Embed Size (px)

Citation preview

MCI (P) 137/11/2012 Ref No: RM2012_0234 1 of 17

Regional Market Focus

Phillip Securities Research Pte Ltd

4 December 2012

Hong Kong

China Railway – Benefit from re-acceleration of urban rail building! Recommendation: Accumulate Previous close: HK$4.48 Fair value: HK$5.20

The Company is one of the leaders of China transportation infrastructure group. The approval of railway as well as urban rail projects by the government has its positive influence on the domestic capital construction sector and the Company performance is undergoing recovery. For the first nine months of 2012, the Company realized operating income of RMB319.6 billion, which decreased by 4.8% year-on-year, slightly better than the YOY 11% decline of H1. It realized RMB4.27 billion net profits attributable to the listed company, up by 17.8% YOY, much better than the YOY 2.2% decline of H1, and EPS was RMB0.20. Even after deducting profit and loss impact of non-recurring items, the Company profits still increased by about 8% YOY, better than its peers.

For the first three quarters, the Company gross margin rose by 0.8 percentage from the 6.7% of the same period of last year to 7.5%, and Q3 gross margin basically leveled off with Q2 considering the single quarter performance of Q3. Future gross margin is expected to stay stable with recovery of the Company railway orders. Meanwhile, as the Ministry of Railway started to speed up payment of arrears after September, the Company financial status somewhat improved, and amount receivable slightly declined by 2.7% to RMB93.77 billion from the beginning of the year. net outflows of operating activities drastically declined by 49% to RMB12.47 billion year-on-year.

For the first three quarters, the Company secured new orders of RMB450.6 billion, up by 26% YOY, taking a quarter-by-quarter rise trend. Non transport orders including municipal and housing sprang up, while traditional railway and highway orders dropped substantially. As of the end of Q3, the Company uncompleted orders had reached RMB1.17 trillion, 2.54 times of the same period of 2011, so ample orders suffice to support development of the Company in next two years.

Counter-cyclical fluctuation is one of the features for urban rail and railway capital construction, and slack economy makes construction of such infrastructure construction more urgent, policies having been released in a concentrated fashion recently. With urbanization development as well as government further move to overhaul traffic jam and environmental pollution, we keep relatively optimistic about future development of the urban rail market. Against the background, tendering of a number of projects is expected to restart, which will drive growth of the Company new orders.

For valuation, we predict the diluted EPS of Company for 2012-2013 will reach RMB0.375 and RMB0.464, equivalent to HK$0.47 and HK$0.58. Comprehensively considering the Company advantageous position in the industry as well as promotion space of urban rail and housing business for the Company profitability, we grant 12-month target price of HK$5.2, equivalent to an expected 9-time PE for the end of 2013, hence accumulate rating.

Singapore

Singapore Banking Sector – MAS loans Update

Singapore’s total DBU loans outstanding registered y-y growth of 17.9% to S$479.4 billion in Oct 2012. Business loans and Consumer loans reported growth of 19.1% y-y and 16.3% y-y respectively.

M-m, loans growth in Oct 2012 was higher. Total loans grew 1.5%, compared to 0.7% in Sep 2012. Business loans grew 1.3% m-m, while Consumer loans grew faster at 1.8% m-m.

58.0% of total loans comprise of Business loans, with the remaining attributed to Consumer loans.

We are neutral on the Singapore Banking Sector, and will present a detailed outlook in our upcoming Singapore Banking Sector report.

Thailand

Thai Vegetable Oil – Company Update Recommendation: BUY Previous close: Bt23.30 Fair value: Bt27.75

High selling prices should enable TVO to post record earnings for CY12 though 4QCY12 results are expected to be weaker than 3QCY12.

Looking ahead into CY13, earnings are likely to be softer than CY12 as selling prices may not rise as much as in CY12.

We maintain a ‘BUY’ call on TVO with a target price of Bt27.75/share.

Regional Market Focus

4 December 2012

2 of 17

Strategy Views

- Country Strategy: China & HK, 23 Nov / Thai, 9 Nov / US, 24 Oct / Indon, 27 Sept / S'pore, 3 Sept / Malaysia, 31 Aug - Global Macro, Asset Strategy: 9 Oct / Update, 25 Oct Morning Commentary

- STI: -0.14% to 3065.7 - MSCI SE Asia: +0.15% to 843.9 - Hang Seng: -1.19% to 21767.8 - MSCI APxJ: -0.09% to 452 - Euro Stoxx 50: +0.28% to 2582.4 - S&P500: -0.47% to 1409.5 Transport Sector Update – SIA looking to sell Virgin: By Derrick Heng, SG Equity Strategist Sale of SIA's stake in Virgin Atlantic would unlock hidden value in the stock and release cash to the group. While we do not rule out the possibility for special dividends, we believe that any cash proceeds would more likely be redeployed into investments. Discussions on the sale is preliminary and we expect neutral stock impact. Olam’s rights cum bonds and warrants: By Joshua Tan, Hd of Research For 1000 Olam shares: 313 US$1.00 bonds yielding 6.75% due 2018 (US$750m raised) + 162 free detachable warrants for a new Olam share at strike price US$1.291 (potentially US$500m). Fully underwritten by Temasek. Obviously a move to put to rest doubts about its balance sheet after Muddy Waters, only we think it might have the opposite effect coming so soon off the back of the war of words. The warrants are dilutive even though Olam had said it was done with equity raisings. While we do not have coverage on Olam, our view is this: Olam’s asset heavy strategy warrants profit growth rates in the high teens at least and eventual free cash generation to justify all that capex. The current share price reflects that growth rates for FY2012 did not materialise. Investors who hold this stock need to keep a tab that such growth rates resume. Property Sector Update – Far East Orchard & Straits Trading By Travis Seah, REIT Analyst (This update is in response to a question posed at yesterday’s Weekly Webinar). On 26 Nov 2012, Far East Orchard Limited (FEOL) has inked a non-binding memorandum of understanding (MOU) with The Straits Trading Company Limited (STC) to explore the proposed acquisition of 50% interest in three hotels in Australia, namely, Rendezvous Studio Hotel Perth Central, Rendezvous Grand Hotel Melbourne and Rendezvous Hotel Perth and 50% interest in STC’s 50% stake in Costal Coffee Pty Ltd., a café business in Australia. Furthermore, the MOU also allows FEOL to explore the proposed acquisition of STC’s entire hospitality management business in its wholly-owned subsidiary (Hospitality Management Company). As part of the transaction, STC will have the right to subscribe up to 20% of the share capital of the enlarged Hospitality Management Company. We see the 50-50 joint venture to own the three hotels and café business, as well as the proposed acquisition of hospitality management business as a strategic partnership for both parties. STC had been recording net losses from its regional hotel operations for the past few years including the first nine months of the current financial year. With the collaboration, STC can leverage on FEOL’s experience in hospitality operations in a bid to reverse the losses, despite FEOL being a new entrant to Australia’s hospitality market, while FEOL would (1) diversify its hospitality portfolio beyond Singapore, and (2) be able to penetrate the mature but growing hospitality market in Australia which has a high barrier to entry due to exorbitant construction costs to establish hotel properties.

MARKET OUTLOOK: By Joshua Tan, Hd of Research Yesterday morning we said that although trading signals for stocks are still generally positive, we’re a little cautious on technical reasons as well as the way fiscal cliff negotiations are going. Our stance today is a little stronger on the negative side and short term traders may want to consider mounting positions on the short side. Technicals: the S&P500 indeed rejected off the 50dma and 1417 neckline – a confluence of resistance, while the STI’s brief foray beyond the upper downward sloping trendline (yesterday’s webinar slides shows this trendline, pls ask your dealer for a copy) was sold into to close slightly below it – not a super strong rejection but a rejection nonetheless and should be seen in context of broader market action. The HIS and HSCEI have also halted their upward trajectory. (see Phillip CFD for trading indices) Global macro data has been signalling a stabilization and giving hope to a reacceleration – the only major country which gave a backward November number on the manufacturing PMI was the US! China flipped into expansion on the HSBC Mfg PMI, corroborating the official PMI which strengthened, while even the EZ’s rate of contraction eased. Thus fiscal cliff uncertainty continues to be a drag and poses a challenge for the US economy.

