Embed Size (px)

Citation preview

Redevelopment/Joint Development of Real

Estate

By CA Anil Sathe

SCOPE

Taxation aspects of Redevelopment/Joint Development in the case of :-

• Owner - Individual

• Co-operative Housing Society

• Members of the Society

• Tenants

• Issues u/s 43CA & 50C

CA Anil Sathe

Impact of decision in CIT VS BalbirSingh Maini 398 ITR 531 (SC)

Key takeaways of the decision:

a. In order to qualify as a transfer of a capital asset u/s 2(47)(v), an agreement of the nature referred to Sec. 53A must be a registered agreement.

b. The object of Sec. 2(47)(vi) is to bring within the tax net a de facto transfer of any immovable property. The idea is to tax transactions where, although the title may not be transferred in law, but in substance, the title is transferred .

c. For capital gains to be charged, profits & gains must arise i.e. they must either be received or accrued. CA Anil Sathe

Redevelopment Agreements - Individual

Issues:

In the case where there is a plot of land with a structure, the tax consequences in the following situations will be different :-

1. Both, land as well as structure, are sold/transferred;

2. Structure is demolished by the owner & the land is transferred;

CA Anil Sathe

Redevelopment Agreements - Individual

(Continued)

3. The owner reserves a part of the development potential to himself;

4. Consideration is monetary and/or is in the form of a constructed area.

CA Anil Sathe

Redevelopment Agreements

Tax issues in typical situations in Mumbai:

1. Building in which some units are occupied by owners & others are occupied by tenants.

2. Consideration receivable in monetary terms as well as in the form of residential units by the owners.

3. Permanent alternate accommodation received by the tenant.

CA Anil Sathe

Joint Development Agreements

Implications of Sec. 45 (5A) of the Income Tax Act, 1961 where capital gain arises to an individual or a HUF, from transfer of a capital asset, being land or building, under a specified agreement -

• Capital gains are chargeable in the year in which certificate of completion for whole or part project is issued by the Competent Authority;

CA Anil Sathe

Joint Development Agreements

(Continued)

• Consideration shall be deemed to be the stamp duty value, of the share of the individual, as on the date of issue of the certificate as increased by the monetary consideration.

CA Anil Sathe

Joint Development Agreements

There are several issues as regards to Sec. 45 (5A), few of them being:

1. What would be the position if the owner has undertaken some development activity and thereafter enters into a development agreement?

2. What would be the position if an Occupancy Certificate is received, but the Completion Certificate has not yet been received?

CA Anil Sathe

Joint Development Agreements

3. What is the date of transfer u/s 45 (5A) ?

4. If completion certificate is not received, but a phase of a project is complete & the owner disposes off the units allotted to him, then what would be the position?

CA Anil Sathe

Issues in regard to Capital Gains in the hands of Landlords

• Scope of sec. 2(47)(v) - Is registration of Development agreement necessary for applicability of sec. 2(47)(v).

• Meaning of term “possession” in context of Sec. 2(47)(v).

• Explanation 2 to sec. 2(47) inserted by FA 2012.

CA Anil Sathe

Issues in regard to Capital Gains in the hands of Landlords

Point of accrual of income:• Date of execution of the Development Agreement.

• Date of handing over of possession of land to developer.

• Date of handing over of possession of land to developer together with a General Power of Attorney authorizing him to transfer his share of property.

• Date on which the first sale deed is executed for undivided share in land for the developer’s share.

• Impact when major / entire consideration has passed.

CA Anil Sathe

Redevelopment –Co-operative Societies –Tax Issues

• Legal title of both land and structure belongs to the society.

• Beneficial ownership of the residential units vests with the members of the society.

• Consideration paid to the Society in monetary terms for grant of development rights.

• Consideration paid to the society for permitting use of TDR acquired by the developer in the reconstruction process.

