Embed Size (px)

Citation preview

A statistical sampling plan, designed especially

for auditors, that would help reduce

nonsampling error by organizing available data

into a quantifiable form for decision-making

RELATING STATISTICAL SAMPLING

TO AUDIT OBJECTIVES

BY ROBERT K. ELLIOTT AND JOHN R. ROGERS

FOR many years independent auditors have beenencouraged to use statistical sampling pro-

cedures in conducting audit tests. The advantageshave been pointed out in many books and articles onthe subject. Most auditors trained in the last decadehave been exposed to statistical sampling duringtheir formal training and encouraged to use it. TheAmerican Institute of Certified Public Accountantshas encouraged its use. Notwithstanding all of thisencouragement, use of statistical techniques is stillnot widespread within the profession. Althoughmany factors contribute to the lagging implementa-tion of statistical techniques, two stand out as mostimportant;

1. Statistical techniques have generally been cum-bersome to apply manually.

2. Statistical techniques have not been adequatelyrelated to common audit objectives.

With the general availability of eomputers inauditing, the cumbersome aspects of statisticalsampling procedures need no longer be done manu-ally. The eomputer will handle the intricacies ofsample size calculation, sample selection and evalu-ation effortlessly and without mechanical error.Computerization of statistical techniques will vir-tually eliminate the first major deterrent to the useof statistical sampling in auditing.

However, the second major deterrent must stillbe eliminated before statistical sampling can bewidely implemented. TTie purpose of this article isto suggest an approach to relating statistical tech-niques to audit objectives.

AUDIT OBJECTIVES

The overall objective of an auditor in carryingout the attest function is to make reasonably certain

that financial statements examined by him are ma-terially correct.^ He tlierefore wishes to find mate-rial errors in the financial statements if they exist.To do this he employs numerous procedures, one ofthe most important being the examination of docu-mentary evidence. Auditors long ago abandonedany attempt to examine documentary evidence foreach and every item represented in the financialstatements. The resulting partial (or sample) exam-ination must introduce an element of uncertaintyinto his conclusions, for he must draw inferencesfrom incomplete information. This is true whetheror not the auditor uses statistical sampling proce-dures.

The uncertainty resulting from partial examina-tion may fnistrate the auditor's desire for materiallycorrect financial statements in two distinct ways:

1. Financial statements may be correct, but he mayerroneously conclude they are incorrect andeither qualify his opinion or unnecessarily insistupon adjustments.

2. Financial statements may be materially in error,but he may erroneously conclude that they arecorrect and give an unqualified opinion.

Although financial statements may be in error byany amount (from zero on up), it is only necessaryto control audit risks at the points of zero error andmaterial error (that is, exactly the amount specifiedby the auditor as material) in order to meet theoverall audit objective. Therefore, for the remain-der of this article, only these two magnitudes oferror will be considered. The level of risk at all othermagnitudes ean be observed in Figure 1, page 51.

"Materially correct" in this context means "fairly pre-sented in conformity with generally accepted accountingprinciples."

46 THE JOURNAL OF ACCOUNTANCY, JULY 1972

For convenience, the risk of rejecting perfectly cor-rect financial statements will be referred to as the a(alpha) risk, and the risk of accepting financialstatements in error by exactly a material amountwill be referred to as the f3 (beta) risk.

These two risks exist even when the auditor usesjudgment sampling procedures, but they cannot inany way be quantified. The result is that, in somecases, auditors do less work than necessary to con-trol these risks and, in other cases, more work thannecessary. When too little work is done, the auditoris not efiFeetively carrying out the attest function.When too much work is done, the auditor is carry-ing out the attest function effectively, but at anexcessive cost.

USE OF STATISTICAL TECHNIQUES

Statistical sampling procedures are ideally suitedto measure the a and /? risks inherent in partial (ortest) examinations. Tf the auditor will state what aand p risks are justified, and what amount he con-siders material for a given account, a statistical testcan be designed to meet these eriteria. The abilityto measure, in this case, means there is an ability tocontrol.

When the auditor performs a documentary exam-ination, he may have either or both of two objec-tives:

1. To establish the effectiveness of systems and pro-cedures, in order to plan the type, extent andtiming of other audit procedures.

2. To establish the material correctness of a finan-cial statement amount.

Any relevant test of material correctness must bestated in dollar terms. Statistically, it must be a test

ROBERT K. ELLIOTT, CPA, is manager inthe executive office of Peat, Marwick, Mit-chell ir Co. in New York City. He is amember of the AICPA and the Pennsyl-vania Institute of CPAs. His article, "As-pects of Behavioral Accounting" was pub-lished in Statements in Quotes in the April197! JOURNAL. Mr. Elliott received hisbachelor's degree from Harvard College

and his M.B.A. degree from Rutfiers University. JOHN R.ROGERS. CPA, is a partner of Peat, Mar-wick, Mitchell ir Co., in New. York City.He .•serves on the Institute's committee onstatistical mmpUng and is a member of theNew York State Society of CPAs and theCanadian Institute of Chartered Account-ants. Mr. Rogers received his bachelor'sdegree from Dartmouth College and hisM.B.A. degree from Amos Tuck School ofBusiness Administration.

of variables. An attribute test, conversely, can ex-press conclusions only in terms of rates of occur-renee, not dollars.

An attribute test can indicate, for example, thatthe error rate in eertain documents is probably nomore than a certain percentage. While this may beof some use to the auditor, it is not a conclusion thatcan be measured in terms of financial statementimpact. A low error rate does not necessarily meanthat the financial statements are materially correct,nor does a high error rate mean the opposite. Theprincipal usefulness of the technique is to assistthe auditor in making qualitative judgments aboutthe operation of internal controls and aceountingsystems. These judgments may then be used inplanning the type, extent and timing of other auditprocedures, but they cannot normally be used fordirect audit conelusions conceming fair presenta-tion of the financial statements.

