Embed Size (px)

Citation preview

© OECD/IEA 2016© OECD/IEA 2016

Heymi Bahar Project ManagerRenewable Energy DivisionInternational Energy [email protected]

Energiforsk, Stockholm, 18 January 2017

Medium-‐ Term Renewable Energy Market Report 2016

© OECD/IEA 2016

Context

n A year of records for renewable electricityØ A record amount of new capacity was installed in 2015

Ø Total capacity has now overtaken coal

n COP21 Paris Agreement gives momentum to renewables

n Local air pollution & energy security are also key drivers

n Energy investment flows confirm shift to renewables

n But policy makers need to heighten their commitments and provide investors more clarity & certainty

© OECD/IEA 2016

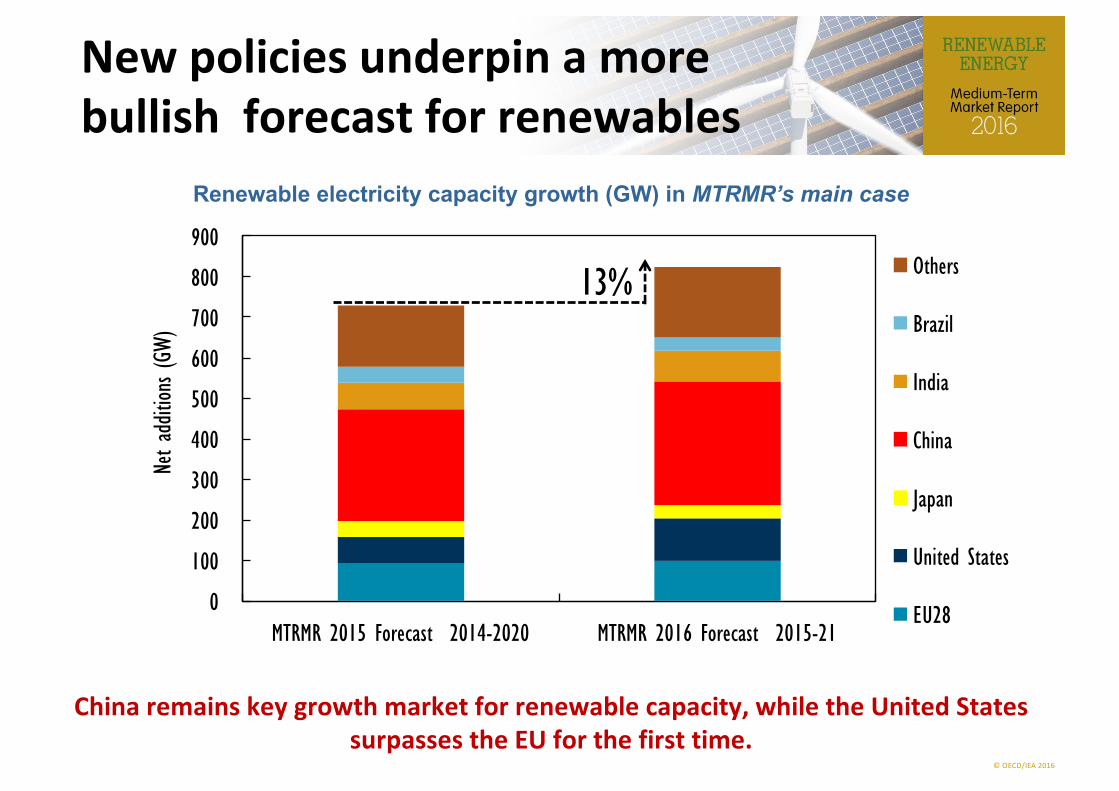

New policies underpin a more bullish forecast for renewables

China remains key growth market for renewable capacity, while the United States surpasses the EU for the first time.

Renewable electricity capacity growth (GW) in MTRMR’s main case

13%

0

100

200

300

400

500

600

700

800

900

MTRMR 2015 Forecast 2014-2020 MTRMR 2016 Forecast 2015-21

Net a

dditio

ns (G

W)

Others

Brazil

India

China

Japan

United States

EU28

© OECD/IEA 2016

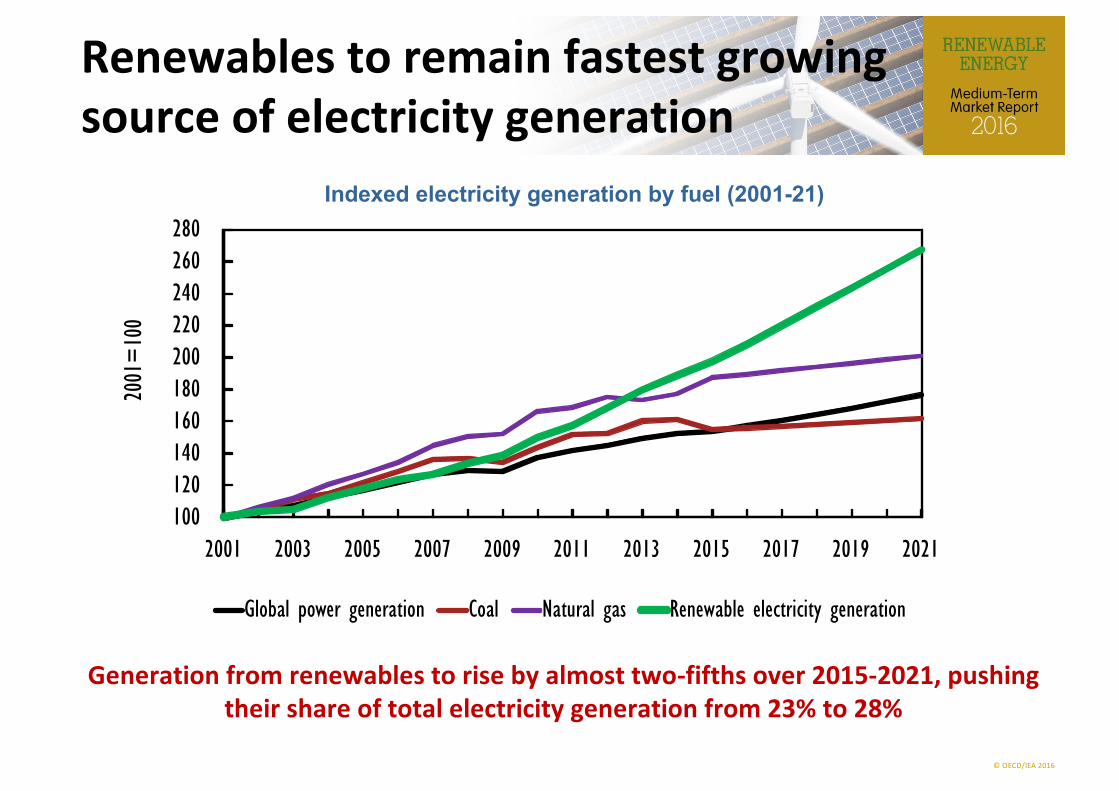

Renewables to remain fastest growing source of electricity generation

Generation from renewables to rise by almost two-‐fifths over 2015-‐2021, pushing their share of total electricity generation from 23% to 28%

