Embed Size (px)

Citation preview

RemoteArea

Benefits

February 2006

Taxation Education for Government Agencies

Remote Area Benefits FBT 2006

Introduction ........ ........ ........ ................. ........ ........ ....... ........ ........ ........ ........ ......... ........ ........ ........ 2Housing fringe benefits - generally........ ........ ........ ........ ........ ........ ......... ............... ........ ........ ....... 2

What is a housing benefit? ........ ........ ........ ................ ........ ........ ........ ........ ........ ........ ........ .......2Valuation rules........ ........ ........ ........ ........ ........ ........ ........ ........ ........ ........ ................ ........ ........ . 2Benefits Provided in Australia ........ ........ ........ ................ ......... ........ ....... ........ ........ ........ ........ ..3Reductions in taxable value ........ ........ ........ ........ ........ ......... ........ ....... ........ ........ ........ ............. 3

Relocation – temporary accommodation ........ ........ ........ ........ ......... ........ ........ ............... ....... 3Temporary accommodation at former location ........ ........ ........ ........ ........ ........ ......... ............. 4Temporary accommodation at new location ........ ........ ......... ....... ........ ........ ........ ................ .. 4

Exempt housing benefits - Remote area housing benefits ........ ........ ......... ....... ........ ........ ........ ....6What does the phrase 'customary for employers in the industry' mean in relation to theprovision of fringe benefits to employees? ........ ........ ........ ........ ........ ......... ........ ....... ........ ....6

Board fringe benefits........ ........ ........ ........ ........ ......... ........ ....... ........ ........ ........ ................ ...... 10Taxable value ......... ........ ........ ....... ........ ........ ........ ........ ......... ........ ........ ............... ........ ........ 10Meals provided by others ........ ......... ........ ....... ........ ........ ........ ................ ......... ........ ....... .......10Meals which are not board fringe benefits ........ ......... ........ ....... ........ ........ ........ ................ ...... 10Otherwise deductible ......... ........ ........ ....... ........ ........ ........ ........ ......... ........ ........ ............... .....11Exempt board benefits ........ ........ ........ ................ ........ ......... ....... ........ ........ ........ ........ ........ ...11

Residential fuel (section 59) ........ ........ ........ ........ ......... ........ ........ ............... ........ ........ ........ ......11Remote area housing assistance (section 60) ........ ........ ......... ....... ........ ........ ........ ................ 12Remote area holiday transport - not subject to ceiling (section 61) ........ ........ ........ ........ .........21

Remote area holiday transport - subject to ceiling (section 60A) ........ ........ ........ ........ ........ ........22Remote area home ownership schemes (sections 65CA to 65CC)......... ........ ........ ............... .....23‘Fly-in fly-out’ arrangements - residual benefits (subsection 47(7)) ......... ........ ........ ............... .....23Certain meals provided to primary production employees (section 58ZD) ......... ........ ........ ....... ..23

Remote Area Benefits FBT 2006

2

Introduction

This article provides a summary of those fringe benefit concessions that are specifically aimed atemployers and/or employees in remote areas. It is not meant to be an all-encompassingcommentary on every benefit that is available to employers that are located in remote areas.

The summary is based on various commercial commentaries and ATO publications. We haveadded our own commentary to highlight important issues.

Housing fringe benefits - generally

What is a housing benefit?

An employee is provided with the right to use a unit of accommodation and that unit ofaccommodation is the usual place of residence of the employee.Includes:

a house, flat or home unit accommodation in a house, flat or home unit accommodation in a hotel, motel, guesthouse, bunkhouse or other living quarters a caravan or mobile home, or accommodation in a ship or other floating structure.

The use of shared accommodation as a usual place of residence is nonetheless a housing fringebenefit.

Section 25 of the FBTAA ("the Act") stipulates that the existence of a housing right granted to aperson during a year of tax constitutes a benefit to that person. Section 136 defines a housingright as the granting of a lease or licence to occupy or use a unit of accommodation as theperson's usual place of residence. Circumstances in which the provision of accommodation wouldnot constitute a housing right, for example, would be where an employee is living away from hisor her usual place of residence in order to carry out the duties of employment, or is travelling inthe course of employment. In the former case, the benefit would be exempt under sub-section47(5), while in the latter it would be effectively exempted by the operation of section 52 by reasonthat, had the employee incurred the cost of providing the accommodation, that cost would havebeen deductible under the income tax law.

Valuation rules

Reference to the market value of the right to occupy the unit of accommodation. Disregard- any rights of the occupant to have expenses associated with the occupancy (eg. Electricity orgas) paid by the employer or someone elseWhere gas or electricity is provided without charge to the employee, the market rental value ofthe housing benefit would need to reflect that condition.- any onerous conditions of the occupancy that relate to the occupant’s employment (eg. Beingon call for duty) are disregarded

The object is to ascertain the market rental value by reference to the property that is occupied,and to disregard any matters particular to the person or persons who occupy it. Market rental iswhat a willing but not anxious person would be prepared to pay the owner to occupy the particularpremises in its existing condition if it were placed on the open market for rent.

Remote Area Benefits FBT 2006

3

Benefits Provided in Australia

Remote area housing benefits are exempt. (See page 6)

There are two sub-categories of these benefits for valuation purposes. The first is where theperson providing the accommodation is carrying on a business of providing the sameaccommodation to the public and the unit of accommodation is a caravan or mobile home or is ina hotel, motel, hostel or guesthouse.

The second sub-category is any other accommodation.Caravan, mobile home, hotel, motel, hostel or guesthouse and person providing the benefit iscarrying on a business which consists of providing such accommodation to the public.

Benefit is: market rental value of the accommodation, reduced by any rent or other considerationpaid by the employee.

If provided to an employee of the hotel, Caravan Park, etc., and is identical or similar to thatprovided to paying guests, then the taxable value is 75% of the market rental value, less theamount of any rent paid.

An alternative to long-term value is an amount equal to 15% of the daily rate charged to casualguests can be adopted.

Other accommodationBenefit is: market rental value reduced by any rent or other consideration paid by the employeeby reference to the period employee had the right to use the accommodation.

The alternative is to base later years on the first year’s market rental value. Calculate an annualrental value for the first year and thereafter applying an inflation factor. Where market rentalvalue could be expected to have increased by at least 10%, the value of the housing benefit mustbe determined by reference to the ‘new’ market rental value.