Although a statistical attribute test may be ofsome use in examining systems and controls, it is byno means necessary. Generally, in examining sys-tems the auditor seeks a qualitative conclusion (forexample, the controls over cash disbursements aregood). Seldom does he need precise measurementof rates of occurrence, such as would be providedby an attribute test. Neither is he overly concernedw ith a and ^ risk levels.

When the auditor needs quantifiable conclusions,though, he will be best served by a variables test(usually one in which the results are stated in dol-lars). Therefore, the remainder of this artiele willconcern itself solely with variables tests designedto establish the material correctness of financialstatement amounts.

PUBLISHED LITERATURE

Surpri.singly, there does not appear to be anypublished literature which deals explicitly with theuse of statistical technique.s to measure and eontrolthe auditor's a and P risks with respeet to variablestesting. The AICPA programed instruction series(An Auditor's Approach to Statistical Sampling,Volumes I through IV) and all known textbooksand articles known to us on audit u.ses of variablessampling refer to and use variables estimation tech-niques. They propose that the auditor sample a pop-ulation at a given confidence and precision to esti-mate the true value.

Generally, the auditor is advised to relate confi-dence to the level of internal control and precisionto materiality, but he is not given guidanee inplaeing numerical values on confidence and preci-sion. Furthermore, he is not given any advice onwhat to do with the statistical results. These arecorrectly asserted to be auditing, not statistical,matters. However, without some assistance in un-

THE JOURNAL OF ACCOUNTANCY, JULY 1972 47

derstanding how statistical inferences can be re-lated to auditing objectives, most auditors are re-luctant to use statistical techniques. Even whenthey are used, an auditor is not able explicitly tocontrol his a and fi risks. That is, an auditor whohas statistically tested $10 million in accounts re-ceivable and has 95 per cent confidence that thetrue value is between $9 million and $9,500,000 hassome useful audit information, but, based on thestandard approaeh, he cannot come to any eonclu-sion as to what a and ^ risks he has incurred.

In the absence of guidance, many auditors revertto rules of thumb in applying statistical techniques.The following approaeh is t>-pieal: let precision(P) equal the amount considered material (M) foran account; let the confidence level (CL) be 95 percent if internal eontrol is poor, or less (say 80 percent) if internal control is excellent; if the statisticaleonfidence interval- includes the book value, acceptit as correct, otherwise reject the book value.

If the auditor consistently follows such a plan,with its predefined decision rule, it is possible tocompute the a and ^ risks he is assuming. If thebook value is correct, there is a probability of 1 —CL that the sample estimate plus or minus the preci-sion will not include the book value, resulting in re-jection of the book value. Tlius a equals 1 — CL. Onthe other hand, if the book value is in error by anamount equal to the predetermined measure ofmateriality (M), one half of all sample estimatesplus or minus the precision will include the bookvalue, resulting in accepting the book value. Thus(i equals .50. In fact, /? equals approximately .50no matter what confidence level the auditor uses.^

Use of such a plan may not be optimal for audit-ing. The auditor uses a lower confidence level wheninternal control is good. But a lower confidencelevel implies a higher a risk. Thus the better thecontrols and the more likely the book value is tobe correct, the higher is the auditor's risk of reject-ing the book value. Conversely, the auditor's riskof accepting a value which is in error by the amountpredefined as material remains a high 50 per centwhether such an error condition is likely (poor con-trol) or unlikely (sood eontrol).

A more logieal objective of the auditor would beto adjust his fi risk for different internal eontrol con-ditions, not his a risk. Thus, some auditors havecompensated by simply letting precision equal one

half the amount considered material. (This adjust-ment generally results in quadrupling the samplesize.) This plan has a and (i risks that can be calcu-lated also. In fact:

a - 1 - CLfi ^ a/2.

While this adjusted approach at least reduces fi toa lower level, it still leaves the auditor more likelyto reject a book value when the controls are judgedto be good. Also, a and /? are always fixed in a two-to-one relationship, which may not be desirable.And, finally, in the adjusted approach, use of a con-fidence level of 95 per cent implies a jS of .025, whichseems unneeessarily low for typical audit circum-stances. If the auditor could justifiably accept ahigher value, he could be satisfied with smallersample sizes.

Variables estimation cannot be used to limit aand y9 risks without the existence of a predefineddecision rule for interpreting sample results. Thecommonly used decision rules may not result in thebe.st a and fi risk levels for auditing.

HYPOTHESIS TESTING

The auditor's objective can be better achieved bystatistical hypothesis testing. A statistical hypothe-sis test is specifically designed to discriminate be-tween two hypotheses with precisely defined a andfi ri.sks. In auditing, there fortunately exist two veryconvenient alternate hypotheses, which permit de-cisions highly relevant for auditing use. These hy-potheses are as follows:

Ho: The financial statement amount is correct.

H]: The financial statement amount is materiallyin error.

Now a is the risk of rejecting Ho if Ho is true, and ^is the risk of accepting Ho if Hi is true.

Civen three parameters—M (the amount consid-ered material), a and /?—the auditor can design asuitable hypothesis test for auditing a financialstatement amount

It is easy to convert the hypothesis test into anequivalent test stated in terms of eonfidence andprecision. The decision rule is that the book valuewill be aecepted if it is included in the eonfidenceinter\'al, but rejected otherwise. The conversion isexpressed as follows:

CL = 1 — a2 The statistical confidence interval is the range of values

around the statistical point estimate which is expected tocontain the tnie value with the specified confidence.

