Embed Size (px)

Citation preview

Restoring Confidence: Measuring and Managing Performance in Pensions

Bernard Marr, Jocelyn Blackwell and Kenneth Donaldson

December 2006

Restoring Confidence: Measuring and Managing Performance in Pensions

Page 2 of 35

Higham Dunnett Shaw plc (HDS) is a leading provider of consultancy and outsourcing solutions to the Life and

Pensions industry, with clients including major corporate pension schemes, pension trustees and leading

financial services institutions. The company employs over 500 people in offices across the UK, from management

consultants and actuaries through to experienced customer management and administration staff.

Key areas of expertise include:

� Improving quality and efficiency in the administration of corporate pension schemes, delivering:

− a broad spectrum of consultancy services for pension schemes and third party pension scheme

administrators. These focus on helping them to get the most out of their administrative functions and

to deliver a superior service to members

− pension scheme administration services, with proven procedures that can substantially improve the

efficiency and quality of the administration process, including for discontinued schemes

− Pension Protection Fund (PPF) preparation services, building on our recognised expertise as a market

leader in this field to assist professional trustees through the PPF assessment period

� Customer management, from building customer loyalty through to the effective handling of complaints. HDS

is a leading player in the outsourced mortgage endowment complaints arena and has processed hundreds of

thousands of complaints for a number of leading financial institutions.

www.hdsplc.com

Cranfield School of Management is a world-class university business school, renowned for its strong links with

industry and business. It is committed to providing practical management solutions through a range of activities

including postgraduate degree programmes, management development, research and consultancy.

www.som.cranfield.ac.uk

© Higham Dunnett Shaw plc and Cranfield School of Management, 2006

Restoring Confidence: Measuring and Managing Performance in Pensions

Page 3 of 35

Contents

Introduction .............................................................................................................................................4

Past Priorities and Present Challenges ..................................................................................................6

The Importance of Strategic Performance Management........................................................................9

Priorities (Minimising Risk, Maximising Value) and How They Influence the Process .........................14

Developing a Matrix for Administrative Performance in Pensions: A Case Study................................16

Summary and Conclusion.....................................................................................................................22

Appendix I: Examples of performance indicators .................................................................................24

Appendix II: Our Research Methodology ..............................................................................................32

About the Authors .................................................................................................................................33

Endnotes/Further Reading....................................................................................................................35

Restoring Confidence: Measuring and Managing Performance in Pensions

Page 4 of 35

Introduction

In the UK today there is widespread pessimism about the capabilities of pension schemes to deliver on their

promises. Behind this perception there is no doubt that pensions are indeed in a mess: problems with the way

schemes have been funded, how their investments have performed, the level of tax levied on them and the way

in which they have been run have fed a public and media appetite for financial scandal. Combined deficits are

estimated at around £1 trillion. This crisis of confidence has coincided with the much discussed “demographic

time bomb” which will see, in the next two decades, the largest retired population ever, both in absolute numbers

and as a proportion of the working population.

In the corporate world, it has long been recognised that to get to the top, and to stay at the top, an organisation

needs a strong governance framework linked to a co-ordinated system of strategic performance management

that together drives towards a common and clearly articulated goal. This thinking has not yet been fully

embraced by the pension industry. We believe that the solution to many of the problems faced by pension

schemes is to create strong and effective governance and administration that will enable trustees and sponsors

to minimise risk and maximise value in their schemes.

Higham Dunnett Shaw and Cranfield School of Management have developed an approach to measuring and

managing performance in pensions which can help the industry address some of these issues. Using clear

explanations, easily understood examples and a case study from the BP Pension Fund, one of the largest and

most progressive pension schemes in the UK, this paper aims to equip readers with the understanding and tools

with which to create their own excellent administration to support a superb and trusted pension scheme. The key

tool is known as MAPP – a Matrix for Administration Performance in Pensions.

This paper considers where MAPP will fit into the operation of a pension scheme, how it can be implemented and

how administrators and trustees can use the MAPP framework to create and maintain a well administered

scheme where all interested parties (members, sponsor, regulator) understand, and can see, its strengths, know

where it is going, know the route it will take and know how to monitor its progress along the way in order

continuously to learn and improve performance.

Administration excellence is the key to unlocking the potential for pension schemes (both “defined benefit” (DB)

and “defined contribution” (DC)) to once again be the trusted and effective providers of retirement security for

their millions of members. Standards have improved but still compare badly with other financial sectors such as

banking, where countless million transactions are routinely processed every day to astonishing levels of

accuracy, engendering a high level of trust and loyalty in their customers. By comparison, our experience is that

around one in three pension schemes suffer systematic, wholesale administration errors and omissions.

Examples are provided in this paper.

Restoring Confidence: Measuring and Managing Performance in Pensions

Page 5 of 35

The authors thank the BP Pension Fund for providing the focus and the initial funding for this work. We are also

very grateful to the organisations whose participation in our benchmark survey formed the foundation of MAPP.

These leading organisations include BP, Unilever, Masterfoods, Philips Electronics UK and Shell UK.

The lessons and findings presented in this paper might also be of interest to other financial service providers

such as banks and insurance companies, since they are facing similar issues.

Restoring Confidence: Measuring and Managing Performance in Pensions

Page 6 of 35

Past Priorities and Present Challenges

Pension provision has never been more topical, for all the wrong reasons, as these recent national headlines

demonstrate:

� “Pension deficit sinks historic firm”i

� “Pensions regulator under fire for Kvaerner deal - Fears that fund covering 31,000 former employees could

collapse”ii

� “300 retirement funds in danger of collapse, warns watchdog”iii

� “Marconi cursed by gaping pension hole”iv

� “Pension fund trustees force firm into administration”v

� “Pensions black hole set to reach £1 trillion”vi

� “Royal Mail faces £2bn pension deficit rise”vii

A pension scheme is simply a promise, made on trust, to pay retirement income in the future. It is a promise

founded on the strength of the funding targets, the returns on investments and the quality of the scheme’s

administration. Of these three, while funding and investment issues have been extensively scrutinised in the

industry and in the media, administration is the one that has over the years received the least attention either

from pension scheme trustees themselves or in the wider world. And yet properly structured administration can

support the direction of the scheme by supplying the information on which informed decision may be based.

Good administration can mean the difference between a scheme that does no more than tick the boxes to avoid

compliance failings and a scheme that actively and confidently sets out to provide a service that, through its

excellence, promotes member confidence and a sense of wellbeing.

The Pensions Regulator’s perspective

The problems facing members of DB (or final salary) schemes due to underfunding are now well known, but the

impact of operational risk on both DB and DC (or money purchase) schemes is far less widely appreciated.

However, the Pensions Regulator now has administration and governance firmly in its sights and has identified

two of its three principal challenges over the next three years asviii

:

� “To improve the governance of work-based pension schemes: There will be year-on-year improvement in the

extent to which trustees demonstrate knowledge and understanding of the governance requirements for their

schemes.”

� “To reduce the risks to members of work-based defined contribution pension schemes: Trustees and others

involved in running DC schemes (such as providers, administrators and employers) will have a clear

understanding of the significant risks inherent in such arrangements, especially in relation to administration,

member awareness and investment, and how they should be mitigating them.”

Restoring Confidence: Measuring and Managing Performance in Pensions

Page 7 of 35

The problems with DB pension provision notwithstanding, the Pensions Regulator has concluded that even

members of DC schemes could face difficulties in securing future payments because of poor record keeping.ix

John Ashcroft, head of strategy at the Pensions Regulator, said that such schemes faced significant risks,

especially in relation to pension administration with issues such as lost paperwork, contributions being paid at the

wrong rate or incorrect unit prices being applied. Such administration issues are by no means confined to DC,

with the older generation of highly complex DB schemes being particularly vulnerable.

The employer’s perspective

The key reason why employers offer a pension scheme is ‘to attract and retain quality people’, or at least this is

the common rhetoric that is proffered as an answer. But where is the hard evidence that scheme members and

potential new joiners appreciate, or even begin to understand, the value of the offer that is being made to them?

Huge amounts are poured into pension schemes every year, far too often without proper attention being paid to

the entire rationale for making the pension promise in the first place – as a key strategic Human Resources (HR)

tool to attract and retain the best personnel.

A key administration function is to ensure that members are informed about and understand their benefits and

that all records are correct and payments are accurate. Administration manages the communications and, as

such, controls the quality and effectiveness of the relationship between the trustees and scheme members. Get

the administration wrong and you damage the trust as well as the key HR benefit of a pension. If members do not

understand the benefits and do not appreciate them, then companies might as well not offer pensions at all.

‘Administration’ in this context includes: ensuring at all times the integrity of membership data, maintaining the IT

platform, paying the right benefits at the right time to the right people, collecting and investing contributions,

preventing fraud or theft, keeping standard explanatory texts clear, readable and up-to-date, regulatory

compliance, general support for the trustees, preparing the accounts, and day-to-day liaison with members, the

sponsoring employer, the trustees and all other interested parties.

The trustees’ perspective

Despite the pitfalls and risks inherent in running a pension department, administration struggles to receive the

attention it deserves. It rarely makes an appearance on trustees’ agendas as it is not considered a priority and

when it does, it is often restricted to a five minute summary at the end of a meeting. Yet, without efficient and

effective administration, trustees would fail to meet one of their main duties: to ‘act in accordance with the Trust

Deed & Rules’. Millions of pounds are spent every year monitoring investment performance but how much

budget is allocated to monitoring administration performance?

In their defence, trustees will argue that compared with the investment risk, operating risks are trivial and have

minimal impact. Here is a real example to show how this is not the case:

Restoring Confidence: Measuring and Managing Performance in Pensions

Page 8 of 35

Trustees’ lack of attention to data management and internal controls can also impede strategic HR objectives for

the scheme. An HR director may wish to implement an e-strategy, to enable members to find out about their own

benefits online, and to do simple ‘what if’ calculations. But very often the membership data is of such poor quality

that exposing the administration database (or a subset of it) online would simply be embarrassing. This means

that the trustees must either spend some money up front to fix the problem or continue with a highly manual,

back-office, Victorian quill and ink service. You may guess which solution is more frequently adopted.

Governance, Administration and Internal Controls

While there may be a range of definitions for the term ‘governance’, in this context, a strong governance system

will follow explicit, agreed processes and principles to control, manage and organise available resources to an

agreed strategic end. A good governance system also

requires a controlled system for review and change. The

benefit derived from good governance is efficient use of

resources to meet the trustees’ stated objectives, in an

environment where risks are known and appropriately

mitigated. Without explicit governance, outcomes are less

likely to relate to the trustees’ objectives.

The Pensions Regulator has published several codes of

practice as guidance for trustees and, although not

mandatory, should encourage the industry to adopt these

and drive them forward. In particular, the codes of practice

covering Trustee Knowledge & Understanding and Internal

Controls expect trustees to devote more attention to the

administrative aspects of running a pension scheme.

This move is to be welcomed, but it will take time. The pensions industry – trustees, advisers, employers, unions,

regulators, government, media and 16 million members of occupational pension schemes – is starting to debate

pension strategy. What can be learned from looking outside the pension box?

The following chapters consider how the industry can learn from leading thinking in strategic performance

management.

In a recent migration of member data from one administrator to another, countless errors were found in the

electronic records. Worse still, a box containing 300 paper files relating to members whose records had

never been entered into the electronic database was discovered. This meant that the formal actuarial

valuation of the pension scheme (in which the funding position was assessed and contributions set) could not

have included these liabilities – resulting in a major understatement of the scheme’s financial obligations.

Similarly, the reporting in the company’s Annual Report and Accounts was also incorrect.

