Embed Size (px)

Citation preview

RegulatoryseachangeforOTCderivatives:Theclearingandmarginingrevolution

May2014

SOLUMFINANCIALwww.solum‐financial.com

2

Introduction

Over‐the‐counter(OTC)derivativesmarketsatlarge–andtheirinfrastructureinparticular–havebeenakeyareaofcapitalmarketsparticularlyaffectedbytheregulatoryreformsenactedoverthepastfewyears.Inthewakeofthefinancialcrisis,globalpolicymakers(startingwiththeG‐20agreementofSeptember2009)agreedonaseriesofmeasuresdesignedtoimprovethetransparencyandtherobustnessoftheOTCderivativesmarket.Thispaperhighlightsthemajorchangesthathavetakenplacetodateandthesignificantassociatedchangesinthewayfinancialinstitutionsmanagetheimpactedbusinesses.

There are variousdifferences in the contours of the regulatory agenda inEurope (EMIR/MiFID) vs. theUS(Dodd‐FrankActandCFTC/SECregulations)–mostnotablyintermsoftherespectivetimelines,butalsowithrespect to scope, regulated entities and extent of the measures. However, the pillars of OTC derivativesregulatory reform are fairly comparable across jurisdictions and are broadly anchored to themajor statedprinciples of i) increased transparency and ii) decreased interconnectedness of instutions trading in thosemarkets.

Inparticular,allOTCderivativescontractsdeemedtobestandardisedwillhavetobemovedtoexchangesorelectronictradingplatforms,andclearedthroughcentralcounterparties1.Moreover,forthosetransactionsthatarenotcentrallycleared,bilateralmarginrequirementsandhighercapitalchargeswillbeinorderalongwithaswatheofmeasuresdesignedtoimprovetheriskmanagementandtransparencyofsuchmarkets.

In sum, themajor objectives of improved transparency, robustness and decreasing interconnectedness areachievedthroughthefollowingmajorpillarsofglobalOTCderivativesreform:

mandatoryreportingtotraderepositories exchangeand/orelectronictradingofstandardisedOTCderivatives mandatorycentralclearingforstandardisedderivatives bilateralmarginrequirements,highercapitalchargesandtightenedriskmanagementpracticesfornon‐

centrallyclearedOTCderivatives

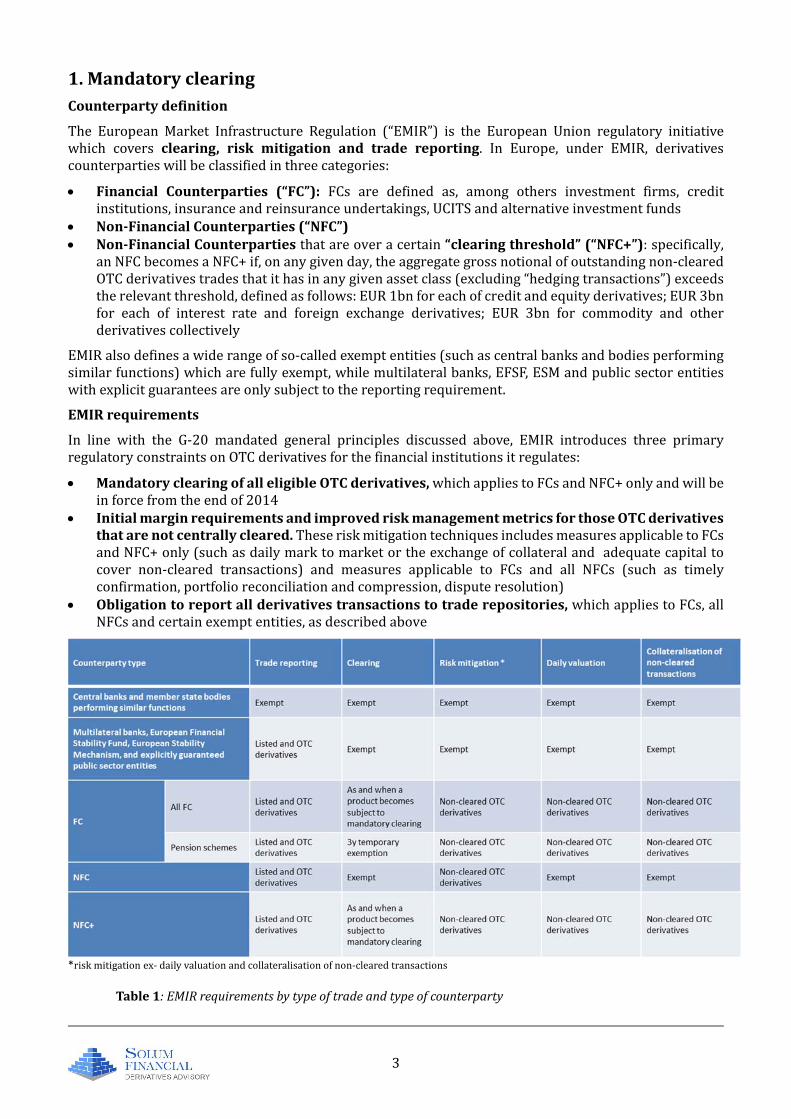

Todate,theendresultofthisOTCderivativesregulatoryavalanchehasbeenamaterialreductionofoutstandingOTC bilateral risk, through compressions and steadymigration towards central counterparty platforms, asshowninChart1.