Indexed electricity generation by fuel (2001-21)

100120140160180200220240260280

2001 2003 2005 2007 2009 2011 2013 2015 2017 2019 2021

2001

=10

0

Global power generation Coal Natural gas Renewable electricity generation

© OECD/IEA 2016

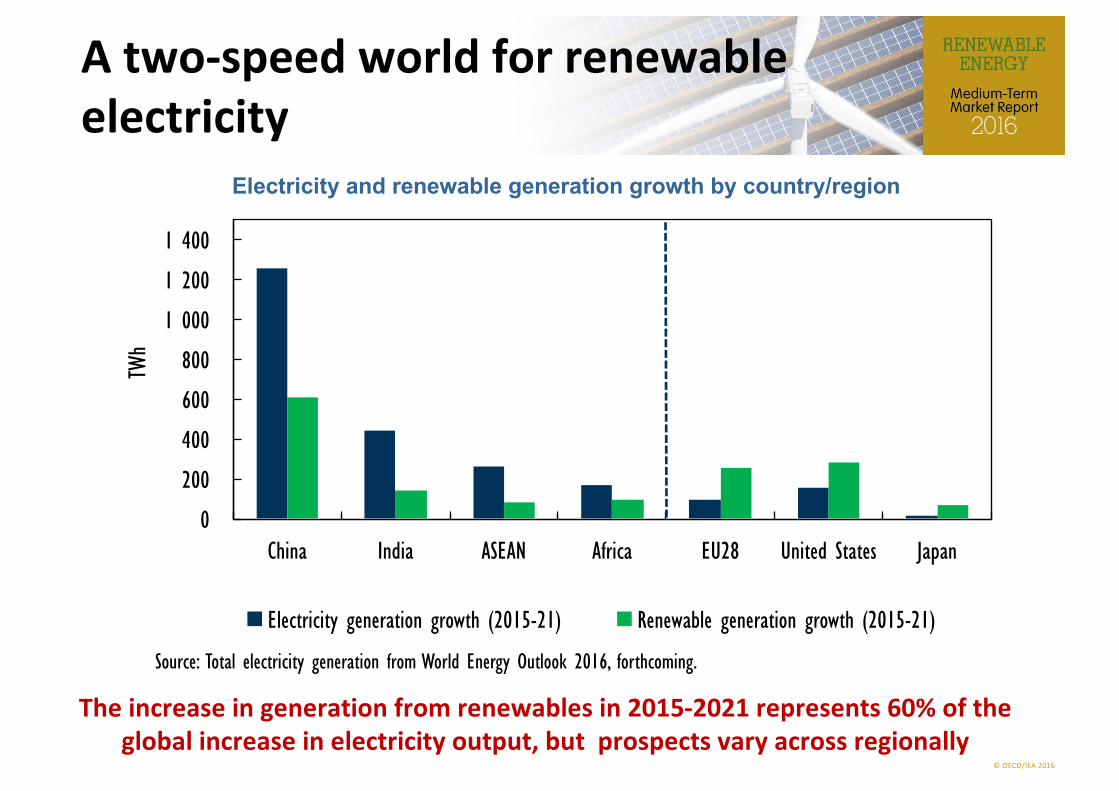

A two-‐speed world for renewable electricity

The increase in generation from renewables in 2015-‐2021 represents 60% of the global increase in electricity output, but prospects vary across regionally

Electricity and renewable generation growth by country/region

0

200

400

600

800

1 000

1 200

1 400

China India ASEAN Africa EU28 United States Japan

TWh

Electricity generation growth (2015-21) Renewable generation growth (2015-21)

Source: Total electricity generation from World Energy Outlook 2016, forthcoming.

