Embed Size (px)

Citation preview

MICA (P) 012/01/2012 Ref. No.: SG2012_0239 1 of 12

Religare Health Trust

Exposure to India’s Healthcare Sector Industry: Real Estate Operations

Phillip Securities Research Pte Ltd

16 October 2012

Report type: IPO Factsheet Company Overview Religare Health Trust, a business trust, comprising healthcare assets in India. Its mandate is to invest in medical and healthcare assets and services in Asia, Australasia and global emerging markets, including medical and healthcare asset developments. RHT’s initial portfolio consists of 11 clinical

establishments, four greenfield clinical establishments and two operating hospitals valued at S$748mn

At the IPO price of S$0.90, RHT is trading at one time to its book value and appears inexpensive

The institutional tranche was 2.5 times oversubscribed What is the news? RHT is scheduled to list on the third week of Oct-12. Approximately S$510.8mn will be raised from the public offering. 95% of the proceeds will be uitilised to partially fund the initial portfolio. Its initial portfolio consists of 11 clinical establishments (S$714mn), four greenfield clinical establishments (S$29mn) and two hospitals managed and operated by RHT (S$5mn), which are all geographically diversified across India. How do we view this? RHT provides unique value proposition for investors to have exposure to the growing demand of quality healthcare services in India and Asia Pacific. We like RHT’s service fee revenues term structure that offers both downside protection (15 years term with annual escalation of 3%) and upside potential (7.5% of Fortis companies’ operating revenue). In addition, rising affluence in upper middle class segment and underserved Indian healthcare market would benefit RHT. Foreign exchange risk is the main concern for RHT but forward contracts are put in place to hedge the currency translation up to FY2014. Investment Actions? On the valuation, RHT is priced at one time to book. The price of RHT appears inexpensive on the P/B basis relative to the rich P/B valuation of Ascendas India Trust (a-iTrust) at 1.27 times which is way above its historical P/B mean of 0.83. Annualised FY13 dividend yield of 9.0% including the distribution wavier (up to FY2014), looks appealing given the current slow growth and yield-starved period. By stripping out the distribution wavier, the yield is around 6.5% which is lower than a-iTrust yield of 7.1%. The institutional tranche was 2.5 times oversubscribed according to the news flow compared to Courts Asia which was 3.4 times subscribed.

Fig.1. IPO statistics and offering Summary Issuer: Religare Health Trust (RHT)Listing: SGX-STOffering type: Initial Public OfferingSponsor: Fortis Healthcare LtdIPO Price: S$0.90 per uints

Implied Yield 9.0% (Forecast Year 2013 (annualized))9.1% (Projection Year 2014)

Offering size: c.S$510mn567.5mn units (72.0%)

Sponsor stake: Sponsors will retain 28.0% stake (220.7 mn units)

Lock-up period for sponsor:

Six months for 100% and a further of six months for 50% after the listing date.

Distribution: Reg S only; Semi-annual basis (payout ratio till Mar 2014: 100%)

Joint Global Coordinator and Joint Bookrunner:

CIMB, DBS, Normura, Reliare, Stanchart

Source: Trust and PSR Fig.2. Indicative Timetable 1-9 Oct Roadshow and bookbuilding12-Oct Expected Registration12-16 Oct Expected Public offer period19-Oct Expected Listing Source: Trust and PSR AnalystTravis [email protected]+65 6531 1229

Religare Health Trust Singapore Equities Research 16 October 2012

2 of 12

Business Overview Religare Health Trust (RHT) is a business trust with an investment mandate to invest in medical and healthcare assets and services in Asia, Australasia and global emerging markets. RHT also involved in medical and healthcare asset developments. Its initial portfolio consists of 11 clinical establishments (S$714mn), four greenfield clinical establishments (S$29mn) and two hospitals managed and operated by RHT (S$5mn), which are all geographically diversified across India. Fig. 3. Location of clinical establishments and operating hospitals in India

Source: Trust Fig.4. Snapshot of operational and assets information

% increaseCurrent pperational beds 1782 beds Installed bed capacity 3197 beds 79.4%Potential bed capacity 4617 beds 44.4%

(% of initial porfolio valuation)

60.3%> 50 years remaining lease 26.1%< 50 years remaining lease 13.7%

(% of initial porfolio valuation)

