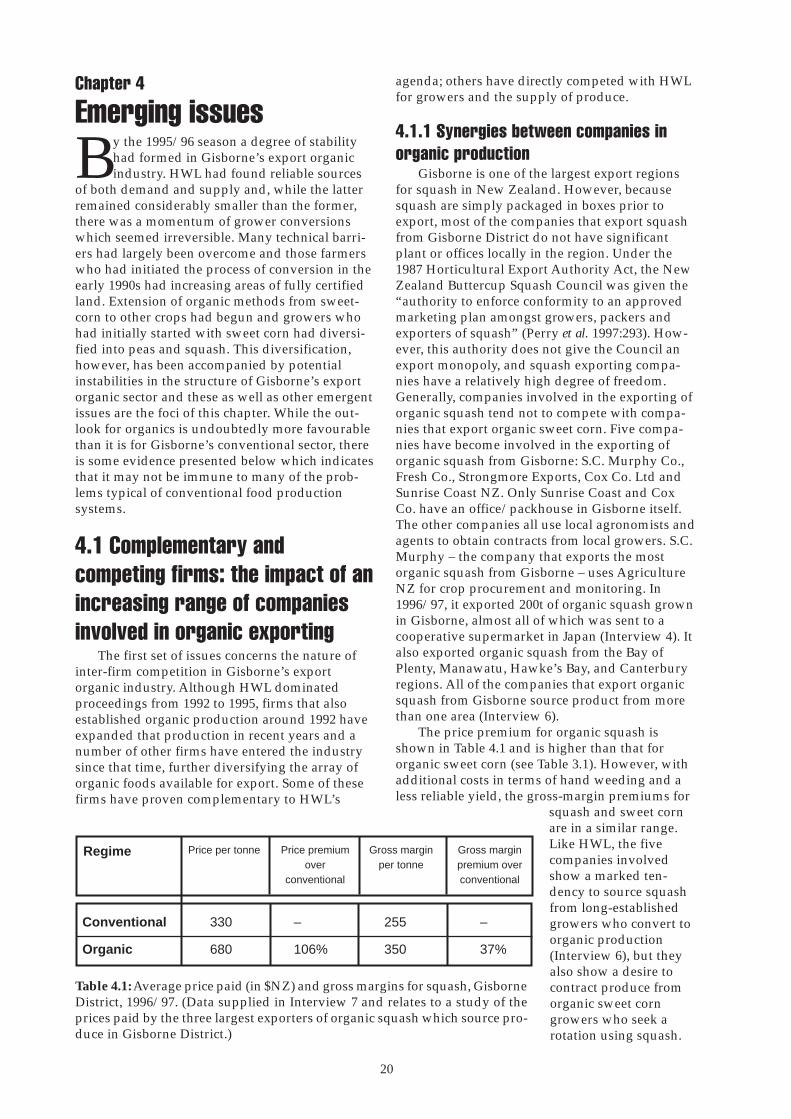

during recent years, with most of this expansionwithin the sphere of organic cropping. In the1996/97 season, HWL’s Gisborne suppliers grewabout 2000t of organic sweet corn (Zea mays) andorganic peas (Pisum sativum), and five othercompanies exported a total of 650t of squash(Cucurbita spp., usually C. maxima). In recent years,organic fruit production has increased and recentconversions of orchardists mean that this growthwill continue. Organic persimmons (Diospyroskaki) and organic wine are the main contributors tothat increase. Experimentation on mixed proper-ties with a full rotation of organic crops involvingsweet corn, squash, peas, and green-manure cropsgrown over the winter is particularly significant.This development places Gisborne ahead ofcomparable regions like Canterbury which havenot yet been able to achieve a full rotation in high-value organic crops and stock. Some stakeholdersin Gisborne’s organic industry are confidentlypredicting that the adoption of a full rotation willlead to sustained expansion of the local industry,establishing Gisborne as New Zealand’s premierorganic growing region.

1.3 Research ProcessAs was the case in the two reports published

thus far in the current series, there were two mainresearch methods employed in this study.

Strategic Interviewing – In August of 1997, aninterview program was conducted with 25 partici-pants who have a stakeholding in the local organ-ics industry. These interviews were ‘interactive’ inthe sense that the form of interviewing was notthe set-survey method. Rather, each intervieweewas given as much room as possible to direct thestructure of their interview. The composition ofmembers in this interview program is presented inTable 1.1:

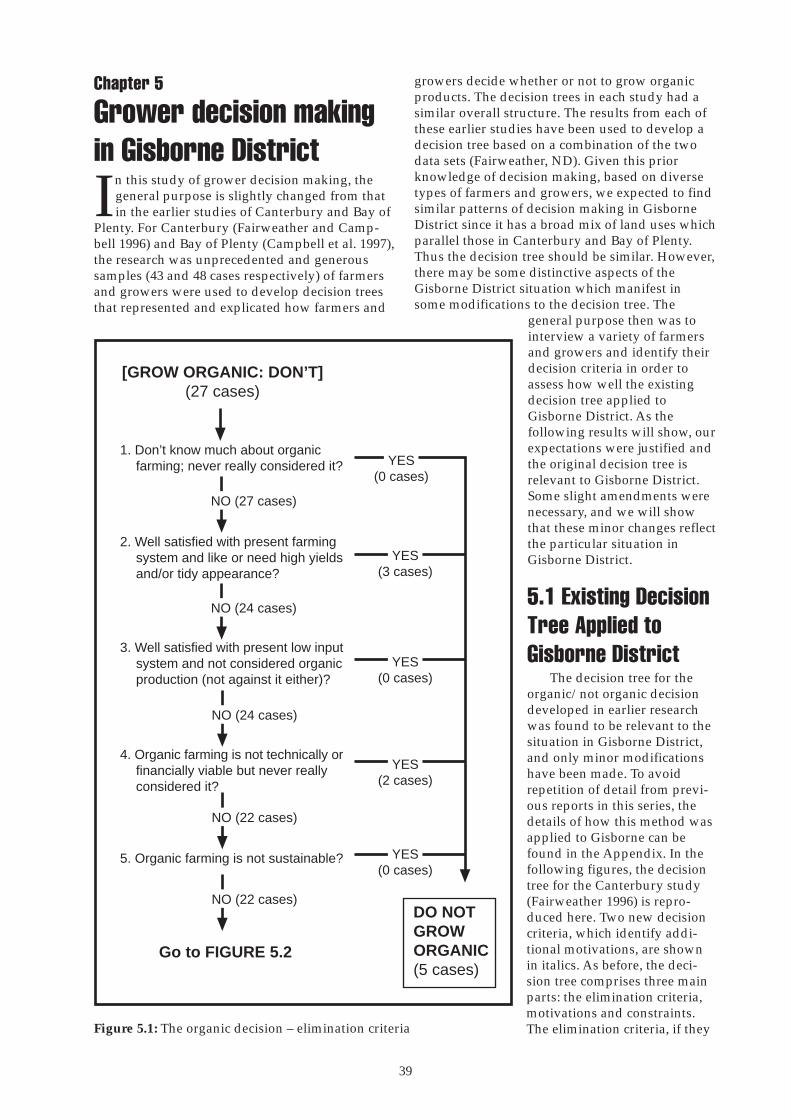

Ethnographic Decision Tree Modelling – Decisionmaking of growers was assessed by interviewing

27 people. The criteria used by these growers inmaking decisions about organic production wereidentified and used to assess the relevance of thedecision tree derived from the earlier Canterburystudy.

