Embed Size (px)

DESCRIPTION

Devices for Dissonance :. Reflexive Modeling and Systemic Risk. Daniel Beunza & David Stark. Dissonance. Dissonance fosters discovery by prompting reflexivity. Dissonance. Dissonance fosters discovery by prompting reflexivity. - PowerPoint PPT Presentation

Citation preview

Reflexive Modeling and Systemic Risk

Daniel Beunza & David Stark

Devices for Dissonance:

Dissonance

Dissonance fosters discoveryby prompting reflexivity.

Dissonance

Dissonance fosters discoveryby prompting reflexivity.

Disagreement about what is valuablemakes it possible to discover new resourcesof value.

How do traders deal with the fallibility of their models?

In the literature, disasters are traced to the behavior of traders, depicted as

1) reckless

In the literature, disasters are traced to the behavior of traders, depicted as

1)reckless

and as

2) overly cautious (“herding”)

Processes that provoke doubtcan lead to overconfidence

Reflexivity about Models

This is a pipe organ in largest hall of Moscow House of Music. Posted by Irina at 20:55

Labels: instuments, theatre

This is a pipe organ in largest hall of Moscow House of Music. Posted by Irina at 20:55

Labels: instuments, theatre

[a declarative speech act]

“I apologize.”

“I apologize.”

[a performative speech act]

Performativity in economic sociology:

Financial models are not representations. They are interventions that format, shape, perform markets. Their use brings new economic objects (markets) into being.

Models are market making.

“This is the way that people get from point A to point B.”

A model is performative when its use increases its predictive capabilities.

This is a pipe organ.

A financial model is not a representation;

A financial model is not a representation; it is an intervention.

The arbitrage traders we studied do the same.

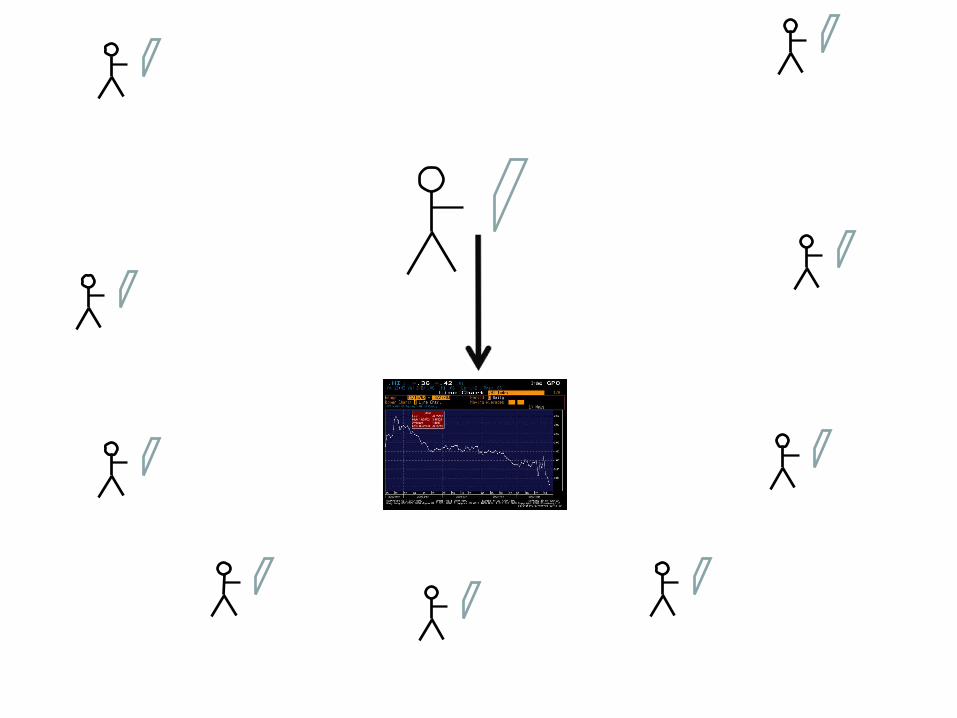

The trading room is populated with devices for doubt.

Traders do not simply use models and devices that perform the market. They also create and use devices for reflexivity.

This reflexivity is not exterior to (or above) the structures of socially distributed calculation but is an integral part of it.

Arbitrage is a (reflexively) skilled performance.

And this reflexivity is not of the individualbut is social and material.

Epistemic challenges of using models in arbitrage

Methodological constraint: a single morning at a single desk in an abritrage trading room.

Calculation in merger arbitrage involvesthe dissonance between two sets of probability estimates:

1) probability estimates derived at the desk using proprietary models, databases, and instrumentation.

2) “implied probablity” – the aggregate probability estimates of the trader’s rivals

a given trading desk makes probability estimates based on models, proprietary databases, and instrumentation

V= (1-)PNS +PS

The trader’s models and instrumentation are powerful scopes for viewing the markets.

But scopes that reveal can also conceal. If you take your model for granted, you can lose your shirt.

To avoid cognitive lock-in, the traders turn to socio-technical networks outside the trading room.

relation between the trader and his rivals

The spread plot in merger arbitrage

The spread plot is a representation of an economic object that does not have a price and is otherwise not observable, co-produced by the positioning of actors who use it to confront their interpretations and re-evaluate their positions.

time

$

Target

Acquirer

Decoding the spread plot

“Backing out” implied probability

The spread plot instantiates the diversity of dispersed anonymous actors.

dissonance

Reflexive modeling

Dissonance disrupts.

It prompts reflexivity.

Each of the (materially mediated) relations provokes reflexivity about the other.

?

re-search

Reflexive modeling

Differs from ‘herding’

Here, dissonance prompts re-search

Reflexivity is not self-awareness or conceptual transcendence.

So as not to be captive of an epistemic trap, traders use devices for dissonance.

?

?

?

WARNING

WARNING

The same devices for doubt can also be devices for overconfidence, leading to arbitrage disasters.

The strength of reflexive modeling is based on the fact that it leverages the cognitive independence among dispersed and anonymous actors.

The strength of reflexive modeling is based on the fact that it leverages the cognitive independence among dispersed and anonymous actors.

But this same process suggests the possibilities of cognitive interdependence among the rival traders in the professional arbitrage community.

Just as reflexive modeling can typically be a source of correction, so this same cognitive interdependence among traders can, in rare but dramatic instances, lead to the amplification of error.