Embed Size (px)

Citation preview

Savills World Research Ireland Residential

RESIDENTIALPROPERTYQ1 2015

SUPPLY

DEMAND

Transactional ActivityBuyer and Seller ProfilesSupply and DemandNew HomesRental MarketRegional Markets savills.ie/research

FIGURE 1Dundarave Estate, Bushmills, Co. Antrim

Sold by Savills Country HomesThis was the largest residential transaction (house & land) on the island of Ireland in 2014

Residential Property Q1 2015

MORE MODERATE PRICE GROWTHAHEAD AS RECOVERY BECOMES ESTABLISHED

reland’s economy expanded by almost 5% in the first three quarters of 2014 and GDP is now only 1.7% below the pre-recession peak in 2007.

The initial phase of the recovery was led by exports growth. However domestic demand is now also contributing positively to growth. Over 100,000 new jobs have been created since Q1 2012 and, since the beginning of 2013, the net gain has all been in full time positions. As a result, aggregate disposable incomes are now rising again, and this trend will gather further momentum as the labour market tightens and our improving public finances allow scope for fiscal easing.

The labour market recovery is feeding through to a palpable improvement in confidence, and macro-economic forecasts for the Irish economy are now likely to be upgraded following the ECB’s announcement of a massive quantitative easing (QE) programme on 22nd January. Not only will this cause the Euro to devalue further, boosting exports, investment and jobs growth, it should also lead to lower interest rates and an improved flow of credit. Partly offsetting this, however, are the new Central Bank restrictions on mortgage lending which will make it harder for First Time Buyers (FTBs), particularly single buyers in Dublin, to get started on the housing ladder. In saying that, we do not expect the Central Bank’s measures to have a major impact on house price growth. By diverting first time buyers into the private rented sector the new rules will initially drive up rents. In due course this will attract investors and the only long term effect will be on the mix of buyers.

Overall, then, the macroeconomic context remains broadly supportive for the housing market. Due to this, and the ongoing demand / supply imbalance, we expect further house price increases in 2015. However, as the base increases it naturally becomes more difficult to sustain very high rates of price growth. For this reason our view is that house prices will rise more moderately in 2015 than they did last year. ■

I

Source: PSRA

GRAPH 1Percentage Change in Residential Property Transactions

-40

-20

0

20

40

60

80

Q1

2011

Q2

2011

Q3

2011

Q4

2011

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

% C

hang

e Y/

Y

Dublin Outside Dublin

03

FIGURE 231-33 Merrion Road, Ballsbridge, Dublin 4

Launched by Savills New Homes in January 2015Exclusive 2 & 3 bed apartments

Residential Property Q1 2015

Source: Savills Research

GRAPH 3Investor Sales as Percentage of Total - 2014

0

5

10

15

20

25

30

35

40

45

Q1

Q2

Q3

Q4

% o

f Tra

nsac

tion

s

04

Transactional ActivityNationally, there were over 42,000 housing transactions in 2014 – a 41% increase on 2013. The increase was somewhat lower in Dublin at 34%. However, this does not appear to reflect any deterioration in liquidity – on the contrary, according to a recent Daft Report, more than 3,500 Dublin properties were listed for sale on December 1st 2014, an increase of more than one third on the same date 12 months previously.

Instead, we believe that the slower rate of transactions growth in Dublin is better explained by affordability – after two years of compounding house price growth in the capital, agents are reporting that buyers are now beginning to show signs of resistance to further increases. This is particularly evident at the upper end of the price spectrum where affordability issues, combined with a greater availability of stock in the €800,000 - €1.2m price range, have taken some heat out of the market. In saying that, the mid-range of the Dublin market remains quite active with a congested pool of FTBs, Traders-Up and Traders-Down competing for properties in the €400,000 - €600,000 bracket. Moving up a category, there is also strong competition from traders-up and down at the €600,000 to €800,000 level.

In terms of locations, the hot spots in Dublin continue to be in the south-side postcodes of Dublin 4, 6 and 6w. Demand also remains very strong in the affluent neighbourhoods of South County Dublin, particularly along the coast. On the north side of the city, there is strong demand in Castleknock and in the perennially popular coastal neighbourhoods which include Clontarf, Sutton and Malahide.

