Embed Size (px)

Citation preview

Alm Brand

Results for Q1 2015 Webcast presentation 12 May 2015

Financial highlights of Q1 2015

Pre-tax profit: DKK 202m

Forward-looking activities: Pre-tax profit: DKK 276m

Winding-up activities: Loss: DKK 74m • Writedowns: DKK 63m

G R O U P

Non-life Insurance Pre-tax profit: DKK 257m

• CR: 80.1 • Run-off gain: 10.1 • Expense ratio: 16.3% • Premium growth: 0.2%

Life and Pension Pre-tax profit: DKK 26m

• Risk result: DKK 13m • Bonus potential: DKK 1.1bn • Bonus rate: 11.5%

Banking Pre-tax profit: DKK 6m

• Writedowns: DKK 6m • Growth in lending • Growth in full-service

customers

2

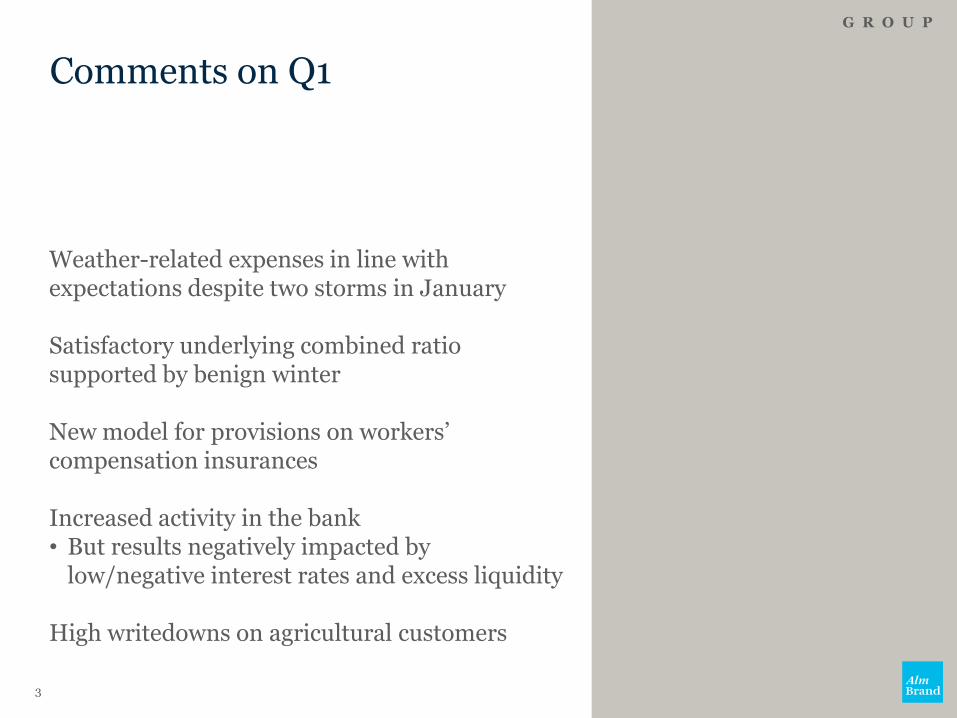

Comments on Q1

Weather-related expenses in line with expectations despite two storms in January Satisfactory underlying combined ratio supported by benign winter New model for provisions on workers’ compensation insurances Increased activity in the bank • But results negatively impacted by

low/negative interest rates and excess liquidity High writedowns on agricultural customers

G R O U P

3

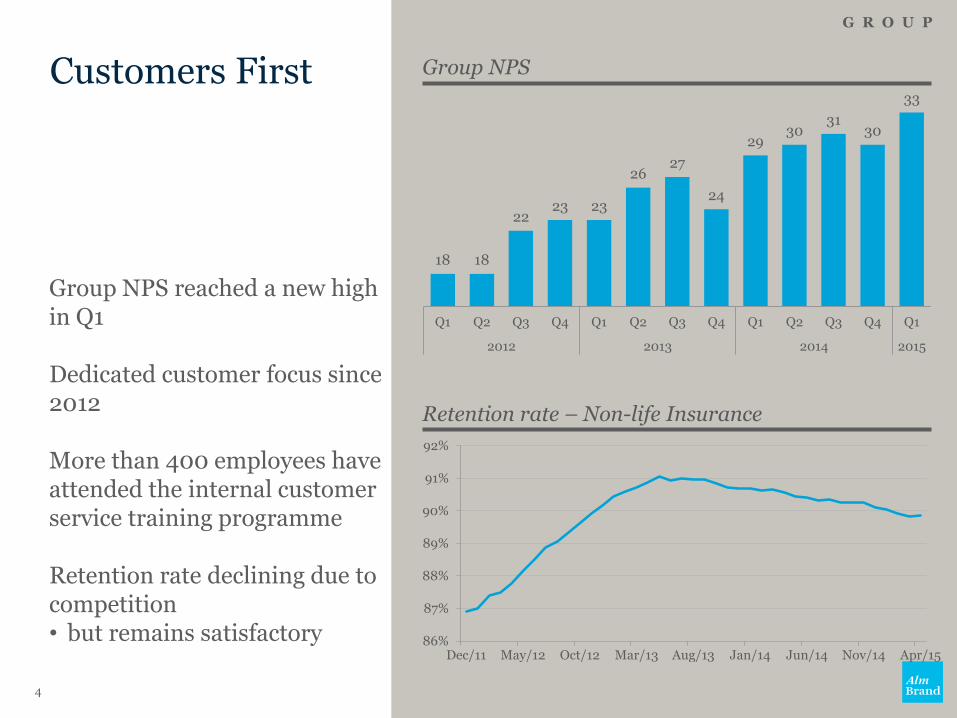

Customers First

Group NPS reached a new high in Q1 Dedicated customer focus since 2012 More than 400 employees have attended the internal customer service training programme Retention rate declining due to competition • but remains satisfactory

