Embed Size (px)

Citation preview

This English translation of the authentic German text serves merely information purposes. The official wording in German can be found in the Austrian Federal Law Gazette (Bundesgesetzblatt – BGBl.). 1

Regulation of the Financial Market Authority (FMA) on the Solvency of Credit Institutions

Solvency Regulation

(Solvabilitätsverordnung – SolvaV)

Federal Law Gazette II No.

374/2006 original version

as amended by

Federal Law Gazette II No

253/2007

On the basis of Article 21d para. 6, Article 21f para. 4, Article 22 para. 7, Article 22a para. 5 no. 5, Article 22a para. 7, Article 22b paras. 10 and 11, Article 22d para. 5, Article 22e paras. 5 and 6, Article 22f para. 2, Article 22g para. 9, Article 22h para. 7, Article 22j para. 2, Article 22k paras. 4 and 9, Article 22l para. 4, Article 22n para. 5, Article 22o para. 5 and Article 22p para. 5 of the Banking Act (Bankwesengesetz – BWG; Federal Law Gazette No. 532/1993 as last amended by Federal Law Gazette I No. 141/2006), the following regulation has been issued with the consent of the Federal Minister of Finance:

Table of Contents

Part 1: General Provisions Article 1. Purpose Article 2. Definitions

Part 2: Credit Risk

Chapter 1: Standardised Approach to Credit Risk

Section 1: General Provisions

Article 3. General Provisions

This English translation of the authentic German text serves merely information purposes. The official wording in German can be found in the Austrian Federal Law Gazette (Bundesgesetzblatt – BGBl.). 2

Section 2: Risk Weights

Article 4. Exposures to Central Governments or Central Banks Article 5. Exposures to Regional Governments, Local Authorities and Legally Recognised

Religious Communities Article 6. Exposures to Public-Sector Entities, Administrative Bodies and

Non-Commercial Undertakings Article 7. Exposures to Multilateral Development Banks Article 8. Exposures to International Organisations Article 9. Exposures to Institutions Article 10. Assignment of Weights for Exposures to Institutions Article 11. Exposures to Corporates Article 12. Retail Exposures Article 13. Exposures Secured by Real Estate Property Article 14. Residential Mortgage Loans Article 15. Commercial Mortgage Loans Article 16. Past Due Exposures Article 17. High-Risk Items Article 18. Exposures in the Form of Covered Bonds Article 19. Additional Requirements for Covered Bonds Secured by Real Estate Article 20. Weighting of Exposures in the Form of Covered Bonds Article 21. Short-Term Exposures to Credit Institutions and Corporates Article 22. Exposures in the Form of Shares in Investment Funds Article 23. Exposures in the Form of Rated Shares in Investment Funds Article 24. Average Risk Weight for Exposures in the Form of Shares in Investment Funds Article 25. Other Items Article 26. Trust Assets and Bonds from Direct Issuance Article 27. Asset Sale and Repurchase Agreements and Outright Forward Purchases Article 28. Credit Protection for a Basket of Exposures

Section 3: Use of Credit Assessments from External Credit Assessment Institutions

Article 29. Use of Credit Assessments from External Credit Assessment Institutions Article 30. General Provisions regarding Use Article 31. Use of Multiple Credit Assessments Article 32. Issuer and Issue Credit Assessments Article 33. Short-Term Credit Assessments for Exposures Article 34. Short-Term Credit Assessments for Facilities Article 35. Domestic and Foreign Currency Items

Chapter 2: Internal Ratings Based Approach

Section 1: General Provisions

Article 36. General Provisions

This English translation of the authentic German text serves merely information purposes. The official wording in German can be found in the Austrian Federal Law Gazette (Bundesgesetzblatt – BGBl.). 3

Section 2: Minimum Requirements

Article 37. Rating Systems Article 38. Structure of Rating Systems Article 39. Assignment of Exposures Article 40. Integrity of the Assignment Process Article 41. Use of Models Article 42. Documentation of Rating Systems Article 43. Models Obtained from Third-Party Vendors Article 44. Data Maintenance Article 45. Stress Tests Article 46. Qualification of Obligor Default Article 47. Overall Requirements for Own Estimates Article 48. Requirements regarding PD Estimates for Exposures to Central Governments

and Central Banks, Institutions and Corporates Article 49. Requirements regarding PD Estimates for Retail Exposures Article 50. Requirements for Own LGD Estimates Article 51. Requirements regarding LGD Estimates for Exposures to Central Governments

and Central Banks, Institutions and Corporates Article 52. Requirements regarding LGD Estimates for Retail Exposures Article 53. Requirements for the Estimation of Conversion Factors Article 54. Requirements regarding Conversion Factor Estimates for Exposures to Central

Governments and Central Banks, Institutions and Corporates Article 55. Requirements regarding Conversion Factor Estimates for Retail Exposures Article 56. Requirements for the Recognition of Personal Collateral in Parameter Estima-

tion Article 57. Additional Requirements for Assessing the Effect of Credit Derivatives Article 58. Requirements for Purchased Receivables Article 59. Validation of Internal Estimates Article 60. Quantitative Requirements for Internal Models for Equity Exposures Article 61. Qualitative Requirements for Internal Models for Equity Exposures Article 62. Validation and Documentation of Internal Models for Equity Exposures Article 63. Responsibility of Directors and Credit Risk Control Requirements Article 64. Duties of the Internal Audit Unit

Section 3: Calculation of Exposure Values

Article 65. Calculation of Exposure Values Article 66. Exposure Values of Equity Exposures Article 67. Exposure Values of Other Assets

This English translation of the authentic German text serves merely information purposes. The official wording in German can be found in the Austrian Federal Law Gazette (Bundesgesetzblatt – BGBl.). 4

Section 4: Risk Parameters PD, LGD and M

Article 68. PD Estimates for Exposures to Central Governments and Central Banks, Insti-tutions and Corporates

Article 69. LGD Estimates for Exposures to Central Governments and Central Banks, Insti-tutions and Corporates

Article 70. Residual Maturity for Exposures to Central Governments and Central Banks, Institutions and Corporates

Article 71. PD and LGD Estimates for Retail Exposures Article 72. Equity Exposures under the PD/LGD Method

Section 5: Risk-Weighted Exposure Amounts and Expected Loss Amounts

Article 73. Risk-Weighted Exposure Amounts and Expected Loss Amounts Article 74. Exposures to Central Governments and Central Banks, Institutions and Corpo-

rates Article 75. Retail Exposures Article 76. Defaulted Exposures Article 77. Equity Exposures Article 78. Other Assets Article 79. Exposures in the Form of Shares in Investment Funds Article 80. Dilution Risk Article 81. Expected Loss Amounts Article 82. Treatment of Expected Loss Amounts

Chapter 3: Credit Risk Mitigation

Section 1: Credit Protection

Article 83. Credit Protection

Subsection 1: Real Collateral and Netting

Article 84. On-Balance-Sheet Netting Article 85. Master Netting Agreements Covering Repurchase Transactions, Securities and

Commodities Lending or Borrowing Transactions and Other Capital Market-Driven Transactions

Article 86. Method-Based Eligibility of Real Collateral Article 87. Financial Collateral Article 88. Unrated Debt Securities Issued by Institutions Article 89. Investment Fund Shares Article 90. Additional Financial Collateral under the Comprehensive Method Article 91. Additional Eligibility for Calculations under the Internal Ratings Based Approach Article 92. Real Estate Collateral Article 93. Receivables Article 94. Other physical collateral Article 95. Other Types of Collateral

This English translation of the authentic German text serves merely information purposes. The official wording in German can be found in the Austrian Federal Law Gazette (Bundesgesetzblatt – BGBl.). 5

Subsection 2: Personal Collateral

Article 96. Protection Providers Article 97. Double Default Article 98. Credit Derivatives Article 99. Internal Hedges

Section 2: Minimum Requirements

Subsection 1: Minimum Requirements for Netting and Master Netting Agreements Article 100. Netting Article 101. Master Netting Agreements Subsection 2: Minimum Requirements for Other Physical Collateral Article 102. Financial Collateral Article 103. Real Estate Collateral Article 104. Valuation of Real Estate Collateral Article 105. Receivables Article 106. Value of Receivables Article 107. Other physical collateral Article 108. Value of Other Physical Collateral Article 109. Other Types of Collateral Article 110. Financial leasing Subsection 3: Minimum Requirements for Personal Collateral Article 111. Requirements for All Personal Collateral Article 112. Operational Requirements Article 113. Sovereign and Other Public-Sector Counter-Guarantees Article 114. Additional Requirements for Personal Collateral other than Credit Derivatives Article 115. Guarantee Schemes Eligible for the Purpose of Credit Risk Mitigation Article 116. Additional Requirements for Credit Derivatives Article 117. Mismatches Article 118. Double Default

Section 3: Effects of Credit Risk Mitigation

Subsection 1: Article 119. General Article 120. Cash, Securities and Commodities under Repurchase Transactions or Securi-

ties or Commodities Lending or Borrowing Transactions Article 121. Credit-Linked Notes Article 122. On-Balance-Sheet Netting

This English translation of the authentic German text serves merely information purposes. The official wording in German can be found in the Austrian Federal Law Gazette (Bundesgesetzblatt – BGBl.). 6

Subsection 2: Master Netting Agreements Article 123. Master Netting Agreements Covering Repurchase Transactions, Securities and

Commodities Lending or Borrowing Transactions, and Other Capital Market-Driven Transactions

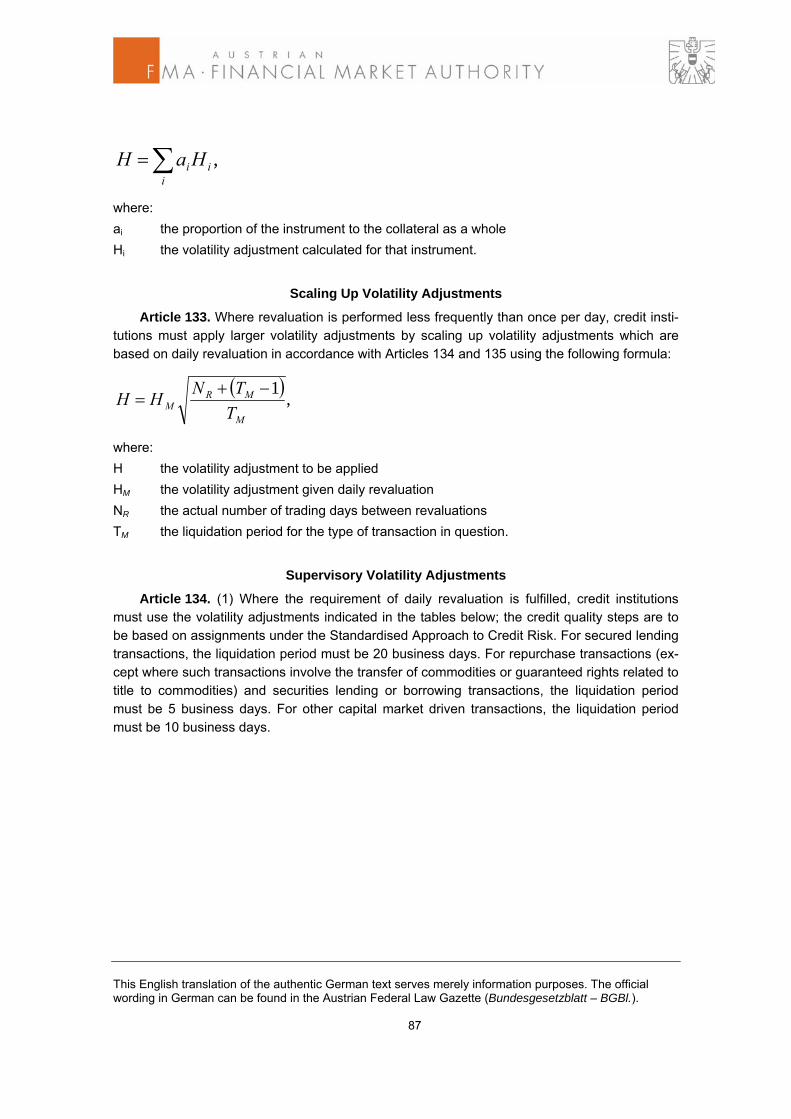

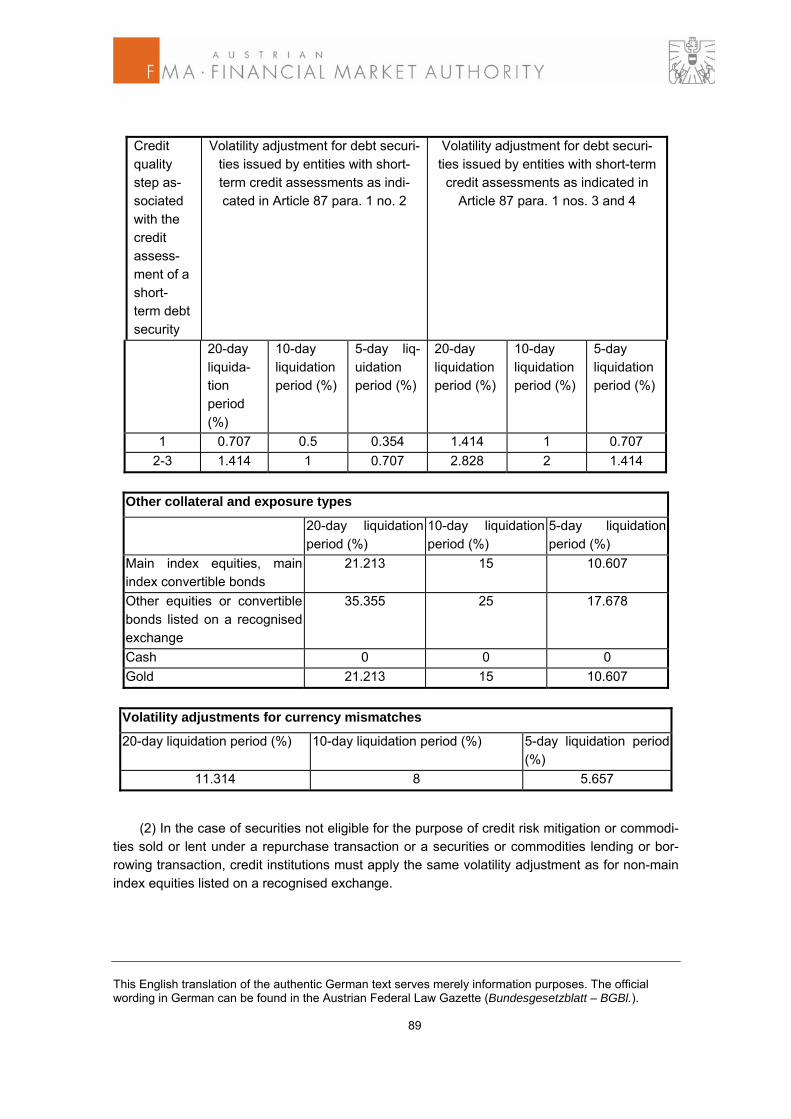

Article 124. Net Position in Commodities and Securities Article 125. Volatility Adjustments Article 126. Volatility Adjustment for Foreign Exchange Risk Article 127. Adjusted Exposure Value Article 128. Internal Model Method Subsection 3: Other Real Collateral Article 129. Financial Collateral Article 130. Financial Collateral Simple Method Article 131. Financial Collateral Comprehensive Method Article 132. Volatility Adjustments for the Value of Financial Collateral Article 133. Scaling Up Volatility Adjustments Article 134. Supervisory Volatility Adjustments Article 135. Own Estimates of Volatility Adjustments Article 136. Quantitative Requirements for Own Volatility Adjustments Article 137. Qualitative Requirements for Own Volatility Adjustments Article 138. Application of 0% Volatility Adjustments Article 139. Weighted Exposure Amounts and Expected Loss Amounts for Financial Collat-

eral Article 140. Other Collateral Eligible for the Purpose of Credit Risk Mitigation under the

