Embed Size (px)

Citation preview

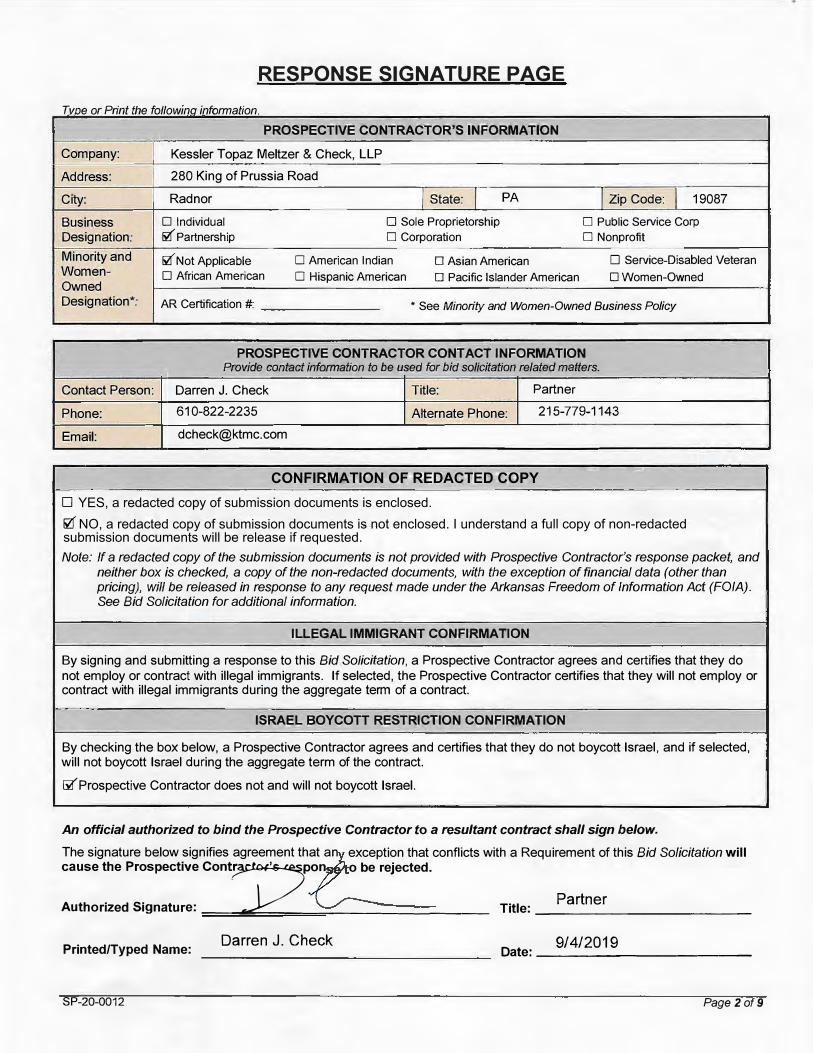

RESPONSE SIGNATURE PAGE

Tvne or Print the fol/owma m orrnatton. . f;

Company:

Address:

City:

- -

PROSPECTIVE CONTRACTOR'S INFORMATION Kessler Topaz Meltzer & Check, LLP

280 King of Prussia Road

Radnor I State: I PA I Zip Code: J 19087

Business 0 Individual □ Sole Proprietorship D Public Service Corp lief' Partnership Designation: D Corporation D Nonprofit

Minority and lief' Not Applicable Women-

D American Indian D Asian American D Service-Disabled Veteran

Owned D African American D Hispanic American □ Pacific Islander American □ Women-Owned

Designation*: AR Certification #: * See Minority and Women-Owned Business Policy

-

PROSPECTIVE CONTRACTOR CONT ACT INFORMA 'flON Provide contact information to be used for bid solicitation related matters.

Contact Person: Darren J. Check Title: Partner

Phone: 610-822-2235 Alternate Phone: 215-779-1143

Email: [email protected]

- ---- --

0' NO, a redacted copy of submission documents is not enclosed. I understand a full copy of non-redacted submission documents will be release if requested.

□ YES, a redacted copy of submission documents is enclosed.

Note: If a redacted copy of the submission documents is not provided with Prospective Contractor's response packet, and neither box is checked, a copy of the non-redacted documents, with the exception of financial data ( other than pricing), will be released in response to any request made under the Arkansas Freedom of Information Act (FOfA). See Bid Solicitation for additional information.

ILLEGAL IMMIGRANT CONFIRMATION

By signing and submitting a response to this Bid Solicitation, a Prospective Contractor agrees and certifies that they do not employ or contract with illegal immigrants. If selected, the Prospective Contractor certifies that they will not employ or contract with illegal immigrants during the aggregate term of a contract.

ISRAEL BOYCOTT RESTRICTION CONFIRMATION

By checking the box below, a Prospective Contractor agrees and certifies that they do not boycott Israel, and if selected, will not boycott Israel during the aggregate term of the contract.

[i(Prospective Contractor does not and will not boycott Israel.

An official authorized to bind the Prospective Contractor to a resultant contract shall sign below.

exception that conflicts with a Requirement of this Bid Solicitation will o be rejected.

The signature below signifies agreement that an cause the Prospective Cont

?on

Authorized Signature:---�---=----------------Partner Title: _____________ _

Printed/Typed Name: Darren J. Check

SP-20-0012

Date: __ 91_4_12_0_1_9 ______ _

Page 2 of9

CONFIRMATION OF REDACTED COPY

9/13/2019

Darren J. Check, Partner Kessler Topaz Meltzer & Check, LLP

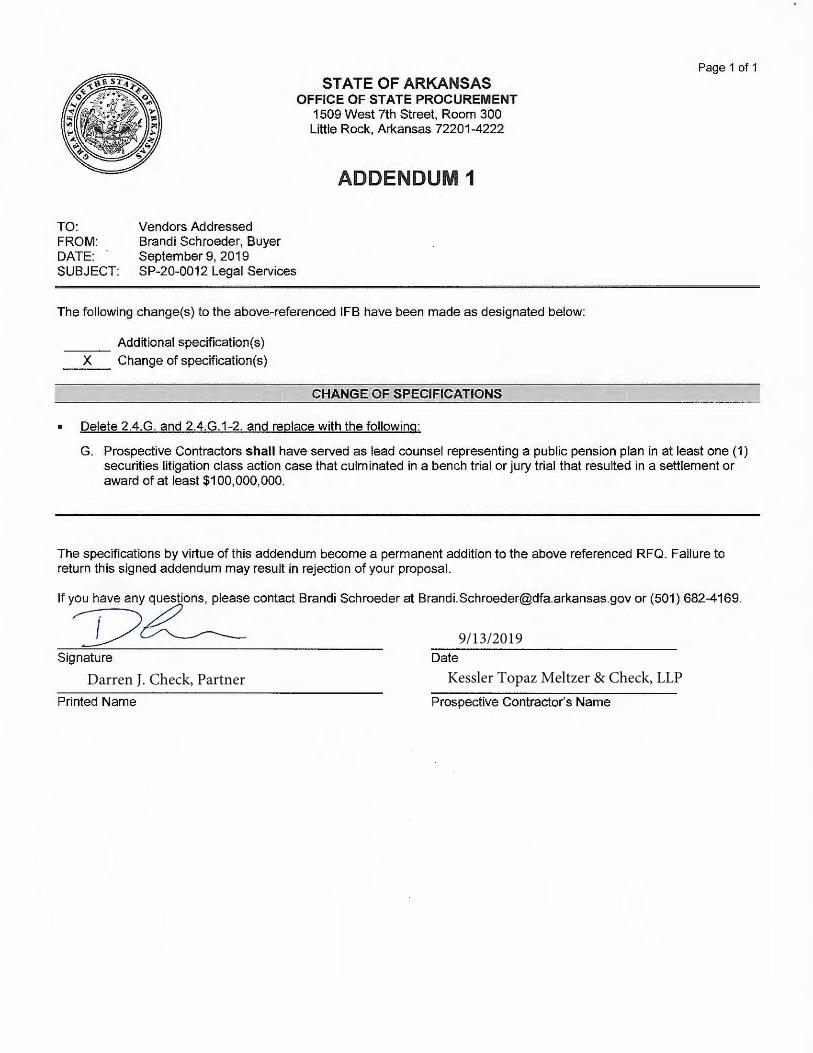

TO: FROM: DATE: SUBJECT:

Vendors Addressed Brandi Schroeder, Buyer September 9, 2019 SP-20-0012 Legal Services

ST ATE OF ARKANSAS OFFICE OF STATE PROCUREMENT

1509 West 7th Street, Room 300 Little Rock, Arkansas 72201-4222

ADDENDUM 1

The following change(s) to the above-referenced IFB have been made as designated below:

Additional specification(s) ---X --- Change of specification(s)

CHANGE OF SPECIFICATIONS

• Delete 2.4.G. and 2.4.G.1-2. and replace with the following:

Page 1 of 1

G. Prospective Contractors shall have served as lead counsel representing a public pension plan in at least one (1) securities litigation class action case that culminated in a bench trial or jury trial that resulted in a settlement or award of at least $100,000,000.

The specifications by virtue of this addendum become a permanent addition to the above referenced RFQ. Failure to return this signed addendum may result in rejection of your proposal.

