Embed Size (px)

Citation preview

Report No. 1 5063-AR

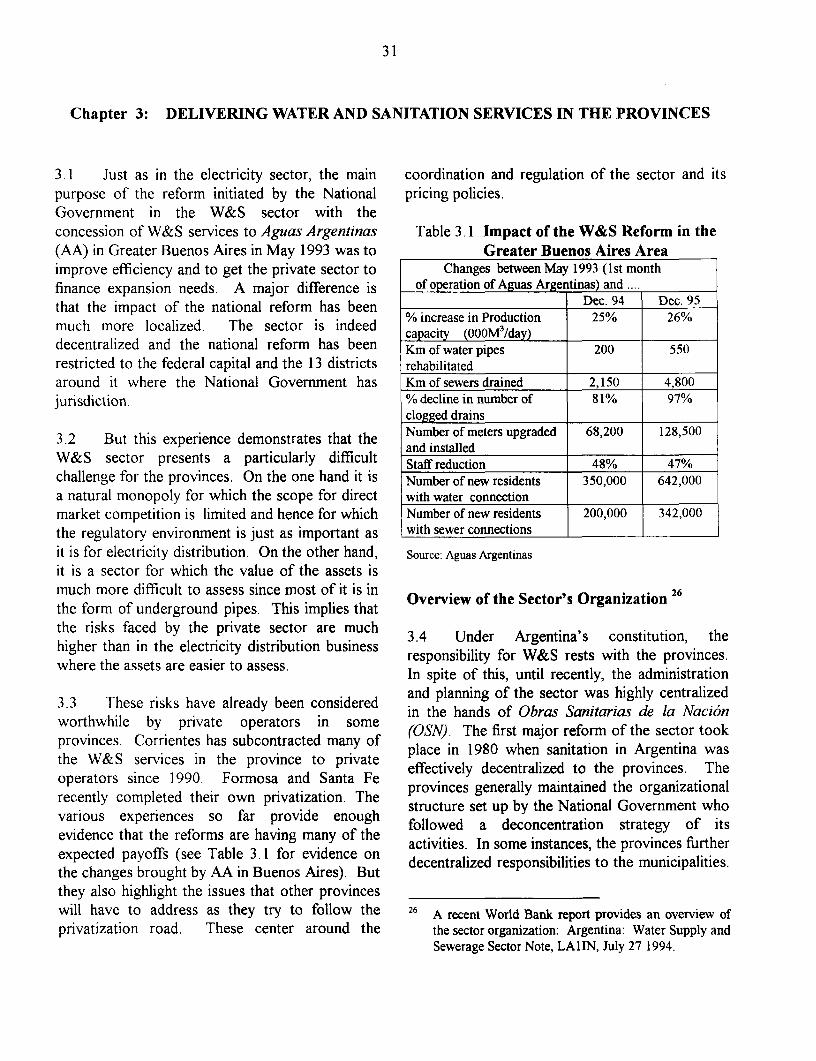

ArgentinaReforming Provincial Utilities:Issues, Challenges and Best PracticeJune 6, 1996

Infrastructure DivisionCountry Department ILatin America and the Caribbean Region

4 ' '2' ' ,,.''0 , :, -:,,,:f... .

, ,.,_ .

* ou~v r - h W -, - ,, ,.,*

CURRENCY EQUIVALENTS

Currency Unit - Argentine Peso (A$)

US$ = A$1

WEIGHTS AND MEASURES

The Metric System is used throughout this report.

FISCAL YEAR

January I to December 3 1

ACRONYMS

AyE Agua y EnergiaCAMMIESA Compafiia Administradora del Mercado Mayorista Electrica Sociedad An6nimaCFE Federal Council of Electric EnergyCOFAPYS Consejo Federal de Agua Potable y SaneamientoENOHSA Ente Nacional de Obras Hidricas de SaneamientoES The National Energy RegulatorENRE Ente Nacional Regulador de la ElectricidadETOSS Ente Tripartito de Obras y Servicios SanitariosGUMA Gran Usuario MayorGUME Gran Usuario MenorLRMC Long-run marginal costNARUC National Association for Regulatory Utility CommissionersNRRI National Regulatory Research InstitutePPAD Precio de la potencia puesta a disposici6nRMBA Reforma Metropolitana de Buenos AiresSADI Sistema Argentino de Interconexi6nSRNAH The Secretariat of Natural Resources and Human EnvironmentSPAR Provincial Service for Drinkable Water and Rural SanitationSWR Subsecretariat of Water ResourcesPWS Public Works SecretariatW&S Water and Sanitation Services

PREFACE

This report has been prepared by a team led by Antonio Estache (LA1IU) based on the findings ofmissions to Argentina in February 1995 and in June 1995. The core team included Claude Crampes(Universitd de Toulouse, Institut d'Economie), Marianne Fay (AF lET), Walter Garcia-Fontes (UniversitatPompeu Fabra, Barcelona), Frannie Humplick (PRDEI), and Thomas-Oliver Nasser (MIT and Institutd'Economie Industrielle, Toulouse). The report also benefited from background papers by XavierFreixas (Universitat Pompeu Fabra, Barcelona), Felix Helou (Consultant), Martin Rodriguez-Pardina(Consultant), Ben Shin (PSD) and Warrick Smith (PSD). Also we would like to thank Secretary Zapata,Mr. Segnana and Mr. Vega, our main counterparts during the mission, for providing us with atremendous amount of information and allowing us to meet key counterparts from the Provinces ofBuenos Aires, C6rdoba, Mendoza, Neuqu�n, Santa Fe, Santiago del Estero, Tierra de Fuego andTucum�n. Finally, we would like to thank Secretary Bastos and Undersecretary Rotaeche for very usefuldiscussions and insights.

Background Papers Supporting the Report

Fay, M. (1994), "Infrastructure and Growth in Argentina", mimeo, the World Bank, LAIIN

Fay, M. and A. Estache (1995), "Regional Growth in Argentina: Determinants and Policy Options",mimeo, The World Bank, LAI IN

Freixas, X. and W. Garcia-Fontes (1995), "Infrastructure Financing for Argentina's Provinces: Issuesand Options", mimeo, the World Bank, LA1fl�4

Humplick, F. (1995), "Infrastructure Performance in the Provinces of Argentina", mimeo, The WorldBank, LAlIN

Humplick F., and T. 0. Nasser (1995), "Risk in Provincial Infrastructure Provision: An Investor'sPerspective", mimeo, The World Bank, LAlIN

Rodriguez-Pardina, M. and F. Helou (1995), "Comparaci6n de Marcos Regulatorios en Argentina",mimeo, The World Bank, LAIIN

Smith, W. and B. Shin (1995), "Regulating Infrastructure: Funding Regulatory Agencies", mimeo, TheWorld Bank, LAlIN

Smith W. and B. Shin (1995), "Regulating Infrastructure: Perspectives on Decentralization", mimeo, TheWorld Bank, LAI IN

ARGENTINA

REFORMING PROVINCIAL UTILITIES:

ISSUES, CHALLENGES AND BEST PRACTICE

TABLE OF CONTENTS'

Executive Sum m ary .............................................. i

Chapter 1: INTRODUCTION .......................................... ,.1The Need for Credible Provincial Commitment .................... ....................... IWhat Competition in Utilities Entails ........................................... , . 2What Contract-Based Regulation Entails ........................................... 5Does the Provincial Choice of Regulatory RegimesMatter to a Potential Investor? ........................................... 6What Decentralized Regulation Entails ........................................... 7

Chapter 2: REFORMING ELECTRICITY DISTRIBUTION IN THE PROVINCES ................ 9Overview of the sector's Organization ............................................................... 9The "Regulators" ....................... 14Contracts as the Main Regulatory Tool ........................... 17How Competition Works ........................... 18Pricing ...... , .. ,,,,,.,.... 18Investment and Tariffs ................................. 26Summary of the Main Recommendations ................................. 29Generation ................................. 29Transmission ................................. 29Distribution ................................. 29Regulation ................................. 30

Chapter 3: DELIVERING WATER AND SANITATIONSERVICES IN THE PROVINCES ......................................... 31Overview of the Sector's Organization ......................................... 31The "Regulators" ......................................... 32Contracts as the Main Regulatory Tool ......................................... 33How Competition Works ......................................... 36

lThis report was produced under the supervision of Mr. Gobind Nankani, Director; Mr. Asif Faiz, Division Chief,Infrastructure and Urban Development; and Mr. Danny Leipziger, Lead Economist, Country Department I, Latin Americaand the Caribbean Regional Office. The peer reviewers for the early drafts were Messrs. 1. Kessides, PSD and L. Guasch,LATAD.

Pricing .............................................. 37Investment and Tariffs ............................................. 40Summing up the Main Recommendations ................ ............................ 41On Tariff Design ............................................ 42On Contract Selection ............................................ 42On Institutional Reform ............................................ 42

Chapter 4: DEVELOPING A PROVINCIAL REGULATORY CAPACITY ....... 43Breaking with the Past ...................................................... 43Constraints and Trade-Offs ...................................................... 44Sectoral Breadth of Authority ...................................................... 45Is Representation Needed in Each Municipality? ................................................... .. 46Minimization of Regulatory Demands ....................................................... 46Size of Agency Staff ...................................................... 47Strengthening Regulatory Capacity ...................................................... 48Funding the Regulatory Agency ...................................................... 49Organizing Interprovincial Cooperation on Regulatory Matters ............................... 50Summing Up ....................................................... 50

