Embed Size (px)

Citation preview

Tuesday , 12 May 2015

1 Refer to last page for important disclosures.

R e g i o n a l M o r n i n g N o t e s

PLEASE CLICK ON THE PAGE NUMBER TO MOVE TO THE RELEVANT PAGE.

REGIONAL Sector Plantation Page 2Apr 15: Substantial jump in palm oil inventory to 2.19m tonnes, above market expectations on strong palm oil imports and strong FFB yield recovery.

CHINA Sector Automobile Page 4April PV sales slow, dragged by sedans. Downgrade DFM from BUY to HOLD. Top pick is GWM.

Update Dongfeng Motor (489 HK/HOLD/HK$13.32/Target: HK$14.00) Page 6Ytd sales miss expectations. Downgrade to HOLD with target price cut from HK$15.00 to HK$14.00.

INDONESIA Sector

Retail Page 9MPPA and LPPF will benefit from their expansion into eastern Indonesia. Local retailers will continue to lead the market. Ban on alcoholic beverages will affect AMRT.

MALAYSIA Sector Plantation Page 111Q15 results preview: Expect weak results on low production and CPO prices.

Update Genting Malaysia (GENM MK/BUY/RM4.30/Target: RM4.76) Page 13Proposed stake sale of GENHK is mildly positive.

SINGAPORE Sector Aviation Support Service Page 16SATS likely to outperform, and we estimate a 25% rise in final dividend. Maintain UNDERWEIGHT.

Results First Resources (FR SP/BUY/S$1.81/Target: S$2.40) Page 181Q15: Net profit of US$28.9m (-48.9% qoq, -33.9% yoy) due to lower ASP and lower sales volume. Results are within expectation as 1Q is seasonally weaker.

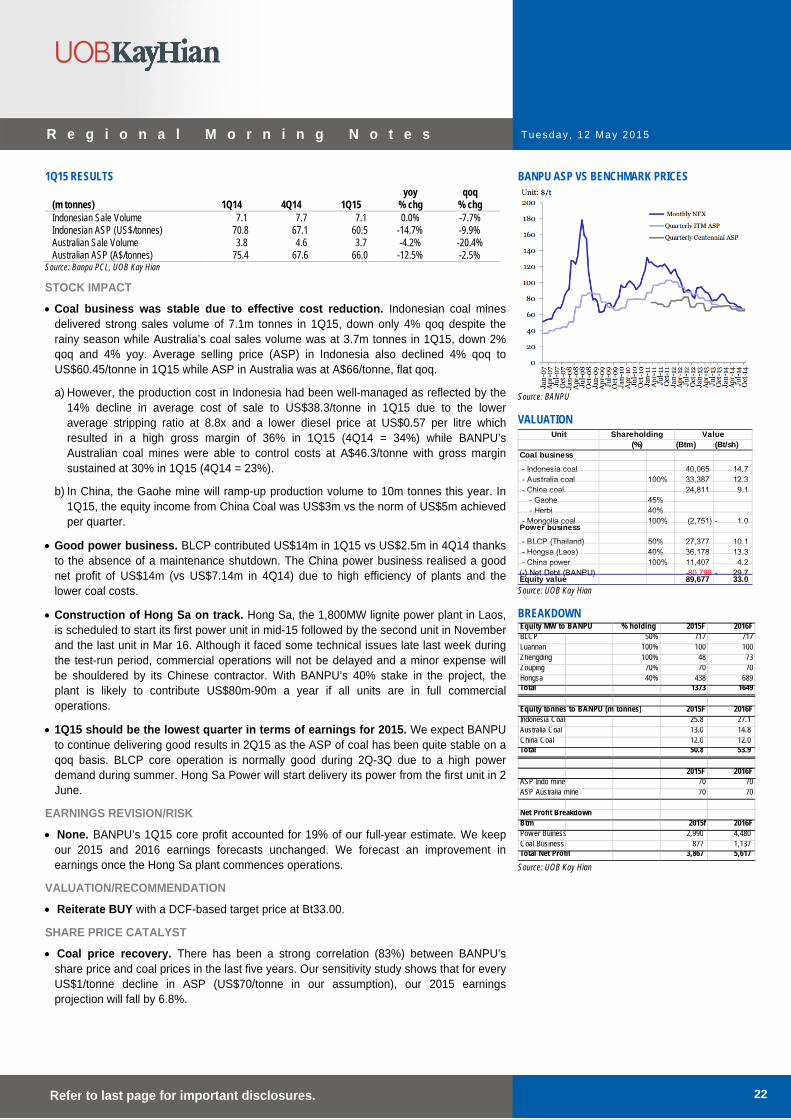

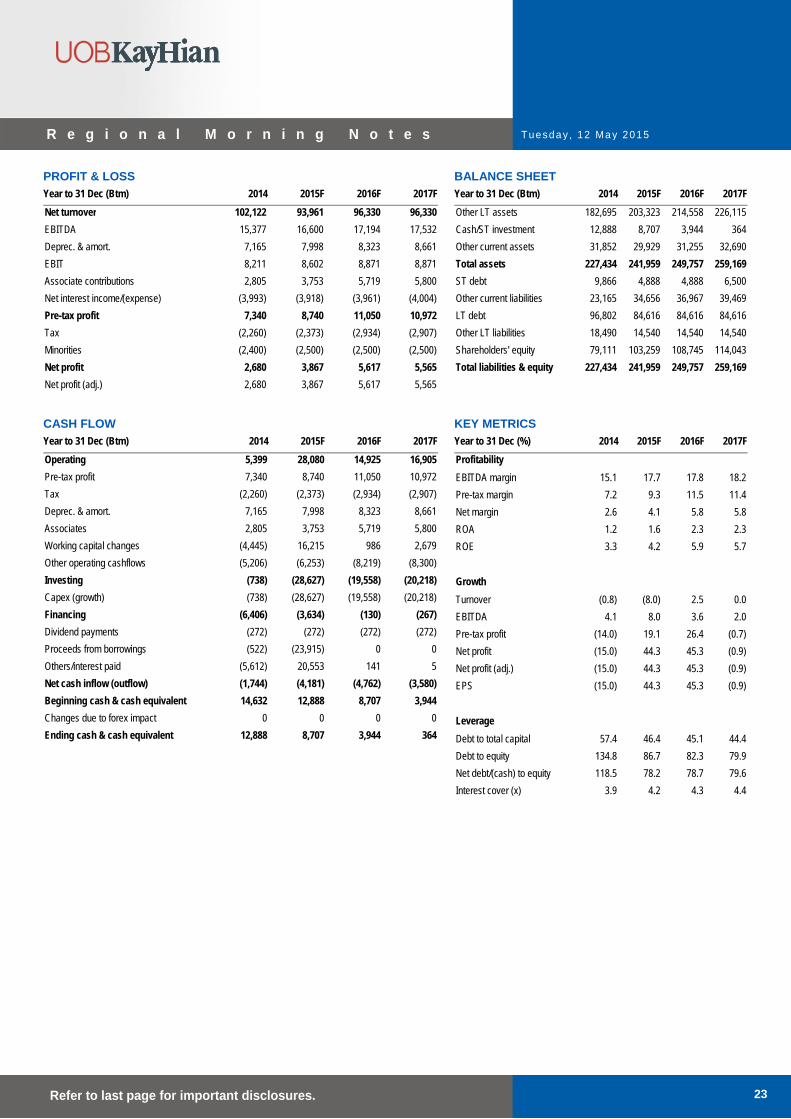

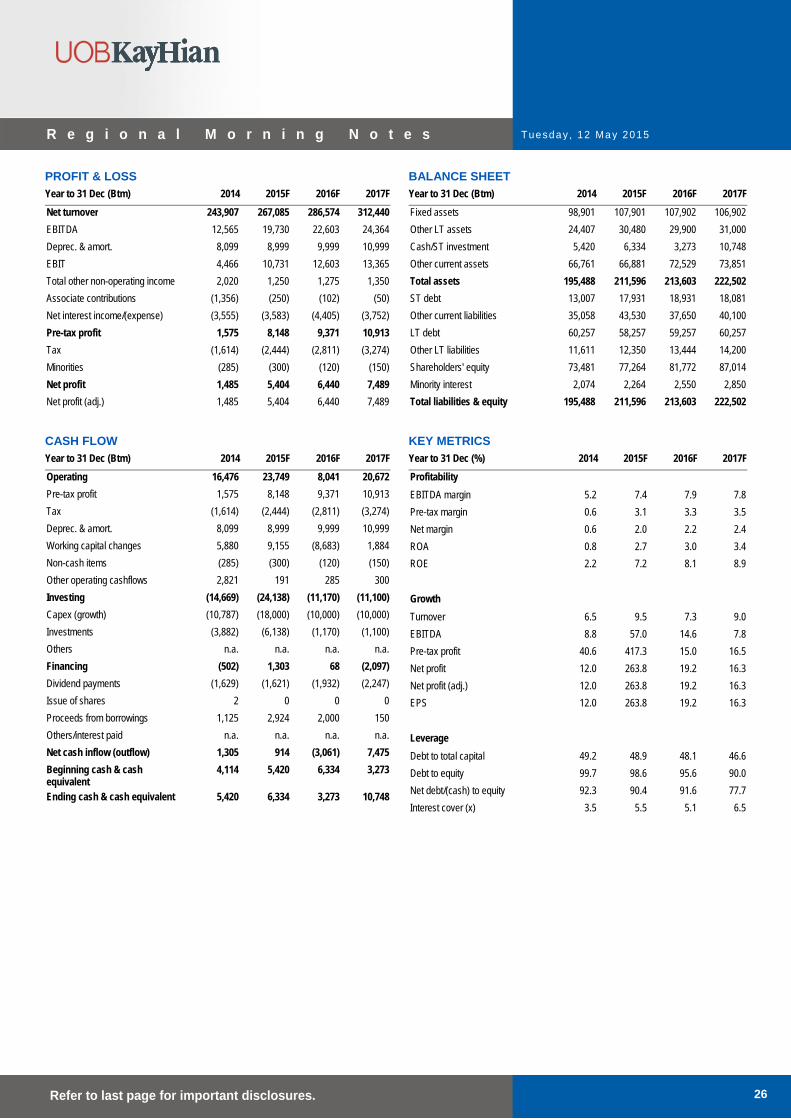

THAILAND Results Banpu (BANPU TB/BUY/Bt29.00/Target: Bt33.00) Page 211Q15: Results come with no surprises.

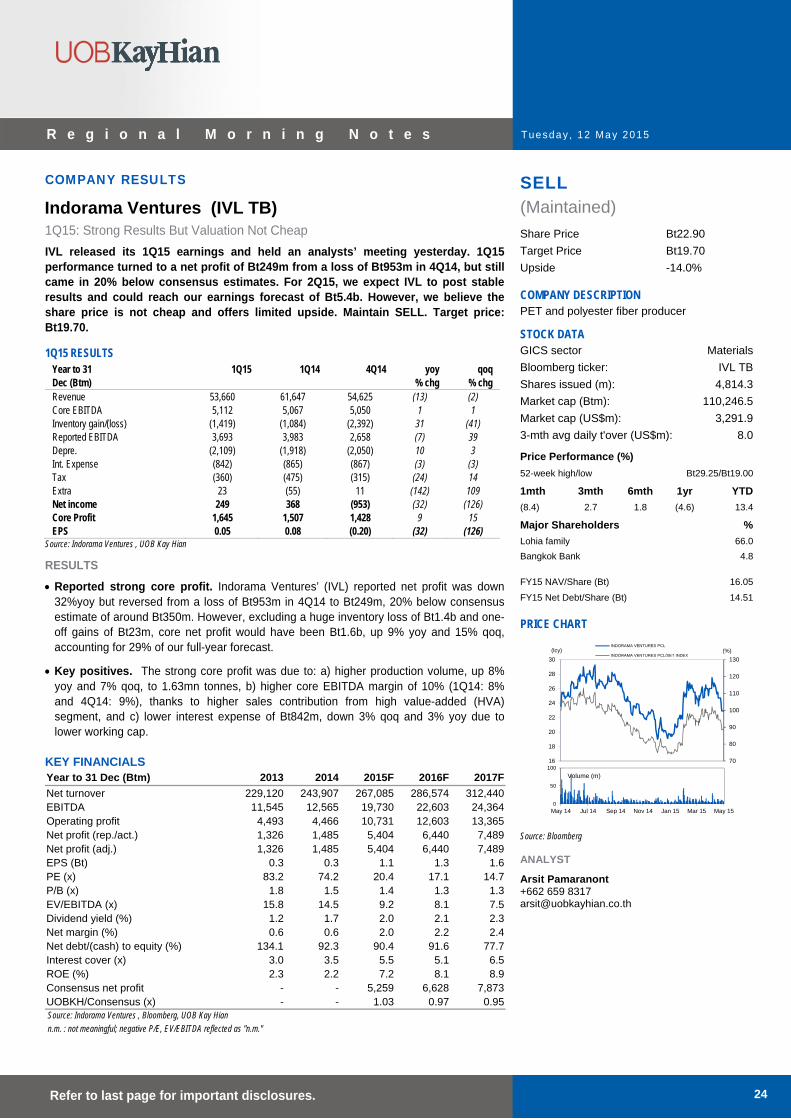

Indorama Ventures (IVL TB/SELL/Bt22.90/Target: Bt19.70) Page 241Q15: Strong results but valuation not cheap.

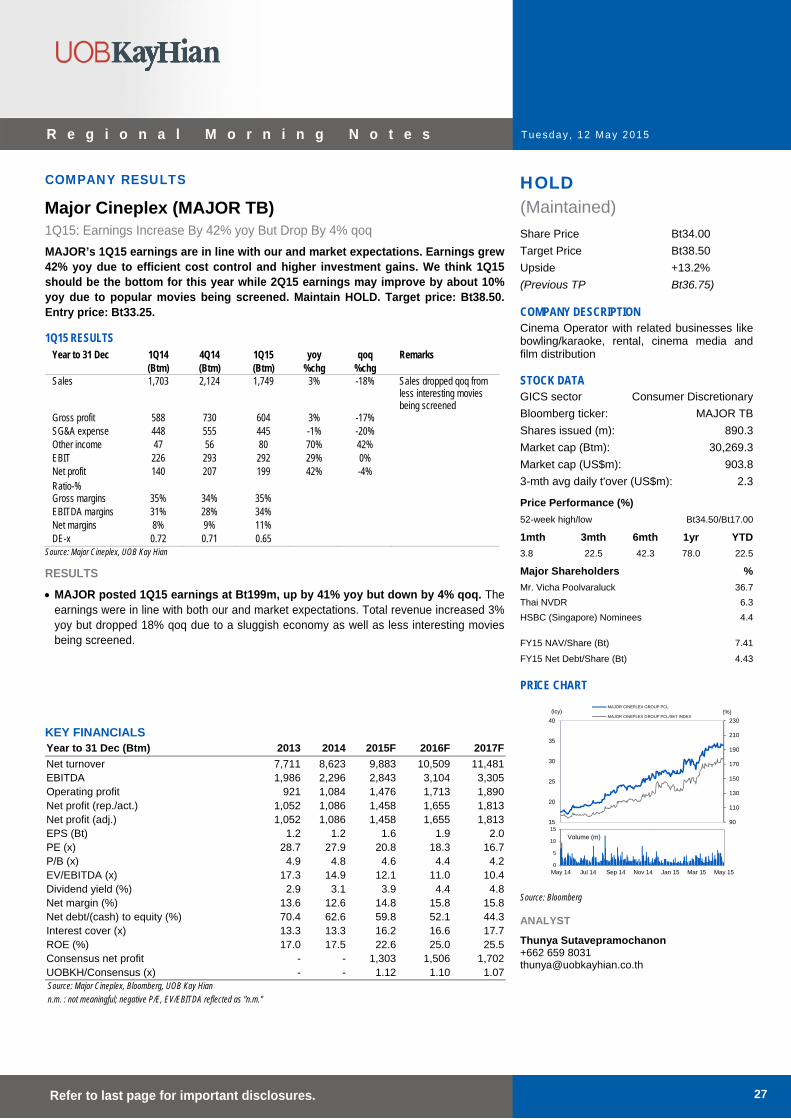

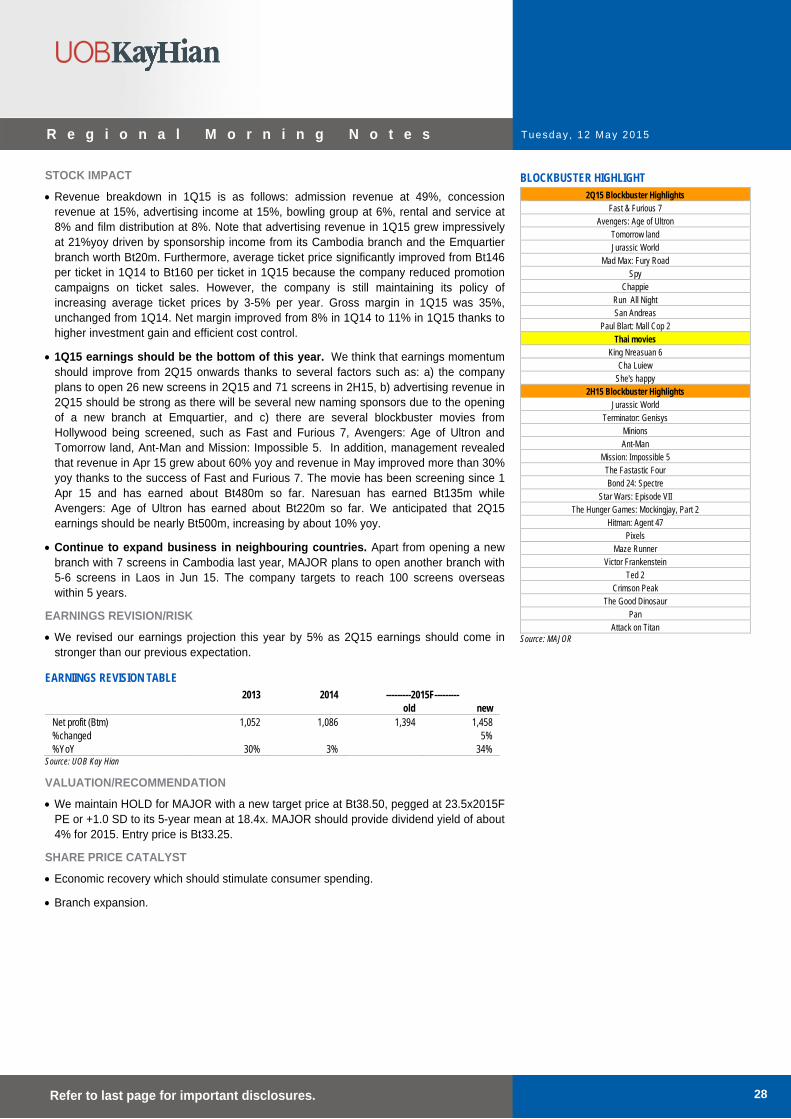

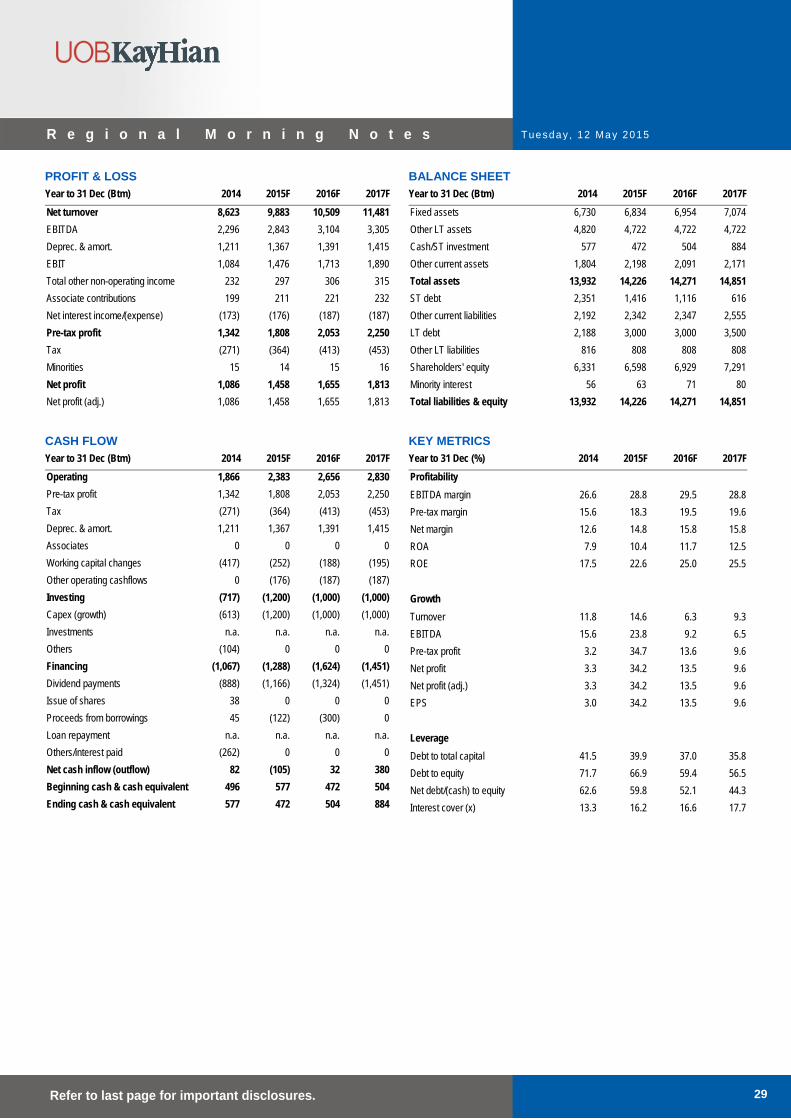

Major Cineplex (MAJOR TB/HOLD/Bt34.00/Target: Bt38.50) Page 271Q15: Earnings up 42% yoy, but down 4% qoq.

