Embed Size (px)

Citation preview

Report No 4693-SEY

Seychelles: Issues and Optionsin the Energy Sector

FFILE COPY

January 1984

Repot of the joint UNDP/Wrld Bank Energy Sector Assessment ProgramThts document has a restricted distribution. Its contents may not be disclosedwithout authorization from the Government, the UNDP or the World Bank.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

JOINT UNDP/WORLD BANK ENERGY SECTOR ASSESSMENT PROGRAM

REPORTS ALREADY ISSUED

Country Date No.

Indonesia November 1981 3543-IND

Mauritius December 1981 3510-MAS

Kenya May 1982 3800-KE

Sri Lanka May 1982 3792-CE

Zimbabwe June 1982 3765-ZIM

Haiti June 1982 3672-HA

Papua New Guinea June 1982 3882-PNG

Burundi June 1982 3778-BU

Rwanda June 1982 3779-RW

Malawi August 1982 3903-MAL

Bangladesh October 1982 3873-BD

Zambia January 1983 4110-ZA

Turkey February 1983 3877-TU

Bolivia April 1983 4213-BO

Fiji June 1983 4462-FIJ

Solomon Islands June 1983 4404-SOL

Senegal July 1983 4182-SE

Sudan July 1983 4511-SU

Uganda July 1983 4453-UG

Nigeria August 1983 4440-UNI

Nepal August 1983 4474-NEP

Gambia November 1983 4743-GM

Peru January 1984 4677-PE

Costa Rica January 1984 4655-CR

FOR OFFICIAL USE ONLY

Report No. 4693-SEY

SEYCHELLES

ISSUES AND OPTIONS IN THE ENERGY SECTOR

January 1984

This is one of a series of reports of the Joint UNDP/World Bank EnergySector Assessment Program. Funding for this work has been provided, inpart, under the supplementary "Small-Country Assessment Program" financedby the Swedish Government through the UNDP, and the work has been carriedout by the World Bank. This report has a restricted distribution. Itscontents may not be disclosed without authorization from the Government,the UNDP or the World Bank.

ABSTRACT

The economy of the Seychelles is highly dependent ontourism. Because of a decline in tourism, the demand for petroleum andeconomic growth have fallen off over the past three years. However,despite the drop in petroleum consumption, the cost of imports has notchanged much, so reducing the oil import bill is a pressing priority.Substituting fuel oil for gas oil in power generation was the first stepin reducing oil import costs in 1982. As the Government of Seychelleswants to develop and integrate several outer islands into the nationaleconomy, it has devised a 20-year integrated energy project to developrenewable energy technologies. This report reviews these and otherenergy issues, and recommands: (i) institutional reorganization; (ii) arestructuring of the Seychelles Integra ed Energy Project and ongoingtechnical assistance programs; (iii) technical assistance for petroleumexploration; (iv) evaluation of least cost petroleum supply options; and(v) rationalization of the petroleum pricing structure.

Abbreviations

ACCT Agence de Cooperation Culterelle TechniqueCID Center of Industrial DevelopmentDTCD Department of Technical Cooperation and DevelopmentGOS Government of SeychellesIDC Island Development CompanyMPER Ministry of Planning and External RelationsNRDC National Research and Development CouncilORSTOM Office pour le Recherche Scientifique et Technique d'Outre MerOTEC Ocean Thermal Energy ConversionRDU Research and Development Unit (The name of this unit is now

changed to Energy and Technology Division)SEC Seychelles Electricity CorporationSIEP Seychelles Integrated Energy ProjectSPTC Seychelles Public Transport CorporationUNFSSTD United Nations Financing System for Science and Technology

DevelopmentWECS Wind Energy Conversion SystemWEL Works Enterprise Limited

This report is based on the findings of an energy assessment Missionwhich visited Seychelles in June 1983. The Mission comprised Messrs. ZiaMian (Mission Chief), Thorild Persson (consultant: power), Sture Haal(consultant: power system efficiency), Lars Kristoferson (consultant:biomass and renewables), A. Van Gelder (consultant: forester) and KapilThukral (Researcher). The Mission was assisted by Messrs. Akin Oduolowuand D. Eicher in reviewing the technical information on petroleum explo-ration. Secretarial assistance was provided by Mr. Jagdish Lal andMrs. J. Regino-Suarez. The report was discussed with the Government ofSeychelles in Victoria in January 1984.

Currency Equivalents

Currency: Seychelles Rupees (SR)1 US$ = SR 7.83 (1976)1 US$ = SR 6.32 (1979)1 US$ = SR 6.55 (1982)

Measurements

Bbl Barrel = 42 US gallons; 159 litersboe barrel of oil equivalent = 5.99 million btuGWh gigawatt hour = million kilowatt hourskJ kilojoulekm kilometer = 1,000 meterskV kilovolt = 1,000 voltskW kilowatt = 1,000 wattskWh kilowatt hour = 1,000 watt hoursM3 cubic meterMW megawatt = 1,000 kilowattsp.a. per annumTOE (toe) tonnes of oil equivalent = 39.68 million Btu;

10 million kcaltonne metric ton = 1,000 kg

Energy Conversion Factors

Fuel TOE per Physical Units 1/

Liquid Fuels (tonnes) 2/

Avgas 1.04LPG 1.08Gasoline 1.05Kerosene/Jet Fuel 1.03Gas Oil 1.02Marine Diesel Oil 1.10Fuel Oil 0.98

Electricity (MWh) 3/ 0.25

Biomass Fuels (tonnes)

Fuelwood = 0.35Coconut Husk = 0.40Coconut Shell = 0.50Sawmill Offcuts = 0.35Cinnamon Residues = 0.35

1/ 1 toe = 10 million kcal= 39.68 million BTU

2/ Avgas = 1415 liters/tonneLPG = 1846 liters/tonne

Gasoline = 1353 liters/tonneKero/jet fuel = 1234 liters/tonneGas Oil = 1184 liters/tonneMarine Diesel Oil 1175 liters/tonneFuel Oil = 1059 liters/tonne

3/ Converted at thermal efficiency of 34%.

Table of Contents

Page No.

SUMMARY OF FINDINGS AND RECOMMENDATIONS . ............ i-iv

I. ENERGY AND THE ECONOMY . . ........................... 1

Country Situation ............................... 1Energy Use ..................................................... 3

II. PETROLEUM SUBSECTOR REVIEW ................... ...... 5Supplies ...................................................... 5Historical Demand ....................................... . 5Demand Projections .... .......................... 8Petroleum Pricing and Import Costs ............ .. 8Hydrocarbon Exploration ........................ .11

III. POWER SUBSECTOR REVIEW ........................... .. 14

Supply/Demand ...................... ............ . 14Load Forecast ..................... . 15Fuel Substitution .. .... ..................... .. 17Power Tariffs........ ........................ .... 18Power Supply Options ................................ . 19

IV. RENEWABLE ENERGY OPTIONS ........... o ............ .. 20

Introduction ............................... .................. 20Biomass Resources .... .. ......................... 20

Coconut Residues .......... ............... . ..... . 20Cinnamon ...................................... 21Sawmill Residues and Logging Wastes.......... 21Other Land Use Categories ... 22Biomass Options ... ............ 22

Other Renewables ............ ... .......... . 24Biomass Technologies ................. ........................... 25Biogas ........... , ........................... 25Solar Crop Drying ............... . ... ....... 25Solar Water Heating .. ... .......... . ............ . 25Photovoltaics ........................ ....................... 26Wind .................................................... 26Ocean ............................... .. .... ... . 26

Wave/Tidal .................................................. 27Mini Hydro .................................... 27Activated Charcoal ........................... . 28Outer Islands ................................. 28

Conclusion ....... .................... . 29

V. ENERGY INSTITUTIONS AND TECHNICAL ASSISTANCE...... 30Energy Planning and Administration .............. 30Seychelles Electricity Corporation .............. 31

Organization ChartsResearch and Development Unit, MPER ............. 33

Seychelles Electricity Corporation Limited ...... 34

Page No.Annexes

Annex I: Notes on the Energy Balance . ........... 35Annex II: Technical Assisl:ance Needs .................. ..... 36

Statistical Annex

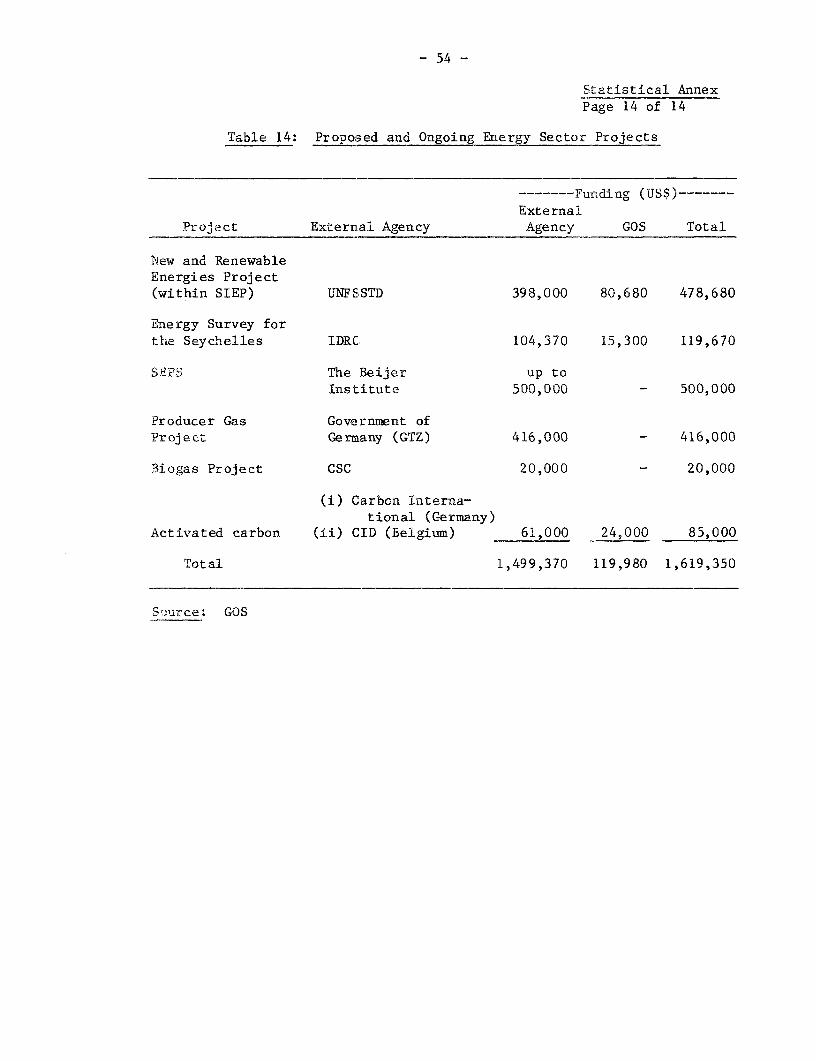

1. Petroleum Demand (1975-1983) ..... ..... 412. Sectoral Consumptionl of Petroleum Products (1982)vo. 423. Petroleum Price StruCture: Effective May 1983..,, 1 .... 434. Petroleum Import Costs (January-June, 1983)........ 445. Sales of Electricity by Sector . .456. Mahe: Expected Increase in Demand (Base Load - 1982) 467. SEC - Conditions of Installed Units .................. 478. Transformer Substations on Mahe and Praslin (1983)... 489. Praslin: Power Demanid Projections (1981-1985) ........ 4910. Praslin: Projected Fuel Demand for Power Generation.. 5011. GDP by Industrial Origin (1978-81) ................... 5112. GDP Forecasts (1982--1990)v ........................ .. 5213. Foreign Trade (1979--82) ......................... 5314. Proposed and Ongoing Energy Sector Projects .54

Tables in Text

1 Trends in GDP and Petroleum Demand (1976-82) ........... i1.1 GDP Trends (1976-1982 . , .. .... . ,e ee......vv ..... e...c 11.2 Foreign Trade . ......... ... .. 21.3 Petroleum Import Costs .................... 21.4 Energy Balance, 1982.......................... 42.1 Inland and Total Petrcleum Product Demand (1975-82)..,. 62.2 Inland Demand for Petroleum Products (1975-82) ......... 62.3 Inland Petroleum DemarLd by Sector (1982)........ ...... 72.4 Petroleum Demand Projections . . 82.5 Retail Prices of Petrcleum Products, May 1983 .......... 92.6 Index of Relative Prices of Selected