^ For any confidence level over 80 per cent, p = .50. Tf theconfidence level is less than 80 per cent, p is slightly less.For example, if the confidence level is 70 per cent, P =.48, and if the confidence level is 60 per cent, P = .45.

Xy. is the normal table value which includes an area of.5 — X. For example, Z ^^- = 1.645. This fonTiiila is an ap-proximation, but it is more than 99,9 per cent accurate aslong as a does not exceed .1 and /? does not exceed .5.

48 THE JOURNAL OF ACCOUNTANCY, JULY 1972

Thus, if the auditor wants to have no more than a5 per cent chance of rejecting a given account bal-ance if it is correct, and no more than a 5 per centchance of accepting the balance if it is in error by$1,000 or more, he should use a confidenee levelof 95 per cent (CL = 1 — .05) and a precision of$544 ( P = 1000/(1 + 1.645/1.96)).

The advantage of the hypothesis test approach isthat it permits the auditor to recognize and eontrolthe a and 9 risk levels. It also provides a correctdecision rule for using the statistical results. And,finally, it is stated in the most relevant audit tenns.

Use of a hypothesis test, however, requires someguidelines in selecting the parameters to be used.The following three headings deal with selectionof a, /? and M parameters.

DETERMINATION OF ACCEPTABLE a RISK

The a risk is the probability the auditor will rejectcorrect financial statement balances. However, ifthe auditor's tests point to rejection, he will usuallyinvestigate further to ascertain and correct thecauses. There is little likelihood of actually eom-mitting sueh an error. For statistical purposes,therefore, the risk can be considered as the risk thatthe auditor will unnecessarily be forced to performfollow-up work when an aeeount balanee is erro-neously rejected. The costs associated with this riskare only those of this unnecessary audit work. Thereis a theoretical optimum value for a (between 0and 1) which will minimize total cost, but it is notpractically possible to solve for this value. It is prob-able that the optimum value is relatively low, say.1 or less. Since sample sizes are substantially largerwhen a is less than .05, a value in the range .05 to.10 appears most reasonable."' The most practicalapproach would be for the auditor to select an ac-ceptable a level and then use it for all statisticaltests as a matter of policy.

DETERMINATION OF ACCEPTABLE fi RISK

The /? risk is of critical importance to the auditor;in fact, minimization of the overall ^ risk is the rea-son for the existenee of the public accoimting pro-fession. Therefore, when a given audit is eomplete,the auditor wants to have a great deal of assurancethat he has not given an unqualified opinion on(that is, accepted) materially incorrect financialstatements. If his only source of reliance were hisstatistical tests, it is clear that a very low fi riskwould be required. However, there are many otherfactors in the typical audit. Two of the most criti-cal are disciissed below.

•'For reasons given under the heading "Audit AdjustmentsRr.siillinR From Stiitistical Sampling" (page 53), a valueof .05 is recommended.

Internal control. The iirst factor the auditor mustconsider when selecting a ^ risk for a specific sta-tistical test is the degree of risk that a material erroreould oeeur in the area being examined. This riskis inversely related to the quality of internal controlin the given area, as good controls will tend to pre-vent the occurrence of errors and will help detectand correct those which nevertheless occur. Whencontrols are good, the auditor's risk is lower, and hecan eonsequently test at a higher /3 level.

In judging controls, the auditor need only eon-cern himself with those specific controls to be reliedupon in increasing his p risk. Once he decides torely upon controls, however, he must test them forcompliance and efiFeetiveness. Conversely, there isobviously no need for a compliance test when con-trols are evaluated as nonexistent, because, in thiscase, no reliance will be placed on the controls whenselecting a /3 level. Furthermore, since the purposeof compliance testing is to permit restrietion ofother work, it would not be logieal to spend moreeffort on the compliance test than can be saved inthe test of financial statement amounts. The auditorshould evaluate, before making thi.s decision, whichapproach will be more efficient. He shoiild remem-ber the purpose of the compliance test and omit itwhen it is not required or justified.

Even the most effective system of internal controlwill not prevent deliberate override of the controlsby management personnel. Therefore, the auditormust consider the risk of material error throughmanagement override of the system of internalcontrol. Although it is impossible to determine withcertainty those cases in which management hasoverridden the internal controls, it should gen-erally be possible to evaluate tliis risk throughconsideration of such factors as the type of organi-zation being audited, the susceptibility of the areabeing examined to misstatement, the requirementfor management judgment in determining theamounts in the records and prior experience inauditing the financial statements of the client. Notethat the evaluation is not intended to assess theprobability that management is overriding the eon-trols, but merely whether the area being examinedpresents any signifieant potential for override.

For example, if an auditor were testing revenueand expense aecounts of a nonprofit organization, hewould usually assess the risk of override as verylow. If he were testing the allowance for doubtfulaccounts in a commercial enterprise, however, hemight assess the risk as signifieant, even though hebelieved that the management of the particularclient would not in fact override the internal con-trols. On the other hand, if he were cheeking com-putation of withholding taxes on payroll checks fortliis second client, he would probably assess the

THE JOURNAL OF ACCOUNTANCY, JULY 1972 49

risk as low, for there would be little potential gainto management in overriding controls in this area.

The evaluation of this risk is not based on thecharacter of the management; it is not a moral judg-ment and no shadow is cast upon the managementby an evaluation that there is a signifieant risk ofoverride.

Whenever the auditor has assessed the risk ofoverride as signific;uit, he should limit his relianceon internal control, whether or not he has any evi-dence or reason to believe that management hasoverridden the controls. Therefore, he should testat a lower fi level, or more accurately, he shouldnot increase his /3 level in reliance upon internaleontrol.