© OECD/IEA 2016

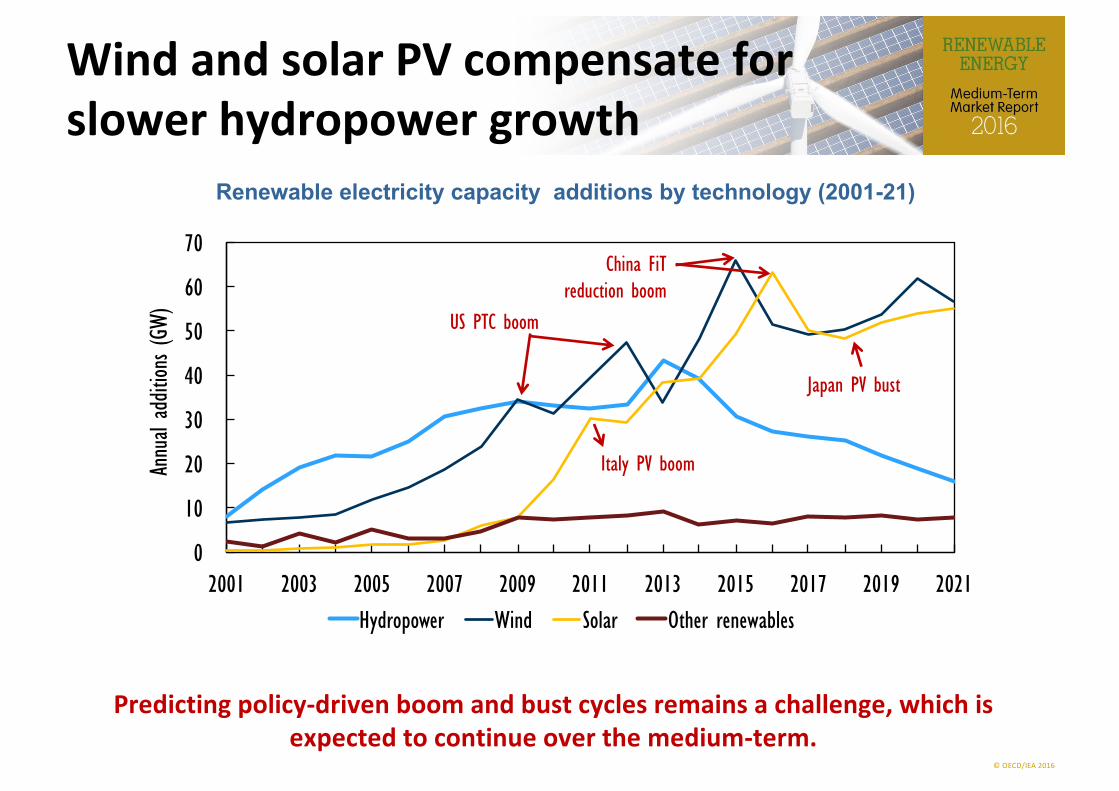

Wind and solar PV compensate for slower hydropower growth

Predicting policy-‐driven boom and bust cycles remains a challenge, which is expected to continue over the medium-‐term.

0

10

20

30

40

50

60

70

2001 2003 2005 2007 2009 2011 2013 2015 2017 2019 2021

Annu

al ad

dition

s (GW

)

Hydropower Wind Solar Other renewables

Italy PV boom

China FiTreduction boom

US PTC boom

Japan PV bust

Renewable electricity capacity additions by technology (2001-21)

© OECD/IEA 2016

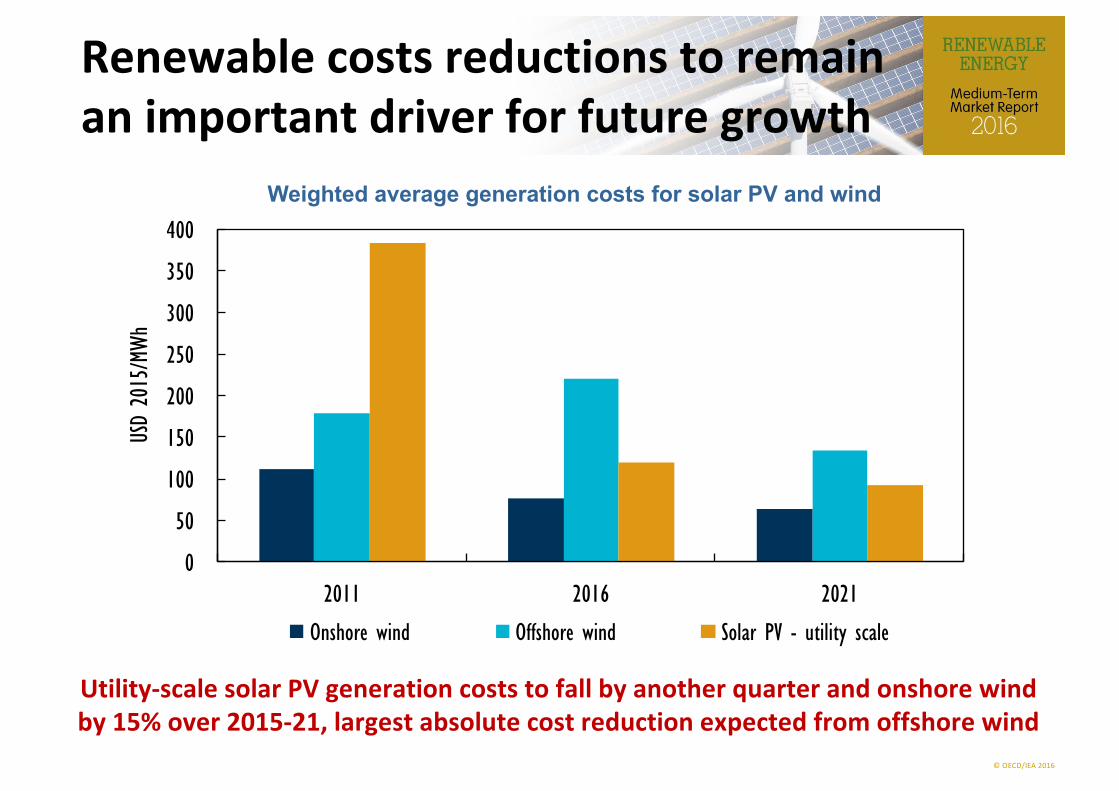

Renewable costs reductions to remain an important driver for future growth

Utility-‐scale solar PV generation costs to fall by another quarter and onshore wind by 15% over 2015-‐21, largest absolute cost reduction expected from offshore wind

