Embed Size (px)

Citation preview

REGULATORY ACTIVITIES IN THE ENERGY SECTOR OF ANALYSED COUNTRIES OF THE MEDITERRANEAN

May 2006

The views expressed do not imply the expression of any opinion whatsoever on the part of the Italian Department for Public Administration, and Formez.

2

Table of contents

Foreword ...................................................................................3

Key Observations.....................................................................4

1. Algeria ...................................................................................7

1.1. Electricity sector ..........................................................7

1.2 La Commission de Régulation de l’Electricité

e du Gaz (CREG)..........................................................8

1.3 Hydrocarbons.............................................................11

2. Egypt....................................................................................12

2.1 Electricity .....................................................................12

2.2 Electric Utility and Consumer Protection

Regulatory Agency (EUCPRA)..................................16

3. Jordan .................................................................................18

3.1 Electricity ....................................................................18

3.2 The Electricity Regulatory Commission ...................21

4. Lebanon..............................................................................23

4.1 The electricity market................................................23

5. Morocco .............................................................................25

5.1 The electricity market................................................25

5.2 The liberalisation of the electricity market .............26

6. Tunisia ..................................................................................29

6.1 The electricity market................................................29

6.2 The hydrocarbons market ........................................30

3

Foreword

The research document is part of a broader line of work that the C.A.I.MED. Centre for Administrative Innovation in the Euro-Mediterranean Area – a centre created jointly by the United Nations and the Italian government dealing with administrative cooperation between European and Mediterranean countries - has dedicated to the evolution of administrative innovation in the Mediterranean area. C.A.I.MED studies and analyses have paid particular attention to infrastructure, especially energy infrastructure, while the telecommunications and transportation sectors will be the object of future studies. In particular, we have focused on network infrastructures and on the authorities in charge of their regulation, in light of the fact that the European Commisssion – Meda and the new Neighbourhood Policies have destined 70% and 80% of total financing to MEDA countries to this sector.

This initial contribution was undertaken in collaboration with ISPI (Istituto per gli Studi di Politica Internazionale).

4

Key observations

The research examines the liberalisation process in the telecommunications, energy and transport markets of the following Mediterranean countries: Algeria, Egypt, Jordan, Lebanon, Morocco and Tunisia. Particular attention is given to statutory developments and also to activities performed by the public Antitrust authorities or by independent agencies, aimed at the regulation and/or safeguard of competition. The picture that emerges is varied both in terms of sector and country.

The liberalisation process, and by consequence the development of antitrust market regulation authorities, is at its most advanced in the telecommunications sector. In this sector, all the examined countries have already created, (or in the case of Lebanon, are about to create) a market regulation authority, even though great variations occur from country to country in terms of the autonomy and efficiency of these institutions.

The energy sector is, on the other hand, a much more mixed bag; however, the overall development of genuine antitrust authorities is lagging behind. Of the six Mediterranean countries examined, only three have made some progress, in a not particularly encouraging context. Algeria is a special case: the country is a big hydrocarbons producer, and is trying to kick start the liberalisation of the energy sector, but is meeting serious obstacles caused by traditional organisation methods and a rentière economy dependent on energy exports. The increase in oil prices in the last three years has not helped the drive towards liberalisation: increased oil revenues bolster the state’s financial position (which at the end of 2002 was heavily burdened by foreign debt, although its liquid currency reserves are now twice the size of its foreign debt), thus enabling the country to increase its commitment to delivering public services and the construction of infrastructure.

In the transport sector, the Existing Antitrust authorities are basically control bodies (some countries have an excess of them) for specific sub-sectors or activities, totally independent from the competent ministry and without any autonomy in the regulation of a market that in any case remains largely under State control.

However it is no coincidence that the countries most advanced in terms of economic liberalisation (and therefore also in terms of independent regulation of markets), are those that have experienced severe debt crises (Morocco in the early 1980s and Jordan at the end of the 1980s) and then have managed without long term support from the international financial institutions. In this context, market liberalisation has been less a directive from the International Monetary Fund and the World Bank, than an independent economic decision. At a later stage, when the reform and liberalisation processes have received internal political-social backing, they have been gradually extended to other sectors, including the ones dealt with in these pages.

The ongoing financial difficulties of the most rapidly liberalised countries seem to have helped shape the decisions regarding what sectors should be most urgently liberalised. Thus, in all countries priority has been given to the telecommunications sector; by releasing operating licences to foreign mobile telephony companies, rich dividends could be counted on to help permanently debt-ridden public purses. Morocco was at the forefront of this process, and it is precisely in Morocco that we find the Antitrust authority that has most efficiently demonstrated its independence from government, when in 2002 it opposed the attempt to bring the entire telecommunications sector back under public control.

5

In the energy field, insufficient finances have severely limited the opening up of the market. The scarcity of public resources for infrastructure investment has led to the issue (again in Morocco, but also in Egypt and Jordan) of licensing contracts (such as the Build-Operate-Transfer scheme, or others similar to this) for the construction of new power stations. These contracts have allowed the ingress of foreign partners, but have not created a genuine market. In effect, several producers are lined up before a single buyer (the public electricity distribution network) and the independent producers negotiate tariffs within the Build-Operate-Transfer contract, selling the product to the State at this price or at least with a profit margin.

The fact that financial considerations (as well technological factors, in the case of mobile telephony networks) are relevant in the choices made on the independent liberalisation and regulation of markets indicates that not all the Mediterranean countries examined here have prioritised the creation of competitive markets in the public services sector, even where technological or social considerations no longer justify the maintenance of monopolies.

Despite this backward state of affairs, all the countries have demonstrated a gradual expansion of liberalisation, which is now spreading to the most resistant countries, such as the firmly centralised Tunisia, or Lebanon, where a market economy operates in a complex political context (public and para-state appointments distributed through a spoils-system based on ethnic-confessional community) that complicates the liberalisation of public utility services.

