Embed Size (px)

Citation preview

+2degC

Third Report | 2017

Renewable Energy and Energy Efficiency in Developing CountriesContributions to Reducing Global Emissions

UN Environment promotes environmentally sound practices

globally and in its own activities This publication is printed on 100 recycled paper

using vegetable - based inks and other eco-friendly practices Our distribution policy aims to

reduce UN Environmentlsquos carbon footprint

Togu Cover inside GreenDotindd 1 112509 94923 AM

A digital copy of this report is available at 1gigatoncoalitionorg

Copyright copy United Nations Environment Programme 2017

This publication may be reproduced in whole or in part and in any form for educational or non-profit purposes without special permission from the copyright holder provided acknowledgement of the source is made The United Nations Environment Programme would appreciate receiving a copy of any publication that uses this publication as a source

No use of this publication may be made for resale or for any other commercial purpose whatsoever without prior permission in writing from the United Nations Environment Programme

Disclaimer

The designations employed and the presentation of the material in this publication do not imply the expression of any opinion whatsoever on the part of the United Nations Environment Programme concerning the legal status of any country territory city or area or of its authorities or concerning delimitation of its frontiers or boundaries Moreover the views expressed do not necessarily represent the decision or the stated policy of the United Nations Environment Programme nor does citing of trade names or commercial processes constitute endorsement

ISBN No 978-92-807-3671-7

Job No DTI2132PA

Renewable Energy and Energy Efficiency in Developing CountriesContributions to Reducing Global Emissions

Third Report | 2017

+2degC

LEAD AUTHORS Yale University Angel Hsu Carlin Rosengarten

Amy Weinfurter Yihao Xie

REN21 Evan Musolino Hannah E Murdock

REVIEWERS

Niklas Houmlhne Markus Hagemann and Takeshi Kuramochi

(NewClimate Institute) Philip Drost (UN Environment)

Nathan Borgford-Parnell and Hanxiang Cong (Institute for

Governance and Sustainable Development) Zhao Xiusheng

(Tsinghua University China)

COUNTRY INITIATIVE AND DATA CONTRIBUTORS Case study support We thank and acknowledge following individuals for their valuable

assistance providing consultation feedback and information to

inform the case studies

Jaime Acuntildea (Univalle)Adedoyin Adeleke (Centre for Petroleum

Energy Economics and Law University of Ibadan) Ayooluwa Adewole

(Centre for Petroleum Energy Economics and Law University of

Ibadan) Godwin Aigbokhan (Renewable Energy Association of

Nigeria (REAN)) Habiba Ali (SOSAI Renewable Energies Company)

Centro Regional de Produccioacuten maacutes Limpia (CRPML) Corporacioacuten

Autoacutenoma Regional del Valle del Cauca (CVC) Tolu Fakunle (Centre

for Petroleum Energy Economics and Law University of Ibadan)

Eitan Hochster (Lumos Global) Janet Kajara (Kampala Capital

City Authority (KCCA)) Shehu Ibrahim Khaleel (Renewable Energy

Resources Development Initiatives (RENDANET)) Edison Masereka

(Kampala Capital City Authority (KCCA)) Nolbert Muhumuza (Awuma

Biomass) Tanya Muumlller Garcia (Secretary of Environment Mexico

City) Eleth Nakazzi (Kampala Capital City Authority (KCCA)) Ines

Restrepo-Tarquino (Univalle) Patricia Ugono (Solynta) Uvie Ugono

(Solynta) Paola Andrea Vaacutesquez (GEADES-UAO) Sandra Vaacutesquez

(El Castillo)

Multistakeholder partnerships Patrick Blake (enlighten U4E) Callum Grieve (Sustainable Energy

for All (SEforALL)) Martin Hiller (Renewable Energy and Energy

Efficiency Partnership (REEEP)) Irma Juskenaite (Climate Technology

Centre and Network (CTCN)) Tatiana Kondruchina (Climate and

Clean Air Coalition (CCAC)) Celia Martinez (District Energy in Cities

Initiative) Wei-Shiuen Ng (International Transport Forum OECD)

Eva Kelly Oberender (Renewable Energy and Energy Efficiency

Partnership (REEEP)) Ellen Paton (UK International Climate Fund

(ICF)) Quinn Reifmesser (Renewable Energy and Energy Efficiency

Partnership (REEEP)) Andrea Risotto (NDC Partnership) Nora

Steurer (The Global Alliance for Buildings and Construction (GABC))

Jukka Uosukainen (Climate Technology Centre and Network (CTCN))

Maria van Veldhuizen (Renewable Energy and Energy Efficiency

Partnership (REEEP)) Gunnar Wegner (Energizing Development and

Climate Mitigation (EnDev)) Elke Westenberger (Moroccan Climate

Change Competence Centre (4C Maroc)) Laura Williamson (REN21)

Peter Wright (Sustainable Energy for All (SEforALL))

Data gathering Markus Kurdziel (IKI) Sarah Leitner (IKI) Karoline Teien Blystad

(Norfund) Lucie Bernatkova (EIB) Cyrille Arnould (EIB) Aglaeacute Touchard-

Le Drain (EIB) Martina Jung (KfW) Milena Gonzalez Vasquez (GEF)

David Elrie Rodgers (GEF) Ichiro Sato (JICA) Yoji Ishii (JICA)

THOMSON REUTERS

A contribution from Thomson Reuters report ldquoGlobal 250

Greenhouse Gas Emitters A New Business Logicrdquo is included in

chapter 3 Lead Authors

David Lubin Constellation Research and Technology John

Moorhead BSD Consulting Timothy Nixon Thomson Reuters

The authors would like to thank and acknowledge the important

contributions of Chris Mangieri Dan Esty and Jay Emerson of Yale

University and Constellation Research and Technology

Important data and analytics support was provided by Frank Schilder

Thomson Reuters Research amp Development Adam Baron from

Thomson Reuters Content Analytics and Ian van der Vlugt from CDP

PROJECT MANAGEMENT AND COORDINATION

Zitouni Ould- Dada (UN Environment)

Rashmi Jawahar Ganesh (UN Environment)

REN21

The 1 Gigaton Coalition would like to thank and acknowledge the

invaluable assistance of REN21 namely Hannah E Murdock for

research coordination and Linh H Nguyen for research support

DESIGN AND LAYOUT Weeksde Webeagentur GmbH

ACKNOWLEDGEMENTS

5

1 INTRODUCTION 10

2 DEVELOPING COUNTRIESrsquo EFFORTS AND ACHIEVEMENTS IN ENERGY EFFICIENCY AND RENEWABLE ENERGY 13

21 POLICY DEVELOPMENT 14 211 Targets 14

212 Policy instruments 16

3

NON-STATE AND SUBNATIONAL CONTRIBUTIONS TO RENEWABLE ENERGY AND ENERGY EFFICIENCY 20

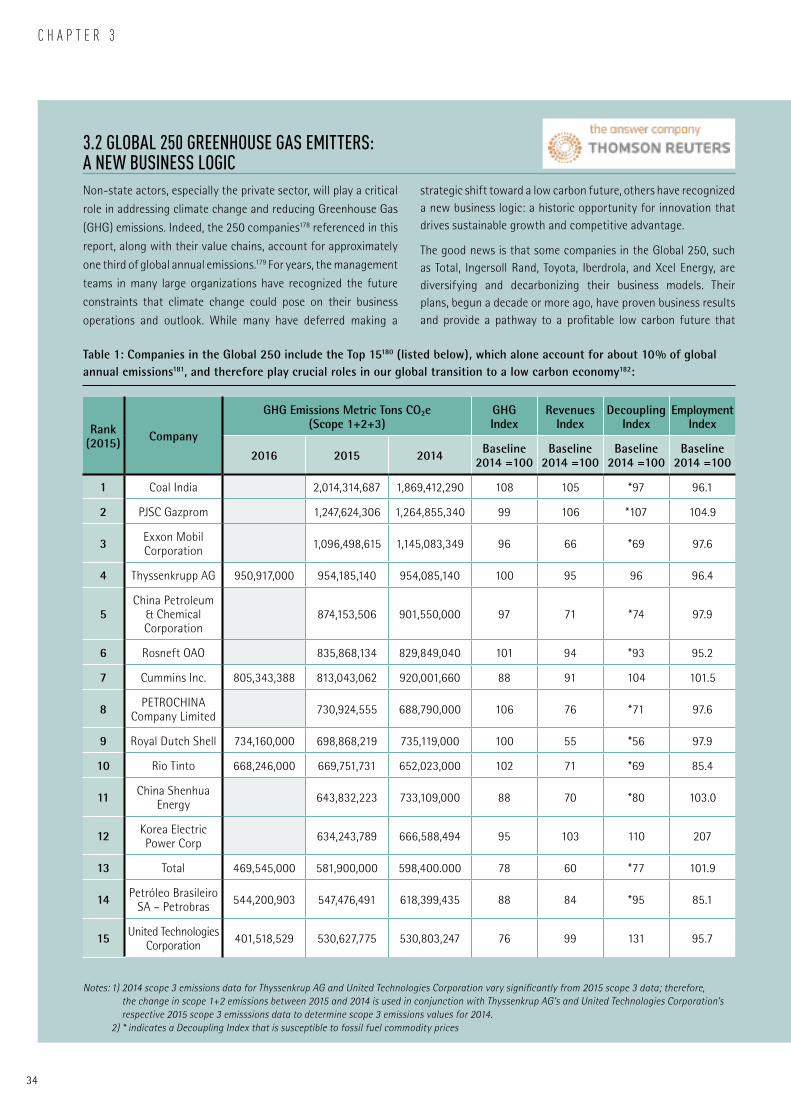

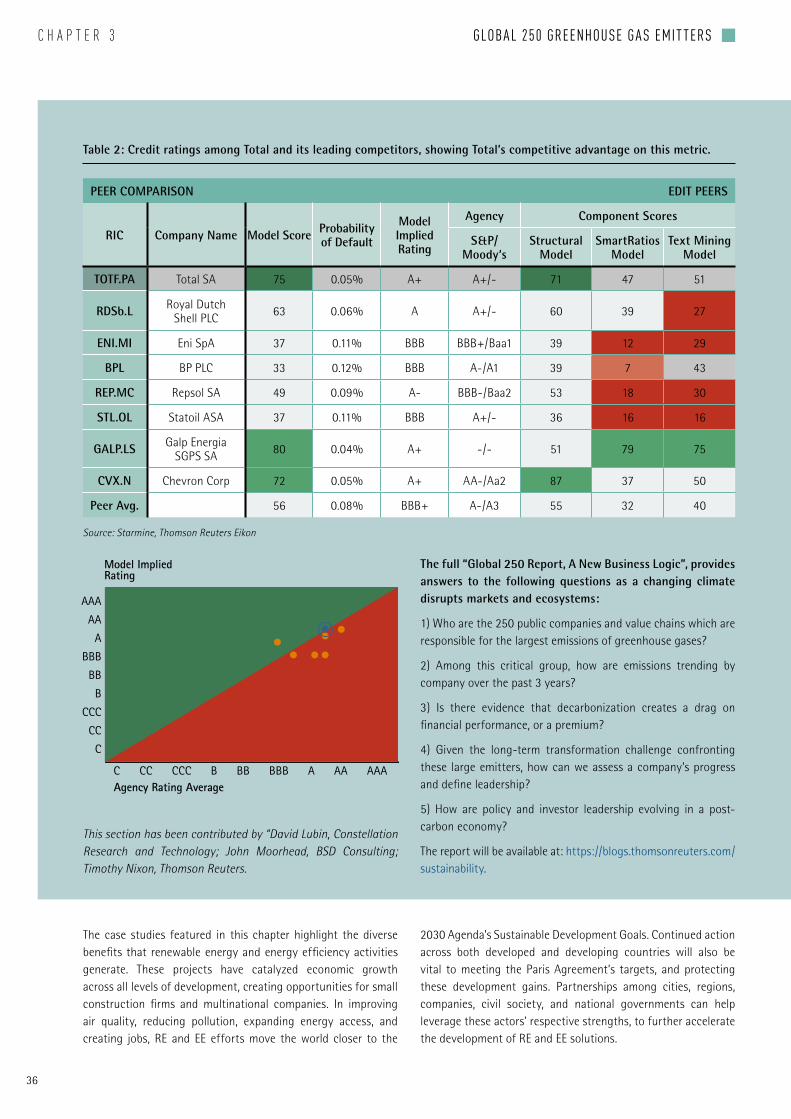

31 CASE STUDIES 22 32 EXCERPT FROM GLOBAL 250 GREENHOUSE GAS EMITTERS A NEW BUSINESS LOGIC 34

4 15- AND 2- DEGREE COMPATIBILITY A NEW APPROACH TO CLIMATE ACCOUNTING 37

41 DEVELOPING 15- AND 2- DEGREE COMPATABILITY CONDITIONS 38

42 COMPATABILITY TABLES 41

43 PROJECT-LEVEL COMPATABILITY 50

5 DATABASE ASSESSMENT 56

51 AGGREGATED IMPACT 57

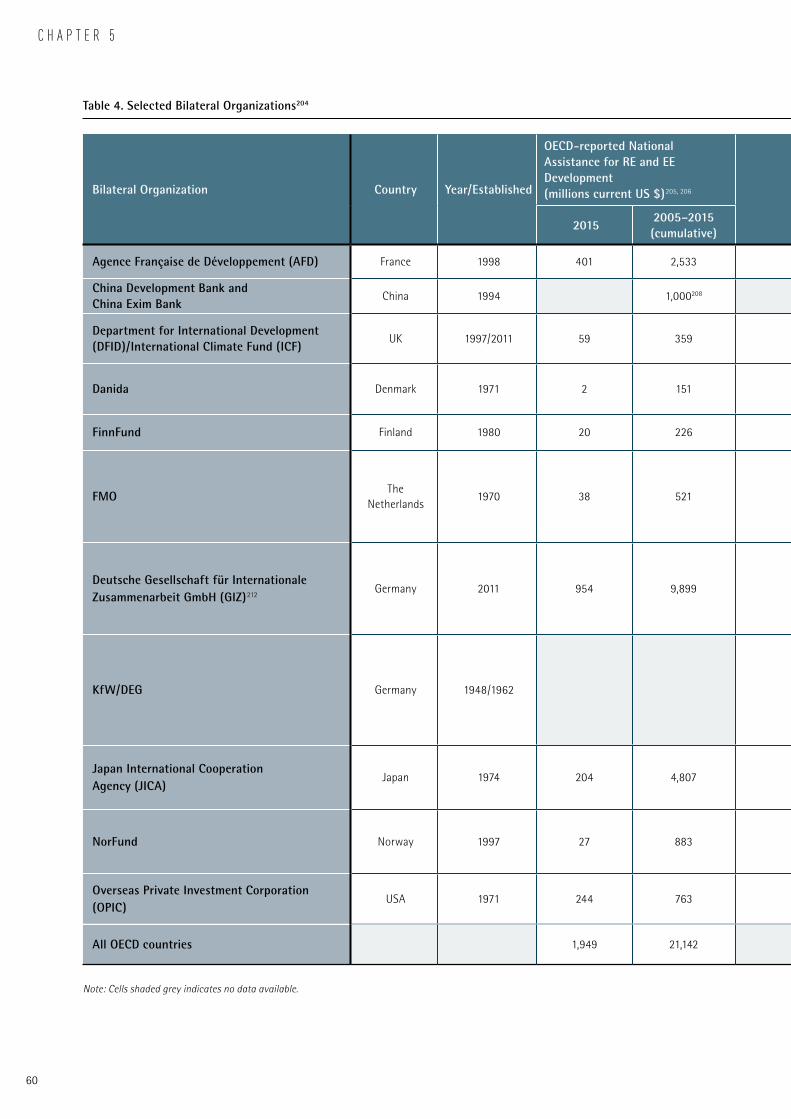

52 SELECTED BILATERAL INITIATIVES 59

53 SELECTED MULTILATERAL INITIATIVES 63 531 Multistakeholder partnerships 68

6 CONCLUSION 75

A ANNEX I DETAILED DESCRIPTION OF MITIGATION IMPACT CALCULATIONS 77

ACKNOWLEDGEMENTS 4

FOREWORD 6

KEY MESSAGES 7

EXECUTIVE SUMMARY 8

+2degC

TABLE OF CONTENTS

References 82

Glossary 87

Acronyms 88

Impressum 89

6

Even if the pledges in the Paris Agreement on Climate Change are

implemented we will still not reduce greenhouse gas emissions

enough to meet the goals The UN Environment Emissions Gap

Report 2017 states that for the 2degC goal this shortfall could be

11 to 135 gigatonnes of carbon dioxide equivalent For the 15degC

goal it could be as much as 16 to 19 gigatonnes We urgently need

more ambitious action to close these gaps So this latest 1 Gigaton

Coalition Report helps to focus those efforts by quantifying the

progress secured through renewable energy and energy efficiency

Electricity touches almost every aspect of our lives yet nearly

a quarter of the population still lacks access to safe clean and

affordable energy Around the world people continue to seek

less polluting options for everyday needs like lighting heating

water cooking and sanitation It should be no surprise then that

renewable power capacity is growing faster than all fossil fuels

combined with a record increase of about 9 from 2015 to 2016

Particularly when bi-products include better health education

security and economic growth

Take cities which are responsible for 75 of global greenhouse gas emissions They can also be a big part of the solution by adopting

to energy efficient buildings electric transport cycle schemes and waste conversion For example in New Delhi India the health of

local communities is severely affected by growing mountains of waste being dumped in open spaces The city and private sector are

tackling this by investing in waste-to-energy-plants These reduce toxic emissions and transform waste into electricity The plantrsquos

community center offers employment and artisan training to about 200 local women For Badru Nisha this income has enabled

her to save 70000 rupees (US $1100) and build a house for relatives in Bihar state This program helps women build their skills

and confidence and provides them with some financial security and independence This is just one of many stories inspiring local

governments mayors businesses and civil society to join forces for significant environmental economic and public health benefits

This report comes at a critical moment to support the growing number of non-state actors showing leadership to deliver the Paris

Agreement We hope it will motivate donors initiatives and countries to build on their achievements while inspiring more public and

private sector stakeholders to join this global effort

FOREWORD

HE Boslashrge BrendeMinister of Foreign AffairsNorway

Erik SolheimUN Environment Executive Director and Under-Secretary- General of the United Nations