Weighted average generation costs for solar PV and wind

0

50

100

150

200

250

300

350

400

2011 2016 2021

USD

2015

/MWh

Onshore wind Offshore wind Solar PV - utility scale

© OECD/IEA 2016

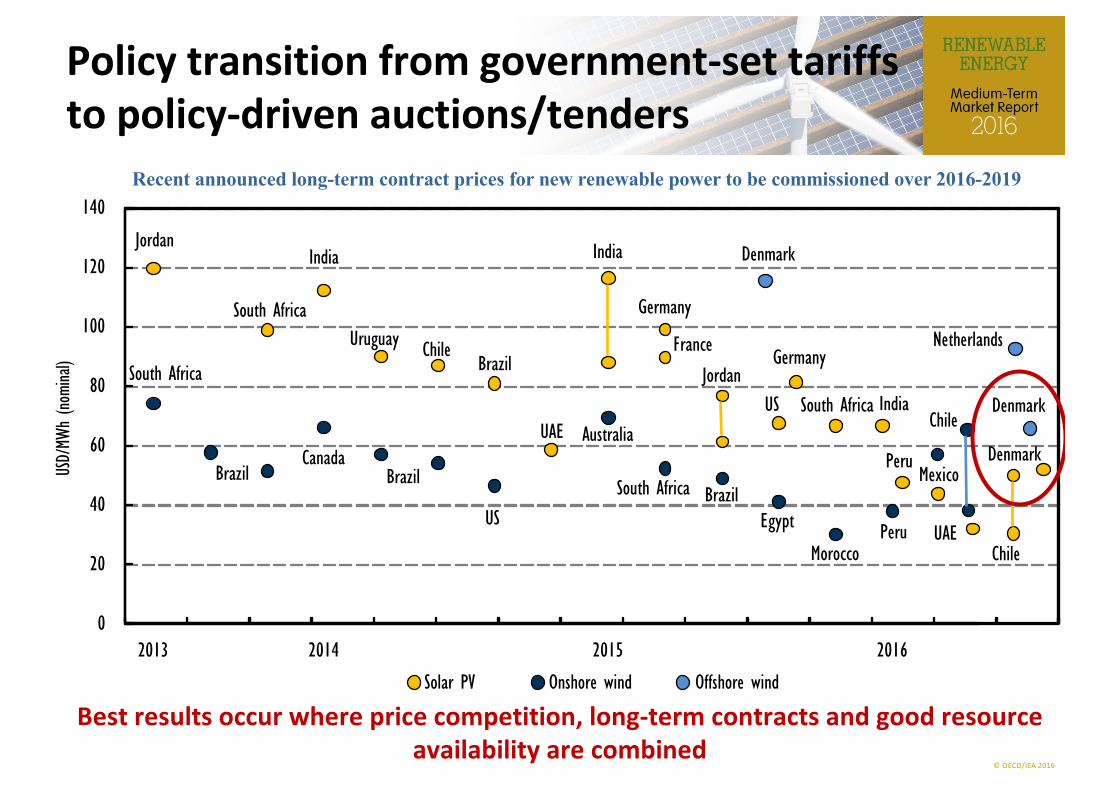

Best results occur where price competition, long-‐term contracts and good resource availability are combined

0

20

40

60

80

100

120

140

2013 2014 2015 2016

USD/

MWh

(nomi

nal)

Jordan

South Africa

BrazilCanada

Brazil

US

Australia

South Africa BrazilEgypt

MoroccoPeru

South Africa

India

Uruguay ChileBrazil

India

Germany

FranceJordan

Denmark

US South AfricaUAE

India

PeruMexico

Solar PV Onshore wind Offshore wind

GermanyNetherlands

UAE

Chile

Chile

Recent announced long-term contract prices for new renewable power to be commissioned over 2016-2019

Denmark

Denmark

Policy transition from government-‐set tariffs to policy-‐driven auctions/tenders

© OECD/IEA 2016

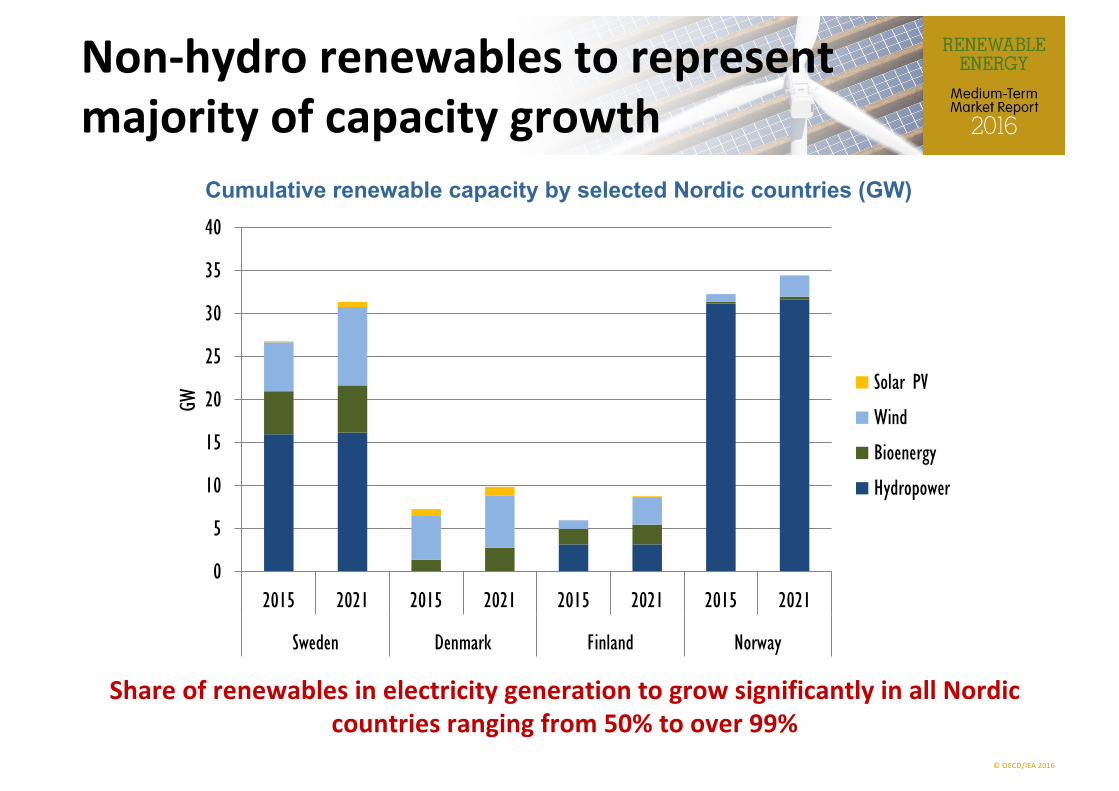

Non-‐hydro renewables to represent majority of capacity growth

Cumulative renewable capacity by selected Nordic countries (GW)

Share of renewables in electricity generation to grow significantly in all Nordic countries ranging from 50% to over 99%