This evolving situation could allow a significant role for processes of harmonisation with European standards, as called for by the Euro-Mediterranean Partnership (within the Association Agreements) and above all by the European Neighbourhood Policy (in the Action Plan, with some countries already signed up, and others in negotiations).

The role of Neighbourhood Policy in the development of material and immaterial networks in Mediterranean countries is dealt with in other research, either completed or underway as part of this project.

6

The subsequent pages contain a roundup of the single markets and an examination of the following antitrust authorities and/or competent bodies:

ENERGY Country Authority Year created Algeria Commission de régulation de l’électricité et du gaz (CREG)

Autorité de Régulation des Hydrocarbures (ARH)

2005

2005 Egypt Egyptian New and Renewable Energy Authority (NREA)

Electric Utility and Consumer Protection Regulatory Agency

1986

1997 Jordan Electricity Regulatory Commission 2001

Lebanon Currently in discussion Morocco Currently in discussion

7

1 The energy market in Algeria

1.1. Electricity sector The law 02-01 of 5 February 2002 (http://www.grte-cit.dz/Telechargement/txt_loi_ele.pdf) called for the electricity and pipeline gas sectors to be opened up to competition, thus ending the monopoly position of Sonelgaz, which became a joint stock company with presidential decree. The reform introduced a stable normative framework intended to attract private finance and legally separate the functions of generation, transport and distribution. It also called for:

freedom of installation in the field of electricity production;

regulated monopolies in the transport and distribution networks;

introduction of third party access into the networks;

distribution of licensing concessions;

creation of a regulatory body, the Commission de Régulation de l’Electricité e du Gaz (CREG).

This law also provided for environmental protection and called for the development of renewable energy sources. A decree on the costs of diversification of electricity production, entered into force on 25 March 2004, introduced an incentive scheme for electricity produced from renewable sources. A company named New Energy Algeria (NEAL) was set up to support the development of these kinds of projects. It has two public shareholders, (Sonatrach and Sonelgaz) and one private shareholder, the Algerian firm SIM.

The law should have prepared the way for liberalisation by 2005 through the following actions:

opening of electricity production to full private competition.

creation of two affiliated branches of Sonelgaz: one responsible for gas, and the other in charge of electricity distribution. In June 2002 the government announced that the two branches would be open even to foreign private investment. However nothing has happened by the end of 2005, and there remains great uncertainty over the level of commitment towards full deregulation of the energy sector.

Creation of a system operator who would act to maintain a balance between demand and supply. This should be a private (joint stock) company with no involvement in the production of energy.

Creation of an electricity market operator (joint stock)

However a series of obstacles stand in the way of liberalisation of the market. Firstly, private capital is experiencing great difficulty in flowing into production. In fact the State – through Sonelgaz1, which has a monopoly in the generation, transmission and distribution of electricity – is omnipresent and remains the biggest investor. A further problem is the excessive centralisation of management. The functional efficiency of the sector is not improving and costs to the consumer have not decreased. 1 Sonelgaz output reaches 6460 MW, of which 6039 MW is for the interlinked network in the north, and the rest for the isolated networks in the south.

8

The goal of the creation of a minimum 30% open market for electricity and gas distribution, has therefore been postponed until 2007.

With an effective output of 6.000 megawatts, 95%of the country’s power requirements is covered (a percentage similar to that of the OECD countries). More than 4 million households are Sonelgaz subscribers. Furthermore, the natural gas distribution network (19,000km) reaches 36% of households directly. Sonelgaz has planned to satisfy increasing demand by investing more than 12 billion dollars up to 2010 for maintenance of the electricity network, and to boost its output capacity. In order to cope with increased demand for electricity, estimated at 7% in the 2002-2011 period, Sonelgaz plans to construct ten power stations by 2010.

In May 2001 the Algerian Energy Company (AEC) was created, combining Sonatrach and Sonelgaz, the two most important public companies in the energy sector. This affiliated company manages energy production and seawater desalination projects, using private foreign investment. Three companies have been created:

1. Kahrama – the American firm Black & Veatch, initially holding 80% of its shares, now retains 5% after a huge investment drive by the AEC, which now has 95%. The company is planning the creation of an electricity production and seawater desalination installation at Arzew;

2. SKS, 20% owned by Canadian company SNC Lavalin, is to construct a power station at Skikda;

3. HWD: this company is 70% owned by the American company Ionics and is managing the construction of a desalination plant in Algiers.

Most of the population and economic activity is concentrated in the northern coastal strip of the country, so it is not surprising that the highest consumption levels and the biggest power stations (thermal) are found here. In the interior and the southern areas of oil and gas deposits, the gas turbine method is used. On an overall scale, natural gas is the chief means of electricity production in Algeria.

Link-ups at regional level currently exist with Morocco and Tunisia. Studies are being made on the possibility of undersea cable connections with Italy (Algeria-Sicily and Algeria-Sardinia).

1.2 La Commission de Régulation de l’Electricité e du Gaz (CREG) The Commisson was called for by law 02-01 of 5 February 2002 (which also defined its competences), and was instituted on 24 February 2005 by the Algerian Prime Minister, as an independent body with legal personality and financial autonomy. It is financed by revenues from tariffs and its budget is approved by the energy minister. It is governed by a board of directors comprising a president and three directors proposed by the energy minister and appointed by presidential decree. Its main objective is to guarantee the competitive and transparency functioning of the electricity and gas market, in the interests of consumers and operators.

The duties of the CREG are listed in article 115 of the abovementioned law. They can be summed up thus:

The CREG sets the payment to the operators for transport and distribution, the tariffs for use of the network and tariffs for the clients. It also sees to the management of electricity and gas funds and ensures the compatibility of the companies.

