Embed Size (px)

Citation preview

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 1/89

PREFACE

In Masters of Business Administration, Internship Program is an important part to

give students an opportunity to have experience of practical field. Unless and until the

students experience the novelty of practical work, their knowledge of what they study

in theoretical courses remains incomplete. The most important point in an InternshipProgram is that the student should spend their time in a true manner and with the spirit

to learn practical orientation of theoretical study framework.

This internship report is on my eight weeks practical training at United Bank Limited

Hussain Agahi Branch, Multan. In this internship report I have tried to give details

about the United Band Limited, working and the functions of different departments of

the bank.

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 2/89

ACKNOWEDGEMENT

First of all, I thank my all respected teachers for providing me comprehensive knowledgeabout Business Administration Courses and also for providing me the opportunity tocomplete my internship program in UBL to enhance my practical knowledge about

banking sector of Pakistan. I am also indebted to the followings because without theirhelp, I would not be able to achieve this practical knowledge:

Hussain Agahi Branch Multan

Mr. Habib Ullah Khan (VP-Sales) Mr. Haji Nusrat (AVP-Operations) Mr. Mirza Qamar Baig (Advances Department) Mr. Habib-ur-Rehman Sheikh (Staff Manager)

Chowk Fawara Branch Multan

(Branch Manager Mr. Zafarullah Khan (OG-II Officer)

Mr. Jamil (Cashier)

Muhammad

Saleem

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 3/89

HISTORY OF BANKING

³Bank is a pipeline through which currency moves into and out of circulation.´

Bank accepts deposits and repays cash to its customers on their demand. The Bank

borrows money at a lesser rate of interest and lends it to the borrowers at a higher rate.

It is thus a profit-lending concern. Bank cannot lend all the money that has been

deposited with it. It has to keep a certain portion of the total deposits in cash with

them in order to meet the cash requirements of the individuals and business concern.

Banking History Word Bank is said to be derived from the words Banc usor Banque or Bank. Thehistory of banking is traced to as early as 2000 BC. The priests inGreece used to keepmoney and valuables of the people in temples. These priests thus acted as financial

agents. The origin of banking is also traced to early goldsmiths. They used to keepstrong safes for storing the money and valuables of the people. The persons who hadsurplus money found it safe and convenient to deposit their valuables with them.The FIRST STAGE in the development of modern banking, thus, was the acceptingof deposits of cash from those persons who had surplus money with them.The goldsmiths used to issue receipts for the money deposited with them. Thesereceipts began to pass from hand to hand in settlement of transactions because peoplehad confidence in the integrity and solvency of goldsmiths. When it was found thatthese receipts were drawn in such a way that it entitles any holder to claim thespecified amount of money from goldsmiths. A depositor who is to make the

payments may now get the money in cash from goldsmiths or pay over the receipt tothe creditor. These receipts were the earlier bank notes. The SECOND STAGE in

development of banking thus was the issue of bank notes.The goldsmiths soon discovered that all the people who had deposited money withthem did not come to withdraw their funds in cash. They found that only a few

persons presented the receipt for encashment during a given period of time. They alsofound that most of the money deposited with was lying idle. At the same time, theyfound that they were being constantly requested for loan on good security. Theythought it profitable to lend at least some of the money deposited with them too theneedy persons. This proved quite a profitable business for the goldsmiths. Theyinstead of charging interest from the depositors began to give them interest on themoney deposited with them. This was the THIRD STAGE, in the development of

banking.By experience the banks came to know that they could keep a small proportion of thetotal deposits for meeting the demands of customers for cash and the rest they couldeasily lend. They allowed the depositors to draw over and above the money actuallystanding to their credit. In Economics terminology we can say that they allowed theoverdraft facilities to their depositors. This was the FOURTH STAGE, indevelopment of banking.When every bank issues receipts and most of them allowed the overdraft facilities,there was then too much confusion in the banking system. The banks in order to earn

profits could not keep adequate reserves for meeting the demands of the customers for

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 4/89

cash. The failures on the part of the bankers to return money caused widespreaddistress among the peoples.

In order to create confidence among the people, steps were taken to regulate the banking organization. A conference was held in Nuremberg in1548. It was decided

that a bank should be set up by the state, which should streamline the bankingorganization and technique. The first central bank was formed inGenevain 1578.

Bank of England was established in 1694. The responsibility of issuing of notes isnow entrusted to a central bank of each country.

COMMERCIAL BANKING INPAKISTAN:

At the time of partition total number of Banks were 38 only. Out of these Banks

the Pakistani Banks were only 2 , Indian Banks 29 & Exchange Banks were 7. Thetotal of deposits of Pakistani Banks was Rs.880 Million. & advances were Rs: 198Million.. According to banking companies ordinance Banks are the companies, whichtransacts the business of Banking in Pakistan.

Commercial Banks have constituted the most important [part of the intuitional creditin the economy of Pakistan. Being the largest source of credits, BankingIndustry is a

pivot of whole the economic activities in Pakistan. Section 37(2A) of State Bank of Pakistan Act 1965 lays down that the Banks must have paid-up capital & reserve of not less then Rs: 5 Lac & fulfilling certain other requirements for declaring as³Scheduled Bank´.

At the time of independence Bank services was badly affected. But with the passageof time these are improving. The government of Pakistan nationalized all Banks inearly 1974. This act was done to minimize control of few hands over banking. Butthis step was proved e futile for the

Banking in Pakistan. So the Govt. had to revise its decision in1990. Two Banks(Allied Bank Of Pakistan Limited & Muslim commercial Bank Of PakistanLimited have been denationalized. Since then Banks were working well. Now

slogan of the Banks is to serve their customers in the best possible manner.

Professor Berton:³ Banks are the guardian & distributor of money ³.

Similarly we can say that it is a pipeline thorough which currency moves into &outside the circle. Banks accept deposited of money and repay it on demand. Bank

borrows money at lesser rate of interest & lends it at higher rate of interest. In thisway Banks earn money. Bank do not lend all money they collect, they keep certain portion of it as reserve to meet the uncertain demand of the customer.

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 5/89

FUNCTIONS OF A COMMERCIAL BANK

In general terms the functions of a commercial bank can be classified under the

following main heads.

1. ACCEPTING DEPOSITS

Some people have an excess money and they want to deposits it to some honest man

or an institution which can give them some profit. So the first function of commercial

bank is to receive deposit there are three types of deposits.

1.1 Demand Deposits or Current Deposits

Some people deposit their excess money in the current accounts and they can

withdraw their money deposited in this account at any time during the banking hours,

so bank is not ready to give interest on it.

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 6/89

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 7/89

1.2 Fixed Deposits

These deposits are fixed for a particular period. Commercial banks also pay an

interest on these accounts. An important thing related to it is the varying interest rates

for the different period deposits. Interest rate increases with the increase in the fixed

deposit period.

1.3 Saving Deposits

To create the habit of savings, bank accepts the saving deposits and pays an interest

on these deposits. And this rate of interest is greater than the demand deposits.

2. ADVANCING LOANS

Bank also advances the loans to the merchants and charges the interest. It is the major

source of its income. It also issues the loan for short term, medium term and for long

term. And bank receives the higher interest from the borrower for the long term loans

offered.3. DISCOUNTING OF BILL

Commercial banks also discount the bills and facilitate the business; for example one

businessman purchases anything from another person and promises to pay after one

month. The seller will write a bill to the buyer and there will be an order that after one

month the buyer will pay the amount to the seller. Buyer will sign on the bill. In other

words buyer will accept the responsibility of that amount. If seller is in need of

money, he will take it to the bank and will receive the money by discounting the bills.

The commercial bank also may rediscount it from the central bank.

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 8/89

4. CHEAP MEDIUM OF EXCHANGE

By issuing cheques and drafts bank provides cheap, medium of exchange.

5. TRANSFER OF MONEY

The commercial bank is very helpful in transferring the money from one place to

another by issuing the drafts. This is very popular concept in the modern world and

widely used in the business community.

6. CUSTODIAN OF PRECIOUS ARTICLES

Banks also provide lockers for the safety of precious articles. So now everyone can

secure his precious metals like gold, silver, etc., and bank charges a very nominal

charge for this facility.

7. AGENCY SERVICES

Commercial Banks also perform the duty of an agent. It collects and pays on the

behalf of the customers.

8. INVESTMENT

On behalf of the customers all the banks also make an investment in different

companies and industries. And banks receive nominal charge from the customers.

9. CREATION OF CREDIT

It also creates and extends the volume of credit.

10. FACILITATING TRADE ACTIVITIES

It also provides the finance to the foreign trade. Letter of credits are issued by the

commercial banks for the foreign payments.

11. PURCHASE AND SALE OF SECURITIES

The commercial bank purchases and sells the securities, for itself and sometimes on

the behalf of the costumes.

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 9/89

12. ACTING AS A TRUSTEE

If a client directs his bank to act as a trustee in the administration of a business, the

bank performs this responsibility.

ROLL OF COMMERCIAL BANK IN THE ECONOMY

DEVELOPMENT OF PAKISTAN:

Banks play an important role in the economic development of country. If our Bankingsystem is not in accordance to the economic requirement then how it can play a vitalrole in our developments. The State Bank of Pakistan is at the apex and all thecommercial Banks have to follow the rules of State Bank of Pakistan. Role of the

banking sector can be judged by the following facts:

SAVING MOBILIZATION:

The commercial Banks namely United Bank Limited Pakistan, Habib Bank Ltd,Allied Bank Of Pakistan Ltd. & National Bank has opened Branches in urban areas &rural areas to mobilize savings of people.