Chart1:Asmaller,leanerOTCderivativesmarket

1 In a February 2014 paper, ISDA estimated that as of mid-year 2013, 90% of the interest rate derivatives products subject to the clearing obligation to date had been cleared.

3

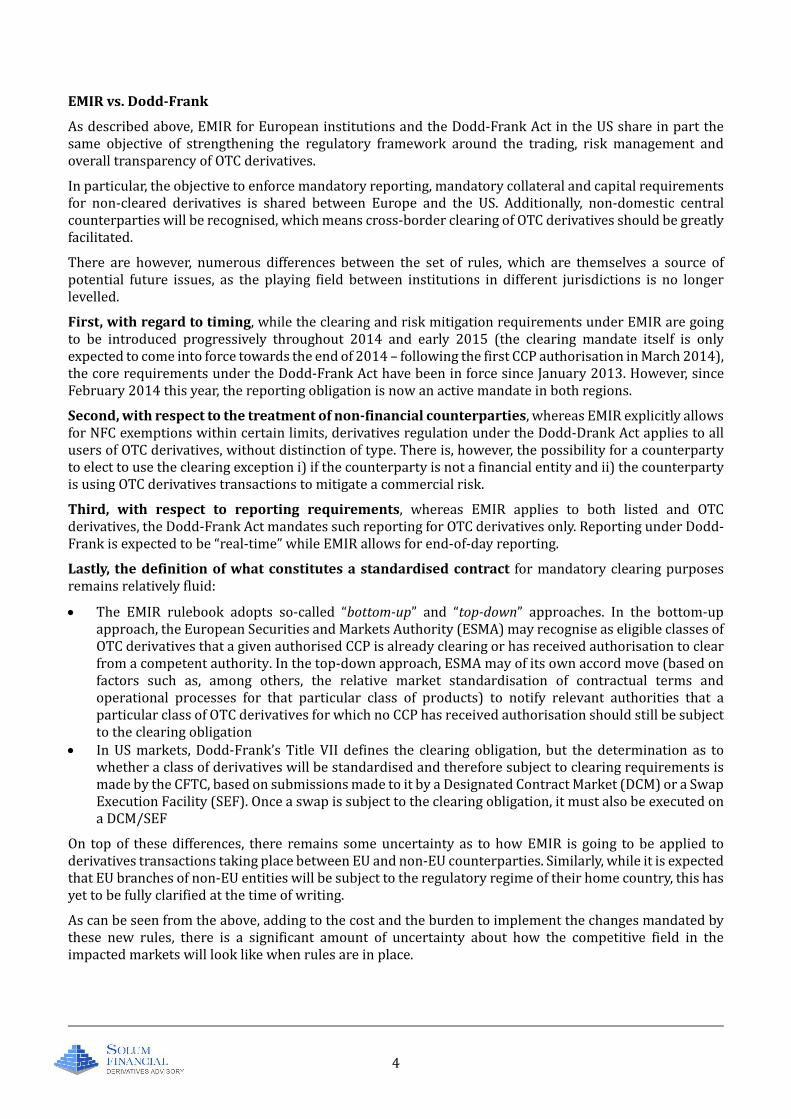

1.MandatoryclearingCounterpartydefinition

The European Market Infrastructure Regulation (“EMIR”) is the European Union regulatory initiativewhich covers clearing, risk mitigation and trade reporting. In Europe, under EMIR, derivativescounterpartieswillbeclassifiedinthreecategories:

Financial Counterparties (“FC”): FCs are defined as, among others investment firms, creditinstitutions,insuranceandreinsuranceundertakings,UCITSandalternativeinvestmentfunds

Non‐FinancialCounterparties(“NFC”) Non‐FinancialCounterpartiesthatareoveracertain“clearingthreshold”(“NFC+”):specifically,

anNFCbecomesaNFC+if,onanygivenday,theaggregategrossnotionalofoutstandingnon‐clearedOTCderivativestradesthatithasinanygivenassetclass(excluding“hedgingtransactions”)exceedstherelevantthreshold,definedasfollows:EUR1bnforeachofcreditandequityderivatives;EUR3bnfor each of interest rate and foreign exchange derivatives; EUR 3bn for commodity and otherderivativescollectively

EMIRalsodefinesawiderangeofso‐calledexemptentities(suchascentralbanksandbodiesperformingsimilarfunctions)whicharefullyexempt,whilemultilateralbanks,EFSF,ESMandpublicsectorentitieswithexplicitguaranteesareonlysubjecttothereportingrequirement.