The Medium Term Strategy Document,

published by the Pensions Regulator on 28 April

2006, states the following:

“Poor governance of many schemes”

“Our experience is that the standard of

governance of many schemes, particularly

smaller ones, is poor. Our in-house research

shows clear evidence of low standards of

trustee knowledge and understanding,

particularly in schemes with under 1,000

members.”

Restoring Confidence: Measuring and Managing Performance in Pensions

Page 9 of 35

The Importance of Strategic Performance Management

In order to compete, or indeed to survive, today’s businesses require strategic performance management

approaches which enable them to measure and manage what really mattersx

. The wrong approach will often

perpetuate dysfunctional behaviour and jeopardise performance. Three key components of this problem are:

1. an incomplete picture of the strategy;

2. the wrong performance measures; and

3. a wrong approach towards managing performance.

The world of pension administration is a good place to look for bad examples:

� Strategy: Pension administration as a core component of the overall service offering rarely, if ever, has an

articulated strategy and where it has, that is rarely linked back to the overall strategy of the company and the

trustees.

� Measurement: If there is a system of measurement (and too often administration performance is not

monitored at all) then that measurement will focus of a few key measures (in reality, the things that are

easiest to measure), such as how often target turnaround times were breached in the last three months.

� Management: the combination of the above speaks for itself. If this was not enough, the Pensions

Regulator is aware of many small pension schemes where the trustees (who are responsible for the total

governance of the scheme) – are not even aware that they are trustees!

Our experience shows that around one in three pension schemes suffers from systematic, wholesale

administration errors and omissions which have to be rectified before any work on creating a long-term and well

run administration can start. The range of common ills is staggering:

� Automatic inflation-linked increases paid at 5% per annum regardless of the actual level of inflation, year

after year after year.

� Spouses’ pension details jumbled up and linked to the wrong pension scheme member.

� Early retirement pensions calculated on an outrageously generous footing (completely disregarding the

actual basis of calculation, which was a perfectly sensible one): and this despite the fact the scheme was

virtually bankrupt – thus accidentally robbing Peter to pay Paul.

� Contributions received were unchecked, unreconciled, and unattributed: they simply sloshed around in a

bank account, rather that being invested according to members’ instructions.

� Invalid announcements forming the basis of changes to the scheme’s Rules, without following any due

process.

� Pensionable salary wrongly calculated – a big error in a DB pension scheme.

� Temporary bridging pensions paid in perpetuity.

Restoring Confidence: Measuring and Managing Performance in Pensions

Page 10 of 35

Managing administration performance strategically will help to address these issues. strategic performance

management is about creating an environment in which organisational performance becomes everyone’s

responsibility. This involves a clear understanding of the strategic direction by everyone in the organisation as

well as their accepted responsibility for continuous refinement of the strategy and its execution. In such an

environment, relevant performance indicators are collected to inform strategic decision making and

understanding at all organisational levels, and to monitor the correctness and relevance of assumptions; not

simply put into reports that no one really cares about.

SPM may therefore be defined as the organisational approach to define, assess, implement, and continuously

refine and improve strategy and performance. It encompasses methodologies, frameworks, and indicators that

help organisations to formulate their strategy and enable employees and other stakeholders to gain the insight

required to challenge strategic assumptions, refine strategic thinking, and most importantly inform strategic

decision making, learning, and improvement.

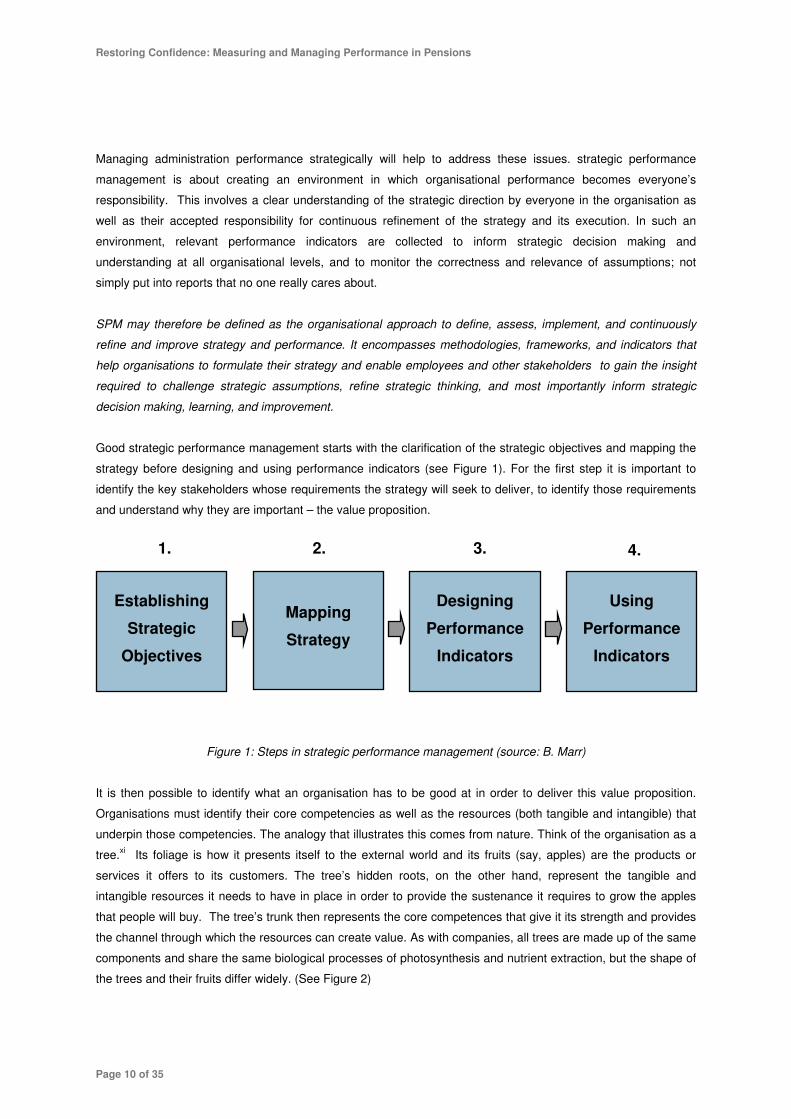

Good strategic performance management starts with the clarification of the strategic objectives and mapping the

strategy before designing and using performance indicators (see Figure 1). For the first step it is important to

identify the key stakeholders whose requirements the strategy will seek to deliver, to identify those requirements

and understand why they are important – the value proposition.

Figure 1: Steps in strategic performance management (source: B. Marr)

It is then possible to identify what an organisation has to be good at in order to deliver this value proposition.

Organisations must identify their core competencies as well as the resources (both tangible and intangible) that

underpin those competencies. The analogy that illustrates this comes from nature. Think of the organisation as a

tree.xi Its foliage is how it presents itself to the external world and its fruits (say, apples) are the products or

services it offers to its customers. The tree’s hidden roots, on the other hand, represent the tangible and

intangible resources it needs to have in place in order to provide the sustenance it requires to grow the apples

that people will buy. The tree’s trunk then represents the core competences that give it its strength and provides

the channel through which the resources can create value. As with companies, all trees are made up of the same

components and share the same biological processes of photosynthesis and nutrient extraction, but the shape of

the trees and their fruits differ widely. (See Figure 2)

Establishing

Strategic

Objectives

Mapping

Strategy

Designing

Performance

Indicators

Using

Performance

Indicators

1. 2. 4. 3.

Restoring Confidence: Measuring and Managing Performance in Pensions

Page 11 of 35

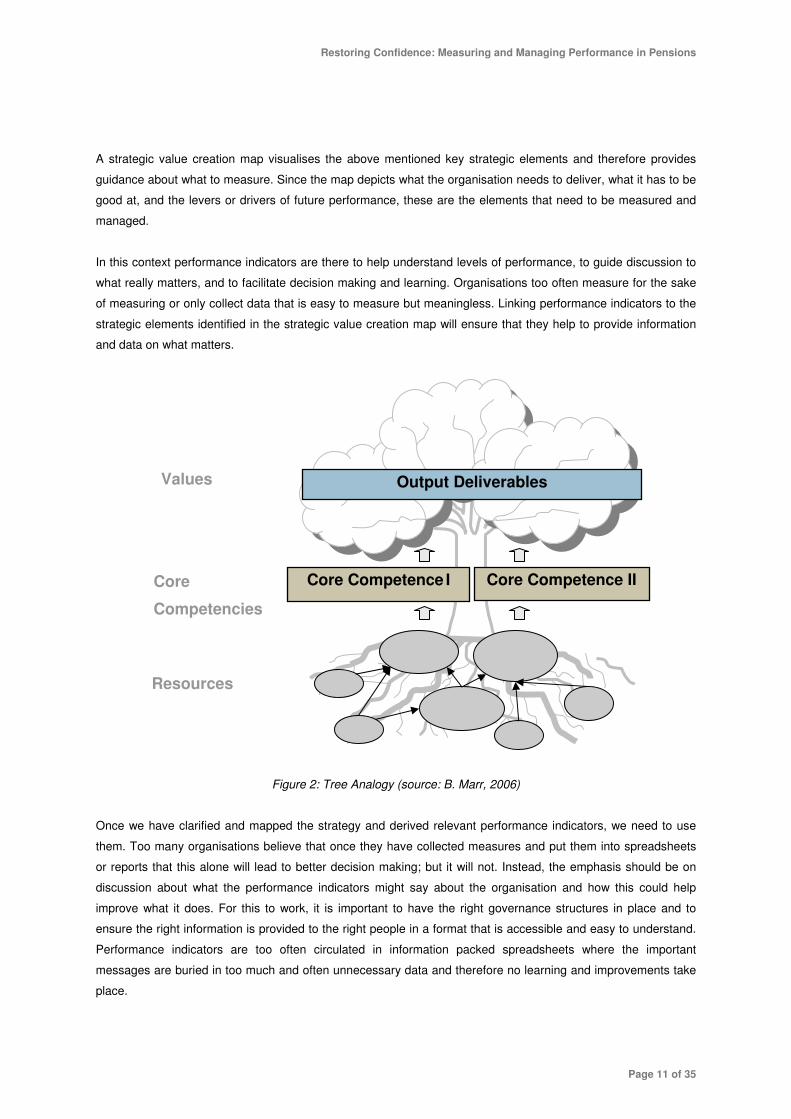

A strategic value creation map visualises the above mentioned key strategic elements and therefore provides

guidance about what to measure. Since the map depicts what the organisation needs to deliver, what it has to be

good at, and the levers or drivers of future performance, these are the elements that need to be measured and

managed.

In this context performance indicators are there to help understand levels of performance, to guide discussion to

what really matters, and to facilitate decision making and learning. Organisations too often measure for the sake

of measuring or only collect data that is easy to measure but meaningless. Linking performance indicators to the

strategic elements identified in the strategic value creation map will ensure that they help to provide information

and data on what matters.

Figure 2: Tree Analogy (source: B. Marr, 2006)

Once we have clarified and mapped the strategy and derived relevant performance indicators, we need to use

them. Too many organisations believe that once they have collected measures and put them into spreadsheets

or reports that this alone will lead to better decision making; but it will not. Instead, the emphasis should be on

discussion about what the performance indicators might say about the organisation and how this could help

improve what it does. For this to work, it is important to have the right governance structures in place and to

ensure the right information is provided to the right people in a format that is accessible and easy to understand.

Performance indicators are too often circulated in information packed spreadsheets where the important

messages are buried in too much and often unnecessary data and therefore no learning and improvements take

place.

Output Deliverables

Core Competence I Core Competence II

Resources

Core

Competencies

Values

Restoring Confidence: Measuring and Managing Performance in Pensions

Page 12 of 35

Many other transaction-focused industries, such as banking and insurance have made significant progress over

the past decade by adopting principles of strategic performance management.

