Embed Size (px)

Citation preview

Forthcoming: Journal of Forecasting

Regression-based Modeling of Market Option Prices: with Application to S&P500 Options

Gurupdesh Pandher∗

Revised Version: September 2006

Abstract

This paper presents a simple empirical approach to modeling and forecasting market option prices using localized option regressions (LOR). LOR projects market option prices over localized regions of their state space and is robust to assumptions regarding the underlying asset dynamics (e.g. log-normality) and volatility structure. Our empirical study using three years of daily S&P500 options shows that LOR yields smaller out-of-sample pricing errors (e.g. 32% one-day-out) relative to an efficient benchmark from the literature and produces option prices free of the volatility smile. In addition to being an efficient and robust option modeling and valuation tool for large option books, LOR provides a simple to implement empirical benchmark for evaluating more complex risk-neutral models. Keywords: option pricing, regression, volatility smile, S&P500. © All rights reserved. Please do not quote without author permission.

∗Address: Department of Finance, DePaul University, 1 East Jackson Boulevard, Chicago, IL 60604. Email: [email protected]; Phone: (312) 362-5915; Webpage: http://mozart.depaul.edu/~gpandher

1

I. INTRODUCTION

In their seminal work on option pricing, Black and Scholes (1973) and Merton

(1973) propose the risk-neutral valuation framework for identifying the equilibrium price

of a contingent claim. This methodology is based on the insight that, if the price risk of

the option can be dynamically hedged by trading in the underlying asset, then, to rule out

arbitrage, the hedged position must earn the same return as the risk-free security. Over

the past three decades, considerable research effort has gone into extending the initial

Black-Scholes-Merton framework by relaxing certain assumptions and incorporating

additional features in the asset return process (e.g. jumps, mean-reversion, stochastic

volatility). Relatively little progress has been reported, however, in the development of

empirical approaches to modeling market option prices.

This paper presents a relatively simple, but effective, empirical method for

modeling and predicting option prices based on localized option regressions (LOR)

where market option prices are projected over localized regions of their state space. The

method does not require assumptions regarding the asset price distribution (e.g. log-

normality), volatility structure and hedging behavior of risk-neutral models and offers a

robust data-driven method for valuing option books. While the LOR methodology may

appear deceptively simple, the empirical model and our surprising findings have not been

reported in the previous literature.

The LOR approach may be motivated by observing that how well risk-neutral

theory and models are able to explain actual market option prices depends on the extent

to which the assumptions and mechanics behind the risk-neutral arbitrage arguments hold

in actual markets. These include assumptions on the dynamics and probability

distribution of the underlying asset prices and the ability to efficiently hedge the option’s

price risk. The wide choice of available models, assumptions and estimation error in key

parameters implies that the relationship between option prices from theoretical models

2

and observed market prices is not unique and is necessarily approximate. LOR attempts

to empirically capture the relationship between market option prices and state variables

found to be important in risk-neutral option pricing theory.

Innovations in the derivatives literature following Black and Scholes (1973) and

Merton (1973) include the discrete risk-neutral framework of Cox, Ross and Rubinstein

(1979), jumps in the asset return process, deterministic volatility functions, stochastic

volatility, non-parametric estimation of option models and generalization using Levy

processes. The deterministic volatility approach adjusts the asset pricing lattice to

incorporate the volatility smile effect in market options (Derman & Kani (1994),

Rubinstein (1994)) while the jump, stochastic volatility and GARCH class of option

models attempt to theoretically address Black-Scholes anomalies like the ‘volatility

smile’ (Hull & White (1987), Heston (1993), Duan (1995), Bates (1996), Ritchen &

Trevor (1999), Duffie, Pan and Singleton (2000), Heston and Nandi (2000), Lehnert

(2003) and others). Carr and Lu (2004) use time-changed Levy processes to provide a

unified treatment of option pricing models where asset returns exhibit jumps, stochastic

volatility and correlations with volatility.

To evaluate the LOR model, we compare its performance with the efficient

Black-Scholes implementation of Dumas, Fleming and Whaley (1998) based on implied

volatility regressions. The literature also refers to their method as the “Practitioner

Black-Scholes” (PBS) model and it has become a common benchmark for evaluating new

models in the options literature. Using S&P500 options, Dumas, Fleming and Whaley

(1998) show that the PBS model compares favorably with binomial option models

calibrated using deterministic volatility functions (Derman and Kani (1994), Dupire

(1994) and Rubinstein (1994)). The PBS benchmark is also used by Heston and Nandi

(2000) to evaluate the performance of a closed-form GARCH option pricing model and

Christoffersen and Jacobs (2004) find that the PBS model with aligned loss functions

3

outperforms more complex models such as the stochastic volatility model of Heston

(1993).

A semi-nonparametric approach is employed by Ait-Sahalia and Lo (1998) where

implied volatility from kernel regressions is used in the Black-Scholes-Merton model to

determine option prices. The proposed LOR approach differs from both Ait-Sahalia and

Lo (1998) and Dumas, Fleming and Whaley (1998) in that it does not use Black-Scholes

or any other risk-neutral model to generate option prices. Instead, LOR is based on direct

projections of option prices onto their localized state space.

Our empirical study using three years of daily S&P500 index options (38,487

daily prices) shows that i) the LOR model yields significantly smaller in-sample and out-

of-sample pricing errors than the PBS implementation of Dumas, Fleming and Whaley

(1998) and ii) LOR options are largely free of the volatility smile effect. For example,

the one-day-out average pricing error (prediction RMSE) for LOR is $0.53 while it is

$0.70 for the PBS benchmark. Moreover, PBS pricing errors exceed LOR by 32.4%,

13.2% and 2.8% at one-day, two-day and three-day out-of-sample horizons, respectively

(see Table IV). Comparison with other studies using the same sample, such as Bakshi,

Cao and Chen (1997), further demonstrates that LOR is very competitive with stochastic

volatility models. We also find that the volatility smile is virtually non-existent in option

prices generated by the LOR approach (see Table VII and Figure 2).

An important practical implication of these results is that a relatively

straightforward econometric approach based on locally projecting option prices onto their

state process offers the potential of serving as an efficient alternative option

modeling/valuation tool, as well as a benchmark for evaluating the performance of more

complex structural risk-neutral models. Another attractive feature of the LOR approach

is its simplicity and ease of implementation. The localized regressions are much easier to

implement and use less data than the neural-networks approach to option valuation

4

proposed in Hutchinson, Lo and Poggio (1994), where two years of simulated daily

Black-Scholes prices on S&P500 futures are used to train the neural-network algorithm.

LOR methodology requires a much shorter estimation window and our empirical analysis

of Section IV provides very good results using a moving estimation window of 50 days.

We are not able to compare the empirical performance of LOR with the neural network

approach as the study of Hutchinson, Lo and Poggio (1994) is based on simulated data

and does not use market-traded option prices.

The paper is organized as follows. Section II introduces four candidate option

regression models and describes essential aspects of the LOR methodology including

localization to the option strike-maturity space, the out-of-sample forecasting procedure

and the benchmark PBS Black-Scholes model. The S&P500 options data is described in

Section III. The in-sample and out-of-sample performance of the models is reported in

Section IV along with an analysis of the volatility smile effect in LOR option prices. The

conclusion follows in Section V.

5

II. LOCALIZED OPTION REGRESSION MODELING

We begin by describing four candidate regression specifications that will serve as

the basic workhorse models for localized option regression (LOR) modeling. These

option regressions are sequentially localized to regions of the option state space based on

their maturity and strike price. The out-of-sample implementation of the LOR is also

described as it represents a natural pricing application where model parameters estimated

from recent options are used to estimate new option values.

A. Structural & Reduced-form Option Regressions

Let V represent the value of a given market-traded option (e.g. call, put) with

underlying asset price S (e.g. index, stock, currency, bond), time of option expiration T

(in trading days), strike price K , asset return volatility σ , and the risk-free interest rate

r . Further, tT −=τ is the option’s remaining time-to-maturity, where ],0[ Tt∈ is any

time up to option expiration.

We consider two classes of localized option regressions - structural and reduced-

form models – which locally project derivative prices on their state process based on the

underlying asset price, strike price, time-to-maturity, implied volatility and the risk-free

rate. The state space includes linear, quadratic and interaction terms arising among the

state variables. The structural specification models the option’s non-linear behavior

around the strike price through the “moneyness” variable KSm /= (ratio of the current

asset value to strike price), while the reduced-form specification models this directly in

terms of the strike price.