RHT clinical establishments 95.4%Greenfield clinical establishments 3.9%

0.7%(% of initial

porfolio valuation)32.9%63.7%3.5%

*Number of beds as at 30 June, 2012

QuaternaryTertiarySecondary

Operating hospitals

Beds capactiy*

Land tenure

Income breakdown

Value chain of healthacare services

Freehold

Source: Trust and PSR

RHT is well-positioned to grow organically with the potential to ramp up the current operational beds from 1,782 beds to 4,617 beds. The bulk of the properties carry freehold titles (60.3%) as well as land with leases more than 50 years (26.1%). All the 17 clinical establishments and operating hospitals provide high-end healthcare services, with tertiary and quaternary segments both chalked up 96.6% of its initial portfolio. In addition, significant portion of the income is generated from the clinical establishments, forming 99.3% of the initial portfolio. Use of proceeds

Acquisition of the initial portfolio and CCPS subscription (~94.8%)

Issue and debt-related costs (~5.1%) Working capital (~0.2%)

Investment highlights 1) Latent potential in Indian healthcare sector: India being the second most populous country in the world coupled with the portion of aged population projected to increase from 5.0% (c.58.1 million people) in 2010 to 5.2% (c.65.0 million people) in 2015 by Frost and Sullivan, we see there is great potential for healthcare sector in India to grow exponentially. Rising affluence in upper middle class segment, increasing healthcare coverage, and underserved Indian healthcare market would generally benefit the private healthcare operators like RHT, whose clinical establishments serve patients at the upper stream of the value chain. 2) Diversified medical and healthcare assets and service across India: Its portfolio of 11 clinical establishments and four greenfield clinical establishments and two operating hospitals are strategically located in India. These clinical establishments and operational hospitals offer a range of healthcare services such as cardiac sciences and neurosciences to patients. 3) Solid and established operating track record: The sponsor has an operating record of more than 10 years in delivering integrated healthcare service in Pan Asia-Pacific region spanning 10 countries including India, Singapore, Australia, New Zealand and Vietnam. Some of the hospitals are of higher quality standards and achieve international accreditation from Joint Commission International (JCI). It is evidenced that the sponsor had grew the revenue for its healthcare business at a solid CAGR of 52.7% from FY2008 (S$126mn) to FY2012 (S$685mn). 4) Strong potential for organic and inorganic DPU growth: 95.4% of the service fee is contributed from the 11 RHT clinical establishments which provide stability while upside potential can come from the development of greenfield clinical establishments. In addition, the two-tier fee structures (with long 15 years term and an option to extend another 15 years on mutual agreement), base and variable fees, present organic growth potential through annual increase of 3% on the base fee while the variable fee is tied to the 7.5% of underlying asset’s operating revenues.

Religare Health Trust Singapore Equities Research 16 October 2012

3 of 12

On the inorganic front, the Indian healthcare market is highly fragmented, with close to 95% of private hospitals being standalone according to Frost and Sullivan. All these smaller hospitals could represent potential acquisition opportunities for RHT. Besides that, RHT has been granted a right of first refusal (ROFR) for any proposed offer by the sponsor. Risk factors Currency translation risks RHT’s revenue and distribution are reported and distributed in Singapore dollars and hence weak Indian Rupee is an earnings risk. Net asset value of RHT will also be adversely affected due to Singapore dollar appreciation. Forward contracts are however put in place to hedge 100% against the currency risks for forecast year 2013 and the projection year 2014. Increasing competition in healthcare industry The healthcare industry remains highly competitive despite significant supply gap in healthcare facilities in India. RHT faces competition from major players such as Apollo hospitals and Manipal Hospitals and, to a lesser extent, government-owned hospital, smaller private hospital groups and new entrants. Challenges in employment To recruit, attract and retain skilled medical staffs is of a major challenge in India healthcare industry with density of doctors and nurses being significantly below the global average in accordance to Frost and Sullivan. In order to retain the employees, various opportunities such as secondments are provided to them to equip a broad overview of the medical and healthcare services. This kind of career development opportunities enhances employees’ business knowledge beyond their core technical expertise. In addition, revenue-sharing for some doctors should also help to attract and retain talent. Geographical concentration The initial portfolio is located in India, which exposes RHT to geographic concentration risks. RHT’s hospital occupancy can fall in the event of downturn in India’s healthcare sector, and therefore adversely impact RHT’s revenue and depreciation in property value of RHT’s portfolio. This in turn affects the RHT’s operations and ability to make distribution. Management Chief Executive Officer: Mr Ravi Mehrotra Prior experience:

Managing Director and Global Head, Retail & Intermediary Channels, PineBridge Investments (Hong Kong)

Managing Director, AIG Investments (Hong Kong) President, Franklin Templeton Asset Management

