Embed Size (px)

Citation preview

REPARIS Vienna Workshops "Ethics in the Accountancy Profession" March 14-15, 2006

1

ADOPTION AND IMPLEMENTATION

OF A PROFESSIONAL CODE OF ETHICS IN MOLDOVA

Marina Shelaru, Executive Director, Association of Professional Accountants and Auditors of the Republic of Moldova (ACAP RM)

REPARIS Vienna Workshops "Ethics in the Accountancy Profession" March 14-15, 2006

2

AGENDA

I. Accounting Profession in Moldova: ACAP Overview

II. Legal Framework on Auditing - Current status III. Implementation of Ethics Code in Moldova

IV. Difficulties & solutions

V. Future Actions, Developments & Issues to Consider

REPARIS Vienna Workshops "Ethics in the Accountancy Profession" March 14-15, 2006

3

I. ACCOUNTING PROFESSION in MOLDOVA ACAP - Association of Professional Accountants and Auditors of Moldova, est.1996, IFAC member 1998, CIPA based full membership. Acting as NGO. (Over 800 members: coverage ≈ 14% of accountants and 15% of licensed auditors )

AFAM - Association of Audit Organizations of Moldova, est. 1997, around 30 audit firms, MoF approved auditors; acting as trade association. (Coverage ≈ 30% of audit firms)

AACM – Association of Auditors & Consultants in Management, est.2003, individuals (43) & NGOs (2); acting as NGO.

Conclusion: Coverage is very low. No market demand.

REPARIS Vienna Workshops "Ethics in the Accountancy Profession" March 14-15, 2006

4

MISSION ACAP RM

• To grant the assistance in developing the professional accounting and auditing in the Republic of Moldova, to provide its members with information and guidance, as well as to render services at the highest professional level

• ACAP commonly shared goal: “ The development of a sustainable accounting and auditing profession in the Republic of Moldova”

ASSOCIATION OF PROFESSIONAL ACCOUNTANTS AND AUDITORS OF THE REPUBLIC OF MOLDOVA – UPDATE: August, 1996- March, 2006

REPARIS Vienna Workshops "Ethics in the Accountancy Profession" March 14-15, 2006

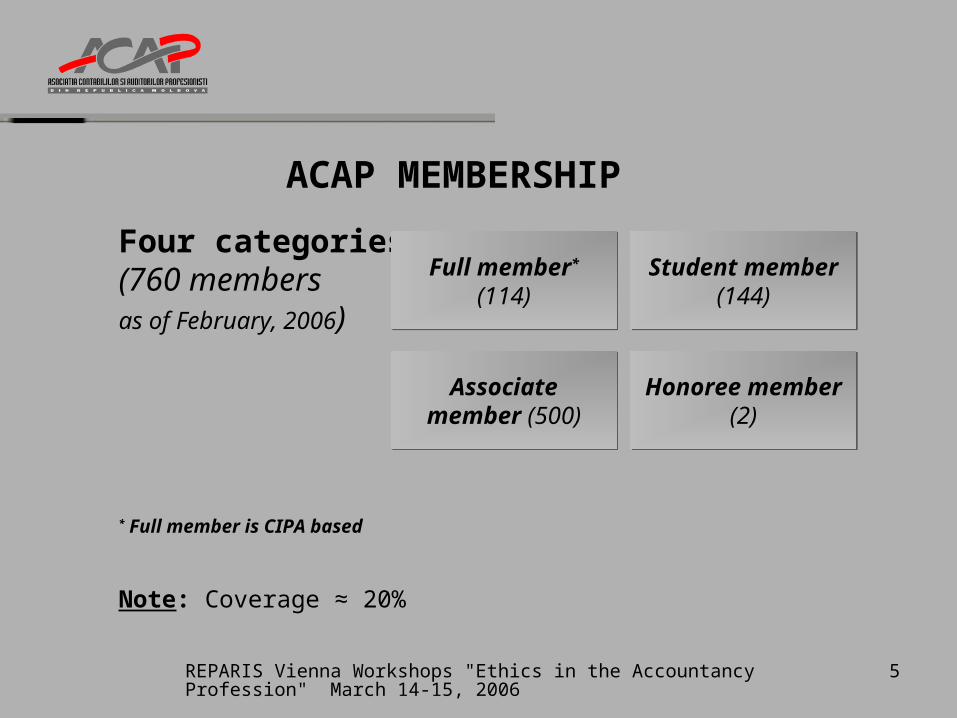

5

Four categories: (760 membersas of February, 2006)