If you have any questions, please contact Brandi Schroeder at [email protected] or (501) 682-4169. v~ Signature Date

Printed Name Prospective Contractor's Name

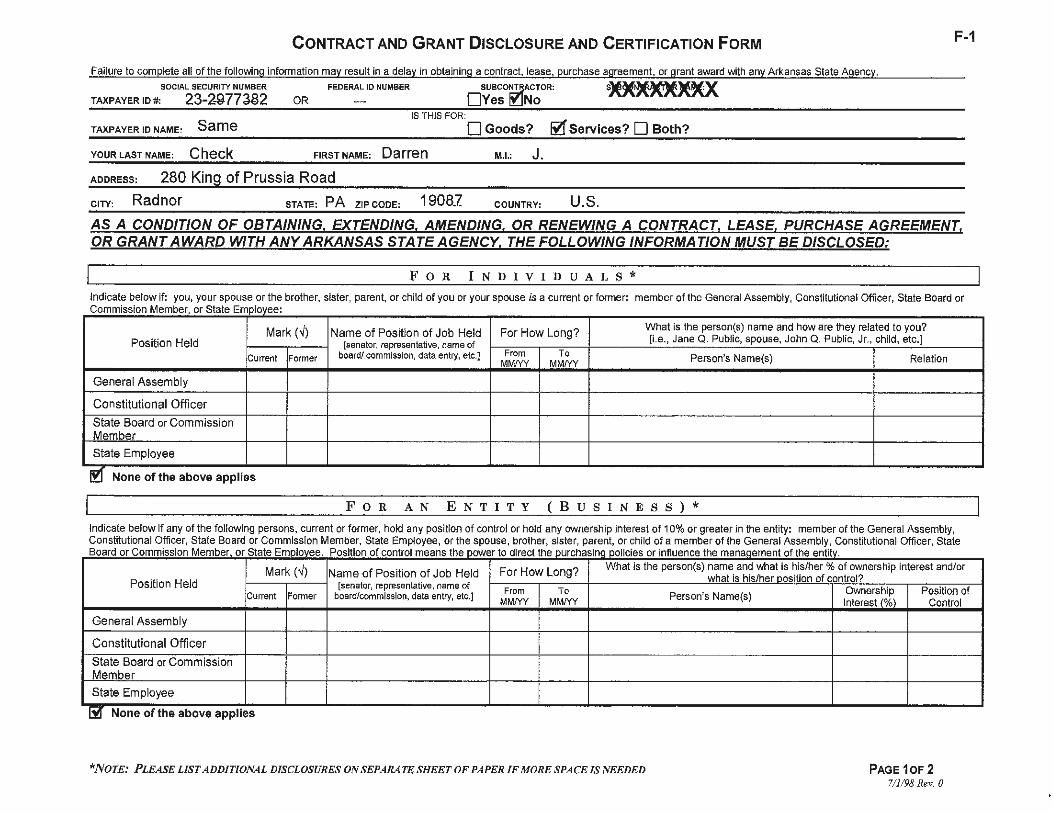

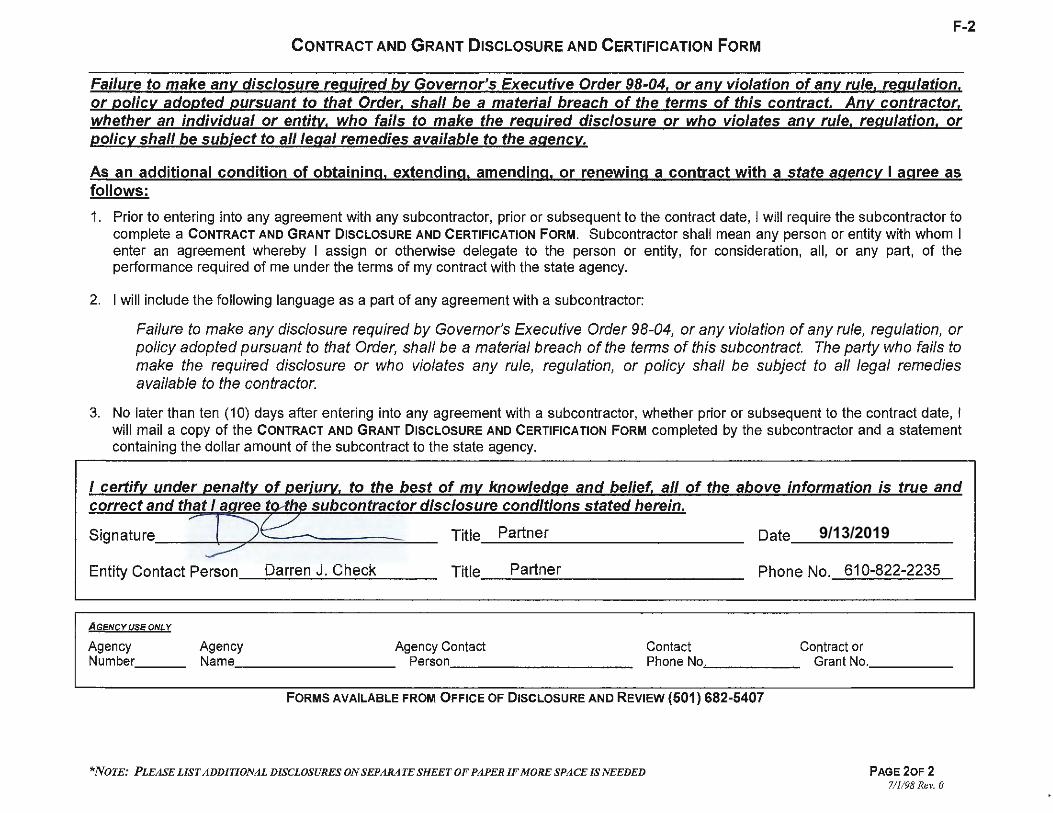

CONTRACT AND GRANT DISCLOSURE AND CERTIFICATION FORM

Failure to complete all of the following information may result in a delay in obtaining a contract, lease, purchase agreement, or grant award with any Arkansas State Agency.

SOCIAL SECURITY NUMBER FEDERAL ID NUMBER SUBCO~CTOR: s)E:~~~ TAXPAYER ID#: 23-2977JS2 OR □Yes ~No

TAXPAYER ID NAME: Same

YouR LAST NAME: Check

IS THIS FOR:

□ Goods?

FIRsT NAME: Darren M.I.: J.

ADDRESS: 280 King of Prussia Road

CITY: Radnor STATE: PA ZIP CODE: 1908-'Z COUNTRY:

~ Services? D Both?

U.S.

F-1

AS A CONDITION OF OBTAINING, EXTENDING, AMENDING, OR RENEWING A CONTRACT, LEASE, PURCHASE AGREEMENT, OR GRANT AWARD WITH ANY ARKANSAS STATE AGENCY. THE FOLLOWING INFORMATION MUST BE DISCLOSED:

FOR INDIVIDUALS*

Indicate below if: you, your spouse or the brother, sister, parent, or child of you or your spouse is a current or former: member of the General Assembly, Constitutional Officer, State Board or Commission Member, or State Emplovee:

Mark(✓) Name of Position of Job Held For How Long? What is the person(s) name and how are they related to you? (i.e., Jane Q. Public, spouse, John Q . Public, Jr., child, etc.] Position Held [senator, representative, name of

Current Former board/ commission, data entry, etc.] From To Person's Name(s) Relation MM/YY MM/YY

General Assembly

Constitutional Officer

State Board or Commission Member

State Employee

l!1 None of the above a p plies

FOR AN ENTITY (BUSINESS)*

Indicate below if any of the following persons, current or former, hold any position of control or hold any ownership interest of 10% or greater in the entity: member of the General Assembly, Constitutional Officer, State Board or Commission Member, State Employee, or the spouse, brother, sister, parent, or child of a member of the General Assembly, Constitutional Officer, State Board or Commission Member or State Emolovee. Position of control means the cower to direct the ourchasina oollcies or influence the manaaement of the entitv.

Mark(✓) Name of Position of Job Held For How Long? What is the person(s) name and what is his/her % of ownership interest and/or

what is his/her oosition of control? Position Held [senator, representative, name of From To Ownership Position of Current Former board/commission, data entry, etc.)

MM/YY MMIYY Person's Name(s) Interest{%) Control

General Assembly

Constitutional Officer

State Board or Commission Member

State Employee

ljf None of the above applies

*NOTE: PLEASE LIST ADDITIONAL DISCLOSURES ON SEP ARA TE SHEET OF PAPER IF MORE SPACE IS NEEDED PAGE 10F 2 7/1/98 Rev. 0

9/13/2019

F-2 CONTRACT AND GRANT DISCLOSURE AND CERTIFICATION FORM

Failure to make any disclosure required by Governor's Executive Order 98-04, or any violation of any rule, regulation. or policy adopted pursuant to that Order, shall be a material breach of the terms of this contract. Any contractor, whether an individual or entity, who fails to make the required disclosure or who violates any rule. regulation. or policy shall be subject to all legal remedies available to the agency.

As an additional condition of obtaining, extending, amending, or renewing a contract with a state agency I agree as follows:

1. Prior to entering into any agreement with any subcontractor, prior or subsequent to the contract date, I will require the subcontractor to complete a CONTRACT AND GRANT DISCLOSURE AND CERTIFICATION FORM. Subcontractor shall mean any person or entity with whom I enter an agreement whereby I assign or otherwise delegate to the person or entity, for consideration, all, or any part, of the performance required of me under the terms of my contract with the state agency.

2. I will include the following language as a part of any agreement with a subcontractor:

Failure to make any disclosure required by Governor's Executive Order 98-04, or any violation of any rule, regulation, or policy adopted pursuant to that Order, shall be a material breach of the terms of this subcontract. The party who fails to make the required disclosure or who violates any rule, regulation, or policy shall be subject to all legal remedies available to the contractor.

3. No later than ten (10) days after entering into any agreement with a subcontractor, whether prior or subsequent to the contract date, I will mail a copy of the CONTRACT AND GRANT DISCLOSURE AND CERTIFICATION FORM completed by the subcontractor and a statement containing the dollar amount of the subcontract to the state agency.

I certify under penalty of periury, to the best of my knowledge and belief. all of the above information is true and correct and that I a ree t h subcontractor disclosure conditions stated herein.

Title Partner Date ________ _

Title Partner Phone No. 610-822-2235 Entity Contact Person __ D_a_r_re_n_J_._C_h_e_c_k __ _ --------------

AGENCY USE ONLY

Agency Agency Agency Contact Contact Contract or Number __ _ Name_________ Person _________ _ Phone No~. _ _ __ _ Grant No. ____ _

FORMS AVAILABLE FROM OFFICE OF DISCLOSURE AND REVIEW (501) 682-5407

*NOTE: PLEASE LIST ADDITIONAL DISCLOSURES ON SEPARA TE SHEET OF PAPER IF MORE SPACE IS NEEDED PAGE 20F 2 711/98 Rev. 0

Kessler T

opaz M

eltzer & C

heck

Non

Discrim

ination

, An

ti- H

arassmen

t & E

qu

al Em

ploym

ent O

pp

ortun

ity Policy

Kessler T

opaz, in accordance with good practice and federal, state and local law

, maintains that

no Firm

employee or applicant for em

ployment w

ill be discriminated against or harassed because

of age, marital status, color, race, creed, sex, religion, national origin, sexual orientation,

ancestry, citizenship, disability, military/veterans status or any other characteristic protected by

applicable law.