EMIRrequirements

In line with the G‐20 mandated general principles discussed above, EMIR introduces three primaryregulatoryconstraintsonOTCderivativesforthefinancialinstitutionsitregulates:

MandatoryclearingofalleligibleOTCderivatives,whichappliestoFCsandNFC+onlyandwillbeinforcefromtheendof2014

InitialmarginrequirementsandimprovedriskmanagementmetricsforthoseOTCderivativesthatarenotcentrallycleared.TheseriskmitigationtechniquesincludesmeasuresapplicabletoFCsandNFC+only(suchasdailymarktomarketortheexchangeofcollateralandadequatecapitaltocover non‐cleared transactions) and measures applicable to FCs and all NFCs (such as timelyconfirmation,portfolioreconciliationandcompression,disputeresolution)

Obligationtoreportallderivativestransactionstotraderepositories,whichappliestoFCs,allNFCsandcertainexemptentities,asdescribedabove

*riskmitigation ex‐dailyvaluationandcollateralisationofnon‐clearedtransactions

Table1:EMIRrequirementsbytypeoftradeandtypeofcounterparty

4

EMIRvs.Dodd‐Frank

Asdescribedabove,EMIRforEuropeaninstitutionsandtheDodd‐FrankActintheUSshareinpartthesame objective of strengthening the regulatory framework around the trading, risk management andoveralltransparencyofOTCderivatives.

Inparticular,theobjectivetoenforcemandatoryreporting,mandatorycollateralandcapitalrequirementsfor non‐cleared derivatives is shared between Europe and the US. Additionally, non‐domestic centralcounterpartieswillberecognised,whichmeanscross‐borderclearingofOTCderivativesshouldbegreatlyfacilitated.

There are however, numerous differences between the set of rules, which are themselves a source ofpotential future issues, as the playing field between institutions in different jurisdictions is no longerlevelled.

First,withregardtotiming,whiletheclearingandriskmitigationrequirementsunderEMIRaregoingto be introduced progressively throughout 2014 and early 2015 (the clearing mandate itself is onlyexpectedtocomeintoforcetowardstheendof2014–followingthefirstCCPauthorisationinMarch2014),thecorerequirementsundertheDodd‐FrankActhavebeeninforcesinceJanuary2013.However,sinceFebruary2014thisyear,thereportingobligationisnowanactivemandateinbothregions.

Second,withrespecttothetreatmentofnon‐financialcounterparties,whereasEMIRexplicitlyallowsforNFCexemptionswithincertainlimits,derivativesregulationundertheDodd‐DrankActappliestoallusersofOTCderivatives,withoutdistinctionoftype.Thereis,however,thepossibilityforacounterpartytoelecttousetheclearingexceptioni)ifthecounterpartyisnotafinancialentityandii)thecounterpartyisusingOTCderivativestransactionstomitigateacommercialrisk.

Third, with respect to reporting requirements, whereas EMIR applies to both listed and OTCderivatives,theDodd‐FrankActmandatessuchreportingforOTCderivativesonly.ReportingunderDodd‐Frankisexpectedtobe“real‐time”whileEMIRallowsforend‐of‐dayreporting.

Lastly,thedefinitionofwhatconstitutesastandardisedcontract formandatoryclearingpurposesremainsrelativelyfluid:

The EMIR rulebook adopts so‐called “bottom‐up” and “top‐down” approaches. In the bottom‐upapproach,theEuropeanSecuritiesandMarketsAuthority(ESMA)mayrecogniseaseligibleclassesofOTCderivativesthatagivenauthorisedCCPisalreadyclearingorhasreceivedauthorisationtoclearfromacompetentauthority.Inthetop‐downapproach,ESMAmayofitsownaccordmove(basedonfactors such as, among others, the relative market standardisation of contractual terms andoperational processes for that particular class of products) to notify relevant authorities that aparticularclassofOTCderivativesforwhichnoCCPhasreceivedauthorisationshouldstillbesubjecttotheclearingobligation

InUSmarkets,Dodd‐Frank’sTitleVII defines the clearingobligation, but thedetermination as towhetheraclassofderivativeswillbestandardisedandthereforesubjecttoclearingrequirementsismadebytheCFTC,basedonsubmissionsmadetoitbyaDesignatedContractMarket(DCM)oraSwapExecutionFacility(SEF).Onceaswapissubjecttotheclearingobligation,itmustalsobeexecutedonaDCM/SEF

On topof thesedifferences, there remains someuncertainty as tohowEMIR is going tobe applied toderivativestransactionstakingplacebetweenEUandnon‐EUcounterparties.Similarly,whileitisexpectedthatEUbranchesofnon‐EUentitieswillbesubjecttotheregulatoryregimeoftheirhomecountry,thishasyettobefullyclarifiedatthetimeofwriting.