• Consideration in non-monetary terms –Community hall, etc. CA Anil Sathe

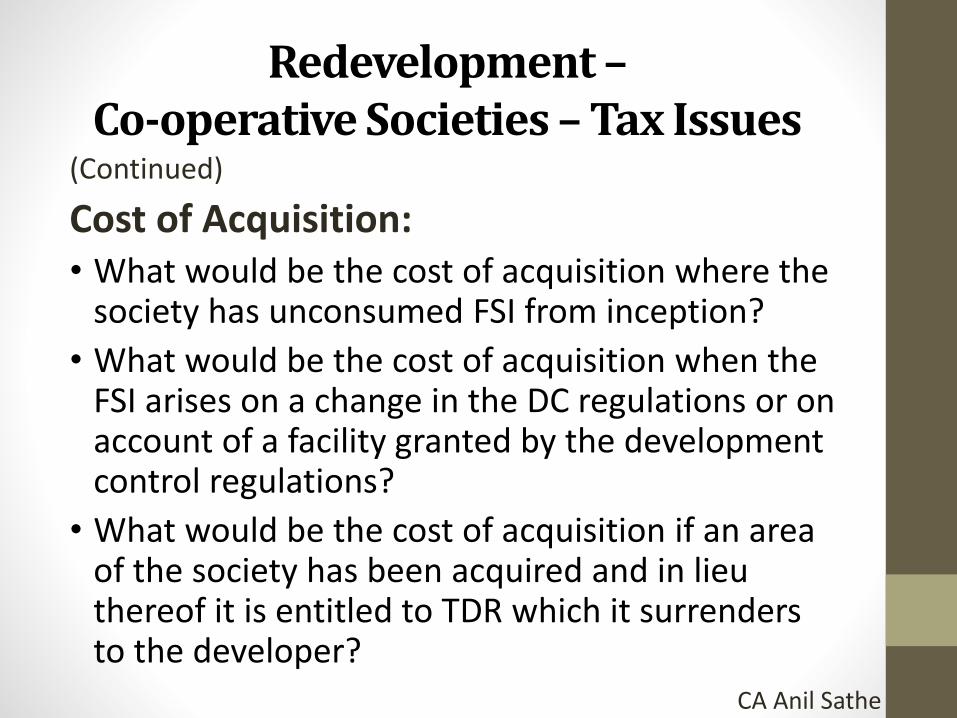

Redevelopment –Co-operative Societies –Tax Issues

(Continued)

Cost of Acquisition:• What would be the cost of acquisition where the

society has unconsumed FSI from inception?

• What would be the cost of acquisition when the FSI arises on a change in the DC regulations or on account of a facility granted by the development control regulations?

• What would be the cost of acquisition if an area of the society has been acquired and in lieu thereof it is entitled to TDR which it surrenders to the developer?

