Embed Size (px)

Citation preview

FORWARD SALE CONTRACT (FSC) SCHEME

TO FACILITATE THE DEVELOPMENT OF

AN ELECTRICITY FUTURES MARKET

IN SINGAPORE

REQUEST FOR INTEREST

23 MAY 2013 ENERGY MARKET AUTHORITY 991G ALEXANDRA ROAD #01-29 SINGAPORE 119975 www.ema.gov.sg

Disclaimer:

The information in this Paper is not be treated by any person as any kind of advice. The

Energy Market Authority shall not be liable for any damage or loss suffered as a result of

the use of or reliance on the information given in this Paper.

1

TABLE OF CONTENT

1. Executive Summary .................................................................................................. 2

2. Background ............................................................................................................... 4

3. Previous Public Consultation .................................................................................... 5

4. Summary of feedback and the EMA’s Assessment .................................................. 5

5. The Forward Sale Contract (FSC) scheme ............................................................... 8

6. Implementation Timeline ......................................................................................... 18

2

FORWARD SALE CONTRACT SCHEME (FSC) TO FACILITATE THE

DEVELOPMENT OF AN ELECTRICITY FUTURES MARKET IN SINGAPORE

REQUEST FOR INTEREST

1. Executive Summary

1.1. The Energy Market Authority (EMA) issued a public consultation paper on 22 October

2012 to seek feedback on the suggested implementation approach and roadmap for the

development of an electricity futures market in Singapore. The consultation exercise

closed on 19 November 2012 and stakeholders including generators, an exchange,

consumers and interested parties (such as potential new entrants) responded to the

consultation.

1.2. In the public consultation paper, the EMA requested feedback from stakeholders on the

Forward Sales Contract (FSC) scheme, which provides incentives for generators

through long term contracts of up to 3 years in return for them participating as market

makers in the electricity futures market. Market making (MM) requires the putting up of a

two-way pricing (i.e. both buy and sell) within a pre-determined price spread, and is

intended to create the liquidity for the establishment of the electricity futures market. The

EMA has further refined the FSC scheme after careful consideration of the feedback

received.

1.3. This paper provides details on how the FSC scheme works and the process for the EMA

to ascertain whether there is sufficient interest to proceed with the development of the

electricity futures market. There are two key stages in the process. In the pre-

qualification (Memorandum of Understanding (MOU) and proposal submission) stage,

an interested generator will submit to the EMA a signed MOU with an exchange of its

choice, together with a proposal specifying the pathway for the development of the

electricity futures market that is agreed between the interested generator and that

exchange for the EMA’s consideration. Upon the EMA’s review that the proposal

submitted is in accordance with the objectives of the baseline parameters specified in

this paper, the EMA will subsequently announce the exchange of industry’s choice. In

the event that more than one exchange is selected during this stage, the exchange that

is selected by the majority of the generators will be the exchange of industry’s choice. A

generator who did not select the exchange of industry’s choice as its choice of

exchange can still proceed to the bidding stage but will have to work with the exchange

of the industry’s choice based on the proposal accepted by the EMA.

1.4. Generators who submitted an MOU (regardless of the exchange they have chosen) are

pre-qualified to proceed to the bidding stage. In this stage, pre-qualified generators will

submit a bid for the FSC volumes they would like to be allocated, in return for the MM

volumes they are willing to commit in the electricity futures market. The EMA will

subsequently inform the respective generators of the FSC volumes they have been

allocated, after which they will be required to work with the exchange of industry’s

choice to prepare for the launch of the electricity futures market, which should be no

3

later than 6 months after EMA has informed the generators of the FSC volumes they

have been allocated.

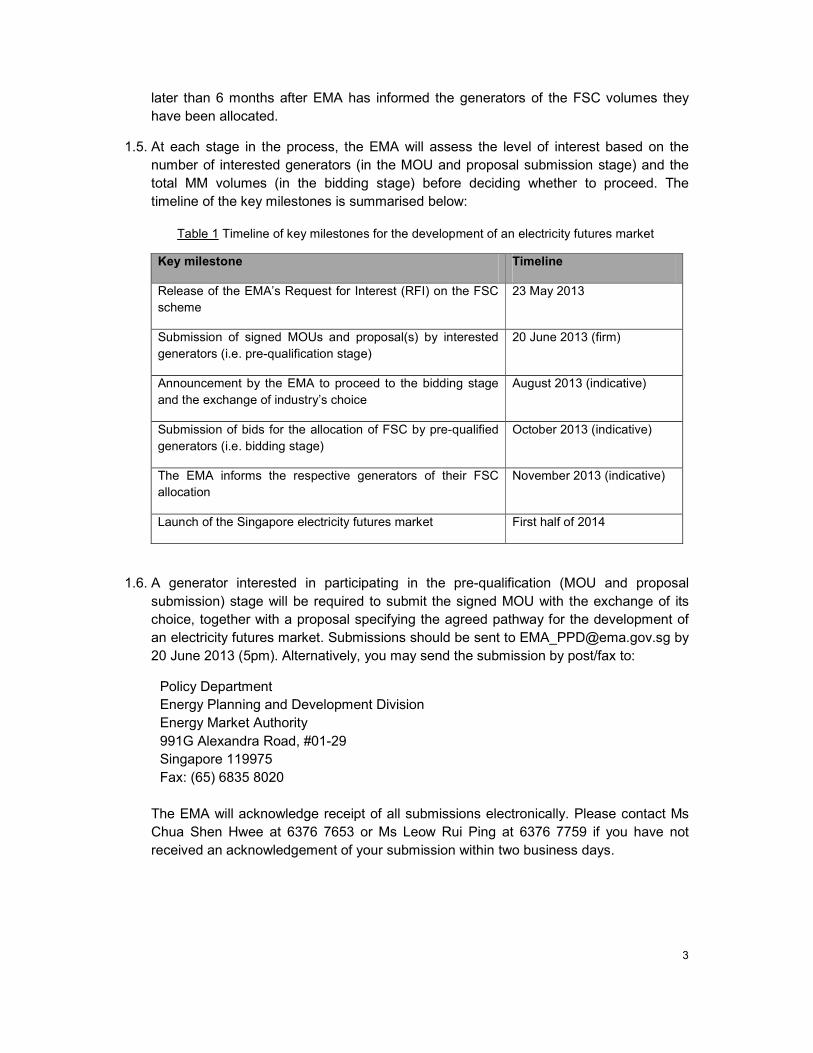

1.5. At each stage in the process, the EMA will assess the level of interest based on the

number of interested generators (in the MOU and proposal submission stage) and the

total MM volumes (in the bidding stage) before deciding whether to proceed. The

timeline of the key milestones is summarised below:

Table 1 Timeline of key milestones for the development of an electricity futures market

Key milestone Timeline

Release of the EMA’s Request for Interest (RFI) on the FSC

scheme

23 May 2013

Submission of signed MOUs and proposal(s) by interested

generators (i.e. pre-qualification stage)

20 June 2013 (firm)

Announcement by the EMA to proceed to the bidding stage

and the exchange of industry’s choice

August 2013 (indicative)

Submission of bids for the allocation of FSC by pre-qualified

generators (i.e. bidding stage)

October 2013 (indicative)

The EMA informs the respective generators of their FSC

allocation

November 2013 (indicative)

Launch of the Singapore electricity futures market First half of 2014

1.6. A generator interested in participating in the pre-qualification (MOU and proposal

submission) stage will be required to submit the signed MOU with the exchange of its

choice, together with a proposal specifying the agreed pathway for the development of

an electricity futures market. Submissions should be sent to [email protected] by

20 June 2013 (5pm). Alternatively, you may send the submission by post/fax to:

Policy Department

Energy Planning and Development Division

Energy Market Authority

991G Alexandra Road, #01-29

Singapore 119975

Fax: (65) 6835 8020

The EMA will acknowledge receipt of all submissions electronically. Please contact Ms

Chua Shen Hwee at 6376 7653 or Ms Leow Rui Ping at 6376 7759 if you have not

received an acknowledgement of your submission within two business days.

4

2. Background

2.1. The National Electricity Market of Singapore (NEMS) has been in operation since 2003

with the objective of promoting the efficient supply of competitively priced electricity. It

comprises a spot wholesale market for energy, regulation and reserve electricity

products. The electricity retail market has also been gradually liberalised, where non-

residential consumers with an average monthly consumption above 10,000 kWh can

choose to be contestable. There are also plans to further expand retail contestability

with a lowering of the contestability threshold to 8,000kWh (in Apr 2014) and 4,000kWh

(in Oct 2014).

2.2. The development of an electricity futures market, which supports the trading of “forward”

electricity products, will complement both the existing wholesale and retail electricity

markets. It is also a platform for industry players and financial intermediaries to use

electricity and related financial instruments for risk management and investment

activities. The outcome is a more efficient supply of electricity in the wholesale and retail

markets, which will benefit industry stakeholders and electricity consumers. Given the

size of Singapore’s market, the key challenge to the development of the electricity

futures market is to ensure sufficient initial liquidity.

2.3. The development of an electricity futures market will benefit stakeholders across the

industry as it is an effective platform for efficient trading to manage volatility and mitigate

risks, including addressing any imbalances in demand and supply in the electricity

market.

- For the generators, the electricity futures market provides an additional option to

manage their commercial and operational risks.

- For contestable consumers, the futures market provides an additional platform for

them to lock in long term prices, and at the same time enables them to view the

forward electricity prices as a reference for their electricity retail packages.

- For potential new entrants, the electricity futures market will help to lower barrier

to entry for the electricity market by providing new independent retailers the

option to use the futures market to secure fixed price contracts for their

consumers. This will enhance retail competition to the benefit of consumers.

2.4. The EMA issued a public consultation paper on 22 October 2012 to seek feedback on

the suggested implementation approach and roadmap for the development of an

electricity futures market in Singapore. In the public consultation paper, the EMA

requested feedback on the FSC scheme, which provides incentives for generators

through long term contracts of up to 3 years (FSCs), in return for them participating as

market makers in the electricity futures market. The EMA has further refined the FSC

scheme after careful consideration of the feedback received.

2.5. This paper sets out the process for the EMA to ascertain whether there is sufficient

interest to proceed with the development of an electricity futures market.

5

3. Previous Public Consultation

3.1. The EMA received feedback from the following group of stakeholders (see Table 2). The

respondents’ feedback and EMA’s corresponding responses are detailed in “Response

to Feedback on the Development of an Electricity Futures Market in Singapore’” set out

in Appendix 1.

Table 2 Stakeholders who provided feedback to the EMA’s consultation

Stakeholder Group Respective Parties

Licensees • PacificLight Power

• Senoko Energy

• Tuas Power Generation

• YTL PowerSeraya

Financial institutions • Singapore Exchange Limited (SGX)

Consumers and other

interested parties

• Changi Airport Group (CAG)

• Origin Energy

• Petrochemical Corporation of Singapore (PCS)

• Panasonic Corporation

• Singapore Oxygen Air Liquide (SOXAL)

• The Pwee Foundation

4. Summary of feedback and the EMA’s Assessment

4.1. Feedback from the licensee(s)

4.1.1. The generators generally recognise the benefits of an electricity futures market

which provides them with more risk management and hedging options. Some

generators have raised concerns over the actual delivery of benefits due to the lack

of liquidity and the costs of trading in such a market, and also whether standardized

futures contracts are better than existing hedging mechanisms such as customised

over-the-counter (OTC) contracts. In addition, several generators have raised

specific questions with respect to the electricity futures market product

specifications and requirements.

4.2. Feedback from the exchange(s)

4.2.1. The EMA notes the divergence in views over the proposed FSC scheme. This is in

contrast with the comments by most generators who generally prefer the phased

approach indicated in the public consultation paper which allows for gradual build-

up of skills and capabilities in futures trading. SGX’s feedback is for an accelerated

pathway through more stringent specifications on the market makers to build up the

initial liquidity.

4.3. Feedback from the consumer(s)

4.3.1. Some consumers asked whether the development of an electricity futures market

could create additional volatility in their electricity prices and whether there are

6

safeguards in place for consumers. In addition, there are concerns raised about the

benefits of such a market, including how an electricity futures market can enhance

competition in the wholesale and retail electricity markets, given the size of the

electricity market in Singapore and the vertical ownership structure between most

generators and retailers.

4.4. The EMA’s Assessment

4.4.1. Based on the feedback received in response to the public consultation paper, the

EMA has further refined the details of the FSC scheme. One key principle the EMA

has taken into consideration is for the participation in the electricity futures

market to be voluntary. The electricity futures market is intended to be an

additional platform for stakeholders to use electricity and related financial

instruments for risk management and investment activities, and complement the

other market platforms that are already available. As such, the successful

development of an electricity futures market should not result in stakeholders being

worse off compared to the existing arrangements. In particular, participation in the

FSC scheme and trading in the electricity futures market is voluntary for the

generators. This will allow the electricity futures market to work in tandem with

existing mechanisms such as the OTC trading activities. Similarly, from the

perspective of electricity consumers, the electricity futures market is not intended to

replace the existing mechanisms to hedge their electricity purchases, but to provide

an additional option for consumers to manage their risks.