A ‘new’ market rental value must also be found if alterations have the effect of reducing themarket rental value by at least 10%.

If the accommodation was occupied at different times during the first year by different employees,and if the market rental values differed, the annual rental value for indexation purposes is theweighted average of the annual equivalent of the market rental value of each employee’s periodof occupancy.

Reductions in taxable value

Relocation – temporary accommodationThis concession reduces to nil the taxable value of fringe benefits arising from the provision oftemporary accommodation (including household goods) to an employee who changes his or herusual place of residence in the course of employment or in order to commence employment.

Remote Area Benefits FBT 2006

4

Temporary accommodation at former locationThe concession applies to temporary accommodation at the employee’s former location only ifthe temporary accommodation is necessary because the former home is unavailable orunsuitable for occupancy because of furniture removal or other factors relating to the relocation.In that case, the concession is applicable to the temporary accommodation during a maximum21-day period ending on the day when the employee starts work at the new location.

Temporary accommodation at new locationEmployee must begin to make sustained and reasonable efforts to buy or lease suitable long-term accommodation as soon as reasonably practicable after starting work at the new locality.

The concession is limited to an occupancy period that begins seven days prior to the day whenthe employee starts work at the new location and ends when the employee could reasonably beexpected to occupy the home after it has been purchased or leased.

The concession is ordinarily limited to a maximum occupancy period of four months. However,there are two exceptions to this time limit:

where the employee gives the employer a declaration (see below) which outlines theefforts being made to find suitable long-term accommodation, then the concession mayapply for a maximum of six months, and

where the employee:- owned a home at the former locality but sold it within six months of starting work atthe new locality and, during that period, attempted to buy a home at the new locality,and- the employee gives the employer a declaration (see below) which outlines theefforts being made to find suitable long-term accommodation;then the concession may apply for a maximum of 12 months.

In either case, the concession will end before the four months, six months or 12 months elapse ifthe employee ceases to make reasonable and sustained efforts to buy or lease suitable long-termaccommodation.

Remote Area Benefits FBT 2006

5

Temporary accommodation relating to relocation declaration

Sections A and D of the form must be completedplus either of Sections B and CSECTION AI, ______________________________________________________________

(name)declare that for the purpose of commencing employment with_____________________________________________________________

(name of employer)At__________________________________________________________________________

(locality/address of employer)that I commenced sustained efforts to acquire a long term place of residence on__________ 20_____; (date search-period commenced) and(complete either Section B or Section C, whichever is applicable, where a period in excess of fourmonths has elapsed since the search commenced)

SECTION BIf the employee did not have a proprietary interest in their former residence:(Where the unit of accommodation is occupied on a date subsequent to completion of the initial fourmonth search period but prior to six months after commencement of the initial search period)I entered into a contract to permanently occupy a unit of accommodationon __________ 20_____; (date)and commenced occupation (on a date subsequent to the completion of the initial four month searchperiod but prior to six months after the commencement of the initial search period) of the unit ofaccommodation on__________ 20_____; or (date)(Where the employee is unable to locate a suitable permanent unit of accommodation after sixmonths from the commencement of the initial search period :)

As at __________ 20_____ despite sustained efforts,(date six months from the commencement of the initial search period)I have been unable to locate a suitable permanent unit of accommodation; or

SECTION CIf the employee held a proprietary interest in their former residence:I entered into a contract to sell my former residence on ________ 20_____ and;(date within six months of the commencement of the initial search-period)either (indicate whichever is appropriate):commenced occupation of a unit of accommodation on __________ 20_____ (date)which I intend to occupy as my new long term residence; ordespite sustained efforts, I have been unable to locate suitable long-term accommodation within aperiod of 12 months from when my initial search commenced.

SECTION DTemporary accommodation at________________________________________________ (address)was required for the period __________ 20_____ to __________ 20_____ (date)solely because I was required to change my usual place of residence in order to perform the duties ofmy employment.

Signature______________________________

Date______________________________

Remote Area Benefits FBT 2006

6

Exempt housing benefits - Remote area housing benefits

A housing benefit qualifies as a remote area housing benefit if the following conditions aresatisfied:

for the whole of the tenancy period the unit of accommodation is in a remote area for the whole of the tenancy occupied by a current employee and the usual place of

employment of the employee is in the remote area it is customary in that industry for employers to provide free or subsidised residential

accommodation to employees, (from 1st of April 2006 this condition will no longerapply) and

it is necessary for the employer to provide free or subsidised accommodation foremployees or to arrange for the provision of such accommodation for any of the followingreasons:

the nature of the employer’s business is such that employees are liable to movefrequently from one residential location to another

there is insufficient suitable residential accommodation otherwise available at or near theplace or places where the employees are employed, or

it is customary for employers in that industry to provide free or subsidisedaccommodation for employees.

For most employers, accommodation is in a remote area if it is not in or near an urban centre.

The accommodation must be located at least:40 kilometres from a town with a census population of 14 000 to less than 130 000:or at least 100 kilometres from a town with a census population of 130 000 or more (populationfigures based on the 1981 Census).

If the accommodation is in Zone A or B (for income tax purposes) it must be located:at least 40 kilometres from a town with a census population of 28 000 to less than 130 000:or at least 100 kilometres from a town with a census population of 130 000 or more.

The Commissioner has discretion, where the circumstances warrant it, to treat a person whoresides or works in an area that is adjacent to an eligible urban area as residing or workingoutside that area if persons who live or work near that person are outside the area.

Extension of the exemption

This extended exemption will apply in relation to housing benefits provided for employees of: a public hospital that is a PBI a government body where the duties of the employee are exclusively performed in, or in

connection with, a public hospital that is a PBI a public hospital other than a government hospital a hospital carried on by a non-profit society or a non-profit association a charitable institution, and a police service.

For such benefits, accommodation will be treated as being in a remote area where it is situated atleast 100 kilometres from a town with a census population of 130 000 or more.