A

ll applications for employm

ent will be considered w

ithout regard for any of the factorsidentified above.

E

mployee benefits, privileges, prom

otions and corrective action measures and all other

terms and conditions of em

ployment shall be determ

ined without regard for the factors

identified above.

All assignm

ents shall be made w

ithout regard to the factors identified above as they relateto either the client or F

irm’s personnel.

The F

irm w

ill not tolerate, condone or allow harassm

ent or discrimination by any F

irm

permanent or tem

porary employee, m

anager, supervisor, co-worker, client, custom

er, independent contractor, opposing counsel, court personnel or other non-em

ployee who conducts

business with the F

irm. V

iolations of this policy may result in disciplinary action, up to and

including imm

ediate discharge. In this regard, please note that the Firm

retains the right to punish conduct that, in its sole discretion, it deem

s to be inappropriate, discriminating and/or

harassing, regardless of whether such conduct is illegal. C

onduct prohibited in this policy is unacceptable in the w

orkplace and in any work-related setting outside the w

orkplace, such as during business trips, business m

eetings and business-related social events.

SE

XU

AL

HA

RA

SS

ME

NT

: For purposes of this policy, sexual harassm

ent is defined, as in the U

.S. E

qual Em

ployment O

pportunity Com

mission G

uidelines, as unwelcom

e sexual advances, requests for sexual favors and other verbal or physical conduct of a sexual nature w

hen, for exam

ple (i) submission to such conduct is m

ade either explicitly or implicitly a term

or condition of an individual’s em

ployment; (ii) subm

ission to or rejection of such conduct by an individual is used as the basis for em

ployment decisions affecting such individual; or (iii) such conduct has

the purpose or effect of unreasonably interfering with an individual’s w

ork performance or

creating an intimidating, hostile or offensive w

orking environment.

Sexual harassm

ent may include a range of subtle and not so subtle behaviors and m

ay involve individuals of the sam

e or different gender. Depending on the circum

stances, these behaviors m

ay include, but are not limited to: epithets, slurs or negative stereotyping; threatening,

intimidating or hostile acts; denigrating jokes and display or circulation in the w

orkplace of

e

written or graphic m

aterial that denigrates or shows hostility or aversion tow

ard an individual or group (including through e-m

ail).

SA

ME

SE

X H

AR

AS

SM

EN

T: S

exual harassment can involve m

ales or females being harassed

by employees of either sex.

Although sexual harassm

ent typically involves a person in a greater position of authority as the harasser, individua ls in positions of lesser or equal authority also can be found responsible for engaging in prohibited harassm

ent.

SE

X B

AS

ED

HA

RA

SS

ME

NT

: That is, harassm

ent not involving sexual activity or language (e.g., m

ale supervisor yells only at female em

ployees and not males), m

ay also constitute discrim

ination if it is severe or pervasive and directed at employees because of their sex.

OT

HE

R H

AR

AS

SM

EN

T: T

his policy also strictly prohibits harassment on the basis of any

other protected characteristic. Under this policy, harassm

ent is verbal or physical conduct that denigrates or show

s hostility or aversion toward an individual because of a person’s race, color,

creed, religion, national origin, age, marital status, sexual orientation, ancestry, citizenship,

disability, military/veterans status, or any other characteristics protected by law

or that of his/her relatives, friends or associates, and that: (i) has the purpose or effect of creating an intim

idating, hostile or offensive w

ork environment; (ii) has the purpose or effect of unreasonably interfering

with an individual’s w

ork performance; or (iii) otherw

ise adversely affects an individual’s em

ployment opportunities.

Harassing conduct includes, but is not lim

ited to: epithets, slurs or negative stereotyping; threatening, intim

idating or hostile acts; denigrating jokes and display or circulation in the w

orkplace of written or graphic m

aterial that denigrates or shows hostility or aversion tow

ard an individual or group (including through e-m

ail).

CO

MP

LA

INT

PR

OC

ED

UR

E: T

he Firm

strongly encourages applicants for employm

ent and em

ployees to report all perceived instances of discrimination or harassm

ent – regardless of the offender’s identity or position. Individuals w

ho believe they have experienced conduct that they believe is contrary to the F

irm’s policy or w

ho have concerns about such matters should file their

complaints w

ith the department head, a S

enior Partner or Hum

an Resources B

EF

OR

E the

conduct becomes severe or pervasive. E

mployees should not feel obligated to file their

complaints w

ith the department head or a S

enior Partner first before bringing the m

atter to the attention of H

uman R

esources.

Em

ployees who have experienced conduct they believe is contrary to this policy have an

obligation to take advantage of this complaint procedure. A

n em

ployee’s failu

re to fulfill this

obligation

could

affect his or her righ

ts in p

ursu

ing legal action

. The availability of this

complaint procedure, how

ever, does not preclude individuals who believe they are being

e

subjected to harassing conduct from prom

ptly advising the offender that his or her behavior is unw

elcome and requesting that it be discontinued.

Retaliating against an individual for reporting a violation of this policy or for participating in the

investigation of a claim of discrim

ination or harassment is a serious violation of this policy and

will be subject to disciplinary action up to and including im

mediate term

ination of employm

ent. A

cts of retaliation should be reported imm

ediately to Hum

an Resources.

It is the policy of the Firm

to investigate complaints of discrim

ination or harassment and to take

responsive action. All inquiries, com

plaints and investigations are treated confidentially to the extent consistent w

ith a complete and thorough investigation. M

isconduct constituting harassm

ent, discrimination or retaliation w

ill be dealt with appropriately. R

esponsive action may

include, for example, training, a referral to counseling and/or disciplinary action such as a

warning, reprim

and, withholding of a prom

otion or pay increase, reassignment, tem

porary suspension w

ithout pay, termination of em

ployment or any other action the F

irm believes is

appropriate given the circumstances.

False and m

alicious complaints of harassm

ent, discrimination or retaliation – as opposed to

complaints w

hich, even if erroneous, are made in good faith – m

ay be cause for appropriate disciplinary action, up to and including term

ination of employm

ent.

Finally, this policy should not, and m

ay not, be used as a basis for excluding or separating individuals of a particular gender, or any other protected characteristic, from

participating in business or w

ork-related social activities or discussions in order to avoid allegations of harassm

ent. The law

and the policies of the Firm

prohibit disparate treatment on the basis of sex

or any other protected characteristic, with regard to term

s, conditions, privileges and prerequisites of em

ployment. T

he prohibitions against harassment, discrim

ination and retaliation are intended to com

plement and further these policies, not to form

the basis of an exception to them

.

An em

ployee who has any questions or concerns about the E

qual Em

ployment O

pportunity program

or this policy should contact Hum

an Resources.

e

Response to the Arkansas Teacher Retirement System ("ATRS") Request for Qualifications for Legal Services ("RFQ No. SP-20-0012")

Due: September 19, 2019

State of Arkansas Office of State Procurement

1509 West 7th Street, Room 300Little Rock, Arkansas 72201-4222

KESSLERTOPAZ MELTZERCHECK LLP

' Al{)'Il~ ........... Arkansas Teacher Retirement System

VIA FED EX State of Arkansas Office of State Procurement Attn: Brandi Schroeder, OSP Buyer 1509 West Seventh Street, Room 300 Little Rock, AR 72201-4222 T: 501-682-4169

September 12, 2019

KESSLERTOPAZMELTZERCHECK LLP

ATTORNEYS AT LAW

Writer' s Direct Dial: (610) 822-2235 E-Mail: [email protected]

Re: Response to the Arkansas Teacher Retirement System ("ATRS") Request for Qualifications for Legal Services ("RFQ No. SP-20-0012")

Dear Ms. Schroeder:

Thank you for the opportunity to provide you, the Office of State Procurement, and the A TRS with a response to the above referenced RFQ. Enclosed please find the response of Kessler Topaz Meltzer & Check, LLP ("Kessler Topaz" or the "Firm") (one (1) original, three (3) complete copies and four (4) electronic versions included).

Please allow this executed letter to serve as evidence of my authority to bind Kessler Topaz to a resultant contract. We are confident that we can provide A TRS with the highest quality service in this important area and look forward to the opportunity to continue working together. Please do not hesitate to contact me if you have any questions or require any additional information.

DJC/nbl Enclosure

Very truly yours,

KESSLER TOPAZ MELTZER & CHECK, LLP

Darren J. Check, Esquire Partner

280 King of Prussia Road, Radnor, Pennsylvania 19087 T. 610-667-7706 F. 610-667-7056 [email protected]

One Sansome Street, Suite 1850, San Francisco, California 94104 T. 415-400-3000 F. 415-400-3001 [email protected]

WWW.KTMC.COM

SP-20-0012

DISCLOSURE INFORMATION

• These items will not be scored as part of the response evaluation; however, failure to provide the required items

will result in rejection of a Prospective Contractor’s response.

• Prospective Contractor may expand the space under each item/question to provide a complete response.

Describe all actual, potential, or appearances of conflicts of interest involving principal or lead attorneys in your law firm that may affect your law firm’s representation of ATRS. Provide an explanation.

Identify any known relationships, either business or personal, which your law firm or a member of your law firm has with any ATRS Board of Trustee member, investment consultant, investment manager, or key employee of ATRS. If aware of none, state "None." (A list of ATRS Board members, investment consultants, investment managers, and key employees can be provided upon request. A formal conflicts check will be required prior to contracting.)

Identify any relationships, either business or personal, which your law firm or a member of your law firm has with a person known to you to have substantial business dealings with ATRS or its affiliates. If aware of none, state "None."

Identify any other known conflicts of interest your law firm or a member of your law firm has with any ATRS Board of Trustee member, investment consultant, investment manager, or key employee of ATRS. If aware of none, state "None."

None.

None.

None.

None.

