Embed Size (px)

Citation preview

Regional Corridors in South Asia: Regional Cooperation Agenda

Prabir DeRIS, New Delhi

Presentation at 5th South Asia Economic Summit (SAES)

September 11-13, 2012Islamabad, Pakistan

South Asia has high unrealised tradeCountry 2010 2010 2017 P/A

Unrealized trade, 2010

(US$ billion) (US$ billion) (US$ billion) (2010) (%)Actual trade

(A)Potential trade (P)

Potential trade (P)

Afghanistan 8.74 20.04 36.92 2.29 56.39

Bangladesh 42.44 87.10 123.48 2.05 51.28

Bhutan 1.49 2.98 21.00 2.00 49.97

India 573.71 798.98 2163.58 1.39 28.19

Maldives 1.37 2.20 7.43 1.60 37.66

Nepal 4.46 13.78 69.62 3.09 67.62

Pakistan 65.28 90.14 165.63 1.38 27.58

Sri Lanka 23.91 44.92 268.11 1.88 46.78

Total 721.40 1060.14 2855.77 1.4 45.68

Note: Based on a gravity modelSource: Author

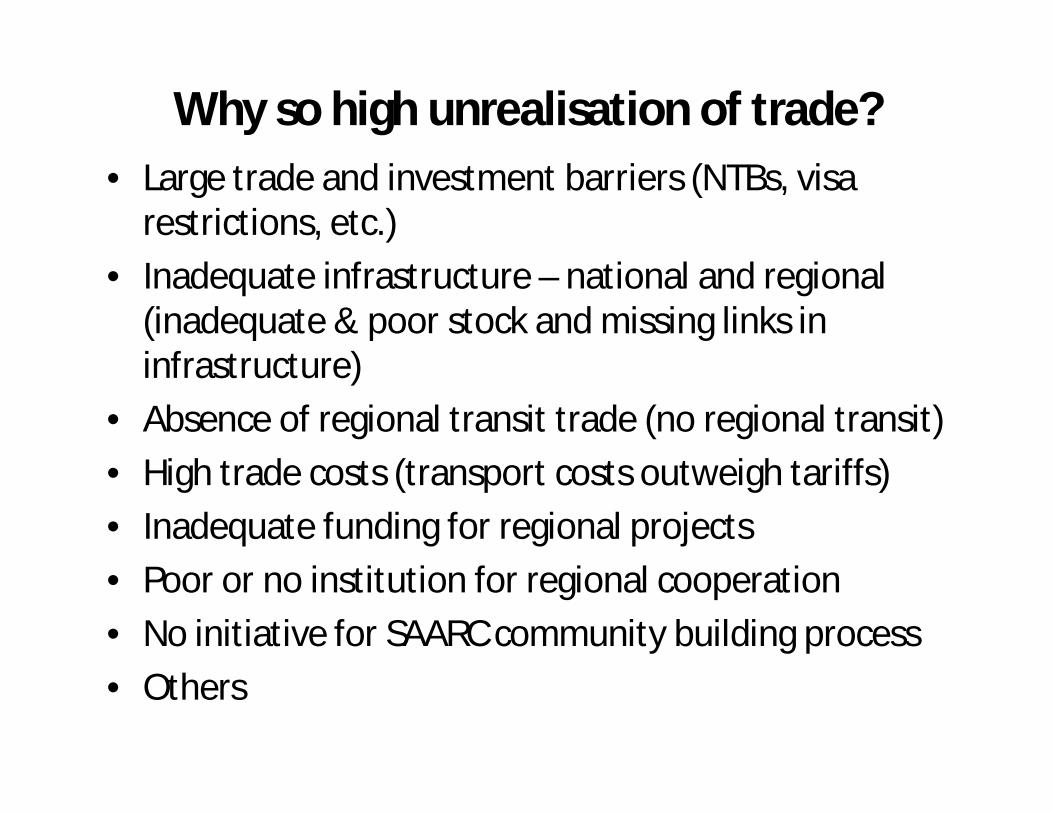

Why so high unrealisation of trade?• Large trade and investment barriers (NTBs, visa

restrictions, etc.)• Inadequate infrastructure – national and regional

(inadequate & poor stock and missing links in infrastructure)

• Absence of regional transit trade (no regional transit)• High trade costs (transport costs outweigh tariffs)• Inadequate funding for regional projects• Poor or no institution for regional cooperation• No initiative for SAARC community building process• Others

Example - NTBs in India – Pakistan trade (1/2)

Tariff barriers

Customs dutiesSpecial additional duties (SAD)Countervailing duties

Non-tariff barriers

Stringent visa regimesTrade distorting subsidiesOverland transportation limitationAir travel restrictionSea transportation restriction Transit restrictionPort of call restriction

Finance measures

Cumbersome payment systemsRestrictive official foreign exchange allocationRegulations concerning terms of trade for import paymentsNon-acceptance of letter of credit High commission of foreign banks offering letter of creditLack of bank branches

Quality control measures

License with no specific ex-ante criteriaLicense for selected importersSanitary and phytosanitary measures

Technical barriers to trade

Marking requirementsLabeling requirementsTesting, inspection and quarantine requirementsPre-shipment inspection/certificate acquisition

NTBs in India – Pakistan trade (2/2)

Source: De, Raihan and Ghani (2012) ‘What does MFN Trade mean for India and Pakistan? Can MFN be a Panacea?’ Mimeo, World Bank, Washington, D.C based on Taneja (2012), Khan (2011), Husain (2012)

Example - Poor connectivity in India –Pakistan

Sector Particular

Road transportation (passenger bus services)

Delhi – Lahore

Amritsar-Nankana Sahib

Amritsar – Lahore

Poonch – Rawalakot*

Srinagar – Muzaffarabad*

Rail transportation (passenger train services)

Delhi – Lahore

Munabao - Khokrapar

Shipping links Mumbai – Karachi

Air links

Delhi – Lahore

Mumbai – Karachi

Gas pipeline TAPI*

Electricity links Amritsar – Lahore*

Border (land) customs for trade

Wagah – Attari

Poonch - Rawalakot

Srinagar - Muzaffarabad

Monabao- Khokhrapar*

*Proposed / to be operational Source: Updated from De (2009)

Some major challenges (micro level) to trade in South Asia

1. Lack in simplification and harmonization of trade procedures, more particularly at the border.

2. No regional transit as yet3. Absence of regional corridor and modern

corridor management techniques4. No master plan for SAARC connectivity as yet5. Lack of financing and no resource mobilisation

plan for implementing regional connectivity projects

6. No regional institution for trade facilitation.

Definition, Rationale, & Literature

Regional corridors - definition

Economic corridor = Sum over all public capital, national or otherwise

Transport corridor Institutional infrastructure

Communication infrastructure

Trade corridor

Human infrastructure

GMS EWEC

n

iiXY

1

Transport corridor

Logistics corridor

Economic corridor

Catalysts: Trade facilitation, logistics services, a.o.

X Y

A B

Narrow vs. Broad CorridorsCA+CB+CH ≤ CAB

Corridor

Rationale - regional corridors1. Sustained economic growth has increased the

demand for transport and logistics services.2. Efficient transport networks have become more

important to regional cooperation, in both absolute and relative terms, as tariff-based barriers to economic cooperation have generally declined.

3. Better infrastructure would encourage fragmentation of production in the region, enhance the regional and global trade, and help realize South Asian integration process.