Other audit procedures. The other factor the audi-tor must consider is the nature and effectiveness ofother auditing procedures he may be applying inthe areas under examination. If he is performinganalytical reviews of the ratios and trends and/oradditional detail audit procedures, his reliance onthe statistical test is obviously less than it would bein the absence of these other procedures. He cantherefore use a higher fi level. It is extremely im-portant to note, however, that in increasing his ftlevel in reliance upon other pnx^edures, the auditorshould evaluate very carefully any unusual condi-tions revealed by any of the tests performed. Hecannot find an unusual condition in one test andthen ignore it because his other tests fail to reveal it.The failure of any single test to reveal a condition ofinterest is not positive indication that it does notexist; therefore unti.sual circumstances revealed inany test require further investigation regardless ofthe outcome of other tests.

For convenience, we can consider two types ofotlier auditing procedures and classify them as tovviiether they are significantly effective or only mod-erately efFective. A significantly effective additionaltest would be a test with a relatively high probabil-ity of discovering material error conditions whichexist (e.g., most detail tests), while a nioderatrlyeffective test would have a fair probability of dis-covering material errors (e.g., many well-designedanalytical tests). For example, assume the audittest in question were a prieo test of inventory. Thefollowing additional tests would ordinarily be sig-nificantly effective: comparison of carr\ ing priceswith subsequent sales prices as adjusted to excludenormal gross profit, testing to published price quo-tations, confirmations with vendors, detailed ap-praisals, etc. The following tests would ordinarilybe moderately effective: analysis of gross profitratios by product lines, disciissions with knowledge-able and reasonably disinterested persons, analysisof standard eost system and variances, etc.

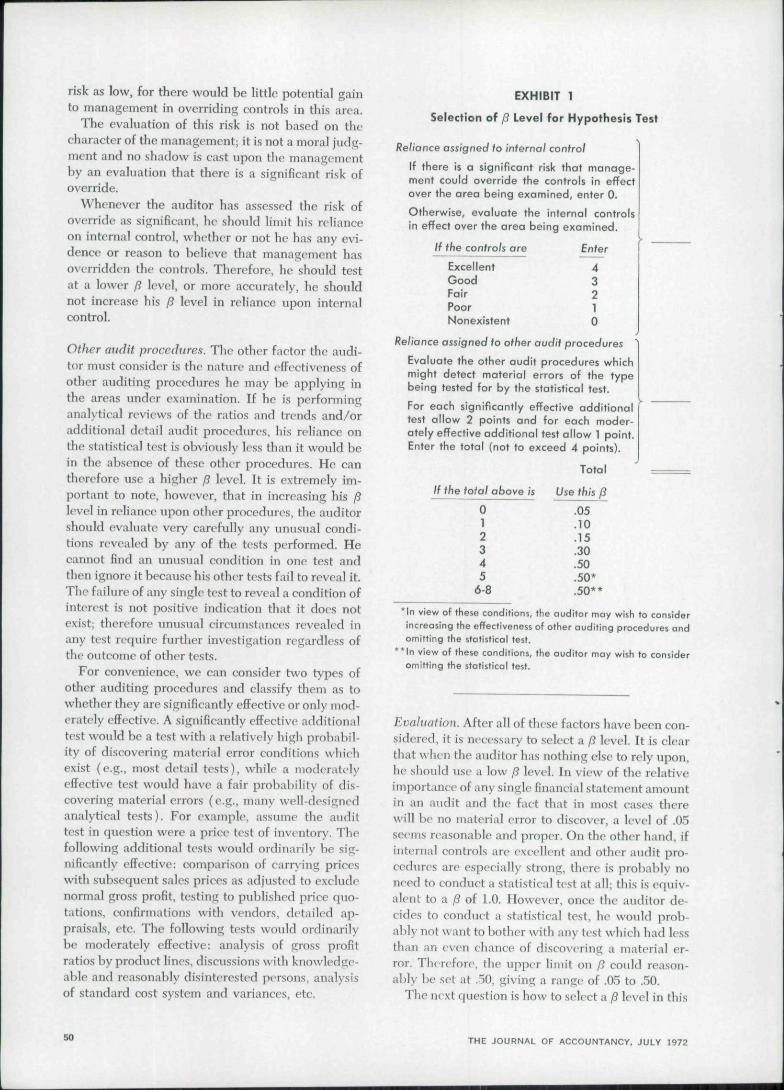

EXHIBIT 1

Selection of ft Level for Hypothesis Test

Reliance assigned to internal control

If there rs a significant risk that manage-ment cauld override the controls in effectover the area being examined, enter 0.

Otherwise, evaluate the internal controlsIn effect over the area being exomined.

f ihe controls are

ExcellentGoodFairPoorNonexistent

Enter

43210

Re/(ance assigned to other audit procedures

Evaluate the other audit procedures whichmight detect material errors of the typebeing tested far by the statistical test.

For eoch significontly effective additionaltest allow 2 points and for each moder-otely effective additional test allow 1 point.Enter the total (not to exceed 4 points).

If the total ofaove is

012345

6-8

iiiiiii

Use this fi

.05

.10

.15

.30

.50.50*.50**

*ln view of these conditions, the auditor moy wish to considerincreosing the effectiveness of other ouditing procedures andomifting the statistical test.

**in view of these conditions, the auditor moy wish to consideromitting the statistical test.

Evaluation. After all of these factors have been con-sidered, it is necessary to select a /? level. It is clearthat when the auditor has nothing else to rely upon,he siiould use a low fi level. In view of the relativeimportance of any single financial statement amountin an audit and tlie fact that in most eases therev 'ill be no material error to discover, a level of .05seems reasonable and proper. On the other hand, ifinternal controls are excellent and other audit pro-eechii-es are especially strong, there is probably noneed to conduct a statistical test at all; tliis is equiv-alent to a ^ of LO. However, once the auditor de-cides to conduct a statistical test, he would prob-ably not want to botlier with any test whidi had lesstlian an even chance of discovering a material er-ror. Therefore, the upper limit on fi eould reason-ably be set at .50, giving a range of .05 to .50.