A number of specifications and functional forms were initially considered. To

make the presentation manageable, we narrow consideration to the four best performing

classes of reduced-form and structural option regression models. The first two models

project market options onto a linear and quadratic state-space of the state variables

6

( S ,τ , K , r ) using the reduced-form and structural specifications. The other two models

additionally include implied volatility IVσ as an additional predictor. For the purpose of

concreteness, an explicit representation of the four models is given below.

Reduced-form Model (RLOR):

ετααταατααατααααταααα

+++++++++++++++=

rKrKSrSSKrKSrKSV

14131211109

28

27

26

2543210 (1)

Structural Model (SLOR):

ετααταατααατααααταααα

+++++++++++++++=

rKrKmrmmKrKmrKmV

14131211109

28

27

26

2543210 (2)

Reduced-form Volatility Model (RLOR-V):

εσατσασασασασα

τααταατααατααααταααα

+++++++

++++++++++++++=

rKS

rKrKSrSSKrKSrKSV

IVIVIVIVIVIV 201918172

1615

14131211109

28

27

26

2543210

(3)

Structural Volatility Model (SLOR-V):

εσατσασασασασα

τααταατααατααααταααα

+++++++

++++++++++++++=

rKm

rKrKmrmmKrKmrKmV

IVIVIVIVIVIV 201918172

1615

14131211109

28

27

26

2543210

(4)

Initially, the complete models above with all quadratic and interaction terms were

considered1. In the empirical implementation, however, the statistical insignificance of

some coefficients leads to a reduction in model size (see Table III for estimates).

2Other functional forms were also investigated, including variants of (1)-(4) with logs of i) the dependent variable, ii) the independent variables and iii) both. The second set of models frequently lead to multicollinearty problems as the logged quadratic and interaction terms become linearly related to the main effects. Further, models where the dependent variable is the log-option price were found to be inferior to the simpler models with the option price as the dependent variable. For example, our analysis in Section IV.C identifies model (3) as the best specification. Its log-likelihood and deviance in the complete sample is -38,066 and 24,080, respectively, while the same for the log-option price is -51,817 and 63,136. While R-squares are not directly comparable, the adjusted R-square for model (3) is 0.9962 (see Table III) while the same for its log-price variant is 0.9532. Examination of alternative forms leads to the conclusion that the simple linear specification works best in terms of efficiency and pricing errors (these results are not reported in the interest of brevity).

7

For a more compact representation, if Z represents the (row) vector of

explanatory variables in (1)-(4), then the above option regressions may be generically

expressed as

εα += ZV (5)

where α is the parameter vector.

The option regressions with implied volatility (SLOR-V and RLOR-V) are

motivated by the importance of volatility in the Black-Scholes model. Implied volatility

is estimated numerically by inverting (6) on the market option price:

),,,,(1 στσ rKSBSIV−=

where )()(),,,,( στστ τ −−= − dNedSNrKSBS r (6)

is the Black-Scholes call option formula with ( ) σττσ )2/()/ln( 2++= rKSd .

For the volatility LOR models (3)-(4), a mechanism for estimating implied

volatility over the strike-maturity space is also required. This is done by adopting the

implied volatility estimation of Dumas, Fleming and Whaley (1998) and is further

discussed in Section B below.

B. Localized Option Regression (LOR) Modeling

In localized option regression modeling, models (1)-(4) are sequentially estimated

by maturity-moneyness clusters over a rolling estimation window (indexed by q ). This

estimation scheme reflects a natural valuation application of LOR where model

parameters estimated from recent market option data are used to price new options as

predicted values.

8

B.1 Localization

The localization of the option regressions (1)-(4) to sequential maturity-

moneyness clusters is represented generically by

εα += ),(),( cqZcqV (7)

where ),( cqV is the market price of an option with state variables Z in estimation period

q and maturity-moneyness cluster c and ),( cqα is the parameter vector.

Localization is defined by clusters formed from maturity-moneyness groups. Let

{ }piii ,...,1],,( 1 ==Τ +ττ represent option maturity groups with delineation points

pτττ <<< ...21 . Similarly, { }ljmm jj ,...,1],,( 1 ==Μ + represent option moneyness

groups with lmmm <<< ...21 . Thus, there are pl localized clusters formed by the

combinations Μ×Τ∈c .

There is, of course, some flexibility in the determination of the length of the

estimation window and localization clusters and some analysis is required to identify an

efficient delineation by balancing the trade-off between model fit and sample size

(however, this needs to be performed only once for a particular type of option and need

not be repeated in subsequent LOR applications). While increased localization may

improve the fit of the option regression in individual clusters, it also reduces the sample

size for estimating model parameters in each cluster. Since we are primarily interested in

the potential of LOR as a modeling and valuation tool, we focus on its out-of-sample

performance in determining the length of the estimation cycle and the localization

clusters. Here, over-fitting due to increased localization can lead to poor out-of-sample

performance.

Similar issues arise in the nonparametric option-pricing approach of Ait-Sahalia

and Lo (1998) where implied volatility is modeled using kernel regressions. Kernel

regressions provide a weighted average of observed values around a characteristic point

9

(e.g. ( S ,τ , K , r )), where more weight is given to points closer to the characteristic point.

The performance of the estimator is highly sensitive to the bandwidth of the kernel

density function. When the bandwidth is too small (relative to optimal), the estimator is

under-smoothed and exhibits high variance but low bias. Meanwhile, the estimator

becomes over-smoothed if the bandwidth is too high. In this case, its variance is low but

its bias increases.

Applying the LOR methodology of this Section (II) to the S&P500 options used

in our empirical study, we quickly identified an efficient localization based on two broad

moneyness groups ( { }]1.1,1(],1,9[.=Μ ), three maturity groups

( { }]367,100(],100,50(],50,7[T = ) and a moving estimation window of q =50 days (the

maximum maturity of options in our sample is 367 days). The efficient localization is

determined by evaluating the out-of-sample errors of LOR option prices under various

formulations of the moneyness-maturity groups (Μ and Τ ). Call options prices at

maturity exhibit a “hockey-stick” payoff centered at the moneyness value 1/ == KSm .

Our construction of the moneyess groups avoids the non-linearity resulting from this kink

by considering the following two candidate groupings: { }]1.1,1(],1,9[.=Μ and

{ }]1.1,05.1(],05.1,1(],1,95(.],95,.9[.=Μ . The second set leads to more refined localized

clusters for LOR modeling. Similarly, we considered coarser and more refined sets for

the maturity groups given by the following three sets: { }]367,100(],100,7[=Τ ,

{ }]367,100(],100,50(],50,7[=Τ and { }]367,200(],200,150(],150,100(],100,50(],50,7[=Τ .

[Table I about here]

One-day out-of-sample pricing errors generated by the six different combinations

of Μ and Τ are reported in Table 1 (generation of out-of-sample LOR option prices is

10

described in IV.E). Interestingly, greater localization does not necessarily decrease the

over-all pricing error due to over-fitting. For example, we find that the two moneyness

grouping based on 10% intervals for the moneyness variable KSm /= yield better

performance (1, 2 and 3 days out) than refinement to four groupings separated by

intervals of 5%. The lowest pricing errors occur for the localization based on

{ }]1.1,1(],1,9[.=Μ and { }]367,100(],100,50(],50,7[=Τ . We select these moneyess-

maturity sets to define our efficient localization for the empirical study of Section IV.

B.2 Implied Volatility Forecasting

The first step in determining new option prices using the LOR method involves

estimating and identifying the best LOR model from the candidates (1)-(4). If either of

the volatility models RLOR-V (3) or SLOR-V (4) are selected, then the regressor state

space also includes implied volatility IVσ in addition to ),,,( rKS τ . In this case, an

estimate of volatility in the out-of-sample period is required. A method for doing this is

described next before considering the estimation of out-of-sample LOR option prices.

Volatility estimates are obtained from the implied volatility regressions proposed

by Dumas, Fleming and Whaley (1998, DFW). They model the relationship between

implied volatility and the option’s strike and maturity over recent market prices and use

the estimated volatilities to obtain Black-Scholes option values in the out-of-sample

period. Among the various volatility regressions analyzed by DFW, the best candidate is

identified as

ετβτβτββββσ ++++++= KKKIV 52

432

210 . (8)

Let d represent the sample period (e.g. day, week) over which the implied

volatility regression will be estimated (note that d is much smaller than the rolling

11

estimation window q used in LOR modeling). Therefore, the parameters of the implied

volatility regressions may be represented as

ετβτβ

τββββσ

+++

+++=

Kdd

dKdKdddIV

)()(

)()()()()(

52

4

32

210 , qd ∈ , (9)

for each period d . As done in a number of other studies (e.g. Dumas, Fleming and

Whaley (1998), Christoffersen and Jacobs (2004)), we select the estimation period d for

the volatility regression (9) to be one trading day. This means that in determining the n -

day out-of-sample option prices, volatility parameter estimates from day nd − are used

to predict implied volatilities in day d (we used “day” for “period” without any loss of

generality).

