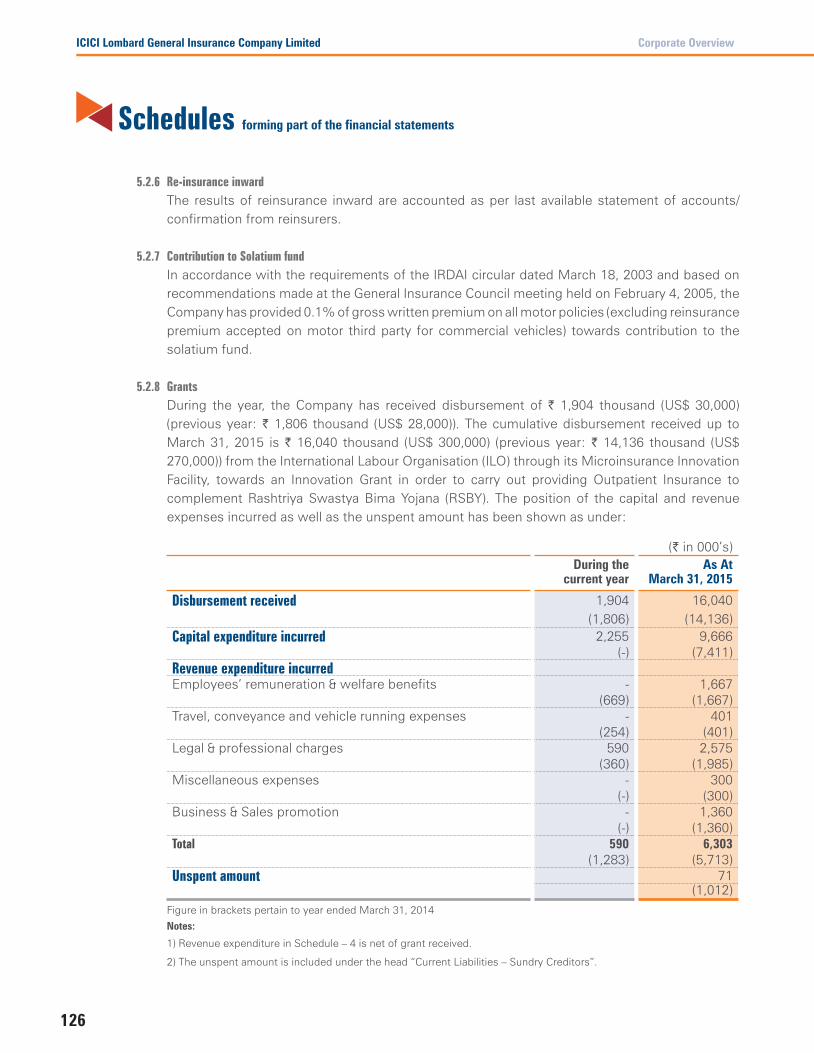

Embed Size (px)

Citation preview

Annual Report2014 -15

Responding to our customers the fair, fast and friendly way

Forward-looking statementIn this Annual Report, we have disclosed forward looking information to enable investors to comprehend our prospects and take investment decisions. This report and other statements - written and oral - that we periodically make contain forward looking statements that set out anticipated results based on the management’s plans and assumptions. We have tried, wherever possible, to identify such statements by using words such as ‘anticipate’, ‘estimate’, ‘expects’, ‘projects’, ‘intends’, ‘plans’, ‘believes’, and words of similar substance in connection with any discussion of future performance. We cannot guarantee that these forward looking statements will be realised, although we believe we have been prudent in our assumptions. The achievements of results are subject to risks, uncertainties and even inaccurate assumptions. Should known or unknown risks or uncertainties materialise, or should underlying assumptions prove inaccurate, actual results could vary materially from those anticipated, estimated or projected. Readers should keep this in mind. We undertake no obligation to publicly update any forward looking statement, whether as a result of new information, future events or otherwise.

Inside the Report

CORPORATE OVERVIEW 2-11

ICICI Lombard at a Glance 2

Performance Highlights FY 2015 3

Awards and Accolades 4

Corporate Information 5

Message from the Chairperson 6

Message from the Chairman, Fairfax Asia 8

Message from the Managing Director and CEO 10

BUSINESS OVERVIEW 12-37

General Insurance Sector Overview 14

Organisational Structure 15-34

Wholesale Insurance Group 15

Government Business Group 17

Retail Group 24

Shared Services 28

Corporate Social Responsibility 35

STATUTORY REPORTS AND FINANCIAL STATEMENTS 38-141

Directors’ Report 38Corporate Governance 58Management Report 69Auditors’ Report 79Balance Sheet 84Profit and Loss Account 85Revenue Accounts 86Schedules 88Receipts and Payment Account 140

Responding to our customers the fair, fast and friendly wayIn a rapidly changing world, where customers are becoming discerning and well informed, the traditional product-driven approach does not work. This is more relevant for insurance, where the product offering is essentially a ‘Promise’ that needs to be fulfilled in the event of an untoward incident. The quality of services and the expertise and experience that go with it thus become critical differentiators to win customers in a competitive landscape.

Quality and consistency of customer interaction, irrespective of the function, is important to ensure a seamless experience for our customers. For them, we are a single entity and we need to align ourselves to this perspective. We therefore place a lot of emphasis on pan-organisational integration and a uniform communication protocol. Our guiding principle for this is clear: ‘Be fair, fast and friendly to the customer’.

ICICI Lombard General Insurance Company Limited (ICICI Lombard) is one of India’s leading private sector general insurance company. It brings together the expertise of ICICI Bank (India’s second largest bank) and Fairfax Financial Holdings Limited (a Canada based diversified financial services company).

Ever since inception, ICICI Lombard has been catering to varied customer aspirations by providing prudent risk management solutions in a fair, fast and friendly manner. The solutions are innovative and supported by internationally benchmarked service quality standards.

The offerings take a holistic approach to customer wellbeing and the Company remains a reliable single-point destination

for varied customer requirements. Quality and consistency of customer interaction and building a relationship of trust have always been the Company’s key focus areas.

The product and service offerings include:

Motor Insurance

Health Insurance

Travel Insurance

Home Insurance

Specialty Lines Insurance

Property Insurance

Marine Insurance

Mass Health Insurance

Weather Insurance

The Company is committed to serving customers with transparency during the entire

lifecycle of the relationship: from the policy advise stage to renewals and claims. ICICI Lombard’s excellence in products and services is backed by a robust technology infrastructure, and the Company is further investing in elevating its technological expertise. ICICI Lombard continues to strengthen its industry leadership by being ahead of the curve in terms of products and services.

Growing with Customer-first Approach

13.87 MILLIONPolicies issued in FY2015

3.43 MILLIONClaims settled in FY2015

253Pan-India branches in FY2015

` 69.14 BILLIONGross Written Premium (GWP) in FY2015

7,736Head Count

2

Corporate OverviewICICI Lombard General Insurance Company Limited

Revenue Growth(Gross Written Premium ` in million*)

71,34164,200

‘ 1 3 ‘ 1 4 ‘ 1 5

69,140

* Excluding Motor TP inward

Profit Before Tax(` million)

5,202

2,817

‘ 1 3 ‘ 1 4 ‘ 1 5

6,907

Policy Growth(Number of policies sold)

11,222,084

9,184,196

‘ 1 3 ‘ 1 4 ‘ 1 5

13,866,799

Combined Ratio(%)

105.4106.5

‘ 1 3 ‘ 1 4 ‘ 1 5

104.5

Financial Performance FY2015

Annual Report 2014-15 3

Business Overview Statutory and Financial Section

Claims Leader Award, 2014The Company received the ‘Claims Leader’ award in the General Insurance Category for its excellence in claims settlement at the 4th annual edition of the Indian Insurance Awards, 2014.

Best Mobile Application AwardThe Company won the ‘Best Mobile Application’ award at the Asia Insurance Technology Awards, 2014. ICICI Lombard received the recognition for its application that allows policy issuance on mobile devices, thus providing fast and seamless service to its customers at the time of purchase and claims.

ATD Best Winner AwardICICI Lombard was conferred with the Association for Talent Development (ATD) BEST Award 2014 for the third time (earlier known as ASTD BEST). The Company was ranked among the top 20 global organisations for its employee talent development initiatives.

Best IT Implementation AwardICICI Lombard received the ‘Best IT Implementation’ award for its customer oriented service delivery model ‘Business Assurance’ at the Banking Frontiers Finnoviti Awards, 2014. This is a testimony to the Company’s approach of owning customer service SLAs for cashless hospitalisation of claims.