+2degC

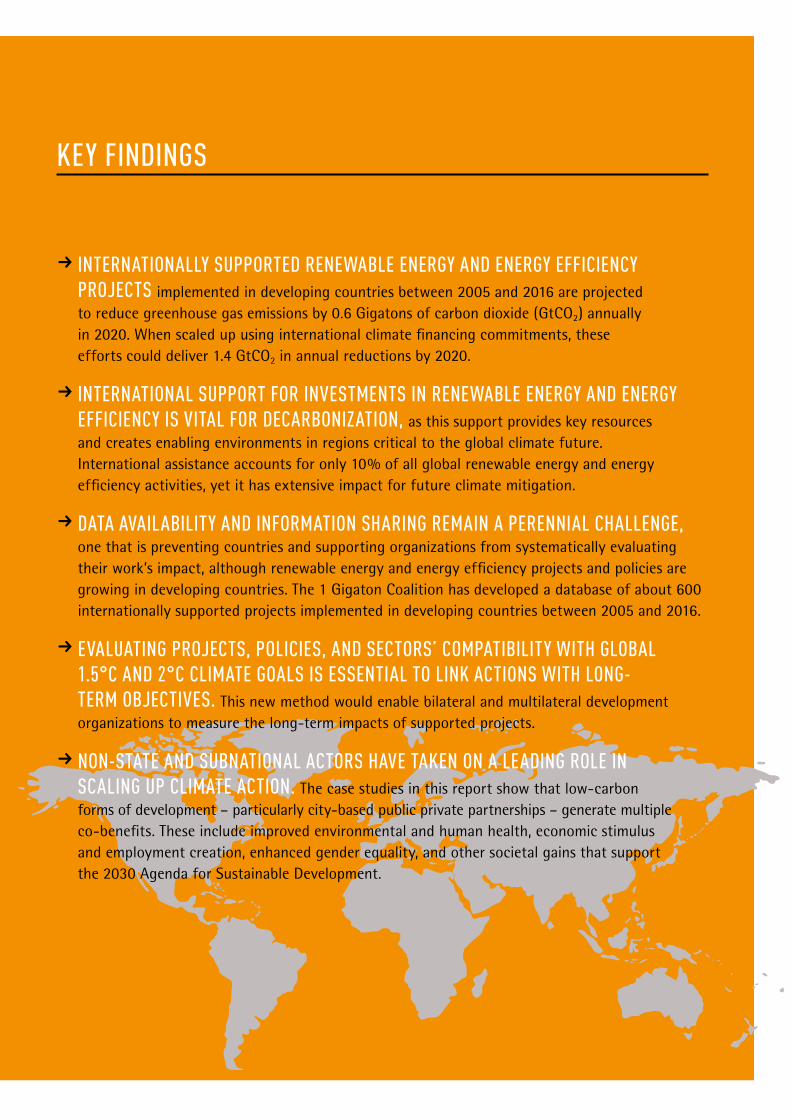

KEY FINDINGS

R INTERNATIONALLY SUPPORTED RENEWABLE ENERGY AND ENERGY EFFICIENCY PROJECTS implemented in developing countries between 2005 and 2016 are projected to reduce greenhouse gas emissions by 06 Gigatons of carbon dioxide (GtCO2) annually in 2020 When scaled up using international climate financing commitments these efforts could deliver 14 GtCO2 in annual reductions by 2020

R INTERNATIONAL SUPPORT FOR INVESTMENTS IN RENEWABLE ENERGY AND ENERGY EFFICIENCY IS VITAL FOR DECARBONIZATION as this support provides key resources and creates enabling environments in regions critical to the global climate future International assistance accounts for only 10 of all global renewable energy and energy efficiency activities yet it has extensive impact for future climate mitigation

R DATA AVAILABILITY AND INFORMATION SHARING REMAIN A PERENNIAL CHALLENGE one that is preventing countries and supporting organizations from systematically evaluating their workrsquos impact although renewable energy and energy efficiency projects and policies are growing in developing countries The 1 Gigaton Coalition has developed a database of about 600 internationally supported projects implemented in developing countries between 2005 and 2016

R EVALUATING PROJECTS POLICIES AND SECTORSrsquo COMPATIBILITY WITH GLOBAL 15degC AND 2degC CLIMATE GOALS IS ESSENTIAL TO LINK ACTIONS WITH LONG-TERM OBJECTIVES This new method would enable bilateral and multilateral development organizations to measure the long-term impacts of supported projects

R NON-STATE AND SUBNATIONAL ACTORS HAVE TAKEN ON A LEADING ROLE IN SCALING UP CLIMATE ACTION The case studies in this report show that low-carbon forms of development ndash particularly city-based public private partnerships ndash generate multiple co-benefits These include improved environmental and human health economic stimulus and employment creation enhanced gender equality and other societal gains that support the 2030 Agenda for Sustainable Development

Developing countries are achieving low-cost emissions reductions through renewable energy (RE) and energy efficiency (EE) projects and initiatives The focus of this report is to evaluate the impact of these projects in terms of measurable greenhouse gas emissionsrsquo reductions to help close the emissions gap needed to meet the 2degC climate goal

EXECUTIVE SUMMARY

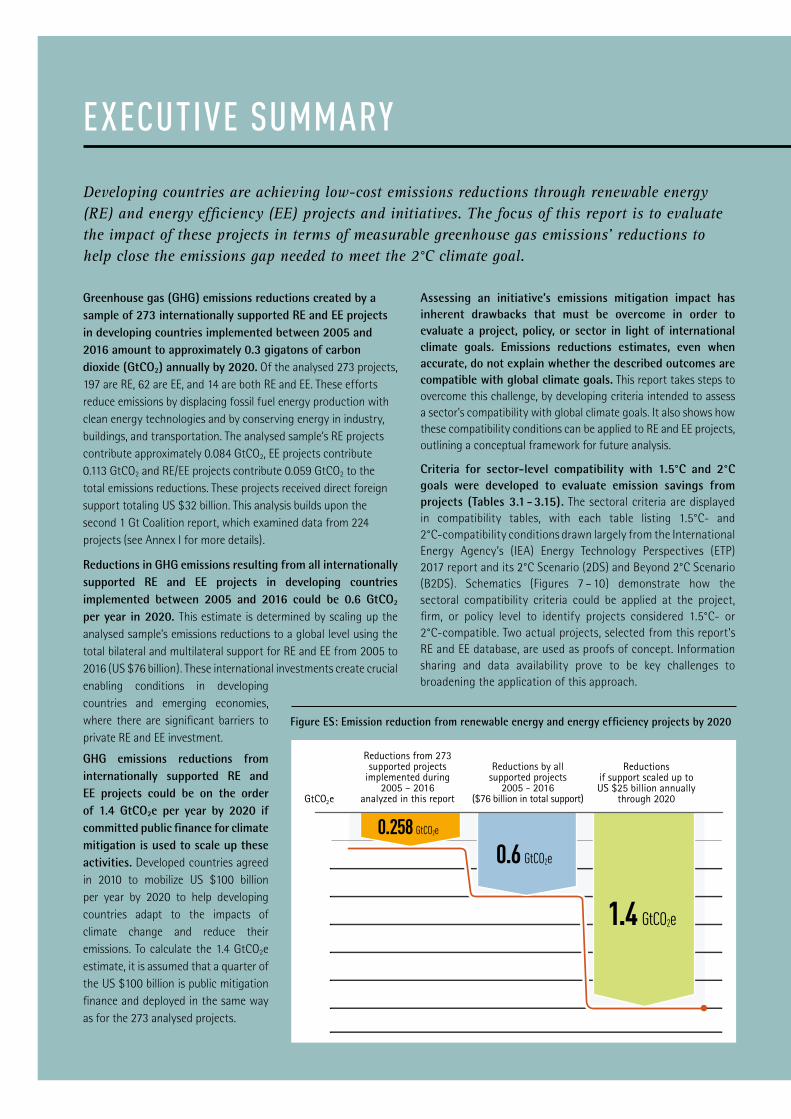

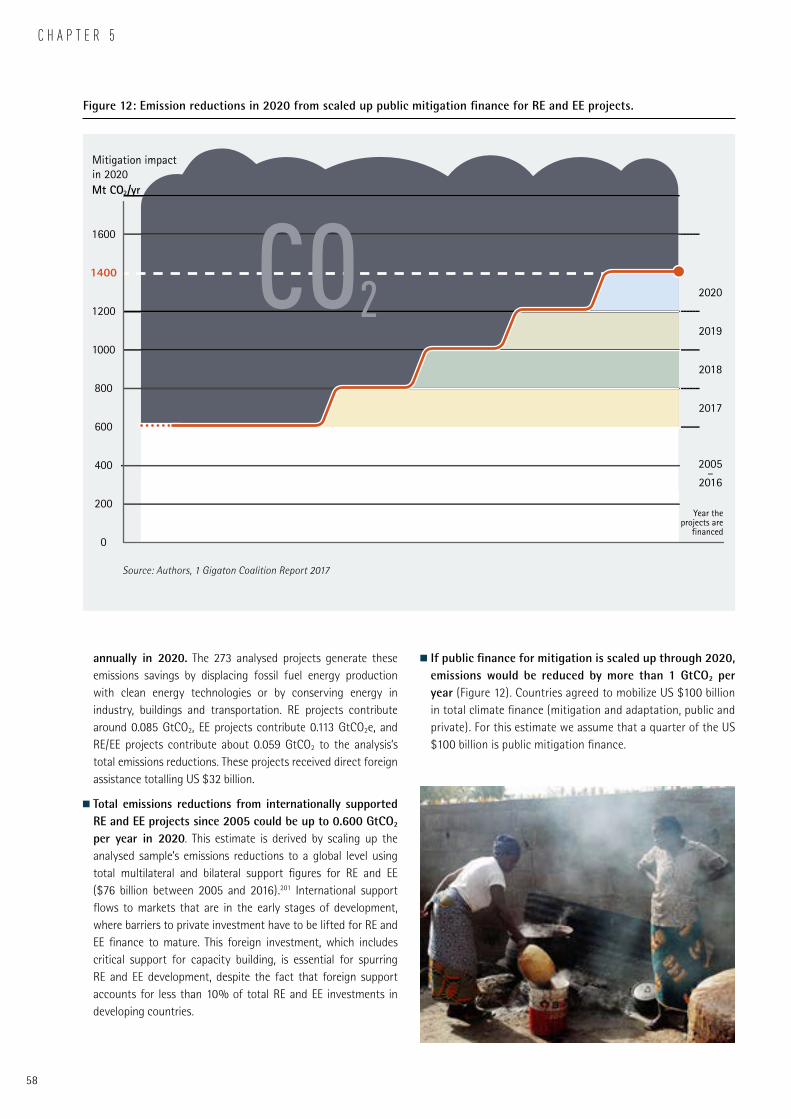

Greenhouse gas (GHG) emissions reductions created by a sample of 273 internationally supported RE and EE projects in developing countries implemented between 2005 and 2016 amount to approximately 03 gigatons of carbon dioxide (GtCO2) annually by 2020 Of the analysed 273 projects 197 are RE 62 are EE and 14 are both RE and EE These efforts reduce emissions by displacing fossil fuel energy production with clean energy technologies and by conserving energy in industry buildings and transportation The analysed samplersquos RE projects contribute approximately 0084 GtCO2 EE projects contribute 0113 GtCO2 and REEE projects contribute 0059 GtCO2 to the total emissions reductions These projects received direct foreign support totaling US $32 billion This analysis builds upon the second 1 Gt Coalition report which examined data from 224 projects (see Annex I for more details)

Reductions in GHG emissions resulting from all internationally supported RE and EE projects in developing countries implemented between 2005 and 2016 could be 06 GtCO2 per year in 2020 This estimate is determined by scaling up the analysed samplersquos emissions reductions to a global level using the total bilateral and multilateral support for RE and EE from 2005 to 2016 (US $76 billion) These international investments create crucial enabling conditions in developing countries and emerging economies where there are significant barriers to private RE and EE investment

GHG emissions reductions from internationally supported RE and EE projects could be on the order of 14 GtCO2e per year by 2020 if committed public finance for climate mitigation is used to scale up these activities Developed countries agreed in 2010 to mobilize US $100 billion per year by 2020 to help developing countries adapt to the impacts of climate change and reduce their emissions To calculate the 14 GtCO2e estimate it is assumed that a quarter of the US $100 billion is public mitigation finance and deployed in the same way as for the 273 analysed projects

Assessing an initiativersquos emissions mitigation impact has inherent drawbacks that must be overcome in order to evaluate a project policy or sector in light of international climate goals Emissions reductions estimates even when accurate do not explain whether the described outcomes are compatible with global climate goals This report takes steps to overcome this challenge by developing criteria intended to assess a sectorrsquos compatibility with global climate goals It also shows how these compatibility conditions can be applied to RE and EE projects outlining a conceptual framework for future analysis