KESSLERTOPAZf) MELTZERCHECK u,

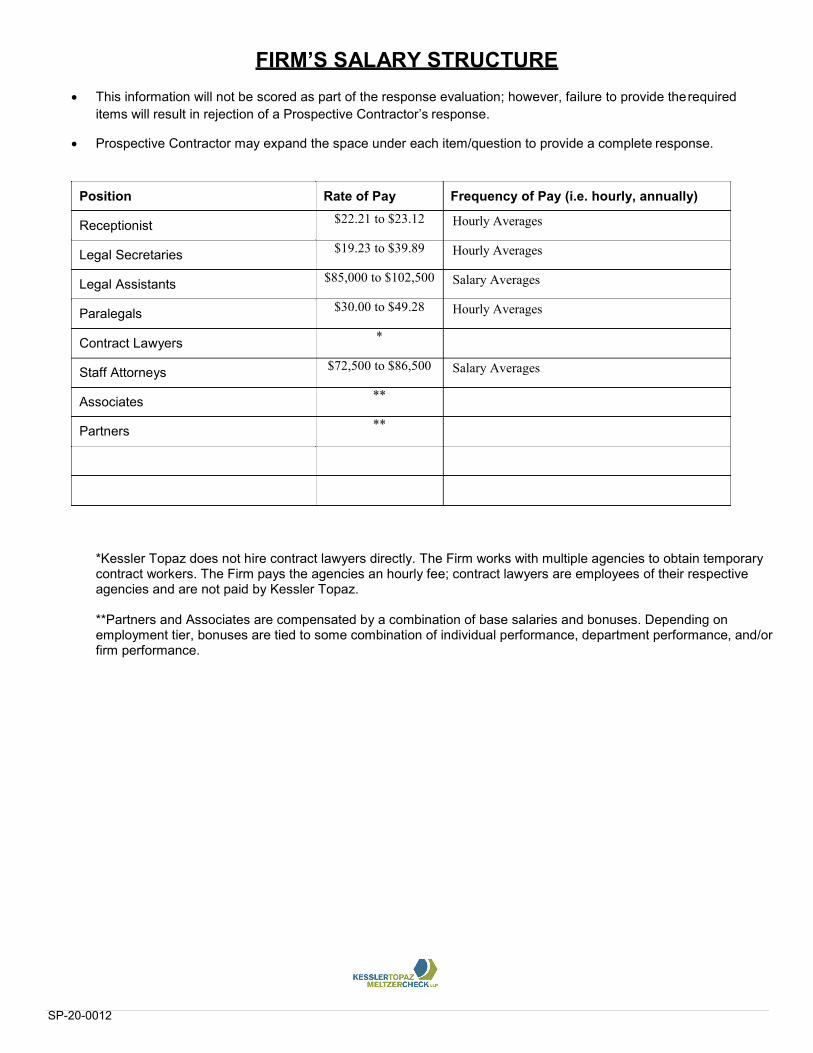

FIRM’S SALARY STRUCTURE • This information will not be scored as part of the response evaluation; however, failure to provide the required

items will result in rejection of a Prospective Contractor’s response.

• Prospective Contractor may expand the space under each item/question to provide a complete response.

Position Rate of Pay Frequency of Pay (i.e. hourly, annually)

Receptionist $22.21 to $23.12 Hourly Averages

Legal Secretaries $19.23 to $39.89 Hourly Averages

Legal Assistants $85,000 to $102,500 Salary Averages

Paralegals $30.00 to $49.28 Hourly Averages

Contract Lawyers *

Staff Attorneys $72,500 to $86,500 Salary Averages

Associates **

Partners **

*Kessler Topaz does not hire contract lawyers directly. The Firm works with multiple agencies to obtain temporarycontract workers. The Firm pays the agencies an hourly fee; contract lawyers are employees of their respectiveagencies and are not paid by Kessler Topaz.

**Partners and Associates are compensated by a combination of base salaries and bonuses. Depending on employment tier, bonuses are tied to some combination of individual performance, department performance, and/or firm performance.

SP-20-0012

KESSLERTOPAZf) MELTZERCHECK u.,

SP-20-0012 Page 1 of 46

INFORMATION FOR EVALUATION • Provide a response to each item/question in this section. Prospective Contractor may expand the space under each

item/question to provide a complete response.

• Do not include additional information if not pertinent to the itemized request.

Maximum RAW Score

Available

E.1 QUALIFICATIONS AND EXPERIENCE

A. Describe your firm’s law firm and law practice, including historical background, number andlocation of firm offices, number of attorneys, major areas of practice, and national andinternational jurisdictional experience.

Since 1987, Kessler Topaz Meltzer & Check, LLP (“Kessler Topaz” or the “Firm”) has specialized in the prosecution of securities class actions and has grown into one of the largest and most successful shareholder litigation firms in the field. With offices in Radnor, Pennsylvania (headquarters) and San Francisco, California, the Firm is comprised of 179 employees, including 94 attorneys as well as an experienced support staff consisting of 85 paralegals, in-house investigators, legal clerks and other personnel. With a large and sophisticated client base comprised of many of the most prominent institutional investors in the world, Kessler Topaz has developed an international reputation for excellence and has extensive experience prosecuting securities fraud actions in state and federal courts on a class and individual basis. For the past several years, the National Law Journal has recognized Kessler Topaz as one of the top securities class action law firms in the country. In addition, the Legal Intelligencer regularly awards Kessler Topaz with its Class Action Litigation Firm of The Year award. Lastly, Kessler Topaz and several of its attorneys are regularly recognized by Legal 500 and Benchmark: Plaintiffs as leaders in our field.

Over the last two decades the Firm has seen steady growth in both our client base and roster of significant shareholder litigation cases we are prosecuting. Kessler Topaz currently represents, advises, and works with many of the largest public pension funds and other institutional investors in the United States and from around the world. Some examples of our clients include the Arkansas Teacher Retirement System, Arkansas Public Employees Retirement System, the Arkansas State Highway Employees’ Retirement System, the California State Teachers’ Retirement System, the New York State Common Retirement Fund, the Ohio State Retirement Systems, the State of New Jersey – Division of Investment, the Pennsylvania Public School Employees Retirement System, the North Carolina Retirement System, the State of Michigan Retirement System, the Maryland State Retirement & Pension System, the Virginia Retirement System, the Iowa Public Employees’ Retirement System, the South Carolina Retirement System, the Employee Retirement System of Rhode Island, PGGM - Dutch National Pension Fund, Forsta AP-Fonden – First Swedish National Pension Fund, Fjarde AP-Fonden – Fourth Swedish National Pension Fund, Sjunde AP-Fonden – Seventh Swedish National Pension Fund, Danske Invest Management A/S, Nordea Invest Fund Management A/S, and Danica Pension Fund. Most recently Kessler Topaz was retained by the Alaska Permanent Fund Corporation, the State of Alaska Department of Revenue (Treasury Division), Dimensional Fund Advisors LP, Aberdeen Asset Management, Delaware Investments, the Russell Investment Company Funds, and Manning & Napier, to litigate claims related to the massive fraud at Petróleo Brasileiro S.A. (Petrobras).

For the past several years, Kessler Topaz has been responsible for some of the most significant securities class action recoveries on behalf of institutional investors. Since 2007 alone, the Firm has recovered over $11 billion on behalf of shareholders, which included settlements in cases against Tyco International ($3.2 billion), Bank of America ($2.425 billion), Southern Peru Copper Corporation ($2 billion), Wachovia ($627 million), Lehman Brothers ($616 million), Countrywide Financial Corp. MBS Litigation ($500 million), Bank of New York Mellon ($504 million), Allergan ($250 million), JPMorgan ($150 million) and Hewlett-Packard ($100 million).

Currently, Kessler Topaz is serving as lead or co-lead counsel in many of the largest and most significant securities actions currently pending in the United States, including actions against: General Electric, Qualcomm, Xerox, Celgene and SeaWorld Entertainment, Inc., among others. As demonstrated by the magnitude of these high-profile cases, we take seriously our role in advising clients to seek lead plaintiff

5 points

KESSLERTOPAZf) MELTZERCHECK UP

SP-20-0012 Page 2 of 46

appointment in cases, paying special attention to the factual elements of the fraud, the size of losses and damages, and whether there are viable sources of recovery.

Additionally, the Firm has a robust shareholder Derivative and Mergers & Acquisition Litigation Department which has been a leader in prosecuting shareholder actions in state and federal courts across the country. This Department has been at the forefront of representing institutional investors in all types of shareholder derivative and class actions, including cases involving or on behalf of companies such as Facebook, Inc., News Corporation, Monster Worldwide, Southwest Airlines, Comverse Technology, Encore Capital Group, Alcoa, Abaxis, and Brookfield Homes Corporation. These actions have focused on corporate governance abuses, such as the recent options backdating scandal, excessive executive compensation, insider trading, violations of stockholder voting rights and stockholder-approved equity plans, board entrenchment, violations of corporate bylaws and certificates of incorporation, and conflicted transactions with controlling shareholders. This Department also specializes in takeover litigation, and actively representing institutional investors in actions where shareholders are not receiving fair value for their investments. Notable recent actions include Genentech, Inc., Amicas, Inc., American Italian Pasta Company, and GSI Commerce, Inc.

Kessler Topaz is also very proud of its trial experience in cases against (or on behalf of) Energy Transfer Equity L.P. (“ETE”), Ebix, Inc., Longtop Financial Technologies Ltd., Southern Peru Copper Corporation, Dole Foods Co, Inc., and BankAtlantic Bancorp. Our trials against BankAtlantic (2010) and Longtop (2014) were only the tenth and thirteenth trials, respectively, to reach a verdict since the enactment of the Private Securities Litigation Reform Act of 1995 (“PSLRA”). Separately, in February 2018, August 2018, October 2011 and February/March 2015, the Firm concluded trials in the Delaware Court of Chancery in stockholder actions on behalf of Energy Transfer Equity, L.P., Ebix, Inc., Southern Peru Copper Corp. and former Dole Foods Co., Inc. shareholders/unitholders. In ETE, following a three-day trial, Kessler Topaz, and its Delaware co-counsel, secured a post-trial ruling that ETE’s general partner had issued preferred units to insiders in violation of the governing limited partnership agreement, one of the few successful challenges brought against managers of publicly traded limited partnerships. In Ebix, an unusual case concerning the company chairman and his board-awarded executive compensation, Kessler Topaz, obtained substantial revisions to the compensation arrangement in a post-trial settlement valued at $53 million. In Southern Peru, following a week-long trial, Kessler Topaz secured the largest damage award in Delaware Chancery Court history -- $2 billion. This award was upheld by the Delaware Supreme Court in August 2012. In Dole, following a nine day trial, Kessler Topaz won a $148 million verdict -- representing the second-largest post-trial verdict ever in merger litigation, behind only the Firm’s landmark $2 billion verdict in Southern Peru.