Internal Ratings Based Approach Article 141. Alternative Valuation of Real Estate Collateral Article 142. Weighted Exposure Amounts and Expected Loss Amounts for Mixed Pools of

Collateral Article 143. Deposits with Third-Party Institutions Article 144. Pledged Life Insurance Policies Article 145. Collateral pursuant to Article 95 no. 3 Subsection 4: Personal Collateral Article 146. Valuation of Personal Collateral Article 147. Personal Collateral Denominated in Different Currencies Article 148. Weighted Exposure Amounts and Expected Loss Amounts for Securitisation

Transactions Article 149. Weighted Exposure Amounts and Expected Loss Amounts under the Standard-

ised Approach to Credit Risk Article 150. Weighted Exposure Amounts and Expected Loss Amounts under the Internal

Ratings Based Approach

This English translation of the authentic German text serves merely information purposes. The official wording in German can be found in the Austrian Federal Law Gazette (Bundesgesetzblatt – BGBl.). 7

Subsection 5: Accounting for Maturity Mismatches Article 151. Maturity Mismatches Article 152. Maturity Mismatches in Financial Collateral Article 153. Maturity Mismatches in Personal Collateral Subsection 6: Article 154. Basket Protection Subsection 7: Article 155. Combinations of Credit Risk Mitigation in the Standardised Approach

Chapter 4: Securitisation Positions Section 1: Calculation of Risk-Weighted Exposure Amounts and Expected Loss

Amounts

Article 156. Effective Transfer of Exposures in a Traditional Securitisation Article 157. Effective Transfer of Credit Risk in a Synthetic Securitisation Article 158. Calculation of Risk-Weighted Exposure Amounts for Exposure Portfolios Secu-

ritised in a Synthetic Securitisation pursuant to Article 22d para. 2 Banking Act Article 159. Treatment of Maturity Mismatches in Synthetic Securitisations Article 160. Calculation of Risk-Weighted Exposure Amounts – General Principles Article 161. Calculation of Risk-Weighted Exposure Amounts under the Standardised Ap-

proach to Credit Risk Article 162. Treatment of Securitisation Positions in a Second Loss Tranche or Better in an

ABCP Programme under the Standardised Approach to Credit Risk Article 163. Treatment of Unrated Liquidity Facilities under the Standardised Approach to

Credit Risk Article 164. Reduction of Risk-Weighted Exposure Amounts under the Standardised Ap-

proach Article 165. Calculation of Risk-Weighted Exposure Amounts under the Internal Ratings

Based Approach Article 166. Ratings Based Method Article 167. Use of Inferred Ratings under the Internal Ratings Based Approach Article 168. Internal Assessment Approach for Positions in ABCP Programmes under the

Internal Ratings Based Approach Article 169. Supervisory Formula Method Article 170. Liquidity Facilities under the Internal Ratings Based Approach Article 171. Recognition of Credit Risk Mitigation for Securitisation Positions under the In-

ternal Ratings Based Approach Article 172. Calculation of Minimum Capital Requirements for Securitisation Positions with

Credit Risk Mitigation under the Ratings Based Method Article 173. Calculation of Minimum Capital Requirements for Securitisation Positions with

Credit Risk Mitigation under the Supervisory Formula Method

This English translation of the authentic German text serves merely information purposes. The official wording in German can be found in the Austrian Federal Law Gazette (Bundesgesetzblatt – BGBl.). 8

Article 174. Reduction of Risk-Weighted Exposure Amounts under the Internal Ratings-

Based Approach Article 175. Calculation of Additional Risk-Weighted Exposure Amounts for Securitisations

of Revolving Exposures with Early Amortisation Provisions under the Standard-ised Approach to Credit Risk

Article 176. Calculation of Additional Risk-Weighted Exposure Amounts for Securitisations of Revolving Exposures with Early Amortisation Provisions under the Internal Ratings Based Approach

Article 177. Securitisations subject to early amortisation provisions and consisting of retail exposures which are uncommitted and unconditionally cancellable without prior notice

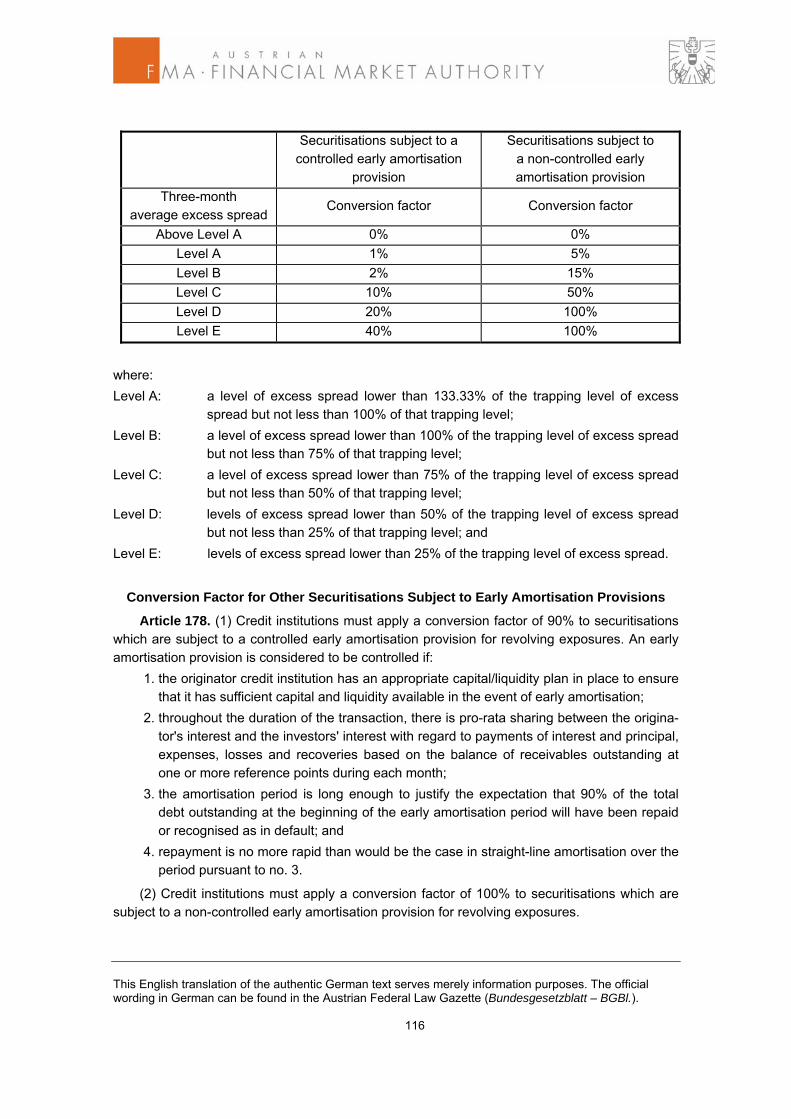

Article 178. Conversion Factor for Other Securitisations Subject to Early Amortisation Pro-visions

Article 179. Highest Minimum Capital Requirement for Securitisations of Revolving Expo-sures

Section 2: Use of Credit Assessments from External Credit Assessment Institutions

Article 180. Requirements for Credit Assessments Article 181. Use of Credit Assessments

Part 3: Operational Risk

Chapter 1: Basic Indicator Approach

Article 182. Minimum Capital Requirements Article 183. Relevant Indicator Article 184. Basis of the Relevant Indicator

Chapter 2: Standardised Approach

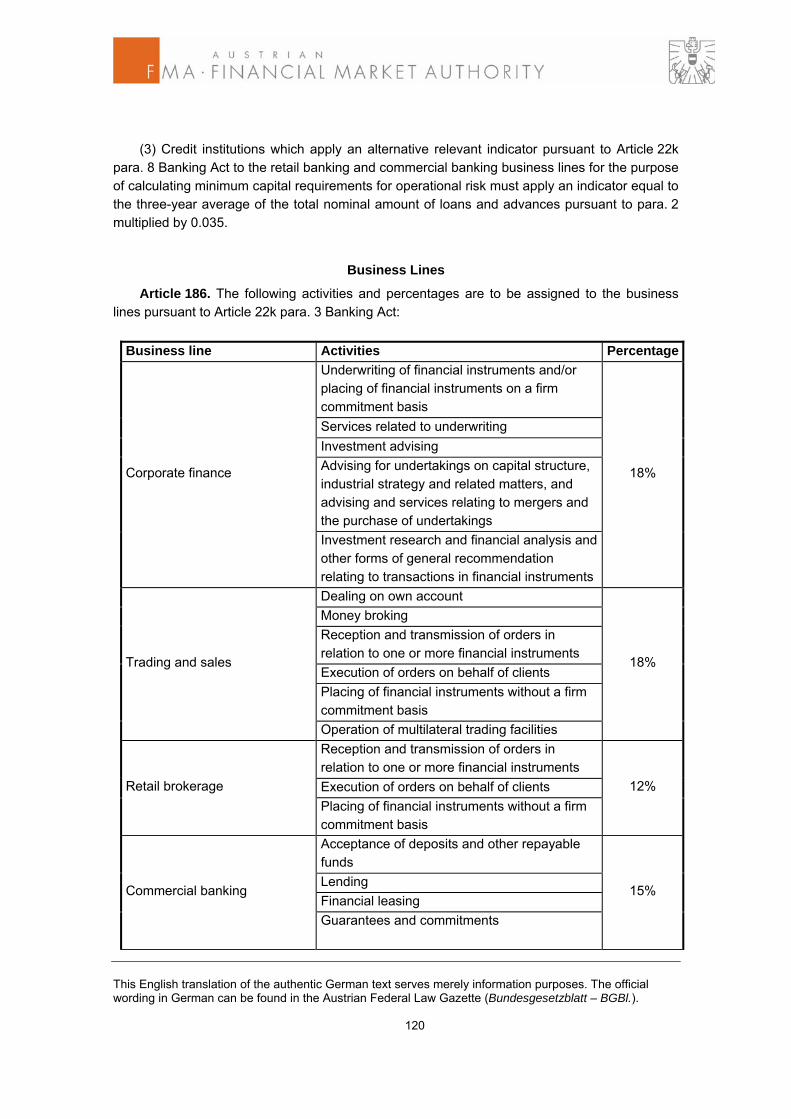

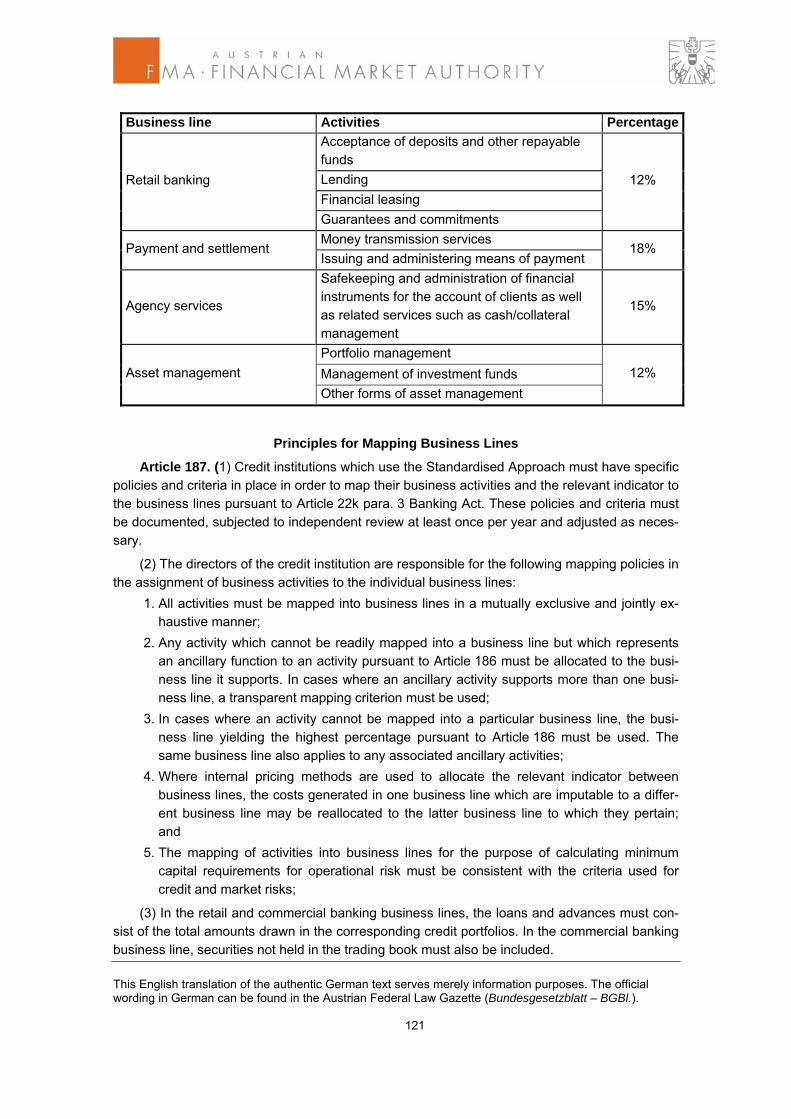

Article 185. Minimum Capital Requirements Article 186. Business Lines Article 187. Principles for Mapping Business Lines

Chapter 3: Advanced Measurement Approach

Article 188. Advanced Measurement Approach Article 189. Quantitative Standards Article 190. Internal Data Article 191. External Data Article 192. Scenario Analysis Article 193. Business Environment and Internal Control Factors Article 194. Recognition of Insurance and Other Risk Mitigation Techniques

This English translation of the authentic German text serves merely information purposes. The official wording in German can be found in the Austrian Federal Law Gazette (Bundesgesetzblatt – BGBl.). 9

Part 4: Risk Types Pursuant to Article 22o para. 2 Banking Act Chapter 1: Trading Book Section 1: General

Article 195. Trading Intent Article 196. Assignment to the Trading Book Article 197. Internal Hedges

Section 2: Valuation Methods

Article 198. Marking to Market Article 199. Marking to Model Article 200. Independent Price Verification Article 201. Valuation Adjustments or Reserves Article 202. Systems and Controls

Section 3: General Provisions Regarding Position Risk

Article 203. Netting of Positions and Currency Translation Article 204. Treatment of Derivatives Article 205. Position Risk in Repurchase Transactions and Securities Lending or Borrowing

Transactions

Section 4: Special Provisions Regarding Position Risk

Article 206. General and Specific Position Risk Article 207. Specific Position Risk Associated with Interest Rate Instruments Article 208. General Position Risk Associated with Interest Rate Instruments Article 209. Specific and General Position Risk Associated with Equity Instruments Article 210. General and Specific Position Risk Associated with Stock-Index Futures Article 211. Investment Fund Shares in the Trading Book Article 212. Specific Position Risk Associated with Trading Book Positions Hedged by

Credit Derivatives Article 213. Underwriting Article 214. Settlement Risk Article 215. Free Deliveries Article 216. Counterparty Credit Risk Article 217. Expected Loss Amounts for Counterparty Credit Risk

This English translation of the authentic German text serves merely information purposes. The official wording in German can be found in the Austrian Federal Law Gazette (Bundesgesetzblatt – BGBl.). 10