Thai Oil (TOP TB/SELL/Bt56.25/Target: Bt43.00) Page 301Q15: Results in line with expectations.

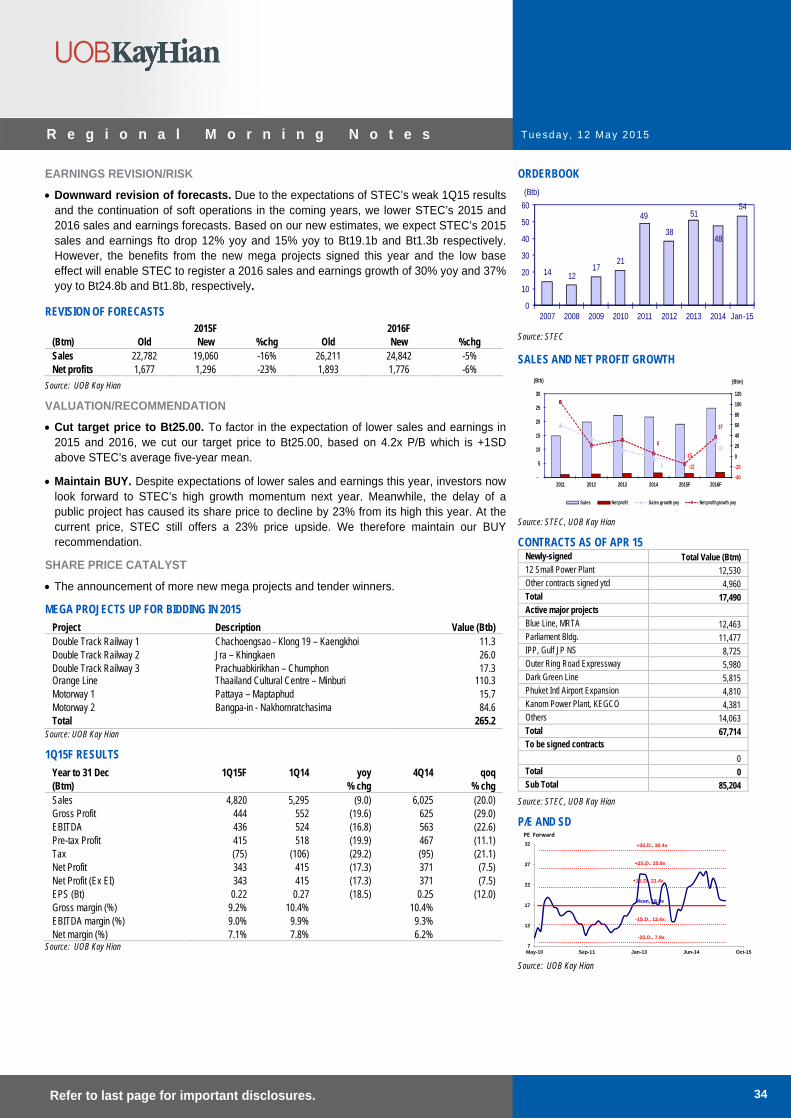

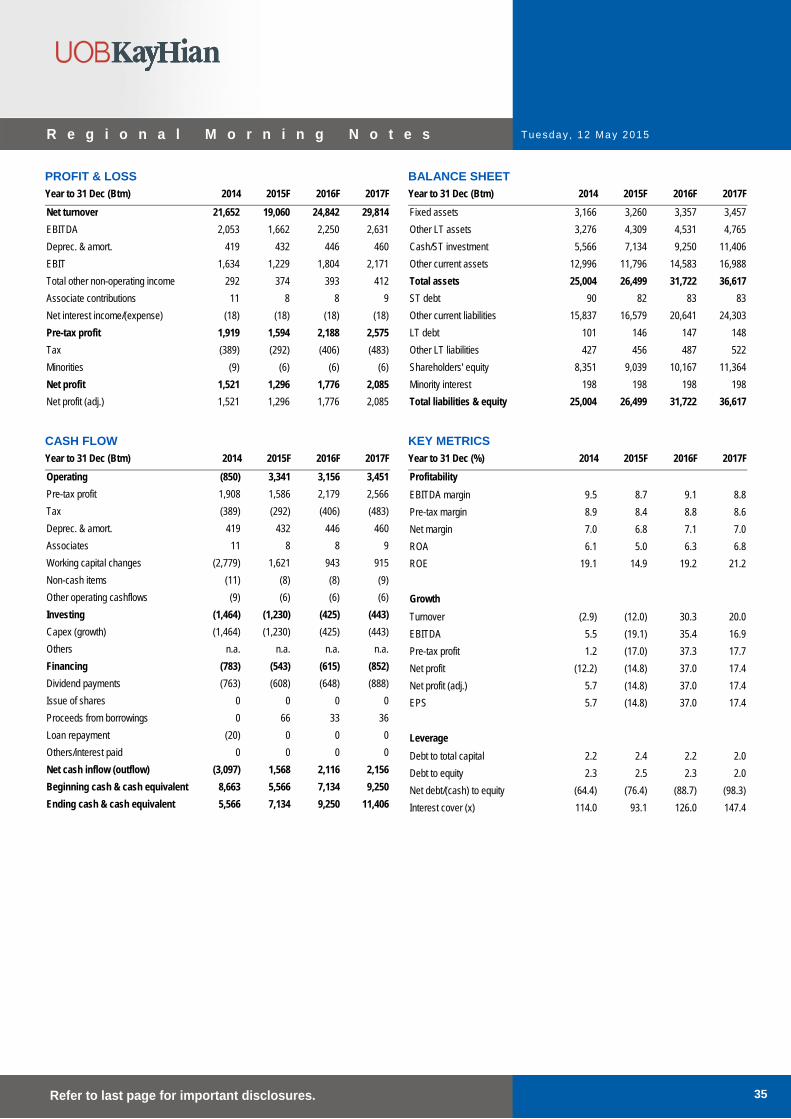

Update Sino-Thai Engineering & Construction (STEC TB/BUY/Bt20.30/Target: Bt25.00) Page 33Expect weak 1Q15 results.

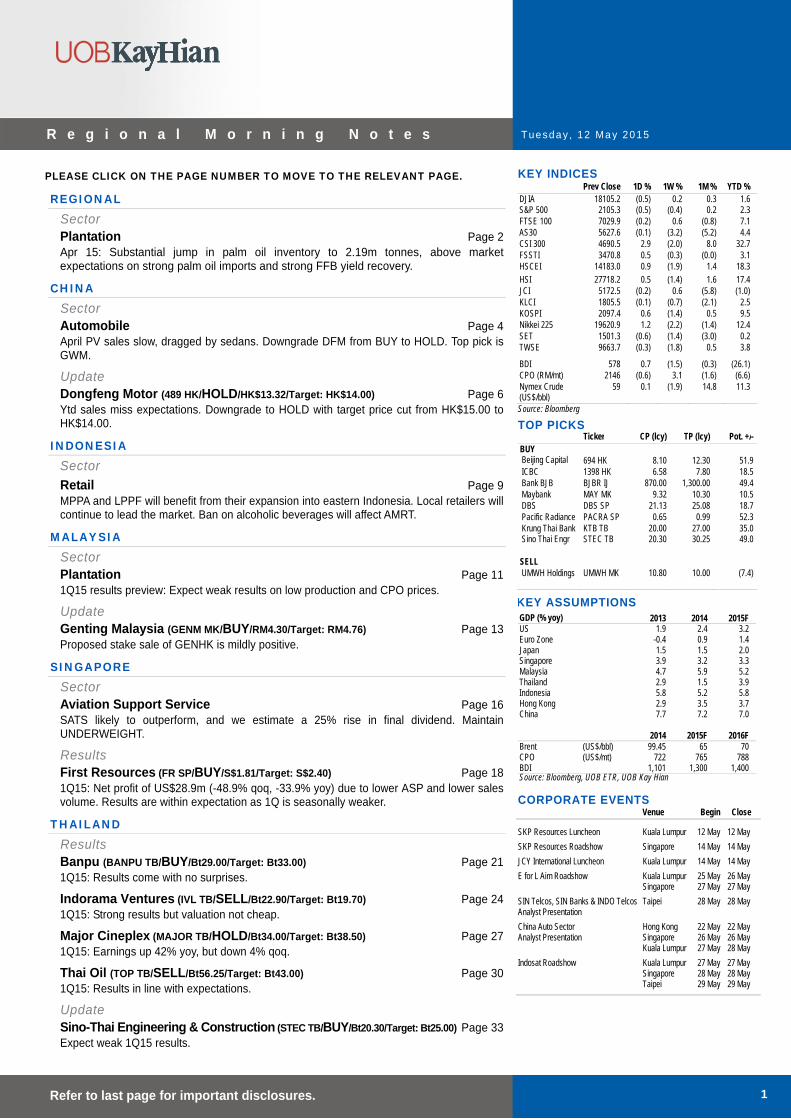

KEY INDICES Prev Close 1D % 1W % 1M % YTD % DJIA 18105.2 (0.5) 0.2 0.3 1.6 S&P 500 2105.3 (0.5) (0.4) 0.2 2.3 FTSE 100 7029.9 (0.2) 0.6 (0.8) 7.1 AS30 5627.6 (0.1) (3.2) (5.2) 4.4 CSI 300 4690.5 2.9 (2.0) 8.0 32.7 FSSTI 3470.8 0.5 (0.3) (0.0) 3.1 HSCEI 14183.0 0.9 (1.9) 1.4 18.3 HSI 27718.2 0.5 (1.4) 1.6 17.4 JCI 5172.5 (0.2) 0.6 (5.8) (1.0) KLCI 1805.5 (0.1) (0.7) (2.1) 2.5 KOSPI 2097.4 0.6 (1.4) 0.5 9.5 Nikkei 225 19620.9 1.2 (2.2) (1.4) 12.4 SET 1501.3 (0.6) (1.4) (3.0) 0.2 TWSE 9663.7 (0.3) (1.8) 0.5 3.8 BDI 578 0.7 (1.5) (0.3) (26.1) CPO (RM/mt) 2146 (0.6) 3.1 (1.6) (6.6) Nymex Crude (US$/bbl)

59 0.1 (1.9) 14.8 11.3

Source: Bloomberg

TOP PICKS Ticker CP (lcy) TP (lcy) Pot. +/-

( )BUY Beijing Capital 694 HK 8.10 12.30 51.9 ICBC 1398 HK 6.58 7.80 18.5 Bank BJB BJBR IJ 870.00 1,300.00 49.4 Maybank MAY MK 9.32 10.30 10.5 DBS DBS SP 21.13 25.08 18.7 Pacific Radiance PACRA SP 0.65 0.99 52.3 Krung Thai Bank KTB TB 20.00 27.00 35.0 Sino Thai Engr STEC TB 20.30 30.25 49.0

SELL UMWH Holdings UMWH MK 10.80 10.00 (7.4)

KEY ASSUMPTIONS GDP (% yoy) 2013 2014 2015F US 1.9 2.4 3.2 Euro Zone -0.4 0.9 1.4 Japan 1.5 1.5 2.0 Singapore 3.9 3.2 3.3 Malaysia 4.7 5.9 5.2 Thailand 2.9 1.5 3.9 Indonesia 5.8 5.2 5.8 Hong Kong 2.9 3.5 3.7 China 7.7 7.2 7.0 2014 2015F 2016F Brent (US$/bbl) 99.45 65 70 CPO (US$/mt) 722 765 788 BDI 1,101 1,300 1,400 Source: Bloomberg, UOB ETR, UOB Kay Hian

CORPORATE EVENTS

Venue Begin Close

SKP Resources Luncheon Kuala Lumpur 12 May 12 May

SKP Resources Roadshow Singapore 14 May 14 May

JCY International Luncheon Kuala Lumpur 14 May 14 May

E for L Aim Roadshow Kuala Lumpur 25 May 26 May Singapore 27 May 27 May

SIN Telcos, SIN Banks & INDO Telcos Taipei 28 May 28 May Analyst Presentation

China Auto Sector Hong Kong 22 May 22 May Analyst Presentation Singapore 26 May 26 May Kuala Lumpur 27 May 28 May

Indosat Roadshow Kuala Lumpur 27 May 27 May Singapore 28 May 28 May Taipei 29 May 29 May

Tuesday , 12 May 2015

2 Refer to last page for important disclosures.

R e g i o n a l M o r n i n g N o t e s

SECTOR UPDATE

Plantation – Regional Jump In Inventory

MPOB reported a surge in palm oil inventory to 2.19m tonnes, above market expectation mainly due to strong palm oil imports and strong FFB yield recovery (above 5-year average). Slower exports for April were expected as some shipments were delayed to take advantage of the 0% export tax for May. The jump in inventory is unlikely to lead to price weakness as the market is expecting Indonesia to start B15 blending as the president has signed the new export levy. Maintain MARKET WEIGHT.

WHAT’S NEW

Inventory at 5-month high. MPOB reported palm oil inventory of 2.19m tonnes (+17.6% mom, +24.2% yoy), above market expectation of 2.09m tonnes. The sharp increase was mainly due to a jump in CPO production (+13.3% mom, +8.8% yoy) and increase in palm oil import (+44.8% mom, +39.8% yoy) while export stayed flat mom.

CPO production continued to pick up. Good weather and yield recovery has resulted in the strong growth in CPO production across Malaysia. Peninsular Malaysia reported double-digit yoy growth of 16.9% in CPO production growth, which came mainly from Johor, Negeri Sembilan and Kedah. However, for 4M15, it was still down 6.3% yoy due to the lagged impact from the dry weather in 1Q14. Going forward, we expect CPO production to continue picking up as we are entering the high production season.

Exports to grow in May 15. According to Intertek, exports of Malaysian palm oil products for 1-10 May rose 41.3% from the same period in April to 458,677 tonnes as shipments to India and Europe doubled. This was due to palm oil buyers taking advantage of the zero export tax in May 15 as compared with Apr 15 where there was 4.5% export tax rate imposed. Exports to India were down substantially by 70.6% mom in Apr 15 likely due to shipments being delayed to May 15.

ACTION

Maintain MARKET WEIGHT. CPO prices are likely to stay range-bound as the market is waiting for clearer demand outlook especially from Indonesia, ie the implementation of the new exports levy and clearer procedure of how biodiesel subsidy will be reimbursed to producers. However, in our view this is only a supportive measures to keep CPO price above RM2,000/tonne, and is not a strong enough catalyst to rerate the sector.

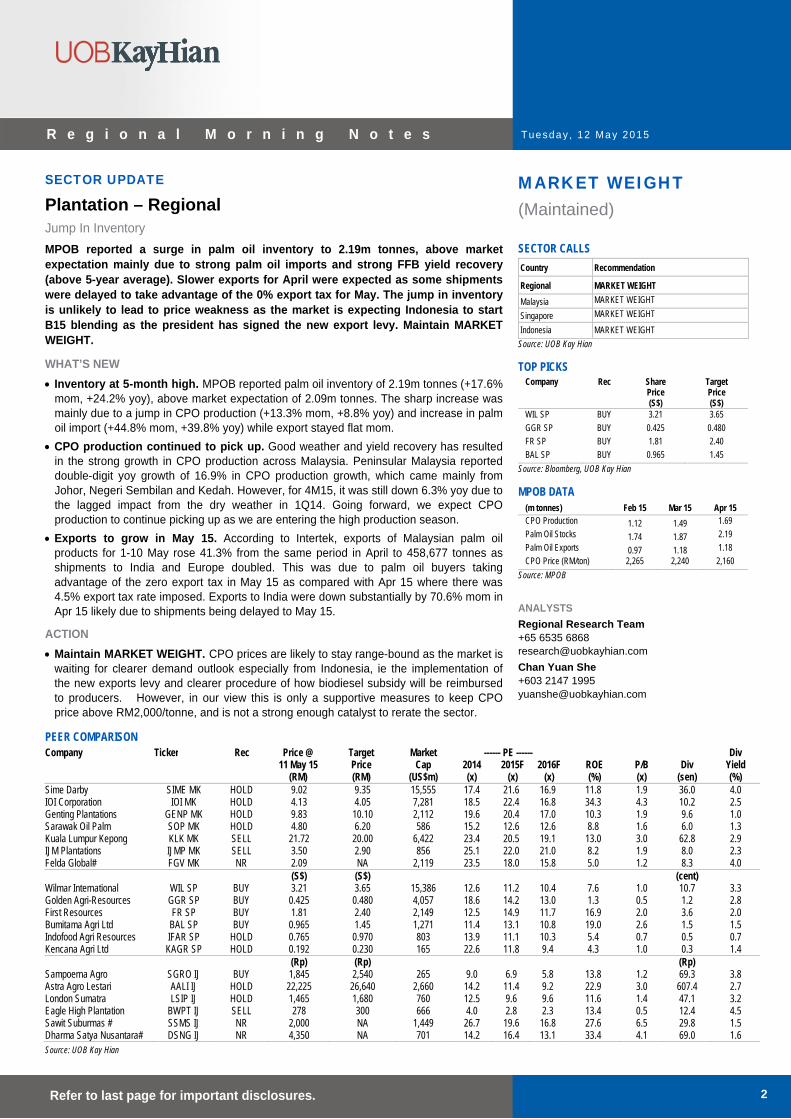

MARKET WEIGHT (Maintained) SECTOR CALLS

Country Recommendation

Regional MARKET WEIGHT

Malaysia MARKET WEIGHT

Singapore MARKET WEIGHT

Indonesia MARKET WEIGHT

Source: UOB Kay Hian TOP PICKS

Company Rec Share Price (S$)