G R O U P

Group NPS

18 18

22 23 23

26 27

24

29 30

31 30

33

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2012 2013 2014 2015

4

86%

87%

88%

89%

90%

91%

92%

Dec/11 May/12 Oct/12 Mar/13 Aug/13 Jan/14 Jun/14 Nov/14 Apr/15

Retention rate – Non-life Insurance

fjern evt. pladsholderen

NON-LIFE INSURANCE Highlights

Pre-tax profit of DKK 257m

• Technical result better than expected

– Combined ratio of 80.1

– Combined ratio excl. run-offs of 90.2

• Positive investment return

– Satisfactory returns on mortgage deeds and equities

N O N - L I F E I N S U R A N C E

Pre-tax profit DKKm

5

139 133 135

245

25

10

-3

12

164

143 132

257

2012 2013 2014 2015

Q1

Technical result

Investment return after technical interest

Combined ratio better than expected Combined ratio of 80.1 - Better than expected • Run-off gains improved CR by 10.1 ppts

– Approx. half was related to the new model on workers’ compensation insurances

• Weather-related and major claims better than expected

Underlying combined ratio of 81.5

• Discounting increased CR by 0.7 ppt • Number of claims down by 3.7% – Very few theft claims – Benign winter resulted in few motor claims

• Higher average claims

Expense ratio down Y/Y • Lower than expected

N O N - L I F E I N S U R A N C E

Combined ratio

6

73.2 72.6 72.4

63.8

15.7 16.8 16.8

16.3

88.9 89.4 89.2

80.1 81.8 82.0 81.1 81.5

2012 2013 2014 2015

Q1

Claims ratio incl. reinsurance

Gross expense ratio

Underlying combined ratio

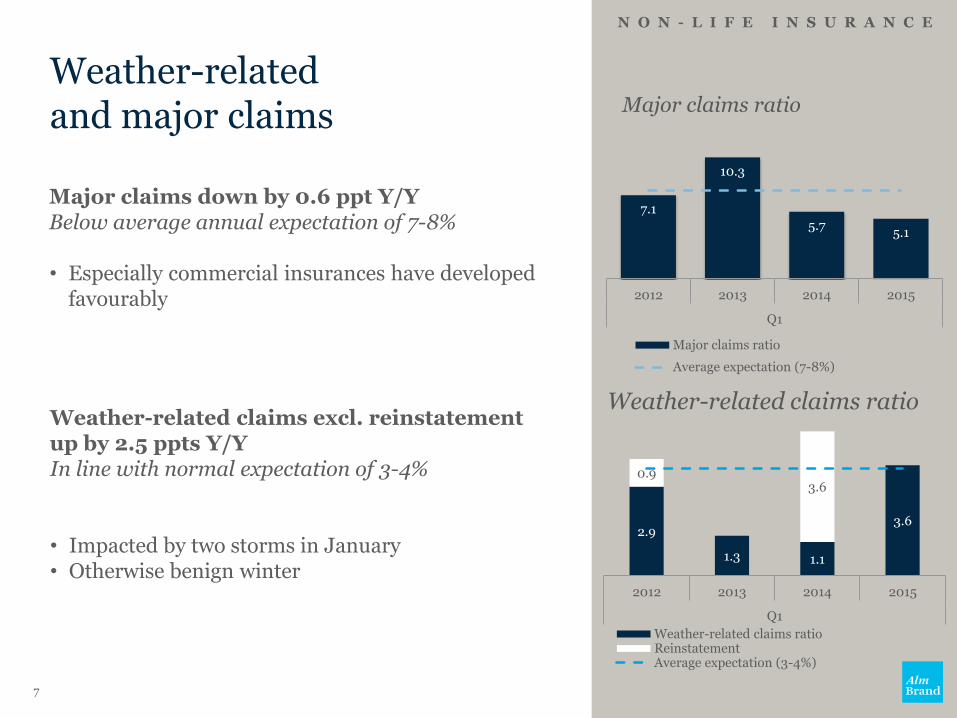

Weather-related and major claims

N O N - L I F E I N S U R A N C E

Major claims ratio

Major claims down by 0.6 ppt Y/Y Below average annual expectation of 7-8%

• Especially commercial insurances have developed

favourably

Weather-related claims excl. reinstatement up by 2.5 ppts Y/Y In line with normal expectation of 3-4%

• Impacted by two storms in January • Otherwise benign winter

Weather-related claims ratio

7

7.1

10.3

5.7 5.1

2012 2013 2014 2015

Q1

Major claims ratio

Average expectation (7-8%)

2.9

1.3 1.1

3.6

0.9 3.6

2012 2013 2014 2015

Q1

Weather-related claims ratio Reinstatement Average expectation (3-4%)

