Embed Size (px)

Citation preview

Reinsurance Extracting Value from Reinsurance Analytics

Steve Mathews FIA CERA

Batuhan Avci

November 2013

© 2013 Towers Watson. All rights reserved.

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Agenda

Motivation

Reinsurance considerations

Case study

Next steps

© 2013 Towers Watson. All rights reserved.

towerswatson.com

1

Motivation

© 2013 Towers Watson. All rights reserved.

Proprietary and Confidential. For Towers Watson and Towers Watson client use only. © 2013 Towers Watson. All rights reserved.

towerswatson.com

3

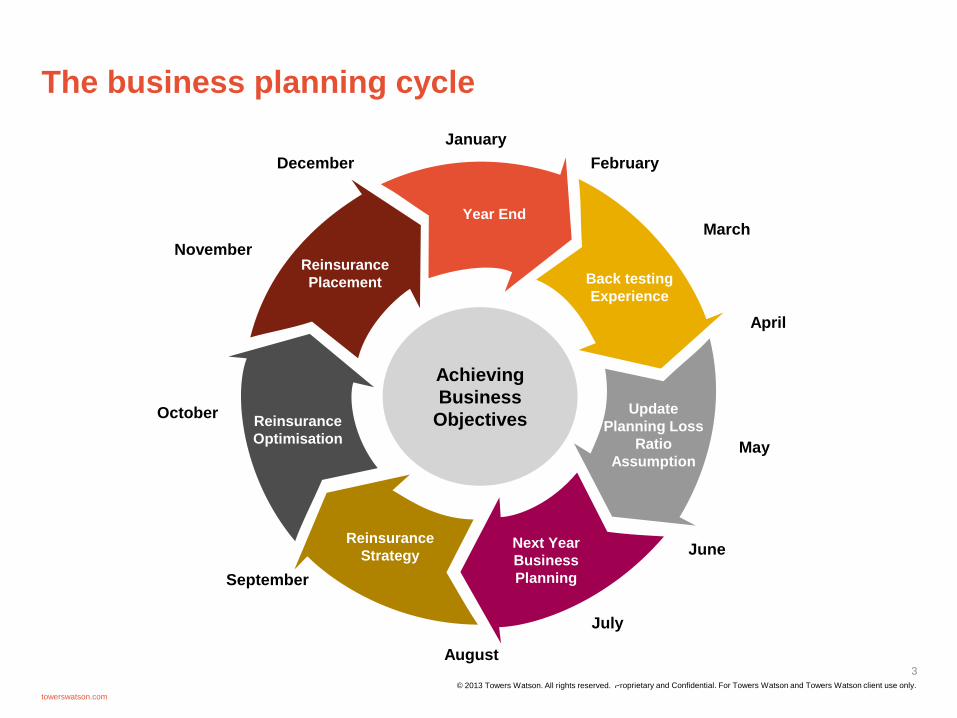

The business planning cycle

Year End

Back testing

Experience

Update

Planning Loss

Ratio

Assumption

Next Year

Business

Planning

Reinsurance

Strategy

Reinsurance

Optimisation

Reinsurance

Placement

January

February

March

April

May

June

July

August

September

October

December

Achieving

Business

Objectives

November

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Why buy reinsurance?

© 2013 Towers Watson. All rights reserved.

towerswatson.com

4

Supplements capital

Provides capacity

Reduces risk exposure

Smooths results

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

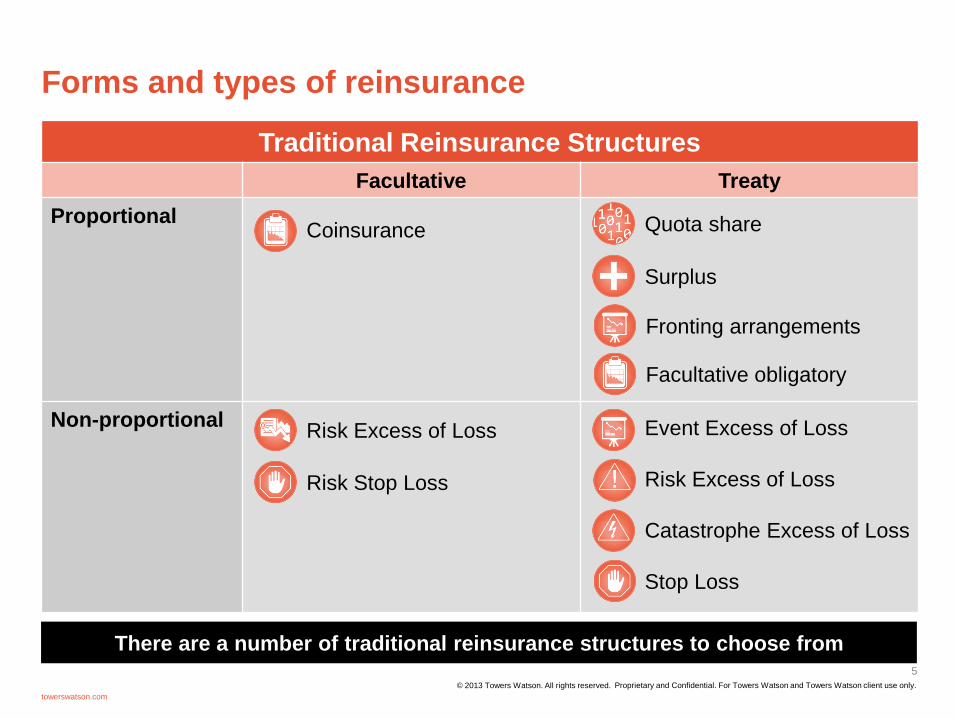

Forms and types of reinsurance

Traditional Reinsurance Structures

Facultative Treaty

Proportional

Non-proportional

There are a number of traditional reinsurance structures to choose from

© 2013 Towers Watson. All rights reserved.

towerswatson.com

5

Risk Excess of Loss

Risk Stop Loss

Stop Loss

Catastrophe Excess of Loss

Risk Excess of Loss

Event Excess of Loss

Facultative obligatory

Surplus

Quota share Coinsurance

Fronting arrangements

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

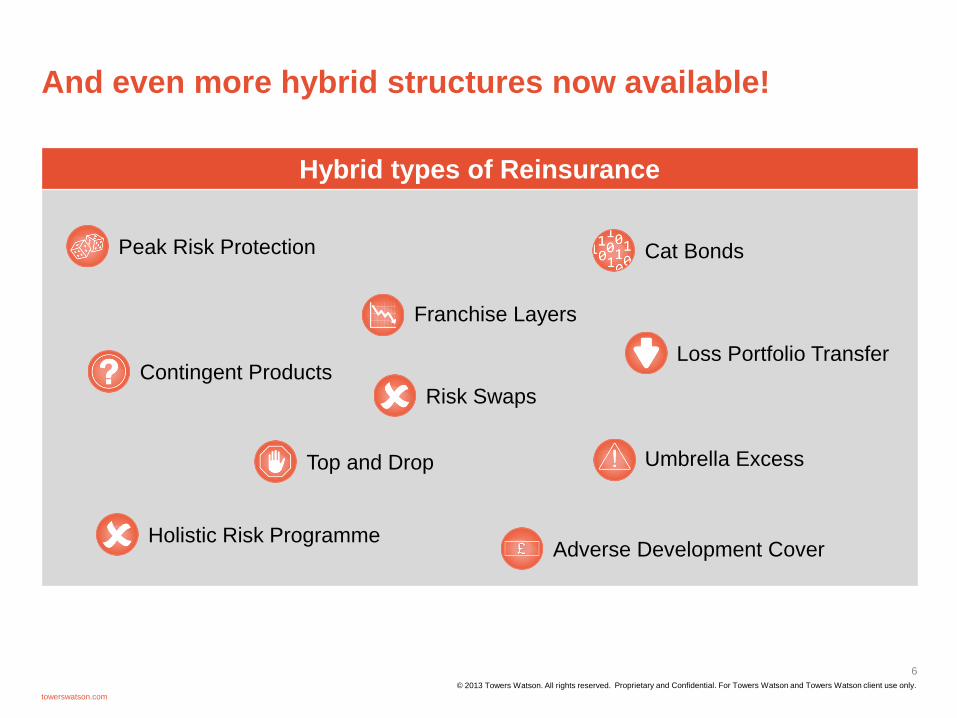

And even more hybrid structures now available!