Awards and Accolades

4

Corporate OverviewICICI Lombard General Insurance Company Limited

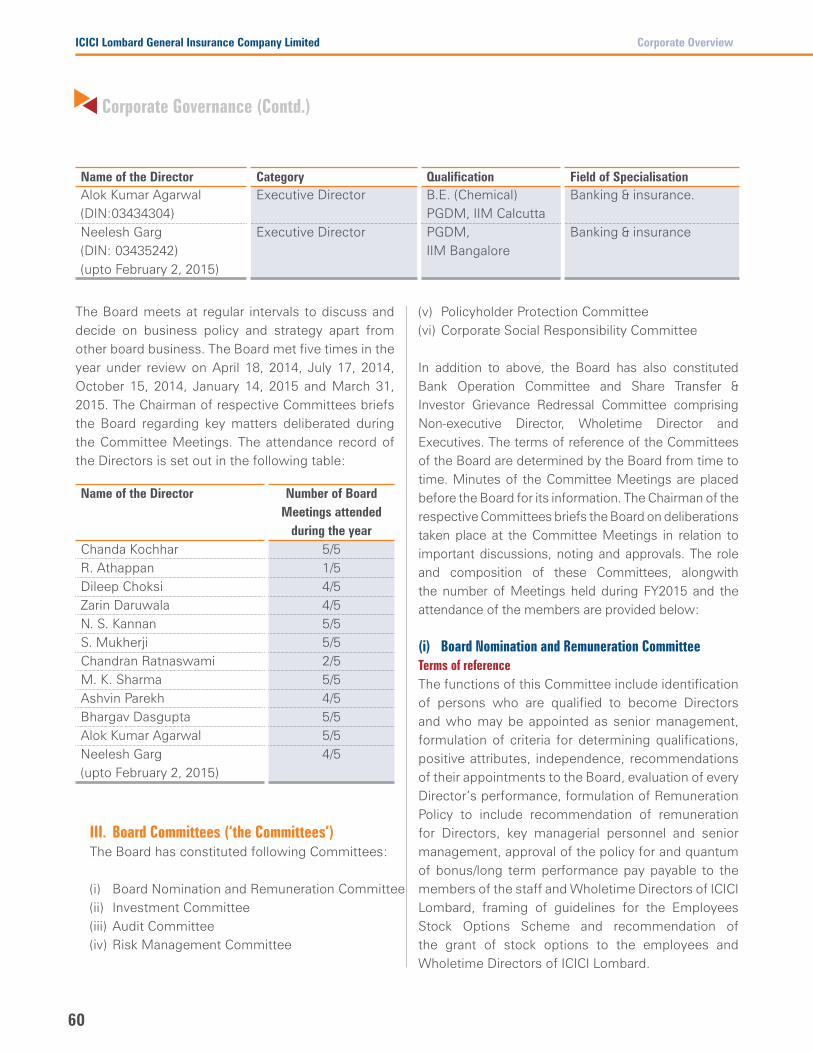

BoardChanda KochharChairperson

R. AthappanDirector

Dileep ChoksiDirector

Zarin DaruwalaDirector

N. S. KannanDirector

S. MukherjiDirector

Chandran RatnaswamiDirector

M. K. SharmaDirector

Ashvin ParekhDirector

Bhargav DasguptaManaging Director & CEO

Alok Kumar AgarwalExecutive Director

Neelesh GargExecutive Director (upto February 2, 2015)

Sanjeev Mantri Executive Director (w.e.f. May 2, 2015)

Board Nomination & Remuneration Committee

M. K. SharmaChairman

Chanda Kochhar

Chandran Ratnaswami

Dilip Choksi

Investment CommitteeChandran RatnaswamiChairman

N. S. Kannan

Bhargav Dasgupta

Manalur Sandilya

S. Gopalakrishnan Gopal Balachandran

Audit CommitteeDileep ChoksiChairman

R. Athappan S. Mukherji

M. K. Sharma

Ashvin Parekh

Risk Management CommitteeS. MukherjiChairman

R. Athappan

Ashvin Parekh Bhargav Dasgupta

Policyholder Protection CommitteeM. K. SharmaChairman

S. Mukherji

Chandran Ratnaswami

Bhargav Dasgupta

Corporate Social Responsibility CommitteeM. K. SharmaChairman

S. Mukherji

R. Athappan

Bhargav Dasgupta

AuditorsKhandelwal Jain & Co.Chartered Accountants

Chaturvedi & Co.Chartered Accountants

Corporate Information

Annual Report 2014-15 5

Business Overview Statutory and Financial Section

Dear Shareholders,

Fiscal 2015 was an eventful year for India. The decisive electoral mandate and the range of policy initiatives taken by the new government have led to renewed optimism about the future prospects of the Indian economy. The country’s fundamental economic growth drivers continue to be strong, and the right policy measures should see us achieving a sustainable higher growth trajectory.

With an expanding economy, a young and aspiring population and low insurance penetration, the domestic general insurance industry is expected to grow at a robust pace. The passing of the Insurance Laws (Amendment) Bill by the Parliament was a landmark step. In addition to enhancing the foreign ownership limit in the sector from 26% to 49%, the legislation contains several enabling measures, which

Chanda Kochhar Chairperson

Message from the Chairperson

6

Corporate OverviewICICI Lombard General Insurance Company Limited

Skill development is a critical need to help India realise the potential of its demographic dividend. We are contributing to this area with ICICI Foundation to drive inclusive growth.

The initiatives of our people are crucial in building an organisation that is always ready to respond to customers’ requirements in a convenient and transparent manner. I am proud of the team’s dynamism and passion. I am confident that with the hard work of our entire team and the support of our stakeholders, we will take the organisation to the next level of growth in the coming years.

Chanda Kochhar Chairperson

should facilitate the long-term development of the industry.

At ICICI Lombard, we are poised to strengthen our position in an industry, which is getting increasingly competitive with new players entering the sector. We continue to enjoy the trust and support of a wide range of customers, and are committed to address their risk protection needs and grow sustainably. In fiscal 2015, our performance reflected our focus on a sustainable profitable growth, backed by prudent underwriting and pricing and appropriate risk selection. We also enhanced our capabilities in areas with strong potential for growth such as liability insurance and specific preferred segments.

Service to the customer has taken centre-stage in all facets of financial services, whether it is banking or insurance. Even as we cherish the trust that our customers and stakeholders place in us, we continue to work towards strengthening this faith through our product and service initiatives. Fiscal 2015 witnessed multiple catastrophes including the floods in Jammu & Kashmir and cyclone in Andhra Pradesh. To help our customers affected by these events, we ensured smooth processing of claims. Our team focused on handholding the customers and continuously assisting them.

We continued to play our role of a responsible corporate citizen.

We continue to enjoy the trust and

and are committed to address their risk

our focus on a

Annual Report 2014-15 7

Business Overview Statutory and Financial Section

Message from the Chairman, Fairfax Asia

Dear Shareholders,

A lot has changed in the Indian landscape in the last year. The decisive results from the May 2014 elections have led to a renewed outlook, for the nation, driven by purpose and optimism. The establishment of a majority and a reform-oriented government is slated to go a long way in enabling India to establish its position as

a dominant force in the global economy in the coming years.

The recently passed Insurance (Amendment) Bill 2015 is a welcome move for India’s insurance industry. With FDI limits enhanced, the much awaited and enabling policy measure has been announced. At the same time,

Ramaswamy Athappan Chairman, Fairfax Asia Limited

8

Corporate OverviewICICI Lombard General Insurance Company Limited

the industry matures, these competencies will stand in good stead for the Company.

Technological advancements, especially in the online space, are becoming critical to the ability of an organisation to service its customers effectively. We are happy to see the progress made by ICICI Lombard in terms of adopting the latest technology and introducing innovative services for customers on the online platform. Besides, utilising technology as a business enabler to achieve cost and operational efficiencies are steps in the right direction.

Over the years, the Company has expanded its role from targeting business leadership to also excelling as a responsible corporate citizen. Even as the Company takes up community building initiatives, we are touched by the efforts of ICICI Lombard’s strong employee base to volunteer for programmes that benefit underprivileged children among others.

As we look ahead, Fairfax Group’s global experience and technical expertise will continue to strengthen ICICI Lombard’s leadership in India’s general insurance sector. We are confident that our partnership with ICICI Lombard will achieve many more milestones in the coming years.

Ramaswamy Athappan Chairman Fairfax Asia Limited

other amendments including empowerment of regulatory bodies will facilitate the announcement of timely and contextual measures. This will serve well for the long-term prospects of the industry.

Our association with ICICI Lombard continues to strengthen year on year. Guided by a common ethos and perspective, we are poised to continue playing a leading role in the long term development of the nation’s insurance industry. India stands at an interesting cross-road today given its young population and rising incomes. This will create new avenues for insurers as customers seek to mitigate risks to their lives and personal assets in an endeavour to harness new opportunities to grow. For us, expanding into opportune markets is a priority as we seek to play a larger role in the global insurance realm. India fits in perfectly in this framework, given its long-term growth prospects, low penetration and macro-economic framework.

ICICI Lombard has always led the industry in terms of identification of new opportunities, product innovation and setting new benchmarks in service standards. This has been an outcome of its deeply customer-centric approach, which defines every aspect of its business focus. At the same time, the Company has taken long strides in terms of strengthening its underwriting and risk management capabilities. As competition intensifies, and

ICICI Lombard has

industry in terms of

has been an outcome

Annual Report 2014-15 9

Business Overview Statutory and Financial Section

Dear Shareholders,

Fiscal 2015 was a momentous year for India. The decisive electoral mandate in the May 2014 elections has provided the much needed platform to rejuvenate the country’s growth agenda. While this has not translated into immediate growth revival, India is poised to return to the days of robust fiscal growth fuelled by enabling regulations, pro-expansion reforms focused on infrastructure, manufacturing and overall economic progress. The intent to streamline policies for ease of doing business and fostering entrepreneurship are also measures to look forward to.

For the General Insurance industry, the pace of growth reduced to 10.62% in fiscal 2015, the slowest in the last four years. Limited pick-up in new automobile sales impacted Motor Insurance, the largest industry segment. The Corporate Insurance segment witnessed pricing pressures and poor demand given the limited investment scenario. Having said this, an improvement in the macroeconomic scenario, expected revival in corporate earnings and consumer sentiments should help the industry return to the double-digit growth trajectory in the near future.