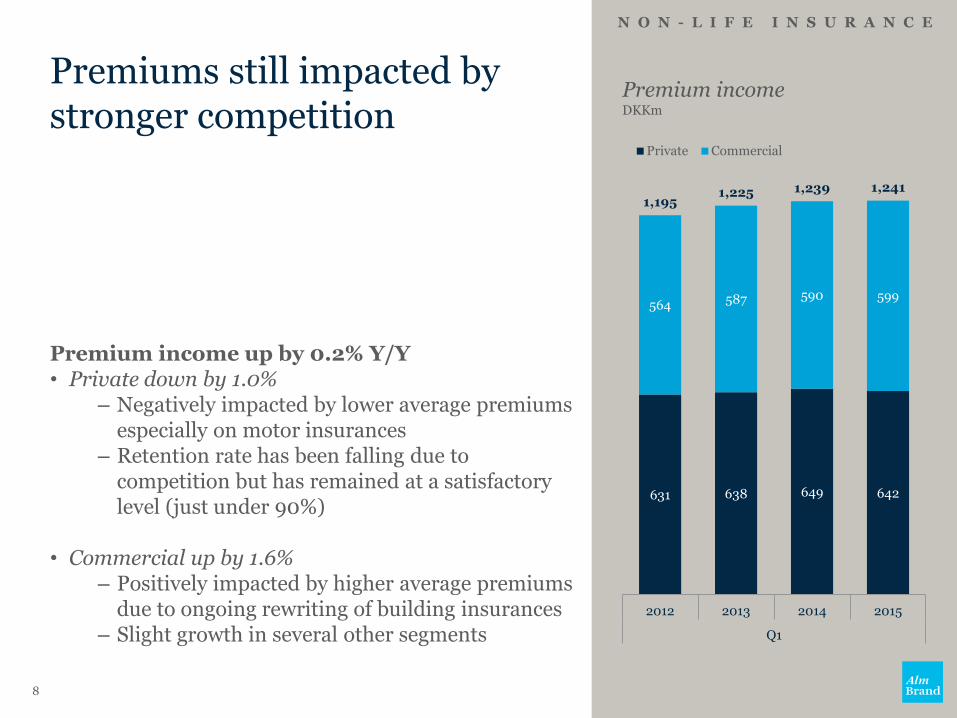

Premiums still impacted by stronger competition

Premium income up by 0.2% Y/Y • Private down by 1.0%

– Negatively impacted by lower average premiums especially on motor insurances

– Retention rate has been falling due to competition but has remained at a satisfactory level (just under 90%)

• Commercial up by 1.6% – Positively impacted by higher average premiums

due to ongoing rewriting of building insurances – Slight growth in several other segments

N O N - L I F E I N S U R A N C E

Premium income DKKm

8

631 638 649 642

564 587 590 599

1,195 1,225 1,239 1,241

2012 2013 2014 2015

Q1

Private Commercial

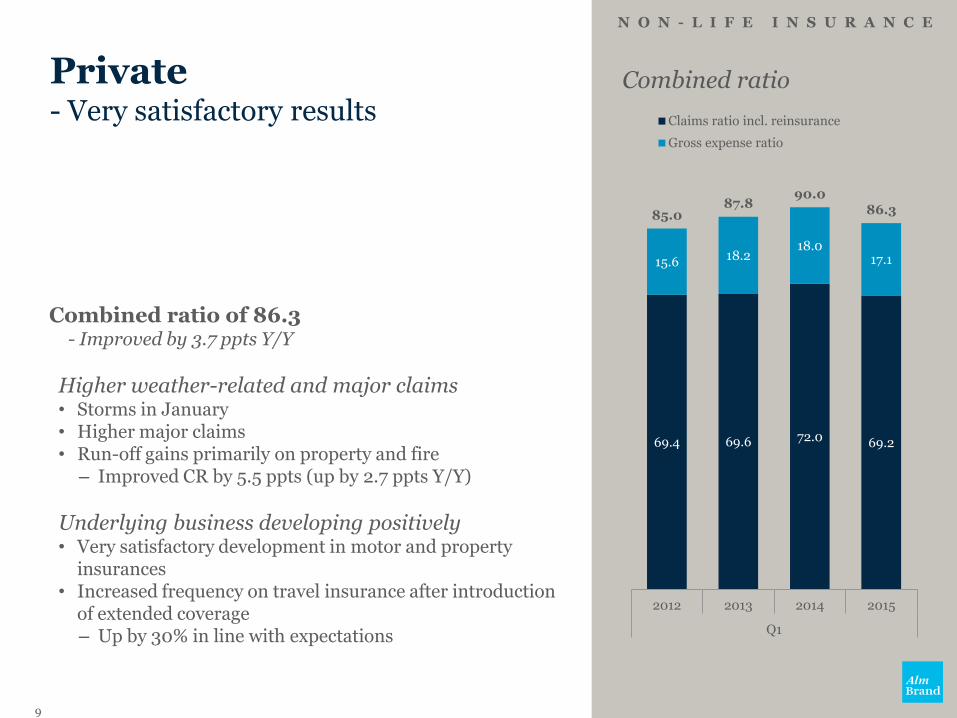

Private - Very satisfactory results

Combined ratio of 86.3 - Improved by 3.7 ppts Y/Y

Higher weather-related and major claims • Storms in January • Higher major claims • Run-off gains primarily on property and fire

– Improved CR by 5.5 ppts (up by 2.7 ppts Y/Y)