The Bank of Tokyo-Mitsubishi (BTM), one of the world’s largest banks which manages more than $608 billion in

assets across more than 700 locations in Japan and throughout the world, has illustrated how strategic

performance management can be implemented.xii

Leaders at BTMHQA, who direct its Americas operations from

the bank’s New York offices, realised that it is critical for everyone in their organisation to understand the

strategic direction of the firm. In their strategy map, the bank identified their overall goal as maximising net

income after credit costs. This is achieved by increasing fee income, maximising income from core customers,

minimising credit costs, and enhancing cost efficiency. Their customer value proposition is to be recognised as

the best foreign bank operating in the Americas by providing reliable lending capabilities, an extensive global

network, and service quality that meets high standards for accuracy and speed. The core internal processes that

need to be in place are abilities to manage risks, grow revenues, and enhance productivity. BTMHQA identified

people in the business as the key driver of performance, and therefore set strategic objectives for succession

planning, training and work environment, among others. After implementing the strategic performance

management approach people became more strategic in their thinking. The strategy map facilitated strategic

discussions and ensured that the right performance indicators were used to manage what matters.

Another case study is provided by the TT Club, a leading provider of insurance and related risk management

services for the international transport and logistics industry.xiii

The company has its global headquarters in the

City of London, but has 20 office locations around the world. Customers range from the world’s largest shipping

lines, busiest ports, global freight forwarders and cargo handling terminals, to smaller companies operating in

niche markets. The project to implement the principles of strategic performance management was driven by their

desire to clarify their strategic objectives and value drivers and to regain an ‘A’ rating for financial strengths,

which the company lost a few years ago. The TT Club decided that its value proposition was to provide

sustainable financial security for the global transport industry by offering excellent and customised insurance

covers and value added services that people trust. It identified three key competencies:

� The claims handling and delivery of services such as risk assessments and advice.

� The deep understanding of the industry and changing client demands and underwriting requirements.

� The ability to build and maintain close relationships with the industry which gives the TT Club the status of an

independent body of the industry.

The value drivers underpinning these include, among others their processes and systems, its reputation and

recognition as a specialist and member of the transport industry, relationships with the transport industry as well

as with reinsurers and brokers, and its ability to recruit, train, develop, and retain good people. At the centre of

the strategy is its capital strength and access to reinsurance. The clear strategic focus, the design of meaningful

indicators, and the continuous constructive review of these, have all helped the TT Club to regain its ‘A’ rating

and to become a strategy focused organisation.

Restoring Confidence: Measuring and Managing Performance in Pensions

Page 13 of 35

Another example comes from a direct banking operation (Banking 365) of the Bank of Ireland’s retail division,

who adopted strategic performance management at its inception.xiv

The strategic vision was graphically mapped

in order to link vision, strategic themes, strategic objectives and operational measures through cause-and-effect

relationships. This allowed them to identify business processes, people, technology and IT systems as key

drivers of future performance, with three strategic themes (sales, operational efficiency, and service). Indicators

were then developed for each of these drivers and regularly reviewed in weekly performance meetings. Here, a

great emphasis was placed on benchmarking their own indicator data in order to identify current performance

levels and future performance targets. This systematic approach has led not only to impressive sales growth but

also significantly improved processes through automated services, high customer satisfaction, and 81%

employee satisfaction, which is a world-class benchmark, considering that the primary delivery channel is through

their call centre operation.

Pension administration clearly has some catching up to do…

Restoring Confidence: Measuring and Managing Performance in Pensions

Page 14 of 35

Priorities (Minimising Risk, Maximising Value) and How They Influence the Process

During this research, we found that when it comes to the overall strategic direction and value proposition of

pension administration companies, they seem to fall somewhere between Minimising Costs and Risks and

Maximising HR Value (see figure 3).

For open schemes (the dwindling number of DB schemes and the growing number of DC schemes that are open

to new members), emphasis may be placed on maximising the scheme’s effectiveness within the overall HR

strategy. This may translate in practice to excellent communication tools and channels, a high degree of focus

on customer satisfaction, a willingness to engage in educational programmes, seminars and to offer guidance

where appropriate. The delivery team may be organised in such a way that the vast majority of enquiries could

be dealt with all the way through by most people in the team. Whoever a member initially contacted will usually

be able to answer or resolve the question. Service standards have to be excellent, as a poor experience in terms

of the administration function can quickly diminish employee appreciation of the value of the benefit being

offered.

For closed schemes (where no new members are accepted), the emphasis may be reducing the cost impact of

the legacy left by the old pension scheme. This may lead to a highly transactional and standarised approach,

with little more than the minimum requirements of compliance with regulation being offered to members. In this

case the delivery team may be organised along functional lines, so that certain types of processes (death claims,

retirements etc) are dealt with by the relevant specialist. Indeed, such an emphasis can also be found in

schemes (both DB and DC) that are still open to new members and are therefore being actively used in the

recruitment process.

Figure 3: Pension Administration Value Proposition

Pension Administration

Minimising Cost and Risks Maximising HR Value

� Transactional approach

� Functional specialisation

� Automation

� Tight checks and reconciliation

� Educate and communicate

� Multi-disciplinary teams

� Automation

� Tight checks and reconciliation

Restoring Confidence: Measuring and Managing Performance in Pensions

Page 15 of 35

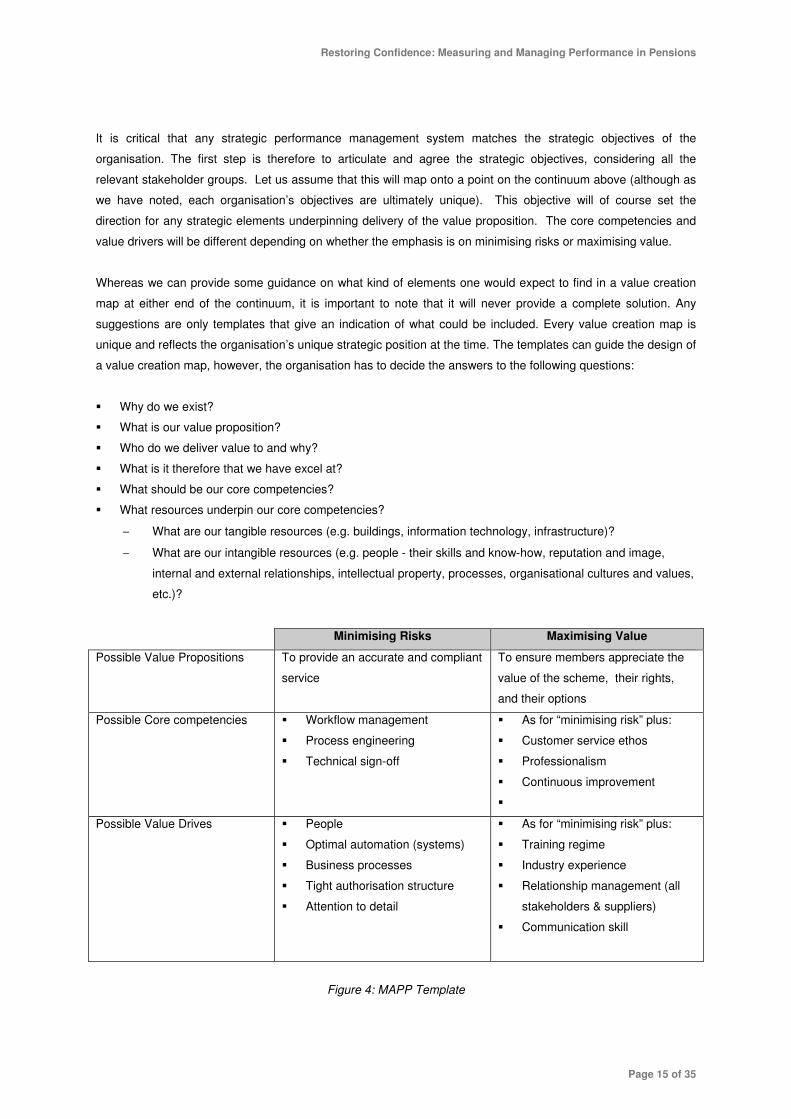

It is critical that any strategic performance management system matches the strategic objectives of the

organisation. The first step is therefore to articulate and agree the strategic objectives, considering all the

relevant stakeholder groups. Let us assume that this will map onto a point on the continuum above (although as

we have noted, each organisation’s objectives are ultimately unique). This objective will of course set the

direction for any strategic elements underpinning delivery of the value proposition. The core competencies and

value drivers will be different depending on whether the emphasis is on minimising risks or maximising value.

Whereas we can provide some guidance on what kind of elements one would expect to find in a value creation

map at either end of the continuum, it is important to note that it will never provide a complete solution. Any

suggestions are only templates that give an indication of what could be included. Every value creation map is

unique and reflects the organisation’s unique strategic position at the time. The templates can guide the design of

a value creation map, however, the organisation has to decide the answers to the following questions:

� Why do we exist?

� What is our value proposition?

� Who do we deliver value to and why?

� What is it therefore that we have excel at?

� What should be our core competencies?

� What resources underpin our core competencies?

− What are our tangible resources (e.g. buildings, information technology, infrastructure)?

− What are our intangible resources (e.g. people - their skills and know-how, reputation and image,

internal and external relationships, intellectual property, processes, organisational cultures and values,

etc.)?

Minimising Risks Maximising Value

Possible Value Propositions To provide an accurate and compliant

service

To ensure members appreciate the

value of the scheme, their rights,

and their options

Possible Core competencies � Workflow management

� Process engineering

� Technical sign-off

� As for “minimising risk” plus:

� Customer service ethos

� Professionalism

� Continuous improvement

�

Possible Value Drives � People

� Optimal automation (systems)

� Business processes

� Tight authorisation structure

� Attention to detail

� As for “minimising risk” plus:

� Training regime

� Industry experience

� Relationship management (all

stakeholders & suppliers)

� Communication skill

Figure 4: MAPP Template

Restoring Confidence: Measuring and Managing Performance in Pensions

Page 16 of 35

Developing a Matrix for Administrative Performance in Pensions: A Case Study The BP Pension Fund

Below we will outline how the BP Pension Fund put strategic pension administration into practice. Recognised as

one of the leading pension providers, the BP Pension Fund wanted to improve the way it measured and

managed its pension administration. As outlined in the introduction, the BP Pension Fund has been instrumental

in this research as it provided the focus and the initial funding.

The BP Pension Fund is one of the largest and best funded pension schemes in the UK. Its assets at the time of

the last report and accounts exceeded £12bn. It currently provides pensions to 38,428 people, and a further

30,901 people who have not yet retired will depend on it in whole or in part for security in their old age. It is

looked after by a trustee, which in this case is in fact a trustee company, BP Pension Trustees Ltd.

Introduction to the project

In August 2005, Higham Dunnett Shaw, working in conjunction with Bernard Marr of the Centre for Business

Performance at Cranfield School of Management, was appointed by BP Pension Trustees Ltd to lead a project to

recommend a strong governance framework specifically in relation to the pension administration function. Dr

Reg Hinkley, the Chief Executive Officer of the trustee company, wanted to start measuring and managing what

really mattered. He saw a clear need for evidence that the administration team was achieving the desired level of

service, in order to deliver a state of the art administration service for the Fund’s members, in line with the

strategic vision. Dr Hinkley acknowledged that without an explicit strategic direction and appropriate performance

indicators in place strong governance would be mere wishful thinking.

Dr Hinkley and his fellow directors of the trustee company were determined that their governance structure and

mechanisms should be second to none. BP plc, one of the most prestigious and recognisable brands in the

world, had spent considerable effort ensuring that governance in relation to the worldwide affairs of the company

was both rigorous and comprehensive. The Board of the trustee company had adopted a parallel framework.