Further, Kessler Topaz has been at the forefront of representing institutional investors in shareholder litigation outside the United States – a growing area of importance given the U.S. Supreme Court’s 2010 decision in Morrison v. National Australia Bank. Kessler Topaz was co-counsel in the groundbreaking Royal Dutch Shell European Shareholder Litigation case that that recovered €323.8 million on behalf of non-U.S. investors in the Dutch Enterprise Court. More recently, Kessler Topaz, in partnership with local counsel, successfully concluded shareholder cases against Ageas, N.V. (successor entity to Fortis Bank, N.V.) (€1.3 billion; largest shareholder recovery in Europe to date), Royal Bank of Scotland in the UnitedKingdom (£900 million settlement), Olympus Corporation in Japan (¥11 billion settlement) and againstSino-Forest in Canada (CDN $117 million settlement). In addition, the Firm is currently litigating a classaction in Canada against Agnico Mining Corp., a group action in France against Vivendi Universal, S.A.,an action in Japan against Toshiba, and a recently filed action in Germany against Volkswagen. Lastly,we are currently following more than 100 non-U.S. actions for our clients, and have alerts set up in 25countries to advise us each time a new action is filed. For these many reasons, we feel that the Firm isespecially well positioned to continue to serve and represent ATRS in an increasingly global market.

For detailed information on our extensive U.S. shareholder litigation experience, please refer to the Firm’s response to Questions B. through E. below – outlining numerous matters which the Firm has, or is currently, prosecuted(ing) on behalf of our clients. With regard to our international shareholder litigation experience, below please find detailed information on the matters we have resolved and/or are currently pursuing around the world.

International Shareholder Litigation Experience

Again, Kessler Topaz has been at the forefront of representing institutional investors in shareholder litigation outside the United States – a growing area of importance since the U.S. Supreme Court’s 2010 decision in Morrison v. National Australia Bank. Kessler Topaz has been involved in twelve (12) international securities litigation cases in the past five years alone. Kessler Topaz’s first involvement with international securities litigation was in the groundbreaking Royal Dutch Shell European Shareholder Litigation case (“Royal Dutch Shell”). In Royal Dutch Shell, Kessler Topaz assisted local counsel in the recovery of $352 million on behalf of non-U.S. investors. This settlement of securities fraud claims on a

KESSLERTOPAZf) MELTZERCHECKu,

SP-20-0012 Page 3 of 46

class-wide basis under Dutch law was the first of its kind, and sought to resolve claims exclusively on behalf of European and other non-United States investors. Uncertainty over whether jurisdiction for non-U.S. investors existed in a 2004 class action filed in federal court in New Jersey prompted a significant number of prominent European institutional investors from nine countries, representing more than one billion shares of Shell, to actively pursue a potential resolution of their claims outside the United States. Among the European investors which actively sought and supported this settlement were Alecta pensionsförsäkring, ömsesidigt, PKA Pension Funds Administration Ltd., Swedbank Robur Fonder AB, AP7 and AFA Insurance, all of which were represented by Kessler Topaz.

This case challenged the Firm a great deal, requiring mastery of non-U.S. class action law, extraordinary travel requirements, liaising with local Dutch counsel, and the uncertainty of how the litigation would conclude. Ultimately, the Firm made the decision to pursue this action not only in order to provide an avenue for recovery for our clients, but also to gain invaluable international litigation experience. The Firm has been able to use the Royal Dutch Shell litigation model as a template for pursuing actions that must be pursued outside of the United States. Indeed, Kessler Topaz has successfully investigated, organized, funded, and represented large groups of institutional investors in the following actions that have reached a successful resolution:

1. Ageas, N.V.: In January of 2011, the Firm and its partners established a Dutch Foundation andfiled a claim on behalf of more than 200 institutional investors with €2 billion in losses against Fortis Bank,N.V. (“Fortis”) and its successor companies BNP Paribas and Ageas NL. The case against Fortis aroseout of the subprime mortgage crisis and alleged fraud in connection with the company’s failed 2007attempt to acquire Dutch bank ABN Amro Holding NV (ABN Amro). Specifically, we alleged that Fortismisrepresented the value of its collateralized debt obligations, its exposure to subprime-related mortgage-backed securities, and the extent to which the decision to acquire ABN Amro jeopardized its solvency.After the acquisition failed, Fortis encountered financial difficulties and broke up in the fall of 2008. Itsinvestors lost as much as 90% of the value of their investments. Our lawsuit survived rigorousjurisdictional challenges before both the Utrecht District Court and the Dutch Court of Appeals. Therewere other actions filed against Fortis by different groups of investors in both the Netherlands and inBelgium. In July 2018, the Dutch Court approved a global multi-party settlement for €1.3 billion with thedefendants. The settlement is the largest shareholder recovery in Europe to date.

2. Royal Bank of Scotland: The Firm represented and funded a large group of institutional investorsin an action against Royal Bank of Scotland (“RBS”) for its billions in losses in market value stemmingfrom facts which suggested that RBS materially mislead investors with respect to its true exposure tosubprime-related assets and collateralized debt obligations and inflated the value of its assets includingthose assets it acquired from the Dutch bank ABN Amro. A settlement of £900 million on behalf ofshareholders was reached and given full approval.

3. Olympus Corp.: On behalf of a number of institutional investors, the Firm pursued a case inTokyo, Japan against Olympus Corp. The case against Olympus was based on allegations that Olympusand certain of its officers and directors violated their duties under Japanese Company Law and committedaccounting and securities fraud between 1998 and 2011. The allegations against Olympus stemmed fromOlympus’ public disclosure in November 2011 concerning the falsity of its financial statements. On June28, 2012, we filed a complaint against in Tokyo on behalf of 47 plaintiffs with over ¥ 19 billion in claimeddamages. In June 2013, we filed a second complaint on behalf of 41 additional plaintiffs with total claimsfor over ¥ 16 billion in damages Following the filing of the second complaint, Olympus agreed tomediation and, a third group of 12 claimants, who had not previously filed a complaint, were also added tothe claims. Kessler Topaz and its partners were able to convince Olympus to agree to mediation. KesslerTopaz was an active participant in the mediation and successfully negotiated an ¥11 billion settlementwith Olympus.

Beyond these three group actions, the Firm has also taken an active role in pursuing securities class action litigation in Canada in order to protect the interests of the Firm’s clients trading securities in Canadian markets. For example, Kessler Topaz was U.S. counsel to a European institution serving as a named plaintiff on behalf of investors pursuing Canadian securities claims against Agnico Eagle Mines Limited (Agnico). In this capacity, the Firm assisted Canadian counsel in developing and prosecuting claims arising from Agnico’s failure to disclose ongoing operational issues at its Goldex mine prior to the suspension of mining operations at the mine in October 2011. In February 2016, courts in Ontario and Quebec approved a CDN$17 million settlement of the claims against Agnico. The Agnico settlement is notable in that a companion case in the U.S. (which covered purchasers of Agnico’s stock on a U.S. stock exchange and was based on nearly identical facts) had previously been dismissed.

In addition to these successfully concluded cases, the Firm is currently engaged in representing clients in shareholder litigation in the following actions outside the United States:

KESSLERTOPAZf) MELTZERCHECKu,

SP-20-0012 Page 4 of 46

1. Vivendi Universal, S.A.: The Firm is representing and funding a number of institutional investorsin a direct action venued in Paris, France, against Vivendi Universal, S.A. and Jean-Marie Messier(Vivendi’s former CEO) arising from the facts tried in the securities class action In re Vivendi UniversalSecurities Litigation in the Southern District of New York. The Paris suit represents investors whopurchased Vivendi’s securities on the Paris Bourse and whose claims were excluded from the U.S.litigation due to the Supreme Court’s decision in Morrison v. National Australia Bank.

2. Sino-Forest and Valeant Pharmaceuticals International, Inc.: The Firm, in partnership withlocal Canadian firms, is litigating two class actions in Canada against Sino-Forest and ValeantPharmaceuticals International, Inc. in an effort to protect investments our clients made on the Torontoexchange. Our involvement has allowed us to assist our clients in pursuing litigation in Canada. At thesame time, and because securities fraud class actions are relatively new in Canada, we have been ableto offer the Canadian firms our expertise in prosecuting the cases. In the Sino-Forest case, Judge Perellof the Ontario Superior Court of Justice recognized the value of our involvement when he decided thecarriage motion. In the Reasons for Decision, Judge Perell noted that Kessler Topaz has “a very highprofile and excellent reputation as counsel in securities class action lawsuits in the United States.”

In Valeant, Kessler Topaz is serving as U.S. counsel to a European client seeking to represent investors who purchased the Company’s shares on the Toronto Stock Exchange. The Valeant action was filed following revelations that the Company concealed its reliance on affiliated specialty pharmacies to distribute certain of its high-priced drugs and improperly recording sales to these specialty pharmacies in order to artificially inflate revenue. The Company’s reliance on affiliated specialty pharmacies is currently the subject of a probe by the United States Department of Justice.

In both the Sino-Forest and the Valeant cases the Firm has been active in assisting Canadian counsel with litigation strategy, crafting legal arguments, preparing and defending client depositions, and settlement negotiations. In Sino-Forest, while the action against the company is still pending, we helped negotiate a claims settlement with Ernst & Young, the Company’s auditor, for approximately $117 million Canadian. The $117 million settlement is the largest payment ever made by an auditor in Canada to settle a class action.

3. Banco Espirito Santo: The Firm is representing and funding a group of institutional investors whohold senior Banco Espirito Santo bonds in a recently filed action against the Bank of Portugal. The actionis an administrative challenge against the Bank of Portugal’s December 29, 2015 decision to re-transfercertain senior notes from Novo Banco S.A. back to the now defunct Banco Espirito Santo. When BancoEspirito Santo collapsed in August of 2014, the Bank of Portugal created a new bank, Novo Banco, andtransferred all assets and some bonds to Novo Banco. On December 29, 2015, the Bank of Portugaldecided to retransfer €2 billion worth of bonds from Novo Banco (which has assets) back to BancoEspirito Santo (which has no assets and is currently in bankruptcy proceedings). The result is thatbondholders lost at least 90% of the value of their bonds.