Chapter 2: Options Risk

Article 218. General Article 219. Gamma Risk Article 220. Vega Risk Article 221. Scenario Matrix Method

Chapter 3: Commodities Risk and Foreign Exchange Risk

Article 222. Minimum Capital Requirement for Commodities Risk Article 223. Minimum Capital Requirement for Foreign Exchange Risk

Chapter 4: Market Risk Models

Article 224. General Article 225. Qualitative Standards Article 226. Market Risk Factors Article 227. Quantitative Standards Article 228. Back-Testing Methods Article 229. Methods of Determining the Multiplier Article 230. Stress-Testing Methods Article 231. Combinations of Models and Standardised Methods Article 232. Criteria for the Approval of Models Used to Calculate Minimum Capital Re-

quirements for Specific Position Risk and Incremental Default Risk

Part 5: Counterparty Credit Risk of Derivative Instruments, Repurchase Transactions, Securities or Commodities Lending or Borrowing Transactions, Long Settlement Transactions and Margin Lending Transactions

Chapter 1: Specification of Application

Article 233. Specification of Application

Chapter 2: Mark-to-Market Method

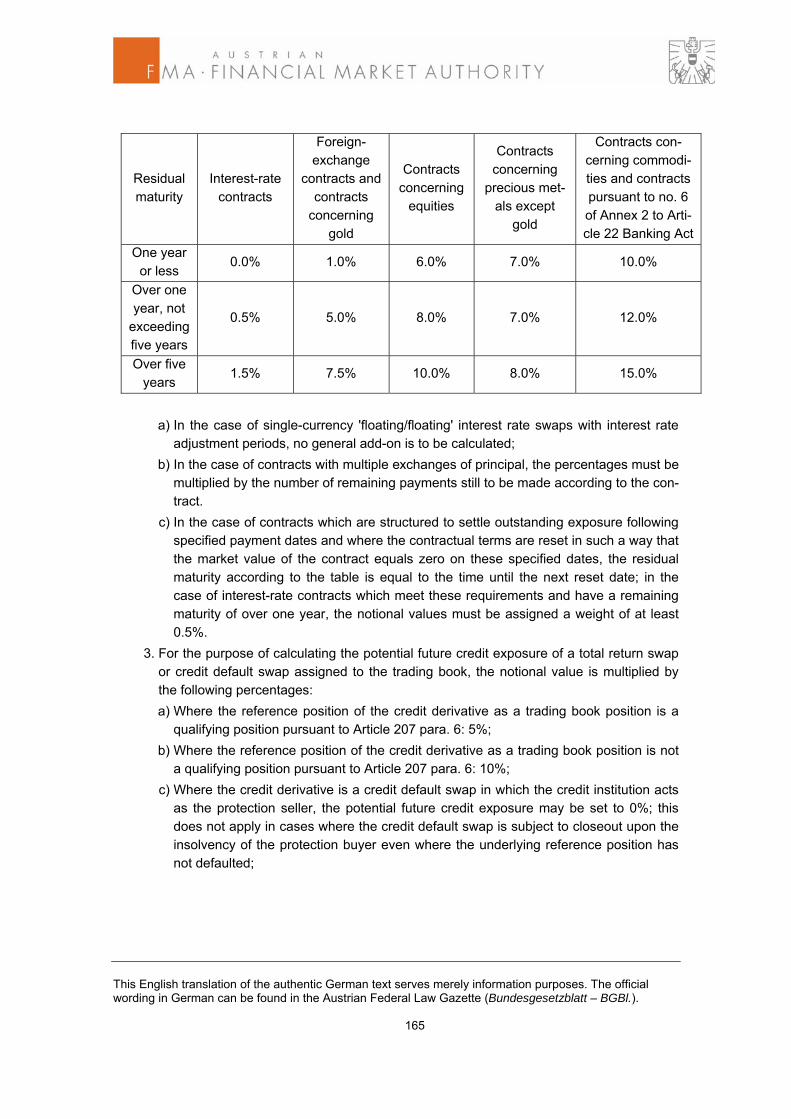

Article 234. Mark-to-Market Method

Chapter 3: Original Exposure Method

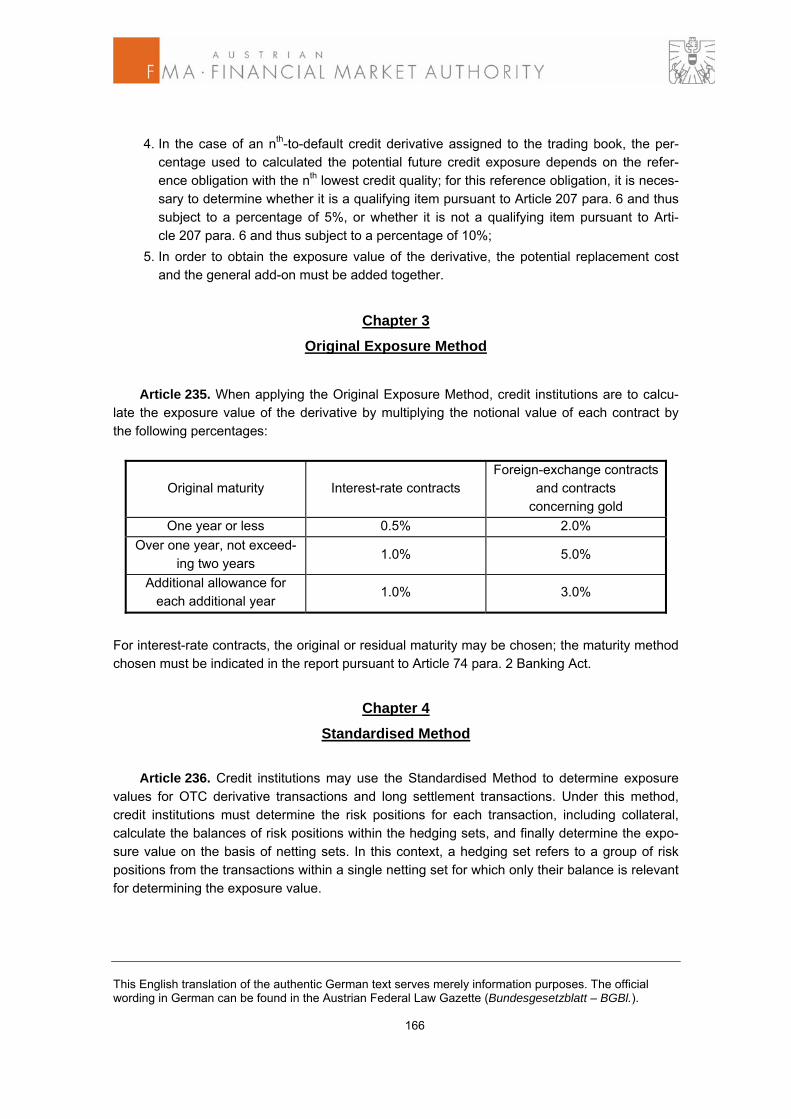

Article 235. Original Exposure Method

This English translation of the authentic German text serves merely information purposes. The official wording in German can be found in the Austrian Federal Law Gazette (Bundesgesetzblatt – BGBl.). 11

Chapter 4: Standardised Method

Article 236. Standardised Method Article 237. Payment Leg Article 238. Assignment to Risk Positions Article 239. Size of Risk Position Article 240. Hedging Set Article 241. Counterparty credit risk multiplier (CCRM) Article 242. Exposure Value Article 243. Internal Procedures

Chapter 5: Internal Model Method

Article 244. Internal Model Method Article 245. Exposure Value Article 246. Own Estimates of the Scaling Factor Article 247. Correlation of Market and Credit Risk Factors Article 248. Netting Sets with Margin Agreements Article 249. Organisational Unit for Counterparty Credit Risk Management Article 250. Counterparty Credit Risk Management Article 251. Stress Tests Article 252. Internal Auditing Article 253. Integration of the Model into the Risk Management System Article 254. Integrity of the Model Article 255. Model Validation

Chapter 6: Contractual Netting

Article 256. Contractual Netting Article 257. Types of Netting Agreements and Conditions for Application Article 258. Recognition of Netting Agreements Article 259. Netting Agreements: Potential Future Credit Exposure Article 260. Netting Agreements: Net-to-Gross Ratio Article 261. Netting Agreements under the Standardised Method and Internal Models

Part 6: Transitional and Final Provisions Article 262. Transitional Provisions Article 263. References Article 264. Repeals Article 265. Entry into Effect

This English translation of the authentic German text serves merely information purposes. The official wording in German can be found in the Austrian Federal Law Gazette (Bundesgesetzblatt – BGBl.). 12

Part 1: General Provisions

Purpose

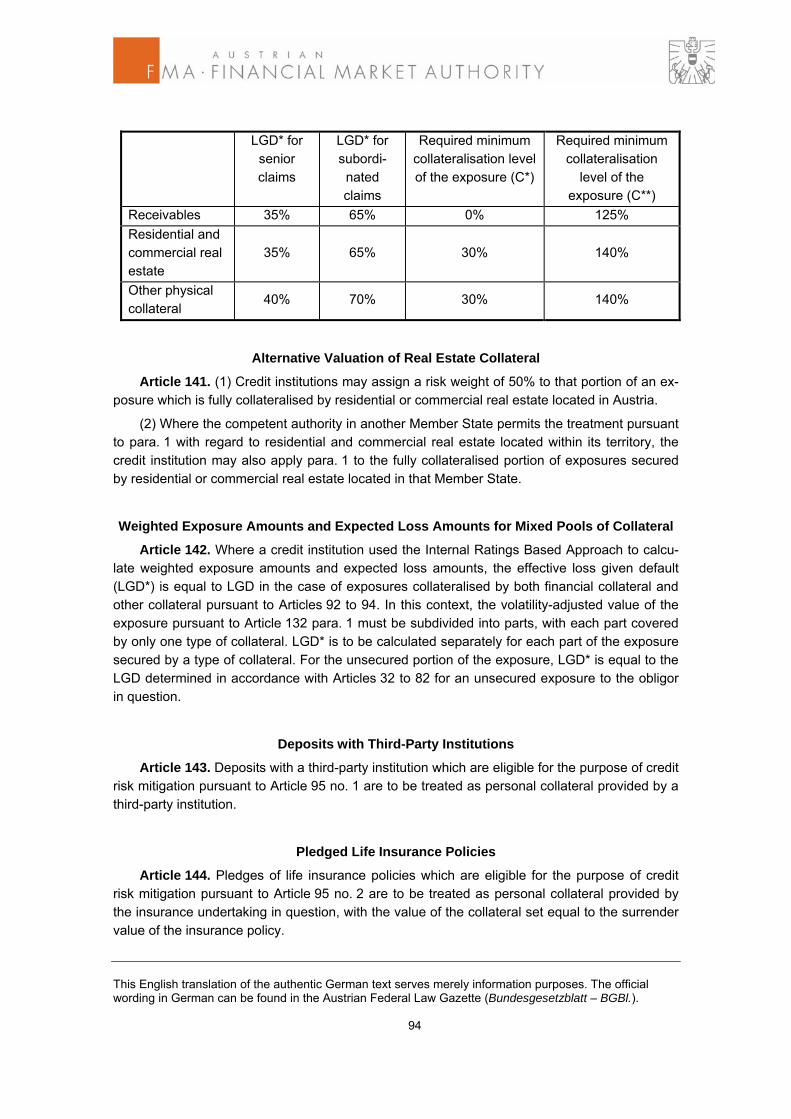

Article 1. This regulation serves to transpose Directive 2006/48/EC of the European Par-liament and of the Council relating to the taking up and pursuit of the business of credit institu-tions (OJ No. L 177 of 30 June 2006, p. 1) and Directive 2006/49/EC of the European Parlia-ment and of the Council on the capital adequacy of investment firms and credit institutions (OJ No. L 177 of 14 June 2006, p. 201) into Austrian law where those directives have not already been implemented in the Banking Act, Federal Law Gazette No. 532/1993 as last amended by Federal Law Gazette I No. 141/2006 or in other FMA regulations. This regulation governs the calculation of minimum capital requirements for credit institutions pursuant to Article 22 para. 1 Banking Act.

Definitions

Article 2. (1) For the purposes of this regulation, the terms listed below are defined as fol-lows: 1. Central counterparty: an entity that legally interposes itself between counterparties to

contracts traded within one or more financial markets, becoming the buyer to every seller and the seller to every buyer;

2. Long settlement transactions: transactions where a counterparty undertakes to deliver a security, a commodity, or a foreign exchange amount against cash, other financial in-struments, or commodities at a settlement or delivery date that is contractually specified as later than five business days after the date on which the credit institution enters into the transaction.

(2) For the purposes of Articles 156 to 179 (Securitisation positions), the terms listed below are defined as follows: 1. Kirb: 8% of the risk-weighted exposure amounts that would be calculated under the

Internal Ratings Based Approach in respect of the securitised exposures had they not been securitised, plus the amount of expected losses associated with those exposures calculated under those provisions;

2. Clean-up call option: a contractual option for the originator to repurchase or extinguish the securitisation positions before all of the underlying exposures have been repaid, when the amount of outstanding exposures falls below a specified level;

3. Excess spread: finance charge collections and other fee income received in respect of the securitised exposures net of costs and expenses;

4. Liquidity facility: a securitisation position arising from a contractual agreement to provide funding to ensure the timeliness of cash flows to investors;

5. Asset-backed commercial paper programme (ABCP program): a programme of securiti-sations in which the securities issued predominantly take the form of commercial paper with an original maturity of one year or less.

This English translation of the authentic German text serves merely information purposes. The official wording in German can be found in the Austrian Federal Law Gazette (Bundesgesetzblatt – BGBl.). 13

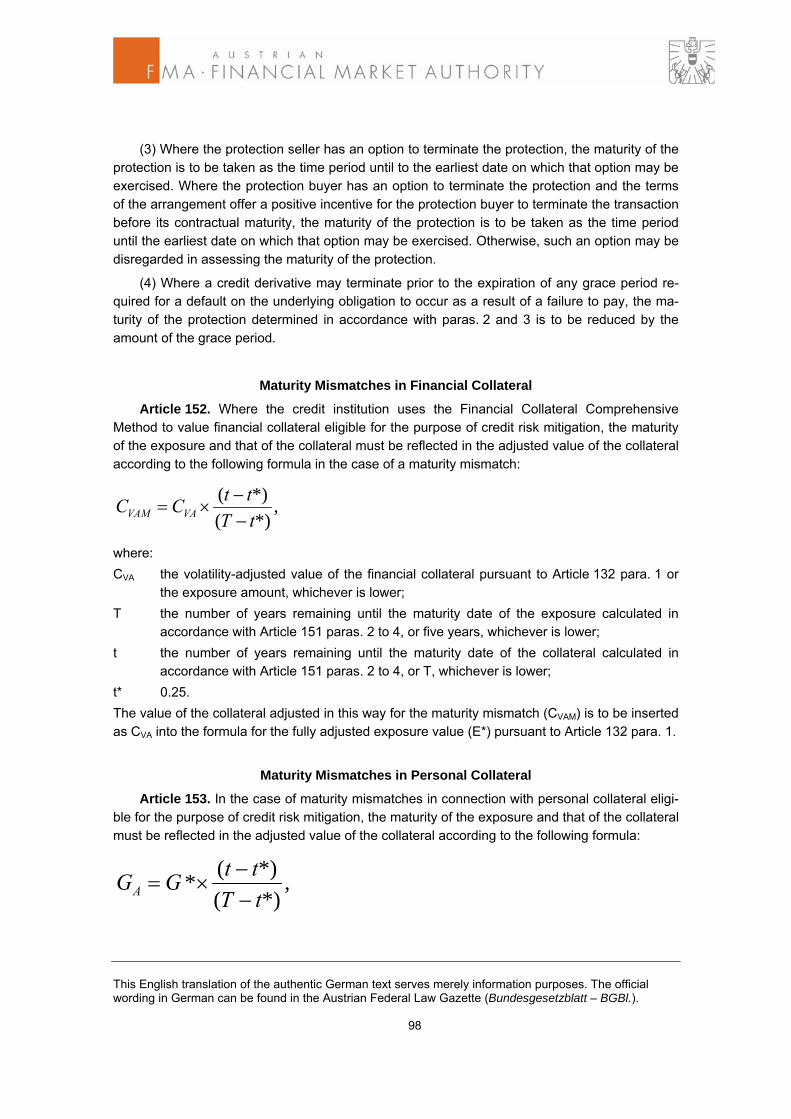

For the purposes of Articles 233 to 261 (Counterparty Credit Risk for Derivatives, Repur-chase Transactions, Securities or Commodities Lending Transactions, Long Settlement Trans-actions and Margin Lending Transactions), the terms listed below are defined as follows: 1. Derivatives: derivatives pursuant to Annex 2 to Article 22 Banking Act and, for credit

institutions which invoke Article 22q Banking Act, all over-the-counter (OTC) instruments in the trading book;

2. Netting set: a group of transactions with a single counterparty that are subject to a le-gally enforceable bilateral netting arrangement and for which netting is recognised under Articles 256 to 261 and Articles 22g to 22h Banking Act.