* Full member is CIPA based

Note: Coverage ≈ 20%

ACAP MEMBERSHIP

Full member* (114)

Full member* (114)

Student member (144)

Student member (144)

Associate member (500)

Associate member (500)

Honoree member (2)

Honoree member (2)

REPARIS Vienna Workshops "Ethics in the Accountancy Profession" March 14-15, 2006

6

MEMBER SERVICES

Certification program

various training programs,

social and educational events,

the exclusive distribution of specialized literature (members of ACAP are offered substantial discounts),

editions of information and normative bulletins, affinity program,

rich library and the legislative database

REPARIS Vienna Workshops "Ethics in the Accountancy Profession" March 14-15, 2006

7

ACAP PERMANENT COMMITTEES

CERTIFICATION, EDUCATION AND TRAINING

PUBLIC RELATIONS & PUBLICATIONS

MEMBERSHIP, NOMINATIONS AND REGIONAL DEVELOPMENT

LEGISLATION & STANDARDS

FINANCE & TREASURY

ETHICS COMMITTEE

REPARIS Vienna Workshops "Ethics in the Accountancy Profession" March 14-15, 2006

8

ACAP STRATEGY

ACAP

Universities

Today’s Accounting

Professionals

Tomorrow's Accounting

Professionals

International best practices

Based Standards

REPARIS Vienna Workshops "Ethics in the Accountancy Profession" March 14-15, 2006

9

ACAP Relationships

AWG - Accounting Working GroupSRO –Self Regulatory Organizations (IFAC, ECCAA, SEEPAD, CECCAR, UFPA,, etc.)

ASWG - Auditing Standards Working GroupSCSM - State Commission for Securities MarketNB - National Bank

MINISTRY OF FINANCE MINISTRY OF EDUCATION

ENTERPRISES

A W G

SROs

A S W GUNIVERSITIES &

COLLEGES

SCSM NBM

ACAP

REPARIS Vienna Workshops "Ethics in the Accountancy Profession" March 14-15, 2006

10

ACAP ACCOMPLISHMENTS • Increased membership of ACAP from 33 on 1996 to over 1900 members in 2002• International Federation of Accountants (IFAC) accepted ACAP as an Associate

(1998) and then as an Full Member (2004). ACAP Chair -member of IFAC Developing Nations Permanent Task Force (DNPTF)

• Full Membership with South Eastern Partnership on Accountancy development (SEEPAD) and Eurasian Council of Certified Accountants and Auditors (ECCAA), IFAC Regional Grouping

• Organized the Three National Conferences of Professional Accountants and Auditors (1998-2000)

• Completed the Enterprise Manual, which facilitated the conversion to NAS of an estimated 20,000 enterprises, the Tax Manual, the Financial Accounting Manual (in partnership with Academy of Economic Studies of Moldova)

• Prepared for approval 36 National Standards on Auditing based on ISA, Code of Ethics

REPARIS Vienna Workshops "Ethics in the Accountancy Profession" March 14-15, 2006

11

ACAP ACCOMPLISHMENTS (CONT.)

• Implemented national and international (CIPA) certification programs and exams for accountants based on IFAC education standards (88 CAPs, 1 CIPA)

• Assisted in strengthening partnership with the University of Nebraska at Omaha (UNO) in developing new accounting curriculum and exchanges of professors (2001-2003)

• Held over 400 seminars in various accounting disciplines which were attended by 6,900 participants in past three years

• Held Training Sessions for over 80% of the licensed audit firms in the Audit of Financial Statements According to the National Standards on Auditing (in Fall 2000)

• Held Roundtables on IFAC IES, on discussions of new drafts on Accounting and Auditing Laws, on CIPA Program Promotion, etc..

