Embed Size (px)

Citation preview

WHAT’S AHEADFOR

COMMODITY PRICES &

FARMLAND VALUES

Remarks by Mark PearsonIndependent Community Bankers

Nashville, TennesseeMarch 12, 2012

Back in Production…Any Way Possible

Source: Matt Leavitt

10-Year Corn Prices

Source: NASS

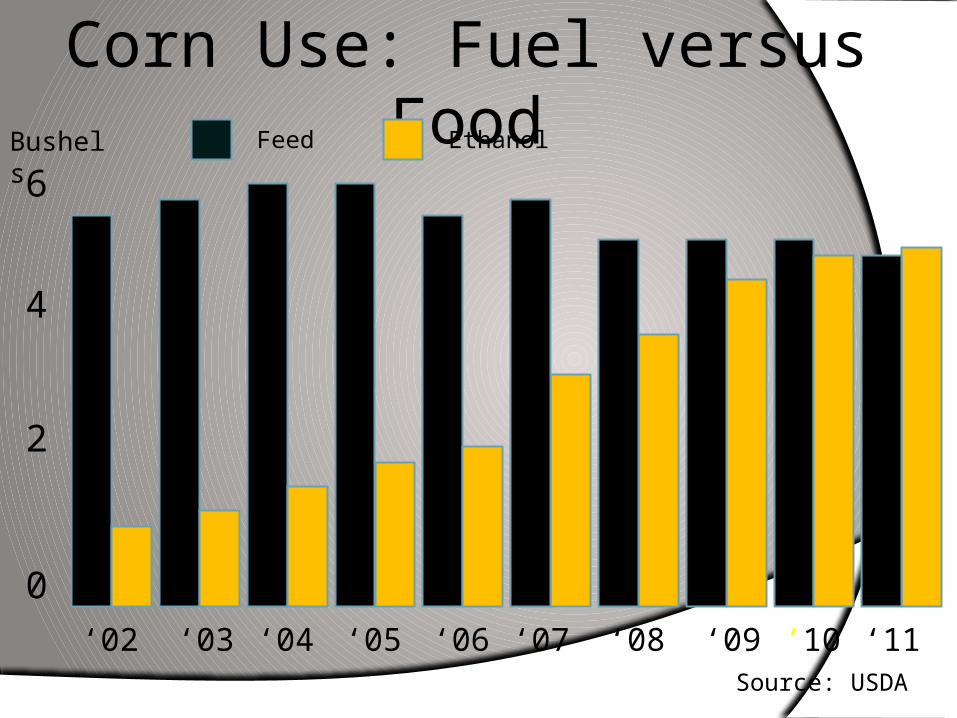

Corn Use: Fuel versus Food

Source: USDA

‘02

EthanolFeed

6

4

2

0

Bushels

‘03 ‘05‘04 ‘06 ‘08‘07 ‘09 ‘10 ‘11

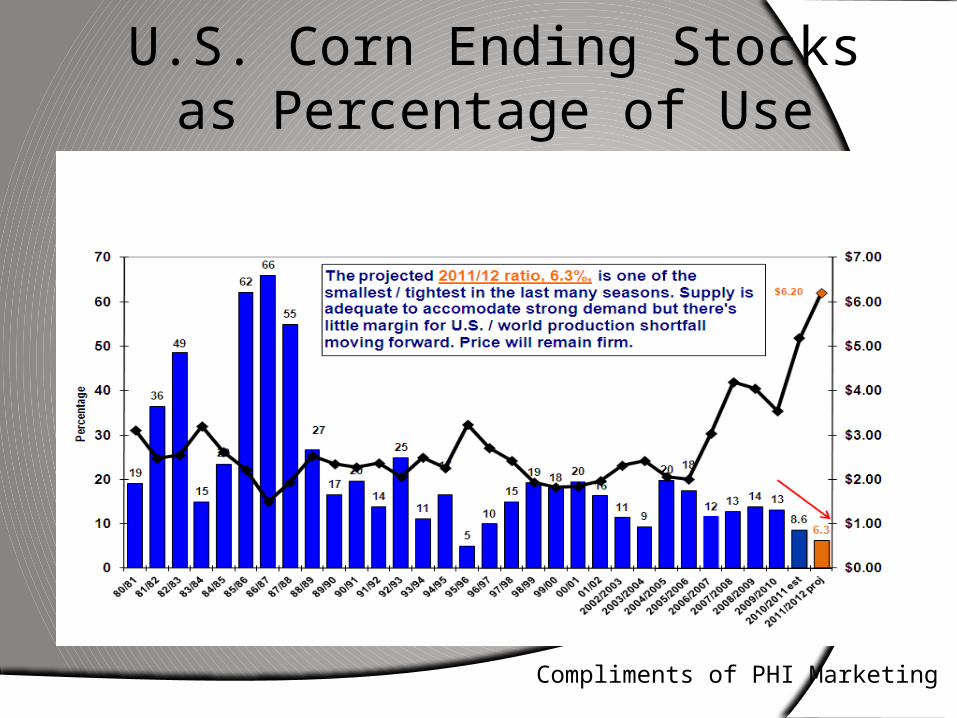

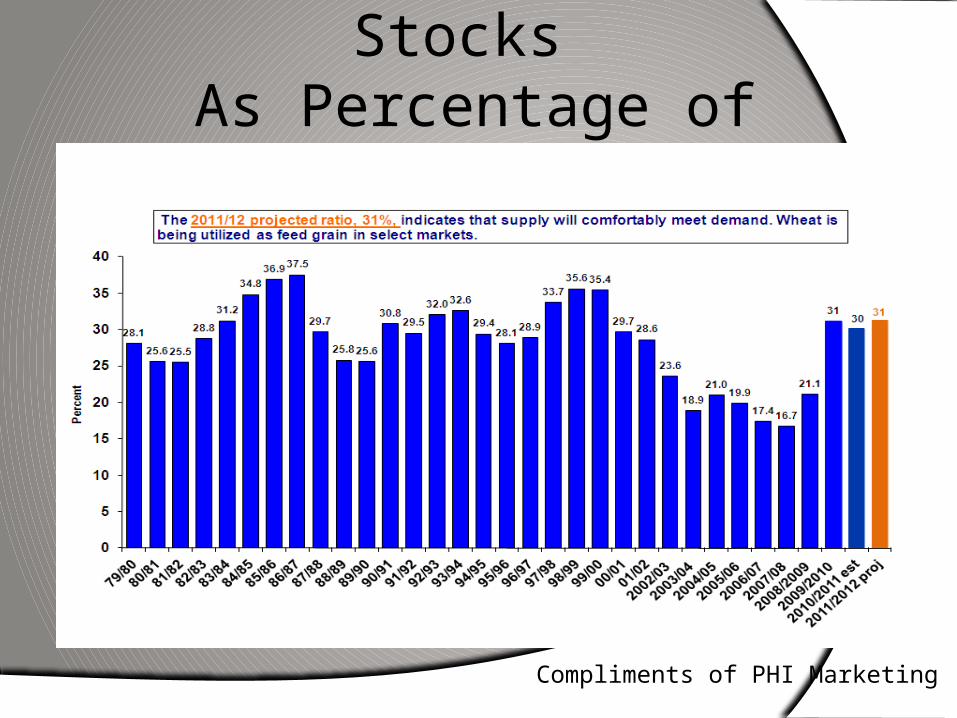

U.S. Corn Ending Stocksas Percentage of Use

Compliments of PHI Marketing

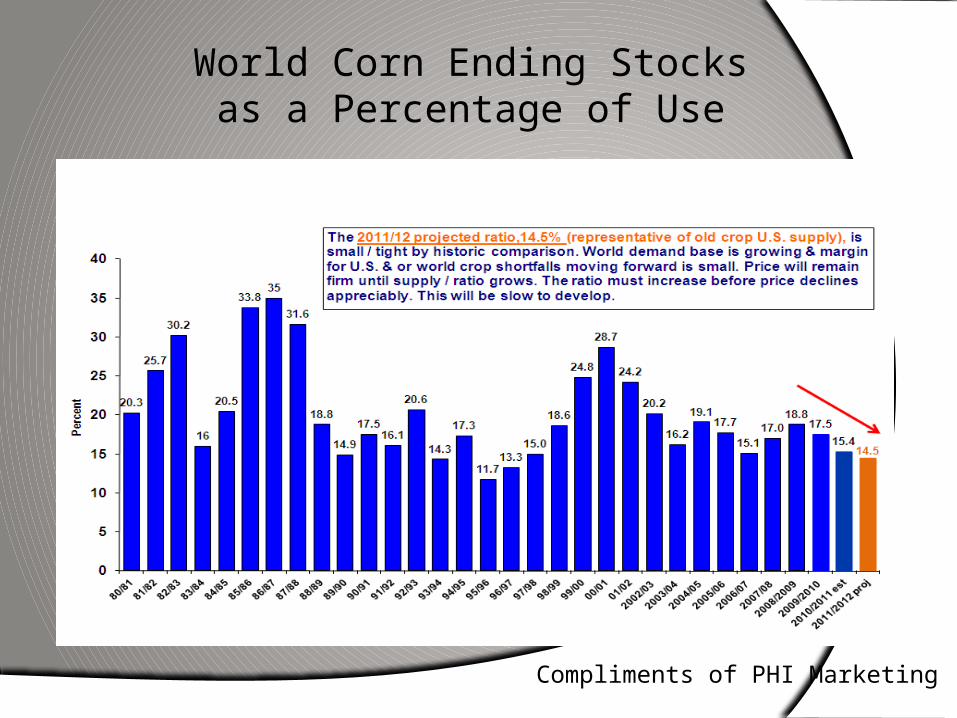

