Embed Size (px)

Citation preview

Regulatory RadarJanuary 2017

Reporting period 1 till 31 January 2017

Regulatory Radar | January 2017 | EY

◄ Home

Quick Links

Regulatory Radar January 2017

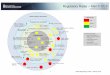

Regulatory Radar

Key Themes Timeline

Prudential ConsumerProtection

StructuralReform

CapitalMarkets

Cluster

Page 2

Regulatory Radar | December 2016 | EY

◄ Home

2. Degree of changes in monthHigh Low

1. Action for EY clientsHigh Low

3. Changes to previous month

Legend:

Regulatory Radar January 2017

► EBA – IRBA- Authorisation for the use ofabridged data histories

► ESMA - MiFID II - Transaction reportingrequirements

This month’s key themes

LeverageRatio

Risk Managementand Governance

Capital

Liquidity

Tier bankingsystem

DepositGuaranteeDirective

Bankingstructure reform

ShadowBanking

Marketinfrastructureand tradingactivities

Consumerprotection

Privacy Policy

Anti MoneyLaundering

Investmentcapital

Other participants on thefinancial market

Compliance

Reporting

Risk Data

Reporting

Audit Reform

Page 3

Overview – International / EU updates

SingleSupervisoryMechanism

Actuarial

International/EU

Regulatory Radar | January 2017 | EY

◄ Home

Regulatory RadarPrudential (1/3)

Category Theme Description Author Sector Impact TimelineCapital IRBA:

Authorisation forthe use ofshortened datahistories

Delegated Regulation on specifying conditions for data waiverpermissions published.

The main conditions are:► Evidence for the lack of appropriate longer data series► Data waiver permissions shall only be granted for the first 5

years from the date an institution started implementing theIRB Approach

► Exposures which were not included in the portfolio at thetime when the institutions first implements the IRB Approachshall also not be allowed for data waiver permission

► Exclusion of exposures to central governments, central banksand institutions from the data waiver permission

► Inclusion of exposures to corporates only if there are notstructurally characterized by few or no observed defaults.

The Delegated Regulation is addressed to all authorities andinstitutions which want to apply the IRB Approach.

It is based on Art.180 (3)(a), Art.181 (3)(b) and Art.182 (4)(b)of the Regulation (EU) Nr. 575/2013 (CRR).

See EY Regulatory Radar 01/2015.

Journalof theEU

BCM ► Facilitation of the approval of the IRB approach(data base)

► Need for additional data quality validationprocedures for shorter data series to avoidinaccurate data

03.02.2017

BCM: Banking & Capital Markets; AM: Asset Management; INS: Insurance; O: Overall

Page 5

Regulatory Radar | January 2017 | EY

◄ Home

Regulatory RadarPrudential (2/3)

Category Theme Description Author Sector Impact TimelineCapital (cont‘d.) CRD IV- editorial

changesNote:The corrigendum of the Directive 2013/36/EU is published in the Journal of the European Union.

Articels affected are such as:► Art 26 (1) Information obligations and penalties,► Art. 133 (3) Requirement to maintain a systemic risk buffer,► Art. 141 (6) Restrictions on distributions,► Art 142 (1) Capital Conservation Plan, and► Art.158 (5) Significant branches.

The corrigendum contains editorial changes and amendments on the indication of Articles.

CRR- editorialchanges

Note: The corrigendum of the Regulation (EU) No. 596/2014 is published in the Journal of the European Union.

Articels affected are such as:► Art. 19 (2) Entities excluded from the scope of prudential consolidation,► Art. 36 (1) Deductions from Common Equity Tier 1 items,► Art. 56 Deductions from Additional Tier 1 items, and► Art. 284 (6) Exposure value (CCR).

The corrigendum contains editorial changes and an amendment to the formula concerning the effective expected positive exposure(effevtive EPE) of Art.284 (6) CRR.

List of Danish O-SIIs

Note:Notification of DFSA about 6 Systemic important institutes in Denmark. For this institutions higher buffer according to CRD are required.

Liquidity

Reporting

BCM: Banking & Capital Markets; AM: Asset Management; INS: Insurance; O: Overall

Page 6

Regulatory Radar | January 2017 | EY

◄ Home

Regulatory RadarPrudential (3/3)

Category Theme Description Author Sector Impact TimelineRisk Manage-ment &Governance

Leverage Ratio No updates this month

Risk Data No updates this month

BCM: Banking & Capital Markets; AM: Asset Management; INS: Insurance; O: Overall

Page 7

Regulatory Radar | January 2017 | EY

◄ Home

Regulatory RadarConsumer Protection (1/1)

Category Theme Description Author Sector Impact TimelineConsumerProtection

MiFID II:Transactionreportingrequirements

Guidelines (final) for transaction reporting and technicalrequirements & templates detailing the relevant reportingrequirements under MIFID II and MIFIR. Increased scope ofregulatory requirements on reporting entities in the followingareas:► reference data,► transparency,► double volume cap and► transaction reporting directly to NCAs.

See EY Regulatory Radar 10/2016.

ESMA BCM The provision of additional data by reportingentities to submit transaction reports as well asthe mechanism to be used by them, includesfurther validations, schemas and technicalspecifications. Hence:► institutions may need to capture additional

data and/or have additional operational costs► institutions may need to review their

processes and controls, as well as startplanning for transition to MiFID II.

Referencedata: July2017;Transparencydata & doublevolume capdata: Sept.2017;Transactionreporting:03.01.2018

Compliance No updates this month

MoneyLaundering No updates this month

Privacy Policy No updates this month

Reporting No updates this month

BCM: Banking & Capital Markets; AM: Asset Management; INS: Insurance; O: Overall

Page 8

Regulatory Radar | January 2017 | EY

◄ Home

Regulatory RadarStructural Reform (1/1)

Category Theme Description Author Sector Impact TimelineBankingstructurereform

No updates this month

Tier bankingsystem

No updates this month

DepositGuaranteeDirective

No updates this month

Audit Reform No updates this month

SingleSupervisoryMechanism

No updates this month

BCM: Banking & Capital Markets; AM: Asset Management; INS: Insurance; O: Overall

Page 9

Regulatory Radar | January 2017 | EY

◄ Home

Regulatory RadarCapital Markets (1/4)

Category Theme Description Author Sector Impact Timeline

ShadowBanking

Re-hypothecationand collateral re-use

Note:FSB-Report regarding Re-hypothecation and collateral re-use: Potential financial stability issues, market evolution and regulatory approaches published.

Main Content► potential financial stability issues and explanation of the evolution of market practices and current regulatory approaches to the re-hypothecation of

client assets and collateral re-use.► possible harmonisation of regulatory approaches to the re-hypothecation of client assets and any residual financial stability risks associated with

collateral re-use.