Underlying business developing positively • Very satisfactory development in motor and property

insurances • Increased frequency on travel insurance after introduction

of extended coverage – Up by 30% in line with expectations

N O N - L I F E I N S U R A N C E

Combined ratio

9

69.4 69.6 72.0 69.2

15.6 18.2 18.0

17.1

85.0 87.8

90.0 86.3

2012 2013 2014 2015

Q1

Claims ratio incl. reinsurance

Gross expense ratio

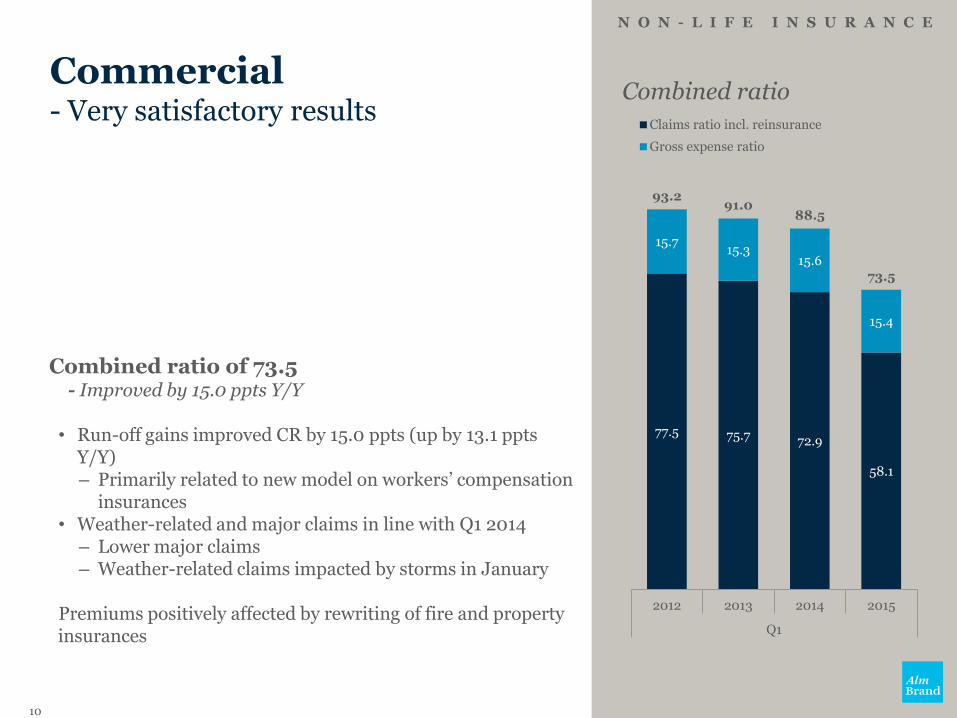

Commercial - Very satisfactory results

Combined ratio of 73.5 - Improved by 15.0 ppts Y/Y

• Run-off gains improved CR by 15.0 ppts (up by 13.1 ppts

Y/Y) – Primarily related to new model on workers’ compensation

insurances • Weather-related and major claims in line with Q1 2014

– Lower major claims – Weather-related claims impacted by storms in January

Premiums positively affected by rewriting of fire and property insurances

N O N - L I F E I N S U R A N C E

Combined ratio

10

77.5 75.7 72.9

58.1

15.7 15.3

15.6

15.4

93.2 91.0

88.5

73.5

2012 2013 2014 2015

Q1

Claims ratio incl. reinsurance

Gross expense ratio

fjern evt. pladsholderen

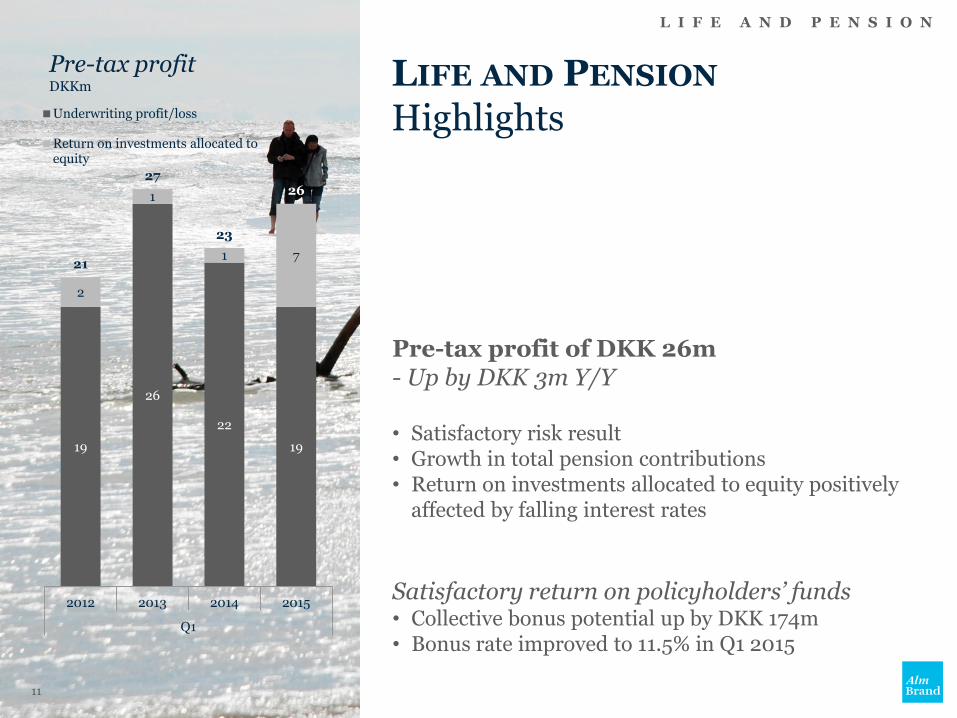

LIFE AND PENSION Highlights

Pre-tax profit of DKK 26m - Up by DKK 3m Y/Y • Satisfactory risk result • Growth in total pension contributions • Return on investments allocated to equity positively

affected by falling interest rates

Satisfactory return on policyholders’ funds • Collective bonus potential up by DKK 174m • Bonus rate improved to 11.5% in Q1 2015