Position of interviewee in organics industry Interview No.

Export/processing company managers and marketers 1, 2, 3, 4 and 5

Agronomists and other advisers 6, 7, 8 and 9

Managers of low-input and/or fruit production initiatives 10 and 11

Stakeholders in the (domestic) organic food movement 12, 13 and 14

Organic viticulturists 15 and 16

Organic crop (pea, sweetcorn, squash) growers 17, 18, 19, 20, 21 and 22

Organic deer farmers (both formerly organic crop growers) 23 and 24

BIO-GRO NZ representative 25

Table 1.1: Participants in the strategic interviews.

4

Chapter 2

Contexts for horticulturalproduction in GisborneDistrict

It will be shown in Chapter 3 that many of theforces which led to Gisborne becoming asignificant region for organic production in

New Zealand had their origin outside of theDistrict. However, there are a number of internalfeatures which have helped to accelerate thedevelopment of organics in the region and haveled to the success of organic producers. Severalchange dynamics have recently encouraged movesinto niche production by primary producers. Thegrowth in organic production is related to thisbroader trend. Three key topics will be examined:

• The growing conditions in the area, which areappropriate for organic horticulture;

• The social situation of Gisborne District, whichhas made people in the area sensitive to theneed for economic diversity and new economicprojects;

• The changing relationship between agricultureand horticulture, which has led to the recentand rapid uptake of niche horticultural produc-tion.

This brief account will draw extensively onresearch previously conducted by one of thepresent report’s authors (Coombes 1997). Thatresearch also examined the social, physical andsectoral changes in the District which have en-couraged its people to search for new economicalternatives.

2.1 Physical featuresThe first aspect of the physical geography of

the area which has encouraged the growth ofniche production relates to the effects of spatialisolation. Gisborne was one of the more difficultfrontiers in New Zealand for European settlers toestablish themselves as small producers (Oliver &Thompson 1971). To the north and west ofGisborne City, the Huirau and Raukumara Rangesrestricted travel and trade with the northern citesof Auckland and Hamilton (see Figure 1.1). To thesouth, the rugged terrain through which theMohaka river flows restricted access to Napierand Wellington. After the establishment ofGisborne City, interaction between the area andthe rest of the country was mainly through PortGisborne which was both shallow and based onan unreliable slipway from the Turanganui River,so even coastal trade proved difficult. Further

north along the East Coast, travel was particularlydifficult and until the 1920s no proper road hadbeen formed and towns such as Tolaga Bay,Ruatoria and Hicks Bay were connected by acoastal horse trail. Today, sealed roads haveimproved access to the District, but travel times tothe area remain relatively high. Gisborne is one ofthe most expensive cities to fly to in New Zealand,and negligible air freight arrives at GisborneAirport.

There are both negative and positive effects ofthis isolation. Because they are not on high-volume routes, primary producers face highercosts in terms of transporting their produce tonational and international markets. This hasmeant that agriculture and horticulture inGisborne District have always been more marginalthan in other areas of the country. One of thepositive aspects of this isolation is that a constantfear brought about by the marginal nature ofprimary production on the East Coast has madesome of its people reasonably progressive in termsof adopting new production forms and new crops(Interviews 1, 2, 3, 6, 8, 23). This tendency towardsadaptation has meant that the typical fears aboutorganic production are, to some degree, negated.Furthermore, there is considerable potential tomarket isolation as a component of the organicimage. With respect to New Zealand’s position inglobal trade, HWL recognised the wider potentialof such isolation when it began experimentingwith organic production in the early 1990s. Afterthe takeover of that company by H.J. Heinz Co.,this strategic potential was further reinforced byTony O’Reilly (the CEO of H.J. Heinz Co.) whosuggested that relative isolation from the environ-mental problems of the northern hemispherepresented New Zealand with the ability to marketitself as a ‘green’ country producing healthy food.

While the early initiatives were based aroundHWL, members of the wider organic agriculturemovement also lend support to the idea thatGisborne is ideally suited for organic production.Bob Crowder – an important figure in the NewZealand organic industry – met with Gisbornepeople interested in organics during 1993 andsuggested that:

“Gisborne’s pastoral and croppingindustries have a wonderful chance to turn theDistrict’s isolation into an asset and build anenvironment based on balanced organicprinciples” (quoted in Scott 1993: 9).

During his 1993 visit, Crowder also noted thatthe region’s growing conditions were particularlysuitable for producing organic food (ibid.). Ingeneral, the District suffers from soil erosion, butthis problem is largely confined to the hill country.Large areas of flat land also exist, especially on thePoverty Bay/Waipaoa flats and to a lesser extent

5

on the Uawa River flat at Tolaga Bay and theWaiau River Valley near Ruatoria. These consist ofgood quality soils, with a mix of yellow-brownloams and rich alluvial deposits. The quality of thesoil is such that out of the 20,200ha of flat land onthe Gisborne plains, 17,000ha can be used forhorticulture (MAF 1968), the most resource inten-sive form of primary production. The climate ofthe area is particularly suited to horticulturalproduction. The mean annual temperature –14.5oC – is one of the highest for all districts inNew Zealand which combines with a high aver-age for annual sunshine hours to create favourablegrowing conditions (Hessel 1981:12). The combi-nation of high average temperature and a longgrowing season means that the Gisborne District,and especially the area towards East Cape, is wellsuited to the growing of semi-tropical and eventropical fruits. It also means that it is one of thebest suited areas in New Zealand for sweet cornproduction. Average rainfall is a moderate1200mm per annum. In areas where there is a highamount of rainfall, organic production can bemore difficult, because these conditions can favourthe growth of weeds.

However, there is one climatic factor whichnegatively affects all forms of primary productionon the East Coast. The area is particularly suscep-tible to cyclones and one such event – CycloneBola which occurred in 1988 – persisted for fourdays and led to millions of dollars of crop andstock losses. Given the rugged and deforestednature of the surrounding hill country, soil erosionis now recognised as the region’s primary hazard,especially during abnormal cyclonic events, and isa serious threat to the long-term sustainability ofagriculture and horticulture. After 1988, manypastoral farmers abandoned their hill-countryland to the East Coast Forestry Project (seeBlaschke & Peterson 1994) and other commercialforestry programs. Some farmers have diversifiedtheir existing, low-country land to other, moreintensive uses, such as horticulture, in order tomake up for this loss of revenue. Consequently,this new phase of on-farm diversification hascontributed to a recent increase in the extent ofhorticultural activity in the District.