Ascanbeseenfromtheabove,addingtothecostandtheburdentoimplementthechangesmandatedbythese new rules, there is a significant amount of uncertainty about how the competitive field in theimpactedmarketswilllooklikewhenrulesareinplace.

5

2.CentralCounterparties(CCP)

Whiletheyhavebeenanimportantparticipantincapitalmarketsforalongtime,centralcounterparties(orCCPs)havetakenamuchmoreprominentroleatthecentreofOTCderivativesregulatoryreform,asthose OTCmarkets transition from oneswhere transactions used tomostly occur on a bilateral basisbetween financial institutions to an infrastructure where the clearing house plays an increasinglyimportantriskintermediationpart.

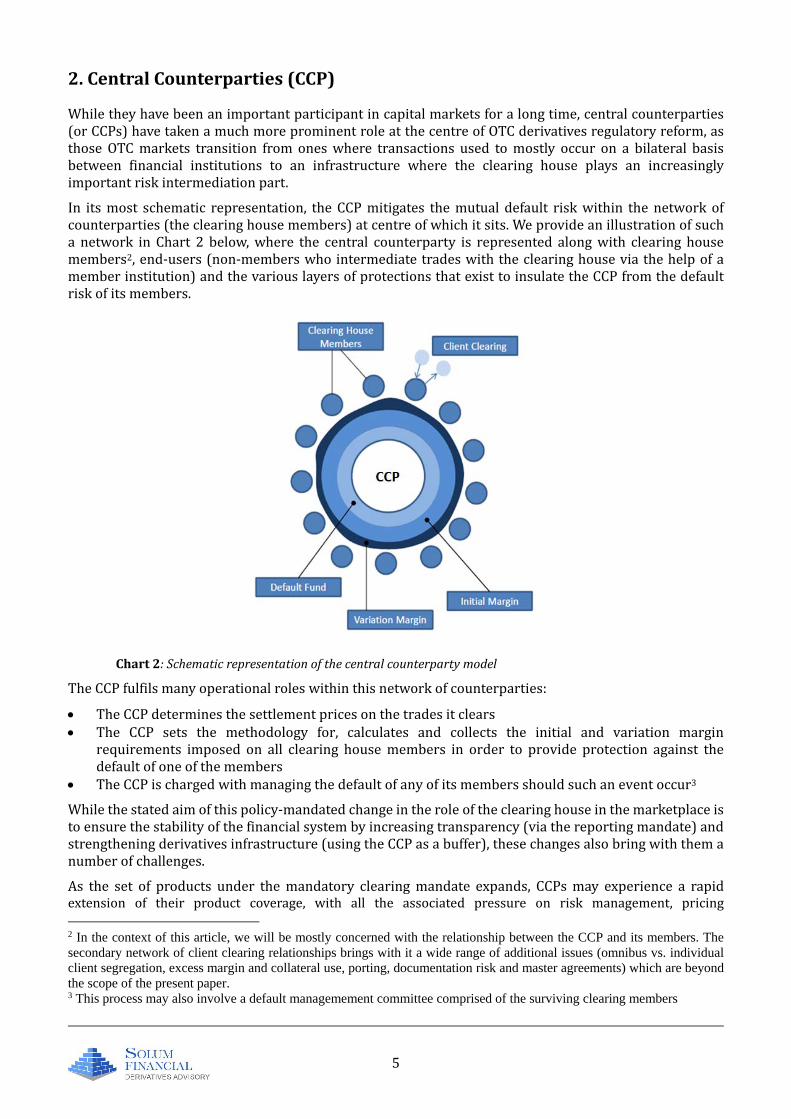

In itsmost schematic representation, theCCPmitigates themutual default riskwithin thenetworkofcounterparties(theclearinghousemembers)atcentreofwhichitsits.Weprovideanillustrationofsucha network in Chart 2 below,where the central counterparty is represented alongwith clearing housemembers2,end‐users(non‐memberswhointermediatetradeswiththeclearinghouseviathehelpofamemberinstitution)andthevariouslayersofprotectionsthatexisttoinsulatetheCCPfromthedefaultriskofitsmembers.

Chart2:Schematicrepresentationofthecentralcounterpartymodel

TheCCPfulfilsmanyoperationalroleswithinthisnetworkofcounterparties:

TheCCPdeterminesthesettlementpricesonthetradesitclears The CCP sets the methodology for, calculates and collects the initial and variation margin

requirements imposed on all clearing housemembers in order to provide protection against thedefaultofoneofthemembers

TheCCPischargedwithmanagingthedefaultofanyofitsmembersshouldsuchaneventoccur3

Whilethestatedaimofthispolicy‐mandatedchangeintheroleoftheclearinghouseinthemarketplaceistoensurethestabilityofthefinancialsystembyincreasingtransparency(viathereportingmandate)andstrengtheningderivativesinfrastructure(usingtheCCPasabuffer),thesechangesalsobringwiththemanumberofchallenges.