0

5

10

15

20

25

30

35

40

2015 2021 2015 2021 2015 2021 2015 2021

Sweden Denmark Finland Norway

GW

Solar PV

Wind

Bioenergy

Hydropower

© OECD/IEA 2016

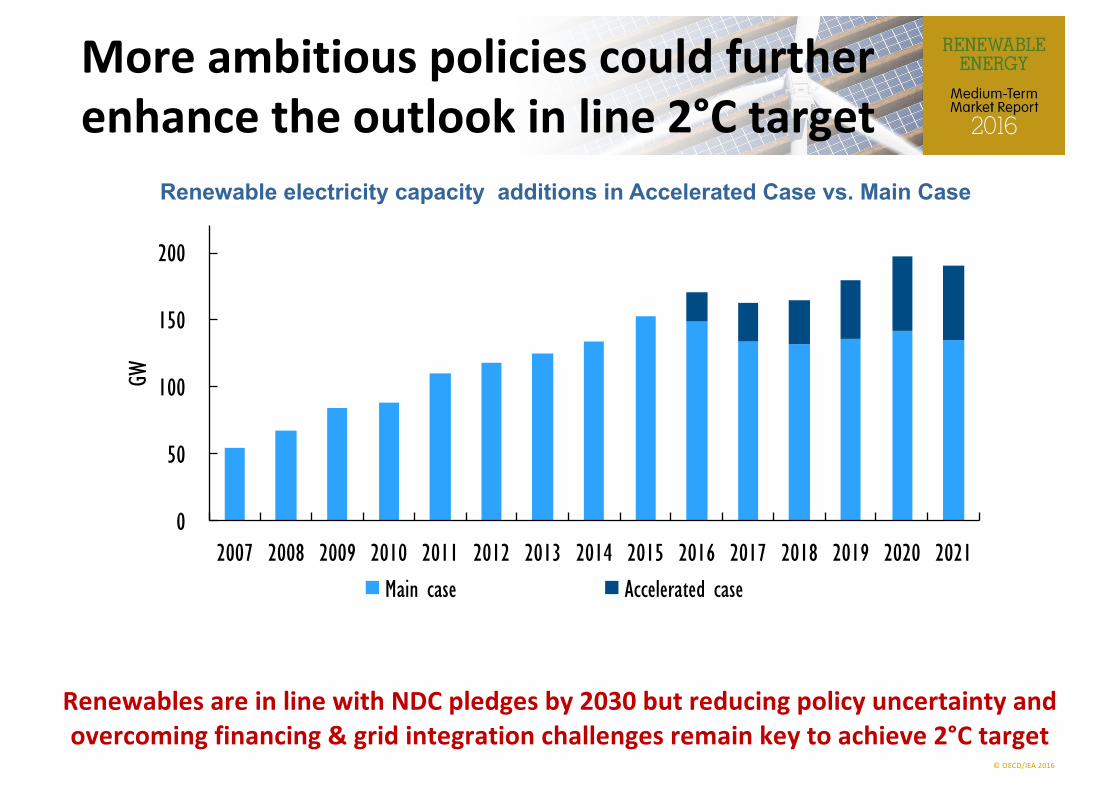

More ambitious policies could further enhance the outlook in line 2°C target

Renewables are in line with NDC pledges by 2030 but reducing policy uncertainty and overcoming financing & grid integration challenges remain key to achieve 2°C target

Renewable electricity capacity additions in Accelerated Case vs. Main Case

0

50

100

150

200

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

GW

Main case Accelerated case

© OECD/IEA 2016

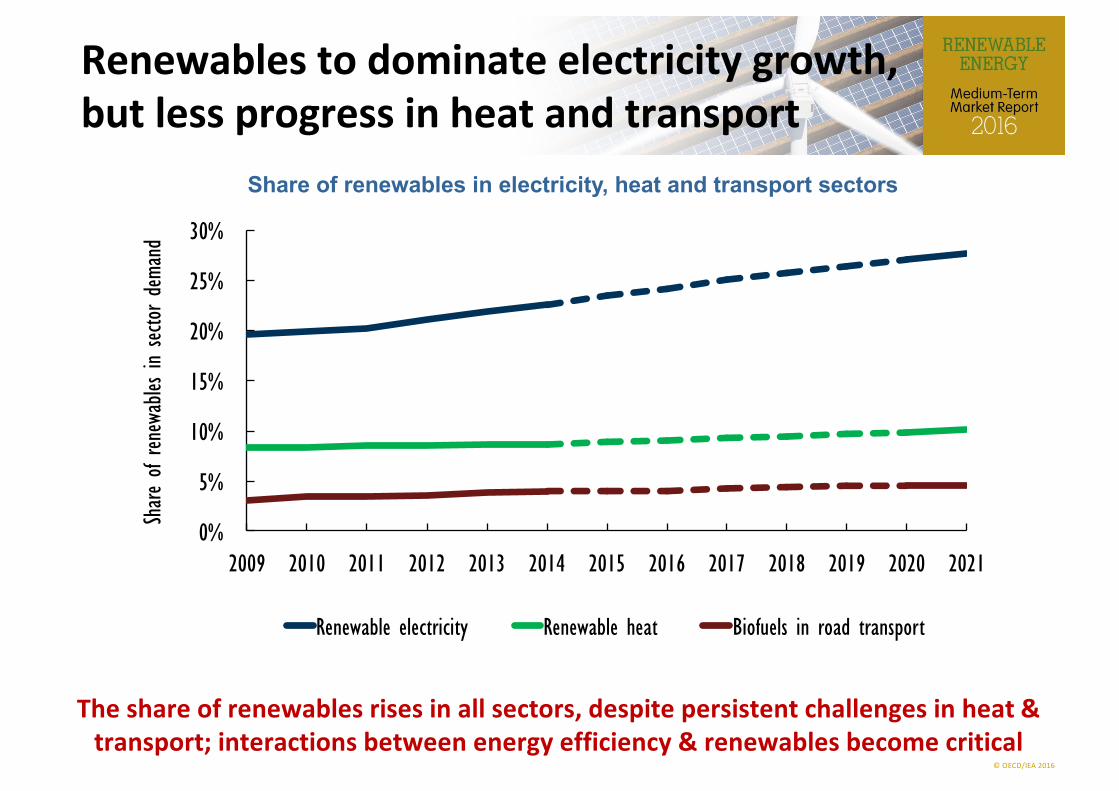

Renewables to dominate electricity growth, but less progress in heat and transport

The share of renewables rises in all sectors, despite persistent challenges in heat & transport; interactions between energy efficiency & renewables become critical