The commission was to work within this overarching governance framework to:

1. establish objectives for the Fund, based on interviews with representatives of the relevant stakeholders –

the trustee company on behalf of the scheme members, the Company and the Administration Team – and a

strategy to achieve those objectives.

2. examine the available resources and recommend a set of performance indicators that could be used in the

first instance by the pension manager in the daily business of running the team, and secondly by Dr Hinkley

and the trustee company in obtaining reassurance and advance warning of any issues that may be likely to

arise.

Restoring Confidence: Measuring and Managing Performance in Pensions

Page 17 of 35

3. set out a reporting and control framework within which the above performance management, including a

review and change control structure, could operate

4. in parallel, establish a risk management framework in relation to the administration function, again with

monitoring and reporting lines to the trustee company .

Establishing Strategic Objectives

Based on interviews with trustees, company representatives and key people within the pension administration

function a revised statement of strategic objectives was drawn up. The views of the stakeholders were broadly

aligned but differently nuanced. The revised statement was therefore subject to iteration and development before

it was finalised in a workshop prior to ultimate sign-off by the directors of the trustee company. In essence, the

BP Pension Fund positioned itself on the far right of the Pension Administration Value Proposition continuum

outlined above. Its strategic value proposition is…

‘to deliver a professional, personal and progressive pension administration service for our members.’

Mapping Strategy

The next step was then to identify and map the underpinning core competencies and value drivers. This was

done in a facilitated brainstorming session with the core project team.

Mapping Strategy

Designing

Performance

Indicators

Using Performance

Indicators

1. 2. 4. 3.

Establishing Strategic

Objectives

Establishing

Strategic

Objectives

Mapping Strategy

Designing

Performance

Indicators

Using Performance

Indicators

1. 2. 4. 3.

Restoring Confidence: Measuring and Managing Performance in Pensions

Page 18 of 35

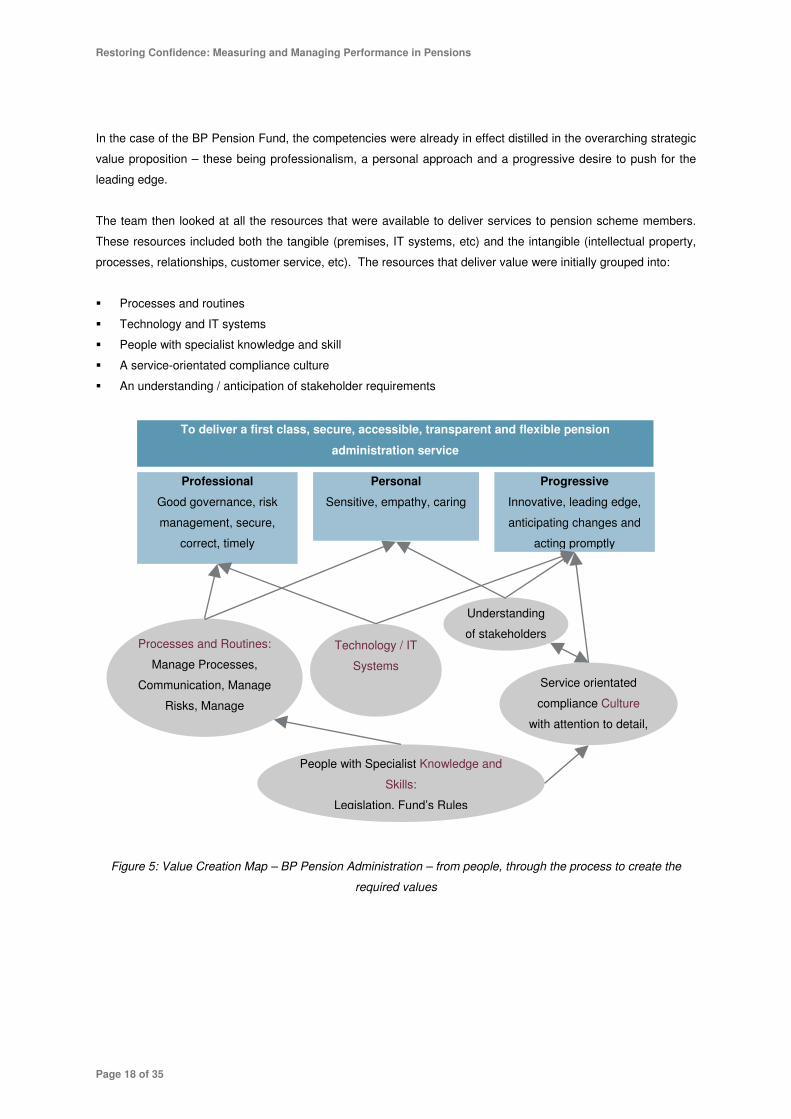

In the case of the BP Pension Fund, the competencies were already in effect distilled in the overarching strategic

value proposition – these being professionalism, a personal approach and a progressive desire to push for the

leading edge.

The team then looked at all the resources that were available to deliver services to pension scheme members.

These resources included both the tangible (premises, IT systems, etc) and the intangible (intellectual property,

processes, relationships, customer service, etc). The resources that deliver value were initially grouped into:

� Processes and routines

� Technology and IT systems

� People with specialist knowledge and skill

� A service-orientated compliance culture

� An understanding / anticipation of stakeholder requirements

Figure 5: Value Creation Map – BP Pension Administration – from people, through the process to create the

required values

People with Specialist Knowledge and

Skills:

Legislation, Fund’s Rules

Processes and Routines:

Manage Processes,

Communication, Manage

Risks, Manage

Technology / IT

Systems

To deliver a first class, secure, accessible, transparent and flexible pension

administration service

Professional

Good governance, risk

management, secure,

correct, timely

Service orientated

compliance Culture

with attention to detail,

Understanding

of stakeholders

Progressive

Innovative, leading edge,

anticipating changes and

acting promptly

Personal

Sensitive, empathy, caring

Restoring Confidence: Measuring and Managing Performance in Pensions

Page 19 of 35

Designing Performance Indicators

Having arrived at a working version of a value creation map (above), the team next drilled down to a task level.

We looked at the hundreds of different tasks that are performed in delivering services, and related the above

resources back to the tasks.

This enabled us to start to draw out a comprehensive definition of how a resource such as a ‘service orientated

compliance culture’ relates to the various tasks required to deliver the service in accordance with the overall

strategy and so start to arrive at a list of indicators. This overall list was then distilled and grouped into a set of

key indicators for the pension manager and the trustee company.

The performance indicators included traditional lagging measures such as ‘number of retirement calculations

performance within the required turnaround time’.

However, crucially, they also included leading indicators of performance. These give the pension manager /

trustee company advance warning that there may be an issue that requires attention.

For example, as few pension schemes are 100% automated, manual calculations are always required. Where

there are manual calculations, there is a possibility of error, and checks must be in place to catch these. Where

the initial calculation is incorrect, time will be spent on rectification. Rectification rates should be stable or

diminishing: if they escalate this could indicate a number of things:

� Inadequate training

� Lack of motivation

� Pressure due to inadequate staffing levels

� Inaccurate data in which the calculations are made

� Lack of clear process / checklists to follow

Taken together, the full set of leading and lagging indicators enable BP’s pension manager, working with Dr

Hinkley and the directors of the trustee company, to monitor performance, identify potential issues to be

addressed, and act upon the information in order to continuously improve performance.

Establishing Strategic

Objectives

Mapping Strategy

Designing

Performance

Indicators

Using Performance

Indicators

1. 2. 4. 3.

Restoring Confidence: Measuring and Managing Performance in Pensions

Page 20 of 35

In our experience of working with all manner of clients, including external, third party administrators, in-house

teams and insurance companies, we believe that the system we have developed in conjunction with BP Pension

Trustees Ltd puts Dr Hinkley and his team firmly at the forefront of thinking in relation to governance and strategic

performance management.

We have given some examples of performance indicators in Appendix 1

Using Performance Indicators

New performance indicators must be implemented with care, particularly if they are linked to incentives. It is

critical that indicators are used in an honest and objective manner in order to identify shortcomings and improve

performance. If indicators are used within a command-and-control environment and a blame culture it will often

drive dysfunctional behaviour.

Mike Bourne of the Centre for Business Performance at Cranfield School of Management recalls the following

example to illustrate over-dependence on performance measurements leading to dysfunctional behaviour. xv

“An airline believed that the speed at which passengers received their baggage at the end of the flight was almost

as important as the flight itself when considering customer satisfaction. With this in mind, the company decided

to improve baggage delivery performance by introducing a new performance measure, which measured the time

taken for the first bag to be loaded onto the conveyor belt.

“A few days after the measure was implemented, a flight arrived and the baggage was loaded onto a tractor as

usual. Whilst the rest of the team stood around chatting waiting for the tractor to arrive, the team leader jumped

up, ran to the tractor, grabbed the smallest bag and sprinted back to the conveyor belt. The first bag was on the

conveyor belt and the measure had been met. The rest of the bags trundled along on the tractor and were put

onto the conveyor at the previous pace.”

Bearing this salutary lesson in mind, a period of bedding down is necessary. During this time, measures can be

implemented and monitored, to see what effect the very act of measurement may have.

The project team recommended a set of around twenty key indicators in addition to the traditional, retrospective

service level agreement (SLA) measures that are typically in place between the trustees and their administrator.

Establishing Strategic

Objectives

Mapping Strategy

Designing

Performance

Indicators

Using Performance

Indicators

1. 2. 4. 3.

Restoring Confidence: Measuring and Managing Performance in Pensions

Page 21 of 35

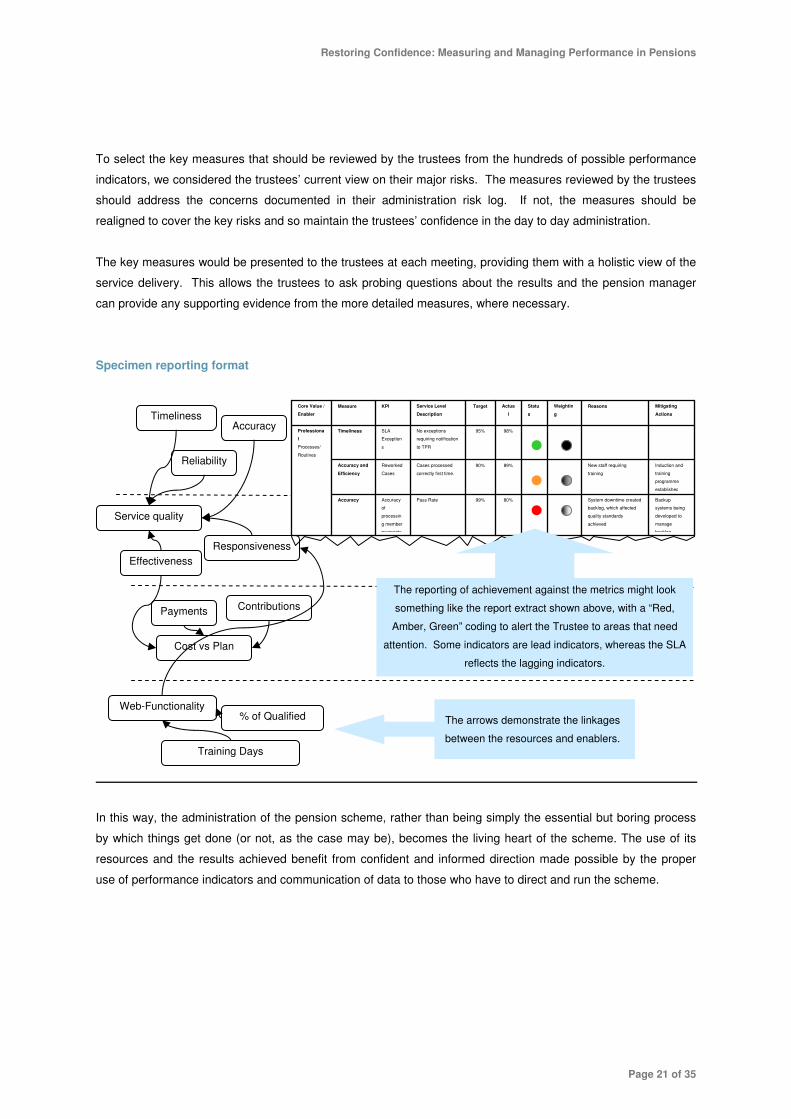

To select the key measures that should be reviewed by the trustees from the hundreds of possible performance

indicators, we considered the trustees’ current view on their major risks. The measures reviewed by the trustees

should address the concerns documented in their administration risk log. If not, the measures should be

realigned to cover the key risks and so maintain the trustees’ confidence in the day to day administration.

