Embed Size (px)

Citation preview

Catherine Napolitano

Deputy General Counsel, OTC Derivatives

INTL FCStone Inc.

May, 2014

Regulatory Roundup

INTL FCStone, Inc. | www.intlfcstone.com

2

• Dodd-Frank Title 7: OTC Derivatives Reform

I. Overview

II. Dodd-Frank Regulation

III. Definitions: Swaps, Options

Forwards, CTO’s

IV. Mandatory Clearing

and End User Exception

V. Swap Execution

Facilities

VI. EFRP’s

VII. Margin and Segregation

VIII. Position Limits

IX. Reporting

X. Recordkeeping

XI. Cross-Border & The Road Ahead

Regulatory Round-up 2014

3

I. Overview

4

Overview

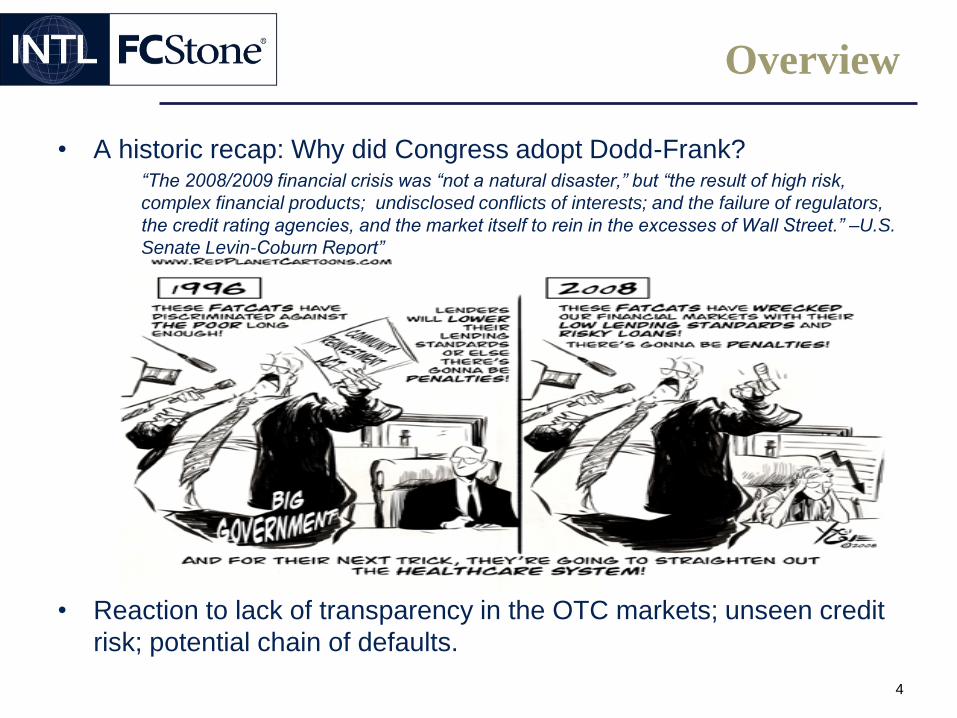

• A historic recap: Why did Congress adopt Dodd-Frank?“The 2008/2009 financial crisis was “not a natural disaster,” but “the result of high risk,

complex financial products; undisclosed conflicts of interests; and the failure of regulators,

the credit rating agencies, and the market itself to rein in the excesses of Wall Street.” –U.S.

Senate Levin-Coburn Report”

• Reaction to lack of transparency in the OTC markets; unseen credit

risk; potential chain of defaults.

5

Overview

• Final law is 1,300 pages long and it is the most comprehensive

overhaul of financial regulation since the Great Depression.

• Title 7: The CFTC and SEC now regulate OTC derivatives (otherwise

known as “swaps”).

• As of April 1, 2014, a total of 280 Dodd-Frank rulemaking requirement

deadlines have passed. This is 70.4% of the 398 total rulemaking

requirements, and 100% of the 280 rulemaking requirements with

specified deadlines.

• Of these 280 passed deadlines, 128 (45.7%) have been missed and

152 (54.3%) have been met with finalized rules. Regulators have not

yet released proposals for 44 of the 128 missed rules.

• Of the 398 total rulemaking requirements, 207 (52.1%) have been met

with finalized rules and rules have been proposed that would meet 93

(23.37%) more. Rules have not yet been proposed to meet 98 (24.6%)

rulemaking requirements.

6

Overview

• Basic Principles of Dodd-Frank

– Registration of “swap dealers,” “major swap participants,” and

swap firms (e.g., Swap IBs) with the CFTC and NFA

– CFTC will mandate that certain swaps and options be cleared

and traded on Exchanges or SEFs (except for “end user”

transactions, discussed below)

– New regulated business model for swap dealers (disclosure,

suitability, anti-fraud, risk management); more documentation

and recordkeeping obligations for both swap dealers and

customers

7

Swap Dealer Registration Exemption

• Exemptions from swap dealer registration:

– The de minimis exemption: no duty to register if small amount of

dealing swap transactions (up to $8 billion; scales down to $3

billion); exempt from registration, but certain requirements apply to

all swaps, including reporting and recordkeeping

– Co-op exemption: swaps between a co-op and its members as CPs

do not count toward de minimis threshold

8

IFM Dodd-Frank Compliance

• INTL FCStone Markets, LLC (“IFM”) registered as a swap dealer

with the CFTC in early 2013

• Established an OTC derivatives compliance function and internal

risk management program around CFTC requirements

• Prepared new OTC derivatives customer onboarding procedures,

including documentation practices and customer disclosure

requirements

• Began reporting swaps to swap data repositories in early 2013

• Monitors CFTC rulemaking developments to assess potential impact

on IFM and its swap customers

9

II. Dodd-Frank Regulation

10

Dodd-Frank Regulation

• The CFTC has jurisdiction to regulate futures, options and swap

transactions, generally excludes forward contracts and spot

transactions (except anti-manipulation enforcement authority).