Fiscal 2015 also marked the passage of the Insurance Amendment Bill. While much has been talked about the enhancement in FDI limits, there are several other positive measures in the bill. The governance freedom accorded to the regulatory authority will facilitate introduction of timely and contextual regulations. For an industry eager to play a larger role in India’s socio-economic development, these measures are in the right direction.

At ICICI Lombard, we maintained our market leadership in fiscal 2015 even as we calibrated our growth by focusing on sustainable businesses. Our Combined ratio (CoR) – a measure of profitability from core operations, improved to 104.5% from 105.4% registered in fiscal 2014. In comparison, industry CoR deteriorated from 112.1% (9M, fiscal 2014) to 113.6% (9M,

friendly across all

our customers is a

Bhargav Dasgupta Managing Director & CEO

Message from the Managing Director & CEO

10

Corporate OverviewICICI Lombard General Insurance Company Limited

and accordingly streamline our processes to ensure a hassle free claim settlement experience for our genuine customers. At the same time, we are expanding our digital footprint, especially in the mobile space, by empowering our customers to meet their non-life insurance requirements at the place of their choice and the time of need. We are also taking forward our thrust on providing risk mitigation solutions instead of mere risk financing. We are offering wellness solutions to reduce the instances and severity of hospitalisation and at the same time a card based Out-patient Department (OPD) product for a comprehensive health insurance package.

We continued to win accolades for our initiatives during the year. We were conferred with the ‘Claim Leader’ award in the General Insurance Category at the fourth annual edition of the Indian Insurance Award 2014 for our claim settlement track record. At the Asia Insurance Technology Award, 2014 we were bestowed with the Best Mobile Application award for our insurance focused mobile application. We also won the ‘Best IT implementation’ award for customer oriented service delivery model ‘Business Assurance’ at the Banking Frontier Finnoviti Awards 2014. Winning the ‘Association for Talent Development Best Award’ 2014 (ATD BEST) for the third time, we were ranked among the top 20 organisations across the world for employee talent

fiscal 2015). Profits before tax increased to 6.91 billion, growing by 32.8%.

We continued to cross new milestones on the customer service front in the fiscal gone by, as we remained focused on our philosophy of customer centricity. We serviced 13.87 million insurance policies, an increase of 23.6% over fiscal 2014 and settled 3.41 million claims. Our claim settlement response improved as we settled 93% of motor claims (own damage) within 30 days compared to 92% in fiscal 2014. On the health insurance side, we maintained our track record honouring over 98% claims within 30 days. Customer grievances reduced, declining by 13% in fiscal 2015.

Taking forward our thrust on customer centricity, we are making fresh investments in our business operations to ensure a seamless experience for our customers. We recently set up in-house call centre operations using state-of-the-art infrastructure, handled by a well-trained and customer oriented resource pool. Being fair, fast and friendly across all our interactions with our customers is a principle that we have adopted and will stand by in all our endeavours.

As we look ahead, we are focusing on specific areas aimed at enhancing the experience of our customers. We are enhancing our capabilities in data analytics to better understand our customers

development initiatives. People are our most valuable assets and we will continue to focus on building a high-performing culture that nurtures talent and empower them to grow.

Even as we perform on the business front, we are committed to play our role as a responsible corporate citizen. Our annual employee volunteering initiative ‘Caring Hands’, launched in 2011 has reached out to over 75,000 underprivileged children cumulatively over the last four years. In fiscal 2015, over 2,400 of our employees took charge of this initiative and reached out to 27,002 children across 96 cities through eye-check camps. Cases of poor vision totalling 3,936 were identified and provided with spectacles. We continued to contribute to other CSR projects in the area of preventive health care and disaster relief, thereby spending over 2% of our average profit of last three years for community building initiatives.

As we progress into fiscal 2016, we have the capability, commitment and confidence to set new benchmarks and reinforce the trust of our customers. We look forward to the new financial year with renewed aspiration to achieve new possibilities.

I thank you wholeheartedly for your support.

Bhargav Dasgupta Managing Director & CEO

Annual Report 2014-15 11

Business Overview Statutory and Financial Section

Pranav Chaturvedi Bengaluru, Karnataka

FAIR

”“I have my two-wheeler (Honda CBR- 250R) insured with ICICI Lombard

and it has been smooth sailing always. I have insured all my vehicles with ICICI Lombard in the past, including a Hero Honda CBZ and Suzuki Wagon-R. The Company is truly customer centric. Its website is easy to navigate for new customers and old. Renewing the policy online is a hassle-free experience. Besides, the claims procedure is not cumbersome and there is transparency at every step. I will always recommend ICICI Lombard to my friends, family and colleagues alike.

In FY2015, India’s general insurance industry continued to grow, but at the slowest rate in last four years. It registered growth of 10.62% as the Gross Written Premium (GWP) grew to ` 805.93 billion in FY2015, as compared to ` 728.53 billion in FY2014.

The key sub-segments of the industry witnessed sluggish growth during the year. Motor insurance, which accounts for over 40% of the industry GWP, witnessed a growth of 10.8% in FY2015, compared to 13.7% in FY2014. The business grew

to ` 374.87 billion in FY2015, as compared to ` 338.25 billion in the previous fiscal. The Corporate segment recorded another year of single digit growth relatively estimated at 6%, compared to 7% a year ago.

Health Insurance segment (including specialised health institutions) displayed a positive picture, recording improved growth as compared to the previous fiscal. The segment increased by 15.6% from ` 176.79 billion in FY2014 to ` 204.43 billion in FY2015.

General Insurance Sector Overview

10.62%Growth in the Gross Written Premium (GWP) in India’s general insurance Industry in FY2015

15.6%Increase in the health insurance segment in FY2015 in India

14

Corporate OverviewICICI Lombard General Insurance Company Limited

WHOLESALE INSURANCE GROUP

The Wholesale Insurance Group caters to large corporate firms across industries and provides every client with customised solutions. It comprises various sub-divisions that include:

Specialised Industry Group that caters to large clients in specialised business segments.

International Business Group to cover international risks of Indian business interests.

Small and Medium Enterprises Group that focuses on MSMEs across industries.

Corporate Solutions Group to provide insurance solutions to large corporate companies across industries.

In FY2015, the Wholesale Insurance Group achieved several key milestones:1. Increased market share across

portfolios

a. Fire Market share increased to 7.2%

in FY2015, compared to 6.6% in FY2014. This was an outcome of a portfolio de-risking strategy, which helped spread concentration risk.

b. Engineering Market share increased to 7.6% in

FY2015 from 7.3% in FY2014, aided by new business, as the Company worked with large public energy conglomerates.

c. Marine ICICI Lombard increased its market

share to 8.2% in FY2015 from 8.0% in FY2014. The Company achieved it by leveraging innovations, such as risk management services, including ‘loss control’ activities of high frequency accounts using Marine Loss Control Engineering (MLCE).

Organisation Structure

Wholesale Insurance GroupOffers integrated insurance solutions to large conglomerates, small and medium enterprises. With fire, marine, engineering, liability solutions, employee group insurance schemes and large-scale health and personal accident covers, there are custom-fit solutions for every client.

Retail GroupServes individual customers through varied channels, such as agents, brokers,bancassurance, telesales, direct alliances, worksites and online. The insurance solutions cover health, home, motor, travel and personal accident space.

Shared Services Includes verticals that provide support and service to business functions. These include underwriting, customer relationship, technology, operations, reinsurance, broking, finance and accounts. Functions, such as human resources, legal, marketing, business analytics unit, administration and fraud control form part of this unit.

Government Business Group Provides insurance solutions to state and central governments or government-owned enterprises and rural customers. The product range includes weather, cattle, health and personal accident related products, among others.

Annual Report 2014-15 15

Business Overview Statutory and Financial Section

d. Liability Liability share witnessed upward

movement from 11.4% in FY2014 to 12% in FY2015 through enhanced channel engagement and network partnerships.

2. Selective approach in price sensitive health portfolio

The Corporate Health segment contributing 34% to the overall corporate insurance business of the industry grew by 15% in FY2015, compared to 8% in the previous one. However, the segment witnessed increased pricing pressures impacting underwriting profitability. The Company calibrated its growth strategy within this space to focus on select businesses that showcased financial viability from a long-term perspective.

3. Strategic initiatives to create market differentiation

The Wholesale Insurance Group focused on offering customer engagement and customised solutions during the fiscal. It introduced several new offerings which include:

a. Health Value Added Services

Wellness: This involved offering primary health care and specific disease management programmes to customers, implementing wellness activities across corporate accounts.

Cashless OPD: The Company launched an industry-first cashless OPD solution during the fiscal year in the form of a cashless OPD card. The offering was aimed at helping corporate enterprises manage the medical cases and expenses of their employees. The innovative offering benefited several large corporate customers and is poised to garner more customers in the coming months.

Managed care programme: Adopting the approach of fixed payment per enrollee, ICICI Lombard’s Managed Care programme improved the overall health index of its corporate clients’ employees, while reducing the total claim ratio.

b. Marine Value Added Services

These programmes were centred on loss control consulting across logistics supply chain. The Company provided customised solutions, such as anti-hijacking and transporter profiling to several corporate clients during the fiscal year. Quick and effective settlement of complex cargo claims were

15%Growth in the Corporate health segment in FY2015 as compared to 8% in FY2014

1341Hospitals were empanelled including 726 private and 615 public in FY 2015 by the Company

Organisation Structure (Contd.)