Regional Market Focus

4 December 2012

3 of 17

On fiscal cliff negotiations: currently the President has asked for US$1tr tax increases on the wealthy, plus US$600b more revenues by closing tax loopholes, and a US$50b infrastructure spend, while offering US$400b of entitlement cuts in return. Republicans have balked as the combined US$1.6b over 10yrs proposal which is 33% more than last year’s proposal of US$1.2tr revenues, while the US$400b spending cuts proposal is the same. Recall that Republican’s could not get past this last year (they were willing to give US$800b revenues max) and talks broke down. Thus, the President, leveraging off his election victory which is also widely seen as a decisive repudiation of Republican ideology – is upping the ante by asking for 33% more while giving the same. Uh oh… Positive niceties over, fight begins. Peering further out into 2013: Assuming we get a deal, we are getting increasingly constructive on the investment climate going into 1H13 - underlying macro conditions see the rate of slowdown in Asia easing and China bottoming. While the US is mixed in our opinion – housing recovery (good), consumption subsidised by savings (mixed), investment sentiment crushed by the fiscal cliff uncertainty (bad) – if a political compromise is reached on the fiscal cliff, a rebound in investment could be catalytic for markets. SG equity strategist favours Capitaland, SATS and SIAEC. MACRO DATA

In US, manufacturing activity reversed into contraction in Nov. Specifically, the ISM manufacturing index slumped from 51.7 in Oct to 49.5 (a 3-year low) in Nov. While it might be tempting to view this weak reading as a temporary distortion due to Hurricane Sandy, we wish to highlight that production has actually gained 1.3 pts m-m (to 53.7). Instead, we reckon that the decline in manufacturing was largely due to to lower new orders (with businesses holding back capex in view of uncertainties shrouding the looming fiscal cliff) as well as a continued contraction in export orders. In Thailand, inflation decelerated from 3.32% y-y in Oct to 2.74% in Nov. Core inflation- which excludes energy and fresh food prices- inched up slightly to 1.85%, from 1.83% in the preceding month, still within the central bank’s target range of 0.5%-3%. Looking ahead, in view of the benign inflation as well as pre-emptive Oct rate cut, we expect BoT to stand pat unless economic activity substantially slows down. In Indonesia, inflation eased from 4.61% y-y in Oct to 4.32% in Nov, owing to lower food prices. Exports continued to decline 7.61% y-y in Oct, following the 9.35% contraction in the preceding month. With inflation print ytd well within the central bank’s year-end target range of 3.5 - 5.5%, we expect Bank Indonesia to continue to stand pat on the back of lower inflation expectations as well as resilient domestic demand. As we have guided previously, a rate cut is unlikely as such a dovish stance would further exacerbate the weakness in rupiah (IDR) in view of Indonesia’s sluggish external balances. In Euro zone, final manufacturing PMI remained at 46.2 in Nov, slight improvement from 45.4 in Oct, but still a contraction in manufacturing activities for the 16th straight month. Flash manufacturing PMI for Germany stayed at 46.8, the same as it was in Oct, indicating a contraction and the gauge for France fell to 44.5 from earlier 44.7, indicating a slightly faster contraction in manufacturing activities. In China, HSBC manufacturing PMI rose to 50.5 in Nov, marking the highest in the last 13 months, indicating a moderate expansion in the nation’s manufacturing sector, compared to 49.5 in Oct. A separate report showed that the government backed non-manufacturing PMI rose to 55.6 in Nov from 55.5 in Oct, indicating a slightly faster expansion in the nation’s non-manufacturing sector. The China’s economy is consolidating strength to bottom out though the pace could be slow as external environment remain uncertain due to the Europe debt crisis and approaching US fiscal cliff. In Taiwan, HSBC manufacturing PMI fell to 47.4 in Nov, compared to 47.8 in Oct, indicating a faster contraction in the island’s manufacturing activities. In Japan, capital expenditure rose by 2.2% y-y in 3q12, slower compared to the 7.7% y-y pace in 2q12. The nation’s economy is likely to run into a recession in the fourth quarter. The bank of Japan would likely continue to play easing card in Dec, though the framework of new government may still be not clear in the new policy meeting on 19 and 20 Dec. In South Korea, CPI fell by 0.4% m-m in Nov, after the 0.1% m-m drop in Oct. On y-y basis, CPI rose by 1.6% y-y, compared to the 2.1% y-y pace in Oct. Though there are signs of stabilization, the nation’s economy is still at a fragile state. The government is holding the benchmark rate at 2.75% and the easing inflation does have granted the government with further scope for benchmark rate cut. In Australia, performance of manufacturing index fell to 43.6 in Nov from 45.2 in Oct, marking a contraction for a ninth consecutive month. Total manufacturing income rose by 1.3% q-q in 3q12, after 1.9% q-q drop in 2q12. Gross operating profit of business fell by 2.9% q-q in 3q12, after a revised 0.3% q-q drop in 2q12. The nation’s retail sales stay unchanged in Oct from Sept, where it advanced 0.5% m-m. An inflation gauge, TD inflation, fell by 0.1% m-m in Nov, reversing the 0.1% m-m gain in Oct. Over the year, price index rose by 2.5%, falling at the middle of the government’s target range of 2-3%. With the non-performing business profit and the inflation staying in target range, the RBA governor may announce a further 25 bps cut in benchmark rate to 3.0% later today.

Regional Market Focus

4 December 2012

4 of 17

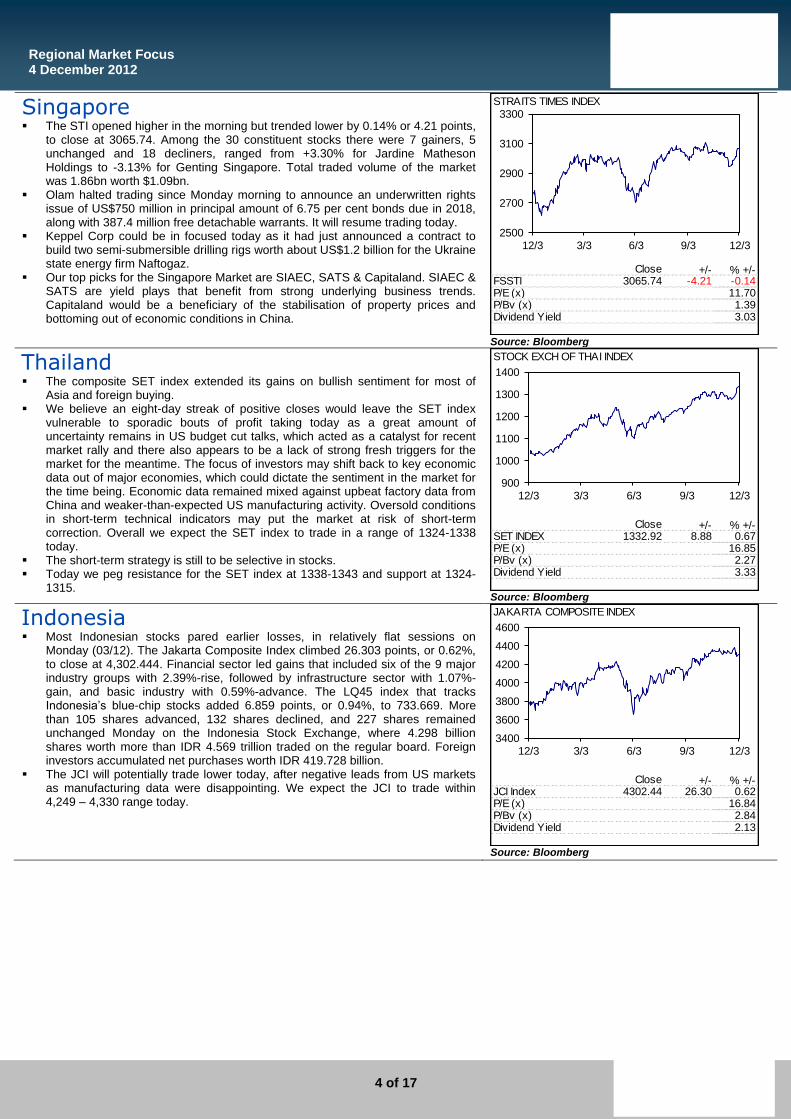

Singapore The STI opened higher in the morning but trended lower by 0.14% or 4.21 points,

to close at 3065.74. Among the 30 constituent stocks there were 7 gainers, 5 unchanged and 18 decliners, ranged from +3.30% for Jardine Matheson Holdings to -3.13% for Genting Singapore. Total traded volume of the market was 1.86bn worth $1.09bn.

Olam halted trading since Monday morning to announce an underwritten rights issue of US$750 million in principal amount of 6.75 per cent bonds due in 2018, along with 387.4 million free detachable warrants. It will resume trading today.

Keppel Corp could be in focused today as it had just announced a contract to build two semi-submersible drilling rigs worth about US$1.2 billion for the Ukraine state energy firm Naftogaz.

Our top picks for the Singapore Market are SIAEC, SATS & Capitaland. SIAEC & SATS are yield plays that benefit from strong underlying business trends. Capitaland would be a beneficiary of the stabilisation of property prices and bottoming out of economic conditions in China.