4. Volkswagen: The Firm is currently representing and funding a group of over 500 institutionalinvestors in securities litigation in Germany against Volkswagen and Porsche concerning Volkswagen’s“dieselgate” emissions scandal that caused substantial monetary damages to Volkswagen and Porscheshareholders. The Firm, its partners, and German counsel filed four separate group complaints betweenMarch 2016 and December 2018, alleging a total of more than €5 billion in damages. Altogether theFirm’s group is the largest group of investors pursuing action against Volkswagen and the group’s claimsrepresent more than 50% of the total monetary value of the 1750 investor claims filed in Germany againstVolkswagen. The proceedings in Germany are being adjudicated via the German model case proceedingsystem (or “KapMuG”) and the court appointed Deka Investments, one of the plaintiffs in our group ofover 500 investors, to serve as the model plaintiff. The court will utilize the model case proceedings inorder to make a determination on common issues of law and fact that apply to all investors who filed suitagainst Volkswagen. The parties are currently continuously exchanging briefing and the Higher RegionalCourt in Braunschweig, Germany is conducting routine oral hearings on various issues presented in themodel case.

5. Toshiba Corporation: The Firm is representing and funding a number of institutional investors insecurities litigation in Tokyo, Japan against Toshiba Corporation. The case against Toshiba arises from aseries of disclosures Toshiba made beginning on April 3, 2015 regarding a discovery of accountingirregularities that ultimately led to a ¥38 billion net loss for FY 2014/2015 and a revision of its pre-tax profitfigures dating back to 2008. The Firm, its partners, and Japanese counsel filed a complaint on behalf of alarge group of investors in late March of 2017. The case is ongoing.

6. Mitsubishi Motors Corporation: The Firm is representing and funding a number of institutionalinvestors in a securities case in Tokyo, Japan against Mitsubishi Motors Corporation. The case againstMitsubishi arises from Mitsubishi’s April 20, 2016 revelation that it had falsely reported the fuel

KESSLERTOPAZf) MELTZERCHECKu,

SP-20-0012 Page 5 of 46

consumption of certain models of its vehicles to the Japanese regulators since 2013. In late June of 2017, Kessler Topaz, its partners, and Japanese counsel filed a complaint in Tokyo on behalf of more than 100 institutional investors. The case is ongoing.

7. Petrobras (Petróleo Brasileiro S.A.): The Firm and its partners are representing and fundingnearly 100 institutional investors in an arbitration against Petrobras before the Market ArbitrationChamber of Brazil. The arbitration stems from the largest corruption scandal in Brazilian history in whichan investigation (dubbed “Operation Car Wash”) revealed that former executives of Petrobras, theBrazilian state-run energy company, had falsely inflated the value of certain projects for their own profitand to pay bribes and kickbacks to politicians. The arbitration is ongoing.

Kessler Topaz has recovered billions of dollars in the course of representing defrauded shareholders from around the world and takes pride in the reputation we have earned for our dedication to our clients. Kessler Topaz devotes significant time developing relationships with its clients in a manner that enables the Firm to understand the types of cases they will be interested in pursuing and their expectations. Further, the Firm is committed to pursuing meaningful corporate governance reforms in cases where we suspect that systemic problems within a company could lead to recurring litigation and where such changes also have the possibility to increase the value of the underlying company.

As an out-growth of our extensive shareholder litigation experience, and as discussed in detail below in our response to Question E.3.A. below, we are proud to offer the most comprehensive portfolio monitoring program in the field (covering both U.S. and non-U.S. litigation) and are also confident that no firm does more than we do to help ensure that institutional investors are getting their money back from securities class action settlements and judgments – by way of claims administration assistance. We currently provide these services to over 300 institutional investors worldwide, via our Securities Tracker team, comprised of thirty (30) attorney and non-attorney professionals. The team includes client service representatives, data intake and claims filing specialists, analysts, client reporting specialists and more. These professionals are focused on monitoring our clients’ investment portfolios, identifying losses in newly filed actions, monitoring cases through to resolution, and importantly, assisting to help ensure our clients are receiving their pro-rata share of proceeds from securities class action settlements and judgments. We currently file proofs of claim (in-house) for over one hundred and fifty (150) of our clients, and have assisted these clients in recovering over $300 million in securities class action proceeds in the past nine (9) years.

The shareholder litigation landscape has changed dramatically in the last ten+ years. The financial crisis and resultant securities cases have tested the mettle of the plaintiffs’ bar -- in battling the largest corporations and most competent defense counsel in the world – in an effort to achieve significant recoveries for shareholders. Further, as ATRS is aware, recent U.S. Supreme Court decisions and corporate actions have continued to curtail shareholder rights. These events have condensed the group of law firms who have been able to thrive in this environment, and who can offer the full complement of shareholder litigation-related services which are essential for institutional investors from a fiduciary standpoint – services which include global shareholder litigation identification, thorough case evaluation, zealous litigation representation, on-going monitoring, and claims administration assistance. For the reasons described herein, Kessler Topaz is hopeful ATRS will recognize the work we have done on behalf of institutional investors, including our zealous representation of ATRS in multiple securities litigation matters, and determine that we merit continuing to be included in ATRS’s pool of shareholder litigation firms going forward.

B. Describe your law firm’s experience successfully prosecuting securities litigation claims forpublic pension funds as lead plaintiff. Provide an overview of your law firm’s top five (5)recovery awards for a public pension plan, including the year each claim was filed, a summaryof the claim, and the outcome of the claim.

For the past several years, Kessler Topaz has been involved in the some of the most important shareholder litigation cases in our field. Since 2007 alone, the Firm has concluded 62 securities litigation cases, recovered over $11 billion on behalf of shareholders, brought six shareholder litigation matters to trial, as well prosecuted numerous shareholder derivative actions and takeover actions resulting in significant corporate governance reforms to wayward companies. The Firm also has 31 securities and direct actions currently pending where we represent public pension plans, another 21 shareholder derivative actions and takeover actions pending in which we represent public pension plans, and several non-U.S. jurisdiction cases pending and slated for trial in 2019/2020. Below please find the Firm’s top five (5) shareholder litigation recoveries for public pension plans and other institutional investors.

5 points

KESSLERTOPAZf) MELTZERCHECKu,

SP-20-0012 Page 6 of 46

Case: In re Tyco International, Ltd. Securities Litigation, No. 02-MD-01335-B (D.N.H.) Client: Voyageur Asset Management Resolution: $3.2 billion settlement. Settlement proceeds distributed. About the Case: Kessler Topaz, as Co-Lead Counsel in this highly publicized securities fraud class action, achieved a $2.975 billion recovery from Tyco International, Ltd. ("Tyco"), representing the largest securities class action recovery from a single corporate defendant in history, and a $225 million recovery from its auditor PricewaterhouseCoopers (“PwC”), representing the largest contribution ever paid by PwC to resolve a securities class action and the second-largest auditor settlement in securities class action history. As presiding Judge Paul Barbadoro aptly stated in his Order approving the final settlement, “[i]t is difficult to overstate the complexity of [the litigation].” Judge Barbadoro noted the extraordinary effort required to pursue the Tyco litigation towards its successful conclusion, which included review of over 82.5 million documents, more than 220 depositions and over 700 discovery requests and responses.

Case: In re Bank of America Corp. Sec. Litig., No. 09 MDL 2058 (DC) (S.D.N.Y.) Clients: PGGM Vermogensbeheer B.V. (Dutch National Pension Fund) and Fjärde AP-Fonden (Swedish National Pension) Resolution: $2.425 billion settlement (6th largest in history) and the implementation of significant corporate governance improvements. About the Case: Kessler Topaz, as Co-Lead Counsel, asserted claims for violations of the federal securities laws against Bank of America Corp. (“BoA”) and certain of BoA’s officers and board members relating to BoA’s merger with Merrill Lynch & Co. (“Merrill”) and its failure to inform its shareholders of billions of dollars of losses which Merrill had suffered before the pivotal shareholder vote, as well as an undisclosed agreement allowing Merrill to pay up to $5.8 billion in bonuses before the acquisition closed, despite these losses. On September 28, 2012, the Parties announced a $2.425 billion case settlement with BoA to settle all claims asserted against all defendants in the action. BoA also agreed to implement significant corporate governance improvements. The settlement, reached after almost four years of litigation with a trial set to begin on October 22, 2012, amounted at the time to 1) the sixth largest securities class action lawsuit settlement ever; 2) the fourth largest securities class action settlement ever funded by a single corporate defendant; 3) the single largest settlement of a securities class action in which there was neither a financial restatement involved nor a criminal conviction related to the alleged misconduct; 4) the single largest securities class action settlement ever resolving a Section 14(a) claim (the federal securities provision designed to protect investors against misstatements in connection with a proxy solicitation); and 5) by far the largest securities class action settlement to come out of the subprime meltdown and credit crisis to date.

Case: In re Southern Peru Copper Corp. Derivative Litigation, Consol. CA No. 961-CS (Del. Ch.) Client: Theriault Trust Resolution: $2 billion trial judgment in Plaintiff’s favor. About the Case: On October 14, 2011, Kessler Topaz and its Delaware co-counsel secured the largest damage award in Delaware Chancery Court history, a $1.3 billion derivative judgment against copper mining company Southern Peru’s majority shareholder Grupo Mexico. The litigation stemmed from Southern Peru’s 2005 acquisition of Minera Mexico, a private mining company owned by Grupo Mexico, for more than $3 billion in Southern Peru stock. Plaintiff alleged that the private company was worth more than a billion dollars less, but that Southern Peru’s board had approved this conflicted transaction in deference to its majority shareholder’s interests. In his trial opinion, Chancellor Leo Strine agreed, writing that Grupo Mexico “extracted a deal that was far better than market, and got real, market-tested value of over $3 billion for something that no member of the special committee, none of its advisors, and no trial expert was willing to say was worth that amount of actual cash.” He concluded that Southern Peru’s “non-adroit act of commercial charity toward the controller resulted in a manifestly unfair transaction.” Discovery in the case spanned years and continents, with depositions in Peru and Mexico. Defendants appealed the historic verdict to the Delaware Supreme Court, which affirmed the Court of Chancery’s judgment on August 27, 2012. The final judgment, with interest, amounted to $2 billion.