16

Corporate OverviewICICI Lombard General Insurance Company Limited

managed by specialists who provided tailor-made solutions for fast recovery, while keeping business interruption at a minimum. ICICI Lombard noted risk improvement in 40% cases, where it offered integrated insurance and risk engineering solutions for reducing high-frequency losses.

c. Property Value Added Services

These programmes were centred on property risk inspections, management of risk measures and personalised solutions, such as anti-fire and theft. ICICI Lombard’s fast assistance, fair practices and friendly services were highly lauded. In FY2015, the Company provided coverage to multiple corporate clients and introduced solutions, such as remote alarm system and fire-hydrant infrastructure.

d. Account Level Planning

Sales personnel were trained to migrate from a product to a solution selling approach. This led to an increase in wallet share of targeted corporate enterprises in FY2015

GOVERNMENT BUSINESS GROUP

ICICI Lombard’s Government Business Group caters to Rural India and provides insurance solutions through government welfare initiatives.

Over the years, ICICI Lombard has introduced various innovative solutions that protect the economically underprivileged sections of the society. In partnership with the government, the Company has delivered bespoke solutions to cater to individual needs. Its affordable products cover risks

and shield customers from setbacks like a failed crop or a major illness. Through evolving and scalable models, innovative product design, technology, speedy claim processing and public-private collaboration, ICICI Lombard endeavours to deliver confidence and security to rural India.

Rashtriya Swasthya Bima YojanaICICI Lombard has been a pioneer in implementing one of the world’s largest and among the most successful mass health insurance programmes, Rashtriya Swasthya Bima Yojana (RSBY). The centrally sponsored scheme illustrates how the government can facilitate the process of insurance benefits reaching to the below the poverty line (BPL) households and workers from unorganised sectors.

Providing health insurance to five members of every BPL family, including the family head, his spouse and up to three dependents, the scheme empowers the beneficiary with the freedom to choose the best possible treatment for his family from the empanelled private as well as public hospitals.

ICICI Lombard’s contribution to the scheme in FY2015:

1. Covered 21.65 lakh BPL families last year

2. Implemented across six states and Union territories, including 53 districts

3. Empanelled 1341 hospitals, including 726 private and 615 public

Saving Lives One of the unique initiatives jointly introduced by the Ministry of Road Transport & Highways and ICICI

and shield customers from setbacks like a

Annual Report 2014-15 17

Business Overview Statutory and Financial Section

Nitin Agarwal New Delhi

FAST

”“The ICICI brand means a lot to me, especially ICICI Lombard. Consistent

product innovation and the culture of speedy and effective response to our queries and concerns make ICICI Lombard stand out in the crowd. I have long been associated with ICICI Lombard as a customer, and the Company has always been helpful in times of need. No wonder, it remains an industry leader. I wish ICICI Lombard all the best for its future endeavours.

Lombard, the ‘Saving Lives’ scheme was launched in July 2013 on a pilot basis. The scheme provides hospitalisation insurance cover to the road accident victims of the Gurgaon- Jaipur stretch of the National Highway – 8 on a cashless basis. Taking care of the immediate needs of hospitalisation during the golden hour, it covers treatment of bodily injury caused by and arising out of a road accident. Six advanced life-saving and five basic life-saving ambulances are located on the identified stretch of the highway to take the victims from the accident spot to the nearest hospital for emergency medical treatment. Under this scheme, cover for the first 48 hours is provided, subject to the limit of ` 30,000 per victim.

ICICI Lombard was given the mandate to replicate the scheme on the Ranchi to Mahulia stretch in FY2015.

Health Insurance Scheme for Handloom WeaversThe scheme caters to weavers and ancillary workers, an important section of India’s unorganised handloom sector. It covers workers engaged in warping, winding, dyeing, printing, finishing, sizing, jhala-making and jacquard cutting. It provides a family coverage towards comprehensive healthcare and medical assistance to the weavers. It also includes a substantial provision for OPD services. The scheme covers pre-existing as well as new diseases with an annual limit of ` 15,000 per family.

Contribution to the schemeICICI Lombard covered 17.5 lakh families under the weavers’ scheme during the period of May to September 2014, post which it was merged with the Rashtriya Swasthya Bima Yojana.

Organisation Structure (Contd.)

20

Corporate OverviewICICI Lombard General Insurance Company Limited

Over 14.5 lakh claims were settled during the said time period.

Health insurance scheme for women sericulturist and workersThe health insurance scheme for women sericulturist and workers aims at empowering women sericulture farmers and workers in private reeling units to access healthcare amenities. It covers women beneficiaries (as the prime insured), her spouse and two children for comprehensive healthcare, including provision for OPD services. With many women beneficiaries availing of the scheme benefits, especially OPD services, the overall healthcare scenario of women has improved in the beneficiary locations.

Contribution to the schemeIn FY2015, the Company enrolled over 63,000 families and issued health cards in the states of Karnataka, Tamil Nadu, Jammu and Kashmir, Jharkhand and Assam.

Weather InsuranceNatural calamities continued to strike in FY2015. It was a year in which drought, floods, cyclones, unseasonal rainfall and hailstorms showed their devastating impact. The country’s food production was estimated to have reduced by 5% as a result of these calamities. ICICI Lombard stood by and served the farmers in a comprehensive way. It implemented the Weather Based Crop Insurance (WBCIS) scheme in 10 states and the Modified Agricultural Insured Scheme (MNAIS) in 17 districts. The Company, through both the schemes, enrolled 1.3 million farmers across the loanee and non-loanee categories.

The Weather Insurance business added ` 2.9 billion to ICICI Lombard’s direct business in FY2015. While the GWP for the WBCIS scheme stood at ` 1.39 billion, the GWP for the MNAIS scheme was ` 1.51 billion.

The Company implemented the scheme in the states of Chhattisgarh, Uttar Pradesh, Karnataka, Rajasthan, Jharkhand, West Bengal, Assam, Jammu & Kashmir, Uttarakhand and Himachal Pradesh. During the year, the Company increased the non-loanee coverage and increased its presence in Karnataka. Close to 1.4 lakh non-loanee farmers were enrolled using banks as intermediaries. ICICI Lombard also started the tablet-based policy coverage of non-loanee farmers, providing faster issuance of policy, using on-the-spot printing technology through mobile printers.

Annual Report 2014-15 21

Business Overview Statutory and Financial Section

Sandip Sathavara Ahmedabad, Gujarat

FRIENDLY

”“The ICICI Lombard team helped me at every step, whenever I had a problem. The Company’s customer-centric approach makes me feel that I am truly cared for. I have always received good suggestions from those I interacted with at the Company. I can say with a lot of conviction that the Company’s customers are its true brand ambassadors.

RETAIL GROUP

ICICI Lombard’s Retail Group continued to focus on the customer at every stage of operations. Harnessing technology to offer innovative risk solutions, it used various tools to keep up with the evolving needs of customers.

With an aim to offer best-in-class service, the Company maintained its stronghold across product lines. In FY2015, ICICI Lombard further reinforced its product portfolios, partner associations and claims management system.

to international

Motor Insurance ICICI Lombard continued to have a strong presence in the motor insurance segment. The Company remained committed to provide superior value proposition to customers at every point of interaction. In FY2015, ICICI Lombard focused on enhancing its channel management and customer life-cycle proposition by expanding its distribution networks, deepening its relationships with manufacturers and agents and implementing technology driven solutions.

Organisation Structure (Contd.)

24

Corporate OverviewICICI Lombard General Insurance Company Limited

ICICI Lombard

customised solutions to

Taking a step further towards being fair, fast and friendly with its customers, it offered seamless claims experience through remote assessment tools, such as tablet /mobile based applications.

ICICI Lombard also received regulatory approval to offer customers long-term product in motor segment, a long-term two wheeler insurance. This created an opportunity for market expansion, while providing hassle-free protection to customers.

Health InsuranceThe retail health insurance segment at the industry level grew rapidly with increased customer awareness and higher investments by insurance companies in expanding their reach to customers. ICICI Lombard continued to invest in creating a strong distribution footprint and innovative products, offering customised solutions to provide risk coverage as per customer requirements. The Company also provided loan protection solutions to customers. The product covered health risks of the insured, and at the same time ensured financial protection against a home loan.

Travel InsuranceThe Company provided wide range of services through the online medium to give its customers convenient solutions for travel insurance. During FY2015, the Company partnered with Falck India Private Limited to strengthen

its claims delivery, and improve its service to international customers.

Focusing on the growing leisure travel segment, ICICI Lombard offered economical solutions to non US travellers. ICICI Lombard secured fresh approvals from embassies of Schengen (a group of 25 European countries) to provide enhanced travel insurance to travellers visiting these countries. The Company offers a comprehensive travel insurance policy to cover unfortunate mishaps or medical emergencies, which might occur while travelling abroad.

SMELimited insurance penetration in the SME segment indicates significant opportunities for ICICI Lombard. The Company focused on identifying profitable segments to drive growth, and endeavoured to delight customers with superior claims and service experience. To achieve the same, the Company developed customised ‘Over-The-Counter’ policies for SMEs, and simplified the underwriting process. It also empowered its field force and agents to rate risks based on pre-defined parameters, ensuring fast processing of policies.

Customer Lifecycle ManagementICICI Lombard strives to provide the best service to its customers not only the first time, but at every stage. The Company ensured hassle-free renewal experience

for customers and proactively connected with them by sending renewal reminders through SMS and emails at periodic intervals. These SMS and emails constituted a link redirecting the customer to the renewal page on its mobile WAP or website, based on the device used.

During FY2015, ICICI Lombard increased its focus on contactability enrichment methods like data washing, sending welcome letters to non contactable customers and to communicate with the maximum number of customers. The additional contact details received from these activities were used at the time of renewals of customers’ insurance policies.