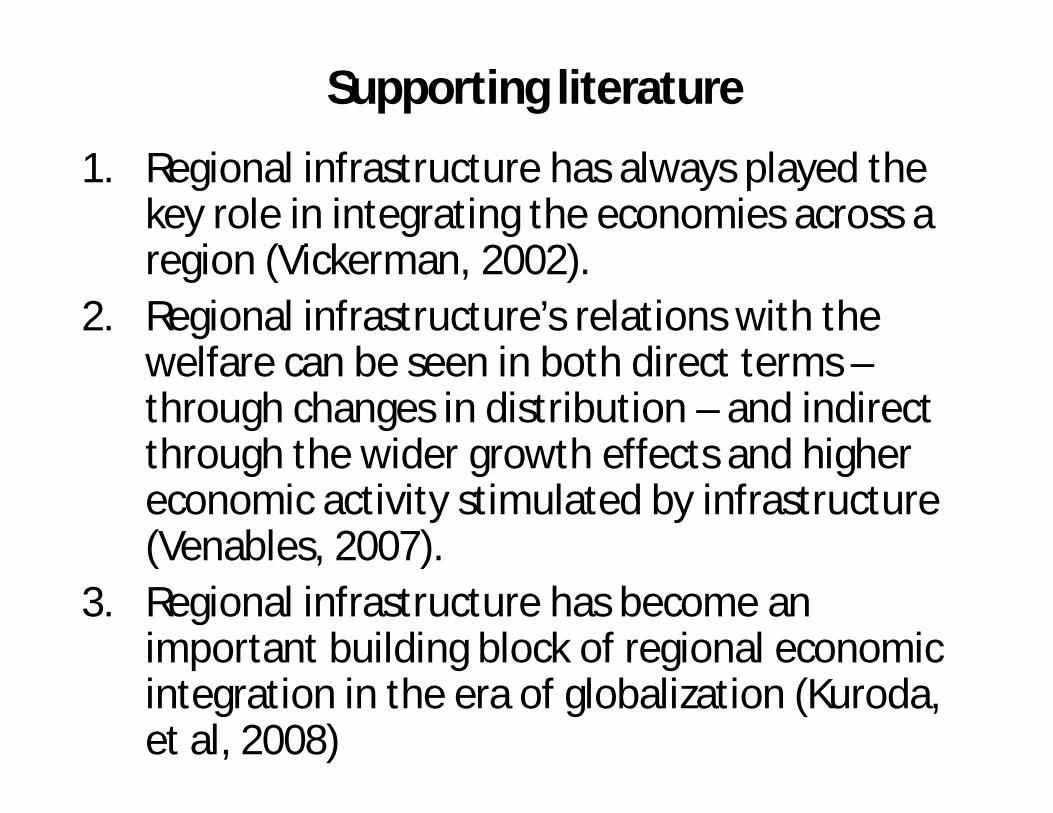

Supporting literature

1. Regional infrastructure has always played the key role in integrating the economies across a region (Vickerman, 2002).

2. Regional infrastructure’s relations with the welfare can be seen in both direct terms –through changes in distribution – and indirect through the wider growth effects and higher economic activity stimulated by infrastructure (Venables, 2007).

3. Regional infrastructure has become an important building block of regional economic integration in the era of globalization (Kuroda, et al, 2008)

Regional corridors help enhance trade flows

Source: Brooks (2008)

Regional Corridors

Regional corridors strengthen production blocks and regional integration

Corridor

Source: Kimura et al (2009)

Regional corridors foster regional cooperation

Afghanistan

Maldives

Pakistan

Sri Lanka

Bangladesh

Bhutan

Nepal

India

SAARC

x9

x2x1

x5

x10

x4x6

x7

x8

x9

X1, x2, ….,xn: countries

Corridor (s)

Source: De (2011)

List of select economic corridors in AsiaSr. No. Corridor Name Countries

1 North -South Economic CorridorPR China, Thailand, Lao PDR, Myanmar and

Viet Nam

2 East-West Economic Corridor Viet Nam, Myanmar, Lao PDR, Thailand

3 South Economic Corridor Thailand, Cambodia, Viet Nam and Lao PDR

4Kunming-Haiphong Transport Corridor-

Noi Bai-Lao Cai Hway PR China, Viet Nam

5 GMS Southern Coastal Road Corridor II Viet Nam

6CAREC Regional Road Corridor

Improvement (Sary Tash-Karamik) Kyrgyz Republic

7 Mekong ICT Project Lao PDR

8 Indonesia/North Java Corridor Indonesia, Indonesia

9 Indonesia/Eastern Sumatra Corridor Indonesia, Sumatra

10 East Asia Industrial Corridor Viet Nam, India, Thailand

11 CAREC Transport Corridor 1b Kazakhstan, PR China, Russian Federation

12 Western Regional Road Corridor Mongolia, PR China, Russian Federation Source: Author based on ADB

Four zones of regional corridors

Zone I

Zone II Zone IV

Zone III

National Regional

Nar

row

Bro

ad

National + Narrow

(Construction, upgrading)

Regional + Narrow

(Trade facilitation, logistics)

Regional + Broad

(Cross-border economic zones)

(Area development, SMEs, rural roads)

National + Broad

Source: Adapted from Srivastava (2011)

SAARC at here

Regional corridors in neighbouring regions

South Asia

SRMTC?

CAREC Economic Corridors

GMS Economic Corridors

Southeast Asia

Central Asia

IMT-GT Economic Corridors BIMP-EAGA

RegionalCorridors

Performance in trade facilitation –mixed results, needs greater

involvement of private sector in TF

South Asia has poor performance in trade facilitation

• Significant progress made in reducing time of import/export since 2005,– but developed economies also improved during that

period• On average, it still takes 30 days to move goods from

factory to deck-of-ship at the nearest seaport– South Asia: 30 days– South-East Asia: 20 days – Developed economies: 10 days

Improvements in TF could bring US$ 250 billion in additional trade for Asia and the Pacific (APEC, 2011)