TABLES

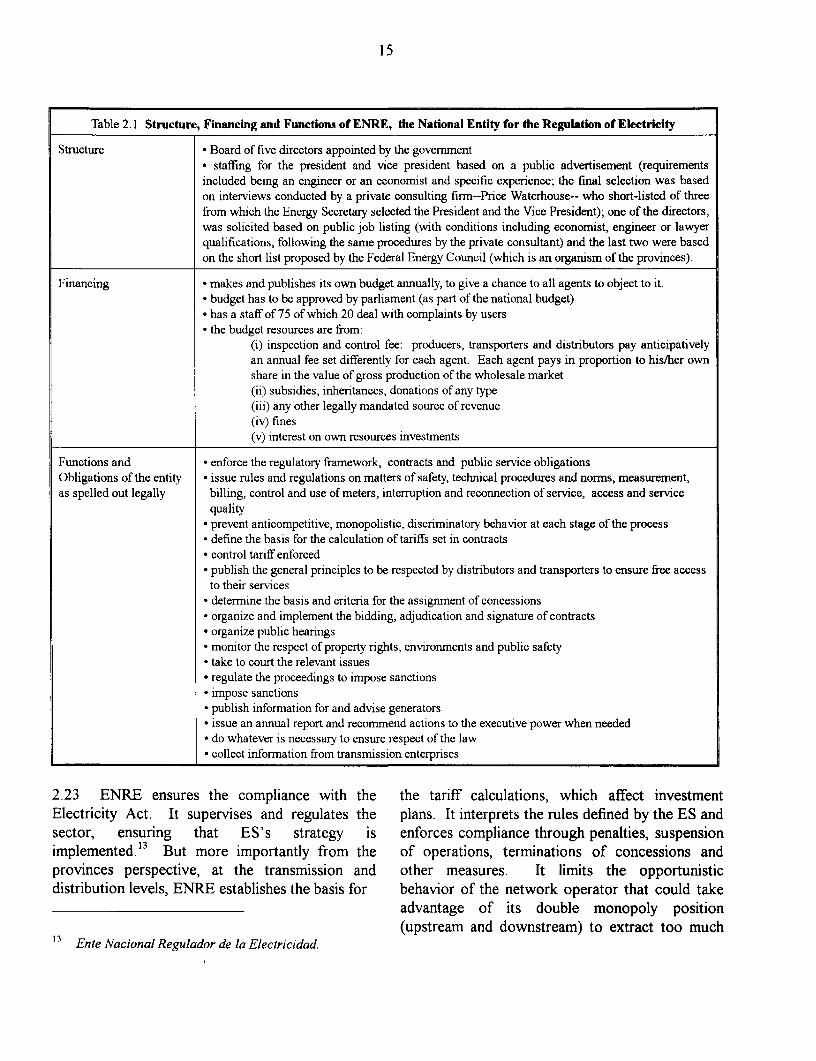

Table 1.1 a Status of Provincial Reforms in Electricity ....................................................... 1Table 1. lb Status of Provincial Reforms in W&S ...................... .. 1..............................ITable 1.2 Summary of Main Concession Contracts ....................................................... 4Table 2.1 Structure, Financing and Functions of ENRE, the National

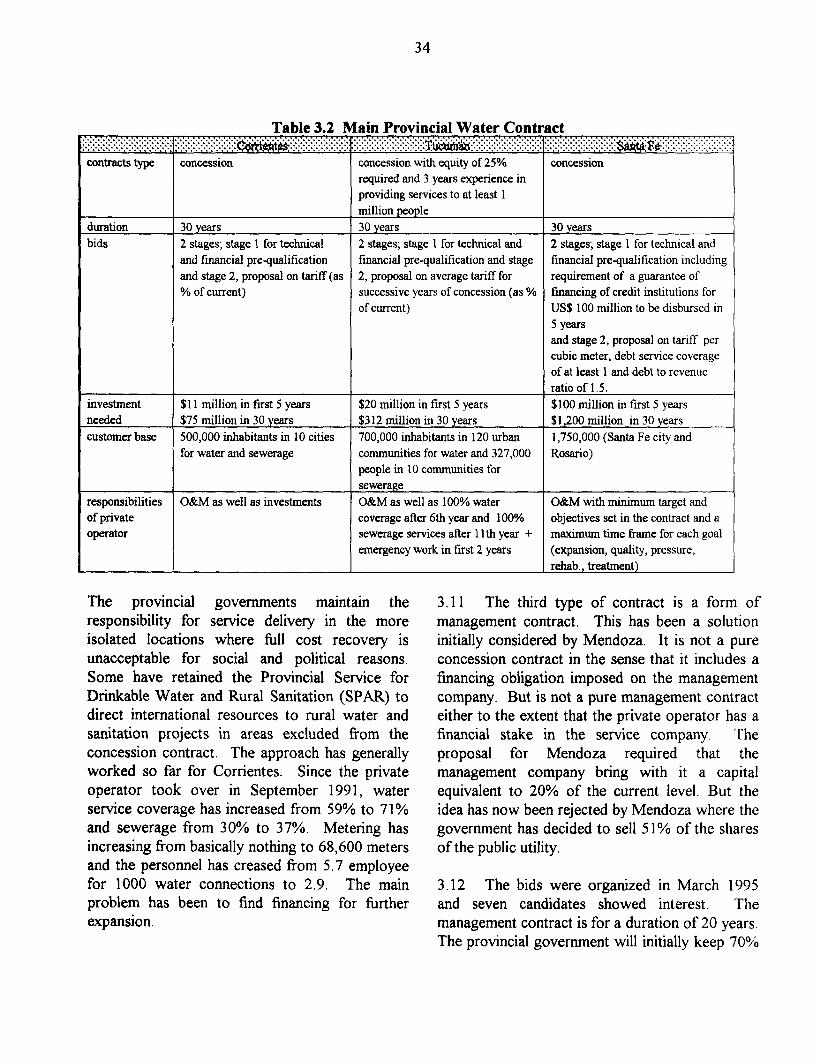

Entity for the Regulation of Electricity ........................ .............................. 15Table 3.1 Impact of the W&S Reform in the Greater Buenos Aires .......................... ................ 31Table 3.2 Main Provincial Water Contract ...................................................... 34

BOXES

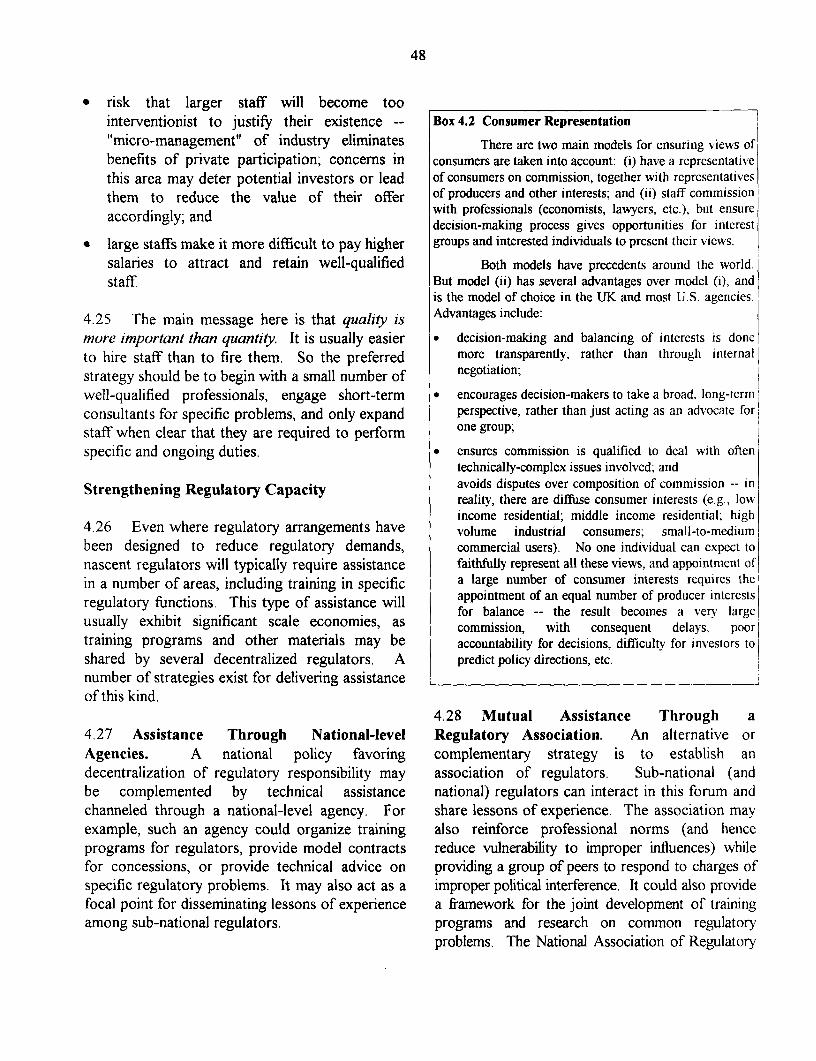

Box 1.1 How to Check if the Reform is being Captured by the Bidders? ............. ...................... 3Box 1.2 Comparing Concession Process in W&S and in Electricity ......................................... ... 5Box 2.1 Who are the Main Generators? ...................................................... 12Box 2.2 Who Transmits where in Argentina? ...................................................... 13Box 2.3 What did the Concessionaires do with their Property Rights

in Distribution? ...................................................... 14Box 2.4 How are the Marginal costs Computed? ...................................................... 19Box 2.5 Dealing with the Seasonality of Prices ...................................................... 23Box 2.6 A Comparison of Tariffs across Provinces ...................................................... 24Box 3.1 The Timing of the Privatization Process in Greater Buenos Aires ............... ................. 33Box 3.2 Goal-Based vs. Process-Based Contracts ...................................................... 35Box 3.3 What Contract Renegotiation Reveals ...................................................... 36Box 3.4 What Yardstick Competition Entails ...................................................... 37

Box 3.5 Why does the Concessionaire Want Meters Everywhere ............................................. 39Box 3.6 What's Wrong with the Average Price of Water in

Argentina's Provinces? ................................................ 40Box 3.7 Willingness to Pay for Sewerage ................................................ 41Box 3.8 Dealing with Social Concerns ................................................ 41Box 4.1 How to Appoint Regulators? ................................................ 44Box 4.2 Consumer Representation ................................................ 48

FIGURES

Figure 2.1 Financial Flows ................................................ 11Figure 2.2 Marginal Cost and Inverse Demand ................................................ 20Figure 3.1 ................................................ 39

ARGENTINA - REFORMING PROVINCIAL UTILITIES: ISSUES, CHALLENGES ANDBEST PRACTICE

EXECUTIVE SUMMARY

This report analyzes the reform needs and options in electricity distribution, and water andsanitation services (W&S) in Argentina's provinces. The main focus is on the regulation of privateoperators since many provincial governments are considering concessioning all or part of theseservices to the private sector to improve quality and rely more on private financing of the sectors'expansion needs. Tariff design and institutional concerns are emphasized in a detailed analysis of thespecific regulatory framework of both sectors, including some issues raised by federal regulationrelevant to the decisions of potential investors in provincial utilities.