World Corn Ending Stocksas a Percentage of Use

Compliments of PHI Marketing

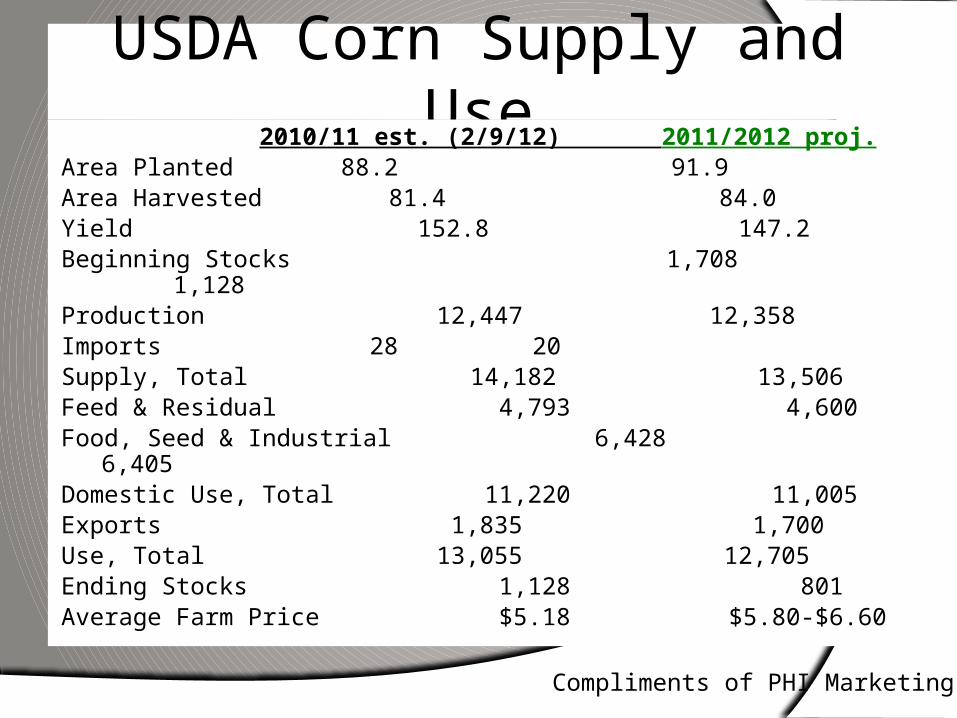

USDA Corn Supply and Use 2010/11 est. (2/9/12) 2011/2012 proj.

Area Planted 88.2 91.9Area Harvested 81.4 84.0Yield 152.8 147.2Beginning Stocks 1,708 1,128Production 12,447 12,358Imports 28 20Supply, Total 14,182 13,506Feed & Residual 4,793 4,600Food, Seed & Industrial 6,428 6,405Domestic Use, Total 11,220 11,005Exports 1,835 1,700Use, Total 13,055 12,705Ending Stocks 1,128 801Average Farm Price $5.18 $5.80-$6.60

Compliments of PHI Marketing

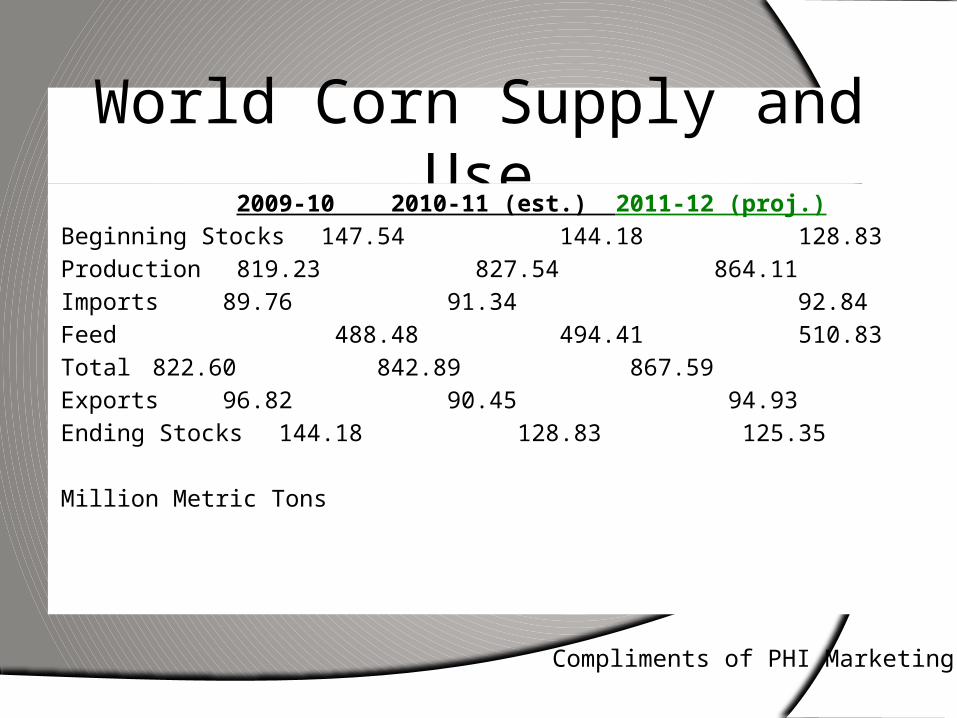

World Corn Supply and Use 2009-10 2010-11 (est.) 2011-12 (proj.)