Part 2: Credit Risk

Chapter 1

Standardised Approach to Credit Risk

Section 1

General Provisions Article 3. In calculating their minimum capital requirements, credit institutions which apply

the Standardised Approach to Credit Risk pursuant to Article 22a Banking Act must adhere to the provisions set forth in this chapter with regard to 1. risk weights and the criteria for their assignment to exposure classes pursuant to Arti-

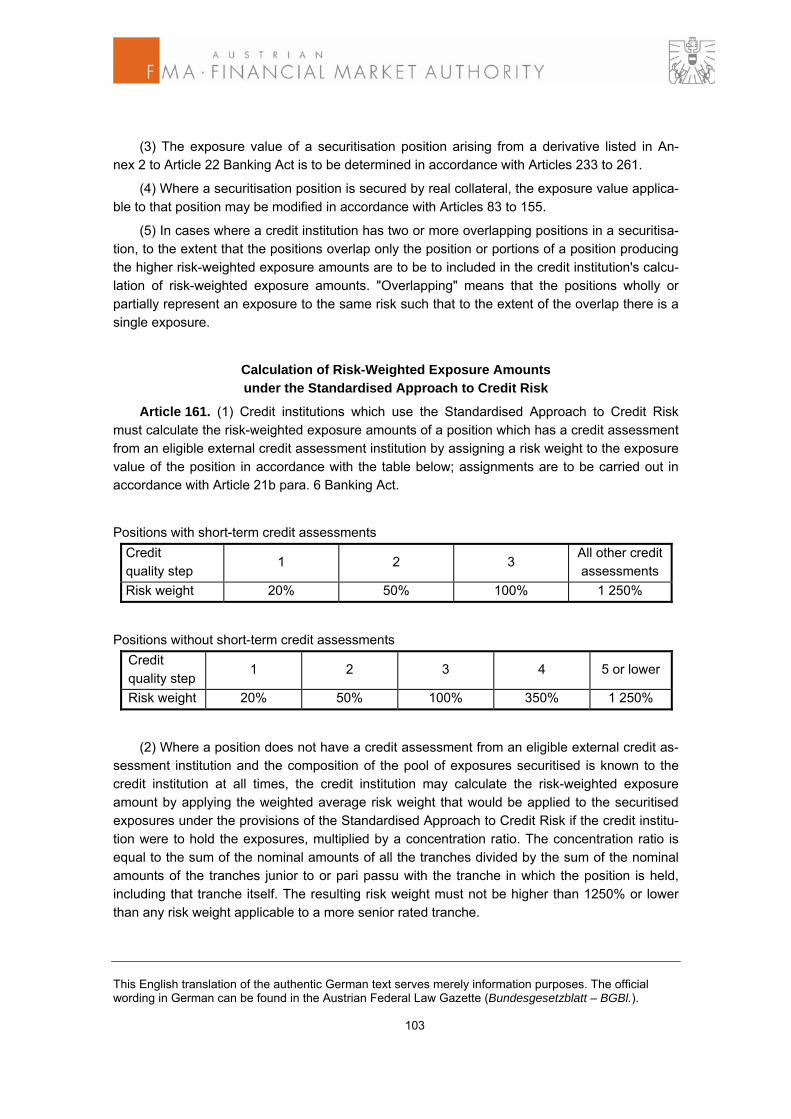

cle 22a para. 4 Banking Act and 2. the use of credit assessments from eligible external credit assessment institutions or

export credit agencies to calculate weights. .

Section 2

Risk Weights

Exposures to Central Governments or Central Banks

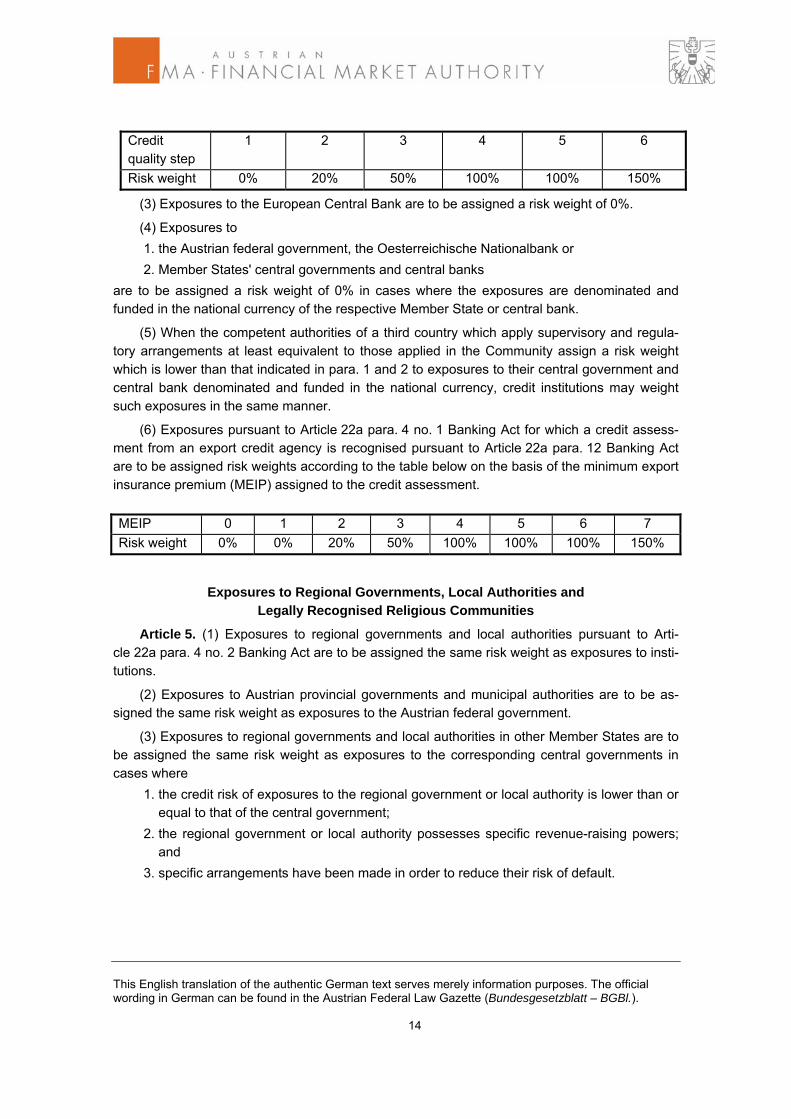

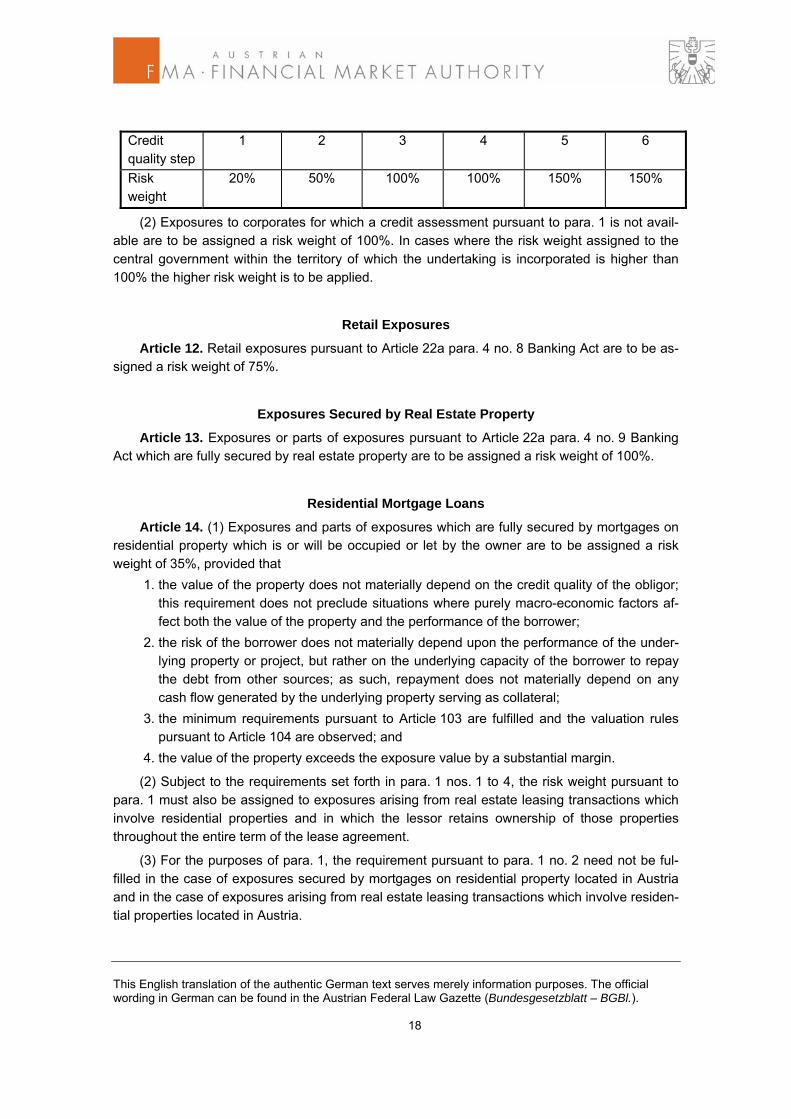

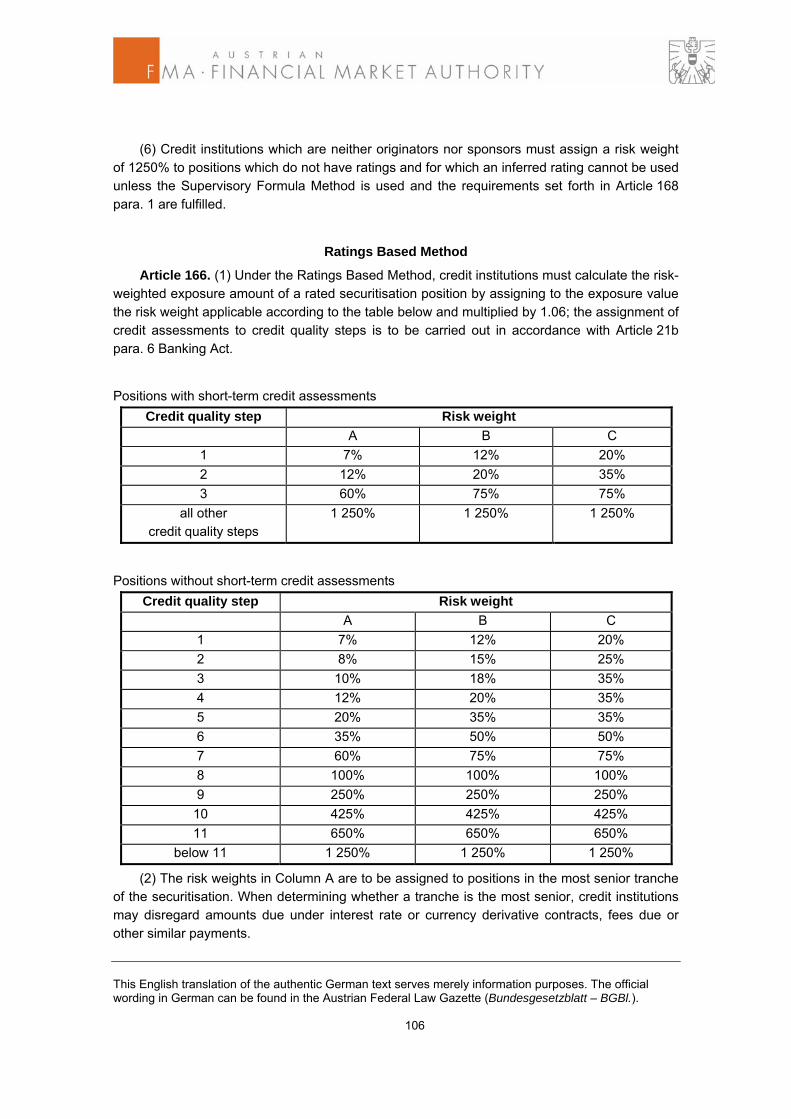

Article 4. (1) Exposures to central governments and central banks pursuant to Article 22a para. 4 no. 1 Banking Act are to be assigned a risk weight of 100%.

(2) Exposures pursuant to Article 22a para. 4 no. 1 Banking Act for which a credit assess-ment from an eligible external credit assessment institution is available are to be assigned risk weights according to the table below. Credit assessments are to be assigned to credit quality steps in accordance with Article 21b para. 6 Banking Act.

This English translation of the authentic German text serves merely information purposes. The official wording in German can be found in the Austrian Federal Law Gazette (Bundesgesetzblatt – BGBl.). 14

Credit quality step

1 2 3 4 5 6

Risk weight 0% 20% 50% 100% 100% 150%

(3) Exposures to the European Central Bank are to be assigned a risk weight of 0%.

(4) Exposures to 1. the Austrian federal government, the Oesterreichische Nationalbank or 2. Member States' central governments and central banks are to be assigned a risk weight of 0% in cases where the exposures are denominated and funded in the national currency of the respective Member State or central bank.

(5) When the competent authorities of a third country which apply supervisory and regula-tory arrangements at least equivalent to those applied in the Community assign a risk weight which is lower than that indicated in para. 1 and 2 to exposures to their central government and central bank denominated and funded in the national currency, credit institutions may weight such exposures in the same manner.

(6) Exposures pursuant to Article 22a para. 4 no. 1 Banking Act for which a credit assess-ment from an export credit agency is recognised pursuant to Article 22a para. 12 Banking Act are to be assigned risk weights according to the table below on the basis of the minimum export insurance premium (MEIP) assigned to the credit assessment. MEIP 0 1 2 3 4 5 6 7 Risk weight 0% 0% 20% 50% 100% 100% 100% 150%

Exposures to Regional Governments, Local Authorities and Legally Recognised Religious Communities

Article 5. (1) Exposures to regional governments and local authorities pursuant to Arti-cle 22a para. 4 no. 2 Banking Act are to be assigned the same risk weight as exposures to insti-tutions.