FINACCING OF DEVELOPMENT PROJECTS:

Banks & other financial institutions like ADBP, IDBP, and PICIC etc. Advancesshort & medium terms loans for financing of the development projects both in the

private & public sectors .So they helping to accelerate the rate of progress (Economic)in the country.

ENHANCING TRADE ACTIVITIES:

The credit institutions collect the savings of people & make them available for facilitating the trade activities both inside & outside the country.

CREATING CLIMATE FOR CAPITAL FORMATION:

A developed baking system stimulates the growth of economy by creating favorableclimate for capital formation in the Country.

HELP OF STATE BANK OF PAKISTAN IN ACHIEVING MONETARY

PUBLISHES:

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 10/89

Commercial Banks under the supervision & guidance of the S.B.P help inimplementing & achieving the objective of monetary policy, which vary from time to

time.

ASSISST IN PLANNED DEVELOPMENT:

Commercial Banks are profit-seeking enterprises. In order to maximize profit theyhave the incentive from S.B.P to maximize the limit of finance. An organizedBanking system keeps balance between the liquidity * profitability, thus assists in the

planed development of the Country.

PROFIT SHARING SCHEME:

Commercial Banks receive surplus balance of the households and business & payinterest on the deposit of client. The depositors instead of having a fixed return on the

deposit will share in the profit & loss of the Bank. The profit & loss schemearrangement is the alternative to interest, under an Islamic economic system, which is

since on the experimental basis in Pakistan.

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 11/89

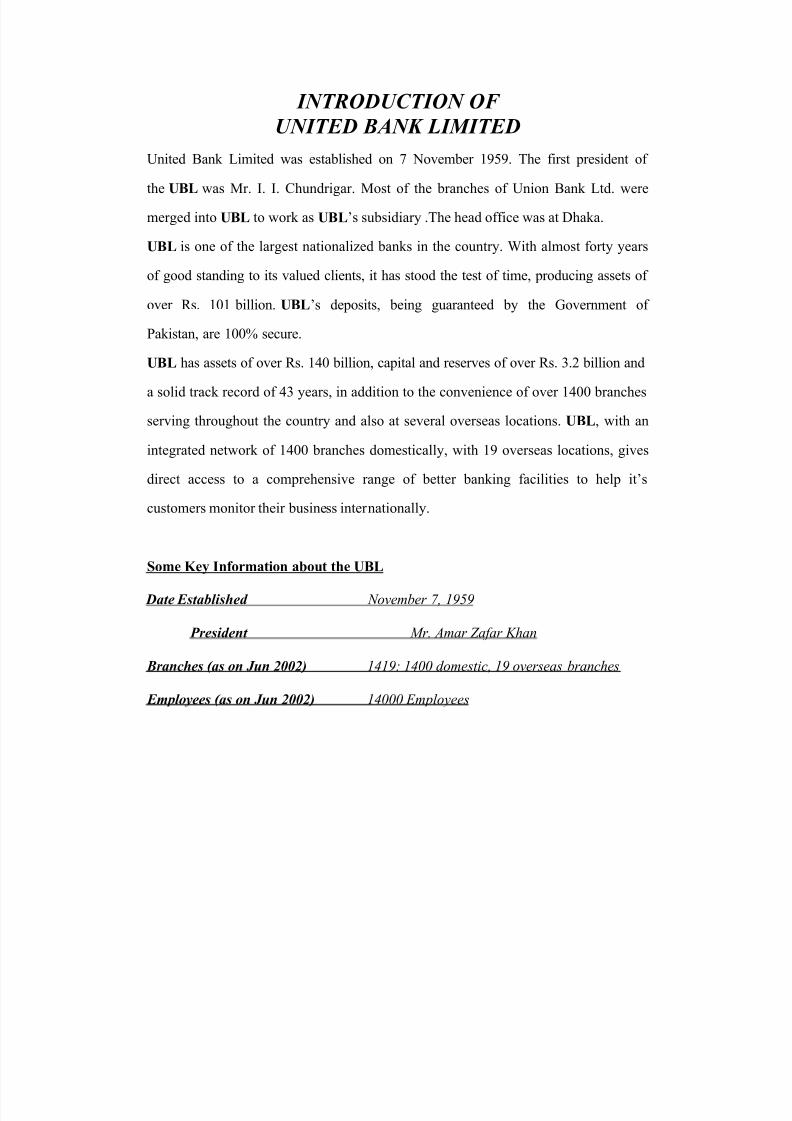

INTRODUCTION OF

UNITED BANK LIMITED

United Bank Limited was established on 7 November 1959. The first president of

the UBL was Mr. I. I. Chundrigar. Most of the branches of Union Bank Ltd. were

merged into UBL to work as UBL¶s subsidiary .The head office was at Dhaka.

UBL is one of the largest nationalized banks in the country. With almost forty years

of good standing to its valued clients, it has stood the test of time, producing assets of

over Rs. 101 billion. UBL¶s deposits, being guaranteed by the Government of

Pakistan, are 100% secure.

UBL has assets of over Rs. 140 billion, capital and reserves of over Rs. 3.2 billion and

a solid track record of 43 years, in addition to the convenience of over 1400 branches

serving throughout the country and also at several overseas locations. UBL, with an

integrated network of 1400 branches domestically, with 19 overseas locations, gives

direct access to a comprehensive range of better banking facilities to help it¶s

customers monitor their business internationally.

Some K ey Information about the UBL

Date Established N ovember 7, 1959

President M r. Amar Zafar Khan

Branches (as on Jun 2002) 1419: 1400 domestic, 19 overseas branches

Employees (as on Jun 2002) 14000 Employees

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 12/89

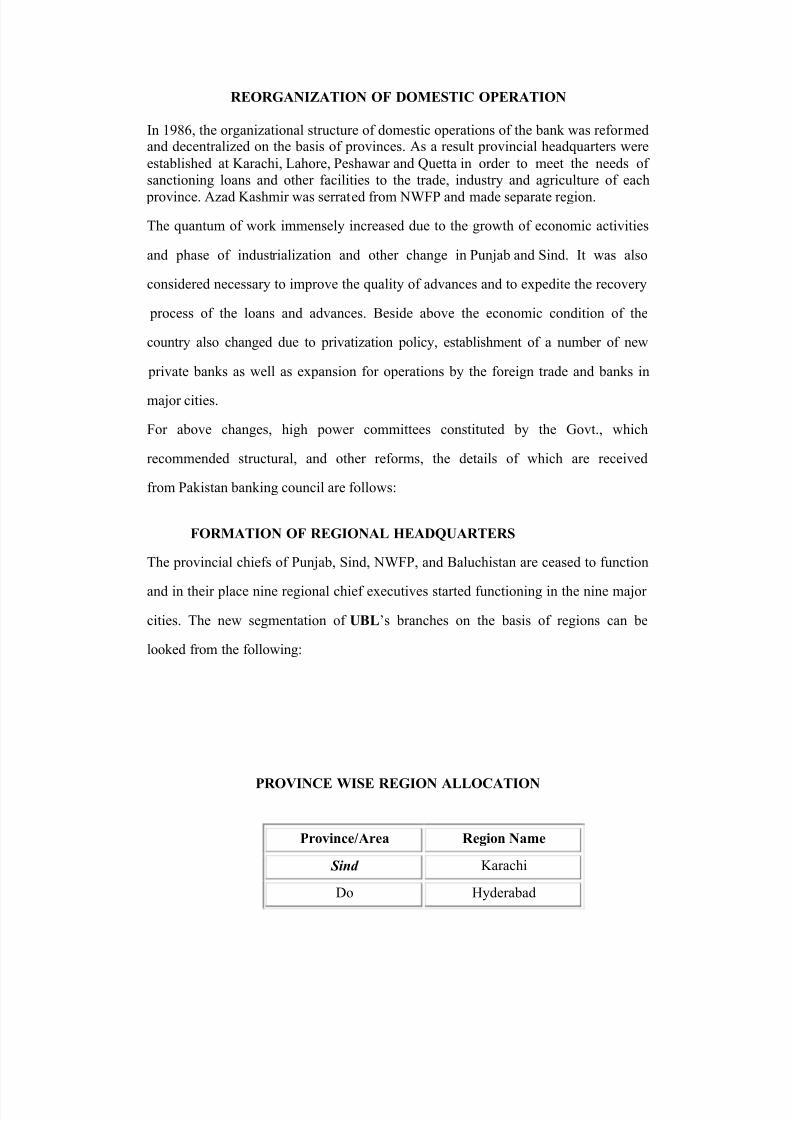

REORGANIZATION OF DOMESTIC OPERATION

In 1986, the organizational structure of domestic operations of the bank was reformedand decentralized on the basis of provinces. As a result provincial headquarters were

established at Karachi, Lahore, Peshawar and Quetta in order to meet the needs of sanctioning loans and other facilities to the trade, industry and agriculture of each

province. Azad Kashmir was serrated from NWFP and made separate region.

The quantum of work immensely increased due to the growth of economic activities

and phase of industrialization and other change in Punjab and Sind. It was also

considered necessary to improve the quality of advances and to expedite the recovery

process of the loans and advances. Beside above the economic condition of the

country also changed due to privatization policy, establishment of a number of new

private banks as well as expansion for operations by the foreign trade and banks in

major cities.