Hybrid types of Reinsurance

© 2013 Towers Watson. All rights reserved.

towerswatson.com

6

Adverse Development Cover

Contingent Products

Holistic Risk Programme

Franchise Layers

Loss Portfolio Transfer

Peak Risk Protection Cat Bonds

Umbrella Excess Top and Drop

Risk Swaps

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Reinsurance in Turkey

There has been a constant small use of excess of loss covers over the last few years

The high use of quota share and surplus treaty reinsurance seen throughout the Turkish

insurance market is an unusual feature by international standards

The prevalence of earthquake risk in Turkey can lead to a competitive disadvantage

amongst insurers with proportional arrangements compared to those with only non-

proportional

Regulations around reinsurance in Turkey are not particularly stringent

Insurers potentially have significant flexibility in exploring various reinsurance structures to meet

their various business objectives

And in the news…

A.M. Best recently downgraded the financial strength rating of Milli Reasurans Turk Anonim Sirketi.

Subsequently, a reduction in the annual premium income by the reinsurer has been observed.

The successful issuance of the catastrophe bond Bosphorus Re Ltd has demonstrated a significant

appetite in the capital markets for a diversifying opportunity

© 2013 Towers Watson. All rights reserved.

towerswatson.com

7

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

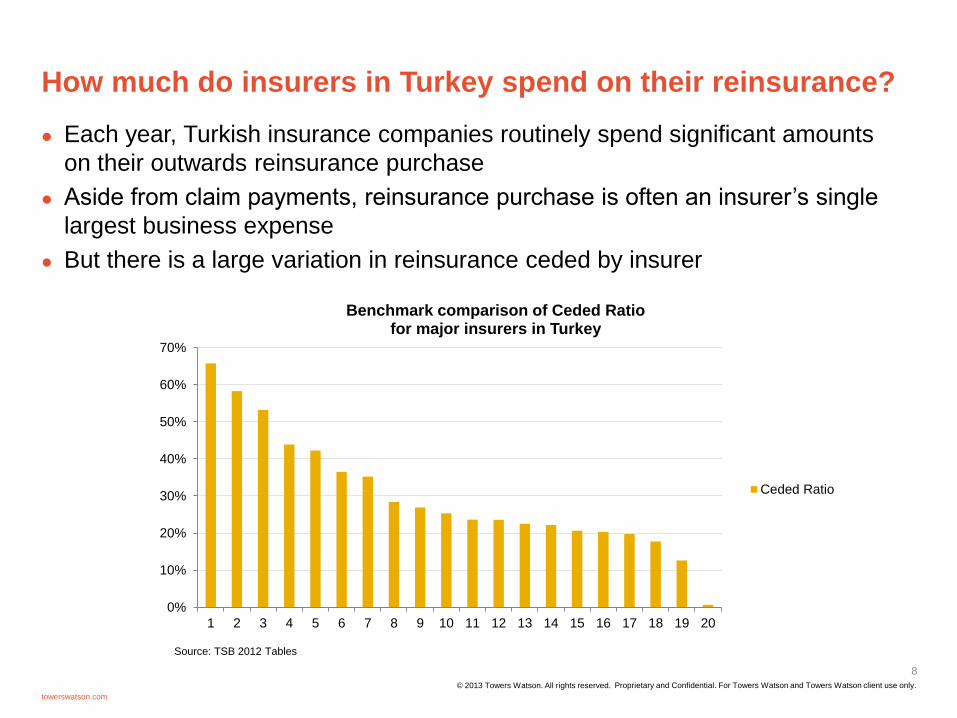

How much do insurers in Turkey spend on their reinsurance?

Each year, Turkish insurance companies routinely spend significant amounts

on their outwards reinsurance purchase

Aside from claim payments, reinsurance purchase is often an insurer’s single

largest business expense

But there is a large variation in reinsurance ceded by insurer

Source: TSB 2012 Tables

© 2013 Towers Watson. All rights reserved.

towerswatson.com

8

0%

10%

20%

30%

40%

50%

60%

70%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

Benchmark comparison of Ceded Ratio for major insurers in Turkey

Ceded Ratio

Reinsurance considerations

© 2013 Towers Watson. All rights reserved.

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

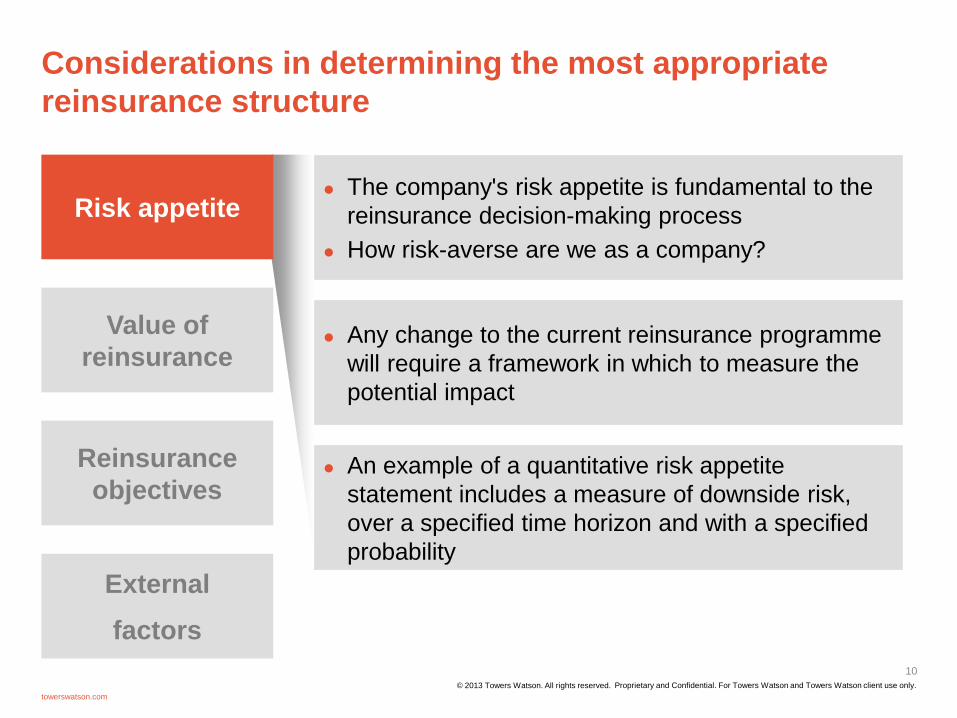

The company's risk appetite is fundamental to the

reinsurance decision-making process

How risk-averse are we as a company?