It protects consumers’ interests by ensuring that public services obligations are carried out;

9

it prepares complaints and appeals of the operators; sets administrative sanctions for the violation of rules or standards; it publishes information that may be useful for the defence of consumers’ interests.

It acts as a conciliation and arbitration body. The CREG conciliation service handles disputes between operators, relating to the application of regulations. There is also an arbitration chamber that delivers judgements in controversies, when called on by one of the parties.

The CREG may hold consultations before making decisions, which may be motivated and public, or open to appeal. It may give judgements; it organises public hearings, it presents the energy minister with an annual report on the execution of its duties and on the evolution of the market.

Table 1 – Algerian electricty network statisitics

2005 Forecast for 2010

8 % growth

Installed power ( MW ) 6700 10 000

Length of transport network

16 500 km 22 000

Length of distribution network 217 500 km 341 000

HT clients (number) 80 -

MT clienti (number) 32 500 -

BT clients (number) 5 500 6 500

Annual investment (millions US $) 1 000 1 000

10

Chart 1 – Trends in electricity sale prices

Chart 2 – Trends in price of gas for domestic consumption d ti

0,00

50,00

100,00

150,00

200,00

250,00

300,00

350,00

400,00

1997 1998 1999 2000 2001 2002 2003 2004 2005

(en

cDA/

kWh) HT

MTBTTOTAL

0,00

5,00

10,00

15,00

20,00

25,00

30,00

35,00

1997 1998 1999 2000 2001 2002 2003 2004 2005

(en

cDA/

th)

HPMPBP

11

1.3 Hydrocarbons Following the electricity sector, some limited reforms were effected in the field of hydrocarbons. The law 5-07 of 28 April 2005, promulgated on 19 July 2005, established that some functions previously executed by the national company Sonatrach would be taken over by two agencies with responsibility for:

Circulating operational information and promoting investment in the hydrocarbons sector, assigning prospecting and/or exploitation contracts, as well as collecting royalties.

Regulating the natural monopolies (transport through pipelines, stockpiling of oil products), ensuring adhesion to norms, standards and regulation of the sector in matters of hygiene, safety and environment.

The titles of the agencies are: Autorité de régulation des hydrocarbures/Hydrocarbon Regulation Authority (ARH) and the Autorité nationales de valorisation de ressources en hydrocarbures National Authority for Valorisation of Hydrocarbon Resources (ALNFT), established in November 2005.

The precise contribution of the State towards the two agencies has yet to be decided, even if this will subsequently diminish, given that they shall be financed directly by the operators in exchange for services rendered. The agencies enjoy autonomy of management and are adminstratively linked to the Ministry of Energy.

The Autorité de régulation des hydrocarbures (ARH) will responsible for ensuring adhesion to norms related to tariffs and free access to the pipeline transport networks, to stockpiling, hygiene, industrial safety, environmental protection, contract tendering for infrastructure construction projects, application of technical norms and standards in accordance with the best international practices. It is also charged with examining the applications for pipeline transport rights and subsequently making recommendations to the energy minister, who grants concessions in the form of regulated authorisation.

The Autorité nationales de valorisation de ressources en hydrocarbures (ALNFT) has the task of promoting operational information and investments, managing databases, granting exploration licences, preparing contracts and related evaluation, allocating prospecting and exploitation areas, tracking and controlling the preparation of prospecting/exploitation contracts, studying and approving development plans. It is also responsible for providing operators with the necessary data for developing investments.

The rules of operation, staffing and financing of the two agencies ought to guarantee impartiality, transparency and competence of their decisions. They cannot invest in or market the hydrocarbons nor hold links with interests allied to their areas of operation, in order to avoid conflicts of interest.

12

2 The energy market in Egypt

2.1 Electricity In recent years, Egypt has launched a restructuring and liberalisation process of the electricity market, a sector originally privately managed and then nationalised in the 1960s. The state however still retains a dominant role, through the Egyptian Electric Holding Company (see below). The market currently comprises a single client.

The first law for the liberalisation of the electricity sector was law no.100 of 1996, which allows national and foreign investors to construct, operate and manage power stations.

In 1997 presidential decree no. 326 called for the creation of the Electric Utility and Consumer Protection Regulatory Agency (EUCPRA). Law no.18 of 1998 established that the distribution companies would be affiliated to the Egyptian Electricity Authority and that all the power stations and high voltage networks would affiliated to this organisation. With law no. 164 (http://www.egyptera.com/en/acts_laws.htm) of 2000, the Egyptian Electricity Authority became a joint stock company and was renamed the Egyptian Electric Holding Company (EEHC). In 2001 the EEHC separated its production and distribution functions. As a result, there are now various production companies that sell to a single transmission company.

The Egyptian electricity market has two sub-markets: 1) the unified electricity system, which covers most of the inhabited area of the country; 2) the isolated markets, mainly the tourists zones of the Red Sea and the Sinai Peninsula.

In the former case, the government owns five power stations: four thermal and one hydroelectric unit. Private participation in the sector is represented by three long term (20 year) BOOT contracts (Build-Operate-Own-Transfer)2 with the Egyptian Electricity Transmission Company (EETC). Four industrial producers are connected to the network and they can emit and absorb electricity according to their needs. However, their market share is quite small. The State-owned companies are currently organised in the form of a single market buyer in which all the production companies sell electricity to a single transmission buyer/company, the EETC. The latter in turn sells electricity to the consumer and to nine State owned distribution companies (see table 1). The existence of a single transmission buyer/transmission company means that competition among the production companies is not possible.

On the other hand, the isolated markets are niche markets; as well as the State companies, there are some private production companies that sell directly to the consumer.