As the set of products under themandatory clearingmandate expands, CCPsmay experience a rapidextension of their product coverage, with all the associated pressure on risk management, pricing 2 In the context of this article, we will be mostly concerned with the relationship between the CCP and its members. The secondary network of client clearing relationships brings with it a wide range of additional issues (omnibus vs. individual client segregation, excess margin and collateral use, porting, documentation risk and master agreements) which are beyond the scope of the present paper. 3 This process may also involve a default managemement committee comprised of the surviving clearing members

6

methodologies,modelvalidation,defaultmanagement–especiallyinlightofthefactthatasthecentralarbiterofpricewithinthesystem,theCCPwillneedtocreateaconsensusonpricingandmarginsettingmethodologiesacceptabletoallitsmembers.

Further, as the recipient and custodian of very significant amounts of collateral under its own marginingprocedures,theCCPwillneedtomanagethesometimesconflictingobjectivesofitscommercialmission(whichwillleadittoseekreturnsonthecashpostedtoit)andtheprudentriskmanagementpracticesrequiredbyitsnewlyenhancedroleasproviderofamarketinfrastructurethatmitigatessystematicrisk.

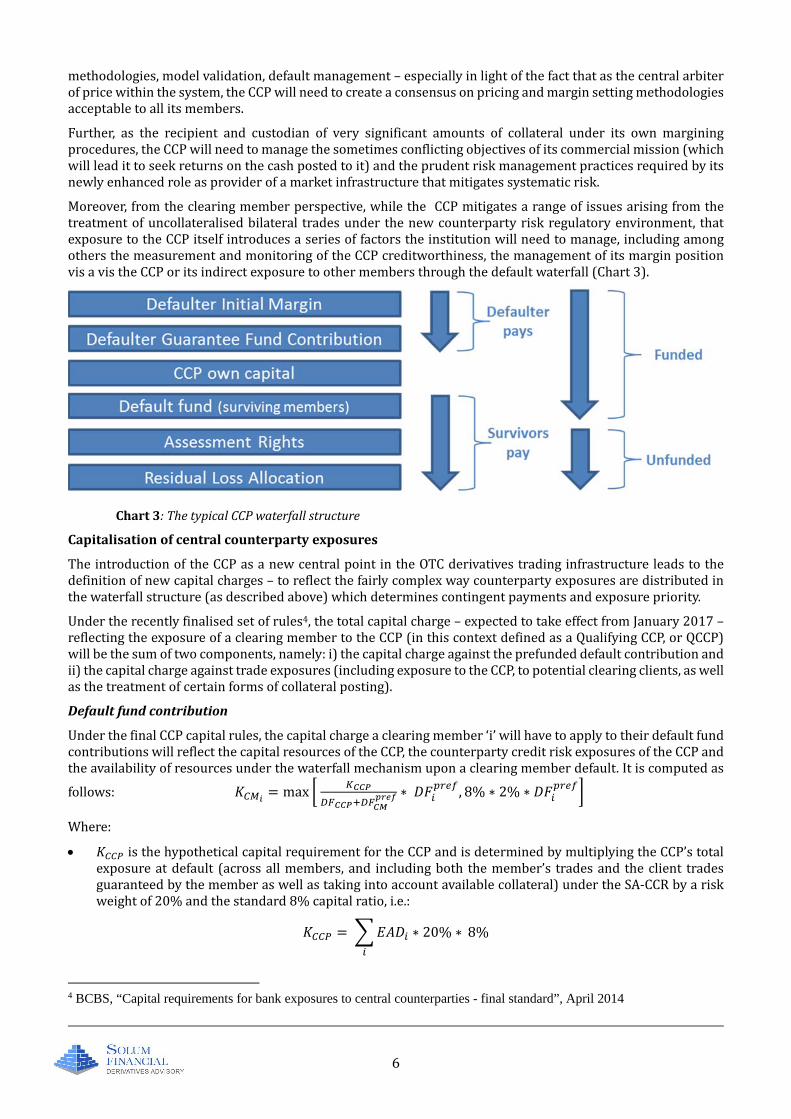

Moreover,fromtheclearingmemberperspective,whiletheCCPmitigatesarangeofissuesarisingfromthetreatmentofuncollateralisedbilateral tradesunder thenewcounterpartyriskregulatoryenvironment, thatexposuretotheCCPitselfintroducesaseriesoffactorstheinstitutionwillneedtomanage,includingamongothersthemeasurementandmonitoringoftheCCPcreditworthiness,themanagementofitsmarginpositionvisavistheCCPoritsindirectexposuretoothermembersthroughthedefaultwaterfall(Chart3).

