Embed Size (px)

Citation preview

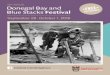

ResourceOne Conference December 2009

First gold pour August 2007

No representation or warranty, expressed or implied is made as to the accuracy or completeness of the information contained in this presentation, and nothing contained herein is, or shall be relied upon as, a promise or representation, whether as to the past or to the future. This presentation does not constitute an offer to sell, or the solicitation of an offer to buy, any securities. Statements in this release that are forward looking statements are subject to various risks and uncertainties concerning the specific factors identified in this presentation and in the Corporation’s periodic filings with the U.S. Securities Exchange Commission, such as estimates and statements that describe the Corporation’s future plans, objectives or goals, including words to the effect that the Corporation or Management expects a stated condition or result to occur. Since forward-looking statements address future events and conditions, they involve inherent risks and uncertainties.

Actual results in each case could differ materially from those currently anticipated in such statements by reason of factors such as the productivity of the Corporation’s mining properties, changes in general economic conditions and conditions in the financial markets, changes in demand and prices for the minerals the Corporation produces including fluctuations in the gold price, litigation, legislative, environmental and other judicial, regulatory, political and competitive developments in areas inwhich the Corporation operates including those related to Mexico, and technological and operational difficulties encountered in connection with the Corporation’s mining activities, and labor related matters and costs.

Cautionary Note regarding Estimates of Measured, Indicated and Inferred Resources: The United States Securities and Exchange Commission permits mining companies, in their filings with the SEC, to disclose only those mineral deposits that a company can economically and legally extract or produce. We use certain terms in this presentation, such as "indicated" and "inferred resources" that the SEC guidelines strictly prohibit us from including in our filings with the SEC. US investors are cautioned not to assume that any or all of measured, indicated or inferred resources are economically or legally mineable or that these resources will ever be converted into reserves. US investors are urged to consider closely the disclosure in our Form 10-K and other SEC filings. You can review and obtain copies of these filings from the SEC’s website at http:www.sec.gov/edgar.html.

Disclaimer

2

3

Introduction

Proven Mine Builders (CGC PRESIDENT DIRECT INVOLVEMENT) El Chanate – MexicoLa Camorra, Revemin –VenezuelaZarafshan –Newmont JV – UzbekistanNumerous – Africa

Experienced Corporate ManagementStrengths throughout corporate management.Strong independent growth driven board of directors.

Solid Platform for GrowthEl Chanate mineSaric Exploration property

Undervalued to PeersLow cost producer trading at less than Net Asset Value.

Why Capital Gold?

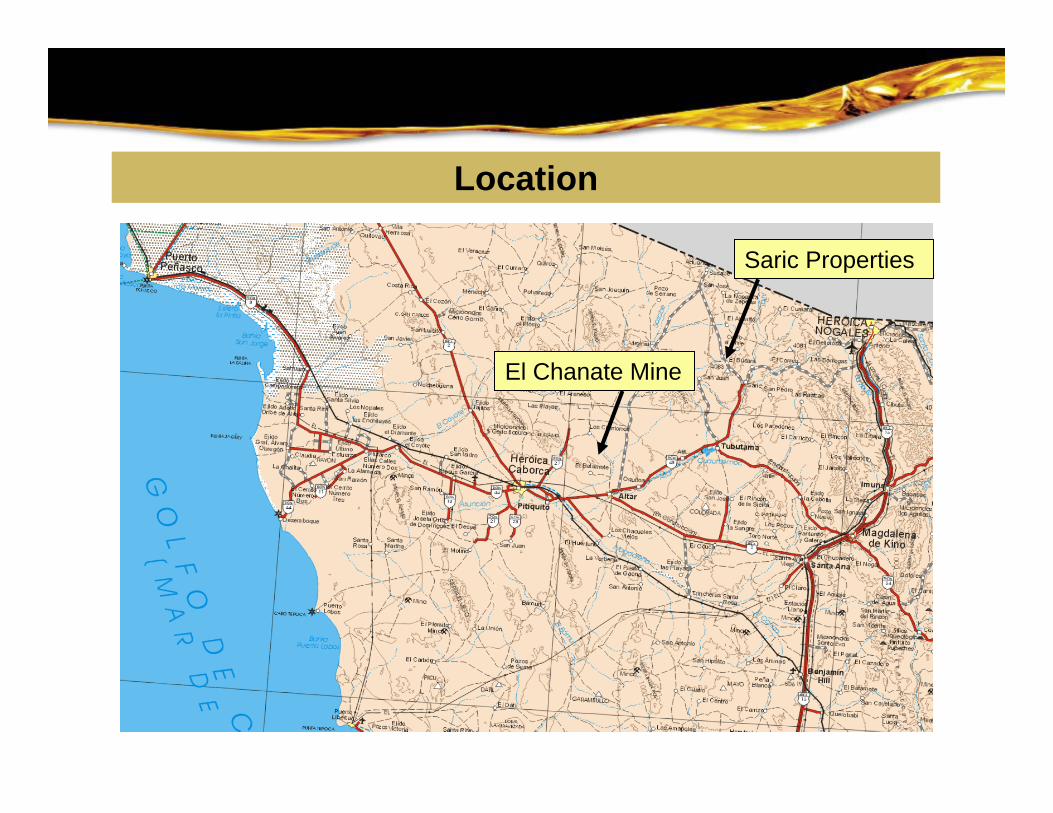

Saric Properties

El Chanate Mine

Location

5

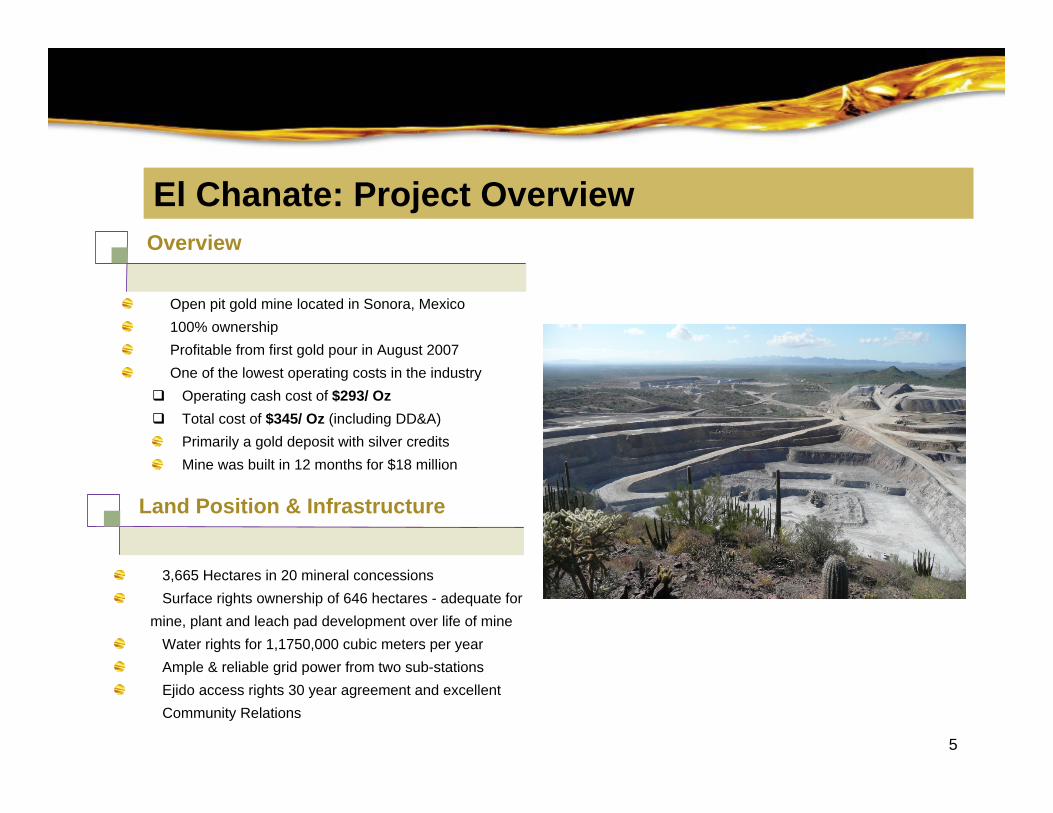

Open pit gold mine located in Sonora, Mexico100% ownershipProfitable from first gold pour in August 2007One of the lowest operating costs in the industry

Operating cash cost of $293/ OzTotal cost of $345/ Oz (including DD&A)Primarily a gold deposit with silver creditsMine was built in 12 months for $18 million

Overview

El Chanate: Project Overview

3,665 Hectares in 20 mineral concessionsSurface rights ownership of 646 hectares - adequate for

mine, plant and leach pad development over life of mineWater rights for 1,1750,000 cubic meters per yearAmple & reliable grid power from two sub-stationsEjido access rights 30 year agreement and excellent Community Relations

Land Position & Infrastructure

6

Platform Base for Growth: Mining Friendly JurisdictionProduction base in mining friendly, politically favorable jurisdictions of MexicoFoundation to prepare for future acquisitions with a focus on gold & silver production in the Americas

• 2010E: 60,000oz @ $293/oz

• 1.5M Oz 2P Reserves

CAPITAL GOLDEL CHANATE

• 2009E: 155,000oz @ $390/oz

• 2.05m Oz 2P Reserves

ALAMOS GOLDMULATOS

• 2009E: 70,000oz @ $448/oz

• 2.4m Oz 2P Reserves

MINEFINDERSDOLORES

• 2009E: 103,000oz @ $390/oz

• 1.36m Oz 2P Reserves.