Petroleum Products .................. ... ........ , 103.1 SEC - Power Supply/Demand Statistics (1982) ............ 143.2 SEC - Power Generation and Sales .............. D.--- 153.3 Power Demand Projections (1982-95),..... ............. 163.4 SEC Average Revenue ......................... . ... . 184.1 Annual Biomass Potential for Main Islands .............. 234.2 Mahe - Potential Mini Hydropower Sites . . . 28

Map s

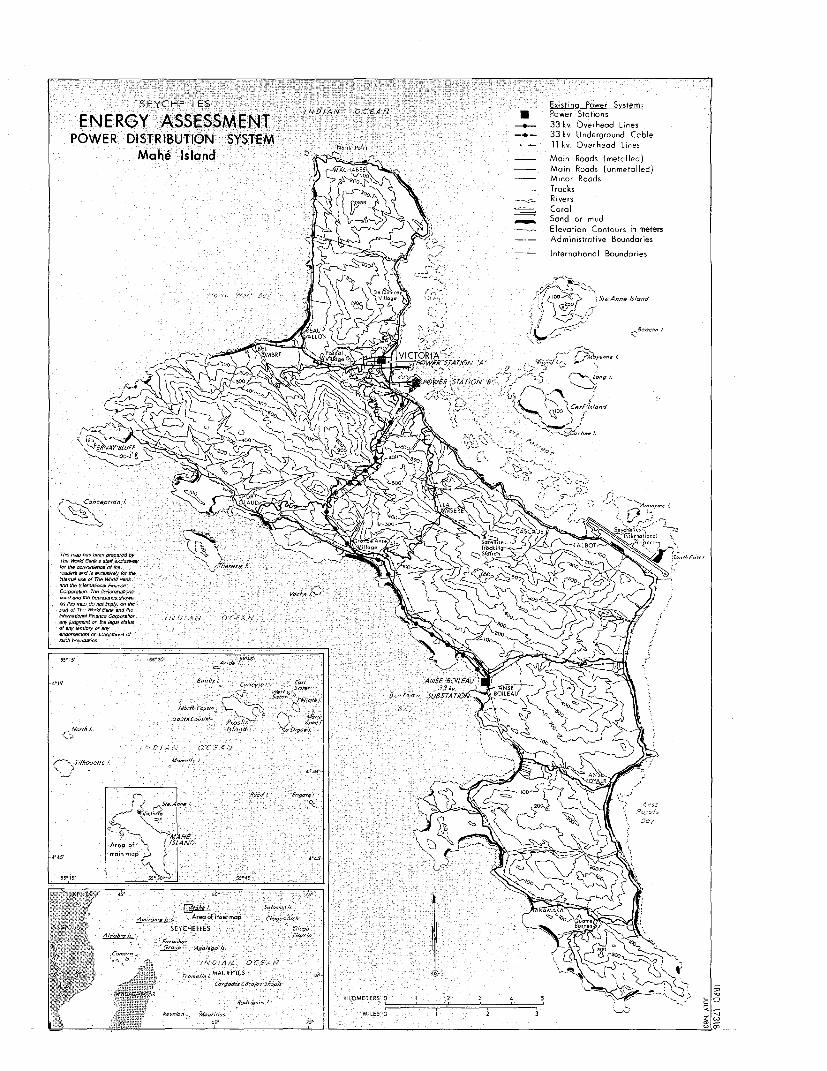

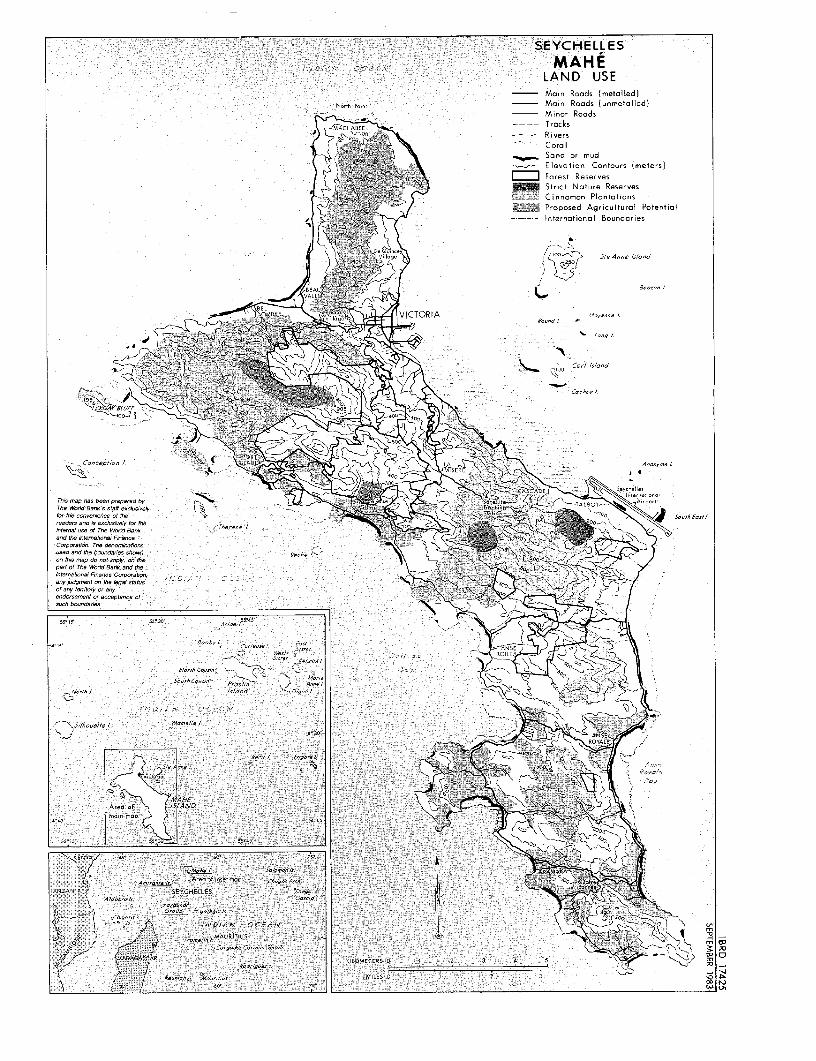

IBRD No. 17318 Power Supply System (Mahe)IBRD No. 17425 Land Use (Mahe)

SUMMARY OF FINDINGS AND RECOMMENDATIONS

1. The Seychelles' economy is highly dependent on tourism, particu-larly from the West European nations; its economic problems are typicalof those of small island, tourism-based, open economies. From 1976 to1979, the economy grew rapidly, at an average rate of ten percent a year,but the economy has declined in the past three years, with negativegrowth averaging 8.7% a year. The economic downturn is due to a sharpdrop in tourist arrivals and copra exports. Between 1976 and 1979, thecost of petroleum imports grew rapidly, from SR 56 million (US$7.2 mil-lion) to SR 130 million (US$19.8 million), and despite the recentdeclines in tourism and the volume of petroleum imports, the cost of oilimports has remained almost unchanged at SR 129 million (US$19.7 million)in 1982. 1/ However, this figure far exceeded merchandise export earn-ings of SR 85 million (US$13 million) in 1982; the cost of petroleumimports in that year amounted to 42% of merchandise export earnings andtourism revenues combined.

Table 1: Trends in GDP and Petroleum Demand (1976-82)

1976 1979 1982

GDP (million 1976 US$) 46.8 62.3 47.4Population ('000) 60 63 65Petroleum demand/capita (toe) a/ 0.37 0.44 0.43Petroleum import costs/capita (US$) a/ 48.3 150.8 169.2

a/ Excludes bunkering.

Source: Statistics Division, Government of Seychelles.

2. The Government of Seychelles (GOS) has a twofold strategy to re-verse the decline in the economy: (i) by encouraging tourism to restoreits 1979 level of activity; and (ii) by diversifying the economy throughthe promotion of fishing and fish exports, and export-oriented indus-tries. If this strategy is successful, GOS expects to see a five percentp.a. long-term real growth in GDP. However, it is likely that any newexport-oriented industries will only have a marginal effect on GDP growthin the near future and that a growth of five percent is overly optimis-tic. The Government and the Mission agreed to use two growth scenarios

1/ The inland petroleum consumption's import cost in 1982 was SR 72.1million (US$11 million) which appears to be high on a per capitabasis because of a low population base.

- ii -

for projecting future energy demand: a 3% p.a. base growth and a 4% p.a.optimistic growth. The use of these two growth scenarios makes littledifference in the forecast. However, it should be noted that Seychelleswill need to be prudent irL its foreign borrowing. Any significant in-crease on commercial terms could lead to a difficult external debtsituation at an early stage.

3. In 1979, the GOS established the Research and Development Unit(RDU) within the Ministry of Planning and External Relations (MPER). Al-though this unit is not formally responsible for energy matters outsidethe areas of renewable energy and adaptive research, it is consideredresponsible for energy planning in the absence of any other body. Re-sponsibilities for the oil and power subsectors also lie within the MPER,but coordination is lacking; important issues relating to petroleumsupplies and pricing, the power sector and energy-related land use havenot been given appropriate priority. Various other energy planning"activities have been started or proposed in Seychelles in an ad hocfashion, and there is a danger of duplication. The Mission thereforerecommends that the energy planning role of the RDU be formalized andthat it be provided with technical support. 1/ The Mission sees thefirst task of the unit and its support to be the evaluation of existingand proposed technical assistance projects, with the aim of redefiningtheir scope to avoid duplication and ensure that the work is designedaccording to stated objectives.

Petroleum Supplies

4. The current inland consumption (excluding bunkering) of petro-leum products is about 1,100 bbl/day (28,100 toe/year) with middle dis-tillates taking more than 75% (Table 2.2). Immediate steps should betaken to relieve the burden of oil imports on foreign exchange resources.First, the possibilities of regional cooperation with neighboringcountries such as Mauritius and Madagascar or Uganda and Burundi to poolimports should be investigated in order to reduce import and transportcosts. Second, the relative retail prices of petroleum products whichencourage the use of diesel and kerosene should be changed to reflectrelative import costs. Third, although passenger cars appear to beoperating efficiently, the efficiency of the public transportation systemcould be improved by modernizing the fleet (introducing fuel efficientmini-buses) and reorganizing the routes and schedules.

1/ The GOS has formally asked the Mission for such support.

- iii -

Hydrocarbon Exploration

5. Except for some airmag surveys done in deep waters, all explora-tion work in Seychelles has been concentrated offshore within the 200meter isobath line. Amoco drilled three offshore wells, two of whichseem to be lacking in thick prospective marine sections and probably have

poor source rocks. The third well did show about 4,000 ft. of poten-tially prospective marine jurassic sediments. While the prospects foroil are uncertain, the area does nevertheless justify an attempt toencourage further exploration. The Mission recommends that a two-stageapproach be followed. First, a fact-finding mission should be sent toevaluate the work done so far and determine the scope and extent offurther assistance needed; depending on the findings of this mission, anexploration promotion team could be organized to prepare a promotionalpackage for sale to the oil industry. In exploration, the GOS should notundertake any drilling itself and, indeed, should normally not evenfinance geophysical surveys.

Power

6. Until 1982, all power generation came from gas oil. In 1982 allfive sets at the 'B' Station (4 x 2.5 MW and 1 x 5 MW) 1/ were convertedto fuel oil to reduce fuel costs. As a result, the Seychelles Electri-city Corporation (SEC) has reduced fuel costs by about 20%. Currently,it is planned to retire four old sets at the 'A' Station and replace themwith a new SMW slow speed diesel unit (fuel oil-based). Although thiswill improve the firm capacity and reliability of the generation system,some old units at the 'A' Station may have to be kept in operationalcondition until the generation system is further expanded. While futuresystem expansion should take into consideration the possible contribu-tions of biomass gasification and mini-hydropower, these options arelikely to make only a marginal contribution, and the system will continueto rely on petroleum-based thermal generation. Plans to expand thegeneration system should also consider the possibility of using coal.Attempts also should be made to reduce peak demand by restructuring thetariffs for the commercial/industrial sector which has a declining block-base. For domestic users, demand related tariffs should be considered.

7. SEC seems to be overstaffed with respect to: (a) its establish-ment of a department in an attemmpt to sell services in competition withprivate contractors; (b) insufficient training and experience in opera-tions and maintenance on the part of the technical staff; and (c) socio-political pressures to keep the redundant staff on payroll. The missionrecommends that this situation be remedied by providing technical and

1/ Firm capacity at the 'B' Station is only 7.5 MW because one unit isalways under maintenance.

- iv -

economic assistance to the SEC in three areas: (i) doing a tariff studyto determine an efficient tariff structure; (ii) a training program foroperating diesel power stations; and (iii) developing a system mainten-ance plan for oil diesel generators. Furthermore, the proposal by SEC toassign energy planning activities to an energy unit within the SEC shouldbe reconsidered, particularly if the recommended reorganization of RDU isimplemented.