Main conclusion. The report strongly endorses the general concessioning strategy followedby most provinces. This strategy has already generated substantial gains in utilities under Federalcontrol. In electricity for instance, tariffs have slightly decreased on average since privatization andquality of service have improved significantly. For instance, the average number of annual serviceinterruptions was cut from at least 7.6 to 5, and the average duration from 23 hours/year to9.9 hours/year. However, not all provinces will be able to follow a strategy relying on privateinvestors as they vary tremendously in terms of potential rate of return and commercial as well as non-commercial risks (including political and fiscal risks). Some of the poorest provinces combine lowpotential return and high risks' levels and are unlikely to be very attractive under deals and regulatoryarrangements that try to shift most of the risk onto the private investors. For these provinces or forthose not wishing to transfer outright the W&S and electricity distribution services to the privatesector, the report offers alternatives. It suggests, in the short run, the commercialization of theseservices through management and service contracts with private companies can serve to establish thecredibility of the provincial commitment to reform. But this should be viewed as a first step towardsthe implementation of concession as it gives investors a chance to obtain more independentinformation on the value of the assets for which they would be bidding

The keys to successful provincial utilities reforms. The National Reforms demonstrate thatto maximize the gains from the "privatization" strategy, the following steps are needed:

* make the most of what competitionfor the market allows,

* give an incentive to new owners to remain concerned with the public interest;

* assign rights and obligations in the contract as clearly as possible,

* anticipate the potential needs for renegotiation;

* define the nature and form of property to maximize accountability,

* do not underestimate the importance of tariff design; and

* prepare and develop the provincial regulatory capacity as carefully as the contract.

ii

Do not underestimate what can be achieved through competition for the market.Whether in the area(s) of operations, management or specific services, competition for the service iscrucial to the success of the current reform efforts. Competition and increased private sectorinvolvement also reduce arbitrary political interference in price setting or employment decisions, forinstance. Although the specific form of private sector involvement in each province will have to betailored to fit local needs, constraints and preferences, the introduction of competition, if implementedcorrectly, will cut total service costs, pass a large share of these cuts to all consumers and improveresponsiveness to users. The success of the approach (in terms of fiscal impact but also in terms ofservice quality and price) depends a lot on the design of the bids to assign the operator's role in aconcession, management or service contract. Some of the provinces are clearly aware of theimportance of this step in the reform process: it ensures the credibility of the provinces'announcements and their commitment to change. For instance, the province of Santa Fecommissioned an independent assessment of the value of the net assets of its utilities (done by aninternationally recognized external expert). This provided independent information on the potentialfiscal impact of the reform. It also revealed up front as much reliable information as possible topotential investors. This type of assessment can also avoid some uncertainties in terms ofrehabilitation needs and reduce the risk of unexpected tariff adjustments as those approved for AguasArgentinas over and above what was agreed in the original contract.

Ensure the managers' and workers' accountability. If property is distributed, the way it isdone can also contribute to the success of the reform. Shares can be sold on the stock market towiden the dissemination of property and hence of accountability as was once considered (buteventually rejected) for Aguas Argentinas. Shares can also be allocated to workers and employees, asfor electricity transmission under federal jurisdiction, giving them an effective incentive to support thereform and to act in the interest of the enterprise. But there are risks in spreading accountability toothinly. This is why it is generally suggested to allow the bidding of packages of shares large enough toallow control by one major interest i.e., to have a strategic investor.

Clearly spell out the rights and obligations of all parties. Under the strategy adopted bythe provinces, contracts (concession, management or services) are the main regulatory instrumentduring the tenure of the private operator. Where and when governments do not have a long trackrecord in dealing with the private sector, contracts need to be drawn as tightly as possible to reduceopportunities for discretionary government actions. Contracts are intended to be enforced accordingto their terms. The provincial reforms will only work if the provincial governments recognize thatonce a private operator takes over, this operator is in charge within the specific terms of its contract.

Anticipate the potential needs for renegotiation. Even if a province has well prepared itscontracts, unforeseen events will happen. This means that even if contracts should be prepared asdocuments that are not intended to be modified and include adjustment mechanisms to avoid the costsand uncertainty of renegotiation, under very specific and very limited circumstances, a limited degreeof contract flexibility may be good public policy. To ensure that the contract is a credible regulatoryinstrument, contract modifications should be based on some fair and workable rules based on clearlyspelled out policy criteria (discussed in the report). These rules should be agreed upon by all involvedparties, and the guarantee of this agreement should be provided by an independent regulator as anhonest broker. Unilateral modification of the rights defined in the contract or the bidding documents(say through request to accelerate investment programs or impediments to tariff adjustments) without

iii

full compensation is tantamount to expropriation and defeats the purpose of the reform. It is the riskof arbitrary government behavior of this kind that historically created the biggest risk for privateinvestors in infrastructure and that continues to deter many deals.

Keep the new private monopolies working in the public interest. Once the contracts havebeen awarded, it may be difficult for the government to get the private operator or managers to focuson the interest of consumers as much as on their own interest. To maximize the incentive for efficientbehavior during the concession, the contracts can require that new auctions be organized at regularintervals as it was done in the case of the electricity distribution concessions orchestrated by theNational Govemment. Another incentive for provincial monopolies to maintain their concern for theinterest of consumers is to rely on some formal comparison of performance across provinces. Thesecomparisons should be widely disseminated (in the media) to increase the public pressure foraccountability. These comparisons can also be used more formally by regulators to push prices totheir lowest possible level ("yardstick competition"). This requires a strong inter-provincialcoordination to standardize information which could be organized by the National Regulators.

Get the tariffs design right. All reformers recognize that the design of tariff formulas are atthe core of effective regulation. However, few appreciate its complexity and relevance to the long-term sustainability of the provincial utility reforms. The report discusses how tariff design matters toensure the best allocation of scarce provincial resources. In the context of this analysis, it identifies afew issues that deserve their immediate attention. Some of these issues are under their direct controland should be handled as part of the reform process. Some are under the responsibility of the NationalGovernment but need to be monitored by provincial reformers to allow them to anticipate theconcerns of potential investors in provincial utilities.

In Electricity, the provinces trying to introduce more efficient pricing of distribution services(including an incentive to maximize productivity gains) should adhere to the tariff methodologycontained in the national electricity law with some adjustments. Chapter 2 shows that:

* If regulation continues to be based on price capping (aims at giving incentive to minimize costs),there is a need to very quickly define a methodology and gather the information needed tocalculate the productivity gains that should be passed on to consumers.

* There is also a need to review the current tariff methodology in order to make sure that the interestof "captive consumers" are protected. The current approach creates a distortion due to thepossibility of direct contracts between "large users" and "generators". The consequence of thesecontracts is that captive consumers (i.e., those who are not large enough to be able to buy withouthaving to go through the distribution companies) may have to pay much higher rates because theyare paying for more expensive wholesale contracts transferred at the time of privatization andlarge users opt out to negotiate cheaper contracts in the wholesale market. This could lead todifficult political problems as "privatized" tariffs may end up increasing significantly in relativeterms for a large share of the consumers. This could be avoided by allowing some more pricingflexibility and some degree of discrimination in prices.

In addition, the provincial governments will have to monitor the developments in transmissionpricing, one of the very few serious outstanding issues in the otherwise very impressive NationalSector Reform. Better and clearer rules (based on economic benefits rather than on energy flows) are

iv

needed to avoid the type of difficulties recently met in discussions of the construction of a fourthtransmission line in the Comahue corridor. Existing rules have a bias towards underinvestmentbecause they fail to assign a clear responsibility for the payment of the construction costs of anyexpansion. Since transmission is the physical instrument to guarantee competition in generation andsupply, this underinvestment is increasingly a concern to potential investors in distribution. Moreover,as more and more provinces privatize their distribution companies, the relationship between thetransmission concessionaires and the distribution concessionaires is likely to change, and the tolls mayhave to be revised to ensure consistency with economically efficient pricing rules and revenueadequacy.

In W&S, Chapter 3 shows that the regulatory challenge is much wider and complex:

* A radical tariff reform is needed to achieve efficiency in the use of water and to finance growinglong-term investment needs, particularly in the sewerage systems. It will involve increasedmetering, eliminating the current tariff for unmetered consumption and redesigning the fixed partof the current two-part tariff used for metered consumption, since it currently leads to multipletypes of cross subsidies, and since it fails to provide much incentive to minimize cost and to investin the expansion of the sewerage system.

* This tariff reform will have to be implemented as part of a wider reform which should aim at theadoption of commercial practices in the sector. This means that the provincial governments willhave to give up many of the controls they are now imposing on their public enterprises and aim atregulatory simplicity when identifying what needs to be controlled/regulated and what need not be(and this will require strong coordination with the National Government).

* The concerns with the high level of uncertainty regarding the asset value and the costs of therehabilitation needs expressed by potential private investors interviewed by the Bank are such thatsome of the provinces will have to consider a slower pace of reform, and will have to focus onshort-term management contracts with an option to transform them into concession contracts inthe longer run. It may also be worth considering the bundling of W&S assets across provinces, ortheir bundling with other assets such as electricity to reduce the overall risk faced or perceived byprivate investors. None of this should affect the efforts to reform tariffs and increase metering.

Develop the provincial regulatory capacity. The most difficult provincial challengeaddressed in the report may be the need to monitor that the behavior of the privatized monopolies areconsistent with the terms of the contract as well as with public aims. This monitoring is neededbecause concessionaires will have strong incentives to behave inefficiently when left unsupervised.The creation of regulatory bodies or the use of the strength of law and courts will be an importantelement in the success of the provincial reform of utilities and Chapter 4 focuses on this exclusively.But there is a need to distinguish between technical and economic regulation in both sectors.Economic regulation does not have the same goals as technical regulation so that its organization isnot necessarily identical to the technical one. For the electricity sector, the difference can beillustrated as follows: at the terminal nodes of the interconnected electric network there is little needfor technical control, but it is a place where provincial distributors can try to exploit their exclusiveposition in front of captive consumers and hence economic regulation may be needed even if technicalregulation is not. Therefore, the skills needed to develop the provincial regulatory capacity are notsimply a recycling of the skills needed to provide the service in a public enterprise. Some of the staff

v

of the former public utility will have to be dismissed and new staff will have to be recruited tointroduce these new skills in the provincial regulatory entities.

Aim at a single independent sector specific agency. While the Report shows that someeconomic regulatory responsibilities may be justified at the provincial level in electricity and W&Seven when technical regulation is not needed, it also shows that if each province must have its ownregulatory capacity, the local entity should be kept to a minimum and only have specific prerogatives,essentially auditing and reporting to the national regulation body. This is particularly important inelectricity because technical dependencies within the network are very strong. Moreover, therecognition of a role for provincial regulation is not an endorsement of the creation of multiple sectorspecific regulatory agencies. The international experience suggests that most provinces would bebetter off with a single independent entity for all utilities. Chapter 4 explains in detail how to achievethat independence in terms of nomination of regulators and financing of the agency.