4.4.2. In addition, in response to the feedback on whether the benefits of an electricity

market will materialise, the EMA has refined the process for the implementation of

the FSC scheme and will only proceed with the development of the electricity

futures market if there is sufficient interest from the generators and exchange(s).

Stakeholders should assess the benefits and costs of participating and operating

such a market when deciding whether to participate in the FSC scheme. In addition,

proposals put forth by the generators and any interested exchange will be required

to be commercially viable, where the costs of the setting up and running of the

market should be recovered from participants in the electricity futures market

through the trading fees charged by the exchange. This will ensure that the

electricity futures market is commercially sustainable over the long term.

Stakeholders, including generators and consumers, can take into consideration the

cost of trading in such a market before deciding whether to participate in the

electricity futures market.

4.4.3. The EMA notes the comments from the generators and the exchange with respect

to the product design and specification of the electricity futures contract. In

designing the FSC scheme including the baseline requirements for the MM

obligations, the EMA has provided scope for the generators and the exchange of

choice to work collectively when determining the market parameters and product

specifications. Hence, the FSC scheme has been refined to allow the generators to

partner an exchange to put forth an appropriate commercial proposal for the EMA’s

consideration. This ensures that the hedging needs of industry stakeholders are

adequately met and also enables the stakeholders to take ownership of the

7

development of the electricity futures market, and for the market to be self-

sustaining in the long term.

4.4.4. With respect to feedback on whether the development of an electricity futures

market will create additional volatility in electricity prices, one of the key benefits of

the electricity futures markets observed in other jurisdictions is that it enables

stakeholders including generators and consumers to manage their risks more

effectively by allowing them to lock in prices for future periods. Hence, the

successful development of an electricity futures market can in fact help consumers

reduce their price volatility. Even if consumers do not choose to hedge directly in

the electricity futures market, the futures market will bring benefits through

enhanced competition in the wholesale and retail markets and the provision of

greater price transparency through the forward price curves established in the

futures market. For example, contestable consumers can access the forward

reference market prices and use electricity futures price as a reference price,

amidst other considerations, before making informed decisions on their electricity

retail contracts. In addition, participation in such a futures market is voluntary –

consumers can make commercial decisions on whether to hedge their electricity

purchases through this market based on considerations such as their risk profile.

The EMA agrees with respondents that it is important to ensure orderly trading

within the electricity futures market. A further refinement to the FSC scheme is that

during the pre-qualification and proposal submission stage, the EMA will require

generators to work with the exchange of choice to propose and highlight the

necessary safeguards to ensure orderly trading for EMA’s consideration.

8

5. The Forward Sale Contract (FSC) scheme

5.1. This section sets out the details of the FSC scheme to encourage the development of an

electricity futures market in Singapore.

5.2. FSC scheme

5.2.1. Under the FSC scheme, generators can choose to enter into FSCs, in return for

participating as market markers in the electricity futures market. The FSCs are fixed

volume indexed price contracts with generators on the sell side and the Market

Support Services Licensee (MSSL), i.e. SP Services, on the buy side.1 Given the

risks associated with MM requirements and corresponding costs, the FSCs provide

participating generators with a certain level of revenue certainty particularly in the

start-up phase where generators are building the necessary capabilities.

5.3. FSC Volume

5.3.1. The total volume for the FSC is 8,400GWh over the 3-year tenure, which is

approximately 6% (per annum) of the forecasted annual electricity demand from

2014 to 2016 (refer to Table 3 below). The volume of FSC (i.e. 700GWh per quarter)

is to be allocated evenly across all time periods in the quarter during the contract

duration.

Table 3 Computation of FSC volume based on forecasted annual electricity demand

Forecasted total annual

electricity sales2

Average forecasted

annual electricity

sales (2014-2016)

Total FSC Volume over

3 years3

Year 2014 2015 2016

Annual

electricity

sales

(GWh)

45,140 46,668 48,249 46,686 8,400

5.4. FSC Price

5.4.1. Participating generators can choose to peg their FSC price to the prevailing

Liquefied Natural Gas Vesting Price (LVP) or Balance Vesting Price (BVP).4 The

choice will be binary (i.e. there will be no weighted blend of both LVP and BVP) for

1 The EMA is in the process of amending the MSS License condition to incorporate FSC as a regulatory

contract to be entered by the MSSL when required by the EMA. As FSCs are voluntary for the generators, there is no need to modify the licence conditions for participating generators.

2 The annual electricity demand for the FSC scheme is based on the forecast as of March 2013. 3 Total FSC volume is computed as such: 6%*46,686GWh*3years (rounded to the nearest hundred). 4 The BVP, as used in the EMA’s Procedures for Calculating the Components of the Vesting Contracts,

refers to the price associated with a Balance Vesting Quantity, which is the Allocated Vesting Quantity less the LNG Vesting Quantity for each half hour period. This will follow the prevailing methodology under the procedures for Vesting Contracts.

9

the respective generators, and the generators will not be allowed to switch between

the price references during the tenure of the FSC scheme.5

5.5. Pre-qualification (MOU and Proposal Submission) Stage

5.5.1. There are 2 stages in the FSC scheme: the pre-qualification (MOU and Proposal

Submission) stage and the bidding stage.

5.5.2. Companies with a generator class of licence as of 20 June 20136 are eligible to

participate in the pre-qualification stage. In this stage, interested generator will have

to sign an MOU with an exchange of its choice.7 The MOU should indicate a

commitment by the generator to work with that exchange to develop an electricity

futures market, including the participation of the generator as a market marker.

5.5.3. In the event that more than one exchange is selected by generators during this

stage, the exchange that is selected by the majority of the generators will be the

exchange of industry’s choice. In such cases, all generators with an MOU

(regardless of the exchange they have chosen) can proceed to the bidding stage.8

5.5.4. In addition to the submission of the MOU, an interested generator will have to

submit a proposal for the EMA’s consideration specifying the pathway for the

development of the electricity futures market that is agreed between the generator

and that exchange based on the baseline parameters specified by the EMA in Table

5 of this paper.

5.5.5. A generator who submitted an MOU with an exchange that is not the exchange of

industry’s choice can still proceed to the bidding stage but will have to work with the

exchange of the industry’s choice based on the proposal accepted by the EMA.