(India)

Qualification: Bachelors of Commerce, University of Mumbai Post Graduate Diploma in Business Management,

Xavier Labour Relations Institute of Jamshedpur (India)

Chief Financial Officer: Mr Pawanpreet Singh Prior experience:

Corporate Controller of Finance, Fortis Chief Financial Officer, Super Religare Laboratories

Limited Deputy General Manager of Accounts, Ballarpur

Industries Limited Qualification:

Bachelor of Commerce, Punjab University, Chandigarh

Chartered Accountant Holder, Institute of Chartered Accountants of India

Head of Strategy: Mr Gurpreet Singh Dhillon Prior experience:

Board of Directors, Religare Capital Markets (London)

Qualification: Bachelor of Laws, University of Essex

Head of Compliance/Investor Relations: Ms Tan Suan Hui Prior experience:

Vice President, Business Development in the Listings Department, SGX-ST

Qualification: Bachelor of Business Administration, National

University of Singapore Peer comparison Ascendas India Trust (a-iTrust), Parkway Life REIT (PLife REIT) and First REIT are used for the peer comparison because of some commonalities with RHT in terms of the trust vehicle, investment focus, industry and the geographical location of property assets. Within the peers, a-iTrust is the closest comparable in our view as both are structured as business trust with exposure in India, and thus sharing the related market risks and trust regulation. Amongst the four trusts, RHT has the lowest gearing ratio (6.1%, assuming S$50m debt) than the rest, implying better inorganic growth prospect through acquisitions and developments. Given the RHT’s target gearing of 30%-40%, about S$250mn to S$400mn of debt headroom could be deployed to finance the capital expenditures (S$82.2mn estimated by the RHT) for the four greenfield developments. The excess balance could be expended in acquiring the pipeline of ROFR properties span across India, Singapore and Vietnam. Fig.5. Right of first refusal property assets Country Hospital Licensed bedsIndia Escorts Okha 289Singapore Fortis Colorectal 31Vietnam Hoan My Saigon Phan Xich Long 200Vietnam Hoan My Da Nang 200Vietnam Hoan My Can Tho 150Vietnam Hoan My Da Lat 200Vietnam Hoan My Minh Hai 50

1120Total Source: Trust and PSR

Religare Health Trust Singapore Equities Research 16 October 2012

4 of 12

RHT’s management fee % to distributable income (based on forecast period 2013) of 11.1% is the lowest of the three comparables. This could be due to the performance fees being tied to the distributable income instead of the net property income which are typically employed by most of the S-REITs. On the valuation, RHT is priced at one time to book. The price of RHT appears inexpensive on the P/B basis relative to the rich P/B valuation of a-iTrust at 1.27 times which is way above its historical P/B mean of 0.83. From the yield angle, RHT stood out from the three comparables, offering c.9.0% yield including the distribution wavier (up to FY2014) compared to India 10-yr government bond yield of 8.1%. Please note that this is based on 100% payout from the total distributable income committed by RHT up to FY2014. By stripping out the distribution wavier, the yield is around 6.5% which is lower than a-iTrust yield of 7.1%.

Religare Health Trust Singapore Equities Research 16 October 2012

5 of 12

Fig.6. Peer comparison table

Religare Health Trust Ascendas India Trust* Parkway Life REIT* First REIT*

Investment focusAsia, Australasia, global emerging

marketsIndia Asia-Pacific Asia

Industry Healthcare Business space Healthcare HealthcareGeographical breakdown by revenue

India (100%) India (100%)Singapore (62%),

Japan (38%)

Indonesia (91%),Singapore (5%),

South Korea (4%)

Sponsor Fortis Healthcare Ascendas Land International

IHH Lippo Karawaci

Current gearing (%) 6.1% (minimum offering price)

33.0% 36.4% 15.9%

Debt headroom (S$mn)** ~400 ~90 ~90 ~200

Mgmt fee % to distributable income 11.07 16.49 17.74 11.46

P / NAV*** 1.00 1.27 1.42 1.3012M annualised DPU yield ~9.0% (FY13) 7.1% (FY13) 4.9% (FY12) 7.5% (FY12)

** Based on allowable and comfortable gearing level: RHT (40%) , a-iTrust (40%), Plife REIT (40%) and First REIT (35%) ***Based on the indicative price for RHT and closing price on 12-Oct-12 for the other three.