Any change to the current reinsurance programme

will require a framework in which to measure the

potential impact

An example of a quantitative risk appetite

statement includes a measure of downside risk,

over a specified time horizon and with a specified

probability

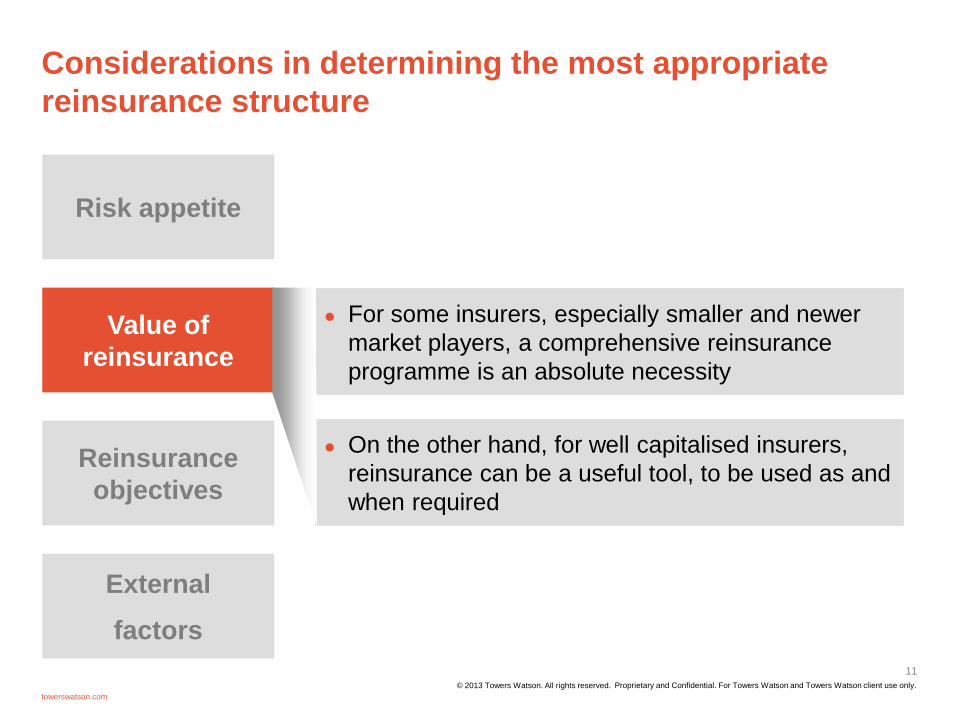

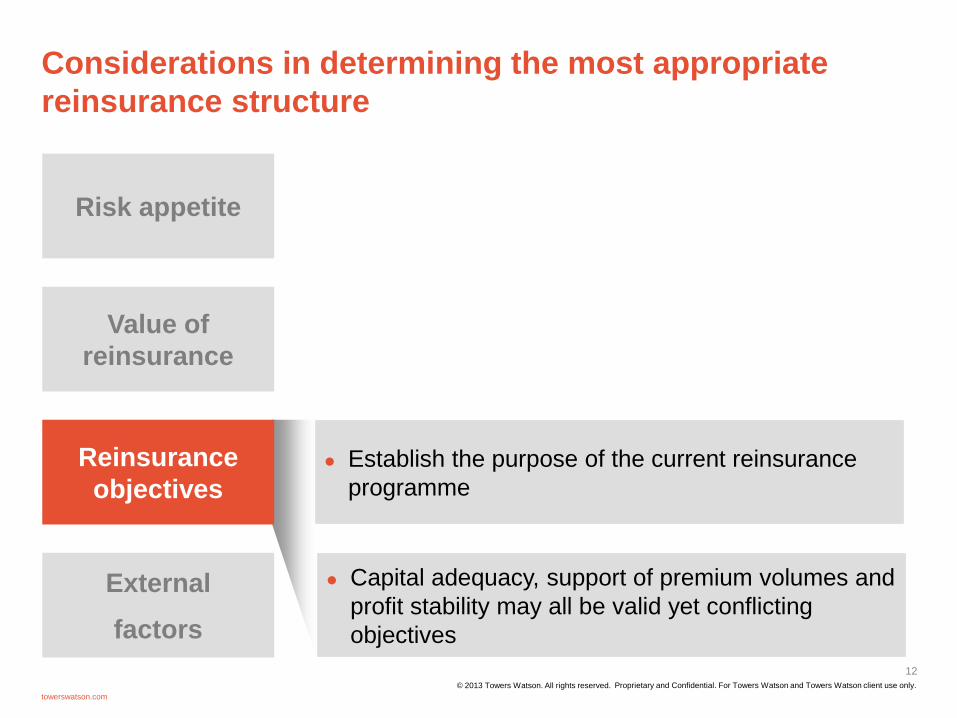

Risk appetite

Value of

reinsurance

Reinsurance

objectives

External

factors

© 2013 Towers Watson. All rights reserved.

towerswatson.com

10

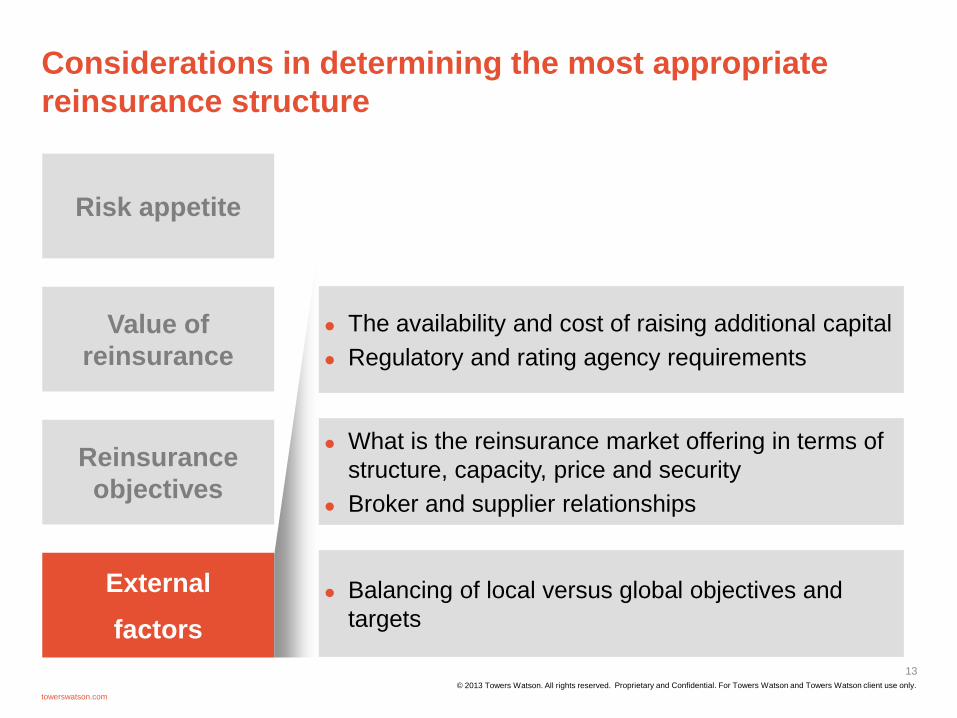

Considerations in determining the most appropriate

reinsurance structure

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Considerations in determining the most appropriate

reinsurance structure

Risk appetite

Value of

reinsurance

Reinsurance

objectives

External

factors

For some insurers, especially smaller and newer

market players, a comprehensive reinsurance

programme is an absolute necessity

On the other hand, for well capitalised insurers,

reinsurance can be a useful tool, to be used as and

when required

© 2013 Towers Watson. All rights reserved.

towerswatson.com

11

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Risk appetite

Value of

reinsurance

Reinsurance

objectives

External

factors

Establish the purpose of the current reinsurance

programme

Capital adequacy, support of premium volumes and

profit stability may all be valid yet conflicting

objectives

© 2013 Towers Watson. All rights reserved.

towerswatson.com

12

Considerations in determining the most appropriate

reinsurance structure

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Risk appetite

Value of

reinsurance

Reinsurance

objectives

External

factors

The availability and cost of raising additional capital

Regulatory and rating agency requirements

What is the reinsurance market offering in terms of

structure, capacity, price and security

Broker and supplier relationships

Balancing of local versus global objectives and

targets

© 2013 Towers Watson. All rights reserved.