Beginning Stocks 147.54 144.18 128.83

Production 819.23 827.54 864.11

Imports 89.76 91.34 92.84

Feed 488.48 494.41 510.83

Total 822.60 842.89 867.59

Exports 96.82 90.45 94.93

Ending Stocks 144.18 128.83 125.35

Million Metric Tons

Compliments of PHI Marketing

May ’12 Corn

Source: CBOT

December ’12 Corn

Source: CBOT

Light Sweet Crude Oil

Source: NYMEX

10-Year Soybean Prices

Source: NASS

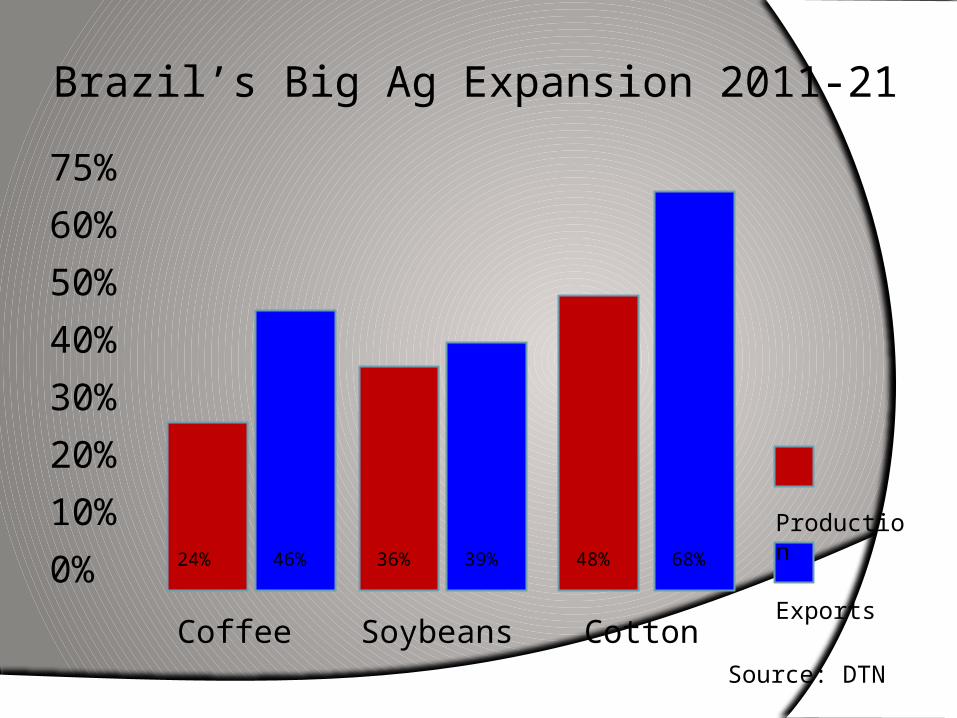

Brazil’s Big Ag Expansion 2011-21

Source: DTN

75%

60%

50%

40%

30%

20%

10%

0%

Coffee Soybeans CottonExports

Production

24% 46% 36% 39% 48% 68%

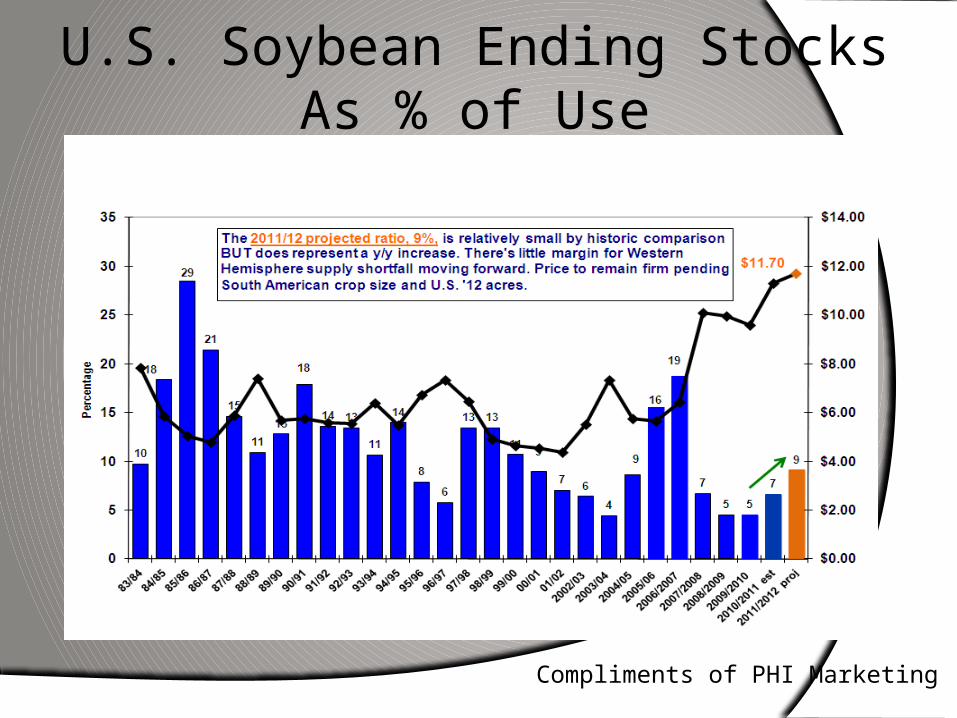

U.S. Soybean Ending Stocks As % of Use

Compliments of PHI Marketing

World Soybean Ending Stocks

as Percentage of Use

Compliments of PHI Marketing

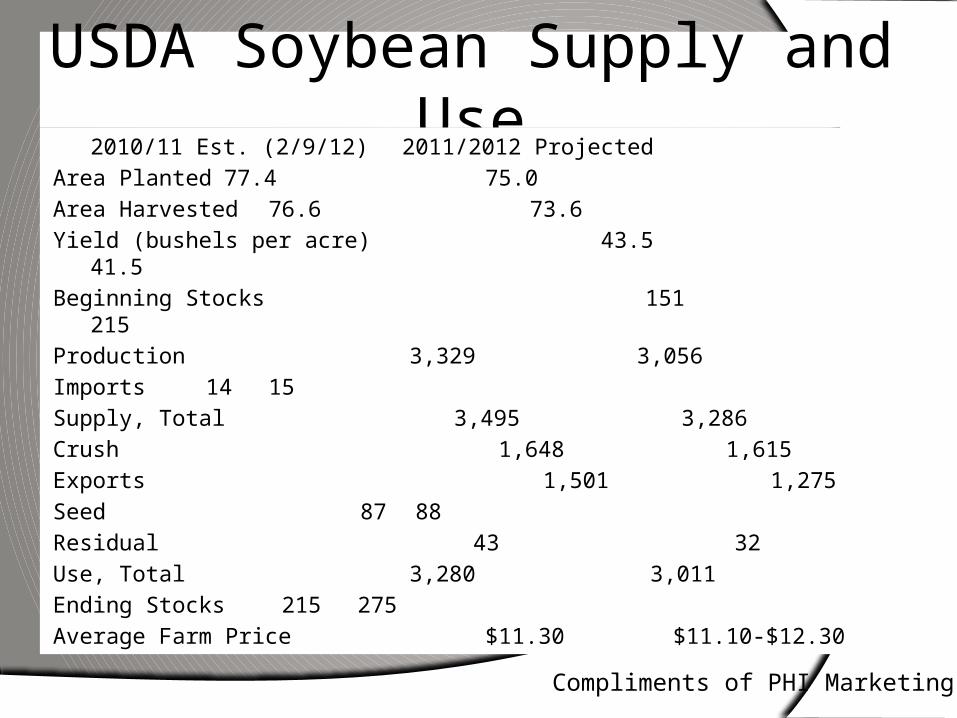

USDA Soybean Supply and Use

2010/11 Est. (2/9/12) 2011/2012 Projected

Area Planted 77.4 75.0

Area Harvested 76.6 73.6

Yield (bushels per acre) 43.5 41.5

Beginning Stocks 151 215

Production 3,329 3,056

Imports 14 15

Supply, Total 3,495 3,286

Crush 1,648 1,615

Exports 1,501 1,275

Seed 87 88

Residual 43 32

Use, Total 3,280 3,011

Ending Stocks 215 275

Average Farm Price $11.30 $11.10-$12.30

Compliments of PHI Marketing

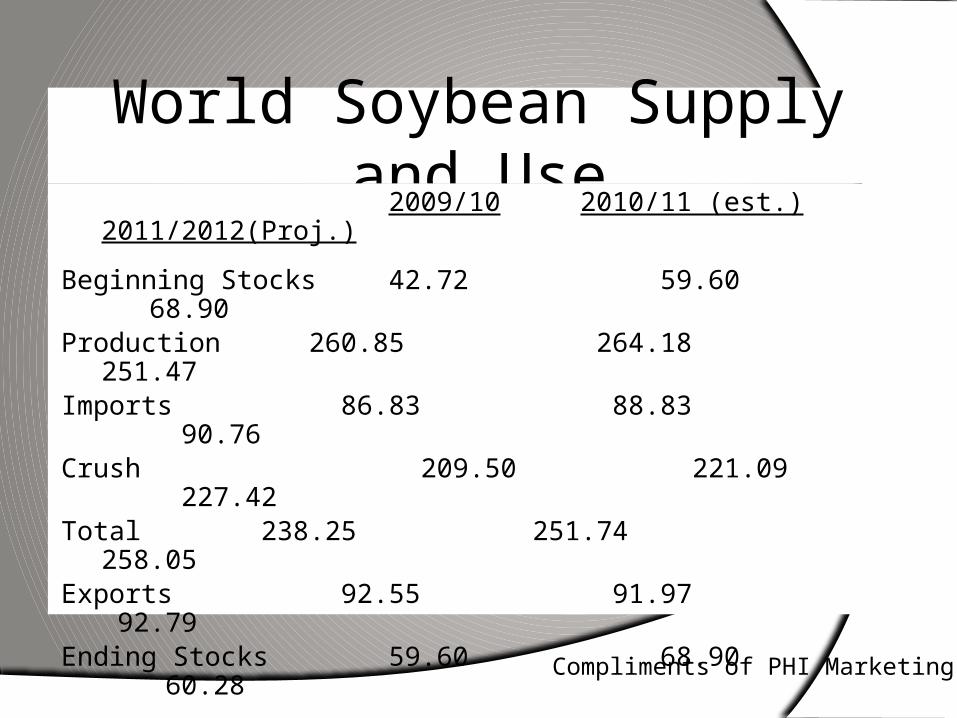

World Soybean Supply and Use 2009/10 2010/11 (est.)

2011/2012(Proj.)

Beginning Stocks 42.72 59.60 68.90Production 260.85 264.18 251.47Imports 86.83 88.83 90.76Crush 209.50 221.09 227.42Total 238.25 251.74 258.05Exports 92.55 91.97 92.79Ending Stocks 59.60 68.90 60.28