GAMMON GOLDOCAMPO

• 2009E: 165,000oz @ $140/oz

• 0.47m Oz 2P Reserves

GOLDCORPEL SAUZAL

• 2009E: 43,000oz @ $545/oz

• 339k Oz 2P Reserves

GAMMON GOLDEL CUBO

• 2009E: 95,000oz @ $560/oz

• 1.3m Oz 2P Reserves

NEW GOLDCERRO SAN PEDRO

• 2009E: 245,000oz @ $460/oz

• 5.6m Oz 2P Reserves

GOLDCORPLOS FILOS

Source: Company fillings and guidance, Street’s Research; El Chanate 2009E Production: June 12, 2009 43-101 Technical Report on El Chanate, prepared by Independent Mining Consultants

7

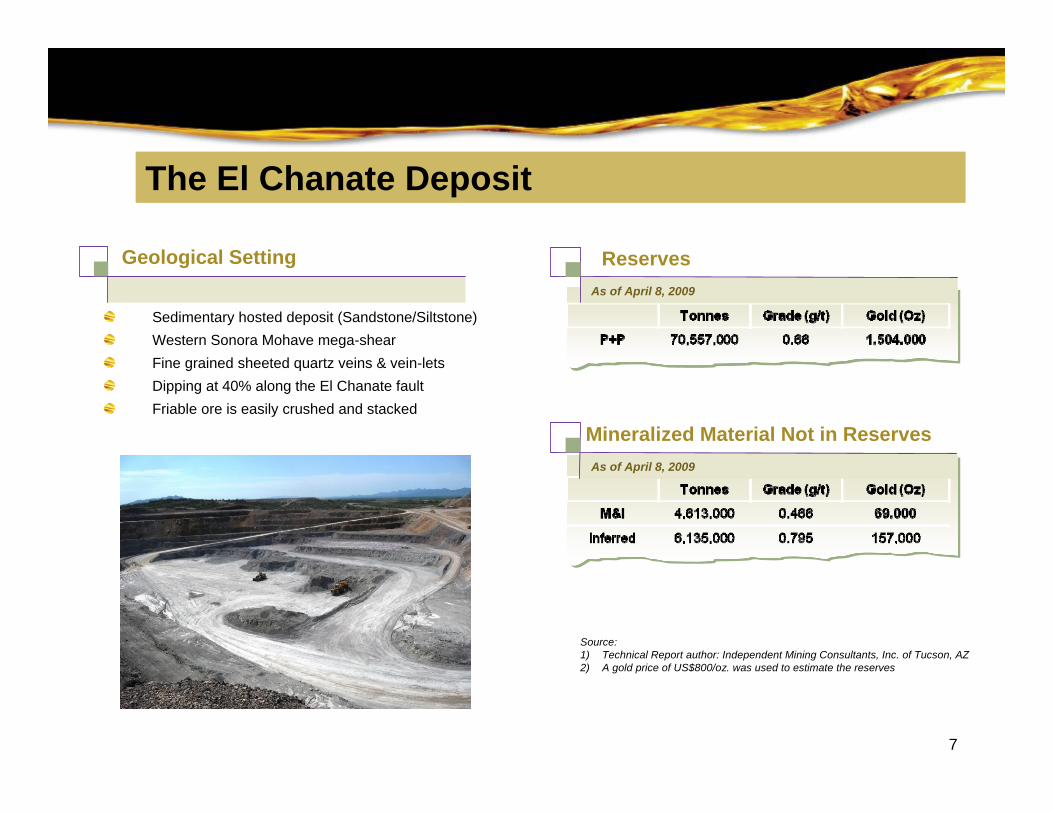

Sedimentary hosted deposit (Sandstone/Siltstone)Western Sonora Mohave mega-shearFine grained sheeted quartz veins & vein-letsDipping at 40% along the El Chanate faultFriable ore is easily crushed and stacked

Geological Setting

The El Chanate Deposit

ReservesAs of April 8, 2009

Source: 1) Technical Report author: Independent Mining Consultants, Inc. of Tucson, AZ2) A gold price of US$800/oz. was used to estimate the reserves

Mineralized Material Not in ReservesAs of April 8, 2009

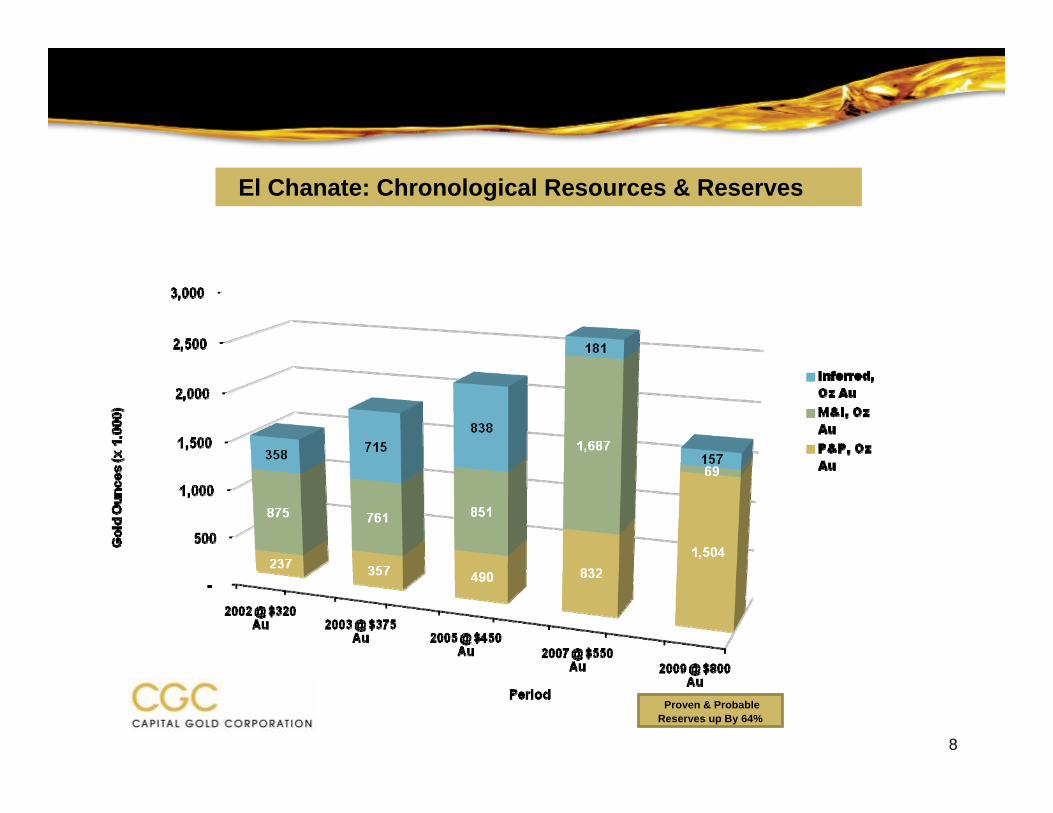

El Chanate: Chronological Resources & Reserves

8

Proven & Probable Reserves up By 64%

9

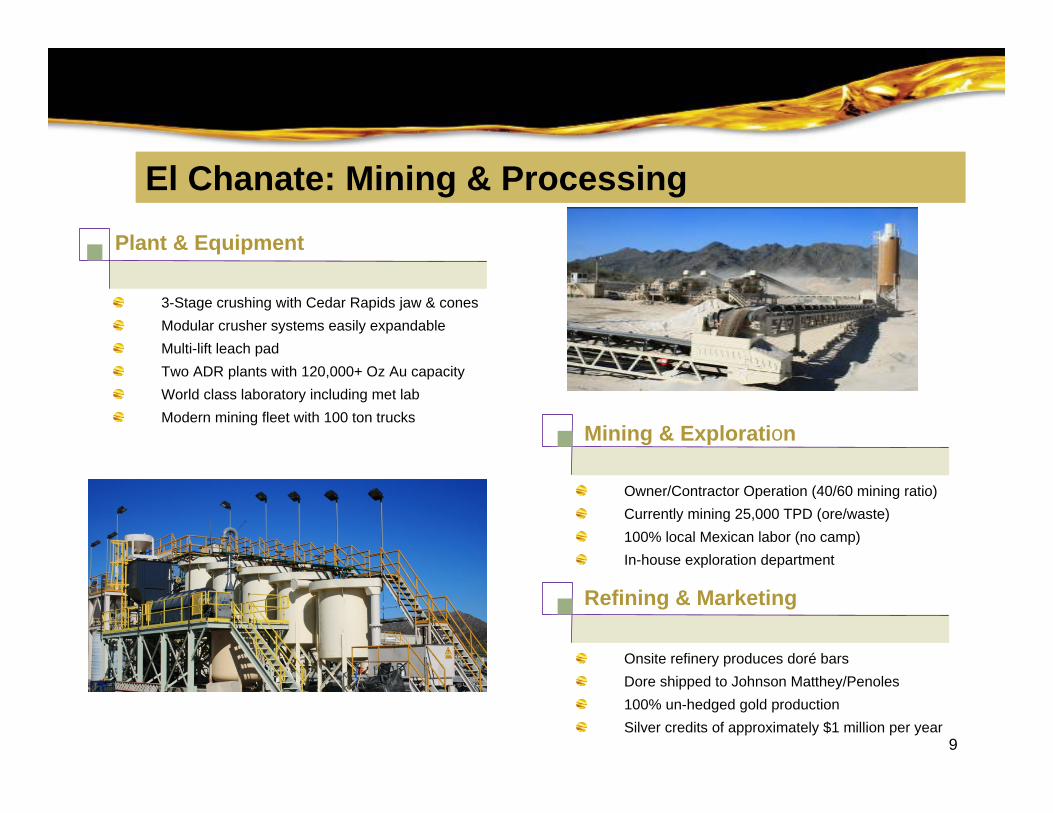

El Chanate: Mining & ProcessingPlant & Equipment

3-Stage crushing with Cedar Rapids jaw & conesModular crusher systems easily expandableMulti-lift leach pad Two ADR plants with 120,000+ Oz Au capacityWorld class laboratory including met labModern mining fleet with 100 ton trucks

Owner/Contractor Operation (40/60 mining ratio)Currently mining 25,000 TPD (ore/waste)100% local Mexican labor (no camp)In-house exploration department

Mining & Exploration

Onsite refinery produces doré barsDore shipped to Johnson Matthey/Penoles100% un-hedged gold productionSilver credits of approximately $1 million per year

