Embed Size (px)

DESCRIPTION

“Refocusing the ECB on output stabilisation and growth through inflation targeting”. Jörg Bibow, Franklin College Switzerland Delivering the Lisbon goals: The role of macro economic policy making 1-2 March 2005, Brussels, CES-ETUC. Inflation targeting [IT] – or not?. - PowerPoint PPT Presentation

Citation preview

1

“Refocusing the ECB on output stabilisation and growth

through inflation targeting”

Jörg Bibow, Franklin College Switzerland

Delivering the Lisbon goals: The role of macro economic policy making

1-2 March 2005, Brussels, CES-ETUC

J Bibow, Franklin College ETUC, Brussels 2 Mar 2005

2

Inflation targeting [IT] – or not?

• Many observers view ECB as an inflation targeter by deeds even if not by words – this is wrong!

• ECB rejects IT and follows ‘two-pillar strategy’ instead, claiming that by delivering on primary goal of price stability it would thereby also fulfil its growth & stabilisation mandate – wrong too!

• What may be right though is that imposing IT upon the ECB could lead to both better growth as well as inflation performance in future.

J Bibow, Franklin College ETUC, Brussels 2 Mar 2005

3

ECB: Inflation targeter in disguise?

• Some observers believe that ECB’s interest rate policies (its ‘deeds’) have been much in line with what IT would have required (CEPR etc).

• In this view, ECB – for some reason – tries to obfuscate its IT approach; lack of transparency and bank’s confusing ‘words’ are regrettable.– That the ECB ‘allowed’ inflation to stay above two

percent for five years in a row is seen as evidence for flexible approach to IT and concern for growth.

J Bibow, Franklin College ETUC, Brussels 2 Mar 2005

4

Actually, ECB’s words & deeds do match – but are both inappropriate!

• From the beginning M3 pillar was meant to continue Buba tradition of hiding policy discretion behind pseudo-monetarist veil.

• From the beginning price stability pillar fully reflected another Buba tradition, namely that sound (‘stability-oriented’) monetary driver is quick in hitting the brake, but abstains from using accelerator – ASYMMETRY!!!

J Bibow, Franklin College ETUC, Brussels 2 Mar 2005

5

Why asymmetry worked for Buba

• Buba approach worked fine for Germany when nominal exchange rates [ER] were stable, trading partners’ inflation higher, and accelerator applied skillfully ‘elsewhere in the world economy’. Troubles emerged as partners’ inflated converged a/o

ER developments put spanner in the works.

• While lacking any skills & experience in properly managing the economy, Buba held a big success. Buba & Buba wisdom blueprint for Maastricht EMU!

J Bibow, Franklin College ETUC, Brussels 2 Mar 2005

6

What Maastricht meant

• To Germany – exporting Buba ‘success story’ undermined its working at home– Provoking deflation as Germany stubbornly goes old way …

• To Euroland – emulating Buba ‘success story’ = asymmetric ‘management’ of domestic demand– Mr Buba Otmar Issing represents this ‘culture’ 100%

• To rest of world – as German disease spreads rudderless economic giant drifts along hoping for strong enough export currents to pull it along– Global imbalances …

J Bibow, Franklin College ETUC, Brussels 2 Mar 2005

7

Understanding the current mess

• Neither ‘external shocks’ nor ‘structural problems’ are to blame

• Instead ECB’s asymmetric policies key to protracted domestic demand stagnationSeries of severe policy blunders

• Imposing IT upon ECB should stop it from reneging on its growth & stabilisation mandate, and lead to better inflation performance too!

J Bibow, Franklin College ETUC, Brussels 2 Mar 2005

8

What inflation targeting is all about

• Forward-looking: keeping tomorrow’s rather than yesterday’s inflation stable around target – ‘Inflation forecast targeting’– Symmetry – deviations in either direction unwelcome

• Inevitably, any short-term inflation forecast derived from forecasted evolution of economy.

• Effectively, IT means actively managing aggregate demand and employment, and thereby inflation – requiring skills & competence!

J Bibow, Franklin College ETUC, Brussels 2 Mar 2005

9

Bank of EnglandInflation targeting success story

• Publication of MPC’s forecast of inflation two years out – basis of policy & communication– Model of transparency & openness in all respects– Frequent & symmetric interest rate adjustments – Smooth cooperation with fiscal policy– Robust and fairly stable wage inflation

• Outcome: Very stable nominal (& real) GDP growth, high employment, and low inflationNB: UK’s problems relate to operating in the

immediate vicinity of stagnating economic giant.

J Bibow, Franklin College ETUC, Brussels 2 Mar 2005

10

IT not at all what ECB does! Revisiting ECB’s key blunders

• (1) Market opposition and the ‘euro puzzle’ • (2) Productivity slump boosts core inflation• (3) Stagnation pushes ‘Instability & Stagnation

Pact’ into reverse gear – ‘tax-push inflation’

• Result: ECB low on ammunition as strong euro prevents yet another free-ride on successful US demand management – euro area seems trapped in a vicious circle of its own making!