L I F E A N D P E N S I O N

Pre-tax profit DKKm

11

19

26

22

19

2

1

1 7 21

27

23

26

2012 2013 2014 2015

Q1

Underwriting profit/loss

Return on investments allocated to equity

Pension contributions

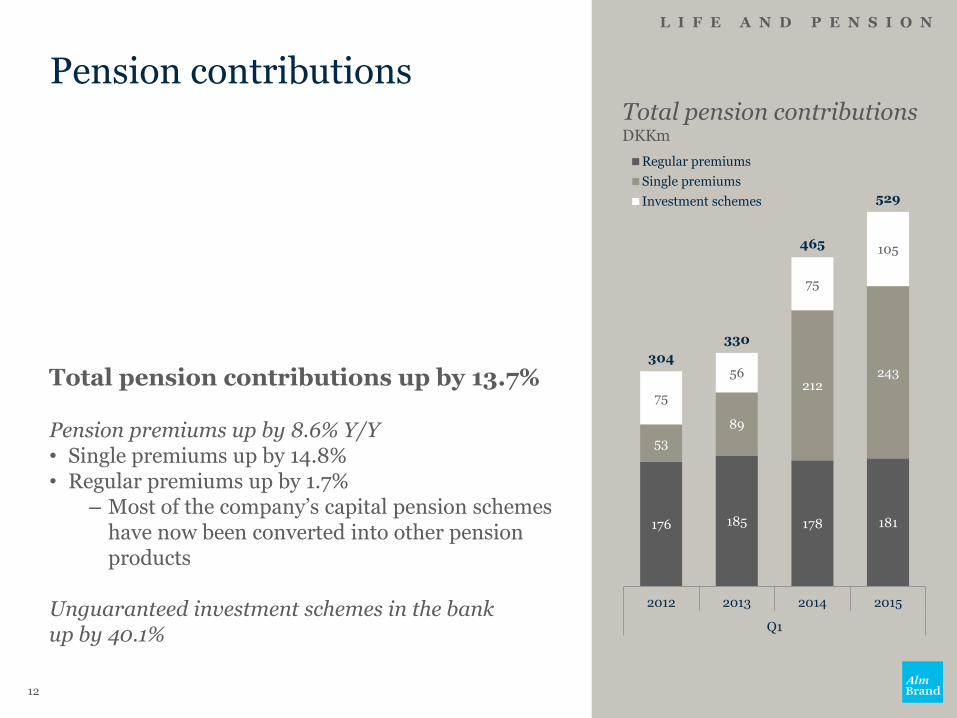

Total pension contributions up by 13.7%

Pension premiums up by 8.6% Y/Y • Single premiums up by 14.8% • Regular premiums up by 1.7%

– Most of the company’s capital pension schemes have now been converted into other pension products

Unguaranteed investment schemes in the bank up by 40.1%

L I F E A N D P E N S I O N

Total pension contributions DKKm

12

176 185 178 181

53

89

212 243

75

56

75

105

304

330

465

529

2012 2013 2014 2015

Q1

Regular premiums

Single premiums

Investment schemes

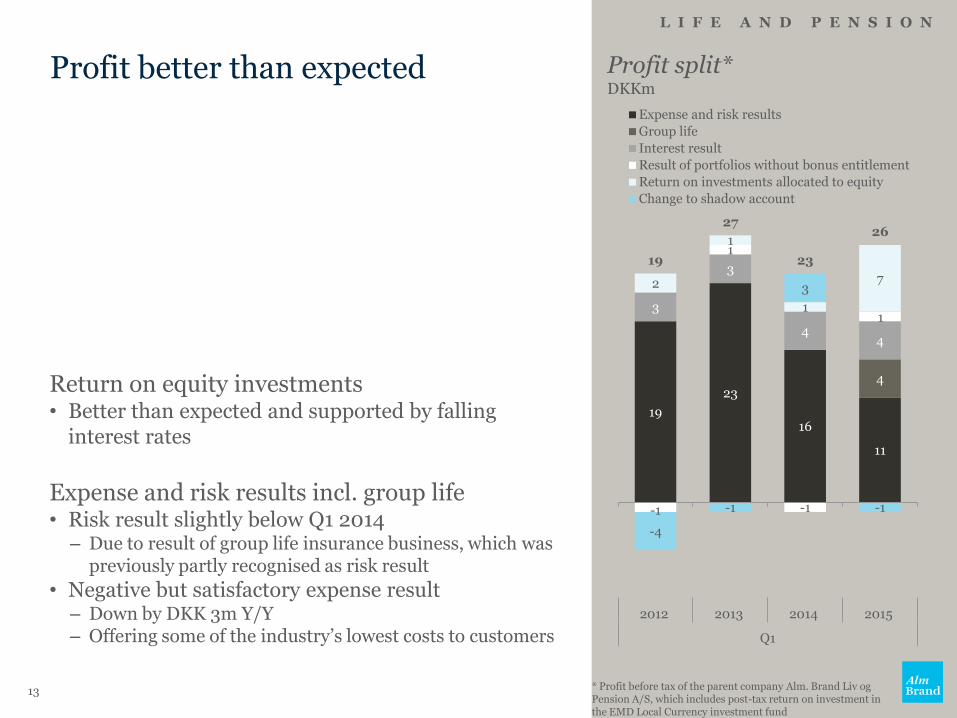

Profit better than expected

Return on equity investments • Better than expected and supported by falling

interest rates

Expense and risk results incl. group life • Risk result slightly below Q1 2014

– Due to result of group life insurance business, which was previously partly recognised as risk result