Refining & Marketing

10

El Chanate: Low Cost Production

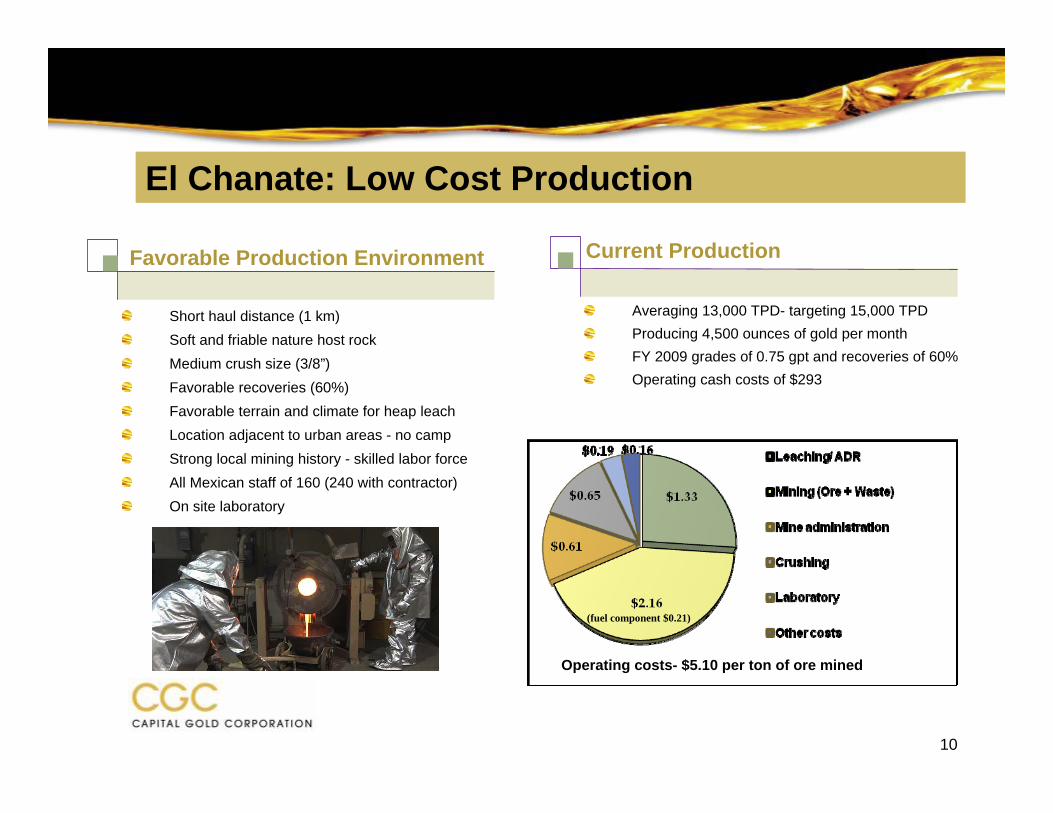

Short haul distance (1 km)Soft and friable nature host rockMedium crush size (3/8”)Favorable recoveries (60%)Favorable terrain and climate for heap leachLocation adjacent to urban areas - no campStrong local mining history - skilled labor forceAll Mexican staff of 160 (240 with contractor) On site laboratory

Favorable Production Environment

Operating costs- $5.10 per ton of ore mined

Current Production

Averaging 13,000 TPD- targeting 15,000 TPDProducing 4,500 ounces of gold per monthFY 2009 grades of 0.75 gpt and recoveries of 60%Operating cash costs of $293

(fuel component $0.21)

11

Capital Gold- Proven Mine Builders

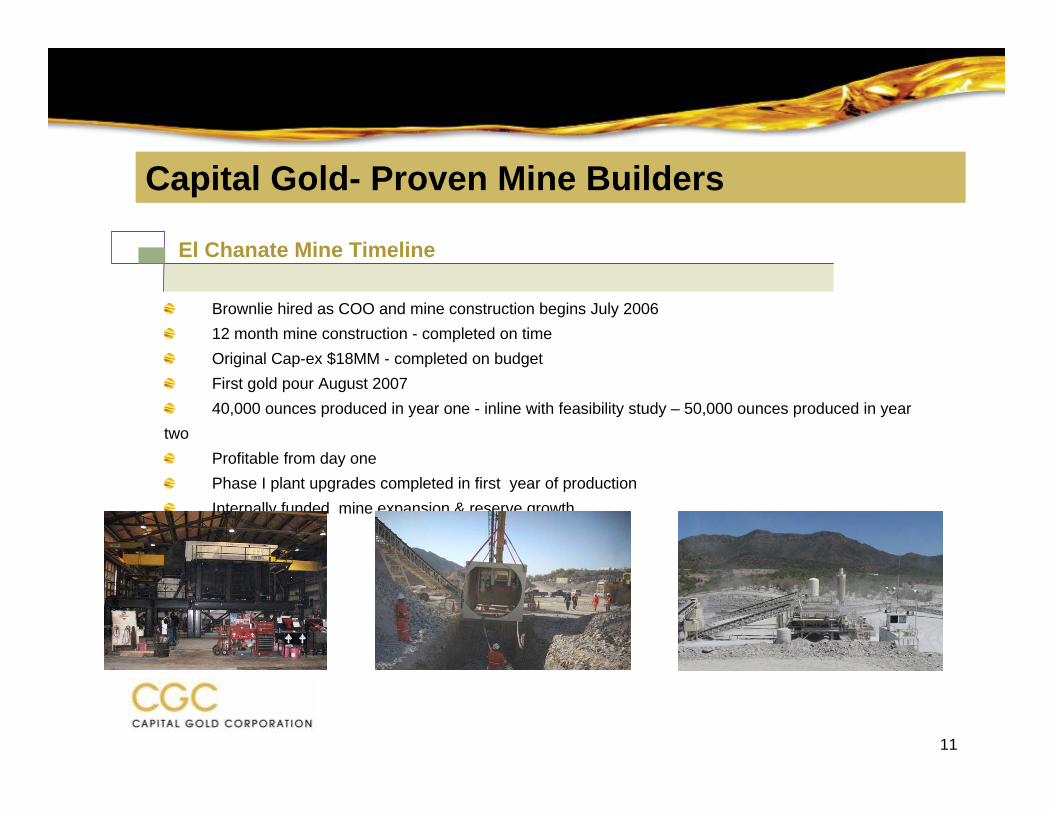

Brownlie hired as COO and mine construction begins July 200612 month mine construction - completed on timeOriginal Cap-ex $18MM - completed on budgetFirst gold pour August 200740,000 ounces produced in year one - inline with feasibility study – 50,000 ounces produced in year

twoProfitable from day onePhase I plant upgrades completed in first year of productionInternally funded mine expansion & reserve growth

El Chanate Mine Timeline

12

El Chanate: Low Cost Production + Growth

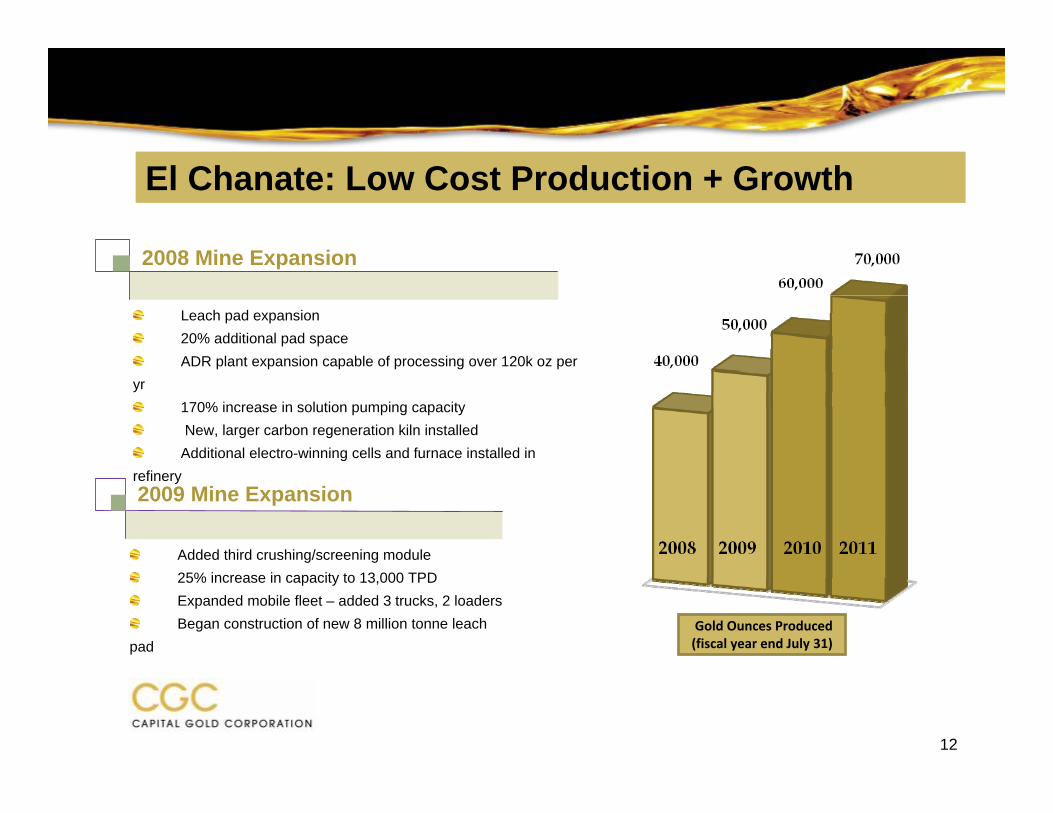

Leach pad expansion20% additional pad spaceADR plant expansion capable of processing over 120k oz per

yr170% increase in solution pumping capacityNew, larger carbon regeneration kiln installed

Additional electro-winning cells and furnace installed in refinery

2008 Mine Expansion

Added third crushing/screening module25% increase in capacity to 13,000 TPDExpanded mobile fleet – added 3 trucks, 2 loadersBegan construction of new 8 million tonne leach

pad

2009 Mine Expansion

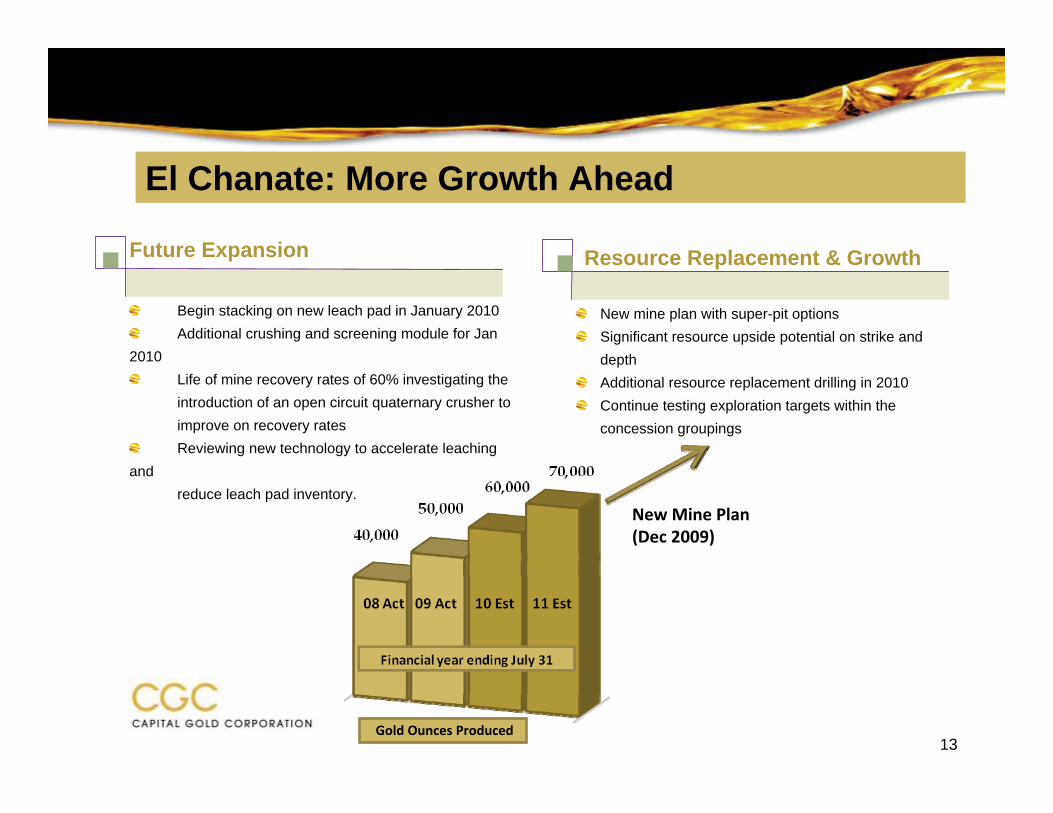

Gold Ounces Produced (fiscal year end July 31)

New Mine Plan (Dec 2009)

13

El Chanate: More Growth Ahead

Begin stacking on new leach pad in January 2010Additional crushing and screening module for Jan

2010Life of mine recovery rates of 60% investigating the introduction of an open circuit quaternary crusher toimprove on recovery ratesReviewing new technology to accelerate leaching

andreduce leach pad inventory.