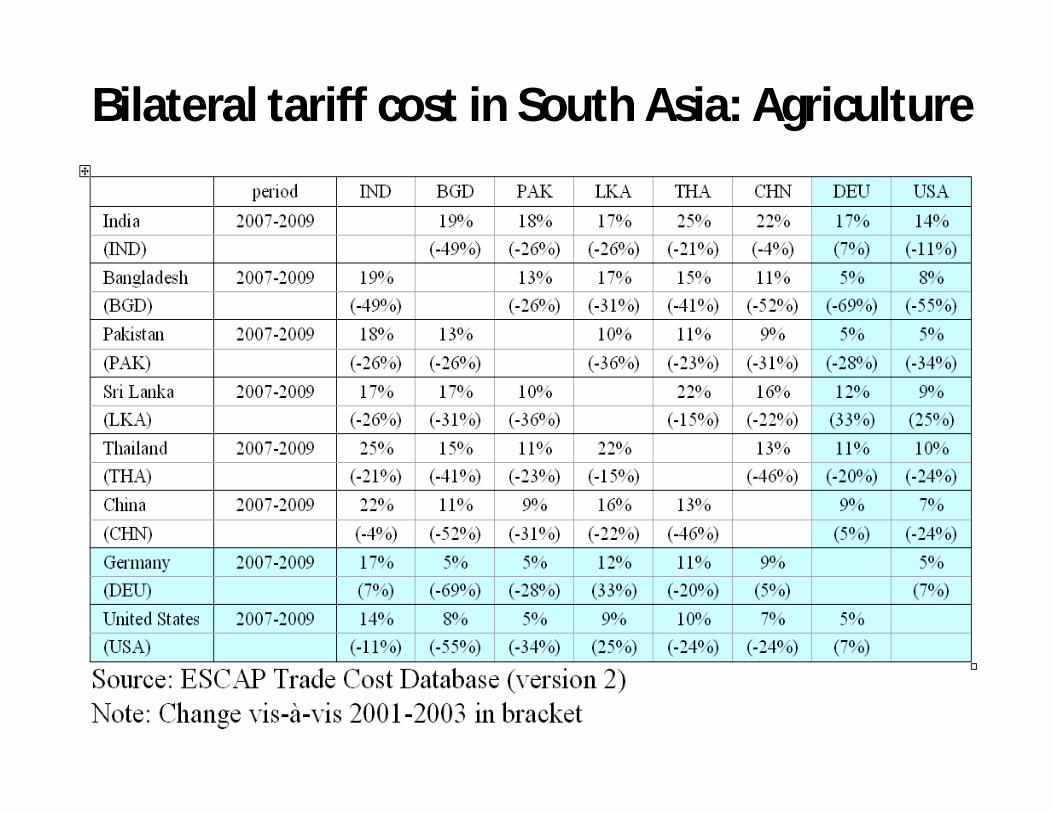

Bilateral tariff cost in South Asia: Agriculture

Bilateral non-tariff trade costs in South Asia: Agriculture

Bilateral tariff cost in South Asia: Manufacturing

Bilateral non-tariff trade costs in South Asia: Manufacturing

What explains changes in the trade costs across countries?*

50+ %

25%

10%

10%

1%

10-30%

60-90%

Natural trade costs(geographic and cultural distance between countries)

0-10%Tariff costs

Policy-relatedNon-Tarifftrade costs

Business environment

Availability/use of ICT services

Liner Shipping Connectivity (port and maritime services efficiency)

Direct cost of trade procedures

Other factors, including:-Indirect cost of trade procedures-Currency / exchange rate-Non-tariff Measures (SPS, TBT)

*simplified representation based on Duval and Uthoktham (2011)

Export takes longer time in LLDCs

YearAfghanistan Bangladesh Bhutan India Maldives Nepal Pakistan Sri Lanka

2006 66 35 38 27 21 43 31 25

2007 67 35 38 27 21 43 22 25

2008 67 28 38 18 21 43 22 21

2009 74 28 38 17 21 41 22 21

2010 74 25 38 17 21 41 22 21

2011 74 25 38 17 21 41 21 21

2012 74 25 38 16 21 41 21 21

Source: Doing Business Database, The World Bank

(Number of Days)

Rising costs of export in LLDCs(US$ per container)

Source: Doing Business Database, The World Bank

Afghanistan

Bangladesh Bhutan India Maldives Nepal Pakistan Sri

Lanka

2006 2,180 902 1,150 864 1,200 1,600 996 647

2007 2,180 902 1,150 864 1,200 1,600 515 647

2008 2,180 844 1,150 820 1,200 1,600 515 660

2009 2,680 905 1,210 945 1,348 1,764 611 715

2010 3,030 905 1,210 945 1,348 1,764 611 715

2011 3,545 920 2,230 1,055 1,550 1,960 611 715

2012 3,545 965 2,230 1,095 1,550 1,960 660 715

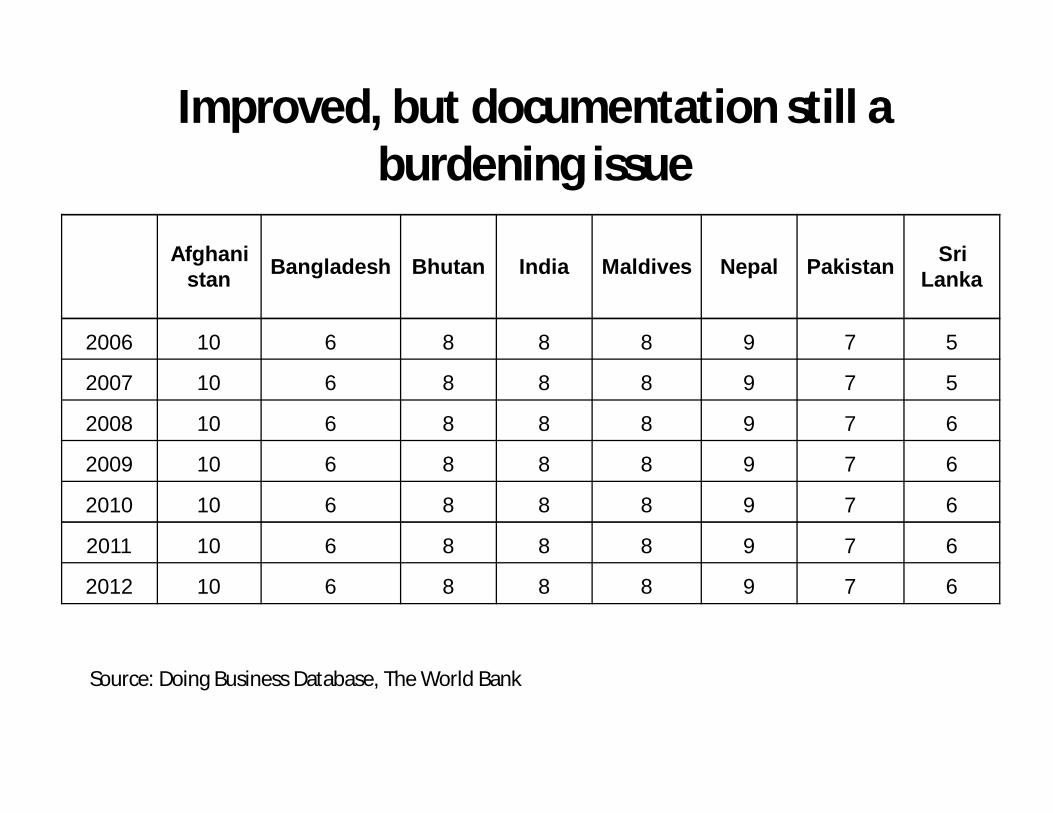

Improved, but documentation still a burdening issue

Afghanistan Bangladesh Bhutan India Maldives Nepal Pakistan Sri

Lanka

2006 10 6 8 8 8 9 7 5

2007 10 6 8 8 8 9 7 5

2008 10 6 8 8 8 9 7 6

2009 10 6 8 8 8 9 7 6

2010 10 6 8 8 8 9 7 6

2011 10 6 8 8 8 9 7 6

2012 10 6 8 8 8 9 7 6

Source: Doing Business Database, The World Bank

Policy-related non-tariff trade costs more important in South Asia – documentation

and inland transit critical to exportExport Time, 2011 Export Cost, 2011

Source: Doing Business Database, World Bank

Customs improved its performance: ExportExport time for selected products and countries in Asia (adjusted), 2010

Source: ESCAPhttp://www.unescap.org/tid/publication/tipub2615.pdf

Field level data

Customs improved its performance: Import0

510

1520

25D

ays

Inland trasportation

Terminal handling

Customs

Document preparation

Fabrics

Used CarsElectronics

Fabrics

Fabrics

Garments

Tea

RubberTyres

Fabrics

Auto Parts

Sugar

Bangladesh China India Japan Nepal Sri Lanka ThailandSource: ESCAPhttp://www.unescap.org/tid/publication/tipub2615.pdf

Import time for selected products and countries in Asia (adjusted), 2010Field level data