The restructuring of the electricity sector is also necessary in order to satisfy internal demand, which grows annually at a rate of 7%. One of the objectives of increased energy production is to promote the use of renewable sources. However, one of the main obstacles on the road to liberalisation is represented by subsidies, chiefly in connection with national consumers.

With regard to cross-border connections, Egypt is a member of the Mediterranean Electricity Ring, which links a number of North African and Middle Eastern countries, and will soon hook up with the European network. Egypt is also cooperating with a number of other African states (Burundi, Eritrea, Ethiopia, Kenya, Ruanda, Sudan, Tanzania and Uganda) in the construction of a network, as part of the Nile Basin Initiative. 2 The planning, financing and construction of the enterprise is led by the private sector, which retains ownership and manages the enterprise until a prearranged date, when ownership reverts to the public sector.

13

Map 1 – National electricity network at the beginning of 2004

Source: Egyptian Ministry of Electricity and Energy

14

Table 1 – Structure of the electricity sector in Egypt

Electricity Utility in Egypt

overnment owned companiesG

Electricity Generation Companies

Cairo Generation Company

East Delta Generation Company

West Delta on Generati

Company

Upper Egypt Generation Company

Hydro Plants Generation Company

New and Renewal Energy

Authority

The Egyptian Electricity Transmission Company

Electricity Distribution companies

North Cairo Distribution Company

South Cairo Distribution Company

Alexandria Distribution Company

Private Sector Companies

EDF Suez Gulf Power Company

)BOOT Project(

EDF Port Said East Power Company

)BOOT Project(

InterGen Sidi Krir Generating Company

)BOOT Project(

Global Energy Company

Alexandria Carbon SAE. Black co

15

North Delta Distribution Company

South Delta Distribution Company

Behaira Distribution Company

Canal Distribution Company

Middle Egypt Distribution Company

Upper Egypt Distribution Company

Om El Goreifat

Mirage

Source: http://www.egyptera.com

16

2.2 Electric Utility and Consumer Protection Regulatory Agency (EUCPRA) This is a Cairo based body with legal personality, affiliated to the Ministry of Electricity and Energy.

The EUCPRA was created by presidential decree 326 of 1997. Decree no. 339 of 2000 (http://www.egyptera.com/en/acts_decree.htm) established its structure, activities and its board of directors, which was formed in 2001.

The main tasks of the agency include:

Ensuring that all activities related to the generation, transmission, distribution and sale of energy are conducted in accordance with current laws and norms, especially where environmental protection is concerned.

Examining, on a regular basis, the plans regarding the generation, transmission, distribution and sale of electrical energy, including relevant investments, in order to guarantee the availability of energy for diverse uses, in conformity with government policy.

Defining norms in matters of competition in generation and distribution of electricity, so that consumer interests are safeguarded.

Ensuring that costs of generation, transmission, and distribution guarantee the interests of all parties involved.

Guaranteeing a fair profit for the electricity companies so that they can continue in business and maintain a solid financial position.

Publishing information, reports, and recommendations for the electricity companies and for consumers.

Examining consumer complaints and settling disputes between the parties involved.

Granting licences for the construction, management and maintenance of projects for the generation, transmission, distribution and sale of electricity.

The agency has a budget made up of funds allocated from the State budget (this is currently not used), revenues for the granting and renewal of licences, from services rendered by the agency to the electricity company users, from the investment of funds, and from donations and subsidies that do not conflict with its objectives.

The agency is directed by a board of directors (see Table 2) reporting to the presidency of the Ministry of Electricity and Energy. Of its ten members, three represent the electricity companies, four represent consumers and the remaining three are technical experts. The main duties of the board are:

Definition of the organisational structure of the agency.

Ratification of procedures for the granting of licences.

Decisions on matters of concessions, renewal and monitoring of licences for projects involving the generation, transmission, distribution, and sale of electricity. It must also supervise the realisation of the projects.

Approval of the annual budget.

17

Table 2 – Structure of the EUCPRA

Source: http://www.egyptera.com/en/e-default.htm

18

3 The electricity market in Jordan

3.1 Electricity A number of important reforms have been launched in the Jordan electricity sector in recent years. Jordanian laws on electricity were modified in 1996 to allow for the privatisation of the sector, which today consists of one main generating company – the Central Electric Generation Company (CEGCO) - 75% owned by the government and 25% by the National Electric Power Company (NEPCO), and three distributors - the Jordan Electric Power Company (JEPCO) providing for the eastern part of the country, the Irbid District Electricity Company (IDECO) for the north, and the Electricity Distribution Company (EDCO) for the south. Transmission, transport and the development of the national HT network was entrusted to the NEPCO – a shareholding public company that in 1996 replaced the Jordan Electricity Authority (JEA), created in 1967. The NEPCO is also responsible for Jordanian linkups with neighbouring countries, and functions as a secretariat for the regional association, the Arab Union of Producers, Transporters and Distributors of Electricity.

The deregulation of the electricity sector, announced by the government on 4 October 1997, aims to achieve 51% privatisation of the CEGCO, 100% privatisation of the EDCO, as well as the surrender of the government’s 55.4% share of IDECO. A new company, the Samra Electric Power Generation Company (SEPGC), with capital of 70.5 million dollars, was set up to exploit the plant at Samra, which will generate 300 MW in combined cycle with a gas turbine installation. This plant, partly constructed by the American company Black & Veatch in association with the Turkish firm Gama Enerji, should be completed in the first half of 2006. The SEPGC, still owned entirely by the government but due to be privatised, should contribute to 20% of the total of electricity generated in Jordan.

The Jordanian market is however not big enough to attract investment, despite the rise in demand. The demand for electricity is broken down thus: domestic consumption - 34%, industry - more than 30%, commercial activity - 15%, water pumping - more than 15% (see table 5). In 2004, the CEGCO generated 94,2% of the electricity, while the remaining 5,8% was produced by other sources (see table 4). The electricity consumption level for 2004 was 8089 million kWh, against 7330 kWh in 2003.