• The Dodd-Frank Act establishes a comprehensive regulatory regime

for market participants transacting “swaps.”

– Definition of “swap” is not always straightforward.

– Financial products historically viewed as swaps, such OTC

commodity swaps and interest rate swaps, are “swaps” .

– Qualifying “commodity trade options” (CTOs) are subject to a

subset of the requirements applicable to “swaps”.

11

Dodd-Frank Regulation (cont’d)

• Swap dealers are subject to CFTC Business Conduct standards

which affects customers by implication

– Sales practice (disclosure, KYC, some suitability)

– Supplemental documentation (customer representations, product

disclosures)

• Swap dealers, FCMs and IBs currently must keep all records

relating to swaps (immediately accessible)

• Customers currently must keep transaction records relating to

swaps (reasonably accessible)

• All are subject to trading and market conduct prohibitions

(manipulation, wash trades, disruptive conduct, deceptive practices,

false and misleading statements)

12

Dodd-Frank Regulation (cont’d)

Are you an ECP?

• Cannot execute OTC transactions with non-ECP counterparties

(except trade options)

• ECP financial qualifications and nature of transaction:

• Individuals: $5 million in investible assets if hedging; $10m if spec

• Corporations: $1 million net worth if hedging; $10m net worth if spec

13

III. Definitions: Swaps, Options, Forwards, CTO’s

14

What is a “Swap”?

• A “swap” is:

– an executory agreement for exchange of payments based on

value of property, rate or quantitative measure and that transfers

financial risk of future change in that value without also

conveying ownership interest in an asset/liability that

incorporates that risk (e.g., rate swap, index swap);

– option on virtually anything;

– an agreement for purchase, sale, payment or delivery dependent

on occurrence, nonoccurrence or extent of occurrence of event

or contingency associated with potential financial, economic or

commercial consequence (e.g., CDS);

– any combination of the above

15

What is a “Swap”? (cont’d)

• Exclusions from “swap”:

– futures

– sale of nonfinancial commodity for deferred delivery, intended to

be physically settled (i.e., forward contract -- bookouts)

– security options, security index options, securities transactions

“subject to” Securities Act and Exchange Act;

– FX options entered into on U.S. securities exchange

– “security-based swap,” other than a “mixed swap”

– agreements where the counterparty is the Federal Reserve or

certain agencies of the US Government

16

What is a “Swap”? (cont’d)

• A “security-based swap” is a “swap” that:

– references a narrow-based security index, or single security or loan.

– is a CDS relating to single issuer(s) in a narrow-based security index

– is a “mixed swap”

• “Narrow-based” has nine or less constituents (e.g., S&P 500 swap is CFTC “swap”, not SEC “security-based swap”)

• Trades referencing government securities are excluded

17

What is an Option?

• An option is a contract in which:

– One party holds the unilateral right, not the obligation, to perform,

Whereas,

– The grantor of the option must perform if the option holder makes an election

18

What is a Forward Contract?

• A forward contract is a sale of a nonfinancial commodity, for

deferred delivery, intended to be physically settled.

• key elements:

– Contract is a commercial merchandizing transaction between

commercial market participants;

– For the sale of a “non-financial” commodity with an enforceable

obligation to make and take delivery;

– Parties intend to physically settle.

– Both parties have the obligation to make or take delivery

• Depends on the facts and circumstances.

19

Embedded Volumetric Options

• To be or Not to be, a Forward - CFTC 7-Part Test

If it’s a forward, it’s not subject to DF. Commodity Options (optionee has the

right but not the obligation to make or take delivery is therefore NOT a

forward). A Forward binds BOTH parties to make or take delivery.

Generally, a Commodity Option is a ‘swap’, however, a forward with

embedded optionality can qualify as a forward and be exempt from DF, even if

it has an element of optionality IF it meets the following 7 factors:

1. Embedded optionality does not undermine the overall nature of the agreement

as a forward;

2. The predominant feature is actual delivery;

3. The embedded optionality cannot be severed and marketed separately;

4. The seller intends physical delivery at the time it enters the agreement;

5. The buyer intends physical delivery at the time it enters the agreement;

6. Both parties are commercial parties; and

20

The 7th Prong

7. The exercise or non-exercise of the embedded volumetric

optionality is based primarily on physical factors or regulatory

requirements that are outside the control of the parties and are

influencing demand for, or supply of, the commodity.

• Following the CFTC’s April, 2014 End User Roundtable, the CFTC

may clarify the ‘seventh prong’. Industry need to use economic

conditions as a factor.

21

Decision Tree for Forward Contracts with Embedded Optionality

22

Commodity Trade Options

• CTOs (swaps) are exempt from most swap regulations IF:

– Both counterparties intend physical settlement; and

– Seller and buyer meet certain requirements.

