Embed Size (px)

Citation preview

Interim Actuarial Valuation Report

of the

NATAL JOINT MUNICIPAL PENSION FUND

(RETIREMENT)

(PF No 12/8/6676/2)

31 March 2016

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 2

CONTENTS

EXECUTIVE SUMMARY 4

INTRODUCTION 8 Previous statutory actuarial valuation report 8 Purpose of the interim actuarial valuation 8 Developments during and subsequent to the valuation period 9 Regulations and amendments 10 Professional guidance 11

FUND STRUCTURE 12

VALUATION INFORMATION 13 Membership data 13 Pensioner data 13 Revenue account 15 Assets per financial statements 16 Investment strategy 16

VALUATION METHOD AND ASSUMPTIONS 18 Valuation method 18 Valuation assumptions 21

VALUATION RESULTS 22 Accrued assets and liabilities 22 Pensioner liabilities 22 Member liabilities 23 Solvency Reserve 23 Risk Reserve 24

CONTRIBUTION RATES 25 Members 25

EXPERIENCE ANALYSIS 27

RECOMMENDATIONS 28 Solvency Reserve 28 Risk Reserve 28 Contribution rates and surcharges 28 Data investigation in respect of suspended pensioners 28

CONCLUSION 29

APPENDICES 30

APPENDIX 1: SUMMARY 30

APPENDIX 2: DATA VERIFICATION 32

APPENDIX 3: VALUATION DATA 33

APPENDIX 4: VALUATION ASSUMPTIONS 40

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 3

APPENDIX 5: VALUATION RESULTS IN TERMS OF PF NOTICE 2 49

APPENDIX 6: EXPERIENCE ANALYSIS 51

APPENDIX 7: LIMITATIONS TO USE OF REPORT 53

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 4

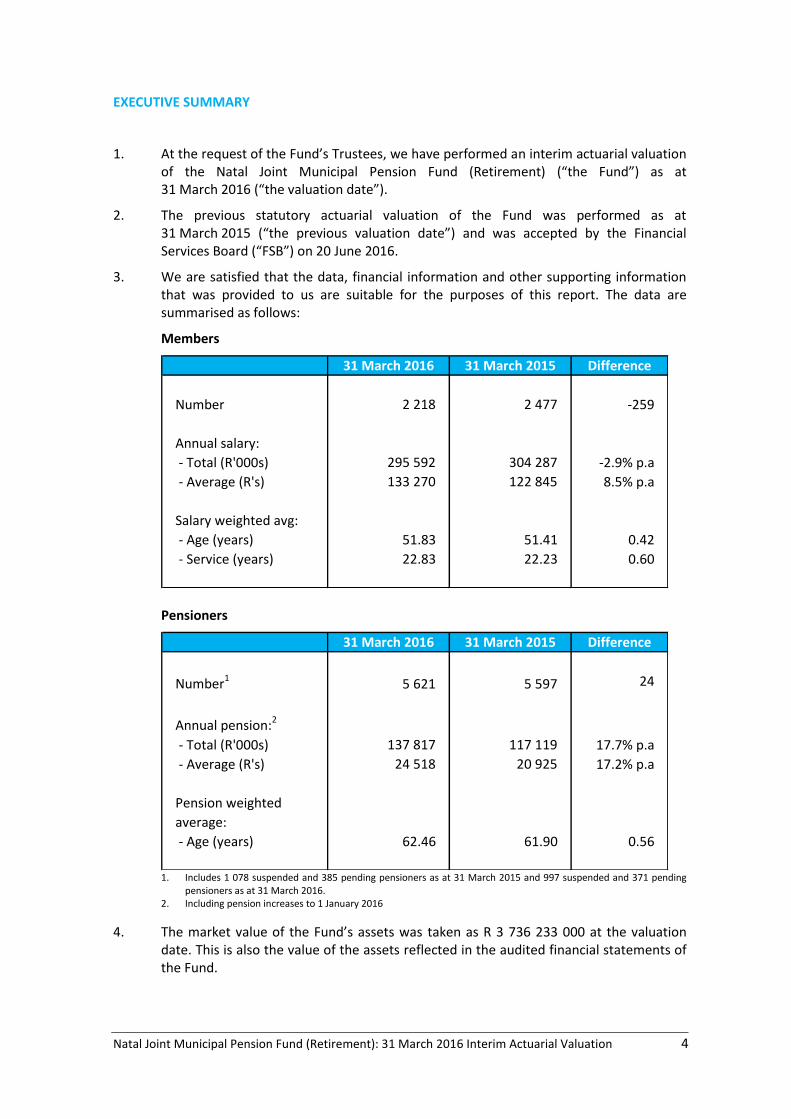

EXECUTIVE SUMMARY

1. At the request of the Fund’s Trustees, we have performed an interim actuarial valuation of the Natal Joint Municipal Pension Fund (Retirement) (“the Fund”) as at 31 March 2016 (“the valuation date”).

2. The previous statutory actuarial valuation of the Fund was performed as at 31 March 2015 (“the previous valuation date”) and was accepted by the Financial Services Board (“FSB”) on 20 June 2016.

3. We are satisfied that the data, financial information and other supporting information that was provided to us are suitable for the purposes of this report. The data are summarised as follows:

Members

31 March 2016 31 March 2015 Difference

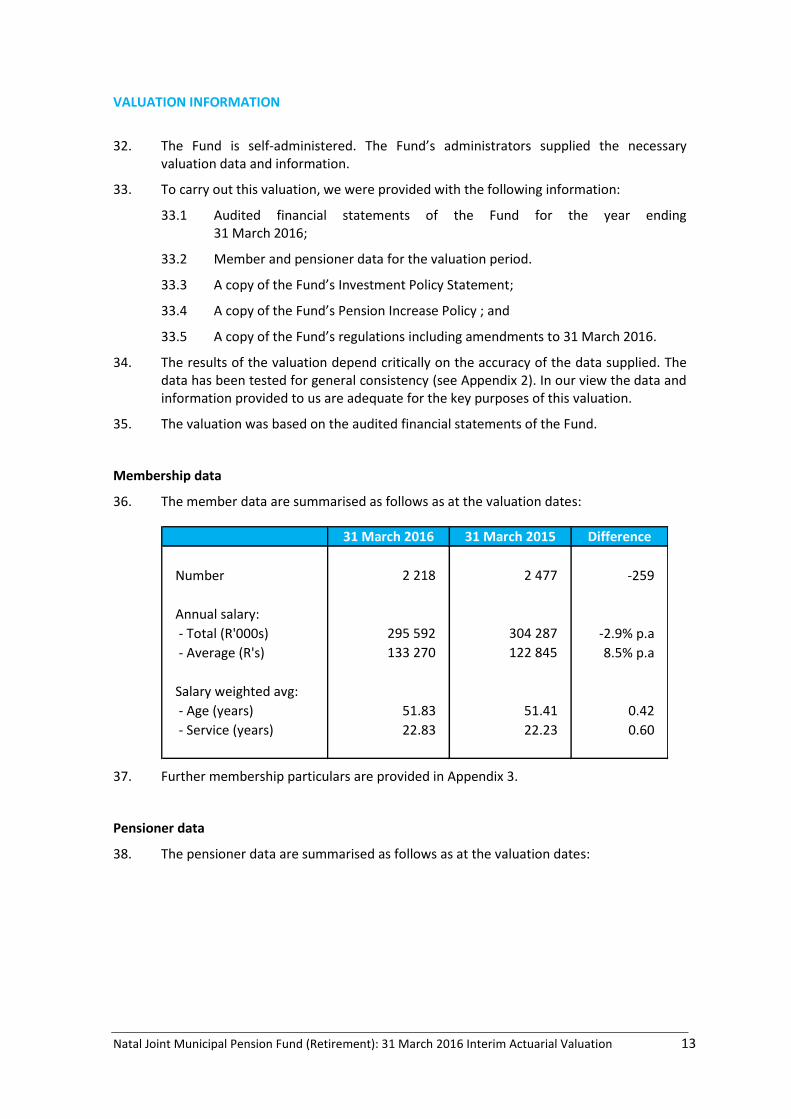

Number 2 218 2 477 -259

Annual salary:

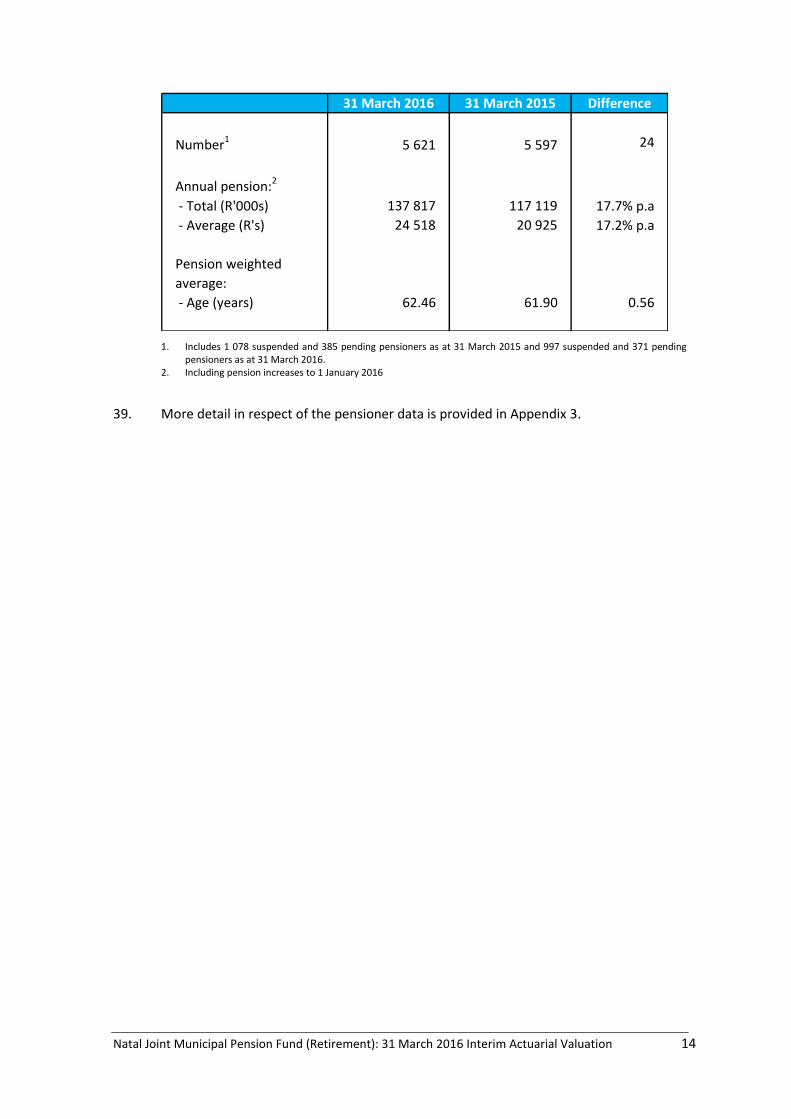

- Total (R'000s) 295 592 304 287 -2.9% p.a

- Average (R's) 133 270 122 845 8.5% p.a

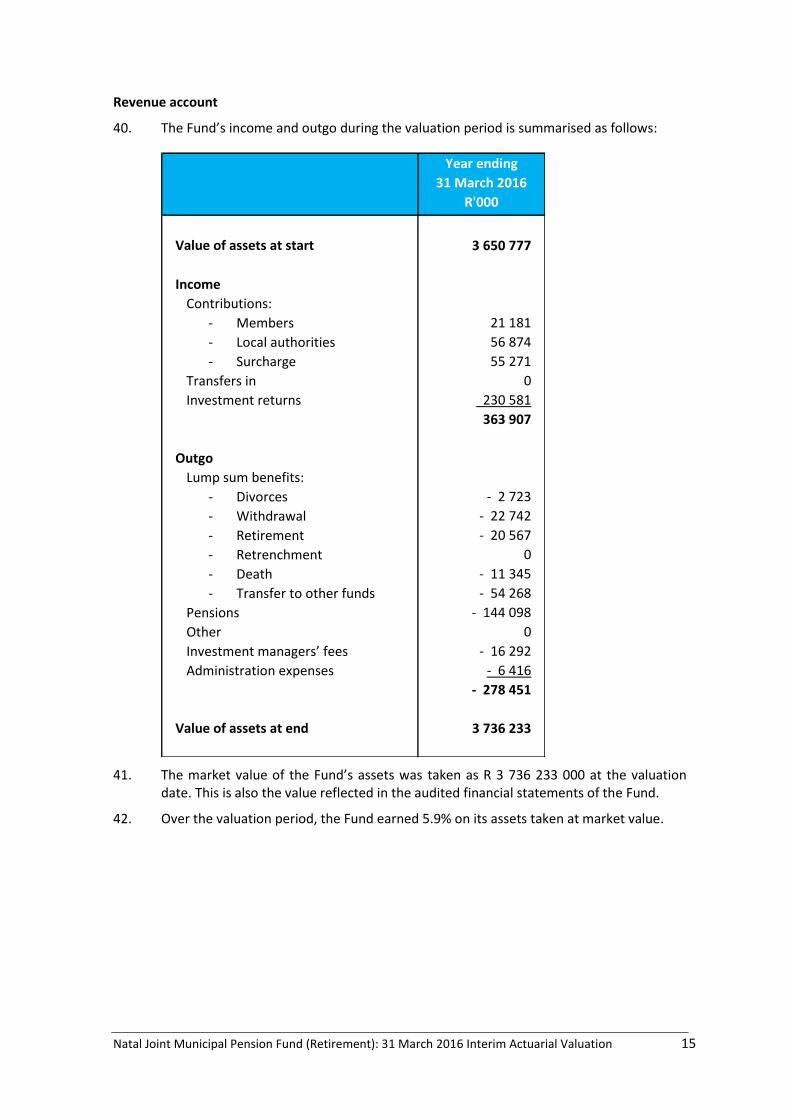

Salary weighted avg:

- Age (years) 51.83 51.41 0.42

- Service (years) 22.83 22.23 0.60

Pensioners

31 March 2016 31 March 2015 Difference

Number1

5 621 5 597 24

Annual pension:2

- Total (R'000s) 137 817 117 119 17.7% p.a

- Average (R's) 24 518 20 925 17.2% p.a

Pension weighted

average:

- Age (years) 62.46 61.90 0.56

1. Includes 1 078 suspended and 385 pending pensioners as at 31 March 2015 and 997 suspended and 371 pending

pensioners as at 31 March 2016. 2. Including pension increases to 1 January 2016

4. The market value of the Fund’s assets was taken as R 3 736 233 000 at the valuation date. This is also the value of the assets reflected in the audited financial statements of the Fund.