Target Price (S$)

WIL SP BUY 3.21 3.65

GGR SP BUY 0.425 0.480

FR SP BUY 1.81 2.40

BAL SP BUY 0.965 1.45

Source: Bloomberg, UOB Kay Hian

MPOB DATA (m tonnes) Feb 15 Mar 15 Apr 15 CPO Production 1.12 1.49 1.69

Palm Oil Stocks 1.74 1.87 2.19

Palm Oil Exports 0.97 1.18 1.18

CPO Price (RM/ton) 2,265 2,240 2,160

Source: MPOB

ANALYSTS

Regional Research Team +65 6535 6868 [email protected]

Chan Yuan She +603 2147 1995 [email protected]

PEER COMPARISON Company Ticker Rec Price @ Target Market ------ PE ------ Div 11 May 15 Price Cap 2014 2015F 2016F ROE P/B Div Yield (RM) (RM) (US$m) (x) (x) (x) (%) (x) (sen) (%) Sime Darby SIME MK HOLD 9.02 9.35 15,555 17.4 21.6 16.9 11.8 1.9 36.0 4.0 IOI Corporation IOI MK HOLD 4.13 4.05 7,281 18.5 22.4 16.8 34.3 4.3 10.2 2.5 Genting Plantations GENP MK HOLD 9.83 10.10 2,112 19.6 20.4 17.0 10.3 1.9 9.6 1.0 Sarawak Oil Palm SOP MK HOLD 4.80 6.20 586 15.2 12.6 12.6 8.8 1.6 6.0 1.3 Kuala Lumpur Kepong KLK MK SELL 21.72 20.00 6,422 23.4 20.5 19.1 13.0 3.0 62.8 2.9 IJM Plantations IJMP MK SELL 3.50 2.90 856 25.1 22.0 21.0 8.2 1.9 8.0 2.3 Felda Global# FGV MK NR 2.09 NA 2,119 23.5 18.0 15.8 5.0 1.2 8.3 4.0 (S$) (S$) (cent) Wilmar International WIL SP BUY 3.21 3.65 15,386 12.6 11.2 10.4 7.6 1.0 10.7 3.3 Golden Agri-Resources GGR SP BUY 0.425 0.480 4,057 18.6 14.2 13.0 1.3 0.5 1.2 2.8 First Resources FR SP BUY 1.81 2.40 2,149 12.5 14.9 11.7 16.9 2.0 3.6 2.0 Bumitama Agri Ltd BAL SP BUY 0.965 1.45 1,271 11.4 13.1 10.8 19.0 2.6 1.5 1.5 Indofood Agri Resources IFAR SP HOLD 0.765 0.970 803 13.9 11.1 10.3 5.4 0.7 0.5 0.7 Kencana Agri Ltd KAGR SP HOLD 0.192 0.230 165 22.6 11.8 9.4 4.3 1.0 0.3 1.4 (Rp) (Rp) (Rp) Sampoerna Agro SGRO IJ BUY 1,845 2,540 265 9.0 6.9 5.8 13.8 1.2 69.3 3.8 Astra Agro Lestari AALI IJ HOLD 22,225 26,640 2,660 14.2 11.4 9.2 22.9 3.0 607.4 2.7 London Sumatra LSIP IJ HOLD 1,465 1,680 760 12.5 9.6 9.6 11.6 1.4 47.1 3.2 Eagle High Plantation BWPT IJ SELL 278 300 666 4.0 2.8 2.3 13.4 0.5 12.4 4.5 Sawit Suburmas # SSMS IJ NR 2,000 NA 1,449 26.7 19.6 16.8 27.6 6.5 29.8 1.5 Dharma Satya Nusantara# DSNG IJ NR 4,350 NA 701 14.2 16.4 13.1 33.4 4.1 69.0 1.6 Source: UOB Kay Hian

Tuesday , 12 May 2015

3 Refer to last page for important disclosures.

R e g i o n a l M o r n i n g N o t e s

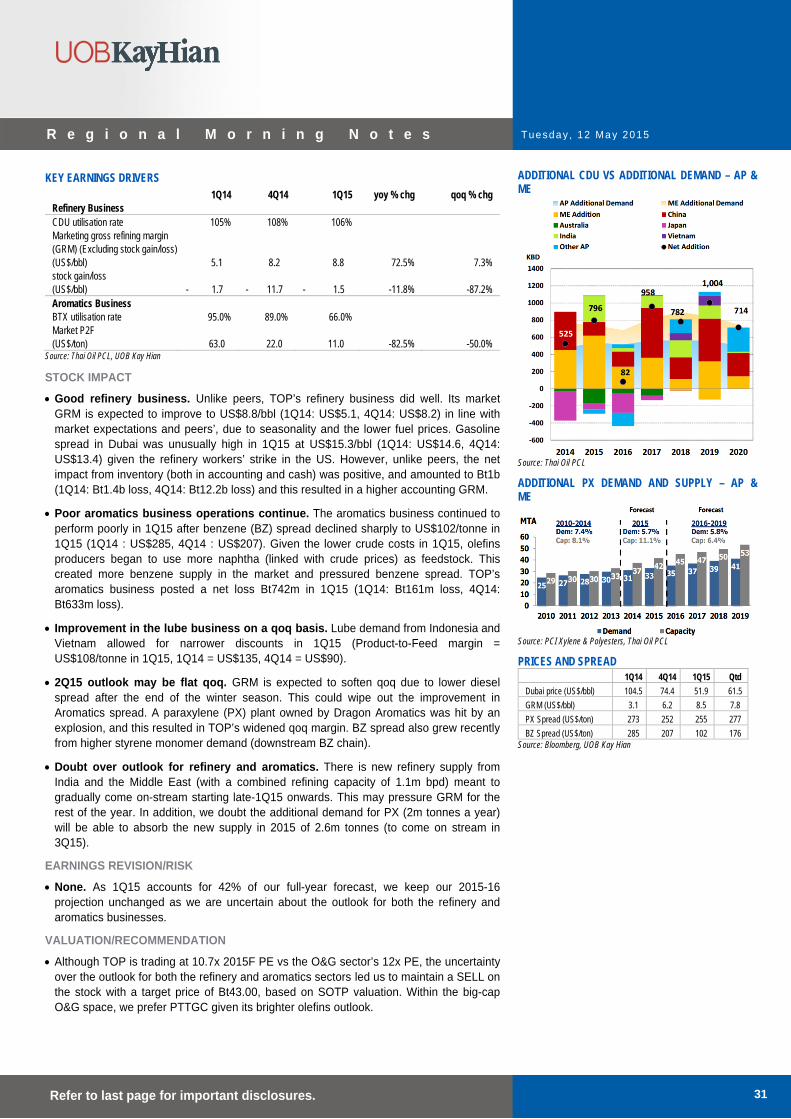

In the current market conditions, we prefer companies with exposure to Indonesia refinery and biodiesel as it allows them to take advantage of the new measures and also companies with higher production growth which can mitigate the weak CPO prices.

ESSENTIALS

CPO production continued to pick up. MPOB reported CPO production of 1.69m tonnes, up 13.3% mom and 8.8% yoy. This was in line with market expectation. The growth in production came mainly from Sabah (+17.3% mom, -3.9% yoy) followed by Sarawak (+15.4% mom, +8.4% yoy) and Peninsular Malaysia (+10.7% mom, +16.9% yoy). Peninsular Malaysia’s FFB yield has increased sharply to well above its 5-year range, likely due to good weather and recovery from the monsoon flood. However, CPO production for 4M15 was still down by 6.3% yoy with Sabah reporting a 13.8% yoy contraction due to weaker FFB yield in 3M15 as a result of the monsoon rain.

Exports stayed flat in Apr 15. Exports stood at 1.18m tonnes (-0.6% mom, -7.4% yoy). This was better than market expectation. Exports to China and EU have picked up by 97.9% and 15.6% mom. However, these were offset by the decline in exports to India (-70.6% mom, -45.7% yoy). For 4M15, exports were down 13.6% yoy on weak exports to China, EU and Pakistan.

SECTOR CATALYSTS

Crude oil prices. Return of non-mandated biodiesel demand if crude oil prices recover above US$80/bbl.

Possibility of El Nino. El Nino conditions will lead to severe drought in Southeast Asia. Dry conditions have already been observed in many parts of Malaysia and Indonesia since Feb 15, but it is still too early to deduce the impact on production. The situation must be monitored closely and if El Nino conditions occur, the sector’s production potential will deteriorate for 2016.

ASSUMPTION CHANGES

CPO price assumptions are currently under review. Our current earnings expectation are based on CPO price assumptions of RM2,525/tonne for 2015 and RM2,600/tonne for 2016. Ytd average CPO price is RM2,226/tonne (-17% yoy).

A 10% cut to our CPO price assumptions for both 2015 and 2016 will lead to an earnings decline of 11-23% for upstream players and 4-8% for integrated players.

RISKS

Backtracking of biodiesel mandates in Indonesia and Malaysia on lower crude oil prices.

Another year of bumper soybean crops from the US.

STRONG MOM GROWTH BUT 4M15 CPO PRODUCTION STILL DOWN YOY (‘000 tonnes) Mar 15 mom % chg yoy % chg 4M15 yoy % chg

Malaysia 1,693 13.3 8.8 5,471 (6.3) P. Msia 933 10.7 16.9 2,933 (2.1) Sabah 476 17.3 (3.9) 1,609 (13.8) Sarawak 285 15.4 8.4 929 (4.7)

Source: MPOB

EXPORTS TO CHINA CONTINUED TO PICK UP (‘000 tonnes) Mar 15 mom % chg yoy % chg 3M15 yoy % chg Total 1,175 (0.6) (7.4) 4,521 (13.6) China 263 97.9 4.0 676 (32.4) Pakistan 65 6.9 (2.6) 214 (22.9) EU 131 15.6 (2.8) 552 (20.5) India 87 (70.6) (45.7) 767 16.6 US 77 57.1 39.1 243 (8.8) Japan 42 33.6 (19.3) 159 (8.5) Others 511 2.6 (6.6) 1,909 (11.7)

Source: MPOB

STRONG RECOVERY IN APR 15

1.0

1.2

1.4

1.6

1.8

2.0

2.2

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2014 2015

2013 2012

(m tonnes) Malaysian Monthly CPO Production

Source: MPOB

HUGE JUMP IN INVENTORY

1.2

1.4

1.6

1.8

2.0

2.2

2.4

2.6

2.8

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2014 2015

2013 2012

(m tonnes) Malaysian Palm Oil Inventory

Source: MPOB

WEAK EXPORTS

0.8

1.0

1.2

1.4

1.6

1.8

2.0

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2014 2015

2013 2012

(m tonnes) Malaysian Monthly Palm Oil Exports

Source: MPOB FFB YIELD ABOVE ITS 5-YEAR RANGE

Peninsular Malaysia FFB Yield

1.00

1.20

1.40

1.60

1.80

2.00

2.20

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

(tonne/ha)

5-yrs Range2015 Monthly Yield5-yrs Average

Source: MPOB

Tuesday , 12 May 2015

4 Refer to last page for important disclosures.

R e g i o n a l M o r n i n g N o t e s

SECTOR UPDATE

Automobile - China Sales Growth All Coming From SUVs and MPVs

April PV sales came in lower than expected with retail sales up 6% yoy. The disappointment came from sedan sales, which fell 7% yoy in April. SUVs and MPVs remained the primary sales growth drivers with retail sales up 56% yoy and 20% yoy respectively. All carmakers saw a slowdown in sales momentum in April except for GWM. Maintain MARKET WEIGHT. Top pick: GWM (2333 HK/BUY/Target: HK$69.00).

WHAT’S NEW

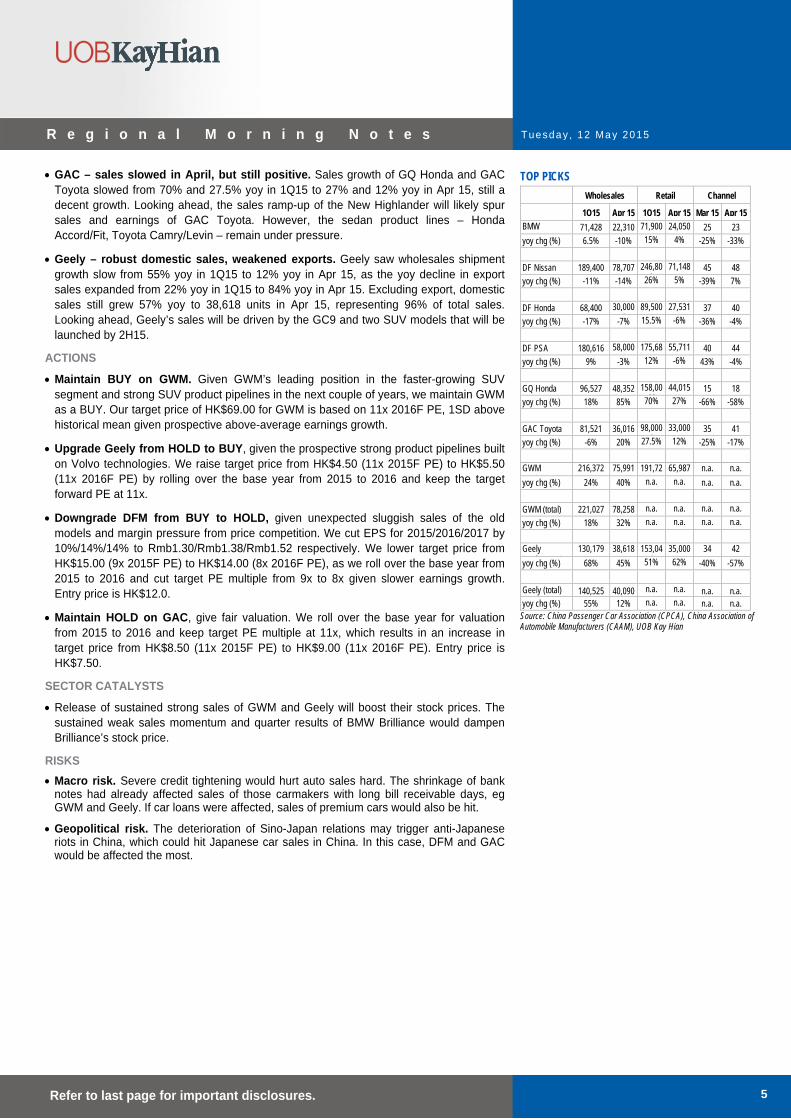

PV sales growth slowed to 6% yoy in April, all growth coming from SUV and MPV. China’s April passenger vehicle (PV) sales came in lower- than expected with wholesales shipment up 4.4% yoy and retail sales up 6.2% yoy to 1.67m units and 1.61m units respectively, according to China Passenger Car Association (CPCA). For 1Q15, the wholesales shipment and retail sales of PVs grew 7.7% yoy and 12.3% yoy to 6.99m units and 6.88m units respectively. The disappointment in April came from sedans whose retail sales dropped 6.6% yoy. All the growth in PV sales came from SUVs and MPVs, of which retail sales surged by 56% yoy and 20% yoy.

All OEMs saw sales slowdown in April, except for GWM. Driven by the burgeoning SUV market, GWM’s sales growth accelerated from 18% yoy in 1Q15 to 40% in Apr 15. However, given the slowdown of the overall sedan market and price cuts by major players (eg Volkswagen and Ford), BMW Brilliance, the three JVs of DFM (DF Nissan, DF Honda and DF PSA), the two JVs of GAC (GQ Honda and GAC Toyota) and Geely all saw a slowdown in retail sales growth in April (see table overleaf).

BMW Brilliance – sales reined in by old product portfolio. BMW Brilliance saw wholesales shipment decline by 10% yoy to 22,310 units in Apr 15, compared with a 6% yoy drop in Mar 15. 4M15 wholesales shipment was only up merely 2% yoy to 93,738 units. The decline in wholesale sales in Mar-Apr 15 was due to dealers cutting back on inventory take-up during the period and asking for bigger rebates given deepened product discounting (>15% now vs 10% a year ago). As such, BMW Brilliance’s 1Q15 net profit fell >40% yoy. Given old product portfolio (no new models before the launch of 2-series by end-15) and intense competition from Mercedes-Benz, BMW has recently agreed to cut sales target for 2Q15. Sales should remain lukewarm throughout the year.

DFM coming under pressure. To our surprise, April sales of DFM weakened across the board with yoy retail sales growth of DF Nissan/DF Honda/DF PSA tumbling to 5%/-6%/-6% in Apr 15 from 26%/15.5%/12% respectively in 1Q15 while channel inventory rebounded mom. This can be attributed to the slowdown in the overall sedan market and price cuts by major players as aforementioned. The launches of the new models (eg DF AX7, DF Honda CR-X, DF Citroen C3-XR, etc.) were more than offset by sales drop of the old models.

MARKET WEIGHT (Maintained) WHOLESALES SHIPMENT OF PVS

Sedan MPV SUV Mini-bus Total

Apr 15 942 165 469 98 1,675

Mar 15 1,073 198 482 116 1,870

Apr 14 1,044 131 310 123 1,609

mom % chg -12.2% -16.6% -2.7% -15.8% -10.4%

yoy % chg -9.7% 26.0% 50.9% -20.4% 4.4%

4M15 4,070 746 1,777 401 6,994

4M14 4,194 613 1,179 510 6,495

yoy % chg -3.0% 21.8% 50.8% -21.5% 7.7%

Source: China Passenger Car Association (CPCA)

RETAIL SALES OF PVS

Sedan MPV SUV Mini-bus Total

Apr 15 913 162 439 96 1,610

Mar 15 1,006 199 462 114 1,782

Apr 14 978 135 281 122 1,516

mom % chg -9.3% -18.9% -5.0% -15.8% -9.7%

yoy % chg -6.6% 19.6% 56.3% -21.1% 6.2%

4M15 3,982 741 1,767 395 6,884

4M14 3,929 611 1,083 507 6,130

yoy % chg 1.4% 21.2% 63.1% -22.2% 12.3%

Source: China Passenger Car Association (CPCA)

ANALYST

Ken Lee +852 2236 6760 [email protected]

PEER COMPARISON

Company Ticker Market Rec Price @ Target ------------ PE ------------ EPS

CAGR PEG ROE Net Gearing Cap 11 May 15 Price 2014 2015F 2016F 2015F 2015F 2015F 2014 (US$m) (HK$) (HK$) (x) (x) (x) (%) (x) (%) (%)

Brilliance 1114 HK 9,011 SELL 13.90 12.00 10.4 10.5 9.0 18.6 0.6 29.4 11.9 BYD 1211 HK 104,273 SELL 49.05 19.00 219.8 96.5 85.4 13.5 7.1 7.8 90.2 Dongfeng Motor 489 HK 14,803 HOLD 13.32 14.00 8.6 8.2 7.7 7.9 1.0 16.5 (17.1) Geely 175 HK 4,598 BUY 4.05 5.50 20.0 9.8 8.3 15.5 0.6 13.4 (24.9) Great Wall Motor 2333 HK 109,889 BUY 54.30 69.0 16.4 11.6 8.9 22.5 0.5 30.0 2.3 Guangzhou Auto 2238 HK 55,788 HOLD 8.20 9.00 13.3 13.4 11.0 16.6 0.8 10.9 (7.3) Sector 13.7 10.7 9.0 16.2 0.7 20.1 (7.0)

Source: Bloomberg, UOB Kay Hian

Tuesday , 12 May 2015

5 Refer to last page for important disclosures.

R e g i o n a l M o r n i n g N o t e s

GAC – sales slowed in April, but still positive. Sales growth of GQ Honda and GAC Toyota slowed from 70% and 27.5% yoy in 1Q15 to 27% and 12% yoy in Apr 15, still a decent growth. Looking ahead, the sales ramp-up of the New Highlander will likely spur sales and earnings of GAC Toyota. However, the sedan product lines – Honda Accord/Fit, Toyota Camry/Levin – remain under pressure.

