Embed Size (px)

Citation preview

Regional Issues and Program Committee

September 30, 2003

Larry D. Jones, Agricultural Economics

Farm Numbers, Kentucky1940-2001

88

267

0

50

100

150

200

250

300

1940

1945

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2001

2002

Thousands

Year

Farm Numbers

Source: Ky Ag. Statistics

WHAT IS A FARM?

What is a Farm?• Government says that a farm is a

business that has $1000 gross sales of food and fiber per year

• OR

• Could sell $1000 annually

Farm Cash Receipts—Kentucky1991-2002

0

500

1000

1500

2000

2500

3000

3500

4000

Source: KY Agricultural Statistics

Millions $

Total

Livestock

Crops

Kentucky Crop Receipts, 2002 ($1.15 Billion)

443

555

6583

5 Tobacco

Row Crops

Hay

Hort

Other

Millions $Source: KY Ag. Statistics

Kentucky Livestock Receipts, 2002($1.96 Billion)

406

506

20974

760

Cattle/CalvesPoultryDairy ProductsHogsHorses/Mules

Source: KY Ag Statistics

Millions $

D istribution of K Y Farm C ash R eceipts-1991 and 2002

15%

26%

2%24%

8%

15%

10%

H orses

T obacco

P oultry

B eef

D airy

R ow C rops

O ther

2 4 %

1 4 %

1 6 %

1 3%

7 %

1 8%

8 %

1991 = $3 .2 B illion 2002 = $3 .11 B illion

Net Cash Returns from Ag. SalesKY and U.S. Avg. Per Farm

8270

12660

9055

15801

11909

22260

0

5000

10000

15000

20000

25000

1987 1992 1997

KYUS

Dollars Per Farm

Year Source: 1997 Census

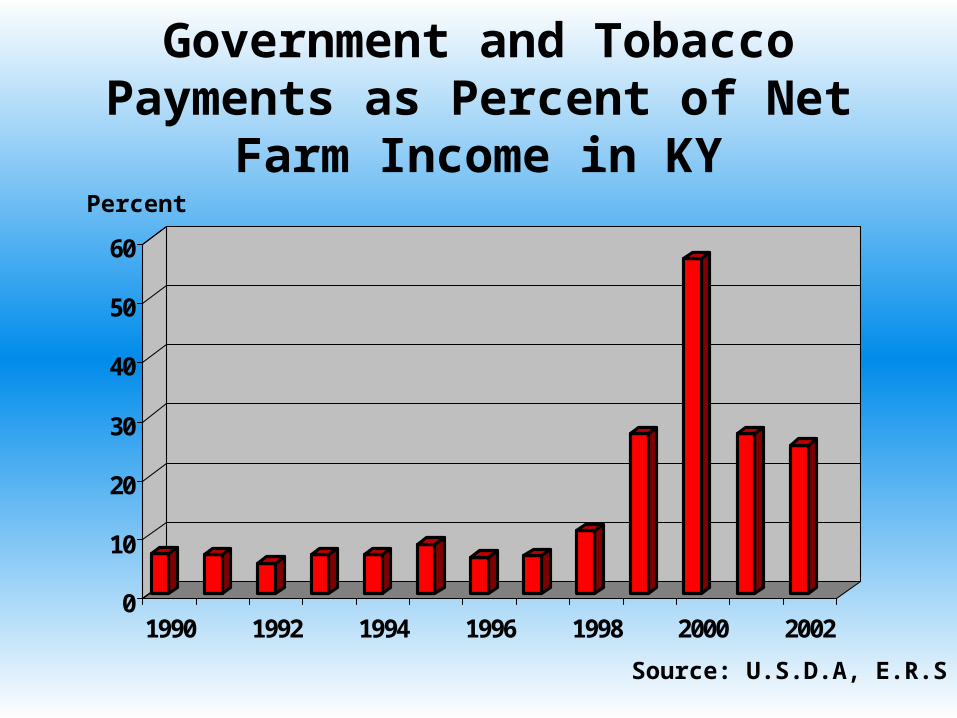

Government and Tobacco Payments as Percent of Net Farm Income in KY

0

10

20

30

40

50

60

1990 1992 1994 1996 1998 2000 2002

Source: U.S.D.A, E.R.S

Percent

KY Ag. Production-2002 Commodity National Rank

• Burley Tobacco 1• Equine 1• Other Hay 3• Beef Cows 8• Poultry 12• Corn 15• Soybeans 15• Milk Cows 18• Hogs 19• Alfalfa Hay 27