2.2 Social and cultural featuresDuring 1997, a number of high-profile reports

on the effects of poverty in Gisborne District wereprominent in the national media. Inadequatehousing, poor access to health resources and theineffectiveness of local education systems receivedconsiderable attention, and all are symptomatic ofthe wider effects of poverty. The District’s unem-ployment level has typically been the highest in

the country, with nearly 15% actively seekingwork (NZ Census of Population and Dwellings1991 – Gisborne/Hawke’s Bay Regional Re-port:11). In some towns, such as Ruatoria, theMaori unemployment level is over 70% (ibid.). Atthe governmental, Runanga3 and District Councillevel, considerable attention has been given tonew employment schemes for the area. In general,the unemployment problems are so significantthat there is strong support shown when investorsdesire to establish a new type of production on theEast Coast (Interview 9). As is the case with spatialisolation, a negative factor such as high unem-ployment can lead to adaptive attitudes.

Gisborne District, along with Northland, isone of only two areas in the country where Maoriregularly comprise over 50% of the population incensus meshblocks. The official proportion ofMaori in the Gisborne District population is 40%(NZ Census of Population and Dwellings 1991 –Gisborne/Hawke’s Bay Regional Report:27), butwith informal housing arrangements and the factthat many Maori on the East Coast attempt andsucceed in avoiding the census (see Coombes1997), that figure may well be an underestimate.In several of the towns along the East Coast,Maori represent over three quarters of the popula-tion (NZ Census of Population and Dwellings1991—Gisborne/Hawke’s Bay Regional Re-port:26-27). Maori have a considerable history ofhorticulture in the area. Captain Cook, on visitingAnaura Bay, was surprised by the techniques andtechnology that were employed by Maori in theirgardens, as he was by the quality and quantity ofthe produce.

In more recent times, Ngati Porou – the pre-dominant iwi – have attempted to renew theirinterest in horticulture. Considerable resourcesand land have been returned to local iwi in the1980s and 1990s as part of successive govern-ments’ attempts to meet their obligations underthe Treaty of Waitangi. Large areas of land havealso recently come out of long-term leases whichalienated Ngati Porou from their land. Increasedflexibility in how those resources are used hasbeen granted by the Te Ture Whenua Maori Act(1993) and, utilising this flexibility, many landincorporations attempt to diversify their pastoralholdings. Some have entered wine, kiwifruit(Actinidia deliciosa) and fresh-market vegetableproduction. In the research for Coombes (1997), itwas found that many local kaumatua were anx-ious to see the re-establishment of communally-based but commercially-oriented gardens bothbecause of a ‘sustainability’ ethic and as part ofemployment initiatives. Notably, several of theseleaders commented on the success of one large

3 Referring to Te Runanga o Ngati Porou, and Te Runanga o Turanganui a Kiwa – the councils of the two majoriwi in the District.

6

organic farm4, and stated that they wanted tofollow this lead because it was seen to be particu-larly appropriate for the nature of their land, andthe composition of their hapu.

During the 1990s, Maori have returned to theirGisborne turangawaewae in considerable num-bers (Butterworth 1991), but they are not the onlygroup to migrate there in recent times. The migra-tion of ‘lifestylers’ to the region is a strong dy-namic for economic change in Gisborne District(Coombes 1997). Public perception of this group isthat they are generally uninterested in pursuingemployment. However, not all lifestylers move tothe East Coast for recreational pursuits and manyarrive with considerable assets. The East Coast is agrowing destination for international tourists.Many such tourists have decided to emigrate onthe basis of their holiday experiences, and severalhave already become involved in such ‘alterna-tive’ economic practices in Gisborne as ecotourismand ‘health’ industries. In the other reports in thisseries, migrants from Europe and ex-urbanlifestylers were shown to have had an importantrole in the evolution of organic production. Al-though there is less evidence for such a role inGisborne District5, there is a some potential forfuture involvement by this group in the Gisborneorganic industry if their numbers continue toincrease.

2.3 Restructuring of agricultureand horticulture

The first European settlers of the Gisbornearea believed that the district was most suited topastoral forms of agriculture. For over one hun-dred years, extensive sheep farming was the maineconomic activity on the East Coast and a numberof large pastoral estates developed. Likewise,Maori land incorporations also tended to conformto this faith in large-scale pastoral agriculture.Apirana Ngata introduced a series of Maori landreforms in the 1930s which were adopted on anational basis, but the degree of amalgamationand centralisation of Maori land was greatestamongst his own iwi of Ngati Porou. The successof this economic form was dependent on thecontinuation of coastal shipping around the EastCoast. Large wharves were built at Tolaga Bay,Waima at Tokomaru Bay, Waipiro Bay and HicksBay, and with each was associated a relativelysmall freezing works. During the inter-war period,this proved successful but, with the decline ofcoastal shipping, all of these freezing works hadclosed by the 1950s. Even though the Kaiti freez-ing works in Gisborne City expanded to replacethe smaller freezing works, these infrastructural

changes threatened the long-term viability ofpastoral agriculture. By the late 1970s and early1980s, it was recognised that pastoral agriculturewas considerably more marginal in GisborneDistrict than elsewhere, and it was accepted thatits extent was upheld mainly by state subsidies,especially supplementary minimum prices(SMPs). When SMPs were removed, stock num-bers reduced rapidly through the 1980s and theKaiti freezing works suffered from serious levelsof under-capacity. With the post-Bola move toforestry, this problem worsened and, in 1994, theKaiti works closed.

Although the closure had a considerableimpact on the collective psyche of the region, themove was simply the climax of a more long-termshift away from pastoral agriculture. In its place,horticulture has become more prominent. Cropproduction, especially for tomatoes, grew rapidlyin the 1950s when J. Wattie Canneries Ltd. estab-lished a cannery in Gisborne City. Pea, bean andsweet corn production further expanded whenWatties added a freezing operation to theirGisborne plant in the 1960s. Fruit, especiallystonefruit and citrus, were processed for a periodof time, and lower quality maize – used mainly asa stock feed – has been significant since the 1950s.Forestry was also part of this program of diversifi-cation. The East Coast Forestry Project had itsroots in a governmental scheme established in1967, which had land stability and employmentobjectives.

From this platform, the process of diversifica-tion increased significantly in the 1980s. Aroundthat time, horticultural production was seen as thekey to Gisborne’s future. Sixteen kiwifruit or-chards were established on the Uawa River flatwith a pack-house at Tolaga Bay, and many otherkiwifruit orchards were developed on the PovertyBay/Waipaoa flats. The country’s largest singlevineyard was planted in the Waiapu Valley, nearTikitiki. Other vineyards were established in areaswhich had no history of grape production. Thoseareas which did have a history of viticulture,especially the Poverty Bay/Waipaoa flats, saw theexpansion of the production of Chardonnay andRiesling varieties. When the citrus industry wasderegulated in 1982, orange orchards also in-creased on the Poverty Bay flats. As HWL consoli-dated its tomato processing operation in Hastings,Cedenco Foods Ltd. opened a tomato processingfactory in Gisborne City in 1986 and sought toincrease the level of tomato production. At thetime of its peak operation in the mid-1990s,Cedenco was supplied by 8 large growers andanother 50 small growers as well as leasing con-siderable quantities of cropping land under its

4 The manager of which was interviewed for the present report (Interview 18).5 See Section 3.2.1.

7

own name. There was considerable optimism inthe 1980s that Gisborne was undergoing a periodof fortuitous economic restructuring which wouldsee a successful diversification of its primaryproduction.