Geely – robust domestic sales, weakened exports. Geely saw wholesales shipment growth slow from 55% yoy in 1Q15 to 12% yoy in Apr 15, as the yoy decline in export sales expanded from 22% yoy in 1Q15 to 84% yoy in Apr 15. Excluding export, domestic sales still grew 57% yoy to 38,618 units in Apr 15, representing 96% of total sales. Looking ahead, Geely’s sales will be driven by the GC9 and two SUV models that will be launched by 2H15.

ACTIONS

Maintain BUY on GWM. Given GWM’s leading position in the faster-growing SUV segment and strong SUV product pipelines in the next couple of years, we maintain GWM as a BUY. Our target price of HK$69.00 for GWM is based on 11x 2016F PE, 1SD above historical mean given prospective above-average earnings growth.

Upgrade Geely from HOLD to BUY, given the prospective strong product pipelines built on Volvo technologies. We raise target price from HK$4.50 (11x 2015F PE) to HK$5.50 (11x 2016F PE) by rolling over the base year from 2015 to 2016 and keep the target forward PE at 11x.

Downgrade DFM from BUY to HOLD, given unexpected sluggish sales of the old models and margin pressure from price competition. We cut EPS for 2015/2016/2017 by 10%/14%/14% to Rmb1.30/Rmb1.38/Rmb1.52 respectively. We lower target price from HK$15.00 (9x 2015F PE) to HK$14.00 (8x 2016F PE), as we roll over the base year from 2015 to 2016 and cut target PE multiple from 9x to 8x given slower earnings growth. Entry price is HK$12.0.

Maintain HOLD on GAC, give fair valuation. We roll over the base year for valuation from 2015 to 2016 and keep target PE multiple at 11x, which results in an increase in target price from HK$8.50 (11x 2015F PE) to HK$9.00 (11x 2016F PE). Entry price is HK$7.50.

SECTOR CATALYSTS

Release of sustained strong sales of GWM and Geely will boost their stock prices. The sustained weak sales momentum and quarter results of BMW Brilliance would dampen Brilliance’s stock price.

RISKS

Macro risk. Severe credit tightening would hurt auto sales hard. The shrinkage of bank notes had already affected sales of those carmakers with long bill receivable days, eg GWM and Geely. If car loans were affected, sales of premium cars would also be hit.

Geopolitical risk. The deterioration of Sino-Japan relations may trigger anti-Japanese riots in China, which could hit Japanese car sales in China. In this case, DFM and GAC would be affected the most.

TOP PICKS

Wholesales Retail Channel

1Q15 Apr 15 1Q15 Apr 15 Mar 15 Apr 15

BMW B illi

71,428 22,310 71,900 24,050 25 23

yoy chg (%) 6.5% -10% 15% 4% -25% -33%

DF Nissan 189,400 78,707 246,802

71,148 45 48

yoy chg (%) -11% -14% 26% 5% -39% 7%

DF Honda 68,400 30,000*

89,500 27,531 37 40

yoy chg (%) -17% -7% 15.5% -6% -36% -4%

DF PSA 180,616 58,000*

175,685

55,711 40 44

yoy chg (%) 9% -3% 12% -6% 43% -4%

GQ Honda 96,527 48,352 158,000*

44,015 15 18

yoy chg (%) 18% 85% 70% 27% -66% -58%

GAC Toyota 81,521 36,016 98,000*

33,000 35 41

yoy chg (%) -6% 20% 27.5% 12% -25% -17%

GWM ( l t)

216,372 75,991 191,722

65,987 n.a. n.a.

yoy chg (%) 24% 40% n.a. n.a. n.a. n.a.

GWM (total) 221,027 78,258 n.a. n.a. n.a. n.a.

yoy chg (%) 18% 32% n.a. n.a. n.a. n.a.

Geely ( l t)

130,179 38,618 153,046

35,000 34 42

yoy chg (%) 68% 45% 51% 62% -40% -57%

Geely (total) 140,525 40,090 n.a. n.a. n.a. n.a. yoy chg (%) 55% 12% n.a. n.a. n.a. n.a.

Source: China Passenger Car Association (CPCA), China Association of Automobile Manufacturers (CAAM), UOB Kay Hian

Tuesday , 12 May 2015

6 Refer to last page for important disclosures.

R e g i o n a l M o r n i n g N o t e s

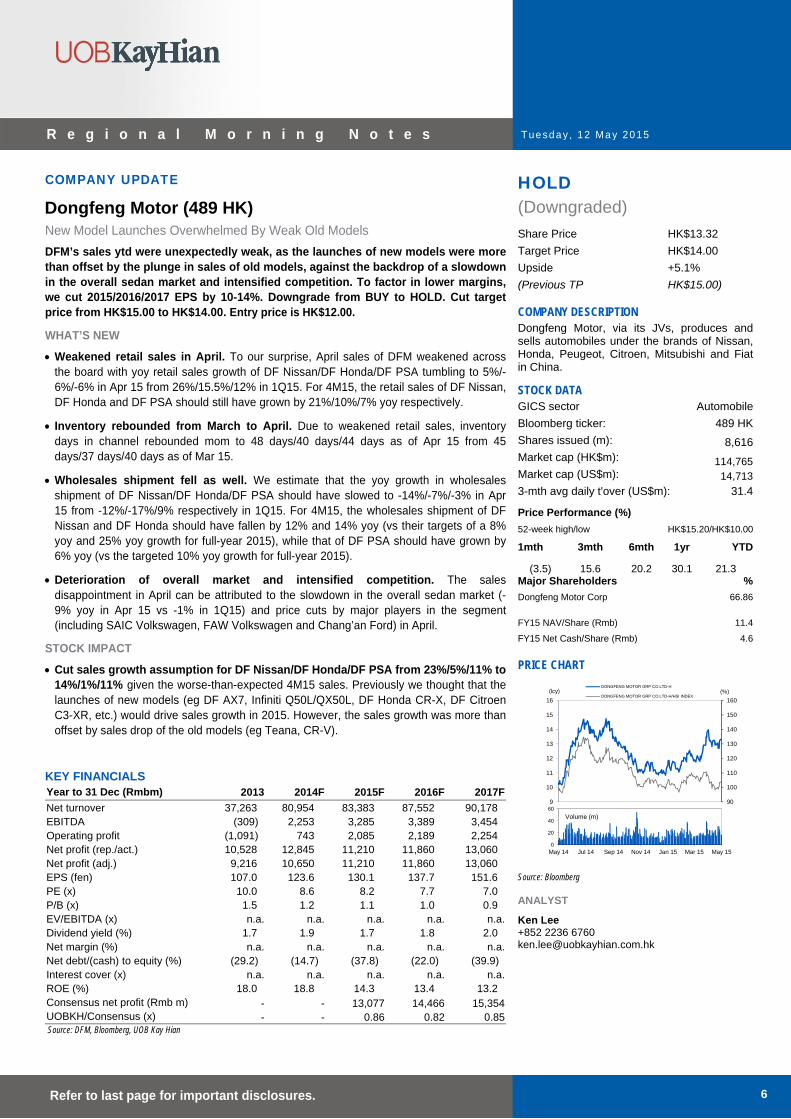

COMPANY UPDATE HOLD

(Downgraded)

Share Price HK$13.32

Target Price HK$14.00

Upside +5.1%

(Previous TP HK$15.00)

COMPANY DESCRIPTION Dongfeng Motor, via its JVs, produces and sells automobiles under the brands of Nissan, Honda, Peugeot, Citroen, Mitsubishi and Fiat in China.

STOCK DATA GICS sector Automobile

Bloomberg ticker: 489 HK

Shares issued (m): 8,616Market cap (HK$m): 114,765Market cap (US$m): 14,713

3-mth avg daily t'over (US$m): 31.4

Price Performance (%) 52-week high/low HK$15.20/HK$10.00

1mth 3mth 6mth 1yr YTD

(3.5) 15.6 20.2 30.1 21.3 Major Shareholders %

Dongfeng Motor Corp 66.86

FY15 NAV/Share (Rmb) 11.4

FY15 Net Cash/Share (Rmb) 4.6

PRICE CHART

90

100

110

120

130

140

150

160

9

10

11

12

13

14

15

16

(%)(lcy)DONGFENG MOTOR GRP CO LTD-H

DONGFENG MOTOR GRP CO LTD-H/HSI INDEX

0

20

40

60

May 14 Jul 14 Sep 14 Nov 14 Jan 15 Mar 15 May 15

Volume (m)

Source: Bloomberg

ANALYST

Ken Lee +852 2236 6760 [email protected]

Dongfeng Motor (489 HK)

New Model Launches Overwhelmed By Weak Old Models

DFM’s sales ytd were unexpectedly weak, as the launches of new models were more than offset by the plunge in sales of old models, against the backdrop of a slowdown in the overall sedan market and intensified competition. To factor in lower margins, we cut 2015/2016/2017 EPS by 10-14%. Downgrade from BUY to HOLD. Cut target price from HK$15.00 to HK$14.00. Entry price is HK$12.00.

WHAT’S NEW

Weakened retail sales in April. To our surprise, April sales of DFM weakened across the board with yoy retail sales growth of DF Nissan/DF Honda/DF PSA tumbling to 5%/-6%/-6% in Apr 15 from 26%/15.5%/12% in 1Q15. For 4M15, the retail sales of DF Nissan, DF Honda and DF PSA should still have grown by 21%/10%/7% yoy respectively.

Inventory rebounded from March to April. Due to weakened retail sales, inventory days in channel rebounded mom to 48 days/40 days/44 days as of Apr 15 from 45 days/37 days/40 days as of Mar 15.

Wholesales shipment fell as well. We estimate that the yoy growth in wholesales shipment of DF Nissan/DF Honda/DF PSA should have slowed to -14%/-7%/-3% in Apr 15 from -12%/-17%/9% respectively in 1Q15. For 4M15, the wholesales shipment of DF Nissan and DF Honda should have fallen by 12% and 14% yoy (vs their targets of a 8% yoy and 25% yoy growth for full-year 2015), while that of DF PSA should have grown by 6% yoy (vs the targeted 10% yoy growth for full-year 2015).

Deterioration of overall market and intensified competition. The sales disappointment in April can be attributed to the slowdown in the overall sedan market (-9% yoy in Apr 15 vs -1% in 1Q15) and price cuts by major players in the segment (including SAIC Volkswagen, FAW Volkswagen and Chang’an Ford) in April.

STOCK IMPACT

Cut sales growth assumption for DF Nissan/DF Honda/DF PSA from 23%/5%/11% to 14%/1%/11% given the worse-than-expected 4M15 sales. Previously we thought that the launches of new models (eg DF AX7, Infiniti Q50L/QX50L, DF Honda CR-X, DF Citroen C3-XR, etc.) would drive sales growth in 2015. However, the sales growth was more than offset by sales drop of the old models (eg Teana, CR-V).

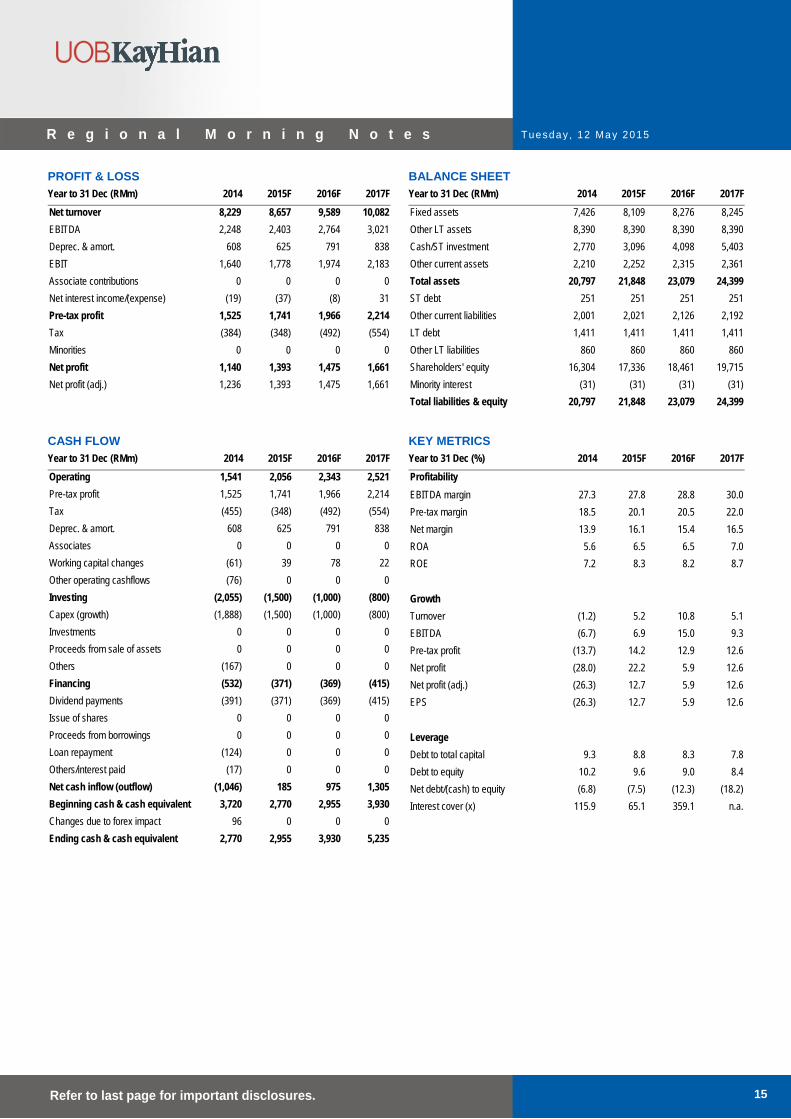

KEY FINANCIALS Year to 31 Dec (Rmbm) 2013 2014F 2015F 2016F 2017F

Net turnover 37,263 80,954 83,383 87,552 90,178 EBITDA (309) 2,253 3,285 3,389 3,454 Operating profit (1,091) 743 2,085 2,189 2,254 Net profit (rep./act.) 10,528 12,845 11,210 11,860 13,060 Net profit (adj.) 9,216 10,650 11,210 11,860 13,060 EPS (fen) 107.0 123.6 130.1 137.7 151.6 PE (x) 10.0 8.6 8.2 7.7 7.0 P/B (x) 1.5 1.2 1.1 1.0 0.9 EV/EBITDA (x) n.a. n.a. n.a. n.a. n.a. Dividend yield (%) 1.7 1.9 1.7 1.8 2.0 Net margin (%) n.a. n.a. n.a. n.a. n.a. Net debt/(cash) to equity (%) (29.2) (14.7) (37.8) (22.0) (39.9) Interest cover (x) n.a. n.a. n.a. n.a. n.a. ROE (%) 18.0 18.8 14.3 13.4 13.2 Consensus net profit (Rmb m) - - 13,077 14,466 15,354UOBKH/Consensus (x) - - 0.86 0.82 0.85Source: DFM, Bloomberg, UOB Kay Hian

Tuesday , 12 May 2015

7 Refer to last page for important disclosures.

R e g i o n a l M o r n i n g N o t e s

Lower margin. Given the slowdown in the sedan market and intensified competition, we believe DFM will need to provide more price discount to stimulate sales. We cut the net margin assumption on the JVs for 2015/2016/2017 from 4.8%/4.8%/4.8% to 4.2%/3.9%/3.9% respectively.

EARNINGS REVISION/RISK

Cut 2015-16 EPS by 10-14%. Given the aforementioned lower sales and margin assumption, we cut our core EPS forecasts for 2015/2016/2017 by 10%/14%/14% to Rmb1.30/Rmb1.38/Rmb1.52 respectively. Our forecasts imply a core EPS growth of 5%/6%/10% in 2015/2016/2017 respectively, which are 14-18% below consensus, given our lower margin assumptions.

PSA as a swing factor. DFM acquired a 14% stake in PSA for €800m in 2014 and since 2Q14, DFM has booked in PSA as an associate. PSA made a €706m net loss in 2014. However, DFM booked Rmb2.09b in shared profit from associates in 2014, by virtue of the Rmb2,055m in revaluation gain from its investment in PSA, given the PSA stock price rally. From 2015, PSA’s profit/loss will start to impact DFM’s bottom-line. While the street expects a turnaround from PSA, we assume zero profit contribution from PSA. If PSA registers a loss again in the next few years, this would hurt DFM’s bottom-line. We estimate that a €100m in net profit (loss) for PSA would translate into a Rmb125m in shared profit for DFM, or 1% of 2015 bottom-line.

Geopolitics is a major risk. Risk to our earnings estimates will be mainly geopolitics, eg Japanese car sales in China could be hurt by large-scale anti-Japanese riots as seen in Sep 12. However, as long as the escalating Sino-Japan tension as a result of the Diaoyu Islands (Senkaku Islands in Japanese) dispute or other issues do not trigger such riots in China, sales of Japanese cars in the country should not be affected.

VALUATION/RECOMMENDATION

Downgrade from BUY to HOLD. Based on our latest EPS estimates, the stock now trades at 8.2x 2015F PE and 7.7x 2016F PE, compared with historical mean of 9x. Given the prospective slower-than-historical average earnings growth (merely 5-6% in 2015-16 vs >10% historically), we cut the target PE multiple from 9x to 8x (a discount to historical mean). Besides, we roll over the base year for valuation from 2015 to 2016. That results in a cut in target price from HK$15.00 to HK$14.00. Given limited upside, we downgrade DFM from BUY to HOLD.