Case: In re Lehman Brothers Securities and ERISA Litigation, No. 09-md-2017 (S.D.N.Y.) Client: Alameda County Employees’ Retirement Association Resolution: $616 million settlement. Final approval granted by the Court on June 26, 2012 and November 28, 2013. About the Case: Plaintiffs alleged that the registration statements and prospectuses used to market Lehman’s numerous offerings leading up to its bankruptcy contained false and misleading information and omitted material facts regarding Lehman’s net leverage, risk management and concentration of risks. A $616 million settlement was reached on behalf of shareholders — $426 million of which came from various underwriters of the Offerings, representing a significant recovery for investors in this now bankrupt entity. In addition, $90 million came from Lehman’s former directors and officers (which is significant considering the diminishing assets available to pay any future judgment) as well as $99 million from Lehman’s auditor Ernst & Young.

KESSLERTOPAZf) MELTZERCHECKu,

SP-20-0012 Page 7 of 46

Case: Luther, et al v. Countrywide Financial Corp., et al., No. 12-cv-05125 (C.D. Cal.) Client: Maine State Retirement System Resolution: $500 million settlement; final approval received on December 5, 2013. About the Case: This settlement in the amount of $500 million on behalf of investors who purchased mortgage-backed securities issued by Countrywide Financial Corporation (“Countrywide”) represents the largest MBS class action recovery under the Securities Act in history. Plaintiffs alleged that Countrywide and various of its subsidiaries, officers and U.S. investment banks violated Sections 11, 12(a) (2) and 15 of the Securities Act of 1933 by making materially false and misleading statements in over 450 prospectus supplements relating to the issuance of more than $300 billion in Subprime and Alt-A MBS and the quality of the loans underlying the MBS. The matter further alleged that when information pertaining to the loans materialized, the value of the MBS declined, damaging investors. The settlement, which received final court approval on December 5, 2013, was achieved through prolonged mediation after more than five years of hard fought litigation.

C. Describe your law firm’s experience prosecuting securities litigation cases in the last five (5)years. Provide an overview of the claims that includes the year each claim was filed, a summaryof the claim, and the outcome of the claim.

Below please find a sample of shareholder actions the Firm has prosecuted in the last five (5) years (note: please refer to the Firm’s response to Question E.1.A. above (“International Shareholder Litigation Experience”) for a description of our recent international shareholder litigation matters). Again, in addition to these resolved matters, the Firm currently has 31 securities and direct actions currently pending where we represent public pension plans, another 21 shareholder derivative actions and takeover actions pending in which we represent public pension plans, and several non-U.S. jurisdiction cases pending and slated for trial in 2019/2020.

Securities Class Actions

Case: In re Allergan, Inc. Proxy Violation Securities Litigation, Case No. 8:14-cv 2004-DOC-KESx (C.D. Cal.) Client: Iowa Public Employees Retirement System Resolution: Settlement of $250 million; final approval granted August 14, 2018. About the Case: Kessler Topaz was appointed co-lead counsel on behalf of a class all persons and entities who sold Allergan, Inc. (“Allergan”) common stock between February 25, 2014 and April 21, 2014 and were harmed as a result of allegations of insider trading on behalf of defendants: (a) Pershing Square Capital Management, L.P. and various of its affiliates, and (b) Valeant Pharmaceuticals International, Inc., and various of its affiliates. The complaint alleged that the defendants purchased Allergan stock with material, non-public information during the class period, and by communicating material, non-public information, defendants violated, among other things, Section 14(e) of the Securities Exchange Act of 1934, as amended by the Williams Act of 1968 (the “Williams Act”), codified in 15 U.S.C. § 78n(e), as well as Exchange Act Rules 14a9 and 14e-3, codified at 17 CFR § 240.14e-3 andpromulgated by the SEC under the Exchange Act. According to the complaint, in exchange for insideinformation regarding Valeant’s plans to launch a hostile takeover and tender offer for fellowpharmaceutical company Allergan, Pershing Square Capital Management, L.P. agreed to secretly acquirenearly 10% of Allergan’s stock and commit those shares to support Valeant’s bid. On January 26, 2018,the involved parties reached a settlement in principle. On March 19, 2018, the court preliminarilyapproved the settlement and granted final approval on August 14, 2018.

Case: In re JPMorgan Chase & Co. Securities Litigation, 12-CV-03852-GBD (S.D.N.Y.) Client: Sjunde AP-Fonden (Swedish National Pension) Resolution: $150 million settlement reached Dec. 18, 2015, final approval granted May 10, 2016. About the Case: In November 2012, Kessler Topaz filed a Consolidated Amended Class Action Complaint in the Southern District of New York, alleging that JPMorgan Chase & Co. (“JPMorgan” or the “Company”) and various individual Defendants, including Chief Executive Officer James Dimon, violated Sections 10(b) and 20(a) of the Securities Exchange Act of 1934 and Rule 10b-5 promulgated thereunder, by making or authorizing materially false and misleading statements relating to the Company’s risk management policies and the proprietary trading activities of JPMorgan’s Chief Investment Office -- activities which ultimately led to over $6 billion in losses to the Company as a result of massive, proprietary bets placed on exotic credit derivatives by the so-called “London Whale,” a trader in the Chief Investment Office. As co-lead counsel, Kessler Topaz fended off defendants’ motion to dismiss, and succeeded in winning a hard-fought battle to win class certification for JPMorgan investors, thus prompting JPMorgan to settle the case.

5 points

KESSLERTOPAZf) MELTZERCHECKu,

SP-20-0012 Page 8 of 46

Case: In re HP Securities Litigation, C-12-5980 (N.D.Cal.) Client: PGGM Vermogensbeheer B.V. (Dutch National Pension Fund) Resolution: $100 million settlement; final settlement approval granted on November 16, 2015. About the Case: Kessler Topaz secured a $100 million recovery for Hewlett-Packard investors in June 2015 in a securities fraud action stemming from the company’s ill-fated $11 billion acquisition of British software maker Autonomy Corp in 2011. The action, filed in early 2013, alleged that HP and several of its current and former top officials, including CEO Meg Whitman, made false and misleading statements to investors about Autonomy’s valuation and financial reporting practices, prior to HP’s move to take an $8.8 billion write-down on the company in Nov. 2013. Kessler Topaz represented lead plaintiff PGGM Vermogensbeheer B.V. (Dutch National Pension Fund) and served as sole lead counsel in the matter. Final approval was granted November 16, 2015.

Case: In re Endo International PLC Securities Litigation, Case No. 17-CV-03711 (E.D. Pa.) Client: SEB Investment Management AB Resolution: $82.5 million settlement reached on July 11, 2019; pending court approval. About the Case: Kessler Topaz, as lead counsel and on behalf of Plaintiffs, alleged that throughout the Class Period, Defendants made false and/or misleading statements and/or failed to disclose that: (1) Reformulated Opana ER ("Opana") was not resistant to crushing; (2) Reformulated Opana was not abuse-deterrent and its use carried an inherent risk of abuse by grinding, snorting, or injecting; and (3) Reformulated Opana was contributing to an opioid public health crisis. Endo would ultimately remove Reformulated Opana from the market. When the true details entered the market, the lawsuit claims that investors suffered damages.

In addition, the Firm alleged that the Registration Statement, filed with the Securities and Exchange Commission and issued in connection with Endo's June 2, 2015 public offering of Endo common stock, contained untrue statements of material fact and omitted material facts. The Offering Materials failed to disclose material adverse trends, including the increase in reformulated Opana ER abuse by injection and related serious adverse events and failed to disclose the most significant risk factors that rendered the offering speculative or risky. Specifically, it was alleged that that the Company faced a material risk of regulatory action with respect to reformulated Opana ER, in that the FDA would require the drug's removal from the market on account of the material adverse safety risks and trends in intravenous abuse rates observed with the drug in post-marketing safety data.

Case: In re MGM Mirage Securities Litig., No. 2:09-cv-01558-GMN-VCF (D. Nev.) Clients: City of Philadelphia Board of Pensions and Retirement, Luzerne County Retirement System Resolution: $75 million settlement; final approval granted March 1, 2016. About the Case: Kessler Topaz served as Co-Lead Counsel in this securities fraud class action in the United States District Court for the District of Nevada. This action asserted claims for violations of the federal securities laws against MGM Mirage (nka MGM Resorts International) (“MGM” or “the Company”) and certain of MGM’s former officers and directors, who were alleged to have issued materially false and misleading statements and omitted material information regarding the Company’s financial condition, its access to financing, and the budget and schedule for CityCenter, a multi-building development featuring a casino, hotel, residential units, retail, restaurants, and entertainment venues. After 6 years of litigation, a settlement of $75 million was reached. The Court granted final approval on March 1, 2016.

Case: Jahm v. Bankrate, Inc., et al., No. 9:14-cv-81323 (S.D. Fla.) Client: City of Los Angeles Fire and Police Pension System Resolution: $20 million settlement; approved on February 6, 2017. About the Case: Plaintiffs alleged that Bankrate issued materially false and misleading financial statements, concurrently failing to disclose material adverse facts regarding the Company's publicly reported financial results between October 16, 2012 and September 15, 2014. Specifically, on September 15, 2014, the Company filed a Form 8-K with the Securities and Exchange Commission ("SEC") disclosing that the SEC had begun a formal investigation into Bankrate's financial reporting during 2012, with the principal focus on the financial quarters ended March 31, 2012, and June 30, 2012. As a result of the SEC investigation and its underlying issues, Bankrate announced that its previously issued financial statements for each of the fiscal years 2011, 2012, and 2013 should no longer be relied upon pending the conclusion of a complete internal review of the issues at the heart of the investigation. On the release of the news, the Company's share price fell from a close of $13.82 on September 12, 2012, to close at $11.92 on September 15, 2014.