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 5

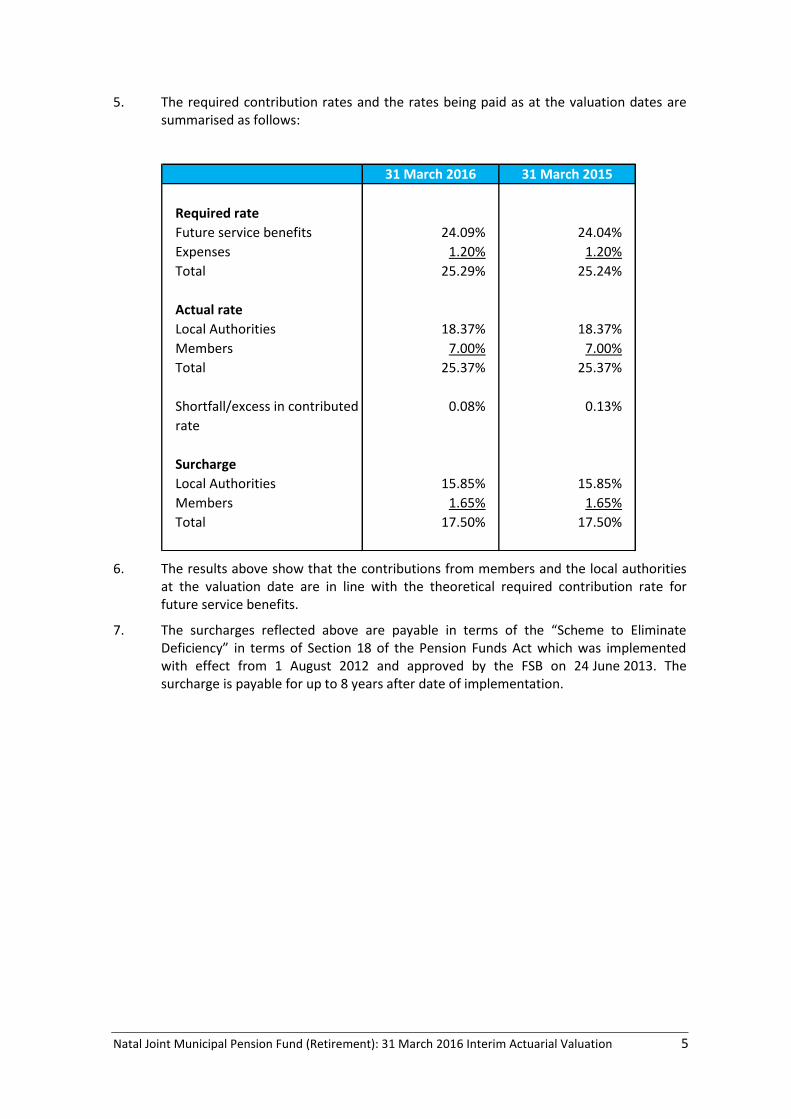

5. The required contribution rates and the rates being paid as at the valuation dates are summarised as follows:

31 March 2016 31 March 2015

Required rate

Future service benefits 24.09% 24.04%

Expenses 1.20% 1.20%

Total 25.29% 25.24%

Actual rate

Local Authorities 18.37% 18.37%

Members 7.00% 7.00%

Total 25.37% 25.37%

Shortfall/excess in contributed

rate

0.08% 0.13%

Surcharge

Local Authorities 15.85% 15.85%

Members 1.65% 1.65%

Total 17.50% 17.50%

6. The results above show that the contributions from members and the local authorities at the valuation date are in line with the theoretical required contribution rate for future service benefits.

7. The surcharges reflected above are payable in terms of the “Scheme to Eliminate Deficiency” in terms of Section 18 of the Pension Funds Act which was implemented with effect from 1 August 2012 and approved by the FSB on 24 June 2013. The surcharge is payable for up to 8 years after date of implementation.