REPARIS Vienna Workshops "Ethics in the Accountancy Profession" March 14-15, 2006

12

ACAP GOALS & PERSPECTIVES:

• One of the main goal: to cover substantial number of accountants in the country; Increase Active Membership Rolls

• Enrich and Expand The Accountant//Auditor Certification Program

• Work on implementation of IFAC Statements of Membership Obligations

• Inform Members, Firms and All Others Involved in Accountancy Education about IFAC IES

• Work towards Implementation of IFAC Ethics and Quality control requirements even without Direct Responsibility

• To achieve the role as the influencer in accounting profession’ development in Moldova and as the good standing representative of Moldova’s accounting and auditing professionals,

• Dedicate substantial efforts to eliminating its dependency on external funding sources.

REPARIS Vienna Workshops "Ethics in the Accountancy Profession" March 14-15, 2006

13

POSITION OF IFAC MEMBER BODY

Code of Ethics for Licensed auditors and professional accountants should be based directly on IFAC Code of Ethics (June 2005)

Cooperation with the Ministry of Finance on new regulations and AA reform implementation

New Law on Auditing should provide a comprehensive regulatory framework for a significant improvement in the audit practice

Understanding of benefits for professional membership at least with one of existing professional organizations. (e.g. UK, Romania, Russia, etc.)

REPARIS Vienna Workshops "Ethics in the Accountancy Profession" March 14-15, 2006

14

II. THE LEGAL FRAMEWORK on AUDITING - CURRENT STATUS

The Law on Auditing dates back to 1996. Regulations on certification of auditors and licensing of auditing

activity approved by the Ministry of Finance – certification is done by Attestation Commission under MoF.

37 National Standards on Auditing and 7 National Auditing Practice Statements approved by the Ministry of Finance and published by 2005.

Code of Professional Conduct for Auditors and Accountants of the Republic of Moldova – issued by MOF.

Conclusion: Major problem in current legal framework – no effective enforcement mechanisms.

REPARIS Vienna Workshops "Ethics in the Accountancy Profession" March 14-15, 2006

15

THE NSA, CODE OF PROFESSIONAL CONDUCT, AND LAW ON AUDIT

DEVELOPMENT PROCESS

• Joint effort by MOF, SROs, audit practitioners, accountancy academia

• The Working Group on the Development of NSA under the auspices of MOF renewed

• NSAs and the Code of Professional Conduct are published in the Monitorul Oficial Government Newspaper

REPARIS Vienna Workshops "Ethics in the Accountancy Profession" March 14-15, 2006

16

CURRENT STATUS

National Standards on Auditing (NSA) are Based on ISA (1999 and 2000 IFAC technical pronouncements)

NSAs are effective for audits of financial statements covering periods beginning on January 1, 2001

The new Draft Law on Audit is being debated by the Government with subsequent submission to the Parliament and approval till end of 2006 – is trying to comply with the current best practices

REPARIS Vienna Workshops "Ethics in the Accountancy Profession" March 14-15, 2006

17

REVISED DRAFT OF NEW AUDIT LAW

Subject to be approved by the Parliament in 2006

Shall Became in force since 2008

General Provisions:PIOB creation Annual Meeting of Auditors Written qualification exam with content largely

compliant with IFAC education guidelines, (by State)CPD requirements – 40 hours per yearAccreditation of CPD providers, (by State)

REPARIS Vienna Workshops "Ethics in the Accountancy Profession" March 14-15, 2006

18

CODE OF PROFESSIONAL CONDUCT OF AUDITORS AND ACCOUNTANTS OF THE

REPUBLIC OF MOLDOVA

The Code is based on IFAC Code for Professional Accountants as revised in January 1998

Approved by the Ministry of Finance and published on March 15, 2001

The Code is effective January 1, 2002

REPARIS Vienna Workshops "Ethics in the Accountancy Profession" March 14-15, 2006

19

CODE’ S STRUCTURE

Part A – framework applies to professional accountants in public practice and employed professional accountants unless otherwise specified (all professional accountants)

Part B – professional accountants in public practice

Part C – employed professional accountants (professional accountants in business)

REPARIS Vienna Workshops "Ethics in the Accountancy Profession" March 14-15, 2006

20

FUNDAMENTAL PRINCIPLES:

1. INTEGRITY

2. OBJECTIVITY

3. PROFESSIONAL COMPETENCE AND DUE CARE

4. CONFIDENTIALITY

5. PROFESSIONAL BEHAVIOR

6. TECHNICAL STANDARDS

REPARIS Vienna Workshops "Ethics in the Accountancy Profession" March 14-15, 2006

21

TO WHOM CODE IS APPLY?