Annual Report 2014-15 25

Business Overview Statutory and Financial Section

”

FAIR

”“I have a lot of appreciation for ICICI Lombard. The Company’s products

technological platform for purchasing Home, Overseas Travel, Motor and Health Insurance is truly commendable. It’s convenient and manageable for any person. I must also mention the fact that the Company is truly transparent and trustworthy, which counts a lot for a customer like me.

Chhaya Kulabkar Mumbai, Maharashtra

SHARED SERVICES

Reinsurance During FY2015, ICICI Lombard’s reinsurance programme continued to pursue both proportional and non-proportional treaties. The Company structured the reinsurance programme, keeping in mind its philosophy of purchasing adequate cover to protect the value-at-risk. For FY2015, the Company maintained its retention across key product segments. To protect the net account against single large losses and natural disasters, it continued to buy appropriate risk and catastrophe

statistics for claim

reinsurance. It also got its net retained exposures, modelled by international agencies to ensure adequacy of limit of catastrophe reinsurance. The Company continued to purchase reinsurance protection for its speciality portfolio comprising liability, aviation, weather and offshore energy. ICICI Lombard strengthened its association with ScorRe, Swiss Re and Hannover Re for its key reinsurance programmes, while General Insurance Corporation (GIC) remained the Company’s largest reinsurance partner.

Organisation Structure (Contd.)

28

Corporate OverviewICICI Lombard General Insurance Company Limited

UnderwritingIn FY2015, ICICI Lombard introduced new add-on covers in its motor insurance portfolio. These included extended warranty and engine protect covers along with a host of customised offerings. Continued improvement in processes led to over 50% reduction in complaints and queries posed by the customers. Efficient and effective management of claims in the J&K floods and Hudhud cyclone in Andhra Pradesh, was appreciated by the High Court, as well as respective State Governments.

In case of health insurance, the Company adopted a selective underwriting approach, which positively influenced profitability. Implementation of e-Cashless module enabled the empanelled hospitals to process cashless requests faster. Simultaneously, implementation of scan mode of processing for reimbursement claims led to productivity enhancement, and also improved customer response time by 25%.

The Company also streamlined its property and marine risk management solutions to create processes for systematic study of risk exposures, and deliver tailored solutions, which include online fire and burglary detection, electrical audit and thermography, fire extinguishing solutions, project cargo survey and anti-hijacking solutions. This solution based

approach brought in the required differentiation for the Company in an otherwise competitive market.

The Company continued to adopt advanced technologies for serving customers. In FY2015, it introduced mobile based risk inspection, which enabled penetration in smaller sized adverse risk segments, and also leveraged in-house technology for identifying fraudulent claim trends, and thereby ensure genuineness of claims paid. In FY2015, the Company sustained its position among the best in the published statistics for claim performance.

Cost ManagementThe cost management team constantly endeavours to maximise value and build cost effective tools to benefit internal and external customers.

The Company continued to optimise costs in FY2015 through cost planning, co-ordination, control and reporting of cost data. During the year, ICICI Lombard gained cost savings in travel and communication expenses. The cost management team continued to spread cost saving awareness among employees through simple and effective tools.

InvestmentsIn FY2015, the Company achieved superior total return on its investment portfolio, compared to the benchmark.

Investments at ICICI Lombard are governed by the core value investing principles of the Company. Its asset mix is determined by two important factors: availability of superior investments at the right price and claim liabilities. The asset allocation strategy of the Company ensures liquidity, security and diversification. To strengthen the existing business, and efficiently manage risks arising out of duration, market, credit, legal and operation, the Company strictly follows commensurate risk management.

ICICI Lombard’s investments amounted to ` 92.38 billion in FY2015, an increase of 14.8%. In the last five years, the Company’s investment portfolio has grown at a Compounded Annual Growth Rate (CAGR) of 20.50%. In FY2015, the Company achieved a realised return of 10.29%, while the total

92.38 BILLIONInvestments were made by the Company in FY2015

20.50%CAGR in the Company’s investment portfolio in the last five years

Annual Report 2014-15 29

Business Overview Statutory and Financial Section

return was 17.84%. In a span of five years, the realised return and the total return have averaged 9.78% and 10.39% respectively. In the same year, ICICI Lombard’s ratio of year-end investment assets to net worth stood at 3.49 times. Over the last 12 years, the average total return was 10.92%, compared to 9.24% generated by the benchmark composite.

Additionally, ICICI Lombard’s investment assets of funds representing third party motor pool amounted to ` 6.07 billion with YTM of 8.46%. Realised return for FY2015 from this portfolio was 11.46%.

OperationsDuring FY2015, ICICI Lombard ensured excellence in its service performance, improving on the various dimensions of service quality i.e. responsiveness, empathy, assurance and reliability. The Company’s operations team

has centralised policy issuance under the Motor segment to enhance quality of delivery, and to improve service levels. Speedy response to the customer has been ensured by creating a priority channel. ICICI Lombard has also set up a direct interaction channel with corporate customers in Group policies to reduce the Turn Around Time (TAT), by close to 75%.

The Company has created the scale and capability in its operations function to service the growing and diverse needs of various business units within the organisation. ICICI Lombard successfully managed the volume of low ticket size products like two-wheelers, while keeping operating costs low. This has been managed by seamless integration with various systems and processes of distribution partners like Honda, Hero, IOCL & BPCL petrol pumps and various lending institutions.

The Company continued to manage operations related to the agency channel in a smooth and efficient manner. ICICI Lombard enhanced its systems to provide release of commissions on a daily basis, and also provided for automation of a large number of reports.

Customer Support and PEGIn an increasingly competitive industry, post-sales support can be the source of differentiation and value creation, as well as a crucial imperative to retain customers, and at the same time attract new customers.

ICICI Lombard aims at providing the best post-sales support with its contact centre, which serves as a critical touch point for the customer to experience the brand and its services. Driven by the professionalism, integrity and empathy of the Company’s people, it focuses on providing a personal touch to the customer. ICICI Lombard aspires to make life easier for its customers by delivering simple-to-understand products that specifically answer individual needs, and address their pain points. Besides, the organisation endeavours to offer best-in-class customer experience at the time of claim or ‘moment of truth’. It continuously makes its processes clear and transparent, and is fair to its customers, as it believes its purpose is to protect customer’s assets, while enriching their lives.

In a bid to better engage with customers further, the Company successfully in-sourced its call centre operations for three business functions, viz. Customer Service, e-Channel and i-Healthcare. This initiative led to enhanced resource efficiency and service improvements.

Contact centre agents are the Company’s most important brand ambassadors, and serve customers with a strong service orientation. It successfully completed hiring and training of leaders, managers and the support staff of its Customer Response Management (CRM) team. The team’s focus was on quality of

Organisation Structure (Contd.)

30

Corporate OverviewICICI Lombard General Insurance Company Limited

resolution provided to customers, and improving the percentage of first-time resolutions. Due to concerted efforts of the Call Resolution Time (CRT) team, first call resolution increased from 68% to 80%. The Company’s cross-functional teams continued to work seamlessly on all on-going operations.

The Company redesigned processes, making them simple and fast. Moreover, it provided skill development training, using its training tool - COMPASS. Operational efficiency of customer impacting processes improved, leading to an increase in service levels from 59% to 95%.

ICICI Lombard got control of the entire technology platform for its call centre, after completing the first phase of in-housing of technology infrastructure in July, 2014. It has placed an active set-up in Navi Mumbai and Hyderabad locations to route calls geographically. This gives the Company flexibility to route calls to the alternate location, in case of a downtime at one location.

The aforementioned efforts helped the Company reduce complaints by 13% in FY2015. After the Call centre was in-housed, repeat calls reduced to 2%, in comparison to 6% in the previous year when an outsourced call centre was operational. The ratio of complaints to total policies issued stood at 0.04% for FY2015 as against 0.06% for the previous fiscal.

13%Reduction in customer complaints in FY2015 of the Company

95%Increase in service levels of the Company in FY2015 as compared to 59% in FY2014

Annual Report 2014-15 31

Business Overview Statutory and Financial Section

FAST

”“My experience with ICICI Lombard has been extremely positive. The

Company’s execution capabilities are aligned to international standards. Every department works in a professional manner and the team appreciates the fact that the customer needs fast and effective response during a crisis. Whenever a friend or a relative asks me to suggest the name of a trustworthy insurance service provider in the general insurance

Rajeev Mishra Kolkata, West Bengal

Human Resource Customer expectations are changing. They seek greater convenience, improved speed of delivery and enhanced ease in transactions. Recognising this, ICICI Lombard has re-architected processes externally, as well as internally for its employees to deliver onto the promise of being fair, fast and friendly. To align to this philosophy, ICICI Lombard’s team needs to be more agile, and

demonstrate the ability to take prompt decisions. This is where Deeksha Learning Center (DLC), the umbrella brand established for all learning initiatives, continued to play a pivotal role by providing employees with the requisite knowledge and skills to enable agility and faster decision-making.

To deepen the knowledge levels of the various teams, the Company enhanced its sub-capability pockets from 27 to 66, in the last four years. The learning ladder and certification programmes were aligned in a way that enabled the team to make fair and faster decisions for customers. The Company has a vibrant team of Maroon and Maroon + certified employees. Code Maroon is an internal certification, which is a benchmark in the General Insurance

industry. Maroon + certification is offered in association with CII, London. ICICI Lombard has adopted ‘Leaders as Teachers’ philosophy, by constituting DLC Council to reinforce the critical learning for the team. Currently, the Company has 338 employees, who are instrumental in creating subject matter content, training and assessment.