Biomass and Renewables

8. Biomass currently is the only domestic alternative to importedoil. 1/ However, the Mission believes the impact of biomass and otherrenewable energy sources on the granitic group of islands will not besignificant because of: (i) the limited number of end-use options; and(ii) the limited accessibility of biomass due to the difficult terrain onMahe. Certain applications, such as producer gas and mini-hydro schemes,however, should be evaluated to determine this potential and to find waysof substituting these for imported oil. Steam turbines using coconuthusks and shells as fuel may be used on outer islands as an alternativeto gasifier units. Steam turbines are not only a proven technology, butalso easy to use, while the commercial viability of producer gas systemsunder variable load conditicns is still not established. For the outerislands the contribution of biomass for power generation and crop dryingis, however, more promising. To properly evaluate energy supply options,the Mission recommends that energy studies in progress within the SIEPinclude the establishment of an adequate data base, an evaluation ofland-use options from a combined energy/agricultural perspective, anevaluation of possible energy conservation activities and studies on thefeasibility of selected renEwable energy sources. With respect to ongo-ing programs on producer gas and biogas, priority should be given totests on outer islands.

1/ A major biomass and renewable energies study, known as the SIEP(Seychelles Integrated Energy Project), is currently underway.

I. ENERGY AND THE ECONOMY

Country Situation

101 The Republic of Seychelles comprises about 100 islands with atotal land area of 400 sq. km. About 88% of the total population(65,000) lives on Mahe. Thirty-two of the islands are granitic andrugged, and none are more than 60 km. from Mahe; the other islands arecoralline and are more widely spread. The temperature varies relativelylittle during the year (Mahe averages 30°C), but rainfall varies consid-erably from island to island. Through the Island Development Company(IDC), the GOS plans to develop permanent settlements of 100-500 peopleon eight coralline islands 1/ over the next ten years.

1.2 The economy of Seychelles is open, with imports accounting for76% of GDP in 1982. Following their independence in 1976, the Seychellesexperienced a ten percent real growth in GDP, primarily caused by an ex-pansion in tourism which lasted until 1979. The share of tourism-relatedactivities 2/ grew from 14.7% of GDP in 1976 to 19.5% in 1979. Tourismbegan to decline in 1980 3/ due to the recession in western Europe (whichhad supplied more than 62% of the tourists to Seychelles since 1977), andwas further affected by an attack of mercenaries on Mahe internationalairport in November 1981, Between 1979 and 1982, GDP fell 8.7% a year.

Table 1.1: Seychelles - GDP Trends (1976-1982)(1976 prices)

Growth % p.a.1976 1979 1982 a/ 1976-79 1979-82

GDP (SR million) 366.4 488.1 371.1 10.0 (8.7) b/

a/ Preliminary estimate.b/ Brackets indicate negative figures.

Source: Statistics Division, Government of Seychelles.

1/ Desroches, Coetivy, Farquhar, Cosmoledo, Astove, Providence, Marie-Louise and Desnoef.

2/ Hotels, restaurants, handicrafts, air transport and allied services,taxis, car rentals and recreation services.

3/ Number of tourist arrivals. 37,721 in 1975; 64,995 in 1978; 78,852in 1979; 71,762 in 1980; 60,425 in 1981; and 47,280 in 1982.

1.3 The Seychelles' balance of payments is characterized by a grow-ing deficit. Between 1979 and 1982, the terms of trade worsened asprices for major export products fell sharply (by 30% for copra, 25% forfish). Table 1.2 shows the country's major export products and balanceof trade.

Table 1.2: Seychelles - Foreign Trade(SR Million)

1979 1982

Domestic Exports 30.9 20.3Re-exports 83.7 64.9Total Exports 114.6 85.2Total Imports 534.8 638.6Trade Balance (4 20.2)a/ (553.4)a/

a/ Brackets indicate negative figures.

Source: Annex Table 11.

1.4 Commercial energy needs are met entirely from imported petrole-um. The petroleum import bill for inland use (excluding bunkers) rosefrom SR 23.0 million (US$2.9 million) in 1976 to SR 60.2 million (US$9.5million) in 1979. In 1982, petroleum imports for domestic consumption(inland) were about SR 72.1 million (US$11.0 million). The inland petro-leum import bill far exceeded the value of domestic exports (SR 20.3million or US$3.1 million in 1982) but was only 29.1% of earnings frommerchandise exports and tourism (1982). Although the petroleum importbill is relatively small, its growing burden on the narrow export base ofthe economy is a cause for concern to the GOS. This cost can be reducedto some extent by fuel substitution in the power and hotel industries,conservation measures in the transport sector, and by pooling the pro-curement of products with other countries in the region.

Table 1.$: Petroleum Import Cost

1979 1982

SR Million US$ Million SR Million US$ Million

Total petroleum imports 130.2 20.6 129.0 19.7Bunkering 70.0 11.1 56.9 8.7Net Inland Imports 60.2 9.5 72.1 11.0Inland petroleum imports as

percent of total imports 10.7 11.3

Source: Statistics Division, Government of Seychelles.

- 3 -

1.5 The Government is concerned about the current decline in the

economy and has outlined a strategy to reverse this trend through:(i) encouraging tourism to restore its 1979 level of activity (about79,000 tourist arrivals) by 1985/86, 1/ and then to increase touristarrivals to 100,000 by 1988 (these can be handled by existing facilities)and sustain it at that level; and (ii) diversifying the economy by pro-moting fishing and fish exports, and by encouraging export-orientedindustries. The Government is hopeful that if it achieves these targets,the economy will grow at about five percent a year. However, it islikely that any new export-oriented industries will have only a marginaleffect on GDP. For projecting future energy demand, therefore, theMission agreed with the GOS to use: (i) a base real growth in GDP ofthree percent a year; and (ii) an optimistic growth of four percent ayear beyond 1985.

Energy Use

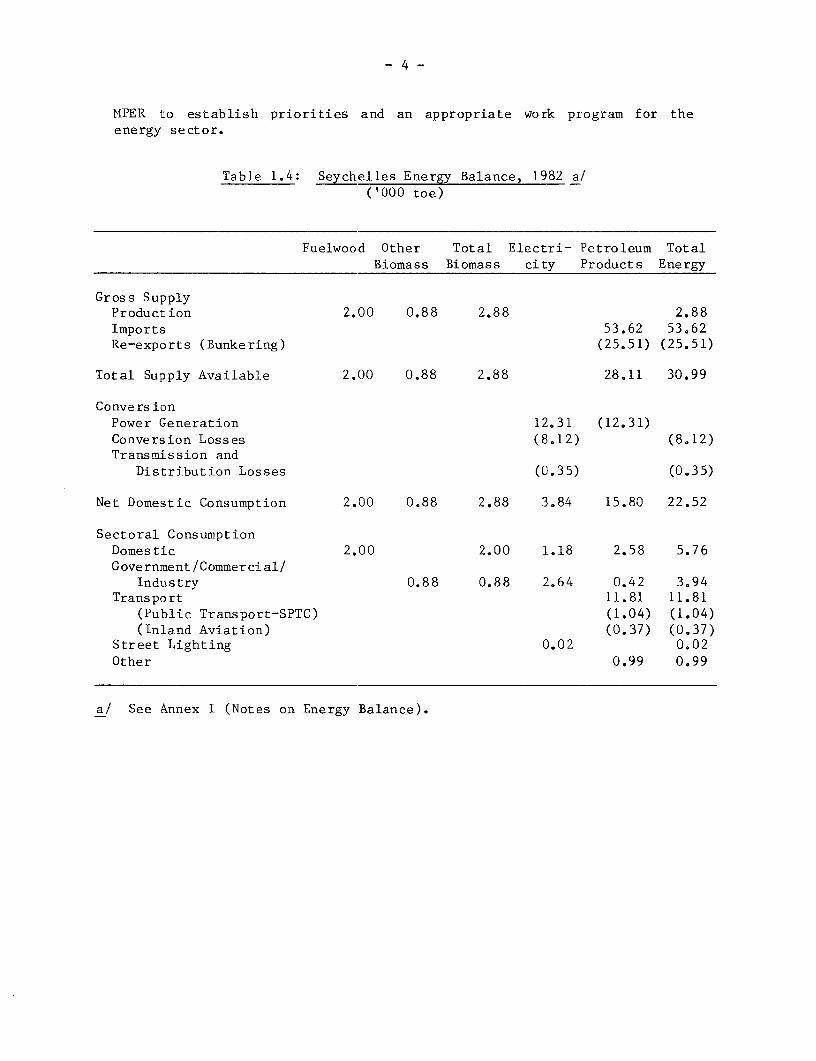

1.6 Because of the size and openness of the economy, the energy sec-tor is small and simple. Although indigenous biomass potential of thegranitic group of islands is estimated to exist at 10,000 toe, because ofdifficult access and high collection/transport costs, uses for thesesources are limited. Data are scarce, but the Mission estimates thatfuelwood in the country represents about nine percent of total energyuse, mainly by the household sector. The total easily accessible poten-tial of biomass is estimated at about 6,000 toe which would representabout 19% of current estimated energy use. Maintaining this level ofutilization would require costly and difficult collection procedures.Commercial energy imports are entirely petroleum-based, and per capitainland consumption (excluding bunkers) is estimated at 2.9 boe. Thisconsumption level is higher than in countries in a similar income group,such as Fiji (2.2 boe) and Mauritius (1.1 boe). The public and privatetransport sector, with 44% of total demand, dominates net commercialenergy use. Power generation is entirely thermal-based and uses about44% of oil imports. The estimated energy balance for 1982 is shown inTable 1.4; as data on local resources are poor and not readily available,the Mission recommends that the Ministry of Planning and ExternalRelations (MPER), which is responsible for the energy sector, regularlygather and refine the information needed to draw up the balance.

1.7 The major issues in the energy sector are: (i) how to reducethe growing burden of petroleum imports through alternative importarrangements and conservation; (ii) how to promote and accelerate explo-ration activities for oil and gas; (ii ) how to encourage fuel substitu-tion and develop new options for powe! generation; and (iv) how to re-define and restructure the Research and Development Unit (RDU) within the

1/ The Government expects the number of tourist arrivals to be about47,000 in 1983, and about 56,000 in 1984.

- 4 -

MPER to establish priorities and an appropriate work program for theenergy sector.

Table 1.4: Seychelles Energy Balance, 1982 a/('000 toe)

Fuelwood Other Total Electri- Petroleum TotalBiomass Biomass city Products Energy

Gross SupplyProduction 2.00 0.88 2.88 2.88Imports 53.62 53.62Re-exports (Bunkering) (25.51) (25.51)

Total Supply Available 2.00 0.88 2.88 28.11 30.99

ConversionPower Generation 12.31 (12.31)Conversion Losses (8.12) (8.12)Transmission and

Distribution Losses (0.35) (0.35)

Net Domestic Consumption 2.00 0.88 2.88 3.84 15.80 22.52

Sectoral ConsumptionDomestic 2.00 2.00 1.18 2.58 5.76Government /Commerci al/

Industry 0.88 0.88 2.64 0.42 3.94Transport 11.81 11.81

(Public Transport-SPTC) (1.04) (1.04)(Inland Aviation) (0.37) (0.37)

Street Lighting 0.02 0.02Other 0.99 0.99

a/ See Annex I (Notes on Energy Balance).