The next question is how to select a fi level in this

50 THE JOURNAL OF ACCOUNTANCY, JULY 1972

FIGURE 1

1.00

.95

.90 -

.80

ACCEPTANCE CHARACTERISTICSOF HIGHEST AND LOWESTRECOMMENDED 0 LEVELS

.70 -ooCO

OZ

U .50 -

O .40

<CDOoe:

.30 -

.20

.05

-

-

-

-

^--a .05

\

\

\

\

\

^P= .50

\\

^0^ .05

.5 1.0 1.5 1.84 2.0

ERROR IN BOOK VALUE(MEASURED IN MATERIALITY UNITS)

2.5 3.0

range. By combining all of the relevant factorsmathematically and making some conservative esti-mates of values, it is possible to compute reasonable^ values, which will result in an overall fi risk of .05or less, when considering the statistical test in con-junction with various combinations of other rele-vant factors. This has been done, and the results areset forth in Exhibit 1, opposite. Although the result-ing levels are eomputed values, it is imjxirtant tonote that they appear quite reasonable when relatedto the conditions giving rise to them.

In order to demonstrate the value of increasingfi to the justifiable maximum, some relative samplesizes follow, based on a certain population witiifixed a and M values (the same sample size rela-tionship would hold in all cases):

0510153050

Sample Size340275235160100

The probabilities of accepting book values in errorby various amounts for the highest and lowest rec-ommended /i levels ( assuming a fixed a of .05) aregiven in Figure 1, above, (which is based on a nor-mal distribution of sample means). It is worth not-ing that even when the auditor chooses a ;ff of .50, hestill has only a small chance (.05) of accepting ascorrect a book value in error by 1.84 times his mea-sure of materiaUty and a still smaller chance if the

THE JOURNAL OF ACCOUNTANCY, JULY 1972 51

error is greater than that).The explicit eonsideration of both of the above

factors in the determination of ^ may go beyondcurrent practice, which seems to eoneentrate prin-cipally upon the evaluation of internal control (not-withstanding the provisions of the 1964 statementof the statistical sampling committee of the Ameri-can Institute of CPAs, which also relates the levelof statistical testing to the other audit procedures).It is clear, however, that other factors may be ofequal importance with internal eontrol in manycases. Evaluation of these factors requires auditjudgment, but these types of judgment are requiredfor all audit tests, not just statistical ones."

DETERMINATION OF M

The third parameter the auditor must specify isthe measure of materiality (M). That measure de-fines the alternative hypothesis:

Ho: True value = book value.Hj: True value = book value ± M.

Some auditors may object to the requirement tospecify M in advance, but it is conceptually similarto evaluating errors after their discovery as to theirmateriality. The auditor must have some standardsfor doing this, so he should be able to apply thesestandards in advaneo and specify a maximum dol-lar amount of errors which he would be willing toaccept.

Most auditors would welcome some guidance inspecifying M, yet there are no generally acceptedcriteria for quantifying the measure of materiality.Although it is impossible to prescribe definitive eri-teria in this area, it is at least possible to suggestsome general limitations and considerations.

Before considering the mea.sure of materiality fora given audit test, it is necessary to examine materi-ality for financial statements as a whole. (This willbe designated M,i, or overall materiality, and is eon-sidered to be the smallest amount by which the fi-nancial statements could be in error and still requirea qualified auditor's opinion.) Mo should not be too

«Statement on Auditing Procedure Nn. 3.3, Chapter 6,Paragraph 9 states: "The amount and kind.? of evidentialmatter required to snpport an informed opinion are mat-ters for the auditor to determine in the exercise of hisprofessional judcnient after a careful study of the circum-stances in the particular case. In making .such decisions,he should consider the nature of the item under examina-tion: the materiality of possible errors and irreRularities;the degree of risk involved, which is dependent on theadequacy of the internal control and the susceptibility ofthe given item to conversion, manipulation, or misstate-ment; and the kinds and competence of evidential matteravailalile."

large, for then financial statements would be insuf-ficiently precise. Conversely, it should not be toosmall either. Nearly every amount in financial state-ments includes elements of estimation and uncer-tainty. In the aggregate, this uncertainty may bequite large. It would not be very logical to concen-trate auditing effort on minor refinements in indi-vidual accounts which will be swamped by theaggregate uncertainty in the financial statements.Furthermore, sample sizes increase very rapidly asmateriality decreases; this mandates use of the larg-est Mo consistent with overall audit objectives.

Readers of financial statements are usually mostinterested in net income (and such related factorsas funds generated). It is therefore probable thatthe auditor will begin his determination of materi-ality with net income. Since any change.s in incomewill be partially offset by changes in such profit-related charge.-;' a.s inrame taxes and profit sluu ingexpense, these should also be considered in deter-mining materiality. (Only rarely would a statisti-cally located difference result in a permanent timingdifference for tax purposes.) Therefore, if theauditor considers the measure of materiality to be5 per cent of net income, he would set Mo as follows:

5? of net income

1 — marginal rate of incomedetermined charges^.

Naturally, the resulting figure is .subjeet to theauditor's judgment. In some cases, he may wi.sh tolower or raise the figure, based on other consider-ations. For example, if the company is in or near abreak-even .situation, a fixed percentage of incomewould result in an impractically small measure ofmateriality; in .such a case, the auditor might con-sider u.sing the company's average net income or anormal return on investment instead of net income.Also, when there are extraordinary items on the in-come statement, it may often be appropriate to basemateriality on income before extraordinary items.