What does the phrase 'customary for employers in the industry' meanin relation to the provision of fringe benefits to employees?N.B from 1st of April 2006 this condition will no longer apply

The phrase occurs in the following sections of FBTAA:

Remote Area Benefits FBT 2006

7

- sections 29 and 142 dealing with remote area housing fringe benefits- section 143 dealing with remote area holiday transport

A benefit will be accepted as being customary where it is normal or common for employees ofthat class or job description in that industry to be provided with the same or similar benefits. It isnot necessary that all or even the majority of employees in the industry receive the benefit. Wherethe provision of the benefit is unique, rare or unusual within an industry it would not be acceptedas being customary.

In defining the employer's industry, the ATO will accept categorisation based on any recognisedindustry classification system. Examples of these are the industry codes for business incomeused by the ATO (listed in the company income tax return instructions), and Australian and NewZealand Standard Industrial Classification (ANZSIC) codes.

The ANZSIC has a structure comprising categories at four levels, namely Divisions (the broadestlevel), Subdivisions, Groups and Classes (the finest level). For example, the operations of a winemaker fall within the following categories:

Division: Manufacturing Subdivision: Food, Beverage and Tobacco Manufacturing Group: Beverage and Malt Manufacturing Class: Wine Manufacturing.

It will be open for an employer to argue that their operations fall within any of the four levels ofclassification.

Employers may seek a private ruling from the ATO on whether it is customary within their industryfor a particular benefit to be provided. An industry group, with the written consent of employers,may also seek such a ruling.

Remote Area Benefits FBT 2006

8

Example Exempt remote area housing benefits – disqualifying arrangements

Facts

An employer customarily provides residential accommodation to staff in remote areas.The employer employs a manager under a contract basis.The employee currently leases a house privately and pays the rent from after tax earnings.The employer proposes to enter into a new rental agreement with the landlord immediately afterthe termination of the employee's rental agreement on the same property with the same landlordand provide a housing benefit to the employee as the employee's usual place of residence.

Decision

The provision of a housing benefit to the employee in a remote area by an employer who entersinto a rental agreement with a landlord for a residential property immediately after thetermination of a previous rental agreement of that same property between the employee and thelandlord, will not invoke the application of subparagraph 58ZC(2)(e)(ii) of the FBTAA.

Reasons

Where the employer is located in a remote area, the employer provides accommodation to itsemployees as their usual place of residence and the requirements of section 58ZC of theFBTAA are satisfied, the housing benefit is an exempt remote housing benefit.

A housing benefit provided to an employee by an employer, as a result of the termination of anexisting rental agreement between the employee and the landlord and the commencement of anew lease agreement between the employer and the same landlord at an arm's length basis onthe same property, will not necessarily invoke the application of subparagraph 58ZC(2)(e)(ii) ofthe FBTAA to disentitle the remote area housing benefit exemption provided under section58ZC of the FBTAA.

The housing right acquired by the employer through the new rental agreement entered into withthe landlord and subsequently provided to the employee does not necessarily represent anarrangement that was entered into for the purpose or for the purposes that included the purposeof enabling the employer to obtain the benefit of the application of this section.

Remote Area Benefits FBT 2006

9

It is considered that the creation of a housing right as an exempt benefit, emanating from thedecision to novate a lease, is an arrangement which would be inclusive of the purposes to obtainthe benefit of the application of this section.

Example Exempt remote area housing benefits – Disqualifying arrangements

Facts

As part of salary packaging, an arrangement (being a tripartite contract involving the employee,landlord and employer) was proposed that would shift the rights and obligations of the tenancyagreement, including the obligation to make the rental payments, from the employee to theemployer. This proposal was made in recognition of the earlier decision that as an employer in aremote area, something would have to be done if it were to successfully compete for and retain itsbetter staff.

As a result of the novation, the employer would have the right to use the unit of accommodationbut allow the employee to live in it rent-free until such time as the employee ceases to be inemployment. In the event of a termination of the employment of the employee, the novated leasebetween the employer and the landlord would be extinguished and the original rental leasebetween the landlord and the employee resurrected. The employee and the employee's familyhave resided in the rented accommodation prior to commencing employment with the employer.

Decision

The novation of an existing rental agreement for a house in a remote area, (between theemployer, employee and landlord) does not create the provision of an exempt remote areahousing benefit.

Reasons

For a remote area housing benefit to be exempt it is necessary that all of the requirements ofsection 58ZC of the FBTAA be satisfied.Whilst:(1) the unit of accommodation and the employee's usual place of employment are not at alocation in, or adjacent to an eligible urban area,(2) the provision of such housing is commonplace within the industry and would be in accordancewith the term 'customary in the industry' and(3) it is necessary for the employer to provide the employee such accommodation because it iscustomary for employers in the industry to provide such a housing benefit, the overall housingright must not represent an arrangement that was granted for the purpose or for the purposes thatincluded the purpose, of enabling the employer to obtain the benefit of the application of thissection.

Remote Area Benefits FBT 2006

10

Board fringe benefits

Definition

The provision of a meal to an employee is a board fringe benefit if the employee is entitled to theprovision of accommodation and the following conditions are satisfied:

there is an entitlement under an industrial award to be provided with at least two meals aday, or under an employment arrangement at least two meals a day are ordinarilyprovided

the meal is supplied by the employee's employer (if the employer is a company, the mealmay be supplied by a related company in a wholly-owned group)

the meal is cooked or prepared on the employer's (or related company's) premises or ona work site or place adjacent to a work site, and

the meal is supplied on the employer's premises (or the work site) or on the premises of arelated company.

Taxable value

The taxable value of a board fringe benefit is $2.00 per meal per person ($1.00 per person ifunder the age of 12). This is reduced by any amount paid for the meal by the employee.Incidental refreshments such as morning and afternoon teas supplied as part of board are exemptfrom FBT.

Meals provided by others

Where an employer contracts an employee's services to another person who provides theemployee with board meals on his or her premises, the meals are board fringe benefits and theemployer still has the FBT liability.

Meals which are not board fringe benefits

The following meals are not board fringe benefits:meals provided at a party, reception or other social functionmeals provided in a dining facility open to the public, except for board meals provided toemployees of a restaurant, motel, hotel, etc., andmeals provided in a facility principally used by a particular employee.

Some common examples of meals which may be board fringe benefits are: meals provided in a dining facility located on a remote construction site, oil rig or ship,

and meals provided to a live-in housekeeper or to a resident teacher in a boarding school.