For above changes, high power committees constituted by the Govt., which

recommended structural, and other reforms, the details of which are received

from Pakistan banking council are follows:

FORMATION OF REGIONAL HEADQUARTERS

The provincial chiefs of Punjab, Sind, NWFP, and Baluchistan are ceased to function

and in their place nine regional chief executives started functioning in the nine major

cities. The new segmentation of UBL¶s branches on the basis of regions can be

looked from the following:

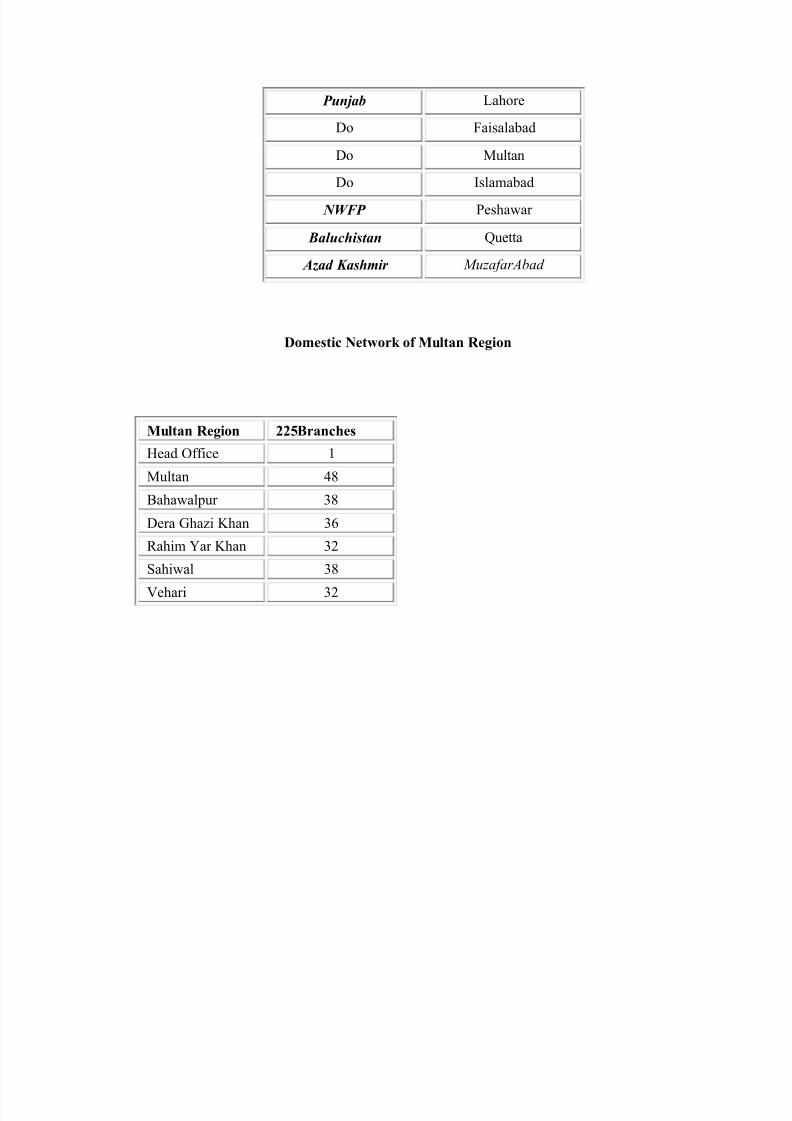

PROVINCE WISE REGION ALLOCATION

Province/Area R egion Name

Sind Karachi

Do Hyderabad

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 13/89

Punjab Lahore

Do Faisalabad

Do Multan

Do Islamabad

NWFP Peshawar

Baluchistan Quetta

Azad Kashmir M uzafarAbad

Domestic Network of Multan R egion

Multan R egion 225Branches

Head Office 1

Multan 48

Bahawalpur 38

Dera Ghazi Khan 36

Rahim Yar Khan 32

Sahiwal 38

Vehari 32

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 14/89

COMMUNITY SERVICES

UBL is committed to the welfare of Pakistan. It lends to farmers for the purchase of

tractors, superior quality seed and fertilizers. UBL further fosters the individual

welfare and well being of the common man by lending house building finance and

loans to set up small businesses. UBL has played a leading role in the dissemination

of Computer Technology in Pakistan and is dedicated to the promotion of sports.

j Agricultural Loans

j Small Business Scheme

j UBL Computer Training Institute

j Staff Colleges of UBL

j UBL Sports Complex

AGRICULTURAL LOANS UBL¶s agricultural loans on easy terms and conditions to small-scale land owning

farmers boost the country¶s economy and yield greener harvests. UBLenables farmers

to buy good quality seeds, fertilizers, pesticides and agricultural implements.

SMALL BUSINESS SCHEME Under the Small Business Scheme, UBL is providing loans on easy terms to those

who wish to set up their own small-scale business. This scheme is aimed at spreading

prosperity in the country by reducing unemployment. As more and more people start

their own industrial units, the country will move steadily towards economic self-

reliance.

UBL COMPUTER TRAINING INSTITUTE UBL is a pioneer in the computerization of banking in Pakistan, and now plays a

leading role in the dissemination of Computer Technology in Pakistan and is proud to

be a part of the Government¶s Computer Literacy Program aimed at preparing the

younger generation to meet the challenges of tomorrow.

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 15/89

UBL, the leading user of Computer Technology in the Banking Sector has set up most

modern facilities at Muzaffarabad, Azad Kashmir, and Sheikhupura for imparting

training to the educated youth under the Government¶s Computer Literacy Program.

These centers are equipped with state of the art hardware and audio-visual aids and

are manned by experienced professionals.

STAFF COLLEGES OF UBL The UBL has three staff colleges, which are generating banking trained personnel.

These colleges are at Karachi, Lahore and Rawalpindi, established in 1964, 1978 and

1977 respectively. These staff colleges are providing facilities of training to the

employees of the bank so as to meeting the growing need of the banking field and

coping with the changing environment of the country.

UBL SPORTS COMPLEX

In addition to providing professional banking services, the bank continued to play an

important role in the promotion of sports in the country. Towards this end, the bank

has already constructed a big sports complex in Karachi, where all types of facilities

for sports like cricket, hockey and flood light courts for tennis and basketball have

been provided.

CONSUMER BANKING

UTILITY BILL COLLECTION � UBL has over 1300 branches collecting electricity, gas, telephone and WASA, and

other utility bills like demand notice for telephone connection during business hours.

�

Almost all the branches have special utility bills collection counters with sun-sheltersand drinking water.

� Separate booths for utility bill collection are available at all major cities for the

convenience of the public.

� Branches in all major cities have electronic bill collection machines. And now-a-

days UBL management is trying to launch on-line banking system in all over

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 16/89

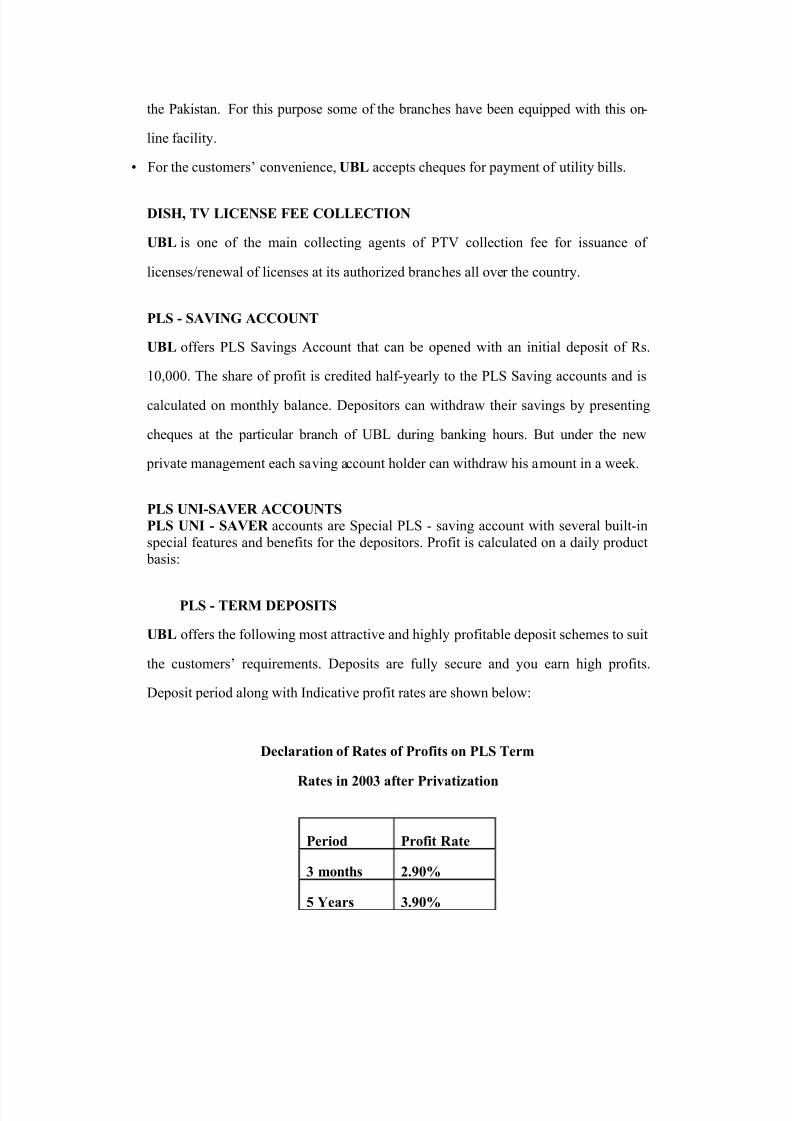

the Pakistan. For this purpose some of the branches have been equipped with this on-

line facility.