Tuesday , 12 May 2015

8 Refer to last page for important disclosures.

R e g i o n a l M o r n i n g N o t e s

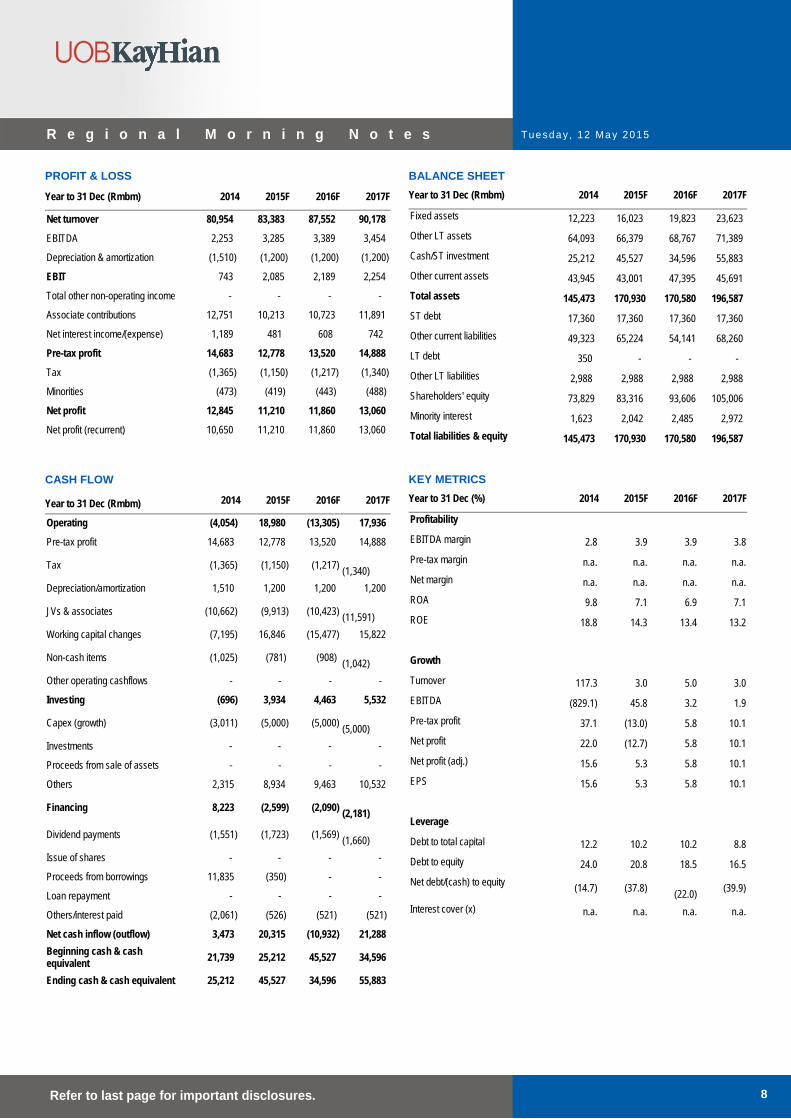

PROFIT & LOSS

Year to 31 Dec (Rmbm) 2014 2015F 2016F 2017F

Net turnover 80,954 83,383 87,552 90,178

EBITDA 2,253 3,285 3,389 3,454

Depreciation & amortization (1,510) (1,200) (1,200) (1,200)

EBIT 743 2,085 2,189 2,254

Total other non-operating income - - - -

Associate contributions 12,751 10,213 10,723 11,891

Net interest income/(expense) 1,189 481 608 742

Pre-tax profit 14,683 12,778 13,520 14,888

Tax (1,365) (1,150) (1,217) (1,340)

Minorities (473) (419) (443) (488)

Net profit 12,845 11,210 11,860 13,060

Net profit (recurrent) 10,650 11,210 11,860 13,060

BALANCE SHEET Year to 31 Dec (Rmbm) 2014 2015F 2016F 2017F

Fixed assets 12,223 16,023 19,823 23,623

Other LT assets 64,093 66,379 68,767 71,389

Cash/ST investment 25,212 45,527 34,596 55,883

Other current assets 43,945 43,001 47,395 45,691

Total assets 145,473 170,930 170,580 196,587

ST debt 17,360 17,360 17,360 17,360

Other current liabilities 49,323 65,224 54,141 68,260

LT debt 350 - - -

Other LT liabilities 2,988 2,988 2,988 2,988

Shareholders' equity 73,829 83,316 93,606 105,006

Minority interest 1,623 2,042 2,485 2,972

Total liabilities & equity 145,473 170,930 170,580 196,587

CASH FLOW

Year to 31 Dec (Rmbm) 2014 2015F 2016F 2017F

Operating (4,054) 18,980 (13,305) 17,936

Pre-tax profit 14,683 12,778 13,520 14,888

Tax (1,365) (1,150) (1,217) (1,340)

Depreciation/amortization 1,510 1,200 1,200 1,200

JVs & associates (10,662) (9,913) (10,423) (11,591)

Working capital changes (7,195) 16,846 (15,477) 15,822

Non-cash items (1,025) (781) (908) (1,042)

Other operating cashflows - - - -

Investing (696) 3,934 4,463 5,532

Capex (growth) (3,011) (5,000) (5,000) (5,000)

Investments - - - -

Proceeds from sale of assets - - - -

Others 2,315 8,934 9,463 10,532

Financing 8,223 (2,599) (2,090) (2,181)

Dividend payments (1,551) (1,723) (1,569) (1,660)

Issue of shares - - - -

Proceeds from borrowings 11,835 (350) - -

Loan repayment - - - -

Others/interest paid (2,061) (526) (521) (521)

Net cash inflow (outflow) 3,473 20,315 (10,932) 21,288

Beginning cash & cash equivalent 21,739 25,212 45,527 34,596

Ending cash & cash equivalent 25,212 45,527 34,596 55,883

KEY METRICS Year to 31 Dec (%) 2014 2015F 2016F 2017F

Profitability

EBITDA margin 2.8 3.9 3.9 3.8

Pre-tax margin n.a. n.a. n.a. n.a.

Net margin n.a. n.a. n.a. n.a.

ROA 9.8 7.1 6.9 7.1

ROE 18.8 14.3 13.4 13.2

Growth

Turnover 117.3 3.0 5.0 3.0

EBITDA (829.1) 45.8 3.2 1.9

Pre-tax profit 37.1 (13.0) 5.8 10.1

Net profit 22.0 (12.7) 5.8 10.1

Net profit (adj.) 15.6 5.3 5.8 10.1

EPS 15.6 5.3 5.8 10.1

Leverage

Debt to total capital 12.2 10.2 10.2 8.8

Debt to equity 24.0 20.8 18.5 16.5

Net debt/(cash) to equity (14.7) (37.8) (22.0)

(39.9)

Interest cover (x) n.a. n.a. n.a. n.a.

Tuesday , 12 May 2015

9 Refer to last page for important disclosures.

R e g i o n a l M o r n i n g N o t e s

SECTOR UPDATE

Retail - Indonesia Aprindo: What Will Work In The Retail Sector In 2015

The Indonesia Retailers Association views the key drivers for success in 2015 as: a) retailers who expand into eastern Indonesia will enjoy high SSS growth, b) local products are key, c) caps on store count, zoning and franchise are not yet applied on a wide scale, and d) discounting is still very important. The potential beneficiaries are LPPF and MPPA while ANRT could lose out due to the ban on alcohol sales in minimarts. Maintain MARKET WEIGHT on the sector.

WHAT’S NEW

Slowdown in SSS growth and retail sales. In 2014, Aprindo said Indonesia retailers generated Rp168t in sales and believe sales would grow only 6% yoy to Rp178t in 2015. The slow growth is due to weak purchasing power which has hit retailers, who are expected to report an average same-store sales (SSS) growth of about 5%.

Strong SSS growth in eastern Indonesia. Aprindo said Matahari Department Stores could generate SSS growth of above 10% in 2014 because of its expansion into eastern Indonesia. There is virtually no competition while there is actually untapped purchasing power there. MPPA and LPPF have done very well in the cities such as Kupang and Jayapura. According to LPPF, its 10% SSS growth was because of the middle class in Indonesia. (Note 1Q15 SSS growth of LPPF slowed to 5.4% while RALS’s SSS declined 3.3% yoy)

To succeed: Localised product and knowledge. According to Aprindo, retailers will need local products and knowledge to succeed in Indonesia. Merchandises in Jakarta are different than those in Makassar and retailers must work with local suppliers to tap into the local markets. Taste is different from region to region and fresh vegetables and fruits have to be sourced locally as there is no nationwide cold storage distribution. Aprindo explains that local knowledge is the reason behind the success of regional retailers such as Yogya and Macan Yaohan.

Short-term pressure on SSS growth at minimarts as the alcohol ban takes effect. Aprindo views SSS growth of minimarkets and convenience stores could slow as the nationwide ban on selling alcoholic beverages in minimarkets takes effect. Drinks make up 11-12% of all minimarkets’ sales and of the 11-12% sales, 35-40% come from alcoholic beverages (beer, spirit, wine etc). Selling alcoholic beverages in supermarkets and hypermarkets is still allowed.

Potential beneficiaries: LPPF and MPPA; potential losers: AMRT, ACES. The key takeaway from our meeting is that LPPF and MPPA could benefit from their expansion into eastern Indonesia, while AMRT could see slower SSS growth due to the nationwide ban on alcoholic beverage sales in minimarkets ACES could be affected if the 80% local content rule is enforced upon retailers, and it is currently seeking for an exemption.

MARKET WEIGHT (Maintained) LPPF - 12M PE BAND (SINCE RELISTING)

Source: Bloomberg, UOB Kay Hian

MPPA – 12M FOR PE BAND (SINCE RELISTING)

Source: Bloomberg, UOB Kay Hian

AMRT – 12M PE BAND

Source: Bloomberg, UOB Kay Hian ANALYST

Stevanus Juanda + 6221 2993 3845 [email protected]

PEER COMPARISON

Current Price (Rp)

Market Cap (US$m)

PE (x) P/B (x) EV/EBITDA (x) Dividend yield (%)

ROE (%) Net Gearing

(%) Ticker Company 2015F 2016F 2015F 2016F 2015F 2016F 2015F 2016F 2014 2015F

MPPA IJ Matahari Putra Prima 3,930 1,607 35.2 29.4 6.0 5.2 20 16 0.7 0.8 18.0 18.5 (26.2) LPPF IJ Matahari Department Store 16,875 3,744 25.9 21.3 44.9 22.3 18 16 1.8 2.3 n.a. 289.6 (54.5) AMRT IJ Sumber Alfaria Trijaya 560 1,644 33.8 26.7 5.9 5.1 10.6 9.1 0.9 1.1 20.3 18.6 146.2 RALS IJ Ramayana Lestari Sentosa 760 410 14.5 13.5 1.5 1.5 7.0 6.2 3.6 3.4 10.8 11.1 (50.2) HERO IJ Hero Supermarket 2,060 655 n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. 0.8 n.a. (3.6) CSAP IJ Catur Sentosa Adiprana 530 117 n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. 15.2 n.a. 91.1 ACES IJ Ace Hardware Indonesia 680 887 19.8 16.9 4.21 3.5 14.2 12.0 1.1 1.2 26.0 22.4 (15.4) MAPI IJ Mitra Adiperkasa 5,250 663 29.6 17.0 3.0 2.6 9.5 7.7 0.3 0.6 3.0 11.2 111.6

Average 26.5 20.8 10.9 6.7 13.2 11.2 1.4 1.6 13.5 61.9 24.9 Median 27.8 19.2 5.0 4.3 12.4 10.6 1.0 1.1 15.2 18.5 (9.5)

Source: Bloomberg, UOB Kay Hian

Tuesday , 12 May 2015

10 Refer to last page for important disclosures.

R e g i o n a l M o r n i n g N o t e s

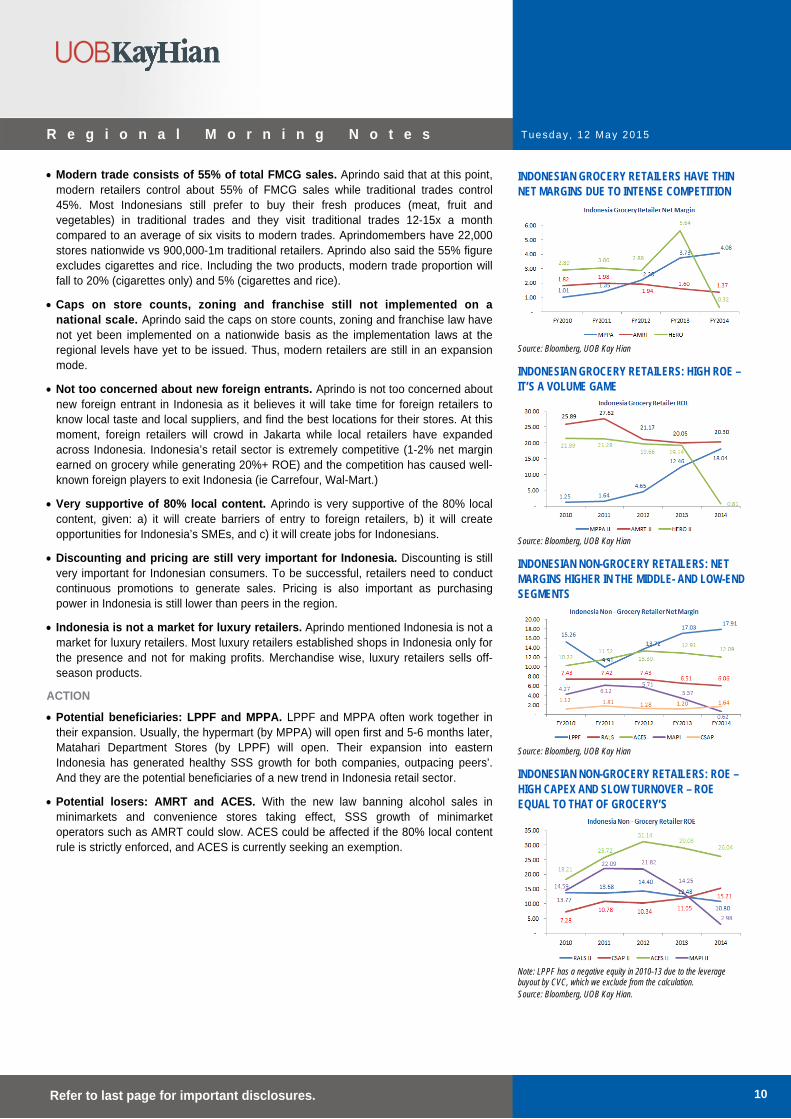

Modern trade consists of 55% of total FMCG sales. Aprindo said that at this point, modern retailers control about 55% of FMCG sales while traditional trades control 45%. Most Indonesians still prefer to buy their fresh produces (meat, fruit and vegetables) in traditional trades and they visit traditional trades 12-15x a month compared to an average of six visits to modern trades. Aprindomembers have 22,000 stores nationwide vs 900,000-1m traditional retailers. Aprindo also said the 55% figure excludes cigarettes and rice. Including the two products, modern trade proportion will fall to 20% (cigarettes only) and 5% (cigarettes and rice).

Caps on store counts, zoning and franchise still not implemented on a national scale. Aprindo said the caps on store counts, zoning and franchise law have not yet been implemented on a nationwide basis as the implementation laws at the regional levels have yet to be issued. Thus, modern retailers are still in an expansion mode.

Not too concerned about new foreign entrants. Aprindo is not too concerned about new foreign entrant in Indonesia as it believes it will take time for foreign retailers to know local taste and local suppliers, and find the best locations for their stores. At this moment, foreign retailers will crowd in Jakarta while local retailers have expanded across Indonesia. Indonesia’s retail sector is extremely competitive (1-2% net margin earned on grocery while generating 20%+ ROE) and the competition has caused well-known foreign players to exit Indonesia (ie Carrefour, Wal-Mart.)

Very supportive of 80% local content. Aprindo is very supportive of the 80% local content, given: a) it will create barriers of entry to foreign retailers, b) it will create opportunities for Indonesia’s SMEs, and c) it will create jobs for Indonesians.

Discounting and pricing are still very important for Indonesia. Discounting is still very important for Indonesian consumers. To be successful, retailers need to conduct continuous promotions to generate sales. Pricing is also important as purchasing power in Indonesia is still lower than peers in the region.

Indonesia is not a market for luxury retailers. Aprindo mentioned Indonesia is not a market for luxury retailers. Most luxury retailers established shops in Indonesia only for the presence and not for making profits. Merchandise wise, luxury retailers sells off-season products.

ACTION

Potential beneficiaries: LPPF and MPPA. LPPF and MPPA often work together in their expansion. Usually, the hypermart (by MPPA) will open first and 5-6 months later, Matahari Department Stores (by LPPF) will open. Their expansion into eastern Indonesia has generated healthy SSS growth for both companies, outpacing peers’. And they are the potential beneficiaries of a new trend in Indonesia retail sector.

Potential losers: AMRT and ACES. With the new law banning alcohol sales in minimarkets and convenience stores taking effect, SSS growth of minimarket operators such as AMRT could slow. ACES could be affected if the 80% local content rule is strictly enforced, and ACES is currently seeking an exemption.

INDONESIAN GROCERY RETAILERS HAVE THIN NET MARGINS DUE TO INTENSE COMPETITION

Source: Bloomberg, UOB Kay Hian

INDONESIAN GROCERY RETAILERS: HIGH ROE – IT’S A VOLUME GAME

Source: Bloomberg, UOB Kay Hian

INDONESIAN NON-GROCERY RETAILERS: NET MARGINS HIGHER IN THE MIDDLE- AND LOW-END SEGMENTS

Source: Bloomberg, UOB Kay Hian

INDONESIAN NON-GROCERY RETAILERS: ROE – HIGH CAPEX AND SLOW TURNOVER – ROE EQUAL TO THAT OF GROCERY’S

Note: LPPF has a negative equity in 2010-13 due to the leverage buyout by CVC, which we exclude from the calculation. Source: Bloomberg, UOB Kay Hian.

Tuesday , 12 May 2015

11 Refer to last page for important disclosures.

R e g i o n a l M o r n i n g N o t e s

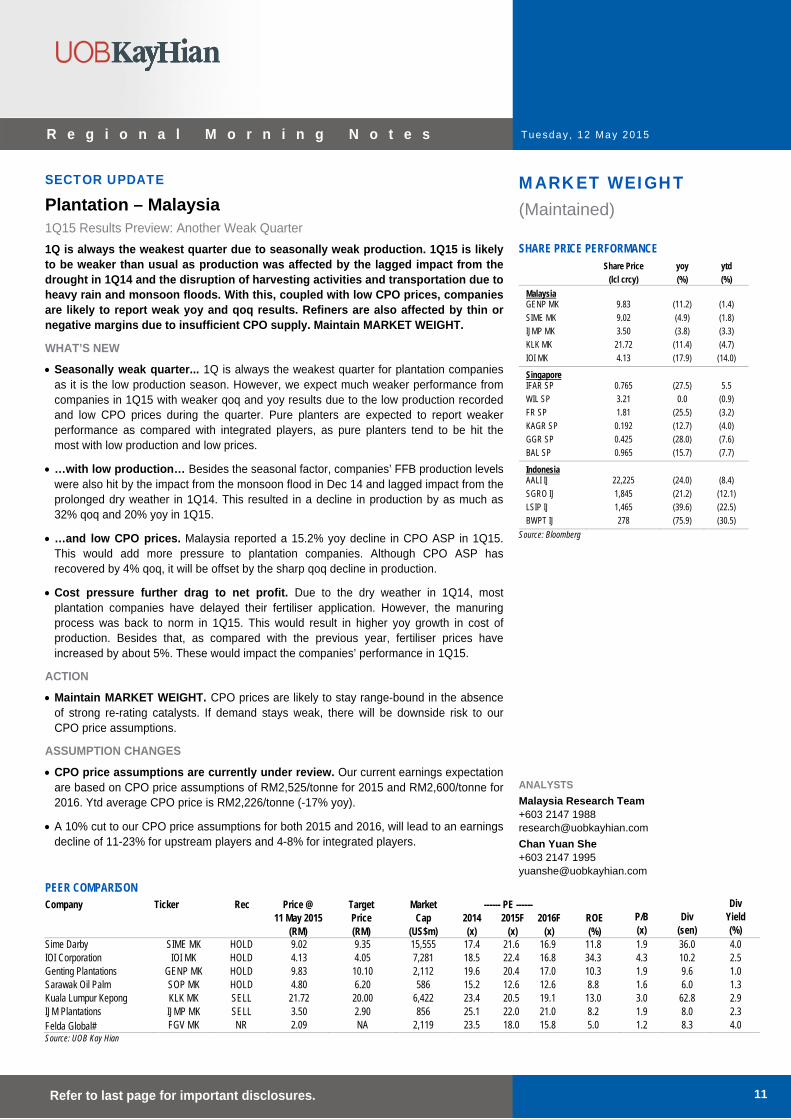

SECTOR UPDATE

Plantation – Malaysia 1Q15 Results Preview: Another Weak Quarter

1Q is always the weakest quarter due to seasonally weak production. 1Q15 is likely to be weaker than usual as production was affected by the lagged impact from the drought in 1Q14 and the disruption of harvesting activities and transportation due to heavy rain and monsoon floods. With this, coupled with low CPO prices, companies are likely to report weak yoy and qoq results. Refiners are also affected by thin or negative margins due to insufficient CPO supply. Maintain MARKET WEIGHT.