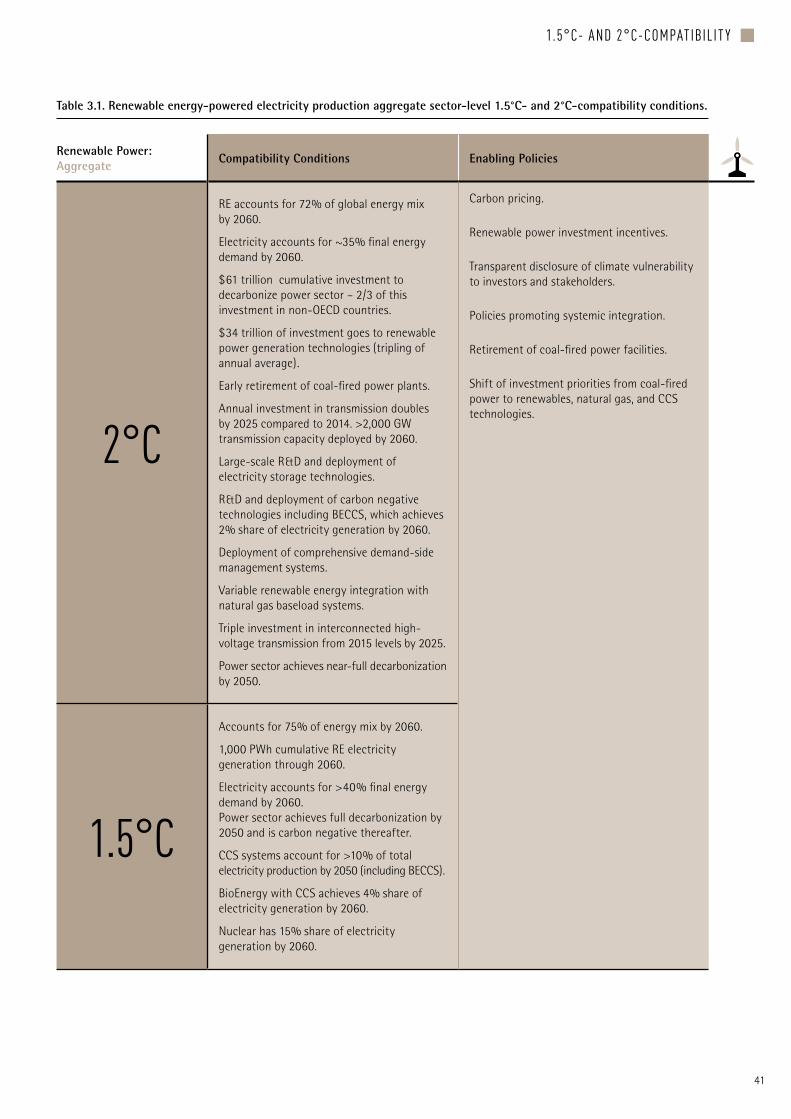

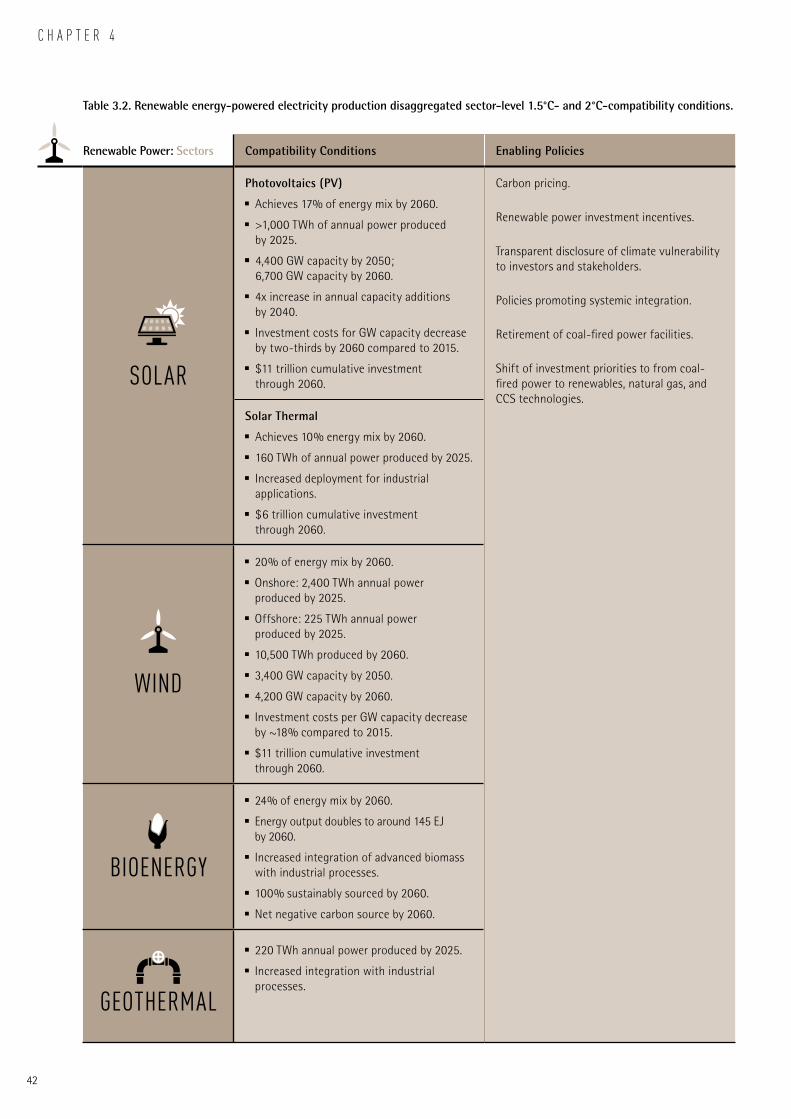

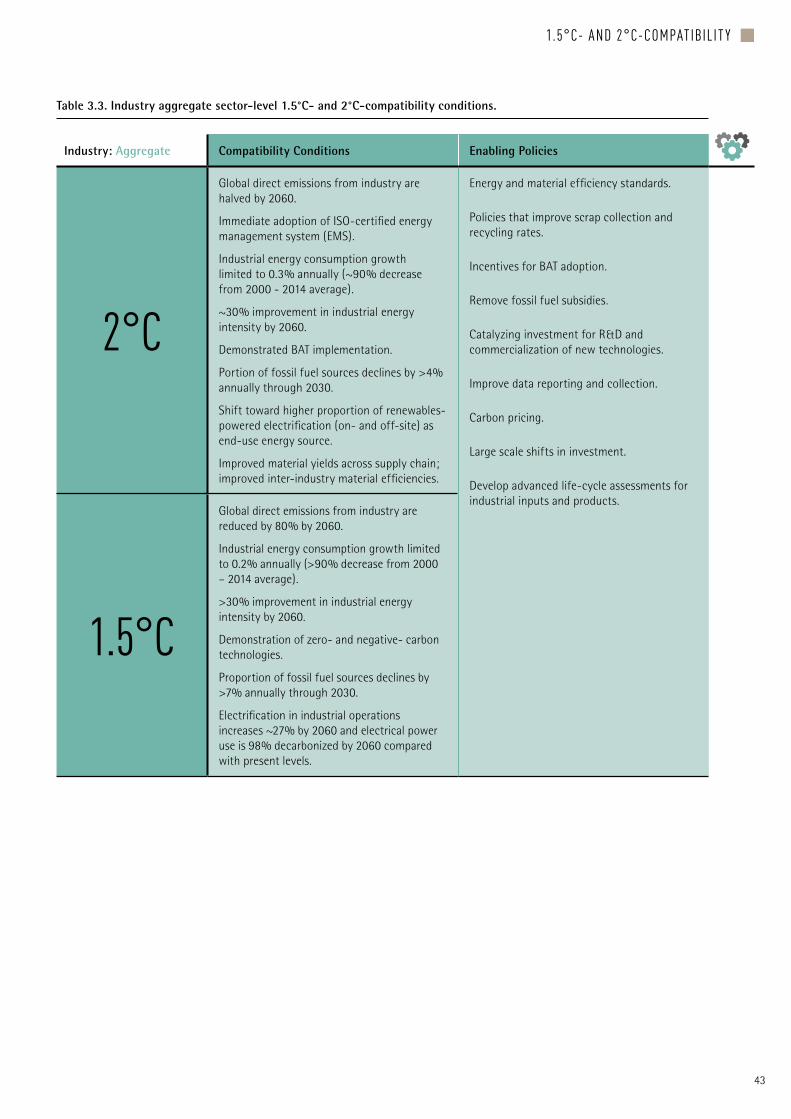

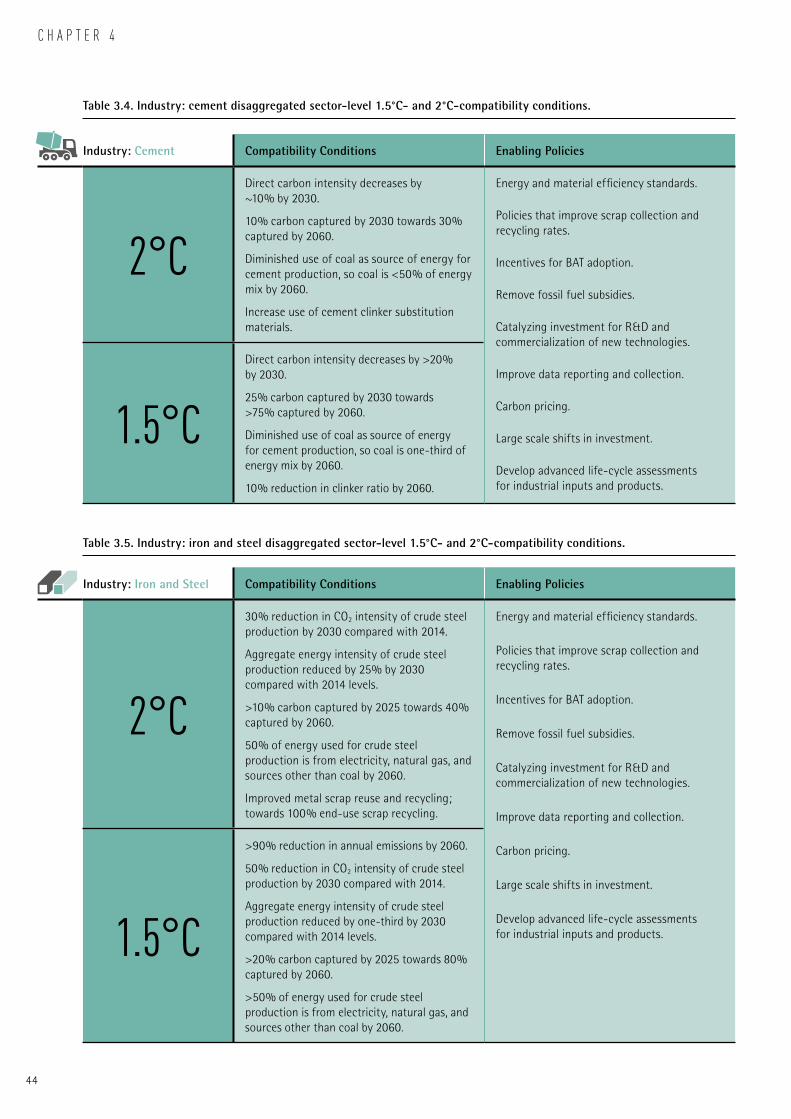

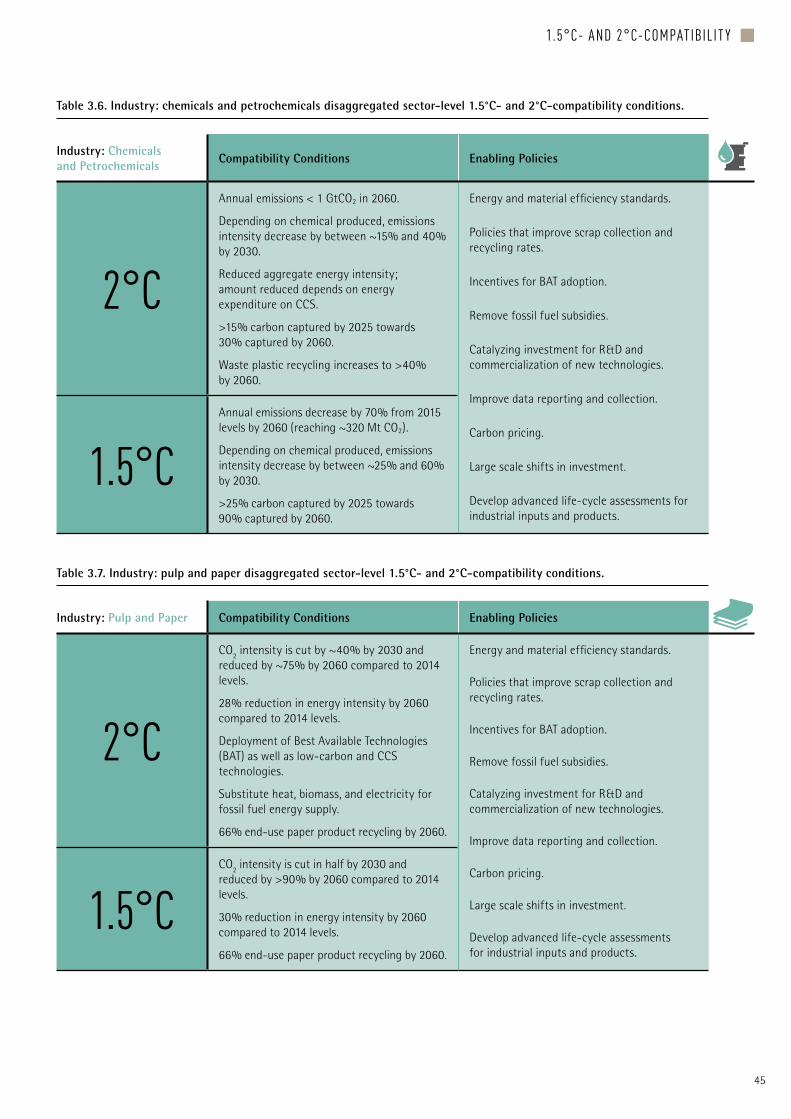

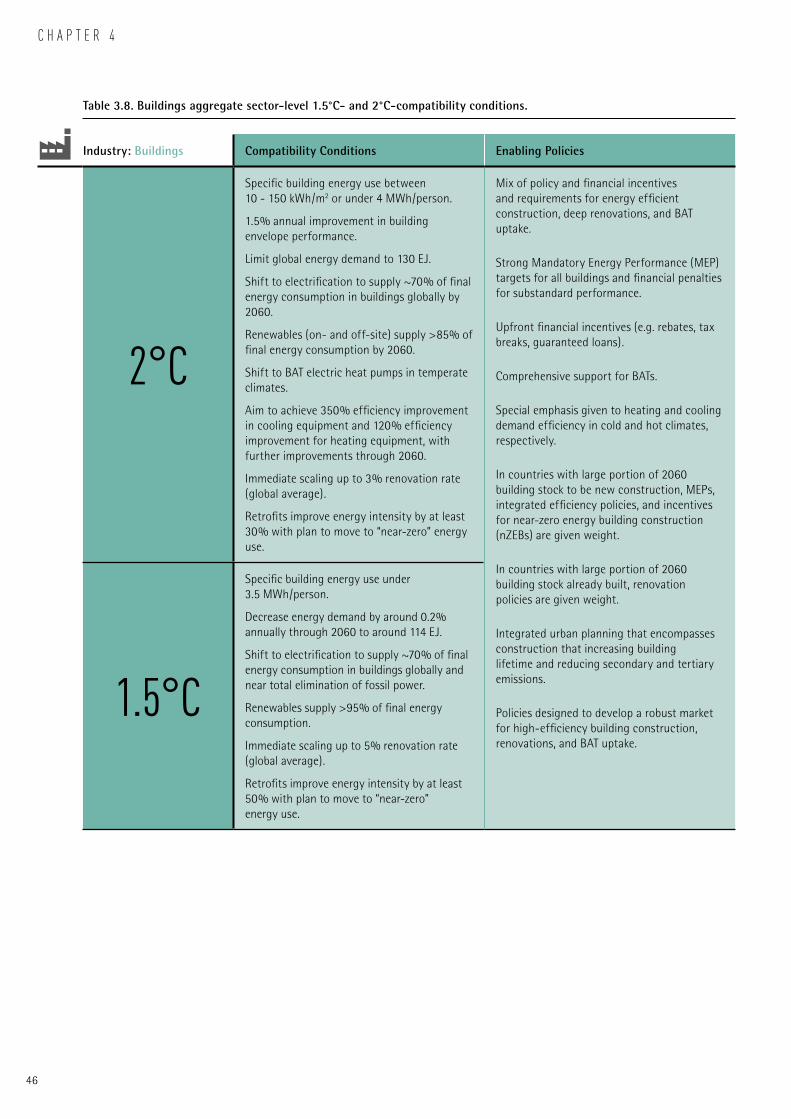

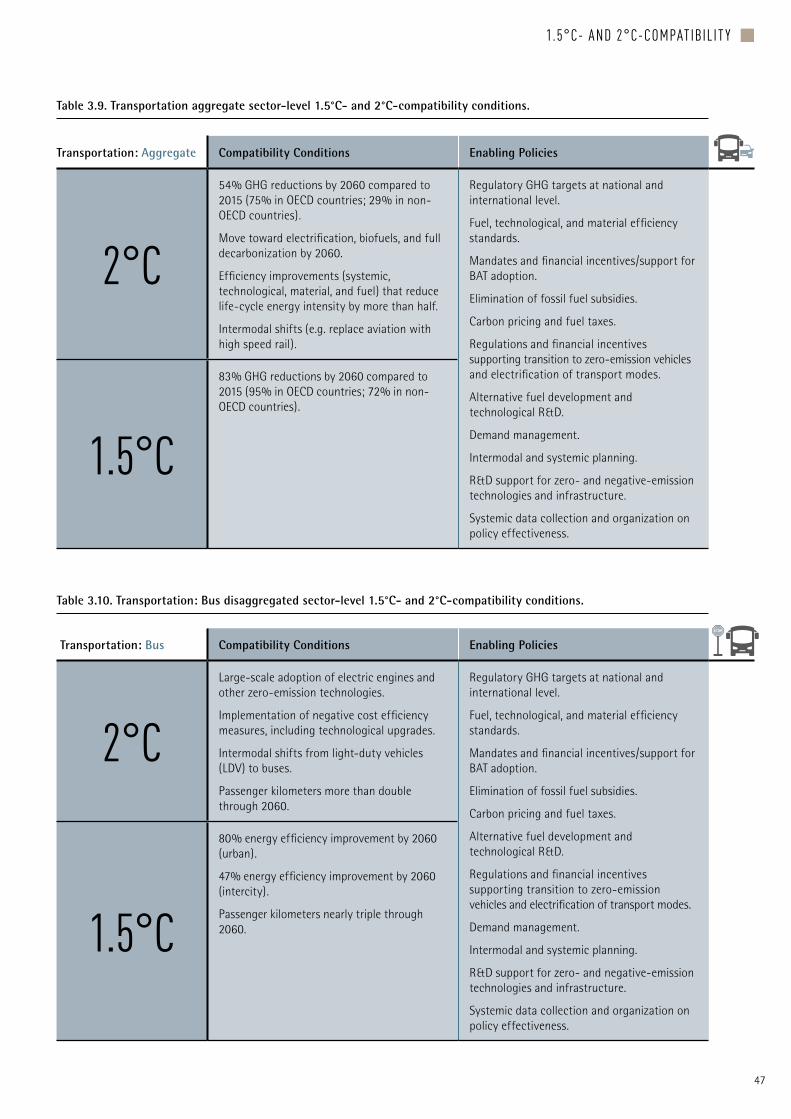

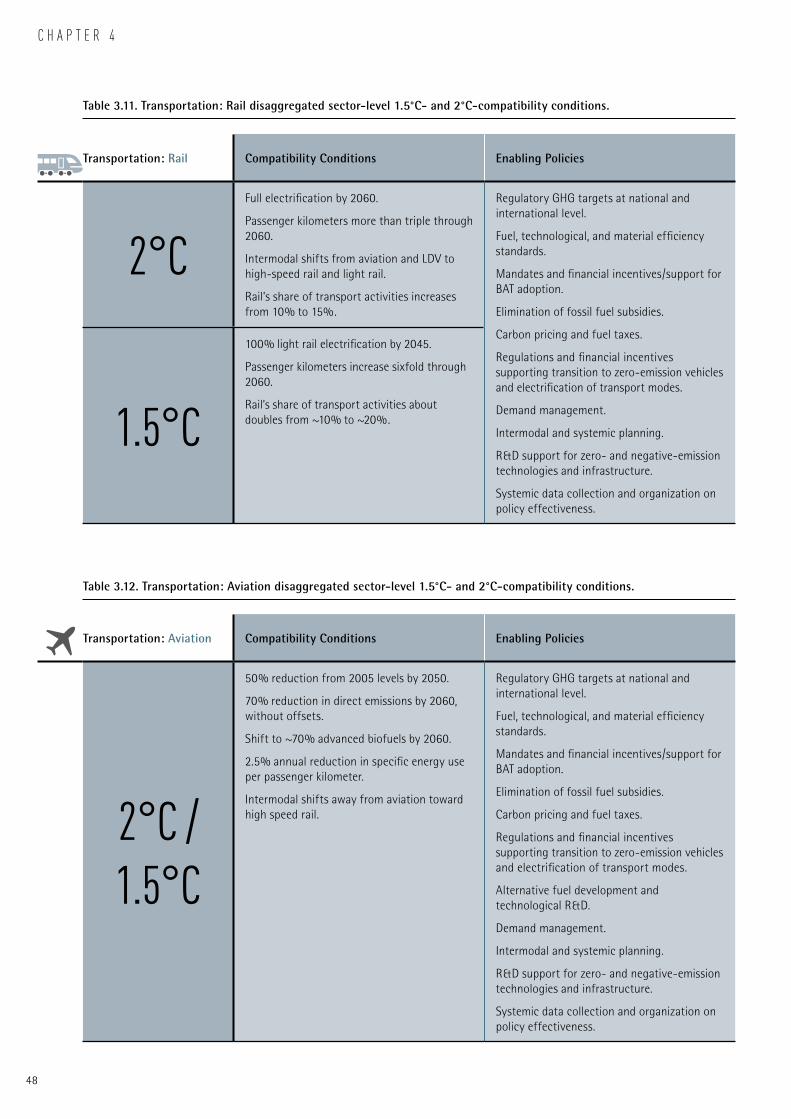

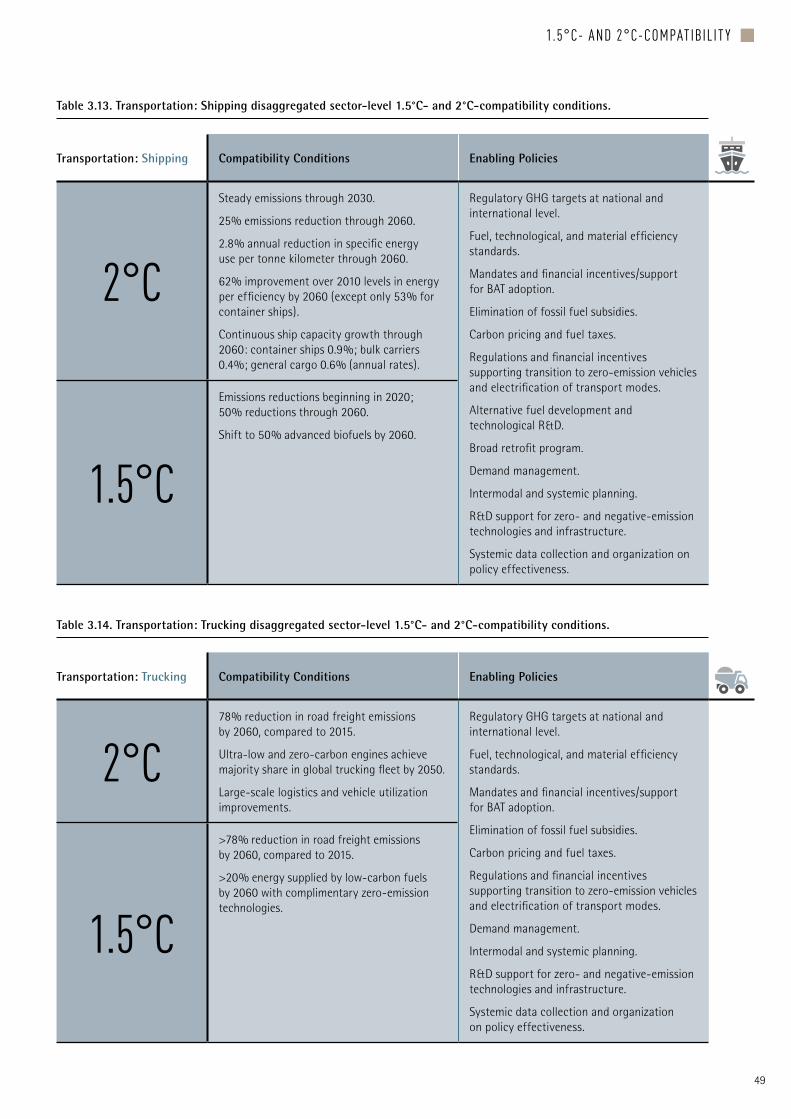

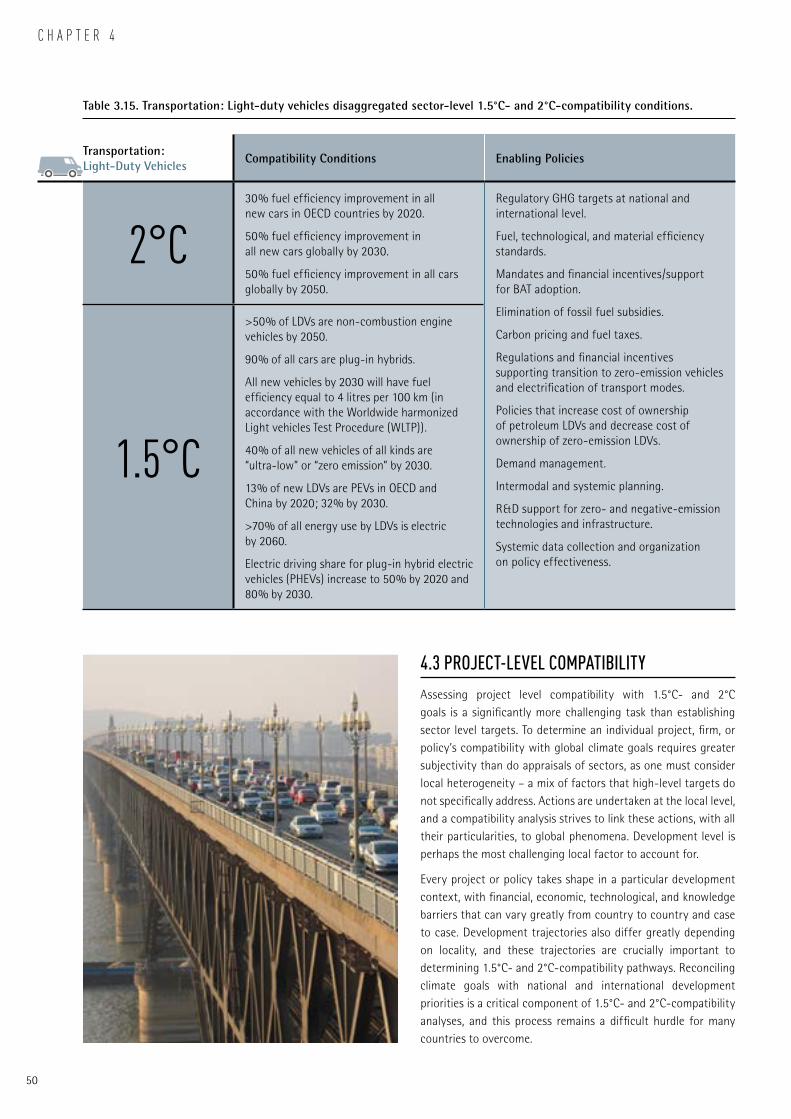

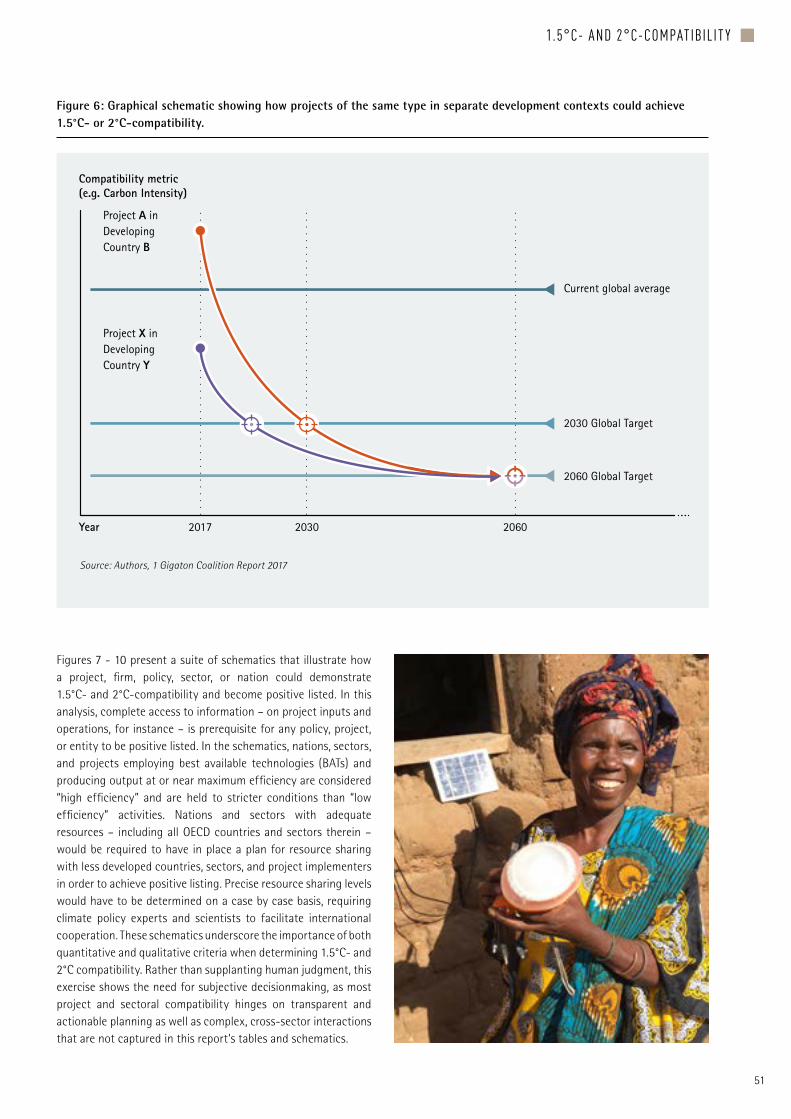

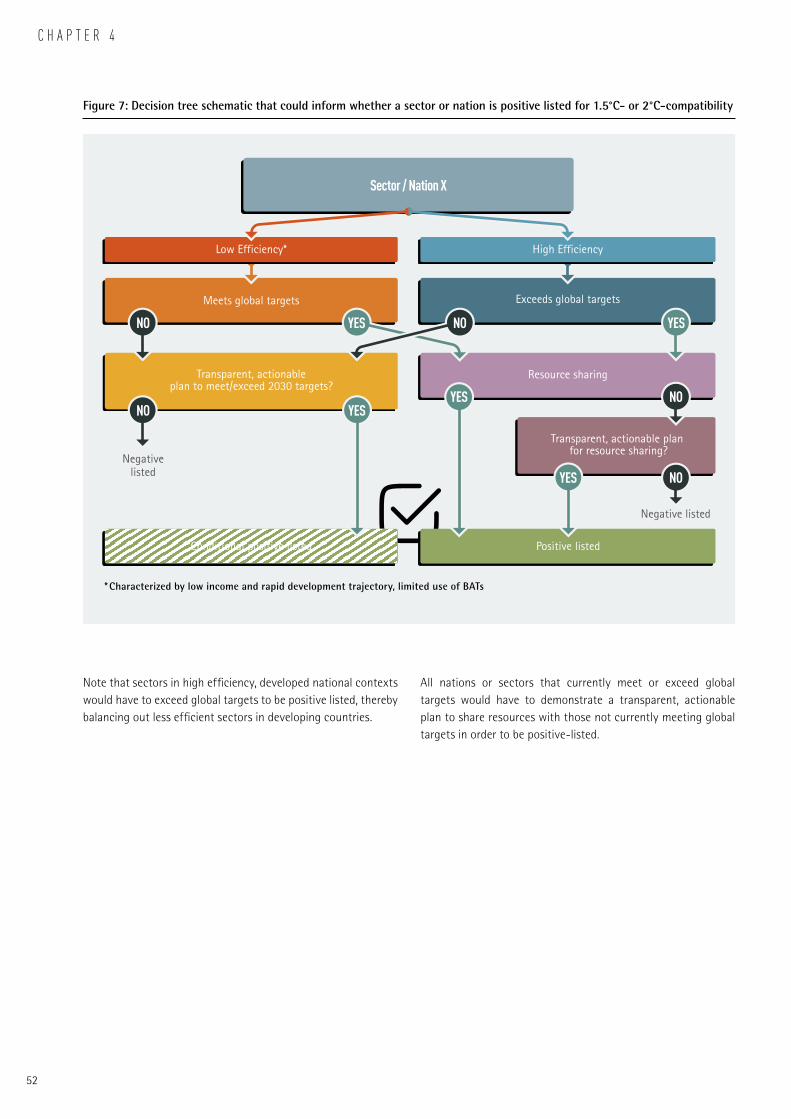

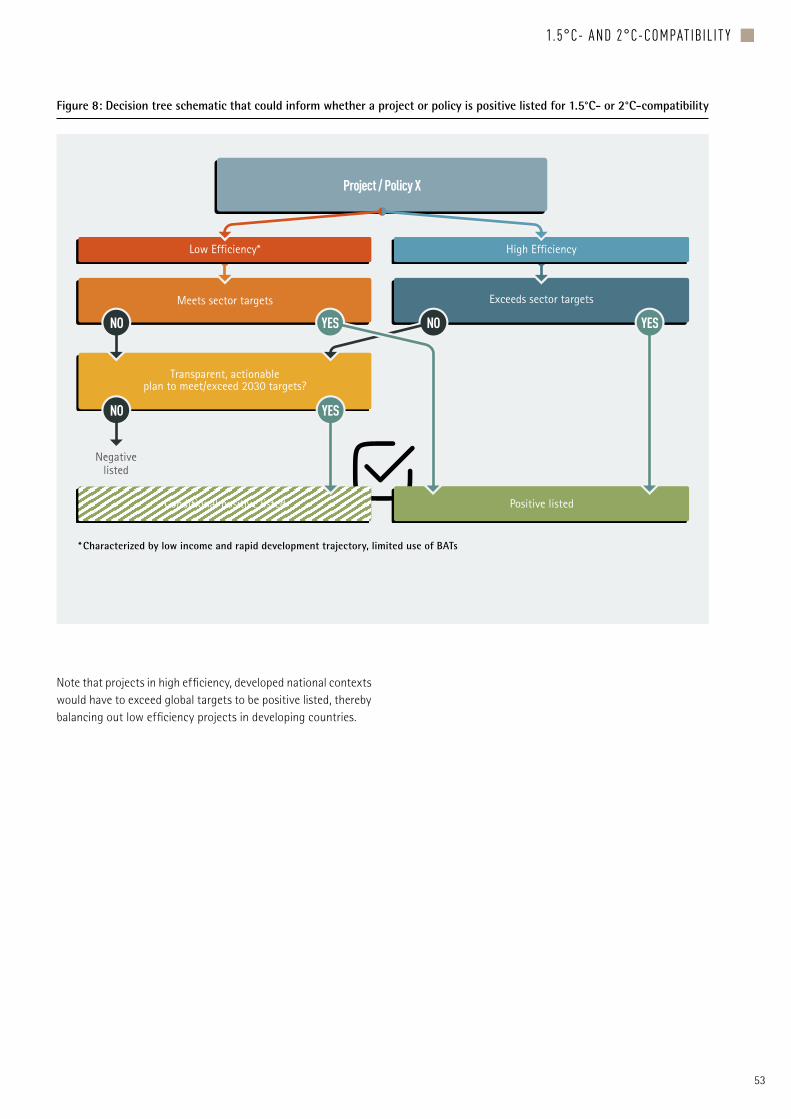

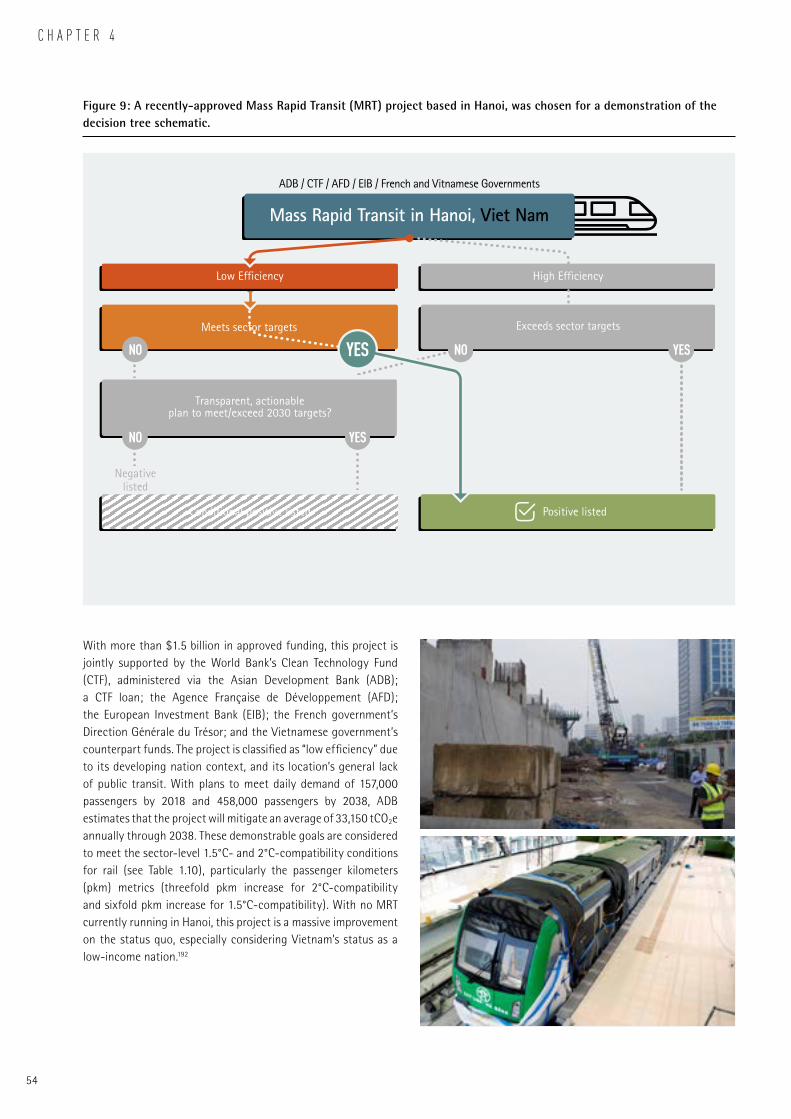

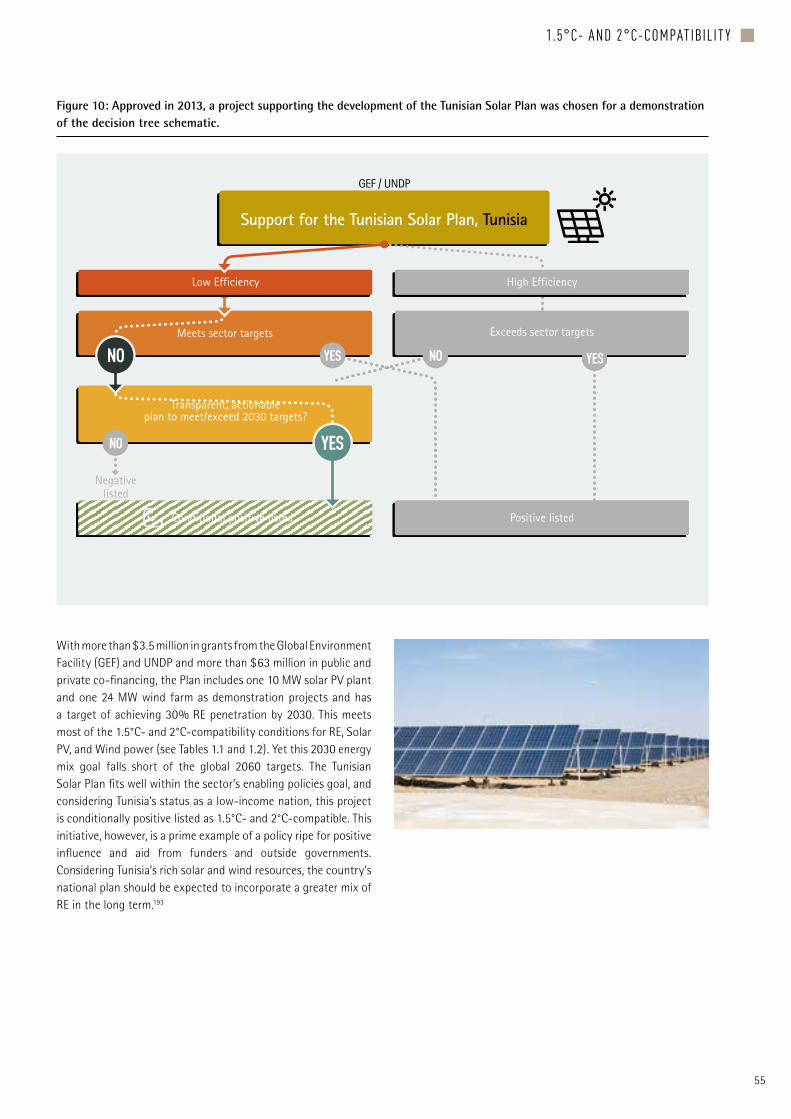

Criteria for sector-level compatibility with 15degC and 2degC goals were developed to evaluate emission savings from projects (Tables 31 - 315) The sectoral criteria are displayed in compatibility tables with each table listing 15degC- and 2degC-compatibility conditions drawn largely from the International Energy Agencyrsquos (IEA) Energy Technology Perspectives (ETP) 2017 report and its 2degC Scenario (2DS) and Beyond 2degC Scenario (B2DS) Schematics (Figures 7 ndash 10) demonstrate how the sectoral compatibility criteria could be applied at the project firm or policy level to identify projects considered 15degC- or 2degC-compatible Two actual projects selected from this reportrsquos RE and EE database are used as proofs of concept Information sharing and data availability prove to be key challenges to broadening the application of this approach