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 6

8. The financial position of the Fund as at the valuation dates is summarised in the following table:

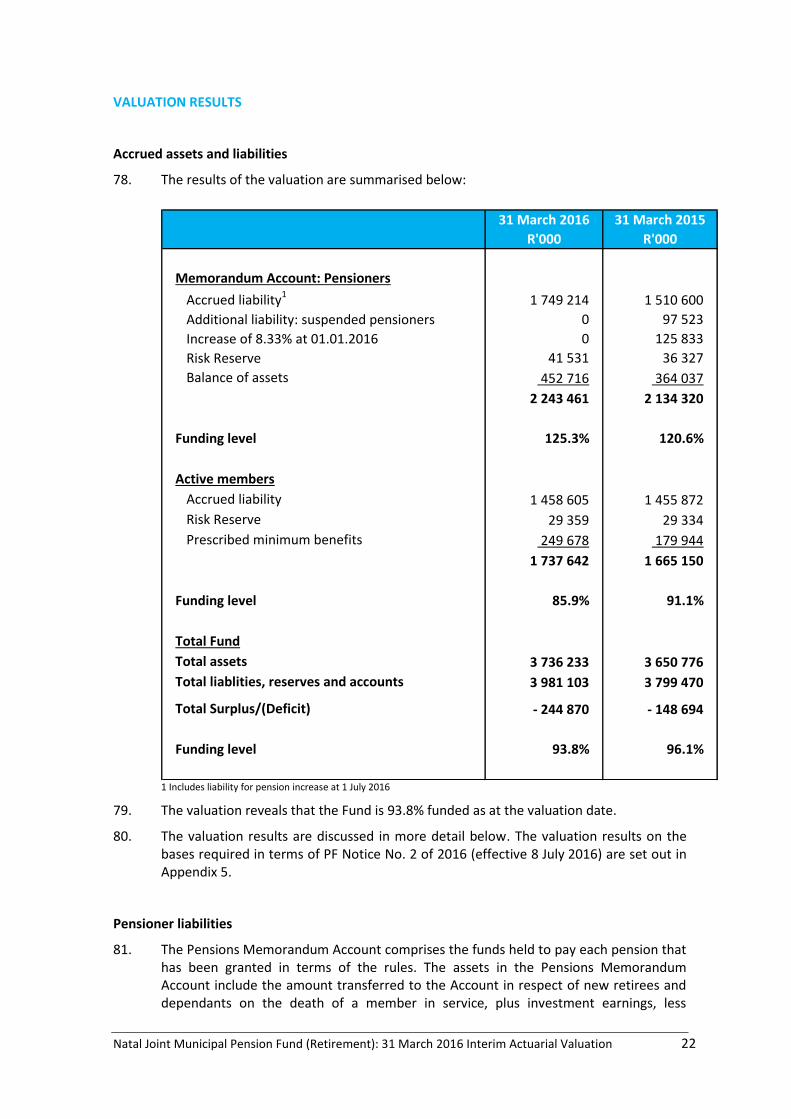

31 March 2016 31 March 2015

R'000 R'000

Memorandum Account: Pensioners

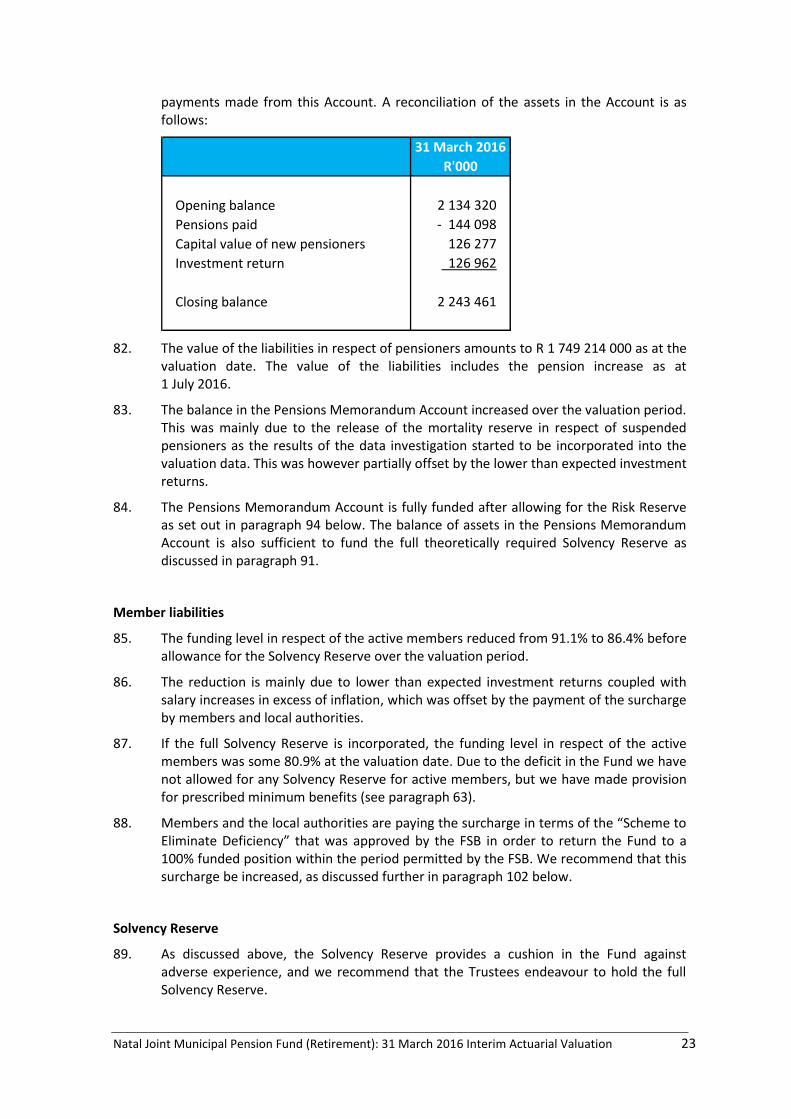

Accrued liability11 749 214 1 510 600

Additional liability: suspended pensioners 0 97 523

Increase of 8.33% at 01.01.2016 0 125 833

Risk Reserve 41 531 36 327

Balance of assets 452 716 364 037

2 243 461 2 134 320

Funding level 125.3% 120.6%

Active members

Accrued liability 1 458 605 1 455 872

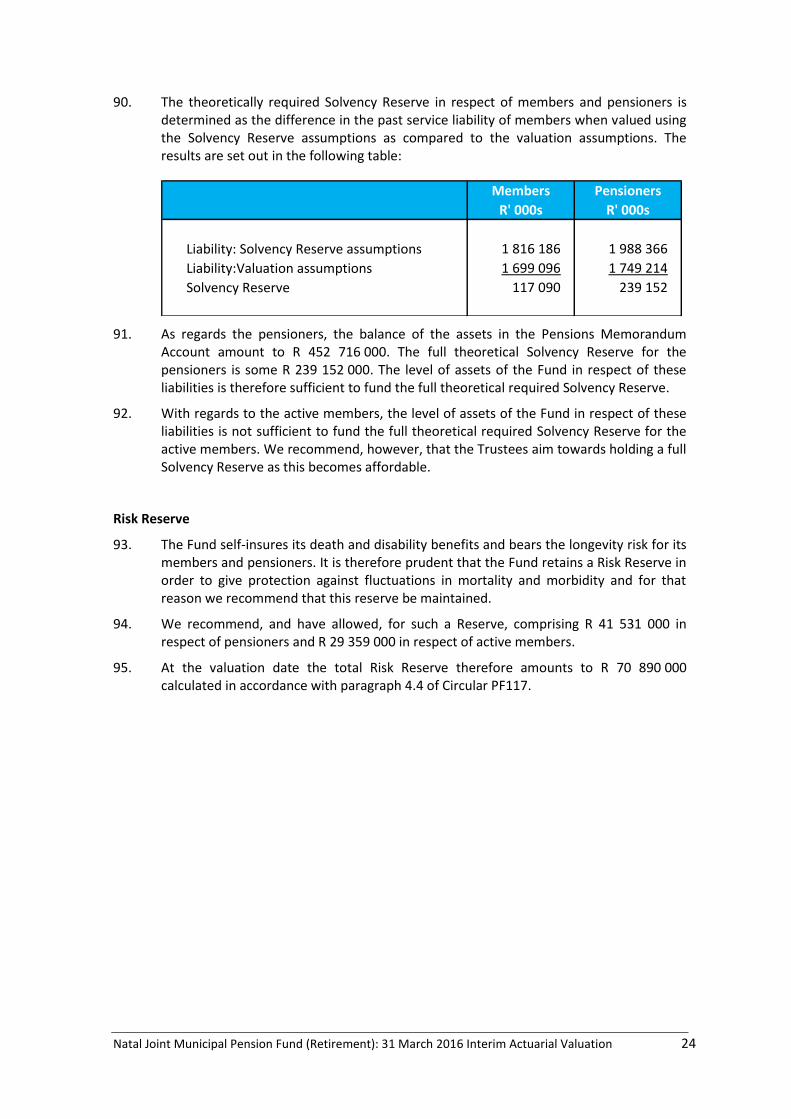

Risk Reserve 29 359 29 334

Prescribed minimum benefits 249 678 179 944

1 737 642 1 665 150

Funding level 85.9% 91.1%

Total Fund

Total assets 3 736 233 3 650 776

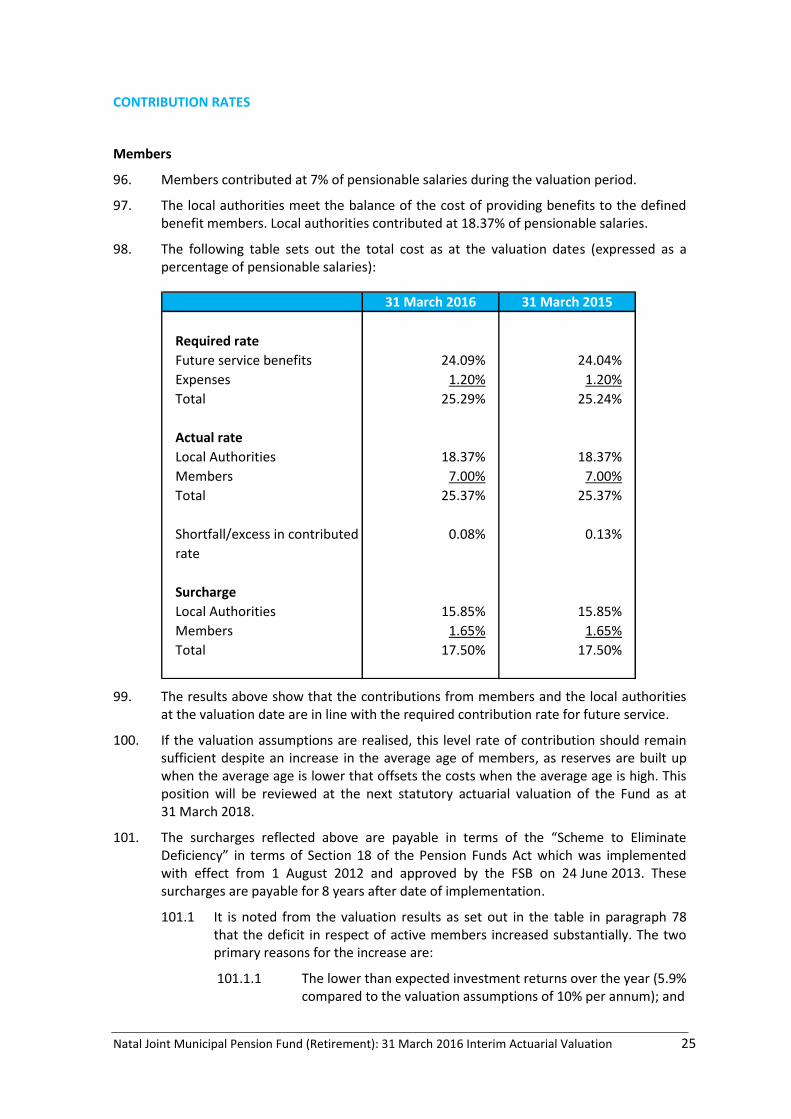

Total liablities, reserves and accounts 3 981 103 3 799 470

Total Surplus/(Deficit) - 244 870 - 148 694

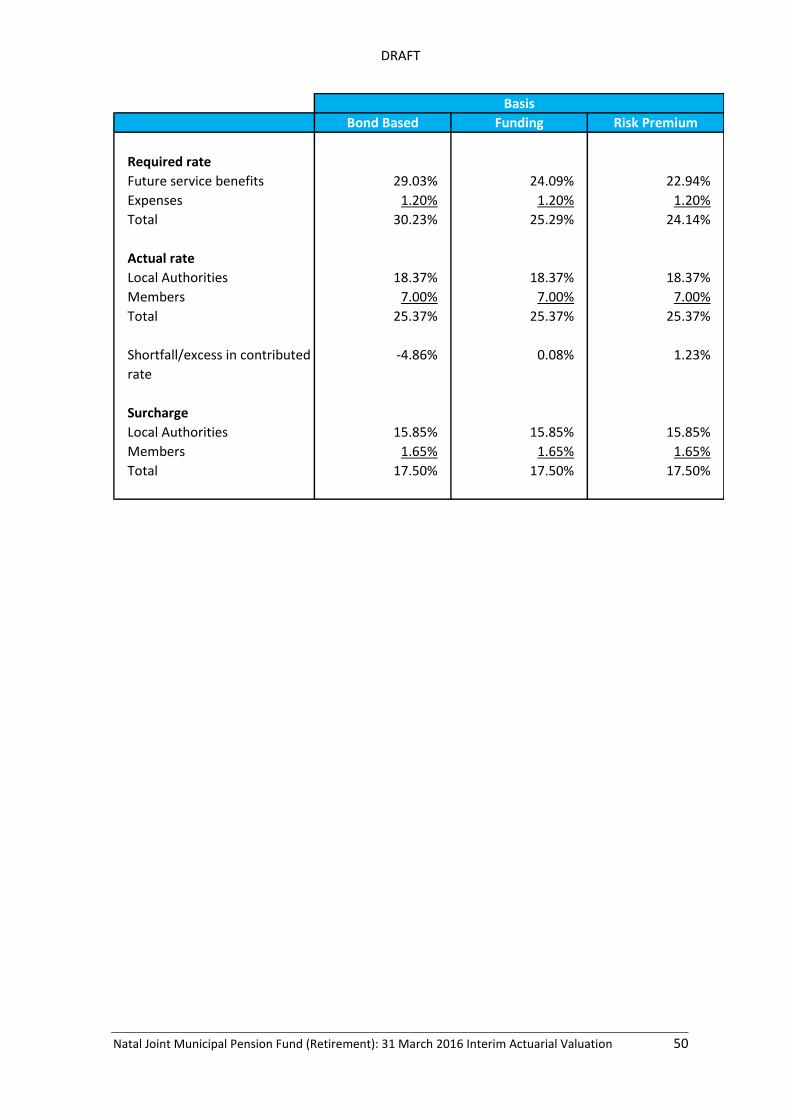

Funding level 93.8% 96.1%

1 Includes liability for pension increase at 1 July 2016 after the valuation date

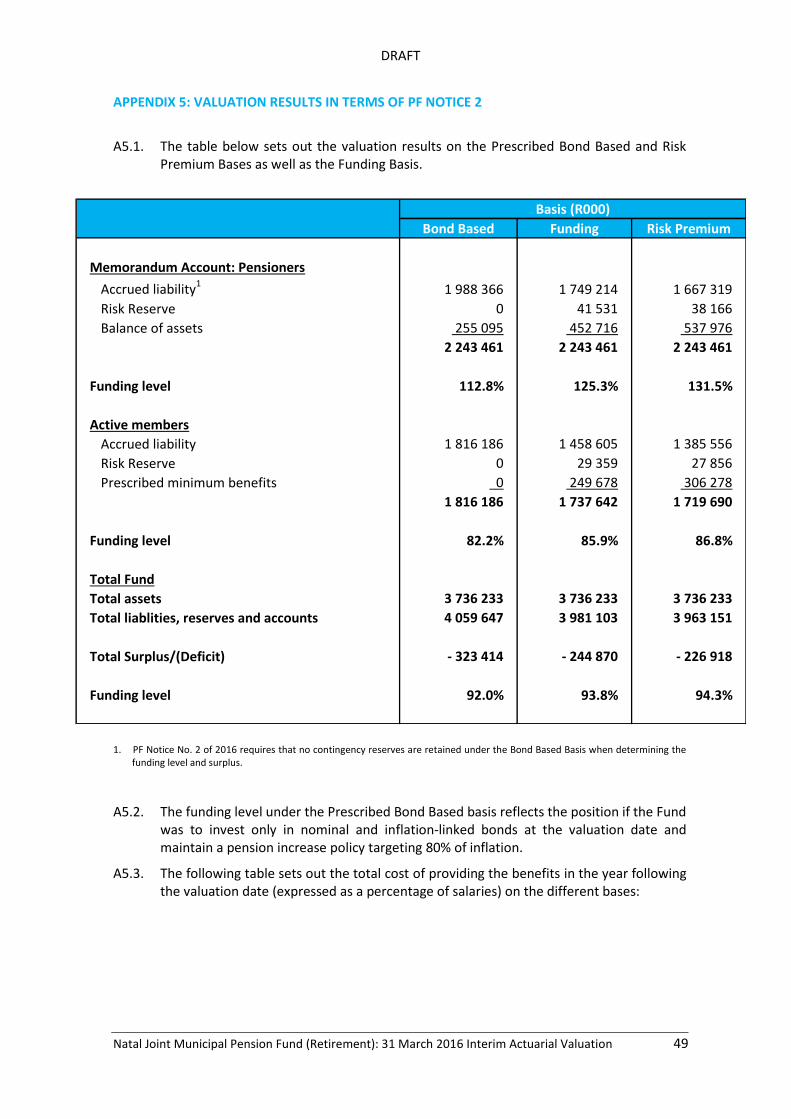

9. The valuation results on the bases required in terms of PF Notice No. 2 of 2016 (effective 8 July 2016) are set out in Appendix 5.

10. It is noted from the above table that the deficit in respect of active members increased substantially. The two primary reasons for the increase are:

10.1 The lower than expected investment returns over the year (5.9% compared to the valuation assumptions of 10% per annum); and

10.2 The salary increases which were significantly above inflation (9.4% compared to valuation assumptions of 7% plus a promotional scale).

11. The surcharge at the current level of 17.5% of pensionable salaries is not sufficient to eliminate the deficit within the time span permitted by the FSB (see paragraph 7). We therefore recommend that the surcharge being paid by the local authorities be increased from 15.85% to 20% of pensionable salaries as set out in paragraph 12.2 below.

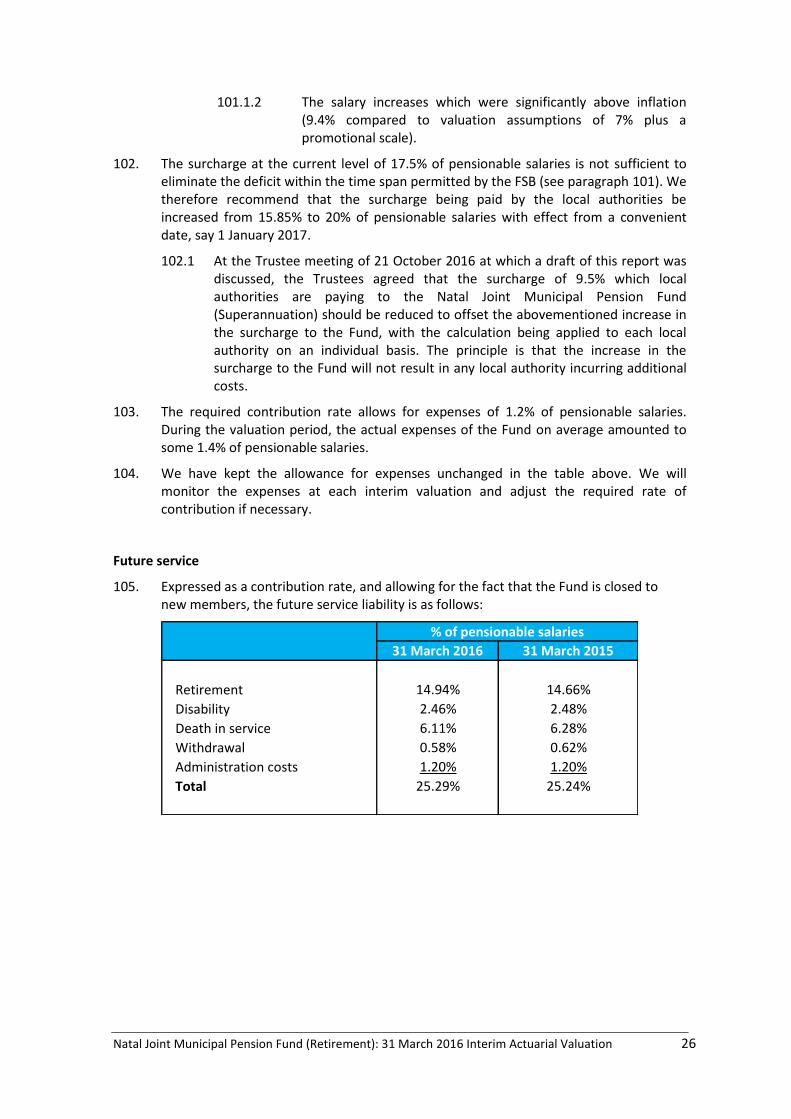

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 7

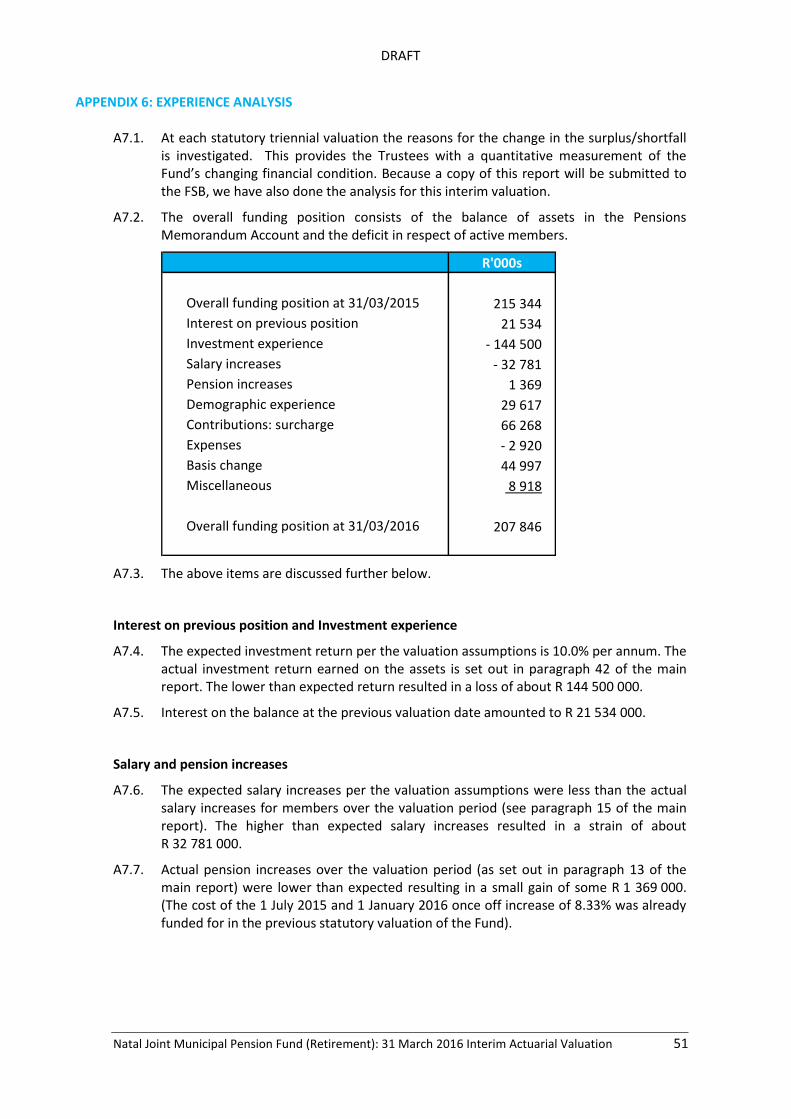

12. The key findings and recommendations in the report are:

12.1 The valuation reveals that the Fund is 93.8% funded on the “best estimate” Funding basis as at the valuation date, and also not fully funded on the other bases as set out in PF Notice No. 2 of 2016.

12.2 We recommend that the current surcharge of 17.5% of pensionable salaries that is being paid in terms of the “Scheme to Eliminate Deficiency” in order to eliminate the deficit be increased with effect from a convenient date, say 1 January 2017; the portion being paid by the local authorities should be increased from 15.85% to 20% of pensionable salaries, so that the total surcharge increases from 17.5% to 21.65% of pensionable salaries. This should be done in conjunction with the steps discussed in paragraph 102.1 of the main report.

12.3 We recommend that, as soon as the deficit in the Fund is eliminated, the Trustees investigate the possibility of increasing the benefits to align with those of the Superannuation Fund.

12.4 The Fund self-insures its risk benefits. The lump sum element of these benefits is relatively small, with the major element comprising of annuity payments. We are satisfied that, given the recommended Risk Reserve, the Fund’s reinsurance arrangements are appropriate.

12.5 We are satisfied that the asset composition on the valuation date is appropriate to the nature of the liabilities and that the investment strategy of the Fund is suitable for the Fund.

13. In our view the Fund is not in a sound financial position as at the valuation date but the deficit is being funded by the surcharge that is being paid. Based on the increase in the surcharge that is recommended above, we expect the deficit to be eliminated within the period allowed in the “Scheme to Eliminate Deficiency”.

______________ __________ ______________ __________

ARTHUR ELS (FASSA FIA CFP® CFA CERA) RIA VAN DER MERWE (FASSA FIA) VALUATOR ACTUARY

In my capacity as an employee of In my capacity as an employee of ARGEN Actuarial Solutions ARGEN Actuarial Solutions Our primary professional regulator is the Actuarial Society of South Africa October 2016

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 8

INTRODUCTION

1. At the request of the Fund’s Trustees, we have performed an interim actuarial valuation of the Natal Joint Municipal Pension Fund (Retirement) (“the Fund”) as at 31 March 2016 (“the valuation date”).

2. This report is addressed to the Fund’s Trustees. Any other party placing any reliance on this report is encouraged to firstly consult with the Trustees and ourselves.

3. The previous statutory actuarial valuation of the Fund was performed as at 31 March 2015 (“the previous valuation date”) and was accepted by the Financial Services Board (“FSB”) on 20 June 2016.

4. The one year period between the valuation dates is referred to as the “valuation period”.

5. The Fund is registered in terms of the Pension Funds Act and approved by the South African Revenue Services for Income Tax purposes.

6. This report has been peer reviewed by an independent Consulting Actuary, Mr Jeremy Andrew, and his feedback has been taken into account.

Previous statutory actuarial valuation report

7. The 31 March 2015 statutory actuarial valuation report made the following recommendations:

7.1 That the surcharge of 17.5% of pensionable salaries continues to be paid;

7.2 That a Risk Reserve be maintained for both active and pensioner liabilities and that a Solvency Reserve be maintained for pensioner liabilities; and

7.3 That pensioners receive the prescribed minimum pension increase as set out in the Act as well as a once-off increase of 8.33% at 1 January 2016 in respect of their 13th pension cheque benefit expectation.

8. The above recommendations were accepted by the Fund’s Trustees and implemented.

Purpose of the interim actuarial valuation

9. The purpose of this interim actuarial valuation is:

9.1 To assess whether the existing assets of the Fund are sufficient to cover the Fund’s accrued liabilities towards its members for service prior to the valuation date, and towards its pensioners;

9.2 To analyse the change in the financial position of the Fund during the valuation period;

9.3 To determine the contribution rate that is required in order to fund the future benefits of the members;

9.4 To review the requirement for the contingency reserve accounts and assess whether these accounts are appropriately funded and to review the build up thereof;

9.5 To assess whether the Fund’s reinsurance arrangements are appropriate;

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 9

9.6 To assess whether the nature of the assets of the Fund is suitable to match the nature of the liabilities of the Fund and whether the investment strategy is appropriate;

9.7 To determine whether the targeted pension increase is sustainable and the likelihood of it being realized; and

9.8 To recommend an appropriate contribution rate to amortise any deficit.

10. This report is an interim actuarial valuation report and as such a copy of this report does not have to be submitted to the Registrar of Pension Funds. However, in terms of the “Scheme to Eliminate Deficiency” the Registrar must be furnished with all interim valuation reports performed for the Fund, and hence a copy of this report will be submitted to the Registrar’s office.