Million Metric Tons

Compliments of PHI Marketing

May ’12 Soybeans

Source: CBOT

November ’12 Soybeans

Source: CBOT

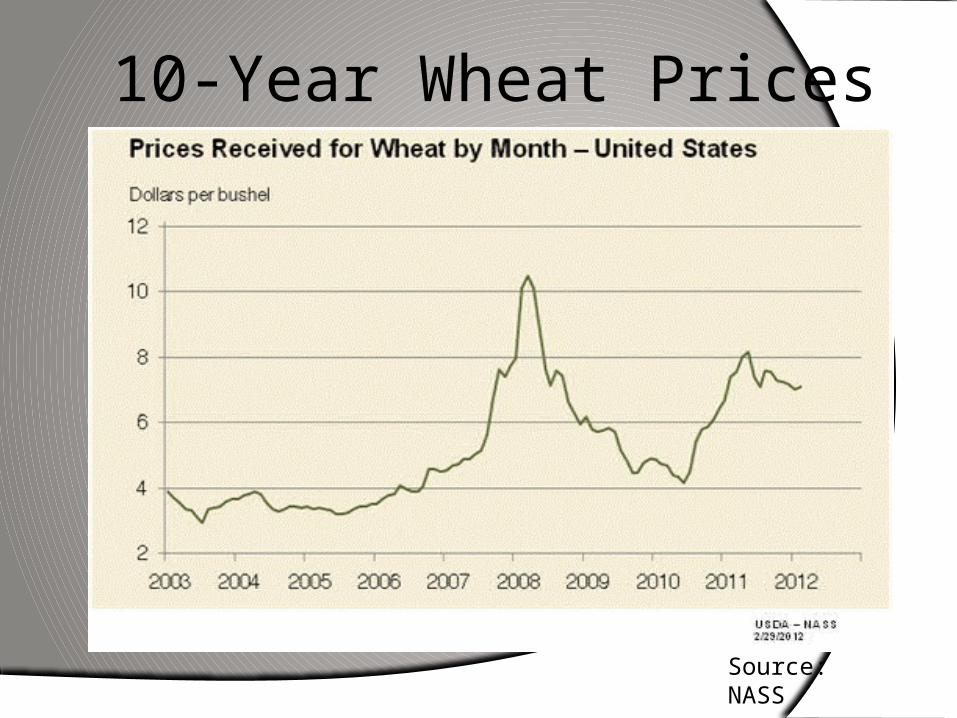

10-Year Wheat Prices

Source: NASS

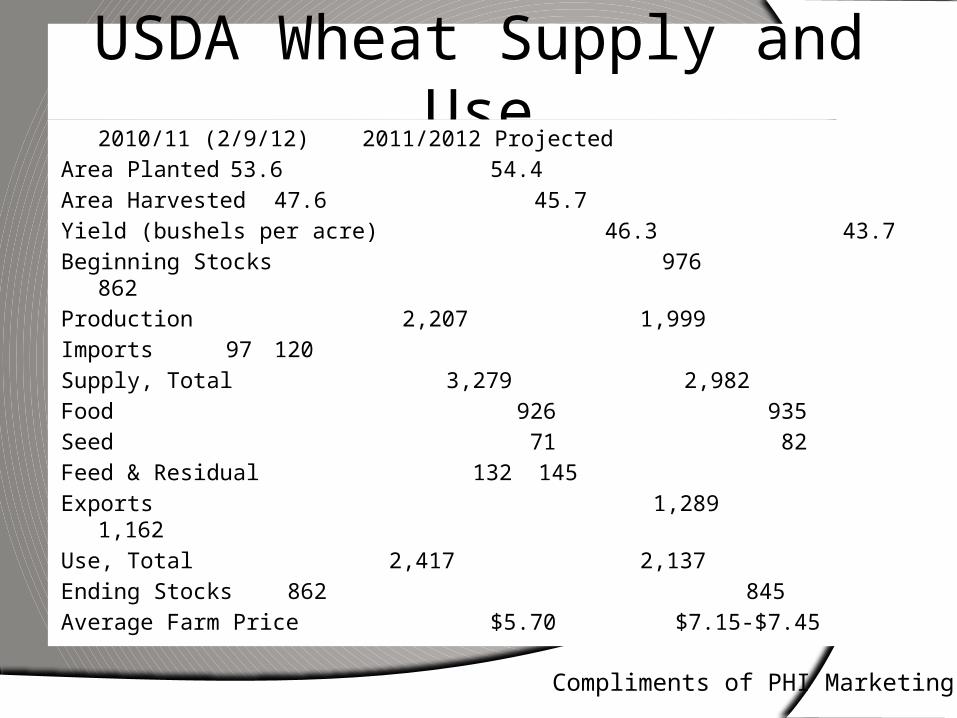

USDA Wheat Supply and Use

2010/11 (2/9/12) 2011/2012 Projected

Area Planted 53.6 54.4

Area Harvested 47.6 45.7

Yield (bushels per acre) 46.3 43.7

Beginning Stocks 976 862

Production 2,207 1,999

Imports 97 120

Supply, Total 3,279 2,982

Food 926 935

Seed 71 82

Feed & Residual 132 145

Exports 1,289 1,162

Use, Total 2,417 2,137

Ending Stocks 862 845

Average Farm Price $5.70 $7.15-$7.45

Compliments of PHI Marketing

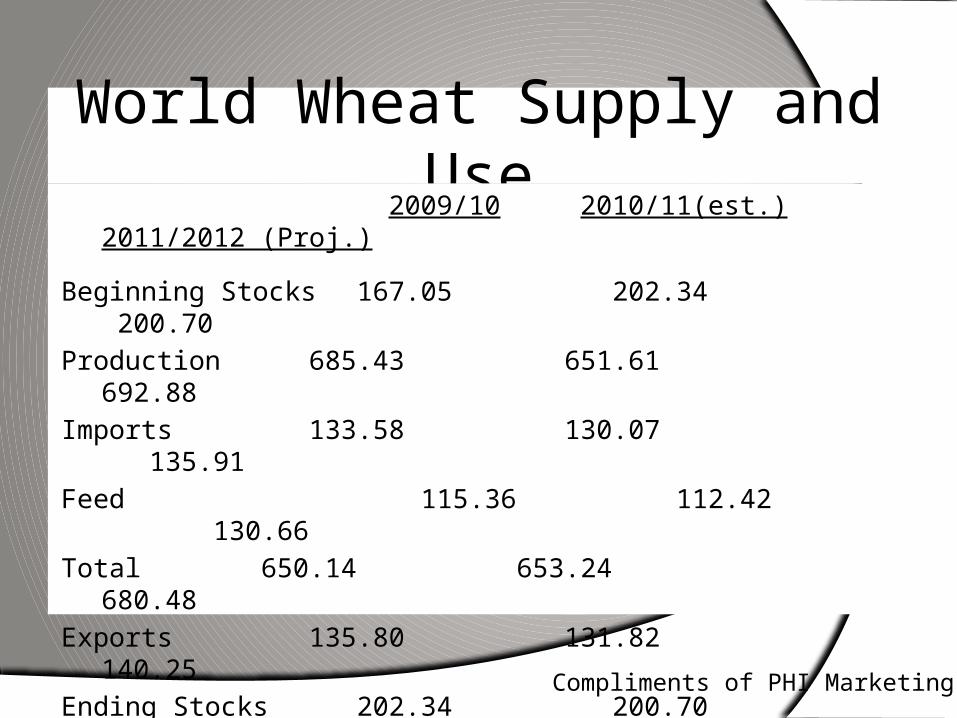

World Wheat Supply and Use

2009/10 2010/11(est.) 2011/2012 (Proj.)