GtCO2e

Reductions from 273 supported projects

implemented during 2005 ndash 2016

analyzed in this report

Reductions by all supported projects

2005 - 2016 ($76 billion in total support)

Reductions if support scaled up to US $25 billion annually

through 2020

0258 GtCO2e 06 GtCO2e

14 GtCO2e

Figure ES Emission reduction from renewable energy and energy efficiency projects by 2020

9

EXECUTIVE SUMMARY g

City governments are increasingly collaborating with the private sector to address common challenges related to climate change and sustainable development The Intergovernmental Panel on Climate Change (IPCC) has indicated that achieving a 15degC- or 2degC-compatible future is a very challenging task yet almost all the technologies needed to build this future are commercially available today This report shows that many countries are acting to reduce emissions through RE and EE programmes and that when policies are well-designed both local and global communities benefit The six case studies presented in this report describe the social economic and environmental benefits that RE and EE programmes bring to the localities where they are implemented They highlight innovative initiatives implemented in a diverse set of cities and regions

bull NEW DELHIrsquoS municipal government has partnered with Infrastructure Leasing and Financial Services Environment (ILampFS Environment) to build a waste-to-energy plant that will save approximately 82 million tons of greenhouse gas emissions over its 25-year lifespan while reducing the landfillrsquos area and air and water pollution The project helps transition former waste-pickers to new jobs directly hiring 70 people at the new plant and has created a community center that provides support and job training to approximately 200 local women

bull NANJING China worked with the electric vehicle industry to add 4300 electric vehicles to its streets between 2014 and 2015 This transition has helped the city reduce emissions by 246000 tons of carbon dioxide equivalent (CO2e) in 2014 while saving over US $71 million in lower energy bills

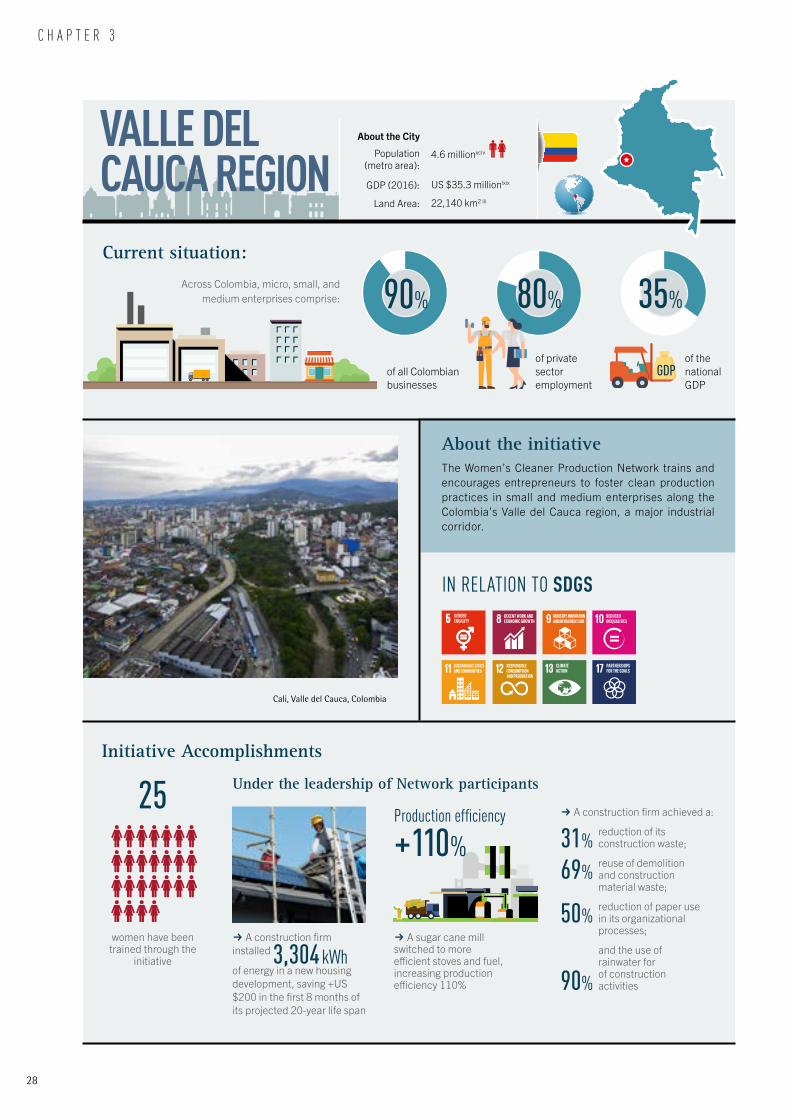

bull In the industrial VALLE DEL CAUCA corridor of Colombia The Womenrsquos Cleaner Production Network developed action plans to reduce industrial pollution and address climate change in small and medium-sized enterprises The initiative has created a host of benefits including a 110 percent increase in enterprise production efficiency and a new residential solar installation program

bull In LAGOS and in many other Nigerian cities private companies are piloting new approaches to make solar energy more accessible and affordable A partnership between a solar start-up and local telecommunications provider has brought solar power to 50000 homes clinics schools and businesses benefiting more than 250000 people and creating 450 new jobs

bull Ugandarsquos capital city KAMPALA has partnered with businesses to scale up an array of clean cooking technology initiatives installing 64 improved eco-stoves in 15 public schools constructing biodigesters in 10 public schools and funding companies that train women and youth to produce low-carbon briquettes from organic waste

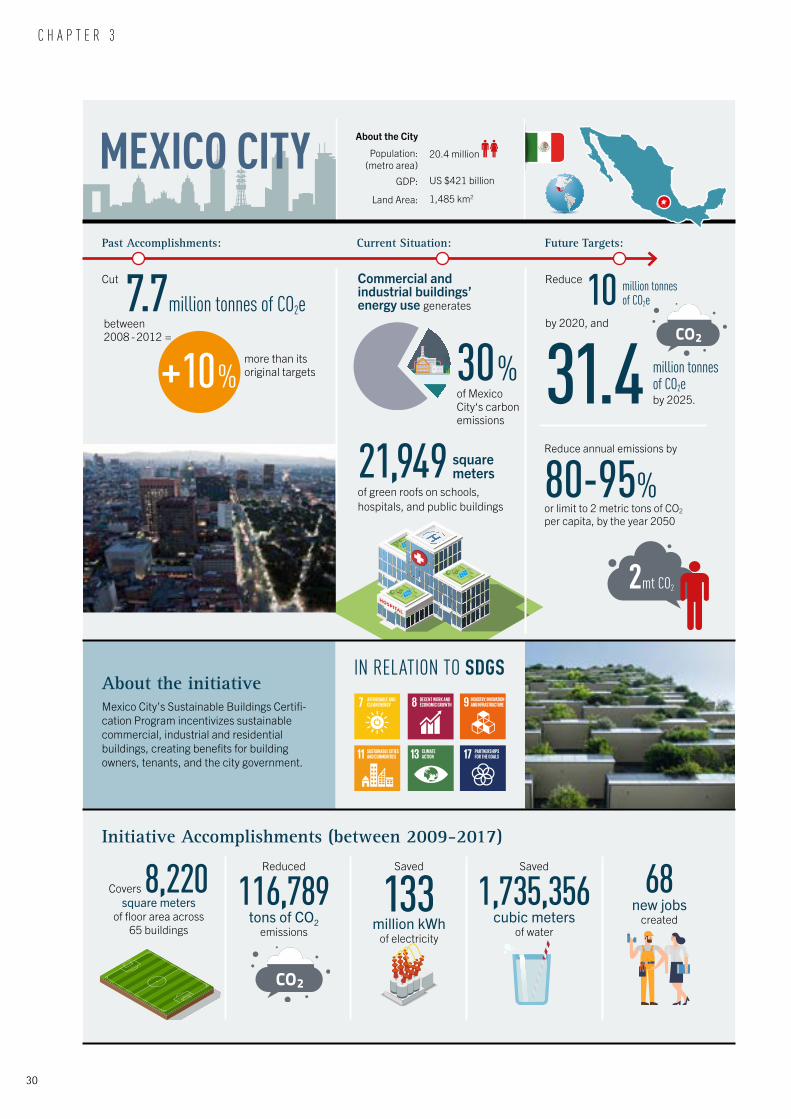

bull MEXICO CITYrsquoS Sustainable Buildings Certification Programme developed and implemented in partnership with the local construction and building industry covers 8220 square meters of floor area across 65 buildings and has reduced 116789 tons of carbon dioxide (CO2) emissions saved 133 million kilowatt-hours (kWh) of electricity and 1735356 cubic meters of potable water and created 68 new jobs between 2009 and 2017

These case studies demonstrate the feasibility and benefits of a low-carbon future through the various RE and EE activities undertaken in cities in collaboration with private sector groups Expanding this type of public-private sector engagement would harness expertise funding technology and data from both arenas to help overcome barriers to action and accelerate the pace of climate action

Governments and non-state actors will gather at COP 23 in November to discern a path forward for implementing the Paris Agreementrsquos central provisions Data sources needed to evaluate progress towards achieving the 15degC or 2degC climate goals are key points under discussion This report provides pertinent information and evidence showing how internationally supported RE and EE projects and initiatives implemented in developing countries are contributing to narrowing the emissions gap ndash the difference between the status quo and the 15degC and 2degC goals The reportrsquos case studies show the social and economic co-benefits associated with these emissions reductions particularly when city governments partner with private companies to enact emissions savings programs These initiatives have great potential to motivate countries and non-state actors to build new channels for collaboration to raise their ambitions and scale up their efforts The 1 Gigaton Coalition will continue to promote RE and EE efforts evaluate their emissions impacts and show how they contribute to achieving both international climate objectives and Sustainable Development Goals (SDGs)

C H A P T E R 1

New Delhi India

New Delhilsquos waste- to-energy initiatives convert more than 50 percent of the citylsquos daily waste into energy and fuel

R Details see page 22

INTRODUCTION

1 Energy-related carbon dioxide (CO2) emissions have stabilized showing no growth in 2016 for the third year in a row yet global energy consumption is predicted to increase 48 percent by 20401 Developing countries where rapid economic growth is the main driver of rising energy demand will account for the vast majority of this future increase in energy consumption1 2

To meet the Paris Agreementrsquos goal to limit global temperature to no more than 2degC and aim to hold warming to 15degC global emissions must peak around 2020 and then rapidly decline in the following three decades approaching zero by 20503 The emissions gap however has widened from last yearrsquos estimates The 2017 United Nations Environment Programme (UN Environment) Emissions Gap Report finds that by 2030 there will be a gap of 11 ndash 135 GtCO2e between countriesrsquo Paris climate pledges and the goal to limit global temperature rise to 2degC The gap widens to 16 ndash 19 GtCO2e when considering the 15degC goal4

11

INTRODUCTION g

Renewable energy (RE) and energy efficiency (EE) projects in developing countries are crucial means of narrowing the emissions gap and decarbonzing future energy growth In 2016 a record 1385 gigawatts (GW) of new capacity of RE was installed mostly in developing countries and emerging economies some of which have become key market players5 Evaluating how RE and EE projects translate to measurable emissions reductions to closing the emissions gap and to creating a 15degC or 2degC compatible future is the focus of this report

The climate imperative is clear we must act now and with ambition to decarbonize human activities in order to meet global climate goals The latest climate scenarios produced by the worldrsquos leading international scientific bodies show that our window to prevent dangerous global warming is rapidly narrowing as humanityrsquos carbon budget ndash the total amount of carbon dioxide that can be emitted for a likely chance of limiting global temperature rise ndash diminishes year on year The Intergovernmental Panel on Climate Change (IPCC) found in its Fifth Assessment Report (2014) that the world will warm by between 37degC to 48degC by 2100 if humanity pursues a ldquobusiness as usualrdquo pathway This level of warming scientists agree would be disastrous for human civilization To give us a better than 66 chance to limit global warming below 2degC ndash the scientific communityrsquos agreed upon threshold for what societies could reasonably manage ndash the IPCC reports that atmospheric CO2 concentrations cannot exceed 450 ppm by 2100 This limit means that the worldrsquos carbon budget through the year 2100 is less than 1000 Gt CO2e Considering a 15degC limit our carbon budget falls to under 600 Gt CO2e through 21006

UN Environmentrsquos Emissions Gap Report 2017 which focuses on the gap between the emissions nations have pledged to reduce and the mitigation needed to meet global temperature goals developed a ldquolikelyrdquo (gt66 chance of achieving the target) 2degC warming model under which annual global GHG emissions would need to stabilize around 52 GtCO2e through 2020 and then fall precipitously to 42 GtCO2e by 2030 and 23 GtCO2e by 2050 To have a greater than 50 chance of containing warming to 15degC the 2017 Gap Report projects a greater drop in annual emissions to 36 GtCO2e by 2030 ndash a significantly lower estimate than what the 2016 Emissions Gap report suggested Under both scenarios annual global emissions appear to go negative ndash meaning that more carbon is absorbed than produced ndash by 2100 These projections are starkly divergent from baseline business as usual emissions projections as well as scenarios that account for the Nationally Determined Contributions (NDCs) that countries pledged in the Paris Agreement By 2030 there is a 135 GtCO2e difference between the annual emissions in the 2017 Gap

Reportrsquos unconditional NDC scenarios and its 2degC trajectory and a 19 GtCO2e gap between the NDCs and 15degC trajectories7

This gap points to an urgent need to increase the ambition scope and scale of carbon mitigation efforts worldwide Each sector in every nation must lead the way with ambitious actions to decarbonize and governments must enact plans and policies for sharp emissions reductions if we are to meet the 15degC or 2degC targets Nearly one-half of lower middle income countries (GNI per capita between US $1006 and $3955) and one-fourth of low income countries (GNI per capita less than US $1005) have made RE a primary focus of their NDCs8 One-third of lower middle income countries and 19 percent of low-income countries have adopted EE as a main focal instrument in their NDCs9 Many of these countries lack energy access for the majority of their population suffer from the effects of poor indoor and outdoor air quality and are striving to rapidly develop their economies to reduce poverty ndash needs that can be partly addressed through RE and EE efforts Intergovernmental coordination and support are key catalysts for the requisite RE and EE initiatives as developed nations transfer expertise technologies and funding to developing countries to create enabling environments for carbon-neutral growth Yet beyond global emissions reduction goals what specific targets should nations sectors and individual firms use to guide their actions How do funding organizations policymakers and implementing groups know at what point their operations are compatible with the 15degC and 2degC targets

The growth in RE and EE projects in developing countries in the last decade demonstrates the potential for these efforts to contribute to global climate mitigation and to narrow the emissions gap A lack of data and harmonized accounting methodology however have prevented the bilateral and multilateral organizations that support these efforts from systematically evaluating their impact The 1 Gigaton Coalition supports these organizationsrsquo efforts in developing countries where growth in RE and EE projects have potential to transition economies to low-carbon trajectories The Coalition works to build a robust knowledge base and support the development of harmonized GHG accounting methods These tools will aid analysis of RE and EE initiatives that are not

12

INTRODUCTION gC H A P T E R 1

+2degC

First Report | 2015

Narrowing the Emissions Gap Contributions from renewable energy and energy efficiency activities

+2degC

Second Report

Renewable energy and energy efficiency in developing countries contributions to reducing global emissions

2016

directly captured in UN Environmentrsquos Emissions Gap Report or in other assessments of global mitigation efforts Through the compilation and assessment of developing country RE and EE efforts between countries partners and collaborative initiatives the 1 Gigaton Coalition promotes these efforts and strives to measure their contribution to reducing global greenhouse gas emissions reductions

PREVIOUS 1 GIGATON COALITION REPORTSThe 1 Gigaton Coalition has released two reports to date The 1 Gigaton Coalition 2015 report aimed to quantify RE and EE contributions to narrowing the 2020 emissions gap The 2015 report was the first of its kind to assess and quantify RE and EE projectsrsquo global climate mitigation potential This analysis used a comparison between the IEA World Energy Outlook (WEO) current policy scenarios and a no-policy scenario derived from the IPCC scenarios database to estimate the energy sectorrsquos total emissions reductions The analysis found that EE and RE projects in developing countries could result in emission reductions on the order of 4 GtCO2 in 2020 compared to a no-policy baseline scenario

The 1 Gigaton Coalition 2016 report refined the approach developed in the inaugural 2015 report expanding the database of internationally supported RE and EE projects in developing countries from 42 to 224 The larger database includes projects implemented between 2005 and 2015 receiving direct foreign support totalling US $28 billion These projects were estimated to reduce GHG emissions by an aggregate 0116 GtCO2 annually in 2020 Avoided GHG emissions were calculated by multiplying the annual energy saved or substituted by a project (determined for RE projects by using the power generation capacity and the technology- and country-specific capacity factors and for EE projects through a projectrsquos documentation) by country-specific grid electricity CO2 emission factors The 2016 report estimated that all internationally supported RE and EE projects would reduce emissions by up to 04 GtCO2 annually in 2020 and that if public finance goals for climate mitigation were met supported projects could reduce emissions by 1 GtCO2 per year in 2020