II. PETROLEUM SUBSECTOR REVIEW

Supplies

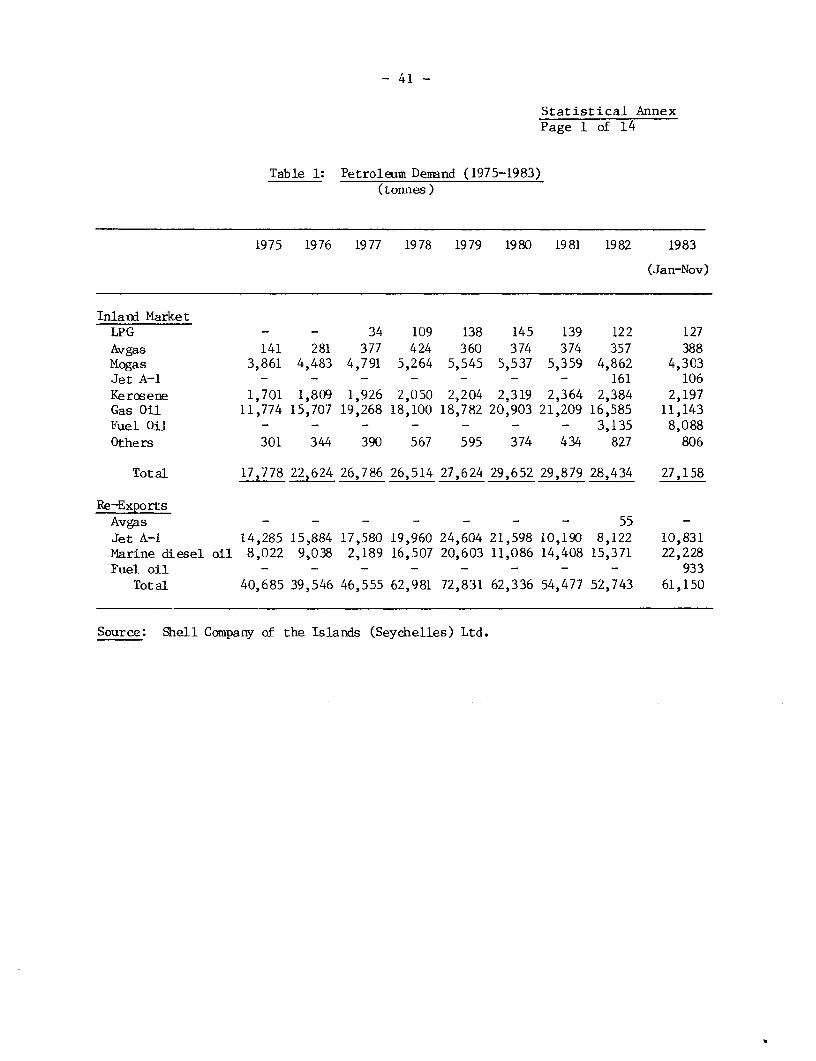

2.1 The principal source of petroleum product supplies is Bahrain,although imports in small quantities also come from Kenya and the Repub-lic of South Africa (RSA). Petroleum imports come in General Purpose(GP) Tankers, except for LPG 1/ which is imported in 48-kg cylinders fromthe RSA. The tanker, which arrives once every six weeks, is sometimesshared with Mauritius, Djibouti and the Reunion. The Seychelles receives8,000-10,000 tonnes of petroleum products per shipment at a freight costof US$18.25/long ton for clean products (except avgas). Imports anddistribution are directly handled by the Shell Company of the Islands(Seychelles) Limited, which is the only company operating in thecountry. The company operates five retail outlets on Mahe and two onPraslin. Total storage capacity on Mahe is 22,308 tonnes, representing159 days cover of consumption at the current level. 2/ In the Mission'sview, the current distribution system and storage facilities are adequateand work well.

Historical Demand

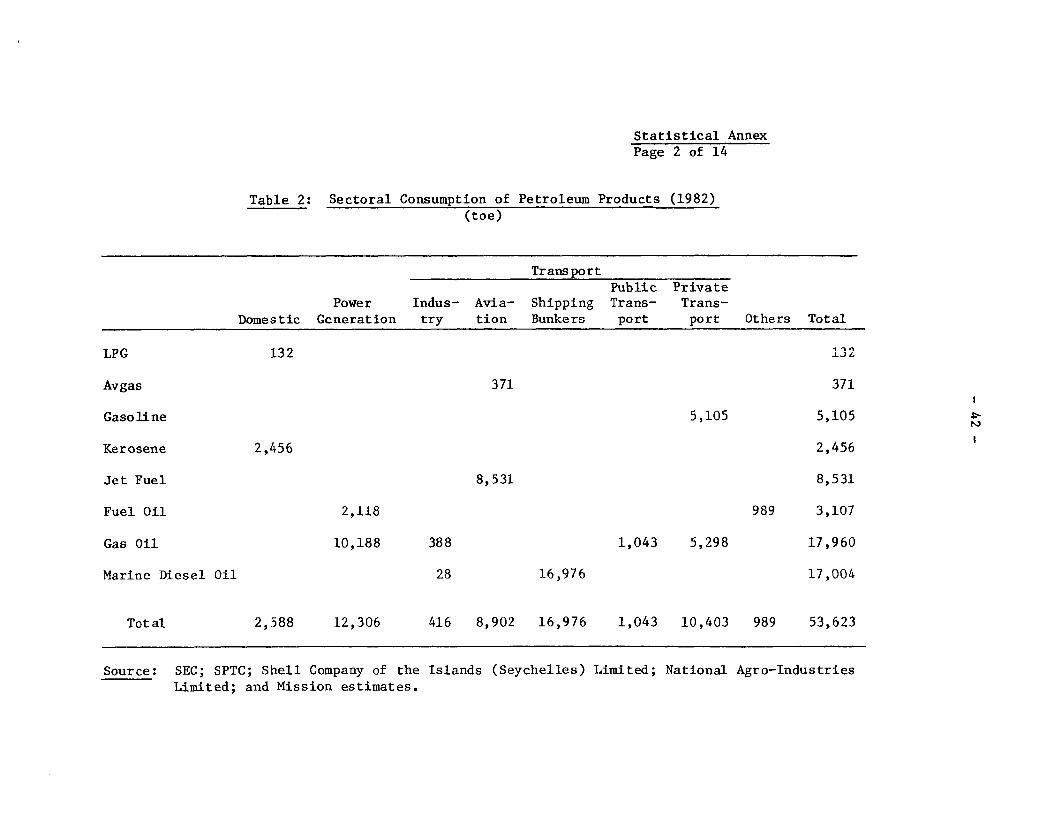

2.2 Between 1975 and 1979, petroleum demand increased at 16.2% ayear, primarily from increasing tourist arrivals (1.2). Tourist arrivalspeaked in 1979 at about 79,000, as did petroleum imports at 75,778 toe(including imports for bunker). International bunkering and tourismmoved in parallel during 1975 and 1979, increasing at 19.3% and 20.6%p.a. respectively. The major increases were in jet turbo fuels, whichincreased from 14,714 toe in 1975 to 25,342 toe in 1979, and in marinediesel oil for bunkers, from 8,824 toe to 22,663 toe. With the slump intourism after 1979, the frequency of airline flights and ship calls tothe Seychelles declined sharply. As a result, the demand for jet turbo-fuel and marine diesel oil fell by 30.4% p.a. and 9.2% p.a. between 1979and 1982. As the decline in tourism averaged 16% p.a., total interna-tional bunkering uplifts (including airlines) declined by 19.0% p.a. overthe period, and in 1982 they constituted about 48% of total petroleumdemand.

1/ Mix of propane (50%) and butane (50%).

2/ This capacity includes black oil storage of 6,800 tonnes (for poweruse) and storage of 3,578 tonnes at the international airport. Inaddition, the SEC has a storage capacity of 1.6 million liters(about 1,350 tonnes) on Mahe and 0.2 million liters (about 160tonnes) on Praslin.

-6 -

Table 2.1: Inland and Total Petroleum Product Demand (1975-1982)

1975 1979 % Growth p.a. 1982 % Growth p.a.'000 toe % '000 toe. % 1975-79 '000 toe % 1979-82

Inland Demand 18.0 43.3 27.8 36.7 11.5 28.1 52.4 0.4

InternationalBunkers 23.5 56.7 48.0 63.3 19.5 25.5 47.6 (19.0)

Total Demand 41.5 100.0 75.8 100.0 16.2 53.6 100.0 (10.9)

Source: Shell Company of the Islands (Seychelles) Limited and MPER.

2.3 Table 2.2 gives a breakdown of the internal consumption ofpetroleum products by fuel type between 1975 and 1982. Total consumptionincreased from 18,000 toe in L975 to 28,000 toe in 1979 (11.5% p.a.growth), and further to 28,116 toe in 1982. Between 1979 and 1982, theinland demand for petroleum increased only marginally, at 0.4% p.a.because of the increase in powEr generation and household use of kero-sene. Gas oil (diesel oil), LPG and gasoline registered major drops of4.1%, 4.0% and 4.3% p.a., respectively. The only increase was in kero-sene demand, at 2.7% p.a.

Table 2.2: Seychelles - Inland Demand for PetroleumProducts (1975-82)

1975 1979 1982 % Growth p.a. a/toe % toe % toe % 1975-79 1979-82

LPG -- -- 149 0.5 132 0.5 -- (4.0)Avgas 147 0.8 374 1.3 371 1.3 26.3 (0.3)Gasoline 4,054 22.6 5,822 21.0 5,105 18.1 9.5 4(4.3)Kerosene 1,752 9.8 2,270 8.2 2,456 8.7 6.7 2.7Gas Oil 12,009 66.8 19,158 69.0 16,917 60.2 12.4 (4.1)Fuel Oil .. .. .. .. 3,135 11.2

Total 17,962 100.0 27,773 100.0 28,116 100.0 11.5 0.4

a! Figures in brackets represent negative growth.

Source: Shell Company of the Islands (Seychelles) Limited; MPER.

2.4 In 1982, fuel oil was imported for the first time as a partialreplacement for gas oil in power generation. The combined demand of fuel

-7-

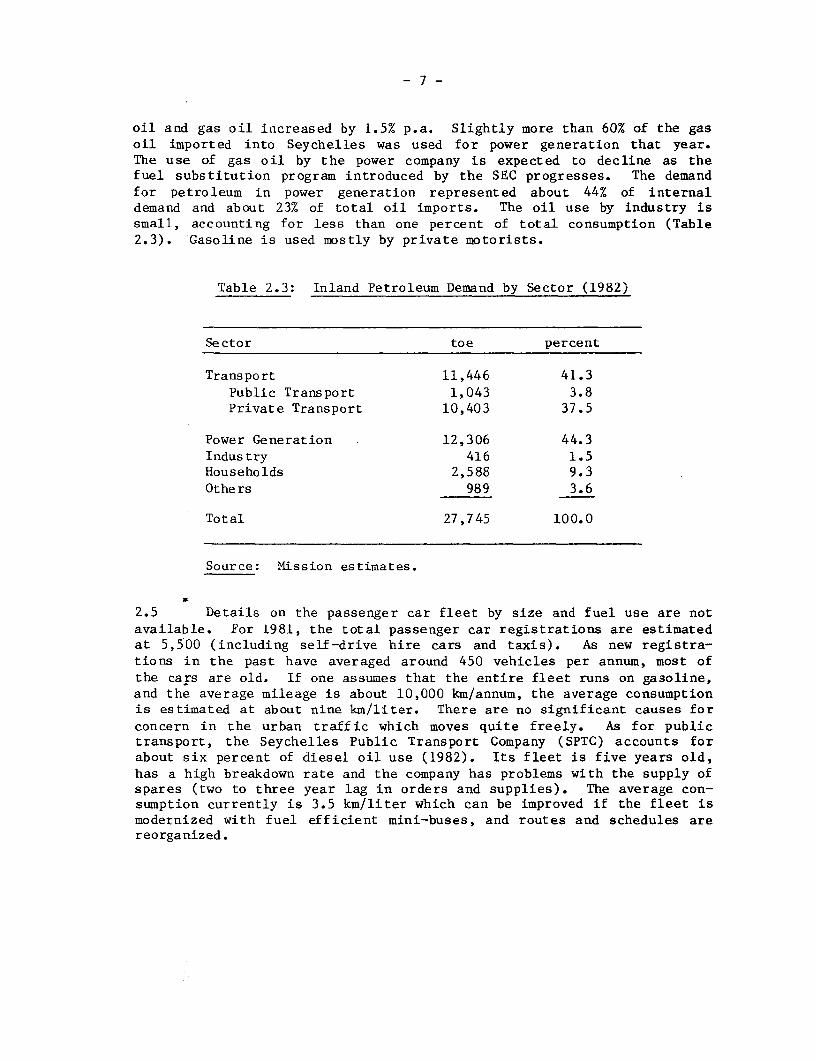

oil and gas oil increased by 1.5% p.a. Slightly more than 60% of the gasoil imported into Seychelles was used for power generation that year.The use of gas oil by the power company is expected to decline as thefuel substitution program introduced by the SEC progresses. The demandfor petroleum in power generation represented about 44% of internaldemand and about 23% of total oil imports. The oil use by industry issmall, accounting for less than one percent of total consumption (Table2.3). Gasoline is used mostly by private motorists.

Table 2.3: Inland Petroleum Demand by Sector (1982)

Se ctor toe percent

Transport 11,446 41.3Public Transport 1,043 3.8Private Transport 10,403 37.5

Power Generation 12,306 44.3Indus try 416 1.5Households 2,588 9.3Others 989 3.6

Total 27,745 100.0

Source: Mission estimates.