The opening of the sector to privatisation has been slower than expected. The search for a strategic partner for the CEGCO began in March 2004 with the government’s decision to sell 51% of the company. About ten proposals of interest were presented to the Executive Privatisation Commission (EPC), and these were reduced to around two after the definitive withdrawal of the Malaysian group Malakoff and the Indian Reliance Energy Ltd, in the last months of 2005. One reason for the difficulty in selling off the share was the CEGCO’s huge 282 million dollar debt.

The Independent Power Producer (IPP), is a new company that is also encountering difficulty in attracting investment for its Amman East Power Project, which is to be situated at Al Manakher (25 km from Amman) and will produce 300-400 MW with a BOO (Build-Own-Operate)3 contract. The closing date for tender proposals, initially set for 21 December 2005, has been postponed until 16 March 2006. This plant is supposed to be the lynch pin of an NEPCO development plan that will involve the strengthening of the connection with Syria to the north and Egypt to the south, as well

3 The planning, funding and construction of the project is led by the private sector, which remains proprietor and manager of the enterprise.

19

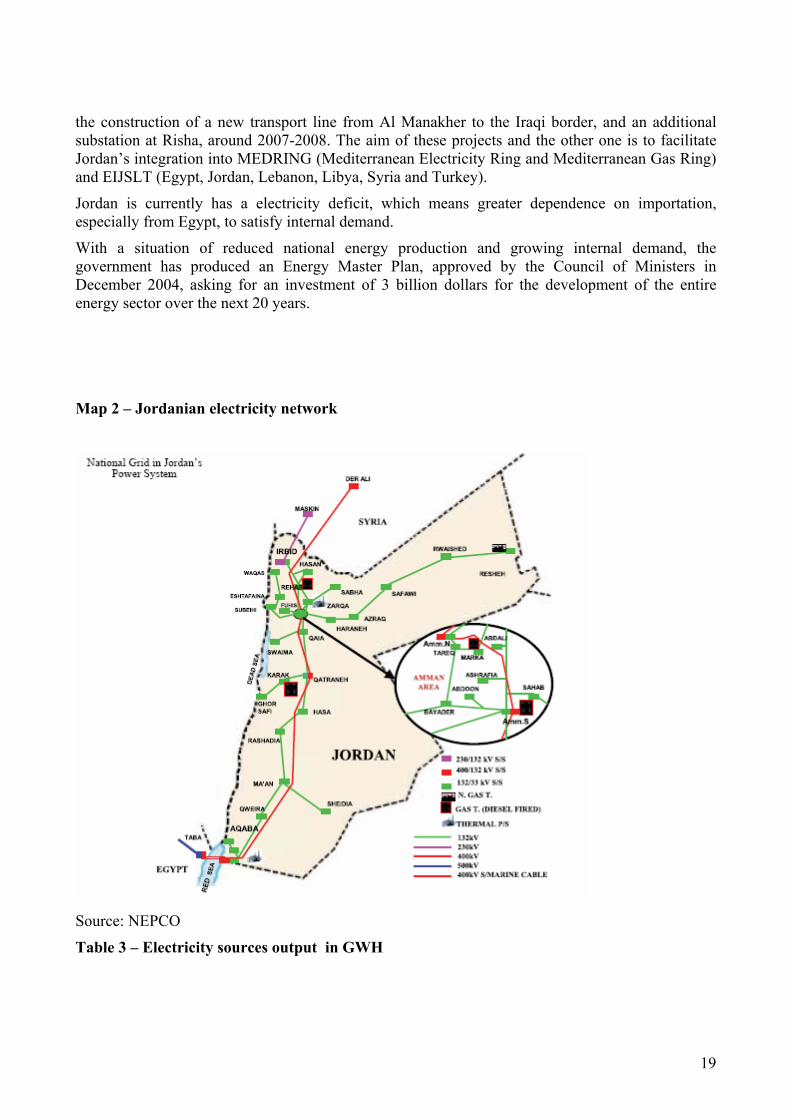

the construction of a new transport line from Al Manakher to the Iraqi border, and an additional substation at Risha, around 2007-2008. The aim of these projects and the other one is to facilitate Jordan’s integration into MEDRING (Mediterranean Electricity Ring and Mediterranean Gas Ring) and EIJSLT (Egypt, Jordan, Lebanon, Libya, Syria and Turkey).

Jordan is currently has a electricity deficit, which means greater dependence on importation, especially from Egypt, to satisfy internal demand.

With a situation of reduced national energy production and growing internal demand, the government has produced an Energy Master Plan, approved by the Council of Ministers in December 2004, asking for an investment of 3 billion dollars for the development of the entire energy sector over the next 20 years.

Map 2 – Jordanian electricity network

Source: NEPCO

Table 3 – Electricity sources output in GWH

20

Table 4 – Electrical energy generated and imported

Table 5 – Breakdown of electricity consumption

Source: NEPCO

21

3.2 The Electricity Regulatory Commission The Electricity Regulatory Commission (ERC), created in January 2001, is regulated by law no. 63 of 2002, known as the “General Electricity Law” (http://www.memr.gov.jo; text in English) The ERC, which reports to the Presidency of the Council of ministers, is endowed with legal personality and enjoys full financial and administrative independence.