CA Anil Sathe

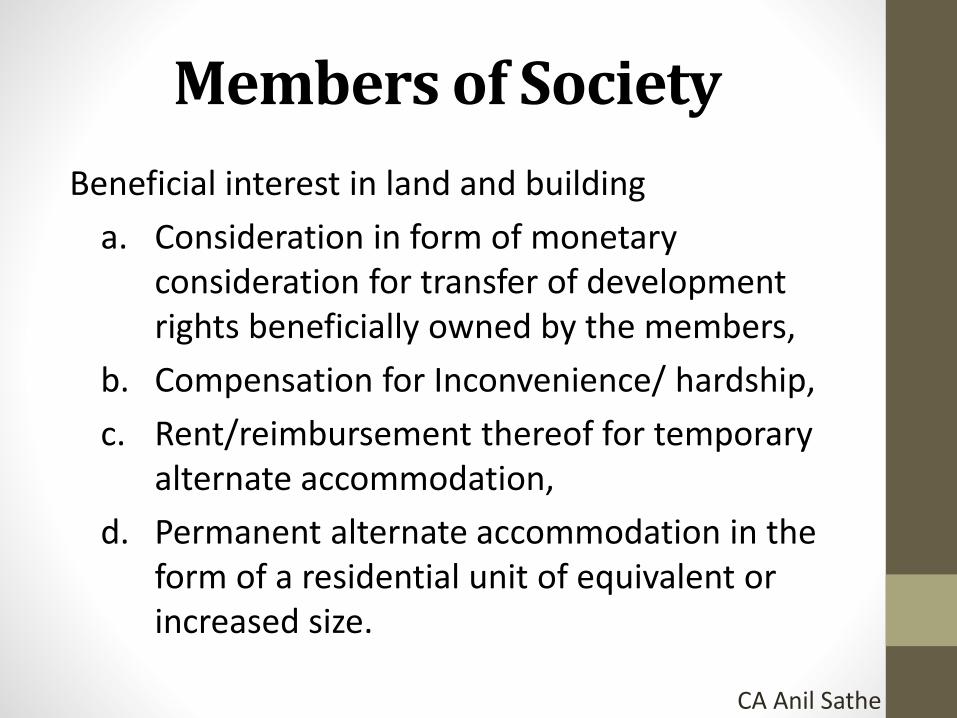

Beneficial interest in land and building

a. Consideration in form of monetary consideration for transfer of development rights beneficially owned by the members,

b. Compensation for Inconvenience/ hardship,

c. Rent/reimbursement thereof for temporary alternate accommodation,

d. Permanent alternate accommodation in the form of a residential unit of equivalent or increased size.

Members of Society

CA Anil Sathe

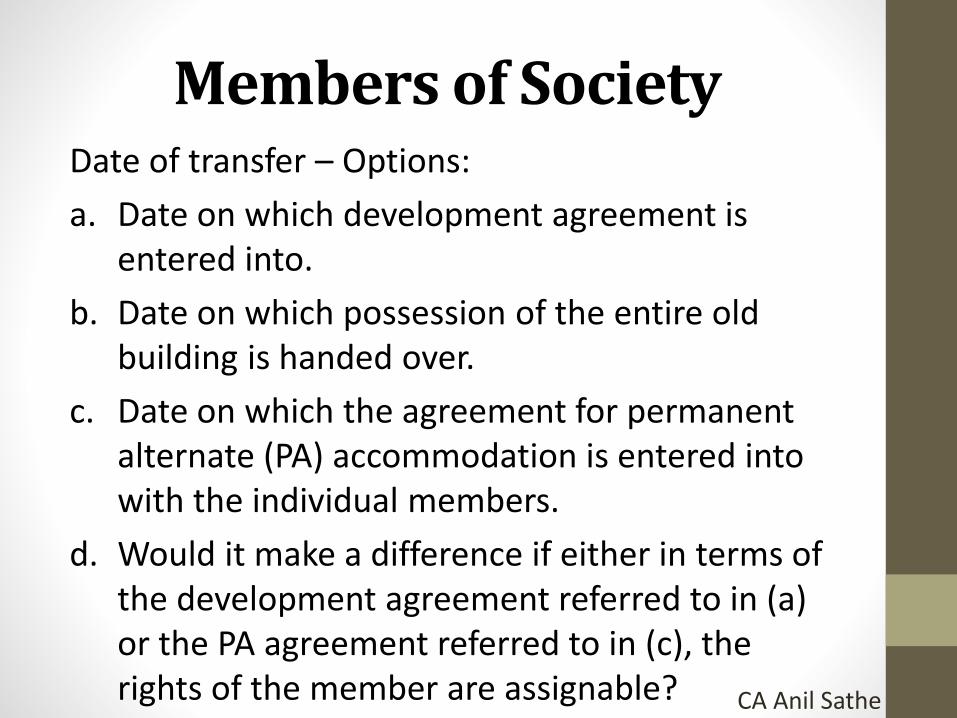

Date of transfer – Options:

a. Date on which development agreement is entered into.

b. Date on which possession of the entire old building is handed over.

c. Date on which the agreement for permanent alternate (PA) accommodation is entered into with the individual members.

d. Would it make a difference if either in terms of the development agreement referred to in (a) or the PA agreement referred to in (c), the rights of the member are assignable?