However, an article in the first edition of theGisborne Herald for the 1990s, suggested that thisdiversification program was failing: “The 1980swere a decade that promised much but producedlittle” (Conway 1980:8). With recognition ofoversupply in the wine industry, the vines atWaiapu were uprooted. For kiwifruit growers,declining world prices after 1988 and CycloneBola combined to devastate the industry inGisborne and the kiwifruit packhouse at TolagaBay closed down. At one point up to 50 kiwifruitorchards had been planned for the area aroundTolaga Bay, but only three survived after theclosure of the packhouse. The most notable failurewas the collapse of Cedenco in 1996, only twoyears after a considerable expansion of itsGisborne factory6. Nevertheless, these aspects ofthe region’s diversification from agriculture tohorticulture have been replaced by other horticul-tural ventures which are more small-scale in theirorientation. Macadamia (Macadamia ternifolia),feijoa (Feijoa sellowiana) and avocado (Perseagratissima) production in the East Cape region hasgrown considerably during the 1990s. Other‘exotic’ foods such as persimmons, mandarins(Citrus reticulata) and truffles (Tuber melanosporum)have also been grown in recent times on thePoverty Bay flats. Specialist markets also devel-oped, such as the supply of fresh vegetables,especially squash and onions, for export and off-season production of broccoli for the Japanesemarket. In general, diversification from agricul-ture to horticulture in Gisborne District did notfail completely, but has increasingly been targetedtowards niche operations. With the area’s growingconditions being appropriate for ‘exotic’ fruits andcrops which need long growing seasons or off-season production, specialised production ofvalue-added horticultural goods appears to be thebest hope for Gisborne District. Organic fruits andvegetables are just one type of these niche prod-ucts.

6 The major part of Cedenco’s operation – its tomato processing facility – was transferred to Australia. Someprocessing activity remains at the Gisborne plant, but this is very limited compared to the scope of the company’sinfluence in the area during the period 1992-1996.

8

Chapter 3

Initial development oforganic horticulture inGisborne District

In the previous chapter, it was established thatboth agriculture and horticulture in GisborneDistrict are undergoing a period of substantial

restructuring. That restructuring has incorporatedtwo dynamics: first, a farm-level move away fromdependence on pastoral production and intomixed-production including horticulture; and,second, movement of horticultural operations intovalue-added and niche production. The purposeof this chapter is to evaluate how those dynamicshave affected the evolution of organic horticulturein Gisborne District. The chapter concentrateslargely on the activities of one company – Heinz-Wattie Ltd. (HWL) – and its efforts to establish anorganic sweet corn operation since 1991. The closeattention given to HWL reflects two importantcharacteristics of the initial development oforganic horticulture in Gisborne District. Whereasthe Canterbury (Campbell 1996) and Bay of Plenty(Campbell et al. 1997) cases highlight how com-mercial exporting of organics can grow out of anexistent domestic industry, export of organic foodfrom the Gisborne area grew rapidly despiteinherently low levels of domestic production andconsumption of organic produce. The secondcharacteristic of the initial moves towards theexport of organic produce is the dominance ofHWL in organics between 1992 and 1995. Chapter4 evaluates the increase in small and medium sizecompanies entering the organic industry since thattime, as well as the increasing range of organicproducts grown in Gisborne, but in the first half ofthis decade HWL and its sweet corn growers werethe industry pioneers, so the company warrantsspecific attention in this chapter.

3.1 The structural position ofHeinz-Wattie Ltd. in the early1990s

Given the initial dominance of HWL in theevolution of Gisborne’s organic industry it ispertinent to examine the motivations of thatcompany with respect to organic production. Themotivations for HWL’s organic sweet corn initia-tive cannot be separated from either the wider‘Grow Organic With Watties’ program7, the chang-ing fortunes of its conventional products or its

changing status and structure as a company. Allthese factors have bearing on the type of organicsweet corn operation that developed in Gisbornein the early 1990s.

3.1.1 Motivations for organic exportingIn the first report of this series (Campbell

1996), Heinz-Wattie Ltd. was shown to haveplayed a major part in the development of organicexporting from Canterbury. In that case, the mainexport goods were peas and carrots, but themotivating factors for producing those goods arealso relevant to the development of organic sweetcorn in Gisborne, especially as the strategy forboth provinces emerged in tandem. Campbell(1996:25ff) identified four factors which influencedHWL’s decision to pursue organic product lines:

• Preserving access to First World markets. Theexperiment with organics was only one part ofthis strategy, but quickly became its mostsuccessful component;

• The unfavourable position of bulk commodi-ties in the world vegetable market in the 1980sand 90s which required experiments in market-ing. Improved marketing became an evengreater priority when H.J. Heinz Co. took overWattie Frozen Foods Ltd.. The new manage-ment brought a more marketing-orientedapproach compared to the production focus ofthe prior owners, Goodman Fielder Wattie Ltd.(Interview 1, see also Roche 1996).

• Organic production was also considered to bedesirable because it added value to existingproducts without requiring a costly restructur-ing of processing facilities.

• In part, HWL was responding to requests fromJapanese buyers regarding the ‘clean andgreen’ qualities of HWL products and somecompanies specifically desired an organicproduct. While HWL already marketed itsmainstream produce as the result of lesschemically-intensive production methods thanthe market alternatives, by linking the main-stream product to a fully organic product,market performance was improved. Organicproducts could act as a ‘keyhole product’,improving the market standing of mainstreamproducts, and gaining access to new, previ-ously disinterested buyers.

Campbell (1996) also identified another factorwhich was the independent conversion of previ-ously conventional and long-term HWL growersto organic production in Canterbury, whichprovided HWL with some organic product toexport. This did not occur in Gisborne where there

7 The HWL promotional program for attracting conventional growers to organic production. See Section 3.2.3.Henceforth, GOWW.

9

were almost no existing organic growers whocould be contracted to grow sweet corn.

3.1.2 The specific need for organic corn infrozen mixes

There were, however, some factors that sepa-rate HWL’s motivations for developing organicproduction in Gisborne from what occurred in itsother supply regions. Sweetcorn was always goingto be an integral part of the larger HWL organicsprogram as it can be used in combination withpeas and carrots to create new products for theJapanese market. Peas and corn are able to be soldseparately, but there is less demand for organiccarrots and they are not sold as an individualproduct. Organic carrots have been successfullymarketed, however, using a pea/carrot/sweetcorn mix which is popular in the Japanese market(Interview 1). Consequently, production of organicsweet corn has enabled HWL to expand its prod-uct range from a focus on peas, to include sweetcorn, and mixed vegetables. This made sweet cornan important part of the HWL strategy for Japan,and as the best growing conditions for sweet cornin the vicinity of HWL’s four freezing plants are inGisborne, it is clear as to why HWL was particu-larly interested in fostering organic production inthe region.

Furthermore, organic sweet corn tends toattract a higher premium in the market than otherorganic frozen vegetables (Interview 2), and sellsat between 40-50% more (per processed tonne)than organic peas or carrots (Interview 1). Thesehigh premiums help to offset higher costs ofproduction. To a significant degree, therefore, thegrowth of organic horticulture in Gisborne Districtis accounted for by its suitability to grow oneparticular crop that meets one company’s specificsourcing and marketing needs. Many of the otherorganic crops/companies in Gisborne have devel-oped in a successional or ancillary nature8 to theHWL sweet corn operation and there is somedoubt as to whether they would have been estab-lished so easily in the absence of organic sweetcorn production.