Meals supplied to family members living with an employee who is entitled to meals under theemployment agreement or award are also treated as board meals and are subject to valuationunder these rules.

Remote Area Benefits FBT 2006

11

Such meals may be property fringe benefits, or if provided by a tax-exempt body may be tax-exempt body entertainment fringe benefits.

Otherwise deductible

If a board fringe benefit is provided to an employee in circumstances where, if the employee hadpaid for the meal, the employee would have been entitled to an income tax deduction, then thetaxable value of the board fringe benefit is reduced to nil.

Exempt board benefits

Board meals provided to an employee who is employed in a primary production business that islocated in a remote area, are exempt benefits under section 58ZD of the FBTAA.

Residential fuel (section 59)

This section refers to any form of fuel (including electricity) used for domestic purposes.

For use in connection with the employee’s usual place of residence, the taxable value of thefringe benefit may be reduced in the following circumstances:

the fringe benefit is an expense payment fringe benefit, a property fringe benefit or aresidual fringe benefit, and

the employee is also the recipient of:- a remote area housing benefit that is an exempt benefit ;- a remote area housing loan fringe benefit;- a remote area housing rental fringe benefit.

NOTE THAT THE CONCESSION IS NOT AVAILABLE UNLESS ONE OF THE THREESPECIFIC BENEFITS MENTIONED ABOVE ARE PROVIDED TO THE EMPLOYEE.

THUS THE 50% CONCESSION FOR FUEL IS NOT AVAILABLE WHERE THE EMPLOYEE ISIN RECEIPT OF AN EXPENSE PAYMENT BENEFIT WHERE THE EMPLOYER PAYS ORREIMBURSES THE INTEREST ON A MORTGAGE LOAN.

A remote area housing loan fringe benefit is a loan fringe benefit that satisfies the followingrequirements:

the loan fringe benefit arises from a housing loan provided in connection with theemployee’s usual place of residence, and

if the loan fringe benefit was instead a housing fringe benefit, it would be a remote areahousing benefit that is an exempt benefit.

A remote area housing rental fringe benefit is an expense payment fringe benefit which satisfiesthe following requirements:

the expense payment fringe benefit arises from rent paid in connection with theemployee’s usual place of residence, and

if the expense payment fringe benefit was instead a housing fringe benefit, it would be aremote area housing benefit that is an exempt benefit.

Taxable Value

The amount of the reduction in taxable value is 50%.

Remote Area Benefits FBT 2006

12

Remote area housing assistance (section 60)

Under certain conditions the taxable value of the fringe benefit arising from the provision ofhousing assistance may be reduced by 50%.

Broadly, those conditions are similar to the conditions required for remote area housing fringebenefits, except that these housing assistance benefits are not housing benefits.

For the purpose of this concession, the various forms of housing assistance are: a payment or reimbursement of rent (expense payment fringe benefit) -note: where the

housing assistance is a payment or reimbursement of rent the taxable value of the fringebenefit is reduced by 50% of the gross rent incurred by the employee

the making of a housing loan (loan fringe benefit)

NOTE THAT THIS BENEFIT IS A ‘LOAN FRINGE BENEFIT’ IN NATURE. IT ARISES FROMTHE EMPLOYER (OR ASSOCIATE) MAKING THE LOAN; OR A LOAN BEING MADE BY ATHIRD PARTY UNDER AN ARRANGEMENT.

a payment or reimbursement of the interest accrued on a housing loan (expensepayment fringe benefit)

NOTE THAT THIS BENEFIT IS AN ‘EXPENSE PAYMENT BENEFIT’ IN NATURE. IT ARISESFROM THE EMPLOYER (OR ASSOCIATE) PAYING THE INTEREST ON ANY LOAN. THAT IS,THE LOAN NEED NOT HAVE BEEN MADE BY THE EMPLOYER (OR ASSOCIATE) OR BY ATHIRD PARTY UNDER AN ARRANGEMENT.

the provision of land, or house and land (property fringe benefit) the payment or reimbursement of the cost of acquiring land, or house and land (expense

payment fringe benefit), and the payment received by the employee in respect of the granting to the employer of a

repurchase option on the house, or the payment in respect of the repurchase of theemployee's house (property fringe benefit).

Remote Area Benefits FBT 2006

13

Example Remote area housing: Disqualifying arrangements

The current employee commenced employment with the employer some years ago. Theircontract of employment was finalised five months after commencement. The term of thecontract was 5 years, and is to expire shortly.

The employee has requested an early renewal of their contract together with financialassistance towards interest accrued on their personal home mortgage for the purchase of theemployee's principal place of residence.

Upon the employee's commencement in the position, the employer supported the employeeand family in relocating to the area and finding a principal place of residence. Subsequently,the employer commenced payment of a monthly rent to a real estate agent for the employee'susual place of residence.

The employee then voluntarily ceased this rental benefit arrangement, the formal contracthaving been in place for 11 months. The employee has now approached the employer to re-commence a similar benefit for interest accrued on a home loan to purchase a property (ratherthan rental) some two years after ceasing to receive the previous benefit.

In respect of the above situation, the following FBT implications result: Payments to a third party for interest accrued on an employee's home mortgage

would constitute an expense payment fringe benefit under the FBTAA. An employee who ceased to receive an expense payment benefit for rental payments

could later receive a benefit in respect of interest accrued on a home loan, withoutcontravening the limitations contained in S 60(2)(d) of the FBTAA.

An early renewal of a contract of employment between an employer and an employeewould not necessarily contravene the limitations in S 60(2) of the FBTAA.

A current employee could receive an expense payment fringe benefit withoutcontravening the limitations in S 60(2)(d) of the FBTAA.

An employer can offer to provide benefits in respect of remote area housing to newappointees, and still obtain the reduction of taxable value available under Section 60of the FBTAA.

Remote Area Benefits FBT 2006

14

Example Remote area housing: reduction of taxable value - remote area housing loaninterest

Is the employer entitled to claim a 50% reduction in the taxable value of the expense paymentfringe benefit, as it relates to interest in respect of a remote area housing loan, in the followingcircumstances?