Future Expansion

New mine plan with super-pit optionsSignificant resource upside potential on strike and depthAdditional resource replacement drilling in 2010Continue testing exploration targets within the concession groupings

Resource Replacement & Growth

Gold Ounces Produced

14

Exploration Potential – Saric “El Oso”

100% owned concession totalling over 2,300 hectares12 additional leased concessions totally 1,800 hectaresMineralization is hosted by shear zones and quartz stock work zones in volcanic and intrusive

rocksPhase I drill program began in May 2008 - 7 holes for a total of 415 metersPhase II drill program began in Feb 2009 - 25 RC holes totaling 2,150 metersPhase lll drill program began in Sept 2000- 41 RC holes totaling 3,560 metersGeochemical sampling and geophysical surveys completedExcellent access near town of Saric only sixty miles on paved road from El ChanateAerial mapping conducted November 2009

Overview

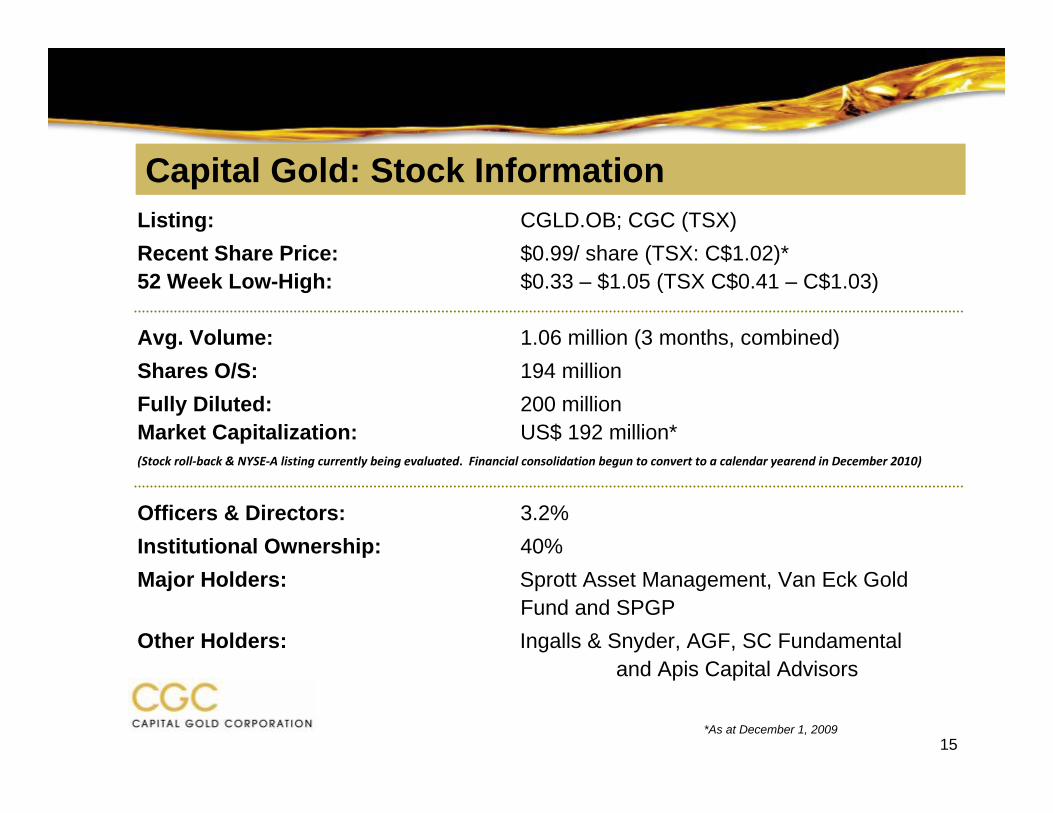

Listing: CGLD.OB; CGC (TSX) Recent Share Price: $0.99/ share (TSX: C$1.02)*52 Week Low-High: $0.33 – $1.05 (TSX C$0.41 – C$1.03)

Avg. Volume: 1.06 million (3 months, combined)Shares O/S: 194 millionFully Diluted: 200 millionMarket Capitalization: US$ 192 million*(Stock roll‐back & NYSE‐A listing currently being evaluated. Financial consolidation begun to convert to a calendar yearend in December 2010)

Officers & Directors: 3.2% Institutional Ownership: 40%Major Holders: Sprott Asset Management, Van Eck Gold

Fund and SPGPOther Holders: Ingalls & Snyder, AGF, SC Fundamental

and Apis Capital Advisors

Capital Gold: Stock Information

15*As at December 1, 2009

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

Dec-08 Feb-09 Mar-09 Apr-09 Jun-09 Jul-09 Aug-09 Oct-09 Nov-09

Pric

e (U

S$)

-

1,500

3,000

4,500

6,000

7,500

9,000

Volu

me

(000

's)

Volume Price

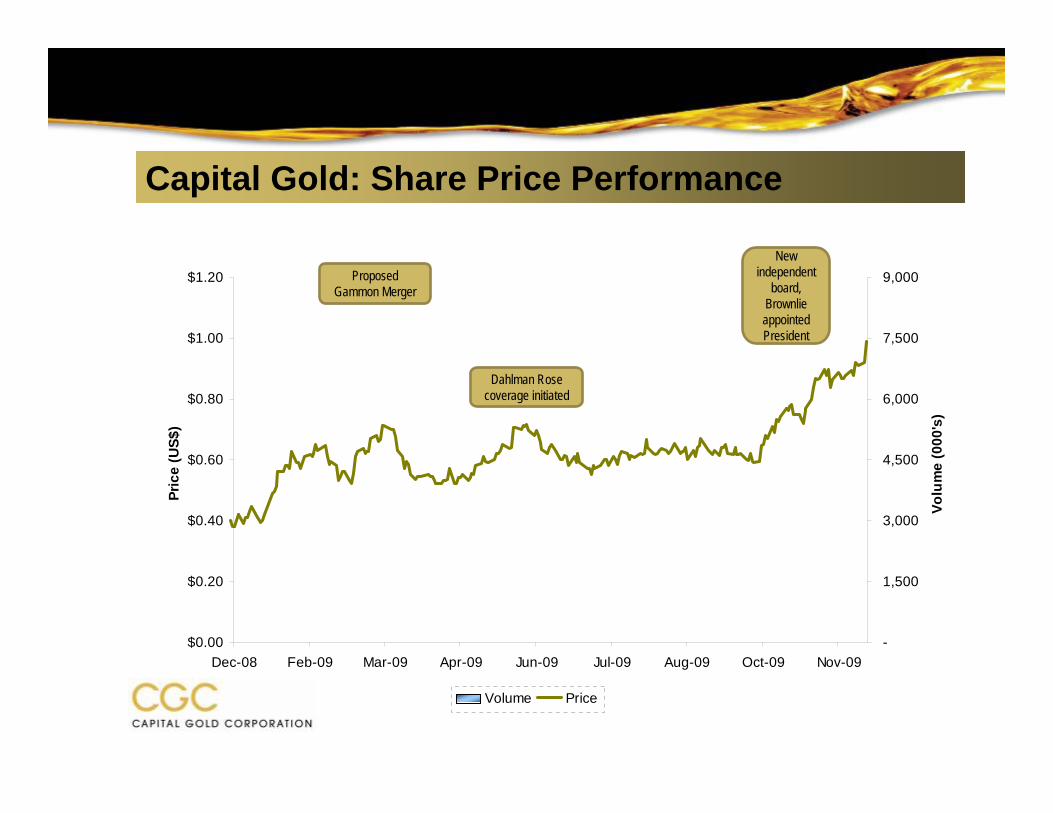

Capital Gold: Share Price Performance

ProposedGammon Merger

Dahlman Rose coverage initiated

New independent

board, Brownlie appointed President

17

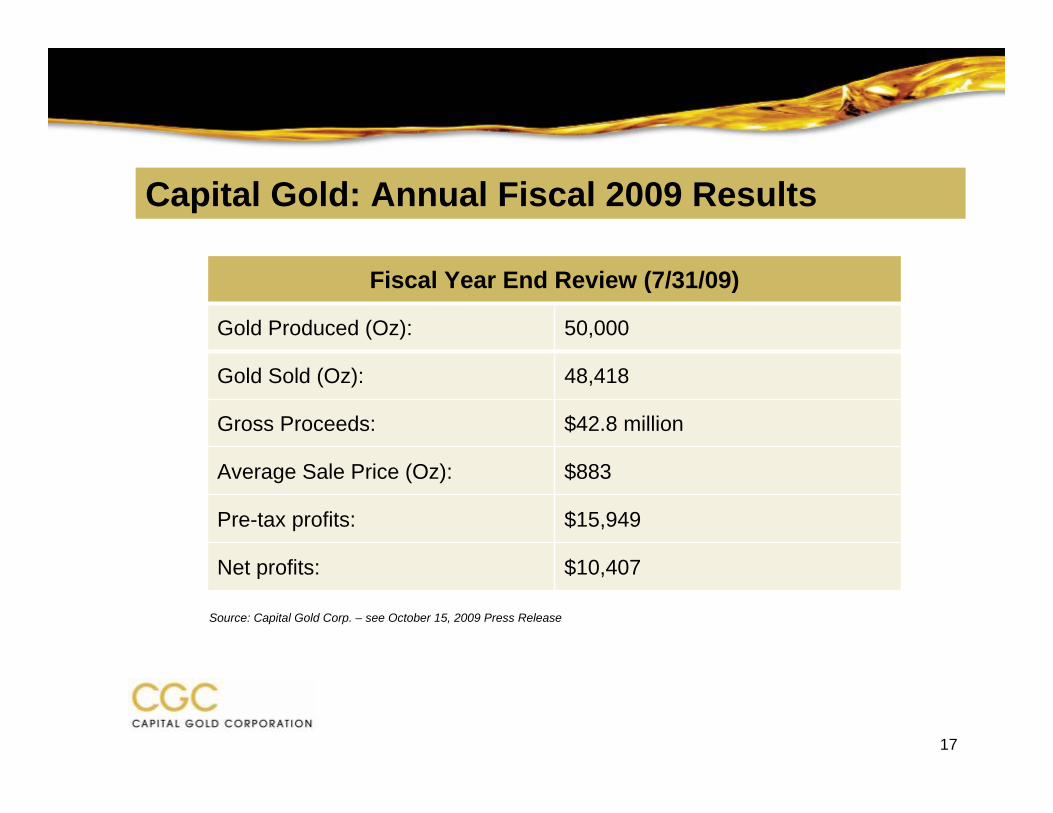

Capital Gold: Annual Fiscal 2009 Results

Fiscal Year End Review (7/31/09)