The key measures would be presented to the trustees at each meeting, providing them with a holistic view of the

service delivery. This allows the trustees to ask probing questions about the results and the pension manager

can provide any supporting evidence from the more detailed measures, where necessary.

Specimen reporting format

In this way, the administration of the pension scheme, rather than being simply the essential but boring process

by which things get done (or not, as the case may be), becomes the living heart of the scheme. The use of its

resources and the results achieved benefit from confident and informed direction made possible by the proper

use of performance indicators and communication of data to those who have to direct and run the scheme.

Timeliness Accuracy

Reliability

Service quality

Effectiveness

Responsiveness

Payments Contributions

Cost vs Plan

Web-Functionality % of Qualified

Training Days

Weightin

g

Backup

systems being

developed to

manage

backlog

Induction and

training

programme

established

Mitigating

Actions

System downtime created

backlog, which affected

quality standards

achieved

New staff requiring

training

Reasons

Statu

s

80% 99% Pass Rate Accuracy

of

processin

g member

payments

Accuracy

89% 90% Cases processed

correctly first time.

Reworked

Cases

Accuracy and

Efficiency

98% 95% No exceptions

requiring notification

to TPR

SLA

Exception

s

Timeliness Professiona

l

Processes/

Routines

Actua

l

Target Service Level

Description

KPI Measure Core Value /

Enabler

The arrows demonstrate the linkages

between the resources and enablers.

The reporting of achievement against the metrics might look

something like the report extract shown above, with a “Red,

Amber, Green” coding to alert the Trustee to areas that need

attention. Some indicators are lead indicators, whereas the SLA

reflects the lagging indicators.

Restoring Confidence: Measuring and Managing Performance in Pensions

Page 22 of 35

Summary and Conclusion

A pension scheme depends vitally on the strength of its funding, the returns on investments and the quality of its

administration. It is the last of these that enables people to understand their position in relation to the scheme –

what it means for them, what the risk and rewards may be, what choices they can make. The fact that trust has

substantially been lost is partly due to the poor quality of administration. The cause of this can be traced back to

poor systems of governance – an issue that is now firmly on the Pension Regulator’s agenda.

A strong governance system will follow explicit, agreed processes and principles to control, manage and organise

available resources to an agreed strategic end.

It follows therefore, that pension schemes require a clearly articulated and agreed goal. Once this has been

agreed – by all the parties with an interest in the scheme – then around this it is possible to create a directed and

rational system of controls in order to martial the available and finite resources that are available to deliver that

objective.

Companies have for many years used Strategic Performance Measurement (SMP) to exactly this end. We have

adapted that thinking for the pension industry and have created a MAPP – a matrix for administration

performance in pensions:

Restoring Confidence: Measuring and Managing Performance in Pensions

Page 23 of 35

It is a fact that confidence in the pensions framework has been severely dented. It is also a fact that service

standards within the industry lag behind other financial products. It is no coincidence that other industries have

embraced strategic performance management to help them clarify their thinking and to implement improvements.

The renewed focus of the Pensions Regulator on governance is to be welcomed. The MAPP framework,

embraced by forward thinking trustees such as the BP Pension Fund, provides a way forward for trustees and

employers to understand and deliver the most appropriate service for their members given the real constraints of

budget and resource.

Establishing Strategic

Objectives

Mapping Strategy

Designing Performance

Indicators

Using Performance

Indicators

1. 2. 4.3.

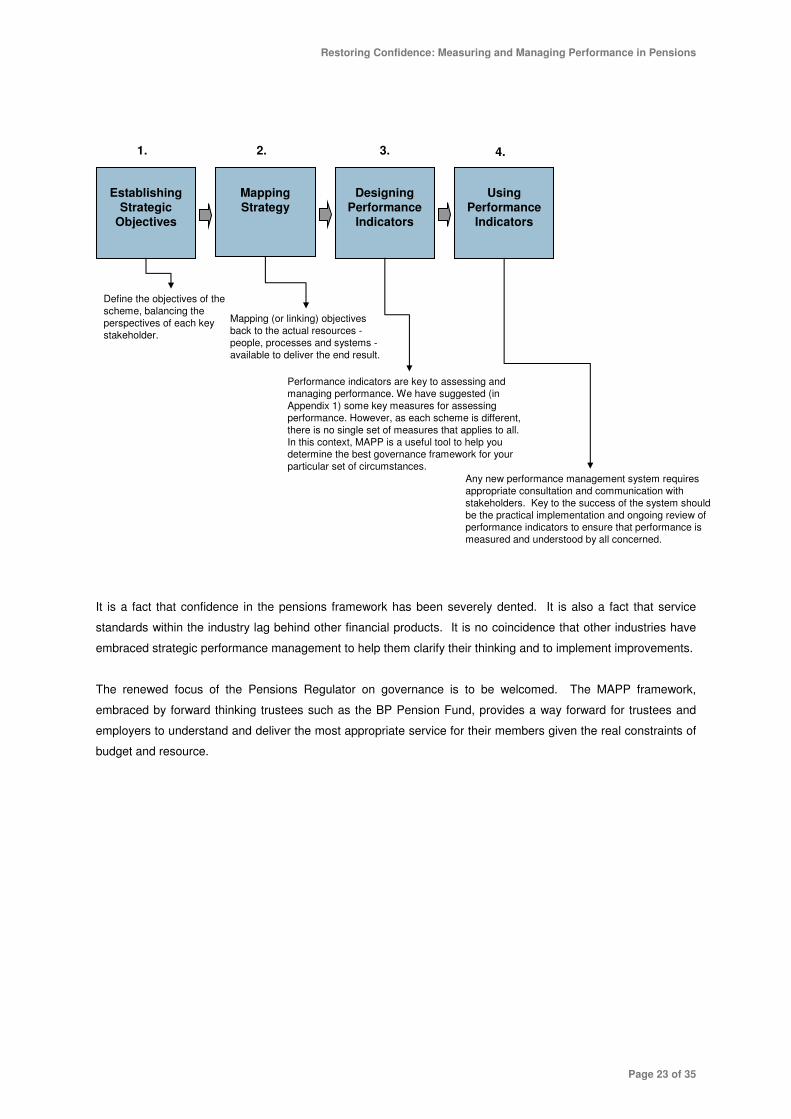

Define the objectives of the scheme, balancing the perspectives of each key stakeholder.

Mapping (or linking) objectives back to the actual resources -people, processes and systems -available to deliver the end result.

Performance indicators are key to assessing and managing performance. We have suggested (in Appendix 1) some key measures for assessing performance. However, as each scheme is different, there is no single set of measures that applies to all. In this context, MAPP is a useful tool to help you determine the best governance framework for your particular set of circumstances.

Any new performance management system requires appropriate consultation and communication with stakeholders. Key to the success of the system should be the practical implementation and ongoing review of performance indicators to ensure that performance is measured and understood by all concerned.

Restoring Confidence: Measuring and Managing Performance in Pensions

Page 24 of 35

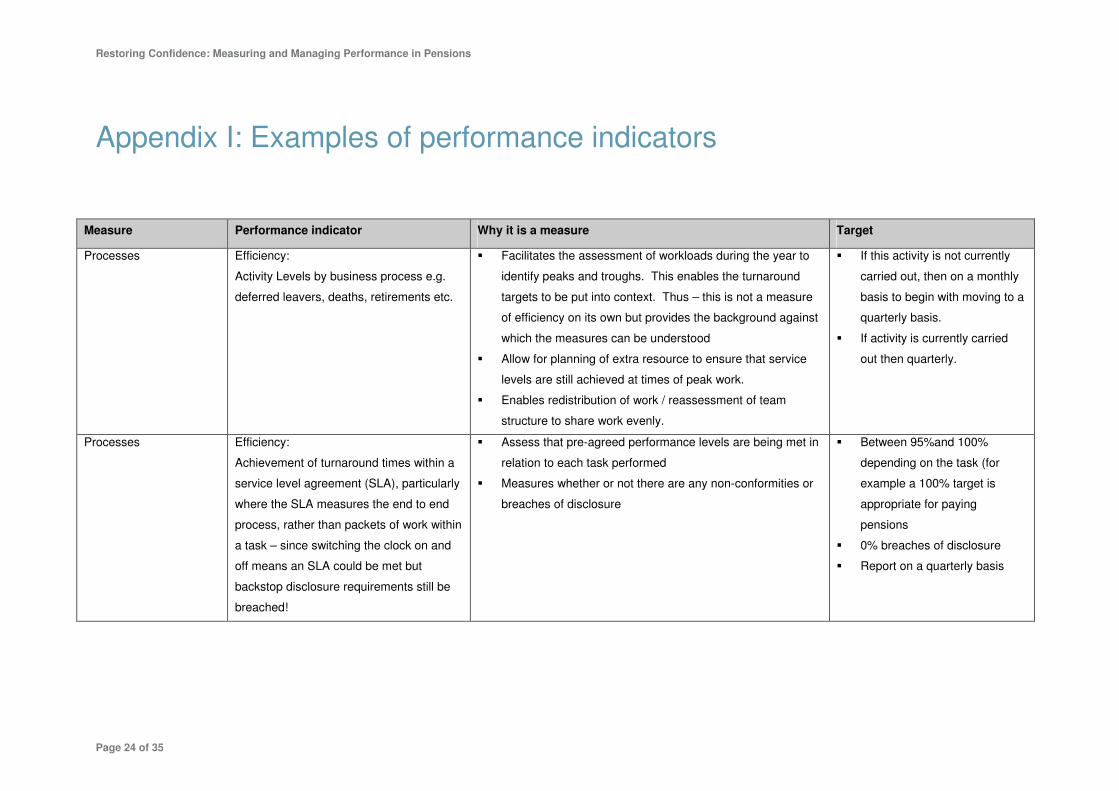

Appendix I: Examples of performance indicators

Measure Performance indicator Why it is a measure Target

Processes Efficiency:

Activity Levels by business process e.g.

deferred leavers, deaths, retirements etc.

� Facilitates the assessment of workloads during the year to

identify peaks and troughs. This enables the turnaround

targets to be put into context. Thus – this is not a measure

of efficiency on its own but provides the background against

which the measures can be understood

� Allow for planning of extra resource to ensure that service

levels are still achieved at times of peak work.

� Enables redistribution of work / reassessment of team

structure to share work evenly.

� If this activity is not currently

carried out, then on a monthly

basis to begin with moving to a

quarterly basis.

� If activity is currently carried

out then quarterly.

Processes Efficiency:

Achievement of turnaround times within a

service level agreement (SLA), particularly

where the SLA measures the end to end

process, rather than packets of work within

a task – since switching the clock on and

off means an SLA could be met but

backstop disclosure requirements still be

breached!