Close +/- % +/-FSSTI 3065.74 -4.21 -0.14P/E (x) 11.70P/Bv (x) 1.39

3.03Dividend Yield

STRAITS TIMES INDEX

2500

2700

2900

3100

3300

12/3 3/3 6/3 9/3 12/3

Source: Bloomberg

Thailand The composite SET index extended its gains on bullish sentiment for most of

Asia and foreign buying. We believe an eight-day streak of positive closes would leave the SET index

vulnerable to sporadic bouts of profit taking today as a great amount of uncertainty remains in US budget cut talks, which acted as a catalyst for recent market rally and there also appears to be a lack of strong fresh triggers for the market for the meantime. The focus of investors may shift back to key economic data out of major economies, which could dictate the sentiment in the market for the time being. Economic data remained mixed against upbeat factory data from China and weaker-than-expected US manufacturing activity. Oversold conditions in short-term technical indicators may put the market at risk of short-term correction. Overall we expect the SET index to trade in a range of 1324-1338 today.

The short-term strategy is still to be selective in stocks. Today we peg resistance for the SET index at 1338-1343 and support at 1324-

1315.

Close +/- % +/-SET INDEX 1332.92 8.88 0.67P/E (x) 16.85P/Bv (x) 2.27

3.33Dividend Yield

STOCK EXCH OF THAI INDEX

900

1000

1100

1200

1300

1400

12/3 3/3 6/3 9/3 12/3

Source: Bloomberg

Indonesia

Most Indonesian stocks pared earlier losses, in relatively flat sessions on Monday (03/12). The Jakarta Composite Index climbed 26.303 points, or 0.62%, to close at 4,302.444. Financial sector led gains that included six of the 9 major industry groups with 2.39%-rise, followed by infrastructure sector with 1.07%-gain, and basic industry with 0.59%-advance. The LQ45 index that tracks Indonesia’s blue-chip stocks added 6.859 points, or 0.94%, to 733.669. More than 105 shares advanced, 132 shares declined, and 227 shares remained unchanged Monday on the Indonesia Stock Exchange, where 4.298 billion shares worth more than IDR 4.569 trillion traded on the regular board. Foreign investors accumulated net purchases worth IDR 419.728 billion.

The JCI will potentially trade lower today, after negative leads from US markets as manufacturing data were disappointing. We expect the JCI to trade within 4,249 – 4,330 range today.

Close +/- % +/-JCI Index 4302.44 26.30 0.62P/E (x) 16.84P/Bv (x) 2.84

2.13Dividend Yield

JAKARTA COMPOSITE INDEX

3400

3600

3800

4000

4200

4400

4600

12/3 3/3 6/3 9/3 12/3

Source: Bloomberg

Regional Market Focus

4 December 2012

5 of 17

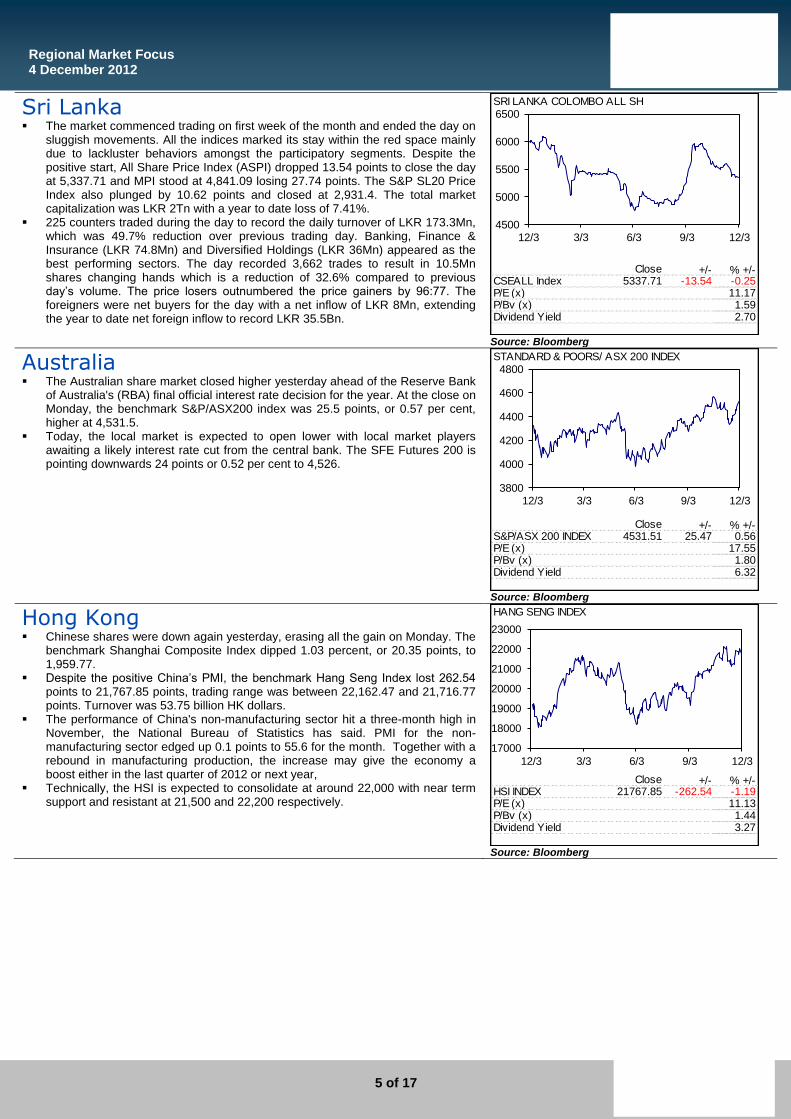

Sri Lanka The market commenced trading on first week of the month and ended the day on

sluggish movements. All the indices marked its stay within the red space mainly due to lackluster behaviors amongst the participatory segments. Despite the positive start, All Share Price Index (ASPI) dropped 13.54 points to close the day at 5,337.71 and MPI stood at 4,841.09 losing 27.74 points. The S&P SL20 Price Index also plunged by 10.62 points and closed at 2,931.4. The total market capitalization was LKR 2Tn with a year to date loss of 7.41%.

225 counters traded during the day to record the daily turnover of LKR 173.3Mn, which was 49.7% reduction over previous trading day. Banking, Finance & Insurance (LKR 74.8Mn) and Diversified Holdings (LKR 36Mn) appeared as the best performing sectors. The day recorded 3,662 trades to result in 10.5Mn shares changing hands which is a reduction of 32.6% compared to previous day’s volume. The price losers outnumbered the price gainers by 96:77. The foreigners were net buyers for the day with a net inflow of LKR 8Mn, extending the year to date net foreign inflow to record LKR 35.5Bn.

Close +/- % +/-CSEALL Index 5337.71 -13.54 -0.25P/E (x) 11.17P/Bv (x) 1.59

2.70

Dividend Yield

SRI LANKA COLOMBO ALL SH

4500

5000

5500

6000

6500

12/3 3/3 6/3 9/3 12/3

Source: Bloomberg

Australia

The Australian share market closed higher yesterday ahead of the Reserve Bank of Australia's (RBA) final official interest rate decision for the year. At the close on Monday, the benchmark S&P/ASX200 index was 25.5 points, or 0.57 per cent, higher at 4,531.5.

Today, the local market is expected to open lower with local market players awaiting a likely interest rate cut from the central bank. The SFE Futures 200 is pointing downwards 24 points or 0.52 per cent to 4,526.

Close +/- % +/-S&P/ASX 200 INDEX 4531.51 25.47 0.56P/E (x) 17.55P/Bv (x) 1.80

6.32

STANDARD & POORS/ ASX 200 INDEX

Dividend Yield

3800

4000

4200

4400

4600

4800

12/3 3/3 6/3 9/3 12/3

Source: Bloomberg

Hong Kong

Chinese shares were down again yesterday, erasing all the gain on Monday. The benchmark Shanghai Composite Index dipped 1.03 percent, or 20.35 points, to 1,959.77.

Despite the positive China’s PMI, the benchmark Hang Seng Index lost 262.54 points to 21,767.85 points, trading range was between 22,162.47 and 21,716.77 points. Turnover was 53.75 billion HK dollars.

The performance of China's non-manufacturing sector hit a three-month high in November, the National Bureau of Statistics has said. PMI for the non-manufacturing sector edged up 0.1 points to 55.6 for the month. Together with a rebound in manufacturing production, the increase may give the economy a boost either in the last quarter of 2012 or next year,

Technically, the HSI is expected to consolidate at around 22,000 with near term support and resistant at 21,500 and 22,200 respectively.