Share of renewables in electricity, heat and transport sectors

0%

5%

10%

15%

20%

25%

30%

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Share

of r

enew

ables

in se

ctor d

eman

d

Renewable electricity Renewable heat Biofuels in road transport

© OECD/IEA 2016

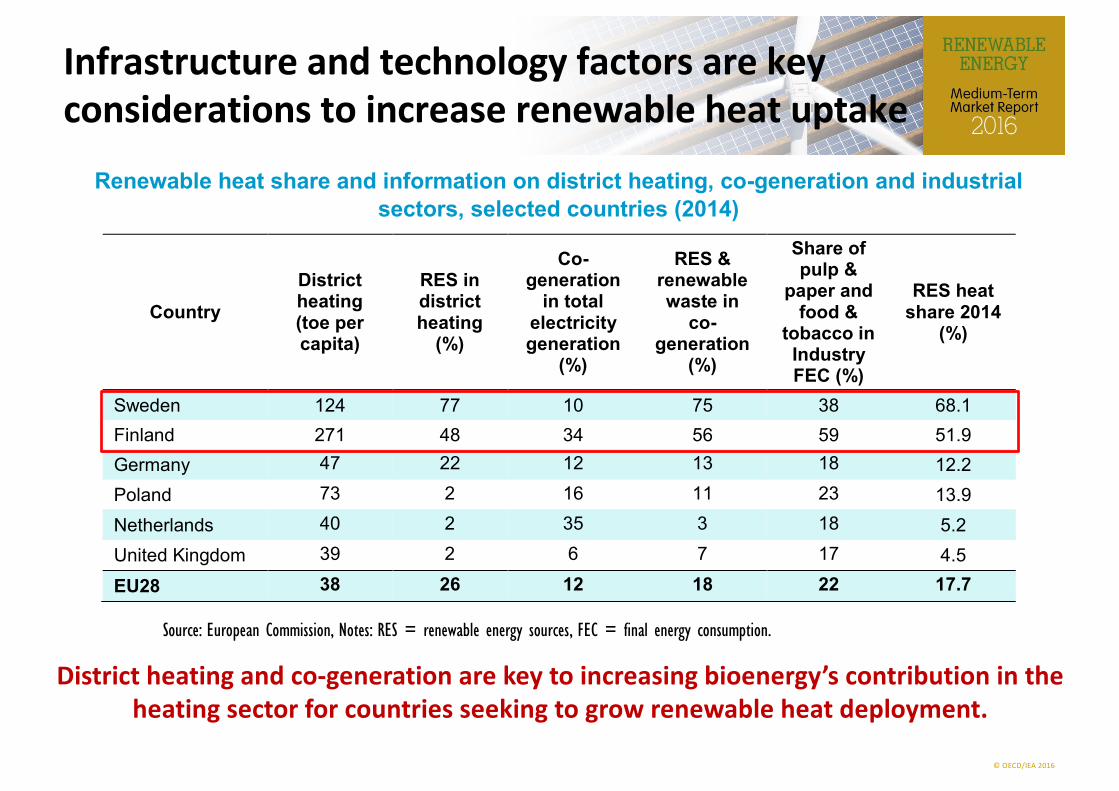

Country District heating (toe per capita)

RES in district heating (%)

Co-generation in total electricity generation

(%)

RES & renewable waste in co-

generation (%)

Share of pulp &

paper and food &

tobacco in Industry FEC (%)

RES heat share 2014

(%)

Sweden 124 77 10 75 38 68.1 Finland 271 48 34 56 59 51.9 Germany 47 22 12 13 18 12.2 Poland 73 2 16 11 23 13.9 Netherlands 40 2 35 3 18 5.2 United Kingdom 39 2 6 7 17 4.5 EU28 38 26 12 18 22 17.7

Infrastructure and technology factors are key considerations to increase renewable heat uptakeRenewable heat share and information on district heating, co-generation and industrial

sectors, selected countries (2014)

District heating and co-‐generation are key to increasing bioenergy’s contribution in the heating sector for countries seeking to grow renewable heat deployment.

Source: European Commission, Notes: RES = renewable energy sources, FEC = final energy consumption.

© OECD/IEA 2016

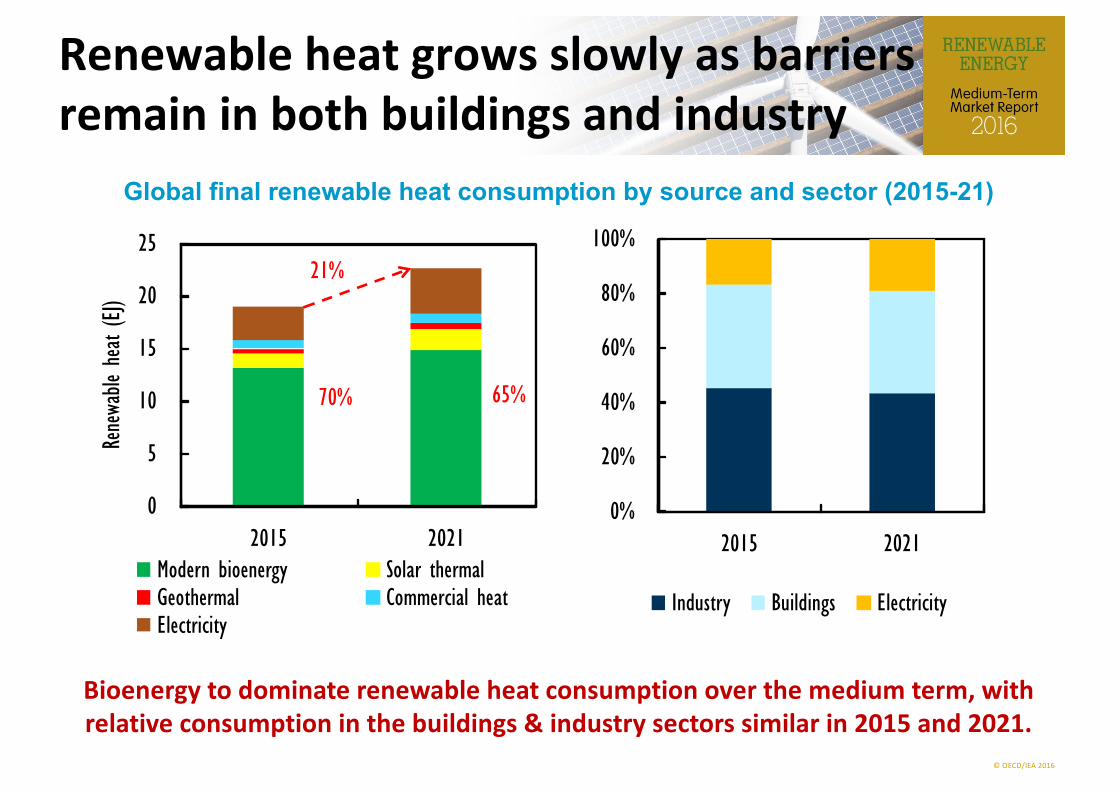

Renewable heat grows slowly as barriers remain in both buildings and industry

Bioenergy to dominate renewable heat consumption over the medium term, with relative consumption in the buildings & industry sectors similar in 2015 and 2021.