5.5.6. The EMA will review the level of interest based on the number of interested

generators, as well as the proposals submitted to ensure alignment with the policy

objectives for the development of a liquid electricity futures market. This will be

followed by an announcement by the EMA on whether to proceed with the bidding

stage and if so, the announcement on the exchange of industry’s choice.

5 The reference prices (both LVP and BVP) are made available by the MSSL at least 7 days prior the start of the quarter.

6 Generation licensees with no generation capacity (i.e. the new power station is yet to be in commercial

operation) are eligible to participate in the FSC scheme. The end date of the FSC for such generators will be aligned with those of the other generators (i.e. the FSC will conclude at the same time for all generators). They can choose to commence their MM agreement and FSC together with the other generators at the start of the FSC scheme, or commence their MM agreement and FSC before commercial operation date of the new power station, whichever is later.

7 A generator can only submit one signed MOU to the EMA. 8 For example, if Generators A, B and C chose exchange X, while Generators D and E chose exchange Y,

exchange X will be the exchange of choice for the industry. The proposals submitted by Generators A, B and C in this case are likely to be broadly similar, since they are with the same exchange, though there could be variations in the MM arrangements between the exchange and the respective generators. Generators A-E can then proceed to the bidding stage and will have to work out MM arrangements with exchange X. In the event of a tie, the EMA will select the exchange based on the merit of the respective proposals.

10

5.6. Bidding Stage

5.6.1. In the bidding stage, a pre-qualified generator will be invited to submit a single bid

of its MM volume in exchange for the FSC volume it would like to be allocated. After

the bidding stage, the EMA will assess whether the MM volumes submitted is

sufficient for a liquid electricity futures market to be launched and subsequently

inform the generators the volume of FSC allocated and the expected MM volume.9

5.6.2. If the total FSC bid submitted by the generators exceeds the FSC volume that the

EMA is prepared to allocate, the EMA may choose to limit the FSC volumes and the

corresponding MM obligations for all participating generators. In such an event, the

EMA will inform the respective generators of the revised FSC volumes and MM

obligations.

5.7. FSC Allocation

5.7.1. The allocation of the FSC volume will be based on the MM volumes for Phase 3.

Pre-qualified generators, can sign up for either of the schemes, depending on the

commercial preference of the respective generators.

(i) Scheme A : FSC allocation with a minimum bid of 1.5MW; and

(ii) Scheme B: FSC allocation with a minimum bid of 3MW in Round 1 and

optional tranches of 0.5MW in Round 2.

The allocation rates for each scheme are detailed in Table 4.The methodology for

the allocation of FSC volumes is intended to encourage generators to sign up for

more MM volumes, which will in turn increase the liquidity in the electricity futures

market. Hence, more FSC volumes are allocated per MW of MM volumes in

Scheme B and for incremental volumes in Round 2 of Scheme B.

Table 4 FSC allocation schemes and rates

Scheme A Scheme B

MM

Volume

Total

FSC

Volume

(over 3

years)

Approximate

Rate of

Allocation

MM

Volume

Total FSC

Volume

(over 3

years)

Approximate

Rate of

Allocation

Round

1 1.5MW 420 GWh

280GWh per

MW of MM 3MW 1,400 GWh

467GWh per

MW of MM

Round

2 - -

0.5MW 370 GWh

740GWh per

MW of MM

9 For example, if a participating generator bids a total of 5MW MM volume in exchange for 2880GWh of FSC

volumes but is only allocated 2,140GWh of total FSC volume (over 3 years) for 4MW of MM volume (based on the FSC allocation rate under Scheme B detailed in Section 5.7), it will only be obligated to fulfil their MM obligations for 4MW with the exchange. However, there will not be restrictions on the generators having a commercial agreement with the exchange over and beyond the minimum MM volume used for the purpose of allocating FSC.

11

5.8. Participation by new generators

5.8.1. In the event that there is unallocated FSC volume after the bidding stage, new

generators within the tenure of the FSC scheme (i.e. prior to the end of Phase 3)

can apply to participate in the FSC scheme. This is applicable only for entities with

a generation licence after 20 June 2013. The end date of the FSCs for such

generators will be aligned with those of the other generators (i.e. the FSCs will

conclude at the same time for all generators). They can choose to commence their

MM agreement and FSC together with the other generators at the start of the FSC

scheme (i.e. Phase 2), or commence their MM agreement and FSC at the start of

the next quarter after the commercial operation date (COD) of their new power plant

(if their COD is later than the start of Phase 2).

5.8.2. There will not be any reallocation of the FSC volume with the entrance of new

participant(s) in the FSC scheme, i.e. FSC volume allocated to the generators will

remain unchanged.