WHAT’S NEW

Seasonally weak quarter... 1Q is always the weakest quarter for plantation companies as it is the low production season. However, we expect much weaker performance from companies in 1Q15 with weaker qoq and yoy results due to the low production recorded and low CPO prices during the quarter. Pure planters are expected to report weaker performance as compared with integrated players, as pure planters tend to be hit the most with low production and low prices.

…with low production… Besides the seasonal factor, companies’ FFB production levels were also hit by the impact from the monsoon flood in Dec 14 and lagged impact from the prolonged dry weather in 1Q14. This resulted in a decline in production by as much as 32% qoq and 20% yoy in 1Q15.

…and low CPO prices. Malaysia reported a 15.2% yoy decline in CPO ASP in 1Q15. This would add more pressure to plantation companies. Although CPO ASP has recovered by 4% qoq, it will be offset by the sharp qoq decline in production.

Cost pressure further drag to net profit. Due to the dry weather in 1Q14, most plantation companies have delayed their fertiliser application. However, the manuring process was back to norm in 1Q15. This would result in higher yoy growth in cost of production. Besides that, as compared with the previous year, fertiliser prices have increased by about 5%. These would impact the companies’ performance in 1Q15.

ACTION

Maintain MARKET WEIGHT. CPO prices are likely to stay range-bound in the absence of strong re-rating catalysts. If demand stays weak, there will be downside risk to our CPO price assumptions.

ASSUMPTION CHANGES

CPO price assumptions are currently under review. Our current earnings expectation are based on CPO price assumptions of RM2,525/tonne for 2015 and RM2,600/tonne for 2016. Ytd average CPO price is RM2,226/tonne (-17% yoy).

A 10% cut to our CPO price assumptions for both 2015 and 2016, will lead to an earnings decline of 11-23% for upstream players and 4-8% for integrated players.

MARKET WEIGHT (Maintained) SHARE PRICE PERFORMANCE

Share Price yoy ytd

(lcl crcy) (%) (%)

Malaysia GENP MK 9.83 (11.2) (1.4)

SIME MK 9.02 (4.9) (1.8)

IJMP MK 3.50 (3.8) (3.3)

KLK MK 21.72 (11.4) (4.7)

IOI MK 4.13 (17.9) (14.0)

Singapore IFAR SP 0.765 (27.5) 5.5

WIL SP 3.21 0.0 (0.9)

FR SP 1.81 (25.5) (3.2)

KAGR SP 0.192 (12.7) (4.0)

GGR SP 0.425 (28.0) (7.6)

BAL SP 0.965 (15.7) (7.7)

Indonesia AALI IJ 22,225 (24.0) (8.4)

SGRO IJ 1,845 (21.2) (12.1)

LSIP IJ 1,465 (39.6) (22.5)

BWPT IJ 278 (75.9) (30.5)

Source: Bloomberg

ANALYSTS

Malaysia Research Team +603 2147 1988 [email protected]

Chan Yuan She +603 2147 1995 [email protected]

PEER COMPARISON Company Ticker Rec Price @ Target Market ------ PE ------ Div 11 May 2015 Price Cap 2014 2015F 2016F ROE P/B Div Yield (RM) (RM) (US$m) (x) (x) (x) (%) (x) (sen) (%) Sime Darby SIME MK HOLD 9.02 9.35 15,555 17.4 21.6 16.9 11.8 1.9 36.0 4.0 IOI Corporation IOI MK HOLD 4.13 4.05 7,281 18.5 22.4 16.8 34.3 4.3 10.2 2.5 Genting Plantations GENP MK HOLD 9.83 10.10 2,112 19.6 20.4 17.0 10.3 1.9 9.6 1.0 Sarawak Oil Palm SOP MK HOLD 4.80 6.20 586 15.2 12.6 12.6 8.8 1.6 6.0 1.3 Kuala Lumpur Kepong KLK MK SELL 21.72 20.00 6,422 23.4 20.5 19.1 13.0 3.0 62.8 2.9 IJM Plantations IJMP MK SELL 3.50 2.90 856 25.1 22.0 21.0 8.2 1.9 8.0 2.3 Felda Global# FGV MK NR 2.09 NA 2,119 23.5 18.0 15.8 5.0 1.2 8.3 4.0 Source: UOB Kay Hian

Tuesday , 12 May 2015

12 Refer to last page for important disclosures.

R e g i o n a l M o r n i n g N o t e s

ESSENTIALS

Weak production. 1Q is usually the weakest production quarter for plantation companies. Therefore, it is a norm for companies to report weaker qoq production growth. However, the drop in production was rather significant in 1Q15 as production was also dragged by the lagged impact from dry weather in 1Q14 and impact from monsoon flood. The floods disrupted transportation and harvesting activities especially in the East Coast region as well as Sabah and Sarawak. IOI Corporation (IOI) and IJM Plantation (IJMP) reported the most significant FFB production drop of 31.8% qoq (-12.5% yoy) and 30.4% qoq (-13.9% yoy) respectively.

Substantial drop in CPO ASP. Malaysia reported 15.2% yoy decline in CPO ASP in 1Q15. This would result a more significant decline in plantation companies’ net profit due to the low production growth. Besides that, companies with larger exposure to East Malaysia would have a greater impact as the discount of CPO ASP in East Malaysia vs Peninsular Malaysia has widened to RM47-72/tonnes as compared with 1Q14’s RM22-33/tonne. Companies that are likely to be affected include IOI, IJMP, Sarawak Oil Palm (SOP) and Genting Plantations (GENP).

Downstream operation is suffering. Refiners have been experiencing negative margins due to insufficient CPO supply affected by the low production season and upstream players are choosing to export more CPO to take advantage of the zero export duty on CPO during the quarter. The differences between RBD olein and CPO price has narrowed to RM87/tonne as compared with RM108/tonne in 1Q14 and RM120/tonne in 4Q14. This will affect companies with refining business such as SOP, IOI, KLK and Sime Darby. However, unlike SOP, IOI and KLK also have exposure to the oleochemical business, which is still commanding a decent margin, as they focus more on niche and higher-margin products. This would help to support the performance for their downstream operation.

Currency depreciation might distort earnings. The rupiah has depreciated by 4.3% qoq (-7.7% yoy) against the US dollar while the ringgit has depreciated by 7.0% qoq (-8.9% yoy) against the US dollar in 1Q15. Thus, earnings for companies with exposure to Indonesia rupiah- and US dollar-denominated loans might be distorted by translation gains or losses arising from the currency depreciation.

SECTOR CATALYSTS

Palm oil shortage. This could have been due to the dry weather in Peninsular Malaysia in 1Q14 and in Kalimantan in late-3Q14.

Restocking in China. Palm oil inventories in China have fallen significantly by 60% from the peak of 1.2m tonnes in Feb 14 to 386,000 tonnes as at 14 Apr 15.

Acceleration in biodiesel blending in Indonesia and Malaysia. Indonesia is now the largest palm biodiesel consuming country. If Indonesia puts in all efforts to meet its B15 requirement, there could be less palm oil available for the global market.

RISKS

Backtracking of biodiesel mandates in Indonesia and Malaysia on lower crude oil prices.

Soybean supply gluts.

WEAKER YOY IN PRODUCTION AND CPO PRICES (tonnes) 1Q14 4Q14 1Q15 qoq % chg yoy % chg FFB Production FGV 1,159,000 1,254,425 930,018 (25.9) (19.8) IJMP 191,374 236,637 164,790 (30.4) (13.9) IOI 781,506 1,002,804 683,718 (31.8) (12.5) SOP 219,741 258,915 198,830 (23.2) (9.5) SIME 2,095,708 2,193,539 2,022,264 (7.8) (3.5) KLK 842,337 954,709 825,549 (13.5) (2.0) GENP 376,933 473,942 374,572 (21.0) (0.6) CPO Price (RM/tonne) Malaysia 2,672 2,178 2,266 4.0 (15.2) Pen. Malaysia 2,677 2,188 2,272 3.9 (15.1) Sabah 2,655 2,127 2,226 4.6 (16.2) Sarawak 2,644 2,127 2,200 3.4 (16.8)

Source: MPOB, Respective companies

SHARP DROP IN MALAYSIA CPO PRODUCTION

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

1Q12 3Q12 1Q13 3Q13 1Q14 3Q14 1Q15

(m tonnes)

-25

-15

-5

5

15

25(%)

Production (LHS)yoy % chg (RHS)

Source: MPOB

NARROWING GAP BETWEEN RBD OLEIN AND CPO PRICES

1,500

2,000

2,500

3,000

3,500

4,000

1Q10 1Q11 1Q12 1Q13 1Q14 1Q15

(RM/tonne)

RBD Olein Prices

CPO Prices

Source: MPOB

DEPRECIATION AGAINST US DOLLAR

9000

9500

10000

10500

11000

11500

12000

12500

13000

13500

Jan 13 Jul 13 Jan 14 Jul 14 Jan 15

(Rp/US$)

2.9

3

3.1

3.2

3.3

3.4

3.5

3.6

3.7

3.8(RM/US$)

USD to IDR (LHS)

USD to MYR (RHS)

Source: Bloomberg

ESTIMATED PLANTED AREA BREAKDOWN (%) Malaysia Indonesia Others GENP 55 45 - IJMP 55 45 - IOI 95 5 - KLK 45 52 3 SIME 52 33 15 SOP 100 - -

Source: Respective companies

US DOLLAR LOAN EXPOSURE % of debt USD denominated GENP 100 IJMP 100 IOI 88 SIME 38 KLK 5 SOP 0

Source: Respective companies

Tuesday , 12 May 2015

13 Refer to last page for important disclosures.

R e g i o n a l M o r n i n g N o t e s

COMPANY UPDATE BUY

(Maintained)

Share Price RM4.30

Target Price RM4.76

Upside +10.7%

(Previous TP RM4.47)

COMPANY DESCRIPTION Casino, resort and theme park operator

STOCK DATA GICS sector Consumer Discretionary

Bloomberg ticker: GENM MK

Shares issued (m): 5,670.4

Market cap (RMm): 24,382.9

Market cap (US$m): 6,769.8

3-mth avg daily t'over (US$m): 4.1

Price Performance (%) 52-week high/low RM4.67/RM3.79

1mth 3mth 6mth 1yr YTD

(2.7) 4.9 3.1 2.6 5.7

Major Shareholders %

Genting Bhd 47.2

FY15 NAV/Share (RM) 2.93

FY15 Net Cash/Share (RM) 0.24

PRICE CHART

80

90

100

110

120

3.50

4.00

4.50

5.00

(%)(lcy)GENTING MALAYSIA BHD

GENTING MALAYSIA BHD/FBMKLCI INDEX

0

5

10

15

May 14 Jul 14 Sep 14 Nov 14 Jan 15 Mar 15 May 15

Volume (m)

Source: Bloomberg

ANALYST

Vincent Khoo, CFA +603 2147 1998 [email protected]

Genting Malaysia (GENM MK)

Proposed Stake Sale In GENHK

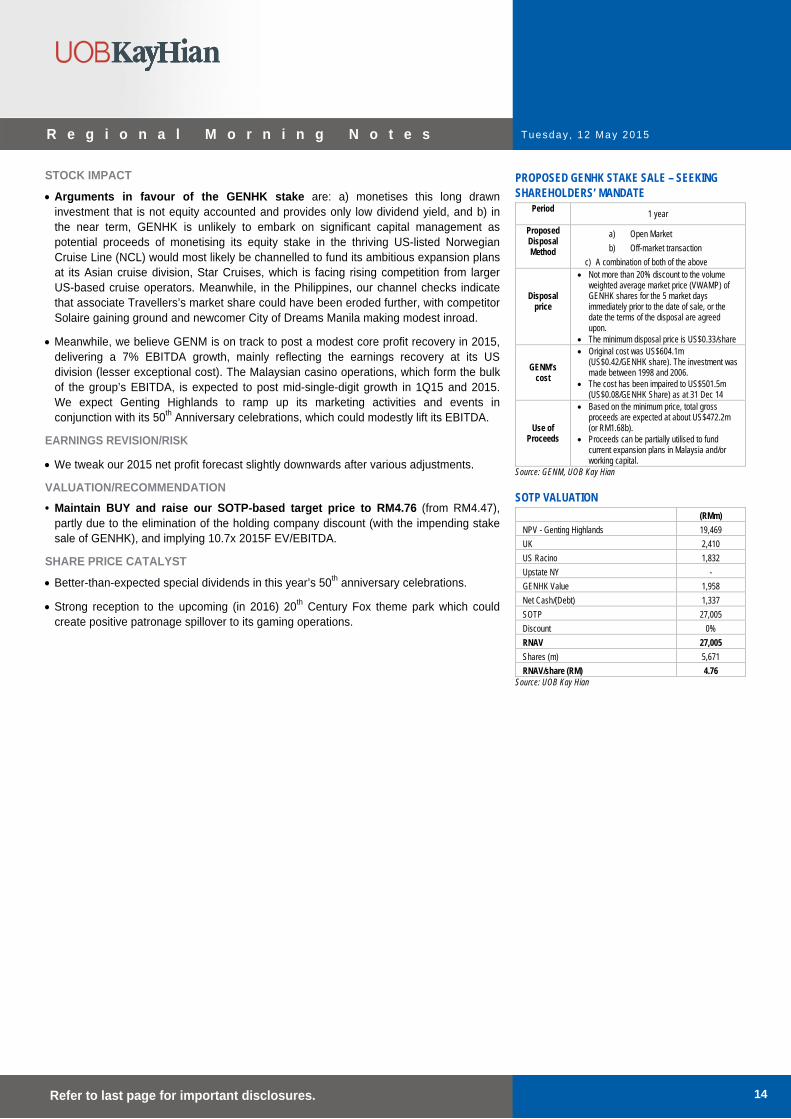

GENM is seeking shareholders’ approval to sell its 17.8% stake in GENHK. We see this as a mild positive on the back of estimated gains of RM1.25b-1.51b, or 21-27 sen/share, based on exit prices of US$0.33-0.38 each. GENHK shares are unlikely to reach our SOTP valuation of US$0.60/share and the sale could improve GENM’s capital management. Maintain BUY and raise our target price to RM4.76 (from RM4.47).

WHAT’S NEW

Genting Malaysia (GENM) is seeking shareholders’ approval to sell its 17.8% stake in Genting Hong Kong (GENHK) for at least US$0.33 each (see details on table overleaf).

We believe the sale process will be transparent, and will appropriately address issues, such as the deal being a potential related-party transaction The Genting Group’s controlling shareholder (Lim family), which owns 60% of GENHK, will likely make a bid for GENM’s stake.

Mildly-positive corporate exercise for GENM. We hope cash-rich GENM will be able to partially utilise the sales proceeds to modestly boost its capital-management efforts, particularly in this year when GENM celebrates the Genting Group’s 50th anniversary. GENM could pocket gains of RM1.25b-1.51b (or 21-27 sen/share) based on exit prices of US$0.33-US$0.38 each. In its announcement, GENM said the proceeds may be partially utilised to fund current expansion plans in Malaysia and/or working capital. Note that while our SOTP valuation for GENHK appears high at US$0.60/share, we expect GENHK to continue trading at significant discount to our valuation for reasons which are explained in the ensuing paragraph.

However, one may argue that the minimum sale price is a tad low, considering that the stock’s 1-year trading range is US0.34-0.41 (closing US$0.37 yesterday), and that the last time it closed below US$0.33 was in 2012.

KEY FINANCIALS Year to 31 Dec (RMm) 2013 2014 2015F 2016F 2017F

Net turnover 8,327 8,229 8,657 9,589 10,082EBITDA 2,409 2,248 2,403 2,764 3,021Operating profit 1,857 1,640 1,778 1,974 2,183Net profit (rep./act.) 1,584 1,140 1,393 1,475 1,661Net profit (adj.) 1,678 1,236 1,393 1,475 1,661EPS (sen) 28.4 20.9 23.5 24.9 28.1PE (x) 15.2 20.6 18.3 17.3 15.3P/B (x) 1.6 1.6 1.5 1.4 1.3EV/EBITDA (x) 9.6 10.3 9.6 8.3 7.6Dividend yield (%) 2.2 1.6 1.8 1.9 2.2Net margin (%) 19.0 13.9 16.1 15.4 16.5Net debt/(cash) to equity (%) (13.1) (6.8) (7.5) (12.3) (18.2)Interest cover (x) n.a. 115.9 65.1 359.1 n.a.ROE (%) 11.1 7.2 8.3 8.2 8.7Consensus net profit - - 1,431 1,613 1,801UOBKH/Consensus (x) - - 0.97 0.91 0.92Source: GENM, Bloomberg, UOB Kay Hian

Tuesday , 12 May 2015

14 Refer to last page for important disclosures.

R e g i o n a l M o r n i n g N o t e s

STOCK IMPACT

Arguments in favour of the GENHK stake are: a) monetises this long drawn investment that is not equity accounted and provides only low dividend yield, and b) in the near term, GENHK is unlikely to embark on significant capital management as potential proceeds of monetising its equity stake in the thriving US-listed Norwegian Cruise Line (NCL) would most likely be channelled to fund its ambitious expansion plans at its Asian cruise division, Star Cruises, which is facing rising competition from larger US-based cruise operators. Meanwhile, in the Philippines, our channel checks indicate that associate Travellers’s market share could have been eroded further, with competitor Solaire gaining ground and newcomer City of Dreams Manila making modest inroad.

Meanwhile, we believe GENM is on track to post a modest core profit recovery in 2015, delivering a 7% EBITDA growth, mainly reflecting the earnings recovery at its US division (lesser exceptional cost). The Malaysian casino operations, which form the bulk of the group’s EBITDA, is expected to post mid-single-digit growth in 1Q15 and 2015. We expect Genting Highlands to ramp up its marketing activities and events in conjunction with its 50th Anniversary celebrations, which could modestly lift its EBITDA.

EARNINGS REVISION/RISK

We tweak our 2015 net profit forecast slightly downwards after various adjustments.

VALUATION/RECOMMENDATION

• Maintain BUY and raise our SOTP-based target price to RM4.76 (from RM4.47), partly due to the elimination of the holding company discount (with the impending stake sale of GENHK), and implying 10.7x 2015F EV/EBITDA.

SHARE PRICE CATALYST

Better-than-expected special dividends in this year’s 50th anniversary celebrations.

Strong reception to the upcoming (in 2016) 20th Century Fox theme park which could create positive patronage spillover to its gaming operations.

PROPOSED GENHK STAKE SALE – SEEKING SHAREHOLDERS’ MANDATE

Period 1 year

Proposed Disposal Method

a) Open Market

b) Off-market transaction

c) A combination of both of the above

Disposal price

Not more than 20% discount to the volume weighted average market price (VWAMP) of GENHK shares for the 5 market days immediately prior to the date of sale, or the date the terms of the disposal are agreed upon.

The minimum disposal price is US$0.33/share

GENM’s cost

Original cost was US$604.1m (US$0.42/GENHK share). The investment was made between 1998 and 2006.

The cost has been impaired to US$501.5m (US$0.08/GENHK Share) as at 31 Dec 14

Use of Proceeds

Based on the minimum price, total gross proceeds are expected at about US$472.2m (or RM1.68b).

Proceeds can be partially utilised to fund current expansion plans in Malaysia and/or working capital.