2.5 Details on the passenger car fleet by size and fuel use are notavailable. For 1981, the total passenger car registrations are estimatedat 5,500 (including self-drive hire cars and taxis). As new registra-tions in the past have averaged around 450 vehicles per annum, most ofthe cars are old. If one assumes that the entire fleet runs on gasoline,and the average mileage is about 10,000 km/annum, the average consumptionis estimated at about nine km/liter. There are no significant causes forconcern in the urban traffic which moves quite freely. As for publictransport, the Seychelles Public Transport Company (SPTC) accounts forabout six percent of diesel oil use (1982). Its fleet is five years old,has a high breakdown rate and the company has problems with the supply ofspares (two to three year lag in orders and supplies). The average con-sumption currently is 3.5 km/liter which can be improved if the fleet ismodernized with fuel efficient mini-buses, and routes and schedules arereorganized.

- 8 -

Demand Projections

2.6 As indigenous economic resources are limited, economic growthwill depend largely on external factors, especially tourism. Under thebase growth scenario, the Mission projects petroleum demand to grow at5.5% a year until 1985, and at: 4.4% thereafter. Total petroleum demandwould be about 63,000 tonnes (including re-exports) in 1985, and 78,000tonnes in 1990. The petroleum product demand mix will change consider-ably as power generation shifts from using gas oil to fuel oil.

Table 2.4: Petroleum Demand Projections('000 tonnes)

1982-19901990 (% Growth p.a.) a/

1982 Base Optimistic Base OptimisticActual 1985 Growth Growth Growth Growth

Avgas 0.4 0.4 0.5 0.5 3.8 3.8LPG 0.1 0.2 0.2 0.2 5.5 5.5Gasoline 5.1 5.6 7.2 7.7 4.4 5.3Turbo Jet Fuel 8.5 15.0 18.0 19.0 9.8 10.5Kerosene 2.5 2.6 3.0 3.1 2.5 2.9Gas Oil 16.9 10.7 12.4 13.1 (3.8) (3.1)Marine Diesel Oil 17.0 18.0 23.0 25.0 3.9 5.0Fuel Oil 3.1 10.5 13.7 14.5 20.3 21.1

Total 53.6 63.0 78.0 83.1 4.8 5.6

a/ Brackets indicate negative growth.

Source: Mission estimates

2.7 Under the optimistic growth scenario, the Mission projectsdemand to increase at 5.6% p.a. to give a GDP elasticity of 1.63, whichis close to the 1976-1979 level. This will bring the total imports in1990 to 83,100 tonnes which is about 14% higher than import levels in1979 (72,800 tonnes). Turbo jet fuel is projected to increase at 10.5%p.a. (1982-1990), which assumes that tourism will be able to repeat itsperformance of the 1970s and that airlines will schedule new flights tothe Seychelles.

-9-

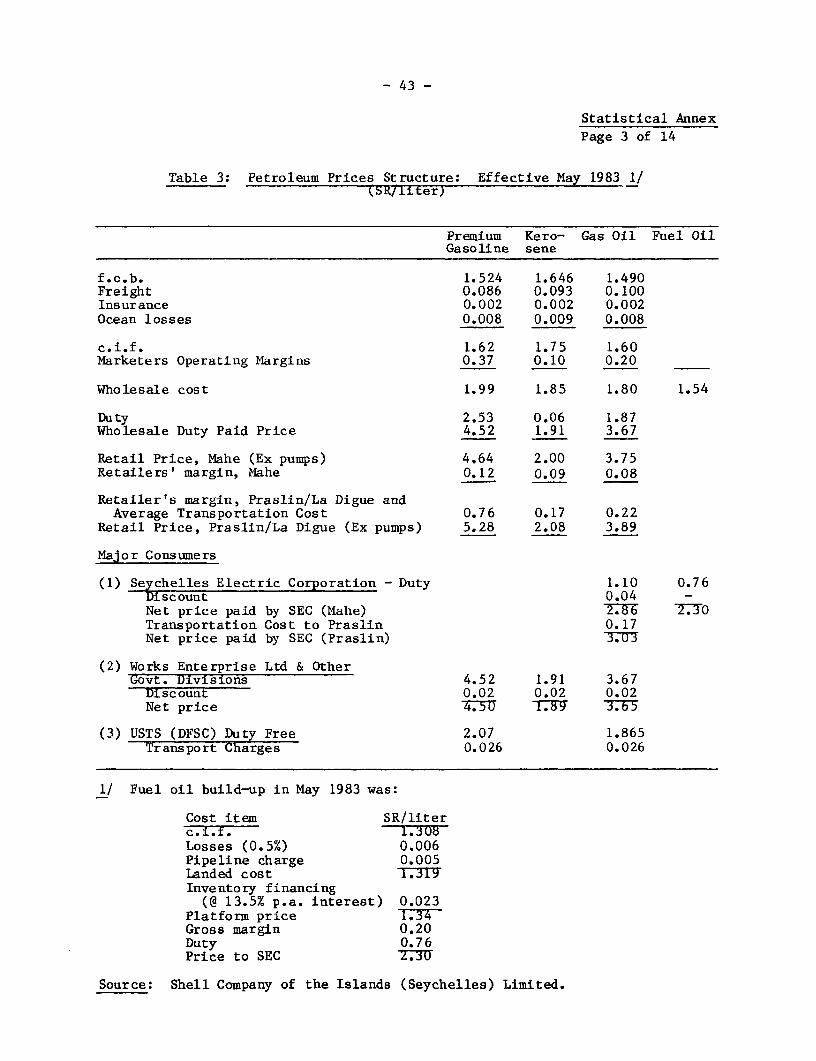

Petroleum Pricing and Import Costs

2.8 A detailed build-up of petroleum import costs is shown in AnnexTable 3, Current platform costs (c.i.f. plus ocean losses) for importinggasoline, kerosene and gas oil are US$39.33/bbl, US$42.49/bbl andUS$38.85/bbl, respectively. These costs compare favorably with costs inother developing countries. 1/ Nevertheless, Seychelles may be able toreduce its freight 2/ and procurement costs by pooling import require-ments with other nations in the region (Mauritius, Comoros, Djibouti,Madagascar and the Reunion). 3/ The Mission recommends that the Govern-ment explore and identify the least-cost supply option, which would re-quire a technical review of: (i) an offshore processing deal for thegroup of countries based on joint crude oil purchases, together withpossible refinery locations for such a deal; (ii) the least-cost trans-port options and tanker size; and (iii) the administrative organizationto arrange and implement the pooling of petroleum purchases by the par-ticipating countries (Annex II).

Table 2.5: Retail Prices of Petroleum Products, May 1983(SR/liter)

Mogas Gas Oil Gas Oil(95 Octane) Kerosene (Retail) (Power Generation)

Platform Cost 1.62 1.75 1.60 1.60Duty 2.53 0.06 1.87 1.10Marketer's Margin 0.37 0.10 0.20 0.20Retail Margin 0.12 0.09 0.08 _

Retail Price 4.64 2.00 3.75 2.90Retail Price(US$/US gallon) 2.68 1.16 2.17 1.68

Source: GOS

1/ The landed costs for major petroleum products consist of: (i) f.o.b.Bahrain, (ii) GP(general purpose vessel)-AFRA including premium forclean products; (iii) insurance at 0.101% of cost and freight; and(iv) ocean losses at 0.5% of c.i.f.

2/ This at times includes up to 35% of the premium on the AFRA ratesfor clean products.

3/ Another possibility may be to procure supplies via Dar-Es-Salaam,Tanzania. Burundi and Uganda have plans to import petroleumproducts from the Middle East and transport them through Tanzania,as an alternative to importing those refined in Kenya. This schemecould be more economical if the same tanker that brought supplies

for Uganda and Burundi to Dar-Es-Salaam could also bring suppliesfor other island nations (including the Seychelles).

- 10 -

2.9 Although the current consumer prices of various petroleum pro-ducts are higher than their c.i.f prices, (Tables 2.5 and 2.6), they donot reflect relative import costs and the international product supply/demand balance. For example, the f.o.b. posting price of kerosene at theexport refinery in Bahrain is 7.5% higher (average 1983 import parity waseight percent higher than gasoline) than that for gasoline (95 octane);in the Seychelles, the retail consumer price of kerosene is about 57%lower (Table 2.6). This disparity was more pronounced before May, 1983when the Government subsidized kerosene. This gives false signals to theconsumers about the availability and relative costs of kerosene and gasoil. The disparity between prices in Seychelles and Bahrain has encour-aged the use of kerosene, especially for cooking, and is the prime reasonwhy kerosene use has continued to increase even during the economicslump.

2.10 Gas oil is retailed at about 19% below the price of gasoline.The price to SEC is 37.5% below that of gasoline. As a result, gas oilhas accounted for more than 71% of total inland demand (1981). The deci-sion to replace gas oil by f uel oil for power generation in 1982 causedthe demand for gas oil to fall to about 60% of the total demand mix.

Table 2.6: Index of Relative Pricesof Selected Petroleum Products (June 1983)

(95 octane gasoline = 100)

SeychellesBahrain Average Im- SeychellesPostings port parity Prices

95 Octane Gasoline 100.0 100.0 100.0Kerosene 107.5 108.0 43.1Gas Oil (Retail) 97.4 99.0 80.8Gas Oil (Power Generation) 97.4 99.0 62.5

Sources: Platt's Oil Gram (June 22, 1983); GOS.

2.11 The relative retail prices of petroleum fuels should be based onrelative import parity costs and signal the realistic relative productsupply/demand situation at the refining centers. A change in the rela-tive prices of currently controlled products (gasoline, gasoil andkerosene) will encourage the use of fuel oil by the SEC. As the SEC isthe only user of fuel oil in the country, it could test the internationalsupplies/costs by inviting tender bids directly from independentsuppliers to obtain best tenns and prices. Concerns regarding the highcost of power to the productive sector from increases in the gas oilprice are unfounded. Currently, the Government levies a SR 0. 7 6/literduty on fuel oil sold to the power company. In the Mission's view, this

- 11 -

duty should be eliminated to improve the competitiveness of exports,import substitution and tourism. A direct duty or sales tax on productsintended for the domestic market may be a better option. This will alsoimprove the financial position of the SEC.

2.12 LPG is currently imported from the RSA in 48 kg bottles. Theex-refinery cost is about US$388/tonne which compares with the Baharainf.o.b. price of US$240/tonne. The f.o.b. cost from RSA is US$439/tonne(excluding the cost of empty bottle return to the RSA which isUS$61/tonne). Freight charges from RSA are US$646/tonne. In theMission's view the current import system is expensive (landed costUS$1147/tonne). If the LPG is imported in bulk and is bottled locally,this cost can be reduced to about US$697/tonne. The Mission recommendsthat the Government consider changing the existing system. The invest-ments required for the new arrangements would be a 120 m3 LPG storagetank and a filling station which will be paid out in a little over oneyear.

2.13 The Mission recommends that the MPER develop an in-house capa-bility to review international petroleum prices to ensure that domesticprices do not get out of line. Essentially this means recruiting a localeconomist 1/ for the reorganized RDU and obtaining the services of apetroleum supplies/pricing specialist to train the economist (Annex II).The local staff, in addition to working on petroleum prices, should alsobe responsible for energy economic work at the unit. The technicalassistance on petroleum supplies/pricing is required on a regional basisfor about five man-months.

Hydrocarbon Exploration

2.14 Petroleum exploration was initiated in 1977, with the award of43 blocks under the petroleum exploration license to: (i) Amoco, BurmahOil, Norcon and Hematite Petroleum (26 blocks); (ii) Siebens (12 blocks);and (iii) Oxoco (5 blocks). Seismic, gravity and magnetic surveys weredone between 1977 and 1980. Amoco later acquired the interests of BurmahOil, Norcon and Hematite and became the sole right holder for explorationon the 26 blocks (almost 18,000 sq. km). Sieben's interests were passedon to Dome and then to Sovereign Oil Company, while Oxoco's interestswere passed on to Santa Fe. After conducting the minimum obligatory geo-physical surveys, these two companies relinquished their interests in1981. Amoco is now the only operator. It drilled the only three wells

1/ In addition to working on petroleum prices, he would be responsiblefor energy project evaluation and monitoring petroleum supplies.

- 12 -

in the country in 1980/81 1/ about 125 km west of Mahe, but all were dryholes. Although no significant hydrocarbon shows were found, the resultswere interesting enough for Amoco to remain active in the area. It hasnot yet surrendered 13 blocks which, according to the Petroleum Agree-ment, should have been surrendered in June, 1982. Amoco has also signedup for geophysical surveys on an additional 300 blocks (230,500 sq.km). Hunting was hired to conduct an airmag survey of 23,000 line km inMay-June 1982. Amoco is now planning a seismic survey (6,000-7,000 linekm) of more than 90 of the original 300 blocks and has the option ofselecting 25 blocks in 1984 for exploration under a new PetroleumAgreement.