B.3 Out-of-Sample LOR Option Pricing

We now consider the use of LOR as an option valuation tool where parameters

estimated over a moving estimation window q are used to generate new option prices as

out-of-sample predictions. LOR option values in the subsequent period 1+q with state

variables ),,,,( IVrKS στ are generated as follows2:

1) No Volatility Case: If the LOR is model (1) or (2)

In this case, an estimate of volatility is not required. LOR option values in period

1+q and maturity-moneyness cluster c are then calculated as

),(),,,(),1;,,,( cqrKSZcqrKSV αττ =+ . (10)

where ),,,( rKSZ τ is the vector of corresponding LOR regressor variables and ),( cqα is

the corresponding parameter vector estimated from market options in the previous period

2Note that the state variables ),,,( rKS τ in the out-of-sample period (e.g. next trading day) are not forecasted and would be known for the option being priced at that moment. For example, at the beginning

12

q and maturity-moneyness cluster c . Similarly, if the LOR model is (2), the LOR

option value is calculated as

),(),,,(),1;,,,( cqrKmZcqrKmV αττ =+ . (11)

2) Volatility Case: If LOR is model (3) or (4)

i) Estimate the next day out-of-sample implied volatility for day nd + as

τβτβτβ

βββτσ

Kddd

KdKddndKIV

)()()(

)()()();,(

52

43

2210

+++

++=+ (12)

where the parameters ))(),(,)(),(),(),(()( 543210 ddddddd ββτβββββ = are estimated

by fitting the volatility regression (9) to implied option volatilities from day d .

ii) LOR out-of-sample option values in period 1+q and maturity-moneyness cluster c

are then obtained as follows:

)1;,( += dKIV τσσ , 11 +∈+ qd ,

RLOR-V model (3): ),(),,,,(),1;,,,,( cqrKSZcqrKSV αστστ =+ (13)

SLOR-V model (4): ),(),,,,(),1;,,,,( cqrKmZcqrKmV αστστ =+ (14)

where ),,,,( στ rKSZ and ),,,,( στ rKmZ are the vectors of LOR regressors according

to (3) and (4), respectively. The corresponding parameters ),( cqα are estimated from

options trading in period q and maturity-moneyness cluster c .

C. The PBS Black-Scholes Benchmark

As discussed earlier, to evaluate the pricing performance of LOR, we use the

efficient Black-Scholes implementation of DFW as a benchmark model. The literature

also refers to their methodology as the “Practitioner Black-Scholes” (PBS) model.

of the trading day in 1+q , the option strike price, stock price and remaining time-to-maturity are all know while the LOR parameter ),( cqα is estimated from the option data in the previous period q .

13

The critical issue for obtaining Black-Scholes option prices is how to infer

volatility across the spectrum of exercise prices and maturities. For this purpose, DFW

identify the best implied volatility regression as

ετβτβτββββσ ++++++= KKKIV 52

432

210 .

Volatility regression parameters estimated from recently observed market option prices

are then used to construct volatility estimates for out-of-sample Black-Scholes option

prices.

As in the case of LOR volatility estimation (9), we apply the DWF volatility

modeling to daily options and use the estimated parameters to predict next-day implied

volatility by strike price and maturity. For any give day d in the sample, the volatility

parameters are estimated from the regression (9).

With q representing the current LOR estimation period, the corresponding PBS

option value with state variables ),,,( rKS τ in the subsequent period 1+q is obtained as

follows:

i) Estimate the out-of-sample implied volatility for day nd + as

τβτβτβ

βββτσ

Kddd

KdKddndKIV

)()()(

)()()();,(

52

43

2210

+++

++=+ (15)

where the parameters ))(),(,)(),(),(),(()( 543210 ddddddd ββτβββββ = are estimated

by fitting the volatility regression (9) to implied option volatilities from day d .

ii) Calculate the Black-Scholes option values for day nd + as

);,( ndKIV += τσσ

)()()();,,,,( 1 στστ τ −−−=+ − dNedNPVDSndrKSPBS r (16)

where ( ) σττσ )2/()/ln( 21 ++= rKSd and PVDS − is the S&P500 index net of the

present value of dividends.

14

III. DATA

Our empirical analysis uses option prices on the S&P500 index options traded on

the Chicago Board of Options Exchange (CBOE). Options written on the S&P500 index

are the most actively traded European-style contracts. This data was selected due to the

high market liquidity of these options and their frequent use in earlier empirical studies.

S&P500 index options have been the focus of many investigations related to the

estimation and performance of option pricing models, risk-neutral densities and implied

volatility analysis (Lamoureux, Christopher and Lastrapes (1993), Heynen (1993), Bates

(1996), Bakshi, Cao and Chen (1997), Aït-Sahalia & Lo (1998), Dumas, Fleming and

Whaley (1998), Das and Sundaram (1999), Jackwerth (2000), Jacquier and Jarrow (2000)

and others).

In particular, Bakshi, Cao and Chen (1997) use a three year sample of daily call

option prices on the S&P500 index from June 1, 1988 to May 31, 1991 to evaluate the

performance of alternative option pricing models including Black-Scholes and extensions

with stochastic volatility, jumps and stochastic interest rates. We are thankful to Gurdip

Bakshi for graciously providing us with this data and its use in evaluating the LOR

methodology facilitates comparison of pricing errors and the volatility smile across

studies. Christoffersen and Jacobs (2004) also use the same sample of S&P500 options

to show that consistency in the choice of loss functions for estimation and evaluation

significantly improves the performance of option models. Their study excludes option

maturities that are less than 60 days and restricts options to be within 5% of being at-the-

money (total of 14,648 options). Our analysis uses a broader range of options with

maturities exceeding 7 days that are within 10% of being at-the-money (28,417 options).

A brief description of the option data is provided below and we refer to Bakshi,

Cao and Chen (1997) for complete details. Panel A of Table II reports the summary

statistics for variables related to daily closing S&P500 call options over the three year

15

sample and Panels B and C give option means and the number of options by moneyness-

maturity combinations.

[Insert Table II about here]

The intra-day bid-ask quotes for S&P500 call options are obtained from the

Berkeley Options Database. For the analysis, option prices are formed by taking the

average of the last reported bid-ask prices (prior to 3:00 pm, Central Standard Time) for

each day in the sample. The corresponding S&P500 index values are synchronous to the

closing option prices and the index series was carefully adjusted for dividend payments.

For the risk-free return, data on daily Treasury-bill bid and ask discounts is used with

maturities up to one year, as reported in the Wall Street Journal. Following convention,

an annualized interest rate was constructed by forming an average of bid-ask Treasury

Bill discounts.

16

IV. EMPIRICAL RESULTS

We now report the results from applying the localized option regression (LOR)

methodology and the efficient PBS Black-Scholes implementation described in Section II

to 28,417 daily market prices on S&P500 call options in the three year sample. Pricing

errors from LOR are also compared with the performance of the stochastic volatility and

jump models studied by Bakshi, Cao and Chen (1997) who use the same data3.

We proceed as follows in the empirical study. First, the best LOR model is

identified from the four structural and reduced-form specifications (1)-(4) described in

Section II. The gains from localization and an in-depth analysis of in-sample and out-of-

sample pricing performance for the selected LOR model are then presented in relation to

the PBS benchmark. Finally, we analyze the presence of the volatility smile effect in

option prices generated by the LOR and PBS models.

A. Main Findings

Before presenting the detailed analysis, the main findings are first summarized

below. Out of the four candidate option regressions, the reduced-form LOR specification

with implied volatility (RLOR-V) is selected as the best LOR model upon localization to

maturity-moneyness clusters. The corresponding LOR models without implied volatility

(RLOR and SLOR) also do relatively well and outperform the PBS benchmark.

RLOR-V yields smaller average pricing errors (RMSEs) both in-sample and out-

of-sample in comparison to the PBS benchmark. One-day out-of-sample pricing errors

are $0.53 and $0.69 for LOR and PBS, respectively (in-sample pricing errors are $0.25

and $0.48, respectively). Further, LOR pricing is more consistent across the whole

spectrum of moneyness and maturity groupings. Over one-day, two-day and three-day

3Christoffersen and Jacobs (2004) also use the same sample to show that the PBS Black-Scholes implementation of Dumas, Fleming and Whaley (1998) outperforms stochastic volatility models.