*The above information is based on 2QCY12 Results

Source: Various Trusts and PSR

Religare Health Trust Singapore Equities Research 16 October 2012

6 of 12

Fig.7. Management fee comparison table

Religare Health Trust Parkway Life REIT Ascendas India Trust First REITVechicle Business Trust REIT Business Trust REIT

Base fee0.4% p.a. of trust property value

0.3% p.a. of value of deposited property

0.5% p.a. of trust property value

0.4% p.a. of value of deposited property

Performance fee 4.5% p.a.of distributable income

4.5% p.a of net property income

4.0% p.a. of net property income

5.0% p.a. of net property income

Trustee fee

0.03% p.a. of trust property value, subject to a min. of S$15,000 p.m.

Shall not exceed 0.03% p.a. of value of deposited asset, subject to minimum of S$10,000 p.m.

0.02% p.a. of trust property value

Not exceeding 0.1% per annum of value of deposited property. Actual fee to be determined from time to time.

Acquisition fee

0.5% of the acquisition price if that sponsor group has direct/indirect interest of more than 50%, or 1.0% of acquisition price for all other cases 1.0% of acquisition price 1.0% of acquisition price 1.0% of acquisition price

Divestment fee0.5% of the sale price of investment

0.5% of the sale price of investment

0.5% of the sale price of investment

0.5% of the sale price of investment

Development fee

2.0% of total project costs for undertaking a development project on behalf of RHT incurred