(2) Exposures to Austrian provincial governments and municipal authorities are to be as-signed the same risk weight as exposures to the Austrian federal government.

(3) Exposures to regional governments and local authorities in other Member States are to be assigned the same risk weight as exposures to the corresponding central governments in cases where 1. the credit risk of exposures to the regional government or local authority is lower than or

equal to that of the central government; 2. the regional government or local authority possesses specific revenue-raising powers;

and 3. specific arrangements have been made in order to reduce their risk of default.

This English translation of the authentic German text serves merely information purposes. The official wording in German can be found in the Austrian Federal Law Gazette (Bundesgesetzblatt – BGBl.). 15

(4) When the competent authorities of a third country jurisdiction which apply supervisory and regulatory arrangements at least equivalent to those applied in the Community treat expo-sures to regional governments and local authorities as exposures to their central government, credit institutions may weight exposures to such regional governments and local authorities in the same manner.

(5) Exposures to legally recognised religious communities are to be treated in the same manner as exposures to regional governments and local authorities. Paras. 2 and 3 are not applicable in this context.

Exposures to Public-Sector Entities, Administrative Bodies and Non-Commercial Undertakings

Article 6. (1) Exposures to public-sector entities, administrative bodies and non-commercial undertakings are to be assigned a risk weight of 100%.

(2) Exposures to public-sector entities and non-commercial undertakings pursuant to Arti-cle 22a para. 4 no. 3 Banking Act which are established in Austria are to be treated in the same manner as exposures to institutions; Article 10 para. 4 is not applicable in this context.

(3) Exposures to public-sector entities established in Austria may be assigned a risk weight of 0% in cases where the Austrian federal government has provided an appropriate guarantee for the exposure.

(4) In cases where exposures to public-sector entities established in other Member States are treated in the same manner as exposures to institutions or to the corresponding central government with the permission of the competent authority, credit institutions may treat expo-sures to those public-sector entities in the same manner.

(5) When the competent authorities of a third country jurisdiction treat exposures to the third country's public-sector entities as exposures to institutions, credit institutions may treat expo-sures to such public sector entities in the same manner if that third country applies supervisory and regulatory arrangements at least equivalent to those applied in the Community.

Exposures to Multilateral Development Banks

Article 7. (1) Exposures to multilateral development banks pursuant to Article 22a para. 4 no. 4 Banking Act, as well as exposures to the Inter-American Investment Corporation, the Black Sea Trade and Development Bank and the Central American Bank for Economic Integra-tion, for which a credit assessment from an eligible external credit assessment institution is available are to be assigned risk weights according to the table below. Credit assessments are to be assigned to credit quality steps in accordance with Article 21b para. 6 Banking Act.

Credit quality step

1 2 3 4 5 6

Risk weight 20% 50% 50% 100% 100% 150%

This English translation of the authentic German text serves merely information purposes. The official wording in German can be found in the Austrian Federal Law Gazette (Bundesgesetzblatt – BGBl.). 16

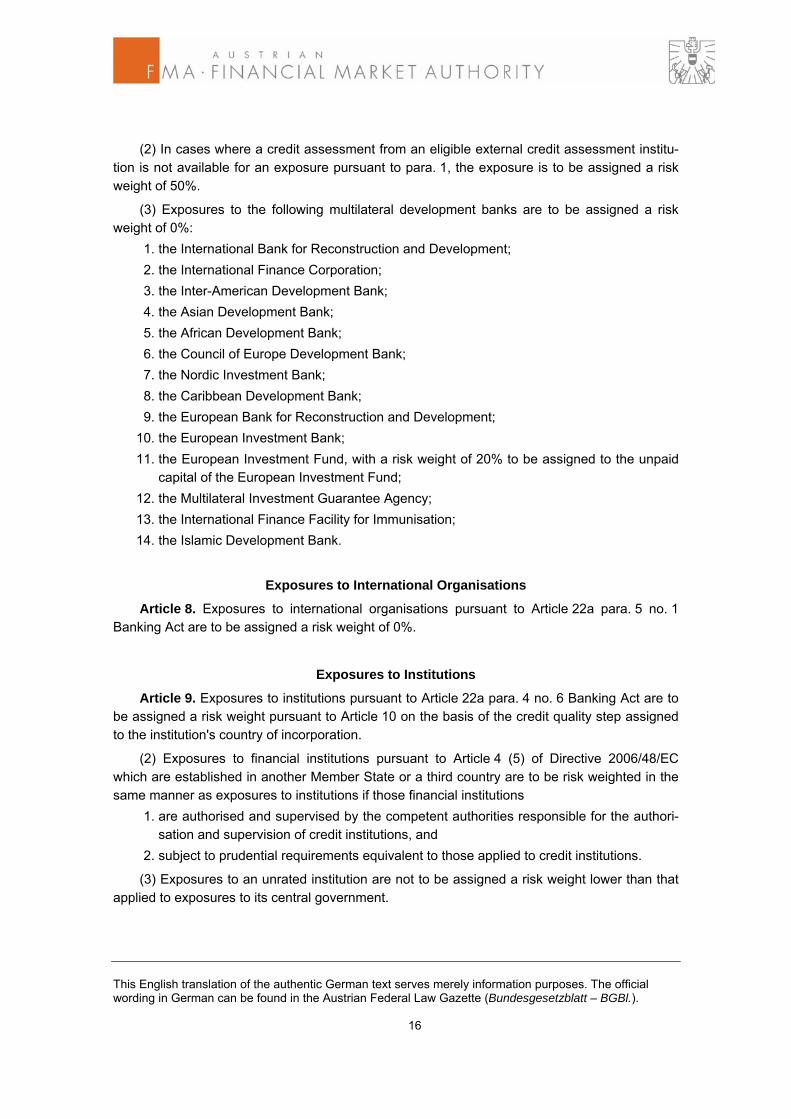

(2) In cases where a credit assessment from an eligible external credit assessment institu-tion is not available for an exposure pursuant to para. 1, the exposure is to be assigned a risk weight of 50%.

(3) Exposures to the following multilateral development banks are to be assigned a risk weight of 0%: 1. the International Bank for Reconstruction and Development; 2. the International Finance Corporation; 3. the Inter-American Development Bank; 4. the Asian Development Bank; 5. the African Development Bank; 6. the Council of Europe Development Bank; 7. the Nordic Investment Bank; 8. the Caribbean Development Bank; 9. the European Bank for Reconstruction and Development; 10. the European Investment Bank; 11. the European Investment Fund, with a risk weight of 20% to be assigned to the unpaid

capital of the European Investment Fund; 12. the Multilateral Investment Guarantee Agency; 13. the International Finance Facility for Immunisation; 14. the Islamic Development Bank.

Exposures to International Organisations

Article 8. Exposures to international organisations pursuant to Article 22a para. 5 no. 1 Banking Act are to be assigned a risk weight of 0%.

Exposures to Institutions

Article 9. Exposures to institutions pursuant to Article 22a para. 4 no. 6 Banking Act are to be assigned a risk weight pursuant to Article 10 on the basis of the credit quality step assigned to the institution's country of incorporation.

(2) Exposures to financial institutions pursuant to Article 4 (5) of Directive 2006/48/EC which are established in another Member State or a third country are to be risk weighted in the same manner as exposures to institutions if those financial institutions 1. are authorised and supervised by the competent authorities responsible for the authori-

sation and supervision of credit institutions, and 2. subject to prudential requirements equivalent to those applied to credit institutions.

(3) Exposures to an unrated institution are not to be assigned a risk weight lower than that applied to exposures to its central government.

This English translation of the authentic German text serves merely information purposes. The official wording in German can be found in the Austrian Federal Law Gazette (Bundesgesetzblatt – BGBl.). 17

Assignment of Weights for Exposures to Institutions

Article 10. (1) Exposures to institutions are to be assigned a risk weight according to the credit quality step assigned to the central government of the jurisdiction in which the institution is incorporated in accordance with the table below. Credit quality step to which central government is assigned

1 2 3 4 5 6

Risk weight 20% 50% 100% 100% 100% 150%

(2) Exposures to institutions incorporated in countries where the central government is un-rated are to be assigned a risk weight of 100%.

(3) Exposures to institutions with an original maturity of three months or less are to be as-signed a risk weight of 20%.

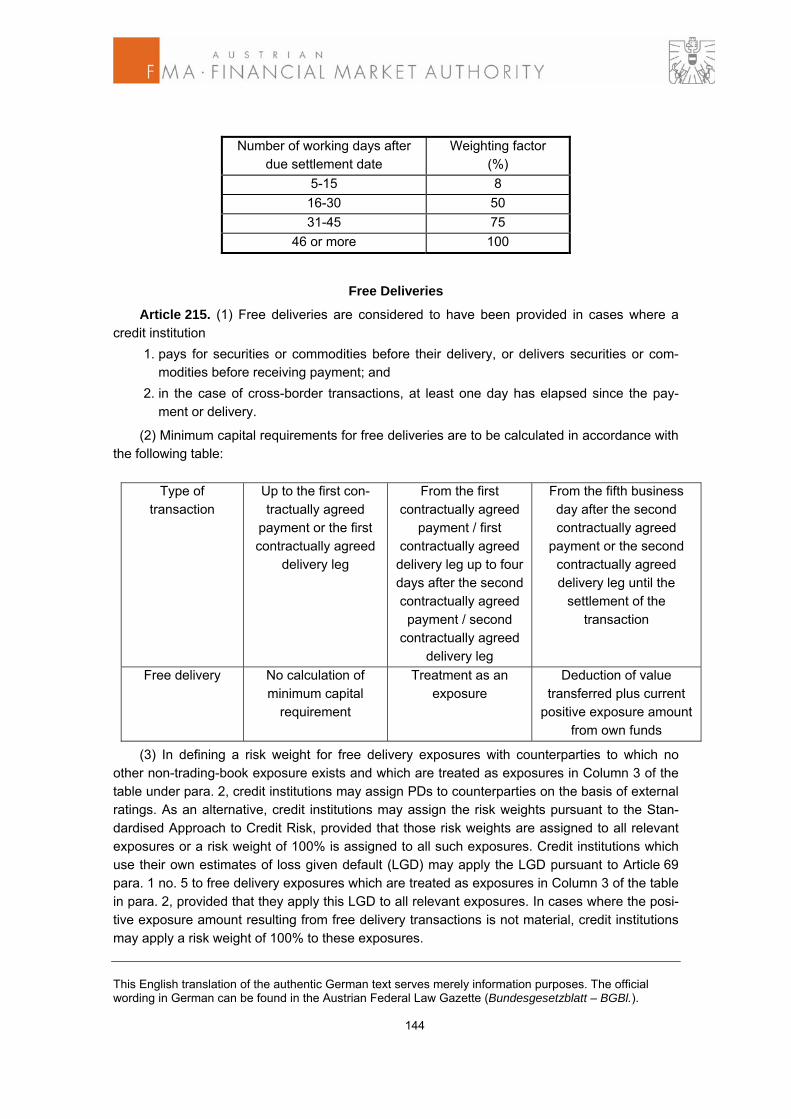

(4) Exposures to institutions with a residual maturity of three months or less denominated and funded in the national currency are to be assigned a risk weight that is one credit quality step below the more favourable weight applicable to exposures to the respective central gov-ernment pursuant to Article 4 paras. 4 and 5.

(5) Investments in equity or regulatory capital instruments issued by institutions are to be risk weighted at 100% unless they are deducted from own funds pursuant to Article 23 para. 13 Banking Act.

(6) Exposures to institutions in the form of minimum reserves required by the ECB or by the Oesterreichische Nationalbank to be held by the credit institution may be assigned the risk weight applied to exposures to the Austrian federal government, provided that 1. the reserves are held in accordance with Regulation (EC) No. 1745/2003 of the Euro-

pean Central Bank of 12 September 2003 or a subsequent replacement regulation, or in accordance with national requirements in all material respects equivalent to that Regula-tion; and

2. in the event of the insolvency of the institution where the reserves are held, the reserves are fully repaid to the credit institution in a timely manner and are not made available to meet other liabilities of the institution.

(7) The liquidity reserve held in accordance with Article 25 para. 13 Banking Act is to be as-signed a risk weight of 0%.

Exposures to Corporates

Article 11. (1) Exposures to corporates pursuant to Article 22a para. 4 no. 7 Banking Act for which a credit assessment from an eligible external credit assessment institution is available are to be assigned risk weights according to the table below. Credit assessments are to be as-signed to credit quality steps in accordance with Article 21b para. 6 Banking Act.

This English translation of the authentic German text serves merely information purposes. The official wording in German can be found in the Austrian Federal Law Gazette (Bundesgesetzblatt – BGBl.). 18

Credit quality step

1 2 3 4 5 6

Risk weight

20% 50% 100% 100% 150% 150%

(2) Exposures to corporates for which a credit assessment pursuant to para. 1 is not avail-able are to be assigned a risk weight of 100%. In cases where the risk weight assigned to the central government within the territory of which the undertaking is incorporated is higher than 100% the higher risk weight is to be applied.

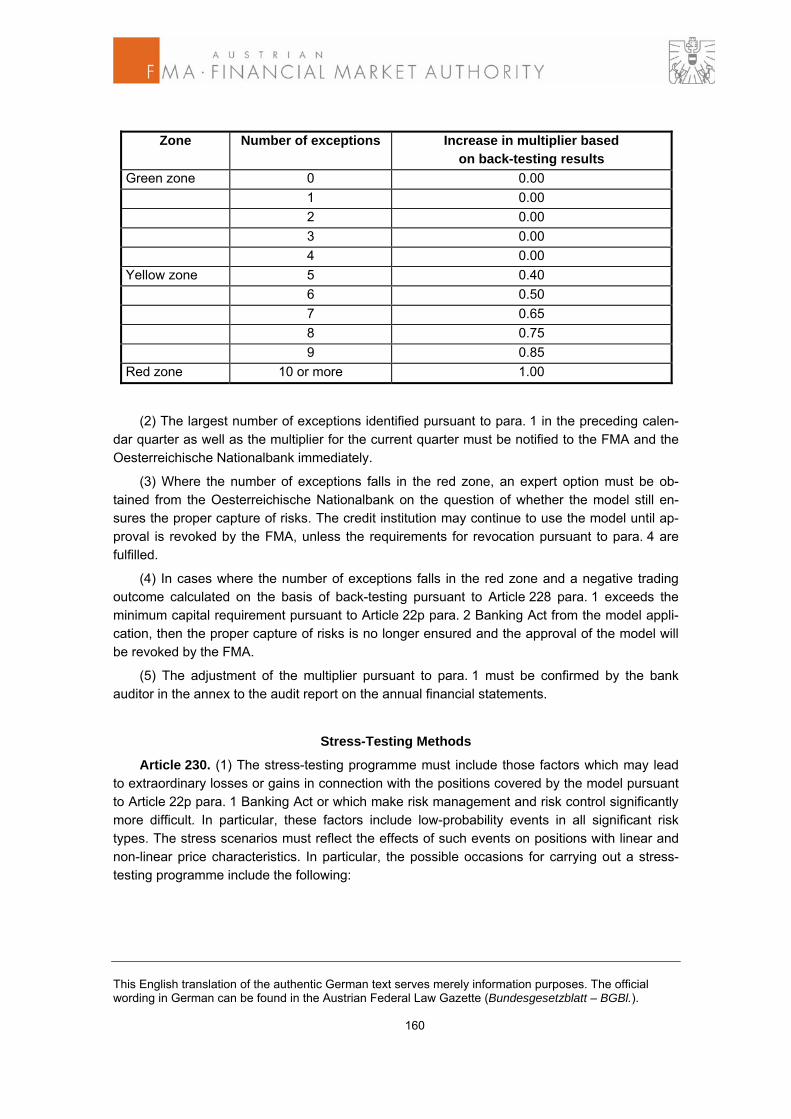

Retail Exposures

Article 12. Retail exposures pursuant to Article 22a para. 4 no. 8 Banking Act are to be as-signed a risk weight of 75%.