– Option seller must be an ECP or a producer, processor or

commercial user of, or merchant handling the commodity or

products or by-products solely related to its business.

– Option seller must have a reasonable belief the buyer is a

producer, processor or commercial user or merchant handling

the commodity or products or by-products; and

– Enter into the transaction solely for purposes related to its

business (i.e., hedging or inventory management).

23

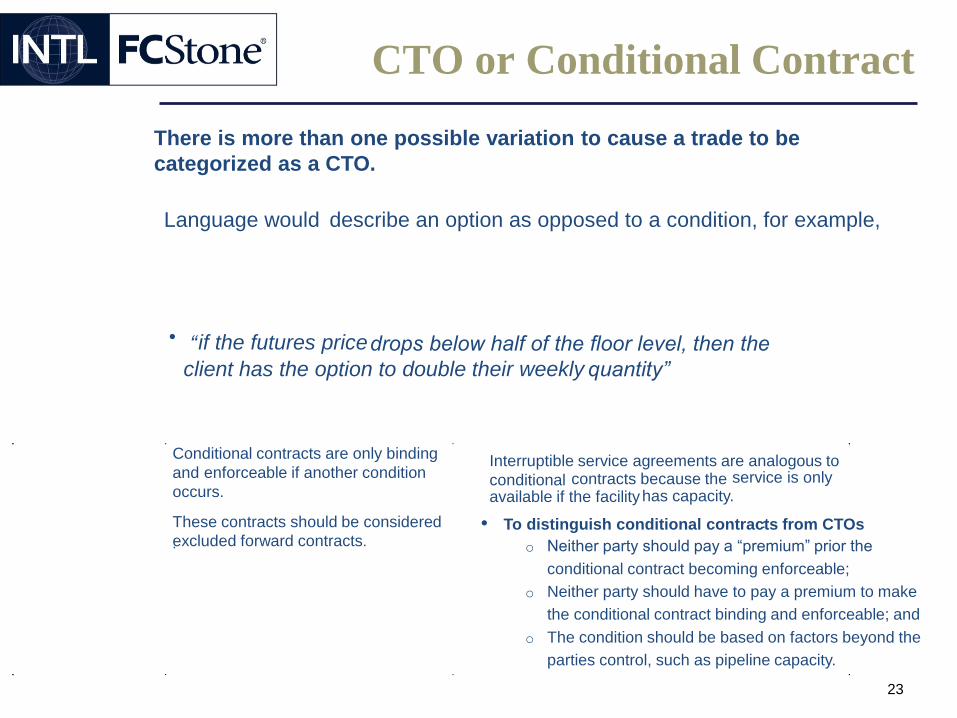

CTO or Conditional Contract

There is more than one possible variation to cause a trade to be

categorized as a CTO.

Language would describe an option as opposed to a condition, for example,

if the futures price “ drops below half of the floor level, then the

client has the option to double their weekly quantity”

Conditional contracts are only binding

and enforceable if another condition

occurs.

These contracts should be considered

excluded forward contracts. .

Interruptible service agreements are analogous to

conditional contracts because the service is only

available if the facility has capacity.

To distinguish conditional contracts from CTOs:

o Neither party should pay a “premium” prior the

conditional contract becoming enforceable;

o Neither party should have to pay a premium to make

the conditional contract binding and enforceable; and

o The condition should be based on factors beyond the

parties control, such as pipeline capacity.

24

Rules Applicable to CTOs

Who Reports CTOs?

• If a CTO counterparty is a SD/MSP, the SD/MSP reports the swap

to the SDR.

• If neither counterparty is a SD/MSP, the counterparties are not

required to report on a trade-by-trade basis IF:

– Parties file annual reports on CFTC Form TO; and

– Notify the CFTC if/when CTOs exceed $1billion in a calendar

year.

• Reports are due March 1st for the previous calendar year. (First

CFTC Form TO was due March 1, 2014 for reporting year-end

December 31, 2013.)