Beginning Stocks 167.05 202.34 200.70

Production 685.43 651.61 692.88

Imports 133.58 130.07 135.91

Feed 115.36 112.42 130.66

Total 650.14 653.24 680.48

Exports 135.80 131.82 140.25

Ending Stocks 202.34 200.70 213.10

Million Metric Tons

Compliments of PHI Marketing

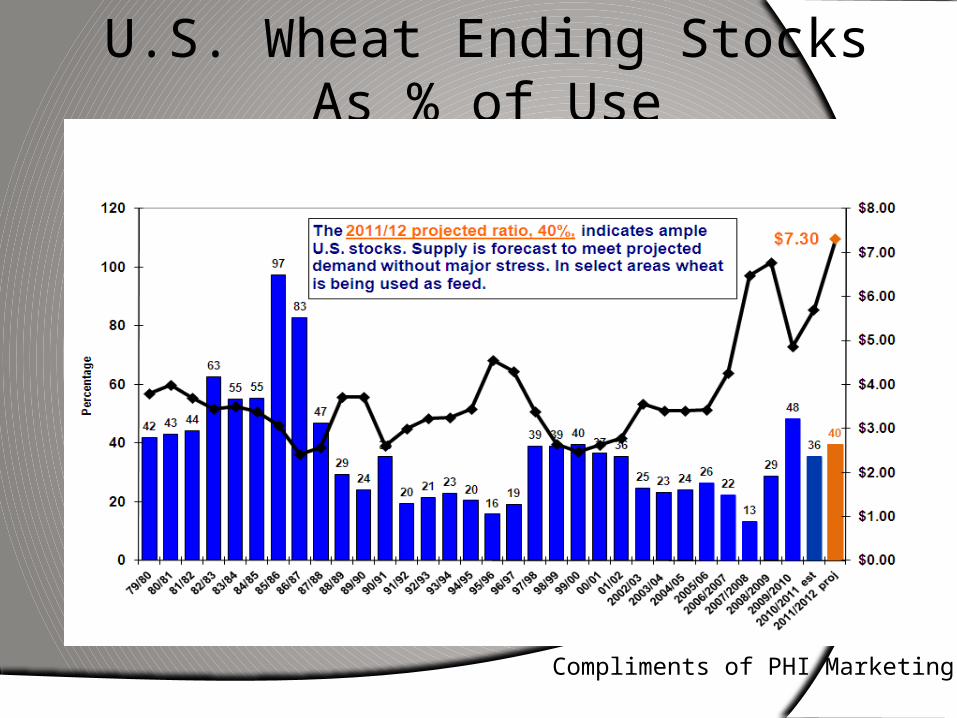

U.S. Wheat Ending Stocks As % of Use

Compliments of PHI Marketing

World Wheat Ending Stocks

As Percentage of Use

Compliments of PHI Marketing

May ’12 Chicago Wheat

Source: CBOT