17

out-of-sample horizons, pricing errors of the PBS benchmark are higher than LOR by

32.4%, 13.2% and 2.8%, respectively. LOR modeling without implied volatility retains

much of its efficiency, providing an error reduction of 19%. Overall pricing errors from

LOR models without implied volatility, namely RLOR and SLOR, are $0.59 and $0.59,

respectively, while the same for the PBS is $0.70.

LOR also compares favorably with more sophisticated models with stochastic

volatility. Its overall pricing error ($0.53) is in the mid-point of error ranges for the

stochastic volatility model ($0.41-0.65) reported by Bakshi, Cao and Chen (1997) using

the same three year sample of S&P500 options. Lastly, we find that out-of-sample option

prices generated by the LOR model are free of the volatility smile/sneer effect while this

effect is present in PBS option prices.

B. Option Regressions without Localization

To study the incremental improvement from localization, we begin by reporting

the performance of the reduced-form and structural option regression models (1)-(4) on

the complete sample without localization to the six moneyness-maturity clusters of Table

I.

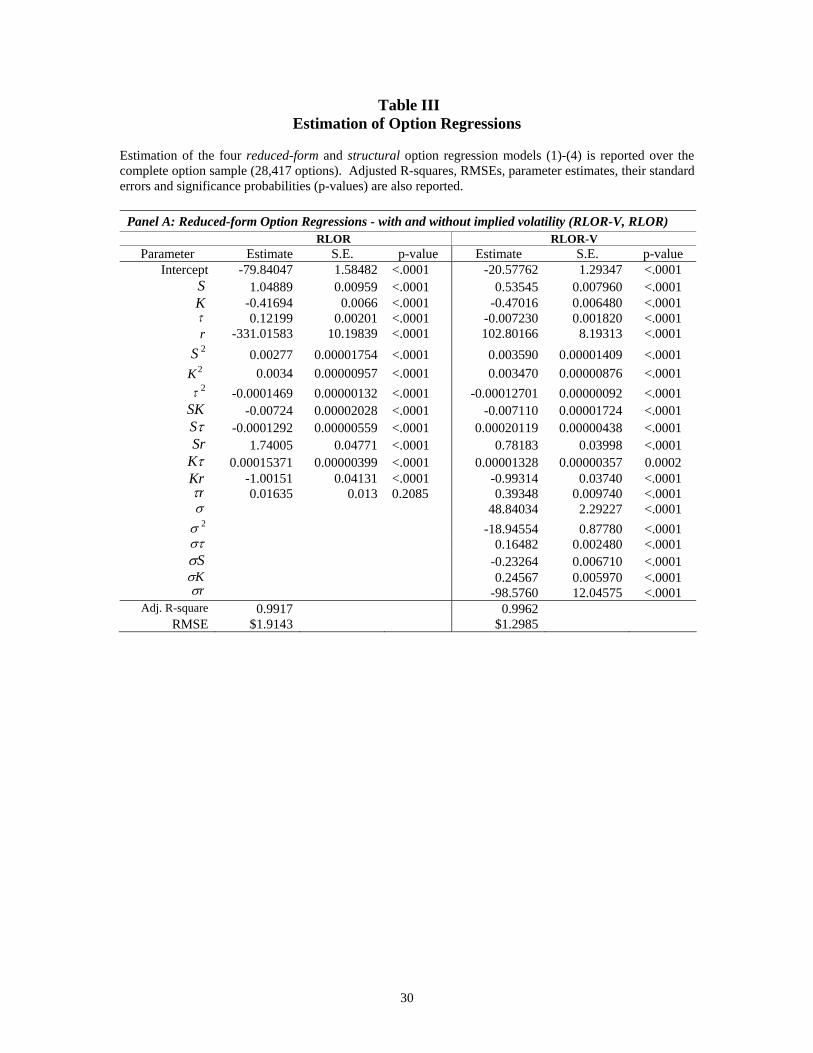

[Table III about here]

Panels A and B show that the fit of the four models, as implied by their R-squares,

is extremely high falling in the range 0.9873-0.9962. The average pricing errors of the

reduced-form models with respect to CBOE market prices (as measured by RMSE) are

uniformly lower than their structural counterparts. Pricing errors for the volatility models

are $1.30 and $1.63 for RLOR-V and SLOR-V, respectively. The same for the no-

volatility models rise to $1.91 and $2.20 for RSLOR and SLOR, respectively.

18

It appears from the global fit that option regressions with implied volatility as a

predictor have a distinct advantage. We see below that this continues to hold when

estimation is sequentially localized to maturity-moneyness clusters although the

difference narrows. Lastly, all parameter estimates reported in Tables III are highly

significant (with most significance probability or “p-values” less than .0001)4.

C. The Best LOR Model

We first identify the best LOR model among the volatility and no-volatility

reduced-form and structural candidates: RLOR (1), SLOR (2), RLOR-V (3), SLOR-V

(4). The in-sample and out-of-sample performance of these models is considered over a

moving non-overlapping 50-day estimation window ( q ) of 22 periods spanning June 1,

1988 to May 31, 1991. This leads to a total of 28,417 options for analyzing in-sample

performance in the -10% to +10% moneyness range ( ∈= KSm / [0.9,1.1]). This same

range of options is typically considered in other empirical studies including Dumas,

Fleming and Whaley (1998) and Christoffersen and Jacobs (2004). Daily volatilities in

the in-sample analysis are estimated from the DFW volatility regression (9) where

implied volatility is regressed on linear and quadratic terms of option maturity and

exercise price.

The out-of-sample horizon is taken to be one, two and three days from the end of

each rolling estimation period q . In the out-of-sample analysis, next-day predicted

volatilities from the DFW volatility regression are used in LOR models with implied

volatilities (SLOR-V and RLOR-V). Out-of-sample LOR and PBS option values are

generated with (10)-(14) and (15-(16), respectively, using DWF volatility parameters

4It should be kept in mind that the data used to estimate LOR model parameters has a minimum option maturity of 7 days. Therefore, option prices from LOR models are valid only for maturities beyond 7 days.

19

from the previous n-th day (n=1, 2, 3). Out-of-sample pricing errors from both models

are plotted by moneyness in Figure 1.

[Figure 1 about here]

[Insert Table IV about here]

From the results reported in Table IV (Panel A and B), we identify the reduced-

form volatility model (RLOR-V) as the best LOR candidate, with its structural

counterpart SLOR-V as a close tie. RLOR-V yields in-sample and out-of-sample (1-day

out) root mean square errors (RMSEs) of $0.25 and $0.53, respectively, while the same

for the PBS model are $0.48 and $0.70, respectively. This amounts to a 48%

deterioration in in-sample pricing efficiency for PBS over RLOR-V and a 32% fall in

out-of-sample efficiency. Further, the higher pricing efficiency of RLOR-V continues to

hold at the 2-day and 3-day out horizons (Panels C and D).

Based on the comparative analysis of the four LOR specifications, we select

RLOR-V as the best localized option regression model for the remaining analysis and

will refer to it simply as “LOR”. LOR modeling without implied volatility, however,

retains much of its efficiency, yielding an error reduction of 19% relative to PBS (one-

day out-of-sample). Overall pricing errors from the LOR models without implied

volatility, namely RLOR and SLOR, are both $0.59 while the same for PBS is $0.70.

This specification has the further advantage of reducing modeling complexity as implied

volatilities do not need to be estimated and forecasted (see Section II.B.2).

20

D. Gains from Localization & In-sample Performance

We now consider the gains from localization and the in-sample performance of

LOR and PBS in greater detail. First, we note a dramatic increase in performance over

the global fit of Section A: the overall pricing error shrinks to $0.25 (RLOR-V) from

$1.30 (RLOR-V, Table II). Second, the overall reduction in pricing error (efficiency

gain) of LOR over PBS is 48.4% (EFF). Further, LOR pricing errors disaggregated by

year and quarter fall in the range $0.15-$0.33, representing gains in pricing efficiency of

34.9%-63.2% over PBS. Third, the coefficient of variation (CV) gives the pricing error

as a percentage of mean call price. These are relatively small, falling in the range 1.91%-

3.19%.

Table V gives a tabulation of pricing errors and efficiency gain by maturity-

moneyness categories. The pricing errors for LOR over the 12 categories fall in the range

of $0.16-$0.33 and correspond to efficiency gains of 14.4%-62.5% over the Black-

Scholes benchmark. We also note that the performance of LOR over option moneyness

is more consistent and stable, as pricing errors are similar in magnitude over the four

moneyness (S/X) ranges from 0.9 to 1.1. For example, among the shortest maturity calls

(less than 50 days), the pricing errors are $0.17, $0.22, $0.20 and $0.18, respectively,

over the moneyness categories [.9,.95], (.95,1.0], (1,1.05], (1.05,1.1], while PBS errors

over the same categories are $0.20, $0.30, $0.32 and $0.37.