Type of Farm Organization

9%4%

1%

86%

Individual

Partnership

Family Corporation

Non-FamilyCorporation

Source: 1997 Agriculture Census

U.S. vs. Kentucky Farmer Profile

• 88% Caucasian

• 18,500 African-Amer.

• 10, 638 Native Amer.

• 8,731 Asian Amer.

• 27,717 Hispanic

• 7.6% Female Operated

• 98% Caucasian

• 523 African Amer.

• 123 Native Amer.

• 38 Asian Amer.

• 405 Hispanic

• 9% Female Operated

Source: 1997 Ag. Census

United States Kentucky

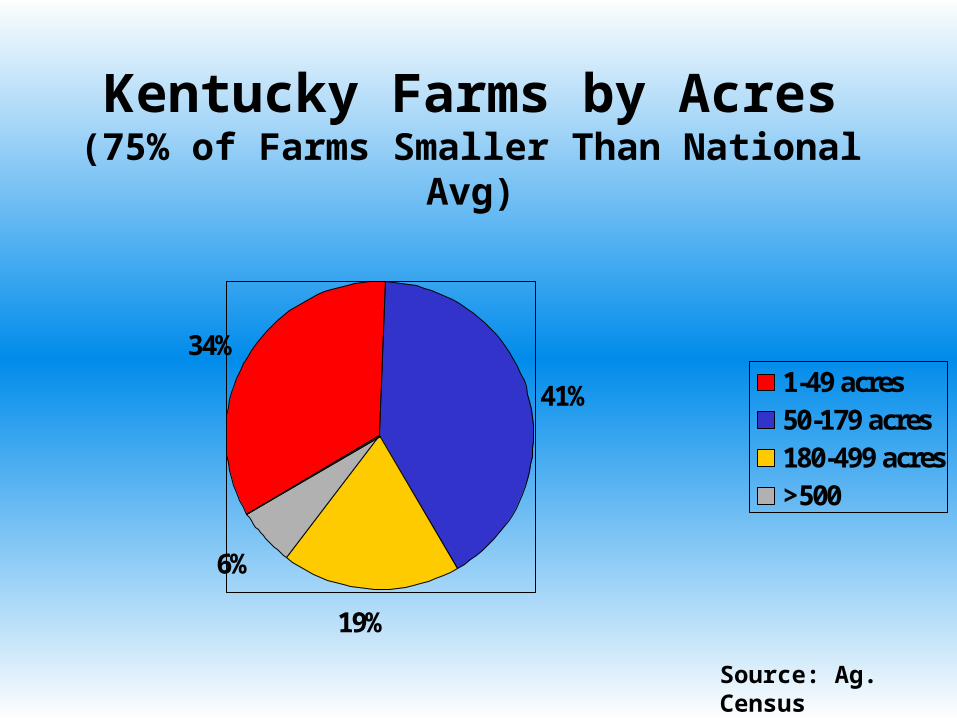

Kentucky Farms by Acres(75% of Farms Smaller Than National Avg)