Now, assuming the auditor is sati.sfied tliat he hasa reasonable value for Mo, the question arises as to

"Income" and "charges" would be replaced by "loss" and"credits" when appropriate.The "nuirRinal rate of income determined charges" is thefraction of the next dollar of income which would betaken by income-determined charges such as income taxesand profit-sharing expense. Assume a company's federaltax rate on additional income is 48 per cent and there is aprofit-sharing plan which requires 10 per cent of pretaxincome to be distributed to employees. If there are noother income determined charges, the "marginal rate ofincome determined charges" is 53.2 per cent (.48 -|- (1 —.48) (.1)).

52 THE JOURNAL OF ACCOUNTANCY. JULY 1972

how to allocate this figure among the various finan-cial statement accounts. Obviously, he should notset M for any statistical test equal to (or largerthan) Mo, for then there would be no margin forerror in any other account in the financial state-ments.

Assume that the materiality (or amount of un-certainty) can be quantified for the audit of everybalance sheet account (this is the case if all bal-ance sheet accounts are statistically audited). Letthe materiality of the ith account be Mi. Also as-sume the same « and p are used in all tests, and thesampling error in all accounts is independent. Thenthe following relationship would be required inorder for the total sampling error to be less than Mowith the desired probability:

How valid are these assumptions? If the auditoruses a fixed a risk and a statistical fi designed toreduee his overall (i risk to a predefined level, the aand fi risks for all statistieally audited accounts willbe approximately equal. If an independent randomSiunple is drawn for each account audited, then thesampling error for each account will he indepen-dent. (Tlie fact that there are biases in the datasuch as deliberate overstatement of assets and un-derstatement of liabilities will not cause any depen-dence in the sampling error for eaeh account.)

The one assumption which fails is the quanti-fiability of sampling error in all accounts, becausealmost certainly never would all accoimts be au-dited statistically. However, the auditor shouldestimate the total uncertainty remaining in the ac-counts not audited statistically. He should reviewthe potential problem areas and estimate the prob-able outside limit of possible error for all these ac-counts. This total must always be less than Mo forotherwise he would not have done sufficient workto give an unqualified opinion. Let this estimatedtotal amount be M,.s,. The auditor would normallyhave a direction in mind for this possible error;therefore, it cannot be considered independent ofthe statistical sampling errors. If the materiality ofthe rth .statistically audited account is Mj, the sta-tistical tests must then meet the following criterion:

In determining Mest. the auditor should considerthe nature of the accounts not statistically audited.If, for example, tliey were capital stock, additionalpaid-in capital and long-tenn debt, not much al-lowance for error would ordinarily be assumed, be-cause each of these accounts could theoretically beaudited to achieve a highly accurate result. On theother hand, if the accounts not audited statisticallyincluded receivables, inventories or accounts pay-able, a rather larger allowance for error would ordi-narily be assumed.

Application of these guidelines to determine Mis admittedly not easy, but will at lc'a.st result in arational determination of M, which will meet over-all audit objectives at a reasonable cost.

AUDIT ADJUSTMENTS RESULTING FROMSTATISTICAL SAMPLING

The hypothesis test approaeh to statistical audit-ing results in a binary decision: accept/reject. If thedecision is accept, the auditor is finished with theaccount (if his assumptions about other auditingprocedures and internal controls, on \\ hich he reliedin raising fi, are sustained). He accepts tlie balanceas correct within the originally specified risk levels.But if the decision is reject, the auditor cannotmerely qualify his opinion. He needs to know whatamount he can accept as materially correct and thenhave the client adjust the books to that amount.

In general, the same sample data used to conductthe hypothesis test can be used to make a dollar-value estimate of an account balance. Given thesample data and the amount specified by theauditor as material, it is possible to calculate theconfidence that any specified value of the aeeountbalance is materially correct.

Under the heading "Determination of Acceptablefi Bisk" (page 49). it was proposed that the auditorassume no more than a 5 per cent probability of ac-cepting materially erroneous aeeount balances. Thestatistical fi used may have been more than .05 be-cause of reliance upon internal eontrol or otheraudit procedures. Once the hypothesis test has re-jected the account balance (because of errors in theaudited balance), the auditor ha.s an indication thatwhatever he relied upon was ineffective. He shouldtherefore adjust his statistical risks so he has nomore than a 5 per cent chance that the estimatedbook value is materially in error.