Do not simply staff the agency with the employees fired by the private operator. Thestaffing level of the agency should be modest and its composition should depend on the requirementsof specific tasks assigned to the regulatory agency. As discussed in the Report, there are many goodpossible criteria for selection (i.e., technical excellence, political representation, ...). With a fewexceptions, the experience considered relevant in the staffing process at the national level was basedon engineering aspects of the sector while economic regulation, the main purpose of these entities, isquite different from technical regulation. This suggests that the selection criteria for the regulatorsshould include expertise in economic fields. While the skills needed to be a good regulator are hard tofind, they are very similar in both, the water and electricity sector, and hence the same resources canbe shared within a single provincial regulatory entity. This means lower resource needs (not only interms of staff but also in terms of equipment) and hence a lower burden on the taxpayers or thebeneficiaries of the services. There are other benefits. For instance, it facilitates learning betweensectors, ensures consistent approaches to central policy questions, and makes the regulator lessvulnerable to industry or political capture. This lower vulnerability enhances the credibility of theagency and reduces risks for investors.

Spell out the implementation strategy. The strategy to implement this regulatory agencycan be flexible. If no agency has been established yet, a core multisectoral framework can be set upfirst and then sectors can be added to the core entity when appropriate. There is no need to wait untilany contract has been signed. The creation of an entity can be instrumental in assisting in theimplementation of the concessioning process. If one agency has already been established, it should notbe too difficult to expand the jurisdiction of the existing agency. This depends of course on howsector specific in design and composition the initial agency is. Finally, if several agencies have alreadybeen created, the best option is to develop a strategy for merging the agencies after an initial period.This strategy tends to be the most difficult and will often be resisted by both the existing regulators(concerned about losing their autonomy and possibly their job) and investors (often preferring thecounterpart they know).

Next Steps. The main conclusion of this report is that there is no single blueprint for theprovinces but that there is strong evidence of a need to further understand regulatory objectives andestablish regulatory rules and regulatory behaviors whatever the specific strategy adopted by aprovince. The ultimate aim is better and cheaper service provisions to the Argentine consumer,

vi

whether she/he lives in Bs.As. or Salta or Tierra del Fuego. The Report also aims to be a discussionreport, namely a vehicle to raise issues and begin the public dialogue necessary to extract the benefitsof a private sector participation in key utilities in Argentina's provinces.

Chapter 1: INTRODUCTION

1.1 Objectives of the report. Most provinces Table 1.la Status of Provincial Reforms in Electricityin Argentina are concerned with the high cost and _ y 1996)poor quality of service in electricity distribution Already concessioned Catamarca, Entre Rios,Formosa, La Rioja, Rio Negro,and water and sanitation (W&S) as well as with San Juan, San Luis, S. Delthe lack of public resources for their rehabilitation Estero, Tucumanand expansion. The report analyzes the reforn At the bidding stage Jujuy, Saltaneeds and options in these two sectors in With privatization and Misiones, NeuquenArgentina's provinces. The main focus is on the regulatory frarneworkregulation of private operators since many definedpregulatio gofprivaterr peratos ansincern m With regulatory Bs.As., Corrientes, Misiones,provincial governments are considering framework pending Santa Feconcessioning these services to the private sector No legal framework C6rdoba, El Chaco, Mendoza,(see Table l.la and 1.lb on the current status) yet or irrelevant Santa Cruz, T. d. Fuego (Chubutand are requesting technical assistance in and La Pampa will keep theiridentifying the main regulatory issues they will cooperatives).have to address. The lessons of the nationalexperience with contract-based regulation and Table 1.lb Status of Provincial Reforms in W&Stariff design as well as institutional issues are 1996_______________ s &

particularly detailed throughout the report--much Already concessioned Corrientes, Formosa, Santa Fe,more so than in previous recent Bank publications TucumAnon these two sectors.' This detailed analysis is At the bidding stage C6rdoba,needed to show explicitly the linkages between: With privatization and S. del Estero, Mendoza(i) tariff design on one hand, and investment regulatory frameworktargets and financing on the other hand, and definedWith regulatory Catamarca, Jujuy, La. Rioja,(ii) national and provincial regulatory issues. framework pending Neuquen, Salta, San Juan

No legal framework Bs.As., El Chaco, Entre Rios,1.2 Road Map. Chapter 2 covers the main yet or irrelevant Rio Negro, San Luis, Santaissues in the privatization of provincial electricity Cruz, Tierra del Fuego;distribution companies. Chapter 3 deals with (Chubut, and La Pampa willW&S services. Chapter 4 discusses the probably maintain theirinstitutional demands of the regulation of private cooperatives)operated utilities. The remainder of this firstchapter reviews the main general policy issues the The Need for Credible Provincial Commitm tprovincial governments will have to address and 1.3 If efficiency in the allocation of scarce

that apply to both sectors: provincial resources and better responsiveness to

* what limited credibility entails user needs are the main policy objectives of the* what competition entails provincial governments, the report endorses the* what contract-based regulation entails general concessioning strategy being followed by* what decentralized regulation entails. most provinces. But not all provinces are equally

attractive to private investors as they varytremendously in terms of potential rate of return

See for example, World Bank Report No. 35 The Power and commercial (some have low potential returnSector in LAC: Current Status and Evolving Issues by R. A. and high risks level) as well as non-commercialMoscote, S. B. Maia, and J. L. Vietti, June 1995.

2

risks (including political and fiscal risks). The these rights (say through request to acceleratereform strategy may have to be tailored to the investment programs or impediments to tariffconstraints imposed by these differences. So what adjustments) without full compensation isare the short run alternatives to concessions? tantamount to expropriation. It is the risk of

arbitrary Government behavior of this kind that

1.4 When a province does not succeed in historically created the biggest risk for privateawarding a concession contract (or does not wish investors in infrastructure. Where and whenthe immediate transfer of the service to the private nnvestors do not as thtyhe Goverinlent, contractssector), the report suggests not to give up on need to be drawn as tightly as possible to reducetrying to introduce more incentives to cut costs in opportunities for discretionary actions by thethe sector but to try instead to rely, at least in the Govemmentshort run, on some form of commercialization ofthese services through management contracts: this 1.6 This suggests that the success of thecan serve to establish the credibility of the privatization process depends closely onprovincial commitment to reform in the view of . how property rights are defined andprivate investors before concessions can become a allocated initially (i.e., will the Governentrealistic option. This gives investors a chance to really give up control in exchange forobtain more independent information on the value efficiency and financing?); andof the assets they would be bidding for (a major * under what circumstances could these rights

issue in the W&S sector) and get the be eventually reallocated (i.e., what are thecommercialization of the service going withoutpulcoiycrtiahtcudledoa

dea2 public policy criteria that could lead to adelay. *2renegotiation of a contract ?).3

What Competition in Utilities Entails 1.7 In the national level reforms, the overall

1.5 It seems clear that provincial governments allocation of property rights to maximize the gainshave generally accepted to introduce competition from competition is the outcome of the followingin their local service monopolies through the three prong strategy:organization for competitive bidding. But the . assign property rights as clearly as possible inmain lesson from the national reform experience the contract;that Argentina's provinces may not have yet beenable to intemalize fully is that the key to * define the nature and form of property tosuccessful competition is to assign property rights maximize the manager's accountability; andon all the resources unambiguously. In other . give an incentive to new owners to remainwords, the Government has to give up control efficient throughout their tenure.over the service and recognize that once a privateoperator takes over, the private operator is incharge within the specific terms of its contract 1 8 The first prong was to rely on sealed-bidswith the Government. Contracts are intended to to assign the operator role in a concessionbe enforced according to their terms. This is what contract for a specified period (electricity, water,creates property rights. Unilateral modification of

3 The existence of market failures such as2 To avoid the creation of an information monopoly in environmental concerns often limits the extent to

favor of the winner of the management contract, clear which property rights can be shifted from thedata publications requirements should be spelled out in Government to a private operator.the contract.

3

etc.). As discussed later, the specific design of the 1.11 The third prong is relevant because thebids is a key determinant of the success of reform. provincial services at stake are local naturalSome of the provinces are clearly aware of the monopolies. Once the concessions have beenimportance of this step in the reform process. The awarded, it may be difficult for the Government towater company in Santa Fe, for instance, get the private operator or managers to focus oncommissioned an independent assessment of the the interest of consumers as much as on their ownvalue of its net assets (done by an external expert interest. Once more, the national reform of thein whom prospective investors had confidence) to electricity sector shows how to reduce the risk.reveal up front as much information as possible to To maximize the incentive for efficient behaviorpotential investors. This avoided some (but not during the concession, the concession contractsall) of the uncertainties in terms of rehabilitation awarded by the National Government in electricityneeds observed in the privatization of Obras require that new auctions be organized at regularPfiblicas in Buenos Aires. (Table 1.2 gives a intervals according to a procedure explained inchecklist of the main features that contracts in any paragraph 2.32.4 Basically, while the electricityprovince should cover). distribution concessions have a duration of 95

years, they are divided into management periods1.9 Just as important, all the requirements of of 10-year (except the first one which lasts for 15the bidding documents have to be internally years) which are allocated every 10 years.consistent and reasonable. They should bechecked for inconsistencies between the tariffs andthe investment and rehabilitation requirements. Box 1.1 How to Check if the Reform Process is beingThis may have been an issue in the bids organized Captured by the Bidders?

for the water concession in C6rdoba. Any serious discrepancy between various financialRequirements to participate should also strike a indicators provided in the bidding documents of the furm to bebalance between quantity (as many as possible) regulated and one of the benchmarks listed below can revealand quality (serious investors) of the offers. They abuses of the regulatory system by the potential operator.should also strike a reasonable balance between Compare the rate of return (ROR) implicit in the bid and:

risks and return for the private investor as 1. the ROR in unregulated firms in similar activities in the

discussed in Box 1.1 region.;2. the ROR the average ROR of the market in Argentina; and

.10 The second prong of this strategy focused 3. the ROR in similarly regulated firms in other provinces

on the nature and form of the dissemination of Over time, the comparison of the variance of rates ofproperty. In the case of Aguas Argentinas, shares return in the sector before and after the inclusion of the new firmwere sold on the stock market to widen the can also provide useful insights on the potential financial impactof the privatization. Typically, utilities are expected to be belowdissemination of property and hence of average risk and their return should vary by less than the marketaccountability. For electricity transmission, shares average. If the bids show anything else, it may reveal that thewere allocated to all staff, giving an incentive to bidder is asking for too much to provide the service. It may also

reflect an attempt b the bidder to compensate for a provinceact in the company's interest. But there are also specific risk that is well above market average. In this case, therisks in spreading accountability too thinly. This specific form of regulation may need to be tuned up as discussedis why it is generally suggested to allow the later in the chapter

bidding of packages of shares large enough toallow control by one major interest (i.e., to have astrategic investor).