Days

22928 0.827 22625 Export procedures in India 124 223 Import procedures in Bangladesh 22 22120 41918 117 1.8 216 115 114 113 112 111 110 2

98 47654 13 2210 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 Procedures

28.25 days

Start

End

28.25 days

Start

End

Sr. No Process Days1 Buy 22 Obtain export permit 13 Contract registration and inspection 44 Excise inspection 25 Obtain cargo insurance 16 Arrange pre-shipment inspection 17 Obtain certificate of origin 18 Obtain SAFTA certificate 19 Submit customs declaration online 1

10Collect and endorse documents for import 1.75

11 Arrange transport for loading 112 Prepare other import documents 213 Provide customs declaration 0.514 Transfer to LCS 415 Parking of goods 216 Customs clearance 217 Send the goods to importer’s warehouse 118 Clear goods through customs 219 Transport to importer's premise 0.7520 Pay 1.50*

Total 28.50**

Time Procedure Chart of Trade in

Cotton Yarn Exporter = India

Importer = Bangladesh

Days

26 25 days 7252423222120 Export Procedures in Sri Lanka 19 218 Import Procedures in India 2 21716 1 1 1 115 2 214 113 0.412 0.25 0.311 0.6 0.310 0.59 18 2 0.0176 1.55 14 33210 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 Procedures

Start

End

Shipping

Start

End

Shipping

Start

End

Shipping

Start

End

Shipping

Time Procedure Chart of Trade in Rubber

TiresExporter = Sri Lanka

Importer = India

Sr. No Process Days1 Buy - conclude sales and contract terms 32 Obtain IEC code 13 Obtain bank related documents 1.54 Prepare all export documents 25 Lodge CUSDEC online 0.016 Pass CUSDEC manually 17 Obtain cargo insurance 0.58 Arrange transport and load on truck 0.69 Transport to port of departure 0.2510 Clear goods through customs at seaport 0.311 Port and terminal handling activities 0.312 Loading container onto vessel 0.413 Vessel information and filling IGM 114 Shipping 215 Allocation of berth 216 Filing Bill of entry & other import papers 117 Filing Delivery Order 118 Immigration 119 Plant quarantine 120 Unloading of goods from vessel 221 Verification of cargo 222 Send the goods to importer’s warehouse 223 Pay to exporter 7

Total days 25

Export process, 2009-10Exporter Product

exportedDestination Business process

No. of Steps No. of Parties

Bangladesh Shrimp Japan 10 14

Bangladesh Garments India 10 (8) 13 (12)

China Garments Japan 9 11

China Electronics Thailand 11 11

India Fabrics Bangladesh 13 16

India Vegetables UAE 12 14

India Fruits EU 13 14

Nepal Veg. ghee India 10 14

Nepal Veg. ghee China 5 10

Sri Lanka Rubber tyres India 7 13

Sri Lanka Tea Japan 7 12

Thailand Auto. parts India 7 11

Thailand Sugar Bangladesh 11 10

Source: ESCAP, http://www.unescap.org/tid/publication/tipub2615.pdf

Import process, 2009-10

Importer Product imported

Origin Business process

Steps involved

Parties involved

India Rubber tyres Sri Lanka 10 13

China Fabrics Japan 6 11

China Auto. parts Japan 6 11

Thailand Electronics China 6 12

Sri Lanka Fabrics India 7 13

Sri Lanka Used cars Japan 3 9

Bangladesh Fabrics India 5 8

Bangladesh Sugar Thailand 4 7

Nepal T&C India 5 10

Source: ESCAP, http://www.unescap.org/tid/publication/tipub2615.pdf

Export documents, 2009-10 Product

exportedDestination Documents Needed

(No.)

Bangladesh Shrimp Japan 24

Bangladesh Garments India 26 (17)

China Garments Japan 14

China Electronics Thailand 17

India Fabrics Bangladesh 18

India Vegetables UAE 22

India Fruits EU 27

Nepal Veg. ghee India 26

Nepal Veg. ghee China 43

Sri Lanka Rubber tyres India 19

Sri Lanka Tea Japan 24

Thailand Auto. parts India 35

Thailand Sugar Bangladesh 39

Source: ESCAP, http://www.unescap.org/tid/publication/tipub2615.pdf

Import documents, 2009-10

Product Imported Origin Documents Needed(No.)

India Rub tyres Sri Lanka 9

China Fabrics Japan 13

China Auto. parts Japan 13

Thailand Electronics China 44

Sri Lanka Fabrics India 19

Sri Lanka Used cars Japan 18

Bangladesh Fabrics India 10

Bangladesh Sugar Thailand 11

Nepal T&C India 20

Source: ESCAP, http://www.unescap.org/tid/publication/tipub2615.pdf

Requirement of export documents and copies, 2009-10

Export ProductDocuments Needed (No.)

from to Types Copies

China Japan Garments 14 28

China Thailand Electronics 14 22

India Bangladesh Fabrics 18 26

India UAE Vegetables 22 26

India EU Fruits 27 29

Thailand India Automobile parts 35 46

Thailand Bangladesh Sugar 39 50

Source: ESCAP, http://www.unescap.org/tid/publication/tipub2615.pdf

Import

Product

Documents Needed (No.)

from to Types Copies

India Sri Lanka Rubber tyres 9 17

China Japan Fabrics 16 37

China Japan Automobile parts 16 37

Thailand China Electronics 44 54

Requirement of import documents and copies, 2009-10

Source: ESCAP, http://www.unescap.org/tid/publication/tipub2615.pdf

Development of regional corridors –some outcomes are building

infrastructure, trade creation, generating production network (supply

chain), improves global and regional competitiveness, narrowing

development gaps, ..…

Intra-South Asia trade flow, 2011

AFG BDG IND MDS NPL PAK SL

South Asia Total

Share (%)

AFG 23.16 141.73 0.00 154.34 0.00 319.23 1.61

BDG 6.51 539.75 0.00 15.38 77.02 18.34 657.00 3.32

IND 517.89 4062.38 121.46 2335.78 2313.89 4890.58 14241.98 71.98

MDS 0.64 33.96 0.00 0.01 19.97 54.58 0.28

NPL 0.00 25.78 492.55 0.01 1.08 1.64 521.06 2.63

PAK 1930.99 635.81 320.59 5.07 1.01 303.05 3196.52 16.16

SL 0.00 25.49 625.09 72.30 0.64 72.21 795.73 4.02

Total 19786.10 100.00

Source: DOTS, IMF

(US$ million)

Trade and connectivity flow – South Asia with neighbouring regions – rising trade not

supported by adequate connectivity

SouthAsia

Central Asia

Southeast AsiaMiddle east/

Gulf

Southwest Asia

ANZ +Pacific

East Asia

Africa

Europe

Trade linkage (strong)Connectivity linkage (weak)

Weak

Moderate

Strong

Source: De (2012)