Gold Produced (Oz): 50,000

Gold Sold (Oz): 48,418

Gross Proceeds: $42.8 million

Average Sale Price (Oz): $883

Pre-tax profits: $15,949

Net profits: $10,407

Source: Capital Gold Corp. – see October 15, 2009 Press Release

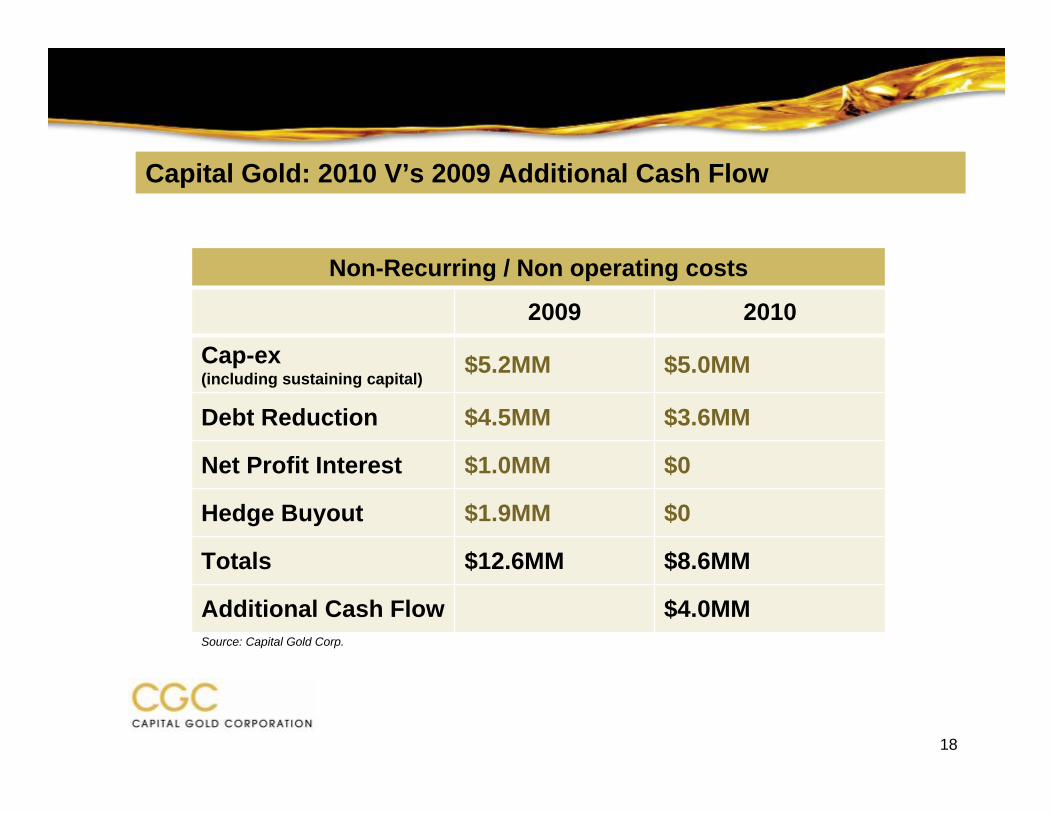

Non-Recurring / Non operating costs

2009 2010

Cap-ex (including sustaining capital)

$5.2MM $5.0MM

Debt Reduction $4.5MM $3.6MM

Net Profit Interest $1.0MM $0

Hedge Buyout $1.9MM $0

Totals $12.6MM $8.6MM

Additional Cash Flow $4.0MM

Capital Gold: 2010 V’s 2009 Additional Cash Flow

Source: Capital Gold Corp.

18

19

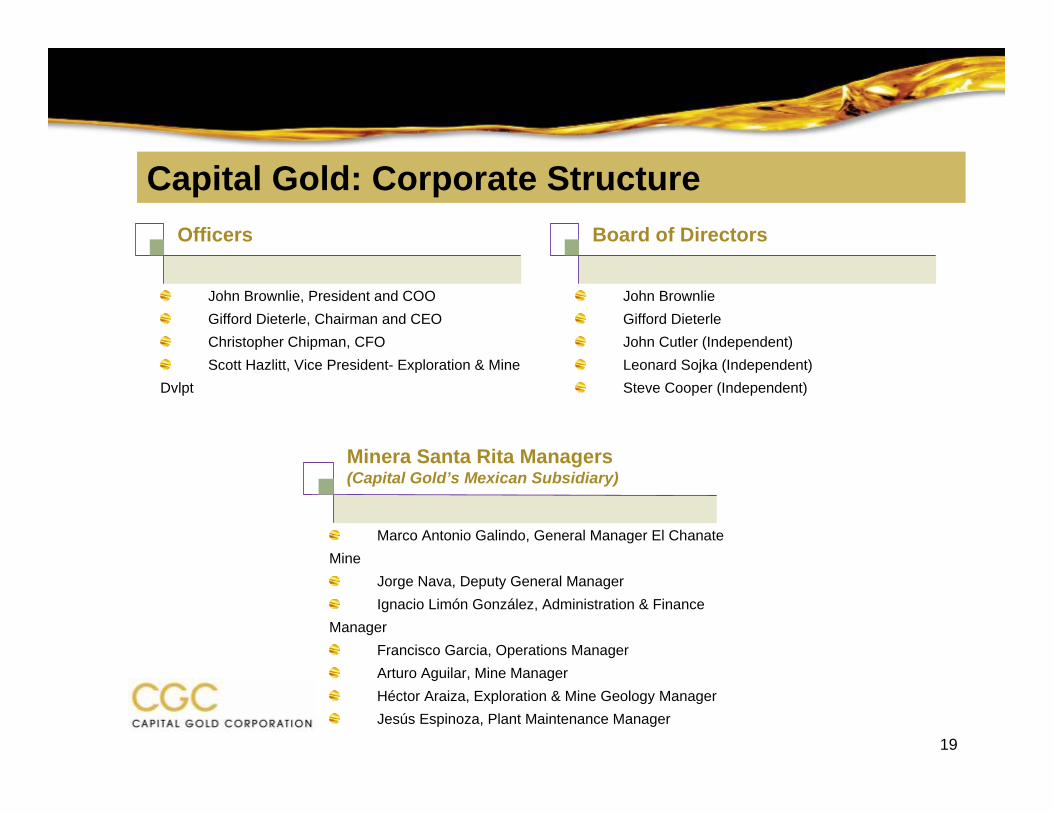

Capital Gold: Corporate Structure

John BrownlieGifford DieterleJohn Cutler (Independent)Leonard Sojka (Independent)Steve Cooper (Independent)

Board of Directors

John Brownlie, President and COOGifford Dieterle, Chairman and CEOChristopher Chipman, CFOScott Hazlitt, Vice President- Exploration & Mine

Dvlpt

Officers

Marco Antonio Galindo, General Manager El Chanate Mine

Jorge Nava, Deputy General ManagerIgnacio Limón González, Administration & Finance

ManagerFrancisco Garcia, Operations ManagerArturo Aguilar, Mine ManagerHéctor Araiza, Exploration & Mine Geology Manager Jesús Espinoza, Plant Maintenance Manager

Minera Santa Rita Managers (Capital Gold’s Mexican Subsidiary)

Firm Analyst

Jennings Capital Inc. Stuart McDougall

Octagon Capital Corporation Rik Visagie

Dahlman Rose & Co. Adam Graf

Hallgarten & Company Christopher Eccelstone

20

Capital Gold: Analyst Coverage

21

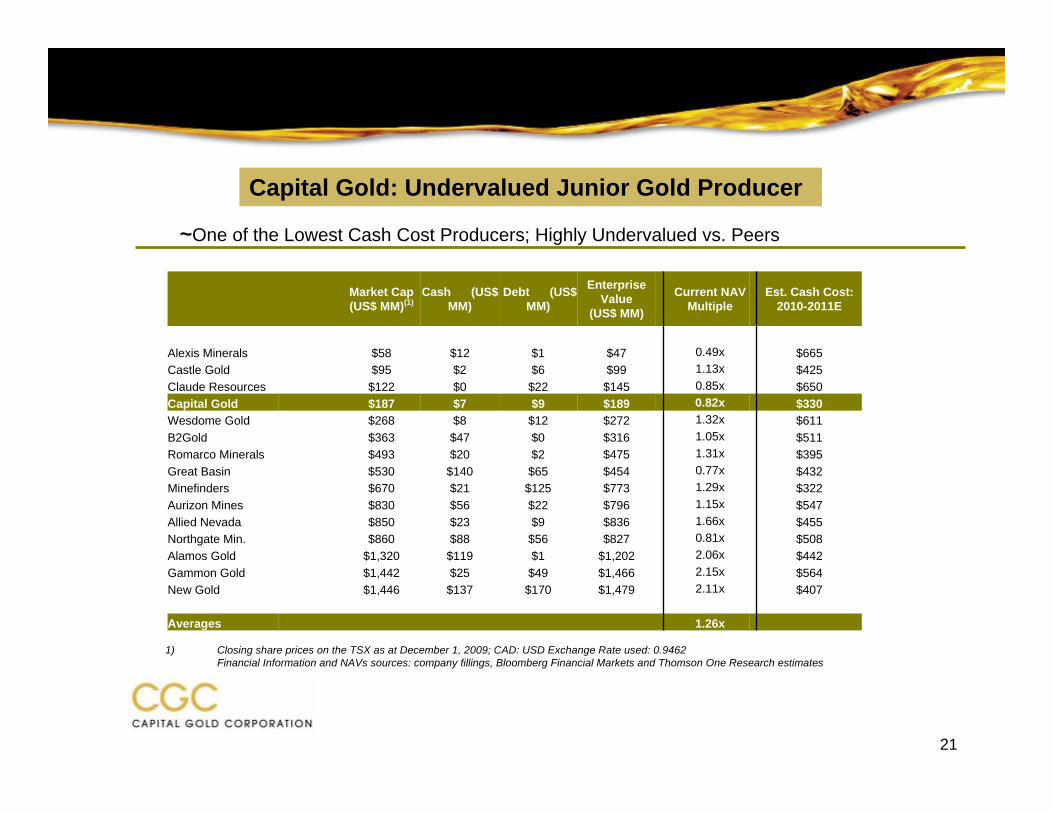

Capital Gold: Undervalued Junior Gold Producer

~One of the Lowest Cash Cost Producers; Highly Undervalued vs. Peers

1) Closing share prices on the TSX as at December 1, 2009; CAD: USD Exchange Rate used: 0.9462Financial Information and NAVs sources: company fillings, Bloomberg Financial Markets and Thomson One Research estimates