2.15 The Government has some data from seismic surveys that were donebetween 1977 and 1980 covering over 5,000 line/km, and from the threewells drilled by Amoco. The data obtained by the Mission shows that thethree wells all passed through a Cretaceous volcanic section at about5,000 to 7,000 feet and then into Cretaceous and Jurassic sediments. Onewell got as far as the Triassic zone. The 5,000 feet of Tertiary post-volcanic sediments are almost all "shelf carbonates", probably porous,water-saturated limestones lacking in cap rocks and unprospective for oiland gas. Prospects for oil and gas are confined to pre-basalt sedi-ments. The situation is similar to that of Mauritius, but there the twoTexaco wells never got through the volcanics to prove older sediments.The fact that such sediments have been proved in the Seychelles is en-couraging. The Owen Bank well is shown to have about 4,000 ft. of marineJurassic sediments below the volcanic layers. The other two wells, ReithBank and Seagul Shoals, seem to lack thick marine sections and are mostlysand and siltstones, probably with poor source rocks.

2.16 The Seycelles arch:Lpelago has small areas of a shallow conti-nental margin less than 200 meters deep which dip sharply into the deepocean basin with water depths exceeding 1,000 meters. The three wellsdrilled by Amoco, and all the previous seismic exploration done by Amoco,Siebens and Oxoco have been concentrated on the shallow water areas, al-though airmag surveys crossed into deep waters as well. Data availableto the Mission are not adequate enough to evaluate the hydrocarbon po-tential in the Seychelles' exclusive economic zone (EEZ), nor was theMission in the position to evaluate the promotional, technical assistanceand training needs of GOS in the petroleum sector. It is therefore re-commended that a fact-finding petroleum Mission visit the country toevaluate its petroleum potential, the exploration and promotional workdone so far, the scope and extent of further assistance needed, and thepossible sources of such assistance. However, the Mission tentativelybelieves a comprehensive data package is needed on the geology and struc-tural characteristics of the basin around the Seychelles (including thethickness of the sediments in the basin) before any further interest inexploration work can be generated. Preparing and distributing such a

1/ Owen Bank No. 1 (14,302 ft.); Reith Bank No. 1 (8,956 ft.); SeagulShoals No. 1 (12,741 ft.).

- 13 -

report to the oil industry could advance the GOS' interest in attractingmore oil companies and accelerating the exploration program. However, inaddition to the data now held by GOS, this work would require the system-atic evaluation and integration of other airmag, seismic and welldrilling data produced over the past few years. 1/ In the Mission'sview, GOS should not undertake any drilling itself and, indeed, shouldnormally not even carry out geophysical surveys. However, the possibi-lity of some complementary airmag or seimic survey for the promotionalpackage cannot be ruled out completely pending the proposed petroleumMission.

1/ The proposed fact-finding petroleum mission should evaluate in somedetail the components of such a promotion package. However, theMission believes that the package would require the services of ageologist and a geophysicist for several months each, depending onhow much data is actually available with GOS. The package mighttake about six months to prepare and cost about US$300,000 (includ-ing the cost of drafting and printing). In addition, further tech-nical assistance and follow-up work might also be necessary for gen-erating new data.

- 14 -

III. POWER SUBSECTOR REVIEW

Supply/Demand

3.1 The Seychelles Electricity Corporation (SEC) was created in 1980under the Companies Act of 1972. The parastatal SEC was formed from theElectricity Division of the Department of Works. Under the ElectricitySupply Act, the company is empowered to supply electricity to all theislands of Seychelles. However, current supplies of power are limited toMahe and Praslin, which house about 95% of the country's population. Atpresent, 67% of all households are connected to electric powersupplies. The Government hopes to expand this to about 76% by 1986.This expansion would extend the supply of power to about 80% of thehouseholds on Mahe and 60% of the households on Praslin and La Digue andwould require SR 23.3 million (US$3.6 million) in additional investments.

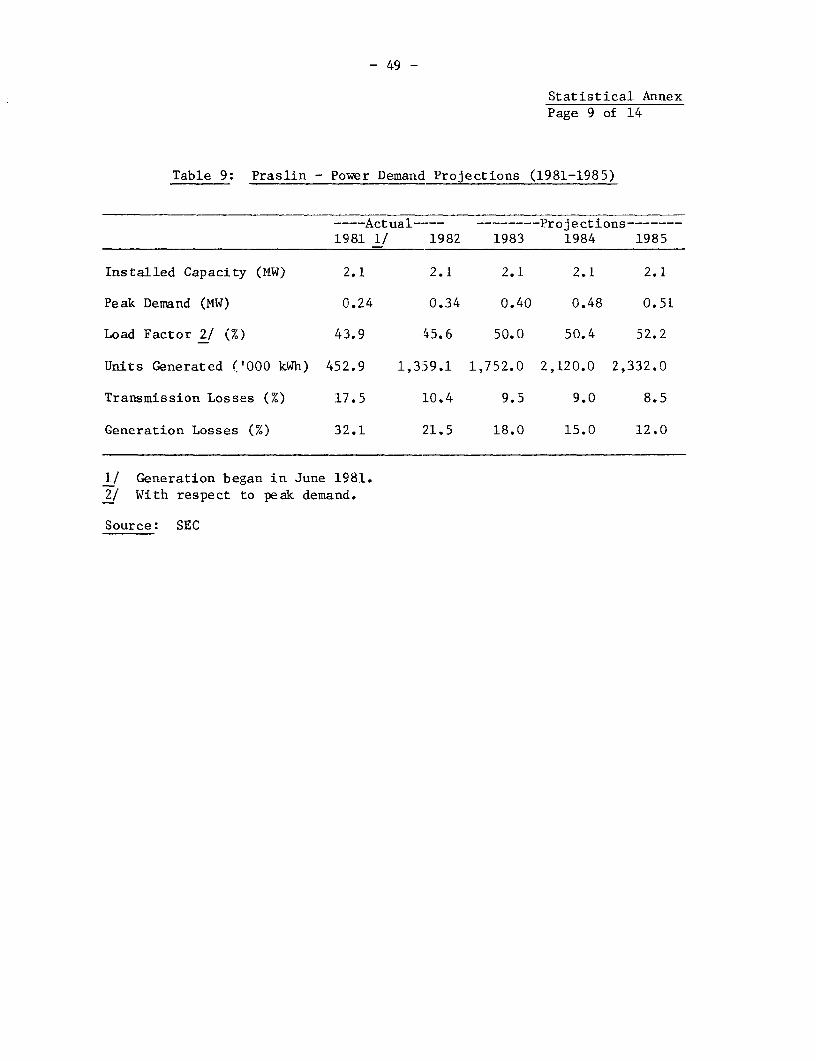

3.2 Mahe has two power stations with a combined installed capacityof 17.4 MW. The firm capacity, however, is only about 9.9 MW, due to thesize and age of units. Peak demand in 1982 was 9.3 MW (Table 3.1) and9.8 MW in 1983. The current firm capacity of 9.0 MW is inadequate tomeet this demand level which is a matter of concern to the SEC and theMission. Peak loads nornally occur during morning and evening hours(10:00-12:00 AM and 7:00-8:00 PM). Mahe has a transmission/distributiongrid along most of its coast, with several cross-country links (IBRD MapNo. 17318). Praslin first received public electricity supply in June,1981 (seven percent of the population lives on this island). Before1981, hotels and other institutions had their own generators which wereunreliable and expensive to operate and maintain. Praslin now has aninstalled capacity of 2.1 MW, which is more reliable. Generation lossesin Praslin are high because of low capacity utilization. However, trans-mission losses are expected to fall below the 1982 level of 10.4% whenpeak demand and load factor increase to 0.51 MW and 52.2% in 1985 (AnnexTable 9). On Mahe, generation and transmission losses can be reduced byinstalling capacitors out in the network. This measure will reduce theextra power generation which is currently needed for high reactive poweron the transmission system. Data on transformer substations in thetransmission/distribution systems of Mahe and Praslin are given in AnnexTable 8.

Table 3.1: SEC - Power Supply/Demand Statistics (1982)

Mahe Praslin

Installed Capacity (MW) 17.4 2.0Peak Demand (MW) 9.3 0.34Load Factor (%) 62.3 45.6Power Generation (GWh) 50.8 1.4Generation Losses (%) 4.3 21.5Transmission Losses (%) 8.2 10.4

Source: SEC

- 15 -

3.3 Electric power sales increased rapidly between 1976 and 1979, at14% p.a. However, the rate declined to 2.0% p.a. after 1979, reflectingthe reversal in economic growth. Table 3.2 shows the breakdown of powersales among domestic, commercial/industrial, and government/street light-ing sectors. The share of sales to the Government and street lightingsectors remained unchanged at 15%, while that of commercial and indus-trial sectors declined marginally from about 55% (1979) to 54% in 1982.This gives an estimated 1.4% p.a. growth in the commercial and industrialsectors. Through SIEP, the SEC should try to encourage electricity con-servation and demand pattern control by educating the consumers and im-posing restrictive peak tariffs.

Table 3.2: SEC - Power Generation and Sales

Average Annual1976 1979 1982 Growth Rate (%)

_GWh %7. GWh GWh x l976-/9 1979-82

Generation 34.5 48.3 52.2 11.9 2.6

Total Sales 28.9 100.0 42.8 100.0 45.4 100.0 14.0 2.0Domestic 8.1 28.0 12.8 30.0 14.1 31.0 16.5 3.3Commerce andIndustry 17.3 59.9 23.5 55.0 24.5 a! 54.0 10.7 1.4

Govt. and StreetLighting 3.5 12.1 6.4 15.0 6.8 a/ 15.0 22.9 2.0

a/ Mission estimates.

Source: SEC

Load Forecast

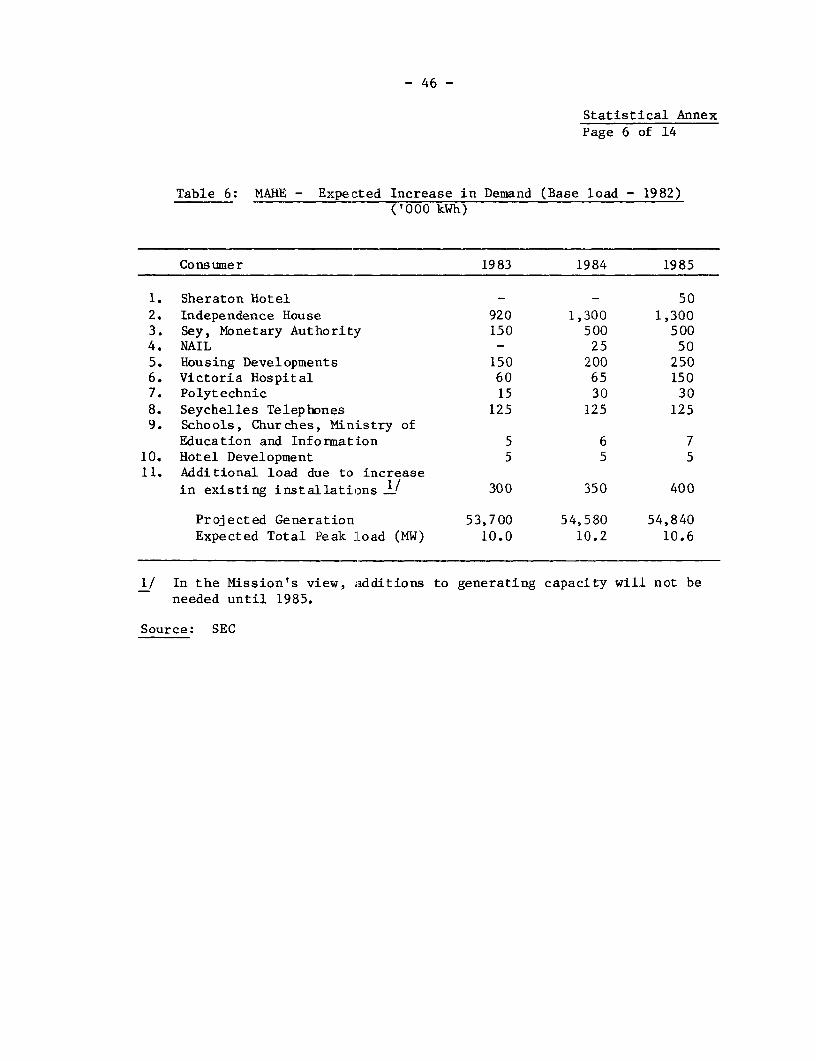

3.4 The Mission prepared power demand forecasts for Mahe up to 1986based on programs currently planned by GOS: (i) to increase tourism tothe 1979 level by 1985/86; (ii) to supply power to about 80% of allhouseholds by 1986; and (iii) to construct various hotels, hospitals,schools, government office buildings etc. (Annex Table 6). The optimis-tic growth scenario assumes that all these objectives will be achieved asplanned, leading to a demand for power generation of 62.1 GWh by 1986(demand growth of 5.5% and 7.0% p.a. for the domestic and commercial andindustrial sectors). However, all these targets may not be met. TheMission projects a base growth scenario demand of 58.3 GWh by the 1986(demand growth of 4.4% and 5.0% p.a. for the domestic and commercial andindustrial sectors). The Mission has based its projections of demandgrowth beyond 1986 on the historical income elasticity of demand for

- 16 -

power of 1.4, 1/ and an annual average load factor of 0.60. 2/ Underthese assumptions, electricity demand on Mahe is projected to increase at4.2% p.a. under the base growth scenario and 5.6% p.a. under the optimis-tic growth scenario (Table 3.3). On Mahe, the SEC plans to install a new5 MW slow speed diesel unit in the next two years and retire all units atStation 'A'. This will only increase the firm capacity to 10 MW, whichis lower than the projected demand of 11.1 MW under the base casescenario (1986). It may be necessary for the SEC to maintain some of theold units at Station 'A' in an operative condition (which are very expen-sive to maintain) to meet any emergency until the system is appropriatelyexpanded. For this the SEC should start preparing a generation expansionplan for the Seventh Unit.