The FSB encourages its member jurisdictions to implement a common basis for authorities to design their regulations with respect to re-hypothecation ofclient assets. The FSB furthermore encourages authorities to consider monitoring collateral re-use activities beyond securities financing transactions asappropriate.

non-CashCollateral Re-Use

Note:FSB- Report regarding Transforming Shadow Banking intoResilient Market-based Finance: non-Cash Collateral Re-Use published.

Main content:► measure and metrics► data elements and reporting

FSB members have agreed to transmit the national aggregated data to the FSB for global aggregation so as to assess global trends in non-cash collateralre-use.

BCM: Banking & Capital Markets; AM: Asset Management; INS: Insurance; O: Overall

Page 10

Regulatory Radar | January 2017 | EY

◄ Home

Regulatory RadarCapital Markets (2/4)

Category Theme Description Author Sector Impact Timeline

Marketinfrastructureandcommercialactivities

EMIR: Exemptionsofcollateralisationfor intragrouptransactions

Note:Conditions/ formulars for the design of the applications of financial and non-financial counterparties with regard to Art. 4 EMIR and third party dimensionpublished.

In case counterparties are not based in the same member states, financial (FC) and nonfinancial counterparties (NFCs) can be exempted from collateralobligations under the conditions of Article 11 para. 6 - 10 EMIR.

EMIR:Amendments ofReporting -Requirements totrade repositories

Note:Delegating Regulation in connection with EMIR about the minimum details of the data to be reported to trade repositories published in the Journal ofEuropean Union.

See EY Regulatory Radar 10/2016.

BCM: Banking & Capital Markets; AM: Asset Management; INS: Insurance; O: Overall

Page 11

Regulatory Radar | January 2017 | EY

◄ Home

Regulatory RadarCapital Markets (3/4)

Category Theme Description Author Sector Impact Timeline

Marketinfrastructureandcommercialactivities

(cont.d.)

EMIR: Format andfrequency oftrade reports

Note:Implementing technical standards on the format and frequency of trade reports to trade repositories published in the Journal of the European Union.

See EY Regulatory Radar 10/2016.

EMIR: Format andfrequency oftrade reports -editorial changes

Note: The corrigendum of the Implementing Regulation (EU) 2017/105 is published in the Journal of the European Union.

The corrigendum only contains editorial changes with reference to the publication date of Implementing Regulation (EU) 2017/105. The correct date ofthe publication is the 26. October 2016.

EMIR - risk-mitigationtechniques fornot centrallycleared OTC-derivative –Correction

Note:Correction fot Art. 37 of Delegated Regulation (EU) 2016/2251 supplementing Regulation (EU) No 648/2012 (EMIR) by the addition of two newparagraphs published by the European Commission.

With this correction the originally intended phase-in provision on variation margin requirements to intra-group transactions will be introduced.

EMIR: TradeRepositories

Note:Guideline (Consultation paper) on transfer of data between trade repositories (TRs) authorised under EMIR pubished.

The guidelines mainly contain:► ensuring competitive multiple-TR environment, and that TR participants can benefit from competing offers,► ensuring quality and aggregation of data available to authorities, even when the TR participant changes the TR to which it reports, and► ensuring always consistency, continuity and harmonization of transfer records from one TR to another TR, including the withdrawal of registration of a

TR.

The proposed guidelines effects the TRs as well as TR participants, reporting entities, counterparties and central counterparties (CCPs).

BCM: Banking & Capital Markets; AM: Asset Management; INS: Insurance; O: Overall

Page 12

Regulatory Radar | January 2017 | EY

◄ Home

Regulatory RadarCapital Markets (4/4)

Category Theme Description Author Sector Impact Timeline

InvestmentCapital

AssetManagement

Note:Final recommendations to address structural vulnerabilities from asset management activities published by FSB.

The 14 recommendations seek to address four financial stability risks:► liquidity mismatch between fund investments and redemption terms and conditions for fund units;► leverage within investment funds;► operational risk and challenges in stressed conditions; and► securities lending activities of asset managers and funds.

No major changes compared to the consultation.

Some of the recommendations will be operationalised by the IOSCO. IOSCO has been asked to complete its work on the liquidity recommendations by theend of 2017 and on leverage measures by the end of 2018. The FSB will regularly review progress in the operationalisation and implementation of therecommendations.

See EY Regulatory Radar 06/2016.

Other Marketparticipants

No updates this month

BCM: Banking & Capital Markets; AM: Asset Management; INS: Insurance; O: Overall

Page 13

Denmark

Regulatory Radar | January 2017 | EY

◄ Home

Regulatory RadarPrudential (1/2)

Page 15

Category Theme Description Author Sector Impact Timeline

Capital PSD2 Draft to law regarding paymentDraft on Law regarding Payment Services and ElectronicMoney (lovbekendtgørelse nr. 613 af 8. maj 2015 ombetalingstjenester og elektroniske) is in public consultation.

The purpose is to adjust the national legislation to fit therevolution of technology and hereby the implementation of theDirective on Payment Services (PSD2 Directive).

The main changes are:► Mew market players that can operate in the market for

payment services (providers of account informationservices and payment initiation services)

► Requirement to deliver upon request from third partyinformation on payment accounts to third party if thecustomer has given his/her consent

► Increased requirements in relation to authentication► Prohibition on profiling of customers► Preserve Danish special rules on cash payments

DanishFSA

BCM The consequences can be:► - New administrative burdens on the banks

and payment institutions as a consequenceof the requirement and obligation to deliveraccount information to the accountinformation service providers.

► - A need for the institutions to updateinternal policies and procedures,

► - Account information services and paymentinitiation services are introduced as newmarket players. Account information serviceproviders must be registered at the DanishFSA and are not subject to a capitalrequirement.

► Payment institutions must obtain permissionfrom the Danish FSA.

Danish special rules:► Duty to hold and receive payment in cash is

preserved (however no longer from 22:00 to06.00)

► Prohibition on profiling of customersregardless if the customer gives his/herconsent

Deadline forcomments andremarks to theDanish FSA on06.02 2017.

Deadline forimplementation of PSD2Directive innational law is13.01.2018.

Implementation expected innational law01.01.2018

Big prospectus The note contains advices concerning public offering ofsecurities or admission to trading on regulated markets forsecurities over 5.000.000 euros, as well as the Danish FSA’sprocedures for approving prospectuses.1. Legal basis2. Before applying (time-plan etc)3. Application4. Processing5. Approval6. Publication7. Fee8. Further information

DanishFSA

BCM Mainly formality changes:► - when you submit the material to the

Danish FSA it should be in electronicalform. Also, reply from the FSA will beelectronic.