25

IV. Mandatory Clearing and End User Exception

26

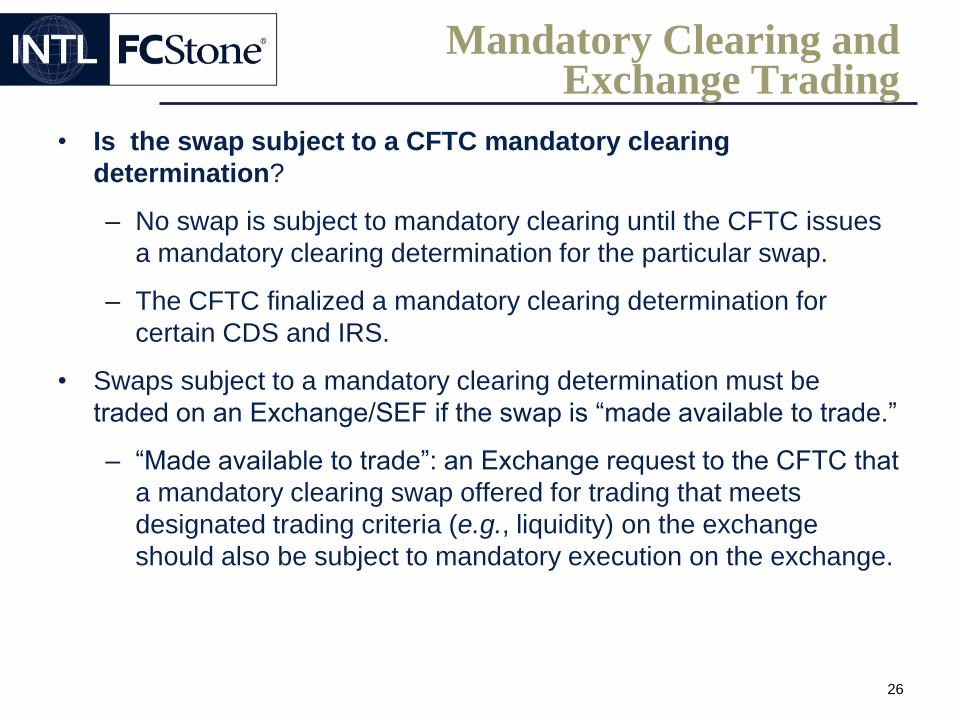

Mandatory Clearing andExchange Trading

• Is the swap subject to a CFTC mandatory clearing

determination?

– No swap is subject to mandatory clearing until the CFTC issues

a mandatory clearing determination for the particular swap.

– The CFTC finalized a mandatory clearing determination for

certain CDS and IRS.

• Swaps subject to a mandatory clearing determination must be

traded on an Exchange/SEF if the swap is “made available to trade.”

– “Made available to trade”: an Exchange request to the CFTC that

a mandatory clearing swap offered for trading that meets

designated trading criteria (e.g., liquidity) on the exchange

should also be subject to mandatory execution on the exchange.

27

Cleared Swaps

• STEP 1: Counterparties enter into a swap, bilateral OTC,

Exchange, or SEF. Each party must have an FCM agreement in

place with an FCM clearinghouse member.

• STEP 2: FCM(s) submit the trade as agents for the parties and

will then submit the trade to a clearinghouse for clearing.

• STEP 3: Trade is accepted for clearing by the clearinghouse.

The original trade is terminated. Two new separate trades arise: (i)

one between the clearinghouse and the dealer-counterparty(or an

FCM affiliate of the dealer); and (ii) one between the customer and

the clearinghouse.

• STEP 4: Margin and Settlement. Each counterparty has exposure

only to the clearinghouse, not to each other.

28

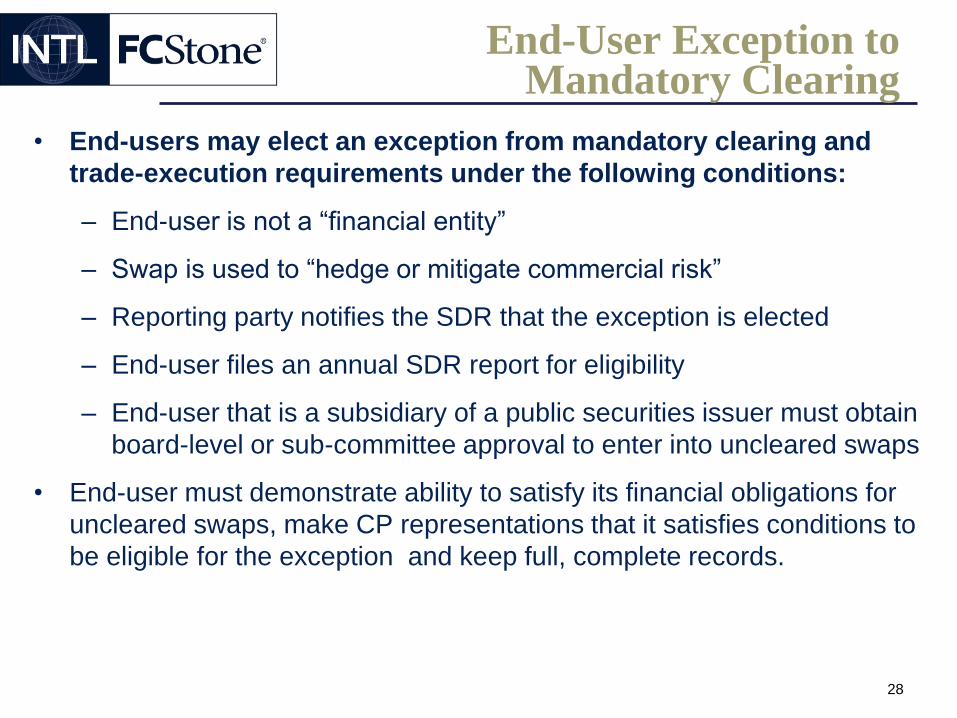

End-User Exception toMandatory Clearing

• End-users may elect an exception from mandatory clearing and

trade-execution requirements under the following conditions:

– End-user is not a “financial entity”

– Swap is used to “hedge or mitigate commercial risk”

– Reporting party notifies the SDR that the exception is elected

– End-user files an annual SDR report for eligibility

– End-user that is a subsidiary of a public securities issuer must obtain

board-level or sub-committee approval to enter into uncleared swaps

• End-user must demonstrate ability to satisfy its financial obligations for

uncleared swaps, make CP representations that it satisfies conditions to

be eligible for the exception and keep full, complete records.

29

Financial Entity

• What is a “Financial Entity?

• A “financial entity” includes commodity pools, swap dealers, MSPs,

private funds and an entity “predominantly engaged” (85% of assets

or revenue) in activities that are “financial in nature.”