� For the customers¶ convenience, UBL accepts cheques for payment of utility bills.

DISH, TV LICENSE FEE COLLECTION UBL is one of the main collecting agents of PTV collection fee for issuance of

licenses/renewal of licenses at its authorized branches all over the country.

PLS - SAVING ACCOUNT UBL offers PLS Savings Account that can be opened with an initial deposit of Rs.

10,000. The share of profit is credited half-yearly to the PLS Saving accounts and is

calculated on monthly balance. Depositors can withdraw their savings by presenting

cheques at the particular branch of UBL during banking hours. But under the new

private management each saving account holder can withdraw his amount in a week.

PLS UNI-SAVER ACCOUNTS PLS UNI - SAVER accounts are Special PLS - saving account with several built-inspecial features and benefits for the depositors. Profit is calculated on a daily product

basis:

PLS - TERM DEPOSITS UBL offers the following most attractive and highly profitable deposit schemes to suit

the customers¶ requirements. Deposits are fully secure and you earn high profits.

Deposit period along with Indicative profit rates are shown below:

Declaration of R ates of Profits on PLS Term

R ates in 2003 after Privatization

Period Profit R ate

3 months 2.90%

5 Years 3.90%

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 17/89

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 18/89

PRODUCTS AND SERVICES

The bank provides its customer various products & services, to cater their need of

investments and other social or business requirements. These Product & Services

offered by the bank are as follows:

UNIZAR Following type of UNIZER accounts are available:

Current Savings Special notice Term deposit accounts

Deposits can be maintained in US$, and other currencies like Yen.

Your UNIZAR account is:

- Freely convertible.- Easily transferable.- Free from all exchange control regulations.- Worldwide access with the flexibility to operate internationally with

real convenience.- Take advantage of the appreciation of foreign currency.- Withdrawal of funds without any restrictions.- Free from all exchange control restrictions.

- The declared rates of profit on UNIZAR deposits for disbursement for the

half year 30-06-2000 is as follows:

SMALL BUSINESS SCHEME

Under the Small Business Scheme, UBL is providing loans on easy terms to those

who wish to set up their own small-scale business. This scheme is aimed at spreading

prosperity in the country by reducing unemployment. As more and more people start

their own industrial units, the country will move steadily towards economic self-

reliance.

The tax descriptions on the UNIZAR account:

Tax Type % Income fax NilWealth tax Nil

With-holding tax Nil

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 19/89

Zakat deduction Nil

The customers can open a UNIZAR account with foreign currency notes or a foreign

remittance in the form of:

j Drafts,

j Cheques,

j Money orders,

j Mail transfers,

j Telegraphic Transfers,

j Travelers Cheques,

j F.E.B.Cs.

j D.B.Cs., subject to rules.

UNICARD

UNICARD is valid throughout Pakistan and is accepted by:

j Airlines

j Prestigious hotels

j Hospitals

j Large super markets

j Petrol stations

j Prestigious stores

j Restaurants

j Supermarkets

With UNICARD there is no hassle of paying bills and counting cash. Just sign the

bills and take your leave.

UBL is the pioneer in introducing Credit Card Culture in Pakistan.

The UNICARD is like passport to carefree enjoyment.

UNICARD saves money of the holder: the holder of the UNICARD have a record of

all the expenditures.

UNICASH

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 20/89

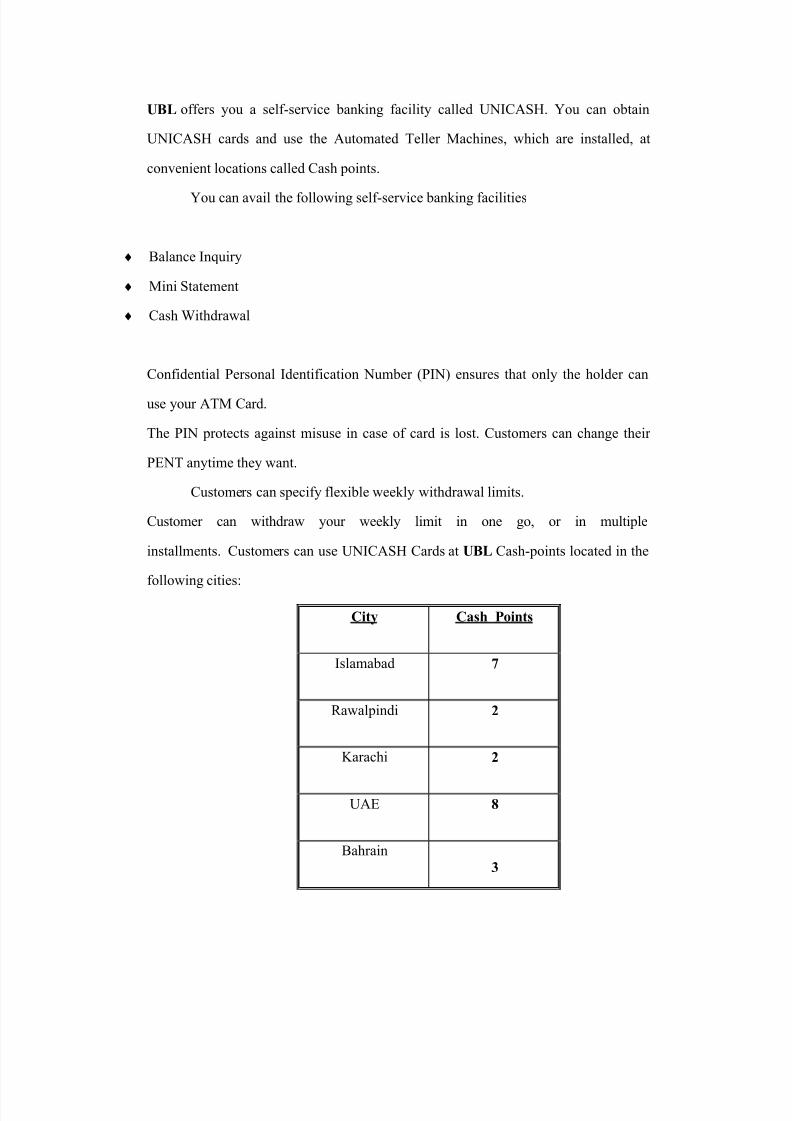

UBL offers you a self-service banking facility called UNICASH. You can obtain

UNICASH cards and use the Automated Teller Machines, which are installed, at

convenient locations called Cash points.

You can avail the following self-service banking facilities

j Balance Inquiry

j Mini Statement

j Cash Withdrawal

Confidential Personal Identification Number (PIN) ensures that only the holder can

use your ATM Card.

The PIN protects against misuse in case of card is lost. Customers can change their

PENT anytime they want.

Customers can specify flexible weekly withdrawal limits.

Customer can withdraw your weekly limit in one go, or in multiple

installments. Customers can use UNICASH Cards at UBL Cash-points located in the

following cities:

City Cash Points

Islamabad 7

Rawalpindi 2

Karachi 2

UAE 8

Bahrain3

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 21/89

RUPEE TRAVELLER CHEQUE

UBL offers the facility of the Rupees Traveler Cheque. UBL Rupee Travelers

Cheques are the ideal and safest way of carrying cash when traveling anywhere

in Pakistan.

y Used for conducting day- to-day business.

y No commission is charged from the purchaser.

y No excise duty on purchase.

y Easy to obtain and encash from all designated 350 branches of UBL.

y Acceptable all over Pakistan.

y Good until used and have unlimited life.

y Easily transferable like an order cheque.

CHAPTER NO. 2

DEPOSIT DEPARTMENT

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 22/89

DEPOSITS DEPARTMENT

Deposits act as a backbone of bank. It is the lifeblood of every bank. These deposits are

source of generating incomes for the bank and for the general public to meet the financial

needs. The supply of money in circulation is also affected by the amount of loans and

advances issued by the bank. The primary economic function of the commercial bank is to

receive the surplus saving money from the general public, individuals, firm, institutions,

public houses and companies and to pay the cheques drawn upon the bank.

The bank accepts the deposits at a low rate of interest and lends it at higher rate of interest,

the difference between the lending and accepting rate is the Source of income for the bank.

Keeping in view the above factors UBL offers the following types of accounts:

1) Current Account

2) Saving Account

3) Fixed Account

The classification of the deposits in to current, saving and fixed accounts is mainly on the

basis of duration and purpose for which the account is maintained at a bank

CURRENT ACCOUNT

Current account is running account because, customer can withdraw deposited amount at

any time, whenever he feels need. The customer can withdraw without any prior notice to

the bank. The bank has to pay the cheque provided within the limits of the account balance.

The main thing is that bank does not pay any kind of interest on current account.

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 23/89

The bank cannot invest the deposited amount under current account heading, because of

the fear of withdrawal. Bank has to keep with it a higher reserve ratio to meet the needs of

the current account holders.