Developments during and subsequent to the valuation period

11. The Trustees revised the Pension Increase Policy effective from 1 September 2013 and specifically included a provision to pay a 13th pension cheque in November of each year subject to affordability. The Pension Increase Policy is summarised as follows:

11.1 Pension increases are granted at 1 July each year. Pensions in payment for less than 1 year at the previous 1 March receive a pro-rata increase;

11.2 The Pension Increase Policy targets pension increases of at least 75% of the annual Headline Inflation averaged over the previous calendar year. The policy gives the Trustees discretion to grant increases up to 100% of the average annual Headline Inflation subject to affordability. In exceptional circumstances, and if affordable, the Trustees may grant increases in excess of the average annual Headline Inflation;

11.3 The Trustees may, on the advice of the actuary, grant a 13th pension cheque to each pensioner in November of each year subject to affordability from the assets in the Pensions Memorandum Account; and

11.4 The Pension Increase Policy will be reviewed at least every three years coinciding with the Fund’s statutory valuation. Any change in the policy will be communicated to pensioners.

12. The Trustees granted a 13th pension cheque to pensioners in November of 2015.

12.1 The 13th pension cheque was introduced to align benefits between the Fund and the Natal Joint Municipal Pension Fund (Superannuation) (“Superannuation Fund”) where this benefit has been paid annually for a number of years so that it has become an expectation of the pensioners in that fund. Pensioners in the Fund therefore have an expectation that the 13th pension cheque will be paid in the same manner as in the Superannuation Fund. However, the amount that is transferred to the Pensions Memorandum Account in respect of a new retiree does not include the cost of the 13th pension cheque, yet those pensioners also receive a 13th pension cheque to the possible detriment of the other pensioners.

12.2 In order to address this situation, the Trustees resolved that current pensioners were to receive a special once-off pension increase of 8.33% with effect from 1 January 2016. This addressed the expectation of current pensioners since they will still receive a 13th pension cheque but in monthly instalments.

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 10

12.3 A 13th pension cheque could continue to be considered in the future from time to time, but only if it can be afforded out of that year’s investment earnings and subject to the Pensions Memorandum Account being financially sound. It is thus expected that a 13th pension cheque will be granted only infrequently in future. This revision of the pension increase policy was made with effect from 1 April 2016 and has been communicated to pensioners subsequently.

13. The following pension increases were granted since the previous statutory valuation:

Date Pension Increase

CPI for year to

31 March

Average CPI for year

to previous 31 Dec

1 July 20152 6.07% 4.0% 6.07%

1 January 20161 8.33%

1 July 20163 4.68% 6.3% 4.58%

1. Special once off increase (refer paragraph 12) 2. Included in the liabilities for the previous statutory valuation 3. Average CPI rounded to be divisible by 12

14. The mortality investigation for female pensioners in the previous statutory valuation of the Fund showed a much lighter than expected mortality if compared with the previous statutory valuation assumptions and also if compared to the assumptions used for other large retirement funds in South Africa. This was not a true reflection of the mortality experience but rather a function of deaths that have not been reported (as can be seen from the large number of suspended pensioners over the valuation period). Following the statutory valuation, a detailed investigation has been performed by the Fund which resulted in a large number of deaths being identified and the number of suspended pensioners being decreased. At the effective date of this valuation the exercise had not yet been completed and hence the valuation still shows a fairly large number of suspended pensioners in the valuation data. Significant progress has however been made by the administrator with the help of tracing agents following the valuation date. The full effect of the investigation will be shown in the next interim valuation of the Fund at 31 March 2017.

15. The average salary increase per annum for members over the valuation period was some 9.4% per annum.

16. The investment return on the assets of the Fund amounted to some 5.9% per annum over the valuation period.

17. Members contributed at 7% of pensionable salaries during the valuation period. Local authorities contributed at 18.37%.

18. A total surcharge of 17.5% of pensionable salaries was paid. Of the surcharge, 1.65% of pensionable salaries is paid by members who joined the Fund prior to 1 July 2002.

Regulations and amendments

19. There have been no changes to the Regulations of the Fund since the previous valuation.

20. The Fund is governed by Regulations that are both promulgated by the provincial authorities and registered by the FSB. The provincial authorities have obliged the Fund to undertake a “Rationalisation of Regulations” project. The Rationalisation project is in

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 11

its final stages and it is expected that the revised Regulations will be submitted for promulgation and registration within twelve months of the valuation date.

21. As part of the rationalisation project, it has been proposed that several benefits provided by the Fund be improved; the cost of such improvements has not been taken into account in the results of this valuation since the possible improvements are still under discussion.

22. The key benefits and conditions set out in the regulations are summarised in Appendix 1.

23. PF Notice No.2 of 2016 was issued by the FSB effective 8 July 2016. This notice deals with actuarial valuation assumptions and financial soundness. Appendices 4 and 5 contain more detail in this regard.

Professional guidance

24. This report adheres to the Standard of Actuarial Practice SAP201 of the Actuarial Society of South Africa and the relevant Board Notices issued by the Financial Services Board.

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 12

FUND STRUCTURE

25. The Fund is governed by its regulations as approved by the Registrar of Pension Funds and promulgated by the provincial legislature of Kwa-Zulu Natal.

26. The Fund is a pension fund and its members and pensioners are entitled to benefits of a defined benefit nature.

27. The Fund is closed to new entrants. Members of the other Natal Joint funds are, however, allowed to transfer into the Fund subject to certain conditions.

28. The benefits and members’ contributions are fixed. The local authorities are responsible for making contributions towards the Fund that meet the balance of the cost of providing the promised benefits.

29. Retiring members receive their pension benefits from the Fund.

30. The Fund’s regulations allow for the Fund to hold a Solvency Reserve, Risk Reserve, Contribution Reserve, Investment Reserve and Data Reserve Account.

31. The assets and liabilities in respect of pensioners are notionally separated in a Pensions Memorandum Account.

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 13

VALUATION INFORMATION

32. The Fund is self-administered. The Fund’s administrators supplied the necessary valuation data and information.

33. To carry out this valuation, we were provided with the following information:

33.1 Audited financial statements of the Fund for the year ending 31 March 2016;

33.2 Member and pensioner data for the valuation period.

33.3 A copy of the Fund’s Investment Policy Statement;

33.4 A copy of the Fund’s Pension Increase Policy ; and

33.5 A copy of the Fund’s regulations including amendments to 31 March 2016.

34. The results of the valuation depend critically on the accuracy of the data supplied. The data has been tested for general consistency (see Appendix 2). In our view the data and information provided to us are adequate for the key purposes of this valuation.

35. The valuation was based on the audited financial statements of the Fund.

Membership data

36. The member data are summarised as follows as at the valuation dates:

31 March 2016 31 March 2015 Difference

Number 2 218 2 477 -259

Annual salary:

- Total (R'000s) 295 592 304 287 -2.9% p.a

- Average (R's) 133 270 122 845 8.5% p.a

Salary weighted avg:

- Age (years) 51.83 51.41 0.42

- Service (years) 22.83 22.23 0.60

37. Further membership particulars are provided in Appendix 3.

Pensioner data

38. The pensioner data are summarised as follows as at the valuation dates:

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 14

31 March 2016 31 March 2015 Difference

Number1 5 621 5 597 24

Annual pension:2

- Total (R'000s) 137 817 117 119 17.7% p.a

- Average (R's) 24 518 20 925 17.2% p.a

Pension weighted

average:

- Age (years) 62.46 61.90 0.56

1. Includes 1 078 suspended and 385 pending pensioners as at 31 March 2015 and 997 suspended and 371 pending

pensioners as at 31 March 2016. 2. Including pension increases to 1 January 2016

39. More detail in respect of the pensioner data is provided in Appendix 3.

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 15

Revenue account

40. The Fund’s income and outgo during the valuation period is summarised as follows:

Value of assets at start 3 650 777

Income

Contributions:

- Members 21 181

- Local authorities 56 874

- Surcharge 55 271

Transfers in 0

Investment returns 230 581

363 907

Outgo

Lump sum benefits:

- Divorces - 2 723

- Withdrawal - 22 742

- Retirement - 20 567

- Retrenchment 0

- Death - 11 345

- Transfer to other funds - 54 268

Pensions - 144 098

Other 0

Investment managers’ fees - 16 292

Administration expenses - 6 416

- 278 451

Value of assets at end 3 736 233

Year ending

31 March 2016

R'000

41. The market value of the Fund’s assets was taken as R 3 736 233 000 at the valuation date. This is also the value reflected in the audited financial statements of the Fund.

42. Over the valuation period, the Fund earned 5.9% on its assets taken at market value.

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 16

Assets per financial statements

43. The assets of the Fund, as set out in the audited financial statements, are summarised in the following table:

Investment 31 March 2016

R'000 %

31 March 2015

R'000 %

Local investments:

- Equities 1 542 516 41.3% 1 688 336 46.2%

- Bonds 893 492 23.9% 891 636 24.4%

- Property 189 386 5.1% 168 773 4.6%

- Cash 179 063 4.8% 120 060 3.3%

- Other1

46 532 1.2% 24 595 0.7%

2 850 988 76.3% 2 893 400 79.2%

Foreign investments:

- Cash 23 781 0.6% 7 520 0.2%

- Equities 961 838 25.7% 847 596 23.2%

- Property 1 081 0.0% 209 0.0%

- Bonds 1 010 0.1% 1 154 0.1%

987 710 26.4% 856 479 23.5%

Total investments 3 838 698 102.7% 3 749 879 102.7%

Net current assets - 102 464 -2.7% - 99 103 -2.7%

Total assets 3 736 234 100.0% 3 650 776 100.0%

1 Consist mainly of commodities

Investment strategy

44. The Fund has a detailed investment strategy which takes into account the results of the asset liability modelling exercise as at 30 September 2012 that was completed in March 2013. The Fund’s strategic asset allocation in terms of this exercise is set out below. The strategic allocation is the structure that is suitable for the liabilities, taking a long term view. Another asset liability modelling exercise will be performed following this valuation and the results are expected to be presented to the Trustees in early 2017.

Strategic

Asset allocation

Local Equities 45.0%

Foreign Equities 20.0%

Cash 3.0%

Fixed interest bonds 22.0%

Property 10.0%

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 17

45. The investment strategy of the Fund targets an investment return of Headline Inflation plus 5% over any rolling 5 year period.

46. The results of the asset liability modelling exercise were used to determine the strategic benchmarks of the Fund as well as the ranges around the benchmarks. The actual asset allocation at valuation date is within the permissible ranges, as set out in the investment mandates given to the Fund’s asset managers.

47. In our view the investment strategy is appropriate for a pension fund such as the Fund.

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 18

VALUATION METHOD AND ASSUMPTIONS 48. In order to value the Fund’s liabilities an actuarial valuation method and valuation

assumptions are required.

Valuation method

49. The valuation method consists of a past service component (service up to the valuation date) and a future service component (service after the valuation date).

Past service

50. The Fund’s liabilities for members’ service to the valuation date and for pensioners was calculated using set of “best estimate” assumptions which are expected to apply over the long-term. Allowance was made for expected salary increases until normal retirement date and pension increases thereafter. The benefits payable by the Fund in future are estimated and these are discounted using the assumed long-term rate of interest, to give the present value of their liabilities for service to the valuation date. A similar approach is taken for pensions in payment. We have also allowed for an administration fee of R 36.75 per month in respect of each pension payable.

51. The Pension Funds Act requires a fund to provide a minimum level of pension increases. In order to meet this requirement, the Fund notionally holds assets that are directly attributable to its pensioners and deferred pensioners, in the Pensions Memorandum Account. Where the value of the pensioner assets exceeds the value of the pensioner liabilities, the excess assets are retained in the Pensions Memorandum Account.

52. We have been provided with information in respect of 997 pensioners whose pensions have been suspended because the Fund has not received proof of existence. These pensions were valued on the assumption that the following proportion of the pensions would again become payable:

Period since payments ceased Proportion

more than 3 years 0

between 2 and 3 years 1/6

between 1 and 2 years 1/2

less than 1 year 5/6

53. The Trustees should also note the outcome of the mortality investigation for female pensioners in the previous statutory valuation as well as the results of the subsequent data investigation as detailed in paragraph 14 resulting in unchanged mortality assumptions from the previous statutory valuation and a release of the mortality reserve as detailed in paragraph 83.

54. We have been provided with details of 371 cases where a spouse’s pension is possibly payable following the death of a member in the service or of a pensioner. The Fund is taking steps to trace dependants of the deceased members and pensioners and it is likely that, in a number of cases, no pension will become payable. For the valuation it was decided to include in the liabilities 50% of the calculated value, so that an amount of R 25 419 000 has been included in the members’ liabilities and R 1 445 000 in the

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 19

pensioner liabilities in respect of spouses of pensioners. This matter will again be investigated following the results of the data investigation referred to above.

Future service

55. The local authorities no longer permit members to join the Fund, so that it has effectively become a closed fund. This implies that the average age of the membership will increase, which in turn will mean an increase in the required rate of contribution. For this and the last statutory valuation the rate of contribution was determined on the “Attained Age” method. This method takes into account the closed nature of the Fund. It projects the expected benefits payable in each future year based solely on service that the member is expected to complete after the valuation date. The projection makes allowance for demographic decrements and for expected future salary increases. The projected values are then discounted at the assumed investment return in order to obtain the present value of the future service liability as at the valuation date.

If the valuation assumptions are realised, this level rate of contribution should remain sufficient despite an increase in the average age of members as reserves are built up when the average age is lower, that offsets the costs when the average age is high. This assumption may not be realised if there are significant unforeseen changes in the membership, for example, if a significant number of members transfer between the Fund and the other Natal Joint funds such is currently the case.

56. There is no future service cost in respect of the pensioners or deferred pensioners.

Solvency Reserve

57. The assumptions used for the above calculations are “best estimate” assumptions of future experience. The Pension Funds Act, and the Fund’s regulations, permit the Fund to maintain a Solvency Reserve in order to provide some protection to the Fund should the actual future financial experience of the Fund turn out to be less favourable than the “best estimate” financial assumptions used to value the defined benefit member and pensioner liabilities.

58. To determine the Solvency Reserve, the same valuation method as set out in paragraphs 50 to 54 above is used, but the financial assumptions are based on the prevailing risk free rates of interest (see paragraph 71 below). Any resulting increase in the past service liability is held as a Solvency Reserve.

59. Legislation does not oblige a fund to hold a Solvency Reserve for purposes of financial soundness. However, being financially sound only on the “best estimate” basis means that there is still a 50% chance of the Fund being in deficit in the future. We thus strongly recommend that, once the deficit is eliminated, the Fund holds a Solvency Reserve in order to provide protection for the interests of the various stakeholders if affordable. For this purpose we have applied the provisions of PF 117, the Circular issued by the Financial Services Board setting out the level of solvency reserves that the Financial Services Board considers reasonable as well as the guidelines set out in PF Notice No. 2 of 2016.

Risk Reserve

60. The Fund self-insures its death and disability benefits and bears the longevity risk for its pensioners. It is prudent to maintain a “Risk Reserve” in order to give some protection

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 20

against fluctuations in mortality and morbidity experience of the members, and against the longevity risk of pensioners.

61. The Financial Services Board’s Circular PF117 sets out a standard for determining such a reserve. A fund may hold a “Risk Reserve” based on the capital that would be required from an insurance company undertaking the business. In the case of the Fund, the Risk Reserve has been determined in accordance with paragraph 4.4 of Circular PF117.

Minimum Benefits

62. The Act prescribes minimum benefits to a member who leaves the Fund other than on retirement or death. For each member the actuarial reserve was compared to the value of the minimum benefit that would become payable at each future date, if the member resigned from the service at that date. Where the latter figure exceeded the actuarial reserve, the difference was added to the liabilities of the Fund. The assumptions underlying the calculation of the prescribed minimum benefits are set out in Appendix 4 (paragraph A4.36 to A4.38).