– “Financial in nature” - trades OTC swaps, financial options,

swaptions, futures, options on futures, and certain forwards that

are cash settled or booked out.

Consult your legal – compliance team to determine whether

activities fall within “financial entity” definition.

30

Hedging or Mitigating Commercial Risk

Swaps that “Hedge or Mitigate Commercial Risk”

These swaps qualify for:

1) the bona fide hedge exemption from position limits

2) hedging treatment under FASB Topic 815

Swaps economically appropriate to reduce risks in the conduct and

management of a commercial enterprise (e.g., the swap hedges

potential changes in the value of assets, liabilities, or services used or

incurred in a commercial business).

31

V. Swap Execution Facilities

32

Types of SEF Participants

• Swap dealers (executing dealers, liquidity and RFQ providers)

• Introducing brokers and Intermediaries

• Asset managers

• Funds

• Prime brokers

• End-users

• Non-U.S. persons

33

SEF Membership

– Members agree to all Rulebook terms, subject to change without

members consent

– SEF monitoring and oversight responsibilities that members

must agree to, include cash penalties for non-compliance

– Membership triggers CFTC regulations (Rule 1.35’s extensive

recordkeeping obligations)

– Available to Eligible Contract Participants (ECPs)

– Must offer fair non-discriminatory access but can set different

categories of participants, if participants within each category are

treated equally

34

SEF Documentation

– User Agreement

– Rulebook

– Bilateral Agreements between other participants with whom you will

be trading (settlement procedures – e.g., ISDA)

– Clearing Agreement with clearing member (for cleared swaps); and

– Brokerage or Prime Brokerage Agreement (with intermediary)

35

SEFs and Intermediaries(Brokers)

• To gain access to SEFs through intermediaries

– Similar to the FCM model used on DCMs, but SEF

intermediation is different because more participants can have

direct access to the SEF.

– Brokerage agreements may need to be modified per SEF rules

• Intermediary issues:

– What is the extent of disclosures they must provide to

participants, and will participants use this information?

– Ensuring ECP status for many participants

– Potential liability for disruptive trading practices

– Non-U.S. intermediaries may need to register as IBs if they have

U.S. customers.

36

SEFs and Asset Managers

• Who is the SEF “Participant”?

• Unclear whether the fund or investment manager is the “Participant”

(i.e., “Member”)

– Asset managers want the fund to be the participant to relieve the investment

manager from transaction liability

• SEF rulebooks typically require asset managers to enter into

“Intermediary Agreements” with their participants –

– Commonly require contract between asset manager and client to “incorporate all

SEF rules,” which may be practically impossible

37

SEFs and Funds

• Confidentiality

– Some funds seek rights to damages if the SEF breaches

confidentiality

– Unclear whether SEFs can enter into such agreements due to

impartial access restrictions

• Issues with jurisdictional matters and dispute resolution for

government and semi-governmental funds

• ERISA plans may be prohibited from dealing with certain

counterparties- could be matched with a “party in interest” on an

order book

38

SEFs and Prime Brokers

• Point of Execution

– Prime brokered swaps were historically not considered to be

executed until sent to the prime broker for credit approval

– Prime brokers do not want SEF-trades to be “executed” until the

prime broker approves them. This causes complications:

– Does execution occur on a SEF? If not, what is the purpose of

the SEF?

– If no execution occurs on the SEF, can ‘Permitted Transactions’

be “negotiated” on a non-SEF platform and “executed”

bilaterally? Who provides confirmations? Who fulfills reporting?

Is the prime broker acting as a multi-to-multi platform, i.e., does it

needs to register as a SEF?

39

SEFs and End-Users

• Liquidity

– If dealers do not trade on SEFs, end-users may seek out single-

dealer platforms for liquidity. This will further decrease liquidity.

– Many end-users still prefer voice brokerage

• What’s the issues with accommodating voice brokerage on a

SEF?

• Sending an RFQ to too many participants can cause information

leakage, which can result in a “winner’s curse”.

• i.e., if other participants can trade ahead of the SD that “wins” the

RFQ, then SDs may quote higher prices to end-users.

• For mandatory cleared swaps, SEFs may also designate MAT. End

users, however, may chose to not clear and not trade. If they chose

the exception, can they trade on a “Permissive Side” of the SEF?

40

SEFs and Cross-Border Issues

What’s the Cross-Border Issue?

• U.S. SEFs can offer trading to anyone, however:

– If non-U.S. Persons participate, their home jurisdiction may

deem a SEF to be ‘doing business’ in that jurisdiction.

– Conversely, a non-U.S. platform offering trading privileges to

U.S. Persons is deemed to ‘do business’ in the US, subject to

SEF registration.

• Does DF apply if a U.S. Person is matched with a non-U.S.

Person on a SEF? Unclear. Substituted compliance pending.

41

VI. EFRPs

42

Futures May not be Pre-Arranged

• Generally, futures and options on futures must be executed by open

outcry on the trading floor or an Exchange electronic platform.

• CFTC permits limited prearranged trades under Block Trades rules

or Exchange of Futures for Related Positions (EFRPs).

• Effective June 2, 2014, CME will prohibit transitory EFRPs

previously permitted in foreign currency, NYMEX energy and

COMEX and NYMEX metals.

• Expect other Exchanges to mirror approach.

43

Exchange Of Futures ForRelated Positions (“EFRPs”)

• A prohibited transitory EFRP is one where execution of an EFRP is contingent upon execution of another EFRP or related position transaction, where transactions result in offset of the related position.