3.1.3 The status of HWL’s Gisborne plantA second set of factors which separate the

HWL motivations for organics in Gisborne fromthe company’s wider organic strategy concernsthe status of its Gisborne plant. Even before theHeinz takeover of HWL, it was evident that theGisborne factory was the most vulnerable of thefour frozen goods factories. Despite having twoadditional factories on site – “Best-Friend” petfoods and “Asahi” frozen prepared meals – HWLGisborne was more dependent on one crop (sweet

corn) than were HWL in Hastings, Christchurch orFeilding. Some difficulties concerned the age andposition of the Gisborne factory. Given its closeproximity to the sea and to the Turanganui riverthat runs through Gisborne City, and with therequirements of the Gisborne District plan fordischarges to water, the possibility of expensiveplant upgrades has been mooted for some time(Interview 18).

Other difficulties were directly related to themain product in the factory – sweet corn. Therewere two main factors that influenced the sweetcorn operation during the 1990s. First, the globalmarket in frozen sweet corn has been subject tostrong fluctuations in supply which have im-pacted on world prices. Consequently, in someseasons the factory operated below capacity(Interview 1, 2). Second, the emergence ofCedenco Foods Ltd. in the mid-90s created anincreased demand for land previously used forsweet corn. This culminated in 1994/95 when thecost of land rentals soared, as did crop prices, withHWL increasing its sweet corn contract price byaround 20% and establishing a system of partialforward payment to growers to meet the Cedencochallenge. While Cedenco’s demise can be par-tially attributed to the unsustainable aspects ofthis competition, HWL’s sweet corn operationsurvived. The combination of world marketfluctuations and competition with Cedenco raiseda number of questions regarding the future for thesweet corn operation at the Gisborne factory.

Interviewees from HWL Gisborne drew a clearlink between the pressures on the Gisborne factoryin the 1990s and the potential for organic sweet-corn (and also pea) processing to underwrite thefuture of the factory. One HWL staff memberhighlighted the relationship between these pres-sures and the development of organics:

“The only future for the plant here is inorganics. So we’ve got out there and promotedit. Our jobs are on the line, so we’ve beenparticularly keen for the Grow Organics withWatties program to be a success. We’ve prob-ably adopted it as our own more than theother Watties field areas have” (Interview 8).

These concerns about the factory’s future –which have created a local dynamic within HWLGisborne towards organics – have been accentu-ated since the Heinz takeover. The Heinz com-pany sets very challenging targets for returns oninvestment, targets which have led to a rethinkthroughout the HWL group about the structureand operation of each of the manufacturingfacilities, including those at Gisborne. In July of1997, these pressures culminated in the announce-

8 See Chapter 4, especially Section 4.1.

10

ment that the pet food and prepacked meal opera-tions would be transferred to Hastings9. As thisreport was being written, further plans are inprogress to sell the frozen vegetables plant to a‘co-packer’ company, which would then be placedon long-term contract to supply HWL with bothconventional and organic produce. This is por-trayed as a ‘win-win’ situation: Heinz would havereduced its exposure in terms of fixed costs andcould concentrate on its high-profit marketingactivities, while a local company would probablyfind the return on investment more than adequatecompared to the high targets set by Heinz.

Whatever the outcome of these negotiations,the long-term move towards an increasing organicthroughput for the HWL Gisborne plant seems setto continue. This is apparent in the current season,for which increased volumes of sweet corn havebeen provided from a slightly reduced number ofcontracts. Proportionately, organic sweet cornproduction continues to increase. In the 1997/98season, 15% of all crops grown for HWL Gisbornewill be organic and this increasing proportionlooks likely to continue for the immediate term(Interview 1).

3.2 The HWL strategy forconverting sweet corn growersto organic production

Therefore, the motivations for HWL’sGisborne interest in organics were a mix of globaltrends, company strategy, the suitability of thedistrict for sweet corn production and a localdynamic rooted in the status of its Gisbornefactory. When these trends combined to inspire aserious attempt at establishing organic sweet cornproduction in 1992, however, a further complica-tion arose. HWL Christchurch had experiencedseveral problems in establishing its organic opera-tion in the Canterbury province from 1990/91 (seeCampbell 1996). Conventional growers had beenslow to react to the premium for peas and, ini-tially, few were convinced to proceed with the 2-3year transition process to obtain BIO-GRO certifi-cation. Although HWL Christchurch ultimatelydepended on its ability to attract conventionalgrowers for the long-term success of its organic

program, it nevertheless proceeded with thatoperation in 1990/91 without the conversion ofmany conventional growers. It was able to do sobecause Canterbury had a history of domesticorganic production from the 1970s, with manylong-term organic growers already certified withBIO-GRO NZ. A further bonus was the presence ofgrowers who had been long-term HWL suppliersbut had independently converted to organicproduction prior to HWL’s organic strategy.Initially, a number of these organic growers signedorganic contracts with HWL Christchurch, andmany remain as key suppliers. In the case ofGisborne during 1991, however, only two indi-viduals of note were BIO-GRO certified – a winegrower with no available land or desire to growsweet corn and a deer farmer with limitedamounts of potential land. Consequently, the lackof a domestic organic industry posed a consider-able barrier to HWL’s desire to establish organicsweet corn production in Gisborne District.

3.2.1 Attracting long-term organicgrowers

In this context HWL Gisborne were: “preparedto break our own rules to get the organics pro-gram off the ground” (Interview 1). Usually, HWLidentify six preferred features of cropping land todecide whether they will contract an individual togrow sweet corn (Interview 1):

• Flat even paddocks for uniform crop develop-ment and optimum machinery operation;

• Larger paddock sizes are preferred for opera-tional efficiency;

• Well drained soil, because wet soil reducesyield and quality and impedes the use ofmachinery;

• Good natural fertility, soil structure and nomajor weed problems;

• Access for heavy vehicles;• Fenced to keep out stock.

Aside from the specificities of the land to beused for sweet corn production, there are otherqualities that are also preferable for sweet cornsuppliers:

9 The primary cause of this transfer relates to the closure of Gisborne’s Kaiti Freezing works two years earlier.This freezing works supplied the majority of the meat off-cuts to ‘Best Friend’ pet foods with the rest being trans-ported in through Hawke’s Bay. Without the freezing works, “Best Friend” was required to import all its meat off-cuts and offal from other centres and it was deemed appropriate to shift that particular part of the plant to a centrewith a meat processing industry sizeable enough to supply all off-cuts from local sources. A second reason for therelocation was that the Gisborne plant was old and needed to be upgraded even if it remained in Gisborne. Overall,the plant relocation demonstrates the Heinz influence on Watties NZ, especially in terms of accelerating therestructuring of the processing divisions in order to meet investment targets.

10 A considerable amount of land is contracted at some distance to Gisborne, but a sliding payment scale is usedwhich places the burden of extra transport costs onto the grower, not HWL. Consequently, closeness of land to thefactory can be a factor in the overall package as to whether a grower should engage in a contract with HWL.