The ERC is charged with the following duties:

• Contribute to the development and maintenance of an efficiently structured electricity sector, capable of supporting economic activity;

• Encourage investment aimed at increasing the operational efficiency of the sector and containing the price of supplying electrical energy;

• Guarantee the delivery of high quality services, in conformity with safety standards;

• Ensure that the companies operating in the sector adhere to current norms in matters of environmental protection and public safety;

• Ensure that licensees provide sufficient quantities of energy to satisfy user demand;

• Ascertain that the prices set by licensees are appropriate and at such a level as to be capable of financing the company’s activities and guaranteeing a return in line with investments;

• Safeguard the interests of consumers and monitor observance of the norms referred to in the licences;

• Regulate the sector impartially, maintaining balanced conduct throughout relations with consumers, licensees, investors and all other parties involved in the sector.

• Settle disputes among operators and between operators and users.

In order to fulfil its duties, the ERC is endowed with a series of prerogatives and powers. They include:

• Grant of licences;

• Define roles conducive to the provision of an electricity service that is efficient and economic, that will engender trust in clients, and that will advance in equal measure with technological developments in the sector;

• Set tariffs, subscription fees, royalties and connection costs;

• Participate in the definition of technical standards related to equipment and electrical installations;

• Participate in the definition of requirements necessary for the implementation of environmental safeguard norms, to which electrical installations must conform;

• Put forward recommendations to the Ministry of Energy and Mineral Resources that will be useful for creating the conditions for the consolidation of the rules and mechanisms of free competition in the electricity market;

• Take clear, justified decisions in relation to controversies between operators and users. Any such decisions can be contested in the High Court of Justice.

22

The workings of the ERC are supervised by the Council of Commissioners and the administrative staff.

The Council of Commissioners comprises five members, including the Director and Vice Director, appointed by the Council of Ministers, upon recommendation by the Prime Minister. The office of member of the Council is incompatible with the existence of direct or indirect interests relating to any division of the electricity sector.

The members of the Council remaining office from two to four years and the mandate is renewable only once.

Meetings of the Council are convened by the Director at least once a month, as necessary according to circumstances. Resolutions are made by majority vote by members present. The Director has the casting vote in situations where there is no clear majority.

23

4 The energy market in Lebanon

The Lebanon imports oil and gas in equal measure.

Although offshore prospecting activities have produced positive results, Lebanon’s domestic demand for hydrocarbons is satisfied entirely by imports.

The level of internal consumption of oil is 108,000 barrels daily. Back in the early 1980s, Lebanon imported crude oil from Iraq and Saudi Arabia and refined it in its installations in Zahrani, in the south of the country, and in Tripoli, in the north. However owing to internal and regional instability, the two refineries were forced to close down.

Until 1988 the Lebanese government held a monopoly position in the oil market, whereas today eight private companies hold licences for the importation and distribution of refined oil products. The oil Directorate, instituted by the Ministry of Energy and Water Resources, sets the prices of petroleum products in line with international price trends.

A project is underway to convert oil-fired power stations to natural gas. It has included the construction of a 26 mile pipeline entitled Gasyle 1, which connects the Syrian plant at Baniyas with the one in Deir al-Ammar-Beddawi, in northern Lebanon. The pipeline was completed in March 2005 and has a transmission capacity of over 1.5 million cubic metres of gas per day, a figure that is destined to double in the next few years. The importation of natural gas is entrusted to a single private licensee.

No laws on competition have yet been passed, nor is there any independent regulatory authority for the sector.

4.1 The electricity market The public company Electricité du Liban (EDL), operating under the control of the Ministry of Energy and Water Resources, has since 1964 held a monopoly in the generation (control and management of power stations), the transmission (transit from the main power stations to the substations) and the distribution (transit from the substations to the intermediate substations to single users) of electrical energy in Lebanon.

EDL generates over 90% of the energy used in the Lebanon, with output in the region of 2000 megawatts. 97% of the power is generated by thermal plants while a marginal amount derives from hydroelectric installations.

There is a total of seven thermal power stations: Zouk, Jieh, Baalbeck, Tyre, Zahrani, Ureiche, Deir Ammar-Beddawi and Alhereesha, together with a transmission network totalling 620 miles and a distribution structure that comprises 58 main substations.

In 2002 law no. 462 was approved, calling for the liberalisation of the market, through the separation of the various bodies appointed to definition of rights of ownership of infrastructure and regulation of the sector. This law has not yet been effectively applied and the EDL continues to operate in accordance with the legislation dating back to 1964.

Law no. 462 does however call for the dismantling of the single, vertical monopolistic structure of the sector, to be divided up into three joint stock companies under state control, labelled “privatised companies” (one for generation, one for transmission, and one for distribution). A maximum 40% share of the generation and distribution companies will be ceded to the private sector within two

24

years of their inception, while the company in charge of transmission will remain the property of the state. Shares still held by the government will put on the market at a later date.

Plans exist for the creation of an independent antitrust authority, the National Electricity Regulatory Body (NERB) with regulatory and watchdog functions in the electricity sector.

The NERB swill be charged with the following tasks:

• guarantee the implementation of regulations in relation to electricity;

• define standards and tariffs;

• settle disputes among operators or between operators and users.

25

5 The energy market in Morocco

Morocco has relatively few energy resources and counts on only a limited level of renewable energy – hydroelectric, wind and solar. Its coal reserves are nearing exhaustion and its reserves of oil and gas are negligible. The country produces about 1,000 barrels of oil per day, and 50 million cubic metres of gas per year. With about 12 million tons of petroleum imported in 2004 (at an outlay of around 2,9 billion dollars) the country is clearly highly dependent on foreign imports (90% of the energy it consumes is imported) and is lacking in energy infrastructures. Any chances of discovering viable deposits of oil or natural gas have been frustrated by the failure of the tests carried out the north east region of the Haut Plateau, while investment-hungry offshore exploration has been put on the back burner.

The country does however play a crucial role in the complex scenario of Mediterranean energy networks, as it accommodates a tract of the Maghreb-Europe (MEP) pipeline.