Despite the increase in overall transactions, market activity is recovering from a low base, and still appears to be at a subdued level compared with the UK. To illustrate, Scotland’s population is just 16% greater than that of Ireland, but Scotland had 68% more housing transactions in Q4 2014. Therefore we would expect to see further increases in transactions levels through the remainder of 2015.

Buyers InvestorsTwelve months ago we predicted that buy-to-let activity would taper off during 2014 as residential property yields continued to squeeze lower. Indeed, this trend was clearly evident in the first three quarters of the year. However, as shown below, there was a surge of buy-to-let activity in the closing months of 2014 and more than half of all investor sales for the year took place in Q4. This uplift was driven by a rush of investors seeking to avail of the Capital Gains Tax (CGT) incentive which expired in December. And, ultimately, it led to investors being the largest single group of buyers in 2014.

Source: Savills Research based on CSO, HMRC

GRAPH 2Housing Transactions Per 1000 of Population

0

1

2

3

4

5

6

England

Scotland

Wales

NorthernIreland

Ireland

Tran

sact

ions

/ 1

000

Q4 2013 Q4 2014

Two game-changing events took place in January which will impact on investor demand going forward. Firstly, a massive quantitative easing programme was announced by the ECB. One effect of this will be to depress the risk-free rate of return, and this will drive investors into higher yielding assets – including residential property. Secondly, as mentioned above, the new Central Bank mortgage lending rules will divert a proportion of would-be first time buyers into the rented sector. This will drive up rents and will ultimately lead to stronger investor demand. Our view is that these two developments fundamentally change the outlook for the investment market and, notwithstanding the removal of the CGT waiver, will ensure continuing strong interest from buy-

to-let investors. This demand is likely to remain focused on high quality apartment units in Dublin 2 and Dublin 4, along with period house conversions which offer small, self-contained, units that are easily managed.

First Time Buyers First Time Buyers were the second largest buyer group in 2014, accounting for over a quarter of all transactions. Indeed, their presence played a big part in the overall market pick-up during 2014 as first timers are inevitably the target market of families that are selling to trade up. Looking ahead, we expect first time buyers to remain active in 2015, particularly outside Dublin where the €220,000 threshold below which FTBs only have to save a 10% deposit offers significant choice. However,

Residential Property Q1 2015

GRAPH 5Cash Only Housing Transactions as a % of Total Transactions

4

14

28 33 36

41 44

48 47 45

39

63

54 49

56 54 52 49

53

0

10

20

30

40

50

60

70

Q2 2010

Q3 2010

Q4 2010

Q1 2011

Q2 2011

Q3 2011

Q4 2011

Q1 2012

Q2 2012

Q3 2012

Q4 2012

Q1 2013

Q2 2013

Q3 2013

Q4 2013

Q1 2014

Q2 2014

Q3 2014

Q4 2014

%

05

Source: Savills Research

GRAPH 4Percentage of Sales by Buyer Type - Volume

0

5

10

15

20

25

30

35

40

FTB Trading Up Trading Down 2nd Home Investor Developer Relocation

% o

f Tot

al

2013

2014

with fewer properties available at this price point in Dublin, many first time buyers will be forced into renting for longer. In saying that, the average age of first time buyers is now around 35, and many have accumulated sufficient savings to allow them buy their own homes in Dublin. These more mature first time buyers tend to bypass the traditional starter homes and go straight to 3 or 4 bed semi-detached properties (either newly built or second hand). Where budgets allow, they have a strong preference to locate as close to public transport links as possible. And, with one eye on the future, many are also buying with proximity to good schools in mind.

Where first time buyers are in their early to mid-twenties, family formation is usually not as high on the agenda. Instead a modern, well laid out, city apartment is the order of the day. Buyers in this age group tend to take more of a lifestyle approach in that they are happy to walk to work and want to enjoy all the social and cultural amenities that living in a European capital city has to offer.