11

• Land should ideally be situated near to thefactory to assist the logistical management ofthe crop10;

• For organic production (and to a lesser extentfor conventional), HWL preferred to deal withproducers exhibiting a particular ‘mind-set’11.

Although HWL committed most of its promo-tional effort for organics to courting their conven-tional growers, initially they approached long-term organic growers and growers who had noexperience growing sweet corn but had suitableland to convert. This was especially the case ifHWL felt their land could comply with the BIO-GRO certification process quickly because theyhad records showing that chemicals and fertilisershad not been used on it for some time. In fact,HWL’s first organic sweet corn grower (1991/92)did not display a number of the preferred qualitiesas summarised above: his land was 60km north ofGisborne near Tolaga Bay; his property had beenseverely flooded by Cyclone Bola four yearsearlier and suffered drainage problems; and hehad never grown sweet corn. He was also (fortui-tously) interested in experimenting with organicsweet corn for philosophical rather than purelyfinancial reasons.

The grower initially provided about 1.5ha ofBIO-GRO certified land and produced sweet cornat 6t/ha12. The following year the land area wasincreased to 3ha and he achieved 10t/ha (Inter-view 23). After four years he discarded sweet cornproduction for two reasons. First, his main inter-ests were in deer farming and he felt “that thesweet corn thing was a bit of a challenge. After itwas up and running it was no longer a challengeand I didn’t want it to be a distraction from myefforts in organic deer farming13” (ibid.). Second,he had become dissatisfied with the overalldirection of HWL’s sweet corn operation. He is“fundamentally opposed to monoculture and anyoperation that preserved the old paradigm oflarge-scale, soil-compacting horticulture” (Inter-view 23). In the period 1992-1994, two otherindividuals from non-horticultural backgroundsbecame involved in growing organic sweet cornlargely for philosophical reasons, but both havesince pulled out citing philosophical and other

reasons.There is an interesting comparison that can be

made to Canterbury at this point. In Canterbury, anumber of long-term/philosophically-orientedorganic growers produced high crop yields forHWL in the 1990s. In Gisborne, no long-termorganic growers, who were previously inexperi-enced with sweet corn, were able to match theaverage yields of conventional sweet corn growerswho converted to organic production. Conse-quently, HWL Gisborne, even more than HWLCanterbury, began to rely on converting conven-tional growers to advance the company’s strategyfor organic sweet corn.

3.2.2 Attracting Maori land trustsWith those three growers and also with two

conventional growers certifying small portions oftheir properties, HWL could source sweet cornfrom a total of 7ha fully certified and a further15ha of BIO-GRO transitional land for the 1992/93season14. However, this area was too small toensure the sustainability of the project. In solvingthis problem of insufficient supply, HWL Gisborneexplored relatively new territory in terms ofgrower-processor arrangements: it proactivelyassisted Maori land-use trusts on multiply-ownedland into organic production. Despite the fact thatonly a few trusts/incorporations entered intoorganic production in the area, this arrangementand its outcomes are given special attention herefor two reasons. First, with such a large proportionof available land in Gisborne District undermultiple Maori ownership the ability of Maori toenter the industry may be a key factor in the long-term growth of organics in the region. Second, theMaori influence is a local characteristic that sep-arates Gisborne from the three other case studiesin the present series of reports.

The first trust to enter organic production –Paripoupou Station – is representative of thesituation for much of the Maori land in GisborneDistrict (Interviews 7, 9). When the governmentsought to purchase a large block of land rangingfrom Tolaga Bay (50km north of Gisborne) toTokomaru Bay (85km north of Gisborne) in the1860s, a number of Maori owners refused to sell.

11 “We just know often whether they will be able to do it – most can’t. They have to be innovative, the type ofgrower that will chase premiums” (Interview 2). For the specifically organic producers, the need for innovation waseven more apparent: “We do not want growers who are just financially driven to change to organics. The mind-setmust also include a willingness to adapt, to take on a challenge, a preparedness mentally to go against convention.Some conventional growers we recognise do not fit this bill” (Interview 1).

12 A typical conventional sweetcorn property achieves 18t/ha. However, this particular grower was happy withthis as a first effort and considered the premium a bonus.

13 See Section 5.3.1.14 Most of this was to be sold as ‘Transition BIO-GRO’. Although HWL could obtain a premium in Japan for

crops ‘in transition’, this was lower than that which could be achieved if the produce was fully certified. However,HWL was prepared to set the ‘Transition BIO-GRO’ sweetcorn price for its growers at 70% higher than for itsconventional crops (ie. not much lower than the 80% premium for full BIO-GRO certified organic) so that the twoyears of transition would not act as a barrier to growers converting to an organic regime.

12

Even though these owners had a shareholderinterest in the entire block of land, a contractresulted which gave those owners a 120ha ‘reser-vation’ at Three Bridges (Interview 19, Oliver &Thompson 1971:99) – 65km north of Gisborne.Initially, there were 11 owners but over the next70-80 years the number of owners swelled throughmultiple inheritance customs to over 600. In theearly 1950s, the station fell into rates arrears,largely because it was unable to attract loanfinance15 to expand and compete with Pakehastation-farms. A compromise was established inthe Maori Land Court under which the ownerswould retain title but only if they leased the landon a long-term basis to a Pakeha station-farmer.The long-term lease was due to expire in 1992. Inadvance of that date, however, Cyclone Bola(1988) had its greatest impact in the Three Bridgesarea, and up to three metres of silt was depositedon the river flat portion of the property. In theyears between Bola and transference, the leaseecarried out no remedial activities, applied nofertilisers nor chemicals and allowed weeds andtwo metre high rushes to infest the property(Interview 19). When the shareholders – nownumbering over 1000 – regained managementcontrol in 1992 they were in no financial positionto remedy these problems and it was used for littlemore than occasional grazing, with its long-termpotential in some doubt.

HWL became aware of the land through ashare-cropper who desired to grow maize on theproperty as a leasee (Interview 2). When thatindividual asked to switch the contract to organicsweet corn, the shareholders’ trust pulled out ofthe agreement, fearing that control of the landwould again be taken from them on a long-termbasis (Interview 7). At this point HWL – “desper-ate for any potential organic land they could gettheir hands on” – attempted to convince the landtrust to convert to organic production because theland had effectively been in fallow for years(Interview 2). The Paripoupou Trust was initiallyinterested in organics because it thought it wouldbe a labour intensive activity which could be usedto employ some of the large number of localunemployed (Interviews 7, 19). HWL informedthem that this would not be the case becausemechanical methods could be used for weedingand harvesting, but the shareholders’ trust de-

cided to continue with the conversion of theproperty. After several months of negotiations,they agreed to year-by-year contracts with HWLto supply organic sweet corn on 45ha – more thandouble the total of organic and transitional landthat HWL had to that point contracted – but stilllacked the start-up capital to realise their dreams.HWL became relatively proactive at this stage,enacting the following initiatives to ensure thatParipoupou was successful. The company:

• Made internal preparations to loan Paripoupoudevelopment capital if no other source could befound (something it almost never does forconventional growers, Interviews 1, 2);

• Began third party negotiations with the localmember of parliament and Te Puni Kokiri(henceforth TPK)16 to gain Mana DevelopmentFund capital. These negotiations led to asuspensory loan of $100,000 being made byTPK which was used for land restoration,including a requisite drainage program (Inter-views 7, 9, 19). This money also helped thestation gain a $200,000 overdraft from a privatebank;

• Gave Paripoupou an “unusually large amountof advice for their initial learning of growingmethods”, including assistance in finding afarm manager/agronomist to help with finan-cial and crop decisions (Interview 7);

• Mitigated the loss Paripoupou made in the firstyear by writing off the value of seed. Becauseof the late decision to plant organic sweet corn,and the considerable effort required to clear45ha of neglected land and prepare a seedbed,the crops were sown very late in a seasonwhich was unusually cool and wet, resulting ina low-yielding first crop. (Interview 1, 19).