towerswatson.com

13

Considerations in determining the most appropriate

reinsurance structure

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

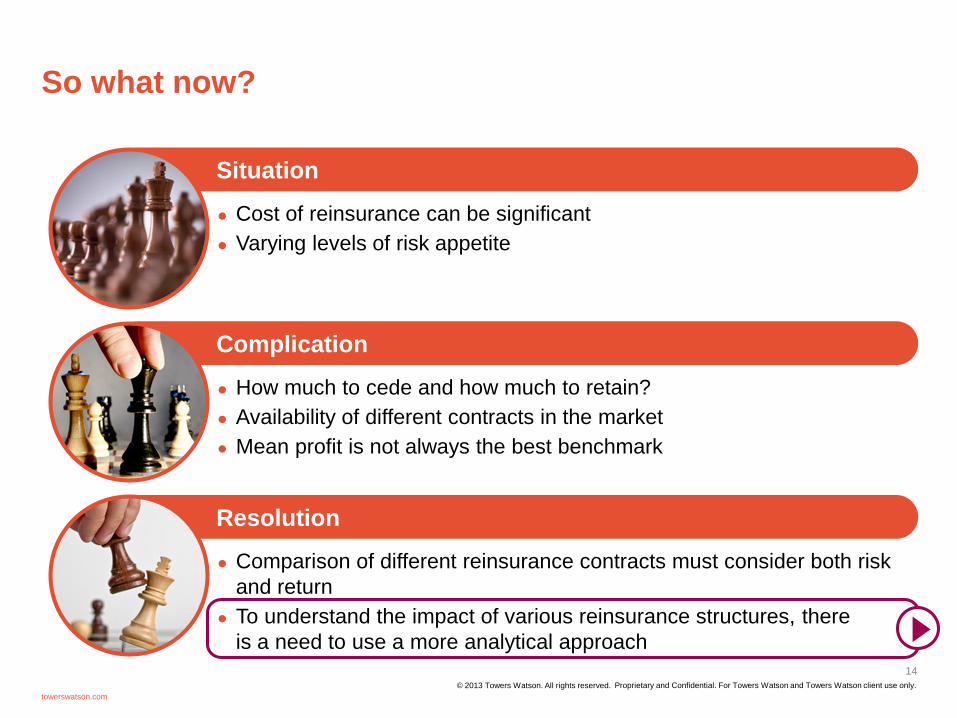

So what now?

© 2013 Towers Watson. All rights reserved.

towerswatson.com

14

Situation

Cost of reinsurance can be significant

Varying levels of risk appetite

Complication

How much to cede and how much to retain?

Availability of different contracts in the market

Mean profit is not always the best benchmark

Resolution

Comparison of different reinsurance contracts must consider both risk

and return

To understand the impact of various reinsurance structures, there

is a need to use a more analytical approach

Case study

© 2013 Towers Watson. All rights reserved.

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

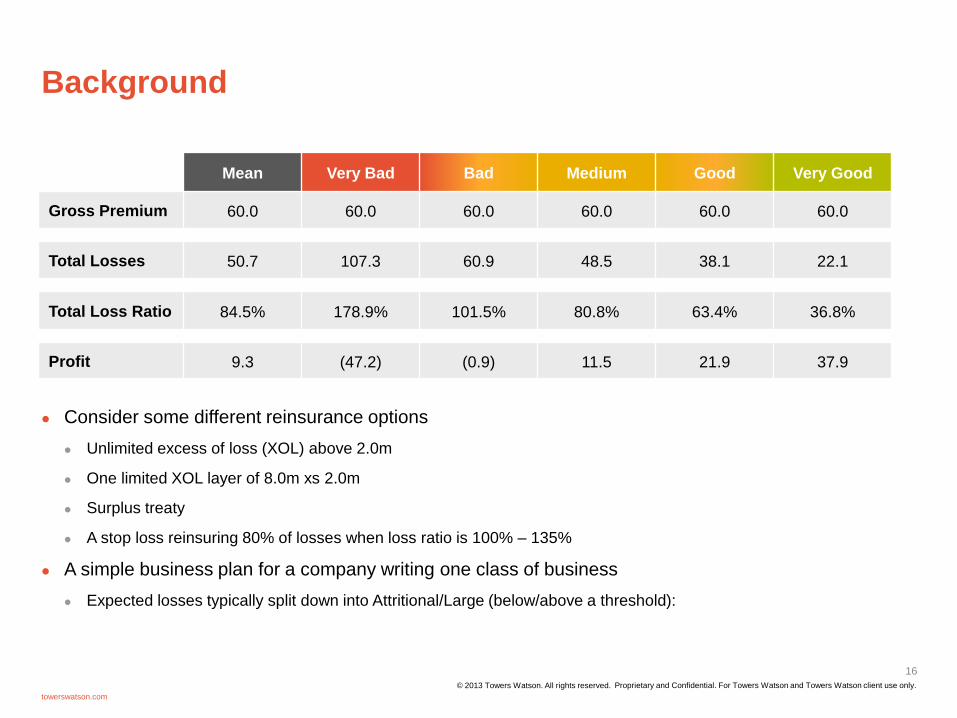

Background

Consider some different reinsurance options

Unlimited excess of loss (XOL) above 2.0m

One limited XOL layer of 8.0m xs 2.0m

Surplus treaty

A stop loss reinsuring 80% of losses when loss ratio is 100% – 135%

A simple business plan for a company writing one class of business

Expected losses typically split down into Attritional/Large (below/above a threshold):

© 2013 Towers Watson. All rights reserved.

towerswatson.com

16

Mean Very Bad Bad Medium Good Very Good

Gross Premium 60.0 60.0 60.0 60.0 60.0 60.0

Total Losses 50.7 107.3 60.9 48.5 38.1 22.1

Total Loss Ratio 84.5% 178.9% 101.5% 80.8% 63.4% 36.8%

Profit 9.3 (47.2) (0.9) 11.5 21.9 37.9

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

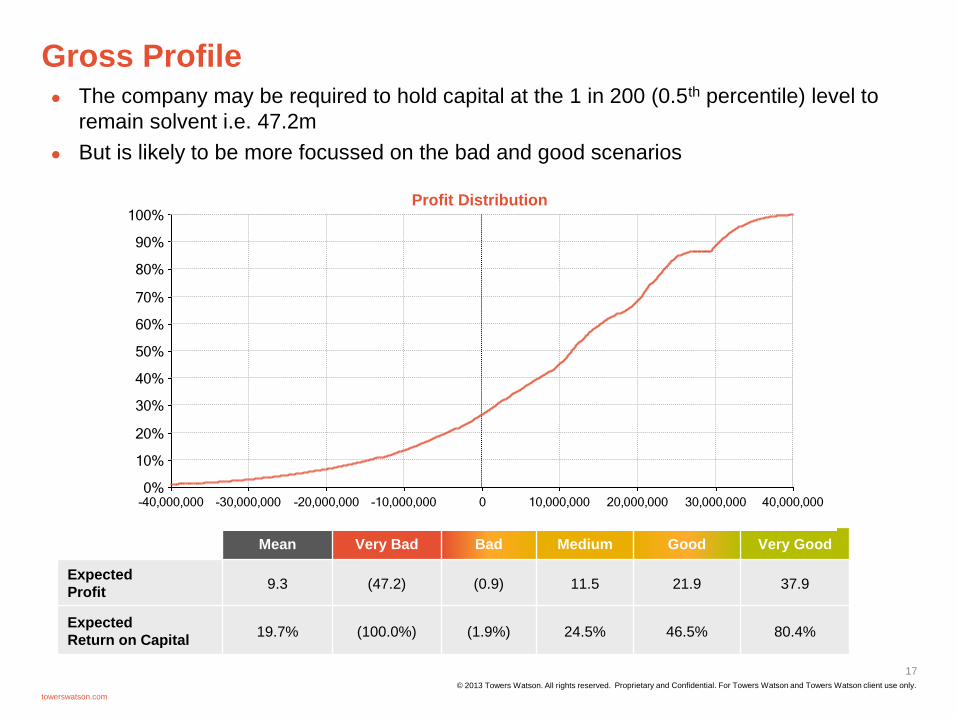

Gross Profile

© 2013 Towers Watson. All rights reserved.