Traders-UpTraders-up fell from being the largest group of buyers in 2013 (two fifths of all sales) to the third largest in 2014 (one quarter of sales). Interestingly, however, there are two contrasting cohorts within this category. The number of mortgage financed traders-up fell by 27% year on year. This may reflect the impact of tighter lending conditions on mortgaged buyers’ ability to close deals at higher price points in the market. In contrast, the number of people trading-up with cash actually increased by 13%, which confirms that there is still a weight of cash looking to mobilise in the Irish residential market.

Cash BuyersAs shown in Graph 5, cash deals have accounted for a declining proportion of total market transactions since the beginning of 2013 (although there was a spike in Q4 2014 due to an influx of cash funded investors ahead of the CGT deadline in December). However, following the ECB’s quantitative easing programme and the new Central Bank rules, our view is that cash funded investors will remain a significant part of the market in 2015. Because they are not limited by bank lending cash buyers tend to be less price sensitive. In this sense, their continued presence will be a factor in further house price growth through the remainder of 2015.

SellersA legacy of the recession is that forced sales have become a more

FIGURE 3Limasol, 6 Marlborough Road, Glengeary, Co. Dublin

Sold by Savills in November 2014

Source: PSRA, IBF and Savills Research

Residential Property Focus

06

Residential Property Q1 2015

Source: Savills Research

GRAPH 6Percentage of Sales by Seller Type - Volume

0

5

10

15

20

25

30

35

Rece

iver

ship

Selli

ng In

vest

men

t

Trad

ing

Dow

n

Trad

ing

Up

Relo

catio

n

Bank

Con

sens

ual S

ale

Deve

lope

r

Oth

er

%

2013 2014

06

FIGURE 416 Elgin Road, Ballsbridge, Dublin 4

Sold by Savills in December 2014

significant feature of the market in recent years. Receivership sales rose from less than one fifth of total transactions in 2013 to over 30% in 2014. In part this reflects the number of large residential portfolios that have been sold - either as direct assets or through loanbook sales - and are now being worked through. While the exiting foreign banks pioneered this approach its success in a rising market means that the domestic banks, which had previously been dealing with distressed assets on a more ad hoc basis, are now also adopting the wholesale model. With prices set to rise further this year we expect this to continue.

The second largest seller group in 2014 was investors who accounted for 25% of deals. This group was dominated by individual buy-to-let investors leaving the market. They are doing so for two reasons. Firstly, on the back of recent house price increases, some are taking the opportunity to cash-in and either cut their losses or exit with a gain. Secondly, the increased costs of managing properties, including the new property tax, have also pushed some smaller investors out of the market. Interestingly, investors have been very active on both the buy and sell sides of the market. This reflects a changing of the guard with opportunistic boom-time investors being displaced by a new breed of more professional, yield-driven investors.