• Negative but satisfactory expense result – Down by DKK 3m Y/Y – Offering some of the industry’s lowest costs to customers

L I F E A N D P E N S I O N

Profit split* DKKm

13 * Profit before tax of the parent company Alm. Brand Liv og Pension A/S, which includes post-tax return on investment in the EMD Local Currency investment fund

19

23

16

11

4

3

3

4 4

-1

1

-1

1

2

1

1

7

-4

-1

3

-1

19

27

23

26

2012 2013 2014 2015

Q1

Expense and risk results

Group life

Interest result

Result of portfolios without bonus entitlement

Return on investments allocated to equity

Change to shadow account

Investment return - Very satisfactory return and improved bonus rate

L I F E A N D P E N S I O N

Strong bonus potential

• Average bonus rate of 11.5%

• Attractive bonus rate for new policyholders of 13.8%

Rate on policyholders’ savings

• Highest rate on private policyholders’ savings in Denmark

U74*

Interest rate group Total

0 1 2 3

Technical interest rate 0.5-1.5 1.5-2.5 2.5-3.5 3.5-4.5

Rate on policyholders’ savings, 2015 4.00 5.00 5.00 6.00

Investment assets (DKKbn) 0.1 5.9 1.9 1.4 3.8 13,1

Bonus rate (%) 13.8 18.6 6.8 4.6 11.5

Return (% YTD) 4.6 5.2 3.0 3.4 4.3

Bonds 100% 58% 51% 74% 78% 65%

Equities 0% 26% 21% 9% 4% 16%

Property 0% 16% 13% 10% 8% 12%

Fixed-income derivatives 0% 0% 15% 7% 10% 7%

*Portfolios without bonus entitlement

14

fjern evt. pladsholderen

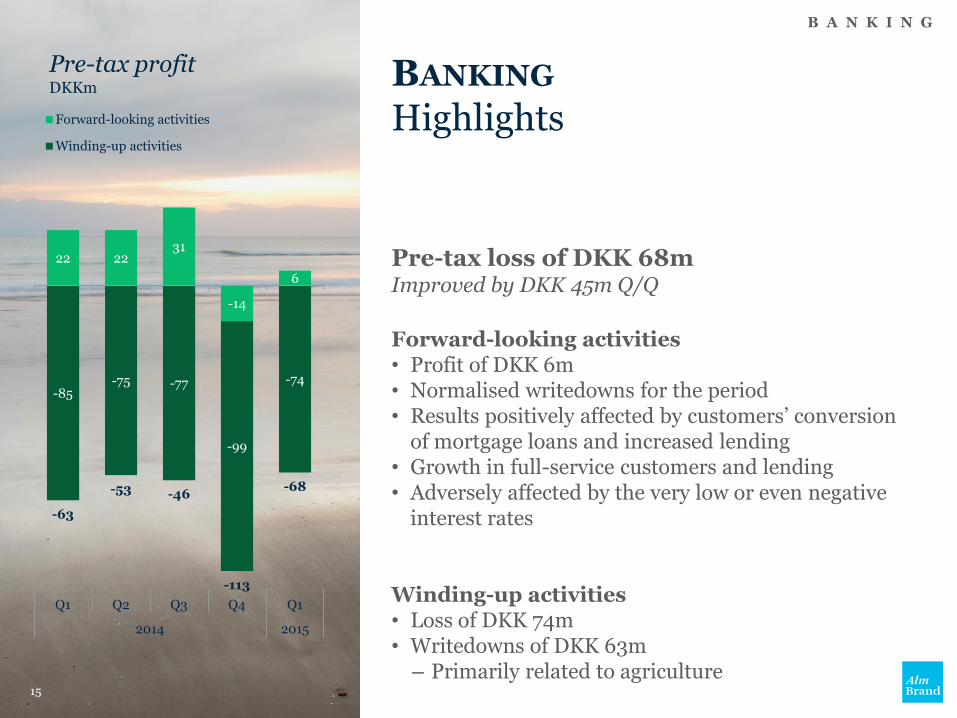

BANKING Highlights

Pre-tax loss of DKK 68m Improved by DKK 45m Q/Q

Forward-looking activities • Profit of DKK 6m • Normalised writedowns for the period • Results positively affected by customers’ conversion

of mortgage loans and increased lending • Growth in full-service customers and lending • Adversely affected by the very low or even negative