• The time period between the transactions is a factor considered in assessing whether the EFRP is transitory; however the legitimacy of the transactions will be evaluated based on whether the transactions have integrity as independent transactions exposed to market risk that is material in the context of the transactions. CME Rule 538.

• Where economically equivalent futures trade on a CME Group Exchange and another Exchange, the contingent execution between two parties of equal and opposite EFRPs on each exchange where the related position components offset and are not subject to market risk is a prohibited transitory EFRP, by the CME. CME Advisory Q&A.13.

• Do’s & Don'ts- what we know Today

44

The Road Ahead

• Significant Rules Expected to Take Effect or Finalized in 2014

– Mandatory Clearing Determinations for F/X and Ag Swaps

– Revised Position Limits for Customers and the Firm

– Swap Dealer Capital and Minimum Margin Requirements

45

VII. Margin and Segregation Requirements

46

Margin and Segregation Overview

SD/MSPs shall meet minimum capital, initial and variation margin

requirements as prudential regulators or CFTC prescribe.

Background-

• CFTC and Prudential Regulators proposed uncleared swap margin

rules in April and May 2011, respectively.

• SEC proposed its rule in January 2013.

• BCBS/IOSCO finalized final policy frameworks on uncleared swap

margin requirements in September 2013.

47

Segregation of Initial Margin

Segregate Uncleared Swap Collateral

• Effective May 5th 2014, counterparty may elect to have an unaffiliated

custodian hold initial margin, for a fee, pursuant to a Collateral Control

Agreement.

• Variation margin is elective, not mandatory.

• Requires SD/MSP to-

i. segregate cash and other collateral for the benefit of the

counterparty; and

ii. maintain collateral separate from the SD/MSPs assets and

interests.

(CFTC Rules 23.700-23.704)

48

Uncleared Swap Collateral (cont’d)

Swap Counterparty Can Change Election- Deadlines

• An election changed prior to the following dates will only impact

uncleared swaps entered into on or after the relevant compliance

date.

• If the Counterparty did not have an OTC agreement with the SD

as of January 6, 2014, the compliance date was May 5, 2014.

• If the Counterparty did have an OTC agreement with the SD as

of January 6, 2014, the compliance date is November 3, 2014.

49

Margin for Cleared Swaps

• Clearing Members must collect customer collateral on cleared

swaps.

– If a customer fails to meet its obligations, the FCM can use the value of

the collateral posted to meet the obligation.

• DCOs must collect margin on a gross basis for each clearing

member’s account.

– DCOs are unable to establish margin requirements by netting one

customer’s positions against another.

50

Margin for ClearedSwaps

Cleared Swaps Margin

• DCOs will set minimum collateral for each type of swap and

determine the minimum level for portfolios of swaps, to include:

• Initial Margin posted as a performance bond to cover potential future

exposures from changes in market value of the position.

– For most OTC derivatives, the DCO must collect enough initial margin

to cover 5 days of market movement with a 99% confidence level.

– For futures and options, the DCO must collect enough initial margin to

cover at least 1 day of market movement with a 99% confidence level.

• Variation Margin needs to cover current exposure since the trade was

executed or the previous mark to market.

• DCOs conduct variation margin collection and payment at least

once a day, some DCOs undertake twice a day.

51

Segregation of CustomerCollateral

FCM Duty to Segregate

• FCM to segregate from its own assets all property deposited by

futures customers to margin, secure, or guarantee futures/options

on futures traded on DCMs.

• Treat customer funds as belonging to the futures customer.

• FCM prohibited from using margined funds to extend credit to

anyone other than the customer who deposited the funds.

• FCM to segregate from its own assets all property deposited by

cleared swap customers to margin transactions in cleared swaps.

(CEA Section 4d(a)(2) and related provisions)

52

Documentation for Cleared Swaps

Futures Customer Account Agreement - Addendum

• The Addendum for Cleared Swaps modifies the form FCA to allow

the FCM customer to clear swaps, in addition to futures.

• Key Addendum provisions:

– Deliver information to the customer about the FCM, collateral,

margin and other requirements

– Margin amounts, payment obligations and eligible collateral

– Events of default and cure periods

– Porting rights, pre-default transfer by customer

– FCM’s treatment of customer collateral

– Assignment

53

Documentation forCleared Swaps (cont’d)

Execution Agreement

Addresses submission of a swap for clearing and what happens if it

fails to clear.

• Give-Up Agreement – Governs assignment of the trade from

executing FCM to Clearing FCM.

• ISDA Master & CSA – If a swap is not ‘made available for trading’,

and not subject to mandatory trading, it can still be executed

bilaterally and submitted to a clearing house for clearing.

• In that case, the swap may still need to be executed under an ISDA

Master Agreement.

• If the swap fails to clear, ISDA Master and CSA terms control.

54

VIII. Position Limits

55

Proposed Rules: Position Limits and Aggregation

Two proposed rules relate to position limits:

1. First rule to establish position limits on 28 “Core Referenced Futures

Contracts” (“CRFCs”) and futures and swaps economically equivalent to the

28 futures contracts (“Referenced Contracts”)

2. Second rule to amend aggregation requirements applicable to position limits

• (CFTC scheduled to hold an ‘Anticipatory Hedging Roundtable’ in June,

2014 and re-open the comment period.)