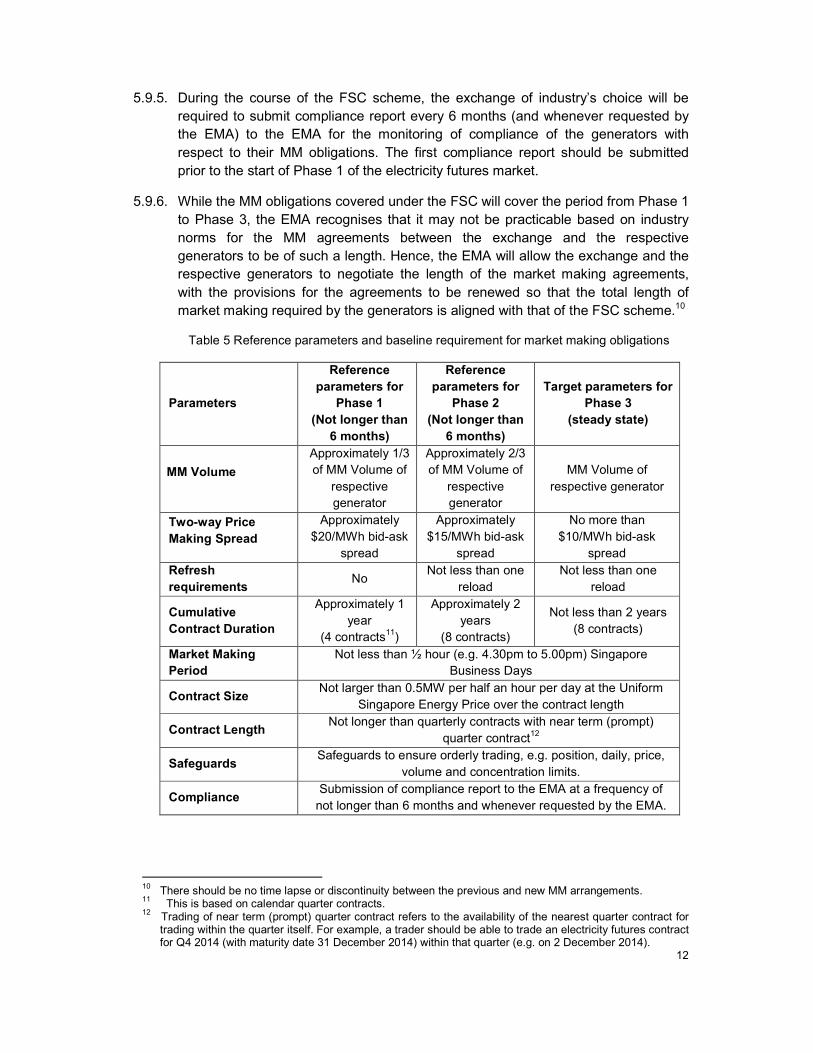

5.9. Baseline requirement

5.9.1. Table 5 describes the reference and target parameters for the electricity futures

market. To allow generators to build the necessary competencies for trading in the

electricity futures market, the development of the electricity futures market will be

staged in terms of both implementation and product type. Under the glide path or

phased approach, the MM volumes and the two-way price making spread will

increase and decrease respectively over three phases.

5.9.2. The reference parameters for Phase 1 and Phase 2, including the length of the

phases, allow generators to build up the necessary skill sets and competencies for

MM through a glide path approach. Phase 3 is the outcome (with the specific target

parameters) that the EMA seeks to achieve within 1 year after the start of the

market (i.e. at steady state). The FSCs will begin in Phase 2 and the total length of

Phase 2 and Phase 3 is 3 years.

5.9.3. In the proposal submitted to the EMA in the pre-qualification stage, interested

generator and the exchange of its choice will specify the pathway for the

development of the electricity futures market that is agreed between the generator

and that exchange based on the baseline parameters specified in Table 5. The

proposal(s) should also highlight the safeguards to be put in place by the exchange

and the generators to ensure orderly trading during each of the phases of the

development. In addition, to ensure that the generators comply with the baseline

requirement throughout the FSCs tenure, the proposal should specify the frequency

(e.g. 6 months and whenever requested by the EMA) for the exchange to submit

compliance report to the EMA.

5.9.4. The MM volume submitted in exchange for the FSC has to comply with the baseline

requirement specified in Table 5. In the event that any of the requirements are not

met as part of the MM arrangements between the generators and exchange, the

FSC will not be allocated to the generators.

12

5.9.5. During the course of the FSC scheme, the exchange of industry’s choice will be

required to submit compliance report every 6 months (and whenever requested by

the EMA) to the EMA for the monitoring of compliance of the generators with

respect to their MM obligations. The first compliance report should be submitted

prior to the start of Phase 1 of the electricity futures market.

5.9.6. While the MM obligations covered under the FSC will cover the period from Phase 1

to Phase 3, the EMA recognises that it may not be practicable based on industry

norms for the MM agreements between the exchange and the respective

generators to be of such a length. Hence, the EMA will allow the exchange and the

respective generators to negotiate the length of the market making agreements,

with the provisions for the agreements to be renewed so that the total length of

market making required by the generators is aligned with that of the FSC scheme.10

Table 5 Reference parameters and baseline requirement for market making obligations

Parameters

Reference

parameters for

Phase 1

(Not longer than

6 months)

Reference

parameters for

Phase 2

(Not longer than

6 months)

Target parameters for

Phase 3

(steady state)

MM Volume

Approximately 1/3

of MM Volume of

respective

generator

Approximately 2/3

of MM Volume of

respective

generator

MM Volume of

respective generator

Two-way Price

Making Spread

Approximately

$20/MWh bid-ask

spread

Approximately

$15/MWh bid-ask

spread

No more than

$10/MWh bid-ask

spread

Refresh

requirements No

Not less than one

reload

Not less than one

reload

Cumulative

Contract Duration

Approximately 1

year

(4 contracts11)

Approximately 2

years

(8 contracts)

Not less than 2 years

(8 contracts)

Market Making

Period

Not less than ½ hour (e.g. 4.30pm to 5.00pm) Singapore

Business Days

Contract Size Not larger than 0.5MW per half an hour per day at the Uniform

Singapore Energy Price over the contract length

Contract Length Not longer than quarterly contracts with near term (prompt)

quarter contract12

Safeguards Safeguards to ensure orderly trading, e.g. position, daily, price,

volume and concentration limits.

Compliance Submission of compliance report to the EMA at a frequency of

not longer than 6 months and whenever requested by the EMA.

10 There should be no time lapse or discontinuity between the previous and new MM arrangements.

11 This is based on calendar quarter contracts.

12 Trading of near term (prompt) quarter contract refers to the availability of the nearest quarter contract for trading within the quarter itself. For example, a trader should be able to trade an electricity futures contract for Q4 2014 (with maturity date 31 December 2014) within that quarter (e.g. on 2 December 2014).

13

5.9.7. The EMA is open to consider other commercial proposal(s) with baseline

requirements for Phase 113 and Phase 2 that fulfils the intended purpose of a

phased approach and at the same time enables the electricity futures market to

achieve sufficient liquidity at steady state. This will provide further scope for the

generators and the exchange of choice to find mutually agreeable pathways during

the initial stage of the development.

5.10. FSC Trial Phase

5.10.1. To allow the generators to build up competency and experience in trading and

market making in the electricity futures market, while limiting their risk and exposure,

generators have an option to exit the FSC scheme within the trial phase (i.e. Phase

1).

5.10.2. Generators who do not wish to continue market making in Phase 2 can withdraw,

but will be required to inform the EMA at least 3 months prior to the start of Phase

2.14 Such generators will not be considered as having breached the FSC scheme,

as the FSCs only commence at the start of Phase 2. In such cases, there will not be

any reallocation of the FSC volume to the remaining generators. Subsequent to that,

generators will not be allowed to exit from the FSC scheme, i.e. from Phase 2

onwards till the end of the scheme.

5.11. Breach of the FSC

5.11.1. Failure to maintain any of the obligations of the MM arrangements from Phase 2

onwards will be considered a breach of the FSC scheme by a generator.

Generators who breach the FSC scheme will be subject to a penalty of the FSC

mark-to-market in-the-money value for the entire FSC tenure plus 10% of the face

value of the entire FSC.15

5.11.2. The FSC penalty (if any) will be returned to contestable consumers through the

Energy Market Company (EMC). This is similar to existing arrangement on the

return of financial penalty to consumers through the Monthly Energy Uplift Charge

(MEUC).16

5.11.3. There will not be any reallocation of the FSC volume to other participating

generators in the event that there is a breach of the FSC by a generator, i.e. FSC

volume allocated to remaining generators will remain unchanged.