Members of Society

CA Anil Sathe

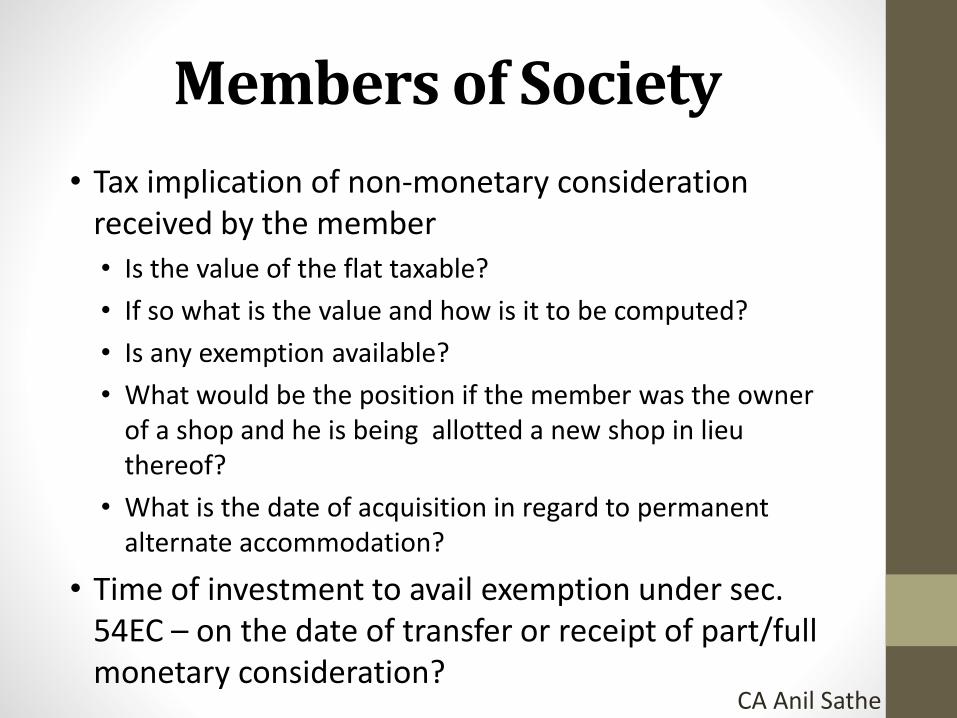

• Tax implication of non-monetary consideration received by the member

• Is the value of the flat taxable?

• If so what is the value and how is it to be computed?

• Is any exemption available?

• What would be the position if the member was the owner of a shop and he is being allotted a new shop in lieu thereof?

• What is the date of acquisition in regard to permanent alternate accommodation?

• Time of investment to avail exemption under sec. 54EC – on the date of transfer or receipt of part/full monetary consideration?

Members of Society

CA Anil Sathe

Redevelopment Tenants• Tax implications in hands of tenants when tenants receive

consideration and vacate the premises.

• Tenants exchange their tenancy rights with ownership rights.

• Accrual of capital gains on surrender of tenancy rights –liable to capital gains tax.

• Merger of inferior right into superior right – whether CG liability arises – CIT vs. Dr.D.A. Irani 234 ITR 850 (Bom.)

• Tenant receiving cash compensation & permanent alternate accommodation – Relief under sec. 54/54F/54EC.

• Manner of receipt of cash compensation - Can whole or part of it can be treated as capital receipt?

• Tenant receiving cash compensation + ownership premises

CA Anil Sathe

Redevelopment Tenants -Issues

• The surrendered premises is

• residential premises,

• residential premises used for personal business by the tenant,

• commercial premises.

• What would be date of the transfer of tenancy rights?

• Date of surrender of possession, or

• Date of allotment of re-developed property? CA Anil Sathe

Section 43CA

• Applies in the case of transfer of an asset (other than a capital asset), being land or building or both.

• Stamp duty value adopted/assessed/assessable to be deemed as the value of consideration.

• The consideration so adopted is to be used for the purpose of computation of profits & gains of business or profession.

CA Anil Sathe

Section 43CA - Issues

• Will the term land & building include development rights?

• What is the meaning of the term transfer in the context of Section 43CA?

• If there is a difference in the consideration as stated in the agreement and the stamp duty value, in which year is such difference to be submitted to tax?

CA Anil Sathe

Section 50C - Issues

• Will it apply to:

1. Tenancy rights?

2. Leasehold rights?

3. Development rights?

4. FSI/TDR?

• What is the position of deemed consideration qua claim u/s 54/54EC/54F?

CA Anil Sathe

THANK YOU

CA Anil Sathe