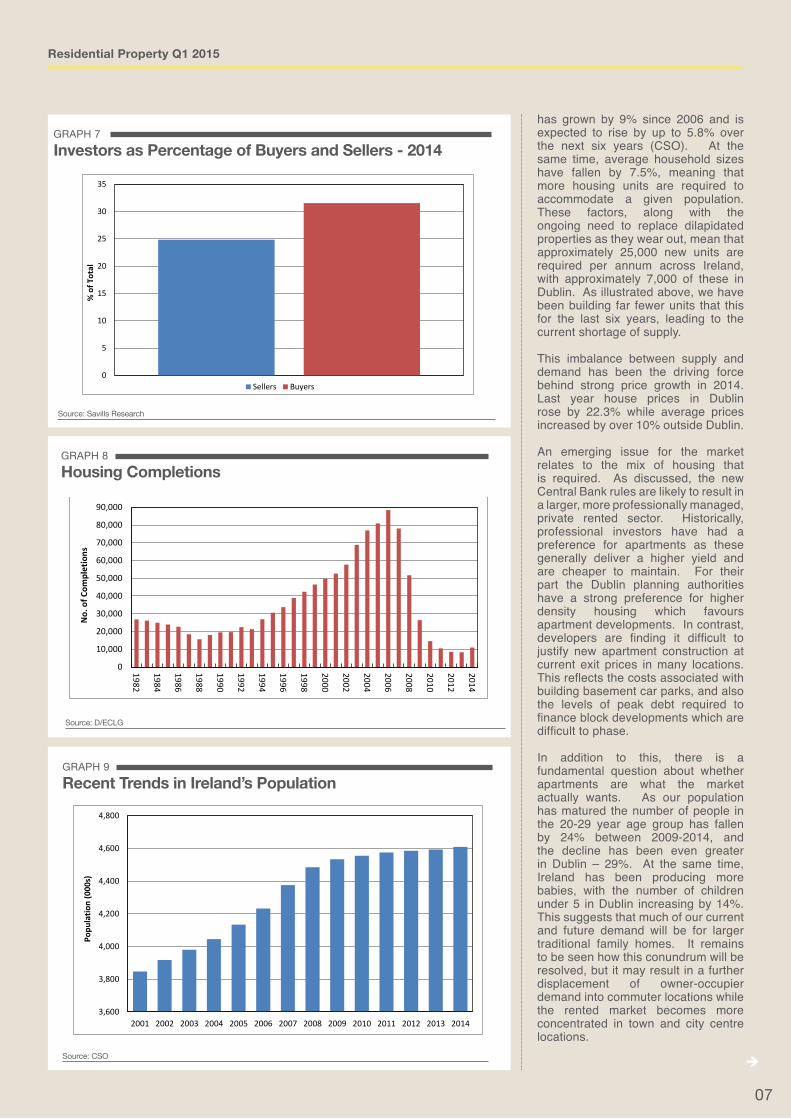

SupplyAn insufficient supply of new housing development is the single most significant impediment to the proper functioning of the residential property market in Ireland. Housing completions hit an all-time low of 8,301 units in 2013, with just 1,360 units completed in Dublin. The situation improved somewhat in 2014 with 11,016 new units added – a 32% uplift, and the first year-on-year increase in new housing completions since 2006. The uplift was even stronger in Dublin where 3,259 units were delivered.

Development activity has been limited by a number of factors; planning requirements that make development inviable at current exit prices, concentrated ownership of sites (particularly in Dublin), prohibitive local authority levies, the 13.5% VAT rate on new homes etc.. Moreover, scarce development finance remains an issue and is contributing to the critically low levels of residential construction activity. Currently there are really no large scale housing developments in progress and, considering the likely construction pipeline, our view is that tight supply will remain a feature of the market for the foreseeable future.

DemandAt the most fundamental level, housing demand is driven by the number of bodies looking for beds. As shown in Graph 9, despite strong net emigration during the economic crisis, Ireland’s population

Residential Property Q1 2015

Source: CSO

GRAPH 9Recent Trends in Ireland’s Population

3,600

3,800

4,000

4,200

4,400

4,600

4,800

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Popu

latio

n (0

00s)

Source: D/ECLG

GRAPH 8Housing Completions

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

No.

of C

ompl

etio

ns

07

Source: Savills Research

GRAPH 7Investors as Percentage of Buyers and Sellers - 2014

0

5

10

15

20

25

30

35

% o

f Tot

al

Sellers Buyers

has grown by 9% since 2006 and is expected to rise by up to 5.8% over the next six years (CSO). At the same time, average household sizes have fallen by 7.5%, meaning that more housing units are required to accommodate a given population. These factors, along with the ongoing need to replace dilapidated properties as they wear out, mean that approximately 25,000 new units are required per annum across Ireland, with approximately 7,000 of these in Dublin. As illustrated above, we have been building far fewer units that this for the last six years, leading to the current shortage of supply.

This imbalance between supply and demand has been the driving force behind strong price growth in 2014. Last year house prices in Dublin rose by 22.3% while average prices increased by over 10% outside Dublin.

An emerging issue for the market relates to the mix of housing that is required. As discussed, the new Central Bank rules are likely to result in a larger, more professionally managed, private rented sector. Historically, professional investors have had a preference for apartments as these generally deliver a higher yield and are cheaper to maintain. For their part the Dublin planning authorities have a strong preference for higher density housing which favours apartment developments. In contrast, developers are finding it difficult to justify new apartment construction at current exit prices in many locations. This reflects the costs associated with building basement car parks, and also the levels of peak debt required to finance block developments which are difficult to phase.