63. Additionally, the total actuarial reserve for each member at the valuation date was compared with the value of the prescribed minimum benefit at the valuation date based on the Earnings Yield published by the FSB at the valuation date, i.e. taking into account market conditions at the valuation date. The additional liability is R 249 678 000. It is noted that members may elect to transfer out of the Fund to one of the other Natal Joint Funds or an external fund; it is established practice that the transfer amount may not be less than the prescribed minimum benefit in order to ensure that members are not prejudiced. It was therefore decided to include the latter figure in the liabilities for this valuation.

64. It would be prudent to include the amount in a Solvency Reserve but the Fund does not have sufficient assets to do so at the valuation date.

65. The Fund has prepared a “Scheme to Eliminate Deficiency” in terms of Section 18 of the Pension Funds Act that aims to eliminate the deficit in the previous statutory actuarial valuation by 2020 or earlier. This scheme was approved by the FSB. Members who exited the Fund during the valuation period received the full value of their benefits set out in the regulations, subject to a minimum of the prescribed minimum benefit.

66. The Pension Funds Act prescribes minimum increases to pensioners. The Act requires the valuator to investigate the pension increases granted to pensioners every three years. The actual increases granted since retirement must be compared to the increase in the Consumer Price Index (CPI) and any shortfall must be credited to the pensioners as an additional increase if affordable. The last comparison in this regard was done as at 31 March 2015. The next investigation in this regard will be performed as part of the statutory actuarial valuation of the Fund at 31 March 2018.

Sensitivity Analysis

67. The Fund’s financial position is sensitive to the key assumptions made in the valuation. The key assumptions are the investment return, salary increase rate and pensioner mortality. All these elements are beyond the direct control of the Fund. A sensitivity analysis is performed at each statutory valuation of the Fund to show the impact of changes in each of these key assumptions on the Fund’s financial position.

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 21

Valuation assumptions

68. The valuation assumptions used to determine the Fund’s past and future service liabilities are determined in line with the requirements for a Funding Basis as set out in the FSB’s PF Notice No. 2 of 2016 and are consistent with the “best estimate” assumptions set out in Circular PF 117. The key financial assumptions for the Funding Basis are:

68.1 Investment returns of 10.0% per annum;

68.2 Price inflation of 6.0% per annum;

68.3 Salary increases of 7.0% per annum, plus a promotional salary scale; and

68.4 Allowance for future pension increases equal to investment returns in excess of 5.0% per annum which is consistent with the Fund’s Pension Increase Policy.

69. These assumptions were also used in the previous statutory valuation.

70. The demographic assumptions are set out in Appendix 4. .

71. In order to determine the Solvency Reserve, financial assumptions have been determined on a basis consistent with the Financial Services Board’s Circular PF 117. The key financial assumptions are:

71.1 Investment returns of 10.15% per annum;

71.2 Price inflation of 7.78% per annum;

71.3 Salary increases of 8.78% per annum, plus a promotional salary scale; and

71.4 Allowance for future pension increases equal to investment returns in excess of 3.75% per annum;

72. The demographic assumptions used to determine the Solvency Reserve are the same as those used to value the liabilities on the “best estimate” assumptions.

73. The Funding valuation assumptions and Solvency Reserve assumptions are discussed in greater detail in Appendix 4. Appendix 4 also includes the derivation of the Prescribed Bond Based and Prescribed Risk Premium bases.

74. The valuation results based on the Prescribed Bond Based and Prescribed Risk Premium bases are shown in Appendix 5.

75. The cost of the benefits provided by the Fund will depend on the actual financial and demographic experience of the Fund, and not on the valuation assumptions which determine the speed at which assets are accumulated in the Fund. The valuation method and assumptions have no direct bearing on the ultimate cost of the defined benefits; they only determine how this cost is recognised and funded over time.

Assets

76. The market value of the Fund’s assets was R 3 736 233 000 at the valuation date. For purposes of the valuation, we have taken the assets at market value.

77. This method of placing a value on the assets of the Fund, together with the Solvency Reserve set out above, is consistent with the long term method of placing a value on the liabilities of the Fund.

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 22

VALUATION RESULTS

Accrued assets and liabilities

78. The results of the valuation are summarised below:

31 March 2016 31 March 2015

R'000 R'000

Memorandum Account: Pensioners

Accrued liability11 749 214 1 510 600

Additional liability: suspended pensioners 0 97 523

Increase of 8.33% at 01.01.2016 0 125 833

Risk Reserve 41 531 36 327

Balance of assets 452 716 364 037

2 243 461 2 134 320

Funding level 125.3% 120.6%

Active members

Accrued liability 1 458 605 1 455 872

Risk Reserve 29 359 29 334

Prescribed minimum benefits 249 678 179 944

1 737 642 1 665 150

Funding level 85.9% 91.1%

Total Fund

Total assets 3 736 233 3 650 776

Total liablities, reserves and accounts 3 981 103 3 799 470

Total Surplus/(Deficit) - 244 870 - 148 694

Funding level 93.8% 96.1%

1 Includes liability for pension increase at 1 July 2016

79. The valuation reveals that the Fund is 93.8% funded as at the valuation date.

80. The valuation results are discussed in more detail below. The valuation results on the bases required in terms of PF Notice No. 2 of 2016 (effective 8 July 2016) are set out in Appendix 5.

Pensioner liabilities

81. The Pensions Memorandum Account comprises the funds held to pay each pension that has been granted in terms of the rules. The assets in the Pensions Memorandum Account include the amount transferred to the Account in respect of new retirees and dependants on the death of a member in service, plus investment earnings, less

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 23

payments made from this Account. A reconciliation of the assets in the Account is as follows:

31 March 2016

R'000

Opening balance 2 134 320

Pensions paid - 144 098

Capital value of new pensioners 126 277

Investment return 126 962

Closing balance 2 243 461

82. The value of the liabilities in respect of pensioners amounts to R 1 749 214 000 as at the valuation date. The value of the liabilities includes the pension increase as at 1 July 2016.

83. The balance in the Pensions Memorandum Account increased over the valuation period. This was mainly due to the release of the mortality reserve in respect of suspended pensioners as the results of the data investigation started to be incorporated into the valuation data. This was however partially offset by the lower than expected investment returns.

84. The Pensions Memorandum Account is fully funded after allowing for the Risk Reserve as set out in paragraph 94 below. The balance of assets in the Pensions Memorandum Account is also sufficient to fund the full theoretically required Solvency Reserve as discussed in paragraph 91.

Member liabilities

85. The funding level in respect of the active members reduced from 91.1% to 86.4% before allowance for the Solvency Reserve over the valuation period.

86. The reduction is mainly due to lower than expected investment returns coupled with salary increases in excess of inflation, which was offset by the payment of the surcharge by members and local authorities.

87. If the full Solvency Reserve is incorporated, the funding level in respect of the active members was some 80.9% at the valuation date. Due to the deficit in the Fund we have not allowed for any Solvency Reserve for active members, but we have made provision for prescribed minimum benefits (see paragraph 63).

88. Members and the local authorities are paying the surcharge in terms of the “Scheme to Eliminate Deficiency” that was approved by the FSB in order to return the Fund to a 100% funded position within the period permitted by the FSB. We recommend that this surcharge be increased, as discussed further in paragraph 102 below.

Solvency Reserve

89. As discussed above, the Solvency Reserve provides a cushion in the Fund against adverse experience, and we recommend that the Trustees endeavour to hold the full Solvency Reserve.

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 24

90. The theoretically required Solvency Reserve in respect of members and pensioners is determined as the difference in the past service liability of members when valued using the Solvency Reserve assumptions as compared to the valuation assumptions. The results are set out in the following table:

Members Pensioners

R' 000s R' 000s

Liability: Solvency Reserve assumptions 1 816 186 1 988 366

Liability:Valuation assumptions 1 699 096 1 749 214

Solvency Reserve 117 090 239 152

91. As regards the pensioners, the balance of the assets in the Pensions Memorandum Account amount to R 452 716 000. The full theoretical Solvency Reserve for the pensioners is some R 239 152 000. The level of assets of the Fund in respect of these liabilities is therefore sufficient to fund the full theoretical required Solvency Reserve.

92. With regards to the active members, the level of assets of the Fund in respect of these liabilities is not sufficient to fund the full theoretical required Solvency Reserve for the active members. We recommend, however, that the Trustees aim towards holding a full Solvency Reserve as this becomes affordable.

Risk Reserve

93. The Fund self-insures its death and disability benefits and bears the longevity risk for its members and pensioners. It is therefore prudent that the Fund retains a Risk Reserve in order to give protection against fluctuations in mortality and morbidity and for that reason we recommend that this reserve be maintained.

94. We recommend, and have allowed, for such a Reserve, comprising R 41 531 000 in respect of pensioners and R 29 359 000 in respect of active members.

95. At the valuation date the total Risk Reserve therefore amounts to R 70 890 000 calculated in accordance with paragraph 4.4 of Circular PF117.

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 25

CONTRIBUTION RATES

Members

96. Members contributed at 7% of pensionable salaries during the valuation period.

97. The local authorities meet the balance of the cost of providing benefits to the defined benefit members. Local authorities contributed at 18.37% of pensionable salaries.

98. The following table sets out the total cost as at the valuation dates (expressed as a percentage of pensionable salaries):

31 March 2016 31 March 2015

Required rate

Future service benefits 24.09% 24.04%

Expenses 1.20% 1.20%

Total 25.29% 25.24%

Actual rate

Local Authorities 18.37% 18.37%

Members 7.00% 7.00%

Total 25.37% 25.37%

Shortfall/excess in contributed

rate

0.08% 0.13%

Surcharge

Local Authorities 15.85% 15.85%

Members 1.65% 1.65%

Total 17.50% 17.50%

99. The results above show that the contributions from members and the local authorities at the valuation date are in line with the required contribution rate for future service.

100. If the valuation assumptions are realised, this level rate of contribution should remain sufficient despite an increase in the average age of members, as reserves are built up when the average age is lower that offsets the costs when the average age is high. This position will be reviewed at the next statutory actuarial valuation of the Fund as at 31 March 2018.

101. The surcharges reflected above are payable in terms of the “Scheme to Eliminate Deficiency” in terms of Section 18 of the Pension Funds Act which was implemented with effect from 1 August 2012 and approved by the FSB on 24 June 2013. These surcharges are payable for 8 years after date of implementation.

101.1 It is noted from the valuation results as set out in the table in paragraph 78 that the deficit in respect of active members increased substantially. The two primary reasons for the increase are:

101.1.1 The lower than expected investment returns over the year (5.9% compared to the valuation assumptions of 10% per annum); and

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 26

101.1.2 The salary increases which were significantly above inflation (9.4% compared to valuation assumptions of 7% plus a promotional scale).

102. The surcharge at the current level of 17.5% of pensionable salaries is not sufficient to eliminate the deficit within the time span permitted by the FSB (see paragraph 101). We therefore recommend that the surcharge being paid by the local authorities be increased from 15.85% to 20% of pensionable salaries with effect from a convenient date, say 1 January 2017.

102.1 At the Trustee meeting of 21 October 2016 at which a draft of this report was discussed, the Trustees agreed that the surcharge of 9.5% which local authorities are paying to the Natal Joint Municipal Pension Fund (Superannuation) should be reduced to offset the abovementioned increase in the surcharge to the Fund, with the calculation being applied to each local authority on an individual basis. The principle is that the increase in the surcharge to the Fund will not result in any local authority incurring additional costs.

103. The required contribution rate allows for expenses of 1.2% of pensionable salaries. During the valuation period, the actual expenses of the Fund on average amounted to some 1.4% of pensionable salaries.

104. We have kept the allowance for expenses unchanged in the table above. We will monitor the expenses at each interim valuation and adjust the required rate of contribution if necessary.

Future service

105. Expressed as a contribution rate, and allowing for the fact that the Fund is closed to new members, the future service liability is as follows:

31 March 2016 31 March 2015

Retirement 14.94% 14.66%

Disability 2.46% 2.48%

Death in service 6.11% 6.28%

Withdrawal 0.58% 0.62%

Administration costs 1.20% 1.20%

Total 25.29% 25.24%

% of pensionable salaries

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 27

EXPERIENCE ANALYSIS

106. At each statutory triennial valuation the reasons for the change in the surplus/shortfall are investigated. No such analysis is usually performed for an interim valuation, but because this report is to be submitted to the FSB, we have included the analysis in Appendix 6. This provides the Trustees with a quantitative measurement of the Fund’s changing financial condition.

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 28

RECOMMENDATIONS

Solvency Reserve

107. The balance of assets in the Pensions Memorandum Account is used to fund the Solvency Reserve in respect of pensioners as well as towards future pension increases.

108. We recommend, in line with good practice, that the Trustees aim to build up the Solvency Reserve in respect of active member liabilities to the full theoretical level as soon as affordable (see paragraph 90).

Risk Reserve

109. We recommend that a Risk Reserve of R 70 890 000 be retained in line with PF117 (see paragraph 94).

Contribution rates and surcharges

110. The contributions from members and the local authorities at the valuation date are in line with the required contribution rate for future service. We recommend that the current rate continue to be paid until the next statutory valuation of the Fund at 31 March 2018 at which time the position will be reviewed.

111. Members and the local authorities are paying a surcharge of 17.5% of pensionable salaries in terms of the “Scheme to Eliminate Deficiency” that was approved by the FSB; however the surcharge is insufficient to return the Fund to a 100% funded position within the period permitted by the FSB. We therefore recommend that the portion of the surcharge that is paid by the local authorities be increased from 15.85% to 20% of pensionable salaries with effect from a convenient date, say 1 January 2017. This will result in the total surcharge being increased from 17.5% to 21.65% of pensionable salaries (also refer to paragraph 102.1).

112. We recommend that, as soon as the deficit in the Fund is eliminated, the Trustees investigate the possibility of increasing the benefits to align with those of the Superannuation Fund.

Data investigation in respect of suspended pensioners

113. We recommend that the administrator finalise the investigation that is currently being carried out into the suspended pensioner records to validate and remove records where a pension is no longer payable before the next financial year end of the Fund and that the exercise be continued on an annual basis thereafter.

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 29

CONCLUSION

114. We have performed an interim actuarial valuation of the Fund as at 31 March 2016. Our recommendations are summarised in paragraphs 107 to 113.

115. The valuation reveals that the Fund is 93.8% funded on the “best estimate” basis as at the valuation date, and also not fully funded on the other bases as set out in PF Notice No. 2 of 2016.

116. We are satisfied that the asset composition on the valuation date is appropriate to the nature of the liabilities and that the investment strategy of the Fund is suitable for the Fund.

117. The Fund self-insures its risk benefits. The lump sum element of these benefits is relatively small, with the major element comprising of annuity payments. We are satisfied that, given the recommended Risk Reserve, the Fund’s reinsurance arrangements are appropriate.

118. In our view the Fund is not in a sound financial position as at the valuation date but the deficit is being funded by the surcharge that is being paid. Based on the increase in the surcharge that is recommended above, we expect the deficit to be eliminated within the period allowed in the “Scheme to Eliminate Deficiency”.

______________ __________ ______________ __________

ARTHUR ELS (FASSA FIA CFP® CFA CERA) RIA VAN DER MERWE (FASSA FIA) VALUATOR ACTUARY

In my capacity as an employee of In my capacity as an employee of ARGEN Actuarial Solutions ARGEN Actuarial Solutions Our primary professional regulator is the Actuarial Society of South Africa October 2016

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 30

APPENDICES

APPENDIX 1: SUMMARY

A1.1. The key benefits and conditions of the Fund are summarised below. Importantly, this is

only a summary of the Fund’s regulations and in the event of any dispute the registered regulations will be the sole point of reference.

Definitions

Final Average Salary

A1.2. The average pensionable salary during the last year prior to retirement.