56

Key Elements of the Proposed Position Limits Regime

Proposed Changes

• Hard Spot Month and Non-Spot Month Limits

• Narrow definition of bona fide hedging

• Risk management exemption limited to “excluded” commodity derivatives

(i.e., financial commodities)

• Expand exemptions from aggregation

57

Core Referenced Futures Contracts

Core Referenced Futures Contracts (“CRFCs”) Subject to Position Limits

Same as 2011 Vacated Position Limits Rule

Legacy Agricultural

CBOT Corn

CBOT Oats

CBOT Soybean Meal

CBOT Soybean Oil

CBOT Soybeans

CBOT Wheat

IFUS Cotton No. 2

KCBT Hard Winter Wheat

MGX Hard Red Spring Wheat

Energy

NYMEX WTI

NYMEX NYH RBOB

NYMEX Henry Hub

NYMEX ULSD HO

Metals

CMX Gold

CMX Silver

CMX Copper

NYMEX Palladium

NYMEX Platinum

Non-Legacy

Agricultural

CME Feeder Cattle

CME Lean Hog

CME Live Cattle

CME Class III Milk

CBOT Rough Rice

IFUS Cocoa

IFUS Coffee

IFUS FCOJ

IFUS Sugar No. 11

IFUS Sugar No. 16

58

Referenced Contracts

Referenced Contracts are subject to position limits.

• They include CRFCs and other futures, options or swaps that are:

– Directly or indirectly linked to the price of a CRFC (e.g., NYMEX WTI

and ICE WTI)

or

– Directly or indirectly linked to the price of the same commodity

underlying the applicable CRFC for delivery at the same location

• CFTC staff has published a list of 464 Referenced Contracts

59

Excluded from the Definition of Referenced Contracts

• Basis Contract- a commodity derivative contract that is cash-settled based

on the difference in price of:

– A CRFC or a commodity deliverable at par, premium, or discount under

a CRFC; and

– The price of either of the following at a different location to the CRFC.

60

Levels of Spot Month Position Limits

• CFTC proposes to set spot month limits at 25 percent of estimated

deliverable supply

• Proposed limits are based on the current exchange spot month limits;

however, the CFTC is considering CME estimates of deliverable supply,

which would significantly increase spot month position limits for several

commodities

61

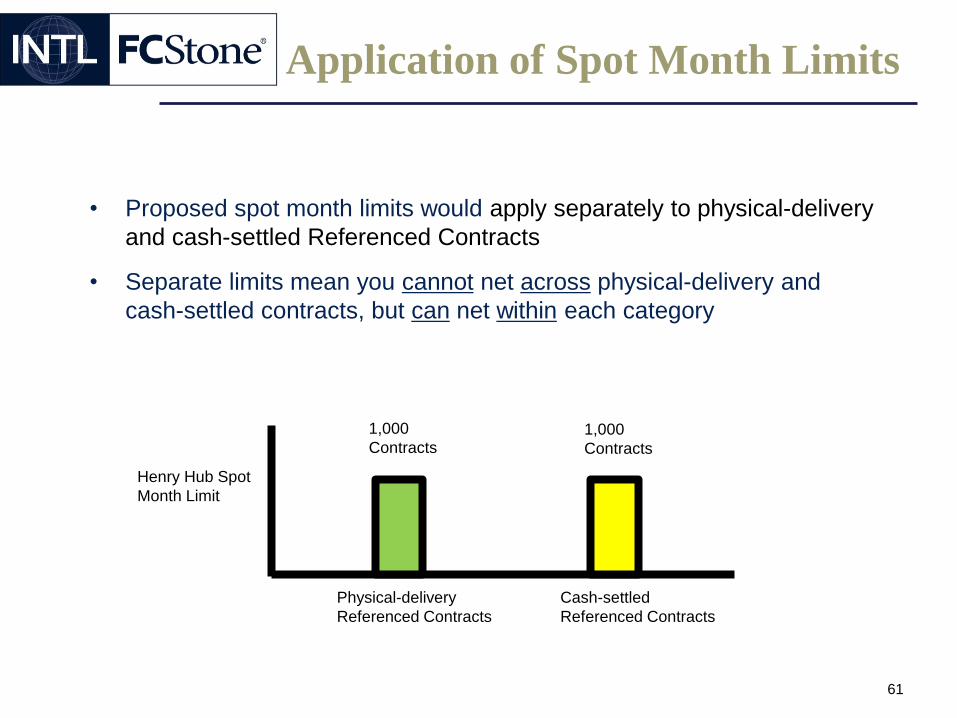

Application of Spot Month Limits

• Proposed spot month limits would apply separately to physical-delivery

and cash-settled Referenced Contracts

• Separate limits mean you cannot net across physical-delivery and

cash-settled contracts, but can net within each category

Physical-delivery

Referenced Contracts

Cash-settled

Referenced Contracts

Henry Hub Spot

Month Limit

1,000

Contracts1,000

Contracts

62

General Definition of Bona Fide Hedging

• CFTC proposes a general definition of bona fide hedging for excluded

(financial) commodities and physical commodities (e.g., metals, energy and

agricultural)

• Bona fide hedge positions for physical commodities must:

– Represent a substitute for positions taken or to be taken in the physical

marketing channel;

– Be economically appropriate for the reduction of risk (only up to pro rata

ownership interest of affiliate or subsidiary);