Exposures Secured by Real Estate Property

Article 13. Exposures or parts of exposures pursuant to Article 22a para. 4 no. 9 Banking Act which are fully secured by real estate property are to be assigned a risk weight of 100%.

Residential Mortgage Loans

Article 14. (1) Exposures and parts of exposures which are fully secured by mortgages on residential property which is or will be occupied or let by the owner are to be assigned a risk weight of 35%, provided that 1. the value of the property does not materially depend on the credit quality of the obligor;

this requirement does not preclude situations where purely macro-economic factors af-fect both the value of the property and the performance of the borrower;

2. the risk of the borrower does not materially depend upon the performance of the under-lying property or project, but rather on the underlying capacity of the borrower to repay the debt from other sources; as such, repayment does not materially depend on any cash flow generated by the underlying property serving as collateral;

3. the minimum requirements pursuant to Article 103 are fulfilled and the valuation rules pursuant to Article 104 are observed; and

4. the value of the property exceeds the exposure value by a substantial margin.

(2) Subject to the requirements set forth in para. 1 nos. 1 to 4, the risk weight pursuant to para. 1 must also be assigned to exposures arising from real estate leasing transactions which involve residential properties and in which the lessor retains ownership of those properties throughout the entire term of the lease agreement.

(3) For the purposes of para. 1, the requirement pursuant to para. 1 no. 2 need not be ful-filled in the case of exposures secured by mortgages on residential property located in Austria and in the case of exposures arising from real estate leasing transactions which involve residen-tial properties located in Austria.

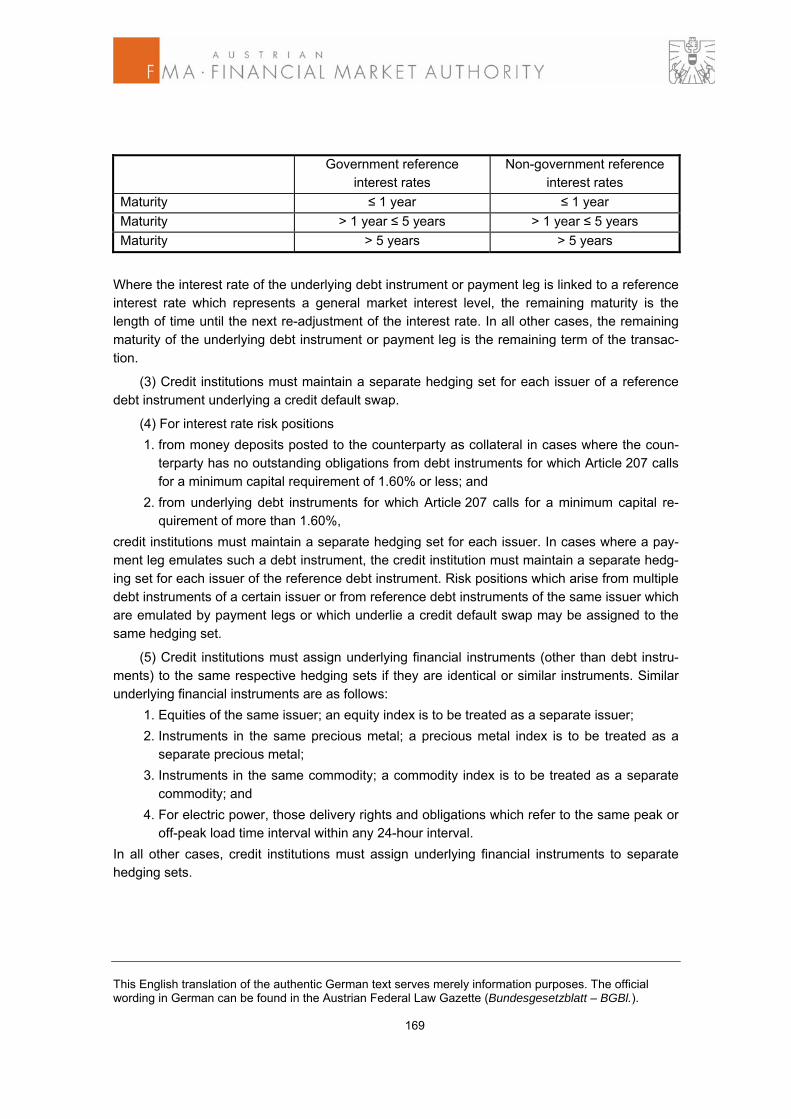

This English translation of the authentic German text serves merely information purposes. The official wording in German can be found in the Austrian Federal Law Gazette (Bundesgesetzblatt – BGBl.). 19

(4) Exposures which are fully secured by mortgages on residential properties located within the territory of another Member State as well as exposures arising from real estate leasing transactions which involve residential properties located in another Member State may be as-signed a risk weight of 35% where the requirement pursuant to para. 1 no. 2 is not fulfilled if the competent authorities in the Member State in question waive that requirement.

Commercial Mortgage Loans

Article 15. (1) In the case of exposures or parts of exposures which are fully secured by mortgages on offices or other commercial premises (commercial real estate property) located in Austria, that part of the exposure which does not exceed 50% of the property's market value or 60% of the property's mortgage lending value, whichever is lower, may be assigned a risk weight of 50%, provided the requirements pursuant to Article 14 para. 1 nos. 1 and 3 are ful-filled. The portion of the exposure which exceeds the limit is to be assigned a risk weight of 100%.

(2) Where the requirements pursuant to Article 14 para. 1 nos. 1 and 3 are fulfilled and the credit institution's exposure is fully secured by its ownership of the property, the weight pursuant to para. 1 is to be applied to exposures arising from real estate leasing transactions which in-volve commercial real estate properties located in Austria and in which the credit institution act-ing as lessor retains ownership of those properties throughout the entire term of the lease agreement.

(3) Exposures pursuant to para. 1 which are fully secured by mortgages on commercial real estate property in another Member State and exposures pursuant to para. 2 which involve commercial real estate property in another Member State may be assigned a risk weight of 50% if and to the extent that such treatment is permitted in the Member State in question.

(4) Exposures which are fully secured by mortgages on commercial real estate properties located within the territory of another Member State as well as exposures arising from real es-tate leasing transactions which involve commercial real estate properties located in another Member State may be assigned a risk weight of 50% where the requirement pursuant to Arti-cle 14 para. 1 no. 2 is not fulfilled if the competent authorities in the Member State in question waive that requirement.

Past Due Exposures

Article 16. (1) The secured part of a material past due exposure pursuant to Article 22a para. 4 no. 10 Banking Act is to be assigned a risk weight of: 1. 100% in cases where value adjustments are no less than 20% of the unsecured part of

the exposure gross of value adjustments, or where the exposure is fully secured by col-lateral pursuant to Article 22h para. 1 Banking Act, the specific minimum requirements pursuant to Articles 100 to 118 are not fulfilled, the credit institution has ensured the good quality of the collateral using strict operational criteria and value adjustments amount to 15% of the exposure gross of value adjustments;

2. 150% in all other cases.

This English translation of the authentic German text serves merely information purposes. The official wording in German can be found in the Austrian Federal Law Gazette (Bundesgesetzblatt – BGBl.). 20

(2) An obligation is considered material in accordance with Article 22b para. 4 no. 10 Bank-ing Act when, on the basis of the total items due and the credit facility/limit, the customer's total past due instalments including unpaid charges and interest as well as overruns of overdraft limits are greater than 2.5% of the total of all overdraft limits advised to the customer (adjusted for exchange rate fluctuations) and exceed an amount of EUR 250.

(3) For the purpose of defining the secured part of the past due item, the same collateral as that eligible for credit risk mitigation purposes may be used.

(4) In the case of past due exposures secured by residential real estate properties, those exposures which are weighted at 35% must be assigned a risk weight of 50% if value adjust-ments are no less than 20% of the exposure gross of value adjustments; otherwise, they are to be assigned a risk weight of 100% of the exposure net of value adjustments. Past due expo-sures secured by commercial real estate property are to be assigned a risk weight of 100%.

High-Risk Items

Article 17. (1) High-risk exposures pursuant to Article 22a para. 5 no. 4 Banking Act and exposures in the form of high-risk investment fund shares are to be assigned a risk weight of 150%.

(2) Non past due items which are assigned a risk weight of 150% pursuant to Articles 4 to 28 and para. 1 and for which value adjustments have been established may be assigned a risk weight of: 1. 100% if value adjustments are no less than 20% of the exposure value gross of value

adjustments; and 2. 50% if value adjustments are no less than 50% of the exposure value gross of value

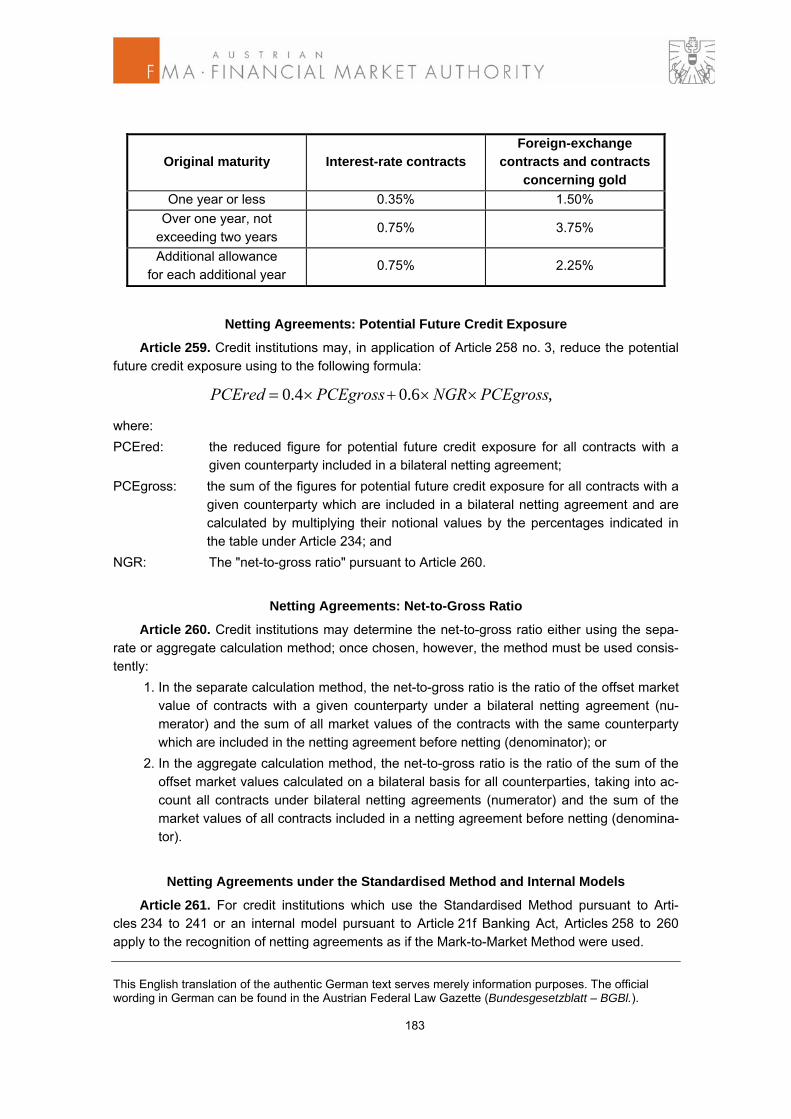

adjustments.

Exposures in the Form of Covered Bonds

Article 18. (1) Covered bonds mean bonds as defined in Article 20 para. 3 no. 7 Invest-ment Fund Act 1993 (Investmentfondsgesetz – InvFG 1993) and collateralised by any of the following assets: 1. Exposures to or guaranteed by a) the Austrian federal government or the central governments of Member States; b) Austrian provincial governments, municipal authorities or public-sector entities, and

regional governments, local authorities or public-sector entities in other Member States;

c) the central governments and central banks of third countries, multilateral development banks or international organisations that qualify for credit quality step 1 in the Stan-dardised Approach to Credit Risk or at least credit quality step 2 in the Standardised Approach to Credit Risk provided that the exposures do not exceed 20% of the nomi-nal amount of outstanding covered bonds of the issuing institution; or

This English translation of the authentic German text serves merely information purposes. The official wording in German can be found in the Austrian Federal Law Gazette (Bundesgesetzblatt – BGBl.). 21

d) Regional governments or local authorities in third countries or other public-sector

entities which are risk weighted as exposures to institutions or central governments and central banks pursuant to Article 5 para. 4 or Article 6 para. 5, and qualify for credit quality step 1 or at least credit quality step 2 in the Standardised Approach to Credit Risk provided that the exposures do not exceed 20% of the nominal amount of outstanding covered bonds of the issuing institution.

2. Exposures to institutions which qualify for credit quality step 1 in the Standardised Ap-proach to Credit Risk where the total exposure does not exceed 15% of the nominal amount of outstanding covered bonds of the issuing institution; this limit does not apply to exposures caused by the transmission and management of payments of the obligors of, or liquidation proceeds in respect of, loans secured by real estate to the holders of covered bonds;

3. short-term exposures to institutions with a maturity not exceeding 100 days which qual-ify as a minimum for credit quality step 2 in the Standardised Approach to Credit Risk;

4. mortgages on residential real estate up to 80% of the value of the pledged properties or the principal amount of the liens combined with any prior liens, whichever value is lower;

5. mortgages on commercial real estate up to 60% of the value of the pledged properties or the principal amount of the liens combined with any prior liens, whichever value is lower;

6. liens on ships where the total amount of such liens combined with any senior liens does not exceed 60% of the value of the pledged ships.

(2) For the purposes of para. 1, collateralisation includes situations where the assets de-scribed in para. 1 nos. 1 to 6 are exclusively dedicated in law to the protection of the bondhold-ers against losses.

Additional Requirements for Covered Bonds Secured by Real Estate

Article 19. Where covered bonds are collateralised by real estate, credit institutions must meet the minimum requirements set forth in Article 103 and observe the valuation rules set forth in Article 104.