4 While reducing the problems due to monopolies, thisapproach still implies a need for regulation.

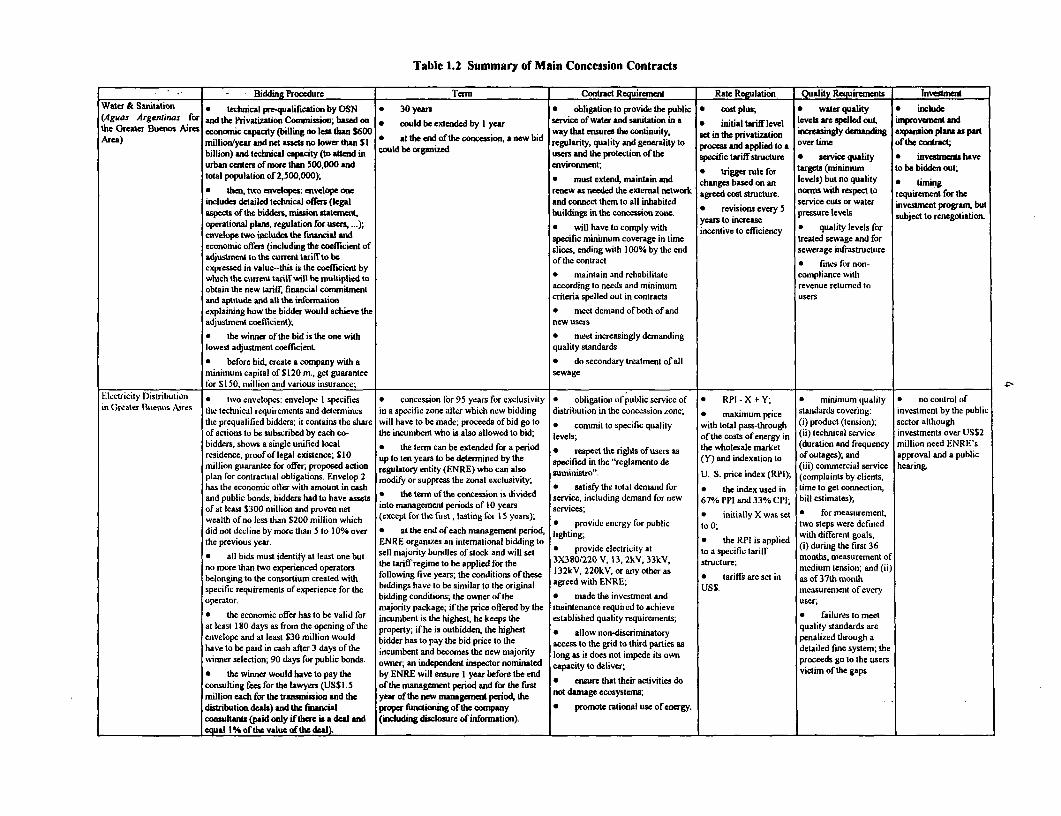

Table 1.2 Summary of Main Concession Contracts

- Bidding Procedure Term Contract Requirement Rate Regulation Quality Requirements InvestmentWater & Sanitation * technical pre-qualification by OSN * 30 years 0 obligation to provide the public 0 cost plus; 0 water quality * include(Aguas Argenninas for and the Privatization Commission; based on * could be extended by I y service of water and s nitation in a * inal tiff level leves are pelled out, improvement andthe Greater Buenos Aires economic capachy (billing no less than $600 way tht ensures the continuity. at in the prvatization icreingy dem expion pls u paiArea) mnillion/year and net assets no lower than SI * at the endrofte concession, anewbid regularity, quality and generality to procem nd applied to a over tine ofthe contract

billion)andtechnical capacity(toatendin couIdbeorganized usr andtheprotcti onofthe specifictariffstndcure * servicquality * invetmentahaveurban centeri of more than 500,000 nd environment; * trigger rule for target (minimum to be bidden out;total population of 2,500,000); * must extend, maintain and changes based on an Icvels) but no quality * timing

a then, two envelopes: envelope one renew as needed the external network agreed cost structure. norms with respect to requirement for theincludes detailed technical offes (legal and connect them to all inhabited service cuts or water investment program, butaspects of the bidders, mission statement, buildings in the concession zone. * reviisons every 5 pressure levels subject to renegotiationaspects afthe biddem, miuion daten-C ~ ~~~~~~~~~~~~~~~years to increaseoperational plans, regulation for users, ...); * will have to comply with incentive to efficiency * quality levels forenvelope two includes the financia and specific minimum coverage in time treated sewage and foreconomic offers (including the coefficient of slices, ending with 100% by the end sewerage infrastructureadjustment to the current tariffto be of the conitract * fines for non-expressed in value--this is the coefficicnt bywhich the current tariff will be multiplied to * maintain and rehabilitate complvane r ithobtain the new tariff, financial commitment according to needs and minimum revenue returnd toand aptitude and all the information criteria spelled out in contracts usersexplaining how the bidder would achieve the 0 meet demand of both of andadjustment coefficient); new users

* the winner of the bid is the one with 0 meet increasingly demandinglowest adjustment coefficienL quality standards

* beforc bid, create a company with a 0 do secondary treatment of allminimum capital of S 20 m., get guarantee sewagefor S150, niillioii and various insurance; ___ ___

Electricity Distribution * two envelopcs: envelope I specifies * concession for 95 years for exclusivity * obligation ol public service of * RPI - X f- Y; * mininium quality * no conitrol ofin Greater Buenos Aircs die technfical requirements anud detemiincs in a specific zone aller whici new bidding distribution in the concession zone; * maximum price standards covering: investment by the public

the prequalified bidders; it contains the share will have to be made; proceeds of bid go to * commit to specific quality with total pass-through (i) product (tension); sector althoughof actions to be subscribed by each co- the incumbent who is also allowed to bid; levels of the costs of energy in (ii) technical service investments over USS2bidders, shows a single unified local * the term can be extended for a pefiod , respect the rights of users as the wholesale market (duration and frequency million need ENRE'sresidence, proof of legal existence; S10 up to ten years to be determined by the specified in the "reglamento de (Y) and indexation to of outages); and approval and a public

million guarantee for offer, proposed action (iii) commercial service hearing.onunrcialservce heringpillion guarantee for offer, proposed aclion regulatory entity (ENRE) who can also suministi-o,. U. S. price index (RPI); (complaints by clients,plan for contractual obligations Envelop 2 modify or suppress the zonal exclusivity;has the economic offer with amount in cash * satisfy th total demand for * the index used in time to get connection,and public bonds; bidders had to, have assets 0 the term of the concession is divided service, including demand for new 67% PPI and 33% CPI; bill estimates);of at least $300 million and proven net into management periods of 10 years services; * initially X was set a for measurement,wealth of no less than $200 million which (except for the first,. lasting for I 5 years); 0 poieeeg o ulc 1 ;toseswr eie

did not decline by more than 5 to 10% over * at the end of each management period, lighting; * the RPI is applied with different goals;the previous year. ENRE organizes an international bidding to poiecctctyatoascfctrff (i) durirng the first 36* all bids must identify at least one but sell n ajority bundles ofstock and will set 3X380p220 Ve 13t 2iV, 33kV, *rtose tRi months, measurement of

no oretha tw exerince opratrs the tariffregime tobe applied for the 3~o20,1,k,3V tutr;medium tension; and (ii)belonging to the consortium created with following five years; the conditions of0these 132kVd 22kh oR * tariffs are set in as of 37th monthspecific requirements of experience for the biddings have to be similar to the original agreed with ENRE; USS measurement of everyGperator. bidding conditions; the ownier of the 0 made the invcstment and user;,

majority package; if the price offered by the niaintenance required to achieve* the economic offer has to be valid for incunmbent is the highest, he keeps the established quality requirements; * failures to meet

at leat t godays s fromthe oening f othequality standards areat evle 180 days as from he opening of the propety; if he is outbidden, the highest * allow non-discriminatory penalized through aenvelope and at least S30 million would bidder has to pay the bid price to the access to the grid to third parties as dpetailed fin systeru thehave to be paid in cash after 3 days of the incumbent and becomes the new majority long as it does not impede its own proceed to te ewinner selection; 90 days for public bonds. owner, an independent inspector nominated capacity to deliver, victim of the gaps

* the winner would have to pay the by ENRE will ensure I year before the end v of the gapsconsulting fees for the lawyers (USS 1.5 of the management period and for the first ensure that their activities domillion each for the transmission and the year of the ne w e not damage ecosystems;distribution deals) and the finacial proper fiusctioning of the company * promote rational use of energy.consultants (paid only if there is a deal and (including disclosure of information).equal 1% ofthe value ofthe deal).

5

What Contract-Based Regulation Entails contract by redefining one of the variables (thecapacity price) in such a way that the distributors

1.12 The concession contract is the main would no longer be penalized (or favored). Thisinstrument used by the national Government to left formula in a range consistent with the "passregulate utilities--although its exact nature varies through ranges" and avoided the original concern.across sectors as seen in Box 1.2. Concessioncontracts and possibly management in some of the 1.14 Should contract revisions be allowed?poorest regions, are likely to be the main This (as well as the national experience withinstrument for the provinces as well. As a rule as transport contracts) shows that even if, as a rule,mentioned before, they should be drawn up as contracts should be prepared as documents thattightly as possible to reduce the need for are not intended to be modified and includediscretionary adjustments. adjustment mechanisms to avoid the costs,

uncertainty of ex-post negotiation, under veryspecific and very limited circumstances, a limited

Box 1.2 Comparing Concession Contracts in W&S degree of contract flexibility may be good public

and in Electricity, policy. But to ensure that the contract is aThe term concession is used for both the W&S and for credible regulatory instrument, the contract

the electricity distribution contracts. Yet these contracts modifications should be based on some fair andare quite different. No shares were sold in the W&S case.All assets remain public and the Government has given the workable renegotiation rules based on clearlyright to a private firm to operate these assets in exchange spelled out policy criteria (as discussed below)for certain obligations in terms of investment which is one and agreed upon by all involved parties. Theyof the main reason why provincial water utilities are trying should always respect the original contractualto attract the private sector. In electricity, the Government rights of the investors; ad-hoc solutions are notdid sell shares, and hence part of its assets, but has . .cattached to it public service obligations--expressed in terms always i the best iterest of all the partiesof service coverage and quality-- instead of specific involved. This is one of the main rationale for aninvestment requirements. independent regulator who can have some

discretion in the implementation of the rules as anhonest broker.