By 1997, Paripoupou had changed its statuswith the Maori Land Court to an incorporation,reflecting its successful standing as a business. Ithad 65ha of BIO-GRO certified land which weresuitable for cropping and had grown sweet cornfor five seasons. The Incorporation has recentlydiversified into squash and peas as part of itsorganic rotation. All concerned parties appearhappy with these outcomes. For its part,Paripoupou overcame its initial problems and inthe third season made a $100,000 profit. Although

15 It is prohibitively difficult for land trusts and incorporations to attract private finance capital as banks arenot prepared to take the risk that is entailed in lending money to managers of land in multiple ownership. Al-though, there have been changes to the appropriate Maori land legislation – especially in the form of the Te TureWhenua Maori Act 1993 – this situation largely remains today.

16 Te Puni Kokiri had itself been restructured in the year before these negotiations and this represented almostthe last payment of Mana funds. The Mana program had been a feature of the old Department of Maori Affairswhich had a proactive developmental mandate and start-up capital for innovative developmental projects on Maoriland. In contrast to this, TPK has basically an advisory role and there is little capital available for Maori today thatwould match this loan. Consequently, there is some doubt as to whether similar operations could eventuate atpresent and the successful conversion to organics by Paripoupou had much to do with serendipity.

13

some of this money has had to be used to over-come a poor 1996/97 season, it has been able topurchase new machinery and “future-proof itselfagainst another Bola by putting a lot of money inthe bank” (Interview 19). The manager ofParipoupou also believes that organics is inkeeping with the stewardship beliefs of Maori onthe East Coast. Both HWL and TPK showcase theproperty as “something special, something uniquewhich shows that Maori can be innovative, thatlarge multinationals don’t have to be rotten andthat both can work together” (Interview 2).

Despite this success, one could not yet claimthat Paripoupou provides a future blueprint fororganic development in the area. Because of thedifficulties experienced in successfully establish-ing Paripoupou as an organic producer, HWL hassubsequently proceeded with caution in dealingwith properties which are characteristic of theMaori norm: land in multiple ownership; landwhich has been damaged by flooding; or ownedby people who are inexperienced sweet cornproducers. Some of these concerns have acted asimpediments to negotiations with land incorpora-tions and HWL have not rushed to repeat theParipoupou situation:

“Paripoupou was a classic case of...‘we’vegot to get this program rolling, we’ll take it!’Well if that same property came up again we’drun a mile because the land is too marginaland the start-up costs too high” (Interview 8).

“Well it happened because we had to gofrom nothing to something right away. Andgetting conventional growers to go organic onany sort of scale at all takes time. Now that wehave sufficient conventional growers that haveconverted we are not likely to go to the sameeffort again” (Interview 2).

There were a number of other reasons whichconcerned HWL managers and agronomists aboutdealing with Maori land. Other individuals fromMaori land trusts had contacted HWL and hadpromised considerable amounts of flat land thatcould go through the BIO-GRO process quicklybut, on further investigation, HWL found thatthese agents had no authority to do so (Interviews2, 8). Some Maori owners were also reported toexpect HWL to incur more of the start-up costthan was usual. During this period, HWL rejectedan offer of 800ha – which would have doubledHWL’s contracted organic land – from anotherincorporation primarily because its location nearRuatoria was too far from the factory, but alsobecause of other prevailing concerns about Maoriincorporations (Interview 2).

Perhaps the greatest threat to the potential fororganics on Maori land came from difficultiesexperienced by a second incorporation to attempt

organic production. From 1994, that incorporationstarted to convert land previously unused or usedfor pastoral farming and in 1994/95 producedtransitional sweet corn for HWL. However, it hada strong desire to be more than just a ‘supplier’ ofan input without a value-added component(Interview 7). Having attracted a loan from agovernmental source, it invested large sums ofmoney in a slush-ice machine for the export oforganic broccoli, with the desire to grow, processand market produce itself. It also invested heavilyin mechanical weeders and other horticulturalmachinery. With little knowledge of horticultureor international marketing and with a sizeableexposure in terms of fixed-capital, the secondincorporation lost a considerable amount ofmoney in the 1996/97 season (Interviews 7, 19)and was subsequently dropped by HWL for being“too risky to deal with” (Interview 8). It willcontinue to operate for the 1997/98 season and itsmanagers still believe in their ability “to cut outthe middle-men: the processors and the market-ers” (Interview 4). Given three years of heavylosses, this belief seems somewhat naive. Thelosses have led to processors and packers whomight otherwise have considered fostering Maoriorganics to be wary about dealing with all Maoritrusts/incorporations (Interviews 4, 7, 9).

Given the extent of Maori land, and also theMaori desire to become involved in organicswhich is seen by some to “conform to our environ-mental ethos” (Interview 9), there is significantpotential for organic agriculture on Maori land inGisborne District. After a cooling off periodfollowing the effort to establish organic produc-tion on the two properties, HWL has recentlyattempted to re-establish the development oforganic sweet corn production on other Maoriland. In 1995, an incorporation approached HWLwith land that met HWL’s criteria, but the result-ing HWL offer was met by a better offer fromanother processor not involved in organics (Inter-view 2). Another venture emerged in Wairoawhere HWL began to lease land from local Maoriowners (several properties having multipleownership arrangements) and to develop whatwas again silty, weed-infested land, for sweet cornproduction. In this development, the local ownerstook no part in the actual production of sweet cornbut simply held the leases and cooperated withHWL’s contracting arrangements. By 1997/98, thisdevelopment included five properties and 100haof land in transition to BIO-GRO certification forsweet corn. The Wairoa project is seen by HWL asan experiment which may overcome some of theperceived difficulties in working with land that is:in multiple ownership; run by committees; poorlydeveloped because of restraints on the owners’ability to raise finance capital; and owned bypeople with no prior experience of sweet cornproduction, but with a desire to become involved

14

in organics (Interview 1).The various successes and failures in the

developing relationship between HWL and Maoriincorporations indicate both the positive potentialof such relations and the barriers that need to beovercome for these developments to continue. Avital factor in Paripoupou’s success was Manafunding, and while HWL was prepared to con-sider a loan in 1992, its supply base is now morefirmly established and such an offer is not likely toeventuate in the future. The Wairoa developmentindicates a possible new phase in this relationship.Recent decisions by the BIO-GRO board to allowcertification of long-term leased land have enabledHWL to consider leasing land from both Maoriand non-Maori owners.