� Assess that pre-agreed performance levels are being met in

relation to each task performed

� Measures whether or not there are any non-conformities or

breaches of disclosure

� Between 95%and 100%

depending on the task (for

example a 100% target is

appropriate for paying

pensions

� 0% breaches of disclosure

� Report on a quarterly basis

Restoring Confidence: Measuring and Managing Performance in Pensions

Page 25 of 35

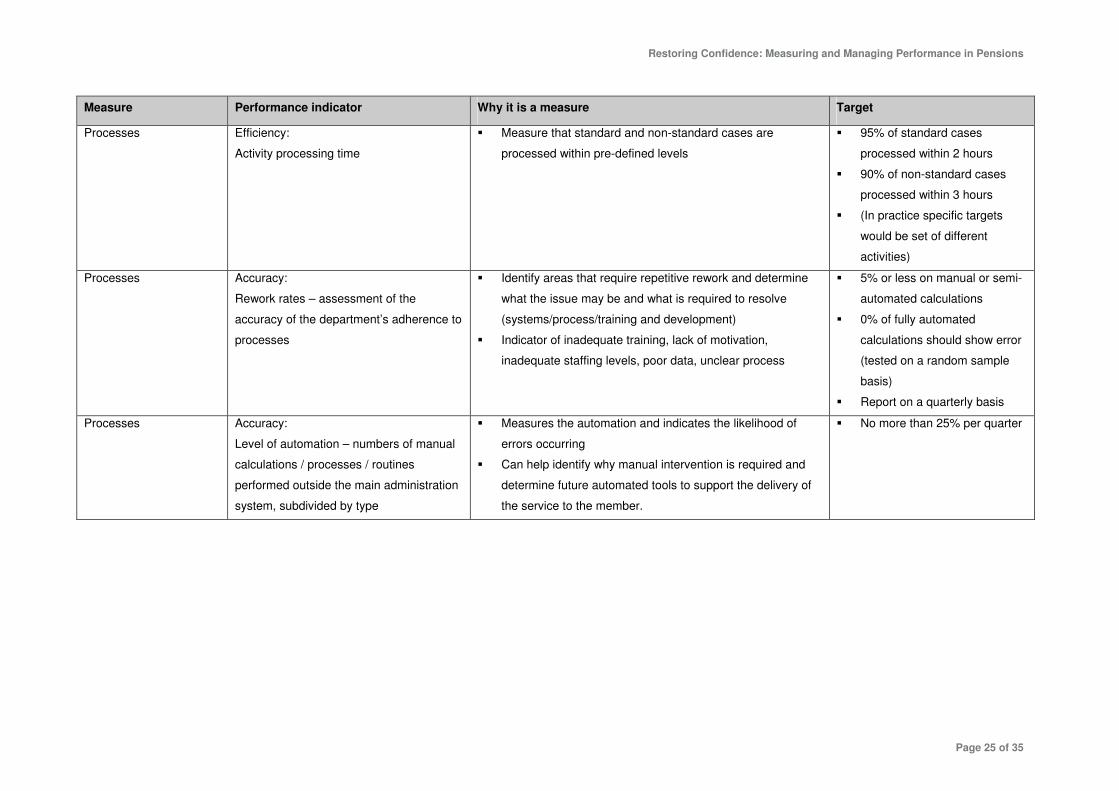

Measure Performance indicator Why it is a measure Target

Processes Efficiency:

Activity processing time

� Measure that standard and non-standard cases are

processed within pre-defined levels

� 95% of standard cases

processed within 2 hours

� 90% of non-standard cases

processed within 3 hours

� (In practice specific targets

would be set of different

activities)

Processes Accuracy:

Rework rates – assessment of the

accuracy of the department’s adherence to

processes

� Identify areas that require repetitive rework and determine

what the issue may be and what is required to resolve

(systems/process/training and development)

� Indicator of inadequate training, lack of motivation,

inadequate staffing levels, poor data, unclear process

� 5% or less on manual or semi-

automated calculations

� 0% of fully automated

calculations should show error

(tested on a random sample

basis)

� Report on a quarterly basis

Processes Accuracy:

Level of automation – numbers of manual

calculations / processes / routines

performed outside the main administration

system, subdivided by type

� Measures the automation and indicates the likelihood of

errors occurring

� Can help identify why manual intervention is required and

determine future automated tools to support the delivery of

the service to the member.

� No more than 25% per quarter

Restoring Confidence: Measuring and Managing Performance in Pensions

Page 26 of 35

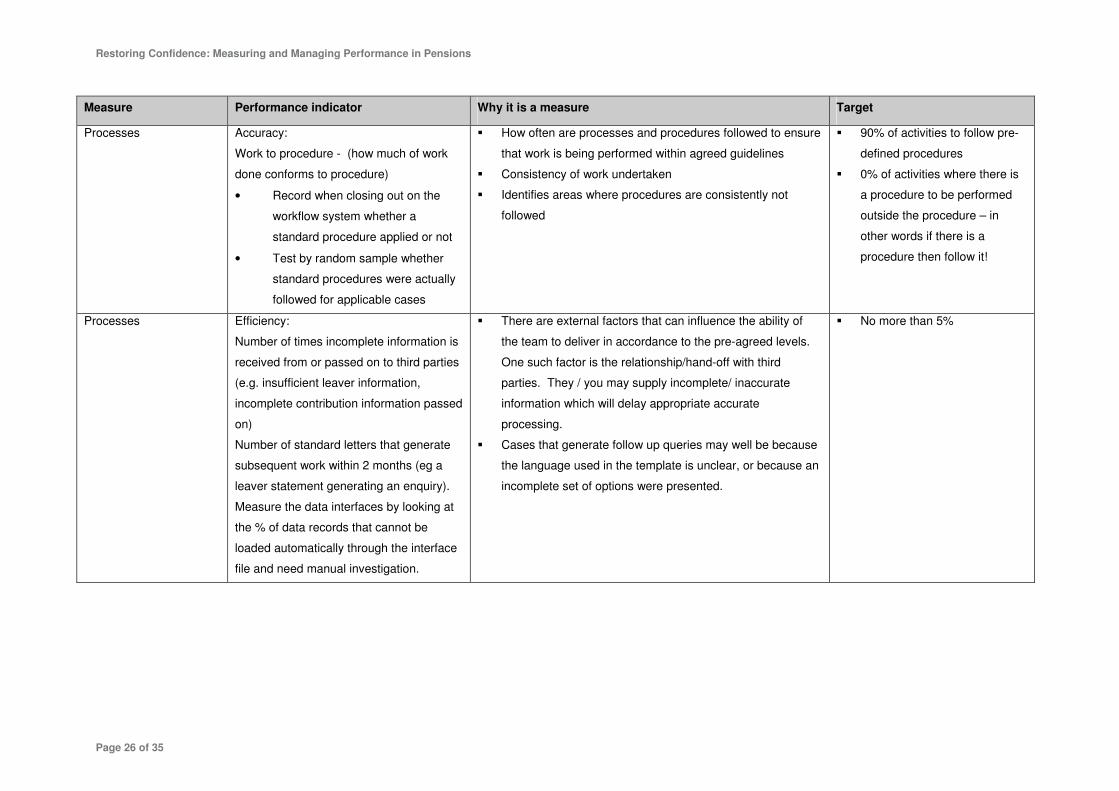

Measure Performance indicator Why it is a measure Target

Processes Accuracy:

Work to procedure - (how much of work

done conforms to procedure)

• Record when closing out on the

workflow system whether a

standard procedure applied or not

• Test by random sample whether

standard procedures were actually

followed for applicable cases

� How often are processes and procedures followed to ensure

that work is being performed within agreed guidelines

� Consistency of work undertaken

� Identifies areas where procedures are consistently not

followed

� 90% of activities to follow pre-

defined procedures

� 0% of activities where there is

a procedure to be performed

outside the procedure – in

other words if there is a

procedure then follow it!

Processes Efficiency:

Number of times incomplete information is

received from or passed on to third parties

(e.g. insufficient leaver information,

incomplete contribution information passed

on)

Number of standard letters that generate

subsequent work within 2 months (eg a

leaver statement generating an enquiry).

Measure the data interfaces by looking at

the % of data records that cannot be

loaded automatically through the interface

file and need manual investigation.

� There are external factors that can influence the ability of

the team to deliver in accordance to the pre-agreed levels.

One such factor is the relationship/hand-off with third

parties. They / you may supply incomplete/ inaccurate

information which will delay appropriate accurate

processing.

� Cases that generate follow up queries may well be because

the language used in the template is unclear, or because an

incomplete set of options were presented.

� No more than 5%

Restoring Confidence: Measuring and Managing Performance in Pensions

Page 27 of 35

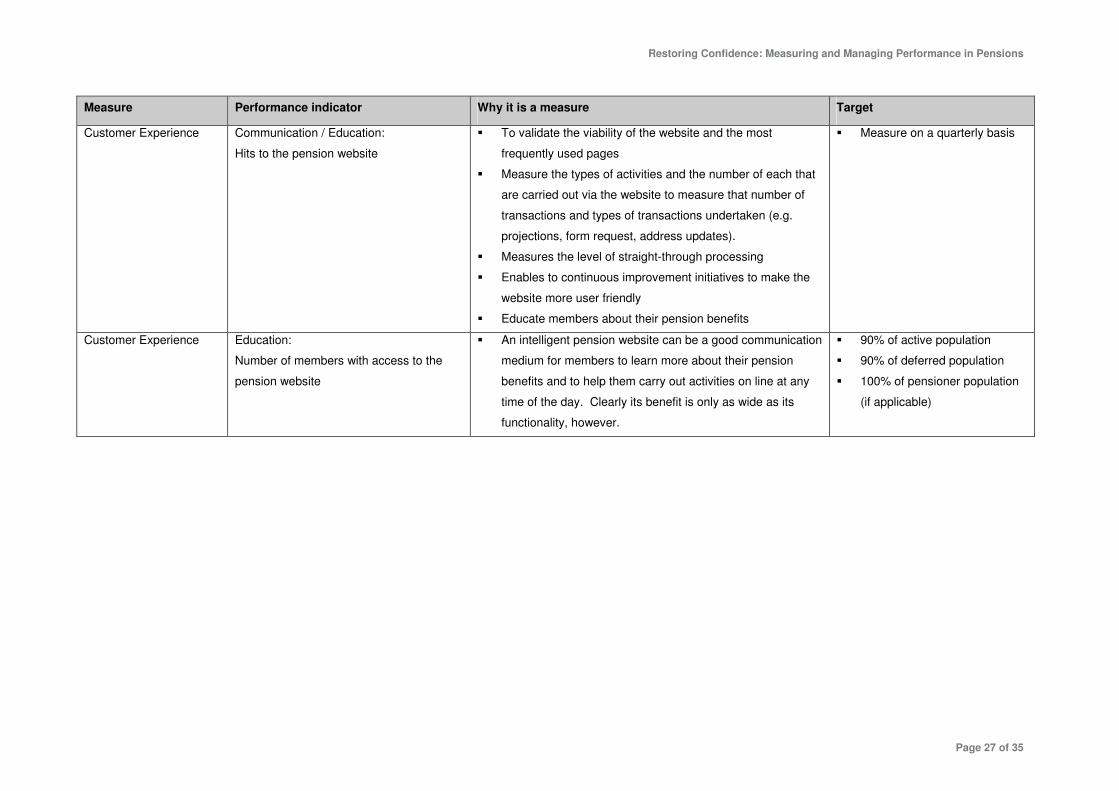

Measure Performance indicator Why it is a measure Target

Customer Experience Communication / Education:

Hits to the pension website

� To validate the viability of the website and the most

frequently used pages

� Measure the types of activities and the number of each that

are carried out via the website to measure that number of

transactions and types of transactions undertaken (e.g.

projections, form request, address updates).