December ’12 Chicago Wheat

Source: CBOT

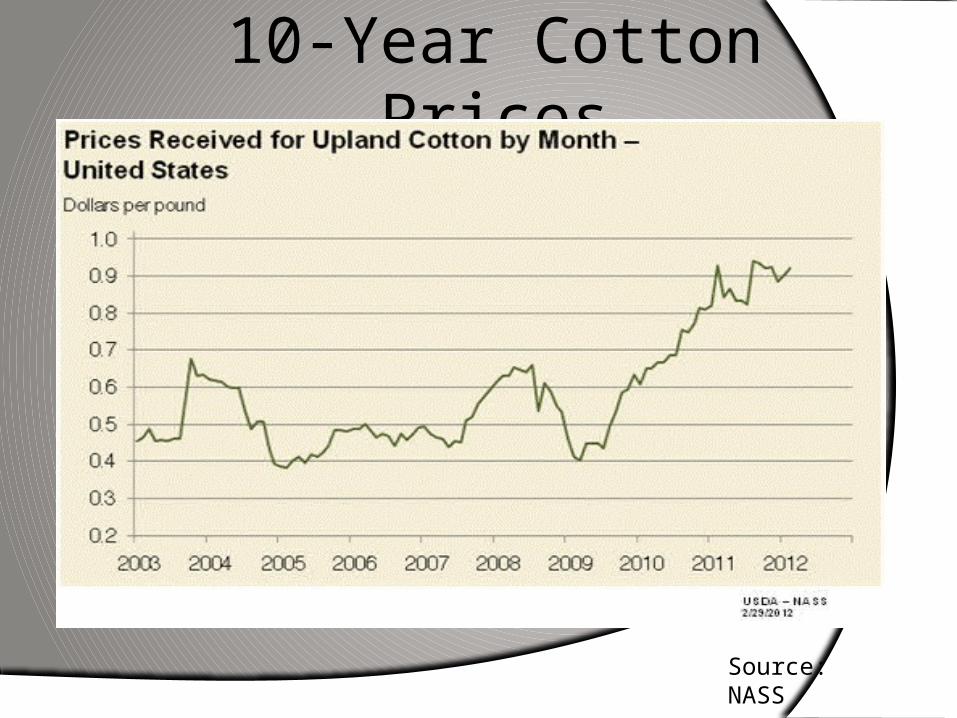

10-Year Cotton Prices

Source: NASS

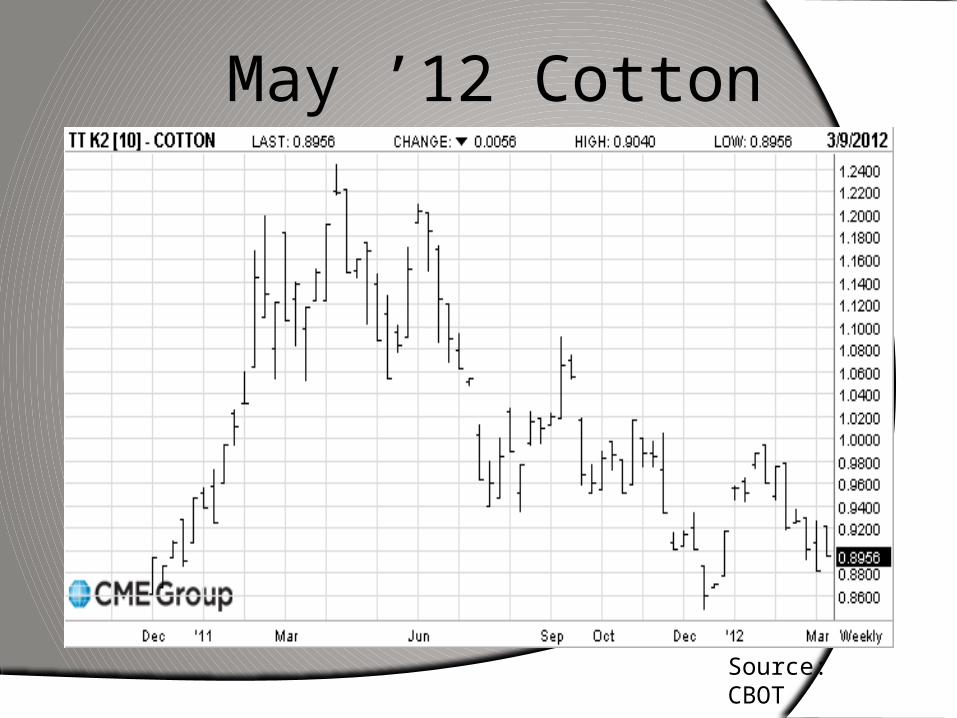

May ’12 Cotton

Source: CBOT

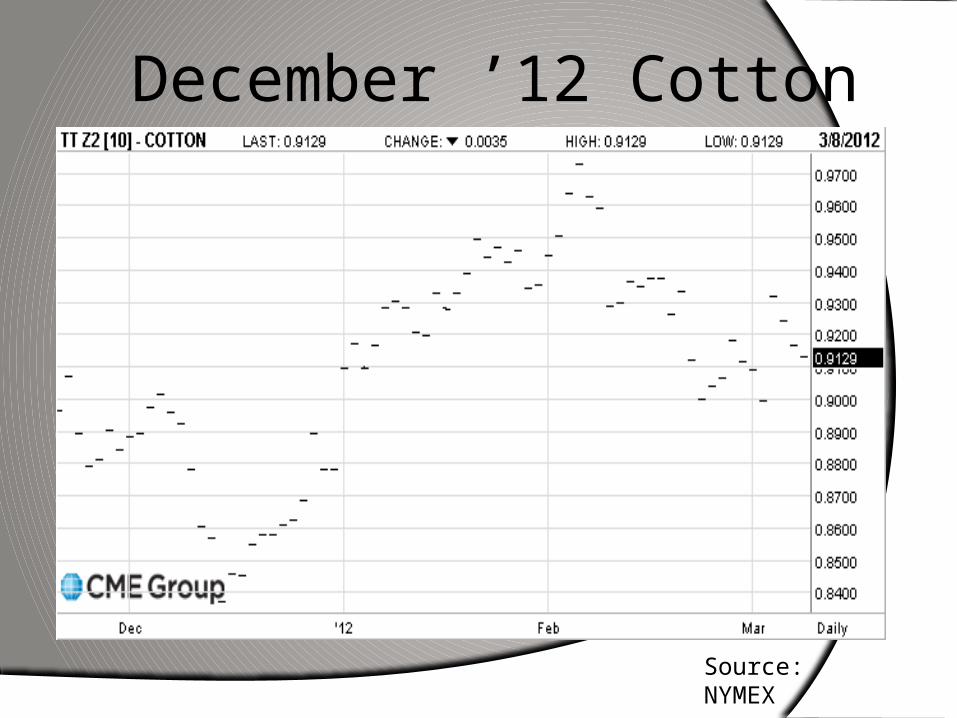

December ’12 Cotton

Source: NYMEX

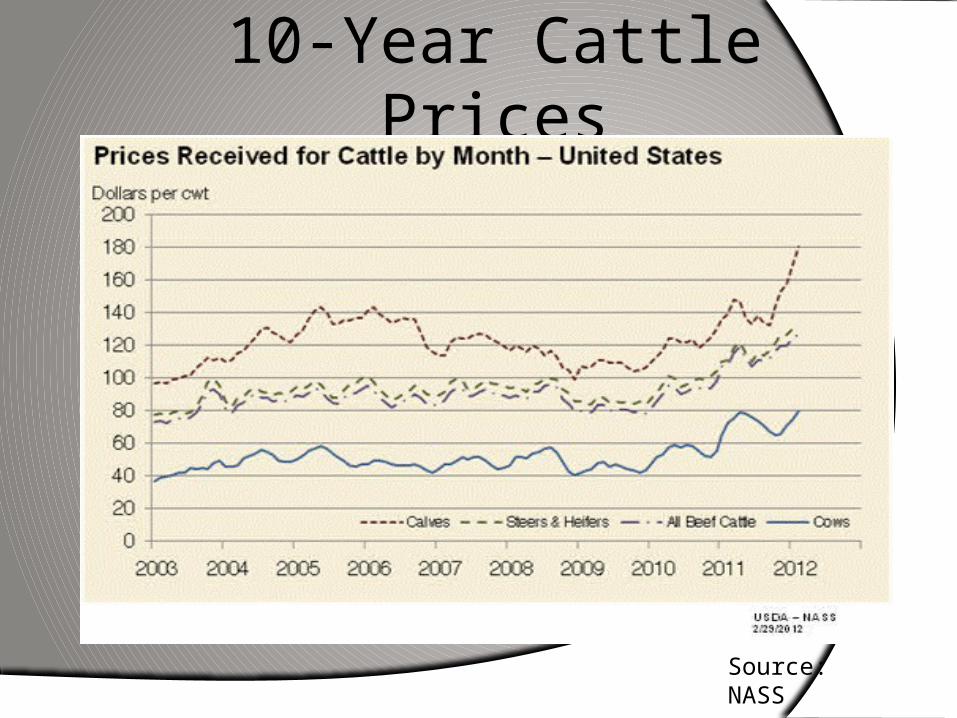

10-Year Cattle Prices

Source: NASS

April ’12 Live Cattle

Source: CBOT

December ’12 Live Cattle

Source: CBOT

April ’12 Feeder Cattle

Source: CBOT

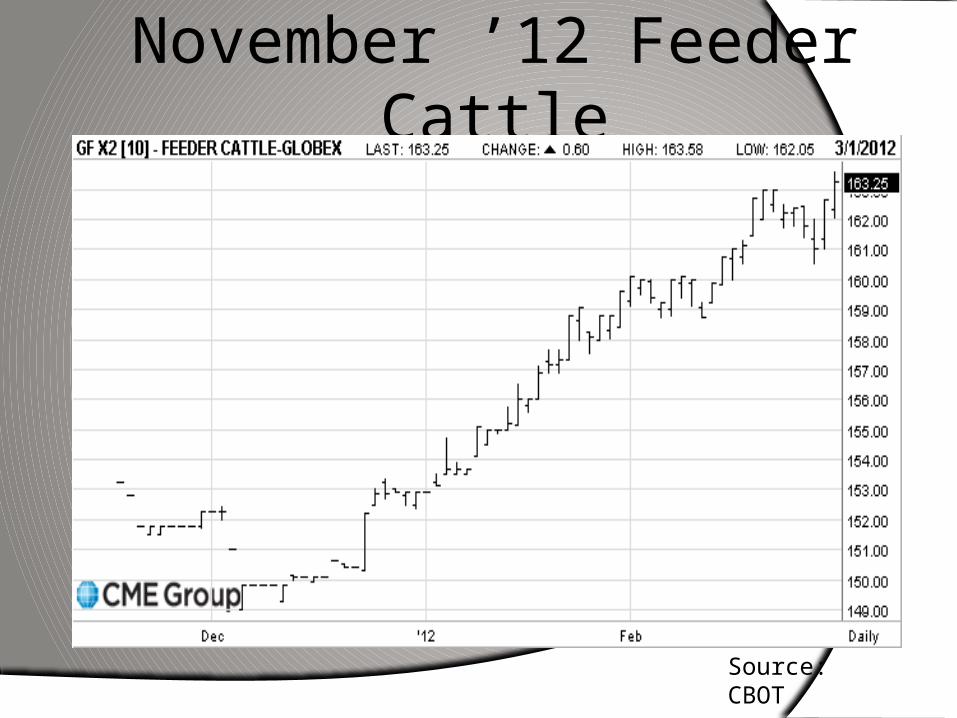