Global final renewable heat consumption by source and sector (2015-21)

0%

20%

40%

60%

80%

100%

2015 2021

Industry Buildings Electricity

0

5

10

15

20

25

2015 2021

Rene

wable

heat (

EJ)

Modern bioenergy Solar thermalGeothermal Commercial heatElectricity

21%

70% 65%

© OECD/IEA 2016

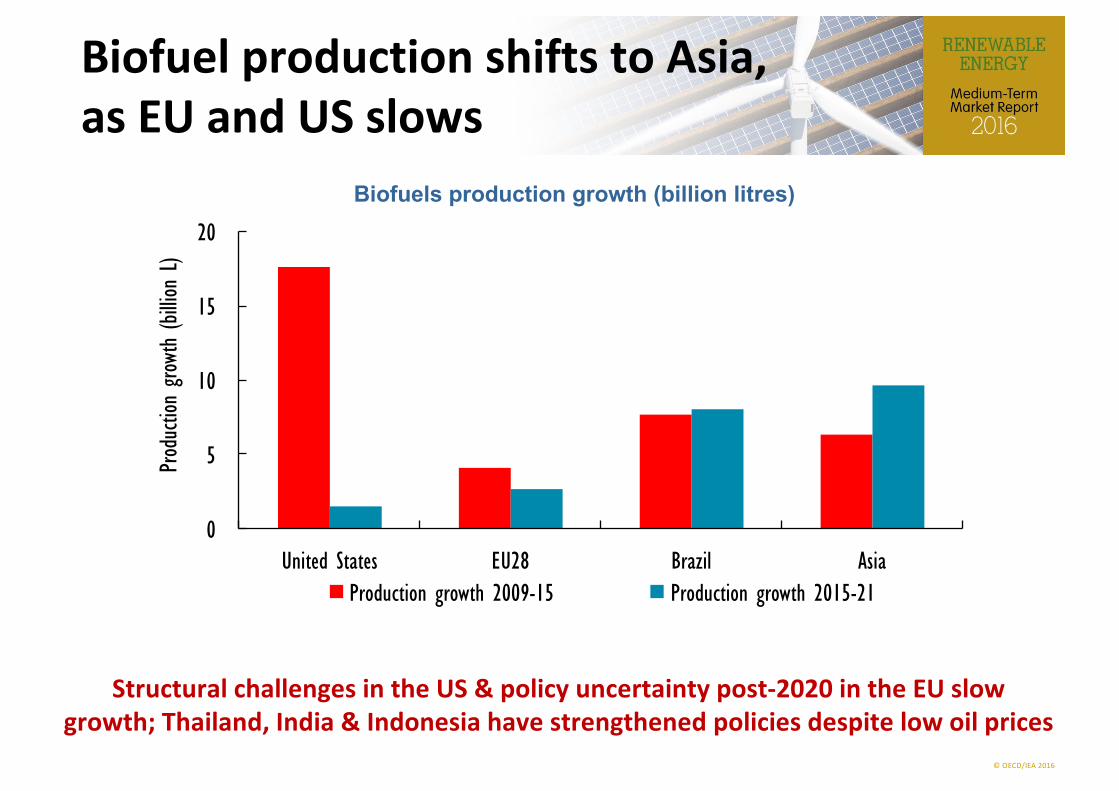

Biofuel production shifts to Asia, as EU and US slows

Structural challenges in the US & policy uncertainty post-‐2020 in the EU slow growth; Thailand, India & Indonesia have strengthened policies despite low oil prices

Biofuels production growth (billion litres)

0

5

10

15

20

United States EU28 Brazil Asia

Prod

uctio

n gro

wth

(billio

n L)