[Insert Table V about here]

The in-sample empirical results demonstrate the superior performance of

localized option regression modeling over the PBS Black-Scholes benchmark in terms of

pricing precision and stability of estimates. We now examine its out-of-sample

performance in greater detail.

21

E. Out-of-Sample Performance

The out-of-sample performance of LOR is an indication of its usefulness and

quality as a pricing tool. We now focus attention on this feature of LOR in comparison to

the PBS benchmark.

Estimation of out-of-sample LOR regression parameters in (10)-(14) is performed

over a moving 50-day non-overlapping window and uses one-day predicted volatilities

from the DFW volatility regression (9). This generates 22 sequential estimation cycles in

our three-year sample and estimation is localized within each cycle to the maturity-

moneyness clusters defined in Table I. The procedure leads to 763, 776 and 776

observations at the one-day, two-day and three-day out-of-sample horizons and the

results are similar regardless of the starting point (various other starting dates in June

1988, aside from June 1, were tried and yielded similar results). Out-of-sample LOR and

PBS option values are generated using DWF volatility parameters from the previous n-th

day (n=1, 2, 3) in (12)-(14) and (15)-(16), respectively. Daily PBS out-of-sample option

prices are constructed from (15)-(16).

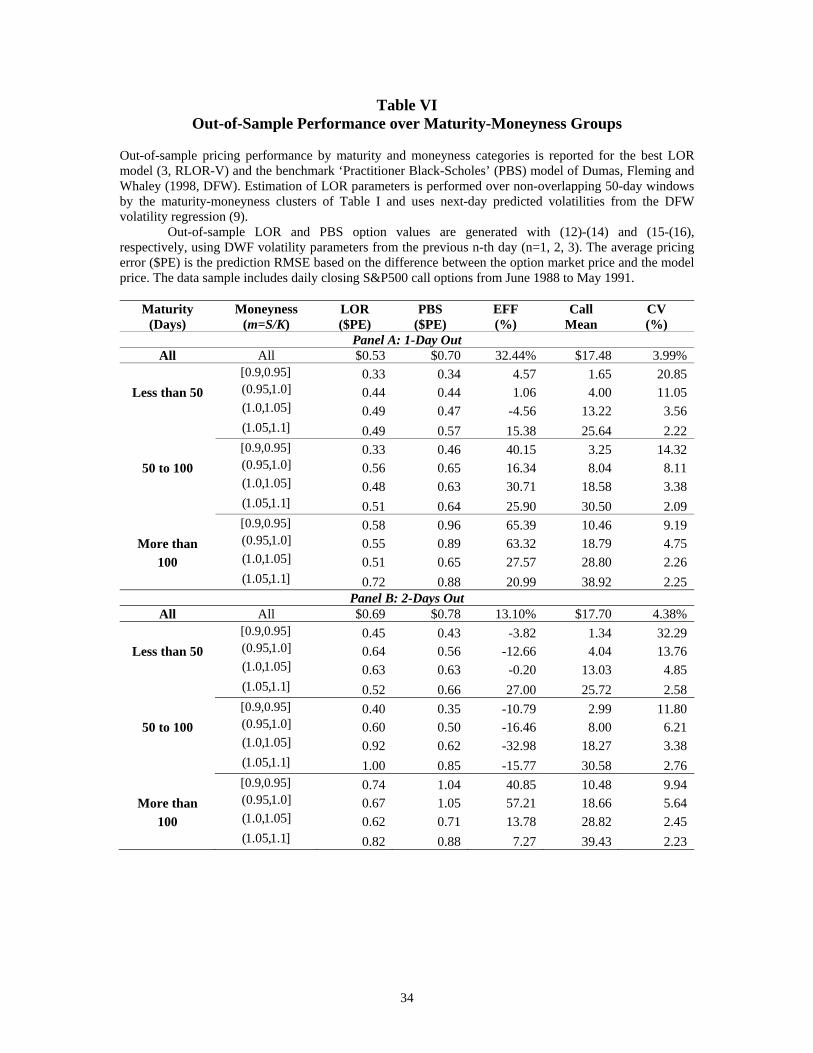

We find that LOR again outperforms the PBS benchmark. Tables IV and VI

show tabulations of pricing errors by year and maturity-moneyness groupings. As

reported earlier, the overall average pricing errors for LOR and PBS (one-day out) are

$0.53 and $0.70, respectively, with an efficiency loss of 32.4% for the benchmark model

(Panel B, Table IV). The LOR pricing error as a percentage of the mean option price

(CV) is 3.99%. With respect to tabulation across maturity-moneyness categories, LOR

dominates PBS in 11 of the 12 groups (Panel A, Table VI). LOR pricing errors fall in the

range $0.33-$0.73 and the same for PBS is $0.34-$0.96. At the longer three-day out

horizon (Panels C, Table VI), LOR pricing remains more efficient at longer option

maturities (>100 days) but underperforms PBS at the mid-maturity (50-100 days).

22

[Insert Table VI about here]

Overall, LOR continues to dominate at the longer two-day and three-day out

horizons, although the difference in pricing errors diminishes (Panels B and C, Table IV).

At the one-day out horizon, overall PBS pricing errors are 32.4% higher than LOR ($0.70

vs. $0.53) while, at the two-day horizon, the overall efficiency loss of PBS relative to

LOR is 13.2% and diminishes to 2.8% at three days out.

The in-sample and out-of-sample results provide confidence in the use of LOR as

an efficient and reliable option valuation tool, and as a robust benchmark for evaluating

the contribution of more complex structural option pricing models. We next examine the

volatility smile characteristics of LOR-based option pricing, after comparing its

performance to stochastic volatility models in the literature.

F. Comparison to Stochastic Volatility Models

As our analysis uses the same sample of S&P500 call options, covering the June

1988 to May 1991 period, as Bakshi, Cao and Chen (1997, BCC), comparison of out-of-

sample pricing errors provides some useful insights into the capability of LOR with

respect to more sophisticated risk-neutral models.

BCC evaluate the performance of alternative option pricing models incorporating

stochastic volatility (SV), stochastic volatility & stochastic interest rates (SVSI) and

stochastic volatility with jumps (SVJ) and compare their performance with Black-

Scholes-Merton (BSM). In their analysis, model parameters and implied volatility are

estimated from previous-day option prices and used to generate next-day prices.

While our analysis employs the DFW method for estimating volatility,

comparison with BCC is useful and informative because it uses the same option data.

BCC do not report overall pricing errors, but tabulate pricing errors by combinations of

23

18 maturity-moneyness categories. Ranges of (one-day out) pricing errors over these

combinations are $0.52-1.89 for BSM and $0.41-0.65 for SV. Their results show that the

BCC implementation of Black-Scholes is dominated by models with stochastic volatility.

The results noted in Section B above (Table IV) show that the overall out-of-

sample pricing error of the selected LOR model ($0.53) is in the mid-point of the range

for the SV model analyzed by BCC using the same sample. This comparison provides

further evidence that LOR modeling is highly competitive with more sophisticated risk-

neutral option models with stochastic volatility in the return process. Moreover, we show

below that the volatility smile problem is largely absent in LOR option prices.

G. The Volatility Smile & Pricing Error Regressions

An important empirical deficiency of the Black-Scholes model is the occurrence

of the volatility smile (or smirk), where the option’s implied volatility depends on the

value of the strike price, usually in a “smile” or “sneer” pattern. To what extent does this

problem occur in LOR option prices?

One way to examine the volatility smile issue is to compute the implied volatility

of option prices across strikes by inverting the Black-Scholes formula. Given the positive

monotonic relationship between volatility and option value, the smile effect in LOR and

PBS option prices may also be alternatively, and directly, analyzed from pricing errors in

price-strike space. We perform this analysis by testing for the following functional

relationship between pricing errors and the option’s moneyness ( SK / ) in the regression

iModel

ii SKSKVV εβββ +++=− 2210 )()( (17)

where Modelii VV − is the pricing error under the respective model (LOR or PBS). The

pricing error regression (17) is analogous to a paired t-test as the price difference

Modelii VV − cancels all common factors effecting option valuation (strike, maturity, index

24

value, interest rate) with the exception of volatility and the regression tests for the

residual’s dependence on the strike price. Further, the monotonic relationship between

option price and volatility ensures that the smile effect is uniquely captured by the error

regression (17).