OVERVIEW OF THE 1 GIGATON COALITION 2017 REPORTThe 1 Gigaton Coalition 2017 report builds upon the first two reports further expanding the database of RE and EE projects from developing countries to calculate the mitigation impact of 273 internationally supported projects in developing countries These projects including 197 RE 62 EE and 14 RE and EE activities are located in 99 countries and supported by 12 bilateral funding agencies and 16 multilateral development banks and partnerships They are categorized for the technologies used to replace fossil fuel energy production with clean energy (ie solar wind biomass and hydroelectricity) and reduce energy consumption in the industrial building and transport sectors In total these projects received US $32 billion in direct foreign support

Evaluating RE and EE projectsrsquo mitigation impact is important to shed light on whether these efforts are reducing global emissions An essential question is whether these efforts lead to long-term decarbonization or low-carbon pathways that are compatible with global goals to limit temperature rise to 15degC and 2degC The 1 Gigaton Coalition 2017 report synthesizes a methodological approach to evaluate the 15degC- and 2degC-compatibility of RE and EE projects intending to guide bilateral and multilateral partners and implementing countries in determining which policies individual projects and entire sectors are consistent with 15degC and 2degC scenarios Drawing from other research initiatives and the International Energy Agencyrsquos (IEA) 2017 Energy Technologies Perspective (ETP) report this analysis provides criteria for 15degC and 2degC-compatibility at the sector level and demonstrates how these criteria could be applied to RE and EE projects

Providing real world examples of RE and EE initiatives in developing countries this report features six in-depth case studies of ongoing programmes and policies in cities throughout the world These case studies demonstrate the compounding benefits to human health the economy and environment that result from smartly planned RE and EE efforts The cases feature collaborative initiatives in which the public sector and private companies work together to develop implement and scale climate action

This report is organized as follows

Chapter 2 provides an overview of the current landscape of RE and EE policies in developing countries Chapter 3 presents six case studies that explore RE and EE programmes that engage the private sector to develop and implement renewable energy and energy efficiency activities The case studies highlight the multiple benefits these initiatives garner across the various cities and regions where they are implemented This chapter also includes a discussion by Thomson Reuters of the emerging low-carbon business paradigm Chapter 4 describes the 15degC- and 2degC-compatibility methods and applications developed for this report providing sector-level compatibility tables and project-level guidance Chapter 5 provides an assessment of the GHG emissions mitigation from RE and EE projects in developing countries based on calculations derived from a project database built for this report Chapter 6 concludes with the reportrsquos key implications for policymakers RE and EE supporting partners and climate actors

Nanjing China

Nanjing was one of the fastest adopters of electric vehicles and has become an important hub for the industry

R Details see page 26

DE VELOPING COUNTRIESrsquo EFFORTS AND ACHIE VEMENTS gC H A P T E R 2

DEVELOPING COUNTRIESrsquo EFFORTS AND ACHIEVEMENTS IN ENERGY EFFICIENCY AND RENEWABLE ENERGY2 This chapter describes the role of policymakers in promoting renewable energy and energy efficiency initiatives in developing countries Data collected by REN21 ndash the global multistakeholder renewable energy policy network ndash is used to illustrate the current status of targets and policies

14

C H A P T E R 2

21 POLICY DEVELOPMENTRenewable energy (RE) and energy efficiencyrsquos (EE) increasingly vital role in the rapid transformation of the energy sectors of industrialized emerging and developing countries continues to be stimulated in part by government actions to incentivize new technology development and deployment Policymakers have adopted a mix of policies and targets to deploy RE and EE to expand energy access provide more reliable energy services and meet growing energy demand while often simultaneously seeking to advance research and development into more advanced fuels and technologies

Recognizing the complementary nature of RE and EE at least 103 countries addressed EE and RE in the same government agency including at least 79 developing and emerging countries while an estimated 81 countries had policies or programmes combining support to both sets of technologies including approximately 75 developing or emerging countries

Adopted together RE and EE can more rapidly help meet national development goals including increasing energy security enhancing industrial competitiveness reducing pollution and environmental degradation expanding energy access and driving economic growth This can be achieved through sector-wide planning such as Chinarsquos 13th Five Year Plan adopted in 2016 which includes specific goals for both RE and EE

Indirect policy support including the removal of fossil fuel subsidies and the enactment of carbon pricing mechanisms such as carbon taxes emission trading systems and crediting approaches can also benefit the RE and EE sectors Carbon pricing policies if designed

effectively may incentivize renewable energy development and deployment across sectors by increasing the comparative costs of higher-emission technologies The removal of fossil fuel subsidies also may level the financial playing field for energy technologies as fossil fuel subsidies remain significantly higher than subsidies for renewables with estimates of the former being at least more than twice as high as those for RE This estimate rises to ten times higher when the cost of externalities and direct payments are included

Developing countries led the way on initiating subsidy reform in 2016 with 19 countries adopting some form of reduction or removal Similarly by year-end 2016 Group of 20 (G20) and Asia-Pacific Economic Cooperation (APEC) initiatives had led to 50 countries committing to phasing out fossil fuel subsidies

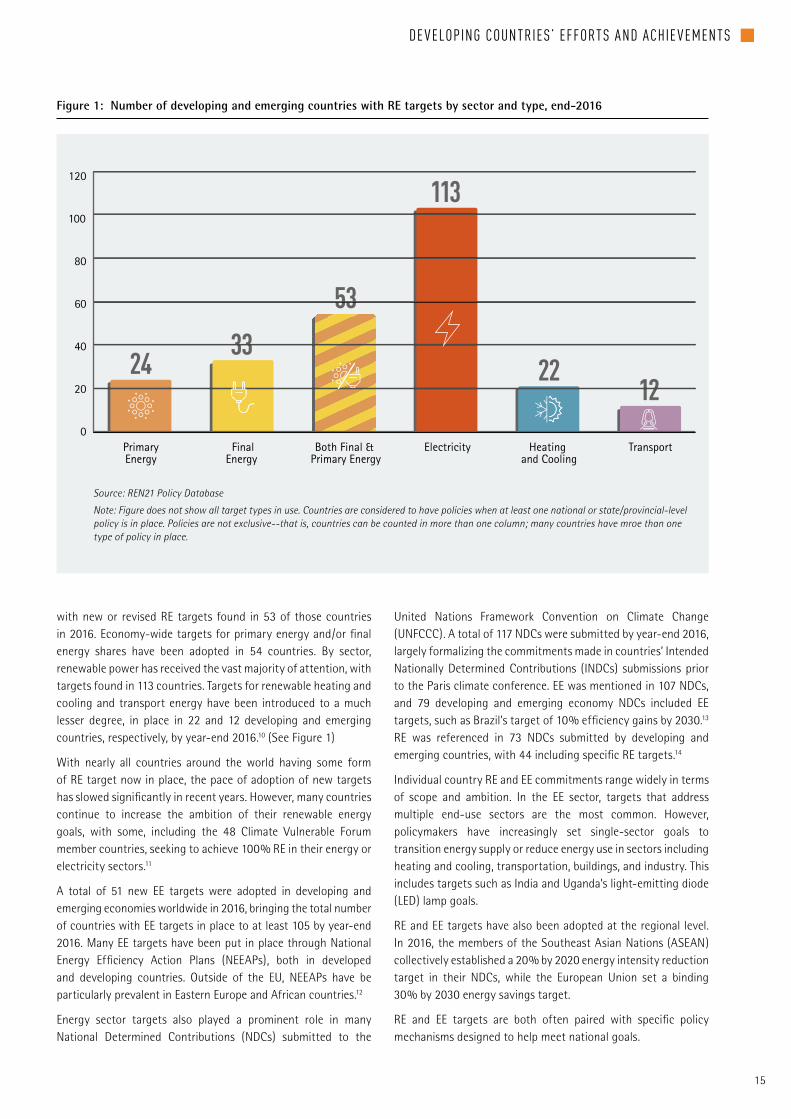

211 TARGETSTargets are an important tool used by policymakers to outline development strategies and encourage investment in EE and RE technologies Targets are set in a variety of ways from all-encompassing economy-wide shares of capacity generation or efficiency to calling for specific technology deployments or new developments in targeted sectors Similarly policymakers at all levels from local to stateprovincial regional and national have adopted targets to outline sector development priorities

Nearly all nations around the world have now adopted RE targets aiming for specified shares production or capacity of RE technologies Targets for RE at the national or stateprovincial level are now found in 124 developing and emerging countries

15

DE VELOPING COUNTRIESrsquo EFFORTS AND ACHIE VEMENTS g

24 33

113

53

2212

TransportHeating and Cooling

Electricity Both Final amp Primary Energy

FinalEnergy

PrimaryEnergy

Number of developing and emerging economies with RE targets by sector and type end-2016

0

20

40

60

80

120

100

Figure 1 Number of developing and emerging countries with RE targets by sector and type end-2016

Source REN21 Policy Database

Note Figure does not show all target types in use Countries are considered to have policies when at least one national or stateprovincial-level policy is in place Policies are not exclusive--that is countries can be counted in more than one column many countries have mroe than one type of policy in place

with new or revised RE targets found in 53 of those countries in 2016 Economy-wide targets for primary energy andor final energy shares have been adopted in 54 countries By sector renewable power has received the vast majority of attention with targets found in 113 countries Targets for renewable heating and cooling and transport energy have been introduced to a much lesser degree in place in 22 and 12 developing and emerging countries respectively by year-end 201610 (See Figure 1)

With nearly all countries around the world having some form of RE target now in place the pace of adoption of new targets has slowed significantly in recent years However many countries continue to increase the ambition of their renewable energy goals with some including the 48 Climate Vulnerable Forum member countries seeking to achieve 100 RE in their energy or electricity sectors11

A total of 51 new EE targets were adopted in developing and emerging economies worldwide in 2016 bringing the total number of countries with EE targets in place to at least 105 by year-end 2016 Many EE targets have been put in place through National Energy Efficiency Action Plans (NEEAPs) both in developed and developing countries Outside of the EU NEEAPs have be particularly prevalent in Eastern Europe and African countries12

Energy sector targets also played a prominent role in many National Determined Contributions (NDCs) submitted to the

United Nations Framework Convention on Climate Change (UNFCCC) A total of 117 NDCs were submitted by year-end 2016 largely formalizing the commitments made in countriesrsquo Intended Nationally Determined Contributions (INDCs) submissions prior to the Paris climate conference EE was mentioned in 107 NDCs and 79 developing and emerging economy NDCs included EE targets such as Brazilrsquos target of 10 efficiency gains by 203013 RE was referenced in 73 NDCs submitted by developing and emerging countries with 44 including specific RE targets14

Individual country RE and EE commitments range widely in terms of scope and ambition In the EE sector targets that address multiple end-use sectors are the most common However policymakers have increasingly set single-sector goals to transition energy supply or reduce energy use in sectors including heating and cooling transportation buildings and industry This includes targets such as India and Ugandarsquos light-emitting diode (LED) lamp goals

RE and EE targets have also been adopted at the regional level In 2016 the members of the Southeast Asian Nations (ASEAN) collectively established a 20 by 2020 energy intensity reduction target in their NDCs while the European Union set a binding 30 by 2030 energy savings target

RE and EE targets are both often paired with specific policy mechanisms designed to help meet national goals

16

C H A P T E R 2

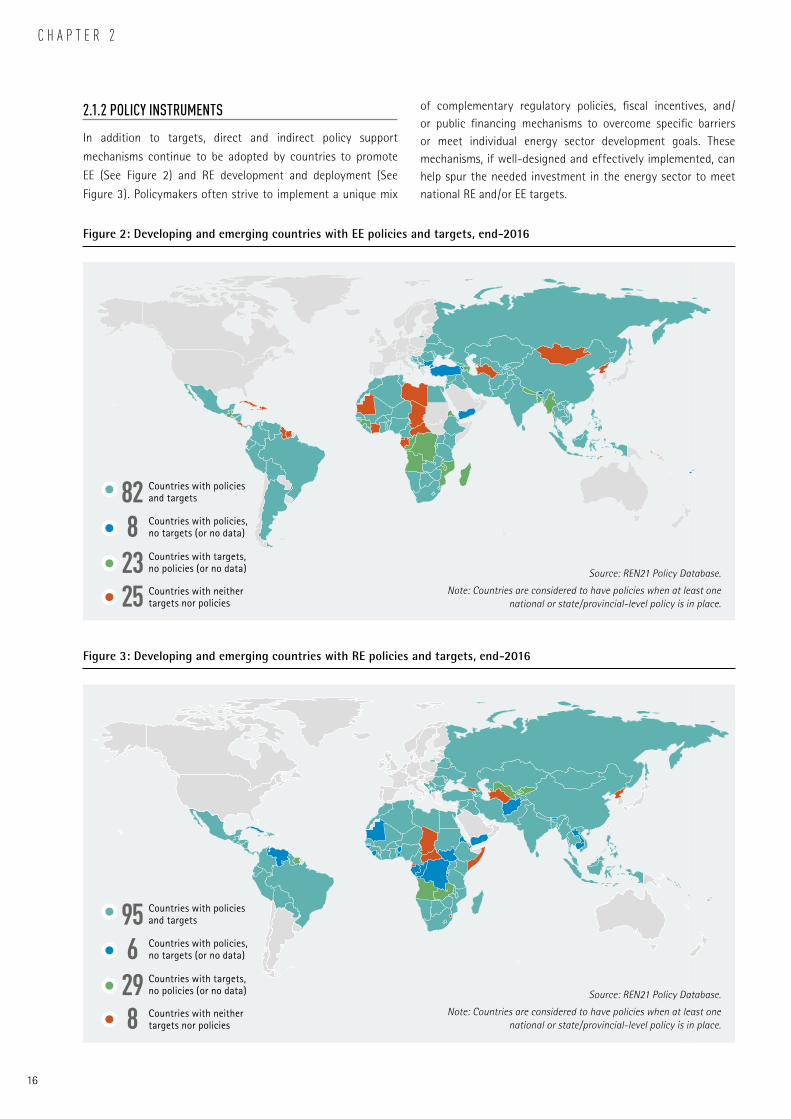

Countries with policiesand targets

Countries with policiesno targets (or no data)

828

Countries with targetsno policies (or no data)23Countries with neither targets nor policies25

Figure 2 Developing and emerging countries with EE policies and targets end-2016

Source REN21 Policy Database

Note Countries are considered to have policies when at least one national or stateprovincial-level policy is in place

Countries with policiesand targets

Countries with policiesno targets (or no data)

956

Countries with targetsno policies (or no data)29

8 Countries with neithertargets nor policies

Figure 3 Developing and emerging countries with RE policies and targets end-2016

Source REN21 Policy Database

Note Countries are considered to have policies when at least one national or stateprovincial-level policy is in place

212 POLICY INSTRUMENTS

In addition to targets direct and indirect policy support

mechanisms continue to be adopted by countries to promote

EE (See Figure 2) and RE development and deployment (See

Figure 3) Policymakers often strive to implement a unique mix

of complementary regulatory policies fiscal incentives andor public financing mechanisms to overcome specific barriers or meet individual energy sector development goals These mechanisms if well-designed and effectively implemented can help spur the needed investment in the energy sector to meet national RE andor EE targets

17

DE VELOPING COUNTRIESrsquo EFFORTS AND ACHIE VEMENTS g

Number of mandatory targets

Number of new targets

TOTAL TARGETS

Number of awareness campaigns

Number of funds

Number of new policies

TOTAL POLICIES

0 4020 60 80 100 120

2851

105

4740

4190

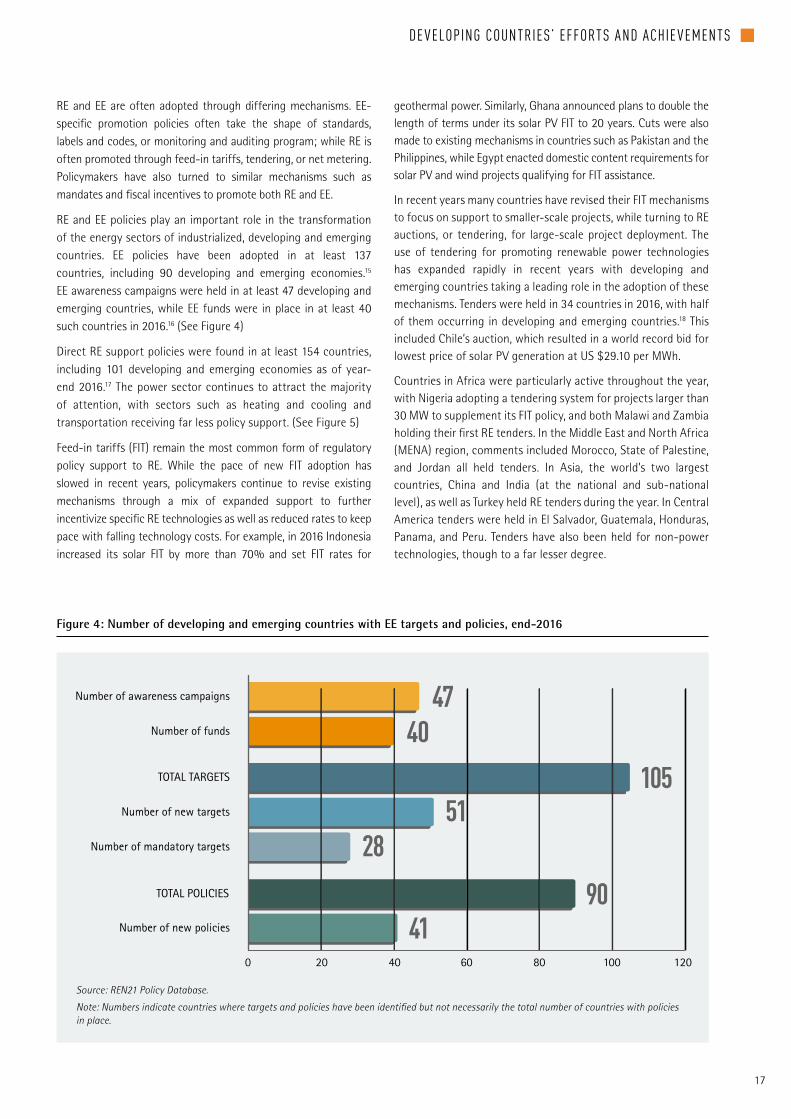

Figure 4 Number of developing and emerging countries with EE targets and policies end-2016