The MEP was conceived with the goal of transporting Algerian gas to Spain and Portugal, and has been operative since 1996. Its 1,850 km length – 45 of which run under the Straits of Gibraltar - is distributed through Algeria (520 km), Morocco (540 km), Spain and Portugal (745 km). The system currently operates at a capacity of around 9 bcm (billion cubic metres) per year, but the intention is to double this capacity, as part of a gradual infrastructure development.

The concession of rights of access for the pipeline earn Morocco a revenue amounting to 7% of the flow of gas, and this can be paid in money or in kind. Given its modest level of gas production and the remote possibilities of discovering deposits of natural gas, Morocco would have to increase its gas imports from Algeria – currently stable at 1 billion cubic metres per year. But any decision in this regard is hampered by tensions that have long existed in relations between the two countries.

Morocco forecasts that its consumption of natural gas will increase beyond 5 bcm by the year 2020. Indications from the Ministry of Energy and Mining say that the largest part of this increase will consist of liquefied natural gas imported through a network of terminals constructed and managed as much by local investors as by foreign sources. Given that each terminal costs around 500 million dollars, the level of investment needed for the realisation of the 2020 are clearly very challenging.

5.1 The electricity market Around 80% of electricity produced is generated by coal and imported petroleum. In 2004 approximately 4,8 million tons of coal and 575,000 tons of diesel were used. A further 5-9% of electricity was generated by hydroelectric power stations. Wind farms account for about 1% of output, although this sector is destined to grow. Solare energy is used almost exclusively in those villages where connection to the national grid is prohibitively expensive. The remaining quotient of energy required to satisfy internal demand is imported from Spain.

The serious inefficiency of the national network, coupled with the lack of available resources, forced the government in 1995 to turn to private foreign finance sources. The use of the BOT (Build-Operate-Transfer) instrument - in effect a licensing system – had a twofold positive effect: the acceleration of the development of the energy sector without taking on the burden of increased public debt.

In order to tackle increased internal demand, the government decided to turn to the private sector. Following the start up of the privately (foreign) owned power stations, and the conclusion of work

26

connecting up to international distribution network, the level of electricity supplied by the state fell to 35% of the total.

The first power station controlled by private capital was the Jorf Lasfar plant, managed by an American-Swiss consortium set up in 1997. More recently the Siemens Power Generation company invested around 250 million dollars for the construcutoin of a combined cycle plant, inaugurated on 19 January 2005 at Tahaddart, in the Asilah area. La Siemens also holds a 20% share of the company that manages the plant. Other partners in this company are the Office National de l’Electricité (with 48% of the capital) and the Spanish energy company Endesa (with 32%). In 205 a generation and storage plant was completed in Afourer, while work moves towards the completion of a modestly sized plant at Dakhla in the western Sahara.

Distribution remains in the hands of the government, managed through the Office National de l’Electricité (ONE). Prices are high in comparison with regional levels, which are currently on a downward trend.

At the end of 2005 the ONE presented a plan for the arrangement of the market into two segments: one regulated by tariffs established by the ONE, and the other based on competition between private companies between private national and foreign companies, for the supply of electricity to enterprise.

5.2 The liberalisation of the electricity market In 1994 the ONE lost its electricity generation monopoly and acquired the right to strike deals with private companies. Currently, the main electricity producer is private firm Jorf Lasfar Energy Company, with a share of over 60%.

Distribution is handled by the ONE and ten municipalised companies under the control of Ministry of the Interior. The municipalised companies of Casablanca, Rabat, Tétouan and Tanghera were privatised in 1997 and are controlled by French capital (the first one by Suez and the other three by Veolia Environnement).

The does however maintain its full monopoly on transport.

The liberalisation process of the electricity sector was kicked off the 1994, at a time when the energy was opening up generally.

The current regulatory structure is based on the following scheme:

• The Ministry of Energy and Mining Activity is responsible for elaborating and implementing national energy policy. It is also in charge of safeguarding the ONE, from the technical point of view;

• The Ministry of Finance is charged with the financial safeguard of the ONE and the municipalised companies;

• The Ministry of the Interior controls the municipalised companies and manages the allocation system of concessions for the distribution of electricity;

• The prices Directorate approves any changes in tariffs;

• The ONE has the task of planning the generation and transport system and making proposals for the restructuring of the tariffs system and regulatory or legislative modifications.

Preparations are being made for reform of the sector, with the following objectives:

27

• Assurance of the competitiveness of prices for industrial clients, in a context of greater openness of the Moroccan economy. In the future, electricity tariffs will have to be aligned with those of the markets of neighbouring countries, especially Spain;

• Encouragement of moves towards greater efficiency for industries that operate in monopoly situations and censure that profits are used towards the reduction of tariffs;

• Establishment of an enduring economic equilibrium. Profits must be capable of covering the costs, taking account of capital repayments and necessary future investments;

• Attraction of private investment, which can contribute to the development of the sector.

Further objectives include:

• The guarantee of a public service that includes:

o Access to electricity for all Moroccan citizens;

o Completion of the rural electrification programme;

o The application of special tariffs for low income families;

• The development of local production capability;

• Equality of access to resources by all actors engaged in distribution.

The levers of reform shall be liberalisation and regulation.

Depending on the stipulations of completed projects, the liberalised market will be based on:

- On one hand, the free choice of electricity suppliers for “eligible clients” who hope to enter this market;

- On the other hand, on the installation of free and willing producers in a system of full competition in this market.

Clients are divided into “eligible” and “non eligible”, depending on their ability to reach a target threshold defined on the basis of annual consumption. This threshold is set in accordance with statutory rules and is destined to gradually diminish.

“Eligible clients” that choose the free market will have access to a multiplicity provisioning sources who will go from Moroccan state and private production to importation, from Spain and possibly Algeria.