April 1, 2004 February 1, 2006

Certified Auditors 173 130

Including those employed with audit firms

125 75

Sole practitioners 8 5

Audit firms 117 101

Listed companies 25 26

Accountants in business - 5,800 industrial entities

REPARIS Vienna Workshops "Ethics in the Accountancy Profession" March 14-15, 2006

22

III. IMPLEMENTATION OF THE ETHICS CODE in MOLDOVA -CURRENT STATUS

Auditing Act does not provide for abiding by a Code of ethics Neither the MoF nor any professional bodies effectively monitor auditors’

compliance with Auditing Standards and the ethics code Quality control for audit work, which appears to be applied mainly only by the

audit firms within international network Auditing practices tend to depart from the standards in several areas (e.g.

third- party confirmation of debtors & creditors; inquiries of subsequent events and the appropriateness of management’s use of the going concern assumption;)

Professional continuing education & development is not mandatory to retain a certificate of auditor and is only carried out by audit firms whose internal policies set such requirements (Note. Currently certificates are issued for a term of 5 years)

The professional examination required for the issuance of the auditor certificate does not comply with related IFAC Education Standards and EU 8th Directive.

REPARIS Vienna Workshops "Ethics in the Accountancy Profession" March 14-15, 2006

23

EXPERIENCE OF IMPLEMENTATION OF THE ETHICS CODE IN MOLDOVA

4 years of experience shows:

As of February 1,2006: 101 audit firms, including 4 of Big Four;

5 sole individuals

73 licensed auditors

Only 3 cases of suspension of audit organizations’ licenses and 1 case of revocation in 2005

REPARIS Vienna Workshops "Ethics in the Accountancy Profession" March 14-15, 2006

24

ETHICS CODE’ S ENFORCEABILITY

The code is not legally enforceable No Ethics problem solving mechanism No enforcement procedures’ existence - no disciplinary committee or sanctions to apply No requests from public “Expectations Gap” Lack of knowledge by companies’ management

related to ethics Conclusion – no effective implementation of the code is possible without effective monitoring/enforcement mechanisms that would cover at least accountants in public practice

REPARIS Vienna Workshops "Ethics in the Accountancy Profession" March 14-15, 2006

25

ENFORCEMENT ACTIVITY by ACAPProvisions of ACAP Strategic Plan for 2003-2008 regarding : --- Code of professional conduct:• Monitoring of observance of the Code of professional conduct,• Appling disciplinary measures to the members

--- Quality control and disciplinary activities:

• committee on quality control of observance of professional standards and ethics, and also to develop its internal procedures for realization of control activity.

• Protection of the legal rights and assertion’ professional interests of members of the association in the solution of disputable and\or conflict issues.

• carry out regular discussions of demands and blames from organizations concerning the members of the association.

• observation the honour and objective approach in the solving of disputes and to follow precisely the legislation while making disciplinary decisions. Note. It is one of the most complex and non-realized issues related to public and state recognition of profession

REPARIS Vienna Workshops "Ethics in the Accountancy Profession" March 14-15, 2006

26

IFAC CODE OF ETHICS (as of JUNE 2005)

Became in force June 30, 2006 for ACAP RM members

Decision subject to be made by ACAP Annual Membership meeting in April 2006 (around 800 members, from which 88 CAPs, 1 CIPA, 2 CPA, 23 licensed auditors)

plans to be submitted to the MoF Working Group for further discussions and approval for all accountants and auditors

REPARIS Vienna Workshops "Ethics in the Accountancy Profession" March 14-15, 2006

27

IV. DIFFICULTIES & SOLUTIONS

Issues: - no government regulation of the AA Profession exists

- no professional regulation of accounting profession exists

Gap of expectations:- understandings of Independence rule

- publicity / disclosures

- advertisements

- companies management and corporate governance culture: luck of understanding regard ethics and audits

REPARIS Vienna Workshops "Ethics in the Accountancy Profession" March 14-15, 2006