5.0% of capex if capex is <S$1m

3.0% of capex if capex is >S$1m

2.0% of the construction cost for development and redevelopment -

Source: Various Trusts and PSR

Religare Health Trust Singapore Equities Research 16 October 2012

7 of 12

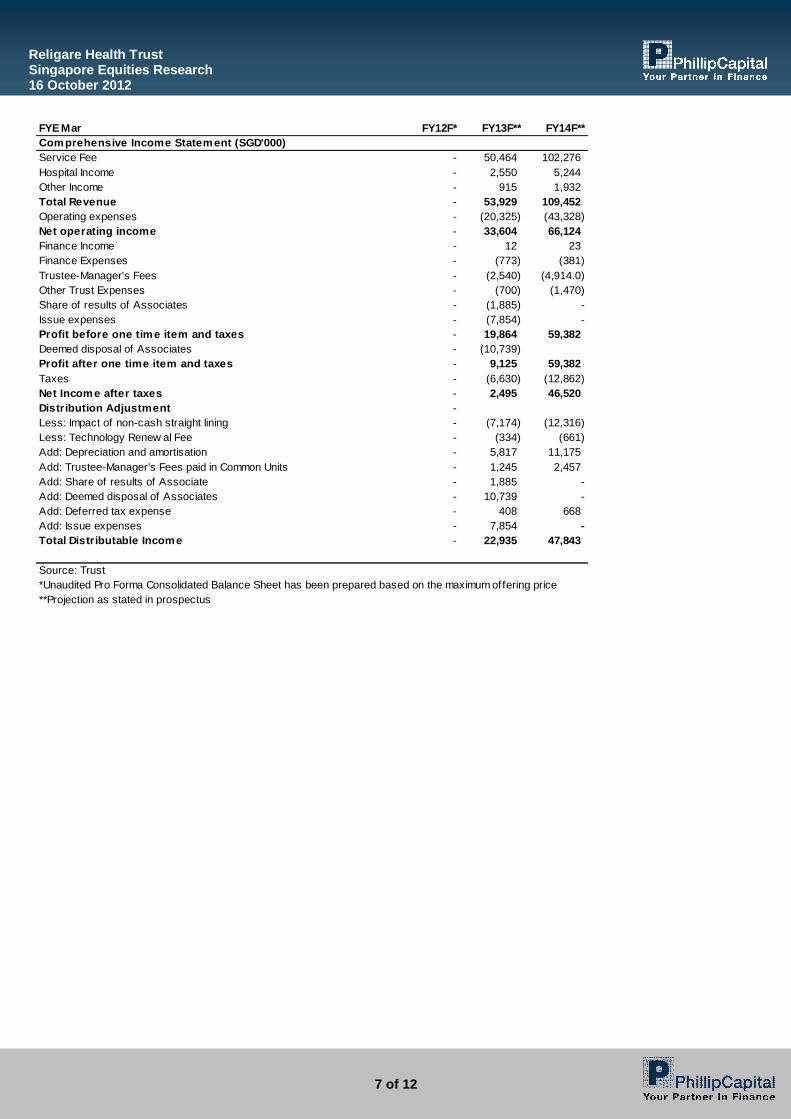

FYE Mar FY12F* FY13F** FY14F**Comprehensive Income Statement (SGD'000)Service Fee - 50,464 102,276Hospital Income - 2,550 5,244Other Income - 915 1,932Total Revenue - 53,929 109,452Operating expenses - (20,325) (43,328)Net operating income - 33,604 66,124Finance Income - 12 23Finance Expenses - (773) (381)Trustee-Manager's Fees - (2,540) (4,914.0)Other Trust Expenses - (700) (1,470)Share of results of Associates - (1,885) -Issue expenses - (7,854) -Profit before one time item and taxes - 19,864 59,382Deemed disposal of Associates - (10,739)Profit after one time item and taxes - 9,125 59,382Taxes - (6,630) (12,862)Net Income after taxes - 2,495 46,520Distribution Adjustment -Less: Impact of non-cash straight lining - (7,174) (12,316)Less: Technology Renew al Fee - (334) (661)Add: Depreciation and amortisation - 5,817 11,175Add: Trustee-Manager's Fees paid in Common Units - 1,245 2,457Add: Share of results of Associate - 1,885 -Add: Deemed disposal of Associates - 10,739 -Add: Deferred tax expense - 408 668Add: Issue expenses - 7,854 -Total Distributable Income - 22,935 47,843

Source: Trust *Unaudited Pro Forma Consolidated Balance Sheet has been prepared based on the maximum offering price**Projection as stated in prospectus

Religare Health Trust Singapore Equities Research 16 October 2012

8 of 12

FYE Mar FY12F* FY13F** FY14F**Balance Sheet (SGD'000)Property, plant and equipment 661,079 - -Intangibles 141,333 - -Investment in Associates - - -Deferred tax assets 1,686 - -Prepayments, deposits and other receivables 1,700 - -Total non-current assets 805,798 - -Inventories 306 - -Trade receivables 889 - -Current tax assets 6,230 - -Prepayments, deposits and other receivables 5,729 - -Cash and cash equivalents 79,009 - -Total current assets 92,163 - -Total Assets 897,961 - -Loans and borrow ings 4,865 - -Employee benef its liabilities 188 - -Other payables 3,264 - -Deferred tax liabilities 85,245Total non-current liabilities 93,562 - -Trade payables 3,256 - -Loans and borrow ings - - -Other payables 71,731 - -Total current liabilities 74,987 - -Total liabilities 168,549 - -Units in issue 563,068 - -Unit issue costs (20,169) - -Capital reserve 211,520 - -Retained earnings (25,007) - -Other reserves - - -Shareholder Equity 729,412 - -Source: Trust *Unaudited Pro Forma Consolidated Balance Sheet has been prepared based on the maximum offering price**Projection as stated in prospectus

Religare Health Trust Singapore Equities Research 16 October 2012

9 of 12

Important Information This publication is prepared by Phillip Securities Research Pte Ltd., 250 North Bridge Road, #06-00, Raffles City Tower, Singapore 179101 (Registration Number: 198803136N), which is regulated by the Monetary Authority of Singapore (“Phillip Securities Research”). By receiving or reading this publication, you agree to be bound by the terms and limitations set out below. This publication has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this document by mistake, please delete or destroy it, and notify the sender immediately. Phillip Securities Research shall not be liable for any direct or consequential loss arising from any use of material contained in this publication. The information contained in this publication has been obtained from public sources, which Phillip Securities Research has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this publication are based on such information and are expressions of belief of the individual author or the indicated source (as applicable) only. Phillip Securities Research has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete, appropriate or verified or should be relied upon as such. Any such information or Research contained in this publication is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the preparation or issuance of this report, (i) be liable in any manner whatsoever for any consequences (including but not limited to any special, direct, indirect, incidental or consequential losses, loss of profits and damages) of any reliance or usage of this publication or (ii) accept any legal responsibility from any person who receives this publication, even if it has been advised of the possibility of such damages. You must make the final investment decision and accept all responsibility for your investment decision, including, but not limited to your reliance on the information, data and/or other materials presented in this publication. Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this material are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this publication is not indicative of future results. This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This publication should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this publication has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this material is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this publication involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks. Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this research should take into account existing public information, including any registered prospectus in respect of such product. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this publication, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the

Religare Health Trust Singapore Equities Research 16 October 2012

10 of 12

preparation or issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this publication. Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment. To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold a interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this publication. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, which is not reflected in this material, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the preparation or issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this material. The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction. Section 27 of the Financial Advisers Act (Cap. 110) of Singapore and the MAS Notice on Recommendations on Investment Products (FAA-N01) do not apply in respect of this publication. This material is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this material may not be suitable for all investors and a person receiving or reading this material should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products. Please contact Phillip Securities Research at [65 65311240] in respect of any matters arising from, or in connection with, this document. This report is only for the purpose of distribution in Singapore.