1.13 However, these contracts, as any othertype of contract, cannot anticipate all exceptions 1.15 When should contract revisions beor qualifications and that corrections are allowed? The challenge is to find a transparentsometimes needed later. Argentina's National mechanism for modifying specific terms of aelectricity regulator (ENRE) was recently contract that do not result in private investors orconfronted with the need to revise a distribution consumers lacking confidence in the contractualcontract. The formulas for the calculation of instrument (i.e., adjusting the price terms of atariffs prevailing initially resulted in a significant contract in line with the terms of that contract).reduction in the profits of distributors in May This mechanism was missing in the otherwise very1994 (although the mistake led to significant impressive national reforms. It is also a keyprofits over the previous 18 months without much ingredient missing from the provincial debate.complaints about this problem then). Thedistributors complained about their profit losses 1.16 The contractual rigidities built into theand ENRE conceded that there was a need to concession agreements are necessary to closerevise the contract but that this required some deals and to create binding commitments amongresearch. The Energy Secretariat (ES) took the participants. However, they make it difficultcharge of the debate and de facto revised the to adapt when there is a need to resolve emerging

6

problems because many of the actors find 1.18 Which public policy criteria? Theadaptation threatening to the privatization public policy criteria to test if a revision is neededcommitments that protect their interests and the have to be spelled out as soon as possible to makewhole fabric of reform. Moreover, clearly each the rules of the game clear to all parties involved.franchisee is likely to attempt to interpret most of They should ensure a transparent basis forthe contractual ambiguities to its own advantage. contractual dispute resolution and related policyThis is why there is a need to continuously decisions, as well as to avoid excessivelymonitor the concession agreements and to assess subjective decisions on the need for or nature ofany need to adjust them. contractual changes. These criteria ease the

judgment as to whether the maintenance of1.17 The assessment of any modification existing provisions is suboptimal to all parties inrequirements, however, needs to be based on a view of a fundamental change in externalgood sense of what went wrong and on a clear set circumstances (e.g., a permanent demand shift) orof public policy criteria: a change in policy priority (e.g, the relative

.How realistic are the government requests importance of services to the poor increases)

once more is known about the state of assets? Possible criteria include:Were there trade-offs not well identified at the * Is the protection of the interests of investors atinitial stage by either the Government or the the baseline levels established in the originalprivate bidders who could have asked then for privatization terms guaranteed'? Should it be?a revision of the specification of the needs, as .How would the overall operation (flexibility,observed in the privatization of the Santa Fe

water company. ~~~~~~variety, responsiveness of operators, quality ofomaintenance and of investment strategies) be

* If minimum demand levels were spelled out in affected by the changes?

the contracts, were they over- or * Would the composition of the financing of theunderestimated? This is common. It may activitybe altered? Would it reduce the publichave been a problem in any of the waterconcessions in Argentina as elsewhere in the share in this financing?world. But was this due to a mistake in the * Would consumer interests be protected?organization of the concession or was it due to What is the nature and source of change ina mistake by the private operator such as scale of operations in response to demand?insufficient market analysis?

* Did the state of the assets deteriorate between If the answers warrant a change to the contract, itthe time the bids were made and the time they should be limited to the specific issue.were actually transferred? If yes, was this due Negotiations should not be reopened for theto the natural phenomena (e.g., the weather) whole contract.or to the fact that the public operators stoppedmaintaining these assets? If it is due to the Does the Provincial Choice of Regulatoryformer, the responsibility may be shared by the Regimes Matter to a Potential Investor?Government and the private concessionaire.In the second case, the concessionaire may 1.19 The two main regulatory optionshave a fair claim on a request to revise the provincial reformers should be picking from are:contract. (i) rate of return (ROR) regulation (as used for

over 20 years the U.S. utilities) and (ii) some formof price cap regulation (recently introduced in the

7

UK privatizations and in the electricity distribution What Decentralized Regulation Entailsin Greater B). Under a ROR regulation, theregulator set a revenue requirement based on a 1.22 The last provincial challenge addressedfirm's accounting costs reflecting operating costs, here is the organization of the monitoring of thetaxes, amortization and allowed ROR. Once the consistency of the behavior of the privatizedrevenue requirement is computed, the regulator monopolies with the public aims. This monitoringdetermines the tariff structure design needed to is needed because concessionaires will have strongrecover aggregate costs. Under a price cap, incentives to behave inefficiently when leftinstead of setting a ROR, the regulation sets a unsupervised. The creation of regulatory bodiesprice ceiling above which the concessionaire or the use of the strength of law and courts will becannot raise prices. Under that cap or ceiling the an important element in the success of theregulated firm can set prices as it wishes. The provincial reform of utilities. They are needed toceiling must be reviewed every two to five years guarantee the increase in efficiency throughto account to productivity improvements, competition in services delivered by natural

monopolies.5 But there is a limit as to how much1.20 Price capping has many potential this institutional role can and should beadvantages over ROR regulation. The main decentralized.advantage for Argentina's provinces is that itgenerates stronger incentives to cut costs and that 1.23 The main economic argument in favor ofthese costs cut eventually get passed on to some degree of decentralization stems from theconsumers. One of its problems is its very need to distinguish between technical anddemanding informational requirements. This can economic regulation. An interconnected electricbe overcome as ENRE's experience is showing network will always need technical regulationalthough it is not straightforward as shown by the with strong coordination between the differentBritish experience. But the main reason why regulating agents, for example through a centralprovincial reformers have to be careful in their dispatching unit. Economic regulation does notchoice is that the specific choice has an impact on have the same goals, so that its organization is notthe risks faced by potential private investors. The necessarily identical to the technical one. Thetwo regimes place very different levels of risks on controllers should be located at the nodes wherethe regulated utilities and hence affect the rate of inefficiencies will more probably occur and thesereturn and the cost of capital in very different nodes may differ for the technical and theways. economic concems.

1.21 A price cap approach implies that the 1.24 Economic Regulation of Electricity.investors puts up with all the risks on its The technical dispatching of energy supply toinvestment. ROR can pass on these risk onto the meet demand is a good opportunity to induceconsumers. So if demand for utility service in any efficiency through merit order. On the contrary,province is highly dependent on the level and type at the terminal nodes of the network there is littleof economic activity in the province, ROR need for technical control but it is a place whereregulation will generally be more effective at distributors can try to exploit their exclusiveprotecting the investor. In other words, high risk position in front of captive consumers.provinces should consider allowing rate of return Consequently, economic regulation is necessary atregulation when it is not finding any privateinvestor interested in providing the services under 5 This has to be supported by a strong commitment toa price cap regime. antitrust but this is a commitment that has to be made

at the national level, not by the provinces.

8

the regional level. But this means neither that one with a single independent entity for all utilitiesagency is necessary in each province nor that the with a modest staffing level dependent on theprovincial regulators are to be independent from requirements of specific tasks assigned to thethe central agency (e.g., ENRE). regulatory authority rather than multiple sector

specific agencies. The main reason is that the1.25 In view of the similarity of problems in skills needed to be a good regulator are hard toseveral provinces, a small number of three or four find. Luckily, the skills needed to be an effectiveinter-provincial agencies should be sufficient. If regulator are very similar in both the water andthe political situation is such that each province electricity sector and hence the same resourcesmust have its own regulatory body, the entity can be shared within a single provincial regulatoryshould be kept to a minimum. Moreover, entity. This means lower resource needs (not onlywhatever their number these local agencies should in terms of staff but also in terms of equipment)have only specific prerogatives, essentially and hence a lower burden on the taxpayers or theauditing and reporting to the national regulation beneficiaries of the services. There are otherbody. This is because technical dependencies benefits. For instance, it facilitates learningwithin an electric network are particularly strong. between sectors, ensures consistent approaches to

central policy questions and makes the regulator1.26 Economic Regulation of W&S. In less vulnerable to industry or political capture.W&S, things are somewhat different since water This lower vulnerability enhances the credibility ofcannot be collected anywhere, neither dispatched the agency and reduces risks for investors.in any direction independently of geographicconsiderations unlike electricity. Water networks 1.28 The implementation of this strategy can beare not national. But this does not imply that each flexible. It is easier to do when agencies have notlocal network in each municipality should be yet been established. A multisectoral frameworkregulated by an independent body, because there can be established first and then sectors can beare important economies of scope in the added to the core entity when appropriate. Thereregulation of pumping, treating and distributing is no need to wait until any contract has beenwater at the local level. The informational, signed. The creation entity can be instrumental intechnical and organizational problems are assisting in the implementation of theisomorphic from one municipality or province to concessioning process. If one agency has alreadythe other. Consequently, the optimal organization been established, it should not be too difficult tofor the regulation of this sector should include a expand the jurisdiction of the existing agency.national entity in charge of the definition of This depends of course on how sector specific ingeneral principles like pricing rules, quality design and composition the initial agency is.standards, uniform statistics (for yardstick Finally, if several agencies have already beencompetition) and provincial entities controlling created, the best option is to develop a strategyand overseeing the application of these rules. for merging the agencies after an initial period.