34%

41%

19%

6%

1-49 acres50-179 acres180-499 acres>500

Source: Ag. Census

Farms and Sales of Ag Products

50

2

31

1115

31

4

56

0

10

20

30

40

50

60

<$10,000 <$100,000 <$499,000 >$500,000

% Farms% Sales

Source: 1997 Ag. Census

Percent

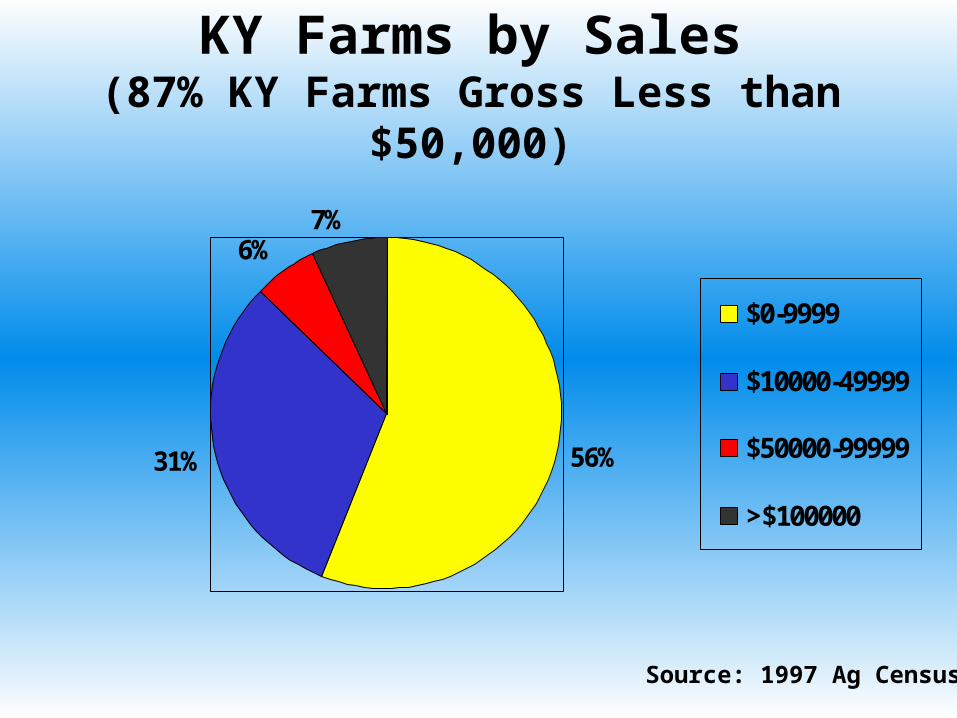

KY Farms by Sales(87% KY Farms Gross Less than $50,000)

56%31%

6%7%

$0-9999

$10000-49999

$50000-99999

>$100000

Source: 1997 Ag Census

Sources of Income for Average Farm Household

(Farm Income is 10% of Total)

10%

53%

18%

7%

12%Farm Income

Wages/Salaries

Off Farm Business

Interest/Dividends

Other Off-FarmIncome

Source: USDA Ag. Resource Mgt. Study

Average Farm and Off-Farm Income for Farm Households

-3438

16,142

44,131

164,469

49,377

38,177

34,460

36,289

-50000 0 50000 100000 150000 200000

< $50,000

$50,000-$249,999

$250,000-$499,999

>$500,000

Off Farm

Farm

Dollars

Size

USDA Ag. Resource Mgt. Study

Importance of Agriculture in Kentucky

• Farming represents 3.2% of state’s economic activity and 6.2% of jobs

• Forestry, inputs, and processing means added 9.5% of economic activity and 11.8% of jobs

• Adding retailing means entire system equals 16.2% of state’s economy and 21.1% of the jobs

Source: Godley and JonesIMPLAN, 2001

Current Trends in Agriculture

• Walmartization of production

• Globalization rewards low cost managers

• New trade agreements

• Shifting role of government policy

• Push for diversification, but….

• Widespread restructuring of agribusiness

Current Trends in Agriculture

• Products replace commodities

• Product safety concerns will grow

• Environmental factors influence location and concentration

• Technology explosion accelerates

• Information is “new” source of competitive advantage

Implications for Markets

• Evolution from commodities to components

• Price change from food and feed to component pricing

• Farm marketing-price takers to negotiators

• Contracting expands

• Markets become “thin”

• Value of information

SUMMARY

• Basic underlying trends continuing

• Think broadly of agriculture—it’s a system to produce and deliver consumer goods

• Importance of healthy rural economies to farm families

• Don’t underestimate the value of objective information in the current environment