13 For example, Phase 1 can be replaced with a simulation exercise that will allow the generators to build trading competencies and the relevant skills for futures trading and MM.

14 The notice period of 3 months is set with the assumption that any changes to the FSC settlement will require a lead time of at least 3 months. This is similar to the lead time stipulated as part of the procedures for vesting contract level review.

15 All mark-to-market in-the-money benefits from the FSC plus 10% of the face value of the entire FSC from the start of the scheme to the end of the FSC tenure are to be returned to the consumers via the wholesale market with immediate effect for the nearest quarter prior to the end of the MM agreement and subsequently every quarterly. There will not be any return of the out-of-the money FSC payouts paid by the generators during the FSC tenure, i.e. any out-of-the-money payouts from the FSC are to be borne by the generators from the start to the end of the FSC tenure. The same penalties apply for generators who fail to give the three-month due notice to the EMA for their intention to exit the FSC scheme during the trial phase.

16 Refer to Chapter 7 of the Market Rules for details of the return of financial penalties through the MEUC.

5.12. FSC Settlement

5.12.1. The allocated FSC volume for each participating generator will be equally

distributed across all day and

(i.e. from the start of Phase 2 to the end of the scheme).

against the Vesting Contract Reference Price (VCRP)

average price per MWh received by

produces in the relevant trading period

5.12.2. Given that the primary beneficiaries of the electricity futures market will be the

contestable consumers, the FSC will be spread across all

(i.e. any debit or credit from the FSC is to be spread across all

consumers’ load, similar to how the vesting contracts

The FSC debits/credits

credits line item.17

5.13. FSC Documentation

5.13.1. The FSC documentation is based upon a standard financial contract, the

International Swaps and Derivatives Association (ISDA) Master Agreement (Second

Edition, 2002), which is typically used between a derivatives dealer and the

counterparty when negotiating derivatives trad

provisions will be included in the 2002 ISDA Master Agreement as the Singapore

Electricity Addendum to the Master Agreement. The FSC will be detailed as a

Confirmation to the Addendum.

documentation. Figure

5.13.2. The participating generators and the MSSL will be the counterparties for the full set

of the FSC documentation (i.e. ISDA Master Agreement, Singapore Electricity

17 While the FSC debits/credits are to be subsumed under the existing vesting debits and credits line item for retail market settlement, the Veswholesale market, which preserves the principle of price transparency.

18 The ISDA is a trade organisation of participants in the market for headquartered in New York, and has created a standardised contract (tenter into derivatives transactions. set out the basic trading terms between the parties; each subsequent trade is then recorded in a Confirmation which references the Master Agreement and Schedule. For a copy of the 2002 ISDA MAgreement, please see www.isda.org

The allocated FSC volume for each participating generator will be equally

distributed across all day and period types for each quarter of the entire FSC tenure

(i.e. from the start of Phase 2 to the end of the scheme). The FSC will be settled

against the Vesting Contract Reference Price (VCRP), which is the weighted

average price per MWh received by each respective generator for the energy it

produces in the relevant trading period.

Given that the primary beneficiaries of the electricity futures market will be the

contestable consumers, the FSC will be spread across all contestable consumers

(i.e. any debit or credit from the FSC is to be spread across all

, similar to how the vesting contracts arrangements currently work

he FSC debits/credits will to be subsumed under the existing vesting debits and

The FSC documentation is based upon a standard financial contract, the

International Swaps and Derivatives Association (ISDA) Master Agreement (Second

Edition, 2002), which is typically used between a derivatives dealer and the

unterparty when negotiating derivatives trade. 18 The relevant Singapore

provisions will be included in the 2002 ISDA Master Agreement as the Singapore

Electricity Addendum to the Master Agreement. The FSC will be detailed as a

Confirmation to the Addendum. Figure 1 shows the structure of the FSC

Figure 1 Structure of FSC Documentation

The participating generators and the MSSL will be the counterparties for the full set

of the FSC documentation (i.e. ISDA Master Agreement, Singapore Electricity

While the FSC debits/credits are to be subsumed under the existing vesting debits and credits line item for retail market settlement, the Vesting Contract and FSC will be settled independently and itemised in the wholesale market, which preserves the principle of price transparency.

is a trade organisation of participants in the market for over-the-counter derivatives, and has created a standardised contract (the ISDA Master Agreement

transactions. The ISDA Master Agreement is usually combined with a Schedule to set out the basic trading terms between the parties; each subsequent trade is then recorded in a Confirmation which references the Master Agreement and Schedule. For a copy of the 2002 ISDA M

www.isda.org.

14

The allocated FSC volume for each participating generator will be equally

period types for each quarter of the entire FSC tenure

The FSC will be settled

, which is the weighted

for the energy it

Given that the primary beneficiaries of the electricity futures market will be the

contestable consumers

(i.e. any debit or credit from the FSC is to be spread across all contestable

currently work).

to be subsumed under the existing vesting debits and

The FSC documentation is based upon a standard financial contract, the

International Swaps and Derivatives Association (ISDA) Master Agreement (Second

Edition, 2002), which is typically used between a derivatives dealer and the

The relevant Singapore

provisions will be included in the 2002 ISDA Master Agreement as the Singapore

Electricity Addendum to the Master Agreement. The FSC will be detailed as a

shows the structure of the FSC

The participating generators and the MSSL will be the counterparties for the full set

of the FSC documentation (i.e. ISDA Master Agreement, Singapore Electricity

While the FSC debits/credits are to be subsumed under the existing vesting debits and credits line item for ting Contract and FSC will be settled independently and itemised in the

counter derivatives. It is ISDA Master Agreement) to

The ISDA Master Agreement is usually combined with a Schedule to set out the basic trading terms between the parties; each subsequent trade is then recorded in a Confirmation which references the Master Agreement and Schedule. For a copy of the 2002 ISDA Master

15

Addendum and FSC Confirmation). To facilitate the industry on the FSC

documentation, the EMA will convene an Industry Working Group for interested

stakeholders to participate in.

5.14. Market information access

5.14.1. To ensure a level playing field in the electricity futures market and to support the

development of a conducive trading environment, the EMA intends to review the

access of information to participants in both the wholesale and futures markets.

5.14.2. Based on a review of the existing physical market information disclosure and a

comparison with best practices from other electricity futures market, the additional

access to information should include, but not limited to generation outage plans,

forecast demand and prices and gas curtailment information. The EMA will be

issuing a separate consultation paper in due course on the review of the access of

market information.