Religare Health Trust Singapore Equities Research 16 October 2012

11 of 12

Contact Information (Singapore Research Team)

Chan Wai Chee Lee Kok Joo, CFA Joshua Tan CEO, Research Head of Research Macro Strategist

Special Opportunities S-Chips, Strategy Global Macro, Asset Strategy +65 6531 1231 +65 6531 1685 +65 6531 1249

[email protected] [email protected] [email protected]

Magdalene Choong, CFA Go Choon Koay, Bryan Derrick Heng Investment Analyst Investment Analyst Investment Analyst

Gaming, US Property Transportation, Telecom. +65 6531 1791 +65 6531 1792 +65 6531 1221

[email protected] [email protected] [email protected]

Ken Ang Travis Seah Ng Weiwen Investment Analyst Investment Analyst Macro Analyst

Financials REITS Global Macro, Asset Strategy +65 6531 1793 +65 6531 1229 +65 6531 1735

[email protected] [email protected] [email protected]

Roy Chen Nicholas Ong Research Assistant Macro Analyst Investment Analyst General Enquiries

Global Macro, Asset Strategy Commodities +65 6531 1240 (Phone) +65 6531 1535 +65 6531 5440 [email protected]

Religare Health Trust Singapore Equities Research 16 October 2012

12 of 12

Contact Information (Regional Member Companies)

SINGAPORE

Phillip Securities Pte Ltd Raffles City Tower

250, North Bridge Road #06-00 Singapore 179101

Tel : (65) 6533 6001 Fax : (65) 6535 6631

Website: www.poems.com.sg

MALAYSIA

Phillip Capital Management Sdn Bhd B-3-6 Block B Level 3 Megan Avenue II, No. 12, Jalan Yap Kwan Seng, 50450

Kuala Lumpur Tel (603) 21628841 Fax (603) 21665099

Website: www.poems.com.my

HONG KONG Phillip Securities (HK) Ltd

Exchange Participant of the Stock Exchange of Hong Kong 11/F United Centre 95 Queensway

Hong Kong Tel (852) 22776600 Fax (852) 28685307

Websites: www.phillip.com.hk

JAPAN

Phillip Securities Japan, Ltd. 4-2 Nihonbashi Kabuto-cho Chuo-ku,

Tokyo 103-0026 Tel (81-3) 3666-2101 Fax (81-3) 3666-6090

Website:www.phillip.co.jp

INDONESIA

PT Phillip Securities Indonesia ANZ Tower Level 23B,

Jl Jend Sudirman Kav 33A Jakarta 10220 – Indonesia

Tel (62-21) 57900800 Fax (62-21) 57900809

Website: www.phillip.co.id

CHINA

Phillip Financial Advisory (Shanghai) Co. Ltd No 550 Yan An East Road,

Ocean Tower Unit 2318, Postal code 200001

Tel (86-21) 51699200 Fax (86-21) 63512940

Website: www.phillip.com.cn

THAILAND Phillip Securities (Thailand) Public Co. Ltd

15th Floor, Vorawat Building, 849 Silom Road, Silom, Bangrak,

Bangkok 10500 Thailand Tel (66-2) 6351700 / 22680999

Fax (66-2) 22680921 Website www.phillip.co.th

FRANCE

King & Shaxson Capital Limited 3rd Floor, 35 Rue de la Bienfaisance 75008

Paris France Tel (33-1) 45633100 Fax (33-1) 45636017

Website: www.kingandshaxson.com

UNITED KINGDOM

King & Shaxson Capital Limited 6th Floor, Candlewick House,

120 Cannon Street, London, EC4N 6AS

Tel (44-20) 7426 5950 Fax (44-20) 7626 1757

Website: www.kingandshaxson.com

UNITED STATES

Phillip Futures Inc 141 W Jackson Blvd Ste 3050

The Chicago Board of Trade Building Chicago, IL 60604 USA

Tel +1.312.356.9000 Fax +1.312.356.9005

AUSTRALIA

Octa Phillip Securities Ltd Level 12, 15 William Street,

Melbourne, Victoria 3000, Australia Tel (03) 9629 8288 Fax (03) 9629 8882

Website: www.octaphillip.com