SAVING ACCOUNT

Saving Account is an important source of funds for the bank. The purpose of this account is

to attract the small saving of the general public. Normally workers, schoolboys and

employees of the organizations use the saving account facility. UBL also provides this facility

to the general public against a certain rate of interest. The new name of this account is now

a day is PLS-Saving Account. If a customer wants to withdraw a large sum of money (above

15000), he will have to give a notice of 7 to 14 days in writing to the bank. Saving account

deposits provide a chance to the bank to invest safely, because customer can withdraw

small amount of balance.

FIXED OR TERM DEPOSITS

Fixed or Time deposits accounts are the major source of the capital for investment for the

bank and cannot be withdrawn as in case of the current account. The amount deposited can

be received back after a certain specified period of time. The rate of interest paid on fixed

Deposits is normally higher than saving Deposits. The rate of interest also varies due to time

period. After the expiry of the period the customer presents the receipt to bank and

received the amount in cash or bank added in the customer accounts as agreed between

bank and customer.

OPENING OF THE NEW ACCOUNT

A customer can open the following three types of accounts:

1) PLS-Saving Account

2) Current Account

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 24/89

3) Fixed Account

1) Opening of saving Account

Saving account is also divided into two types further,

I. Individual saving account

II. Joint Saving Account

I. Opening of Individual Saving Account

An individual person can open this type of account. UBL has defined the following

procedures for the opening of individual saving account:

Signature specimen card, the bank to get authorized signature of the customer as specimen

for avoiding any future discrepancy gives Customer.

Account opening form, when a customer comes to open the new account in the branch he is

given a printed form, to be filled by him. Account opening form consists of full name,

address, and date of birth, occupation, telephone number, and N.I.D. card number.

Guaranteed by the existing account holder, when the new account holder fulfills all the

requirements then he is asked to give some existing account holder guarantee, so that in

future the new account holder may not fraud with the bank.

II. Opening of Joint Saving Account:

Opening procedure for the joint saving is same as in case of individual saving account. Just

the difference is in the account opening form.

Signature specimen card is also used for the same purpose as for the individual saving

account, to avoid future discrepancy.

Account opening form, joint saving opening from has same information more than one time

because more than one person fills this form to open the account. Briefly is that no

one/single person can open this account, as a result it is called joint saving account.

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 25/89

Rules and Conditions for Saving Account:

The account opening person knows the rules and conditions.

This account can be opened only with initially Rs. 100 not less than this amount.

1) PLS- Saving account may be opened by/in the name of individual or jointly, or by charitable

institutions or provident funds or other funds, associations, societies and firms or clubs.

2) For opening of this account application has to submit on the prescribed form by the bank.

3) Customers can deposit money in his account by using pay-in-slip.

4) Customer must check the signature of two officer of the bank on the deposit slip.

5) Withdrawal, depositor cant withdraw more than his balance or one quarter. At least 7 days

notice must be given to bank for withdrawal purposes.

6) Bank cant responsible for a cheque, which has been paid prior to receipt of written

instructions from the drawer countermanding payment.

7) The bank will take care to see that credit and debit entries are correctly adjusted, but if any

mistake is by the depositor/withdrawer than bank will not responsible for the loss.

8) If the account is closed the unused cheques must be returned to the bank for the

cancellation and the balance amount, if any must be withdrawn.

9) The profit or loss on the balance due at the time of death will be paid when bank will declare

its profit/loss for the half year.

10) Death of account holder, in absence of any instructions the credit balance outstanding in any

joint account in the name of two or more persons will be payable to the survivors.

11) The bank to the account holders will supply statement of account every quarter.

12) Amendments of rules, the bank have a right to amend, alter or add to any of these rules with

or without notice to the account holders.

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 26/89

2). Opening Of Current account

A person, businessman and organization can open the followingtypes of current account.

I. Joint Current Account

II. Individual Current Accounts

III. Sole proprietorship Current Account

IV. Partnership Current Account

I. Joint Current Account

More than one person can open joint current account. Minimum balance of this account is

Rs.l0, 000 approx. If a joint holder dies then bank holds the account and refers case to the

court.

Account opening form, this application form is divided into two sides and both sides have

same information which are details of signatory (A, B), name, occupation, nationality, place

and date of birth, national identity card number, business address, employer no. Etc.

II. Individual Current Account

Only one person can open individual current account. Minimum balance in this case is 2500,

if the balance in the account is less than this limit than bank sends a statement to account

holder to maintain the minimum balance. For withdrawal, checkbook is issued and used no

other instrument is used or accepted by the bank. Procedure for opening this account is also

same as in PLS-Saving account just the difference is in opening form information, required by

the bank.

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 27/89

III. Sole Proprietorship Current Account

In sole proprietorship organization a person invests his capital and devotes full time to his

business. Sole proprietor opens this account. Minimum balance that required in this account

is Rs. 1000. All the profit paid on balance will go to the sole proprietor only.

The account opening form of this account is different than others because this form is filled

in the name of the organization. The name of proprietor. Place and Date of birth,

Nationality, Passport number and National Identity Card number, have to mention on this

form.

Documents Required

Following documents certified copies are required with the application:

a) Most recent set of Account

b) Current Municipal Licensee

c) Commercial Registration Certificate.

IV. Partnership Current Account

Partnership current account can be opened with the name of Partnership Company. Before

opening of partnership account shareholders has to decide that how many partners have

right to sign on cheque. The procedure is same for opening such account; the difference is in

the account opening form. Account opening form shows the name in full, nature of business,

principal place of business, address, location, and telephone number, telex number. After

that this form is divided into four sides with the name of A.B.C.D. and showing the same

information mentioned earlier.

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 28/89

Rules and Conditions

1) Bank can close /down any account at any time upon 48 hours write notice, after the opening

of the account.

2) The account number should be mentioned on all correspondence with the bank when

deposits or withdrawals are made.

3) The account holder must maintain the minimum balance requirement that is Rs: 1000.

4) After six-month bank refuse the payment of the cheques (post dated cheques).

5) Bank will not make payment if cheque is made unauthorized.

6) Account holder who is unable to sign, he will affix his left-hand thumb.

7) The cheque amount should not exceed to balance of account.

8) Any person opening a current account is deemed to have read, understood and bound by

the bank rules and conditions of current account.

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 29/89

CHAPTER NO. 3

ACCOUNTS DEPARTMENT

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 30/89

ACCOUNTS DEPARTMENT It is said that accounts department is the backbone of the bank. It plays a vital role in

performing different banking functions. The accounts department atUBL Hussain Agahi

branch is performing its function manually. Different books of accounts relating with other

departments are maintained here. With the help of these books of accounts, accountant

prepares monthly, quarterly, semi-annually and yearly financial statements.

The working in accounts department mainly depends upon voucher system. For each and

every transaction-taking place in the bank vouchers are prepared and through these voucher

contra entries are passed under different heads.

FUNCTIONS OF ACCOUNTS DEPARTMENT

The accounts department performs the following functions:

(a) To prepare and maintain the vouchers.

(b) To maintain and update the ledgers for term deposits.

(c) To update general ledger.

(d) To prepare different periods statements.

Vouchers

Each and every transaction in the bank is made through vouchers; the final place is accounts

department for recording these vouchers. Officer in the accounts departments arranges

these vouchers according to heads of accounts. These vouchers are of two types:

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 31/89

1. Debit Vouchers

2. Credit Vouchers

These two vouchers are again classified into three following types of vouchers:

I. Cash Voucher

II. Clearing Voucher

III. Transfer Voucher

All the daily transaction in cash, transfer and clearing is done through these vouchers. A

sheet is prepared on which all the vouchers, passed during any one working day are

consolidated and summarized. This sheet is called supplementary sheet. It provides help in

preparing Cash Book.

There are two types of supplementary sheets:

Debit Supplementary Sheet:

In which all debit Cash Voucher, Clearing Voucher, Transfer Voucher are included.

Credit Supplementary Sheet:

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 32/89

In which all credit Cash Voucher, Clearing Voucher, Transfer Voucher are included.

Cash Book

It is maintained to keep the record of daily receipts and daily paid vouchers. Cashbook is

consisted on the opening balance and the closing balance of the day. For correct balance of

the cash book there is a need to arrange all the vouchers.

Ledger For Term Deposits

One of the functions of accounts department is to maintain and update the term deposit

ledgers and books manually. Term deposit receipt or TDR ledger is updated after every

month for estimation of profit on customer accounts. Accountant has to prepare different

ledger for all schemes of term deposit. With the help of TDR the accountant prepares

provisional ledger/Summary ledger and also statement of provisional expenses. The profit

after every six-month will be the expense of the branch.

Updating General Ledger

When vouchers are recorded in cashbook then the balance of each head ofaccount is

posted to its ledger account. There are two main heads of the general ledgers, Income

account & Expenditure account. All the accounts fall under one of these two main heads.

Separate ledger register is maintained for every head of account. InUBL all the daily

transactions in deposits, cash, clearing, transfer remittance, foreign exchange; advances are

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 33/89

performed through these daily ledgers. Accounts department Maintains and prepares the

following ledgers and books of accounts:

I. Daily General Ledger Expenses

II. Daily General Ledger Incomes/Receipts

III. Monthly General Ledger Assets

IV. Monthly General Ledger Liability

V. Daily General Ledger Zonal Expenses

VI. Daily General Ledger Inspection expenses.

VII. Daily General Ledger Regional Expenses

VIII. Daily General Ledger Audit Expenses

The format of the entire above ledger is approximately same. General ledger tells about A/C

No., description, previous Balance, Dr. amount, Cr. amount and running balance.