Close +/- % +/-HSI INDEX 21767.85 -262.54 -1.19P/E (x) 11.13P/Bv (x) 1.44

3.27Dividend Yield

HANG SENG INDEX

17000

18000

19000

20000

21000

22000

23000

12/3 3/3 6/3 9/3 12/3

Source: Bloomberg

Regional Market Focus

4 December 2012

6 of 17

Market News

US U.S. regulators probing potential fraud by China-based companies increased pressure on their auditors by formally accusing affiliates of

Big Four firms of withholding documents from investigators. Deloitte Touche Tohmatsu CPA Ltd., Ernst & Young Hua Ming LLP, KPMG Huazhen and PricewaterhouseCoopers Zhong Tian CPAs Limited have refused to cooperate with accounting fraud investigations into nine companies whose securities are publicly traded in the U.S., the Securities and Exchange Commission said in an administrative order yesterday. BDO China Dahua Co. Ltd. was also named by the SEC in the action. China-based companies listed on U.S. exchanges have faced increased scrutiny over the past two years after regulators became concerned that some firms may not be providing accurate financial statements to investors. Investigators have struggled to obtain documents central to the probes because auditors, citing China’s laws, have declined to cooperate. (Source: Bloomberg)

Many executives say they're anxious about the US fiscal cliff negotiations, but Dow Chemical Co's chief executive says he's more

bothered by the messy Chinese leadership transition, which he believes is wreaking greater harm on global markets. "Markets have, in a holistic sense, really been suffering more from China's slowdown than any slowdown here in the United States," Andrew Liveris said during the company's investor day in New York on Monday. China, Dow Chemical's second-largest market by sales, unveiled its new leaders in November after months of speculation about who would assume top roles, as well as controversy about widespread corruption among government officials and the cooling growth of the country's economy. The leadership transition has been "very uncomfortable" for the Chinese and has "created a disruption to their supply chains and created a pause" in economic growth rates, Mr Liveris said. (Source: BT Online)

Singapore A 13-year marriage that started happily enough but soon deteriorated into an unhappy co- existence could soon end in divorce:

Singapore Airlines (SIA) is said to be ready to offload its 49 per cent stake in Richard Branson-controlled Virgin Atlantic. Delta, the second-biggest airline in the United States by revenue, is said to be in talks to buy SIA's stake. British newspapers say that the deal could also be a precursor to Delta's European partner Air France- KLM buying out Mr Branson's entire 51 per cent majority stake in Virgin Atlantic. European Union rules require majority European ownership of a European carrier. SIA did not provide a definitive confirmation of any imminent deal. (Source: BT Online)

Olam played its Temasek trump card yesterday against the onslaught by short-sell research firm Muddy Waters, unveiling a rights issue that will raise up to US$1.25 billion in capital. The rights issue will consist of up to US$750 million in five-year bonds, to be accompanied by warrants that will raise up to US$500 million upon conversion. While the deal is fully underwritten by Credit Suisse, DBS, HSBC and JP Morgan, Olam has gone the whole hog by adding another layer of underwriting. Temasek, which owns about 16 per cent of Olam, has thrown its weight behind the commodities-trading firm, not only committing to take up its pro-rata entitlement of the rights, but to also sop up 100 per cent of the rights not subscribed to by existing shareholders. At a hastily called briefing for media and analysts last evening, Olam's bankers turned out in full besuited force as its chief executive Sunny Verghese gave a presentation on the deal and attempted to send a message to the markets and to Carson Block, the Muddy Waters man shorting his firm's stock. (Source: BT Online)

Eighty-nine people were injured yesterday morning in Jurong Shipyard after the jack-up rig that they were working on listed. Of those hurt, 80 had been discharged from hospital by 8pm after receiving treatment for minor injuries, while six were admitted. The remaining three were kept under observation. The majority of the 89 are foreign workers. In a statement, parent company Singapore Exchange-listed Sembcorp Marine said that all personnel onboard had been accounted for, and there were no fatalities. (Source: BT Online)

SMRT has taken a series of actions in response to the concerns of drivers from China (PRC) who had gone on an illegal strike last week and has also explained to them their pay structure. Speaking in Mandarin yesterday at a town hall meeting with SMRT's PRC drivers, Desmond Kuek, president and chief executive officer of the public transport operator, described their compensation as "fair and equitable", compared to that of their Malaysian counterparts. PRC drivers are on a two-year contract, while Malaysian ones are permanent hires, he said, so "the nature of such short contracts and longer-term employment tenures are necessarily different". He added that PRC drivers are covered for transport, accommodation and utilities amounting to about $275 a month, while Malaysian drivers have to rent a place or return home across the Causeway after work, he said. (Source: BT Online)

Hong Kong

For many months, stock analysts have been trying to drum up some confidence in the moribund A-share market by alluding to the growing interest of overseas investors, including many hedge funds that are looking for bargains. Every positive, even if it's off-hand, comment about the Chinese stock market by the likes of Warren Buffett or George Soros has been enthusiastically promoted by the domestic media as the prelude to an influx of foreign investment capital that could help kick-start a bull run. But most investors don't seem to share the enthusiasm of these drum beaters, choosing rather to stay on the sidelines watching the most widely followed Shanghai Composite Index struggling to stay above the 2,000 level that is seen as a make-or-break psychological barrier. Having been proven wrong so many times, even the most ardent stock market bulls are beginning to doubt whether the current market valuation is too high. This apparently prompted People's Daily to pose the question: Why has the stock market performed so badly when the economy is doing so well? Perhaps more global fund managers are coming to realize that such a mismatch of economic factors cannot last. The improvement in economic fundamentals, indicated by a pickup in exports, in recent months has further boosted their confidence in the prospects of the Chinese stock market. (Source: peopledaily.com.)

Regional Market Focus

4 December 2012

7 of 17

The Chinese currency Renminbi, or yuan, weakened 16 basis points to 6.2908 against the U.S. dollar on Monday, according to the China Foreign Exchange Trading System. In China's foreign exchange spot market, the yuan is allowed to rise or fall by 1 percent from the central parity rate each trading day. The central parity rate of the yuan against the U.S. dollar is based on a weighted average of prices before the opening of the market each business day. (Source: peopledaily.com.)

China’s overseas investment has risen sharply in recent years. And as the country pushes ahead with its “Go-Out” strategy, State Owned Enterprises are being urged to expand outward investment further. “China’s state owned enterprises should continue to seek business opportunities in various sectors worldwide”, Chen Yuan, the newly appointed chairman of Chinese Enterprise Investment Association made the remark at its high-level council meeting in the Great Hall of People, adding that domestic companies need to further expand investment overseas. Chen Yuan said, “As well as attracting inward foreign investment, domestic enterprises should focus more on expanding outward foreign investment, and speed up transformation of outward investment models.” (Source: peopledaily.com.)

Thailand Foreign investors remained net buyers of Thai shares worth Bt1,958.65mn on Mon. (Source: Bisnews)

Thailand's annual headline inflation rate slipped to 2.74% y-y in Nov from 3.32% y-y in Oct as food prices rose less than in Oct which

should give the central bank leeway to keep interest rates low or cut them if needed to boost growth due to global economic woes. (Source: Reuters)

The Administrative Court on Mon dismissed a petition asking it to suspend the NBTC’s process of granting the 3G licenses on 2.1GHz to three bid winners, citing the Office of the Ombudsman had no right to bring the case against the NBTC. With the court ruling, the NBTC can go ahead with the issuing of the 3G licenses within 90 days of the approval of the bidding process, or by Jan 19. (Source: Bangkok Post)

Kasikorn Research Center has forecast Thailand’s annual inflation rate to pick up from 3% to 3%-3.6% in early 2013 as a result of the daily minimum wage hike and volatile energy prices, according to Kasikorn Research Center (KRC). (Source: Post Today)

Indonesia Indonesia`s economic growth in 2013 was predicted to be lower than this year. The indicator of this is the slowing down of the Chinese

economy and the stalled economic growth of the Unites States, the economic growth target of 6 percent for 2013 was just possible, particularly if the Master Plan for the Acceleration and Expansion of Indonesia`s Economic Development (MP3EI) was implemented successfully. n the meantime, if coal is exported, rubber and crude palm oil (CPO) prices will increase. The economic growth can even exceed 6.8 percent or at a range of 7-8 percent if the annual inflation rate reached 9-11 percent and if the MP3EI succeeded in realizing many investment projects. (Source: AntaraNews)

November’s export is projected to decline, but slower than in October. Meanwhile, import is still rising causing the trade balance to surplus again – though still below USD 1 billion. The decline in exports is influenced by the global economic downturn and the fall in commodity prices. IFT’s poll of economists and analysts of domestic and international banking, securities and research agencies shows a median of October 2012’s trade balance at a surplus of USD 620 million, higher than the September’s trade surplus of USD 552.9 million. (Source: Indonesia Finance Today)

November 2012’s inflation is expected to be higher than in October, driven by the rising food prices. Food prices increase due to reduced supply – an impact of flooding. Meanwhile, the decline in prices of gold jewelry – triggered by gold price decrease in the international market, also pulls inflation downward. IFT’s poll of economists and analysts of domestic and international banking, securities and research agencies also shows that the weakening of the rupiah and the rising beef prices in the last few days of November have no significant effect on inflation. (Source: Indonesia Finance Today)