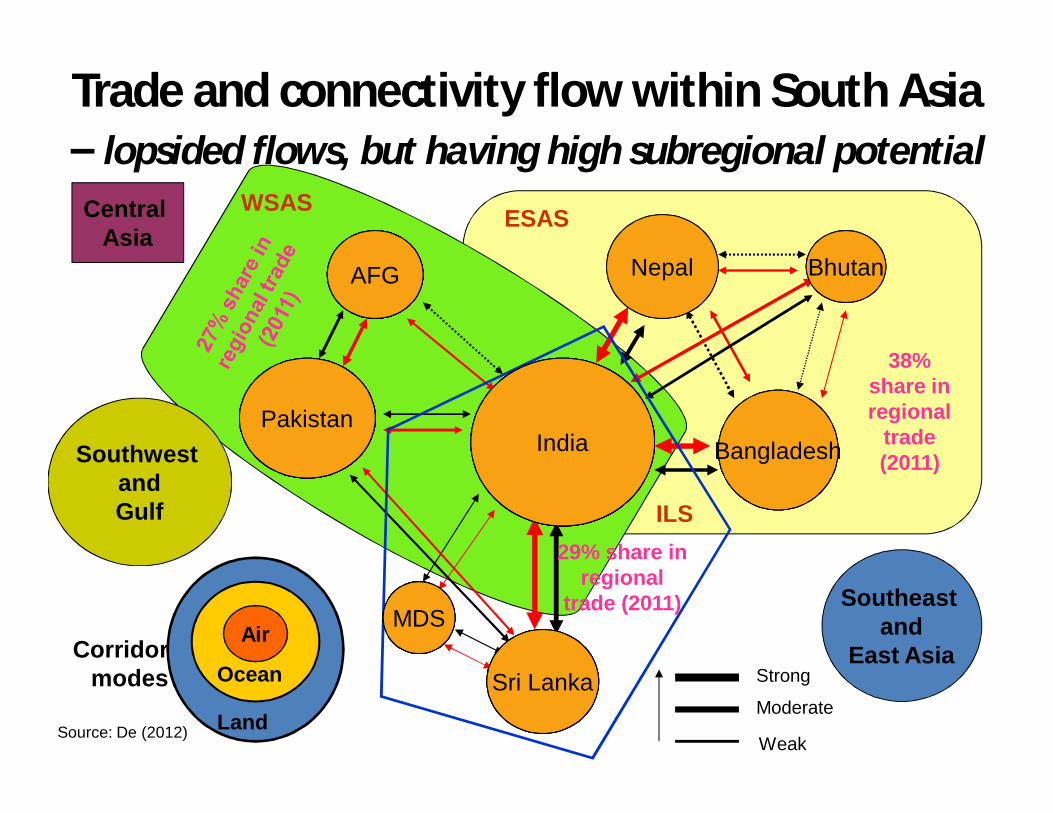

Trade and connectivity flow within South Asia – lopsided flows, but having high subregional potential

PakistanIndia

Sri Lanka

Nepal

Bangladesh

Bhutan

Southeast and

East AsiaMDS

AFG

ESAS

38% share in regional

trade (2011)

WSAS

Southwest andGulf

Central Asia

ILS29% share in

regional trade (2011)

Air

Land

Corridor modes

Pakistan

AFG

IndiaPakistan

AFG

MDS

IndiaPakistan

AFG

Sri Lanka

MDS

IndiaPakistan

AFG

Bangladesh

Sri Lanka

MDS

IndiaPakistan

AFG Bhutan

Bangladesh

Sri Lanka

MDS

IndiaPakistan

AFG Nepal Bhutan

Bangladesh

Sri Lanka

MDS

IndiaPakistan

AFG

Strong

Moderate

Weak

Ocean

Source: De (2012)

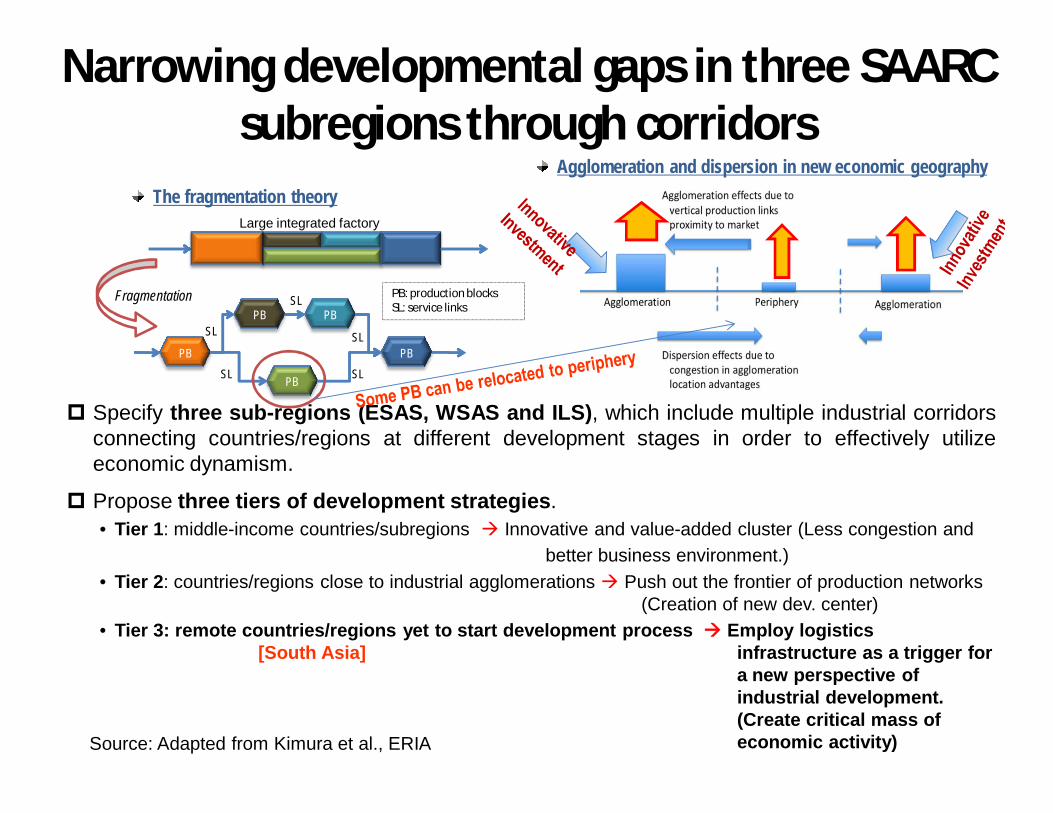

Specify three sub-regions (ESAS, WSAS and ILS), which include multiple industrial corridorsconnecting countries/regions at different development stages in order to effectively utilizeeconomic dynamism.

Propose three tiers of development strategies.• Tier 1: middle-income countries/subregions Innovative and value-added cluster (Less congestion and

better business environment.)• Tier 2: countries/regions close to industrial agglomerations Push out the frontier of production networks

(Creation of new dev. center)• Tier 3: remote countries/regions yet to start development process Employ logistics

[South Asia] infrastructure as a trigger for a new perspective of industrial development. (Create critical mass of economic activity)

PB: production blocksSL: service links

Agglomeration and dispersion in new economic geography

PB

PB

PB PB

PB

SL

SL

SL

SL

SL

Large integrated factory

The fragmentation theory

Fragmentation

Narrowing developmental gaps in three SAARC subregions through corridors

Source: Adapted from Kimura et al., ERIA

Economic welfare higher with improved connectivity and trade facilitation –

(i) Bangladesh – India trade(ii) India – Pakistan trade

What is the emerging direction of trade in South Asia?