Preparation of Different Statements

Accounts department prepares these statements,

a) Statement of Affairs

b) Statement of provisional Income

c) Statement of provisional Expenses

d) Statement of Head office A/C

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 34/89

e) Balance confirmation Book/Report

f) Transfer Book

Statement of affairs is prepared yearly, consisting on the details about assets and liabilities

of the branch. This statement provides assistance in budgeting about branch. Statement of

provisional Income and expense is prepared monthly. Statement of account and balance

confirmation is sent to accounts holders.

LOCKERS

UBL is also providing lockers facilities to its customers. The account department also

maintains the record about lockers. The basic purpose of locker is to provide safe custody to

clients valuable ornaments, jewelry or documents. Almost in all branches, Lockers are

available in different sizes at different rates. For availing this opportunity, customer has to

open his account in the same branch/bank.

Locker Operating Procedure:

Bank provides an application form to the applicant who needs to operate a locker in the

branch. This application form contains all rules and regulation regarding to obtain a locker.

Specimen signature card is also filled in signed by the applicant. Bank assigns a password to

their customer for secrecy. Each locker has duplicate keys. One (master) key is kept by the

bank, and the other by the customer. In case of opening any locker, first of all master key is

applied and then the customer key. If the locker has been obtained jointly then at the time

of the opening, the person signed the application form, should be presented there

otherwise, the bank will not allow to operate the locker. Bank officer has to maintain the

following register for record keeping purposes of locker.

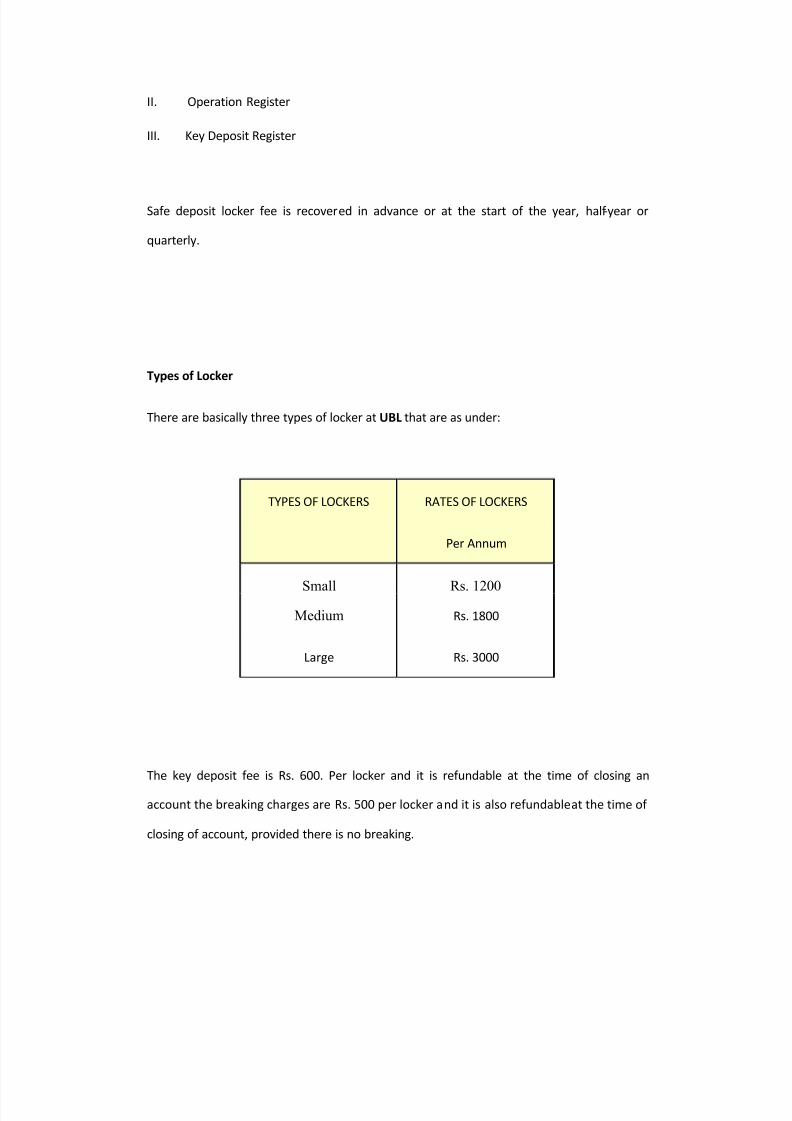

I. Locker Register

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 35/89

II. Operation Register

III. Key Deposit Register

Safe deposit locker fee is recovered in advance or at the start of the year, half-year or

quarterly.

Types of Locker

There are basically three types of locker at UBL that are as under:

TYPES OF LOCKERS RATES OF LOCKERS

Per Annum

Small Rs. 1200

Medium Rs. 1800

Large Rs. 3000

The key deposit fee is Rs. 600. Per locker and it is refundable at the time of closing an

account the breaking charges are Rs. 500 per locker and it is also refundable at the time of

closing of account, provided there is no breaking.

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 36/89

CHAPTER NO. 4

BILLING COLLECTION

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 37/89

BILLS DEPARTMENT

This department basically deals in bills, which come in bank for collection. The bills are

cheques, call deposit, drafts and pay order. These bills are from outstation branches

of UBL or of other banks. This department provides services to customers at low charges to

get their amounts from the nearest branch.

HEADS OF BILLS

There are two main heads of the bills i.e.

y Outward Bills For Collection (OBC)

y Inward Bill For Collection (IBC)

Outward Bills for Collection

Bills department receives cheques or other kinds of bills from its clients. The condition under

Outward Bills for Collection is that the customer must have his account in the branch. This

branch forwards the cheque with schedule or covering letter to that branch on which bill is

drawn. The checking officer of bills department will cross the cheque with special bank

stamp before forwarding the cheque to the other branch.

Outward bills for collection register

Outward bills for collection register is maintained in order to deep the records of all bills for

outward collections. This register is updated two times, first at time of receiving the OBCs

and secondly at the time when confirmation advice is received from the other branch, either

the cheque will be paid or not by the other bank branch. After confirmation of the amount,

confirmation advice is transferred to the sender branch. After confirmation of the amount

and bills, the account of the customer is credited against reasonable charges, which is

income for the bank.

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 38/89

Inwards Bill for Collection

These bills come to branch for payments so branch has to verify these cheques, pay orders,

drafts and call deposits etc. The party account must be opened in that branch which sends it

to paying branch .The responsibility under IBCs of the branch is to verify all the bills within

three days, and should send the bank advice to the originating branch.

Inward bills for collection register

Inward bills for collection register are maintained for future record purposes. Care is made

while posting the amount of bills in the register. Each bill is assigned a number according to

the register series. Every year the number starts from one and continues for the whole year

and next year again from one and so on.

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 39/89

CHAPTER NO. 5

CLEARING

DEPARTEMENT

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 40/89

CLEARING DEPARTMENT

This department welcomes the cheques and other negotiable instruments drawn upon local

branches of other banks. State Bank ofPakistan has a clearinghouse, in which the bank

representative brings cheques and other Institutions and mutual claims of each bank on

other are off set and a settlement is made by the payments. Clearing system is helpful for

both the customers and bank in saving of time, labor and currency involvement.

PROCEDURE FOR CLEARING CHEQUES AND INSTRUMENTS

UBL is a member of SBP and has an account with SBP. The clearinghouse of SBP, through

which branches forward and receive clearing cheques, with a schedule, conducts clearing.

The clerk of forwarding branch prepares the schedule and vouchers of all the clearing

cheque, which he received on that day and sends these cheques to the checking officer.

Checking officer passes these cheques and vouchers by his initials, endorsement stamp and

branch special crossing stamp. Clerk posts the contra entries of these vouchers in the

clearing register. At every day at about 9:05 a.m. Representative of all local banks are in

clearing house of SBP, to receive and forward the cheques.

PROCELURE FOR ADVISING H/O ACCOUNT

All the inter-bank adjustments will be effected through HO account, it will be essential for

the branches to advise head office account about every transaction. The SBP will send a

consolidated debit/credit advice to the branches in respect of clearing cheques delivered or

received from the branches. The amount of the advice will agree with total amount

appearing in the schedule of cheques delivered/received. Copies of all advice will be sent to

head office. The other branches will not send any advice to head office.

TRANSFER DELIVERY

Branch receives the cheques and other negotiable instruments drawn on other branches of

the same bank. Main branch of the UBL handles the transfer deliveries of cheques. The same

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 41/89

clearing cheque procedure will be adopted in the transfer delivery case except both availing

the facility of SBP, In case of cheque drawn on one branch and collected by another branch

for the credit of its constituents the branch delivering the cheques will send a consolidated

debit advice to the drawee branch. Clerk maintains the ledger for transfer deliveries, copies

of all the advice will endorse to head office as usual.

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 42/89

CHAPTER N0. 6

REMITTANCES DEPARTMENT

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 43/89

REMITTANCE DEPARTMENT

Transfer of money or equivalent to money from one branch to another branch of the same

bank is called remittance. Now it has become an easier and safer method both for the client

and banker to transfer their money from one branch to another within the city

or Outside City.

PARTIES INVOLVED

In case of remittances normally two banks are involved, are as under:

Originating Bank Branch

It is the branch, which issued the instrument for remittance.