Source REN21 Policy Database

Note Numbers indicate countries where targets and policies have been identified but not necessarily the total number of countries with policies in place

RE and EE are often adopted through differing mechanisms EE-specific promotion policies often take the shape of standards labels and codes or monitoring and auditing program while RE is often promoted through feed-in tariffs tendering or net metering Policymakers have also turned to similar mechanisms such as mandates and fiscal incentives to promote both RE and EE

RE and EE policies play an important role in the transformation of the energy sectors of industrialized developing and emerging countries EE policies have been adopted in at least 137 countries including 90 developing and emerging economies15 EE awareness campaigns were held in at least 47 developing and emerging countries while EE funds were in place in at least 40 such countries in 201616 (See Figure 4)

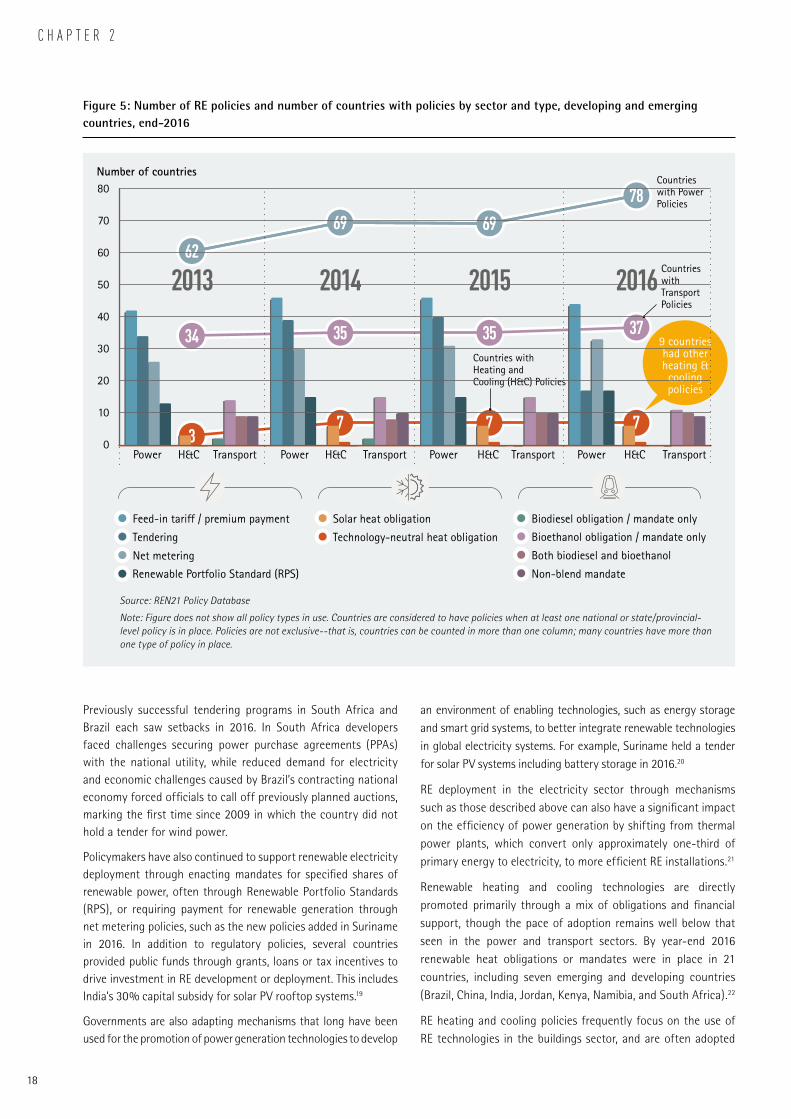

Direct RE support policies were found in at least 154 countries including 101 developing and emerging economies as of year-end 201617 The power sector continues to attract the majority of attention with sectors such as heating and cooling and transportation receiving far less policy support (See Figure 5)

Feed-in tariffs (FIT) remain the most common form of regulatory policy support to RE While the pace of new FIT adoption has slowed in recent years policymakers continue to revise existing mechanisms through a mix of expanded support to further incentivize specific RE technologies as well as reduced rates to keep pace with falling technology costs For example in 2016 Indonesia increased its solar FIT by more than 70 and set FIT rates for

geothermal power Similarly Ghana announced plans to double the length of terms under its solar PV FIT to 20 years Cuts were also made to existing mechanisms in countries such as Pakistan and the Philippines while Egypt enacted domestic content requirements for solar PV and wind projects qualifying for FIT assistance

In recent years many countries have revised their FIT mechanisms to focus on support to smaller-scale projects while turning to RE auctions or tendering for large-scale project deployment The use of tendering for promoting renewable power technologies has expanded rapidly in recent years with developing and emerging countries taking a leading role in the adoption of these mechanisms Tenders were held in 34 countries in 2016 with half of them occurring in developing and emerging countries18 This included Chilersquos auction which resulted in a world record bid for lowest price of solar PV generation at US $2910 per MWh

Countries in Africa were particularly active throughout the year with Nigeria adopting a tendering system for projects larger than 30 MW to supplement its FIT policy and both Malawi and Zambia holding their first RE tenders In the Middle East and North Africa (MENA) region comments included Morocco State of Palestine and Jordan all held tenders In Asia the worldrsquos two largest countries China and India (at the national and sub-national level) as well as Turkey held RE tenders during the year In Central America tenders were held in El Salvador Guatemala Honduras Panama and Peru Tenders have also been held for non-power technologies though to a far lesser degree

18

C H A P T E R 2

Number of countries

Power0

10

20

30

40

50

60

70

80

TransportHampC Power TransportHampC Power TransportHampC Power TransportHampC

2013 2014 2015 2016

Feed-in tariff premium payment

Tendering

Net metering

Renewable Portfolio Standard (RPS)

Solar heat obligation

Technology-neutral heat obligation

Biodiesel obligation mandate only

Bioethanol obligation mandate only

Both biodiesel and bioethanol

Non-blend mandate

Countries with PowerPolicies

Countries withTransportPolicies

Countries with Heating and Cooling (HampC) Policies

7

62

34

69

35

69

35

7

78

37

73

9 countries had other heating amp cooling policies

Figure 5 Number of RE policies and number of countries with policies by sector and type developing and emerging countries end-2016

Source REN21 Policy Database

Note Figure does not show all policy types in use Countries are considered to have policies when at least one national or stateprovincial-level policy is in place Policies are not exclusive--that is countries can be counted in more than one column many countries have more than one type of policy in place

Previously successful tendering programs in South Africa and Brazil each saw setbacks in 2016 In South Africa developers faced challenges securing power purchase agreements (PPAs) with the national utility while reduced demand for electricity and economic challenges caused by Brazilrsquos contracting national economy forced officials to call off previously planned auctions marking the first time since 2009 in which the country did not hold a tender for wind power

Policymakers have also continued to support renewable electricity deployment through enacting mandates for specified shares of renewable power often through Renewable Portfolio Standards (RPS) or requiring payment for renewable generation through net metering policies such as the new policies added in Suriname in 2016 In addition to regulatory policies several countries provided public funds through grants loans or tax incentives to drive investment in RE development or deployment This includes Indiarsquos 30 capital subsidy for solar PV rooftop systems19

Governments are also adapting mechanisms that long have been used for the promotion of power generation technologies to develop

an environment of enabling technologies such as energy storage and smart grid systems to better integrate renewable technologies in global electricity systems For example Suriname held a tender for solar PV systems including battery storage in 201620

RE deployment in the electricity sector through mechanisms such as those described above can also have a significant impact on the efficiency of power generation by shifting from thermal power plants which convert only approximately one-third of primary energy to electricity to more efficient RE installations21

Renewable heating and cooling technologies are directly promoted primarily through a mix of obligations and financial support though the pace of adoption remains well below that seen in the power and transport sectors By year-end 2016 renewable heat obligations or mandates were in place in 21 countries including seven emerging and developing countries (Brazil China India Jordan Kenya Namibia and South Africa)22

RE heating and cooling policies frequently focus on the use of RE technologies in the buildings sector and are often adopted

19

DE VELOPING COUNTRIESrsquo EFFORTS AND ACHIE VEMENTS g

in concert with building efficiency policies and regulations23 Several countries advanced EE through new or updated building codes in 2016 of which 139 are in place worldwide at the national and sub-national level including in at least 9 developing and emerging countries24 This includes Indonesiarsquos efforts to develop a Green Building Code and members of the Economic Community of West African States (ECOWAS) implementing building codes in accordance with a regional directive

Specific financial incentives including grants loans or tax incentives targeted at renewable heating and cooling technologies have been adopted in at least 8 developing and emerging economies In certain cases such as in Bulgaria support to RE heating technologies are included in broader EE financial support programs New developments in 2016 included Chilersquos extension of its solar thermal tax credit and Indiarsquos new loan incentives for solar process heat developers Renewable energy tendering has also been used to scale up deployment in the sector Bids for South Africarsquos long-awaited solar water heater tender closed in early-2016

The industrial sector also has a significant EE policy focus however the development of targeted mechanisms for the promotion of RE in industrial processes remains a challenge for policy makers For EE both Mali and Morocco now require energy audits for large industrial energy users

Transportation-focused RE and EE policies have both been adopted to accomplish a wide range of sector goals including increasing fuel economy or fuel switching to renewable fuels or electric vehicles The vast majority of policy attention particularly in developing countries has been focused on energy use in the road transportation sector While energy use in the maritime rail or aviation transportation sectors is gaining attention concrete RE and EE policy mechanisms have been adopted in only a handful of locations

Fuel economy standards are a primary means of increasing energy efficiency of passenger vehicles in the transport sector At least eight countries plus the EU have now established fuel economy standards for passenger and light-commercial vehicles as well as light trucks including Brazil China India and Mexico25 No developing countries have yet adopted policies for heavy-duty vehicles

RE in the transportation sector is often promoted through mandates specifying required shares or volumes of renewable fuel use Developing countries are often at the leading edge of nations looking to promote fuel switching to renewable transport fuels Biofuel blend mandates were in place at the national or stateprovincial level in 36 countries as of year-end 2016 with developing and emerging countries accounting for 26 of that total26 In 2016 Mexico expanded its blend mandate to cover nationwide fuel use while Argentina Malaysia India Panama Vietnam and Zimbabwe all added or strengthened biofuel andor bioethanol blend requirements

New financial incentives also were introduced in 2016 to promote biofuel production and consumption biorefinery development and RampD into new technologies including in Argentina where biodiesel tax exemptions were expanded and Thailand which provided subsidies to support a trial program for biodiesel use in trucks and military and government vehicles

While national policies remain an important driver of renewables and energy efficiency development municipal policymakers are taking a leading role in the promotion of both RE and EE within their jurisdictions often moving faster and enacting more ambitious goals than their national counterparts As cities continue to band together to mitigate the impacts of global climate change they have turned to RE and EE to transform their energy sectors A number of cities around the world are now seeking to achieve 100 renewable energy or electricity while a growing list of municipalities in developing and emerging economies such as Cape Town (South Africa) Chandigarh (India) and Oaxaca (Mexico) have established ambitious RE goals

C H A P T E R 3

Kampala Uganda

Kampala aims to replace 50 percent of household charcoal use with alternative cook fuels such as biomass or briquettes made from organic waste

R Details see page 24

NON-STATE AND SUBNATIONAL CONTRIBUTIONS TO RENEWABLE ENERGY AND ENERGY EFFICIENCY3 In cities and regions throughout the world governments at all jurisdiction levels are collaborating with private companies funding organizations and civil society to implement renewable energy and energy efficiency programs These activites reduce carbon emissions and create co-benefits including enhanced environmental quality improved public health economic growth and job creation social inclusion and gender equality This chapter includes six case studies of successful public-private collaboration as well as a discussion of the emerging low-carbon business paradigm

21

NON-STATE AND SUBNATIONAL CONTRIBUTIONS g

Renewable energy (RE) and energy efficiency projects (EE) in developing countries often require collaboration from implementing partners such as the private sector and subnational actors This chapter features six case studies that demonstrate some of the strategies that cities businesses and other collaborators are using to support RE and EE activities across developing and emerging economies These examples showcase the social economic and environmental benefits of RE and EE initiatives demonstrating the incentives driving businesses and cities to take leadership roles in implementing them27 28 It also includes an excerpt from Thomson Reutersrsquo forthcoming lsquoGlobal 250 Report A New Business Logicrsquo exploring the motivations and process of companies seeking to decarbonize their business models

Cities and the private sector will be vital to limiting global warming to well below 2degC29 As of 2013 over half of the global population and approximately 80 percent of global GDP resided in cities30 By 2050 the urban population will account for two-thirds of the global population and 85 percent of the global GDP31 Since cities concentrate people and economic activity they also shape energy use urban areas currently make up around two-thirds of global primary energy demand and 70 percent of global energy-related carbon dioxide emissions32 The goals of the Paris Agreement rest on the ability to chart a sustainable urban future ndash through the adoption of renewable energy increasingly efficient use of energy and the design of resilient and low-carbon infrastructure and transport33

Many cities already host innovative climate strategies driven by governments businesses and other actors who see opportunities to lower costs appeal to investors generate new forms of industry and improve quality of life Activities that help cities address climate change also offer opportunities to make progress towards meeting the goals of the 2030 Agenda for Sustainable Development Low-carbon forms of development generate co-benefits such as reduced traffic congestion and improved air quality and public health34 35 36 Between 2007 and 2015 solar and wind power in the United States produced air quality benefits of US $297ndash1128 billion mostly from 3000ndash12700 avoided premature mortalities37

The transition to a low-carbon economy can also reduce poverty and spur job creation38 39 Implementing the RE strategies articulated in the national climate action plans of the United States European Union China Canada Japan India Chile and South Africa would generate roughly 11 million new jobs and save about US $50 billion in reduced fossil fuel imports40 If these countries committed to a 100 percent RE pathway they would generate 27 million new jobs and save US $715 billion from avoided fossil fuel imports41 Collaboration with civil society and local stakeholders can help ensure a just transition to a low-carbon economy that maximizes job creation helps citizens develop new skills and fosters community renewal42

Building compact connected cities also reduces the cost of providing services and infrastructure for urban transport energy water and waste43 In India smart urban growth could save

between US $330 billion and $18 trillion (₹2-12 lakh crores) per year by 2050 ndash up to 6 of the countryrsquos GDP ndash while producing significant savings for households44 Altogether the New Climate Economy estimates that global low-carbon urban actions could generate US $166 trillion between 2015 and 2050 while reducing annual GHG emissions by 37 GtCO2e by 203045

Increasingly different kinds of actors are working together to realize this potential One assessment found that three-quarters of the challenges facing city climate action require support and collaboration with national and regional governments or the private sector46 Cities and companies in particular have grown increasingly interdependent Businesses aim to capture a share of the growing US $55 trillion global market in low-carbon and environmental technologies and products which is often concentrated in cities47 Energy service companies which base their business model on delivering EE solutions generated US $24 billion in revenue in 2015 and employed over 600000 people in China alone48 The global RE sector employed 98 million people in 2016 a 11 increase over 2015 by 2030 this number is expected to grow to 24 million49 Engaging in climate action also helps to mitigate the risk climate change may pose to an organizationrsquos business model and supply chain and enables companies to meet internal and public commitments to address global warming

The private sector can also help develop implement and scale climate and development solutions in urban areas that often struggle to access adequate finance Aside from tax collection most cities face limited options to raise or spend funds the private sector can help access capital to initiate or expand successful projects50 A C40 analysis of some 80 mega-cities identified 2300 high-impact ldquoshovel readyrdquo climate actions that could mitigate 450 MtCO2 ndash close to the annual emissions of the United Kingdom ndash by 2020 if US $68 billion in funds could be unlocked to implement them51

Many of these collaborations are already underway One survey of 627 climate change initiatives across 100 global cities found that private and civil society actors accounted for approximately one quarter (24 percent) of urban climate action and 39 percent of climate action in Asian cities52 Private sector organizations fund and invest in climate action act as service providers deliver operations and maintenance support to projects such as transport or waste management and design and build infrastructure53 Companies have also helped to fill gaps in infrastructure by creating new models for delivering city services such as ride-sharing54 Strategies like microfinance have played important roles in further unlocking the upfront capital vital to developing and implementing urban innovations55 As urban areas expand public-private partnerships that harness different forms of expertise technology and data can help overcome barriers to action and keep pace with citiesrsquo rapid rate of change56 National and regional governments can also help foster this process by crafting policy and financial environments that help RE and EE strategies take root

Current situation

RRR

82 million tons in avoided methane

emissions ndash equivalent to removing all cars from

Delhirsquos roads for

US $ 04 per kWh in avoided

waste treatment costs

200 acres of land valued at over

Rs 2000 crores (US $308 million)

New Delhi

22

C H A P T E R 3

About the initiative New Delhirsquos Integrated Municipal Waste Processing Complex at Ghazipur financed through a private-public partnership with ILampFS Environment reduces emissions while transforming waste into energy This partnership also supports local families through direct hiring and job training