– Arise from a change in value of assets, liabilities, or services; and

– Qualify as an enumerated hedging position

63

Incidental Test & Orderly Trading Requirement

• Incidental test: hedged risks must arise from commercial cash market

activities

• Orderly trading requirement:

– market participants must exercise “ordinary care” when establishing and

liquidating positions;

• evaluated based on totality of facts and circumstances

– “negligent trading” is grounds for disallowing a bona fide hedge

exemption

– CFTC intends to apply the policy in the Disruptive Trading Interpretive

Guidance to the position limits orderly trading requirement

64

Enumerated Hedging Positions

Enumerated hedging positions include hedges of:

– Inventory and fixed-price purchases

– Fixed-price sales

– Unfilled anticipated requirements (limited application in the spot month) & Unfilled anticipated

requirements for resale by a utility

– Hedges by agents

• Plus the following contracts, unless the hedge is a physical-delivery Referenced

Contract held in the last 5 days of trading (agricultural and metals) or the last 3

days of trading (energy):

– Unsold anticipated production

– Offsetting unfixed-price cash commodity sales and purchases

– Anticipated royalties

– Services & Cross-commodity hedges

65

Form 204: Bona Fide Hedge Positions

Filing Threshold What to Report First Report Due Frequency of Filing

(1) Exceeding a

Federal position

limit; or

(2) Exceeding a

reportable position

level in CFTC

Rule 15.03 and

receipt of a special

call from the

CFTC.

Cash market positions

eligible for a bona fide

hedge exemption. Do not

include bona fide hedge

positions reported on Form

604.

COB the last

Friday of the

Month.

Monthly. Continue

reporting until positions

in a given month do not

exceed a position limit.

66

IX. Reporting Obligations

67

Reporting Swap Transactions

Report Swaps to an SDR- A Review

• Bilateral swaps not cleared or SEF- executed are reported by-

– A SD/MSP or financial entity if the other CP an end-user; or

– An end-user, if the other counterparty s also an end-user.

• End-users must agree among themselves who will report.

• Similarly, SDs that trade with other SDs must agree.

• Obtain a Legal Entity Identifier (LEI) or CFTC Interim Compliant

Identifiers (CICIs) from DTCC-SWIFT.

68

Large Trader Reporting

Are you a ‘Large Trader?

• Clearing organizations, clearing members and SDs must file daily

position reports for “paired swaps” economically equivalent to

specified futures contracts.

• To determine position size, swap positions are converted to futures-

equivalent positions.

• All entities holding 50+ gross all-months-combined futures

equivalent positions in contracts covered under Large Trader Rules

are subject to recordkeeping & CFTC’s special calls.

69

Large Trader Reporting (cont’d)

CBOT CME COMEX

ICE Futures

US

KCBOT/MGE

X NYSE/Liffe NYMEX

Corn Butter Copper Cocoa Wheat 100 oz Gold Cocoa

Ethanol Cheese Gold Coffee 5000 oz Silver Brent Financial

Oats Dry Whey Silver Cotton No. 2 Central Appalachian Coal

Rough Rice Feeder Cattle FCOJ Coffee

Soybeans Hardwood Pulp Sugar No. 11 Cotton

Soybean Meal Lean Hogs Sugar No. 16 Light Sweet Crude Oil

Soybean Oil Live Cattle RBOB

Wheat Class III Milk Hot Rolled Coil Steel

Non Fat Dry Milk Natural Gas

Random Length Lumber New York Harbor No. 2 Heating Oil

Softwood Pulp Palladium

Platinum

Sugar No. 11

Uranium

70

X. Recordkeeping Obligations

71

Recordkeeping Obligations

Recordkeeping- A Review

• End-users keep full, complete and systematic records, all pertinent

data and memoranda regarding their swaps, including records

regarding their use of the end-user exception to mandatory clearing.

– Records of all orders (filled, unfilled, or canceled), trading cards,

journals, ledgers, canceled checks, and copies of confirmations.

• End-users keep records regarding cash transactions underlying

futures hedge exemption(s).

• Retained throughout the life of the swap plus five years following

final termination of the swap.

• Retrievable within five business days.

• Available on request to the CFTC, SEC, DOJ or any bank regulator.

72

RecordkeepingObligations (cont’d)

• Members of contract markets or those with trading privileges are

subject to additional recordkeeping obligations (Rule 1.35).

• Retain all records prepared in the course of business dealing in

commodity interests (e.g., futures, swaps, options) and related cash

commodities.

• SDs/MSPs keep pre-execution information (e.g., oral and written

quotes, solicitations, bids, prices and trading information

communicated by telephone, voicemail, faxes, instant messaging,

chat room and other methods of communication.)

• SDs/MSPs keep post-execution information including confirmations,

termination, novation, amendments, margining, collateralization, and

central clearing information.

• Record voice communications.

73

XI. Cross-Border and The Road Ahead

74

Cross Border Issues

Industry Initiatives

* ISDA, SIFMA & IIB

What are the boundaries?

• The swap provisions of the DFA shall not apply to activities outside

the United States, unless activities have a direct and significant

connection with activities in, or effect on, US commerce or

contravene CFTC rules necessary or appropriate to prevent evasion

of the DFA. (DFA Section 722).

Thank You

Catherine E. Napolitano

Deputy General Counsel, OTC Derivatives

INTL FCStone Inc.