November ’12 Feeder Cattle

Source: CBOT

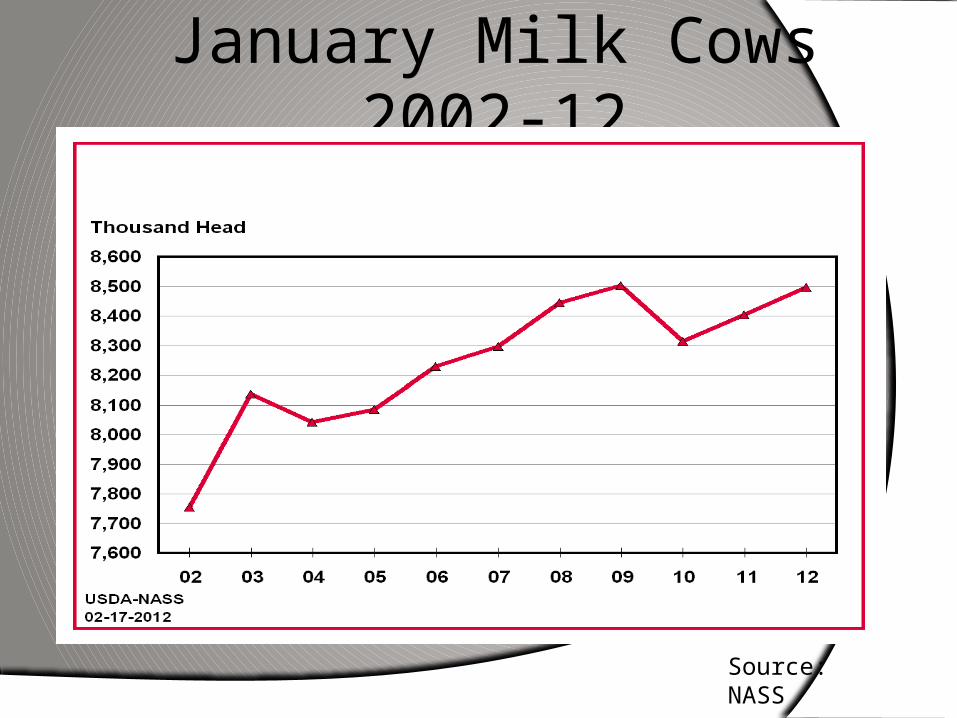

January Milk Cows 2002-12

Source: NASS

April ’12 Class III Milk

Source: CBOT

December ’12 Class III Milk

Source: CBOT

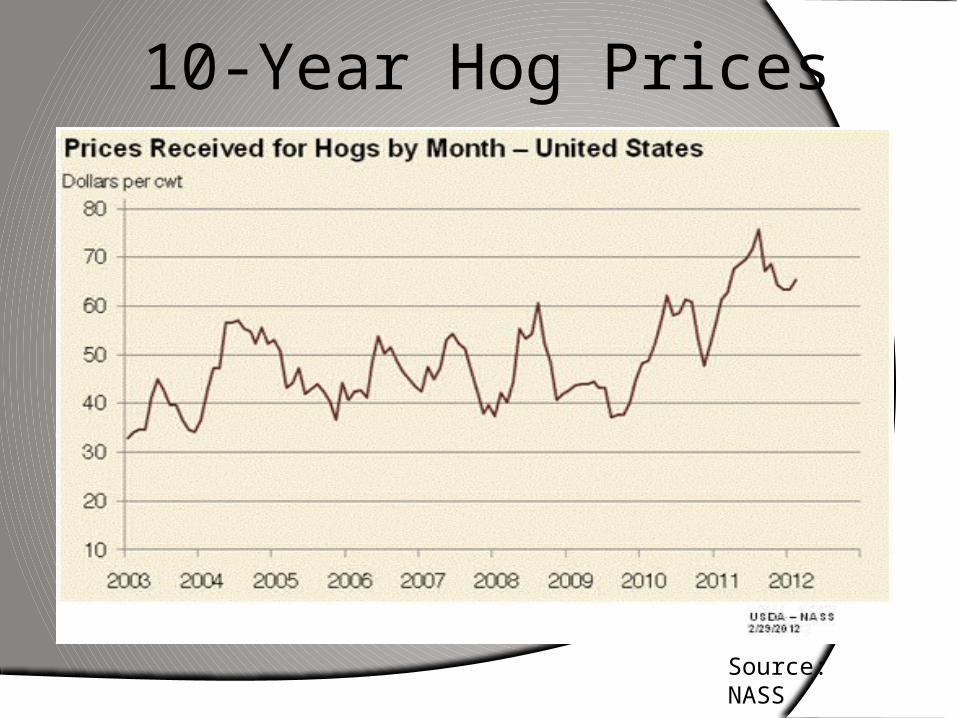

10-Year Hog Prices

Source: NASS

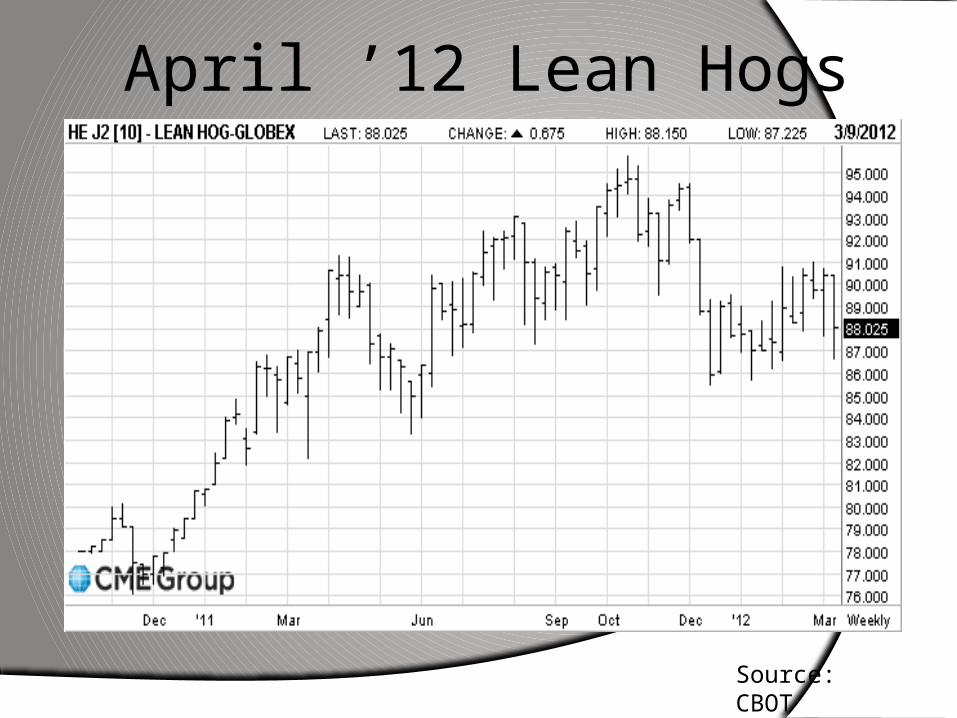

April ’12 Lean Hogs

Source: CBOT

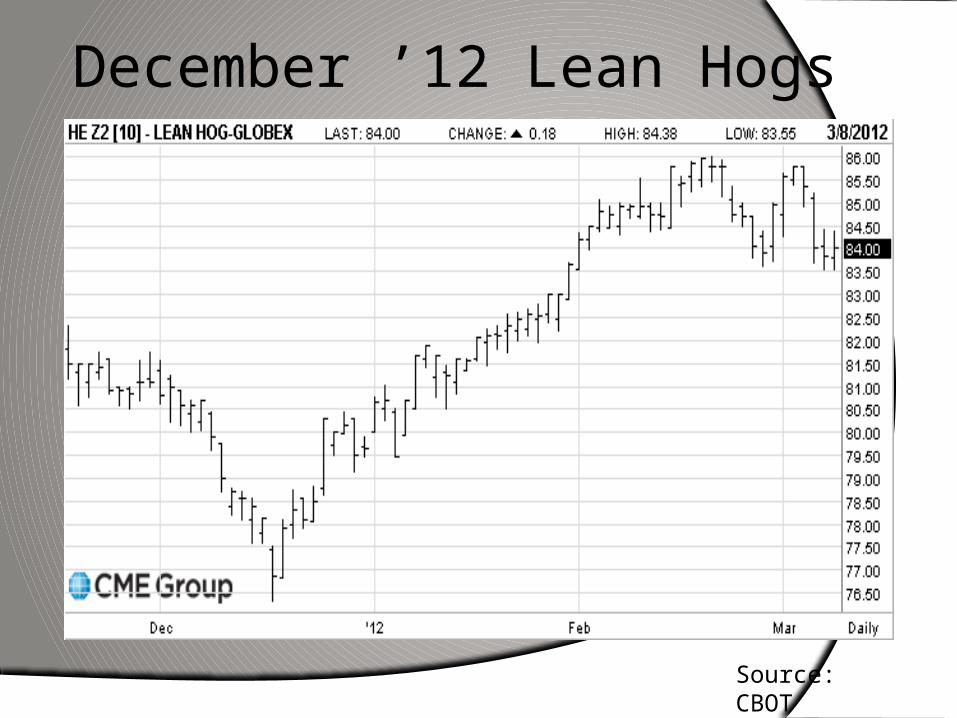

December ’12 Lean Hogs

Source: CBOT

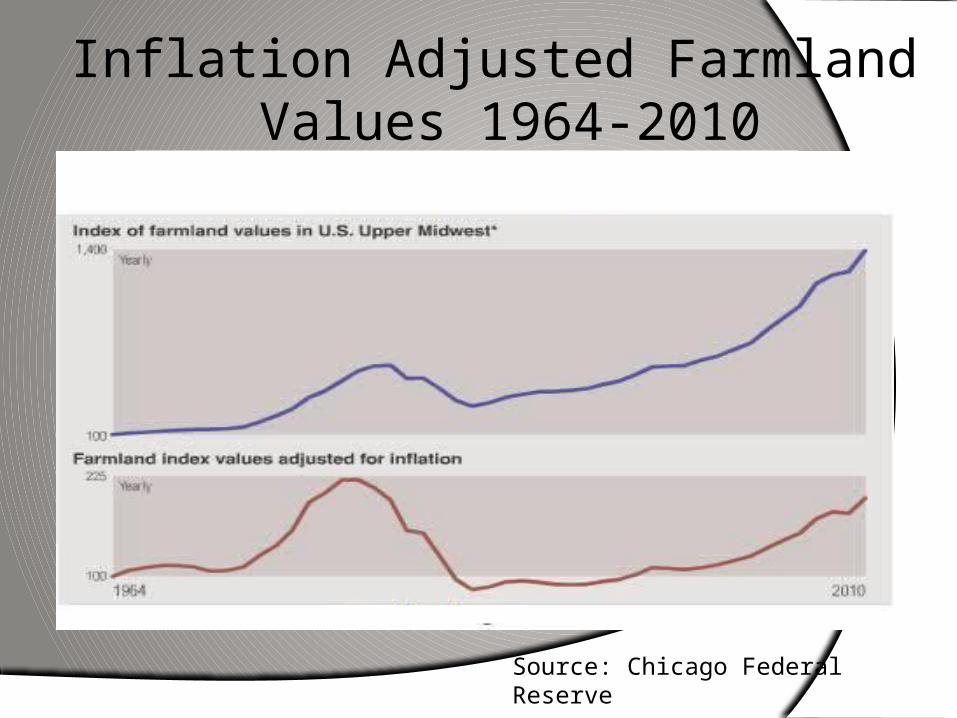

Inflation Adjusted Farmland Values 1964-2010

Source: Chicago Federal Reserve

• Recovering economy• Demographics will drive ag/food product demand• Next world industrial expansion: Africa• U.S. continues to be ag technology leader• U.S., China will drive African development• Infrastructure build-out continues in South America• ‘Youth bulge’ means growth in Middle East, but continued destabilization following Arab Spring• What’s this mean for you: Continued strong demand for U.S. agricultural commodities

Globally Local World: What’s Ahead