The employee owns land on which there is a house. The employee lives in the house which is his or her usual place of residence. The employee has a housing loan with a bank. The loan was entered into to enable the employee to purchase the land and house. The employee is a current employee of the employer. The dwelling is situated in a

'remote area'. The employee works in a 'remote area'. In the employer's industry it iscustomary to provide 'housing assistance' to employees.

The loan is a 'remote area housing loan connected with a dwelling'. The employee incurs $5,000 interest in relation to the housing loan. The employer reimburses the full amount of the $5,000 interest expense incurred.

This reimbursement is an 'expense payment fringe benefit'. There is no 'recipients contribution' made by the employee to the employer.

Paragraph 60(2)(d) of the FBTAA is about not allowing non-arms length arrangements orarrangements entered into for the purposes of obtaining the tax concessions available undersection 60. Paragraph 60(2)(d) does not apply to this arrangement.

Alternative facts

The facts as above continue to apply with the following exception.

Instead of the employer reimbursing the full amount of the $5,000 interest expense incurred,the employer only reimburses (in part), half of the $5,000 interest expense incurred. Thisreimbursement, $2,500, is an 'expense payment fringe benefit' as defined in subsection 136(1)of the FBTAA. Is this still subject to the exemption?

Yes.The expense payment fringe benefit is a reimbursement of the employee's interest incurred inrelation to the employee's remote area housing loan. The recipient of the $5,000 (or $2,500)is an expense payment fringe benefit if the recipient is an employee of the employer.'Recipients expenditure' means, in relation to an 'expense payment benefit', the expenditureincurred by the recipient. The expenditure incurred by the recipient is the amount of theinterest expense incurred by the employee, $5,000. The loan is a 'remote area housing loanconnected with a dwelling' as required. Accordingly, the $5,000 interest expense is 'recipientsexpenditure' which 'is in respect of a remote area housing loan connected with a dwelling'.The employee lives in the dwelling as his or her usual place of residence.

Paragraph 60(2)(d) of the FBTAA does not apply.

Subsection 60(2) of the FBTAA is satisfied. Accordingly, the employer is entitled to a 50%reduction of the taxable value in the expense payment fringe benefit.

Example calculation

Based on the facts (and alternative facts) contained above, the reduction in taxable value ofthe expense payment fringe benefit would be calculated as follows:

$(facts) $(alternativefacts)

Expense payment fringe benefit 5,000 2,500Less 'recipients contribution' nil nilTaxable value before reduction 5,000 2,500Less subsection 60(2) reduction, 50% of taxablevalue, (50% x $5,000 or 2,500)

- 2,500 - 1,250

Reduced taxable value 2,500 1,250

Remote Area Benefits FBT 2006

15

Example Remote area housing: reduction of taxable value - remote area housing rent

Issue

In the following circumstances, is the taxable value of the expense payment fringe benefitreduced by 50% of the gross rent incurred by the employee, when the rent relates to a unit ofremote area accommodation?

The employee leases a house and lives in the house which is the employee's usual place ofresidence.The employee pays rent to the landlord under the terms of the lease.The employee is a current employee of the employer. The dwelling is situated in a 'remotearea'. The employee works in a 'remote area'. In the employer's industry it is customary toprovide 'housing assistance' to employees.During the year the employee incurs rent of $5,000. The employer reimburses the full amountof the $5,000 rent expense incurred. This reimbursement is an 'expense payment fringebenefit'.The rent the employee pays the landlord satisfies the reference in paragraph 60(2A)(b) andsubsection 142(1A) of the FBTAA to 'remote area housing rent connected with a unit ofaccommodation'.There is no 'recipients contribution' made by the employee to the employer.

Paragraph 60(2A)(d) of the FBTAA is about not allowing non-arms length arrangements orarrangements entered into for the purposes of obtaining the tax concessions available undersection 60.

Paragraph 60(2A)(d) of the FBTAA does not apply to this arrangement.

Alternative facts

The facts as above continue to apply with the following exception.Instead of the employer reimbursing the full amount of the $5,000 rent expense incurred, theemployer only reimburses (in part), half of the $5,000 rent expense incurred. Thisreimbursement, $2,500, is an 'expense payment fringe benefit' as defined in subsection 136(1)of the FBTAA. The recipient of the $5,000 (or $2,500) 'expense payment fringe benefit' is theemployee of the employer.

Paragraph 60(2A)(a) of the FBTAA is satisfied.

'Recipients expenditure' means, in relation to an 'expense payment benefit', the expenditureincurred by the recipient. The expenditure incurred by the recipient as described in paragraph20(b) of the FBTAA is the amount of rent incurred by the employee That is, the amount of thegross rent incurred before reimbursement, which is $5,000 in both fact situations.

The rent the employee pays the landlord satisfies the reference in paragraph 60(2A)(b) andsubsection 142(1A) of the FBTAA to 'remote area housing rent connected with a unit ofaccommodation'. During the year, the rent expense accrues and the employee lives in theaccommodation as his or her usual place of residence. Paragraph 60(2A)(c) of the FBTAA issatisfied.

Paragraph 60(2A)(d) of the FBTAA does not apply.Subsection 60(2A) of the FBTAA is satisfied. Accordingly, the employer is entitled to areduction in taxable value equal to 50% of the gross rent incurred by the employee asrelates to the occupation period.

Example cont…

Remote Area Benefits FBT 2006

16

Note: Unlike the reduction contained in subsection 60(2) of the FBTAA the 50% reductioncontained in subsection 60(2A) of the FBTAA refers to 50% of the employee's expenditure(the gross rent) not to 50% of the taxable value.

Example calculation

Based on the facts (and alternative facts) contained above, the reduction in taxable value ofthe 'expense payment fringe benefit' would be calculated as follows:

$(facts) $(alternativefacts)

Expense payment fringe benefit 5,000 2,500Less 'recipients contribution' nil nilTaxable value before reduction 5,000 2,500Less subsection 60(2A) reduction, 50% ofGross rent, (50% x $5,000)

2,500 2,500

Reduced taxable value 2,500 Nil

Remote Area Benefits FBT 2006

17

Example Remote area housing: reduction of taxable value - residential property andemployee's purchase consideration

In the following circumstances, does the employee's expenditure incurred in purchasing ahouse in a remote area satisfy the requirement of being 'recipients expenditure that is incurredwholly to enable the employee to acquire an estate or interest in land on which there is adwelling'?