Source: GENM, UOB Kay Hian

SOTP VALUATION

(RMm)

NPV - Genting Highlands 19,469

UK 2,410

US Racino 1,832

Upstate NY -

GENHK Value 1,958

Net Cash/(Debt) 1,337

SOTP 27,005

Discount 0%

RNAV 27,005

Shares (m) 5,671

RNAV/share (RM) 4.76 Source: UOB Kay Hian

Tuesday , 12 May 2015

15 Refer to last page for important disclosures.

R e g i o n a l M o r n i n g N o t e s

PROFIT & LOSS Year to 31 Dec (RMm) 2014 2015F 2016F 2017F

Net turnover 8,229 8,657 9,589 10,082

EBITDA 2,248 2,403 2,764 3,021

Deprec. & amort. 608 625 791 838

EBIT 1,640 1,778 1,974 2,183

Associate contributions 0 0 0 0

Net interest income/(expense) (19) (37) (8) 31

Pre-tax profit 1,525 1,741 1,966 2,214

Tax (384) (348) (492) (554)

Minorities 0 0 0 0

Net profit 1,140 1,393 1,475 1,661

Net profit (adj.) 1,236 1,393 1,475 1,661

BALANCE SHEET Year to 31 Dec (RMm) 2014 2015F 2016F 2017F

Fixed assets 7,426 8,109 8,276 8,245

Other LT assets 8,390 8,390 8,390 8,390

Cash/ST investment 2,770 3,096 4,098 5,403

Other current assets 2,210 2,252 2,315 2,361

Total assets 20,797 21,848 23,079 24,399

ST debt 251 251 251 251

Other current liabilities 2,001 2,021 2,126 2,192

LT debt 1,411 1,411 1,411 1,411

Other LT liabilities 860 860 860 860

Shareholders' equity 16,304 17,336 18,461 19,715

Minority interest (31) (31) (31) (31)

Total liabilities & equity 20,797 21,848 23,079 24,399

CASH FLOW Year to 31 Dec (RMm) 2014 2015F 2016F 2017F

Operating 1,541 2,056 2,343 2,521

Pre-tax profit 1,525 1,741 1,966 2,214

Tax (455) (348) (492) (554)

Deprec. & amort. 608 625 791 838

Associates 0 0 0 0

Working capital changes (61) 39 78 22

Other operating cashflows (76) 0 0 0

Investing (2,055) (1,500) (1,000) (800)

Capex (growth) (1,888) (1,500) (1,000) (800)

Investments 0 0 0 0

Proceeds from sale of assets 0 0 0 0

Others (167) 0 0 0

Financing (532) (371) (369) (415)

Dividend payments (391) (371) (369) (415)

Issue of shares 0 0 0 0

Proceeds from borrowings 0 0 0 0

Loan repayment (124) 0 0 0

Others/interest paid (17) 0 0 0

Net cash inflow (outflow) (1,046) 185 975 1,305

Beginning cash & cash equivalent 3,720 2,770 2,955 3,930

Changes due to forex impact 96 0 0 0

Ending cash & cash equivalent 2,770 2,955 3,930 5,235

KEY METRICS Year to 31 Dec (%) 2014 2015F 2016F 2017F

Profitability EBITDA margin 27.3 27.8 28.8 30.0

Pre-tax margin 18.5 20.1 20.5 22.0

Net margin 13.9 16.1 15.4 16.5

ROA 5.6 6.5 6.5 7.0

ROE 7.2 8.3 8.2 8.7

Growth

Turnover (1.2) 5.2 10.8 5.1

EBITDA (6.7) 6.9 15.0 9.3

Pre-tax profit (13.7) 14.2 12.9 12.6

Net profit (28.0) 22.2 5.9 12.6

Net profit (adj.) (26.3) 12.7 5.9 12.6

EPS (26.3) 12.7 5.9 12.6

Leverage

Debt to total capital 9.3 8.8 8.3 7.8

Debt to equity 10.2 9.6 9.0 8.4

Net debt/(cash) to equity (6.8) (7.5) (12.3) (18.2)

Interest cover (x) 115.9 65.1 359.1 n.a.

Tuesday , 12 May 2015

16 Refer to last page for important disclosures.

R e g i o n a l M o r n i n g N o t e s

SECTOR UPDATE

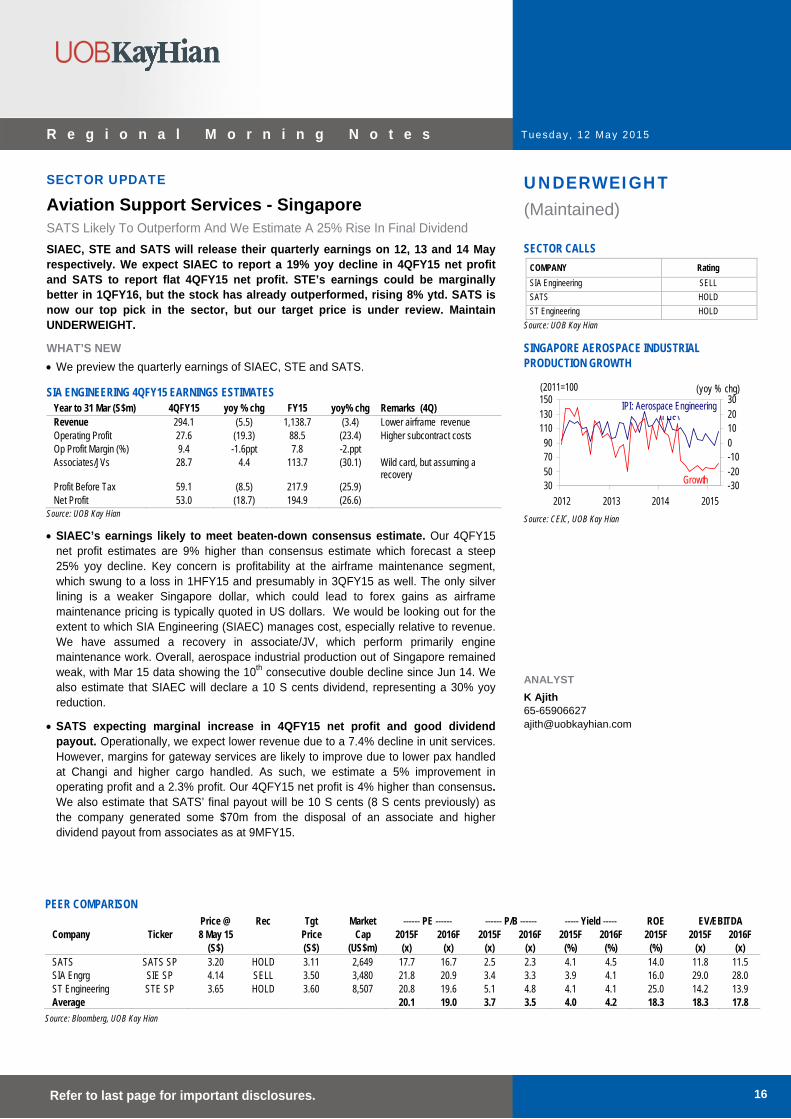

Aviation Support Services - Singapore SATS Likely To Outperform And We Estimate A 25% Rise In Final Dividend

SIAEC, STE and SATS will release their quarterly earnings on 12, 13 and 14 May respectively. We expect SIAEC to report a 19% yoy decline in 4QFY15 net profit and SATS to report flat 4QFY15 net profit. STE’s earnings could be marginally better in 1QFY16, but the stock has already outperformed, rising 8% ytd. SATS is now our top pick in the sector, but our target price is under review. Maintain UNDERWEIGHT.

WHAT’S NEW

We preview the quarterly earnings of SIAEC, STE and SATS.

SIA ENGINEERING 4QFY15 EARNINGS ESTIMATES Year to 31 Mar (S$m) 4QFY15 yoy % chg FY15 yoy% chg Remarks (4Q) Revenue 294.1 (5.5) 1,138.7 (3.4) Lower airframe revenue Operating Profit 27.6 (19.3) 88.5 (23.4) Higher subcontract costs Op Profit Margin (%) 9.4 -1.6ppt 7.8 -2.ppt Associates/JVs 28.7 4.4 113.7 (30.1) Wild card, but assuming a

recovery Profit Before Tax 59.1 (8.5) 217.9 (25.9) Net Profit 53.0 (18.7) 194.9 (26.6)

Source: UOB Kay Hian

SIAEC’s earnings likely to meet beaten-down consensus estimate. Our 4QFY15 net profit estimates are 9% higher than consensus estimate which forecast a steep 25% yoy decline. Key concern is profitability at the airframe maintenance segment, which swung to a loss in 1HFY15 and presumably in 3QFY15 as well. The only silver lining is a weaker Singapore dollar, which could lead to forex gains as airframe maintenance pricing is typically quoted in US dollars. We would be looking out for the extent to which SIA Engineering (SIAEC) manages cost, especially relative to revenue. We have assumed a recovery in associate/JV, which perform primarily engine maintenance work. Overall, aerospace industrial production out of Singapore remained weak, with Mar 15 data showing the 10th consecutive double decline since Jun 14. We also estimate that SIAEC will declare a 10 S cents dividend, representing a 30% yoy reduction.

SATS expecting marginal increase in 4QFY15 net profit and good dividend payout. Operationally, we expect lower revenue due to a 7.4% decline in unit services. However, margins for gateway services are likely to improve due to lower pax handled at Changi and higher cargo handled. As such, we estimate a 5% improvement in operating profit and a 2.3% profit. Our 4QFY15 net profit is 4% higher than consensus. We also estimate that SATS’ final payout will be 10 S cents (8 S cents previously) as the company generated some $70m from the disposal of an associate and higher dividend payout from associates as at 9MFY15.

UNDERWEIGHT (Maintained) SECTOR CALLS

COMPANY Rating

SIA Engineering SELL

SATS HOLD

ST Engineering HOLD

Source: UOB Kay Hian

SINGAPORE AEROSPACE INDUSTRIAL PRODUCTION GROWTH

30507090

110130150

2012 2013 2014 2015

-30-20-100102030

(2011=100 (yoy % chg)

IPI: Aerospace Engineering (LHS)

Growth

Source: CEIC, UOB Kay Hian ANALYST

K Ajith 65-65906627 [email protected]

PEER COMPARISON Price @ Rec Tgt Market ------ PE ------ ------ P/B ------ ----- Yield ----- ROE EV/EBITDA Company Ticker 8 May 15 Price Cap 2015F 2016F 2015F 2016F 2015F 2016F 2015F 2015F 2016F (S$) (S$) (US$m) (x) (x) (x) (x) (%) (%) (%) (x) (x) SATS SATS SP 3.20 HOLD 3.11 2,649 17.7 16.7 2.5 2.3 4.1 4.5 14.0 11.8 11.5 SIA Engrg SIE SP 4.14 SELL 3.50 3,480 21.8 20.9 3.4 3.3 3.9 4.1 16.0 29.0 28.0 ST Engineering STE SP 3.65 HOLD 3.60 8,507 20.8 19.6 5.1 4.8 4.1 4.1 25.0 14.2 13.9 Average 20.1 19.0 3.7 3.5 4.0 4.2 18.3 18.3 17.8

Source: Bloomberg, UOB Kay Hian

Tuesday , 12 May 2015

17 Refer to last page for important disclosures.

R e g i o n a l M o r n i n g N o t e s

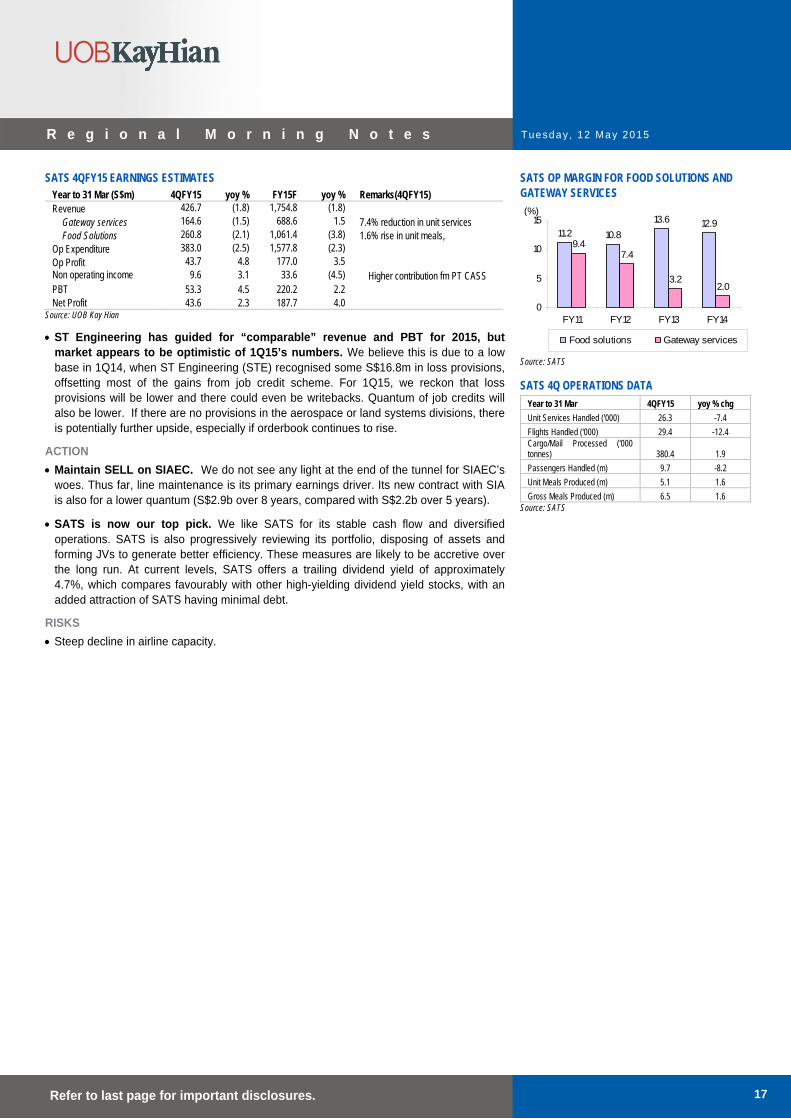

SATS 4QFY15 EARNINGS ESTIMATES Year to 31 Mar (S$m) 4QFY15 yoy % FY15F yoy % Remarks(4QFY15) Revenue 426.7 (1.8) 1,754.8 (1.8)

Gateway services 164.6 (1.5) 688.6 1.5 7.4% reduction in unit services Food Solutions 260.8 (2.1) 1,061.4 (3.8) 1.6% rise in unit meals,

Op Expenditure 383.0 (2.5) 1,577.8 (2.3) Op Profit 43.7 4.8 177.0 3.5 Non operating income 9.6 3.1 33.6 (4.5) Higher contribution fm PT CASS PBT 53.3 4.5 220.2 2.2 Net Profit 43.6 2.3 187.7 4.0

Source: UOB Kay Hian

ST Engineering has guided for “comparable” revenue and PBT for 2015, but market appears to be optimistic of 1Q15’s numbers. We believe this is due to a low base in 1Q14, when ST Engineering (STE) recognised some S$16.8m in loss provisions, offsetting most of the gains from job credit scheme. For 1Q15, we reckon that loss provisions will be lower and there could even be writebacks. Quantum of job credits will also be lower. If there are no provisions in the aerospace or land systems divisions, there is potentially further upside, especially if orderbook continues to rise.

ACTION

Maintain SELL on SIAEC. We do not see any light at the end of the tunnel for SIAEC’s woes. Thus far, line maintenance is its primary earnings driver. Its new contract with SIA is also for a lower quantum (S$2.9b over 8 years, compared with S$2.2b over 5 years).

SATS is now our top pick. We like SATS for its stable cash flow and diversified operations. SATS is also progressively reviewing its portfolio, disposing of assets and forming JVs to generate better efficiency. These measures are likely to be accretive over the long run. At current levels, SATS offers a trailing dividend yield of approximately 4.7%, which compares favourably with other high-yielding dividend yield stocks, with an added attraction of SATS having minimal debt.

RISKS

Steep decline in airline capacity.

SATS OP MARGIN FOR FOOD SOLUTIONS AND GATEWAY SERVICES

11.2 10.812.9

9.47.4

3.22.0

13.6

0

5

10

15

FY11 FY12 FY13 FY14

Food solutions Gateway services

(%)

Source: SATS

SATS 4Q OPERATIONS DATA

Year to 31 Mar 4QFY15 yoy % chg

Unit Services Handled ('000) 26.3 -7.4

Flights Handled ('000) 29.4 -12.4 Cargo/Mail Processed ('000 tonnes) 380.4 1.9

Passengers Handled (m) 9.7 -8.2

Unit Meals Produced (m) 5.1 1.6

Gross Meals Produced (m) 6.5 1.6 Source: SATS

Tuesday , 12 May 2015

18 Refer to last page for important disclosures.

R e g i o n a l M o r n i n g N o t e s

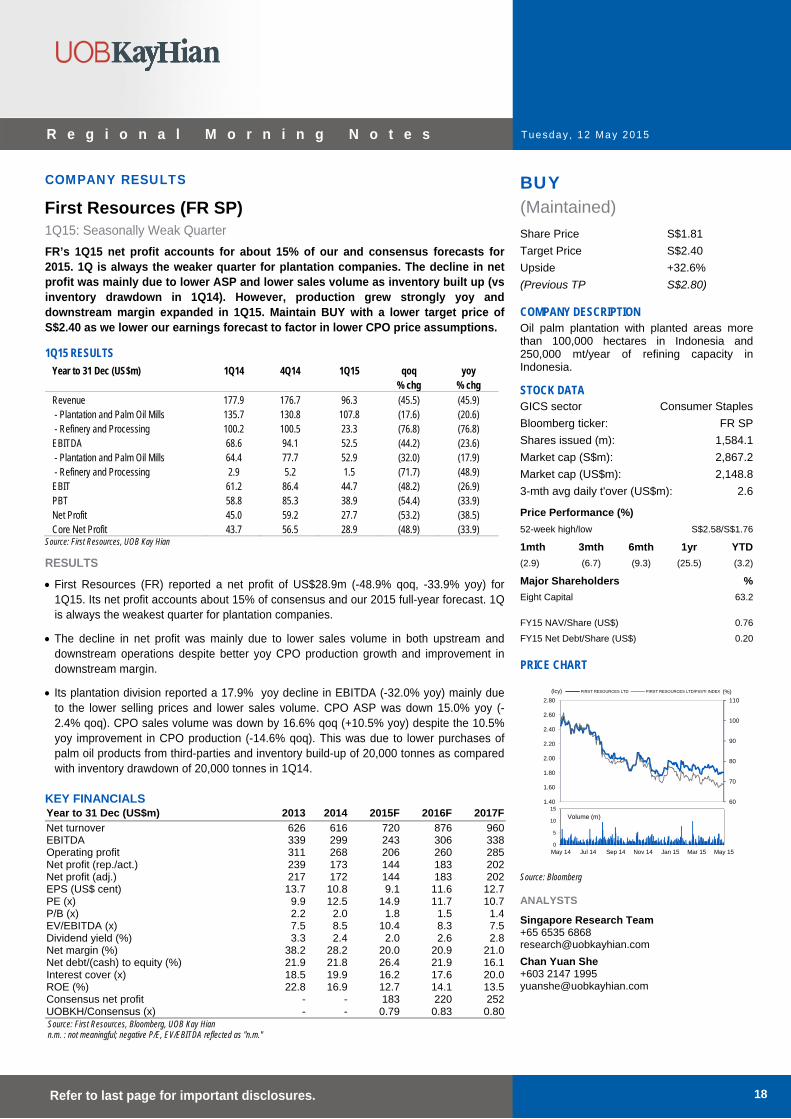

COMPANY RESULTS BUY

(Maintained)

Share Price S$1.81

Target Price S$2.40

Upside +32.6%

(Previous TP S$2.80)

COMPANY DESCRIPTION Oil palm plantation with planted areas more than 100,000 hectares in Indonesia and 250,000 mt/year of refining capacity in Indonesia.