Sri Lanka Core inflation is used to gauge underlying price movements in an economy with food, fuel and other sensitive items being excluded from

the index although some economists argue that core inflation is not an accurate measure of price movements because it leaves out food and fuels. Core inflation in Sri Lanka has increased both on a year-on-year and annual average basis to 7.2 per cent and 5.6 per cent respectively in November 2012, the Central Bank said, from 6.8 per cent and 5.4 per cent respectively the previous month. Inflation, as measured by the Colombo Consumers’ Price Index (CCPI) (2006/07*100), increased to 9.5 per cent in November 2012 on a year-on-year basis from 8.9 per cent in the previous month mainly due to the increase in food prices. Moreover, the inflation rate on an annual average basis increased to 7.2 per cent in November 2012 from 6.8 per cent in October 2012. The CCPI increased by 1.3 per cent in November 2012 over the previous month, with the Index increasing in absolute terms to 167.1 from 165.0 in October 2012. The contribution to the monthly increase in the Index came mainly from price increases in the Food category. (island.lk)

Regional Market Focus

4 December 2012

8 of 17

Australia A slowing economy has cut company profits and wages, damaging the government's plans for returning the budget to surplus and

sealing the case for a pre-Christmas interest rate cut at today's Reserve Bank board meeting. Company profits are now no higher than they were in 2008, ahead of the global financial crisis, and the September quarter was the first time total wages have dropped since September 2009 in the heart of the crisis. (Source: The Australian)

Premier Investments chairman Solomon Lew has slammed the federal government for failing to remove the GST exemption on internet purchases of less than $1000 from foreign companies. Speaking at the company's annual general meeting in Melbourne today, Mr Lew, whose company owns Peter Alexander, Smiggle, Just Jeans and other retail chains, said the "flawed, two-tiered tax system" directly disadvantaged Australian business, including online retailers. Mr Lew, cited the collapse of retailers including Borders, Colorado, Brown Sugar and Fletcher Jones and labour force figures showing that 22,600 jobs had been lost in the retail sector over the past 18 months as evidence the government needed to act quickly. (Source: The Australian)

The federal government has blamed the states for the Council of Australian Governments' failure to meet reform deadlines meant to add billions of dollars to GDP. Ahead of a COAG meeting on Friday, Finance Minister Penny Wong said 17 of 27 national reforms set out in 2008 to deliver a seamless national economy had been agreed. But she said outstanding reforms could not be achieved by the federal government alone. “I understand the concerns of people in the business community who want reform faster,” she told ABC radio. “But as I say to them, `make sure you talk not just to me but go and talk to the states as well', because all of these things have to be agreed across governments.” And in a number of the areas ... where we haven't achieved it, it's not because the federal government has walked away, it's because key states have changed their mind.” (Source: The Australian)

Regional Market Focus

4 December 2012

9 of 17

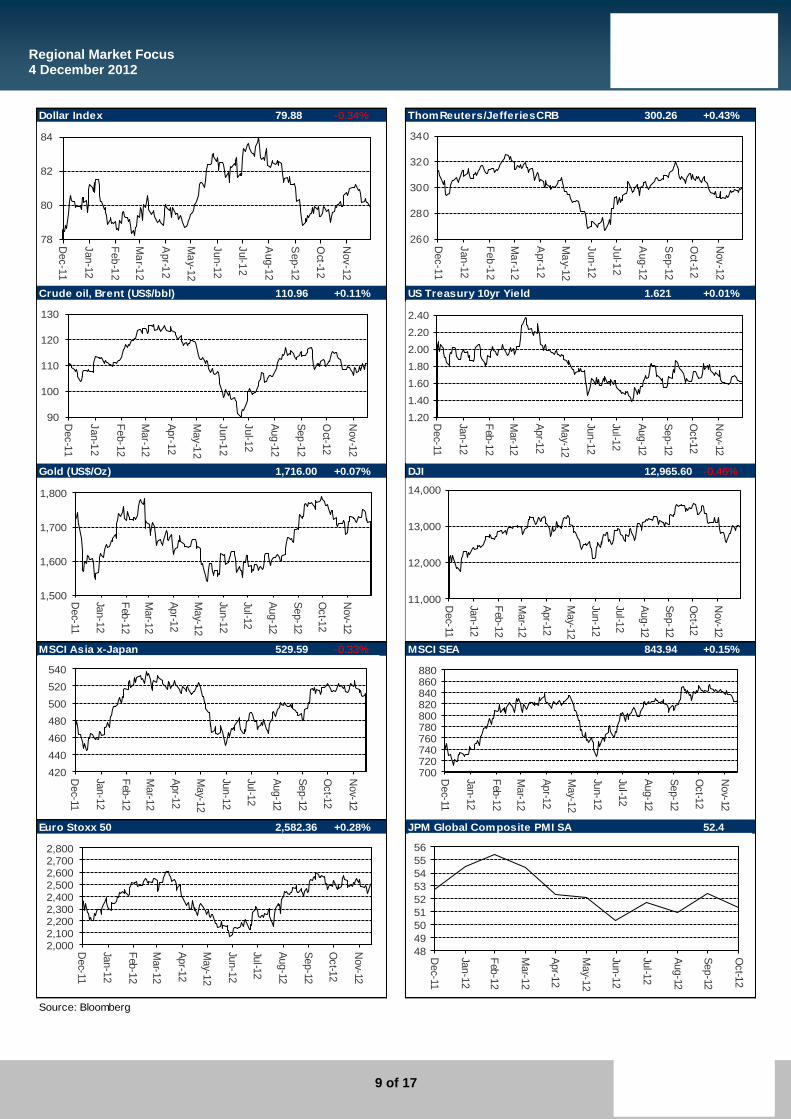

79.88 -0.34% 300.26 +0.43%

110.96 +0.11% 1.621 +0.01%

1,716.00 +0.07% 12,965.60 -0.46%

529.59 -0.33% MSCI SEA 843.94 +0.15%

2,582.36 +0.28% 52.4

Source: Bloomberg

MSCI Asia x-Japan

JPM Global Composite PMI SA

ThomReuters/JefferiesCRB

DJI

Crude oil, Brent (US$/bbl) US Treasury 10yr Yield

Euro Stoxx 50

Dollar Index

Gold (US$/Oz)