The American Society for Training and Development (ASTD), now rechristened as ATD (Association for Training and Development), conferred the ’Best Practices in Learning & Development’ Award to ICICI Lombard for the third time in FY 2014-15.

Central to the philosophy of fair, fast and friendly, ICICI Lombard re-architected its service levels and in-sourced the processes to offer differentiated service through its call centre. The Company’s call centre team comprising 328 members was taken through COMPASS, ICICI Lombard’s service anchor that ensures that an employee understands and offers differentiated experience to the customer and builds trust.

27,002Children were benefitted by the ‘Caring Hands Campaign’ initiative of the Company in FY2015 across 236 municipal schools in 96 cities

Organisation Structure (Contd.)

34

Corporate OverviewICICI Lombard General Insurance Company Limited

Corporate Social Responsibility

ICICI Lombard has been committed towards the wellbeing of communities and the society. Its community projects enable citizens to fulfil their aspirations for a better quality of life.

The Company’s CSR roadmap for FY2015 involved healthcare and disaster relief activities. It also supported various causes, such as education, skill enhancement and sustainable livelihoods through the ICICI Foundation.

Caring Hands CampaignICICI Lombard’s employee driven CSR activity reached out to underprivileged children for the fourth year in a row. Steered towards preventive healthcare, free eye check-up camps were organised across the country for deprived children. In FY2015, the initiative benefited 27,002 children across 236 municipal schools in 96 cities. The activity helped identify 3,936 cases of poor vision that were provided with corrective lenses free of cost. 2,407 employees participated from various locations forming teams that joined hands to plan and execute the entire activity.

In the last four years, ICICI Lombard has reached out to more than 75,000 kids across 250 schools. With the Company’s long-standing commitment towards a better society and future for the country, ICICI Lombard is increasing the scope of its activity with each passing year.

Access to Sanitation and Healthcare (Preventive and Curative)ICICI Lombard, in association with KK Birla Memorial Trust’s Chambal NGO reached out to 6 villages of Kota district in Rajasthan. The six villages (Ballabhpur, Pachara, Pachara Ki Jhopariyan, Kakravada, Motikuan and Dabar) lacking basic healthcare facilities were provided a Mobile Medical Care Unit to offer healthcare facilities at their

doorstep. The unit, along with a doctor and a nursing assistant conducted OPD services, and dispensed medicines on the spot for common ailments. Cases requiring specialised treatments were referred to hospitals. Promoting curative healthcare, the initiative also helped in building awareness regarding health, hygiene and sanitation issues among the villagers.

Annual Report 2014-15 35

Business Overview Statutory and Financial Section

FRIENDLY“ ”

As a customer I have always received convenient and relevant solutions for my insurance requirements. The team believes in quick response and they know their job only too well. That is extremely reassuring and goes a long way in reinforcing trust.

Asif Rafat Husain Mumbai, Maharashtra

38

Corporate OverviewICICI Lombard General Insurance Company Limited

To the Members,

Your Directors have pleasure in presenting the Fifteenth Annual Report of ICICI Lombard General Insurance Company Limited (ICICI Lombard) along with the audited statement of accounts for the financial year ended March 31, 2015.

Industry OverviewThe gross premium of the industry grew from ̀ 728.53 billion in FY2014 to ̀ 805.93 billion in FY2015*, a growth of about 10.62%. Given the pricing challenges in the market, ICICI Lombard decided to scale down its business in the group and mass health insurance segments. ICICI Lombard also adopted a cautious approach in the weather insurance segment. As a result, the gross written premium (GWP) decreased marginally from ` 71.34 billion in FY2014 to ` 69.14 billion in FY2015. ICICI Lombard led the private players in general insurance sector with a market share of 19.0% and an overall industry market share of 8.3%.

Financial Highlights The financial performance for FY2015 is summarised in the following table:

(` billion)FY2014 FY2015

Gross written premium 71.34 69.14Earned premium 43.53 42.35Income from investments 7.88 9.28Profit before tax 5.20 6.91Profit after tax 5.11 5.36

Appropriations The profit after tax (PAT) for the year ended March 31, 2015 is ` 5.36 billion. The profit available for appropriation is ` 9.54 billion after taking into account the balance of profit of ` 4.18 billion brought forward from the previous year. The Directors are pleased to recommend aggregate interim dividends declared and paid during the year of ` 0.89 billion as final dividend for the year. The summary of appropriated profits is as follows:

(` billion)FY2014 FY2015

Balance of profits brought forward (0.93) 4.18Add: Profits during the year 5.11 5.36Total available profits for appropriation 4.18 9.54Less: Equity dividend for the year (interim) - 0.89

Dividend distribution tax - 0.17Transfer to general reserve - -

Leaving balance to be carried forward 4.18 8.48*Source: IRDAI & GI Council

Directors’ Report

` 805.93 BILLIONGross premium of the industry in FY2015

` 5.36 BILLIONProfit after tax in FY2015 of the Company

Annual Report 2014-15 39

Business Overview Statutory and Financial Section

DirectorsMinistry of Corporate Affairs (MCA) vide its circular dated June 9, 2014 clarified that the existing Independent Directors are required to be appointed under the provisions of the Companies Act, 2013 within one year from April 1, 2014 subject to compliance with eligibility and other prescribed conditions. The circular further prescribes that appointment of Independent Directors for a term of less than five years is permissible and appointment for any term (whether five years or less) is to be treated as one term under Section 149(10) of the Act.

Accordingly, the Board at its Meeting held on January 14, 2015 had approved the revision in norms governing tenure of appointment of Independent Directors for a maximum period of ten years to align with the provisions of the Companies Act, 2013. The Board at the same Meeting had approved the appointment of Dileep Choksi and M. K. Sharma, as Independent Directors of ICICI Lombard till Annual General Meeting (AGM) to be held in 2016 and 2017 respectively. Ashvin Parekh, another Independent Director of ICICI Lombard, was appointed in the Annual General Meeting held on June 20, 2014. Ashvin Parekh’s appointment is for a term of five years i.e. upto the Annual General Meeting to be held in 2019.

The Members of ICICI Lombard in the Extra-ordinary General Meeting held on March 4, 2015 had approved the appointment of all Independent Directors for their respective terms i.e. in case of Dileep Choksi till the AGM to be held in 2016, in case of M.K Sharma till the AGM to be held in 2017 and in case of Ashvin Parekh till the AGM to be held in 2019.

All Independent Directors have given declarations that they meet the criteria of independence as laid down under Section 149(6) of the Companies Act, 2013 and ‘fit and proper’ declaration as laid down under Corporate Governance Guidelines of Insurance Regulatory and Development Authority of India (IRDAI).

In terms of the provisions of Section 152 of the Companies Act, 2013, S. Mukherji and Chandran Ratnaswami, being Non-executive Directors of ICICI Lombard would retire by rotation at the forthcoming AGM and are eligible for re-appointment. Both S. Mukherji and Chandran Ratnaswami have offered themselves for re-appointment. Section 152 provides that the Independent Directors would be excluded from the total number of Directors for the purpose of computing the number of Directors whose period of office will be liable to determination by retirement of Directors by rotation.

During the year, Neelesh Garg, Executive Director of ICICI Lombard, expressed his desire to leave ICICI Lombard and the ICICI Group to pursue other opportunities with effect from February 2, 2015. The Board placed on record its deep appreciation for his contribution to ICICI Lombard. The Board at its Meeting held on March 31, 2015 had approved the appointment of Sanjeev Mantri as Executive Director of ICICI Lombard in place of Neelesh Garg with effect from May 2, 2015, subject to the approval of Members of the Company and IRDAI. Sanjeev Mantri was a Senior General Manager at ICICI Bank Limited and led the Bank’s Rural and Inclusive Banking Group. He is a qualified Chartered Accountant and a Cost Accountant. He joined ICICI Bank in 2003 where he led many businesses including Bank’s Small & Medium Enterprises Group. Under his leadership, the Bank was awarded the Asian Banker Award for the Best SME Bank-Asia Pacific in 2010. Board EvaluationThe Companies Act, 2013 vide Section 178(2) provides that every listed company and such other class of companies as may be prescribed shall carry out evaluation of every Director’s performance.

ICICI Lombard, being a prescribed class of company, carried out an evaluation of the performance of the

40

Corporate OverviewICICI Lombard General Insurance Company Limited

Board, its Directors, Chairperson and the Committees. The manner of carrying out the evaluation has been explained in the Corporate Governance Report.

AuditorsThe Joint Statutory Auditors, Khandelwal Jain & Co., Chartered Accountants and Chaturvedi & Co., Chartered Accountants, will retire at the ensuing AGM. On the basis of the recommendation of the Audit Committee, the Board at its Meeting held on April 24, 2015, has proposed the re-appointment of Khandelwal Jain & Co., Chartered Accountants and Chaturvedi & Co., Chartered Accountants, as Joint Statutory Auditors to audit the accounts of ICICI Lombard for the financial year ending March 31, 2016. You are requested to consider their re-appointment.

CapitalThe total capital invested by shareholders till March 31, 2015 including share premium, was ̀ 19.42 billion. The net worth of ICICI Lombard stood at ̀ 28.23 billion at March 31, 2015 as compared to ` 23.81 billion at March 31, 2014. The solvency position of ICICI Lombard at March 31, 2015 was 1.95 times as against minimum of 1.50 times prescribed by IRDAI.