Responding Bank Branch

The branch that receives the instruments for remittances, also known as drawees branch:

TYPES OF REMITTANCE

Remittances are classified into the following two types:

1) Inland Remittance

2) Foreign Remittance

1) Inland remittances

It is a transfer of money from one branch to another branch of the same bank within the

same country. In this case both the parties will be of the same country and same bank.

MODE OF REMITTANCES

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 44/89

United bank limited, uses following types for transfers of money:

1) Demand Draft (DD)

2) Pay Order (PO)

3) Mail Transfer (MT)

4) Telegraphic Transfer (TT)

1.

Demand Draft (DD)

A bank draft is an order instrument issued for payment of a certain sum of money to a

certain person. There are three parties involved:

Drawer: Issuing Bank.

Drawee: The bank on which the draft is drawn.

Payee: The name of person to whom the payment is to be made.

There are two types of demand draft, which are as follows

a) DD Issued

b) DD Payable

a) DD Issued

UBL has a standard application form that must be filled in by the customer for issuance of

Demand Draft.

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 45/89

The DD Application Form contains:

1. Applicants Name

2. Applicants Address

3. Signature of Applicant

4. In Favor of (Payees Name)

5. Drawn on (Name of Drawee Branch)

6. Amount in words and figures.

The Second Officer, Cash Officer and another authorized officer must duly sign this form.

The cheque of the showing the amount of the DD is attached with the application form. The

clerk prepares the demand draft when all the requirements are fulfilled. As a precaution, the

draft should be protecting graphed. In the case protect graph is not available, a sum of the

amount payable must be written in red ink preceded by the words UNDER or NOT OVER.

It is known as Protective Crossing or security notation. Demand draft is then recorded in

the DD issued register and credit advice is sent to the drawer branch.

Banks Charges

The bank recovers different types of charges from the applicant on issuance of DD, including:

I. Central Excise Duty

II. Commission

III. Tax

IV. Postage Charges

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 46/89

b) DD Payable

When the bank branch receives a credit advice issued by another branch and the title of the

advice is demand draft then this is called the Demand Draft Payable or the DD Payable.

Practical procedure regarding to the payment of demand draft, in the United Bank Limited

may be summarized as follows:

1. All drafts drawn on a branch should be routed through the General Ledger Accounts

Draft Payable of the Bills Payable Account. This account is credited by the drawer branch

on receipt of the cover in the form of IBCA.

2. Signatures should be verified on all drafts drawn on a branch.

3. Normally, payment of a draft should be made after receipt of a corresponding credit

advice. In case the advice has not been received, payment should be executed through the

approval of the Manager at the drawees branch who should satisfy himself with regard to

the authenticity of the draft in terms of signatures and otherwise.

4. On receipt of advice from the drawees branch, signatures should be verified if the

amount of a draft exceeds Rs.5000/-

5. The draft when paid should be marked in the DD payable register.

Essential Precautions at the Time of Payment

I. The instrument should be scrutinized properly with regard to name, Drawee branch,

amount in words and figures protect graphic and signatures of officers.

II. The payment should not be effected unless the payee has been identified to the

satisfaction of concerned officials at drawee branch.

III. Extra care should be exercised if the payee falls in the category of non-customers. It

would be better if an account holder verifies the identity of the payee, in such cases.

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 47/89

7. Payment Order (PO)

A bankers Payment Order is an instrument drawn by a banker on himself Implicit in a

payment order is an undertaking on the part of the banker to pay, a certain sum of money,

on the presentation of the instrument. The payment orders are generally issued for anyone

of the following practical purposes:

1. To facilitate all locally payable expenses on account of a bank for the reason that such

payments are not executed through cheques.

2. For the sake of inland and foreign remittances in case where the beneficiaries do not

maintain account with the bank.

3. For all local payments under instructions of the customers for sundry purposes like

payment of insurance premium, payments to third parties, club bills, rent and taxes etc.

The following contains stepwise procedural prescriptions pertaining to the issuance and

payment of payment order:

Issuance

I. For the issuance of payment orders, an application will be tendered on banks

standard form (F-34) by the purchaser giving his name and address thereof In case of

request from the bank s customer for the issuance of the payment orders, a letter in this

respect, will be obtained giving full particulars of the payee authorizing the bank to debit the

account.

II. The cost of the payment order along with an amount of Rs.5/- as commission plus

excise duty will be paid on the counter.

III. In case of letter of authority, the total amount i.e. payment order amount,

commission, excise duty and postage, if any, will be debited to the customers account as

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 48/89

per bank instructions and contra credit will be passed to Bills Payable Payment Orders

Account, commission, excise duty and postage account.

IV. The application for the issuance of payment order the Manager/Second Officer as

the case shall sign (F-34) may be if it is to be issued on bank account.

V. The particulars of the payment order shall be inserted on the blank payment order

leaf either through a typing machine or shall be neatly hand written using indelible ink. The

account shall also be rounded off through a protect graph machine or by hand on top of the

instrument.

VI. Subsequently, the particulars of each payment order shall be recorded in payment

orders issued register. The payment order shall be signed by two authorized officers of the

bank simultaneously authenticating entry in payment order issued register and after

verifying the following:

a) Name, code & address of the issuing branch.

b) Name of the payee.

c) Amount in words and figures.

d) Date of issue.

The amount is rounded off on top of the instrument either through protect graph machine

or neatly by hand-writing.

VII. A stamp containing the following stipulation shall be affixed on the back of each

payment order at the time of issue:

Received payment from United Bank Limited as over leaf on.

Account of______________

Date

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 49/89

VIII. The payment order, then, shall be delivered to the purchaser or to the department

concerned against acknowledgment on the reverse side of F-34 as well as on the counter foil

of the payment order.

Payment

I. The payee shall be duly identified by a bank customer or by Manager / Second

Officer in case the payment order is presented for cash payment on the counter and it will

be ensured that the payment order is properly receipted on its reverse on appropriate value

or revenue stamps.

II. The payment order will then be entered in payment orders issued register after

marking the date of payment against the date of issue in the contra columns under

authentication.

III. The payment order will then be passed for payment as per bank instructions.

IV. The procedure as given above will be adopted in case of all payment orders received

for payment, except that usual precautions shall be observed to ensure that the bank stands

discharged from the payment in due course.

3) Mail Transfer (MT)

Some times a constituent of a bank wants to transfer funds from one account to another or

a non-constituent wishes to remit funds in a particular account maintained at some place

with a branch of the bank or when the accounts are transferred from one branch to another

branch, such amounts/balances areremitted by means of mail transfer. The procedure for

issuance of a mail transfer is the same as discussed for drafts except that the applicant is

provided with a memorandum for money received from him for the issuance of a mail

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 50/89

transfer on a particular branch of the bank. The payee must be an account holder (customer)

of the drawee branch.

PAYMENT OF MT

The procedure for payment is as follows.

I. On receipt of advice from drawer branch, the test should be verified if amount

exceeds Rs. 5,000.

II. The particulars of MT should duly be entered in MT payable register.

III. Following vouchers should be passed after the test has been verified

Dr. Head Office Account Drawer Branch.

Cr. Bills Payable Account MT payable.

IV. When the customers account is to be credited, the following entries are passed:

Dr. Bills Payable Account- MT Payable

Cr. Customers Account.

V. If the payment is to be effected in cash, the entries are:

Dr. Bills payable Account- MT payable

Cr. Cash.

Before making the payment of MT, the drawee branch must ascertain the following:

It is drawn on the same branch.

Payee has signed the revenue stamps of adequate amount.

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 51/89

Payee is properly identified.

Telegraphic Transfer (TT)

Generally a mail transfer advice reaches the drawee branch the next day, when courier

arrangements exist. However, when it is sent through post offices, it usually takes 2 to 3

days to reach its destination. But sometimes an individual whether customer or not,

demands that his funds should be transferred from one place to another through the

quickest means. In such cases, transfer of funds message is passed on through a telegram,

ordinary or express, to the drawee branch of the bank. A tested message is sent to the

drawee branch followed by the confirmation copy. In case the payment is immediately

required by the payee, the tested message is given on the telephone.

Besides normal charges as those recovered on issuance of demand draft, the bank charges

one additional expense i.e. Telephone Charges of amount Rs.100 from the customer.

Payment of TT

A TT facilitates urgent transfer of funds either by a telegram or through telephone. A step-

wise procedure relating to the payment of TT at the drawee branch is as under:

1. The drawee branch receives message either on telephone, or through telegram. In case of a

telegraphic conversation, the concerned official at drawee branch should ask for the proper

identification of the official at the drawer branch. Whereas the message should be decoded

in case of telegram.

2. The particular of the TT should duly be entered in the TT payable register.

3. In case where the customers account is to be credited, following entries be passed:

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 52/89

Dr. TT Account Drawer Branch

Cr. Bills Payable A/C _ TT Payable

Dr. Bills Payable A/C _ TT payable

Cr. Customer s Account.

4. In case where the payment is to be effected in cash, the following vouchers shall be passed:

Dr. Bills Payable A/C TT Payable

Cr. Cash

5. TT should be paid after proper identification.

With-in the country or from abroad, UBL offers the most efficient and price competitive

services. With its large network of branches, it is poised to offer service almost at doorstep

of the customers. UBL is a member of SWIFT

(Society for Worldwide Interbank Financial Telecommunications). It is now the privatized

commercial bank to link up with three international points,Dubai,London and New York.