The regulatory authority entrusted with the task of regulating the electricity sector must:

• Set tariffs;

• Define the level and quality of services;

• Monitor the market;

• Approve planning for generation and transport of electrical energy.

The electricity regulation authority will be conceived as a public body instituted by the Presidency of the Council of Ministers, with legal personality and financial autonomy. It will be fully independent of the operators but with respect to the Moroccan government, its independence will be limited to the decisional phase.

28

The regulatory authority will enjoy, in line with the stipulations of the sectoral reform projects, broad powers of proposal and reserved competence in relation to some matters.

29

6 The energy market in Tunisia

6.1 The electricity market It is ten years since Tunisia launched its partial liberalisation process of the electricity sector. The Tunisian Electricity and Gas Company (TEGC), created by decree law no. 62-8 of 3 April 1962, held a monopoly position in the generation, distribution and transport of electricity until 1996. Law no. 96-27 of 1 April 1996 ended the monopoly of the TEGC exclusively in relation to electricity generation, allowing the State to grant licences to private producers. The conditions and methods of granting concessions were then fixed by decree 96-1125 of 20 June 1996. The decree also established:

that the choice of licensee shall be made through a call for tenders;

the creation of an Inter-parliamentary Commission for Independent Production of Electricity (ICIPE) under the Ministry of Industry, with the job of presenting the benefits to the licensee, of examining offers and submitting decisions and recommendations to the Higher Commission for the Independent Production of Electricity (HCPIE). The ICIPE also has the task of following negotiations with the independent producer chosen in accordance with the Ministry of Industry and Energy (MIE); it must define the specific agreement, the duration of the licence, the benefits accorded to the licensee, the controls and checks that can be made by the MIE, and finally, the information it must impart to the licensee;

the creation of the HCPIE, an inter-ministerial commission charged with making pronouncements on the choice of licensee, for every independent electricity production project.

The first project realised under the new law is the thermal - combined cycle plant at Radès, constructed by private operators through the BOO (Build-Own-Operate) formula; the private entity constructs and manages the plant. Production is then sold to the TEGC, which remains the sole buyer, as well as being the sole distributor and transporter of electricty in the country.

Energy consumption has grown since by 6% since 1995. Currently, 30% of electricity generation in Tunisia is carried out by the TEGC, and the remaining 30% is produced by two private companies (IIP, Independent Power Producers), the Carthage Power Company and the Societé d’Electricité d’El Bibane. 98% per cent of the territory is electrified, and this comprises 100% of urban zones and 96% of rural areas.

Although the thermal plant still have the highest output in power terms, the combined cycle units are in continual development: their output increased by 60% between 2001 and 2004. Natural gas is most used combustible fuel (around 97%) in Tunisian electricity generation. This owes mainly to the fact that the Algeria-Italy gas pipeline that runs through Tunisian territory. In 2007 the proposed Tunisia – Libya pipeline should allow the purchase of a billion cubic metres of gas per, which translates as 25% of the consumption of the gas fired power stations.

Tunisia’s interregional connections are managed through its participation in the Mediterranean Electricity Ring, which unites countries of North Africa and the Near East, and which will in turn link up with the European network.

30

Table 1 – Fuel types used for electricity generation

Fonte: TEGC, Annual report 2003

Chart 1 – Breakdown of electricity consumption

Source: TEGC, Rapporto annuale 2003

6.2 The hydrocarbons market Tunisina hydrocarbons production has remained unchanged in recent years: an increase in gas production has compensated for the reduction in crude oil production.

Existing infrastructure includes a 1260 km long network of oil transportation ducts, made up of 11 pipelines. The main one links southern Algeria with the port of La Skhira and is managed by the company Transport par Pipeline au Sahara (TRAPSA). The transport of gas is handled by a network of 12 pipelines totalling 1900 km. The main pipe is the Transmed, between Algeria and Italy, managed by SERGAZ. Finished petroleum products are transported through the SOTRAPIL managed line connecting Bizerte to the port of Radès.

La Societé Tunisienne des Industries du Raffinage (STIR) manages the only Tunisian refinery at Bizerte, which provides 30% of the country’s requirements. The STIR has held a monopoly in the importation of petroleum products since 1999. Local distributors’ selling price is set by the State.

The market for oil products is shared by five companies: la Société Nationale de Distribution du Pétrole (SNDP), a state company that sells its products under the AGIL brand and controls 47.71% of the market; EXXONMOBIL (an amalgamation of Esso and Mobil); Shell; Totalfinaelf; and Staroil, a private company of the Abbès group.

31

Petrol is distributed by SNDP, Total and Ciment-Bizerte, while LPG is dealt with by Butagaz, Sagaz, Total and SNDP. All these companies buy exclusively from the STIR, and then resell the products at prices set by the State. Price liberalisation should follow the liberalisation of imports, established by Tunisia’s association agreement with the EU by 2008. The association agreement should also determine the suspension of customs levies on all petroleum products and the harmonisation of Tunisian and EU norms related to these products.

The distribution of natural gas in Tunisia is managed by the STEG, which holds a monopoly position.

The exploration, research and exploitation of hydrocarbons and installation that enable these activities, is governed by the Hydrocarbons Code, promulgated with Law no. 99-93 of 17 August 1999 (http://www.anpe.nat.tn/up_pdf/808361.PDF)

In order to increase energy efficiency, under the tenth development plan, the Tunisian government has indicated its intention to:

• encourage foreign investment in exploration by offering incentives;

• reduce national consumption of kerosene and LPG;

• create the necessary conditions for the liberalisation of the market;

• stimulate a move towards the creation of mixed societies in the region, and the development of links with neighbouring countries.

Tunisia has long term hopes of strengthening its role the energy sector, as a transit country for exportation to Europe.