This strategy tends to be the most difficult and1.27 The institutional dimension of will often be resisted by both the existingprovincial regulation. If most provinces regulators (concerned about losing their autonomydeciding to rely on concession contracts for the and possibly their job) and investors (oftendelivery of electricity and W&S service end up preferring the counterpart they know).deciding to create their own regulatory entities, afew words of caution are needed. Chapter 4shows that most provinces would be better off

9

Chapter 2: REFORMING ELECTRICITY DISTRIBUTION IN THE PROVINCES

2.1 The main purpose of the reform of of this report. To be able to identify the optionsArgentina's electricity sector was to reach for reform in the provinces, however, anefficient pricing and production levels in the short- assessment of the achievements of the Nationalterm, and an investment level sufficient to meet program so far is needed. This is why this chapterdemand in the long run. This entailed a major starts with a general overview of the sector as itrestructuring of the sector which started with the stands after the main national reforms. Next itlegal initiative expressing intentions in 1989, was discusses the main institutions that could influencefollowed by the first implementation steps in 1992 the regulatory environment of privatizedand is still going on. provincial distribution companies. It makes it

clear that the provincial regulatory authorities are2.2 The legal basis of the restructuring process not going to be the only institution that will have ais spelled out in the 1989 laws deciding the global strong impact on the return to investment in thereform of the state. For the electricity sector, the provinces. This is also clear in the discussion ofprocess began when the federal government the main regulatory instrument--the contract--andfranchised the distribution and commercialization of the mechanisms of competition. The chapteractivities of SEGBA,6 the vertically integrated concludes with a discussion of pricing inutility supplying electricity to 15 million people in generation, transmission and distribution as thethe Greater Buenos Aires area. The main next rate of return of the private investors in provincialstep was in 1992, with the privatization of the companies will be influenced by the full pricingelectric generation and transmission activities that chain. The chapter concludes with a discussion ofSEGBA was still carrying.7 With these two the importance of an explicit linkage betweenchanges, the original public firm had been tariff design and investment needs in distribution

8vertically disintegrated into seven business units: services.four generation firms, and three distribution firms.These units were either sold or concessioned to Overview of the Sector's Organizationthe private sector through international bids. Thereform in two other state-owned entities, Agua y 2.4 An effective way of visualizing the extentEnergia Elctrica (AyE) and Hidronor, had some of reform in the sector is to follow the financialimplications for a few provinces as some of the flows. Depending on whether a specific activityassets were privatized while the plants located in between generators, transmitters, distributors andareas under provincial responsibility were users is done in a competitive market or not, thetransferred to the provinces concerned. related transactions are regulated in different

ways, as Figure 2.1 illustrates. It shows that2.3 The remaining step in the restructuring of contracts between distributors--and large users--the sector is the reform of the provincial and generators are not regulated and that the spotdistribution companies which is the main interest prices and seasonal prices are also set by the

market. Final users tariffs are, however, regulated

6 Servicios Electricos del Gran Buenos Aires. which should matter to investors in provincialLaw No. 24.065 (December 1991) and DecreeNo. 1.398/92 (January 1992) establishing the 8 Most of the background on the description of the"Electricity Regulatory Framework". In January 1991, sector presented in this chapter is from Bastos, C.M.SEGBA had a generation capacity of 2500 MW and A.A. Abdala (1993), Transformaci6n del sectorsupplying 10.33 TWh. to 4.5m connected customers. electrico argentino, Editorial Antartica, Chile.

10

utilities. So is transmission price and this is 2.7 The market matches electricity demandimportant to these investors since depending on and supply with an hourly price.10 The marketthe effectiveness of this regulation, transmission also allows trade-in contracts, in which suppliersexpansion will be responsive to the distributors' and buyers can freely agree on long-termneeds or will not. The chapter shows how and contracts in quantities and prices as well as morewhy these activities work the way they do and qualitative aspects such as voltage, point ofwhy it matters to the provinces. reception, timing, back-up, etc. But these do not

imply any reranking in the order of dispatch as2.5 The discussion starts with a brief overview discussed below."of the characteristics of each one of the mainactivities, then moves on to discuss the main 2.8 The co-existence of three different types of"regulators" of the sector (in a broad sense). players on the demand side is important toNext, the chapter explains how contracts have recognize as it matters to the value of the assets ofbecome a key regulatory instrument for these a distribution company and for the design of theirfederal regulators and how competition works in tariff policy as discussed later. These playersthat regulated environment. Because pricing is include distributors and (potential) foreign buyerssuch a key component of the effectiveness of the but also large users. Defined as those whose peakreform and of the regulatory function, it is demand is equal or higher than 0. IMW, largediscussed next in some detail. This discussion users have the advantage over other consumers:spells out all the payments for service obligations they are allowed to sign direct contracts withas these are likely to be accepted and internalized generators without having to commercially goby provincial governments in their own reforms. through provincial distributors and henceThe discussion also addresses the linkages increasing the incentive to minimize costs for thebetween tariff design and incentives to invest as operation of distributions services. They are ablethis is, or at least should be, a major concern of to access the MEM directly for at least 50% ofmost provincial governments. It highlights the their total demand.potential consequences for the provinces of failingto address the linkages between tariff design andtransmission expansion.

2.6 Generation. The core of the reform ingeneration was the creation of a wholesale spotmarket, MEM. The provincial companies aremajor actors in this market as it is open to anygenerator--whatever its technology--and the mainusers (distribution companies but also deregulatedlarge users). These can directly buy from anyprovider they chose to on that market9 (seeBox 2. 1).

'° Real time tariff sets the price of the service at anytime, reacts continuously to changes in demand andequalizes demand with capacity at all times.Besides the MEM, there are two other small wholesaleelectricity markets which are not connected to themain transmission system (Misiones and SouthPatagonia). Prices in these markets will be determined

9 Mercado Electrico Mayorista. locally until they are connected with the MEM.

11

Figure 2.1 Financial Flows

G2 X Wholesale spotmarket

Transmission Co| Un

Gi: GeneratorsDi: DistributorsUi: Users

Contracts. Unregulated pricesSpot price. Marginal cost of last dispatched generatorSeasonal price. Forecasted average of spot pricesFinal users tariff Regulated tariff with pass-through of seasonal pricesTransmission tariff Regulated tariff

12

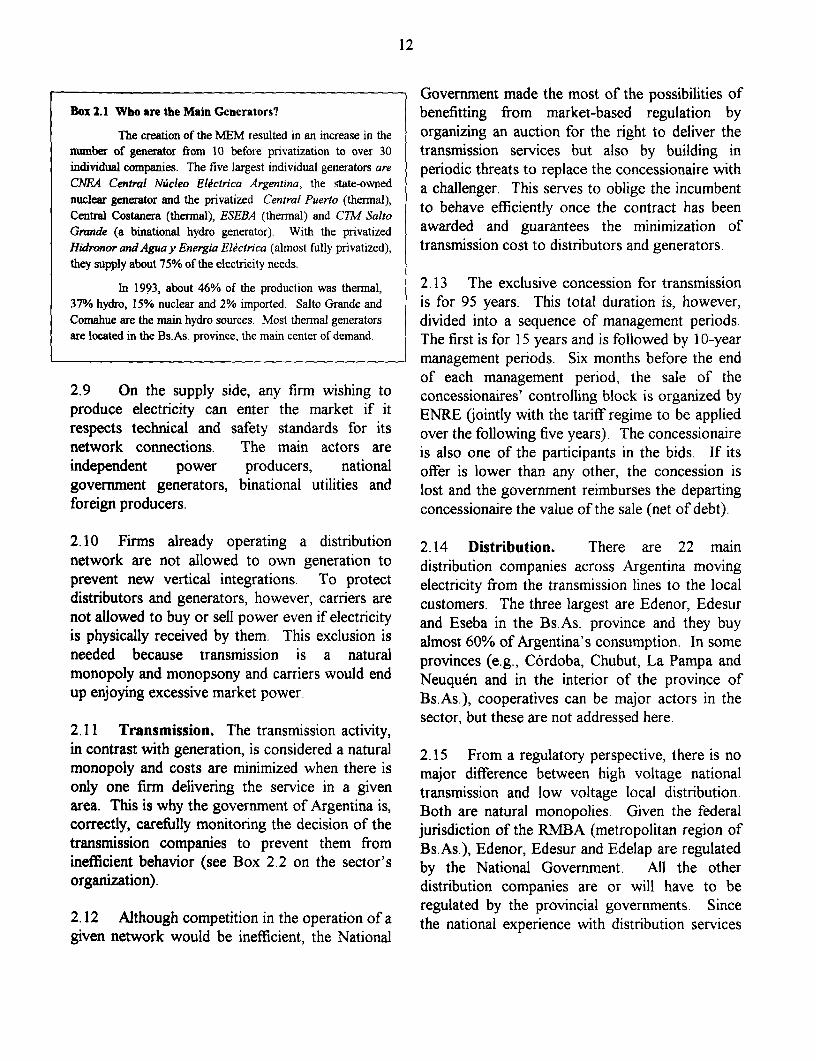

Government made the most of the possibilities ofBox 2.1 Who are the Main Generators? benefitting from market-based regulation by

The creation of the MEM resulted in an increase in the organizing an auction for the right to deliver thenumber of generator from 10 before pnvatization to over 30 transmission services but also by building inindividual companies. The five largest individual generators are periodic threats to replace the concessionaire withCNEA Central Nuicleo E1kctnca Argentina, the state-owned a challenger. This serves to oblige the incumbentnuclear generator and the privatized Central Puerto (thermal), to behave efficiently once the contract has beenCentral Costanera (thermal), ESEBA (thennal) and CTM SaltoGrnde (a binational hydro generator). With the privatized awarded and guarantees the minimization ofHidronor andAguay Energia Eletnca (almost fully privatized), transmission cost to distributors and generators.they supply about 75% of the electricity needs.

In 1993, about 46% of the production was thennal, 2.13 The exclusive concession for transmission37% hydro, 15% nuclear and 2% imported. Salto Grande and iS for 95 years. This total duration is, however,Comahue are the main hydro sources. Most thermal generators divided into a sequence of management periods.are located in the Bs.As. province, the main center of demand. The first is for 15 years and is followed by I 0-year

management periods. Six months before the endof each management period, the sale of the

2.9 On the supply side, any firm wishing to concessionaires' controlling block is organized byproduce electricity can enter the market if it ENRE (jointly with the tariff regime to be appliedrespects technical and safety standards for its over the following five years). The concessionairenetwork connections. The main actors are is also one of the participants in the bids. If itsindependent power producers, national offer is lower than any other, the concession isgovernment generators, binational utilities and lost and the government reimburses the departingf>oreign producers. concessionaire the value of the sale (net of debt).