Leasing of land allows some concerns to beovercome that have acted as barriers to HWLconsidering Maori land17, and this may increasethe number of hectares of organic land owned byMaori incorporations in the future. However,while this will extend organic production, thelease arrangement will almost certainly not carrythe same range of benefits for Maori developmentthan the alternative model evidenced byParipoupou. It can be argued that HWL’s newdirection towards leasing Maori land rather thanallowing local owners to work the land them-selves is overly cautious and it will be perceivedby some as paternalistic. In recent years, there hasbeen a groundswell of Maori concern in Tairawhitiover incorporations that seek profit over employ-ment in their use of Maori land (Coombes 1997).While the Paripoupou example yielded little interms of employment, it represented a directionthat would be far more acceptable to the impover-ished Maori that have fuelled this groundswellthan leasing. More importantly, Ngati Poroudevelopment since 1945 has suffered because of aforced dependence on leasing. For this reason,many local Maori will be unimpressed with a newdirection towards leasing, even if such a directionappeals to their trustees whose range of options isseverely limited by the Te Ture Whenua MaoriAct.

3.2.3 “Grow Organic with Watties”The recruitment of growers for organic pro-

duction in Gisborne differs to the pattern seen inCanterbury where a variety of possible growerswere contracted in the initial rush to build asupply base (even though these growers wereoften, in hindsight, less than suitable). In Canter-bury, it was eventually recognised that the mainpotential for boosting grower numbers lay withthe company’s established conventional growers.Because of the absence of a significant group ofestablished long-term organic growers inGisborne, HWL recognised from the outset thatconventional growers would most closely conformto the desired criteria for converting to organicsweet corn production. GOWW is a promotionaland literature campaign developed in response todifficulties experienced in recruiting growers forHWL’s organic program. Its main goals are todispel misinformation about organic productionand to transfer organic information to growers18.As such, it was primarily targeted to conventionalgrowers who had long-standing relations withHWL, especially those that were consideredinnovative and who might follow the lead of thecompany (Interview 1). It included a series ofinformational brochures which were sent togrowers and outlined the premiums for – and thesmall amount of change required to enter – or-ganic agriculture, but also included group discus-sions, a media campaign, showcase exhibits oforganic farms and public lectures. Private andindividual negotiations with growers have alwaysbeen the primary strategy of HWL recruitment.From 1993 the more organised and broad ap-proach of GOWW contributed to an increasednumber of conventional growers interested inorganic production contacting the company.

The component of the GOWW strategy that, inhindsight, was of most interest to many growers,was the promotion of a premium for organic overconventional production19. It had been consideredby HWL Gisborne that conventional growers wereunlikely to convert to, and sustain, organic pro-duction unless there was a net premium of around20-25% (Interview 2). This incorporated the need

17 It is possible that leasing will also be positively perceived by some Maori growers and, in certain circum-stances, by BIO-GRO NZ. Because of the underdeveloped state of some Maori land, potential growers may beborderline in terms of whether they would be certified by BIO-GRO NZ. In this context leasing could reduce thestart-up risk for both HWL and the land owners and provide a better chance of certification for the land owner at alater date, after HWL has dealt with land-based impediments to organic production. It is probable that BIO-GROwould favour this use of leasing as a stepping-stone to organic production by the land owner. However, it is tooearly to tell whether this scenario will be a reality and it is unlikely that more than a few Maori incorporations,which become involved in organics through leasing, will eventually adopt organic production in their own right.

18 For further information see Report No. 1 (Campbell 1996:25ff).19This has, at times, been a contentious issue. Both in Canterbury and Gisborne, there was some debate within

HWL as to the extent to which the premium should be used to convert growers. Some argued that the premiummight not last in the long-term and that growers should convert for other reasons. Others countered that many ofthe growers were primarily interested in the premium, and some agronomists based their discussions with inter-ested growers around the potential premiums.

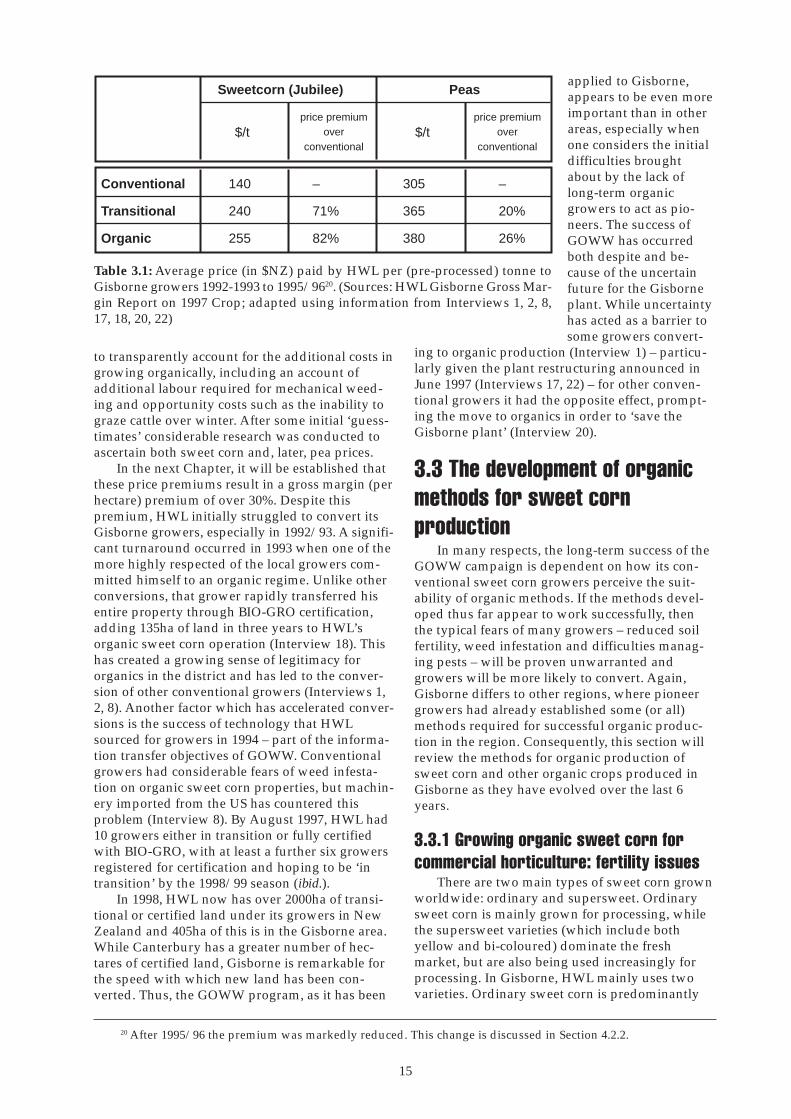

15

to transparently account for the additional costs ingrowing organically, including an account ofadditional labour required for mechanical weed-ing and opportunity costs such as the inability tograze cattle over winter. After some initial ‘guess-timates’ considerable research was conducted toascertain both sweet corn and, later, pea prices.