General equilibrium simulation 1

Effects on Total Imports (% change from the base)

Source: De, Raihan and Kathuria (2012) World Bank WPS # 6155

Effects on Total Exports (% change from the base)

Welfare Effects of Bangladesh – India MFN Trade

Welfare Effects of India - Pakistan MFN Trade

General equilibrium simulation 2

(Equivalent variation in US$ million at 2007 prices)

Source: De, Raihan and Ghani (2012) ‘What does MFN Trade mean for India and Pakistan? CanMFN be a Panacea?’ Mimeo, World Bank, Washington, D.C

Country MFN MFN+BTF Bangladesh 21.08 32.25India 160.71 1406.67Nepal 18.01 32.22Pakistan 99.21 1229.08Sri Lanka 34.92 63.32Rest of South Asia 15.72 21.38China -10.52 -102.62USA -18.39 -122.33EU25 -29.55 -200.94Rest of the World -66.71 -585.41Note: MFN = Most Favored Nation; BTF = Bilateral Trade Facilitation between India and Pakistan Source: GTAP simulation

General equilibrium simulation 3

Country SAFTA without MFN SAFTA with MFN SAFTA+MFN+STF

Bangladesh -132.85 -111.77 1479.56India 1650.02 1810.73 5452.03Nepal 467.03 485.03 1654.21Pakistan 1022.46 1121.67 2618.38Sri Lanka 36.98 71.88 2173.12Rest of South Asia 282.49 298.21 1265.02China -205.69 -216.19 -760.12USA -252.08 -270.47 -985.54EU25 -318.77 -348.32 -1394.91Rest of the World -615.01 -681.72 -3020.78

India – Pakistan MFN and Welfare Effects of SAFTA(EV in million US$ at 2007 prices)

Source: De, Raihan and Ghani (2012) ‘What does MFN Trade mean for India and Pakistan? CanMFN be a Panacea?’ Mimeo, World Bank, Washington, D.C

Note: MFN = Most Favored Nation; STF = Trade facilitation among SAFTA member states

Larger gains in trade facilitation would come from bigger economies – more cooperation

and unilateral actions must

Reporter PartnerActual Trade

Potential Trade

Potential Trade P/A UT

2010 (A) 2010 (P) 2017 (P) 2010 2010

(US$ million) (%)

India

Afghanistan 516.16 1619.96 4961.31 3.138 68.14

Bangladesh 3376.42 18519.71 62528.75 5.485 81.77

Bhutan 345.48 427.21 773.22 1.237 19.13

Maldives 131.63 184.64 210.66 1.403 28.71

Nepal 2322.11 3851.02 11598.71 1.658 39.70

Pakistan 2563.33 9447.58 17376.59 3.686 72.87

Sri Lanka 3797.00 5803.96 22554.18 1.529 34.58

(a) India

Note: Based on a gravity modelSource: Author

Larger gains in trade facilitation would come from bigger economies – more

cooperation and unilateral actions must

Reporter Partner Actual TradePotential

TradePotential

Trade P/A UT

2010 (A) 2010 (P) 2017 (P) 2010 2010

(US$ million) (%)

Pakistan

Afghanistan 1875.67 2474.73 4989.85 1.319 24.21

Bangladesh 457.33 957.57 2075.13 2.094 52.24

Bhutan 0.24 30.99 72.14 131.341 99.24

India 2760.40 7415.73 9350.72 2.686 62.78

Maldives 4.54 14.68 25.39 3.234 69.08

Nepal 1.96 150.89 501.35 76.903 98.70

Sri Lanka 341.50 888.38 1693.41 2.601 61.56

Note: Based on a gravity modelSource: Author

(b) Pakistan

Towards Regional Corridors - Trade (and Transport) Facilitation Progress so Far

SAARC connectivity – mixed progress• Negotiation of Regional Transport and Transit Agreement, and a Regional Motor

Vehicle’s Agreement (ongoing).• SAARC Expert Group finalized the text of the Regional Agreement on Railways in August

2011. • Launch of feasibility studies of pilot projects:

– Birganj and Kathmandu (160 km) completed in October 2008 – negotiation ongoing• Kathmandu-Birgunj-Kolkata/Haldia – rail corridor

– Birgunj-Katihar-Singhabad-Rohanpur-Chittagong with links to Jogbani, Biratnagar and Agartala – rail corridor

– Agartala-Akhaura-Chittagong – rail corridor• Construction between Agartala and Akhaura (14 km) is about to commence.

– Phuntsholing and Hashimara – road corridor– Ferry link - between Colombo and Tuticorin (started already) and Colombo and Cochin – Karachi – Mumbai ferry link– Air link - Malé-New Delhi and Islamabad-New Delhi; – Establishment of modern border crossing facility at Phuntsholing. – Indian ocean cargo cooperation

• On-going projects: – Feasibility study for India - Bhutan rail link– Construction of railway line from Jiribam-Tupui (near to Imphal, India) has commenced– Construction of Kaladan Multimodal Transport project has started in December 2010– Railway infrastructure improvement projects in Sri Lanka– Intermodal connectivity – Air Services Agreement (single ticket to fly between South Asian nations)

• Demonstration run of container train involving Bangladesh, India and Nepal is being planned

Demonstration run of container train between ECO and SAARC?

Source: Drawn based on information of ECO & UNESCAP

Progress in modernizing and opening of land customs stations

• India’s Integrated Check Post (ICPs) project – Attari already started working since April 2012 [spread over 118 acres, a passenger terminal 9,600 s.m; cargo terminal 4,700 s.m; separate import and export warehouses, 10,000 s.m., parking space 50,000 s.m., etc.)

• Opening of Banglabandha – Fulbari land port for trade

• Opening of border haat in Baliamari (Bangladesh) –Kalaichar (India), and fFew more border haats (e.g. between India and Bangladesh) coming up

Progress in Customs cooperation• SAARC Agreement on Mutual Administrative Assistance in

Customs Matter, signed in 2005• The Seventh Meeting of the Sub-Group on Customs Cooperation

(11-12 February 2010) made following recommendations with a view to facilitating trade in goods in SAARC. – Building infrastructure including roads and railways networks near the

LCSs.– Customs clearance procedures at LCSs need to be smoothened;– Customs Administrations may consider a system of customs facilitation in

which export documentation of one Member State could be considered by the Customs Administration in the importing country for the purposes of assessing and clearing the consignment.

– Need for developing an Electronic Data Exchange System within the region, including at LCSs, with a view to ensure better facilitation of trade in goods among the SAARC countries including improved compliance.

– SAARC Secretariat to develop a regional/sub-regional project to set up automated customs clearing mechanism at the designated LCSs.

– Harmonisation of 8-digit tariff lines is needed, and in order to make this task easier, all Member States would further provide upto only 100 8-digit tariff lines with a trade potential of 75% (in value terms) in the region.

Recent development in Customs cooperation• Declaration of the Fifteenth Meeting of the Committee on

Economic Cooperation - Maldives, 15-16 July 2012 (Source: SAARC Secretariat Press Release July 24, 2012)– The Meeting recognised delays in customs clearance

procedures and decided that henceforth electronic copies of specimen signatures and seals of officials authorised to sign SAFTA Certificates of Origin may also be accepted in addition to sending the original copies of such documents in order to save time and to ensure that the consignments are not held up at the customs border points.

• India – Pak customs cooperation agreement, mutual recognition of standards and redressal of trade disputes

Encouraging progress in transit• Common transit is must for a common market• All SAARC countries have in-principally agreed to regional

transit. • Motor Vehicle Agreement is being negotiated.• SAARC Expert Group finalized the text of the Regional

Agreement on Railways in August 2011. • Sub-regional transit has been agreed between India, Nepal,

Bhutan and Bangladesh. – Bilateral document between India and Bangladesh signed

during the state visit of Indian PM to Bangladesh in September 2011 to facilitate overland transit traffic between Bangladesh and India

– Demonstration run of container train between Bangladesh, India and Nepal is getting ready.