Pension age

A1.3. The pension age is 65 years for all members

Normal retirement benefits

A1.4. At the pension age a member is entitled to:

A pension equal to 2.1% of final average salary for each year of continuous service; plus

A gratuity equal to 5.5% of final average pensionable salaries per year of continuous service.

Early retirement benefits

A1.5. Members may retire up to seven years prior to the pension age. The same pension and gratuity as on normal retirement applies reduced in line with the tables in the regulations for each year of early retirement.

Death in service prior to normal retirement age

Lump sum

A1.6. The member’s annual pensionable salary is payable

Spouse’s pension

A1.7. 1.05% of final average pensionable salaries per year of continuous service at date of death and 75% of potential service to the pension age.

Death in retirement

Guarantee period

A1.8. The retiree’s pension is guaranteed for a period of five years from the date of retirement.

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 31

Spouse’s pension

A1.9. 1.05% (0.77% for pensioners who retired before 1 July 1999) of final average pensionable salaries per year of continuous service.

Withdrawal benefits

A1.10. Member’s contributions plus 5/12% for each month of continuous service (the addition is approximately equivalent to compound interest at 10% a year) increased by 5% for each complete year of continuous service up to a maximum of 100% after 20 years of service; or if member has completed ten years of continuous service, a deferred pension and lump sum as for retirement at the pension age payable when he attains the pension age.

Ill Health retirement (more than 10 years of service)

Gratuity

A1.11. Same as for normal retirement

Pension

A1.12. Same as for normal retirement

Ill Health retirement (less than 10 years of service)

Gratuity

A1.13. The greater of the resignation benefit or twice the member’s contributions

Contributions

A1.14. Members contribute at a rate of 7% of pensionable salaries, plus a surcharge of 1.65%

of pensionable salaries in respect of members who were members at 30 June 2002.

A1.15. The local authorities contribute at a rate not lower than that which is determined by the actuary to be required to cover the balance of the cost of providing benefits.

Expenses

A1.16. The administration fees and related expenses are met by the Fund.

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 32

APPENDIX 2: DATA VERIFICATION

Data checks

A2.1. The following data checks were carried out by us:

Reconciling the active membership during the valuation period;

Testing for very high, low, nil or negative salary increases of individual members over the valuation period.

Testing whether the ages and pensionable salaries of individual members were within a reasonable range.

Ensuring that the age and past service of each member did not conflict with the minimum entry age.

Testing the reasonability of each member’s total/accumulated contributions relative to salary and length of service.

Checking the level of pensions against the pensions at the previous valuation date and increases granted since then.

Testing the reasonableness of age differences between pensioners and their spouses.

Checking for changes in the membership details over the valuation period.

Identifying any missing or invalid data fields.

Reconciling the valuation data with the financial statements.

Findings

A2.2. The data checks performed by us did not highlight any reasons to regard the data as being unsuitable for valuation purposes.

A2.3. This is however not a guarantee that the data is completely reliable.

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 33

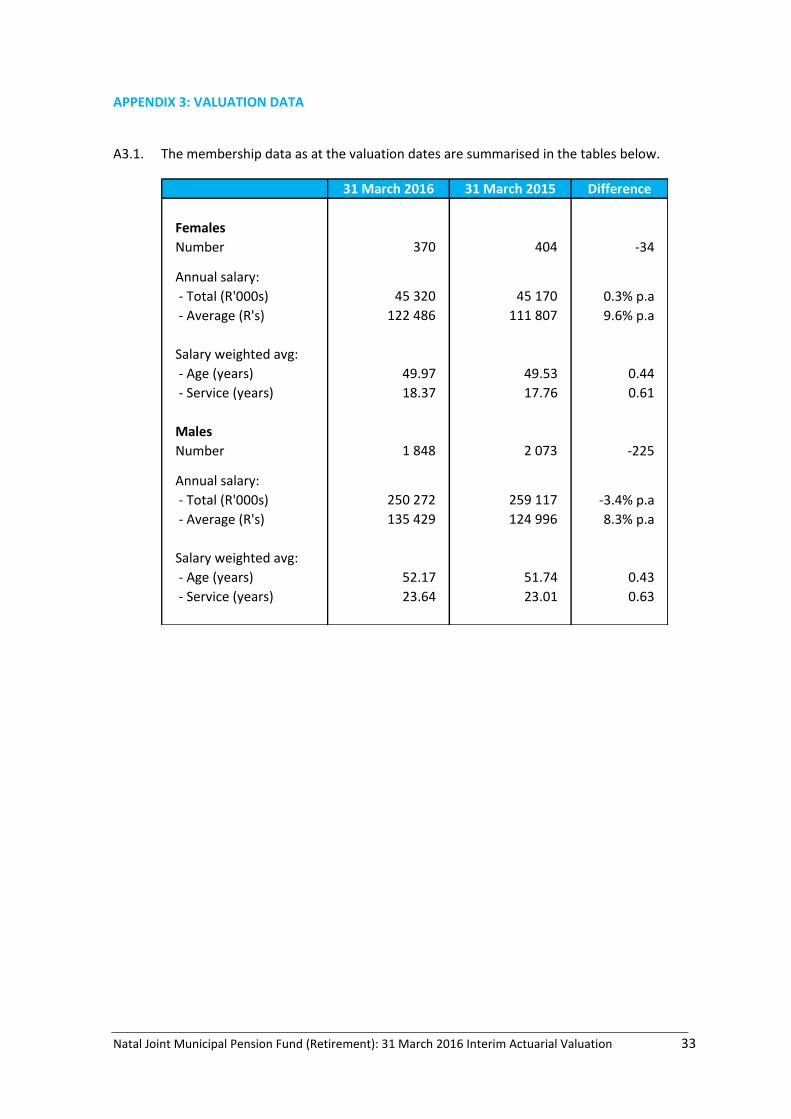

APPENDIX 3: VALUATION DATA

A3.1. The membership data as at the valuation dates are summarised in the tables below.

31 March 2016 31 March 2015 Difference

Females

Number 370 404 -34

Annual salary:

- Total (R'000s) 45 320 45 170 0.3% p.a

- Average (R's) 122 486 111 807 9.6% p.a

Salary weighted avg:

- Age (years) 49.97 49.53 0.44

- Service (years) 18.37 17.76 0.61

Males

Number 1 848 2 073 -225

Annual salary:

- Total (R'000s) 250 272 259 117 -3.4% p.a

- Average (R's) 135 429 124 996 8.3% p.a

Salary weighted avg:

- Age (years) 52.17 51.74 0.43

- Service (years) 23.64 23.01 0.63

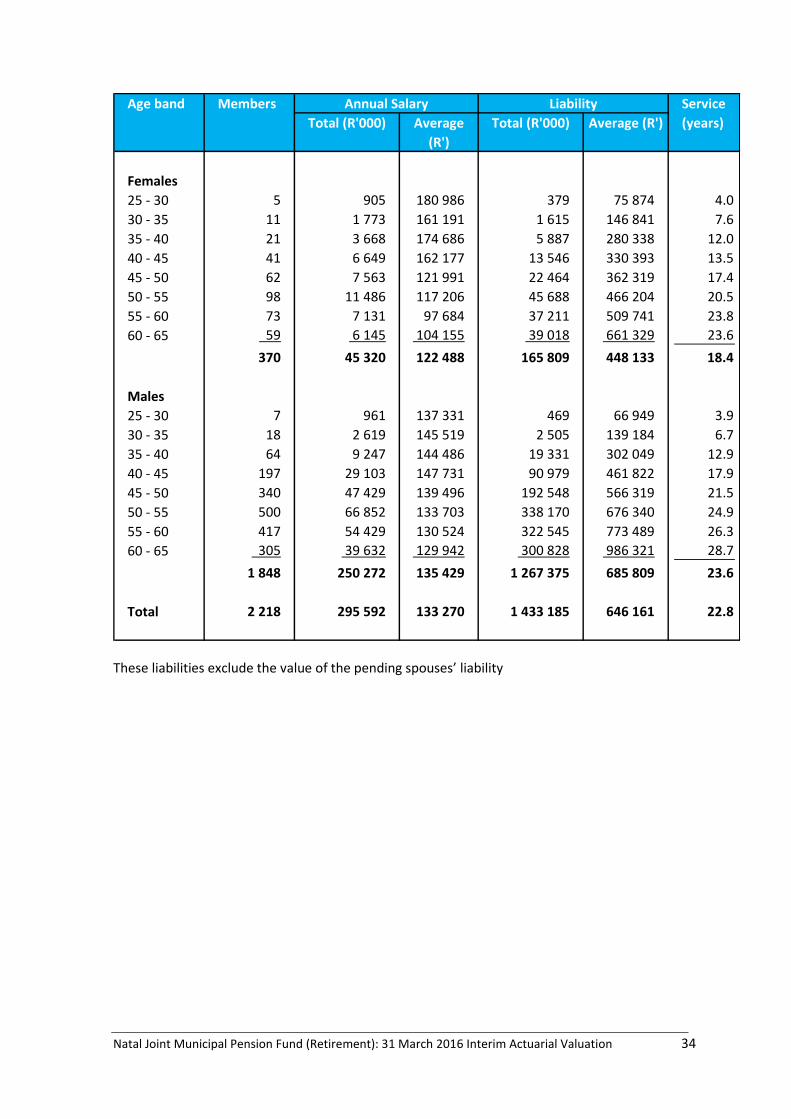

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 34

Age band Members Service

Total (R'000) Average

(R')

Total (R'000) Average (R') (years)

Females

25 - 30 5 905 180 986 379 75 874 4.0

30 - 35 11 1 773 161 191 1 615 146 841 7.6

35 - 40 21 3 668 174 686 5 887 280 338 12.0

40 - 45 41 6 649 162 177 13 546 330 393 13.5

45 - 50 62 7 563 121 991 22 464 362 319 17.4

50 - 55 98 11 486 117 206 45 688 466 204 20.5

55 - 60 73 7 131 97 684 37 211 509 741 23.8

60 - 65 59 6 145 104 155 39 018 661 329 23.6

370 45 320 122 488 165 809 448 133 18.4

Males

25 - 30 7 961 137 331 469 66 949 3.9

30 - 35 18 2 619 145 519 2 505 139 184 6.7

35 - 40 64 9 247 144 486 19 331 302 049 12.9

40 - 45 197 29 103 147 731 90 979 461 822 17.9

45 - 50 340 47 429 139 496 192 548 566 319 21.5

50 - 55 500 66 852 133 703 338 170 676 340 24.9

55 - 60 417 54 429 130 524 322 545 773 489 26.3

60 - 65 305 39 632 129 942 300 828 986 321 28.7

1 848 250 272 135 429 1 267 375 685 809 23.6

Total 2 218 295 592 133 270 1 433 185 646 161 22.8

Annual Salary Liability

These liabilities exclude the value of the pending spouses’ liability

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 35

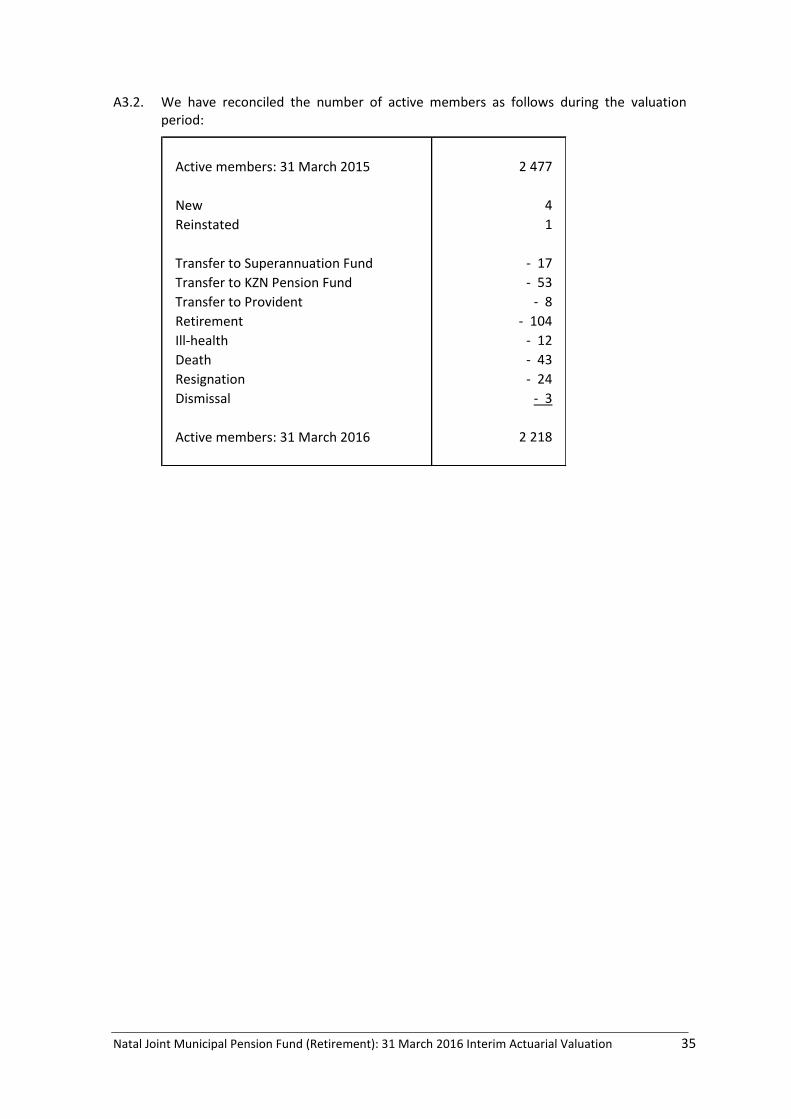

A3.2. We have reconciled the number of active members as follows during the valuation period:

Active members: 31 March 2015 2 477

New 4

Reinstated 1

Transfer to Superannuation Fund - 17

Transfer to KZN Pension Fund - 53

Transfer to Provident - 8

Retirement - 104

Ill-health - 12

Death - 43

Resignation - 24

Dismissal - 3

Active members: 31 March 2016 2 218

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 36

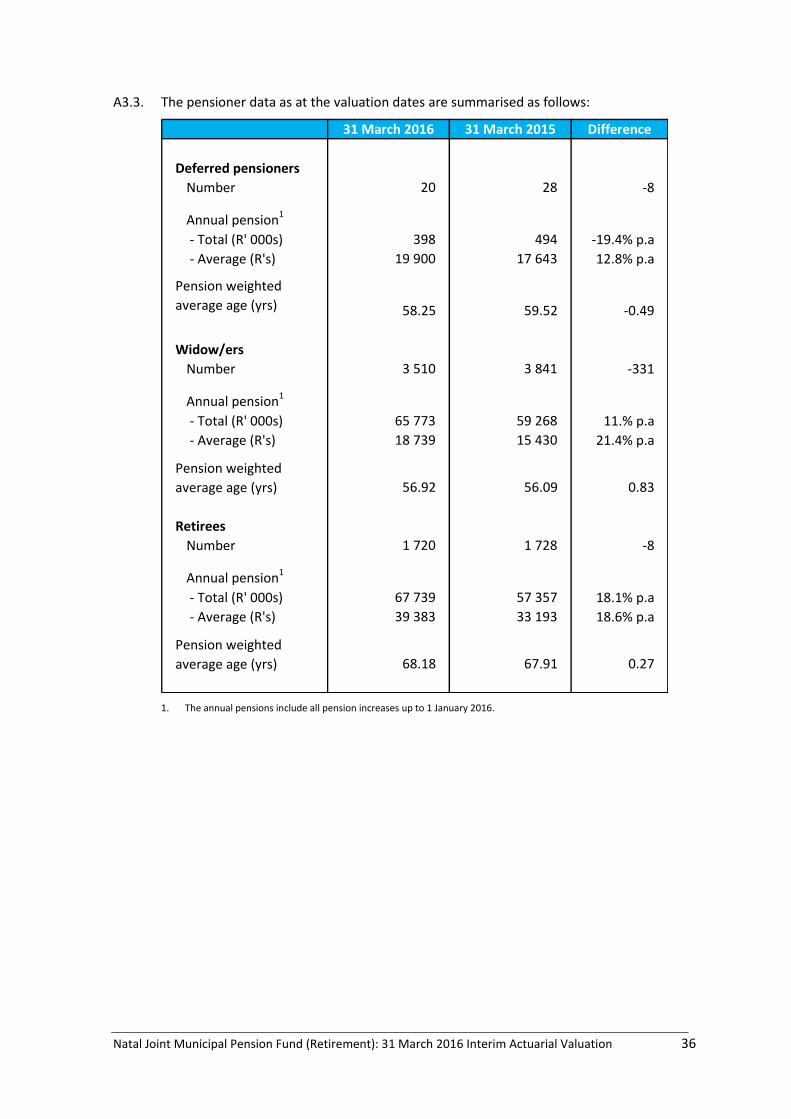

A3.3. The pensioner data as at the valuation dates are summarised as follows:

31 March 2016 31 March 2015 Difference

Deferred pensioners

Number 20 28 -8

Annual pension1

- Total (R' 000s) 398 494 -19.4% p.a

- Average (R's) 19 900 17 643 12.8% p.a

Pension weighted

average age (yrs) 58.25 59.52 -0.49

Widow/ers

Number 3 510 3 841 -331

Annual pension1

- Total (R' 000s) 65 773 59 268 11.% p.a

- Average (R's) 18 739 15 430 21.4% p.a

Pension weighted

average age (yrs) 56.92 56.09 0.83

Retirees

Number 1 720 1 728 -8

Annual pension1

- Total (R' 000s) 67 739 57 357 18.1% p.a

- Average (R's) 39 383 33 193 18.6% p.a

Pension weighted

average age (yrs) 68.18 67.91 0.27

1. The annual pensions include all pension increases up to 1 January 2016.

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 37

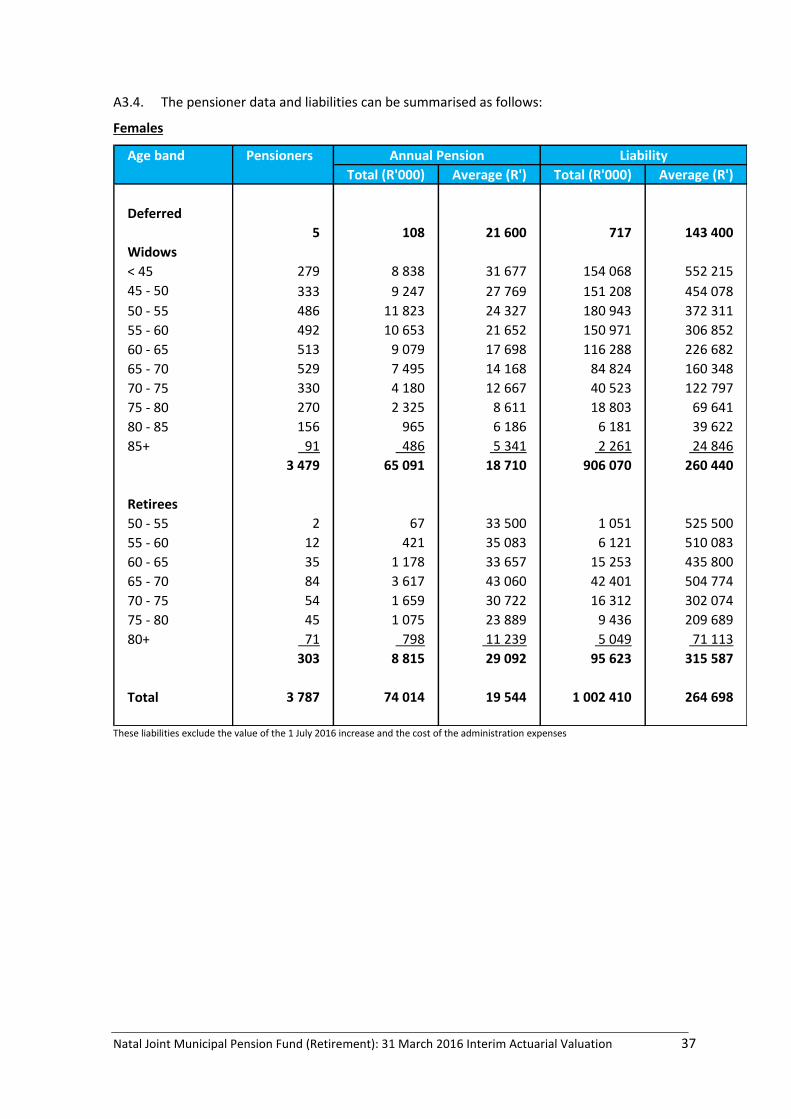

A3.4. The pensioner data and liabilities can be summarised as follows:

Females

Age band Pensioners

Total (R'000) Average (R') Total (R'000) Average (R')

Deferred

5 108 21 600 717 143 400

Widows

< 45 279 8 838 31 677 154 068 552 215

45 - 50 333 9 247 27 769 151 208 454 078

50 - 55 486 11 823 24 327 180 943 372 311

55 - 60 492 10 653 21 652 150 971 306 852

60 - 65 513 9 079 17 698 116 288 226 682

65 - 70 529 7 495 14 168 84 824 160 348

70 - 75 330 4 180 12 667 40 523 122 797

75 - 80 270 2 325 8 611 18 803 69 641

80 - 85 156 965 6 186 6 181 39 622

85+ 91 486 5 341 2 261 24 846

3 479 65 091 18 710 906 070 260 440

Retirees

50 - 55 2 67 33 500 1 051 525 500

55 - 60 12 421 35 083 6 121 510 083

60 - 65 35 1 178 33 657 15 253 435 800

65 - 70 84 3 617 43 060 42 401 504 774

70 - 75 54 1 659 30 722 16 312 302 074

75 - 80 45 1 075 23 889 9 436 209 689

80+ 71 798 11 239 5 049 71 113

303 8 815 29 092 95 623 315 587

Total 3 787 74 014 19 544 1 002 410 264 698

Annual Pension Liability

These liabilities exclude the value of the 1 July 2016 increase and the cost of the administration expenses

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 38

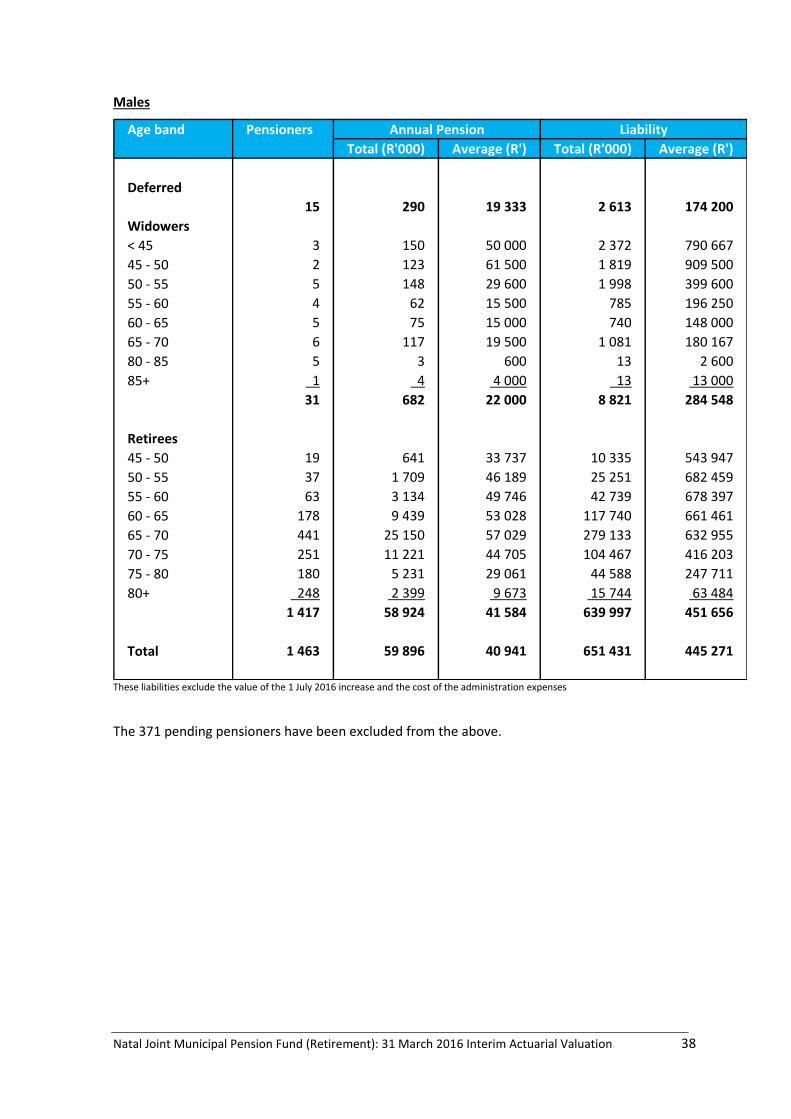

Males

Age band Pensioners

Total (R'000) Average (R') Total (R'000) Average (R')

Deferred

15 290 19 333 2 613 174 200

Widowers

< 45 3 150 50 000 2 372 790 667

45 - 50 2 123 61 500 1 819 909 500

50 - 55 5 148 29 600 1 998 399 600

55 - 60 4 62 15 500 785 196 250

60 - 65 5 75 15 000 740 148 000

65 - 70 6 117 19 500 1 081 180 167

80 - 85 5 3 600 13 2 600

85+ 1 4 4 000 13 13 000

31 682 22 000 8 821 284 548

Retirees

45 - 50 19 641 33 737 10 335 543 947

50 - 55 37 1 709 46 189 25 251 682 459

55 - 60 63 3 134 49 746 42 739 678 397

60 - 65 178 9 439 53 028 117 740 661 461

65 - 70 441 25 150 57 029 279 133 632 955

70 - 75 251 11 221 44 705 104 467 416 203

75 - 80 180 5 231 29 061 44 588 247 711

80+ 248 2 399 9 673 15 744 63 484

1 417 58 924 41 584 639 997 451 656

Total 1 463 59 896 40 941 651 431 445 271

Annual Pension Liability

These liabilities exclude the value of the 1 July 2016 increase and the cost of the administration expenses

The 371 pending pensioners have been excluded from the above.

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 39

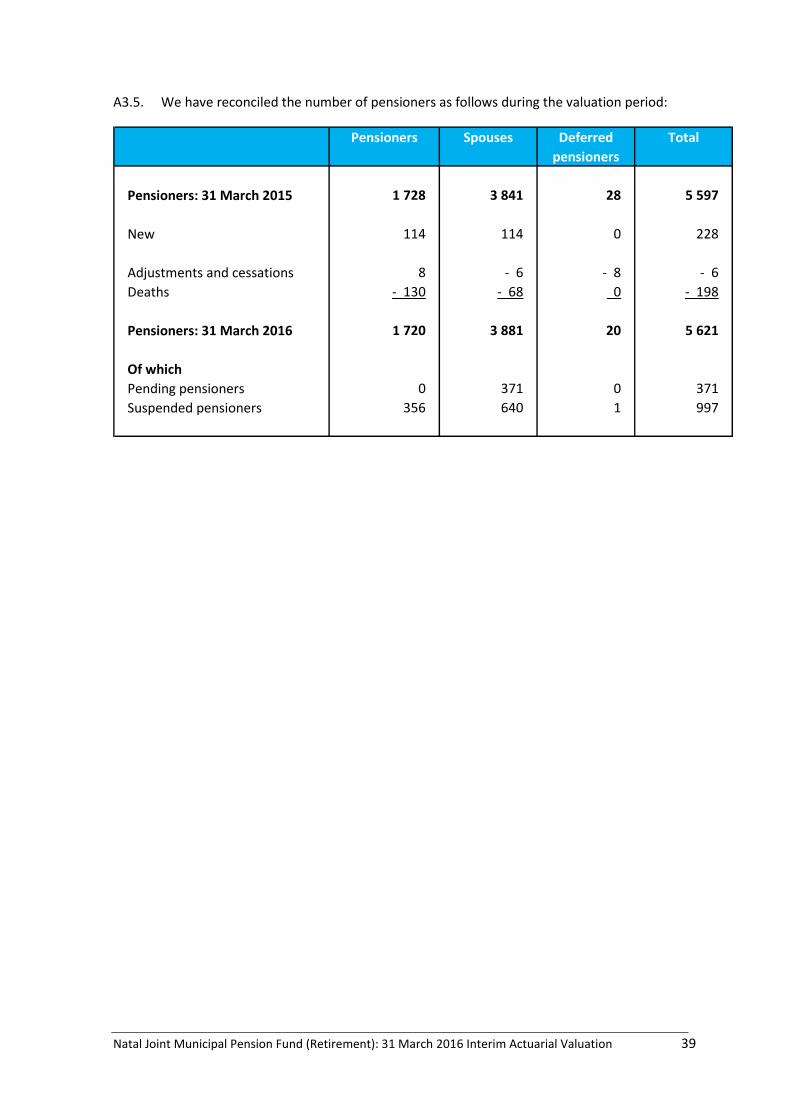

A3.5. We have reconciled the number of pensioners as follows during the valuation period:

Pensioners Spouses Deferred

pensioners

Total

Pensioners: 31 March 2015 1 728 3 841 28 5 597

New 114 114 0 228

Adjustments and cessations 8 - 6 - 8 - 6

Deaths - 130 - 68 0 - 198

Pensioners: 31 March 2016 1 720 3 881 20 5 621

Of which

Pending pensioners 0 371 0 371

Suspended pensioners 356 640 1 997

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 40

APPENDIX 4: VALUATION ASSUMPTIONS

A4.1. In terms of PF Notice No.2 of 2016 the Fund must disclose its valuation results using a “Prescribed Bond Based Basis”. Further, the Fund can also elect to apply a “Funding Basis” as long as this does not result in a weaker valuation result than would be obtained under what PF Notice No. 2 refers to as a “Prescribed Risk Premium Basis”.

A4.2. Below we set out our Funding Basis. Thereafter we set out the Prescribed Bond Based and Prescribed Risk Premium Bases and provide a justification for using our Funding Basis.

A4.3. In addition to holding assets to meet its liabilities, it is desirable that the Fund holds a Solvency Reserve in order to protect its financial soundness against volatility in the investment markets. Another valuation is thus performed for the defined benefit members in order to determine the level of the Solvency Reserve.

A4.4. The Fund was therefore valued on four sets of valuation assumptions:

The first set of assumptions is referred to as the Funding Basis and is used in order to determine the basic liability which has been used for past valuations of the Fund. This is based on a set of “best estimate” assumptions which are expected to apply over the long-term. The benefits payable by the Fund in future are estimated and these are discounted using the assumed investment return, to give the present value of the liabilities for service to the valuation date. A similar approach is taken to pensions in payment.

A second set of assumptions, referred to as the Solvency Reserve assumptions, is used in order to determine the Solvency Reserve. This set of valuation assumptions takes account of investment conditions at the valuation date. The benefits payable by the Fund in the future are estimated and these are discounted using the yield on Government Stock at the date of valuation. Allowance is made for inflation by reference to the yield on inflation-linked bonds at the valuation date. Effectively the Solvency Reserve calculation attempts to estimate the cost of buying out the liabilities at the valuation date using nominal and inflation-linked bonds.

A third and fourth set of assumptions, referred to as the Prescribed Bond Based and Prescribed Risk Premium bases is used in order to determine the valuation results in terms of PF Notice No.2 of 2016. The valuation results on the Prescribed Bond Based and Prescribed Risk Premium Bases are set out in Appendix 5.

Funding and Solvency Bases

General

A4.5. To assess the financial position of the Fund, it is necessary to make a realistic long-term estimate regarding each factor that affects the Fund. A number of factors are considered which are inter-related, often to such an extent that individual elements cannot be considered in isolation.