Case: In re Longtop Financial Technologies Limited Securities Litigation, Civ. No. 11-cv-3658-SAS (S.D.N.Y.) (TRIAL EXPERIENCE*) Clients: Danske Invest Management A/S and Pension Funds of Local No. One, I.A.T.S.E. Resolution: Jury Verdict in Plaintiffs’ favor against former CFO of the company (November 2014) and default judgment order entered in April 2013 which included damages award of $882.3 million against the company.

KESSLERTOPAZf) MELTZERCHECKu,

SP-20-0012 Page 9 of 46

About the Case: In November 2013, serving as sole lead counsel, Kessler Topaz secured a $882.3 million default judgment in a securities class action against Longtop Financial Technologies Limited (“Longtop”) and its Chief Executive Officer, Wai Chau Lin a/k/a Lian Weizhou (“Lin”) that alleged that the China-based software and information technology company falsified its financial records, in violation of federal securities laws.

Kessler Topaz alleged that Longtop was a complete fraud from its initial public offering in October 2007 through the day the New York Stock Exchange permanently delisted Longtop in August 2011, saddling investors with hundreds of millions of dollars in losses and worthless American Depositary Shares (“ADS”). Among other things, plaintiffs claimed that Longtop publically reported false revenues, artificially inflated cash balances, failed to disclose tens of millions of dollars in loan obligations, and falsely reported that Longtop earned quarterly profits.

As detailed in the complaint in February 2010, the market began questioning the legitimacy of Longtop’s financial statements, causing the value of Longtop ADSs to decline. Then in May 2011, Longtop stunned investors when it announced that its outside auditor had abruptly resigned, describing in its resignation letter various fraudulent activities that Longtop had undertaken. Longtop ADSs, which reached a class period high of $42.86 per ADS, are now entirely worthless. The judgment found defendants Longtop and Lin jointly and severally liable to pay damages of $882.3 million plus 9% interest on such amount from February 21, 2008 to the date of payment.

Then, on November 21, 2014, after a three day trial, a New York federal jury entered a verdict holding former Longtop CFO Derek Palaschuk, who served from 2006 to May 2011, liable for the company’s alleged misrepresentations about its financial condition. It marked, at the time, only the 24 securities class action to go to trial and reach a verdict since 1996.

Case: In re Pfizer Securities Litigation, 4-CV-09866 (S.D.N.Y.) Client: Individual Investors Resolution: $486 million settlement; final approval granted on December 21, 2016. About the Case: The Complaint alleged: Throughout the Class Period, Defendants misrepresented and omitted material facts concerning the safety and marketability of Pfizer's Celebrex and Bextra products. Specifically, at all times during the Class Period, Defendants were aware of strong indicators that Celebrex and Bextra, drugs known as "Cox-2 Inhibitors," posed serious undisclosed health risks to consumers, that these undisclosed health risks would limit their marketability, and that the potential financial liability Pfizer faced from the harms these drugs caused posed a serious threat to the Company's finances. Nevertheless, Defendants concealed these facts from the investing public. Toward the close of the Class Period, a series of factual revelations from several sources caused the market to gradually perceive the truth about Pfizer's Bextra and Celebrex products.

For example, on November 4, 2004, the Calgary Herald reported that "Celebrex, a popular pain drug touted as the safe alternative after Vioxx was pulled from drugstore shelves, is suspected of causing at least 14 deaths and numerous heart and brain side effects." Then, on November 10, 2004, the New York Times revealed a study finding that "[t]he incidence of heart attacks and strokes among patients given Pfizer's painkiller Bextra was more than double that of those given placebos." As a result of these and other revelations, Pfizer's share price dropped from a closing price of $29.45 on November 3, 2004 to $27.15 on November 11, 2004 -- a drop of 8%.

Later, Pfizer shocked the market by revealing that "[i]n the Adenoma Prevention with Celecoxib (APC) trial, patients taking 400mg and 800mg of Celebrex daily had an approximately 2.5 fold increase in their risk of experiencing a major fatal or non-fatal cardiovascular event compared to those patients taking placebo, according to the National Cancer Institute (NCI). Based on these statistically significant findings, the sponsor of the trial, the NCI, has suspended the dosing of Celebrex in the study."

Case: Beaver County Employees' Retirement Fund, et al. v. Tile Shop Holdings, Inc., et al., No. 14-cv-786 (D. Minn.)Client: Erie County Employees Retirement System; Beaver County Employees Retirement FundResolution: $9.5 million settlement reached on June 14, 2017.About the Case: Plaintiffs alleged that Tile Shop failed to disclose that one of its largest suppliers,Beijing Pingxiu ("BP"), is an undisclosed related company secretly controlled by Fumitake Nishi, thebrother-in-law of the Company's CEO and a Tile Shop employee. On November 14, 2013, Gotham CityResearch LLC issued a report asserting that Tile Shop: (a) greatly exaggerated its true financialperformance; (b) failed to disclose BP as a material related party supplier; (c) uses BP to overstateinventories, understate cost of sales and overstate gross profits; (d) purchases goods from BP at or nearcost to allow Tile Shop to achieve an artificial cost advantage; and (e) overstates earnings. The complaintasserted that when this adverse information entered the market, the price of Tile Shop shares droppedsubstantially, damaging investors.

SP-20-0012 Page 10 of 46

Direct Actions/Opt-Outs

Case: Dimensional Emerging Markets Value Fund, et al. v. Petroleo Brasileiro S.A. - Petrobras, No. 15-cv-02165 (S.D.N.Y. Mar 23, 2015)Clients: Kessler Topaz represented over 30 institutional investors in 12 direct actions against Petrobras,including Alaska Permanent Fund Corporation, the State of Alaska Department of Revenue (TreasuryDivision), Dimensional Fund Advisors LP, Aberdeen Asset Management, Delaware Investments, theRussell Investment Company Funds, and Manning & Napier.Resolution: These cases were privately settled privately by the parties.About the Cases: These actions were brought against Petrobras, Brazil’s state-owned oil conglomerate,and arose out of a decade-long bid-rigging and bribery scheme that has been called the largestcorruption scandal in Brazil’s history. The actions asserted securities fraud claims on behalf ofpurchasers of Petrobras’s American Depositary Shares trading on the New York StockExchange. Kessler Topaz prosecuted the cases through the completion of discovery, which entailed over40 depositions on an expedited four-month schedule, and up to summary judgment. The firm's effortsincluded a trip to Brazil that resulted in the successful procurement of cooperation from a critical thirdparty witness. Kessler Topaz subsequently obtained a favorable ruling from the court permitting thedeposition of this Brazilian national in the U.S., which the firm conducted. At the time the actionsresolved, Kessler Topaz was in the midst of trial preparation.

Cases: Allianz Global Investors Kapitalanlagegesellschaft MBH, et al v. Merck & Co., Inc., et al., No. 07-cv-04451 (D.N.J. Sept 17, 2007); AFA Livförsäkringsaktiebolag et al. v. Merck & Co., Inc., 07-cv-04024 (D.N.J. Aug 27, 2007)Clients: Allianz Global Investors Kapitalanlagegesellschaft MBH, Allianz Global Investors LuxembourgS.A., Allianz Global Investors Ireland Limited, Skandinaviska Enskildabanken AB,Arbetsmarkinadsforsakringar Pensionsforsakringsaktiebolag, AMF Pension Fondforvaltning AB,Swedbank Robur AB, Danske Invest Administration A/S, Sjunde AP-Fonden (AP7), Fjarde AP-Fonden(AP4), Alecta Pensionsforsakring, Omsesidigt, AFA Sjukforsakringsaktiebolag, AFAtrygghetsforsakkringsaktiebolag, AFA livforsakringsaktiebolagResolution: These cases were privately settled between defendants and opt-out plaintiffs on June 28,2016.About the Cases: Kessler Topaz represented several institutional clients in opt-out litigation againstMerck & Co. Inc. relating to Merck’s representations concerning the cardiovascular risks associated withMerck’s blockbuster drug, Vioxx, which led to the withdrawal of Vioxx from the market. These two caseswere filed following the dismissal of a class action, Reynolds, et al., v. Merck & Co. Inc., et al., 483F.Supp.2d 407 (D.N.J. 2007). Kessler Topaz successful litigated these two opt-out actions, which allegedviolations of New Jersey common law, including common law fraud, negligent misrepresentation, and civilconspiracy.

Case: Connecticut Retirement Plans and Trust Funds et al v. BP, PLC et al., No. 4:12-cv-01272 (S.D.Tex.) Clients: Connecticut Retirement Plans and Trust Funds, North Carolina Department of State Treasurer, Public Employees Retirement Association of Colorado, Los Angeles County Employees Retirement Association, San Diego City Employees’ Retirement System, and the City of Philadelphia Board of Pensions and Retirement Resolution: Direct action filed on April 20, 2012; case is ongoing. About the Case: Kessler Topaz filed a direct action on behalf of three state pension funds and three municipal pension funds against BP plc (“BP” or the “Company”), two of BP’s U.S. subsidiaries and certain of BP officers on the two year anniversary of the explosion aboard the Deepwater Horizon drilling rig which resulted in the historic oil spill in the Gulf of Mexico. The action asserts claims under federal and state law against the Defendants for manipulating the price of BP’s American Depository Shares (“ADS”) and ordinary shares (traded on the London Stock Exchange).

Shareholder Derivative and Takeover Actions

Case: In re Dole Food Co., Inc. Stockholder Lit., No. 8703 (Del. Ch. Ct.) (TRIAL EXPERIENCE*) Client: City of Providence, Rhode Island Resolution: Trial verdict of $148 million in favor of stockholder class. About the Case: Kessler Topaz filed this stockholder class action alleging that Dole’s long-time controlling stockholder and chairman, David Murdock, and Dole’s president and long-time general counsel, C. Michael Carter, breached fiduciary duties owed to Dole’s public stockholders in connection with Murdock’s buyout of the public stockholders in a deal that closed on November 1, 2013. We sought to force Murdock to pay a fair price for Dole’s stock, above the $13.50 per share that Murdock had paid in the take-private transaction. Acting as co-lead counsel for a certified class of former Dole stockholders, and after rebuffing Murdock and Carter’s efforts to have the case dismissed before trial, Kessler Topaz

KESSLERTOPAZf) MELTZERCHECKu,

SP-20-0012 Page 11 of 46