� Measures the level of straight-through processing

� Enables to continuous improvement initiatives to make the

website more user friendly

� Educate members about their pension benefits

� Measure on a quarterly basis

Customer Experience Education:

Number of members with access to the

pension website

� An intelligent pension website can be a good communication

medium for members to learn more about their pension

benefits and to help them carry out activities on line at any

time of the day. Clearly its benefit is only as wide as its

functionality, however.

� 90% of active population

� 90% of deferred population

� 100% of pensioner population

(if applicable)

Restoring Confidence: Measuring and Managing Performance in Pensions

Page 28 of 35

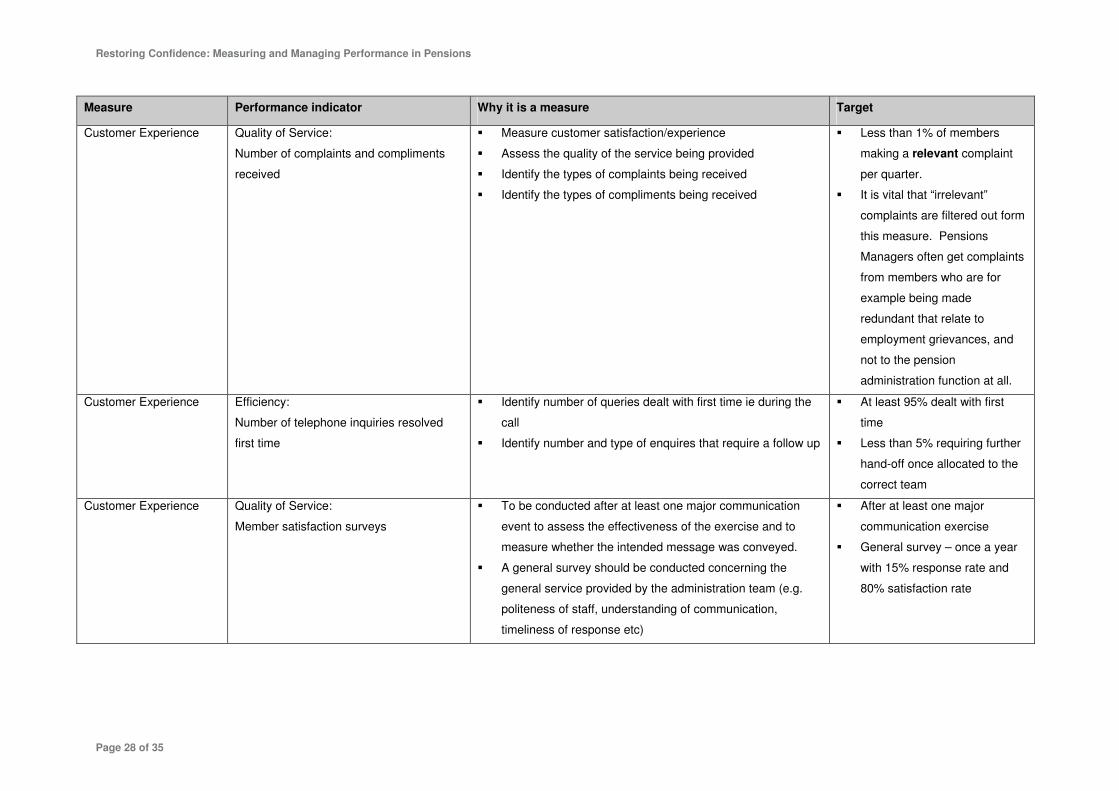

Measure Performance indicator Why it is a measure Target

Customer Experience Quality of Service:

Number of complaints and compliments

received

� Measure customer satisfaction/experience

� Assess the quality of the service being provided

� Identify the types of complaints being received

� Identify the types of compliments being received

� Less than 1% of members

making a relevant complaint

per quarter.

� It is vital that “irrelevant”

complaints are filtered out form

this measure. Pensions

Managers often get complaints

from members who are for

example being made

redundant that relate to

employment grievances, and

not to the pension

administration function at all.

Customer Experience Efficiency:

Number of telephone inquiries resolved

first time

� Identify number of queries dealt with first time ie during the

call

� Identify number and type of enquires that require a follow up

� At least 95% dealt with first

time

� Less than 5% requiring further

hand-off once allocated to the

correct team

Customer Experience Quality of Service:

Member satisfaction surveys

� To be conducted after at least one major communication

event to assess the effectiveness of the exercise and to

measure whether the intended message was conveyed.

� A general survey should be conducted concerning the

general service provided by the administration team (e.g.

politeness of staff, understanding of communication,

timeliness of response etc)

� After at least one major

communication exercise

� General survey – once a year

with 15% response rate and

80% satisfaction rate

Restoring Confidence: Measuring and Managing Performance in Pensions

Page 29 of 35

Measure Performance indicator Why it is a measure Target

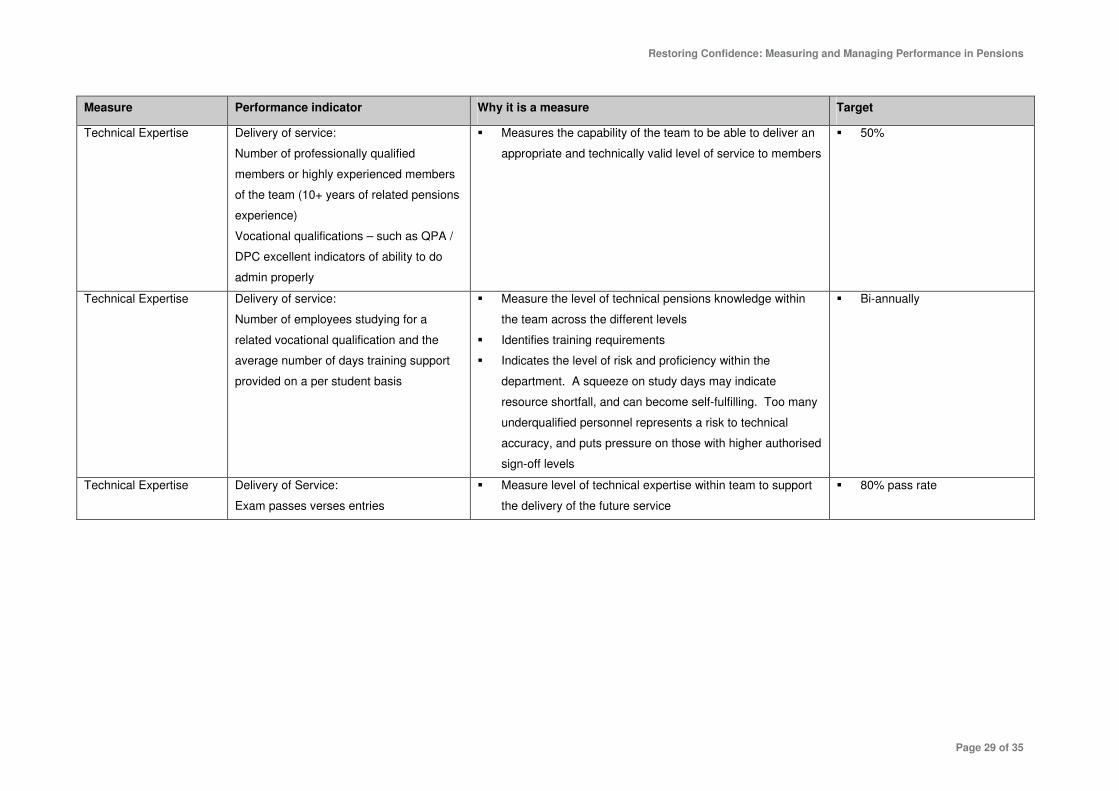

Technical Expertise Delivery of service:

Number of professionally qualified

members or highly experienced members

of the team (10+ years of related pensions

experience)

Vocational qualifications – such as QPA /

DPC excellent indicators of ability to do

admin properly

� Measures the capability of the team to be able to deliver an

appropriate and technically valid level of service to members

� 50%

Technical Expertise Delivery of service:

Number of employees studying for a

related vocational qualification and the

average number of days training support

provided on a per student basis

� Measure the level of technical pensions knowledge within

the team across the different levels

� Identifies training requirements

� Indicates the level of risk and proficiency within the

department. A squeeze on study days may indicate

resource shortfall, and can become self-fulfilling. Too many

underqualified personnel represents a risk to technical

accuracy, and puts pressure on those with higher authorised

sign-off levels

� Bi-annually

Technical Expertise Delivery of Service:

Exam passes verses entries

� Measure level of technical expertise within team to support

the delivery of the future service

� 80% pass rate

Restoring Confidence: Measuring and Managing Performance in Pensions

Page 30 of 35

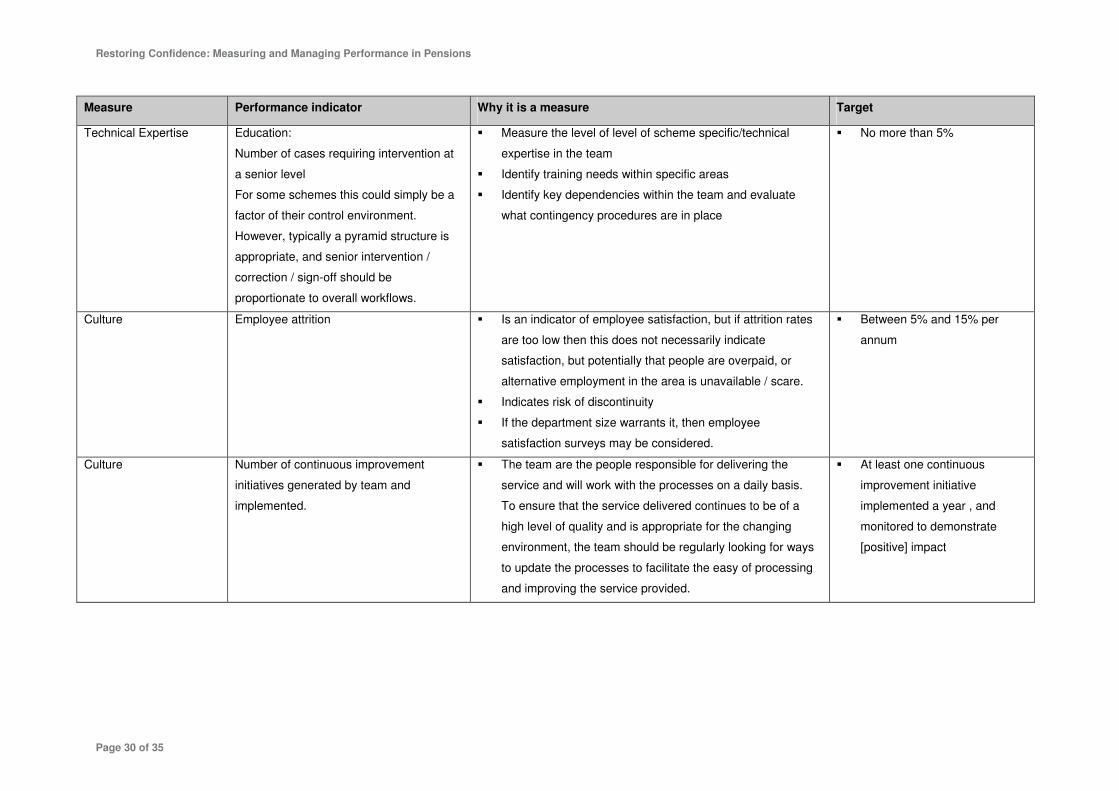

Measure Performance indicator Why it is a measure Target

Technical Expertise Education:

Number of cases requiring intervention at

a senior level

For some schemes this could simply be a

factor of their control environment.