• Huge trade opportunities if Afghanistan – Pakistan Transit Agreement covers Western South Asia and Central Asia

Subregional transit better option to open regional transit

AGH

PAK IND

BHUNPL

BDG

Source: Author

ESAS

WSAS

SOUTH ASIA

Proposed transit

ESAS: Eastern South Asia SubregionWSAS: Western South Asia Subregion

Linking South Asia with neighbours• Uzbekistan – Afghanistan railway line (a section till

Mazar-i-Sharif already opened)• Highway in Afghanistan, aided by India• TAPI gas pipeline• China – Nepal highway and railway • India – Nepal railway project, India – Bhutan railway

project, etc.• India – Myanmar – Thailand trilateral highway (a

section already in operation)• India – ASEAN ocean shipping network • India – ASEAN open sky• Others

Three important developments on regional connectivity (Strong Impact on South Asian

Trade Flow)1. Transit for traffic between India, Bangladesh,

Nepal, and Bhutan.2. Integrated check posts (ICP) in Attari in Punjab,

Moreh in Manipur, Petrapole in West Bengal, and Raxul in Bihar.

3. Pakistan – ECO and India – ASEAN connectivity projects, particularly Mekong – India Economic Corridor (MIEC) and BIMSTEC Trilateral Highway

Mekong – India Economic Corridor

• Envisaged to support India-ASEAN connectivity

• Aims to strengthen production network – regional and otherwise.

• MIEC involves integrating the four Mekong countries (Myanmar, Thailand, Cambodia and Vietnam) with India.

• It connects Ho Chi Minh City (Vietnam) with Dawei (Myanmar) via Bangkok (Thailand) and Phnom Penh (Cambodia) and further linking to Chennai in India.

• It is expected to augment trade with India by reducing travel distance between India and MIEC countries and removing supply side bottlenecks.

• Approx. investment US$ 88 billion.

Emerging Architecture, SAARC and ASEAN

Source: ASEAN-India Connectivity Report 2012, RIS

Deepening South Asian Integration

The Renewed Vision

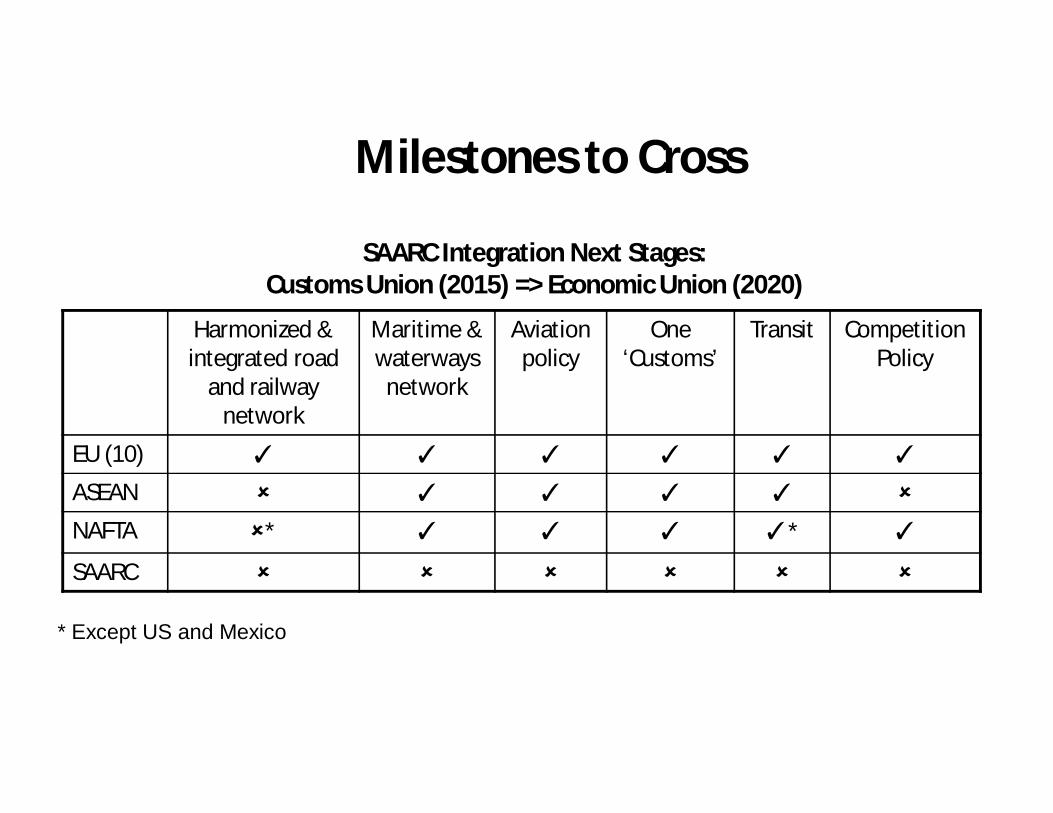

1. With SAFTA, South Asia has entered into the second era of regional integration

2. Vision is to achieve Common (Single) Market through Customs Union and then Economic Union

Milestones to Cross

Harmonized & integrated road

and railway network

Maritime & waterways

network

Aviation policy

One ‘Customs’

Transit Competition Policy

EU (10) ✓ ✓ ✓ ✓ ✓ ✓

ASEAN ✓ ✓ ✓ ✓

NAFTA * ✓ ✓ ✓ ✓* ✓

SAARC

SAARC Integration Next Stages: Customs Union (2015) => Economic Union (2020)

* Except US and Mexico

The Agenda

Source: World Bank

Congested land borders

Unplanned and informal market

Long queue of trucks

3.60hrs

5.00 hrs

78.40hrs

10.00hrs

Loading at Kolkata

Kolkata to Petrapole

Time at Petrapole

Unloading at Benapole

5.10hrsCrossing border returning from Benapole

International border

Total Time = 102.10 hrs. (≈ 4 days)

Kolkata

Bangladesh

India

Case of India (Petrapole) and Bangladesh (Benapole)

3.60hrs

5.00 hrs

78.40hrs

10.00hrs

Loading at Kolkata

Kolkata to Petrapole

Time at Petrapole

Unloading at Benapole

5.10hrsCrossing border returning from Benapole

International border

Total Time = 102.10 hrs. (≈ 4 days)

Kolkata

Bangladesh

India

3.60hrs

5.00 hrs

78.40hrs

10.00hrs

Loading at Kolkata

Kolkata to Petrapole

Time at Petrapole

Unloading at Benapole

5.10hrsCrossing border returning from Benapole

International border

Total Time = 102.10 hrs. (≈ 4 days)

Kolkata

Bangladesh

India

3.60hrs

5.00 hrs

78.40hrs

10.00hrs

Loading at Kolkata

Kolkata to Petrapole

Time at Petrapole

Unloading at Benapole

5.10hrsCrossing border returning from Benapole

International border

Total Time = 102.10 hrs. (≈ 4 days)