towerswatson.com

17

The company may be required to hold capital at the 1 in 200 (0.5th percentile) level to

remain solvent i.e. 47.2m

But is likely to be more focussed on the bad and good scenarios

Mean Very Bad Bad Medium Good Very Good

Expected

Profit 9.3 (47.2) (0.9) 11.5 21.9 37.9

Expected

Return on Capital 19.7% (100.0%) (1.9%) 24.5% 46.5% 80.4%

Profit Distribution_Gross

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

-40,000,000 -30,000,000 -20,000,000 -10,000,000 0 10,000,000 20,000,000 30,000,000 40,000,000

Value

Pe

rce

nti

le

Profit Distribution

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

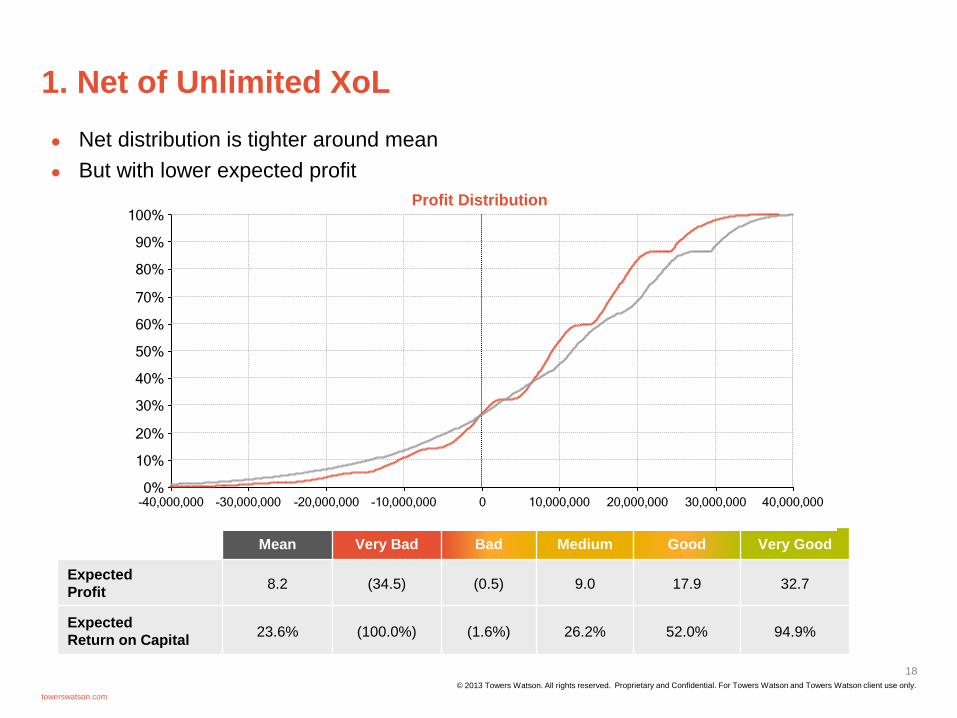

1. Net of Unlimited XoL

© 2013 Towers Watson. All rights reserved.

towerswatson.com

18

Net distribution is tighter around mean

But with lower expected profit

Mean Very Bad Bad Medium Good Very Good

Expected

Profit 8.2 (34.5) (0.5) 9.0 17.9 32.7

Expected

Return on Capital 23.6% (100.0%) (1.6%) 26.2% 52.0% 94.9%

Profit Distribution_Unlimited

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

-40,000,000 -30,000,000 -20,000,000 -10,000,000 0 10,000,000 20,000,000 30,000,000 40,000,000

Value

Pe

rce

nti

le

Profit Distribution

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

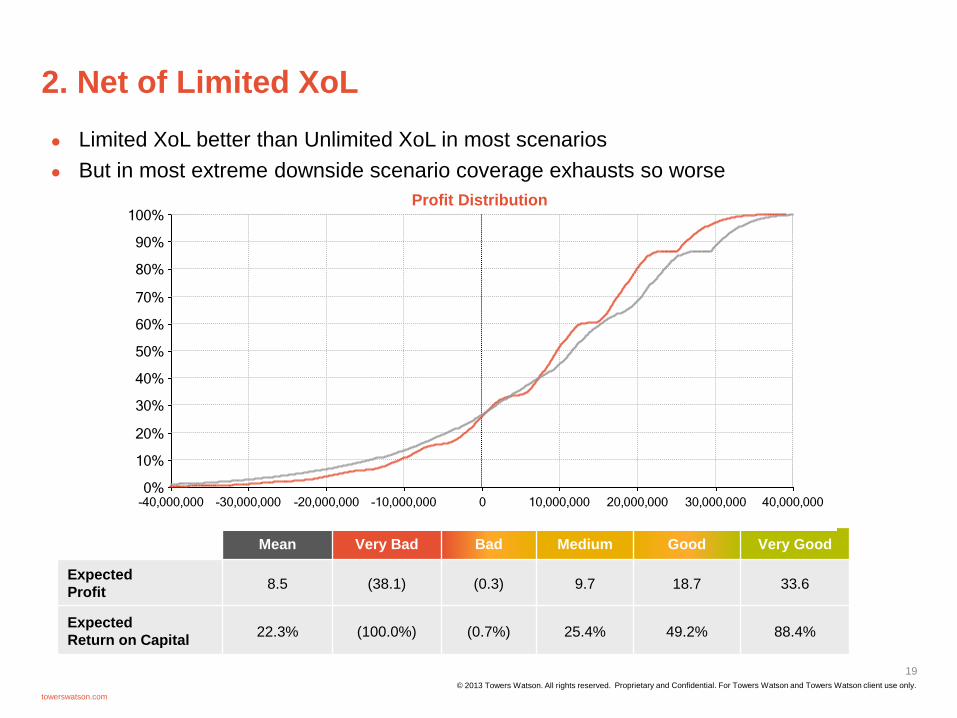

2. Net of Limited XoL

© 2013 Towers Watson. All rights reserved.

towerswatson.com

19

Limited XoL better than Unlimited XoL in most scenarios

But in most extreme downside scenario coverage exhausts so worse

Mean Very Bad Bad Medium Good Very Good

Expected

Profit 8.5 (38.1) (0.3) 9.7 18.7 33.6

Expected

Return on Capital 22.3% (100.0%) (0.7%) 25.4% 49.2% 88.4%

Profit Distribution_Gross_Limited

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

-40,000,000 -30,000,000 -20,000,000 -10,000,000 0 10,000,000 20,000,000 30,000,000 40,000,000