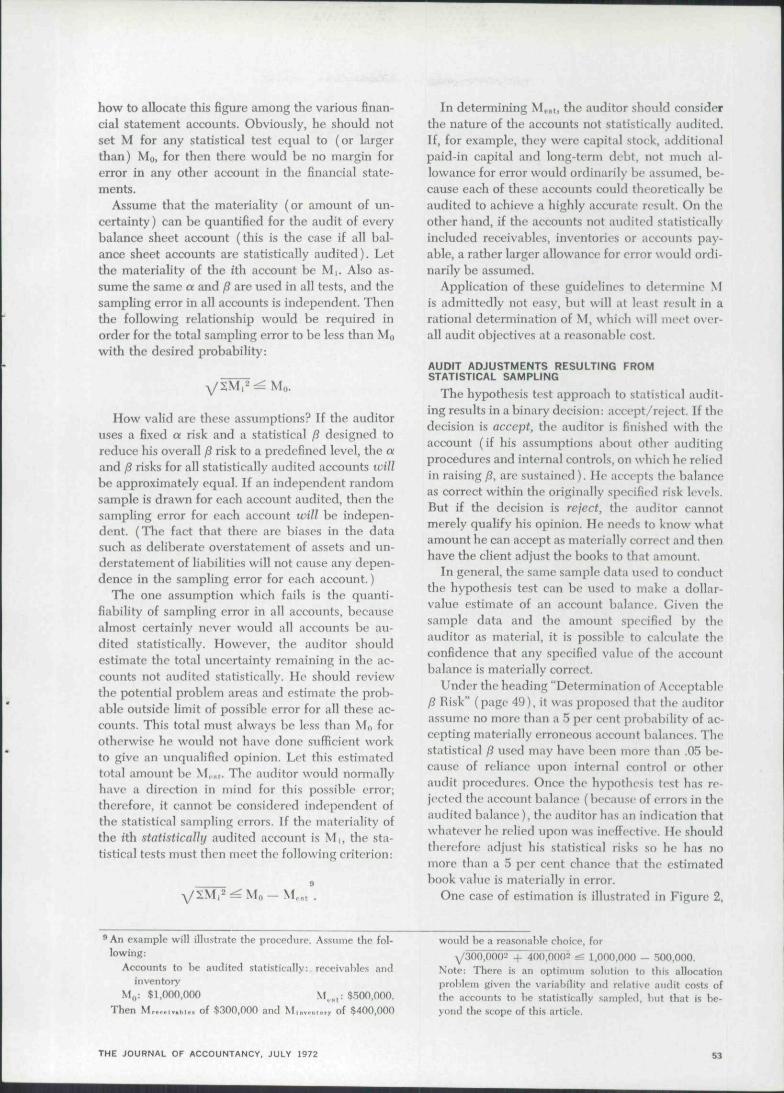

One ease of estimation is illustrated in Figure 2,

"An example will illustrate the procedure. Assnnie the fol-lowing:

Accounts to be audited statistically: receivables andinventory'

M,,; $i,oon,ono M^^^: $500,000.Then M»,,,,.h,» of $300,000 and M,nv,,,.»r. of $400,000

would be a rca.sonable choice, for^300,0002 -f- 40070002 1^ 1,000,000 ~ 500,000.

Note: There is an optirmim solution to this allocationproblem given the variability and relative audit co.fts ofthe accounts to be statL-Jtlcally sampled, but that is be-yond the scope of tbis article.

THE JOURNAL OF ACCOUNTANCY, JULY 1972 S3

FIGURE 2

.95 -

CONFIDENCETHAT ACCOUNTBALANCE ISMATERIALLYCORRECT

\

\

\

\

\

POINTESTIMATE

BOOKVALUE

DOLLAR VALUE OF ACCOUNT BALANCE

Note: figure) 1, 3 and 4 are read as follows: for any value on thehorizontal axis, Ihe confidence thot the true value is within rJi Mof that point is read ofT Ihe vertlcol axis. These figures should nolbe canfused wilh normal curves.

FIGURE 31.00.95 ^ - i . \

CONFIDENCETHAT ACCOUNTBALANCE ISMATERIALLYCORRECT

J

/

11

\

\

\

VPOINT

ESTIMATEBOOKVALUE

DOLLAR VALUE OF ACCOUNT BALANCE

above. In tliis case, the point estimate'" is tJieauditor's best estimate of the corrcet value, but, be-cause of inadequate sample size, he can be only SOper cent confident that if the books are adjusted tothe estimate, there would be no material error inthe account balance. Thus the sample evidence issufficient to convince the auditor that the bookvalue is wrong, but insufficient to say what is rightat a high level of eonfidence. In this ea.se, the sampleis too small to make an estimate at 95 per eent eon-fidence.

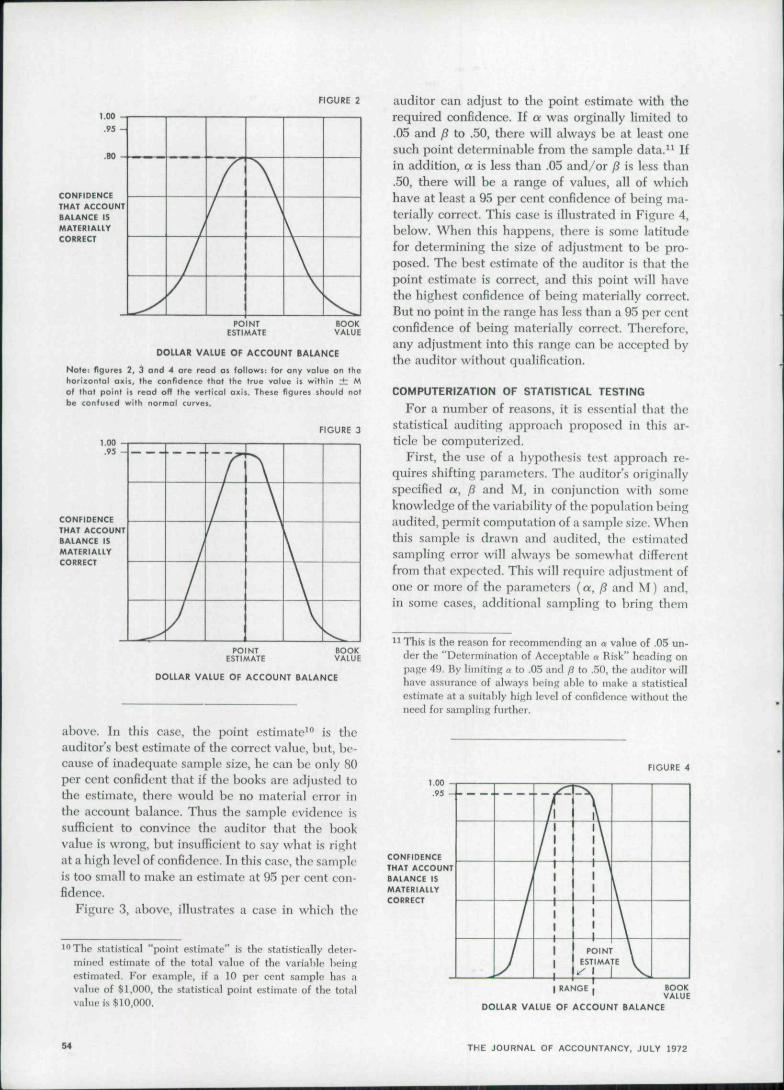

Figure 3, above, illustrates a ease in whieh the

The statistical "point estimate" is the statiKtically deter-mined estimate of the total vahie of the variable beingestimated. For example, tf a 10 per cent sample has avalue of $1,000, the statistical point estimate of the totalvalue is $10,000.