In addition to this, there is a fundamental question about whether apartments are what the market actually wants. As our population has matured the number of people in the 20-29 year age group has fallen by 24% between 2009-2014, and the decline has been even greater in Dublin – 29%. At the same time, Ireland has been producing more babies, with the number of children under 5 in Dublin increasing by 14%. This suggests that much of our current and future demand will be for larger traditional family homes. It remains to be seen how this conundrum will be resolved, but it may result in a further displacement of owner-occupier demand into commuter locations while the rented market becomes more concentrated in town and city centre locations.

Residential Property Focus

08

Residential Property Q1 2015

Source: PRTB and ESRI

GRAPH 10 Percentage Change in Residential Rents

-20

-15

-10

-5

0

5

10

15

2008

Q3

2008

Q4

2009

Q1

2009

Q2

2009

Q3

2009

Q4

2010

Q1

2010

Q2

2010

Q3

2010

Q4

2011

Q1

2011

Q2

2011

Q3

2011

Q4

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

2014

Q3

% C

hang

e Y/

Y

Dublin National Outside Dublin

08

FIGURE 5Ellerslie, Douglas, Cork

On market at €2.75 million

New HomesThe new homes market got off to a good start in 2014 with a number of schemes selling well in the Dublin region. However, sales slowed down later in the year. This was primarily due to the uncertainty created by the Central Bank mortgage lending restrictions. However, with this uncertainty now lifted, we have noticed an increased appetite across the board from new homes buyers.

Two key trends are emerging in the new homes market. Firstly, buyers are increasingly looking to the commuter counties as they are being priced out of Dublin. These buyers are now targeting areas such as Bray and Greystones in North Wicklow, Naas, Cellbridge, Leixlip and Maynooth in Kildare and areas such as Ashbourne in Meath.

Secondly, we are witnessing strong interest in the luxury apartment sector where affluent buyers see value in high-end, well located city centre schemes. These parties are predominantly domestic trade-down buyers, but international buyers have also been active. The majority of these are from the UK and many have ties to Ireland. However the weakening Euro/Sterling exchange rate is also a factor and will continue to drive interest from UK buyers in 2015. While stock levels remain low, we are aware of a number of new homes schemes coming to the market in 2015. The majority of these will contain 3 and 4 bed housing and are located in suburbs of Dublin and the commuter counties. With the central bank changes coming into effect it may be challenging to justify the construction of some traditional housing schemes in less affluent locations as the natural target for these would be first time buyers who may be more restricted. However, we would note that the vast majority of new homes schemes we are involved in are now viable to build and sell with a profit.

Rental MarketDespite a strong tradition of owner-occupation the number of households in rented accommodation in Ireland more than doubled from 145,317 to 305,377 between 2006 and 2011. This shift from owner-occupation to the private rented tenure ensured that rents declined relatively modestly during the economic crisis. Now, with a strong economic recovery underway and with the market tightening due to six consecutive years of subdued house building, rents are rising strongly once again. The latest data from the Private Residential Tenancies Board (PRTB) show residential rents increasing by 9.5% in Dublin and 5.6% nationally.

As outlined above new mortgage lending restrictions were imposed by the Central

Residential Property Q1 2015

09

Bank on 27th January 2015 which will require most buyers to save a larger deposit. In practical terms, this will delay their entry into owner occupation and extend their stay in the private rented sector. In the short term this will add fuel to the current rate of rental growth. Ultimately this will attract investors and we are likely to see a continuation of the trend towards a more professional private rented sector with better quality accommodation on offer.

Cork MarketTraditionally the Cork market has followed trends in Dublin with a 12 month lag. This is still the case; the average house price in Cork City is now €182,000, following a 12.2% increase in 2014. In comparison, the Dublin City price increase was 12.4% this time last year. Overall averages for the Cork market are diluted by its geographical area which spans many small villages and towns in the rural hinterland. However, in the prime suburbs of Cork which include Douglas, Rochestown, Blackrock and Bishopstown, Savills’ average selling price was €545,000 for 2014 compared with €488,000 in 2013.