► - Otherwise minor formality changes thatdo not have any major impact.

Guidance validas of 12.January 2017

Regulatory Radar | January 2017 | EY

◄ Home

Regulatory RadarPrudential (2/2)

Page 16

Category Theme Description Author Sector Impact Timeline

Capital Small prospectus The note contains advices concerning public offering ofsecurities or admission to trading on regulated markets forsecurities between 1.000.000 euros and 5.000.000 euros.

Please note that the draft on law of capital markets issuggesting that de small prospectus rules shall not becontinued.

Guidance on:1. Under which circumstances do the rules apply?2. Where can I find the rules?3. What is the estimated processing time?4. How do I submit a prospectus?5. What is checked by the FSA?6. How will the final approval and publication be carried out?7. Tips for drawing up the prospectus

DanishFSA

BCM Mainly formality changes:► the department where you are able to ask

questions regarding the prospectus rules isnow changed to the Office of CapitalMarkets in FSA (FinanstilsynetsKapitalmarkedskontor).

► The Check List have a specificationregarding the scope areas. It is specifiedthat it is the market value and possible costs(e.g. fees), that are imposed on the investor,that determines the value/size of thetender.

Guidance validas of 12.January 2017

Regulatory Radar | January 2017 | EY

◄ Home

Regulatory RadarConsumer Protection (1/2)

Page 17

BCM: Banking & Capital Markets; AM: Asset Management; INS: Insurance; O: Overall

Category Theme Description Author Sector Impact Timeline

Consumerprotection

AML The draft implements parts of the latest international standardsof the Financial Action Task Force from 2012 and the EuropeanParliament and Council Directive 2015/849/EU of 20 May 2015on prevention of the use of the financial system for moneylaundering and the finance of terror (fourth Anti Money LaundryDirective).

The changes covers a different approach going from currentregulation being primarily rule-based to become more risk-based.The purpose of this draft bill is to strengthen the effort toprevent money laundering and terror finance by furtherdisclosure of financial transactions.

MinistryofBusiness

BCMand INS(life)

The implementation of the 4th AML Directive as wellas recommendations from Financial Action TaskForce covered but is not limited to the followingmaterial possible impact:► The regulation changes to a risk approached

regulation as financial companies and othercompanies in scope must asses the risk of eachcustomer and divide the costumers in riskgroups.

► The scope of the law is amended to cover amongothers game providers and FAIF with directcostumer contact.

► Need for review of current policies andprocedures due to change of processes

► Further requirements regarding beneficialowners

► Requirements to identify national Politicalexposed persons.

► The bill was presented October 13th 2016. Someadjustments and clarifications has been amendedduring the committee.

The bill wasintroduced inthe Danishparliament onOctober 13th

Deadline forchanges to thebill wasJanuary 10th2017

The secondreading will beon February28th 2017 asthe law isexpected toenter intoforce June26th 2017

Non-life insurance The changes covers:► non-life insurance companies from other EU member states

or EØS countries that operates in the Danish market throughbranches will be able to participate in the Danish GuaranteeFund (Garantifonden) on equal terms as Danish companies.

► commit insurance agent institutions, administrationcompanies, sub-agencies and insurance distributioncompanies when doing advertisement of a non-life contractmust specify which insurance company the insurance willbelong to if the insurance company is covered by aguarantee, that will cover the receivables of the client incase of bankruptcy and the name of such guarantee.

► Introduce new information obligations for insurance agentsamong others, when conducting marketing initiatives andsales of non-life agreements.

DanishFSA

INS The bill can potentially have the followingconsequences:► increased investor protection as a consequence

of foreign companies joigning the GuaranteeScheme (Garantiordningen)

► increased information obligations for insuranceagencies, administration companies, sub-agencies and insurance distribution companies.

► Costs in relation to the Guarantee Scheme(Garantifonden) for branches of foreigncompanies among others.

► When joining the Guarantee Fund foreigncompanies and institutions must pay a one-timefee and afterwards a on-going contribution. .

Implementation 01.07.2017

Deadline ofhearing: 22.022017

The bill isexpected inMarch 2017

Regulatory Radar | January 2017 | EY

◄ Home

Regulatory RadarConsumer Protection (2/2)

Page 18

BCM: Banking & Capital Markets; AM: Asset Management; INS: Insurance; O: Overall

Category Theme Description Author Sector Impact Timeline

Consumerprotection

Real Estate The political agreement will give the real estate ownersdecreased costs when conducting changes to theirmortgages. Also, notification of price changes should begiven sooner, now 6 months prior to instead of 3 monthsprior to an increase in contribution rates, interest paymentsand other fees.

The purpose is to focus on mortgage in Denmark in relationto the increased capital requirements from Basel/CRD IV.

Content of the agreement:1. Mortgage- and banks should explain their price

increases better, increase transparency of pricechanges

2. Loan takers should be given longer notice when pricesare increased for their engagements. (changed from 3to 6 months)

3. Increased contribution rates, interest payments andother fees. must be executed, if they are adequatelydescribed.

4. Less fees when repaying loans in the notice period.5. Increased transparency on rate cuts6. More information to the loan takes when giving notice

on price increases7. More information on allocation of costs in the loan offer

from mortgage or other financial institutions8. Better possibilities to change mortgage institute, when

the lending limit is exceeded9. Better possibility to compare and more openness10. Higher liquidity on the mortgage bond market.

Ministry ofBusiness

BCM ► Increased requirements in relation to pricechanges, including the transparencyaround the drivers of the price changes aswell as more specific notificationrequirements should increase transparencyin prices.

► The notification period is extended from 3months to 6 months when increasingcontribution rates, interest rates and otherfees. An economic fine can be issued incase of inadequate warnings which couldcause an economic impact in case ofneglect to comply.

► The mortgage and financial institutions areonly allowed to charge half of thebrokerage and rate cuts or similar fees inrelation to repayment of housing loanswithin a notification period. At the sametime it is forbidden to charge redemptionfee in the notification period.

Thegovernmentwill proposethe necessaryregulation tobeimplementedas soon aspossible.

Regulatory Radar | January 2017 | EY

◄ Home

Regulatory RadarStructural Reform (1/1)

Page 19

Category Theme Description Author Sector Impact Timeline

StructuralReform

Recovery andresolutionplanning

The Danish FSA publishes draft of the Executive Order onchoice of law in terms of crises management for financialinstitutions, mortgage providers and investment companies

The Executive Order implements article 117 in the directivenumber 2014/59/EU regarding recovery and resolution forbanks (BRRD).

The changes in relation to earlier publications are:► The scope of the executive order is expanded and now also

includes incidents, where resolution activities in accordancewith the Act on Restructuring and Resolution of selectedfinancial institutions.