5.15. Prudential Arrangement

There are further trading cost synergies that can be realised through the electricity

futures market, such as allowing the electricity futures contracts to be used to offset

the prudential requirements of market participants in the wholesale electricity

market. As an additional benefit, should the electricity market rules be amended in

future to allow this, for the tenure of the FSC scheme (i.e. up to the end of Phase 3),

only generators who participate in the FSC scheme will be allowed to benefit from

any corresponding prudential arrangements, in recognition for their contribution

towards the establishment of a liquid futures market. For generators who do not

participate in the FSC scheme, they will not enjoy the offsetting of any prudential

requirements during the tenure of the FSC scheme (i.e. up to the end of Phase 3).

5.16. Regulation of the Electricity Futures Market

5.16.1. The electricity futures contract will be regulated by the Monetary Authority of

Singapore (MAS) under the Securities and Futures Act (SFA), if it is launched on a

futures exchange already regulated by the MAS.

5.17. Summary of key changes

5.17.1. Table 6 provides a summary of the key changes (from the consultation paper) to the

implementation approach to the electricity futures market after assessing the

feedback from the public consultation exercise.

16

Table 6 Summary of key changes (from the consultation paper)

No. Key Features

Proposed changes Rationale

1 Two stage process for FSC

In addition to the submission of

MOUs during the pre-qualification

stage, the generator will have to

submit a proposal for the EMA’s

consideration specifying the pathway

for the development of the electricity

futures market that is agreed

between the generator and that

exchange based on the baseline

parameters specified by the EMA in

Table 5 of this paper.

The EMA will review the proposals

submitted to ensure alignment with

the policy objectives for the

development of a liquid electricity

futures market. This will be followed

by an announcement by the EMA on

the exchange of industry’s choice

and commencement of the process

for the bidding stage.

Feedback received from the generator(s) and exchange(s) suggests the divergence in views over the proposed FSC scheme, e.g. product design and specification of the electricity futures contract. As such, the EMA has sought to provide scope for the generators and the exchange of choice to work collectively when determining the market parameters and product specifications. Hence, the FSC scheme has been refined to allow the generators to partner an exchange to put forth an appropriate commercial proposal for the EMA’s consideration. This will ensure that the hedging needs of industry stakeholders are adequately met and also enable the stakeholders to take ownership of the development of the electricity futures market, and for the market to be self-sustaining in the long term.

2

Alterna-tives to Baseline require-ment

The EMA is open to consider other

baseline requirements for Phase 1

and Phase 2 that fulfils the intended

purpose of a phased approach and

at the same time enables the

electricity futures market to achieve

sufficient liquidity at steady state.

In addition to the rationale mentioned above, allowing for alternatives to the baseline requirements will provide further scope for the generators and the exchange of choice to find mutually agreeable pathways during the initial stage of the development.

3 Safe-guards

The proposals submitted to the EMA by interested generators will have to specify the safeguards to be put in place by the exchange and the generators to ensure orderly trading during each of the phases of the development.

Feedback from the consumers and other interested parties highlights concerns over additional volatility in electricity prices with the introduction of the electricity futures market. The EMA agrees with respondents that it is important to ensure orderly trading within the electricity futures market. As such, the FSC scheme has been refined to allow generators to work with the exchange of their choice to propose and highlight the necessary safeguards to ensure orderly trading in the electricity futures market.

4 Refresh require-ment

Refresh requirement is revised to be not less than one in Phase 3 (instead of the proposed single reload requirement followed by best endeavours).

Feedback received from the generator(s) suggests a preference for less onerous refresh requirement. However, to ensure continuous prices are available in the market for participants to enter and exit trading positions, the EMA is of the view that reload requirement should be no less than one.

17

No. Key Features

Proposed changes Rationale

5 Contract length

Minimum cumulative contract length in Phase 3 is two years (instead of the three years proposed). However, there is an additional requirement to have near term (prompt) quarter contract.

19

Feedback from the exchange(s) suggests a preference for shorter cumulative contract duration to increase the confidence of futures market participants in pricing their contracts. To balance the need to offer longer durations for hedging longer dated risks and the need to provide greater pricing confidence, the minimum cumulative contract duration has been revised to 2 years in Phase 3. Given that the tenure of most electricity retail contracts is 1-2 years, having a minimum cumulative contract length of 2 years will not compromise one of the objectives of the EMA which is to facilitate the entry of independent retailers in the market. Feedback from the generator(s) and consumer(s) indicates a preference for shorter length contracts to better align to generators’ planned maintenance schedule and to improve liquidity in the electricity futures market. While the EMA is of the view that variations of contract (e.g. monthly contracts) should be commercially negotiated, we assess that the prompt quarter contract will help to improve the initial liquidity of the electricity futures market.

6 FSC Volume

Volume allocated for the FSC scheme is a fixed MWh pegged at approximately 6% of the average annual electricity demand for three years from 2014 to 2016 (instead of the proposed from 2013 to 2015).

The EMA has reviewed and revised the three years average electricity demand forward to better reflect the energy demand condition during the tenure of the FSC.

7 FSC Allocation

The FSC allocation for participating generators will remain fixed for each generator for the entire FSC tenure. The FSC allocation rate for Round 2 in Scheme B is revised upwards to approximately 0.4% per MWh (instead of 0.3% per MWh). Please refer to Table 4 for the revised allocation rates in GWh.

Feedback from the generator(s) indicates the need for greater clarity on FSC allocation in the event (1) when participating generators exit or breach the FSC, or (2) when new generators subsequently bid for the FSC. In this regard, the EMA confirms that the allocation rate for participating generators will remain unchanged in these events. The EMA has further reviewed and revised the allocation rates on the basis of encouraging greater uptake of the FSC and

19 Near term (prompt) quarter contract refers to the availability of the nearest quarter contract for trading during the quarter itself. For example, a trader will be able to trade an electricity futures contract with maturity date 31 December 2014 on 2 December 2014.

No. Key Features

Proposed changes

8 FSC Settle-ment

Instead of the USEP, the FSC will be settled against the Vesting Contract Reference Price (VCRP), which is equivalent to the weighted average price per MWh received by the respective generator for the energy it produces in the relevant trading period.

9 Participa-tion by new generators

Instead of the the total FSC volumes for to new generators, new generators can apply for the FSC scheme only when there is unallocated FSC volume left after the bidding stage. In addition, instead of limiting new generators’ participation to Scheme A or Round 1 of Scheme B only, new generators can in either of the two schemes under the FSC scheme.