2.10 Firms already operating a distribution 2.14 Distribution. There are 22 mainnetwork are not allowed to own generation to distribution companies across Argentina movingprevent new vertical integrations. To protect electricity from the transmission lines to the localdistributors and generators, however, carriers are customers. The three largest are Edenor, Edesurnot allowed to buy or sell power even if electricity and Eseba in the Bs.As. province and they buyis physically received by them. This exclusion is almost 60% of Argentina's consumption. In someneeded because transmission is a natural provinces (e.g., C6rdoba, Chubut, La Pampa andmonopoly and monopsony and carriers would end Neuquen and in the interior of the province ofup enjoying excessive market power. Bs.As.), cooperatives can be major actors in the

sector, but these are not addressed here.2.11 Transmission. The transmission activity,in contrast with generation, is considered a natural 2.15 From a regulatory perspective, there is nomonopoly and costs are minimized when there is major difference between high voltage nationalonly one firm delivering the service in a given transmission and low voltage local distribution.area. This is why the government of Argentina is, Both are natural monopolies. Given the federalcorrectly, carefully monitoring the decision of the jurisdiction of the RMBA (metropolitan region oftransmission companies to prevent them from Bs.As.), Edenor, Edesur and Edelap are regulatedinefficient behavior (see Box 2.2 on the sector's by the National Government. All the otherorganization). distribution companies are or will have to be

regulated by the provincial governments. Since2.12 Although competition in the operation of a the national experience with distribution servicesgiven network would be inefficient, the National

13

is clearly the model being followed by the potential investors as one of the main risks. Thisprovinces, a brief overview of the rights and is why a commitment to a strict enforcement ofobligation may be helpful. property rights is key to the success of the

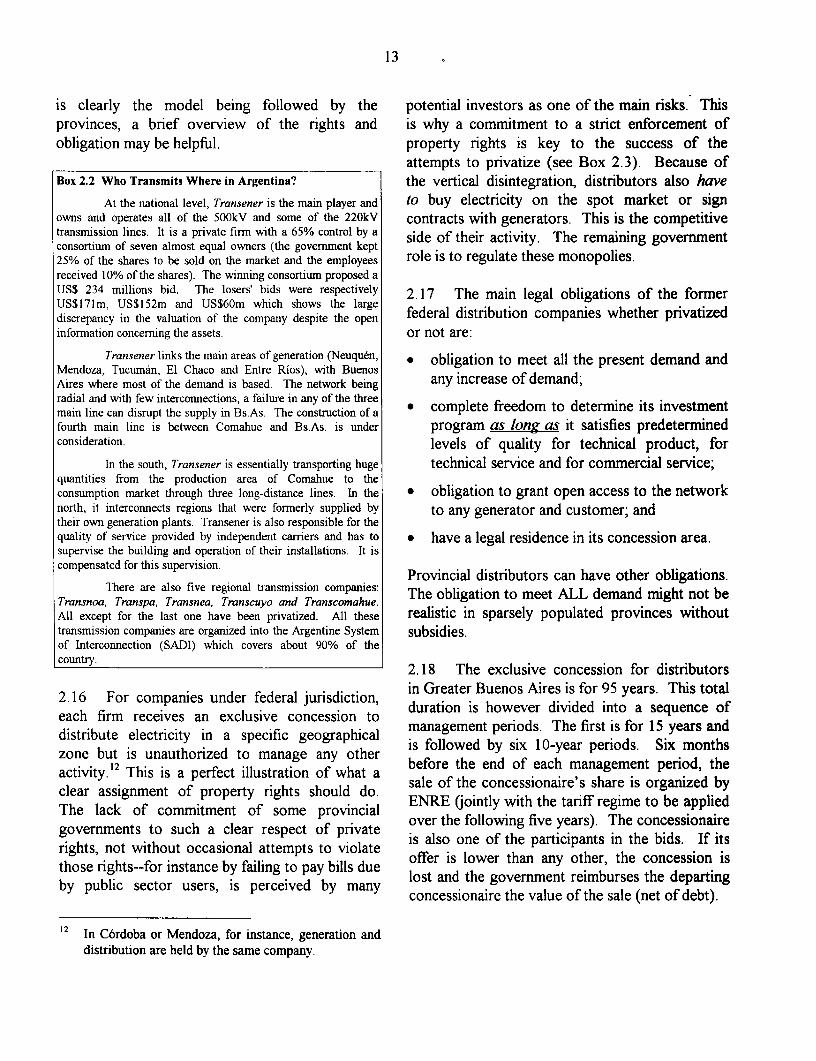

attempts to privatize (see Box 2.3). Because ofBox 2.2 Who Transmits Where in Argentina? the vertical disintegration, distributors also have

At the national level, Transener is the main player and to buy electricity on the spot market or signowns and operates all of the 500kV and some of the 220kV contracts with generators. This is the competitivetransmission lines. It is a private firm with a 65% control by a side of their activity. The remaining govenmentconsortium of seven almost equal owners (the government kept25% of the shares to be sold on the market and the employees role is to regulate these monopolies.received 10% of the shares). The winning consortiumn proposed a

US$ 234 millions bid. The losers' bids were respectively 2.17 The main legal obligations of the formerUS$l7lm, US$1 52m and US$60m which shows the large feraditbuoncm nesw thrpvtzediscrepancy in the valuation of the company despite the open federal distribution companies whether privatizedinformation concerning the assets. or not are:

Transener links the main areas of generation (Neuquen, * obligation to meet all the present demand andMendoza, Tucuman, El Chaco and Entre Rios), with BuenosAires where most of the demand is based. The network being any increase of demand;radial and with few interconnections, a failure in any of the three * complete freedom to determine its investmentmain line can disrupt the supply in Bs.As. The construction of afourth main line is between Comahue and Bs.As. is under program as long as it satisfies predeterminedconsideration. levels of quality for technical product, for

hi the south, Transener is essentially transporting huge technical service and for commercial service;quantities from the production area of Cornahue to theconsumption market through three long-distance lines. In the * obligation to grant open access to the networknorth, it interconnects regions that were formerly supplied by to any generator and customer; andtheir own generation plants. Transener is also responsible for thequality of service provided by independent carriers and has to * have a legal residence in its concession area.supervise the building and operation of their installations. It is

compensated for this supervision. Provincial distributors can have other obligations.There are also five regional transmission companies: The obligation to meet ALL demand might not be

Transnoa, Transpa, Transnea, Transcuyo and Transcomahue.All except for the last one have been privatized. All these realistic in sparsely populated provinces withouttransmission companies are organized into the Argentine System subsidies.of Interconnection (SADI) which covers about 90% of the

country. 2.18 The exclusive concession for distributors

2.16 For companies under federal jurisdiction, in Greater Buenos Aires is for 95 years. This totaleach firm receives an exclusive concession to duration is however divided into a sequence ofdistribute electricity in a specific geographical management periods. The first is for 15 years andzone but is unauthorized to manage any other is followed by six 10-year periods. Six monthsactivity.'2 This a perfect illustration of what a before the end of each management period, theclactivity. ent isfa p.ert iustraio lo waa sale of the concessionaire's share is organized byclear assignment of property rights should do. .The lack of commitment of some provincial ENRE (jointly with the tariff regime to be appliedgovernments to such a clear respect of private over the following five years). The concessionairerights, not without occasional attempts to violate is also one of the participants in the bids. If itsthose rights--for instance by failing to pay bills due offer is lower than any other, the concession isthose rubigh ets or instrce by farceiing etodp bil dy lost and the government reimburses the departing

concessionaire the value of the sale (net of debt).

'2 In C6rdoba or Mendoza, for instance, generation anddistribution are held by the same company.

14

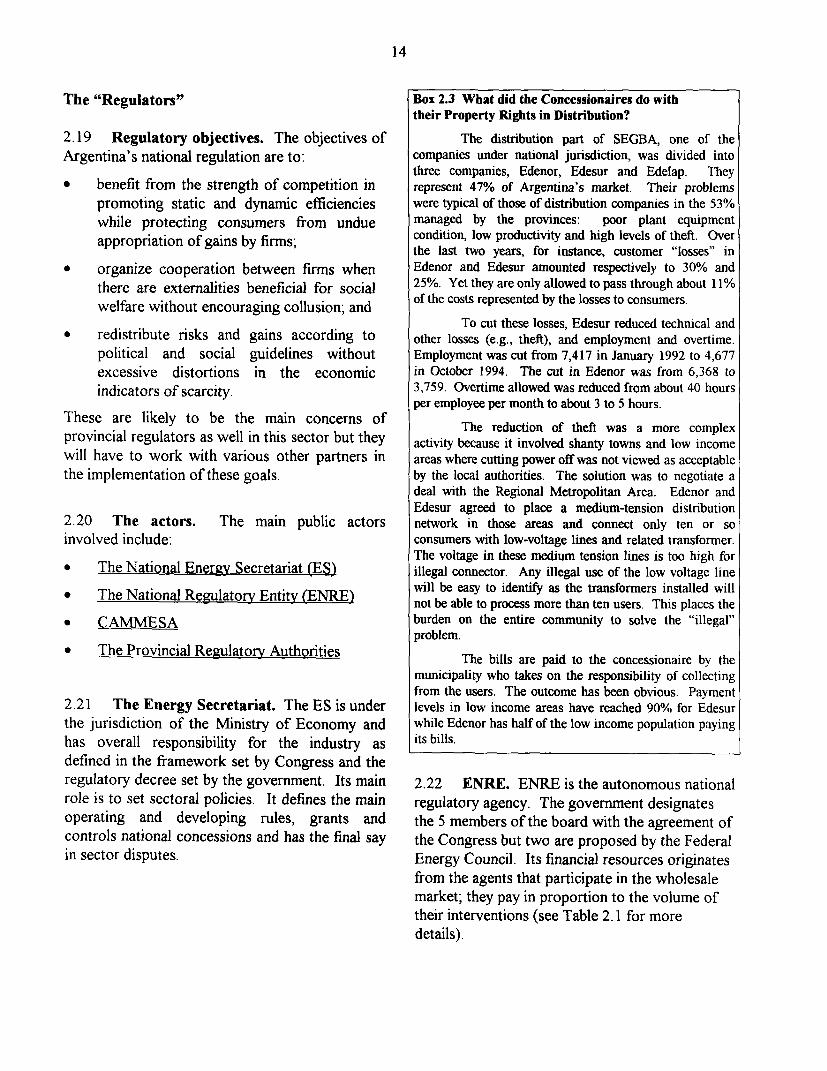

The "Regulators" Box 2.3 What did the Concessionaires do withtheir Property Rights in Distribution?

2.19 Regulatory objectives. The objectives of The distribution part of SEGBA, one of theArgentina's national regulation are to: companies under national jurisdiction, was divided into

three companies, Edenor, Edesur and Edelap. They* benefit from the strength of competition in represent 47% of Argentina's market. Their problems

promoting static and dynamic efficiencies were typical of those of distribution companies in the 53%while protecting consumers from undue managed by the provinces: poor plant equipmentappropriation of gains by firms; condition, low productivity and high levels of theft. Over

the last two years, for instance, customer "losses" inorganize cooperation between firms when Edenor and Edesur amounted respectively to 30% andthere are externalities beneficial for social 25%. Yet they are only allowed to pass through about 11%welfare without encouraging collusion; and of the costs represented by the losses to consumers.

To cut these losses, Edesur reduced technical and* redistribute risks and gains according to other losses (e.g., theft), and employment and overtime.