However, typically a pyramid structure is

appropriate, and senior intervention /

correction / sign-off should be

proportionate to overall workflows.

� Measure the level of level of scheme specific/technical

expertise in the team

� Identify training needs within specific areas

� Identify key dependencies within the team and evaluate

what contingency procedures are in place

� No more than 5%

Culture Employee attrition

� Is an indicator of employee satisfaction, but if attrition rates

are too low then this does not necessarily indicate

satisfaction, but potentially that people are overpaid, or

alternative employment in the area is unavailable / scare.

� Indicates risk of discontinuity

� If the department size warrants it, then employee

satisfaction surveys may be considered.

� Between 5% and 15% per

annum

Culture Number of continuous improvement

initiatives generated by team and

implemented.

� The team are the people responsible for delivering the

service and will work with the processes on a daily basis.

To ensure that the service delivered continues to be of a

high level of quality and is appropriate for the changing

environment, the team should be regularly looking for ways

to update the processes to facilitate the easy of processing

and improving the service provided.

� At least one continuous

improvement initiative

implemented a year , and

monitored to demonstrate

[positive] impact

Restoring Confidence: Measuring and Managing Performance in Pensions

Page 31 of 35

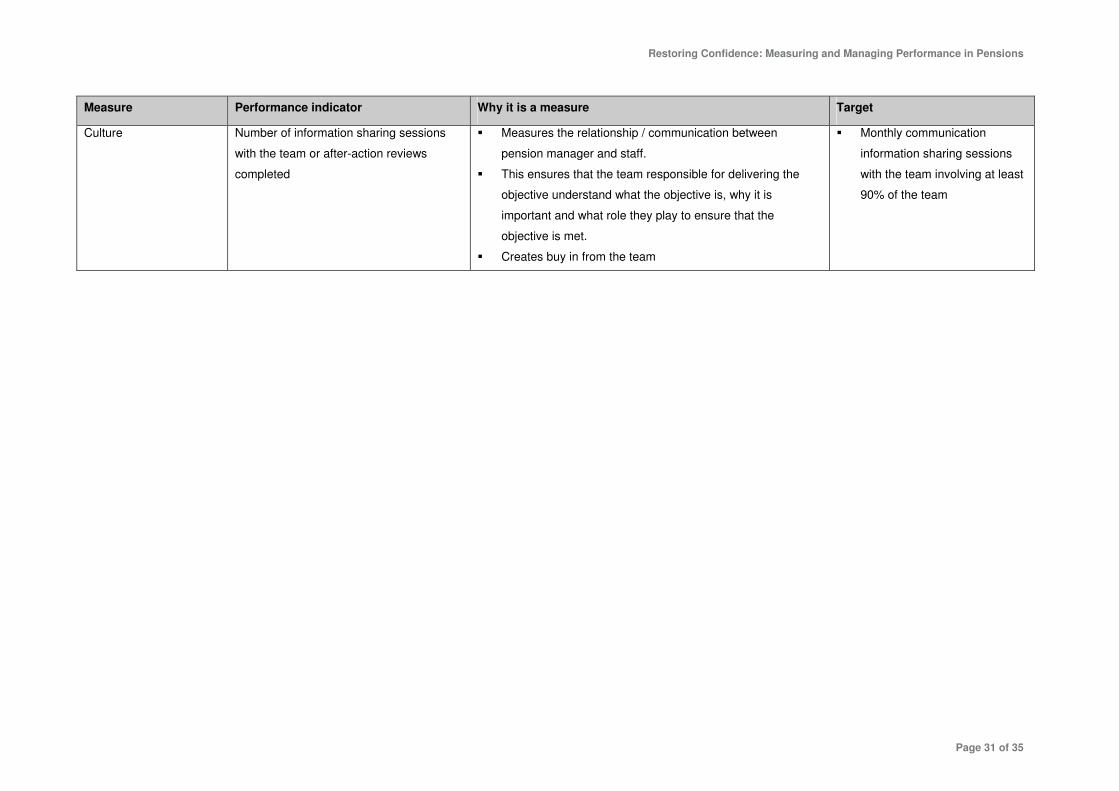

Measure Performance indicator Why it is a measure Target

Culture Number of information sharing sessions

with the team or after-action reviews

completed

� Measures the relationship / communication between

pension manager and staff.

� This ensures that the team responsible for delivering the

objective understand what the objective is, why it is

important and what role they play to ensure that the

objective is met.

� Creates buy in from the team

� Monthly communication

information sharing sessions

with the team involving at least

90% of the team

Restoring Confidence: Measuring and Managing Performance in Pensions

Page 32 of 35

Appendix II: Our Research Methodology

The benchmark group – examining the strategic vision

Following the appointment of Higham Dunnett Shaw, the project team agreed the companies to be invited to form

a benchmark group and formally requested their participation. Over forty interviews were arranged with

representatives from the seven benchmark organisations as well as a number of key stakeholders within BP.

Team members met with a trustee, company representative and the pension manager from each organisation.

A standard template guided each interview to ensure all conversations covered the following areas:

� Your ‘value proposition’ to your people (why do you provide a pension scheme?);

� Core competencies and value drivers (how do you get maximum value out of your pension offering?)

� Measures (how do you measure success or failure?);

� Approach to risk management;

� Governance and management of conflicting interests.

Each interview was written up and agreed by the respective participants and a trend analysis was carried out to

identify any emerging patterns between the various stakeholders and organisations. Certain common themes

surfaced from the BP interviews. This resulted in a reshaping of the working strategic vision into a revised

format, which in BP’s case was based around the triple concept of “Professional, Personal and Progressive”.

The extracts below highlight the focus of the BP interviewees:

…

� “The quality of care must shine through”

� “They won’t find it better handled elsewhere!”

� “Service excellence will minimise issues; therefore

making life easier for the Trustee Board”

Restoring Confidence: Measuring and Managing Performance in Pensions

Page 33 of 35

About the Authors

Bernard Marr is one of the world’s leading experts on strategic performance management

and balanced scorecards. He specialises in the identification, measurement and

management of strategic performance drivers. In this capacity, he has advised and worked

with many leading organisations including Accenture, Astra Zeneca, Barclays, BP, DHL,

Fujitsu, Gartner, HSBC, NovoNordisk, the Home Office, the Royal Air Force, and Royal

Dutch Shell. He has extensive work experience in private companies, public sector

organisations, and governments across North America, Europe, Africa, the Middle East and

Asia, which makes him an acclaimed keynote speaker, consultant, inspiring teacher, and award-winning writer. In

its recent article ‘wise guys’,the CEO Journal recognised Bernard Marr as one of today’s leading business brains.

Having gained management experience in consulting, manufacturing and international trading corporations,

Bernard moved to the University of Cambridge to become a management researcher at the Judge Institute of

Management Studies. Since 1999 he has been a Research Fellow at the renowned Centre for Business

Performance at Cranfield School of Management, he also holds multiple visiting professorships.

Bernard Marr has contributed to over 100 books, reports, and articles on topics such as Balanced Scorecard,

Corporate Performance Management, Strategy Maps, and Intangible Assets. He is the author of the recent books

“Strategic Performance Management: Leveraging and measuring your intangible value drivers”, “Perspectives on

Intellectual Capital: Managing, Measuring and Reporting Intangibles”, “Weighing the Options: BSC Software”,

and “Automating your Scorecard”.

Bernard is chairman of the international PMA IC Group, Intangible Assets Editor of the journal Measuring

Business Excellence, and member of the editorial board of The Handbook of Business Strategy. He also serves

on the editorial boards of many leading journals in the field of managing and measuring performance.

Restoring Confidence: Measuring and Managing Performance in Pensions

Page 34 of 35

Jocelyn Blackwell is a Fellow of the Pensions Management Institute (PMI) and a

member of the PMI Council. She is a major contributor to the “Raising Standards of

Pensions Administration” initiative, a subject about which she is passionate. She is also

the author of many published articles on administration, outsourcing, communications

and technology issues and is a contributing author to Tolley’s Guide to Administration.

Having begun her career as an actuarial analyst, Jocelyn worked for a number of

consultancy firms before establishing Dunnett Shaw in 1986. She has managed a wide variety of projects

delivering strategic, IT and administrative solutions for pension schemes, insurance companies and third party

administrators. Her extensive list of UK clients has included BP Pensions Services, Railway Pensions

Management Ltd, NHS Pensions Agency, Unilever UK, J Rothschild International Assurance and Alexander

Forbes (Johannesburg).

Jocelyn was appointed Chief Executive Officer of Higham Dunnett Shaw in February 2006, following Higham

Group’s acquisition of Dunnett Shaw in 2005.

Kenneth Donaldson joined Higham Dunnett Shaw in 2005 to shape the development

of the company’s pension strategy. He has been involved with a number of projects

spanning traditional pension schemes and the new approaches being taken to liabilities

in the insurance buyout market. Along with Jocelyn Blackwell he led the exercise

commissioned by the BP Pension Fund on which this paper is based.

Kenneth was formerly a director of Hazell Carr where he helped to establish and develop its pension consulting

business into a successful and profitable organisation. A key part of this was a programme of culture change

within the principal Reading site (staffed by some 200 people), which transformed the business from function

based to genuinely client facing service delivery team, and resulted in substantially improved efficiency.

Between 1999 and 2003 he was the actuarial expert speaker and subsequently the Chairman of the Institute of

Actuaries’ seminars on how to manage successfully the focused winding-up of a pension scheme.

Kenneth began his career at Clay and Partners (now part of Aon). His responsibilities included acting as an

expert witness, an independent trustee, consulting actuary and also leading major due diligence exercises, with

particular interest in PFI contracts and pension scheme wind-ups.

Outside the office, Kenneth is closely associated with the “Save the Rhino” charity. He took part in the legendary

“Marathon Des Sables” in 2003 and most recently ran six back-to-back marathons across the Andes. This

gruelling Ultra-Marathon took place at an altitude of over one mile, and involved wearing the famous Rhino

costume designed by Gerald Scarfe.

Restoring Confidence: Measuring and Managing Performance in Pensions

Page 35 of 35

Endnotes/Further Reading i Seib, Christine, April 20, 2006, The Times

ii Inman, Philip, May 12, 2006, The Guardian

iii Inman, Philip, May 12, 2006, The Guardian

iv Murphy, Paul and Finch, Julia, April 30, 2005, The Guardian

v Mawson, James, March 22, 2006, The Independent

vi Daley, J. March 9, 2006, The Independent

vii Buckley, Christine, November 18, 2005, The Times

viii The Pensions Regulator Medium Term Strategy April 2006 Chapter 1

ix Miller, Robert (2006) Poor records ‘put plan payouts at risk’, The Daily Telegraph, Friday, April 28, 2006, page

B3

x This section is based on Marr, B. (2006) Strategic Performance Management: Leveraging and Measuring Your

Intangible Value Drivers, Butterworth-Heinemann, Oxford.

xi This analogy has been used on various occasions, one of the most convincing was by Prahalad, C.K. and

Hamel, G. (1990), 'The Core Competence of the Corporation', Harvard Business Review, Vol. 68, No. 3,

May/Jun, pp. 79. However, tree diagrams can be traced back to the third-century Syrian philosopher’s diagram

named after its developer, ‘Tree of Porphyry’ based upon the work of Aristotle.

xii They use the Balanced Scorecard Approach. For more information please see Kaplan and Norton (2004)

Strategy Maps, Harvard Business School Press, Boston, MA.

xiii For full case study see: Marr, B. (2005) Strategic Performance Management, Butterworth-Heinemann

xiv For more information see: Ashton, C. Transforming Strategic Performance through the Balanced Scorecard –

Case Study: Banking 365.

xv Mike Bourne “Performance Measures: Unnecessary Baggage.” Financial World, January 2002.