1.20

1.40

1.60

1.80

2.00

2.20

2.40

Dec-11

Jan-1

2

Feb

-12

Mar-1

2

Apr-1

2

May-1

2

Jun-1

2

Jul-1

2

Aug-12

Sep-12

Oct-1

2

Nov-12

700720740760780800820840860880

Dec-11

Jan-1

2

Feb

-12

Mar-1

2

Apr-1

2

May-1

2

Jun-1

2

Jul-1

2

Aug-12

Sep-12

Oct-1

2

Nov-12

11,000

12,000

13,000

14,000

Dec-11

Jan-1

2

Feb

-12

Mar-1

2

Apr-1

2

May-1

2

Jun-1

2

Jul-1

2

Aug-12

Sep-12

Oct-1

2

Nov-12

2,0002,1002,2002,3002,4002,5002,6002,7002,800

Dec-11

Jan-1

2

Feb

-12

Mar-1

2

Apr-1

2

May-1

2

Jun-1

2

Jul-1

2

Aug-12

Sep-12

Oct-1

2

Nov-12

48

49

50

51

52

53

54

55

56

Dec-11

Jan-1

2

Feb

-12

Mar-1

2

Apr-1

2

May-1

2

Jun-1

2

Jul-1

2

Aug-12

Sep-12

Oct-1

2

1,500

1,600

1,700

1,800

Dec-11

Jan-1

2

Feb

-12

Mar-1

2

Apr-1

2

May-1

2

Jun-1

2

Jul-1

2

Aug-12

Sep-12

Oct-1

2

Nov-12

78

80

82

84

Dec-1

1

Jan-1

2

Feb

-12

Ma

r-12

Apr-1

2

Ma

y-12

Jun-1

2

Jul-1

2

Aug-1

2

Sep-1

2

Oct-1

2

Nov-1

2

260

280

300

320

340

Dec-1

1

Jan-1

2

Feb

-12

Ma

r-12

Apr-1

2

Ma

y-12

Jun-1

2

Jul-1

2

Aug-1

2

Sep-1

2

Oct-1

2

Nov-1

2

90

100

110

120

130

Dec-1

1

Jan-1

2

Feb-1

2

Mar-1

2

Apr-1

2

May-1

2

Jun-1

2

Jul-1

2

Aug

-12

Sep

-12

Oct-1

2

Nov-1

2

420

440

460

480

500

520

540

Dec-11

Jan-1

2

Feb

-12

Mar-1

2

Apr-1

2

May-1

2

Jun-1

2

Jul-1

2

Aug-12

Sep-12

Oct-1

2

Nov-12

Regional Market Focus

4 December 2012

10 of 17

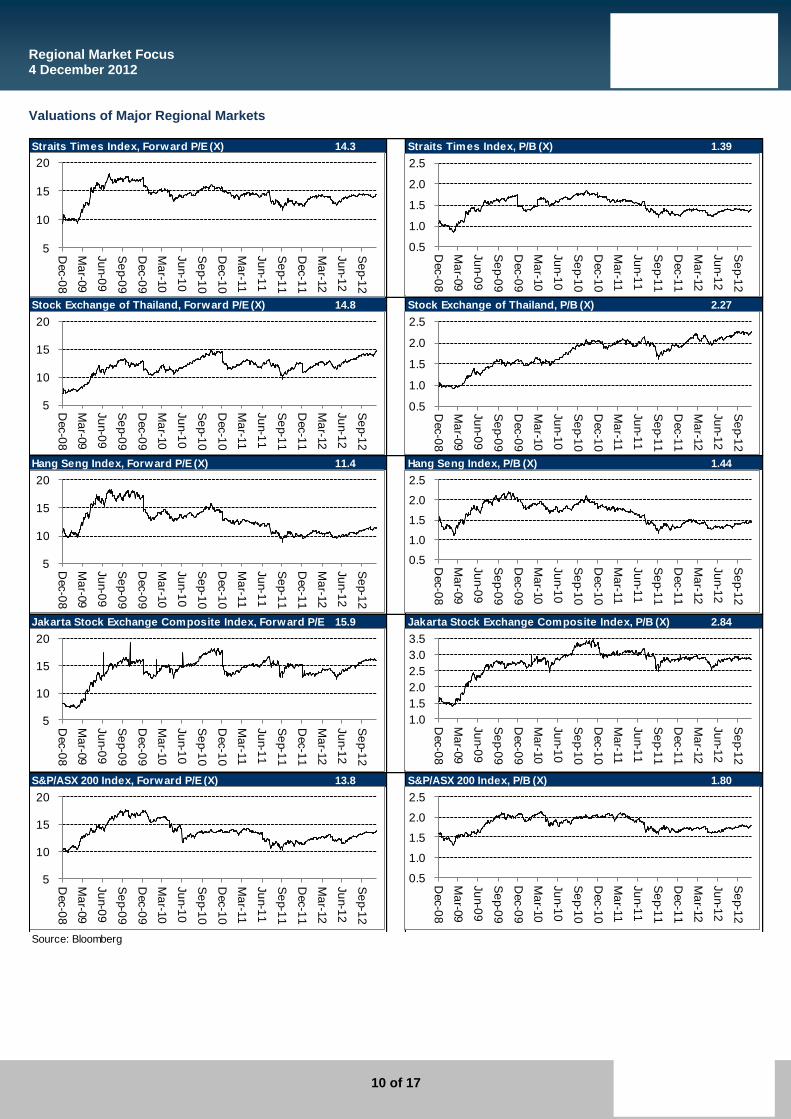

Valuations of Major Regional Markets

14.3 1.39

14.8 2.27

11.4 1.44

15.9 2.84

13.8 1.80

Source: Bloomberg

Jakarta Stock Exchange Composite Index, P/B (X)Jakarta Stock Exchange Composite Index, Forward P/E

Straits Times Index, Forward P/E (X)

Hang Seng Index, Forward P/E (X)

Straits Times Index, P/B (X)

Stock Exchange of Thailand, Forward P/E (X) Stock Exchange of Thailand, P/B (X)

Hang Seng Index, P/B (X)

S&P/ASX 200 Index, Forward P/E (X) S&P/ASX 200 Index, P/B (X)

5

10

15

20

Dec-0

8

Ma

r-09

Ju

n-0

9

Se

p-0

9

Dec-0

9

Ma

r-10

Ju

n-1

0

Se

p-1

0

Dec-1

0

Ma

r-11

Ju

n-1

1

Se

p-1

1

Dec-1

1

Ma

r-12

Ju

n-1

2

Se

p-1

2

0.5

1.0

1.5

2.0

2.5

Dec-0

8

Ma

r-09

Ju

n-0

9

Se

p-0

9

Dec-0

9

Ma

r-10

Ju

n-1

0

Se

p-1

0

Dec-1

0

Ma

r-11

Ju

n-1

1

Se

p-1

1

Dec-1

1

Ma

r-12

Ju

n-1

2

Se

p-1

2

0.5

1.0

1.5

2.0

2.5

Dec-0

8

Ma

r-09

Ju

n-0

9

Se

p-0

9

Dec-0

9

Ma

r-10

Ju

n-1

0

Se

p-1

0

Dec-1

0

Ma

r-11

Ju

n-1

1

Se

p-1

1

Dec-1

1

Ma

r-12

Ju

n-1

2

Se

p-1

2

5

10

15

20

Dec-0

8

Ma

r-09

Ju

n-0

9

Se

p-0

9

Dec-0

9

Ma

r-10

Ju

n-1

0

Se

p-1

0

Dec-1

0

Ma

r-11

Ju

n-1

1

Se

p-1

1

Dec-1

1

Ma

r-12

Ju

n-1

2

Se

p-1

2

0.5

1.0

1.5

2.0

2.5

Dec-0

8

Ma

r-09

Ju

n-0

9

Se

p-0

9

Dec-0

9

Ma

r-10

Ju

n-1

0

Se

p-1

0

Dec-1

0

Ma

r-11

Ju

n-1

1

Se

p-1

1

Dec-1

1

Ma

r-12

Ju

n-1

2

Se

p-1

2

5

10

15

20

Dec-0

8

Ma

r-09

Ju

n-0

9

Se

p-0

9

Dec-0

9

Ma

r-10

Ju

n-1

0

Se

p-1

0

Dec-1

0

Ma

r-11

Ju

n-1

1

Se

p-1

1

Dec-1

1

Ma

r-12

Ju

n-1

2

Se

p-1

2

1.0

1.5

2.0

2.5

3.0

3.5

Dec-0

8

Ma

r-09

Ju

n-0

9

Se

p-0

9

Dec-0

9

Ma

r-10

Ju

n-1

0

Se

p-1

0

Dec-1

0

Ma

r-11

Ju

n-1

1

Se

p-1

1

Dec-1

1

Ma

r-12

Ju

n-1

2

Se

p-1

2

5

10

15

20

Dec-0

8

Ma

r-09

Ju

n-0

9

Se

p-0

9

Dec-0

9

Ma

r-10

Ju

n-1

0

Se

p-1

0

Dec-1

0

Ma

r-11

Ju

n-1

1

Se

p-1

1

Dec-1

1

Ma

r-12

Ju

n-1

2

Se

p-1

2

0.5

1.0

1.5

2.0

2.5

Dec-0

8

Ma

r-09

Ju

n-0

9

Se

p-0

9

Dec-0

9

Ma

r-10

Ju

n-1

0

Se

p-1

0

Dec-1

0

Ma

r-11

Ju

n-1

1

Se

p-1

1

Dec-1

1

Ma

r-12

Ju

n-1

2

Se

p-1

2

5

10

15

20

Dec-0

8

Ma

r-09

Ju

n-0

9

Se

p-0

9

Dec-0

9

Ma

r-10

Ju

n-1

0

Se

p-1

0

Dec-1

0

Ma

r-11

Ju

n-1

1

Se

p-1

1

Dec-1

1

Ma

r-12

Ju

n-1

2

Se

p-1

2

Regional Market Focus

4 December 2012

11 of 17

Source: Bloomberg

World Index

JCI 0.62% 4,302.44

HSI -1.19% 21,767.85

KLCI -0.22% 1,607.35

NIKKEI 0.13% 9,458.18

KOSPI 0.37% 1,940.02

SET 0.67% 1,332.92

SHCOMP -1.03% 1,959.77

SENSEX -0.18% 19,305.32

ASX 0.57% 4,531.51

FTSE 100 0.08% 5,871.24

DOW -0.46% 12,965.60

S&P 500 -0.47% 1,409.46

NASDAQ -0.27% 3,002.20 COLOMBO -0.25% 5,337.71

STI -0.14% 3,065.74

Regional Market Focus

4 December 2012

12 of 17

Date Statistic For Survey Prior Date Statistic For Survey Prior

12/4/2012 Total Vehicle Sales Nov 14.80M 14.22M 12/4/2012 Electronics Sector Index Nov 48.5 47.5

12/4/2012 Domestic Vehicle Sales Nov 11.50M 11.10M 12/4/2012 Purchasing Managers Index Nov 48.9 48.3