28

FACTORS EXPLAINS THE DIFFICULTIES

Lack of understanding of the audit process by economic entities

Governance structures among the companies are limited

Lack of practical experience and technical expertise for applying Standard on Audit and enforcing Code of Ethics

Absence of monitoring and effective sanctions and remedies

Market does not recognize and does not understand (and does not encourage) benefits for accountants to be part of professional organization

REPARIS Vienna Workshops "Ethics in the Accountancy Profession" March 14-15, 2006

29

WHAT PROFESSION COULD BENEFIT FROM ACAP RM

Certification Program in line with IFAC and EU requirements - CIPA

CPD Programs, including SEEPAD Regional seminars

IFAC Publications & updates; other relevant library resources

Training Programs (MoEd Licensed)

Exchange of information (e.g. from international partnerships)

Relatively Low cost membership – for high quality services

REPARIS Vienna Workshops "Ethics in the Accountancy Profession" March 14-15, 2006

30

V. ACTIONS TO BE TAKEN

Approval of New Audit Law

An independent PIOB of auditors should be established

Develop guidelines

Implementing the quality control based on international standards principles

JEEP – Joint Ethics Enforcement Procedures

Strengthen of the professional education & training, Continue Professional Development

Encourage that accountant in public practice to be part of one professional organization

REPARIS Vienna Workshops "Ethics in the Accountancy Profession" March 14-15, 2006

31

FUTURE DEVELOPMENTS

Development of guidelines to support the new Audit law - certification and CPD guidelines

Development of the full blown Manual on Auditing & Ethics Establishment of a system where all newly approved ISAs

and revisions thereof become effective in Moldova without a lengthy leucocratic adoption process

Delegation of some costly activities to professional organizations - e.g. certification, training, drafting and translating standards with subsequent approval by Government body, etc.

Establishing an effective enforcement mechanism – Public Oversight Body and active participation of professional organizations in enforcement

REPARIS Vienna Workshops "Ethics in the Accountancy Profession" March 14-15, 2006

32

Strengths Weaknesses

IFAC Standards Are Adopted Mismatch Between the Law, Rules, Regulations & Capacity to Comply

Capacity Issues are To Be Expected Considering the Short Times Involved

Puts Added Burden on Accelerating Capacities on:

EducatorsRegulatorsUsersPreparers & Auditors

ISSUES TO BE CONSIDERED IN FUTURE*

Compliance & Enforcement

* Source: Dr. Gert Karreman, Carana Corp.: GAEB - GLOBAL ACCOUNTANCY EDUCATION BENCHMARKING FOR SEEPAD

REPARIS Vienna Workshops "Ethics in the Accountancy Profession" March 14-15, 2006

33

Strengths Weaknesses

Disciplinary Committees Established Framework for Disclosure of Substandard Work or Unethical Behavior Is Not In Place or Functioning

Due Process Procedures for Discipline Are Not Developed

Sanctions Are Generally Inadequate

Peer Reviews Have Started No Public Forum to Announce Sanctions

Compliance & Enforcement (continued)

REPARIS Vienna Workshops "Ethics in the Accountancy Profession" March 14-15, 2006

34

Strengths Weaknesses

More CPD Courses are Offered To A Wider Audience

Short on Capacity of Facilities, Trainers and Course Content

Ethics Courses Offered Teaching of Ethics & Values Must Start Early in Schools

Mismatch Between Demands of the Market and Capacity to Deliver

Organized, Functioning and Assisting Members

“Branding” of the Professional Bodies Outputs Has Not Been Accomplished

Certain Segments of the Market Prefers “Certificate” of Imported Brands

International Recognition is Lacking

CPD

REPARIS Vienna Workshops "Ethics in the Accountancy Profession" March 14-15, 2006

35

Strengths vs. Weaknesses

• Quote from Michael Hammer: “. . .The formulas for yesterday’s success are almost guaranteed to be formulasfor failure tomorrow.”

• Chinese Proverb “Tell me … I’ll forget. Show me … I may remember. Involve me… then I’ll understand.”

• Educate Me and I Will Perform!

THANK YOU FOR YOUR ATTENTION!

Contacts: ACAP RME-mail: [email protected], [email protected] Tel.: (+ 373 22) 541-412, 543-408, 541-495