interest rates

Winding-up activities • Loss of DKK 74m • Writedowns of DKK 63m

– Primarily related to agriculture

B A N K I N G

Pre-tax profit DKKm

15

22 22 31

-14

6

-85 -75 -77

-99

-74

-63

-53 -46

-113

-68

Q1 Q2 Q3 Q4 Q1

2014 2015

Forward-looking activities

Winding-up activities

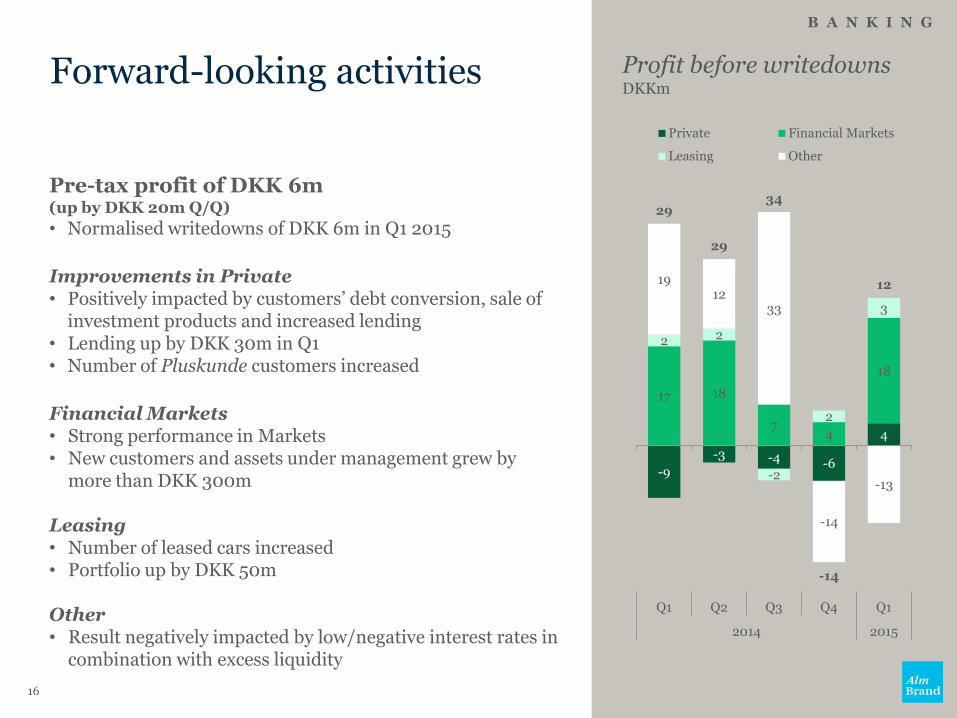

Forward-looking activities

Pre-tax profit of DKK 6m (up by DKK 20m Q/Q)

• Normalised writedowns of DKK 6m in Q1 2015

Improvements in Private • Positively impacted by customers’ debt conversion, sale of

investment products and increased lending • Lending up by DKK 30m in Q1 • Number of Pluskunde customers increased

Financial Markets • Strong performance in Markets • New customers and assets under management grew by