Weighting of Exposures in the Form of Covered Bonds

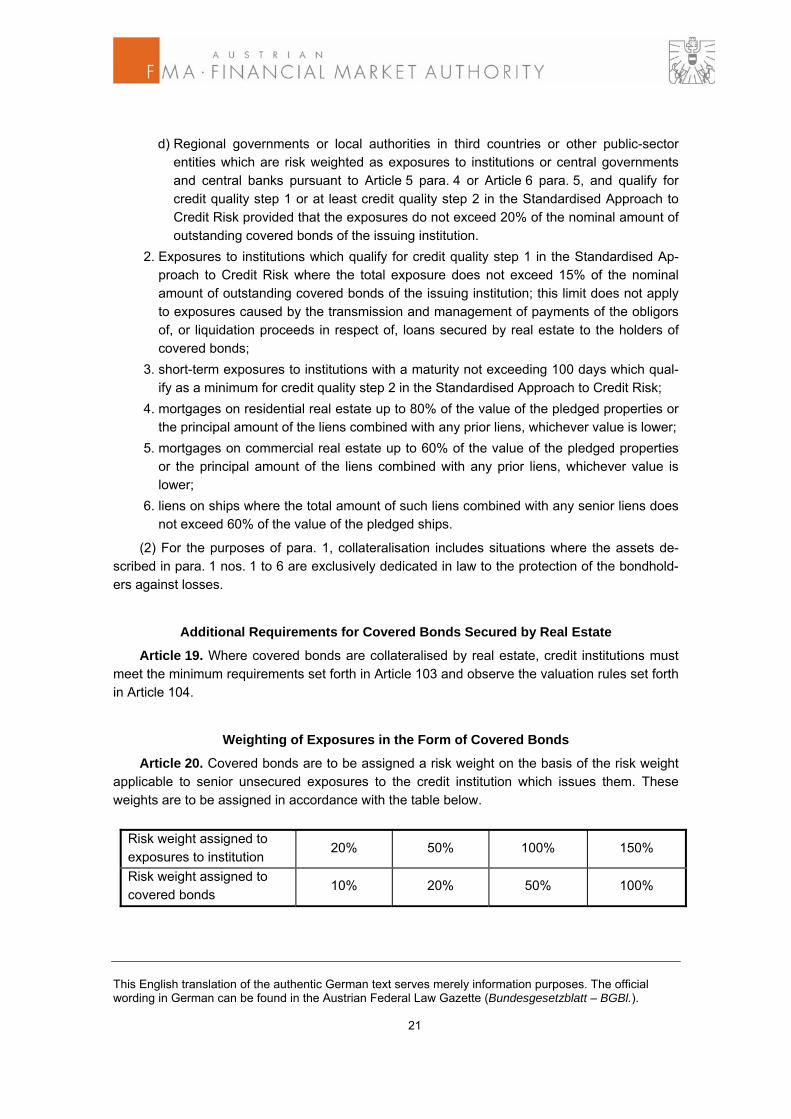

Article 20. Covered bonds are to be assigned a risk weight on the basis of the risk weight applicable to senior unsecured exposures to the credit institution which issues them. These weights are to be assigned in accordance with the table below.

Risk weight assigned to exposures to institution

20% 50% 100% 150%

Risk weight assigned to covered bonds

10% 20% 50% 100%

This English translation of the authentic German text serves merely information purposes. The official wording in German can be found in the Austrian Federal Law Gazette (Bundesgesetzblatt – BGBl.). 22

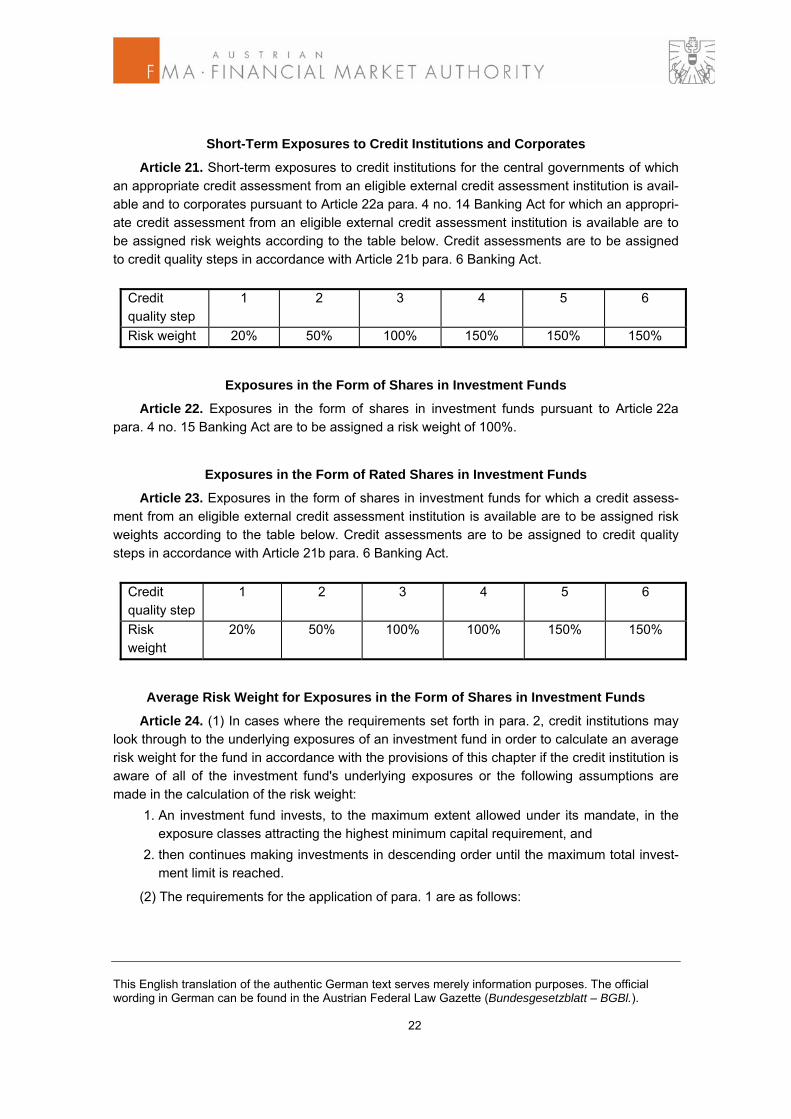

Short-Term Exposures to Credit Institutions and Corporates

Article 21. Short-term exposures to credit institutions for the central governments of which an appropriate credit assessment from an eligible external credit assessment institution is avail-able and to corporates pursuant to Article 22a para. 4 no. 14 Banking Act for which an appropri-ate credit assessment from an eligible external credit assessment institution is available are to be assigned risk weights according to the table below. Credit assessments are to be assigned to credit quality steps in accordance with Article 21b para. 6 Banking Act.

Credit quality step

1 2 3 4 5 6

Risk weight 20% 50% 100% 150% 150% 150%

Exposures in the Form of Shares in Investment Funds

Article 22. Exposures in the form of shares in investment funds pursuant to Article 22a para. 4 no. 15 Banking Act are to be assigned a risk weight of 100%.

Exposures in the Form of Rated Shares in Investment Funds

Article 23. Exposures in the form of shares in investment funds for which a credit assess-ment from an eligible external credit assessment institution is available are to be assigned risk weights according to the table below. Credit assessments are to be assigned to credit quality steps in accordance with Article 21b para. 6 Banking Act.

Credit quality step

1 2 3 4 5 6

Risk weight

20% 50% 100% 100% 150% 150%

Average Risk Weight for Exposures in the Form of Shares in Investment Funds

Article 24. (1) In cases where the requirements set forth in para. 2, credit institutions may look through to the underlying exposures of an investment fund in order to calculate an average risk weight for the fund in accordance with the provisions of this chapter if the credit institution is aware of all of the investment fund's underlying exposures or the following assumptions are made in the calculation of the risk weight: 1. An investment fund invests, to the maximum extent allowed under its mandate, in the

exposure classes attracting the highest minimum capital requirement, and 2. then continues making investments in descending order until the maximum total invest-

ment limit is reached.

(2) The requirements for the application of para. 1 are as follows:

This English translation of the authentic German text serves merely information purposes. The official wording in German can be found in the Austrian Federal Law Gazette (Bundesgesetzblatt – BGBl.). 23

1. The investment fund is managed by a credit institution pursuant to Article 1 para. 1

no. 13 or a company which is subject to supervision in a Member State, or the invest-ment fund is managed by a company incorporated in a third country and subject to gov-ernment supervision which is considered equivalent to that laid down in Community law and cooperation between the competent authorities is sufficiently ensured;

2. The investment fund's prospectus or equivalent document includes information on: a) the categories of assets in which the investment fund is authorised to invest; and b) if investment limits apply, the relative limits and the methodologies to calculate them;

and 3. the business of the investment fund is reported on at least an annual basis to enable an

assessment to be made of its assets and liabilities, income and operations over the re-porting period.

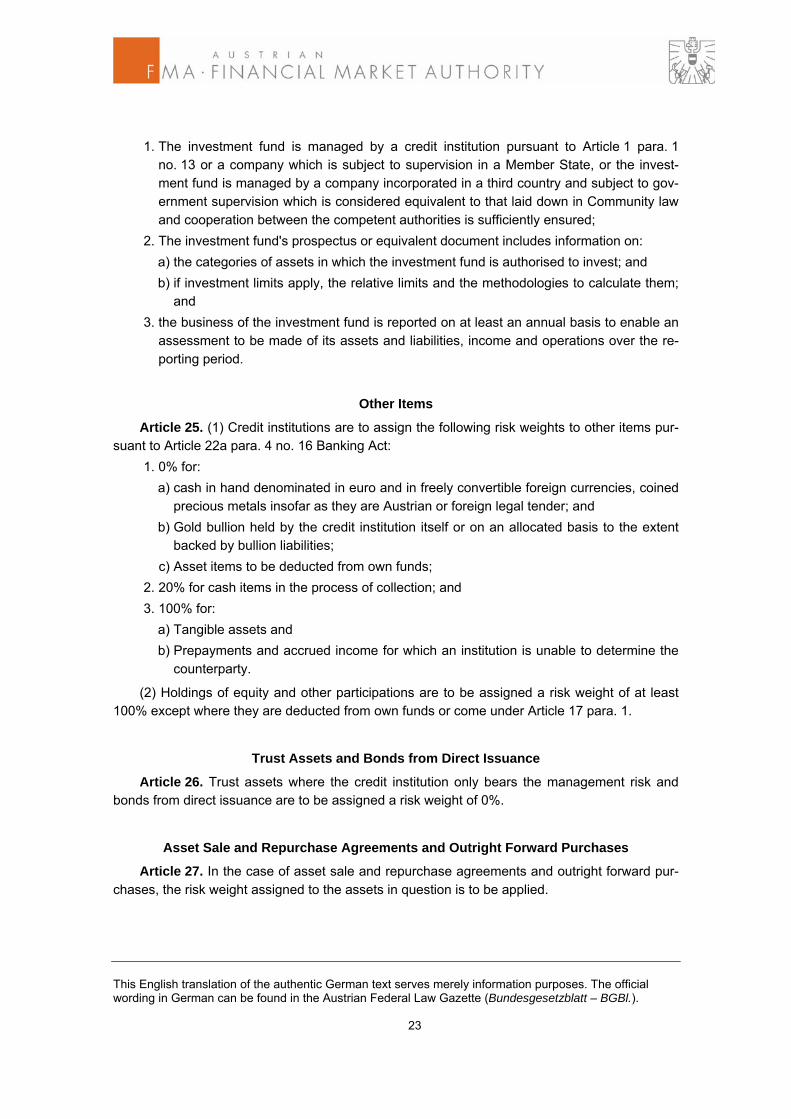

Other Items

Article 25. (1) Credit institutions are to assign the following risk weights to other items pur-suant to Article 22a para. 4 no. 16 Banking Act: 1. 0% for: a) cash in hand denominated in euro and in freely convertible foreign currencies, coined

precious metals insofar as they are Austrian or foreign legal tender; and b) Gold bullion held by the credit institution itself or on an allocated basis to the extent

backed by bullion liabilities; c) Asset items to be deducted from own funds; 2. 20% for cash items in the process of collection; and 3. 100% for: a) Tangible assets and b) Prepayments and accrued income for which an institution is unable to determine the

counterparty.

(2) Holdings of equity and other participations are to be assigned a risk weight of at least 100% except where they are deducted from own funds or come under Article 17 para. 1.

Trust Assets and Bonds from Direct Issuance

Article 26. Trust assets where the credit institution only bears the management risk and bonds from direct issuance are to be assigned a risk weight of 0%.

Asset Sale and Repurchase Agreements and Outright Forward Purchases

Article 27. In the case of asset sale and repurchase agreements and outright forward pur-chases, the risk weight assigned to the assets in question is to be applied.

This English translation of the authentic German text serves merely information purposes. The official wording in German can be found in the Austrian Federal Law Gazette (Bundesgesetzblatt – BGBl.). 24

Credit Protection for a Basket of Exposures

Article 28. (1) Where a credit institution provides credit protection for a basket of exposures under such terms that the nth default among the exposures triggers payment and this credit event terminates the contract, the risk weights pursuant to Articles 22c to 22f Banking Act for securitisation positions are to be assigned if the collateral has an external credit assessment from an eligible external credit assessment institution.

(2) In cases where a credit assessment from an eligible external credit assessment institu-tion is not available for the collateral, the weighted exposure amount is to be calculated as fol-lows: 1. The risk weights of the exposures in the basket are to be aggregated, excluding n-1

exposures, up to a maximum of 1250% and multiplied by the nominal amount of the pro-tection provided by the derivative; and

2. The n-1 exposures to be excluded from the aggregation are to be determined on the basis that each of those exposures produces a lower risk-weighted exposure amount than the risk-weighted exposure amount of any of the exposures included in the aggre-gation.

Section 3

Use of Ratings from External Credit Assessment Institutions Article 29. Credit institutions which use credit assessments from one or more eligible ex-

ternal credit assessment institutions for the purpose of calculating risk weights under the Stan-dardised Approach to Credit Risk must adhere to the provisions of this section when using such credit assessments.

General Provisions regarding Use

Article 30. (1) In cases where credit assessments published by an eligible external credit assessment institution are used, they must be applied in a continuous and consistent way over time.

(2) In cases where credit assessments produced by an eligible external credit assessment institution for a certain exposure class are used, they must be applied consistently to all expo-sures belonging to that exposure class.

(3) Credit institutions may only use credit assessments from an eligible external credit as-sessment institution that take into account all amounts both in principal and in interest owed to it.

This English translation of the authentic German text serves merely information purposes. The official wording in German can be found in the Austrian Federal Law Gazette (Bundesgesetzblatt – BGBl.). 25

Use of Multiple Credit Assessments

Article 31. (1) Where a credit institution pursuant to Article 30 uses credit assessments from an eligible external credit assessment institution and only one credit assessment is avail-able from an eligible external credit assessment institution for an exposure, that assessment is to be used to determine the risk weight to be applied to the exposure.

(2) In cases where two credit assessments from eligible external credit assessment institu-tions are available and the two correspond to different risk weights for an item, the higher risk weight is to be assigned to the exposure.

(3) In cases where more than two credit assessments from eligible external credit assess-ment institutions are available for an item, the two assessments generating the lowest risk weights are to be used. In this context, the following applies: 1. If the two lowest risk weights are different, the higher risk weight is to be assigned; and 2. If the two lowest risk weights are the same, that risk weight is to be assigned.

Issuer and Issue Credit Assessments

Article 32. (1) In cases where a credit assessment exists for a specific issuing program or facility to which the exposure to be weighted belongs, this credit assessment is to be used to determine the risk weight to be assigned to that exposure.

(2) Where no directly applicable credit assessment pursuant to para. 1 exists for a certain exposure, but a credit assessment exists for a specific issuing program or facility to which the exposure does not belong or a general credit assessment exists for the issuer, then that credit assessment is to be used if it produces 1. a higher risk weight than would otherwise be the case or 2. a lower risk weight and the exposure in question ranks pari passu or senior to the spe-

cific issuing program or facility or to senior unsecured exposures of that issuer.

(3) The application of the provisions regarding exposures in the form of covered bonds pur-suant to Articles 18 to 20 is to remain unaffected by the provisions above.

(4) Credit assessments for issuers within a corporate group cannot be used as credit as-sessments of other issuers within the same corporate group.