► Investment companies are included in the scope

► Issuers of electronic money are excluded

► some wording and structural adjustments are conductedthat doesn't cause any material impact to the ExecutiveOrder.

DanishFSA

BCM Rulings made by a foreign court or authorityregarding liquidation procedures or reorganizationmeasures towards credit institutions andinvestment companies and their branches - with aregistered office in another member state within EUor EØS - will be binding and can be executed inDenmark in the same way as it can be in the countryconducting the ruling.

Other changes in relation to earlier publications are:► The scope of the executive order is expanded

and now also includes incidents, whereresolution activities in accordance with the Acton Restructuring and Resolution of selectedfinancial institutions.

► Investment companies are included in the scope

Implementatoin01.07. 2017

Deadline ofhearing:28.02.2017

Finland

Regulatory Radar | January 2017 | EY

◄ Home

Regulatory RadarPrudential (1/1)

Category Theme Description Author Sector Impact TimelineCapital Calculation

principles whencalculating theequalizationamount for aninsurancecompany

Interpretation of FIN-SFA how the equalization amount thatrelates to claims ratio should be calculated for an insurancecompany. The statement clarifies e.g. when interest rateshould be compensated and what is appropriatecompensated interest rate.

FIN-SFA INS ► The statement may require review ofcurrent calculation practices.

26.1.2017

Capital Governmentalproposalregardingchanging thepension trustand insurancefund law

Governmental proposal proposes that the pension trust andinsurance fund law should be amended.Main content:► underwriting reserves could be covered by some

obligations, equities, holdings and other obligations inOECD countries similarly to one's in EEA countries.

► quantitative restrictions in OECD countries that relates tocovering the pension reserve or underwriting reserveswith investments in real estate are proposed to be abated

Ministryof SocialAffairsandHealth

INS ► The new law may enable use of largervariety assets in different geographies forunderwriting reserves.

1.4.2017

Capital Regulation andguidelinesregarding therisk and solvencyassessment of apensioninstitution comeinto effect onFebruary 2,2017

From 1.1.2017 onwards pension providers has to prepare arisk and solvency assessment. Due to this new obligation thecurrent requirement of risk management plan regarding theuse of insurance premiums is removed. As a part of the newsolvency assessment the descriptions of use and monitoringof the employer's solvency instalment, based on theemployer's obligation to contribute, will be included in thenew risk and solvency assessment.

FIN-FSA INS ► The new regulation may require the reviewof current reporting practices.

1.2.2017

Page 21

BCM: Banking & Capital Markets; AM: Asset Management; INS: Insurance; O: Overall

Regulatory Radar | January 2017 | EY

◄ Home

Regulatory RadarCapital Markets (1/1)

Category Theme Description Author Sector Impact TimelineInvestmentCapital

Working grouppublished thestatementregarding thedevelopmentactions ofcrowdfundingmarket

Statement of a working party how the crowdfunding marketshould be developed.

Main content:- change of gift pledge regulation would simplify the donationof fund units- preconditions for debt conversion should be clarified- act on investment services should be modified to enlargethe investor basis by reckoning foundations as investorsPlease refer Regulatory Radar ID's FI-11, FI-15 & FI-19

FinnishMinistryofFinance

BCM/INS

► Note: No impact 1.9.2017

Page 22

BCM: Banking & Capital Markets; AM: Asset Management; INS: Insurance; O: Overall

Norway

Regulatory Radar | January 2017 | EY

◄ Home

Regulatory RadarPrudential (1/1)

Category Theme Description Author Sector Impact TimelineCapital Adaption of the

capitalrequirementregulation to thenew accountingprovisionregulation (IFRS9).

Discussion paper (response):

The FSA and Central bank of Norway emphasizes that thestrict demands for loss allowances following new accountingregulation must not be diluted by including parts of theprovisions in the Tier 2 capital. FSA and Central Bank ofNorway supports an option that is based increasingly onaccounting rules, so that adjustments in capital context areonly made in relation to IFRS 9 step 1, and for thecorresponding engagements by the FASB standard.

CentralBank ofNorwayandNFSA

BCM ► The IFRS 9 - provisions must be included inthe tier 1 capital, not in the tier 2 capital.

Discussionpaper issued forcomment by 13January 2017

Reporting Regulation forcalculation ofcapital return forlife insurancecompanies andpension funds

Regulation:

The regulation extends regulations concerning thecalculation of capital return in the life insurance companiesetc., but is now adapted to the accounting regulations forinsurance companies and the accounting regulations forpension companies.

NFSA INS Minor – technical specifications regarding thecalculation of capital return for life insurers andpension funds.

01.01.2017

Reporting Rapportering forpensjonskasser iforbindelse medårsregnskapet2016

NFSA INS Minor – technical information on how to reportYear End results.

12.01.2017

Page 24

BCM: Banking & Capital Markets; AM: Asset Management; INS: Insurance; O: Overall

Regulatory Radar | January 2017 | EY

◄ Home

Regulatory RadarConsumer Protection (1/1)

Category Theme Description Author Sector Impact TimelineConsumerprotection

Proposal ofimplementingMiFID II andMiFIR. Theproposals involvesubstantialchanges to theSecuritiesTrading Act.

The report contains proposed amendments to the SecuritiesTrading Act, that will contribute to more transparent andwell-functioning markets and increased investor protection.The bill aims to implement forthcoming EEA rules (MIFID IIand MIFIR). The Commission proposes to gather theregulation of investment firms, regulated markets and stockexchange in Securities Trading Act, and to repeal the law onregulated markets (stock exchange Act). The proposalsincludes:

• Amended rules on reporting and publication of trades infinancial instruments• establishment of a new type of trading (organized tradingfacility)• regulation of algorithmic trading• introduction of trade duty for clearing obligationderivatives and listed financial instruments.• stricter disclosure requirements for investment firms andrules on product handling and compensation from othersthan the customer• rules on the establishment of position limits for commodityderivatives• strengthening of the FSA's supervisory and sanctioninstruments

Securities LawCommission

BCM ► Major impact for some players, less impactfor others.

► The biggest impact will be in these areas;► Market Structure - Greater transparency

in the markets by forcing a greater levelof trading from OTC to lit venues

► Transaction Reporting - Increase inmarket transparency – both pre and posttrade, including data on quality ofexecution

► Investor Protection - Greater protectionand information provided tocounterparties to improveunderstanding and transparency oftrades, including transparency on feedistribution and total cost

► Where does the markets see the biggestchallenges;► Data – Granularity and availability of

data is key, with enhanced data feedsrequired

► Systems - Fundamental changes tosystems and increased demands on ITsystems

► Costs – How to provide greatergranularity on costs to clients andimpact on pricing framework

► Client Communications – Need for moreeducation and communication to clientsand relationship management to smoothimpact

► Strategy – Focus on shape of go-forwardtrading model and whether existingbusiness model is still viable given theneed for greater transparency and costimplications

03.jan.18

Page 25

BCM: Banking & Capital Markets; AM: Asset Management; INS: Insurance; O: Overall

Sweden

Regulatory Radar | January 2017 | EY

◄ Home

Regulatory RadarConsumer Protection (1/2)

Category Theme Description Author Sector Impact TimelineConsumerProtection

Automatedinvesting advice

Memorandum from the SFSA.