Transactions in Cork increased by 49% year-on-year in 2014, with 4,480 residential units being traded. This represents 16.7% of all housing transactions in Ireland. All buyer types were represented with strong activity from first time buyers and, of course, investors buying ahead of the CGT incentive expiry last December.

Looking ahead, a number of new developments are due to be released to the market early in the year. Mostly, these represent the completion of sites which had been closed up for a number of years. A challenge for the year ahead will be to replenish the flow of second-hand homes to the market as stock is selling far more quickly than in previous years. The average selling period for prime properties in Cork is now two months. This, coupled with a prolonged construction hiatus over the last six years, is causing a housing shortage. We anticipate the Central Bank restrictions will have less impact on FTBs in Cork while the average buying price for this group remains below the €220,000 bar.

FIGURE 7Clanaisling, Kinsale, Cork

Sale Agreed by Savills

FIGURE 625 The Oaks, Herbert Park Lane, Ballsbridge

Sold by Savills in November 2014

OUTLOOK 2015• Housing demand is likely to remain strong due to demographic

pressures and an improving economic backdrop. However residential building activity will continue to undershoot requirements for the foreseeable future. This imbalance between demand and supply will drive further house price growth in 2015.

• The rate of price growth is likely to moderate this year as the rising base level makes further gains more challenging in percentage terms.

• The Central Bank mortgage lending rules are unlikely to impact on prices or price growth. In the short run, the new rules will force more FTBs in Dublin into rented accommodation. This will drive rents higher. However, over a 12-18 month time horizon, higher rents should attract cash-rich investors who will drive up prices by competing for a finite pool of properties. The only long term effect will be a different mix of buyers.

• Quantitative Easing and the new mortgage rules will result in a larger private rented sector. Already, the typical investor profile is changing – the opportunistic boom-time landlords are rapidly being replaced with more professional, yield-driven investors. This process will continue and will lead to a better standard of rental accommodation in the market.

• Declining affordability in Dublin, combined with demographic trends, will lead to increased demand and sharper house price growth in the commuter counties of Wicklow, Kildare and Meath. ■

010

FIGURE 8College Square, Terenure, Dublin 6W

Launched by Savills New Homes in November 2014Two storey 4 bed houses

FIGURE 9Orwell Lodge Apartments, Orwell Road, Rathgar, Dublin 6

Sale Agreed By Savills in 20147 individual high end apartment in boutique development

Savills plcSavills is a leading global real estate service provider listed on the London Stock Exchange. The company established in 1855, has a rich heritage with unrivalled growth. It is a company that leads rather than follows, and now has over 200 offices and associates throughout the Americas, Europe, Asia Pacific, Africa and the Middle East.

This report is for general informative purposes only. It may not be published, reproduced or quoted in part or in whole, nor may it be used as a basis for any contract, prospectus, agreement or other document without prior consent. Whilst every effort has been made to ensure its accuracy, Savills accepts no liability whatsoever for any direct or consequential loss arising from its use. All reference to floor size is approximate. The content is strictly copyright and reproduction of the whole or part of it in any form is prohibited without written permission from Savills Research.

Ireland Residential Team Please contact us for further information

John McCartneyDirector, Research+353 (0)1 618 [email protected]

Catherine McAuliffeDirector, Residential - Cork+353 (0)21 427 [email protected]

Clarie NearyAssociate, Residential Lettings+353 (0)1 618 [email protected]

Padraic ReidyEconomist+353 (0) 1 618 [email protected]

David BrowneHead of New Homes+353 (0)1 618 [email protected]

Iris KeatingHead of Residential Recovery & Asset Management +353 (0)1 663 [email protected]

Mark ReynoldsDirector+353 (0)1 618 [email protected]

Graham MurrayDirector, Head of Residential +353 (0)1 663 [email protected]

FIGURE10Coopers Wood, Chapel Road, Kinsealy, Co. Dublin.

Savills New Homes launched in February 2015 Two storey 3 & 4 bed houses