Short-Term Credit Assessments for Exposures

Article 33. (1) Short-term credit assessments may only be used for short-term asset items and off-balance sheet transactions constituting exposures to institutions and corporates.

(2) Short-term credit assessments may only be used for the specific items to which the short-term credit assessments refer. They must not be used to derive risk weights for other ex-posures.

This English translation of the authentic German text serves merely information purposes. The official wording in German can be found in the Austrian Federal Law Gazette (Bundesgesetzblatt – BGBl.). 26

Short-Term Credit Assessments for Facilities

Article 34. (1) Notwithstanding Article 33, if a facility for which a short-term credit assess-ment exists is assigned a 150% risk weight, then all unrated, unsecured exposures to that obli-gor – whether short-term or long-term – must also be assigned that risk weight.

(2) Notwithstanding Article 33, if a facility for which a short-term credit assessment exists is assigned a 50% risk weight, then all unrated short-term exposures to that obligor are to be as-signed a risk weight of at least 100%.

Domestic and Foreign Currency Items

Article 35. A credit assessment that refers to an item denominated in the obligor's domes-tic currency cannot be used to derive a risk weight for another exposure to that same obligor that is denominated in a foreign currency.

Chapter 2

Internal Ratings Based Approach

Section 1

General Provisions

Article 36. In calculating weighted exposure amounts and expected loss amounts for expo-sure classes pursuant to Article 22b para. 2 Banking Act and for dilution risk in the case of pur-chased receivables, credit institutions which apply the Internal Ratings Based Approach must fulfil the minimum requirements set forth in this chapter and observe the rules for calculating exposure values and expected loss amounts as well as the risk parameters probability of de-fault, loss given default and effective maturity.

Section 2

Minimum Requirements

Rating Systems

Article 37. The systems used by the credit institution to control and assess credit risk must be sound, ensure system integrity and in any case fulfil the following requirements: 1. The rating systems used ensure a meaningful assessment of obligor and transaction

characteristics, a meaningful differentiation of risk, and accurate and consistent quanti-tative estimates of risk;

2. The internal ratings and own estimates of risk parameters which are applied play an essential role in the credit risk management and decision-making process as well as the credit approval process, the internal capital adequacy assessment process pursuant to Article 39a Banking Act and the risk management system pursuant to Article 39 Banking Act;

This English translation of the authentic German text serves merely information purposes. The official wording in German can be found in the Austrian Federal Law Gazette (Bundesgesetzblatt – BGBl.). 27

3. All data required for reliable credit risk measurement and credit risk management are

collected and stored; and 4. the rating systems and their structure are documented and validated.

Structure of Rating Systems

Article 38. (1) A rating system comprises all of the methods, processes, controls, data col-lection and IT systems that support the assessment of credit risk, the assignment of exposures to grades or pools (rating), and the quantification of default and loss estimates for certain types of exposure. In using rating systems, credit institutions must fulfil the following requirements: 1. In cases where a credit institution uses multiple rating systems, the rationale for assign-

ing an obligor or a transaction to a rating system must be documented and applied in a manner that appropriately reflects the level of risk associated with each obligor or trans-action; and

2. Assignment criteria and processes must be reviewed periodically to determine whether they remain appropriate for the current portfolio and current external conditions.

(2) Credit institutions which use direct estimates of risk parameters may regard those esti-mates as grades on a continuous rating scale.

(3) A rating system for exposures pursuant to Article 22b para. 2 nos. 1 to 3 Banking Act must fulfil the following additional requirements: 1. The rating system must take into account the risk characteristics of the obligor as well

as the transaction; 2. The rating system must have an obligor rating scale which exclusively reflects the quan-

tification of the risk of obligor default; an obligor grade is a classification within the rating system's obligor rating scale on the basis of a specified and distinct set of rating criteria from which estimates of PD are derived. The obligor rating scale must fulfil the following requirements:

a) The obligor rating scale must have a minimum of seven grades for non-defaulted obligors and one for defaulted obligors;

b) The relationship between obligor grades must be documented in terms of the level of default risk each grade implies and the criteria used to distinguish that level of default risk.

c) Where a credit institution's portfolios are concentrated in a particular market segment and range of default risk, then the credit institution must have enough obligor grades within that range to avoid undue concentrations of obligors in a particular grade; sig-nificant concentrations within a single obligor grade must be supported by empirical evidence that the obligor grade covers a reasonably narrow PD band and that the de-fault risk posed by all obligors in the grade falls within that band; and

3. Where own LGD estimates are used, the rating system must have a facility rating scale which exclusively reflects LGD-related transaction characteristics; a facility grade is a classification within the rating system's facility scale on the basis of a specified and dis-tinct set of rating criteria from which own estimates of LGD are derived. Facility grades must fulfil the following requirements:

This English translation of the authentic German text serves merely information purposes. The official wording in German can be found in the Austrian Federal Law Gazette (Bundesgesetzblatt – BGBl.). 28

a) Individual facility grades are defined; the grade definition must include both a descrip-

tion of how exposures are assigned to the grade and a description of the criteria used to distinguish the level of risk across grades.

b) Significant concentrations within a single facility grade must be supported by empiri-cal evidence that the facility grade covers a reasonably narrow LGD band and that the risk posed by all exposures in the grade falls within that band.

(4) In the calculation of weighted exposure amounts for specialised lending exposures pur-suant to Article 74 para. 3, para. 3 above is applicable with the limitation that the obligor rating scale need not exclusively reflect the quantification of the risk of obligor default for these expo-sures, and at least four grades for non-defaulted obligors and at least one class for defaulted obligors must be defined.

(5) A rating system for exposures pursuant to Article 22b para. 2 no. 4 Banking Act must fulfil the following additional requirements: 1. The rating system must reflect both obligor and transaction risk, and capture all relevant

obligor and transaction characteristics; 2. The level of risk differentiation must ensure that the number of exposures in a given

grade or pool is sufficient to enable meaningful quantification and validation of the loss characteristics at the grade or pool level; excessive concentrations of exposures and ob-ligors in the grades or pools must be avoided;

3. The process of assigning exposures to grades or pools provides for a meaningful differ-entiation of risk, provides for a grouping of sufficiently homogenous exposures, and en-ables accurate and consistent estimation of loss characteristics at the grade or pool level; in the case of purchased receivables, the grouping must reflect the seller's under-writing practices and the heterogeneity of its customers; and

4. The following risk drivers must be taken into account in the assignment of exposures to grades or pools:

a) Obligor risk characteristics; b) Transaction risk characteristics, including product and collateral types; c) Delinquency if it is a material risk river for the exposure in question.

Assignment of Exposures

Article 39. (1) Credit institutions must have specific definitions, processes and criteria for assigning exposures to grades or pools within a rating system in order to ensure that 1. the grades or pools are sufficiently detailed to allow the persons charged with assigning

ratings to assign obligors or facilities posing similar risk to the same grade or pool in a consistent manner across lines of business, departments and locations;

2. the rating process is documented in a transparent manner so that third parties can un-derstand the assignment of exposures and evaluate its appropriateness; and

3. the criteria used are consistent with the credit institution's internal lending standards and policies for handling troubled obligors and facilities.

This English translation of the authentic German text serves merely information purposes. The official wording in German can be found in the Austrian Federal Law Gazette (Bundesgesetzblatt – BGBl.). 29

(2) Credit institutions must take all relevant information into account in assigning obligors and facilities to grades or pools. This information must be current and must enable the credit institution to forecast the future performance of the exposure. The less information a credit insti-tution has, the more conservative it must be in its assignments of exposures to obligor or facility grades and pools. In cases where a credit institution uses an external rating as a primary factor determining an internal rating assignment, the credit institution must ensure that it considers other relevant information.

(3) In assigning exposures pursuant to Article 22b para. 2 nos. 1 to 3 Banking Act, credit in-stitutions must also 1. assign each obligor to an obligor grade in the credit approval process; 2. assign each exposure to a facility grade where own estimates of LGD and conversion

factors are used; 3. assign each exposure to a grade pursuant to Article 38 para. 4 in the case of specialised

lending exposures for which the weighted exposure amount is calculated in accordance with Article 74 para. 3;

4. separately rate each legal entity to which the credit institution is exposed, and have ac-ceptable policies regarding the treatment of individual obligors and groups of connected clients; and

5. assign all exposures to the same obligor to the same obligor grade; exceptional cases where separate exposures are allowed to result in multiple grades for the same obligor are:

a) the existence of country transfer risk, depending on whether the exposures are de-nominated in local or foreign currency;

b) cases where personal collateral is reflected in an adjusted borrower grade; c) cases in which consumer protection, banking secrecy, data protection or other legisla-

tion prohibits the exchange of client data; and d) specialised lending for individual transactions.

(4) In the credit approval process, credit institutions must assign each exposure pursuant to Article 22b para. 2 no. 4 Banking Act to a grade or pool.

(5) For overrides of grade or pool assignments, credit institutions must document the situa-tions in which human judgement may override the inputs or outputs of the assignment process and the personnel responsible for approving these overrides. Credit institutions must document these overrides and the personnel responsible. Credit institutions must analyse and assess the performance of exposures whose rating has been overridden, accounting for all responsible personnel.

This English translation of the authentic German text serves merely information purposes. The official wording in German can be found in the Austrian Federal Law Gazette (Bundesgesetzblatt – BGBl.). 30

Integrity of the Assignment Process

Article 40. (1) For exposures pursuant to Article 22b para. 2 nos. 1 to 3 Banking Act, credit institutions must fulfil the following requirements: 1. An independent unit within the credit institution that does not benefit directly from deci-

sions to extend credit must carry out or approve assignments of exposures to grades and periodic reviews of assignments;

2. Assignments must be updated at least on an annual basis; high-risk obligors and prob-lem exposures must be subject to more frequent review, and assignments are to be up-dated as soon as material information on obligor or exposure becomes available; and

3. The credit institution must have an effective process to obtain and regularly update rele-vant information on obligor characteristics that affect PDs and on transaction character-istics that affect LGDs and conversion factors.

(2) For exposures pursuant to Article 22b para. 2 no. 4 Banking Act, the following require-ments must be fulfilled: 1. Obligor and facility assignments must be updated at least annually, and the loss charac-

teristics and delinquency status of each identified risk pool must be reviewed at least annually; and

2. The status of individual exposures within each pool must be reviewed at least annually on the basis of a representative sample, and assignments must be updated as neces-sary.

Use of Models

Article 41. Credit institutions which use statistical models or other mechanical methods to assign exposures to obligor or facility grades or pools must fulfil the following requirements: 1. The credit institution must demonstrate that the model has good predictive power and

that minimum capital requirements are not distorted as a result of its use; 2. The input variables must form an objectively justified and effective basis for the resulting

predictions. 3. The model must not have material biases; 4. The credit institution must have processes in place for vetting data inputs into the model,

including an assessment of the accuracy, completeness and appropriateness of the data;

5. The data used to build the model are representative of the credit institution's current population of obligors and exposures;

6. The model must be validated on an annual basis; this must include monitoring its predic-tive power and stability, a review of the model specification and the testing of model outputs against actual outcomes;

7. The model must be supplemented by all additional relevant information, especially quali-tative factors, which are not captured by the model; the rules defining how this informa-tion is to be combined with the model's output must be documented; and

This English translation of the authentic German text serves merely information purposes. The official wording in German can be found in the Austrian Federal Law Gazette (Bundesgesetzblatt – BGBl.). 31

8. The model must be monitored in order to review model-based assignments, to find and

limit errors associated with model weaknesses, and to ensure that models are used ap-propriately.

Documentation of Rating Systems

Article 42. With regard to rating systems, credit institutions must document the following: 1. the design and operations of the rating systems used; the documentation must provide

information on compliance with the minimum requirements set forth in Articles 37 to 64 and contain a description of the following areas:

a) portfolio differentiation; b) rating criteria; c) the responsibilities of parties/units that rate obligors and exposures; and d) the frequency of assignment reviews, and senior management oversight of the rating

process; 2. the rationale for and analysis supporting the choice of rating criteria; 3. all major changes in the rating process, especially changes made to the rating process

subsequent to the last review by the FMA; 4. the organisation of rating assignment, including the rating assignment process and the

internal control structures; 5. the definitions of default and loss used internally, including evidence of their consistency

with Article 22b para. 5 no. 2 Banking Act; and 6. the methodologies of the statistical models used; in this context, the documentation

must include the following: a) a detailed outline of the theory, assumptions and mathematical and empirical basis of

the assignment of PD estimates to grades, individual obligors, exposures, or pools, and the data sources used to estimate the model;

b) an extensive and rigorous statistical process, including out-of-time and out-of-sample performance tests, for validating the model; and

c) indications of any circumstances under which the model does not work effectively.

Models Obtained from Third-Party Vendors

Article 43. Where a model based on approaches developed by third parties is used, the credit institution itself must demonstrably fulfil all requirements for rating systems and create the documentation.

This English translation of the authentic German text serves merely information purposes. The official wording in German can be found in the Austrian Federal Law Gazette (Bundesgesetzblatt – BGBl.). 32

Data Maintenance

Article 44. (1) For exposures pursuant to Article 22b para. 2 nos. 1 to 3 Banking Act, credit institutions must collect and store the following data regarding their internal ratings: 1. complete rating histories on obligors and collateral providers eligible for the purposes of

credit risk mitigation; 2. the dates on which the ratings were assigned; 3. the key data and methodology used to derive the rating; 4. the person responsible for the assignment of ratings; 5. the identity of defaulted obligors and exposures; 6. the date and circumstances of such defaults; and 7. data on the PDs and realised default rates associated with rating grades and on rating

migrations.

(2) Credit institutions which do not use own estimates of LGDs and/or conversion factors must collect and store data on comparisons of realised LGDs to the values set forth in Article 69 and on comparisons of realised conversion factors to the values set forth in Article 65 para. 9.

(3) In addition to the requirements set forth in para. 1, credit institutions which use own es-timates of LGDs and conversion factors must also collect and store the following data: 1. complete histories of data on the facility ratings as well as LGD and conversion factor

estimates associated with each rating scale; 2. the dates on which the ratings were assigned and on which the estimates were carried

out; 3. the key data and methodology used to derive the facility ratings as well as the LGD and

conversion factor estimates; 4. the person who assigned the facility rating and the person who generated the LGD and

conversion factor estimates; 5. data on the estimated and realised LGDs and conversion factors associated with each

defaulted exposure; 6. data on the LGD of the exposure before and after evaluation of the effects of personal

collateral, for those credit institutions that reflect the credit risk-mitigating effects of such collateral through LGD; and

7. data on the components of loss for each defaulted exposure.

(4) For exposures pursuant to Article 22b para. 2 no. 4 Banking Act, credit institutions must collect and store the following data regarding their internal ratings: 1. the data used in the process of assigning exposures to grades or pools; 2. data on the estimated PDs, LGDs and conversion factors associated with grades or

pools of exposures; 3. the identity of defaulted obligors and exposures; 4. for defaulted exposures, data on the grades or pools to which the exposures were as-

signed over the year prior to default and on the realised outcomes of LGDs and conver-sion factors; and

This English translation of the authentic German text serves merely information purposes. The official wording in German can be found in the Austrian Federal Law Gazette (Bundesgesetzblatt – BGBl.). 33

5. data on LGDs for qualifying revolving retail exposures.

(5) Credit institutions must collect and store all data regarding their internal ratings in ac-cordance with the provisions of Articles 26 and 26a Banking Act.

Stress Tests