The memorandum is a summary of the SFA's views on someaspects of automated investment advice. It states, amongother things, that;

► automated services will play an increasingly important rolein financial markets,

► automated advice can mean better access to investmentadvice,

► there are risks that need to be addressed, such as risksresulting from errors or limitations in the advising tools.

FI sees a web-based market with simplified advice as a step inthe right direction towards an independent advising market thatreaches a broad set of customers. SFA is in favor of thedevelopment taking place, but emphasizes that it is the client'sinterests that must be at the center of development.

SFSA O Due to upcoming regulations such as MiFID II,IDD and PRIIPs, which entails major transitionsand business changes for financial institutions inorder to be compliant, we are now seeing a shiftin how to approach and handle investmentadvice going forward. The market is adjustingand changing their business strategies andproduct offerings in order to simplify the adviseprocess. Automated investment advice, robo-adivse, is a concrete reaction to a stricterregulation.

By this memorandum where the FSA in generalis positive to automated investment advise alsoimpacts the market to changing and develop thisline of service and investment products toapplicable to the automation.

N/A

BCM: Banking & Capital Markets; AM: Asset Management; INS: Insurance; O: Overall

Page 27

Regulatory Radar | January 2017 | EY

◄ Home

Regulatory RadarConsumer Protection (2/2)

Category Theme Description Author Sector Impact TimelineConsumerProtection

LegislativeProposal - MiFIDII and MiFIR

Legislative proposal (lagrådsremiss) from the Ministry ofFinance.

The Minstry of Finance has proposed legislative changes in orderto implement MiFID II and MiFIR. The amendments aresubstantial, the current rules are tightened while new rules areintroduced for securities institutions and stock exchanges. Someof the proposals include:

► requirement of permits for operating OTFs and some datareporting services,

► requirements for control systems to manage the risks ofrobot trading, and,

► stricter rules for advice on investments and► SFSA also get extended oversight- and sanctions capabilities.

The proposal also means that Swedish law will be stricter thanMiFID II in terms of investment advice on an independent basis.

MinistryofFinance

O This legislative proposal has a huge impact onthe market. With MiFID II and MiFIR, banks andinvestment firms are forced to make changesacross the organization in order to becomecompliant. New IT-systems, reportingchannels, product offerings, to mention a fewareas, must be changed and adjusted. In manyways the working processes internally willchange not only between the first lineamongst business units but across all threelines of defense. In an overall perspective thisaffects how the financial industry conductsbusiness going forward.

2018-01-03

BCM: Banking & Capital Markets; AM: Asset Management; INS: Insurance; O: Overall

Page 28

Key Themes

Regulatory Radar | January 2017 | EY

◄ Home

Key ThemesOverview (1/9)Category Theme Development Detail TimelineRisk dataaggregation

Risk Data &Reporting

► „Principles for the effective aggregation of risk data and risk reporting" werepublished in January, 2013 by BCBS 239 (EU level)

► Second progress report on the implementation status on risk data aggregationby BCBS was published in December 2015

► Regulation (draft) on Single Resolution Mechanism approved, including somespecific points of BCBS 239. Scope and Form (Amendment of MaRisk, newRegulations) open

► MaRisk 2/2016 contains national implementation design

► Major impacts on IT architecture, theorganizational and IT management, data qualityframework and risk reporting

2016

Capital Review Tradingbook

► „Changes to the capital rules for the trading book“ from October 2013 (EU-level)

► Published Consultation Paper on outstanding issues related to the generalrevision of the rules for the trading book by BCBS December 2014

► Final FRTB rules published; Final rules for CVA under FRTB are expected inautumn 2016

► CRR II draft with the adoption of the final rules of the FRTB with facilities forinstitutes with smaller trading books (standard procedures can still use)

► Fundamental revision of the guidelines for thestandardized approach and internal models

► Significant capital consumption expected

2016/2017

Securitizationframe factory

► Published revised version of the revision of the securitization framework byBCBS December 2014

► Consultation Paper on delimitation / definition of simple, transparent andstandardized securitization by European Commission published (Feb 2015)

► EBA Opinion on the revision of the BCBS framework, including lower capitalrequirements for qualified securitization

► European Commission has submitted Regulations on the Revision of theSecuritization framework in September 2015

► Public ECB Guidelines for the recognition of the transfer of a significant creditrisk

► Final Standard of revised securitization rules published, with integratedconsultation on the STC - securitisations

► Final EBA-Guideline on implicit support

► Expected increase in capital exposure to newmethods

► Verification securitization strategy required► Expected impact on IT infrastructure and data

management► Lower regulatory requirements for high quality

securizations (STCs)► Establishment of processes to identify STC -

securitisations

Partiallyfrom the

end of 2015

Standardapproach

► Consultation on revision of the standard approach for credit risk in December2014 published by dependence is to be reduced by external ratings andnational discretions

► 2. Consultation paper was published in December 2015, including thereintroduction of external ratings

► Consultation paper on the treatment of accounting provisions based onExpected Credit Loss models in accordance with IFRS 9

► Analyse impact on capital requirements specificto the institution

► Impact on business strategy► Higher volatility of the capital requirements

Open(first consult)

Note: Green text indicates changes to previous month

Page 30

Regulatory Radar | January 2017 | EY

◄ Home

Category Theme Development Detail TimelineCapital(cont‘d)

IRB approach ► Proposals for the revision of the existing regulatory framework by EBA (March2015)

► BCBS consultation paper on the revision of the IRB Approach► Final RTS with the aim to harmonise the evaluation methodology . the IRB

approach in all EU Member States► Consultation paper on the treatment of accounting provisions based on

Expected Credit Loss models in accordance with IFRS 9► Draft guideline on the estimation of PD and LGD as well as the treatment of

outstanding claims

► Significant implications for IRB institutions incase of a review of the existing regulatoryframework / requirements

► IRBA-Rating Systems to be re-calibrated► Depending on whether the bank is already

applying IRBA or is in the approval process► Higher volatility of the capital requirements► Benchmarking exercise on internal models (credit

and market risks) for 2017

2020(first consult)

OpRisk ► Consultative Document on the Revision of the Standard approach to calculatethe OpRisk was published in October 2014