This enables the Bank to provide secure transmission of foreign exchange payments for

trade, home remittances and other transfers in a fully automated manner.

Tez Raftaar

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 53/89

UBL's new remittance service, TezRaftaar offers all overseas Pakistani people the fastest and

the most convenient delivery of their money to their beneficiaries in Pakistan. Best of all,

TezRaftaar is completely cost free and is available at allUBL branches along the Bank's

Network in the Middle East,UK and US.

TezRaftaar has following features:

j Guaranteed delivery within 24 hours to your given address in Pakistan.

j Doorstep delivery by authorized courier or credited to the recipient's account.

j Free of charge transfer service.

j Open to all including those who are not UBL account holders?

j Complete reliability of transaction.

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 54/89

MONEY GRAM

Money gram service is a

person-to-person international money transfer service that allows consumers to

send/receive money around the world in minutes, with no bank account required.

FEATURES OF MONEY GRAM

FAST

With money gram your money can be transferred from almost any country in the world

because it is a reliable and trusted way to send/receive money worldwide.

SAFE

The money gram service is used around the world because it is a reliable and trusted way to

send/receive money worldwide.

CONVENIENT

More than 50,000 MoneyGram agent locations in more than 150 countries; computer

networked to ensure that your money is transferred within minutes.

Easy: (How to Receive your transfer)

1- Sender abroad goes to nearest MoneyGram representative, fills out a form, hands in the

amount he wishes to send and the send (service) fee**, and shows an I.D.

2- Upon completing the transaction, sender will be given a transaction reference number.

3- Sender calls the receiver and informs him of the transaction reference number and the

amount of money sent.

Time is Money, so dont keep your family waiting

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 55/89

4- Receiver can go to any MoneyGram representative, show an I.D, fills out a simple form

mentioning senders name and amount expected.

5- Receiving agent hands over the money to receiver.

NOTE: Currency exchange rate set by MoneyGram or its representatives will be

applied.

CHAPTER NO. 6

CASH DEPARTMENT

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 56/89

CASH DEPARTMENT

This is sensitive department of the branch. No other person is allowed to enter in the

premises of cash department. As obvious from name that this department deals in cash

deposits and payments. Cash department is performing its functions/dutiesmanually. For

payments and receipts, it has to maintain certain sheets, books of accounts and various

ledgers, which are as under:

1) Cash received voucher sheet

2) Cash paid voucher sheet

3) Token register

4) Transaction ledger

5) Pay-In-Slip record

6) Cheque book record

7) Cash balance book

PROCEDURE FOR CASH PAYMENTS

The instrument against which payment is made that is the cheque. Normally the cheques

come for payment in the branch are, cheques received at counter for payment and other

cheques are Clearing or Transfer Cheque. No payment is made against any other monetary

instruments.

Special Considerations When cheque is received for payment special care is taken about the signature of the

account holder, date, no cross or cutting in figures, signature at the back of the cheque

presented for payment. If any thing is found wrong then cheque is dishonored and is given

to customer for rectification. If the cheque is found valid in all respect then Token Clerk

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 57/89

assigns token to the cheque at the back. The same Token is given to the customer as a proof.

The next step is forwarding cheque to the accountant for the verification of the signature

with specimen card signature. If signature are not according to specimen card then the

cheque is returned to customer and token is taken back. In token register a note is written

that cheque returned unpaid. If signature are similar with the specimen card than cheque

amount is posted in Ledger Card/Transaction Ledger. Special care is given to the balance of

the account either favorable or unfavorable.

Overdraft Facility

If the balance in the account is less than the cheque drawn, then bank may extend O/D

facility to its customer but now-a-days this facility is not provided.

Withdraw Limits

If the cheque is up to or less than 10,000 then officer can sanction and in case of greater,

than he has to get approved from his superiors. Finally, after all verifications of the cheque it

is given to the cashier, then payment is made to holder of the cheque. At the same time

cashier maintains the C ash Receive Voucher Sheet.The cashier performs all these duties

manually.

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 58/89

PROCEDURE FOR CASH RECEIVED

For depositing any amount in the account Pay-In-slip is used that is filled by the customer.

The pay-in-slip is consisted on date, A/C no., and particular about the amount to be

deposited in the account. The depositor signs the part of the paying slips, which are retained

by the bank to show acceptance about the entries, made in pay-in-slip. The pay-in-slip serves

as a voucher to Card/Transaction Ledger is only updated with pay in slip. The cashier checks

necessary details provided in the pay-in-slip and count the cash to be deposited and tally

with the figures written in pay in slip and in his hand/counter. If any mistake is found then

first that mistake/error is removed. If there is no one, than cashier fill inC ash Voucher

Received Record Sheet and assigns a voucher no. To both the transactions made in the sheet

and to pay-in-slip. This voucher sheet starts with one and continues for the whole day and

next day again started from one. If all is done well, than accountant authenticates the two

by signing on the two documents posting stamps on the slip. One part of the slip is given to

depositor, and other part is given to clerk for further posting in Ledgers.

The Cashier, at the end of the day has to maintain and balance the cashbook. The cashbook

contains the opening balance, details of payments and receipts. The Manager of the bank

signs the consolidated figures and written in cashbook as closing balance, which will the

opening next day.

Closing Balance = Opening Balance + Receipt - Payments

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 59/89

Chapter No. 7

Human Resources Department

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 60/89

Human Resources Department

Transfers & Postings

Scrutinizing bills (Hospital Bill)

Staff Deceased cases & its Correspondence

Retired employees Cases & its correspondence

All staff legal cases & Court at Multan & Lahore.

Retrenchment cases

Complaints and its correspondence

Fraud & Forgery cases

Mandatory Leaves and its observance.

Staff leaves and other related staff matters

Goals of all Staff

Monthly Statement of Staff

Disciplinary Action Cases

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 61/89

CHAPTER NO. 8

ADVANCES DEPARTMENT

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 62/89

ADVANCES DEPARTMENT

Credit is defined as the sale of goods, services and money claims in the present in return for

a promise to pay in the future. While in banking sector advance is the promise that carries

the repayment of the original amount plus an interest on the principal amount, extended as

advance. The credit/advance is given on the base of the confidence/trust and on the belief

that the customer will be able and willing to pay on the demand or at some future time.

The term credit may not be confused with term Debt. Credit and debt are merely the same

things looked at from two different points of view. When a lender extends credit, the

borrower acquires it. The lender or the creditor has the right to get back payment and the

borrower has the obligation to pay back. Credit can be defined in these words: credit is the

right to receive payment or the obligation to make payment on demand or at some future

time on account of immediate transfer of goods. The first phrase right to receive payment

is used from the point of view of the creditor, as he is to exchange present goods for the

right to receive payment in future. The second phrase, an obligation to make payment on

demand, which is from the debtor point of view. The debtor has an obligation to pay in the

future for the goods required. Credit and debt are two sides of the same shield.

PROCEDURE FOR ADVANCES

The credit officer will have to see the following information from the company:

Name of the Company

Legal Structure

Names of Principal Shareholders/Directors.

Line of Business.

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 63/89

Financial Standing & Respectability.

Repayment capacity/Behaviour.

Your Credit experience including the use of credit facilities.

For this purpose the credit officer takes following steps before advancing credit:

Step 1: Applicant is required to serve some documents to the credit officer whenever

required by him. These documents may include certified Financial Statements, legal

documents regarding property occupied by the borrower. And some other certificates

required by law and prudential regulations of State Bank ofPakistan like property deed,

mortgage of property etc.

Step 2: Now the credit officer will have to analyze the provided financial statements

critically. He will have to see the summary of financial health of the company, or

partnership or the sole trader ship. Then he will have to fill the form containing information

about:

Balance Sheet Line # 01-43

Income Statement Line # 44

64

Balance Sheet Reconciliation Line # 65-83

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 64/89

Analytical and Comparative Ratios Line # 84 - 136

In ratio anlaysis, credit officer has to see the Liquidity, Marketability, Profitability, and

Activity ratios. After this he has to see the comparative Operating/Non-operating Cash

generation statement.

Step 3: While doing this job the credit officer will have to see that the financial

statements are reflecting the true picture according to the GAAP or not, and must fulfill the

requirement of Checklist----Prudential Regulations. This form consists of three pages

regarding the subject matter. For this purpose he has to see the competitors, suppliers,

customers and bankers with whom he is dealing.

Step 4: If the credit officer is satisfied with the financial performance of the company

and other documents, he will write a credit approval containing the relevant information

about the business. He attaches these documents with the proposals he made and forwards

to the Zonal Office. The Zonal Office advance department ensures that the requisite

documents are in order. Further they applied various financial tests, client business

reliability and competitiveness. If the Zonal Chief has the power to sanction the loan, then

he will prepare the sanction advice and sent it back to the relevant branch. If beyond his

limits/powers then send it to regional office.

ELEMENTS OF CREDIT SELECTION

Five Cs are the main elements used for credit selection:

1- Character

The loan officer checks the character of the applicant, his family background, mode of living,

& business.

2- Capacity

The loan officer checks the paying ability of the applicant by his previous experience.

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 65/89

3- Capital

Loan officer checks the business capital and liquid assets worth.

8/4/2019 Report on Ubl 9900

http://slidepdf.com/reader/full/report-on-ubl-9900 66/89

4- Collateral

The loan officer checks collateral like stocks , bonds, B/Es,

5- Condition