12/4/2012 ISM New York Nov -- 45.9 12/5/2012 Automobile COE Open Bid Cat A 5-Dec -- 77291

12/5/2012 MBA Mortgage Applications 30-Nov -- -0.90% 12/5/2012 Automobile COE Open Bid Cat B 5-Dec -- 93004

12/5/2012 ADP Employment Change Nov 125K 158K 12/5/2012 Automobile COE Open Bid Cat E 5-Dec -- 93990

12/5/2012 Nonfarm Productivity 3Q F 2.70% 1.90% 12/7/2012 Foreign Reserves Nov -- $254.22B

12/5/2012 Unit Labor Costs 3Q F -0.90% -0.10% 12/11/2012 Singapore Manpow er Survey 1Q -- 19%

12/5/2012 Factory Orders Oct 0.00% 4.80% 12-17 DEC Retail Sales (YoY) Oct -- 2.50%

12/5/2012 ISM Non-Manf. Composite Nov 53.5 54.2 12-17 DEC Retail Sales (MoM) sa Oct -- -0.50%

12/6/2012 Challenger Job Cuts YoY Nov -- 11.60% 12/14/2012 Unemployment Rate (sa) 3Q F -- 1.90%

12/6/2012 RBC Consumer Outlook Index Dec -- 48.9 12/14/2012 Retail Sales Ex Auto (YoY) Oct -- 3.90%

12/6/2012 Initial Jobless Claims 1-Dec 380K 393K 12/17/2012 Electronic Exports (YoY) Nov -- -0.80%

12/6/2012 Continuing Claims 24-Nov 3275K 3287K 12/17/2012 Non-oil Domestic Exports (YoY) Nov -- 7.90%

12/6/2012 Bloomberg Consumer Comfort 2-Dec -- -33 12/17/2012 Non-oil Domestic Exp SA (MoM) Nov -- -1.20%

12/7/2012 Household Change in Net Worth 3Q -- -$322B 12/19/2012 Automobile COE Open Bid Cat A 19-Dec -- --

Date Statistic For Survey Prior Date Statistic For Survey Prior

12/4/2012 Consumer Confidence Nov -- 77.8 12/5/2012 Purchasing Managers Index Nov -- 50.5

12/4/2012 Consumer Confidence Economic Nov -- 68.1 12/7/2012 Foreign Currency Reserves Nov -- $301.7B

12/7/2012 Foreign Reserves 30-Nov -- $181.5B 12/11/2012 Hong Kong Manpow er Survey 1Q -- 12%

12/7/2012 Forw ard Contracts 30-Nov -- $25.1B 12/13/2012 Industrial Production (YoY) 3Q -- -2.90%

12/14/2012 Foreign Reserves 7-Dec -- -- 12/13/2012 Producer Price (YoY) 3Q -- -0.70%

12/14/2012 Forw ard Contracts 7-Dec -- -- 12/18/2012 Unemployment Rate SA Nov -- 3.40%

17-19 DEC Total Car Sales Nov -- 142839 12/19/2012 Composite Interest Rate Nov -- 0.36%

12/21/2012 Foreign Reserves 14-Dec -- -- 12/20/2012 CPI - Composite Index (YoY) Nov -- 3.80%

12/21/2012 Forw ard Contracts 14-Dec -- -- 12/21/2012 Bal of Paymts - Current A/C 3Q -- -$9.35B

24-27 DEC Customs Exports (YoY) Nov -- 15.57% 12/21/2012 Bal of Paymts - Overall 3Q -- -$7.11B

24-27 DEC Customs Imports (YoY) Nov -- 21.61% 12/27/2012 Exports YoY% Nov -- -2.80%

24-27 DEC Customs Trade Balance Nov -- -$2470M 12/27/2012 Imports YoY% Nov -- 3.30%

12/28/2012 Foreign Reserves 21-Dec -- -- 12/27/2012 Trade Balance Nov -- -42.7B

12/28/2012 Forw ard Contracts 21-Dec -- -- 12/31/2012 Money Supply M1 - in HK$ (YoY) Nov -- --

12/28/2012 Total Exports YOY% Nov -- 14.40% 12/31/2012 Money Supply M2 - in HK$ (YoY) Nov -- --

US Singapore

Economic Announcement

Thailand Hong Kong

Source: Bloomberg

Source: BloombergSource: Bloomberg

Source: Bloomberg

Regional Market Focus

4 December 2012

13 of 17

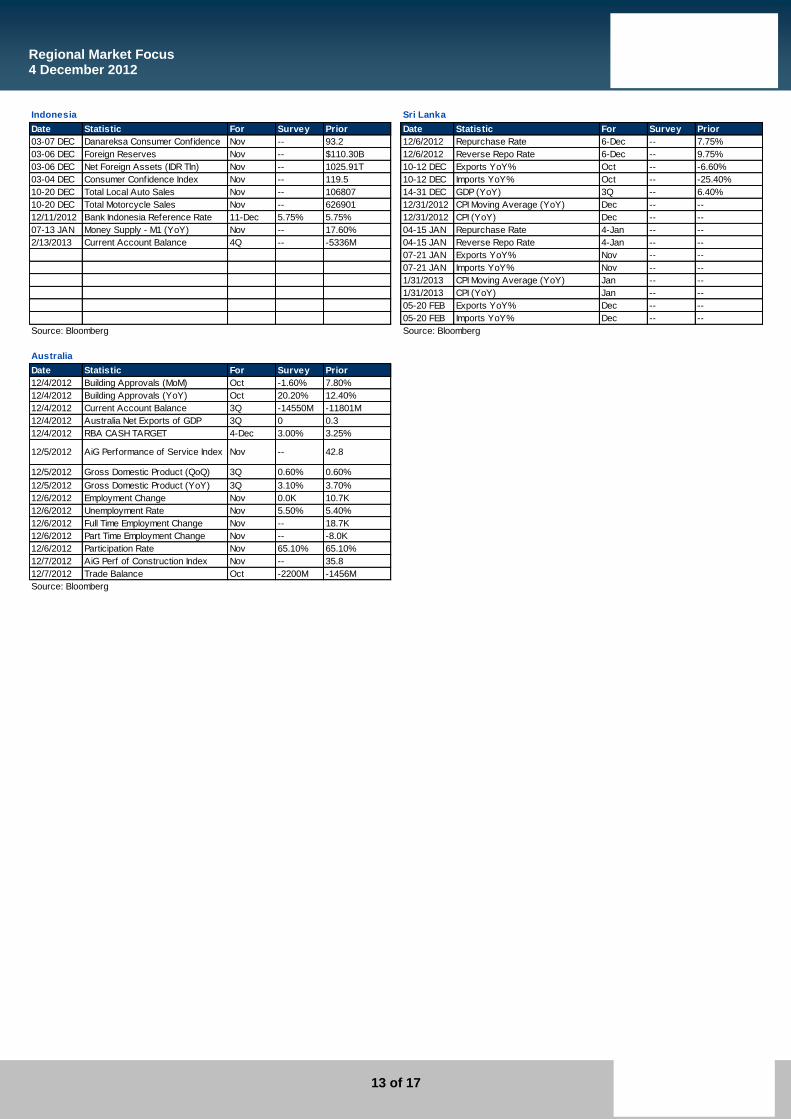

Date Statistic For Survey Prior Date Statistic For Survey Prior

03-07 DEC Danareksa Consumer Confidence Nov -- 93.2 12/6/2012 Repurchase Rate 6-Dec -- 7.75%

03-06 DEC Foreign Reserves Nov -- $110.30B 12/6/2012 Reverse Repo Rate 6-Dec -- 9.75%

03-06 DEC Net Foreign Assets (IDR Tln) Nov -- 1025.91T 10-12 DEC Exports YoY% Oct -- -6.60%

03-04 DEC Consumer Confidence Index Nov -- 119.5 10-12 DEC Imports YoY% Oct -- -25.40%

10-20 DEC Total Local Auto Sales Nov -- 106807 14-31 DEC GDP (YoY) 3Q -- 6.40%

10-20 DEC Total Motorcycle Sales Nov -- 626901 12/31/2012 CPI Moving Average (YoY) Dec -- --

12/11/2012 Bank Indonesia Reference Rate 11-Dec 5.75% 5.75% 12/31/2012 CPI (YoY) Dec -- --

07-13 JAN Money Supply - M1 (YoY) Nov -- 17.60% 04-15 JAN Repurchase Rate 4-Jan -- --

2/13/2013 Current Account Balance 4Q -- -5336M 04-15 JAN Reverse Repo Rate 4-Jan -- --