STOCK DATA GICS sector Consumer Staples

Bloomberg ticker: FR SP

Shares issued (m): 1,584.1

Market cap (S$m): 2,867.2

Market cap (US$m): 2,148.8

3-mth avg daily t'over (US$m): 2.6

Price Performance (%) 52-week high/low S$2.58/S$1.76

1mth 3mth 6mth 1yr YTD

(2.9) (6.7) (9.3) (25.5) (3.2)

Major Shareholders %

Eight Capital 63.2

FY15 NAV/Share (US$) 0.76

FY15 Net Debt/Share (US$) 0.20

PRICE CHART

60

70

80

90

100

110

1.40

1.60

1.80

2.00

2.20

2.40

2.60

2.80

(%)(lcy) FIRST RESOURCES LTD FIRST RESOURCES LTD/FSSTI INDEX

0

5

10

15

May 14 Jul 14 Sep 14 Nov 14 Jan 15 Mar 15 May 15

Volume (m)

Source: Bloomberg

ANALYSTS

Singapore Research Team+65 6535 6868 [email protected] Chan Yuan She +603 2147 1995 [email protected]

First Resources (FR SP)

1Q15: Seasonally Weak Quarter

FR’s 1Q15 net profit accounts for about 15% of our and consensus forecasts for 2015. 1Q is always the weaker quarter for plantation companies. The decline in net profit was mainly due to lower ASP and lower sales volume as inventory built up (vs inventory drawdown in 1Q14). However, production grew strongly yoy and downstream margin expanded in 1Q15. Maintain BUY with a lower target price of S$2.40 as we lower our earnings forecast to factor in lower CPO price assumptions.

1Q15 RESULTS

Year to 31 Dec (US$m) 1Q14 4Q14 1Q15 qoq yoy % chg % chg Revenue 177.9 176.7 96.3 (45.5) (45.9) - Plantation and Palm Oil Mills 135.7 130.8 107.8 (17.6) (20.6) - Refinery and Processing 100.2 100.5 23.3 (76.8) (76.8) EBITDA 68.6 94.1 52.5 (44.2) (23.6) - Plantation and Palm Oil Mills 64.4 77.7 52.9 (32.0) (17.9) - Refinery and Processing 2.9 5.2 1.5 (71.7) (48.9) EBIT 61.2 86.4 44.7 (48.2) (26.9) PBT 58.8 85.3 38.9 (54.4) (33.9) Net Profit 45.0 59.2 27.7 (53.2) (38.5) Core Net Profit 43.7 56.5 28.9 (48.9) (33.9)

Source: First Resources, UOB Kay Hian

RESULTS

First Resources (FR) reported a net profit of US$28.9m (-48.9% qoq, -33.9% yoy) for 1Q15. Its net profit accounts about 15% of consensus and our 2015 full-year forecast. 1Q is always the weakest quarter for plantation companies.

The decline in net profit was mainly due to lower sales volume in both upstream and downstream operations despite better yoy CPO production growth and improvement in downstream margin.

Its plantation division reported a 17.9% yoy decline in EBITDA (-32.0% yoy) mainly due to the lower selling prices and lower sales volume. CPO ASP was down 15.0% yoy (-2.4% qoq). CPO sales volume was down by 16.6% qoq (+10.5% yoy) despite the 10.5% yoy improvement in CPO production (-14.6% qoq). This was due to lower purchases of palm oil products from third-parties and inventory build-up of 20,000 tonnes as compared with inventory drawdown of 20,000 tonnes in 1Q14.

KEY FINANCIALS Year to 31 Dec (US$m) 2013 2014 2015F 2016F 2017F

Net turnover 626 616 720 876 960EBITDA 339 299 243 306 338Operating profit 311 268 206 260 285Net profit (rep./act.) 239 173 144 183 202Net profit (adj.) 217 172 144 183 202EPS (US$ cent) 13.7 10.8 9.1 11.6 12.7PE (x) 9.9 12.5 14.9 11.7 10.7P/B (x) 2.2 2.0 1.8 1.5 1.4EV/EBITDA (x) 7.5 8.5 10.4 8.3 7.5Dividend yield (%) 3.3 2.4 2.0 2.6 2.8Net margin (%) 38.2 28.2 20.0 20.9 21.0Net debt/(cash) to equity (%) 21.9 21.8 26.4 21.9 16.1Interest cover (x) 18.5 19.9 16.2 17.6 20.0ROE (%) 22.8 16.9 12.7 14.1 13.5Consensus net profit - - 183 220 252UOBKH/Consensus (x) - - 0.79 0.83 0.80Source: First Resources, Bloomberg, UOB Kay Hian n.m. : not meaningful; negative P/E, EV/EBITDA reflected as "n.m."

Tuesday , 12 May 2015

19 Refer to last page for important disclosures.

R e g i o n a l M o r n i n g N o t e s

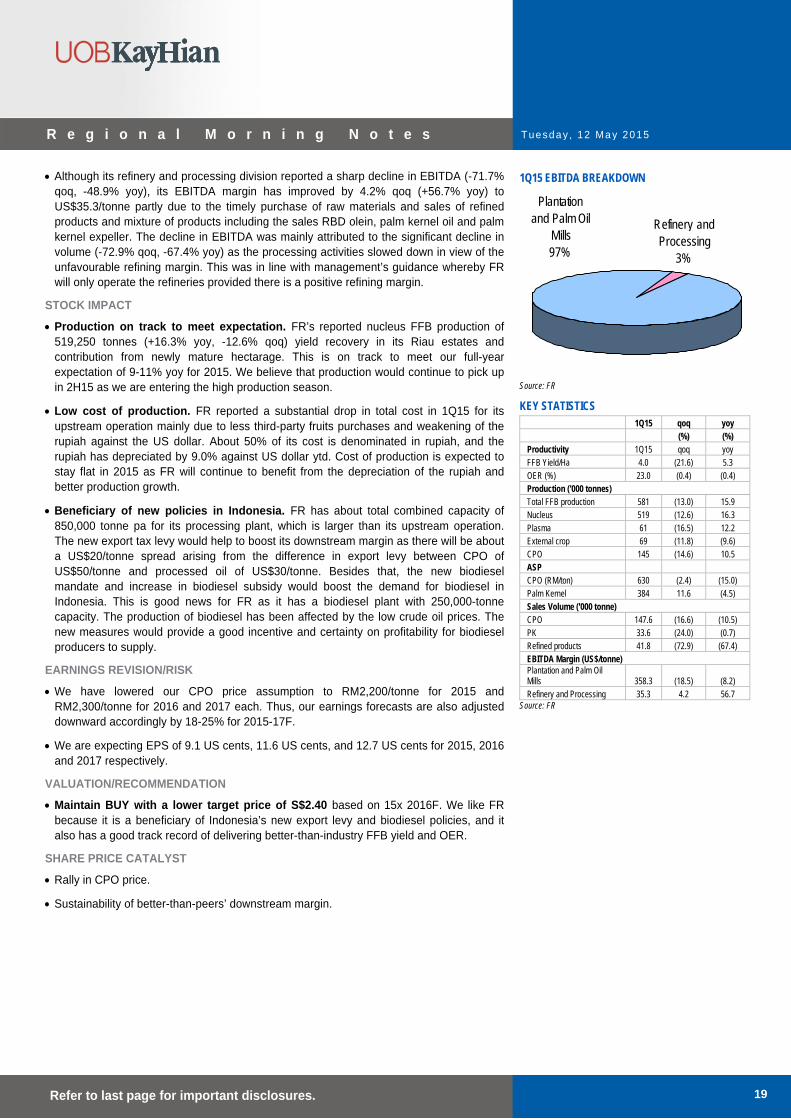

Although its refinery and processing division reported a sharp decline in EBITDA (-71.7% qoq, -48.9% yoy), its EBITDA margin has improved by 4.2% qoq (+56.7% yoy) to US$35.3/tonne partly due to the timely purchase of raw materials and sales of refined products and mixture of products including the sales RBD olein, palm kernel oil and palm kernel expeller. The decline in EBITDA was mainly attributed to the significant decline in volume (-72.9% qoq, -67.4% yoy) as the processing activities slowed down in view of the unfavourable refining margin. This was in line with management’s guidance whereby FR will only operate the refineries provided there is a positive refining margin.

STOCK IMPACT

Production on track to meet expectation. FR’s reported nucleus FFB production of 519,250 tonnes (+16.3% yoy, -12.6% qoq) yield recovery in its Riau estates and contribution from newly mature hectarage. This is on track to meet our full-year expectation of 9-11% yoy for 2015. We believe that production would continue to pick up in 2H15 as we are entering the high production season.

Low cost of production. FR reported a substantial drop in total cost in 1Q15 for its upstream operation mainly due to less third-party fruits purchases and weakening of the rupiah against the US dollar. About 50% of its cost is denominated in rupiah, and the rupiah has depreciated by 9.0% against US dollar ytd. Cost of production is expected to stay flat in 2015 as FR will continue to benefit from the depreciation of the rupiah and better production growth.

Beneficiary of new policies in Indonesia. FR has about total combined capacity of 850,000 tonne pa for its processing plant, which is larger than its upstream operation. The new export tax levy would help to boost its downstream margin as there will be about a US$20/tonne spread arising from the difference in export levy between CPO of US$50/tonne and processed oil of US$30/tonne. Besides that, the new biodiesel mandate and increase in biodiesel subsidy would boost the demand for biodiesel in Indonesia. This is good news for FR as it has a biodiesel plant with 250,000-tonne capacity. The production of biodiesel has been affected by the low crude oil prices. The new measures would provide a good incentive and certainty on profitability for biodiesel producers to supply.

EARNINGS REVISION/RISK

We have lowered our CPO price assumption to RM2,200/tonne for 2015 and RM2,300/tonne for 2016 and 2017 each. Thus, our earnings forecasts are also adjusted downward accordingly by 18-25% for 2015-17F.

We are expecting EPS of 9.1 US cents, 11.6 US cents, and 12.7 US cents for 2015, 2016 and 2017 respectively.

VALUATION/RECOMMENDATION

Maintain BUY with a lower target price of S$2.40 based on 15x 2016F. We like FR because it is a beneficiary of Indonesia’s new export levy and biodiesel policies, and it also has a good track record of delivering better-than-industry FFB yield and OER.

SHARE PRICE CATALYST

Rally in CPO price.

Sustainability of better-than-peers’ downstream margin.

1Q15 EBITDA BREAKDOWN

Refinery and Processing

3%

Plantation and Palm Oil

Mills97%

Source: FR

KEY STATISTICS 1Q15 qoq yoy (%) (%) Productivity 1Q15 qoq yoy FFB Yield/Ha 4.0 (21.6) 5.3 OER (%) 23.0 (0.4) (0.4) Production ('000 tonnes) Total FFB production 581 (13.0) 15.9 Nucleus 519 (12.6) 16.3 Plasma 61 (16.5) 12.2 External crop 69 (11.8) (9.6) CPO 145 (14.6) 10.5 ASP CPO (RM/ton) 630 (2.4) (15.0) Palm Kernel 384 11.6 (4.5) Sales Volume ('000 tonne) CPO 147.6 (16.6) (10.5) PK 33.6 (24.0) (0.7) Refined products 41.8 (72.9) (67.4) EBITDA Margin (US$/tonne) Plantation and Palm Oil Mills 358.3 (18.5) (8.2) Refinery and Processing 35.3 4.2 56.7

Source: FR

Tuesday , 12 May 2015

20 Refer to last page for important disclosures.

R e g i o n a l M o r n i n g N o t e s

PROFIT & LOSS Year to 31 Dec (US$m) 2014 2015F 2016F 2017F

Net turnover 616 720 876 960

EBITDA 299 243 306 338

Deprec. & amort. 31 37 45 53

EBIT 268 206 260 285

Total other non-operating income (3) 0 0 0

Net interest income/(expense) (15) (15) (17) (17)

Pre-tax profit 252 191 243 268

Tax (71) (41) (52) (58)

Minorities (7) (6) (8) (8)

Net profit 173 144 183 202

Net profit (adj.) 172 144 183 202

BALANCE SHEET Year to 31 Dec (US$m) 2014 2015F 2016F 2017F

Fixed assets 338 426 517 600

Other LT assets 1,185 1,295 1,354 1,421

Cash/ST investment 351 288 328 401

Other current assets 124 182 212 228

Total assets 1,998 2,191 2,411 2,650

ST debt 11 12 13 14

Other current liabilities 77 83 89 92

LT debt 572 595 619 644

Other LT liabilities 222 235 246 259

Shareholders' equity 1,063 1,207 1,390 1,591

Minority interest 53 59 54 51

Total liabilities & equity 1,998 2,191 2,411 2,650

CASH FLOW Year to 31 Dec (US$m) 2014 2015F 2016F 2017F

Operating 223 120 195 234

Pre-tax profit 252 191 243 268

Tax (77) (41) (52) (58)

Deprec. & amort. 31 37 45 53

Working capital changes 15 (52) (24) (13)

Other operating cashflows 2 (15) (17) (17)

Investing (215) (130) (150) (150)

Capex (growth) (71) (130) (150) (150)

Investments 0 0 0 0

Proceeds from sale of assets 0 0 0 0

Others (143) 0 0 0

Financing 43 7 (5) (11)

Dividend payments (58) (43) (55) (61)

Issue of shares 0 0 0 0

Proceeds from borrowings 122 100 100 100

Loan repayment 0 (50) (50) (50)

Others/interest paid (22) 0 0 0

Net cash inflow (outflow) 51 (4) 40 73

Beginning cash & cash equivalent 299 291 288 328

Changes due to forex impact 1 0 0 0

Ending cash & cash equivalent 351 288 328 401

KEY METRICS Year to 31 Dec (%) 2014 2015F 2016F 2017F

Profitability EBITDA margin 48.5 33.7 34.9 35.3

Pre-tax margin 40.9 26.6 27.7 27.9

Net margin 28.2 20.0 20.9 21.0

ROA 9.2 6.9 8.0 8.0

ROE 16.9 12.7 14.1 13.5

Growth Turnover (1.8) 17.0 21.7 9.5

EBITDA (11.9) (18.7) 25.8 10.7

Pre-tax profit (19.7) (24.1) 27.0 10.2

Net profit (27.5) (16.8) 27.0 10.2

Net profit (adj.) (20.9) (15.9) 27.0 10.2

EPS (20.9) (15.9) 27.0 10.2

Leverage Debt to total capital 34.3 32.4 30.4 28.6

Debt to equity 54.8 50.3 45.5 41.3

Net debt/(cash) to equity 21.8 26.4 21.9 16.1

Interest cover (x) 19.9 16.2 17.6 20.0

Tuesday , 12 May 2015

21 Refer to last page for important disclosures.

R e g i o n a l M o r n i n g N o t e s

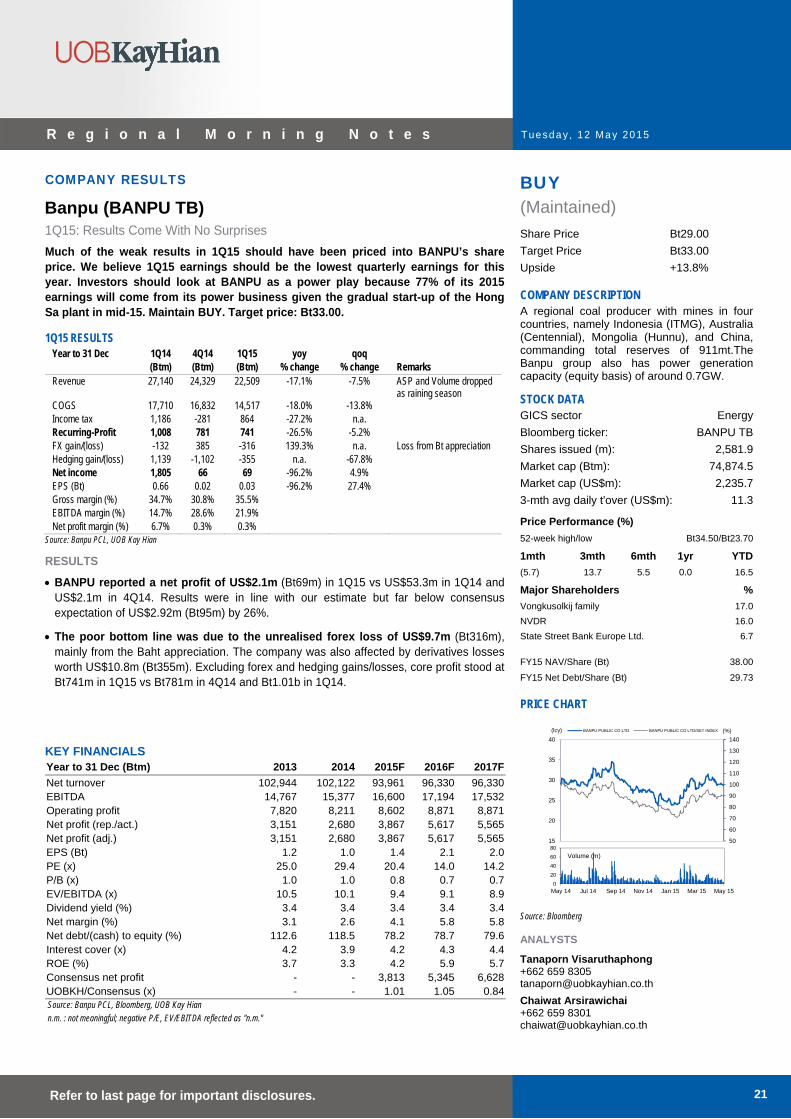

COMPANY RESULTS BUY

(Maintained)

Share Price Bt29.00

Target Price Bt33.00

Upside +13.8%

COMPANY DESCRIPTION A regional coal producer with mines in four countries, namely Indonesia (ITMG), Australia (Centennial), Mongolia (Hunnu), and China, commanding total reserves of 911mt.The Banpu group also has power generation capacity (equity basis) of around 0.7GW.

STOCK DATA GICS sector Energy

Bloomberg ticker: BANPU TB

Shares issued (m): 2,581.9

Market cap (Btm): 74,874.5

Market cap (US$m): 2,235.7

3-mth avg daily t'over (US$m): 11.3

Price Performance (%) 52-week high/low Bt34.50/Bt23.70

1mth 3mth 6mth 1yr YTD

(5.7) 13.7 5.5 0.0 16.5

Major Shareholders %

Vongkusolkij family 17.0

NVDR 16.0

State Street Bank Europe Ltd. 6.7

FY15 NAV/Share (Bt) 38.00

FY15 Net Debt/Share (Bt) 29.73

PRICE CHART

50

60

70

80

90

100

110

120

130

140

15

20

25

30

35

40

(%)(lcy) BANPU PUBLIC CO LTD BANPU PUBLIC CO LTD/SET INDEX

0

20

40

60

80

May 14 Jul 14 Sep 14 Nov 14 Jan 15 Mar 15 May 15

Volume (m)

Source: Bloomberg

ANALYSTS

Tanaporn Visaruthaphong +662 659 8305 [email protected] Chaiwat Arsirawichai +662 659 8301 [email protected]

Banpu (BANPU TB)

1Q15: Results Come With No Surprises

Much of the weak results in 1Q15 should have been priced into BANPU’s share price. We believe 1Q15 earnings should be the lowest quarterly earnings for this year. Investors should look at BANPU as a power play because 77% of its 2015 earnings will come from its power business given the gradual start-up of the Hong Sa plant in mid-15. Maintain BUY. Target price: Bt33.00.

1Q15 RESULTS Year to 31 Dec 1Q14 4Q14 1Q15 yoy qoq (Btm) (Btm) (Btm) % change % change Remarks Revenue 27,140 24,329 22,509 -17.1% -7.5% ASP and Volume dropped