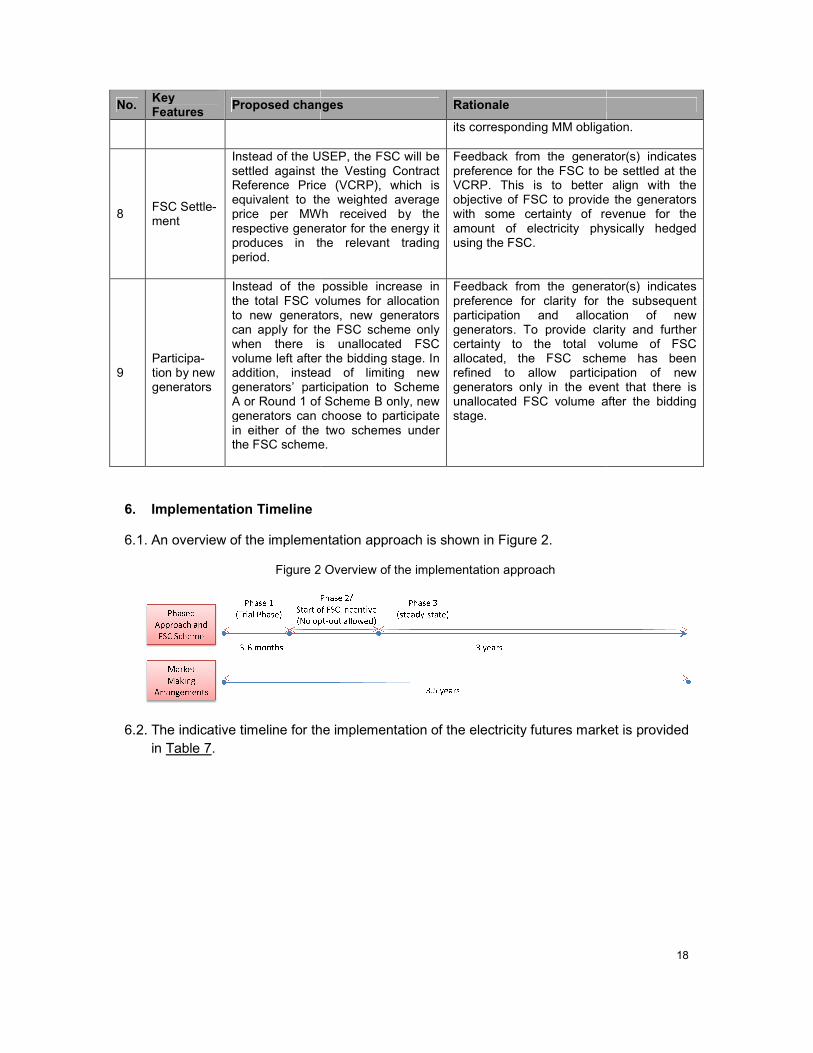

6. Implementation Timeline

6.1. An overview of the implementation approach is

Figure 2

6.2. The indicative timeline for the implementation of the electricity futures market is provided

in Table 7.

Proposed changes Rationale

its corresponding MM obligation.

Instead of the USEP, the FSC will be settled against the Vesting Contract Reference Price (VCRP), which is equivalent to the weighted average price per MWh received by the respective generator for the energy it produces in the relevant trading

Feedback from the generator(s) indicates preference for the FSC to be settled at the VCRP. This is to better align with the objective of FSC to provide the generators with some certainty of revenue for the amount of electricity physically hedged using the FSC.

possible increase in volumes for allocation

new generators, new generators can apply for the FSC scheme only when there is unallocated FSC volume left after the bidding stage. In addition, instead of limiting new generators’ participation to Scheme A or Round 1 of Scheme B only, new generators can choose to participate in either of the two schemes under the FSC scheme.

Feedback from the generator(s) indicates preference for clarity for the subsequent participation and allocation of new generators. To provide clarity and further certainty to the total volume of FSC allocated, the FSC scheme has been refined to allow participation of new generators only in the event that there is unallocated FSC volume after the bidding stage.

An overview of the implementation approach is shown in Figure 2.

2 Overview of the implementation approach

The indicative timeline for the implementation of the electricity futures market is provided

18

its corresponding MM obligation.

edback from the generator(s) indicates preference for the FSC to be settled at the VCRP. This is to better align with the objective of FSC to provide the generators

certainty of revenue for the amount of electricity physically hedged

Feedback from the generator(s) indicates preference for clarity for the subsequent participation and allocation of new generators. To provide clarity and further

tal volume of FSC allocated, the FSC scheme has been refined to allow participation of new generators only in the event that there is unallocated FSC volume after the bidding

The indicative timeline for the implementation of the electricity futures market is provided

19

Table 7 Indicative timeline for the implementation of the electricity futures market

Key milestone Timeline

Release of the EMA’s Request for Interest (RFI) on the FSC

scheme

23 May 2013

Submission of signed MOUs and proposal by interested

generators (i.e. pre-qualification stage)

20 June 2013 (firm)

Announcement by the EMA to proceed to the bidding stage

and the exchange of industry’s choice

August 2013 (indicative)

Submission of bids for the allocation of FSC by pre-qualified

generators (i.e. bidding stage)

October 2013 (indicative)

The EMA informs the respective generators of FSC allocation November 2013 (indicative)

Launch of the electricity futures market, i.e. commencement

of Phase 1

Submission of compliance report by the exchange

First half of 2014 (i.e. N)

Submission of notice (i.e. deadline) to the EMA by any

generator with the intention to exit the FSC scheme.

N + 3 months or less

Commencement of Phase 2 N + 6 months or less

Commencement of Phase 3 N + 1 year

6.3. A generator interested in participating in the pre-qualification (MOU and proposal

submission) stage should submit the signed MOU with the exchange of its choice

together with a proposal specifying the agreed pathway for the development of an

electricity futures market. Submissions should be sent to [email protected] by 20

June 2013 (5pm). Alternatively, you may send the submission by post/fax to:

Policy Department

Energy Planning and Development Division

Energy Market Authority

991G Alexandra Road, #01-29

Singapore 119975

Fax: (65) 6835 8020

The EMA will acknowledge receipt of all submissions electronically. Please contact Ms

Chua Shen Hwee at 6376 7653 or Ms Leow Rui Ping at 6376 7759 if you have not

received an acknowledgement of your submission within two business days.

20

Appendix 1

Response to Feedback on the

Development of an Electricity Futures Market in Singapore