Corporate Social Responsibility (CSR)The Board at its Meeting held on April 18, 2014 had constituted a Corporate Social Responsibility Committee of ICICI Lombard. The Board had approved adoption of Corporate Social Responsibility Policy (Policy) and Plan for CSR activities of ICICI Lombard at its Meetings held on October 15, 2014 and January 14, 2015 respectively.

The approved CSR Policy and report on CSR activities is annexed as “Annexure A”.

Rural and Social ResponsibilityICICI Lombard issued more than 500,000 policies in rural areas and covered more than 75,000 lives falling within the norms of social responsibility, as prescribed by IRDAI.

Directors’ Report (Contd.)

Public DepositsDuring the year under review, ICICI Lombard has not accepted any deposit from the public.

Foreign Exchange Earning and ExpenditureDuring FY2015, expenditure in foreign currencies amounted to ` 3,352.7 million and earning in foreign currencies amounted to ` 1,904.7 million.

Secretarial Audit ReportAs per Section 204 of the Companies Act, 2013 and the Companies (Appointment and Remuneration of Managerial Personnel) Rules, 2014, prescribed class of Companies shall obtain a Secretarial Audit Report from Company Secretary in Practice and such Secretarial Audit Report shall form part of this report.

The Board at its Meeting held on July 17, 2014 had appointed Dholakia & Associates, practising company secretaries, to conduct the secretarial audit of the Company for FY2015. The Secretarial Audit Report confirms that ICICI Lombard has complied with all the applicable provisions of various laws as mentioned in the audit report.

The Secretarial Audit Report is annexed herewith as “Annexure B”.

Extract of Annual ReturnThe details forming part of the extract of the Annual Return in form of MGT 9 is annexed herewith as “Annexure C”.

Related Party TransactionsSection 188(1) of the Companies Act, 2013 prescribed that the company shall not enter into a transaction with a related party (as defined vide clause 76 of Section 2 of the Act), except with the consent of the Board of Directors of the Company with respect to the transactions as prescribed. The Board at its Meeting held on April 18, 2014 had approved the Policy on Related Party Transactions (Policy). The Policy was subsequently amended at the Board Meeting held

Annual Report 2014-15 41

Business Overview Statutory and Financial Section

on January 14, 2015 wherein Audit Committee was empowered to provide omnibus approval for the related party transactions not exceeding ` 10.0 million per transaction.

During the year, ICICI Lombard had entered into related party transactions with the related parties as defined vide clause 76 of Section 2 of the Companies Act, 2013 in the ordinary course of its business and on an arm’s length basis.

The details of materially significant related party transactions entered by ICICI Lombard with related parties (in the ordinary course of its business and on an arm’s length basis) above the defined threshold, as prescribed under Section 188(1) of the Companies Act, 2013 and Rule 15 of the Companies (Meetings of Board and its Power) Rules, 2014, are annexed as “Annexure D”.

All related party transactions are placed before the Audit Committee on a quarterly basis.

None of the Directors has any pecuniary relationships or transactions vis-à-vis the Company.

Whistle Blower PolicyICICI Lombard has formulated a Whistle Blower Policy (Policy) which is designed to provide its employees, a channel for communicating instances of breach in the code of conduct, legal violation, actual or suspected fraud and on the accounting policies and procedures adopted for any area or item. The framework of the Policy strives to foster responsible and secure whistle blowing. This mechanism has been communicated to the employees and posted on ICICI Lombard’s intranet and an extract of the same has been posted on the website of ICICI Lombard.

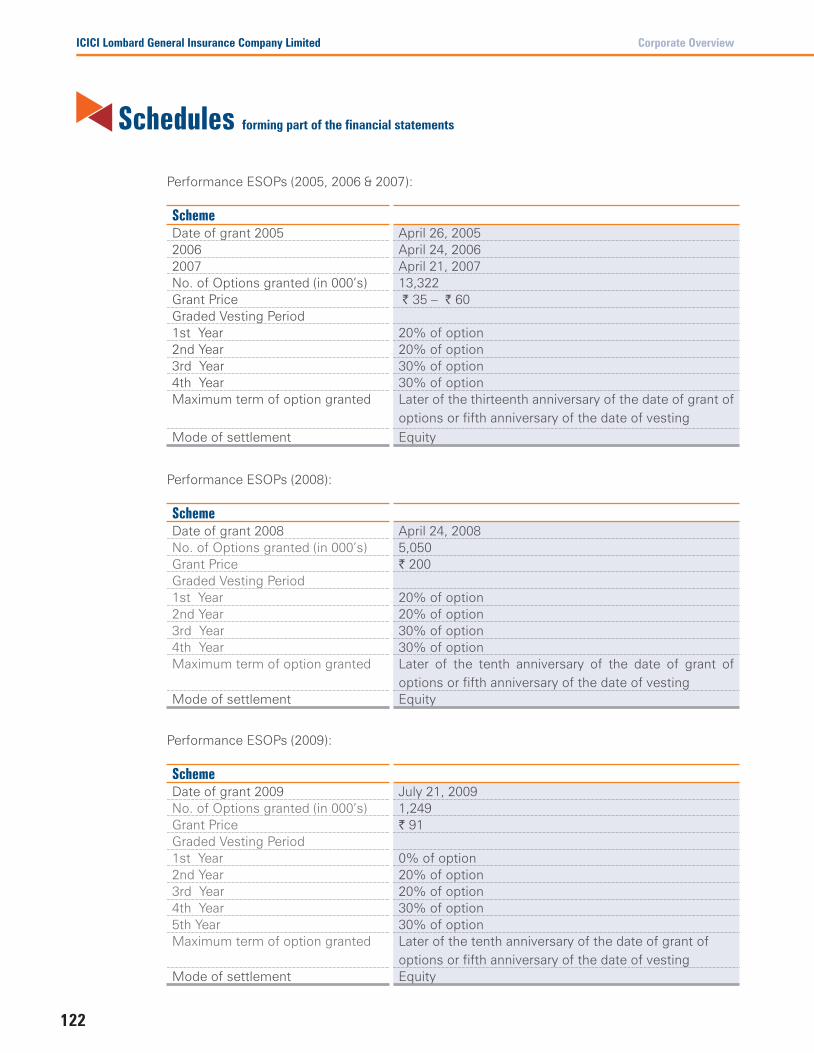

Employee Stock Option Scheme In FY2006, ICICI Lombard had instituted an Employee Stock Option Scheme (ESOS) to enable the employees

and Directors of ICICI Lombard to participate in its future growth and financial success. As per ESOS, the maximum number of options granted to any employee/Director in a year shall not, except with the approval of the Board, exceed 0.10% of ICICI Lombard’s issued equity shares at the time of grant and the aggregate of all such options (net of forfeited/lapsed) is limited to 5% of ICICI Lombard’s issued equity shares on the date of the grant.

The Board at its Meeting held on January 14, 2015 and the Members at the Extra-Ordinary General Meeting held on March 4, 2015 had approved the amendment in the ESOS 2005 to extend the exercise period by three more years in respect of options granted in the years 2005, 2006 and 2007. The said extension will provide additional years to the employees to exercise their options and in the event of ICICI Lombard getting listed during this period, the employees will automatically have the liquidity. In the absence of such extension, the options will start lapsing from April 2015 which will be detrimental to the interests of the employees.

Options granted in the years 2005, 2006, 2007, 2008 and 2010 vest in a graded manner over a four-year period, with 20%, 20%, 30% and 30% of the grants vesting each year, commencing not earlier than 12 months from the date of grant. Options granted for the year 2009 vest in a graded manner over a five year period with no vesting in the first year and 20%, 20%, 30% and 30% of the grant vesting each year in subsequent four years. Options granted for the year 2011 vest in a gradual manner over a two-year period, with 40% and 60% of the grants vesting each year, commencing not earlier than 12 months from the date of grant. Options can be exercised within a period of 13 years in respect of options granted in 2005, 2006 and 2007. Option other than those years can be exercised over a period of 10 years from the date of grant or five years from the date of vesting, whichever is later.

42

Corporate OverviewICICI Lombard General Insurance Company Limited

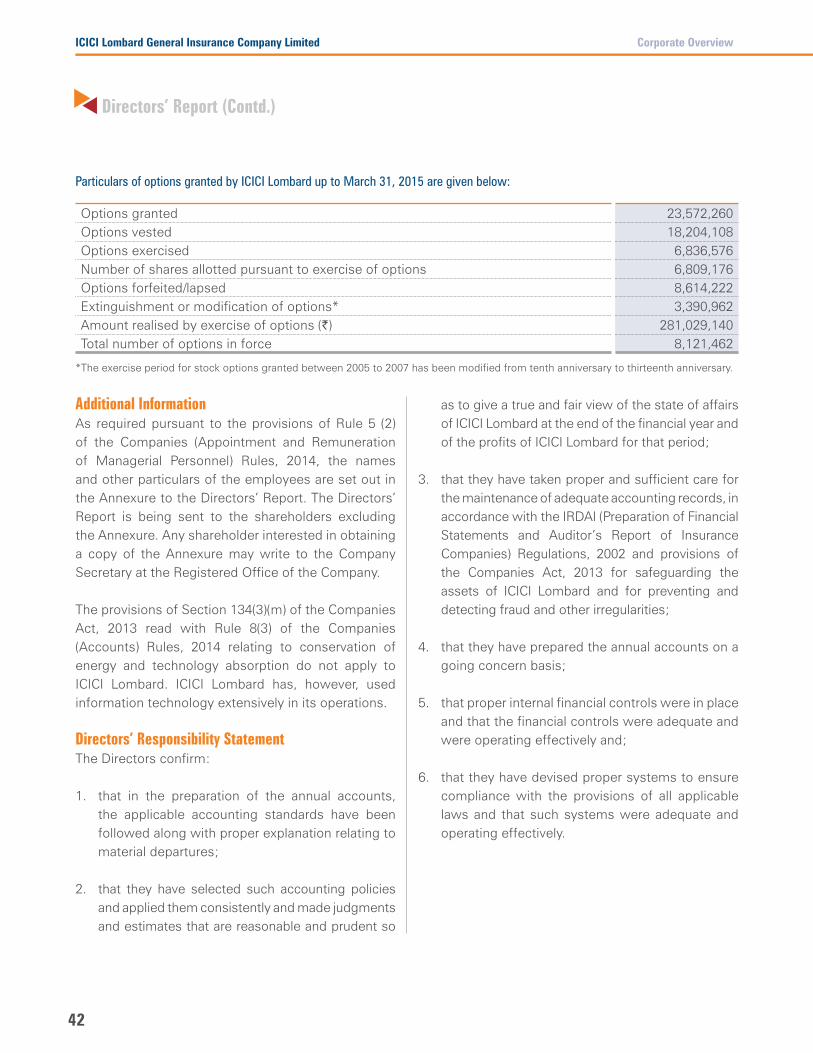

Particulars of options granted by ICICI Lombard up to March 31, 2015 are given below:

Options granted 23,572,260Options vested 18,204,108Options exercised 6,836,576Number of shares allotted pursuant to exercise of options 6,809,176 Options forfeited/lapsed 8,614,222Extinguishment or modification of options* 3,390,962 Amount realised by exercise of options (`) 281,029,140Total number of options in force 8,121,462

*The exercise period for stock options granted between 2005 to 2007 has been modified from tenth anniversary to thirteenth anniversary.

Additional InformationAs required pursuant to the provisions of Rule 5 (2) of the Companies (Appointment and Remuneration of Managerial Personnel) Rules, 2014, the names and other particulars of the employees are set out in the Annexure to the Directors’ Report. The Directors’ Report is being sent to the shareholders excluding the Annexure. Any shareholder interested in obtaining a copy of the Annexure may write to the Company Secretary at the Registered Office of the Company.

The provisions of Section 134(3)(m) of the Companies Act, 2013 read with Rule 8(3) of the Companies (Accounts) Rules, 2014 relating to conservation of energy and technology absorption do not apply to ICICI Lombard. ICICI Lombard has, however, used information technology extensively in its operations.

Directors’ Responsibility StatementThe Directors confirm:

1. that in the preparation of the annual accounts, the applicable accounting standards have been followed along with proper explanation relating to material departures;

2. that they have selected such accounting policies and applied them consistently and made judgments and estimates that are reasonable and prudent so

as to give a true and fair view of the state of affairs of ICICI Lombard at the end of the financial year and of the profits of ICICI Lombard for that period;

3. that they have taken proper and sufficient care for the maintenance of adequate accounting records, in accordance with the IRDAI (Preparation of Financial Statements and Auditor’s Report of Insurance Companies) Regulations, 2002 and provisions of the Companies Act, 2013 for safeguarding the assets of ICICI Lombard and for preventing and detecting fraud and other irregularities;

4. that they have prepared the annual accounts on a going concern basis;

5. that proper internal financial controls were in place and that the financial controls were adequate and were operating effectively and;

6. that they have devised proper systems to ensure compliance with the provisions of all applicable laws and that such systems were adequate and operating effectively.

Directors’ Report (Contd.)

Annual Report 2014-15 43

Business Overview Statutory and Financial Section

ANNEXURE ‘A’

Annual Report on Corporate Social Responsibility (CSR) Activities1. A brief outline of the Company’s CSR policy, including

overview of projects or programs proposed to be undertaken and a reference to the web-link to the CSR policy and projects or programs

Corporate Social Responsibility (CSR) has been a long standing commitment at ICICI Lombard and forms an integral part of its activities. The Company’s objective is to pro-actively support meaningful socio economic development. It works towards developing an enabling environment that will help citizens realise their aspirations towards leading a meaningful life.

In line with its objectives, the following areas have been shortlisted for the CSR roadmap health care, road safety, education, skill development and sustainable livelihoods, support employee volunteering in CSR activities and other areas such as disaster relief.

The CSR policy was approved by the Board of Directors in the Meeting held on October 15, 2014 and subsequently was put up on the ICICI Lombard website. Web-link to the CSR policy:

https://www.icicilombard.com/content/ilom-en/csr-policy/CSR_Policy.pdf

2. The Composition of the CSR Committee

The CSR Committee comprises one Independent Director, two Non-executive Directors and the Managing Director & CEO of ICICI Lombard and is chaired by an Independent Director. The composition of the Committee is set out below:

M. K. Sharma, Chairman (Independent Director) S. Mukherji (Non-executive Director) R. Athappan (Non-executive Director) Bhargav Dasgupta (Managing Director & CEO)

The functions of the Committee include review of CSR initiatives undertaken by the ICICI Lombard, formulation and recommendation to the Board of a CSR Policy indicating the activities to be undertaken by ICICI Lombard and recommendation of the amount of the expenditure to be incurred on such activities, review and recommend the annual CSR plan to the Board, making recommendations to the Board with respect to the CSR initiatives, monitor the CSR activities, implementation and compliance with the CSR Policy and to review and implement, if required, any other matter related to CSR initiatives as recommended/suggested by Companies Act.

3. Average net profit of the Company for last three financial years

The average net profit of the Company for the last three financial years calculated as specified by the Companies Act 2013 was ` 1,354.4 million.

4. Prescribed CSR Expenditure (two per cent of the amount as in item 3 above)

The prescribed CSR expenditure requirement for FY2015 is ` 27.2 million.

5. Details of CSR spent during the financial year (a) Total amount to be spent for the financial year; Total amount spent towards CSR during FY2015

was ` 27.8 million.

(b) Amount unspent, if any : Nil

44

Corporate OverviewICICI Lombard General Insurance Company Limited

(c)

Man

ner i

n w

hich

the

amou

nt s

pent

dur

ing

the

finan

cial

yea

r is

deta

iled

belo

w.

Sr

No

Proj

ects

/ A

ctiv

ities

Sect

orLo

catio

nA

mou

nt

outla

y (b

udge

t)

proj

ect o

r pr

ogra

m w

ise

Am

ount

sp

ent o

n th

e pr

ojec

ts o

r pr

ogra

mes

Cum

ulat

ive

Expe

nditu

re

upto

the

repo

rtin

gPe

riod

Amou

nt

spen

t: Di

rect

or

thr

ough

im

plem

entin

gag

ency

Dis

tric

ts (S

tate

)`

mill

ion

` m

illio

n`

mill

ion

1A

cces

s to

Hea

lthca

re:

Sani

tatio

n an

d H

ealth

care

(P

reve

ntiv

e an

d C

urat

ive)

Pro

gram

mes

, M

obile

Med

ical

Car

e U

nit-a

ssoc

iatio

n w

ith

Cha

mba

l NG

O

Hea

lthca

re6

villa

ges

of K

ota

Dis

tric

t in

Raj

asth

an (B

alla

bhpu

r, Pa

char

a, P

acha

ra K

i Jho

pariy

an,

Kakr

avad

a, M

otik

uan

and

Dab

ar)

0.8

0.8

0.8

Dire

ct

2Ey

e ch

eck-

up c

amps

for

unde

r priv

ilege

d sc

hool

ki

ds le

d by

em

ploy

ees

cove

ring

27,0

09 c

hild

ren.

C

ases

of p

oor v

isio

n pr

ovid

ed w

ith s

pect

acle

s.

Em

ploy

ee

Eng

agem

ent

Con

duct

ed a

t 22

9 sc

hool

s ac

ross

94

citie

s 7.

1(in

clud

ing

empl

oyee

vo

lunt

eerin

g co

st o

f

`

1.7

mill

ion)

7.7

(incl

udin

g em

ploy

ee

volu

ntee

ring

cost

of

`

1.7

mill

ion)

7.7

(incl

udin

g em

ploy

ee

volu

ntee

ring

cost

of

` 1.

7 m

illio

n)

Dire

ct

3D

isas

ter

Rel

ief

cont

ribut

ion

in J

amm

u &

Kash

mir

mat

chin

g em

ploy

ee c

ontr

ibut

ion

Dis

aste

r R

elie

fJa

mm

u &

Kash

mir

5.1

5.1

5.1

Dire

ct

4Pr

ojec

ts o

f IC

ICI

Foun

datio

n fo

r In

clus

ive

Gro

wth

Ski

ll de

velo

pmen

t &

sust

aina

ble

livel

ihoo

ds;

elem

enta

ry

educ

atio

n &

heal

thca

re

Ten

fully

ope

ratio

nal s

kill

deve

lopm

ent c

entre

’s o

pene

d.

Cen

tre’s

loca

ted

in J

aipu

r, Ko

lhap

ur, C

oim

bato

re, P

atna

, H

yder

abad

, Che

nnai

, Ban

galo

re,

Pune

, Guw

ahat

i and

Dur

g. E

lem

enta

ry e

duca

tion

proj

ects

in

Raja

stha

n an

d C

hhat

tisga

rh.

Hea

lthca

re p

rogr

amm

es in

Pur

i (O

dish

a), M

ehsa

na (G

ujar

at),

Bara

n (R

ajas

than

) and

Pun

e (M

ahar

asht

ra)

14.2

14.2

14.2

ICIC

I Fo