► Final specific requirements regarding AMA were published in June 2015► Consultation paper published on revision of standardized approach

► Analyse impact on capital requirements specificto the institution

Open

Liquidity NSFR ► Consultation paper on disclosure of NSFR published in December 2014; finalstandard in June 2015

► In December 2015 EBA published the recommendation for the introduction ofmandatory NSFR (application expected from January 2018)

► European Commission has published a consultation on the implementation ofthe NSFR to gather information of affected parties

► Binding introduction of NSFR proposed by CRR II

► Operational requirements for the calculation andreporting of liquidity ratios (i.a. adjustment ofthe reporting process)

► Compliance with the minimum LCR and the NSFRcould affect the business model and the liquiditymanagement

Immediately(Compliance

with theNSFR from

2018)

LCR ► EBA has published the Delegated Act regarding the liquidity ratio LCR, withwhich they specify details for calculation, in October 2014

► Implementing Regulation regarding LCR templates under deIVO published inMarch 2016

► Draft Guidelines on the Liquidity Coverage Ratio (LCR) disclosure, in particularto uniform tools, published in May 16

► Operative effort in line with the creation ofnotification

► Operative additional effort due to the dailydetermination of LCR ratios

► Review impact of LCR ratios on control andmanagement

Immediately

ALMM ► Final Implementing Regulation regarding ALMM report published in March 2016► Draft of technical implementation standard with new reporting sheet C66 for

the Maturity Ladder

► Consistent data warehouse is needed► Operative effort in line with the creation of

notification is expected► Review impacts on refinancing strategy

Expected by31.03.2016

Note: Green text indicates changes to previous month

Key Themes

Page 31

Overview (2/9)

Regulatory Radar | January 2017 | EY

◄ Home

Key ThemesOverview (3/9)Category Theme Development Detail TimelineBankingstructurereform/releasecontrol banks

Shielding risks ► Tier banking law in June 2013 adopted (Germany)► Published proposal on Bank structural reform of the European Commission in

January 2014. There are substantive differences between the rules. Nationalimplementation of European regulation by the separation of the banking law isopen.

► Basically, the ECB supports the draft regulation, but suggestions forimprovement, particularly in terms of scale, market making and exceptions. TheEuropean Parliament provides a deadline for amendments of the January 27,2015. Vote of the EU Parliament is expected April 2015.

► Hints published on the interpretation and application notes for application tothresholds for personal business, etc. by BaFin

► If necessary, Outsourcing of proprietarytrading in separate Trading Entity required

► High operational implementation effort► Significant impact on risk management,

funding and derivatives business

2015

RiskManagement &Governance

SREP –SupervisoryReview andEvaluationProcess

► Guideline for supervisory review and monitoring process (SREP) published indraft form.

► SREP aims at a holistic assessment of an institution and ends with a gradedassignment of a credit institution (to "failing" or "likely to fail")

► Supervisors should do a quantitative assessment of the risks of bank capital andliquidity (procedure in Germany not been provided)

► EBA published final Guidelines for SREP methods and processes in December2014, further publications about ICAAP and ILAAP were released in end of2015/beginning 2016

► Results stress test will be included with in SREP► EBA published Guideline (draft) on Information and Communication Technology

(ICT) Risks► Guideline (final) on the requirements of ICAAP and ILAAP data

► Inspection and monitoring process will changefundamentally, including methods applied bythe banks for determining its risk and liquidityrisks

► Method changes currently only roughlyrecognizable, yet should prepare futuredirectly supervised actions by the ECB on thischange process (impact analysis capitalrequirements, need for further development inthe corporate control)

Implemen-tation from

2016

Interest rate risk ► In Mai 2015 EBA published a guideline concerning interest rate risks in thebanking book

► In June 2015 BCBS published consultative document showing two alternativesfor future measurement and monitoring of interest rate risk in the banking book(IRRBB)

► Final standard for the revision of the treatment of the interest rate risk in thebanking book (IRRBB)

► CRD V draft with new IRRBB framework published; The proposals largelycorrespond to the EBA guidelines

► BaFin's general availability of the interest rate risk for institutions which havenot yet received a legally binding decision

► General ruling regarding interest rate risk in the banking book published

► Review of procedures and methods formanaging the interest rate risk

► Adaptation of existing procedures and workinstructions

► Revision and adjustment of the methods usedfor the measurement and validation of IRRBB

► Operational impact on the calculation ofadditional capital and reporting requirements

Partiallyalready

beginning in01.01.2016

Page 32

Note: Green text indicates changes to previous month

Regulatory Radar | January 2017 | EY

◄ Home

Key ThemesCategory Theme Development Detail TimelineRiskManagement &Governance(cont.d.)

MaRisk 2016 ► BaFin published in February 2016 consultation draft of the amendment ofMaRisk. Amendments concern IT risks, risk data aggregation, new productprocess, outsourcing, liquidity risk, internal audit, risk reporting

► After consideration of the results of the previous consultation, BaFin hasreleased a new draft for the 5th MaRisk amendment.

► Concern analysis is carried out to identifyadditional requirements. In this context, thetechnical requirements of SREP, BCBS 239,etc., to be considered

► Various implications on existing procedures,processes and systems in risk management,outsourcing, etc., for example. Are reviewingexisting outsourcing relationships andcontracts

Consultationuntil

04.07.2016;Adoption

estimated in2016

Resolution andrecovery plans(incl.Resolutionfonds)

BankingResolution

► Final framework "single resolution regime and Resolution Fund" (SRM) andagreement on the "Directive on the reorganization and liquidation of creditinstitutions" (BRRD) in April 2014 adopted (EU-level), on June 12, 2014published in the Official Journal

► Overview of liability cascade published within the framework of BankResolution.

► BRRD implementation act, so called recovery and resolution implementation actfrom 06.11.2014

► Miscellaneous guidelines and technical standards in connection with BankRecovery and Resolution Directive (BRRD) published, i.a. MREL and Bail-in byEU resolution authorities

► Criteria and principles for an uniform contribution rate for banks to the SingleResolution Fund (EBA)

► Further FSB provisions published in November 2015, i.a. on TLAC or on cross-border recognition and Bail-in clauses

► Determined liability status according to the kind of financial instrument► Delegated regulation of RTS for minimum data requirements of financial

contracts regarding SRM, published by the EU► Proposal with adjustments to MREL due to the adoption of the TLAC standards► CRR II draft and CRD V draft with adjustments in the field of banking structure► 20 high-level guiding principles (consultation) about guiding principle on the

Internal Total Loss-absorbing Capacity of G-SIBs (Internal TLAC) published

► Impact on Funding Strategy / Funding costs► Sustainable business model moves into focus► A recovery plan has to be developed► Review the capital resources and refinancing

strategy► Affected institutes need to ensure that in each

individual case be appropriate information► As of 01.01.2017 a separate ranking class is

created within the insolvency claims under §38of the Insolvency Code ( InsO ) for certainunsecured, unsubordinated liabilities of CRRinstitutions.