Chart3:ThetypicalCCPwaterfallstructure

Capitalisationofcentralcounterpartyexposures

TheintroductionoftheCCPasanewcentralpointintheOTCderivativestradinginfrastructureleadstothedefinitionofnewcapitalcharges–toreflectthefairlycomplexwaycounterpartyexposuresaredistributedinthewaterfallstructure(asdescribedabove)whichdeterminescontingentpaymentsandexposurepriority.

Undertherecentlyfinalisedsetofrules4,thetotalcapitalcharge–expectedtotakeeffectfromJanuary2017–reflectingtheexposureofaclearingmembertotheCCP(inthiscontextdefinedasaQualifyingCCP,orQCCP)willbethesumoftwocomponents,namely:i)thecapitalchargeagainsttheprefundeddefaultcontributionandii)thecapitalchargeagainsttradeexposures(includingexposuretotheCCP,topotentialclearingclients,aswellasthetreatmentofcertainformsofcollateralposting).

Defaultfundcontribution

UnderthefinalCCPcapitalrules,thecapitalchargeaclearingmember‘i’willhavetoapplytotheirdefaultfundcontributionswillreflectthecapitalresourcesoftheCCP,thecounterpartycreditriskexposuresoftheCCPandtheavailabilityofresourcesunderthewaterfallmechanismuponaclearingmemberdefault.Itiscomputedas

follows: max ∗ , 8% ∗ 2% ∗

Where:

isthehypotheticalcapitalrequirementfortheCCPandisdeterminedbymultiplyingtheCCP’stotalexposureatdefault (acrossallmembers,and includingboth themember’s tradesand theclient tradesguaranteedbythememberaswellastakingintoaccountavailablecollateral)undertheSA‐CCRbyariskweightof20%andthestandard8%capitalratio,i.e.:

∗ 20% ∗ 8%

4 BCBS, “Capital requirements for bank exposures to central counterparties - final standard”, April 2014

7

isthecapitalrequirementonthedefaultfundcontributionofmember‘i’

and are the prefunded default fund contribution of the member ‘i’ and the totalprefundeddefaultfundcontributionsofallmembers,respectively

isthetotalCCP’sowncontribution,totheextentthatthisowncontributiontothewaterfalliseitherjuniortoorparipassuwithprefundedmembercontributions

Together,the and termsrepresentthetotalprefundedsizeofthedefaultfund.TotheextentthatthisprefundedamountislargecomparedtothehypotheticalcapitalrequirementoftheCCP(i.e.thedefaultfundislargerthanthehypothetical ),thefactorthatmultiplies willbesmallandthecapitalchargearisingfromagivenclearingmember’sdefaultcontributionmaybealimitedpercentageofthesizeofsuchcontribution–albeitflooredattheequivalentofa2%riskweight.

Such a mechanism should theoretically ensure adequate incentives for clearing members to ensuresufficientparticipationofaCCPintheguaranteefundbycontributinglargeramountsofownresources,inordertokeepthecapitalcostofitsowncontributionlow.

Tradeexposures

Thefinalcapitalruleshaveseenpolicymakersreturntotheflatcapitalisationatthe2%RWlevelforalltradeexposuresfromaclearingmembertotheCCPthatarisefromOTCderivatives(i.e.acombinationofi)currentexposuretotheCCP–likelyasmallintra‐dayamount,ii)potentialfutureexposuretotheCCPandiii)anyamountofinitialmarginthatisnotbankruptcy‐remote,withbankruptcy‐remoteIMsuchasthatpostedinae.g.segregatedaccountattractinga0%riskweight).

Themember’sexposuretotheCCParisingfromthemember’sobligationtorepayaclearingclientforanylossesintransactionvaluesuponaCCPeventofdefaultwillalsobefacingariskweightof2%.

Comparedwithpreviousiterationsofthisrulehowever,theexposureamountforsuchtradesexposures(mostlythroughthepotentialfutureexposurecomponent)willbecomputedaccordingtointernalmodelmethodsifthebankisapprovedforcentrallyclearedproducts,orthroughthenewstandardisedmethodrecentlysetforthbytheBaselCommittee5(theSA‐CCR).

5 BCBS, “The standardised approach for measuring counterparty credit risk exposures”, March 2014

8

3.Non‐clearedDerivatives

Introductionofthe2‐waymarginmodelinbilateralOTCderivativestrading

Whilethemovetowardscentralclearingforawiderangeofso‐calledstandardisedOTCderivativeshassofarbeenthemostvisiblechangefromregulatoryinitiativesandtheonethathaspreoccupiedfinancialinstitutionsthemost,apossiblyevenlargerchangeloomsinthenon‐clearedsegmentsofderivativesmarkets,asregulatorsseektoaligntradingandriskmanagementbehaviourinexoticandnon‐clearedsegmentstothatofstandardisedandcentrallyclearedderivativesproducts.