Issues

After commencing employment with the employer, the employee acquires land on which thereis a house (the property). The property is located in a remote area. The property is acquiredunder a contract of sale.

The employer reimburses the employee all (or part) of the purchase price of the property. Thereimbursement is made with reference to the purchase price of the property, being theexpenditure incurred by the employee.

The reimbursement is an 'expense payment fringe benefit' as defined in subsection 136(1) ofthe FBTAA.

Answer - Yes

Reasons

The employee's expenditure is wholly for that purpose.

Under subsection 60(4) of the FBTAA, an employer is entitled to apply for a 50% reduction inthe taxable value of certain 'expense payment fringe benefits' when the 'recipients expenditureis in respect of remote area residential property'.

Broadly, the subsection discounts by 50% the taxable value of a fringe benefit relating to theprovision of assistance to enable an employee to acquire a 'unit of remote areaaccommodation' (typically, a house in a remote area of Australia).

Subsection 142(2C) of the FBTAA provides rules for determining eligibility for this 50%reduction.

Subsection 142(2C) of the FBTAA sets out the criteria of when 'the recipients expenditure is inrespect of remote area residential property'. Paragraph 142(2C)(c) of the FBTAA includes therequirement that the 'recipient’s expenditure' be incurred wholly 'to enable the employee toacquire an estate or interest in land on which there is a dwelling'. The recipient of the'expense payment fringe benefit' is an employee of the employer. 'Recipient’s expenditure'means, in relation to an 'expense payment benefit', the expenditure incurred by the recipient.The 'recipient’s expenditure' is the employee's purchase price under the contract of sale.

Paragraph 142(2C)(c)of the FBTAA is satisfied.

Subsection 142(2C) of the FBTAA contains other requirements, including at subparagraph142(2C)(g)(ii) that at the time the 'recipient’s expenditure' was incurred, which is the date thecontract of sale was executed, that the employee was a current employee of the employer.Also at the time the 'recipient’s expenditure' was incurred, the usual place of employment mustbe in a remote area.

Remote Area Benefits FBT 2006

18

Example Remote area housing: reduction of taxable value - residential property andemployee's mortgage loan repayments

Issues

The employee owns land on which there is a house (the property).The employee has a home loan with a bank which is secured by way of mortgage over theproperty.The loan with the bank was entered into to enable the employee to acquire the property.The terms of the loan require the employee to make regular repayments in order that the loanbe repaid within the period of the loan.The terms of the loan include that the loan accrues interest and other charges.The interest and charges are added to the loan.The employee makes repayments on the loan which reduces the current (at the repaymentdate) balance of the loan.The employer reimburses the employee all (or part) of the loan repayment(s).The reimbursement is made with reference to the loan repayment(s), being the expenditureincurred by the employee.

Answer

The reimbursement(s) is an 'expense payment fringe benefit' as defined in subsection 136(1)of the FBTAA.

Reasons

An employer is entitled to apply a 50% reduction in the taxable value of certain 'expensepayment fringe benefits' when the 'recipients expenditure is in respect of remote arearesidential property'.Broadly, the subsection discounts by 50% the taxable value of a fringe benefit relating to theprovision of assistance to enable an employee to acquire a 'unit of remote areaaccommodation' (typically, a house in a remote area of Australia).

Subsection 142(2C) of the FBTAA provides rules for determining eligibility for the subsection60(4) of the FBTAA reduction in taxable value.

Subsection 142(2C) of the FBTAA sets out the criteria of when 'the recipients expenditure is inrespect of remote area residential property'. As part of that criteria, paragraph 142(2C)(c) ofthe FBTAA requires that the 'recipients expenditure' be incurred wholly 'to enable theemployee to acquire an estate or interest in land on which there is a dwelling'.

The recipient of the 'expense payment fringe benefit' is an employee of the employer.

'Recipients expenditure', means, in relation to an 'expense payment benefit', the expenditureincurred by the recipient.

The 'recipients expenditure' is the loan repayment.

Example cont…

Remote Area Benefits FBT 2006

19

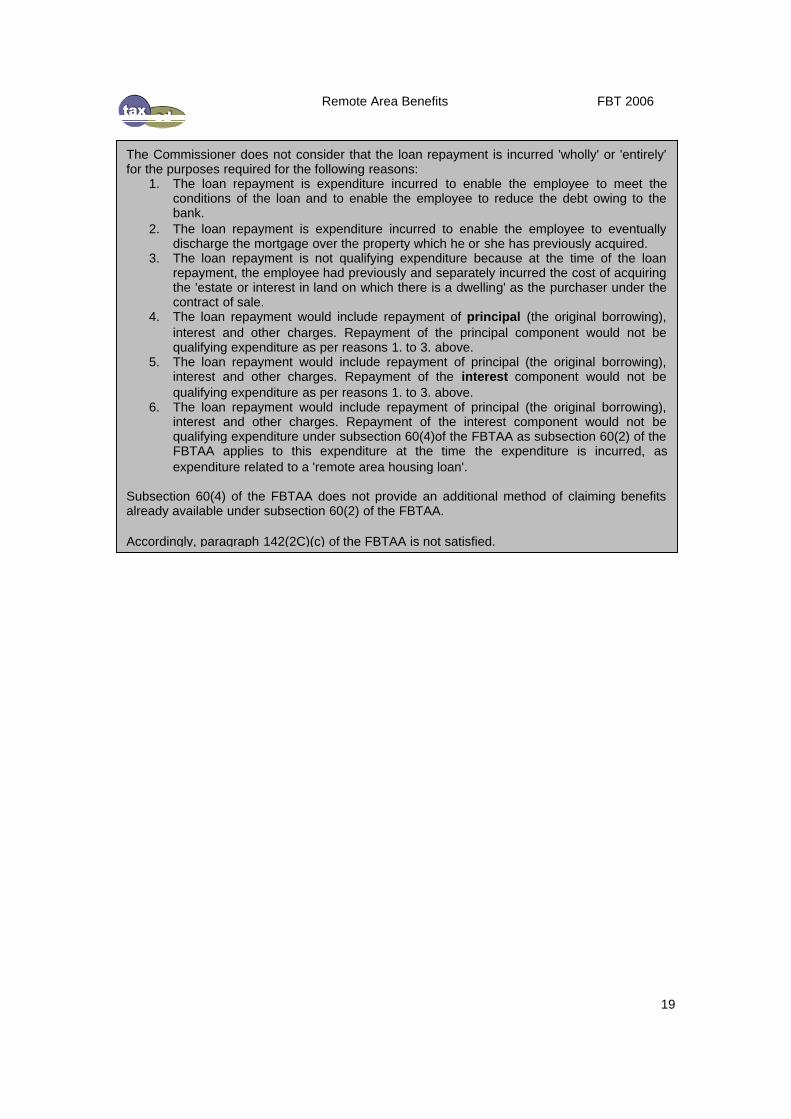

The Commissioner does not consider that the loan repayment is incurred 'wholly' or 'entirely'for the purposes required for the following reasons:

1. The loan repayment is expenditure incurred to enable the employee to meet theconditions of the loan and to enable the employee to reduce the debt owing to thebank.

2. The loan repayment is expenditure incurred to enable the employee to eventuallydischarge the mortgage over the property which he or she has previously acquired.

3. The loan repayment is not qualifying expenditure because at the time of the loanrepayment, the employee had previously and separately incurred the cost of acquiringthe 'estate or interest in land on which there is a dwelling' as the purchaser under thecontract of sale.

4. The loan repayment would include repayment of principal (the original borrowing),interest and other charges. Repayment of the principal component would not bequalifying expenditure as per reasons 1. to 3. above.

5. The loan repayment would include repayment of principal (the original borrowing),interest and other charges. Repayment of the interest component would not bequalifying expenditure as per reasons 1. to 3. above.

6. The loan repayment would include repayment of principal (the original borrowing),interest and other charges. Repayment of the interest component would not bequalifying expenditure under subsection 60(4)of the FBTAA as subsection 60(2) of theFBTAA applies to this expenditure at the time the expenditure is incurred, asexpenditure related to a 'remote area housing loan'.

Subsection 60(4) of the FBTAA does not provide an additional method of claiming benefitsalready available under subsection 60(2) of the FBTAA.

Accordingly, paragraph 142(2C)(c) of the FBTAA is not satisfied.

Remote Area Benefits FBT 2006

20

Example Remote area housing: reduction of taxable value - residential property andemployee's purchase consideration

Issue

After commencing employment with the employer, the employee acquires land on which thereis a house (the property). The property is located in a remote area. The property is acquiredunder a contract of sale. The employer reimburses the employee all (or part) of the purchaseprice of the property. The reimbursement is made with reference to the purchase price of theproperty, being the expenditure incurred by the employee.

Answer

The reimbursement is an 'expense payment fringe benefit' as defined in subsection 136(1) ofthe FBTAA.

Reasons

Under subsection 60(4) of the FBTAA, an employer is entitled to apply for a 50% reduction inthe taxable value of certain 'expense payment fringe benefits' when the 'recipients expenditureis in respect of remote area residential property'.

Broadly, the subsection discounts by 50% the taxable value of a fringe benefit relating to theprovision of assistance to enable an employee to acquire a 'unit of remote areaaccommodation' (typically, a house in a remote area of Australia).

Subsection 142(2C) of the FBTAA provides rules for determining eligibility for this 50%reduction.

Subsection 142(2C) of the FBTAA sets out the criteria of when 'the recipients expenditure is inrespect of remote area residential property'. Paragraph 142(2C)(c) of the FBTAA includes therequirement that the 'recipients expenditure' be incurred wholly 'to enable the employee toacquire an estate or interest in land on which there is a dwelling'.

The recipient of the 'expense payment fringe benefit' is an employee of the employer.

'Recipients expenditure', as defined in section 136(1) of the FBTAA means, in relation to an'expense payment benefit', the expenditure incurred by the recipient as described inparagraph 20(b) of the FBTAA. The 'recipients expenditure' is the employee's purchase priceunder the contract of sale.

The Macquarie Dictionary , 2001, Revised Third Edition, defines the term 'wholly' as meaning:1. entirely; totally; altogether; quite. 2. to the whole amount, extent, etc. 3. so as to comprise

or involve all.

The 'recipients expenditure', being the purchase price under the contract of sale, is consideredto be expenditure incurred wholly or entirely for the purpose of acquiring the property.

Accordingly, paragraph 142(2C)(c)of the FBTAA is satisfied.

Subsection 142(2C) of the FBTAA contains other requirements, including at subparagraph142(2C)(g)(ii) that at the time the 'recipients expenditure' was incurred, which is the date thecontract of sale was executed, that the employee was a current employee of the employer.Also at the time the 'recipients expenditure' was incurred, the usual place of employment mustbe in a remote area.

Remote Area Benefits FBT 2006

21

Remote area holiday transport - not subject to ceiling (section61)

Under an award or industry custom, an employee working in a remote area may be reimbursedfor the costs of travelling from, or may be provided with transport from, the remote area for thepurpose of having a holiday, and similarly, back to the remote area after the holiday. Theemployee may also be entitled to be provided with accommodation and/or meals in connectionwith the transport from, and to, the remote area.

The taxable value of the fringe benefits arising from the transport, accommodation and mealsmay be reduced by half if:

the employee travels from the work locality to the town where he or she lived beforebeing engaged to work at that locality, or

the employee travels to the capital city of the State or Territory in which the work place islocated (for this purpose, Perth and Adelaide are treated as if they were the capital citiesof Christmas Island and the Northern Territory, respectively).

The following requirements must also be satisfied: the holiday is of three working days or more, and where the benefit is an expense payment fringe benefit, proof of the expenditure is

provided to the employer (ie. originals or copies of receipts and/or invoices, or adeclaration in the approved format as shown below).

The reduction in taxable value extends also to holiday transport, accommodation and foodbenefits given to the employee's family, whether accompanied by the employee or not. If a childor the spouse of the employee does not live at the employee's work locality, the concession willalso apply if the holiday travel by the spouse or child is for the purpose of meeting the employee.

If the benefit is a reimbursement for car expenses calculated on a cents-per-kilometre basis, thenthe reduction in taxable value is limited. The maximum reduction is 50% of the amount that wouldbe paid if the reimbursement were to be calculated at a certain rate per kilometre. That rate perkilometre is the rate which is applicable for claiming income tax deductions on a cents-per-kilometre basis. In addition a rate of 0.63 of a cent per kilometre is permitted where more thanone family member travels in the car.