07-21 JAN Exports YoY% Nov -- --

07-21 JAN Imports YoY% Nov -- --

1/31/2013 CPI Moving Average (YoY) Jan -- --

1/31/2013 CPI (YoY) Jan -- --

05-20 FEB Exports YoY% Dec -- --

05-20 FEB Imports YoY% Dec -- --

Date Statistic For Survey Prior

12/4/2012 Building Approvals (MoM) Oct -1.60% 7.80%

12/4/2012 Building Approvals (YoY) Oct 20.20% 12.40%

12/4/2012 Current Account Balance 3Q -14550M -11801M

12/4/2012 Australia Net Exports of GDP 3Q 0 0.3

12/4/2012 RBA CASH TARGET 4-Dec 3.00% 3.25%

12/5/2012 AiG Performance of Service Index Nov -- 42.8

12/5/2012 Gross Domestic Product (QoQ) 3Q 0.60% 0.60%

12/5/2012 Gross Domestic Product (YoY) 3Q 3.10% 3.70%

12/6/2012 Employment Change Nov 0.0K 10.7K

12/6/2012 Unemployment Rate Nov 5.50% 5.40%

12/6/2012 Full Time Employment Change Nov -- 18.7K

12/6/2012 Part Time Employment Change Nov -- -8.0K

12/6/2012 Participation Rate Nov 65.10% 65.10%

12/7/2012 AiG Perf of Construction Index Nov -- 35.8

12/7/2012 Trade Balance Oct -2200M -1456M

Source: Bloomberg

Source: Bloomberg

Indonesia

Australia

Sri Lanka

Source: Bloomberg

PHILLIP RESEARCH STOCK SELECTION SYSTEMS

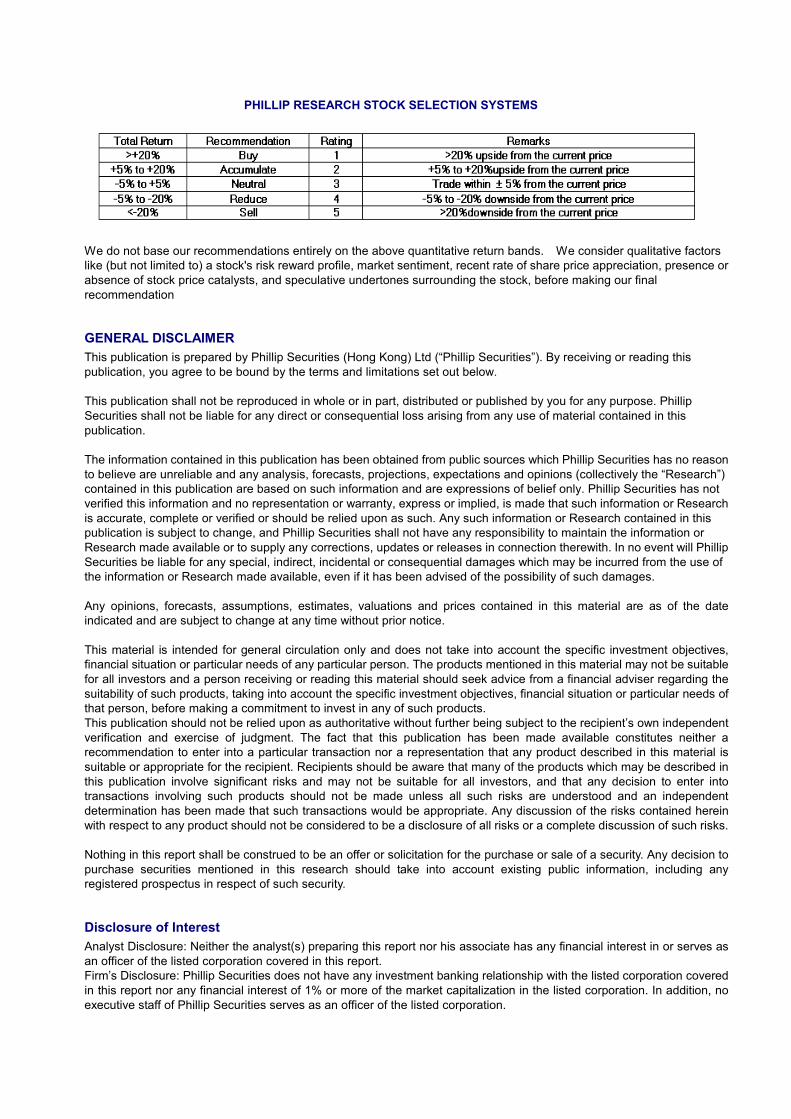

BUY >15% upside from the current price

HOLD Trade within ± 15% from the current price

SELL >15% downside from the current price

We do not base our recommendations entirely on the above quantitative return bands. We consider qualitative factors

like (but not limited to) a stock's risk reward profile, market sentiment, recent rate of share price appreciation, presence or

absence of stock price catalysts, and speculative undertones surrounding the stock, before making our final

recommendation

GENERAL DISCLAIMER

This publication is prepared by Phillip Securities (Hong Kong) Ltd (“Phillip Securities”). By receiving or reading this

publication, you agree to be bound by the terms and limitations set out below.

This publication shall not be reproduced in whole or in part, distributed or published by you for any purpose. Phillip

Securities shall not be liable for any direct or consequential loss arising from any use of material contained in this

publication.

The information contained in this publication has been obtained from public sources which Phillip Securities has no reason

to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”)

contained in this publication are based on such information and are expressions of belief only. Phillip Securities has not

verified this information and no representation or warranty, express or implied, is made that such information or Research

is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in this

publication is subject to change, and Phillip Securities shall not have any responsibility to maintain the information or

Research made available or to supply any corrections, updates or releases in connection therewith. In no event will Phillip

Securities be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of

the information or Research made available, even if it has been advised of the possibility of such damages.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this material are as of the date

indicated and are subject to change at any time without prior notice.

This material is intended for general circulation only and does not take into account the specific investment objectives,

financial situation or particular needs of any particular person. The products mentioned in this material may not be suitable

for all investors and a person receiving or reading this material should seek advice from a financial adviser regarding the

suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of

that person, before making a commitment to invest in any of such products.

This publication should not be relied upon as authoritative without further being subject to the recipient’s own independent

verification and exercise of judgment. The fact that this publication has been made available constitutes neither a

recommendation to enter into a particular transaction nor a representation that any product described in this material is

suitable or appropriate for the recipient. Recipients should be aware that many of the products which may be described in

this publication involve significant risks and may not be suitable for all investors, and that any decision to enter into

transactions involving such products should not be made unless all such risks are understood and an independent

determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein

with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of a security. Any decision to

purchase securities mentioned in this research should take into account existing public information, including any

registered prospectus in respect of such security.

Disclosure of Interest

Analyst Disclosure: Neither the analyst(s) preparing this report nor his associate has any financial interest in or serves as

an officer of the listed corporation covered in this report.

Firm’s Disclosure: Phillip Securities does not have any investment banking relationship with the listed corporation covered

in this report nor any financial interest of 1% or more of the market capitalization in the listed corporation. In addition, no

executive staff of Phillip Securities serves as an officer of the listed corporation.

Phillip Securities (HK)Phillip Securities (HK)Phillip Securities (HK)Phillip Securities (HK) Ltd Ltd Ltd Ltd

2

Availability

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or

entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the

applicable law or regulation or which would subject Phillip Securities to any registration or licensing or other requirement,

or penalty for contravention of such requirements within such jurisdiction.

© 2011 Phillip Securities (Hong Kong) Limited

Phillip Capital – Regional Member Companies

SINGAPORE

Phillip Securities Pte Ltd

Raffles City Tower 250, North Bridge Road #06-00

Singapore 179101 Tel : (65) 6533 6001 Fax : (65) 6535 6631

Website : www.poems.com.sg

MALAYSIA

Phillip Capital Management Sdn Bhd

B-2-6 Megan Avenue II 12 Jln Yap Kwan Seng 50450 Kuala Lumpur Tel : (603) 2166 8099 Fax : (603) 2166 5099

Website : www.poems.com.my

HONG KONG

Phillip Securities (HK) Ltd

11-12/F United Centre 95 Queensway, Hong Kong

Tel : (852) 2277 6600 Fax : (852) 2868 5307

Website : www.poems.com.hk

THAILAND

Phillip Securities (Thailand) Public Co Ltd

15/F, Vorawat Building 849 Silom Road

Bangkok Thailand 10500 Tel : (622) 635 7100 Fax : (622) 635 1616

Website : www.poems.in.th

JAPAN

The Naruse Securities Co Ltd

4-2, Nihonbashi Kabutocho Chuo Ku, Tokyo Japan 103-0026

Tel : (81) 03-3666-2101 Fax : (81) 03-3664-0141

Website : www.naruse-sec.co.jp

UNITED KINGDOM King & Shaxson Ltd

6th Floor, Candlewick House

120 Cannon Street London EC4N 6AS

Tel : (44) 207 426 5950 Fax : (44) 207 626 1757

Website : www.kingandshaxson.com