After a couple of consultation rounds, the Basel Committee (BCBS) and the International Organisation ofSecurities Commissions (IOSCO) has proposed a series of measures in its final policy paper published inSeptemberlastyear6,withrespecttothemarginrequirementsfornon‐centrallyclearedderivatives.

Thekeycentralmeasureintroducedbythedocumentistheintroductionoftwo‐waymarginforallnon‐clearedderivatives (with theexceptionofa limitednumberofproducts, suchasphysicallysettledFX forwardsandswaps, or the FX component in cross‐currency swaps), including, like in the centrally cleared / CCPinfrastructuremodel:

Variationmargin(i.e.collateralasprotectionagainstthebuild‐upofexposuretoacounterparty) Initial margin (i.e. initial overcollateralisation to cover for variation margin shortfalls in case the

counterpartydefaults)

Exemptions

A€50mthreshold,appliedonaportfolioandconsolidatedgroupcounterpartybasis,hasbeendefinedunderwhichIMisnotmandatory.Moregenerally,institutionsthathavelessthan€8bnoftotalnon‐centrallyclearedOTCderivatives(i.e.grossnotionaloutstanding)willbeexemptfromtheinitialmarginingrules.

Inlinewiththeirexemptionsfromclearingrequirementsandbasedonthestatedprinciplethatsuchentitiesposelittletonosystematicrisk,sovereigns,centralbanksandmulti‐lateraldevelopmentbanksareexemptedfrom both collection and posting of collateral. Likewise, non‐financials entities which are deemed nonsystematically important are not covered by the unclearedOTC rules, to the extent that they are generallyexemptfromcentralclearingmandates.

Preservingcollateraltransparency,liquidityandaccessibility

Moreover,drawinglessonsfromthecollateraltroublesexperiencedbythefinancialsystemimmediatelyaftertheLehmanBrothersbankruptcy,policymakershaveagreedtoanoverhaulofcollateralruleswhichisexplicitlyintendedtoensurethatcollateralpostedtoandbyfinancialinstitutionsis“(i)accessiblewhenneededand(ii)providedinaformthatcanbeliquidatedrapidlyandatapredictablepriceeveninatimeoffinancialstress”.Thisis in turn achieved throughmaterially strengthened collateral rules, both in terms of eligibility and of therestrictedabilityoffinancialinstitutionstorehypothecatethecollateralpostedbyandtothemaspartofthemarginingprocess.

The first part of this mandate (accessibility of collateral) is addressed through a vastly restrictedrehypothecationofcollateral,sothatinaneventofdefault,initialmarginmaybeimmediatelyidentifiedandusedagainsttheshortfallsinthepositionsofthedefaultedcounterparty.Twelveconditionsgoverntheabilityforafinancialinstitutiontore‐usethecollateralpledgedtoitbyacustomer,including,amongothers:expressclientconsent,clientnotification,third‐partyassetsegregation,nofourth‐partyrehypothecationfurtherdownthechainanddisclosuretoauthorities,amongothers).Variationmarginontheotherhandmaybere‐pledged.

Withrespecttothesecondpartofthisdualobjective(preservingliquidityandoptimalrealisationofcollateralintimesofhighstress),policymakershaverecommendedthat,withroomleftopenfortheidiosyncraciesofcertain localmarkets,nationalsupervisorsshouldstrictly limit thetypeofcollateraleligible to fulfilmarginrequirementstoliquidandhighqualityinstruments,withtheappropriatehaircutstotakeintoaccountrate,FXorcreditrisk.

Timeline

Asitcurrentlystands,regulatorshavedecidedtophaseinthosenewnon‐clearedderivativesrequirements

6 BCBS, “Margin requirements for non-centrally cleared derivatives”, September 2013

9

throughout2015‐2019,withmandatoryvariationmarginapplyingtoallnewcontractsfromDecember2015onwards,whileinitialmarginistobeintroducedinstaggeredmannerthroughout2015‐2019,startingwiththecounterpartieswith thehighestnotionalof such tradesoutstanding, andmoving towards including smallerentitestowardsthebackendofthisperiod.Allchangeswillbesubjecttoongoingmonitoring,withpossibilitythattherulesmaybefurtherrefinedalongtheway.