Market Cap (US$ MM)(1)

Cash (US$ MM)

Debt (US$ MM)

Enterprise Value

(US$ MM)

Current NAV Multiple

Est. Cash Cost: 2010-2011E

Alexis Minerals $58 $12 $1 $47 0.49x $665Castle Gold $95 $2 $6 $99 1.13x $425Claude Resources $122 $0 $22 $145 0.85x $650Capital Gold $187 $7 $9 $189 0.82x $330Wesdome Gold $268 $8 $12 $272 1.32x $611B2Gold $363 $47 $0 $316 1.05x $511Romarco Minerals $493 $20 $2 $475 1.31x $395Great Basin $530 $140 $65 $454 0.77x $432Minefinders $670 $21 $125 $773 1.29x $322Aurizon Mines $830 $56 $22 $796 1.15x $547Allied Nevada $850 $23 $9 $836 1.66x $455Northgate Min. $860 $88 $56 $827 0.81x $508Alamos Gold $1,320 $119 $1 $1,202 2.06x $442Gammon Gold $1,442 $25 $49 $1,466 2.15x $564New Gold $1,446 $137 $170 $1,479 2.11x $407

Averages 1.26x

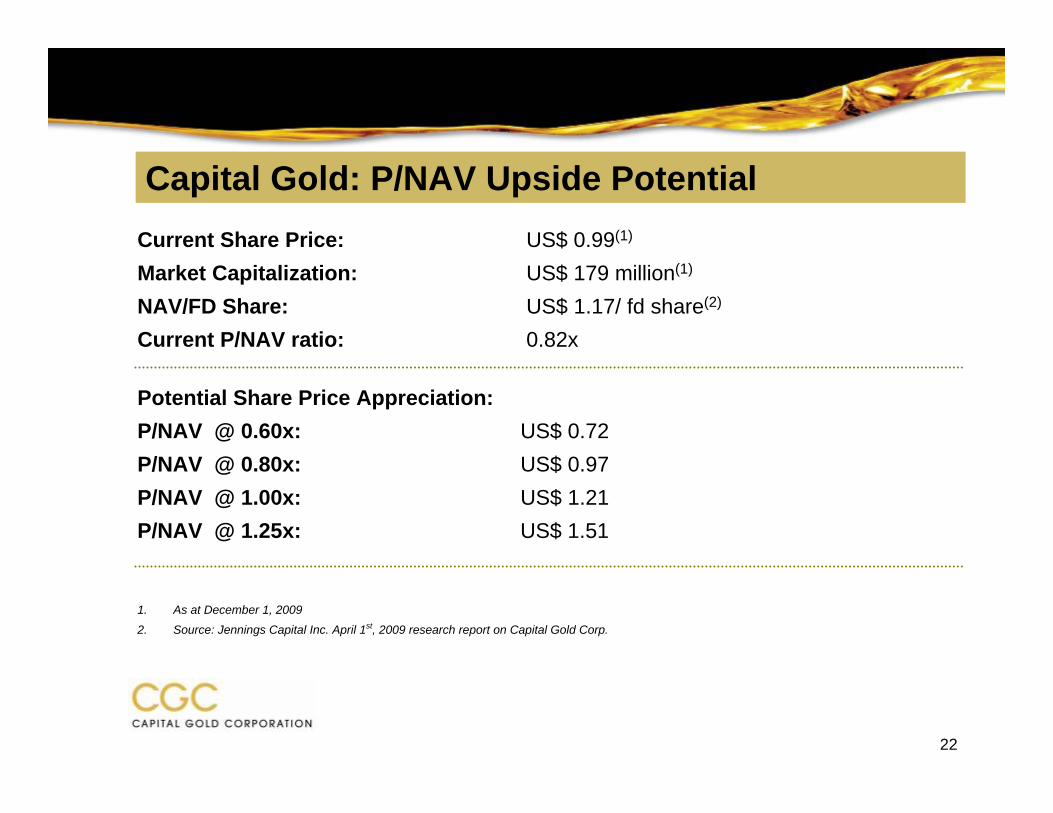

Current Share Price: US$ 0.99(1)

Market Capitalization: US$ 179 million(1)

NAV/FD Share: US$ 1.17/ fd share(2)

Current P/NAV ratio: 0.82x

Potential Share Price Appreciation:P/NAV @ 0.60x: US$ 0.72P/NAV @ 0.80x: US$ 0.97P/NAV @ 1.00x: US$ 1.21P/NAV @ 1.25x: US$ 1.51

Capital Gold: P/NAV Upside Potential

22

1. As at December 1, 2009

2. Source: Jennings Capital Inc. April 1st, 2009 research report on Capital Gold Corp.

23

Capital Gold: The New Mid-Tier Gold Producer

El Chanate MineGrowing Profitable Production & Solid Cash Flow

Proven Mine Builders with an Excellent Mexican Team

24

Conclusion

Proven Mine Builders & Experienced Corporate Management Focused on profitable productionAcquisition & growth strategy focused on Mexico

Solid Platform for GrowthStable low-cost producing mineSeasoned Mexican teamDedicated exploration departmentState of the art onsite laboratory

Undervalued to Peers.82X NAV$137 per ounces of 2P reserves$2272 per ounce of current production

Why Capital Gold?

Source: Capital Gold Corp. as of November 11, 2009.

Appendix

El Chanate upside potential through additional drillingSaric concessions and exploration overview