3.5 The current generating capacity of 2.1 MW on Praslin is suffi-cient (Table 3.3) to meet projected power demand up to 1990. For LaDigue, current plans are to supply power by laying a sub-marine powercable (about 9 km) and take power from Praslin. The maximum demand on LaDigue is roughly 100 kW. The cost of cables is estimated at Ff5.1 mil-lion plus the cost of a standby 200 kW diesel unit on La Digue. TheFrench Government is expected to finance this project. In the Mission'sview, this does not appear to be a least cost option and its economicsneed to be carefuly and appropriately evaluated. A better alternativemay be to install an independent diesel generating station on La Digue.A diesel station on La Digue need not effect the environment adversely.The Mission recommends thai: the Government reevaluate the comparativetechnico/economic aspects of the proposal before going ahead with theproject. The most appropriate option for the smaller islands (La Digue,Providence and Long Island) may be to install small generating stationsbased on biomass; this possibility should be evaluated.

Table 3.3: Power Demand Projections (1982-95) a/

M4ahe Praslin, La DigueBase Case Scenario High Growth Scenario and other Islands

MW GWh 14W GWh MW GWh

1982 9.3 50.8 9.3 50.8 0.3 1.41986 11.1 58.3 11.8 62.1 0.6 3.01990 13.1 68.7 14.7 77.2 0.7 3.51995 16.1 84.4 19.3 101.4 0.9 4.5

a/ These projections do not include possible siting of a BBC relaystation in 1987/88 which would require about 2-3 MW of power.

Source: Mission estimates.

1/ Income electricity of power demand may be lowered to 0.8-1.0 ifsolar water heating replaces power use for water heating in thehotels.

2/ Based on load factors of 0.61 for 1983 and 0.59 which SEC is cur-rently using for its 1985 forecast.

- 17 -

3.6 The major power sector issues are: (i) reducing the cost offuel for generation; (ii) the current tariff structure; (iii) SEC'sstaffing which appears to be excessive; and (iv) power supply optionssuch as mini-hydro and biomass technologies.

Fuel Substitution

3.7 Until 1981, all power was generated by diesel engines operatingon light gas oil. In 1982, the power generation equipment was modifiedand fuel oil was used for power generation for the first time on Mahe(2.2 million liters). The cost of modification is estimated at SR 3.5million (US$533,000). The SEC estimates that fuel oil use in 1983 willincrease to 10.8 million liters and gas oil will decline to 3.1 millionliters. In financial terms, this shift is expected to save the SEC aboutSR 4 million (US$611,000) over 1982 purchases of fuel. On an importparity basis, more than US$300,000 p.a. will be saved in foreign exchangecost for fuel imports (1983 prices). The calorific value 1/ of fuel oilis about 10% higher, while its cost 2/ to SEC is about 20% lower thanthat of gas oil; as a result, fuel costs for generation have decreasedfrom about SR 1.0/kWh (US$0.15/kWh) in 1980 to SR 0.715/kWh (US$0.11/kWh)in May 1983. 3/ The net conversion efficiency has increased by 0.5%since 1980, and the payback period for this substitution is less than oneyear (in financial terms). Although fuel oil can be substituted forlight gas oil on Praslin, SEC has no plans to do so before 1985. Thischange could be achieved at an additional cost of SR 440,000 (US$67,200),with estimated fuel savings of about SR 564,300 (US$86,200) 4/ in 1985(in financial terms and in 1982 prices); the payback time would be lessthan one year. The Mission therefore recommends that fuel oil be intro-duced on Praslin when demand reaches the appropriate level.

Power Tariffs

3.8 With the second round of escalations in petroleum prices in1979, the cost of fuel to the SEC increased and the fuel adjustmentclause in the tariffs was invoked. Four fuel cost adjustments were madein 1979 alone, ranging from S¢3.64/kWh (US¢0.58/kWh) to S¢23.94/kWh

1/ Calorific value - Fuel oil: 41,733 KJ/liter; Gas oil: 38,014KJ/liter.

2/ Fuel oil: SR 2,30/liter; Gas oil: SR 2.86/liter.

3/ Costs are based on data supplied by the SEC and GOS.

4/ In 1982 prices; assuming the transport cost of fuel oil to Praslinis SR 0.17/liter (US$4.13/bbl), which is the same as for gas oil.

- 18 -

(US¢3.79/ kWh). As a result, average unit revenues in 1979 increased by20%, and in 1980 by another 68%.

Table 3.4: SEC Average Revenue(1975-1982)

Year SR/kWh sold Percent Increase

1975 0.42 20.01976 0.46 9.51977 0.53 15.21978 0.54 1.91979 0.65 20.41980 1.09 67.71981 1.27 16.51982 1.30 2.4

Annual Average Increase1975-1979 11.51979-1982 26.0

Source: SEC

3.9 Tariffs on Mahe and i?raslin are uniform. Between 1975 and 1979,the average cost of electricity to the consumer increased by 11.5% p.a.which closely followed OPEC price increases in the marker crude oilpostings (11.8% p.a.). Power prices during 1979-82 increased 26% p.a.,compared to a 23.6% increase in the cost of marker crude oil (ArabianLight). It appears, therefore, that the SEC has followed a sound policyof passing the fuel cost increases on to the customers.

3.10 SEC has two tariff categories. Although fuel costs havedeclined for both categories, tariffs have remained unchanged because SEChas informed that its maintenance and other costs have absorbed the sur-pluses generated through the lower cost of fuel. In 1981, the domesticcategory tariffs were a lifeline block of 50 kWh at SR 1.26/kWh(US¢19.24/kWh), subject to a fixed minimum monthly charge of SR 10. Alladditional power to domestic consumers was sold at a marginally higherrate of SR 1.31/kWh (US¢20.0/kWh). The industrial and commercial tariffsare decreasing block-based. The first 500 kWh is sold at SR 1.46/kWh(US¢22.3/kWh), followed by SR 1.31/kWh (US¢20.0/kWh) for the next 500kWh, and the balance at SR 1.26/kWh (US¢19.24/kWh). The current tariffstructure encourages a wide variation between the base load and peak loaddemands. If future investments in new generation capacity are to be de-layed, a suitable tariff struzture should be devised on time-of-day basisto encourage conservation. In restructuring tariffs, both categoriesshould be brought under a demand related change. To do so a tariff study

- 19 -

is needed by the SEC, for which it would need two man-months of assist-ance. The terms of reference for this assistance are shown in Annex II.

Power Supply Options

3.11 The GOS plans to identify and develop alternative power supplyoptions to reduce gas oil- and fuel oil-based power generation. In theMission's view, the options showing the most potential are mini hydro-power schemes and biomass technologies. Based on current end uses ofelectricity, about 16% of the power is used for water heating; thisfunction could be replaced through the use of solar collectors. TheMission recommends that a coal-based thermal generation option also beconsidered for the next expansion of the generation system.

- 20 -

IV. RENEWABLE ENERGY OPTIONS

Introduction

4.1 Biomass, solar and mini-hydro are the promising domestic energyresources. Given the small area and difficult terrain of the graniticgroup of islands, biomass can only play a limited role in the foreseeablefuture. Biomass and other promising renewable energy sources can cer-tainly make an important contribution on the outer islands where theenergy needs are small and scattered. In 1980, the GOS prepared a threephase, twenty-year program for developing energy resources (SIEP - TheSeychelles Integrated Energy Project). Although the program is con-sidered a master plan for deveLoping energy resources on all islands, itsmain focus is on the long-ter-n substitution of renewable energy optionssuch as solar, wind, Ocean Thermal Energy Conversion (OTEC) and biomasstechnologies. Technical assistance for selected parts of this project isbeing provided by several external aid agencies, including the UN Financ-ing System for Science and Technology Development (UNFSSTD), Agence deCooperation Culterelle Technique (ACCT), Commonwealth Science Council(CSC), UK Overseas Development Association (UKODA), and West Germany. Asmost of these renewable energy options would primarily address thescattered energy needs of the outer islands (which are expected to houseno more than 2,000 people over the next decade), the emphasis and priori-ties of SIEP for the Seychelles need to be reviewed and rationalized,taking into account the immediate and short run energy needs of the mainislands. The Mission recommends that technical assistance be provided toreview and restructure the scope of this project and the supportingtechnical assistance.

Biomass Resources and Potential

4.2 In addition to current supplies of domestic fuelwood, there arethree major sources of biomas3 fuels on the main islands: (i) coconutresidues; (ii) cinnamon stemwood; and (iii) sawmill residues and loggingwastes. Other land use categories could produce biomass, but the yieldwould be low or inaccessible. The only available data suggests the maxi-mum potential supplies of biomass to be about 27,000 tonnes or 10,000 toea year.

Coconut Residues

4.3 Coconut plantations cover about 3,500 ha on the main islands, or18% of the total area. About 100 trees/ha are planted, yielding an aver-age annual production of 30 nuts per tree over a lifespan of 30 years.One coconut palm tree contains about 1 m3 of wood, 30% of which could beused for timber and the remaining part for fuel. Coconut shells havealternative applications (copra drying), while the husks are left in thefield and could be available for fuel production, together with stemwood

- 21 -

from replanted coconut plantations. The Mission estimates that with a30-year replantation cycle and the collection of husks and stemwood,about 12,000 tonnes 1/ of biomass a year (4,400 toe) could be made easilyaccessible. This would require a change in the collection system wherebythe whole nut is transported out of the plantations and then the husk isremoved. A large replantation scheme, which would improve productivityby introducing new, faster-growing coconut species, would make largeramounts of stemwood available. The Mission estimates that about 17,500tonnes of stemwood a year could be made available if replantation weredone after 15 years. If gasifier systems prove technically and economi-cally feasible, dependence on imported petroleum for power generation canbe reduced further by using additional coconut residues which are easilyaccessible.

Cinnamon

4.4 Large areas of the national parks 2/ are under cinnamon cover.After felling, leaves and bark are taken out for processing and the stemsare left to rot in the forest. RDU estimates that about 2,000 tonnes ofstemwood (700 toe) could be used as fuel, if collected; in the Mission'sview, cinnamon stemwood is relatively easy to collect from national parkareas. Currently, the cinnamon industry uses offcuts from the sawmill asthe main fuel for drying, and these could be replaced by cinnamon stem-wood. However, before deciding on this, the economics of additionalcosts incurred for collecting and cutting stemwood should be evaluated.

Sawmill Residues and Logging Wastes

4.5 There are no more than about 2,200 ha of managed forest in theSeychelles. Mahe (1,550 ha), Praslin (450 ha) and Curieuse Island (200ha) have their own management plans, but the yearly production is uncer-tain and depends on the market situation. Managed forests are governmentcontrolled, and mainly designed for logging purposes. Logging is costlyand difficult as roads cannot be justified because of the steep slopes,small catchments (varying from 1-10 ha) and low standing volume per ha.Most of the logs are sold to the parastatal Seychelles Timber Company(SEYTIM) which operates the sawmill on Mahe. The capacity of the mill is10,000 m3 a year, but production in 1981 and 1982 was only 1,500 m3 ayear. As the efficiency of the sawmill (ratio of finished product tologs) is about 35%, approximately 1000 m3 or 750 tonnes of sawmillresidues are available for use as fuel.