Value

Pe

rce

nti

le

Profit Distribution

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

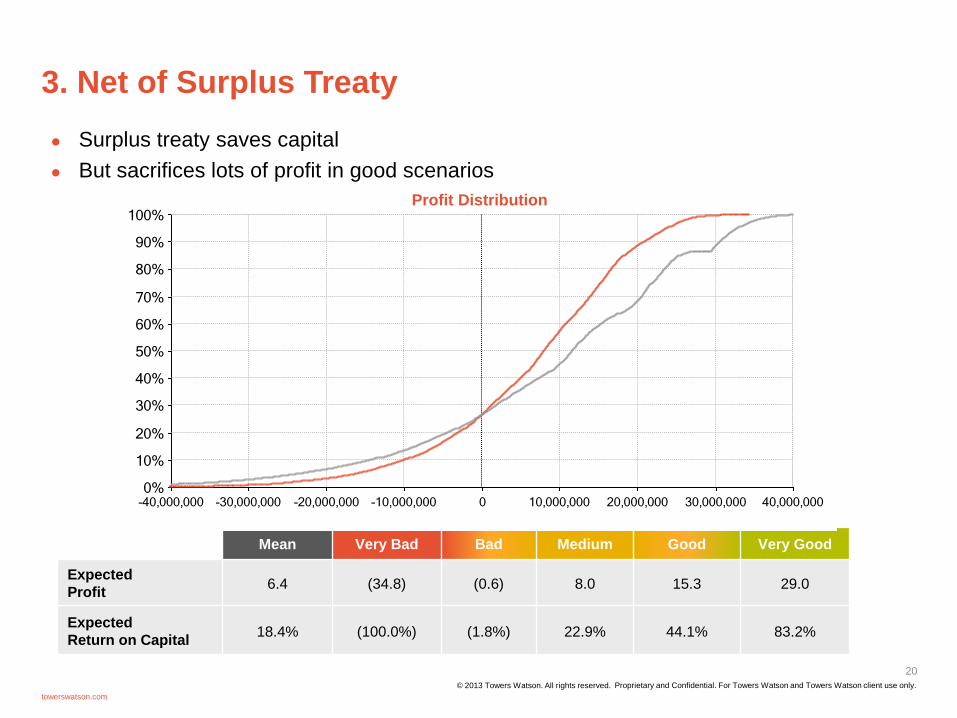

3. Net of Surplus Treaty

© 2013 Towers Watson. All rights reserved.

towerswatson.com

20

Surplus treaty saves capital

But sacrifices lots of profit in good scenarios

Mean Very Bad Bad Medium Good Very Good

Expected

Profit 6.4 (34.8) (0.6) 8.0 15.3 29.0

Expected

Return on Capital 18.4% (100.0%) (1.8%) 22.9% 44.1% 83.2%

Profit Distribution_Surplus Lines

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

-40,000,000 -30,000,000 -20,000,000 -10,000,000 0 10,000,000 20,000,000 30,000,000 40,000,000

Value

Pe

rce

nti

le

Profit Distribution

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

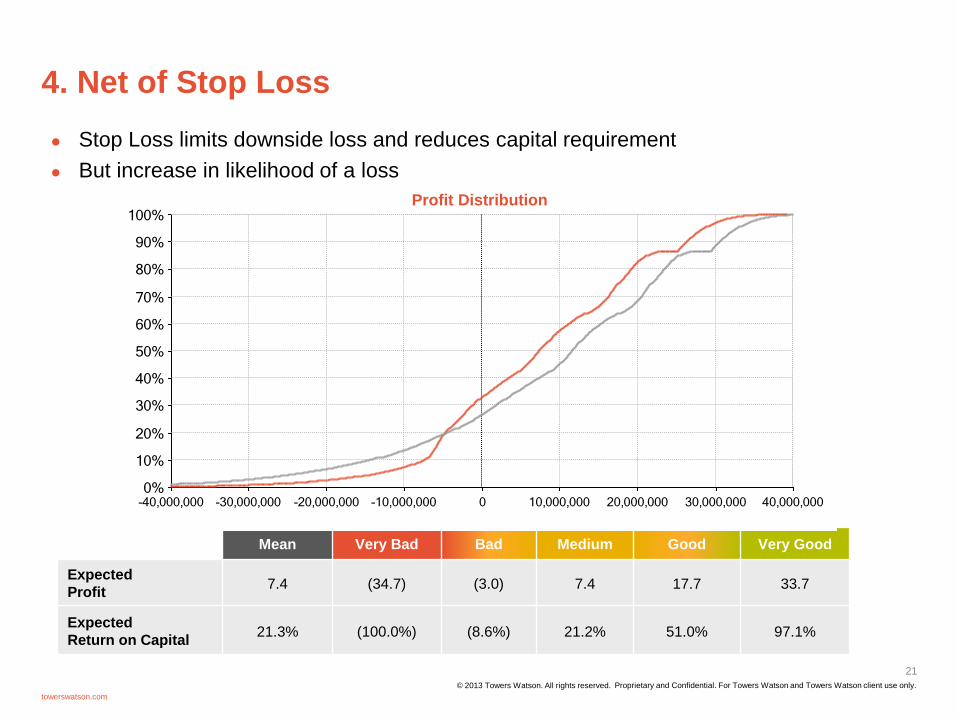

4. Net of Stop Loss

© 2013 Towers Watson. All rights reserved.

towerswatson.com

21

Stop Loss limits downside loss and reduces capital requirement

But increase in likelihood of a loss

Mean Very Bad Bad Medium Good Very Good

Expected

Profit 7.4 (34.7) (3.0) 7.4 17.7 33.7

Expected

Return on Capital 21.3% (100.0%) (8.6%) 21.2% 51.0% 97.1%

Profit Distribution_Gross_Stop Loss

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

-40,000,000 -30,000,000 -20,000,000 -10,000,000 0 10,000,000 20,000,000 30,000,000 40,000,000