Results from the LOR and BS models are reported in Table VII and the fitted

regression values are as follows:

PBS: =− Modelii VV -55.81 + 110.31 )( SK - 54.35 2)( SK (18)

LOR: =− Modelii VV -9.02 + 17.85 )( SK - 8.78 2)( SK (19)

The estimates reveal a very strong smile/sneer effect in PBS option prices while this

effect is virtually non-existent in LOR prices. The linear and quadratic smile parameters

( 1β and 2β , respectively) in the PBS regression are large and strongly significant with

significance probabilities less than .0001. For LOR, the same parameters are much

smaller in magnitude and are not statistically significant from zero.

Predicted values based on the LOR and PBS error regressions (18)-(19) are

plotted in Figure 2. The relatively flat error curve for LOR again points to the negligible

volatility smile effect in LOR option prices in contrast to PBS prices. If model prices

track market prices over moneyness (i.e. capture the volatility smile), then the pricing

error Modelii VV − should be flat with respect to moneyness. In Figure 2, the pricing error

Modelii VV − becomes inverted because PBS model prices PBS

iV over-shoot market prices

iV for away from the money options.

[Figure 2 about here]

Finally, results from our empirical analysis show that not only do LOR option

prices provide smaller pricing errors than the ‘Practitioner Black-Scholes’ (both in-

sample and out-of-sample), but LOR option prices are largely free of the volatility smile

effect.

25

V. CONCLUSION

This paper considers a simple empirical approach to modeling and predicting

market option prices using localized option regressions (LOR). LOR projects market

option prices over localized regions of their state space without requiring assumptions

regarding the asset price distribution (e.g. log-normality), volatility structure and hedging

behavior found in risk-neutral models. The model offers an efficient and robust data-

driven approach to valuing option books.

While the LOR model is deceptively simple, the method and our surprising

findings have not been reported in the previous literature. Our empirical study using

three years of daily S&P500 options (28,417 option prices) finds that LOR yields smaller

out-of-sample pricing errors (e.g. 32% one-day-out) than the efficient Black-Scholes

(PBS) implementation of Dumas, Fleming & Whaley (1998) that has become a common

benchmark for evaluating new option models in the literature (for example,

Christoffersen and Jacobs (2004) show that it empirically outperforms stochastic

volatility models). LOR out-of-sample pricing errors are significantly lower than PBS

(e.g. $0.53 vs. $0.70 one-day-out) and exceed LOR by 32.4%, 13.2% and 2.8% over one-

day, two-day and three-day out-of-sample horizons, respectively. Furthermore, we find

that the volatility smile is virtually non-existent in option prices generated by the LOR

model.

We also find that the corresponding LOR model without implied volatility

outperforms the PBS benchmark. Its overall pricing error one-day out is $0.59 while the

same for PBS is $0.70. This shows that LOR modeling without implied volatility retains

much of its efficiency with an error reduction of 19%. This specification has the

advantage of reducing modeling complexity as implied volatilities do not need to be

estimated and forecasted. LOR also compares favorably with stochastic volatility models

26

analyzed by Bakshi, Cao and Chen (1997) using the same S&P500 option data as in this

paper.

In addition to being an efficient and robust option modeling and valuation tool for

large option books, LOR provides a simple to implement empirical benchmark for

evaluating more complex risk-neutral models. Here, it follows that more complex option

pricing models derived from advanced theoretical arguments should be capable of, at the

very least, outperforming a relatively “agnostic” and simple empirical model in

predicting market option prices.

27

REFERENCES

Aït-Sahalia Y. and Lo, A. (1998). Non-parametric Estimation of State-Price Densities

Implicit in Financial Asset Prices. Journal of Finance, 53, 499-547.

Bakshi, G., Cao, C., and Chen, Z. (1997). Empirical Performance of Alternative Option

Pricing Models. Journal of Finance, 52, 2003-2049.

Bates, D. (1996). Jumps and Stochastic Volatility: Exchange Rate Processes Implicit in

Deusche Mark Options. Review of Financial Studies, 9, 68-107.

Black, F. and Scholes, B. (1973). The pricing of Options and Corporate Liabilities.

Journal of Political Economy, 81, 637-659.

Canina, L. and Figlewski, S. (1996). The Informational Content of Implied Volatilities.

Review of Financial Studies, 6, 659-681.

Carr, P. and Wu, L. (2004). Time-Changed Levy Processes and Option Pricing.

Journal of Financial Economics, 71, 113-141.

Christoffersen, P. and Jacobs, K. (2004). The Importance of the Loss Function in Option

Valuation. Journal of Financial Economics,72, 291-318.

Cox, J., S. Ross and Rubenstein, M. (1979). Option Pricing: A Simplified Approach.

Journal of Financial Economics, 7, 229-64.

Derman, E. and Kani, I. (1994). The Volatility Smile and its Implied Volatility Tree.

Quantitative Strategies Research Notes (Goldman Sachs, New York).

Duan, J. (1995). The GARCH Option Pricing Model. Mathematical Finance, 5, 13-32.

Duffie, D., Pan, J. and Singleton, K. (2000). Transform Analysis and Asset Pricing for

Affine Jump Diffusions. Econometrica, 68, 1343-1376.

Dupire, B. (1994). Pricing with a Smile. Risk, 7, 32-39.

Dumas, B. Fleming, J. and Whaley, R. (1998). Implied Volatility Functions: Empirical

Tests. Journal of Finance, 53, 2059-2106.

Heston, S. L. (1993). A Closed Form Solution for Options with Stochastic Volatility

with Applications to Bonds and Currency Options. Review of Financial Studies,

6, 327-43.

Heston, S. and Nandi, S. (2000). A Closed-form GARCH Option Pricing Model. Review

of Financial Studies, 13, 585-626.

Heynen, R. (1993). An Empirical Analysis of Observed Smile Patterns. Review of

28

Futures Markets, 317-353.

Hull, J. and White, A. (1987). The Pricing of Options on Assets with Stochastic

Volatilities. Journal of Finance, 42, 281-300.

Hutchinson, J. Lo, A. and Poggio, T. (1994). A Nonparametric Approach to Pricing and

Hedging Derivative Securities Via Learning Networks. Journal of Finance, 49,

851-889.

Jacquier, E. and Jarrow, R. (2000). Bayesian Analysis of Contingent Claim Model Error.

Journal of Econometrics, 94, 145-180.

Jackwerth, J. (2000). Recovering Risk Aversion from Option Prices and Realized

Returns. Review of Financial Studies 13 (2), 433-451.

Lamoureux, C. and Lastrapes, W. (1993). The Informational Content of Implied

Volatilities. Review of Financial Studies 6, 659-681.

Lehnert, T. (2003). Explaining Smiles: GARCH Option Prices with Conditional

Leptokurtosis and Skewness. Journal of Derivatives 10, 27-39.

Merton, R.C. (1973). Rational Theory of Option Pricing. Bell Journal of Economics and

Management Science, 4, 141-183.

Merton, R.C. (1976). Option Pricing When Underlying Stock Returns are Discontinuous.

Journal of Financial Economics 3, 125-44.

Ritchen, P. and R. Trevor (1999). Pricing Options Under Generalized GARCH and

Stochastic Volatility Processes. Journal of Finance, 54, 1, 377-402.

Rubenstein, M. (1994). Implied Binomial Trees. Journal of Finance, 49, 771-818.

29

Table I Localization to Moneyness-Maturity Groups

One-day out-of-sample pricing errors for S&P500 option prices from the LOR model are reported over different moneyness and maturity groupings. Moneyness is defined as the S&P500 index value divided by the option’s strike price ( KSm /= ) and maturity represents remaining days to option expiration.

Option Maturity Group

Moneyness Group Average Pricing

Error ($) { }]367,100(],100,7[=Τ { }]1.1,1(],1,9[.=Μ 0.57

{ }]1.1,05.1(],05.1,1(],1,95(.],95,.9[.=Μ 0.62 { }]367,100(],100,50(],50,7[=Τ { }]1.1,1(],1,9[.=Μ 0.53

{ }]1.1,05.1(],05.1,1(],1,95(.],95,.9[.=Μ 0.78 { }]367,200(],200,150(],150,100(],100,50(],50,7[=Τ { }]1.1,1(],1,9[.=Μ 0.92

{ }]1.1,05.1(],05.1,1(],1,95(.],95,.9[.=Μ 1.20

Table II Descriptive Statistics

Summary statistics are reported for closing daily S&P500 call options from June 2, 1988 to May 31, 1991. This sample consists of a total of 28,417 option prices and the same data is also used in the studies of Bakshi, Cao and Chen (1997) and Christoffersen and Jacobs (2004). Panel B reports the statistics by groups based on the option’s remaining time-to-maturity (in days) and its moneyness (S&P500 index value divided by option strike price). Panel C gives the corresponding number of options in each combination.