more than DKK 300m

Leasing • Number of leased cars increased • Portfolio up by DKK 50m

Other • Result negatively impacted by low/negative interest rates in

combination with excess liquidity

B A N K I N G

Profit before writedowns DKKm

16

-9

-3 -4 -6

4

17 18

7 4

18

2 2

-2

2

3

19 12

33

-14

-13

29

29

34

-14

12

Q1 Q2 Q3 Q4 Q1

2014 2015

Private Financial Markets

Leasing Other

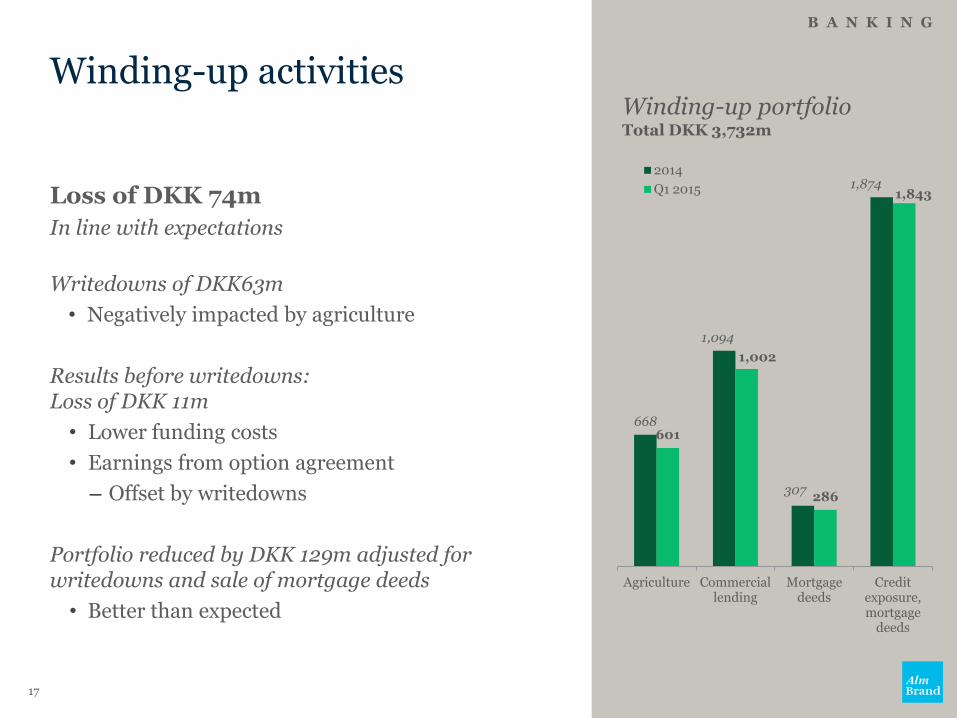

Winding-up activities

Loss of DKK 74m

In line with expectations

Writedowns of DKK63m

• Negatively impacted by agriculture

Results before writedowns: Loss of DKK 11m

• Lower funding costs

• Earnings from option agreement

– Offset by writedowns

Portfolio reduced by DKK 129m adjusted for writedowns and sale of mortgage deeds

• Better than expected

B A N K I N G

Winding-up portfolio Total DKK 3,732m

17

668

1,094

307

1,874

601

1,002

286

1,843

Agriculture Commercial lending

Mortgage deeds

Credit exposure, mortgage

deeds

2014

Q1 2015

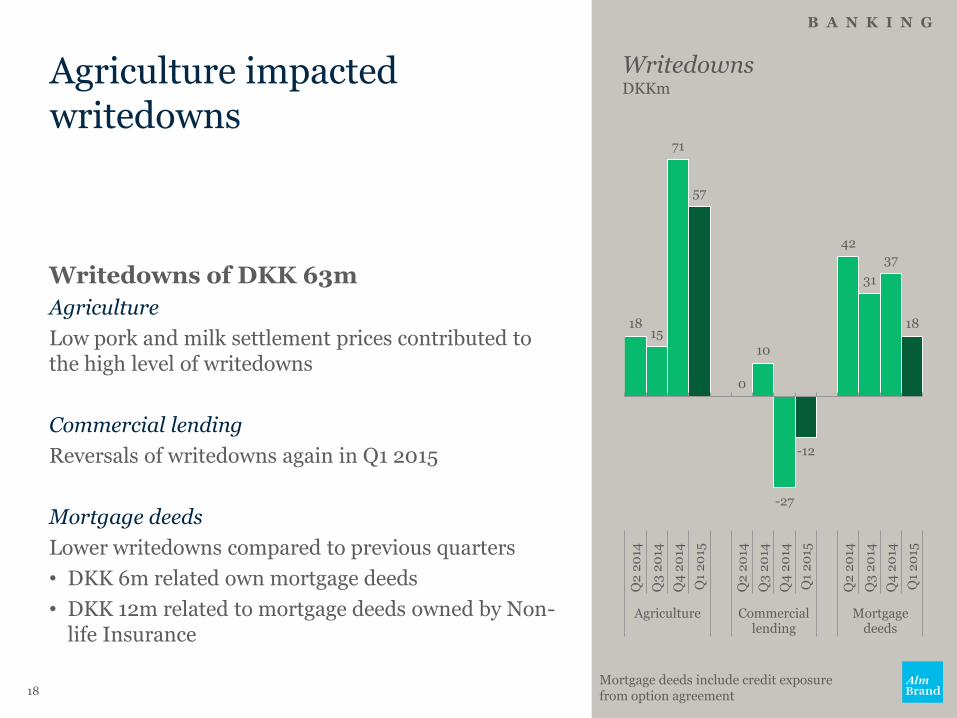

Agriculture impacted writedowns

Writedowns of DKK 63m

Agriculture

Low pork and milk settlement prices contributed to the high level of writedowns

Commercial lending

Reversals of writedowns again in Q1 2015

Mortgage deeds

Lower writedowns compared to previous quarters

• DKK 6m related own mortgage deeds

• DKK 12m related to mortgage deeds owned by Non-life Insurance

B A N K I N G

Writedowns DKKm

18 Mortgage deeds include credit exposure from option agreement

18 15

71

57

0

10

-27

-12

42

31

37

18

Q2

20

14

Q3

20

14

Q4

20

14

Q1

20

15

Q2

20

14

Q3

20

14

Q4

20

14

Q1

20

15

Q2

20

14

Q3

20

14

Q4

20

14

Q1

20

15

Agriculture Commercial lending

Mortgage deeds

CAPITAL MODEL

Excess capital higher than expected

• Risk related to Banking reduced by DKK 110m in Q1

• Dividend payment reduced excess capital by DKK 85m

G R O U P

19

Development in excess capital DKKm

Equity in Q1 2015 was reduced by the dividend payment approved at the AGM

4,506 4,685 4,847 4,906

-665 -556 -526 -509

1,654 925 522 518

5,495

5,054 4,843 4,915

886 906

211 383

2012 2013 2014 Q1 2015

Equity

Tax assets

Tier 2 capital

Excess relative to internal capital target

Full-year outlook for 2015 - Raised by an additional DKK 50m

DKK 350-450m Pre-tax profit

Forward-looking activities: Pre-tax profit of DKK 700-750m

Winding-up activities: Loss of DKK 300-350m Prices on agricultural products expected to impact writedowns negatively

G R O U P

Non-life Insurance Pre-tax profit: DKK 650m • CR at the level of 88 • Expense ratio at the level of 16% • Premiums in line with 2014

Life and Pension Pre-tax profit: DKK 75m • Expects to book risk

allowance for all contribution groups

• Regular premiums expected to grow by 4%

Banking Pre-tax profit: DKK 40m • Writedowns of around

DKK 20m • Negative impact from low

interest rate level

20

Non-life Insurance: Run-off gains lifted the technical result. Topline still impacted by intensified competition

Life and Pension: Growth in pension contributions and improved bonus potential

Banking: Increased customer activity in all continuing activities

Winding-up activities: Still high risk on agricultural lending

Outlook: Pre-tax profit of DKK 350-450m in 2015

G R O U P

21

Highlights

“The statements made in this presentation are based on current expectations, estimates and projections made by management. All statements about future financial performance are subject to risks and uncertainties that could cause actual results to differ materially from those set forth in or implied by the statements. All statements about future financial performance made in this presentation are solely based on information known at the time of the preparation of the last published financial report, and the company assumes no obligation to update these statements, whether as a result of new information, future events, or otherwise.”

22

Alm Brand

Results for Q1 2015 Webcast presentation 12 May 2015