Kolkata

Bangladesh

India

Multiple handling in rail and road

• Trade Procedures at South Asia border points

Source: Based on ADB

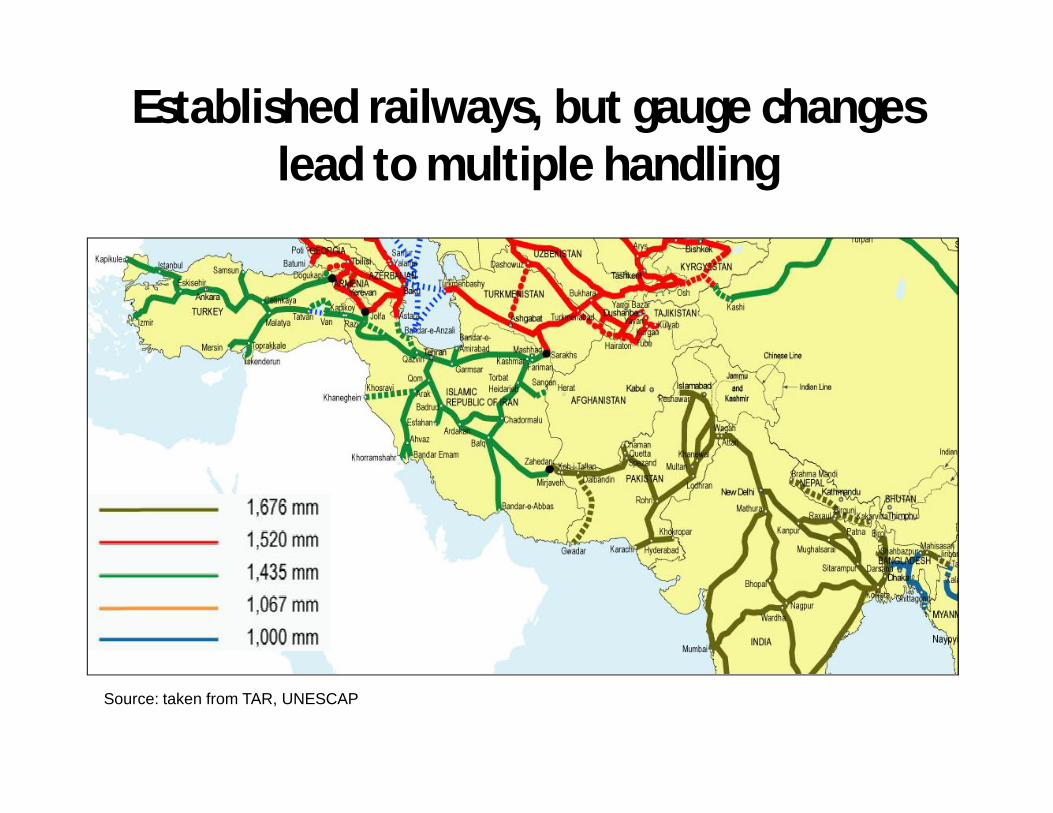

Established railways, but gauge changes lead to multiple handling

Source: taken from TAR, UNESCAP

Need to facilitate express delivery chain in South Asia

Pick-up Local station

Gateway export Hub Gateway

importLocal station Delivery

Source: Author

Cumbersome trade procedures

Source: De (2011)

(i) BPA Charts of Cotton Yarn Export from India to Bangladesh

Cumbersome trade procedures

Source: Hossain and Rahman (2011)

(ii) BPA Charts of RMG Export from Bangladesh to India

Good progress, but manual handling of documentation still in South Asia

Sr. No. Process Submission of Documents

1 Buy Electronic and manual

2 Obtain export permit Electronic

3 Contract registration and inspection Electronic and manual

4 Excise inspection Manual

5 Obtain cargo insurance Electronic

6 Arrange pre-shipment inspection Manual

7 Obtain certificate of origin Electronic and manual

8 Obtain SAFTA certificate Electronic and manual

9 Submit customs declaration Electronic

10 Arrange transport for loading Manual

11 Transfer to LCS Manual

12 Parking of goods Manual

13 Customs clearance Electronic and manual

14 Send the goods to importer’s warehouse Manual

15 Pay Electronic

Indian Export of Fabrics to Bangladesh, 2010

Absence of international conventions on trade & transport facilitation

Convention Afghanistan Bangladesh Bhutan India Maldives Nepal Pakistan Sri Lanka

Convention onRoad Traffic (1968)

No Yes No Yes No No Yes Yes

Convention on Road Signs and Signals (1968)

No No No Yes No No Yes No

Customs Convention on Temporary Importation of Commercial Road Vehicles (1956)

Yes No No No No No No No

Customs Convention on Containers (1972)

No No No No No No No No

Convention on International Transport of Goods under Cover of TIR Carnets (1975)

Yes No No No No No No No

Convention on the Contract for the International Carriage of Goods by Road (1956)

No No No No No No No No

Convention on the Harmonization of Frontier Controls of Goods (1982)

No No No No No No No No

Financing SAARC connectivity

• Set-up SAARC Infrastructure Fund (SIF)• Look for traditional sources – World Bank,

ADB, Islamic Development Bank, countries like Japan, etc.

• Domestic resources for domestic components of connectivity

• Special project development facility (SPDF) for feasibility studies

South Asian corridor integration

• Three strategies:– Asian level planning – UNESCAP– Regional / subregional level planning &

implementations: SAARC Corridors, ADB [SASEC]– National level planning & implementations:

Individual countries, ADB, a.o

Subregional inter-linkages:ECO - SAARC – BIMSTEC – GMS/ASEAN

Delhi

Kolkata

Kabul

Lahore

Dhaka GMS EWEC

Katmandu

Chennai

Chitagong

Dawei

Thimpu

Policy options • Overland connectivity is not a distant dream

– Strengthen Afghanistan - India – Pakistan road, rail and air link

– South Asia Economic corridor!• More direct links among ports. Few ports are directly

connected – No direct call of container shipping

• Open sky???…. few airports are directly connected. – New routes for cargo + passengers – Complete ASA, & implement with all South Asian

countries

Fostering South Asia Connectivity: The Enabling Environment

1. Accession to the International Conventions2. Multimodal Transport and Transit3. Strengthening and Harmonizing Rules, Regulations,

and Standards4. Demonstration Projects5. Financing Cross-border Transport Projects6. Strengthening Coordination among Countries and

Stakeholders7. Closer Cooperation on Security8. Strengthening Regional Cooperation

Some specific recommendations1. Strengthen cross-border infrastructure (move from road corridors to

economic corridors)2. Accept subregional and subsequently regional transit3. Fast track lane and priority of goods in transit to cross the border4. Set-up SAARC Single Window (Customs) (pilot run of authorized economic

operator, AEO; and mutual recognition agreement)5. Simplification and harmonization of trade procedures, more particularly at

border. 6. Introduce modern corridor management techniques in selected corridors7. Promote multimodal transportation (with rail transit, regular container train

in the region)8. Improve the efficiency of border corridors (both side of border improvement

in ICP project in parallel)9. Liberalize visa regime10. Open sky in South Asia11. Effective project coordination among government stakeholders12. Stronger institution (public-private interface) for trade facilitation is urgently

needed. 13. Regional study for SAARC Master Plan of Connectivity should be done.14. Set-up SAARC connectivity coordination committee to coordinate the Master

Plan and its feasibility.

Thank [email protected]

ADB-UNESCAP BPA Study – Trade procedures harmonization study

SASEC Corridors

Target Corridor 1 (Nepal Corridor)

Kakarvitta-Panitanki-Fulbari-Banglabandha

Target Corridor 2 (Bhutan Corridor)

Phuentsholing-Jaigaon-Hasimara-Changrabandha-Burimari

Target Corridor 3 (Nepal Corridor)

Kathmandu-Birgunj-Kolkata

Team Members

Name RemarksPrabir De Team leader

Achyut Bhandari Bhutan

Abid Khan Bangladesh

Tahseen Khan India

Pushpa Rajkarnikar Nepal

Cuong NguyenTasneem Mirza

ADB

Sangwon Lim ESCAP