Value

Pe

rce

nti

le

Profit Distribution

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

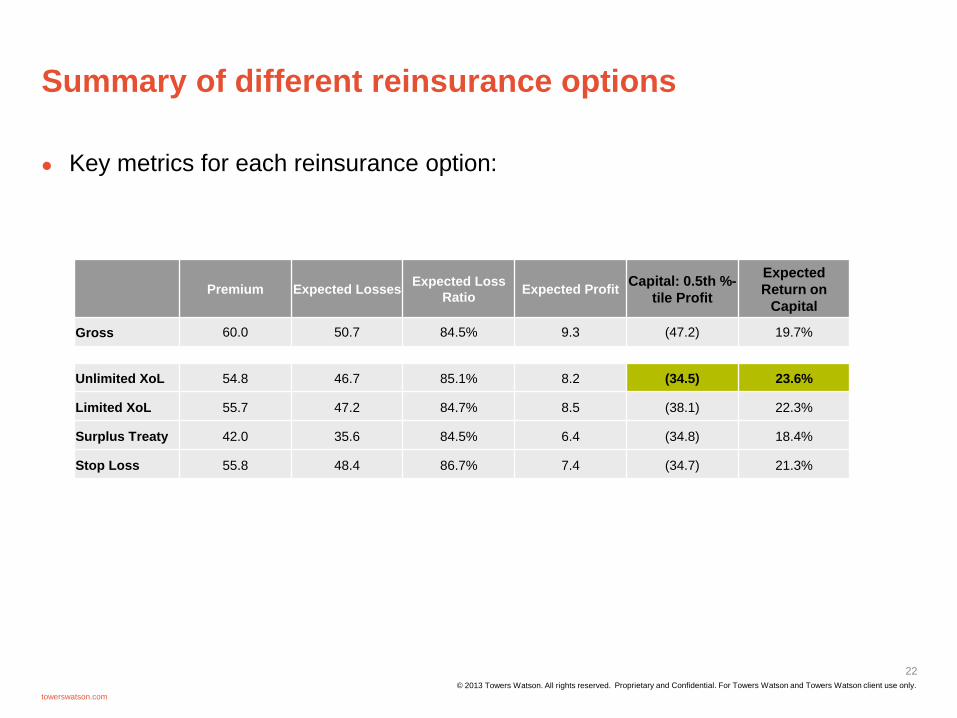

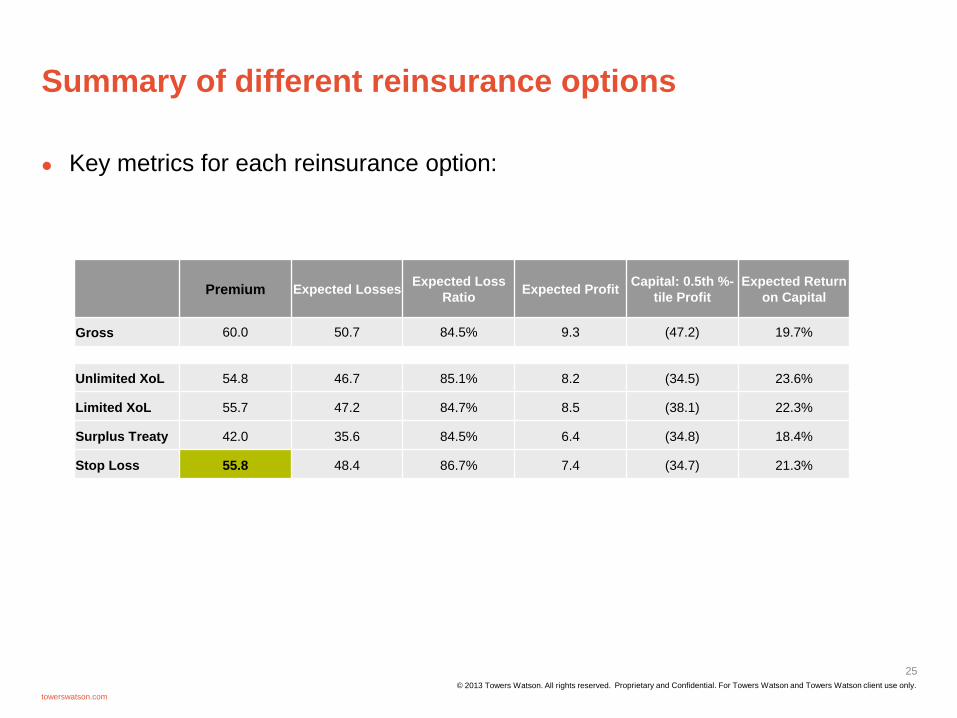

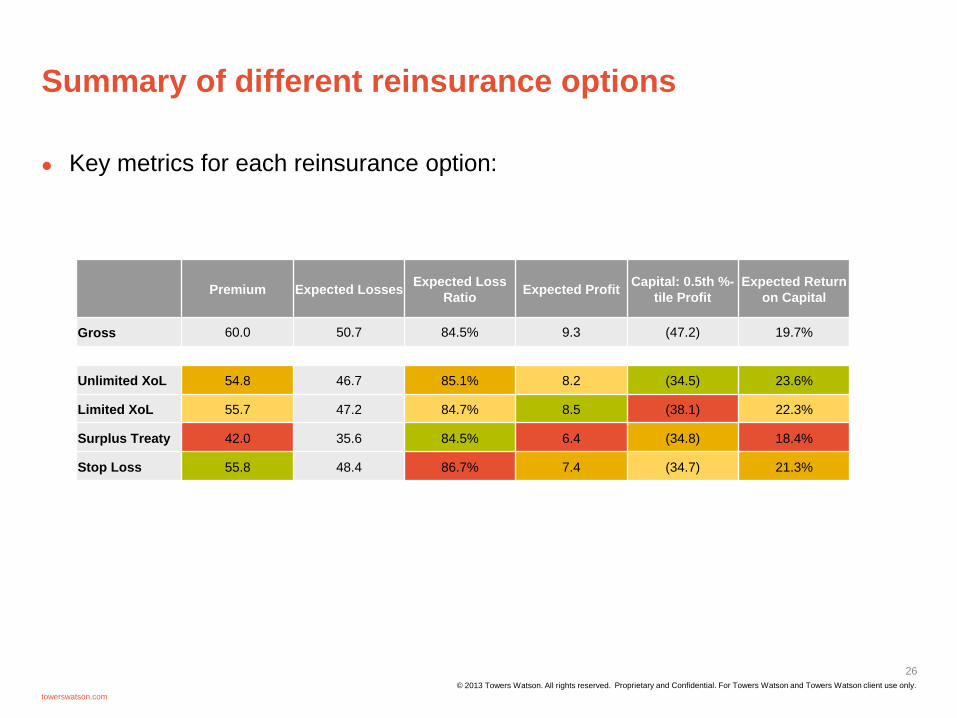

Summary of different reinsurance options

Key metrics for each reinsurance option:

© 2013 Towers Watson. All rights reserved.

towerswatson.com

22

Premium Expected Losses Expected Loss

Ratio Expected Profit

Capital: 0.5th %-

tile Profit

Expected

Return on

Capital

Gross 60.0 50.7 84.5% 9.3 (47.2) 19.7%

Unlimited XoL 54.8 46.7 85.1% 8.2 (34.5) 23.6%

Limited XoL 55.7 47.2 84.7% 8.5 (38.1) 22.3%

Surplus Treaty 42.0 35.6 84.5% 6.4 (34.8) 18.4%

Stop Loss 55.8 48.4 86.7% 7.4 (34.7) 21.3%

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

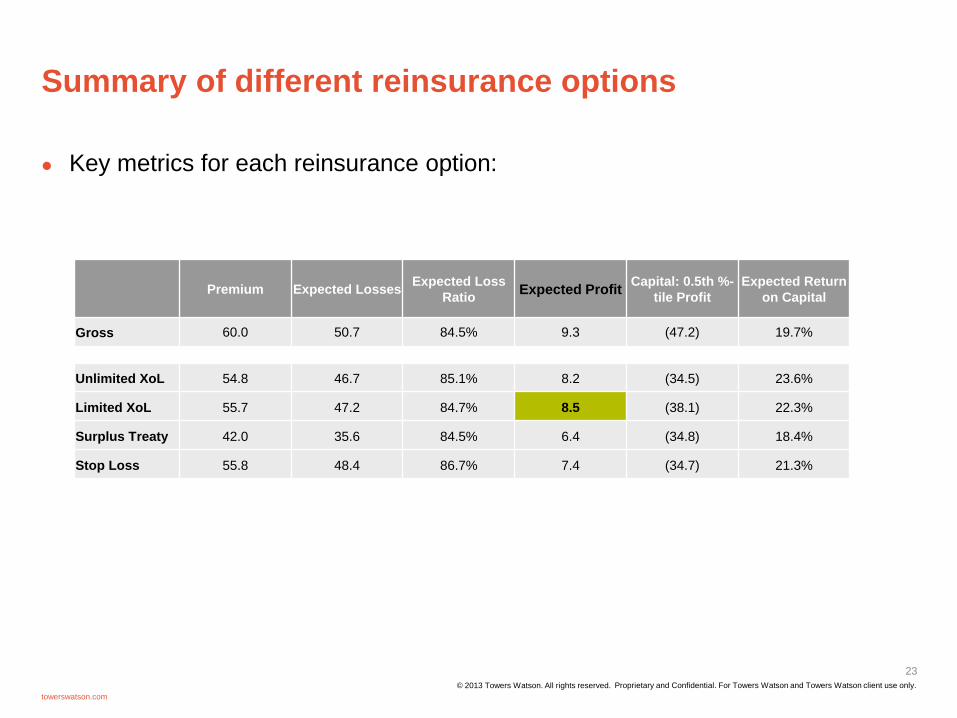

Summary of different reinsurance options

© 2013 Towers Watson. All rights reserved.

towerswatson.com

23

Premium Expected Losses Expected Loss

Ratio Expected Profit

Capital: 0.5th %-

tile Profit

Expected Return

on Capital

Gross 60.0 50.7 84.5% 9.3 (47.2) 19.7%

Unlimited XoL 54.8 46.7 85.1% 8.2 (34.5) 23.6%

Limited XoL 55.7 47.2 84.7% 8.5 (38.1) 22.3%

Surplus Treaty 42.0 35.6 84.5% 6.4 (34.8) 18.4%

Stop Loss 55.8 48.4 86.7% 7.4 (34.7) 21.3%

Key metrics for each reinsurance option:

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

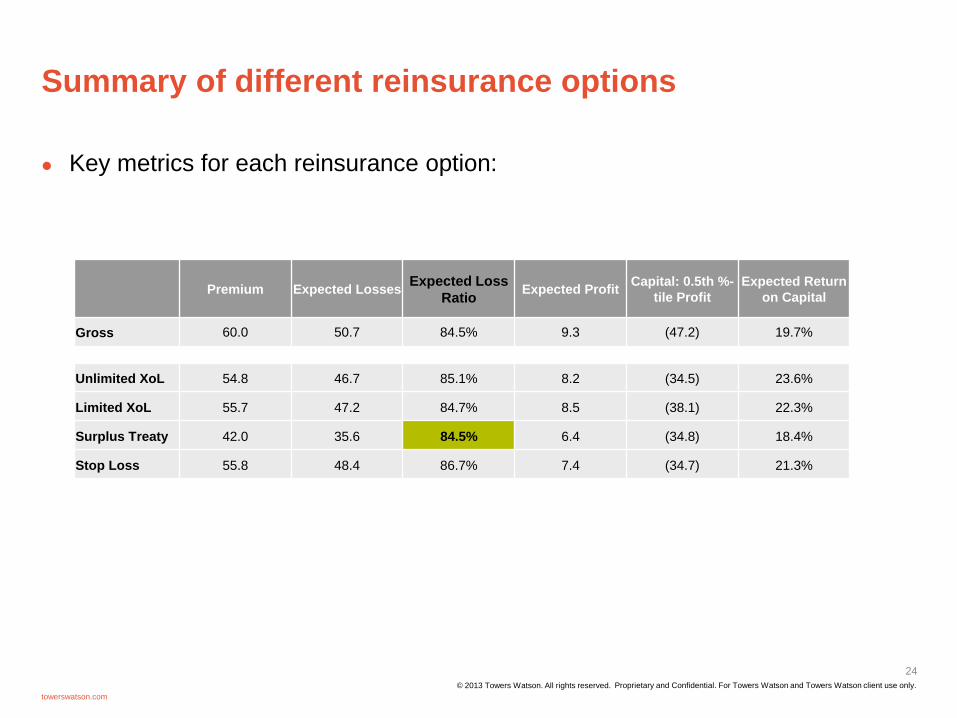

Summary of different reinsurance options

© 2013 Towers Watson. All rights reserved.

towerswatson.com

24

Premium Expected Losses Expected Loss

Ratio Expected Profit

Capital: 0.5th %-

tile Profit

Expected Return

on Capital

Gross 60.0 50.7 84.5% 9.3 (47.2) 19.7%

Unlimited XoL 54.8 46.7 85.1% 8.2 (34.5) 23.6%

Limited XoL 55.7 47.2 84.7% 8.5 (38.1) 22.3%

Surplus Treaty 42.0 35.6 84.5% 6.4 (34.8) 18.4%

Stop Loss 55.8 48.4 86.7% 7.4 (34.7) 21.3%

Key metrics for each reinsurance option:

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Summary of different reinsurance options

© 2013 Towers Watson. All rights reserved.

towerswatson.com

25

Premium Expected Losses Expected Loss

Ratio Expected Profit

Capital: 0.5th %-

tile Profit

Expected Return

on Capital

Gross 60.0 50.7 84.5% 9.3 (47.2) 19.7%

Unlimited XoL 54.8 46.7 85.1% 8.2 (34.5) 23.6%

Limited XoL 55.7 47.2 84.7% 8.5 (38.1) 22.3%

Surplus Treaty 42.0 35.6 84.5% 6.4 (34.8) 18.4%

Stop Loss 55.8 48.4 86.7% 7.4 (34.7) 21.3%

Key metrics for each reinsurance option:

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Summary of different reinsurance options

© 2013 Towers Watson. All rights reserved.

towerswatson.com

26

Premium Expected Losses Expected Loss

Ratio Expected Profit

Capital: 0.5th %-

tile Profit

Expected Return

on Capital

Gross 60.0 50.7 84.5% 9.3 (47.2) 19.7%

Unlimited XoL 54.8 46.7 85.1% 8.2 (34.5) 23.6%

Limited XoL 55.7 47.2 84.7% 8.5 (38.1) 22.3%

Surplus Treaty 42.0 35.6 84.5% 6.4 (34.8) 18.4%

Stop Loss 55.8 48.4 86.7% 7.4 (34.7) 21.3%

Key metrics for each reinsurance option:

Next steps

© 2013 Towers Watson. All rights reserved.

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

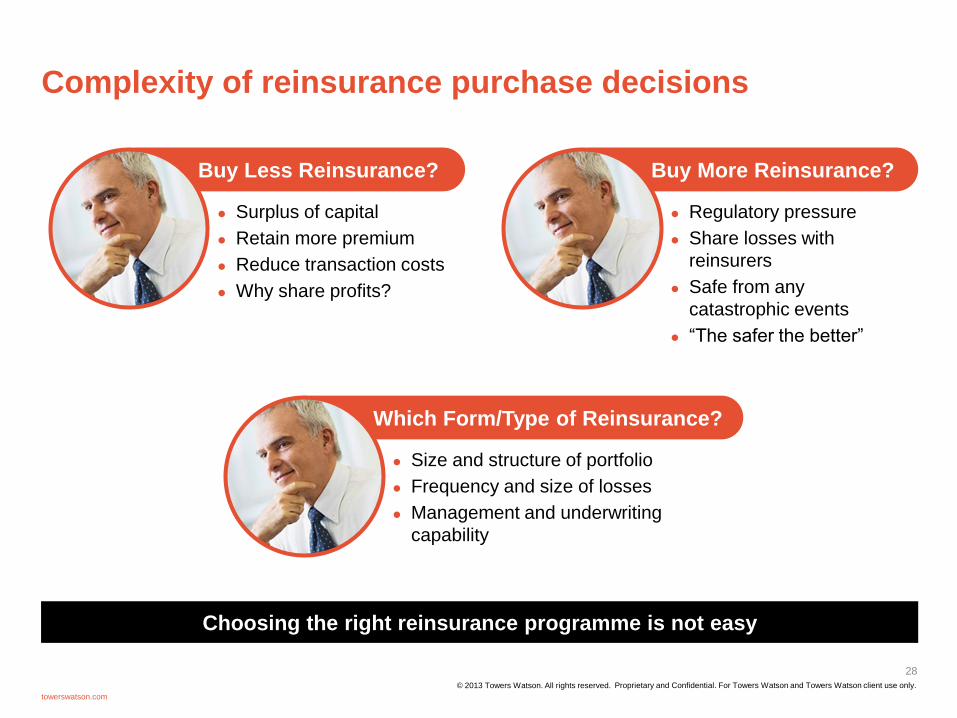

Complexity of reinsurance purchase decisions

Choosing the right reinsurance programme is not easy

Buy Less Reinsurance?

Surplus of capital

Retain more premium

Reduce transaction costs

Why share profits?

Buy More Reinsurance?

Regulatory pressure

Share losses with

reinsurers

Safe from any

catastrophic events

“The safer the better”

Which Form/Type of Reinsurance?

Size and structure of portfolio

Frequency and size of losses

Management and underwriting

capability

© 2013 Towers Watson. All rights reserved.

towerswatson.com

28

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

The reinsurance purchase decision is critical to the success of an

insurance venture

Too much or inappropriate reinsurance spend suppresses profitability

Too little or ineffective reinsurance can expose the venture to excessive risk

Today there are more diverse and complex reinsurance options than

ever before

To evaluate the best reinsurance structure we need:

An analytical review of the business under each reinsurance scenario

Combined with an understanding of the company’s risk appetite

and success measures

Conclusions

© 2013 Towers Watson. All rights reserved.

towerswatson.com

29

Proprietary and Confidential. For Towers Watson and Towers Watson client use only. © 2013 Towers Watson. All rights reserved.

towerswatson.com

30

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.