A4.6. The assumptions used for the valuation take into account the 31 March 2015 valuation assumptions, the experience of the Fund and the experience of similar funds.

A4.7. The actual long-term cost of the benefits depends on the actual experience of the Fund and not on the assumptions adopted. While the assumptions can affect the timing of the emerging cost in the short-term, they have little impact on the long-term cost.

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 41

A4.8. The Fund is required to earn a minimum rate of return on the assets in order to remain financially sound. Therefore projections were made of expected future benefit payments and future investment returns.

Inflation

Valuation assumption

A4.9. It was assumed that inflation over the long-term will be 6.0% per annum, which is within the level of the Reserve Bank’s long term target inflation range. This rate differs markedly from the bond market implied inflation rate at the valuation date as discussed in paragraph A4.10 below.

Solvency Reserve assumption

A4.10. The duration of the Fund’s liabilities is approximately 14 years and we have therefore used a yield of 10.15% per annum which corresponds to bonds with a 14 year term to maturity. The yield on inflation-linked bonds with a 14 year maturity was about 1.87% per annum. We have made an allowance of 0.5% for the inflation risk premium. The difference of 7.78% per annum (10.15% less 1.87% less 0.5%) is the rate of compensation the market requires for inflation at the valuation date. We have therefore assumed an underlying rate of inflation of 7.78% per annum for the liabilities.

Investment return

Valuation assumption

A4.11. The assumed investment return is used as an interest rate to discount expected future cash flows. In estimating the future investment earnings, greater emphasis is placed on the long-term trend as opposed to the short-term experience of the Fund.

A4.12. The Fund has a defined benefit liability in respect of a closed, aging group of defined benefit members and pensioners.

A4.13. The Fund’s strategic asset allocation at the valuation date was 65% equities, 10% property, 3% cash and 22% fixed interest investments.

A4.14. The Investment Policy Statement of the Fund targets a real return above inflation of 5% per annum. We have assumed that investment fees will reduce the return by 0.5% per annum.

A4.15. We have therefore taken the long term nominal investment return expectation to be 10.0% per annum (rounded down).

Solvency Reserve assumption

A4.16. At the valuation date the yield on fixed interest bonds with a 14 year term to maturity was 10.15% per annum.

A4.17. The Fund’s liabilities in respect of the members are predominantly longer term and therefore, for purposes of this valuation, it was thus assumed that the Fund would earn 10.15% per annum and this was the rate used to value the liabilities of the Fund.

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 42

Salary increases

Valuation assumption

A4.18. We have allowed for future salary increases as a result of inflation at 1.0% per annum above inflation, that is at 7.0% per annum.

A4.19. In addition, we provided for merit and promotion increases, as shown in Table 1 below.

Solvency Reserve assumption

A4.20. Allowance was made for pensionable salaries to be increased in future at 1.0% per annum above the assumed rate of inflation (7.78% per annum), a total of 8.78% per annum.

A4.21. In addition, we have allowed for merit and promotion increases as shown in Table 1 below.

Pension increases

Valuation assumption

A4.22. The Pension Increase Policy of the Fund states that pensions will be increased annually by at least 75% of the average increase in inflation or, if greater, the increase affordable out of the investment return earned on pensioner assets (subject to a maximum of 100% of inflation). “Affordability” is determined by investment earnings in excess of 5.0% per annum.

A4.23. Based on an assumed investment return of 10.0% per annum and inflation of 6.0% per annum, pension increases of 75% of inflation require a post retirement interest rate of 5.3% [1.10 divided by (1+0.75 times 0.06)]. In order to provide for at least 75% of inflation it was decided to use a post retirement rate of 5.0% per annum (which provides for a pension increase of approximately 80% (1.1/1.05-1)/0.06=79.365%) of inflation.

A4.24. The Trustees are satisfied that the assets underlying the Pensions Memorandum Account are expected to achieve a real return that is sufficient to allow the Fund to grant pension increases of at least 75% of inflation when combined with a 5.0% per annum post retirement interest rate. This view is supported by the results of the 30 September 2012 asset liability modelling exercise undertaken by the Fund. This will be updated in the next interim valuation of the Fund following the asset liability modelling exercise that is to be undertaken after the valuation date.

Solvency Reserve assumption

A4.25. The implied inflation rate under the Solvency Reserve assumptions is 7.78% per annum (paragraph A4.10 above). A post-retirement rate of interest assumption of 3.75% per annum is therefore required to allow for pension increases of a similar order of approximately 80% of inflation.

Withdrawals

A4.26. Withdrawals consist mainly of voluntary resignations and resignations to avoid dismissal. No special provision is made for exits such as retrenchments and transfers to other funds, since they are approximately financially neutral towards the Fund.

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 43

A4.27. Allowance was made for the prescribed minimum withdrawal benefits in terms of the Pension Funds Second Amendment Act. The outcome of these minimum benefits is that the Fund no longer makes material withdrawal profits in respect of members who leave the Fund prior to retirement.

A4.28. The withdrawal rates used in the previous statutory valuation of the Fund was retained for this interim valuation. Sample rates are set out in Table 2 below.

Mortality

A4.29. For purposes of the valuation we assumed that post-retirement mortality will be in line with the PA(90) mortality table, rated down 1 year allowing for future mortality improvements of 0,50% per annum from 2007 onwards, with an overall improvement in mortality of 10% after 20 years with an additional age rating of +2 years for males. Sample mortality rates are set out in Table 4 below, without any allowance for improvements.

A4.30. The Trustees should take note of the outcome of the data investigation as set out in paragraph 14 of the main report. This meant that the mortality assumptions used in the previous statutory valuation of the Fund could be retained for this valuation and the mortality reserve in respect of suspended pensioners could be released (see paragraph 83 of the main report).

Ill Health retirement

A4.31. We retained the ill health retirement assumptions for both males and females from the previous statutory valuation of the Fund.

A4.32. Sample rates are set out in Table 3 below.

Family statistics and expenses

A4.33. We assumed that on average a husband will be 5 years older than his wife and that 100% of members have an eligible spouse.

119. Expenses of administration are paid by the Fund and have therefore been included in the required contribution rate.

A4.34. We have allowed for an expected expense rate of 1.2% per annum in line with the review by the administrator of the distribution of the expenses between the Fund and the Natal Joint Municipal Pension Fund (Superannuation) and the Kwa-Zulu Natal Joint Municipal Provident Fund (“Natal Joint Funds”). We will monitor the expenses at each interim valuation and adjust the required rate of contribution if necessary.

A4.35. In the case of current pensioners an allowance was made for expenses incurred in the payment of pensions. We have allowed for expenses to be incurred in the payment of pensions, at R 36.75 per pensioner per month, increasing in future at the same rate as the pensions. This is the actual cost of administration that is being applied to the Fund.

Prescribed minimum benefits

A4.36. The Fund determines the minimum benefits prescribed by the Act for defined benefit members on the 40% of Earnings Yield (“EY”) basis.

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 44

A4.37. For each member the actuarial reserve was compared to the value of the minimum benefit that would become payable at each future date, if the member resigned from the service at that date. Where the latter figure exceeded the actuarial reserve, the difference was added to the liabilities of the Fund.

A4.38. For calculating the value of the Prescribed Minimum Benefit the following assumptions were applied:

The deferred pension and gratuity is based on service to the valuation date;

We expect the “40% EY” figures published by the Financial Services Board to average some 3% over the long term and we have therefore applied this figure in calculating the minimum benefit mentioned above;

The pension will be payable from the member’s normal retirement age;

Pre- and post-retirement decrements are as set out above.

A4.39. For the Solvency Reserve the above is repeated using the actual Earnings Yield applicable at the valuation date.

A4.40. Additionally, the total actuarial reserve for each member at the valuation date was compared with the value of the minimum benefit at the valuation date based on the Earnings Yield published by the FSB at the valuation date, i.e. taking into account market conditions at the valuation date. The quantum of the additional calculation is shown in paragraph 63 of the main report.

A4.41. The Pension Funds Act prescribes minimum increases to pensioners. Each pension in payment must be compared to the pension at retirement increased by the full rate of inflation since date of retirement (if affordable). The last comparison in this regard was done as at 31 March 2015 and another comparison will only be performed at the next statutory valuation of the Fund as at 31 March 2018.

Changes in assumptions

A4.42. The valuation assumptions remain unchanged from those used in the 31 March 2015 actuarial valuation with the exception of:

The provision for expenses for pensioners was increased from R400 to R441 per pensioner per annum;

A4.43. The Solvency Reserve assumptions have been changed in line with the change in bond yields over the valuation period.

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 45

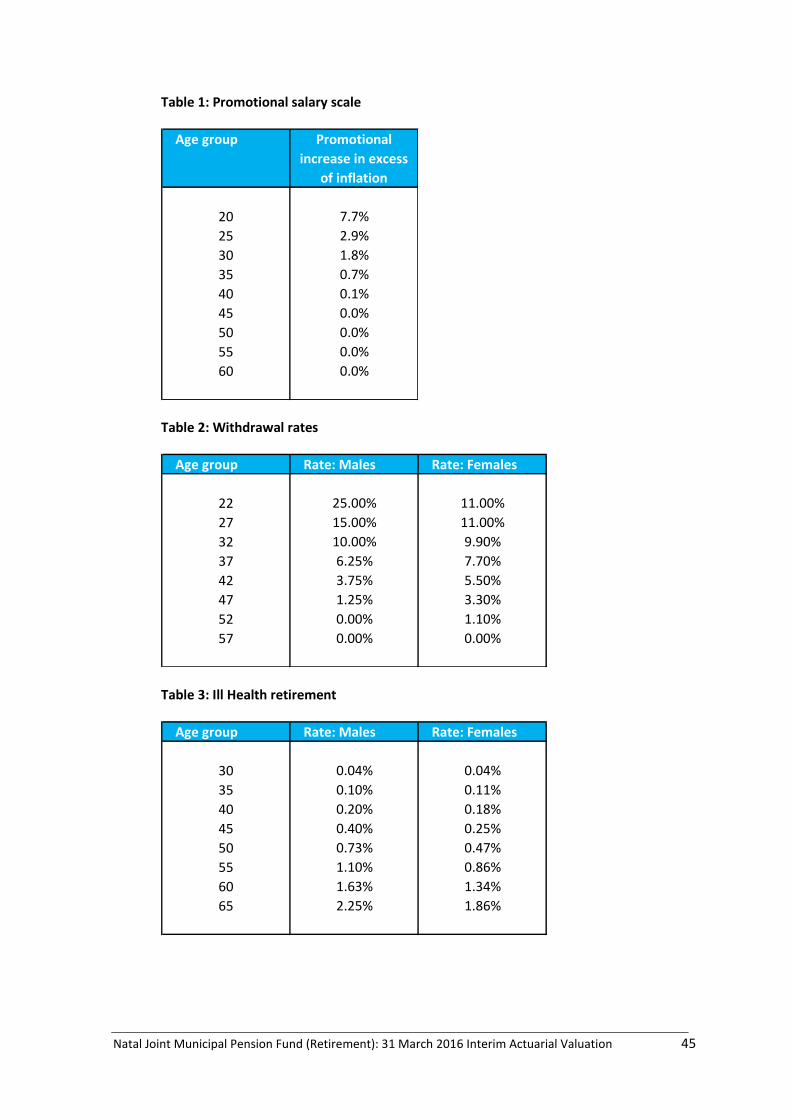

Table 1: Promotional salary scale

Age group Promotional

increase in excess

of inflation

20 7.7%

25 2.9%

30 1.8%

35 0.7%

40 0.1%

45 0.0%

50 0.0%

55 0.0%

60 0.0%

Table 2: Withdrawal rates

Age group Rate: Males Rate: Females

22 25.00% 11.00%

27 15.00% 11.00%

32 10.00% 9.90%

37 6.25% 7.70%

42 3.75% 5.50%

47 1.25% 3.30%

52 0.00% 1.10%

57 0.00% 0.00%

Table 3: Ill Health retirement

Age group Rate: Males Rate: Females

30 0.04% 0.04%

35 0.10% 0.11%

40 0.20% 0.18%

45 0.40% 0.25%

50 0.73% 0.47%

55 1.10% 0.86%

60 1.63% 1.34%

65 2.25% 1.86%

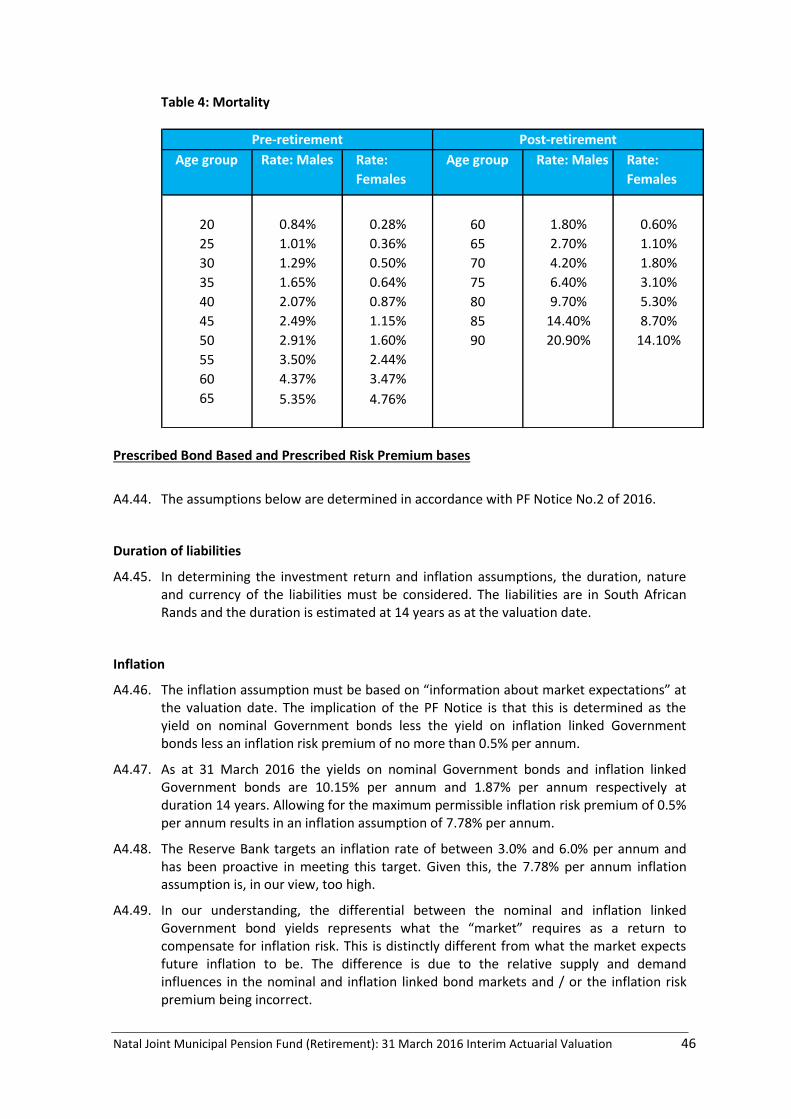

Natal Joint Municipal Pension Fund (Retirement): 31 March 2016 Interim Actuarial Valuation 46

Table 4: Mortality

Age group Rate: Males Rate:

Females

Age group Rate: Males Rate:

Females

20 0.84% 0.28% 60 1.80% 0.60%

25 1.01% 0.36% 65 2.70% 1.10%

30 1.29% 0.50% 70 4.20% 1.80%

35 1.65% 0.64% 75 6.40% 3.10%

40 2.07% 0.87% 80 9.70% 5.30%

45 2.49% 1.15% 85 14.40% 8.70%

50 2.91% 1.60% 90 20.90% 14.10%

55 3.50% 2.44%

60 4.37% 3.47%

65 5.35% 4.76%