Panel A: Descriptive statistics Variable Units Mean Std Min Median Max Kurtosis Skew

Call Option Price (V ) $ 24.48 21.02 0.66 18.75 100.00 1.033 1.205 SP500 Index ( X ) 323.22 32.34 248.71 327.83 389.59 -0.799 -0.319 Exercise Price ( K ) 316.82 40.02 175.00 320.00 425.00 -0.540 -0.074 Risk-free Rate ( r ) 0.0772 0.0100 0.0252 0.0795 0.1009 0.550 -0.731 Time-to-maturity (τ ) Days 115 86 7 95 367 -0.338 0.759 Volatility (σ ) 0.2073 0.0684 0.0819 0.1917 0.8914 14.091 2.834 Panel B: Average call prices by Moneyness-Maturity categories Days-to-Maturity Moneyness ( KSm /= ) ]50,7[ ]100,50( ]150,100( ]200,150( 200>

]95.0,9.0( $1.52 3.12 6.79 9.77 15.40 ]0.1,95.0( $3.83 8.15 13.99 17.87 24.03 ]05.1,0.1( $12.75 18.19 24.40 28.35 34.45 ]1.1,05.1( $25.29 30.39 35.34 38.68 44.87

Panel C: Number of options ]95.0,9.0( 747 1,272 1,221 1,126 1,147 ]0.1,95.0( 3,376 1,962 1,380 1,231 1,198 ]05.1,0.1( 3,275 1,650 1,146 1,045 909 ]1.1,05.1( 2,426 1,173 910 662 677

30

Table III Estimation of Option Regressions

Estimation of the four reduced-form and structural option regression models (1)-(4) is reported over the complete option sample (28,417 options). Adjusted R-squares, RMSEs, parameter estimates, their standard errors and significance probabilities (p-values) are also reported.

Panel A: Reduced-form Option Regressions - with and without implied volatility (RLOR-V, RLOR) RLOR RLOR-V

Parameter Estimate S.E. p-value Estimate S.E. p-value Intercept -79.84047 1.58482 <.0001 -20.57762 1.29347 <.0001

S 1.04889 0.00959 <.0001 0.53545 0.007960 <.0001 K -0.41694 0.0066 <.0001 -0.47016 0.006480 <.0001 τ 0.12199 0.00201 <.0001 -0.007230 0.001820 <.0001 r -331.01583 10.19839 <.0001 102.80166 8.19313 <.0001 2S 0.00277 0.00001754 <.0001 0.003590 0.00001409 <.0001

K2 0.0034 0.00000957 <.0001 0.003470 0.00000876 <.0001 τ 2 -0.0001469 0.00000132 <.0001 -0.00012701 0.00000092 <.0001

SK -0.00724 0.00002028 <.0001 -0.007110 0.00001724 <.0001 τS -0.0001292 0.00000559 <.0001 0.00020119 0.00000438 <.0001

Sr 1.74005 0.04771 <.0001 0.78183 0.03998 <.0001 Kτ 0.00015371 0.00000399 <.0001 0.00001328 0.00000357 0.0002 Kr -1.00151 0.04131 <.0001 -0.99314 0.03740 <.0001

τr 0.01635 0.013 0.2085 0.39348 0.009740 <.0001 σ 48.84034 2.29227 <.0001

2σ -18.94554 0.87780 <.0001 στ 0.16482 0.002480 <.0001

Sσ -0.23264 0.006710 <.0001 Kσ 0.24567 0.005970 <.0001 rσ -98.5760 12.04575 <.0001

Adj. R-square 0.9917 0.9962 RMSE $1.9143 $1.2985

31

Panel B: Structural Option Regressions – with and without implied volatility (SLOR-V, SLOR)

SLOR SLOR-V Parameter Estimate S.E. p-value Estimate S.E. p-value Intercept 61.08867 2.58377 <.0001 117.79971 2.07702 <.0001

m -0.17671 0.01 <.0001 -0.62653 0.007990 <.0001 K -209.1852 2.49143 <.0001 -231.61593 2.20305 <.0001 τ 0.19747 0.00263 <.0001 0.022780 0.002330 <.0001 r -560.72895 17.41768 <.0001 -117.15934 14.75335 <.0001 2m -0.00109 0.00001342 <.0001 -0.00003114 .00001183 0.0085

K2 65.95335 0.86851 <.0001 101.45768 0.90662 <.0001 τ 2 -0.00014274 0.00000151 <.0001 -0.00012235 .00000116 <.0001

mK 0.82669 0.00442 <.0001 0.66122 0.004310 <.0001 τm 0.00004625 0.0000048 <.0001 0.00026438 .00000392 <.0001

mr 0.79347 0.03633 <.0001 -0.10808 0.02872 0.0002 Kτ -0.079 0.00131 <.0001 -0.048250 0.00135 <.0001 Kr 207.8841 13.83197 <.0001 186.71978 14.14917 <.0001

τr 0.00338 0.01484 0.8200 0.38908 0.01222 <.0001 σ 123.04548 3.00817 <.0001

2σ -11.20498 1.16542 <.0001 στ 0.18677 0.00312 <.0001 mσ 0.08025 0.00640 <.0001 Kσ -98.12362 2.10254 <.0001 rσ -101.3339 15.66606 <.0001

Adj. R-square 0.9891 0.9940 RMSE $2.1981 $1.6338

32

Table IV Average Pricing Errors of LOR and PBS Models

The in-sample and out-of-sample performance of the four candidate localized option regression (LOR) models (1)-(4) and the benchmark ‘Practitioner Black-Scholes’ (PBS) model of Dumas, Fleming and Whaley (1998, DFW) is reported. Estimation of LOR parameters is performed over non-overlapping 50-day windows by the maturity-moneyness clusters of Table I. In the in-sample analysis, daily volatilities are estimated from the DFW volatility regression (9) where implied volatility is regressed on linear and quadratic terms of option maturity and exercise price. In the out-of-sample analysis, next-day predicted volatilities from the DFW volatility regression are used in LOR models with implied volatilities (SLOR-V and RLOR-V). Out-of-sample LOR and PBS option values are generated using equations (10)-(14) and (15-(16), respectively, with DWF volatility parameters from the previous n-th day (n=1, 2, 3). The average pricing error ($PE) is the RMSE based on the difference between the option market price and the model price. The efficiency loss (EFF) is the percentage increase in average PBS pricing errors over LOR.

Panel A: In-Sample

Pricing Error (PE or RMSE)

Efficiency Gain (% EFF)

Year Mean PBS RLOR SLOR SLOR-V RLOR-V RLOR-V SLOR-V All $17.08 $0.48 $0.45 $0.45 $0.25 $0.25 48.40% 47.87% 1988 13.24 0.28 0.30 0.30 0.16 0.16 43.06 42.30 1989 16.23 0.48 0.39 0.39 0.21 0.21 56.06 55.64 1990 18.83 0.50 0.51 0.51 0.28 0.28 44.58 44.03 1991 18.20 0.55 0.50 0.50 0.30 0.30 46.97 46.35

Panel B: 1-Day Out All $17.48 $0.70 $0.59 $0.59 $0.53 $0.53 32.44% 31.98% 1988 13.56 0.31 0.46 0.46 0.37 0.37 -15.86 -15.96 1989 16.80 0.49 0.43 0.43 0.42 0.41 18.25 17.23 1990 19.23 0.87 0.69 0.68 0.63 0.63 38.28 38.15 1991 18.26 0.83 0.69 0.69 0.58 0.58 43.53 42.53

Panel C: 2-Days Out All $17.70 $0.78 $0.74 $0.75 $0.69 $0.69 13.10% 13.17% 1988 13.47 0.39 0.66 0.66 0.43 0.43 -8.79 -9.05 1989 16.34 0.54 0.47 0.48 0.48 0.48 12.28 11.54 1990 19.78 0.82 0.77 0.77 0.76 0.76 7.72 8.46 1991 19.48 1.22 1.11 1.11 0.99 0.99 24.36 23.83

Panel D: 3-Days Out All $13.52 $0.76 $0.65 $0.74 $0.74 $0.75 1.98% 2.87% 1988 16.14 0.43 0.67 0.65 0.54 0.55 -22.24 -21.76 1989 19.66 0.68 0.71 0.67 0.64 0.63 7.81 6.51 1990 18.84 0.76 0.98 0.71 0.85 0.87 -12.57 -10.43 1991 13.52 1.11 0.65 0.98 0.83 0.83 33.98 33.32

33

Table V In-Sample Performance by Maturity-Moneyness Groups

Pricing performance by maturity and moneyness categories is reported for the selected localized option regression model (3, RLOR-V) model and the benchmark ‘Practitioner Black-Scholes’ (PBS) model of Dumas, Fleming and Whaley (1998, DFW). Estimation of LOR parameters is performed over non-overlapping 50-day windows by the maturity-moneyness clusters of Table I. Daily volatilities are estimated from the DFW volatility regression (9) where implied volatility is regressed on linear and quadratic terms of option maturity and exercise price. The average pricing error ($PE) is the RMSE based on the difference between the option market price and the model price. The efficiency loss (EFF) is the percentage increase in average PBS pricing errors over LOR. The correlation of variation (CV) is the percentage pricing error relative to the mean option value ($PE/Call Mean). The data sample is based on daily closing S&P500 call options from June 1988 to May 1991.