Pit Designs, Maps & Photos

25

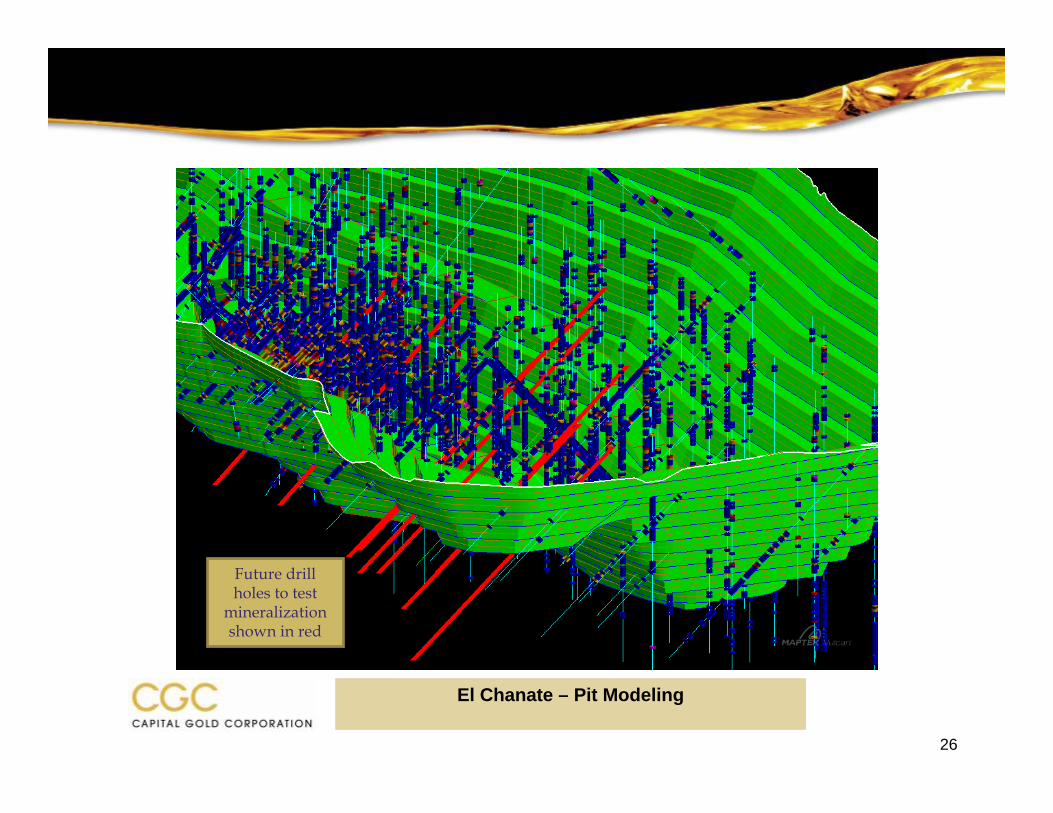

El Chanate – Pit Modeling

Future drill holes to test

mineralization shown in red

26

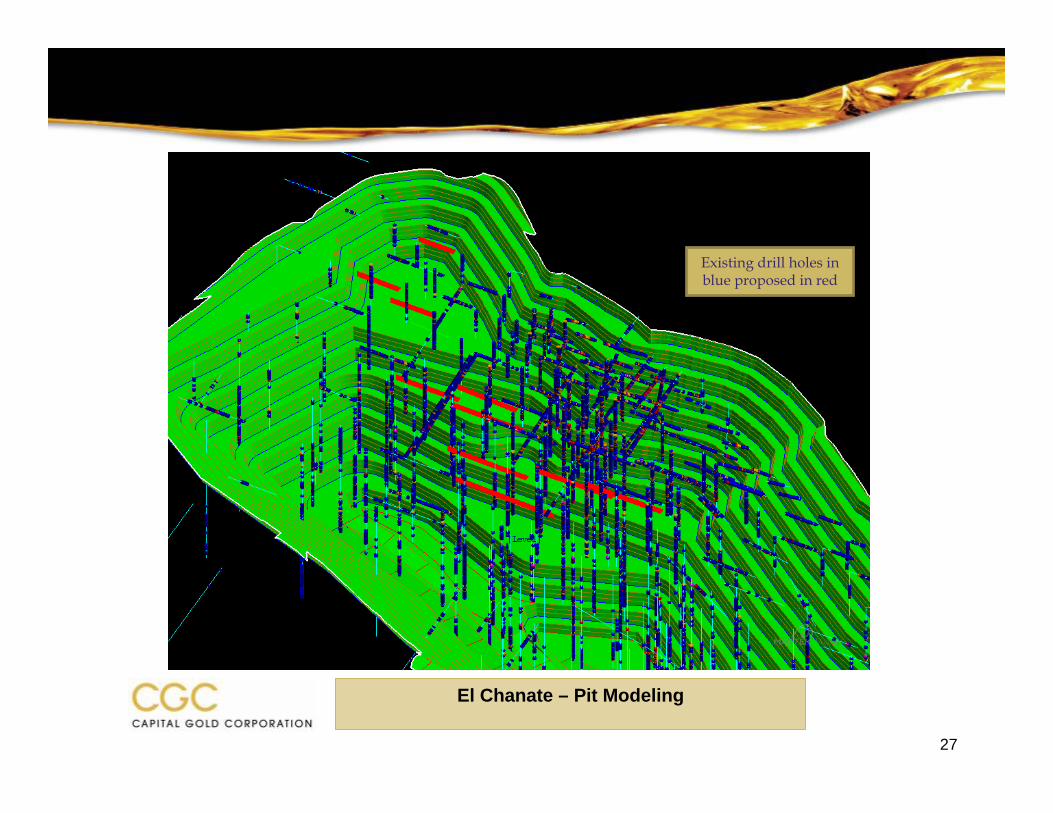

El Chanate – Pit Modeling

Existing drill holes in blue proposed in red

27

El Chanate – Pit Modeling

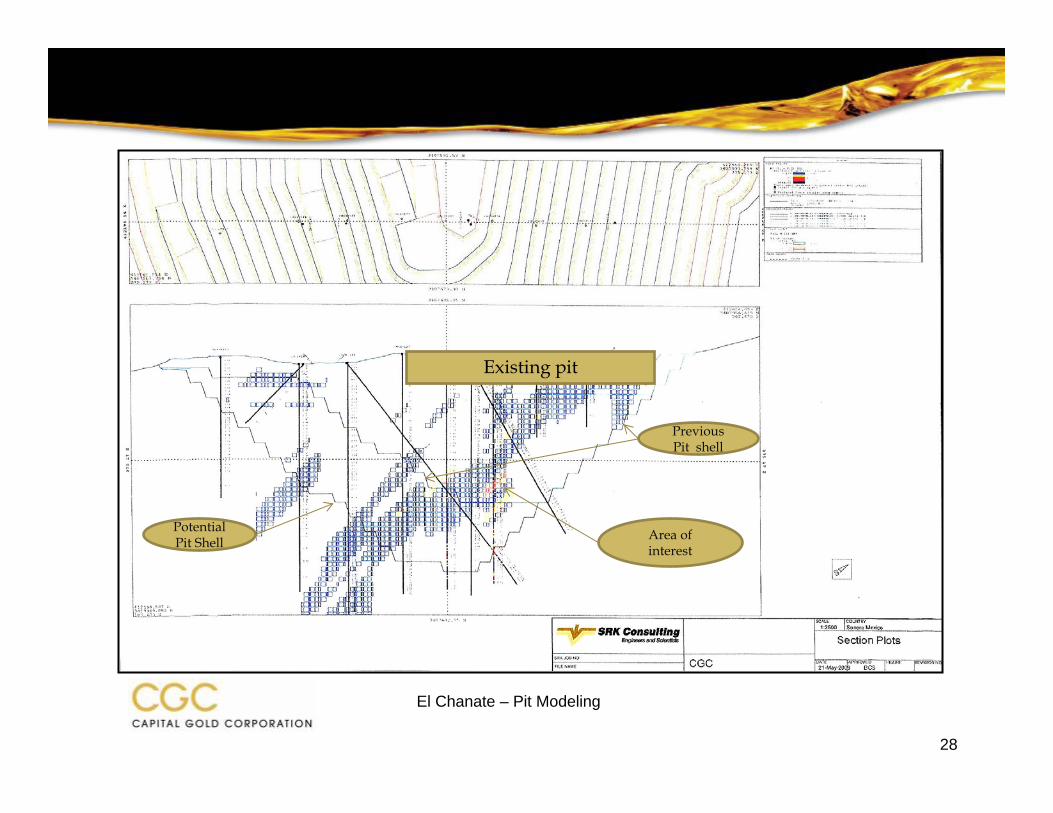

Area of interest

Previous Pit shell

Potential Pit Shell

28

Existing pit

29

El Chanate – Overview & Lab

LaboratoryLeach Pad View from South

30

El Chanate – Current Pit

Mine looking South Mine looking East

31

El Chanate – New Leach Pad Construction

Saric (El Oso) – Geologists Report

In April 2008, we leased 12 mining concessions totaling 1,790 hectares located northwest of Saric, Sonora. In addition, we own a claim of approximately 2,304 additional hectares adjacent to this property. The 4,094 hectare area is accessible by paved roads, and has cellular phone service from hilltops. These concessions and this claim are about 60 miles northeast of the El Chanate mine. Mineralization is evident throughout the concession group and is hosted by shear zones and stockwork quartz veins in volcanic and intrusive rocks. We have completed exploration work consisting of geological mapping, systematic geochemical sampling of rock and soils, geophysical surveys, trenching and aerial mapping.In addition.

Through November we have completed a total of seventy three reverse circulation drill holes. All of these holes were focused on the northern part of concession group near the Sombreretillo Ranch. These holes varied in depth from 100 to 150 meters. SRK of Lakewood Colorado are compiling the data with the intent to define a mineral resource and to advise on the next stage of exploration. Chemex, an independent assay laboratory, are conducting the drill hole assays.

The property lease agreement, which allows us to explore and mine the property, required an initial payment of $45k upon execution of the lease April 4, 2008. In addition, we are required to make ten payments of $25k every four months beginning eight months after execution of the lease agreement. The agreement also contains an option for us to acquire the mining concessions in December 2011 for a cash payment of $1.5 million usd (plus the sum of payments made) or at the end of the 11 payment periods, at Capital’s option or alternatively pay a 1 percent sales royalty capped at $3 million from future mine production.

Capital Gold owned and leased exploration concessions in Sonora Mexico

32

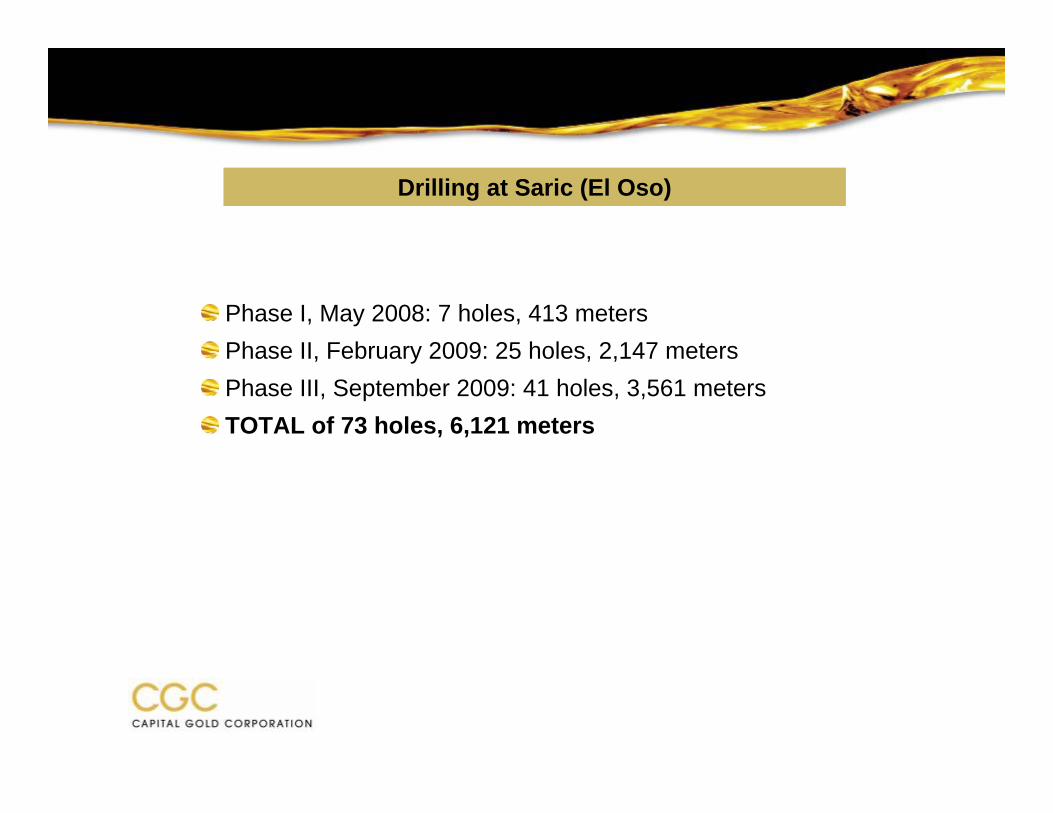

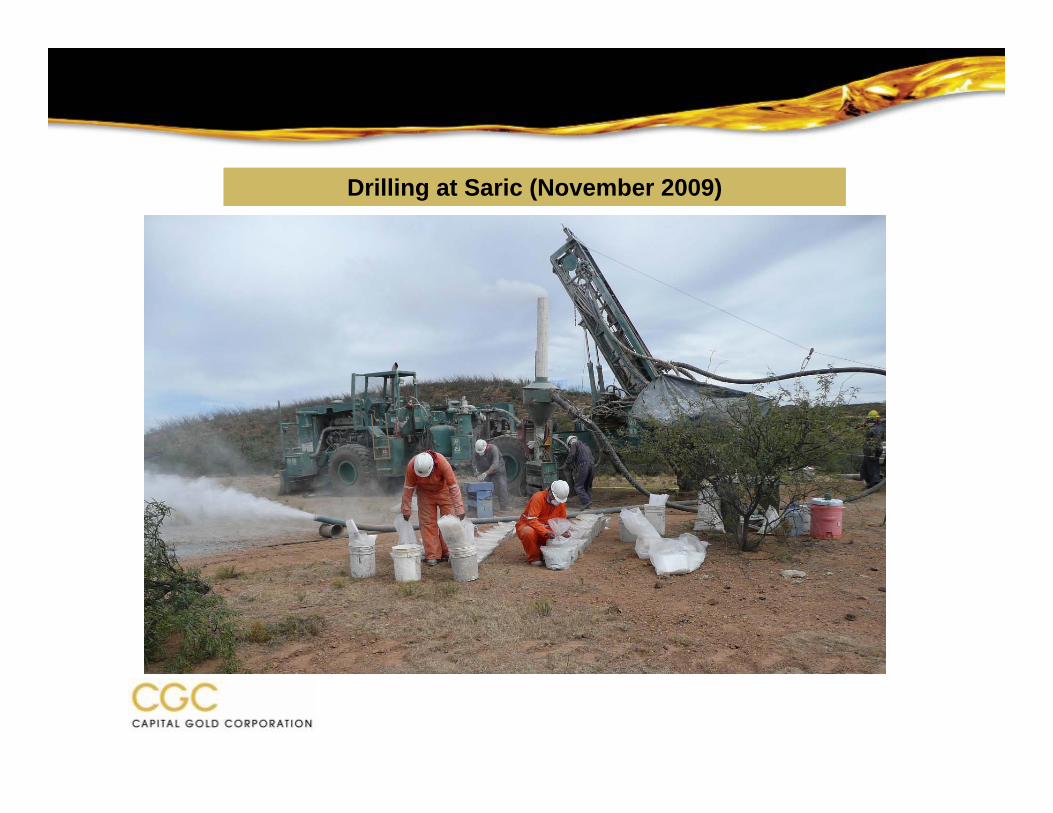

Drilling at Saric (El Oso)