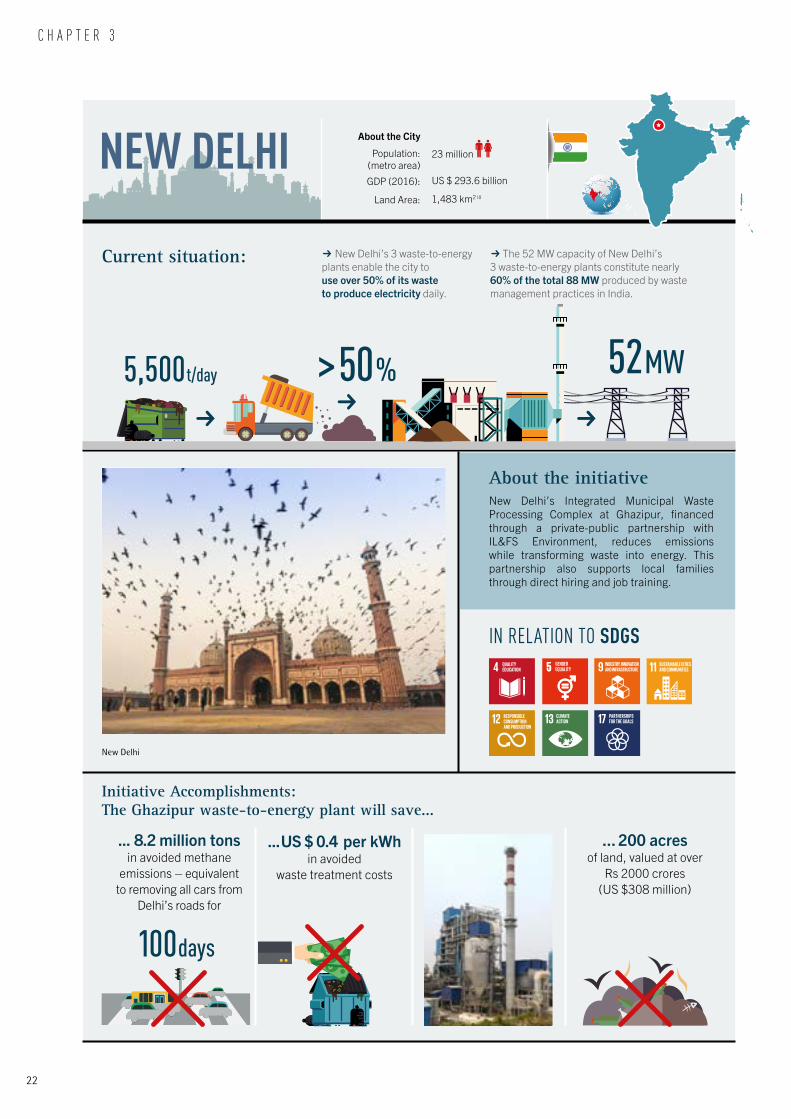

NEW DELHI About the City

Population (metro area)

GDP (2016)

Land Area

23 million

US $ 2936 billion

1483 km2 iii

R New Delhirsquos 3 waste-to-energy plants enable the city to use over 50 of its waste to produce electricity daily

R The 52 MW capacity of New Delhirsquos 3 waste-to-energy plants constitute nearly 60 of the total 88 MW produced by waste management practices in India

gt50 5500 tday 52 MW

Initiative Accomplishments The Ghazipur waste-to-energy plant will save

100 days

IN RELATION TO SDGS

23

CASE STUDIES g

Each day the Integrated Municipal Waste Processing Complex at Ghazipur New Delhi receives approximately 2000 tons of waste about 20 of the cityrsquos 9500-ton waste stream57 Through a public-private partnership between the East Delhi Municipal Corporation and the Infrastructure Leasing and Financial Services Environment (ILampFS Environment) the landfill now includes a waste-to-energy plant which generates an annual 12 MW of power58 It also produces 127 tons of fuel an alternative energy source for cement and power plants59 The Ghazipur plant which began operating in November 2015 will save a projected 82 million tons in avoided methane emissions over its 25-year life span60

The projectrsquos benefits extend beyond its climate impacts Reusing waste will prevent 200 acres of urban land valued at over Rs 2000 crores (US $308 million) from being consumed by the landfill61 62 For ILampFS Environment the plant enables it to engage in Indiarsquos environmental goods and services sector estimated to be worth Rs 250 billion (US $39 billion) and projected to grow 10 to 12 annually63 Across its operations the company reuses 95 of every tonne of municipal solid waste through recycled products or energy generation64

Converting waste to energy and avoiding the expansion of the landfill also lowers the health and safety risks of an open solid waste disposal site65 The plant reduces the amount of leachate the landfill generates saving US $04 per kWh in annual treatment costs66 In managing the Ghazipur plant ILampFS Environment relies on best-in-class technology67 and a Continuous Emission Monitoring System which publishes real-time emission parameters online to meet strict air quality standards68

The project also focuses on supporting the surrounding community of 373 local wastepicker families who live near and work in the landfill salvaging and reselling waste Providing support and retraining to local families is critical to efforts that affect access to the landfill and its materials The Ghazipur plant employs over 70 former waste-pickers directly in the plant69 To foster financial inclusion 400 families received bank accounts and Permanent Account Number cards and kiosk banking was provided to the local community through the State Bank of India Since July 2014 2075 bank accounts have been opened70 71

ILampFS Environment also worked with a nonprofit organization Institute for Development Support (IDS) to establish Gulmeher a community center that offers employment and training to approximately 200 local women who previously earned a living collecting waste at the Ghazipur landfill72 The center which launched in May 2013 grew out of brainstorming sessions IDS held with waste-pickers ILampFS Environment and other stakeholders73 74 To help boost their future employability the center provides training in a variety of jobs75 Women reuse materials from a nearby wholesale flower market to create products including boxes cards diyas and natural holi colors76 In mid-2014 the center partnered with Delhi-based start-up Aakar Innovations to produce inexpensive sanitary napkins that low-income women can afford Aakar Innovations helped train the women and buys and re-sells the products they produce77

In 2014 the community organization converted into a private company with participants also acting as shareholders of the Gulmeher Green Producer Company Limited78 Earnings for the participating women average approximately Rs 5000-6000 (US $77-90) every month79 For Badru Nisha the first woman to join the center this income has enabled her to save 70000 Rs (US $1100) and to build a house for relatives80 In India where only 26 of women participate in the labor force compared to almost 75 of men this organization helps build womenrsquos skills and confidence81 82

Without intervention New Delhi is expected to generate roughly 15750 tons of garbage daily in 202183 For cities facing a similar challenge of managing high volumes of waste with limited land the Ghazipur plant offers a successful strategy plans for replicating it are underway in New Delhi and other Indian cities84 The cityrsquos most recently constructed waste-to-management plant Narela-Bawana also relies on a public-private partnership model and produces compost as well as energy85 As the city and its waste stream continue to grow the private sector plays a powerful role in converting challenges into opportunities for development

TRANSFORMING WASTE INTO ENERGY | INDIA | NEW DELHI

Market in Kampala Uganda

24

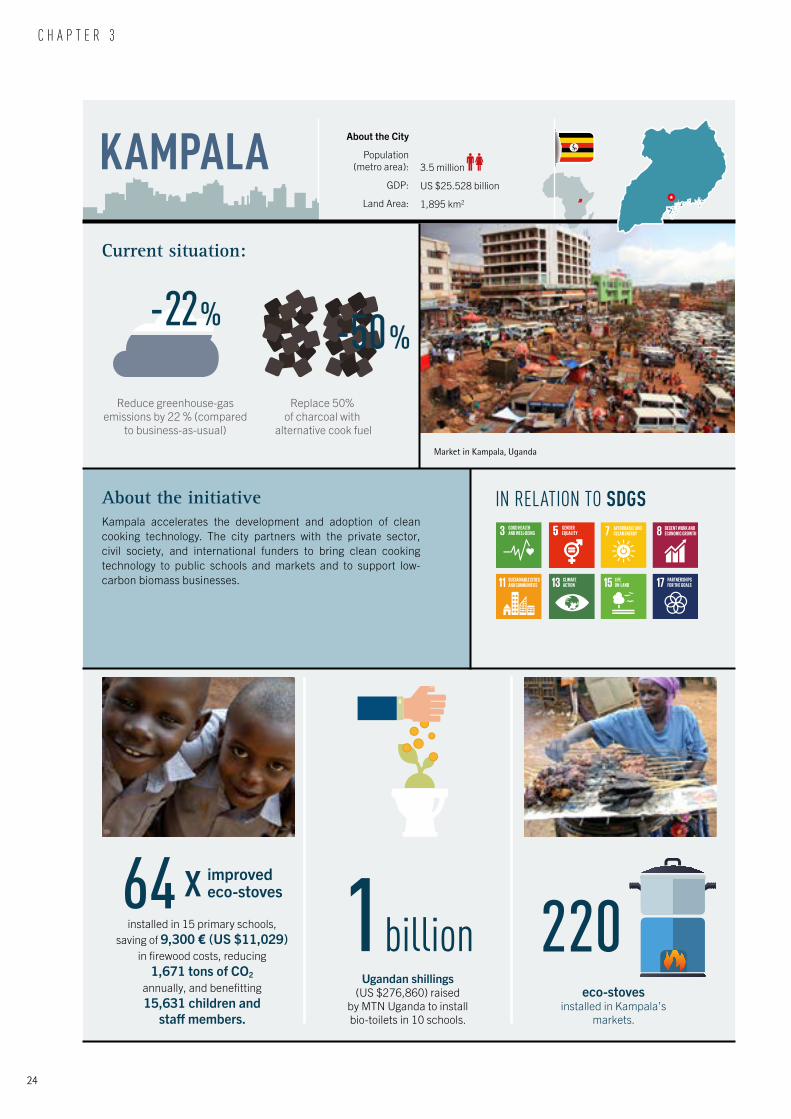

About the initiative Kampala accelerates the development and adoption of clean cooking technology The city partners with the private sector civil society and international funders to bring clean cooking technology to public schools and markets and to support low-carbon biomass businesses

installed in 15 primary schools saving of 9300 euro (US $11029)

in firewood costs reducing 1671 tons of CO2

annually and benefitting 15631 children and

staff members

Ugandan shillings (US $276860) raised

by MTN Uganda to install bio-toilets in 10 schools

eco-stoves installed in Kampalarsquos

markets

improved eco-stoves

KAMPALA

Reduce greenhouse-gas emissions by 22 (compared

to business-as-usual)

Replace 50 of charcoal with

alternative cook fuel

Current situation

-22

About the City

Population (metro area)

GDP

Land Area

35 million

US $25528 billion

1895 km2

-50

C H A P T E R 3

IN RELATION TO SDGS

64 x 2201 billion

25

Kampala has grown rapidly over the past decade becoming home to nearly 2 million people and generating approximately half of Ugandarsquos GDP86 In 2014 the city launched a five-year Climate Change Action Strategy87 to guide its rapid evolution and to ensure it ldquodrives development in the most sustainable wayrdquo88 The plan draws on a diverse array of goals ndash from planting half a million trees to creating traffic-free paths for pedestrians and bicyclists ndash to build Kampalarsquos resilience and protect its most vulnerable populations89

The early years of the Kampalarsquos Climate Change Action Strategy have focused on creating pilot projects and building partnerships that lay the groundwork for expanded action In particular the city has made great strides in implementing a complementary array of clean cooking initiatives Its Climate Change Action Strategy seeks to replace 50 of household charcoal use with alternative cook fuels such as biomass or briquettes made from organic waste90 To pursue this target Kampala provides seed capital and funding to organizations that train youth and women in making biomass briquettes brings biogas digesters and improved cook stoves to public schools and installs eco-stoves at city markets These proof-of-concept demonstrations build confidence and connections with the private sector civil society and bilateral and multilateral funders to help scale up these strategies

MTN Uganda the countryrsquos largest telecommunications company for instance has committed 1 billion Ugandan shillings (US $276860) raised through two annual city marathons to install biogas digesters in 10 public schools91 Their commitment will expand a program piloted at the Kansanga School which turns human animal and food waste into methane gas halving the amount of energy used to cook meals This biogas digester produces approximately 26 MWh annually lowering operating costs and reducing pollution from the firewood or charcoal it replaces92

A collaboration between the Kampala Capital City Authority (KCCA) and French development agency Expertise France supports a complementary effort to bring higher efficiency cooking stoves to 15 new public schools93 with technical support from the Ugandan company SIMOSHI Ltd This effort which has distributed 64 stoves supplied by Uganda Stove Manufacturers Ltd builds on the successful implementation of an eco-stove at another school94 The program has saved schools 9300 euro (US $11029) in firewood costs reduced 1671 tons of CO2 annually and benefitted 15631 children and staff members95 Earnings acquired through the Clean Development Mechanism will be reinvested in the schools to support annual maintenance monitoring and management96 Eventually the project aims to install 1500 stoves in 450 schools benefiting 340000 children and reducing 31286 tonnes of annual CO2 emissions97

Kampala also works with emerging businesses providing seed funding to organizations that train women and youth to produce

low-carbon briquettes from organic waste food scraps and other materials The briquettes burn cleanly without releasing smoke or ash and help avoid deforestation In the words of one customer they are also ldquocheap to use time-saving and energy-savingrdquo98 The briquettes have gained popularity with restaurants hotels households and poultry farmers Kampalarsquos administration is developing a program to further expand the supply of low-carbon fuel and connect producers with more markets99

In addition the city has installed 220 eco-stoves in the cityrsquos marketplaces These stoves can be linked with solar photovoltaic panels that extend stovesrsquo cooking time and can generate electricity for other uses such as lighting a kitchen or charging a battery100 This approach improves working conditions protects the health of the women who typically cook and serve food in these spaces and helps test and fine-tune this technology It also builds awareness and comfort with cleaner cooking technology among smaller business owners who often face financial barriers to the purchase of new equipment

The shift to cleaner cooking technology can deliver vital improvements in public health More than 90 of Ugandan households101 along with many restaurants schools and other places that serve and prepare food cook with wood charcoal The World Health Organization estimates exposure to cookstove smoke contributes to 13000 premature deaths every year in Uganda102 103 In Kampala over 80 of households rely on charcoal for cooking with dramatic impacts on air quality and public health104 Women and girls often face the highest levels of risk as they can spend up to five hours daily cooking in smoky kitchens and can face safety risks in traveling to forests to collect firewood105

The use of clean cooking technology also lessens the risk of fuel shortages The balance between biomass supply and demand remains fragile with large deficits in materials forecasted in and beyond the 2020rsquos106 Since Kampala concentrates Ugandarsquos economic activity and as a result its energy demand it is especially vulnerable to these projected shortfalls but also particularly well-placed to test and develop solutions107

The cityrsquos approach to promoting clean cooking technology reflects the need to ensure that the transition away from the charcoal market generates jobs and creates revenue108 Funding will also continue to be crucial to the cityrsquos ability to facilitate and accelerate the adoption of clean cooking technologies Kampala has teamed up with the World Bank and the University of Washington to develop a climate-smart capital investment plan that aligns new projects with the cityrsquos climate action goals It will continue to leverage partnerships with private and international partners to scale up public funding as it takes the next steps in its climate and development roadmap109

EXPANDING ACCESS TO CLEANER COOKING | UGANDA | KAMPALA

CASE STUDIES g

26

NANJINGCurrent situation

R Shortlisted as one of Chinarsquos National

LOW-CARBON PILOT CITIES

R Added 4300 electric vehicles (EVs)

About the initiative The Nanjing Municipal Government introduced a series of policies to promote the sale use and production of electric vehicles It works with industry to continue transforming the city into a major electric vehicle manufacturing and services hub

Initiative Accomplishments

+4300

-246000t

About the City

Population (metro area)

GDP (2016)

Land Area

821 millionxlv

US $1464 billionxlvi

6598 km2 iii

During 2014-15

R reduced CO2 emissions by 246000 tons

and saved over US $71 million in lower energy bills

R Drew more than 46 EV companies to the city generating annual tax revenues of approximately

C H A P T E R 3

IN RELATION TO SDGS

RENEWABLE ENERGY

EV POLICIES

ELECTRIC VEHICLE MANUFACTURING AND SERVICES HUB

US$ 16 million

27

g

The Chinese city of Nanjing deployed the fastest rollout of electric vehicles in the world adding 4300 electric vehicles to its streets during 2014ndash2015110 This transition to electric vehicles (EV) helped Nanjing reduce CO2 emissions by 246000 tons in 2014111 Nanjingrsquos activities have drastically cut the cityrsquos carbon emissions and use of oil and generated over US $71 million in savings from lower energy bills112

Nanjingrsquos adoption of renewable and electric vehicles is part of a larger economic and environmental bid to transition away from energy and carbon intensive industries like petrochemicals steel and building materials113 that Nanjingrsquos economy once relied on These conventional industries are losing their economic competitiveness while emitting large amounts of greenhouse gases and other pollutants114

The municipal government supported this shift by building compatible infrastructure for electric vehicles introducing tax breaks and electricity price subsidies for EV consumers and promoting the use of renewable-powered vehicles in public services In the 2016 New Energy Automobile Promotion and Application Plan of Nanjing the municipal government aimed to add 500 renewable energy buses 500 service vehicles and 1502 passenger vehicles to its transportation system in 2016115 By 2018 Nanjingrsquos goal is to convert 80 of its bus fleet to be powered by renewable energy116 Nanjing also plans to build 3000 charging stations especially in residential areas and to expand the use of electric vehicles to trucks and vans in the logistics sector117

Nanjingrsquos initiative to promote electric vehicles closely aligns with Chinarsquos national climate energy and macroeconomic policies and it receives support from the central and provincial levels of government On a national level China has set specific targets to develop a sustainable and renewable energy-driven transportation sector as highlighted in both the State Councilrsquos Circular Economy Development Strategy and Near-Term Action Plan and the Ministry of Transportrsquos Guiding Opinions on Accelerating Development of Green Circular Low-Carbon Transportation118 Electric vehicles are a key part of the solution as they enable China to achieve GHG emission reduction targets as well as to grow and restructure its automobile industry

At the provincial level the Jiangsu Provincial Government has signed a Framework Agreement119 with the Ministry of Transport to promote Jiangsursquos development of low carbon transportation The Jiangsu Provincial Government also released the Green Circular and Low-Carbon Transportation Development Plan of Jiangsu Province (2013-2020)120 which included a target to make 35 of public buses and 65 of taxis run on renewable energy across Jiangsu

Through supportive policies and a favorable investment environment Nanjing has established itself as an electric vehicle manufacturing and services hub In 2014-15 Nanjing drew 46 companies connected to the EV sector to the city and earned tax revenues of approximately US $16 million per year121 In 2016 Chinese EV manufacturer Future Mobility Corporation invested US $17 billion to build a factory in Nanjing that has an initial production capacity of 150000 cars per year122 Beijing-based EV rental company Gofun has also introduced its service to Nanjing rolling out 200 electric cars that can be rented via smartphones123

Policy coordination across different levels of government helps explain Nanjingrsquos success Nanjing is a National Low-Carbon Pilot City124 Policies and guidelines from the Central and Provincial Governments give the Municipal Government the confidence and support it needs to conduct pilot programs and test new solutions