SRM: January2016

Note: Green text indicates changes to previous month

Page 33

Overview (4/9)

Regulatory Radar | January 2017 | EY

◄ Home

Key ThemesCategory Theme Development Detail TimelineResolution andrecovery plans(incl.Resolutionfonds)

Recovery Plans ► Recovery and Resolution act with requirements on the design of restructuringplans comes into force (Basis: BRRD)

► MaSan under revision► Final Policy for the design of rehabilitation plans by EBA in June 2014

published; RTS specify the corresponding requirements for Redevelopment andresolution plans (July 2014)

► Delegated regulation specify the circumstances in which contributions can bepostponed or an exclusion is possible

► Draft of delegated regulation on resolution and recovery plans► Comparative analysis of governance arrangements and indicators of recovery

plans published by the EBA► Draft for MaSan Regulation by BaFin

► Application to all CRR institutions, unless anexemption according to § 20 SAG exist

► Restructuring plan has to be set up uponrequest by BAFIN

► Differences with MaSan from April 2014

Entry intoforce

1.1.2015

SingleSupervisoryMechanism

AnaCredit(AnalyticalCredit Dataset)

► Decision establishing a common European credit register by ECB adopted on 24February 2014; Work prior request are published on websites of theBundesbank

► Originally announced finalization and resolution of the Regulation by the ECBfor summer 2015 currently expected nor for Q4 2015

► Draft published AnaCredit Directive in December 2015 (consultation). The draftspecifies Phase I of the project-AnaCredit

► Regulation on the implementation of granular statistical credit reporting systemAnaCredit adopted and published by the Governing Council

► Reporting frequency is principally monthly and sometimes quarterly► Reporting limit of 25,000 euros per borrower at an institution► Query of 89 attributes regarding credit information and credit risks

► Building new data structures with informationfrom finance, risk, and credit areas neededincluding interfaces

► Reregistered lack of information or creatingnew data flows is very likely

► ECB receives extensive possibilities for analysisand benchmarking, precise use by nationalsupervisors and ways of using data banks("Feedback Loop") announced - but notspecified in detail

from 2018

First datademand is to

be expected inmid 2017

Note: Green text indicates changes to previous month

Page 34

Overview (5/9)

Regulatory Radar | January 2017 | EY

◄ Home

Key Themes

Category Theme Development Detail TimelineSingleSupervisoryMechanism(cont.d.)

FinRep 2.0 /HGB FinRep

► In October 2014, the European Central Bank published a consultation paper onthe reporting of supervisory financial information according to national GAAPon the level of individual institutes. The final version of the regulation was thenpublished in March 2015.

► On the basis of the proportionality principle, the standards of the regulation willbe phased-in over time in accordance with the size of the institute. Significantsupervisory institutes were/are already required to comply with the reportingstandards by 12/2015 or 06/2016.

► The majority of less significant supervised institutes will be required to complywith the reporting standards by 06/2017.

► Extended deadline granted until 08.26.2016► Final ITS to implement the amendments from IFRS 9 in the FINREP report

► While larger institutes can already rely upontheir extensive experience in regulatoryreporting, less significant institutes will facesignificant technical and procedural challengesfor the first-time implementation of FinRep.

► Particularly noteworthy are the results fromthe Fin-Rep working group (Big4, banks andsupervisory authorities), which accommodatethe transition from HGB-requirements to theIFRS-oriented reporting tables.

► It is important to pay close attention to areasof intersection between FinRep and otherreporting requirements (i.e. AnaCredit) toensure consistency in reported data andthereby prove soundness in reporting toauditors and authorities

Significantsupervisedinstitutes:2015/2016

Lesssignificantsupervisedinstitutes:2017

MiFID II/MiFIR

Markets inFinancialInstruments

► Updated rules for the Markets in Financial Instruments Directive (MiFID II)adopted on 15.04.2014 by the European Parliament; on 12.06.2014 ruleswere published in the EU Official Journal

► Updated rules for the Markets in Financial Instruments Directive (MiFID II)adopted on 15.04.2014 by the European Parliament; on 12.06.2014 ruleswere published in the EU Official Journal

► Translation into German Law (Draft) of MiFID II, MiFIR, EU Market AbuseDirective/ Regulation, EU Central Securities Depositories Regulation (CSD-R)was published in October 2015

► Directive for reporting and records of businesses and clock synchronizationImplementation shifted into force on 2018

► Publication of proposed directive as supplement to MiFID II.► Various regulatory technical standards with respect to MiFID published by EU

Commission► Q&As on speculative products► Q&As on implementation of investor protection► Guideline (draft) regarding the establishment of target market assessments► Guideline (draft) on the provisions of management bodies of market operators

and data reporting services providers published.► Delegated regulation about the standard methodology for calculation and

application of position limits for commodity derivatives traded on traded venuesand economically equivalent OTC contracts published

► Second Act Amending Financial Market Regulations of the BMF

► Significant organizational effort (time andcosts, for example. Implementation ofprocesses, procedures and controls anddocumentation)

► Extended requirements regarding the datagranularity

► Strategic impacts to be expected► Impact of the standards for approval,

registration and supervisory cooperation toexisting market participants in principle to besmaller

Effective from2017

(expected)

Note: Green text indicates changes to previous month

Page 35

Overview (6/9)

Regulatory Radar | January 2017 | EY

◄ Home

Key Themes

Category Theme Development Detail TimelineData Privacy EU Privacy

Policy basicregulation

► The most significant revision of data protection law at European level since theEU data protection directive from the year 1995

► Binding definition of uniform data protection legislation for data-processingbodies in the EU Member States

► Transition period for the implementation of appropriate measures by May 2018► Discussion paper on regulatory framework with sufficient flexibility in dealing

with Big Data

► Increased documentation and reviewrequirements

► Impact on data protection managementorganization and systems

► Drastic increase possible fines for companies

Entry intoforce on

24.05.2016 ;Applicable

from25.05.2018

EU – U.S.Privacy Shield

► Follow-up regulation of the Safe Harbor scheme, which was declared for invalidby the ECJ in October 2015

► Facilitating the transfer of personal data to companies in the US ( Requirescertification of companies in the US )

► Persistent criticism of the data protection authorities on the effectiveness ofthe new regulation

► Facilitating international data transfers to theUSA in the case of entry into force of the newregulation

► Obligation to implement extended contractualand organizational measures in the event ofinvalidity or non-entry into force of the newregulation