The reduction of taxable value does not apply to a reimbursement of car expenses calculated ona cents-per-kilometre basis unless the employer obtains from the employee a declaration in theapproved format as described below.

Remote Area Benefits FBT 2006

22

Remote area holiday transport declarationSECTION AI, ______________________________________________________________

(name of employee)declare that, for the purposes of having a holiday of not less than three days,_______________________________________________________________

(state who travelled, eg. self, self and family, etc)travelled on __________ 20_____ by _________________________________

(state mode of transport eg. car, plane)from ______________________________ to __________________________

(place of departure) (destination)I also declare that:expenses of $____________ were incurred by me on transport,

(amount in figures)accommodation and meals in undertaking that holiday travel; andI returned to my work location on __________ 20_____

(delete if the travel was not undertaken by self)

(If some or all of the transport expenses reimbursed by the employer were car expenses andthe reimbursement was calculated on a cents-per-kilometre basis, please also complete Bbelow)

SECTION BI declare that the travel was undertaken in my car (or a car leased by me) and that:the car is ________________________________________;

(state make and model of car and whether rotary engine or not)with an engine capacity (in cubic centimetres) of __________;the total number of kilometres travelled in the car between the places of departure anddestination (including the return journey) was __________;the number of family members (apart from myself) travelling in the car was ____________;the amount of the cents-per-kilometre car expenses reimbursed included in the total expensesdeclared above is $_______________

(amount in figures)

Signature______________________________

Date______________________________

Remote area holiday transport - subject to ceiling(section 60A)

Where a particular fringe benefit satisfies all but one of the requirements necessary to gain theconcession described above, a reduction of taxable value may nonetheless be available. If theonly requirement not satisfied is that of the locality of the place to which the employee travelsfrom the remote area, and from which the employee travels to return to the remote area, thetaxable value of the fringe benefit may be reduced by the lesser of 50% of the taxable value and50% of what is called the ‘benchmark travel amount’.

The benchmark travel amount is the usual cost of return travel between the work locality andcapital city of the State in which the work place is located (ie. normally the return economy air fare

Remote Area Benefits FBT 2006

23

plus any incidental costs ordinarily met by the employer under relevant industrial arrangements).The benchmark travel amount is worked out at the beginning of the employee's holiday.

For remote areas in the Northern Territory and for Christmas Island, the reduction in taxablevalue is limited to 50% of the usual cost of travel to Adelaide and Perth, respectively.

Remote area home ownership schemes (sections 65CAto 65CC)

Permits the amortisation of fringe benefits provided in connection with remote area homeownership schemes. The period of amortisation is generally five to seven years.

The benefits may consist of: a discount on the purchase of a home or of land on which to build a home a reimbursement of the cost of buying land and/or building a home, or an option fee entitling the employer to first choice in repurchasing the home.

There must be a restriction on the employee's freedom to sell the house during the amortisationperiod. Must be genuine rather than merely a contrived attempt to take advantage of thisconcession. If the home is repurchased by the employer during the amortisation period, then theunamortised balance is brought to account in that year's FBT return.

Where an employee is forced by a contractual buy-back arrangement to suffer a loss in sellingthe home back to the employer, then 50% of that loss may be deducted from the employer'saggregate taxable values in that FBT year. (The rationale for this reduction is that, taking anoverall view, any fringe benefit given to the employee to facilitate the original purchase of thehouse is being offset by the loss on its resale to the employer.)

‘Fly-in fly-out’ arrangements - residual benefits(subsection 47(7))

Transport provided to employees who work in remote areas or who work on oil rigs or otherinstallations at sea may be an exempt benefit. Exempt where employees are provided withaccommodation at or near the work site on working days and the transport is provided to enablethe employees to return to their usual place of residence on days off and it would beunreasonable to expect the employees to travel to and from work on a daily basis.

Certain meals provided to primary productionemployees (section 58ZD)

Expense payment, property, board or residual benefits arising in respect of the provision of mealson a working day are exempt benefits, if the following conditions are satisfied:

the employer is carrying on a business of primary production the employer's business is carried on in a remote area which is the location of the

employee's primary place of employment the meal is provided to the employee (except where the benefit is a board benefit, in

which case it may also be provided to an associate of the employee), and the provision of the meal does not amount to the provision of a meal entertainment

benefit.

Remote Area Benefits FBT 2006

24

Salary Sacrifice Definition

An arrangement between the employer and the employee, where the employee agrees to foregopart of their future entitlement to salary or wages in return for the employer providing benefits of asimilar cost to the employer. The employee is likely to place greater value on the benefit than itscost to the employer.

Under an effective arrangement: the employee pays income tax on the reduced salary or wagesthe employer may be liable to pay FBT on the fringe benefits provided, and salary-sacrificedsuperannuation contributions are classified as employer superannuation contributions (notemployee contributions) and are taxed in the superannuation fund under tax laws dealingspecifically with this subject.

Contact TaxEd

Tel: 03 9376 0377 ABN: 67 108 062 139Fax: 03 9376 0366 PO Box 1168Email: [email protected] Kensington, 3031Web: www.taxed.com.au

Disclaimer

No delegate or other person should rely on the contents of this document before obtainingadvice from a qualified and professional lawyer, accountant or similar person. The authors,presenters and publishers are not responsible for any actions taken on the basis of anythingcontained in this publication. All persons using this book do so on the understanding that theauthors and publishers will not be responsible for any errors or omissions contained in thispublication. The publisher and authors disclaim any liability and responsibility to any person inrespect of anything and of the consequence of anything done or omitted to be done by anyperson in reliance upon the contents of this publication. The authors and publishers shall haveno responsibility for any act or omission.

Acknowledgments

Some material for this workbook is taken from various State and Federal Government publications; Treasury,Ministerial and Tax Office, and various other sites published in hard copy or found on the Internet.

Copyright

This document is copyright. Apart from any fair dealing for the purposes of private study, research, criticism orreview, as permitted by the Copyright Act, no part may be reproduced by any process without writ ten permission.

© Copyright TaxEd 2006