1/ All biomass is expressed in equivalent tonnes of wood (air dried,20% moisture content).

2/ This land use category covers 3,106 ha on Mahe, 543 ha on Praslinand 283 ha on La Digue.

- 22 -

4.6 If logging residues, currently about 1,500 m3 of branches andtwigs, 1/ were collected, some 1,000 tonnes of biomass could be madeavailablie from forestry operations. However, due to the steep decline inthe charcoal market over the past two years caused by a subsidy on kero-sene (when kerosene was 2-3 times cheaper than charcoal on an energyequivalence basis), its use has been limited. Current offcuts from thesawmill are used in drying cinnamon. If the cinnamon industry can meetits energy requirements from cinnamon stemwood, these offcuts can be usedby the sawmill to meet its own energy needs and export surplus power tothe SEC system. The possibilily of this application should be investi-gated. Expanding current forestry practices significantly by felling oldtrees for fuel production and replanting new, faster growing specieswould be expensive, as present logging, transport and handling costs areabout SR 150-200/tonne (US$22.91-30.55/tonne). Assuming the sawmill isused at 50% capacity, 2/ about 3,300 m3 (2,200 tonnes) of sawmill wastesand 5,000 m3 (2,500 tonnes) of 'Logging residues could be used as fuel forpower generation.

Other Land Use Categories

4.7 The coconut, cinnamon and forest land use categories togethercover about 40% of the area on the granite islands. Estimating the pro-duction capacity of the remaining land (some 12,000 ha) is difficult.Mountains are usually steep and sometimes consist of bare rock or haveonly bush cover. An estimated average biomass production would be onetonne a year per hectare, as agricultural waste is negligible. Totalproduction is estimated at 12,000 tonnes per year. The Mission estimatesthat only about 3,500 tonnes are easily accessible.

Biomass Options

4.8 According to Mission estimates, the current maximum amount ofbiomass available is about 27,000 tonnes a year, equal to some 10,000toe. This assumes, however, that costly and difficult collectionprocedures would be established. The present use of biomass excludingdomestic fuelwood amounts to some 900 toe. No data are available ondomestic fuelwood use, but it is known to be the dominating biomass useon the Seychelles. Based on the development of the kerosene market and aconservative extrapolation from 1977 census data, the Mission estimatesthe current use of fuelwood on Mahe to be not more than 6,000 tonnes ofwood (2,000 toe).

1/ Currently 50% of standing tree volumes.

2/ Considering past trends wien the sawmill was used only up to 30%capacity at most, and likely further economic activity, the sawmillcapacity utilization is not likely to exceed 50% over the nextdecade. Furthermore, Mahe's 1,550 ha of managed forests will not beable to sustain 5,000 m3 of logging for more than a few years.

- 23 -

4.9 Considering the pressing demand for land for non-energy uses(particularly food production), the limited production potential and highcosts of producing biomass, a large-scale substitution of biomass for oilis not likely to occur. However, introducing agroforestry practices onagricultural land is a future possibility, but this would require alarge-scale replantation of the present coconut plantation in order toproduce in sufficient quantities. Viewed from an energy efficiencystandpoint, food and biomass could be advantageously produced together onan agroforesty basis. Using modern agroforestry methods now being de-veloped, producing biomass would conservatively yield 3-5 tonnes per ha ayear; 1/ considering modern agroforestry is adopted on only 50% of the3,500 ha land having coconut plantations at present on the main islands,by 1990 easily accessible biomass for fuel purposes could increase by1,800 toe p.a. to 3,000 toe p.a. Proper land use data is required,however, to determine how to optimize these possible biomass productionsystems. The Mission therefore recommends that land-use expertise beprovided to the GOS to assure that the recently proposed integrated land-use study for the Seychelles takes sufficient account of the needs of theenergy sector.

Table 4.1: Annual Biomass Potential for Main Islands(toe)

Current Potential Projected PotentialCurrently easy access ditticult easy access

Used access

Coconut shells 630husks 1,400stem 3,000 a/ 6,100 b/

Cinnamon 700 1,400 e/Logging wastes 10 g/ 250 900 f/Sawmill residues 250 800 T/Small-scale fuelwood 2,000Managed forests 350 d/ 350 d/Other land use 1,000 T/ 3,200 T/Agroforestry 6,000 c/

a/ According to replantation with 30 years productive lifetime.b/ Assuming a major replantation scheme, available only for a limited number

of years.c/ Based on a 5 tonne/ha yield of biomass for energy on 3,500 ha of land

presently used for coconut.d/ Based on estimates in 4.6 and 4.7.e/ Assuming a doubling of cinnamon production.T/ Assuming that the sawmill is used to 50% capacity; 5,000 m3 /year.g/ Maximum figure charcoal production.

Source: Mission estimates; all figures rounded.

1/ Tests are proposed to establish the feasibility of growing leucaenaor casuarina as an intercrop with coconut to increase biomass yieldson the outer islands.

- 24 -

Other Renewables

4.10 The Research and Development Unit has responsibility for moni-toring several renewable energy projects, the general framework of whichis set by the SIEP. One of the main objectives is to investigate thefeasibility of integrated energy packages using locally available bio-mass, wind and solar energy sources for outer islands. Long-term optionsfor small site-specific renewiable energy sources for the outer islandsare being investigated within Phase I of SIEP, through the New and Renew-able Energy Project (UNDP/81/TOl/A/71/06) and the Biogas Project. Atpresent, only diesel generators are used for power supply on thoseislands.

4.11 Funding for these projects has been provided by the Interim Fundfor Science and Technology for Development (IFSTD), covering work on gas-ifers, solar water heaters, photovoltaic battery chargers and wind-mills. In addition, the project includes the mapping of wind and solarresources, together with planning and training support.

Biomass Technologies

4.12 Tests with producer gas have been going on since 1981. Twounits are located at the RDU Pointe La Rue Test Station, one a movableSwedish design with an output of 30 kVA, the other a 50-kVA German unit.Despite some technical prob]ems, test results with wood and coconutshells have been positive, and results with coconut husks seem quitepromising although still inconclusive. After completing the tests at theRDU station, the Mission recommends that the movable unit be placed on anouter island where the IDC has an active settlement program, and thestationery unit at the Mahe sawmill. This would generate information onday-to-day running and maintenance experience which would be useful inevaluating the viability of the program. Discussions should also be heldwith IDC and the Mahe sawmill to ensure a smooth transition and commit-ment. There are several alternative technologically proven systems forpower production in the 10-50 kW range that use biomass as fuel. Theseinclude steam turbines and reciprocal engines, sterling engines, etc.The Mission recommends that these technologies also be tested by the GOS,with a view to future applications in the Seychelles.

4.13 The possible impact of producer gas on the energy balance forMahe would necessarily be lim:ited because of the high extraction cost ofthe biomass resources. For example, about 6,000 tonnes of wood would berequired each year to provide ten percent (5 GWh) of Mahe's current powerproduction; this corresponds to more than a fivefold increase in forestryoperations or a large scale use of coconut industry residues. However,as the possibilities for outer islands with limited power requirementsand adequate biomass resourcEs are promising, the Mission supports thecurrent producer gas program.

- 25 -

Biogas

4.14 In the Mission's view, biogas can have only limited site-speci-fic applications, such as for cooking on Mahe where most livestock isscattered in small family size holdings. Two pilot biogas units are be-ing tested in Mahe, one large 100 m3 unit at a state farm with some 40cattle, and one smaller 4 m3 unit at a duck farm. The Mission recommendsthat a biogas test unit be installed at two piggeries of 300 pigs onCoetivy. A 5 m3 biogas unit producing about 50 kWh of power per day herewould save an estimated US$12,000 worth of petroleum imports each year,as well as provide additional benefits through better fertilizing andminimal hygienic and fresh water contamination risks.

Solar Crop Drying

4.15 Copra and cinnamon drying are the most promising applications ofsolar drying. However, solar heater designs for these applications havenot been tested. At present, both industries use fuels that are avail-able at no cash charge. 1/ Coconut shells are used in copra drying; incinnamon processing, one factory uses off-cuts from the Mahe sawmill,while a few small farmers use wood. A hybrid system consisting of asolar collector air-preheater and a hot air generator using shells andsawmill off-cuts for heating might be economical and should be investi-gated for application in Seychelles.

Solar Water Heating

4.16 Solar water heating would be an attractive alternative, givenits short payback time and the high cost of producing electricity. About16% of the electricity on Mahe is used for heating water (mainly inhotels and a brewnry). Some hotels also use oil directly for water heat-ing. About 100 m of imported solar water heaters have been installed onMahe; the collector area is distributed roughly equally between some 35private houses 2/ and two hotels. 3/ In the Mission's view, the paybacktime on installing a solar water heater is less than two years. If the

1/ The only costs are incurred in collecting coconut shells or sawmilloff-cuts.

2/ As most households do not have hot water facilities, solar waterheaters would raise the standard of living rather than reduce elec-tricity consumption.

3/ A solar water heating system using two solar collectors which wasinstalled at a cost of SR214,000 in the kitchen and laundry of the104-bed Coral Strand Hotel on Beauvalon Beach (Mahe) in October 1980is claimed to have paid for itself in electricity savings in only10.3 months. This system should be monitored for at least one yearto verify these results.

- 26 -

solar conditions permit (based on the results of ongoing measurements)up to 4,000 m2 of solar ccillectors could be installed at a cost ofUS$600,000 in various hotels within a year to save 4 GWh of gas oil/fueloil-based power. The investors could save a maximum of SR 3 million(US$450,000) in gas oil and fuel oil costs each year. The RDU has re-cently finished developing a domestic design for solar collectors that isbeing evaluated for possible domestic production. Although the cost ofthis unit is claimed to be lower than that of imported units, the limitedsize of the local market and the high costs of establishing adequate pro-duction, maintenance and repair facilities may not justify its localproduction. A decision on local production should, therefore, be care-fully evaluated.

Photovoltaics

4.17 Radio communication systems and several low voltage appliances

such as refrigerators and fluorescent lamps that use photovoltaic powercould be used on the outer islands and scattered settlements which havegood solar insolation patterns. The French are now considering settingup a photovoltaic demonstration unit on Coetivy. The cost of a PV unitwas US$9,000-11,000 per peak kW in 1982; and assuming fuel-oil transportcosts for power generation on the outer islands to be SR 0.40/liter(US$10/bbl) in 1982 prices, fuel costs for fuel oil based power genera-tion would be at least SR 0.7/kWh. However, the Government of Seychellesand IDC should work out the logistics of transporting fuel oil to theouter islands to decide on the cost-effectiveness of PV and other alter-native energy systems. This planning should cover the cost of procuringextra barges or tankers for inter-island fuel oil transport and set-upcosts of storage facilities and generators. This may make PV systemscost effective on some of the outer islands.

Wind

4.18 The limited wind data available suggest that modest wind regimes

exist on Seychelles with average annual speeds of 4-4.5 m/sec. The Is-land Development Company (IDC) has expressed some interest in developingthe wind potential. In the Mission's view, a few applications such asusing wind for water pumping mnay be feasible on outer islands.

4.19 The British Government is financing a project to assess the windenergy potential on the outer islands by mapping their wind regimes. TheBritish Government also is conducting a pilot project to integrate a windturbine generator into the power system of one of the outer islands.Wind speed recording equipment procured from France will be installed onDenis Island to measure wind speeds for one year. The Mission supportsthis program.

Ocean

4.20 Ocean Thermal Energy Conversion (OTEC) No action is planned for

an OTEC system for main island of Mahe, except for oceanographic datacollection which will be done free of charge by Office pour le Recherche

- 27 -

Scientifique et Technique d'Outre Mer (ORSTOM) from France. As Mahe islocated in the middle of a continental shelf, sites suitable for OTEC arenot found closer than 60 km from the shore, where the ocean depth dropsfrom 10-15 m to 1200-1500 m within 3-5 km., and where the ocean tempera-ture drops from 25-30°C on the surface to 4°C at the bottom. In theMission's view, the Government should not take any further action untilthe technical and economic viability of OTEC technology has been proveninternationally. However, integration of energy production and mari-culture activities may be relevant for outer islands because the OTECsites are within 1 km of the outer islands.

Wave/Tidal

4.21 A preliminary assessment of possible wave energy resources onMahe and Praslin was made by Crown Agents (UK) in 1982, but no estimateof generation capacity could be made because wave measurement equipmentwas not installed. The Mission agrees with the Government's view thatwave power and tidal power do not present much potential because waveheights are small, the mean tidal range being only 0.9 m.

Mini-Hydro