Maturity (Days)

Money-ness (m=S/K)

LOR ($PE)

PBS ($PE)

EFF (%)

Call Mean

CV (%)

All All $0.25 $0.48 48.40% $17.08 2.80% ]95.0,9.0[ 0.17 0.20 14.4 1.52 13.26

Less than 50 ]0.1,95.0( 0.22 0.30 27.2 3.84 7.86 ]05.1,0.1( 0.20 0.32 36.8 12.75 2.49 ]1.1,05.1( 0.18 0.37 50.5 25.29 1.45 ]95.0,9.0[ 0.15 0.25 38.7 3.13 7.94

50 to 100 ]0.1,95.0( 0.16 0.29 45.1 8.17 3.58 ]05.1,0.1( 0.16 0.30 44.6 18.28 1.63 ]1.1,05.1( 0.17 0.44 62.5 30.49 1.45 ]95.0,9.0[ 0.33 0.80 58.3 10.58 7.57

More than ]0.1,95.0( 0.31 0.59 46.9 18.40 3.22 100 ]05.1,0.1( 0.28 0.47 39.8 28.68 1.63

]1.1,05.1( 0.27 0.53 48.8 39.19 1.36

34

Table VI Out-of-Sample Performance over Maturity-Moneyness Groups

Out-of-sample pricing performance by maturity and moneyness categories is reported for the best LOR model (3, RLOR-V) and the benchmark ‘Practitioner Black-Scholes’ (PBS) model of Dumas, Fleming and Whaley (1998, DFW). Estimation of LOR parameters is performed over non-overlapping 50-day windows by the maturity-moneyness clusters of Table I and uses next-day predicted volatilities from the DFW volatility regression (9). Out-of-sample LOR and PBS option values are generated with (12)-(14) and (15-(16), respectively, using DWF volatility parameters from the previous n-th day (n=1, 2, 3). The average pricing error ($PE) is the prediction RMSE based on the difference between the option market price and the model price. The data sample includes daily closing S&P500 call options from June 1988 to May 1991.

Maturity (Days)

Moneyness (m=S/K)

LOR ($PE)

PBS ($PE)

EFF (%)

Call Mean

CV (%)

Panel A: 1-Day Out All All $0.53 $0.70 32.44% $17.48 3.99%

]95.0,9.0[ 0.33 0.34 4.57 1.65 20.85 Less than 50 ]0.1,95.0( 0.44 0.44 1.06 4.00 11.05

]05.1,0.1( 0.49 0.47 -4.56 13.22 3.56 ]1.1,05.1( 0.49 0.57 15.38 25.64 2.22 ]95.0,9.0[ 0.33 0.46 40.15 3.25 14.32

50 to 100 ]0.1,95.0( 0.56 0.65 16.34 8.04 8.11 ]05.1,0.1( 0.48 0.63 30.71 18.58 3.38 ]1.1,05.1( 0.51 0.64 25.90 30.50 2.09 ]95.0,9.0[ 0.58 0.96 65.39 10.46 9.19

More than ]0.1,95.0( 0.55 0.89 63.32 18.79 4.75 100 ]05.1,0.1( 0.51 0.65 27.57 28.80 2.26

]1.1,05.1( 0.72 0.88 20.99 38.92 2.25 Panel B: 2-Days Out

All All $0.69 $0.78 13.10% $17.70 4.38% ]95.0,9.0[ 0.45 0.43 -3.82 1.34 32.29

Less than 50 ]0.1,95.0( 0.64 0.56 -12.66 4.04 13.76 ]05.1,0.1( 0.63 0.63 -0.20 13.03 4.85 ]1.1,05.1( 0.52 0.66 27.00 25.72 2.58 ]95.0,9.0[ 0.40 0.35 -10.79 2.99 11.80

50 to 100 ]0.1,95.0( 0.60 0.50 -16.46 8.00 6.21 ]05.1,0.1( 0.92 0.62 -32.98 18.27 3.38 ]1.1,05.1( 1.00 0.85 -15.77 30.58 2.76 ]95.0,9.0[ 0.74 1.04 40.85 10.48 9.94

More than ]0.1,95.0( 0.67 1.05 57.21 18.66 5.64 100 ]05.1,0.1( 0.62 0.71 13.78 28.82 2.45

]1.1,05.1( 0.82 0.88 7.27 39.43 2.23

35

Maturity

(Days) Moneyness

(m=S/K) LOR ($PE)

PBS ($PE)

EFF (%)

Call Mean

CV (%)

Panel C: 3-Days Out All All $0.75 $0.76 1.98% $17.52 4.37%

]95.0,9.0[ 0.39 0.37 -7.02 1.45 25.33 Less than 50 ]0.1,95.0( 0.61 0.48 -21.40 3.87 12.48

]05.1,0.1( 0.57 0.50 -12.59 12.81 3.87 ]1.1,05.1( 0.60 0.58 -4.58 25.03 2.30 ]95.0,9.0[ 0.74 0.30 -59.28 2.87 10.46

50 to 100 ]0.1,95.0( 0.73 0.37 -49.90 7.65 4.79 ]05.1,0.1( 1.26 0.50 -60.18 18.36 2.73 ]1.1,05.1( 1.44 0.67 -53.45 30.61 2.19 ]95.0,9.0[ 0.72 1.24 71.94 10.27 12.10

More than ]0.1,95.0( 0.68 1.07 56.11 18.68 5.72 100 ]05.1,0.1( 0.66 0.73 11.93 28.42 2.58

]1.1,05.1( 0.65 0.73 13.29 39.38 1.86

36

Table VII Regressions of Pricing Errors and the Volatility Smile

The volatility smile effect is LOR and PBS out-of-sample prices is evaluated using the pricing error regression (17). Option pricing errors Model

ii VV − (difference between market and model prices) are regressed on linear and quadratic terms of SK / (strike over price). The regression is analogous to a paired t-test as the price difference Model

ii VV − cancels all common factors effecting option valuation (strike, maturity, index, discount rate) with the exception of volatility, and the residual difference is tested for dependence on strike. The monotonic relationship between option price and volatility ensures that the smile effect is uniquely captured by the price difference Model

ii VV − . The volatility smile is absent if both the linear and quadratic terms of the pricing error regression are not significant.

Model Variable Estimate Standard Error

t-value p-value

PBS Intercept -55.8092 9.1909 -6.07 <.0001 SK / 110.3114 18.3272 6.02 <.0001 ( )2/ SK -54.3526 9.1183 -5.96 <.0001

LOR Intercept -9.0174 7.1079 -1.27 0.2050

SK / 17.8450 14.1737 1.26 0.2084 ( )2/ SK -8.7806 7.0518 -1.25 0.2135

37

Figure 1 Pricing Errors from the LOR and PBS Models by Option Moneyness

Out-of-sample pricing errors from the LOR and PBS models are plotted by option moneyness. The pricing errors are S&P500 market option prices minus model prices (LOR or PBS) and moneyness is defined as the S&P500 index over the option strike price ( KS / ).

38

Figure 2 The Volatility Smile in LOR & PBS Prices

Predicted pricing errors Model

ii VV − are based on estimated parameters of the pricing error regressions (17). They are plotted for both LOR and PBS models against SK / (option strike over price). In the absence of a volatility smile/sneer effect, the differences in market and model option prices ( Model

ii VV − ) would be flat and not vary with the option’s strike (see Table VII for statistical tests). If model prices track market prices over moneyness (i.e. capture the volatility smile), then the pricing error Model

ii VV − should

be flat with respect to moneyness. For the PBS model, the pricing error Modelii VV − becomes inverted

because PBS option prices PBSiV over-shoot market prices iV for away from the money options.