auditor can adjust to the point estimate with therequired confidence. If a was orginally limited to.05 and fi to .50, there will always be at least onesuch point determinable from the sample data." Ifin addition, a is less than .05 and/or fi is less than.50, there will be a range of values, all of whichhave at least a 95 per cent confidence of being ma-terially correct. This case is illustrated in Figure 4,below. When this happens, there is some latitudefor determining the size of adjustment to be pro-posed. The best estimate of the auditor is that thepoint estimate is correct, and this point will havethe highest eonfidence of being materially correct.But no point in the range has less than a 95 per centconfidence of being materially correct. Therefore,any adjustment into this range ean be accepted bythe auditor without qualification.

COMPUTERIZATION OF STATISTICAL TESTING

For a number of reasons, it is essential that thestatistieal auditing approaeh proposed in this ar-ticle be computerized.

First, the use of a hypothesis test approaeh re-quires shifting parameters. The auditor's originallyspecified ot, fi and M, in conjunetion with someknowledge of the variability of the population beingaudited, perniit eomputation of a sample size. Whenthis sample is drawn and audited, the estimatedsampling error will always be somewhat differentfrom that expeetcd. This will require adjustment ofone or more of the parameters (a, fi and M) and,in some cases, additional sampling to bring them

TTiis is the reason for recommending an a value of .05 un-der the "Determination of Acceptable a Risk" heading onpaH<? 49. By limiting « to .05 and p to .50, the auditor willhave a.ssiirance of always being alilc to make a statisticalestimate at a suitably hiph level of confidence without theneed for sampling further.

FIGURE 4

1.00.95

CONFIDENCETHAT ACCOUNTBALANCE ISMATERIALLYCORRECT

BANGE, BOOK' VALUE

DOLLAR VALUE OF ACCOUNT BALANCE

54 THE JOURNAL OF ACCOUNTANCY, JULY 1972

within the required limits. ^ Adjustments of any ofthe parameters results in adjustment of the rejec-tion point for the hypothesis test. While all of thesefactors can be dealt with manually, they are com-plicated enough to eause a high rate of nonsamplingerror and inconvenience in field work.

Second, the use of a hypothesis te.st approaeli willnormally require greater precision than the typicalaudit approach; this means larger sample sizes. ToofFset the inerea.se in sample sizes it is necessary toobtain the benefit of more efficient .statistical pro-cedures, sueh as optimal stratification and correla-tion analysis. The eomputer is invahiable for themore complex computations these procedures re-quire.

And, finally, manual applications of statisticalprocedures have frequently resulted in various non-sampling errors, such as biased sample design, non-random sample seleetion. unwarranted substitii-tions in samples and the like. The eomputer caneliminate or vastly reduce all of these problems.Furthermore, many of the required calculations, ifdone manually, are so onerous as to discourage theuse of statistical techniques.

The requirement for a computer should not he ahardship for any auditor. Most large CPA firmshave generalized computer audit paekages at theirdisposal, and all others have access to such a pack-age through the American Institute of CPAs. All

that is required is to incorporate the statisticalmathematics into these generalized audit programs.

CONCLUSION

The recommended statistical sampling plan hasbeen developed specifically to meet common auditobjectives, and in a way which is convenient forthe auditor to use. If the system is computerized, tlieauditor need not deal with formulas, tables, sampleselection or unfamiliar statistical terminology.'^ Allof this should go a long way toward reducing non-sampling error and auditors' reluctance to use sta-tistieal techniques, while providing a powerfulaudit tool.

This sampling plan (or any other) does not re-place or reduce the need for audit judgment. Ifanything, more judgment is required because manyaudit judgments must now be clearly articulated,and this will nearly always result in their beingmore carefully considered. The auditor must exer-cise considerable judgment in all of the followingareas: seleetion of cases in whieh he will rely onstatistical procedures; evaluation of inputs such asmateriality, internal eontrol, etc.; evaluation of sam-ple items; and the interpretation of results. All thestatistical plan does is to organize the available in-formation into a quantifiable fonn for decision-making.

12 Since p and M are critical to the audit hut a is not, themost logical approach would be to hnld p and M at thespecified values and let « vary within some rea.sonablerange. For example, if the target value for n were .05, thetest mijiht be considered complete as long as p and Mwere met and a were no fireater than .10. Otherwise,further sampling would be required.

1 Note that once a hypothesis test with a fixed a is designed,the auditor's only inputs are hi.s evaluations of materiality,strength of internal control and strength of other auditprocedures. His output is a statistically supportable deci-sion to accept the book value, or a statement of what bookvalue would be acceptable. None of this requires anyfamiliarity with statistical terminology or procedures.

THE JOURNAL OF ACCOUNTANCY. JULY 1972

![Statistical guidelines for sampling marine avian populations... · Statistical Guidelines for sampling marine avian populations Zipkin_IWMC_2012_Session 30.ppt [Compatibility Mode]](https://img.pdfslide.net/doc/110x75/612d84491ecc515869423d16/statistical-guidelines-for-sampling-marine-avian-populations-statistical-guidelines.jpg)