J Bibow, Franklin College ETUC, Brussels 2 Mar 2005

11

Blunder no. 1: Crashing the euro

• ‘Repeating a pattern observed in 1999 and 2000, monetary policy decisions and interest rate differentials [in 2001 too] appeared to influence exchange rates mostly through their effect on growth expectations’ (BIS 2002: 86).

J Bibow, Franklin College ETUC, Brussels 2 Mar 2005

12

• After nearly doubling policy rates within 11 months, thereby crushing domestic demand, ECB had trouble getting its foot off the brake (not to mention using the accelerator as aggressively).

• ECB’s ‘caution’ provoked severe productivity slowdown and corresponding rise in unit-labour costs and core inflationECB’s rear-mirror view meant more ‘caution’, and

hence more stagnation too ...

Blunder no. 2: ‘wait and see’

J Bibow, Franklin College ETUC, Brussels 2 Mar 2005

13

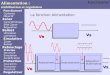

Business of keeping up margins!

Despite very low & stable wage inflation, ‘preemptive’ punishment of employees!

Wait and see as productivity slump pushes up core inflation

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Sources: Eurostat, ECB

annu

al p

erce

ntag

e ch

ange

s

negotiated wages

ulc (MA4)

core HICP

J Bibow, Franklin College ETUC, Brussels 2 Mar 2005

14

Blunder no. 3: ‘tax-push inflation’

• As ‘first line of defense’ (Koehler, IMF) fails, Buba fiscal wisdom kicks in with a vengeance

• Among ever more desperate but vain attempts at pro-cyclical consolidation, hikes in indirect taxes and administered taxes feature prominentlyConspicuous phenomenon: ‘tax-push inflation’

• This upward distortion in headline HICP is behind ECB’s astonishing failure on its primary goal!Clearest evidence on counterproductive macro

policies!

J Bibow, Franklin College ETUC, Brussels 2 Mar 2005

15

Reneging on growth may not pay offA central bank standing in its own way

Misses on ECB's primary objective in 2002-4 owe primarily to tax-push inflation

0

0.5

1

1.5

2

2.5

3

3.5

Source. ECB, EurostatNote. Taxes on tobacco products and measure of administered prices within the services sector (aggregate HICP weight of 5.6%) included here most likely underestimate true tax-push inflation.

Ann

ual p

erce

ntag

e ch

ange

s

headline HICP

HICP excl. tax-push

ECB ceiling

0.7%

Mind the gap!‘tax-push inflation’

J Bibow, Franklin College ETUC, Brussels 2 Mar 2005

16

Monetary & fiscal policy interaction à la Buba/Maastricht

J Bibow, Franklin College ETUC, Brussels 2 Mar 2005

17

What proper inflation targeter would NOT do:

• Misread & provoke markets so that currency crash pushes inflation up

• Carelessly & needlessly provoke productivity slump that pushes inflation up

• Ignoring stagnation and unemployment since resulting fiscal squeeze pushes inflation upEven for the sake of maintaining price stability itself

proper inflation targeter has an interest in sustaining growth & employment, and thereby low inflation.

J Bibow, Franklin College ETUC, Brussels 2 Mar 2005

18

IT and wages – two cases• (1) Wages responsive to economy – both ways!

– Implies linear (upward-sloping) supply curve– This should go with relatively higher inflation target

• (2) Wage inflation unresponsive to economy– Implies nonlinear supply curve (with flat range)– Wage rigidity provides safeguard against deflation,

allowing a relatively lower inflation target. Keynes (1936, ch. 19) argued that case (2 – stable wage unit) actually

makes it easier to run stabilising monetary policy.

J Bibow, Franklin College ETUC, Brussels 2 Mar 2005

19

Euroland: Stable & (too) low wage inflation – and asymmetric MP

Output & employment costs due to two factors:

• (1) price ceiling (‘below 2%’) may be too low

• (2) interest-rate policies asymmetric and systematically misguided VERY ‘forward-looking’ on output recovery & inflation risks

Complacent about slump and deflation risks

• Anti-growth bias even costly in terms of inflation Inflation above two percent for five years is really a miracle!

• Employees/consumers hit by double-whammy!!!

J Bibow, Franklin College ETUC, Brussels 2 Mar 2005

20

Perhaps better end this folly?

J Bibow, Franklin College ETUC, Brussels 2 Mar 2005

21

So what to do about it? Structural reform!

• (1) institutionsEnd antiquated Buba-style central bank independence,

i.e. ‘Unbounded discretion’ & despotism in MP• Both undemocratic & economically inefficient!• Bank of England may serve as model of CBI

Impose IT upon ECB!

• (2) personalitiesEnd series of ‘accidents of personality’(MF) in FrankfurtSelect central bankers who are willing and able to

MANAGE the economy and thereby inflation, since that is what is required – inevitably!

– Please refer to www.levy.org for my research working papers on EMU.