Entry intoforce expected

from July2016

MoneyLaundering

4. EU MoneyLaunderingDirective

► Fourth Money Laundering Directive published on June 5, 2015 by the EU;further specification of the requirements, the introduction of a central registerof beneficial owners of companies

► Guideline ( consultation ) of the Joint Committee with regard to risk factors inthe assessment of AML risks published on October 21, 2015

► Guideline ( consultation ) of the Joint Committee for risk-based approach formonitoring money laundering and terrorist financing published at October 21,2015

► Draft bill for the implementation of the 4. EU Money Laundering Directive, theexecution of the EU Money Transfers Directive and the reorganization of thecentral office for financial transaction investigations published for consultationpublished

► Operating expenses by reviewing and adjustingprocedures, processes, internal systems andthe written organizational rules

Adoption26.06.2017

AccountOpening /Identification

► Revised Directive "Sound management of risks related to money laundering andfinancing of terrorism" ( original directive of January 2014) published by theBCBS on February 4, 2016; demands concerning account opening wereintegrated

► Opinion of the EBA from April 12, 2016 regarding the customer identificationprocess for asylum seekers if sufficient documents to present completeidentification are missing

► Circular BaFin published requirements for the use of video identificationprocedures when opening an account on June 10, 2016. The application will besuspended until December 31, 2016.

► Operational results in relation to theidentification processes

► Esp . with respect to the corresponding videoidentification periodic qualification /verification of employees needed

Immediately

Note: Green text indicates changes to previous month

Page 36

Overview (7/9)

Regulatory Radar | January 2017 | EY

◄ Home

Key Themes

Category Theme Development Detail TimelineConsumerProtection

Packaged Retailand Insurance-basedInvestmentProducts(PRIIPs)

► By the end of 2014, the PRIIP Regulation entered into force► It obligates the creation of basic information sheets on packaged investment

products to retail investors and insurance products with an investment element► By the end of June 2016, the Regulatory Technical Standards (RTS) on basic

information sheets were published in the context of delegates acts► Currently, the PRIIP Regulation shall apply by 01.01.2017► An extended deadline is possible, since the members of the Economic and

Monetary Affairs Committee of the European Parliament have not past thePRIIP-RTS

► Rejection of RTS to the PRIIP-Regulation by the EU parliament to the EUcommission for revision.

► Q&As regarding PRIIPs► Postponement of the first application date for the KIDs to 01.01.2018

► Identification of products which require basicinformation sheets and the classification ofproducts into one of the seven risk categories

► Development of a process for creating basicinformation sheets and its documentation forannual and ad-hoc reviews

► Monitoring process on the change of riskindicators

► Implementation and documentation ofappropriate control mechanisms

► Analysis, design and implementation ofnecessary IT-system changes

► Establishing of criteria/attributes which triggera review on the basic information sheets or theproduct approval process

► Deferred implementation date of the PRIIPRegulation likely. Thus the implementationdeadline is expected to be extended by 6-12months.

from01.01.2017

InsuranceDistributionDirective (IDD)

► In 2003, the Insurance Mediation Directive (IMD) established the necessaryEuropean basis for the distribution of insurance products

► Since 2012, the IMD has been further developed to strengthen consumerprotection

► At the European level, the advanced Insurance Distribution Directive (IDD)entered into force by February 2016

► The IDD is to be implemented into national law by February 23, 2018

► Insurance companies are advised to revise andadjust their business processes and practicesbeyond their pure sales activities

► Considerable need for action in the followingareas is required: product approval process(significant impact on sales, sales planning andproduct policy), conflicts of interest(establishing special procedures to avoidconflicts of interest in insurance investmentproducts) and remuneration systems (the newrules on broker compensation may lead toamendments of the compensation models,however this does not affect fee-basedadvisory)

from23.02.2018

Note: Green text indicates changes to previous month

Page 37

Overview (8/9)

Regulatory Radar | January 2017 | EY

◄ Home

Key Themes

Category Theme Development Detail TimelineConsumerProtection

PSD II ► The Payment Services Directive (PSD) provides the legal foundation for thecreation of an EU - wide single market for payments

► The European Parliament shall adopt the revised Payment Services Directive inOctober 2015

► Entry into force of the PSD II on January 12, 2016 ; Member States mustimplement PSD II within two years into national law

► European Banking Authority (EBA) has to provide within twelve monthsRegulatory Technical Standards (RTS), i.a. to substantiate the requiredcustomer authentication in online banking. First official draft of the RTS isexpected for the second quarter 2016

► Guidelines (draft) on the criteria for competent authorities to consider whenstipulating the minimum monetary amount of the professional indemnityinsurance for payment initiation services (PIS) and account information service(AIS) providers.

► Draft bill on the implementation of the supervisory regulations of the SecondPayment Services Directive in German law published

► By enlarging the scope, other financial marketplayers (especially formerly unregulatedcompanies, as some FinTechs) affected bydefaults on payment services

► Strategic impacts on the business modelspecific to the company to be analyzed

► Operational requirements related to theimplementation of the enhanced safety andliability requirements as well as IT andprocesses (e.g. information- and dislosureobligations)

January 2018

Note: Green text indicates changes to previous month

Page 38

Overview (9/9)

Regulatory Radar | January 2017 | EY

◄ Home

Timeline

Key Themes (1/2)

Page 39

Capital

Trading book

Securitization Framework

New Standardized Approach

New IRBA Framework

New OpRisk Framework

Liquidity NSFR, LCR, ALMM

Risk Management &Governance Risk Data aggregation*

IRRBB

MaRisk 2016

2014 01/2015 01/2016 01/2017 01/2018 01/2019

today

****

** **

****

** **

**

**G-SIFIs D-SIFIs

probably2020

Implementation on europ. Levelopen

Implementation on europ. Levelopen

ALMM NSFRLCR

Categories:PrudentialConsumer ProtectionStructural ReformCapital Markets

Final Regulation (** expected)

Application period (*extended, ** expected)

Transformation period

Regulatory Radar | January 2017 | EY

◄ Home

Timeline

Key Themes (2/2)

Consumer Protection

PRIIPs

Insurance Distribution Directive (IDD)

PSD II

Tier banking system Tier Banking Law*

Banking structurereform BRRD/SAG

Single SupervisoryMechanism

SREP

AnaCredit

Marketinfrastructure MiFID II

2014 01/2015 01/2016 01/2017 01/2018 01/2019

Effective SRM

Separation of decision /setting prohibited transactions

Step IIStep I**

Categories:PrudentialConsumer ProtectionStructural ReformCapital Markets

Final Regulation (** expected)

Application period (*extended, ** expected)

Transformation periodPage 40

today