Production growth 2009-15 Production growth 2015-21

© OECD/IEA 2016

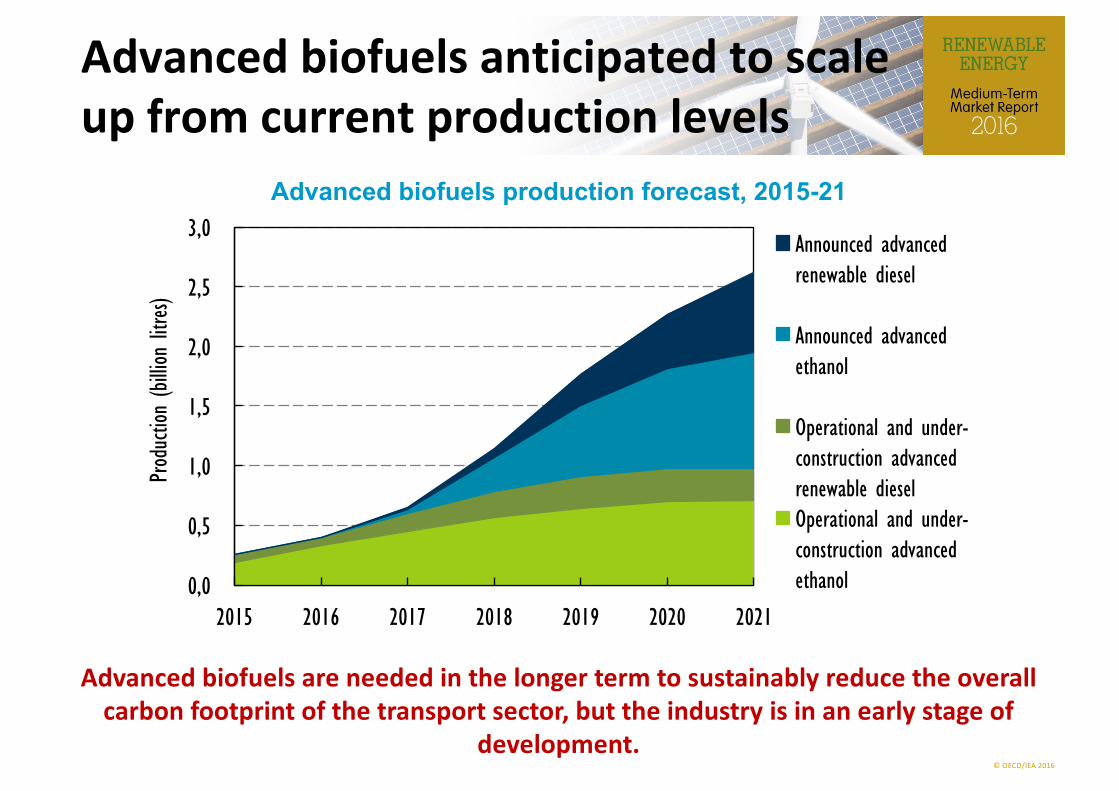

Advanced biofuels anticipated to scale up from current production levels

Advanced biofuels are needed in the longer term to sustainably reduce the overall carbon footprint of the transport sector, but the industry is in an early stage of

development.

Advanced biofuels production forecast, 2015-21

0,0

0,5

1,0

1,5

2,0

2,5

3,0

2015 2016 2017 2018 2019 2020 2021

Prod

uctio

n (bi

llion

litres)

Announced advanced renewable diesel

Announced advanced ethanol

Operational and under-construction advanced renewable dieselOperational and under-construction advanced ethanol

© OECD/IEA 2016

Some important trends to follow for businesses

n Distributed solar PV and smart home – new utility business models

n Electrification of transport – infrastructure and IT

n Off-‐grid electrification in Africa and South East Asia

n Offshore wind cheaper than onshore in Europe

n Market and auction design towards renewable integration

n Advanced biofuels – decarbonisation of aviation and shipping

n Renewable financing industry – diversification of financial products

© OECD/IEA 2016

Conclusions

n Prospects for renewables electricity revised upwards, driven by policy improvements, cost reductions & efforts to improve air quality

n The impact of lower fossil fuel prices on renewables varies by sector. Wind (onshore) & solar PV are the only technologies on track for a 2oC scenario

n Attracting investment in renewables hinges on appropriate market rules & regulations, particularly in markets with slow electricity demand growth

n Progress in renewable growth in the heat and transport sectors remains slow and needs significantly stronger policy efforts.

n IEA is working to accelerate energy transition with its analysis on policy & technology and system integration of renewables.

© OECD/IEA 2016

Thank you. Questions?

TeamYasmina Abdelilah

Heymi BaharUte Collier

Karolina DaszkiewiczPharoah Le FeuvreMegan MercerYasuhiro Sakuma

© OECD/IEA 2016

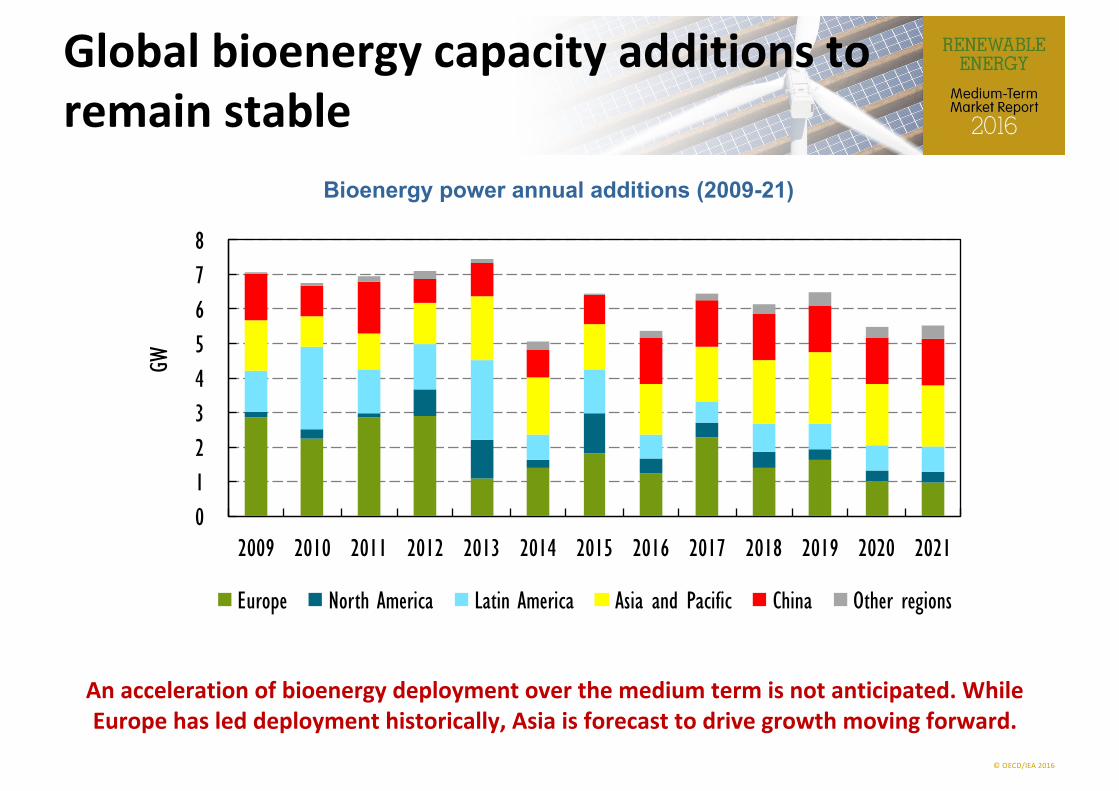

Global bioenergy capacity additions to remain stable

Bioenergy power annual additions (2009-21)

An acceleration of bioenergy deployment over the medium term is not anticipated. While Europe has led deployment historically, Asia is forecast to drive growth moving forward.

012345678

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

GW

Europe North America Latin America Asia and Pacific China Other regions

![2015 Final Heating & Cooling Demand in the Netherlands · General context –Energy intensity • Total final energy demand (FED) [3]: 564 TWh •4.5% of EU28 •7th highest of EU28](https://img.pdfslide.net/doc/110x75/5f4399579fa13d18f002e995/2015-final-heating-cooling-demand-in-the-netherlands-general-context-aenergy.jpg)