Regulatoryconsistency,marketconsensusoninternalmodelsandotherchallenges

ThesesweepingchangesinthewayfinancialinstitutionsareexpectedtoconducttheirmostsophisticatedOTCderivativesbusinessesposenumerousissues:

The consistency of the margining rules with other regulatory requirements is expected to be a keychallenge.Thecombinationofmargining rulesand the liquiditycoverage ratio forexample is likely tocompoundthecollateralpressure

Thealignmentofinitialmarginmeasurementbetweeninstitutionswithsometimesverydifferentmodelsandapproachesmayprovetobeproblematic.Giventhefall‐backoptionofrelyingonthefairlyunattractivestandardised formula (a percentage of total notional) is likely to be too punitive for many marketparticipants, industry solutions will need to be found to harmonise internal models for IM purposes.IndustryinitiativessuchasISDA’sStandardInitialMarginModel7(SIMM)willbeafirststepinresolvingthiscrucialissue

Inthesamevein,theindustryandrespectiveregulatorswillhavetoaddressthetreatmentofcrossborderdiscrepancies, whereby for instance intra‐group internal models have to undergo different approvalprocessesdependingonthejurisdictioninwhichthetradesorthebusinessaretakingplace

The procyclicality of the new rules is another important issue; while transparency and promptmonetisationofcollateralareusefultoolsupontherealisationofacreditevent,itcanbearguedthatthenew requirementsmay increase collateral pressure ahead of such event (and therefore accelerate itsoccurrence)

7 ISDA, “Standard Initial Margin Model for Non-Cleared Derivatives”, December 2013

10

Conclusion

Theintroductionofmandatoryclearingforawiderangeofderivativesproducts,andtheassociatedriseofthecentralcounterpartymodelasamainintermediaryofbusinessinthesemarketsisthesourceofpotentialnewrisksthatmarketparticipantswillneedtoassessandmonitor.

Additionally,thelargecollateralrequirementsarisingfromthecompulsoryriskmitigationmeasuresfornon‐clearedOTCderivativeswillmeanthemanagementofcollateral,andtheoptimisationofitsuse,arelikelytobeprimaryconcernsoffinancialinstitutionsinthenearfuture.

Asboththerangeofstandardisedproductsandtheclearinghouseproductofferingexpand,themovetowardscentralclearingwillcontinuetogaintraction,allowingmultipletransactionswithvariouscounterpartiestobeconsolidatedintoasinglecounterparty(allowingmulti‐lateralnetting),withitsassociatedmargin,capitalandoperationalrelief.

Formoreexotic,lessliquidandbespokeproducts,themarketwilllikelycontinuetooperateonanon‐clearedbasis,astheriskmanagementandoperationaltreatmentofsuchinstrumentsdonotmatchthestandardisationrequirementsofthecentralclearingmodel.

Such drastic changes – across both vanilla and complex products – will have a large range of businessconsequencesthatwillneedtobeaddressedwellaheadoffinalimplementationdeadlines,mainlyaroundthefollowingissues:

Capital, liquidity, credit risk and – as a result of the tradeoff between reduced CCR requirements andincreasedfundingrequirements–collateralmanagementandoptimisation

Processes,systemsandmodelsespeciallywithrespecttotheriskmanagementofnon‐clearedbusiness Datamanagementandtradereporting

When viewed through the lens of the additional costs they introduce for financial institutions (not onlyoperationalcosts,butalsorealonesviathecapitalandcollateralimpactonthelargerinstitution),thenewOTCderivativesrulebookisboundtobeaveryimportantdriveroffurtherconsolidationofbusinessesinthelongerrun: larger, sophisticatedbankswill seek torationalise theirpresence(compressionandnovationof trades,strongadherencetohighercapitalhurdlesfornewbusiness)whileinstitutionswithlimitedmarketshareandrevenueswillneedtoinvestigatewhethertocontinuecompetinginthisareaaltogether.

The endgame, aswas likely the intent of the policymakers, is likely to be a smaller, leanerOTCderivativesmarketplace–butalsoasignificantlymoreconcentratedoneassmallerentitiesdropout,andtheimportanceoftheCCPrises.

11

ContactusSolumFinancial12AustinFriarsCityofLondonEC2N2HEUnitedKingdom+442077869230research@solum‐financial.com

SolumFinancialLimitedisauthorisedandregulatedbytheFinancialConductAuthority

NicolasGakwayaSeniorConsultantnicolas.gakwaya@solum‐financial.com+442077869234JonGregoryPartnerjon@solum‐financial.com+442077869233TeimurazBarbakadzeSeniorConsultantteimuraz@solum‐financial.com+442077869242Thu‐UyenNguyenPartnertu@solum‐financial.com+442077869231VincentDahindenCEOvincent@solum‐financial.com+442077869235

12

SolumDisclaimerThispaperisprovidedforyourinformationonlyanddoesnotconstitutelegal,tax,accountancyorregulatoryadviceoradviceinrelationtothepurposeofbuyingorsellingsecuritiesorotherfinancialinstruments.Norepresentation,warranty,responsibilityorliability,expressofimplied,ismadetooracceptedbyusoranyofourprincipals,officers,contractorsoragentsinrelationtotheaccuracy,appropriatenessorcompletenessofthispaper.All informationandopinions contained in thispaperare subject to changewithoutnotice, andwehavenoresponsibilitytoupdatethispaperafterthedatehereof.Thisreportmaynotbereproducedorcirculatedwithoutourpriorwrittenauthority.