Phase I, May 2008: 7 holes, 413 metersPhase II, February 2009: 25 holes, 2,147 metersPhase III, September 2009: 41 holes, 3,561 metersTOTAL of 73 holes, 6,121 meters

Saric (El Oso)

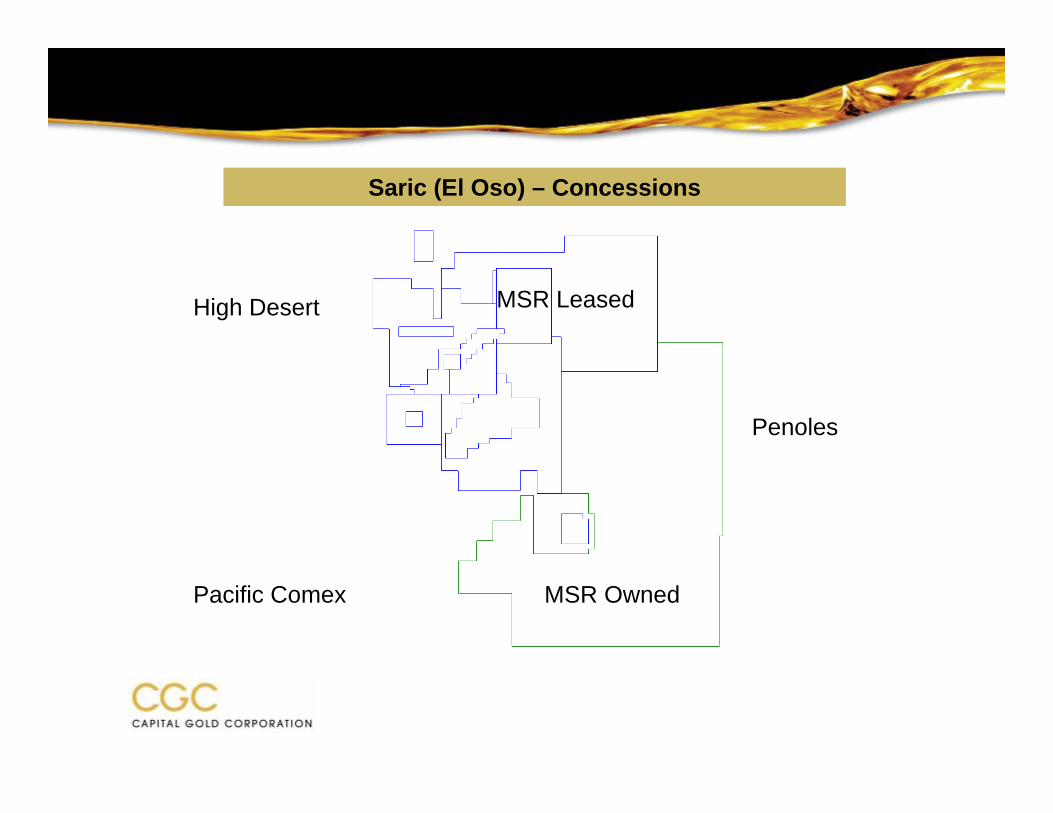

MSR Owned

MSR LeasedHigh Desert

Penoles

Pacific Comex

Saric (El Oso) – Concessions

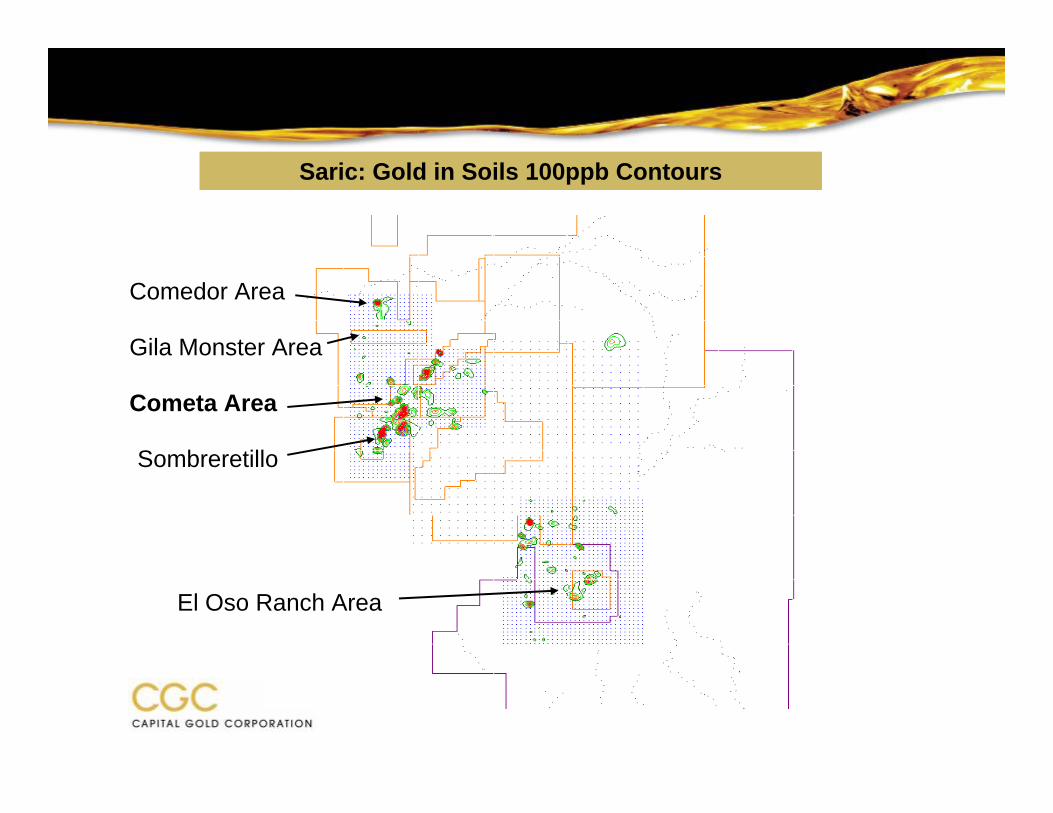

Comedor Area

Gila Monster Area

Cometa Area

Sombreretillo

El Oso Ranch Area

Saric: Gold in Soils 100ppb Contours

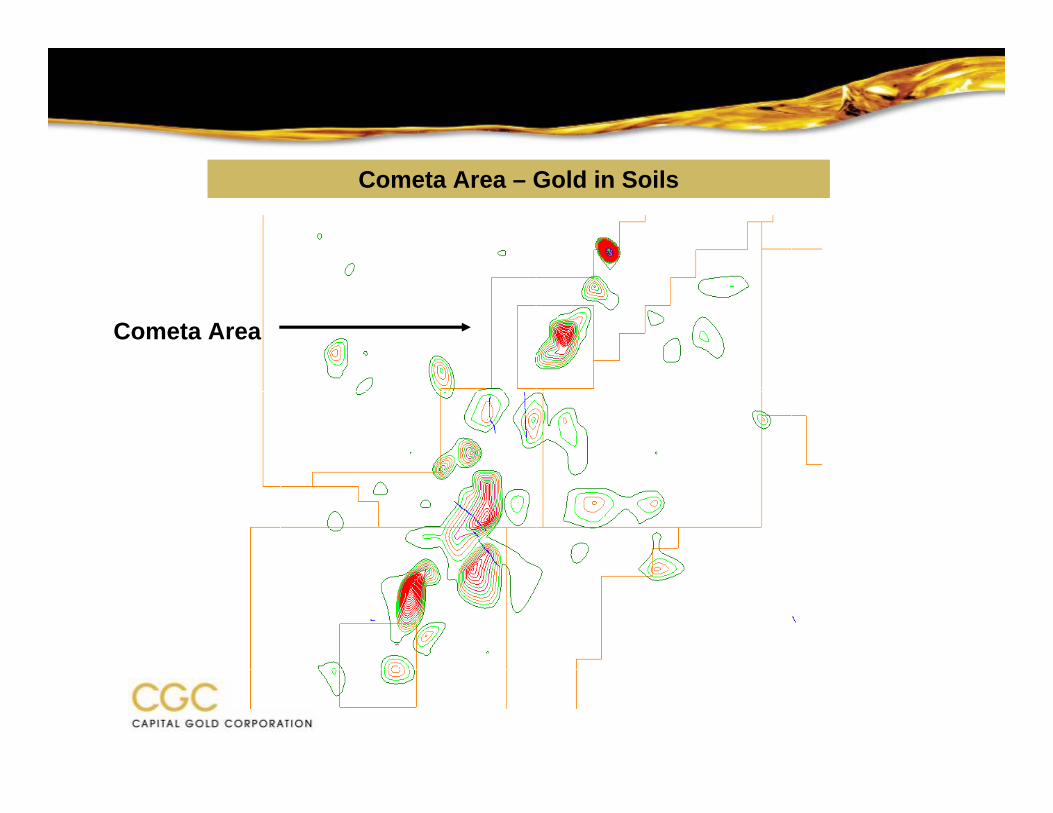

Cometa Area

Cometa Area – Gold in Soils

Drilling at Saric (November 2009)