Embed Size (px)

Citation preview

2016 Category Quantification ReportSorghum Beer in South Africa

Media Feedback

2 / Feedback Report

Product Definitions

Product Definition

Wet-Based Sorghum Beer Sorghum beer sold in ready-to-drink liquid form with very limited shelf life

Dry-Based Sorghum Beer Sorghum in grain form used as an ingredient when making traditional homebrew beer

Beer Powder Instant powdered sorghum beer which is mixed with water and left overnight to ferment

3 / Feedback Report

Market Trends

The sorghum beer market comprises of wet-based and dry-based categories. The dry-based

category is further divided into malt powder and beer powder.

The sorghum beer market declined in volume produced in 2015. The decline may be attributed to

the shortage of sorghum crops available in the country. South Africa does not produce enough

sorghum crop to be used in the production of sorghum beer and rely heavily on imports. The import

costs and the weak Rand-Dollar exchange rate, attributed to the increase in local pricing thereby

affecting volume sold negatively. Some importers experienced delays in product delivery and that

also affected their sales negatively. The drought resulted in farmers not planting sufficient crops,

whilst others preferred to plant crops that yielded a higher price and profit in return, than sorghum in

South Africa.

Wet-based sorghum beer volume declined as it is believed the industry lost a share to other ready-

to-drink alcoholic and non-alcoholic beverages. The 1 litre carton continued to dominate the market

in the face of share erosion. Bulk packaging volume increased but has not reached the same levels

prior to 2012. Bulk packs are expected to continue growing, taking share from the more profitable 1-

2 litre packs.

The malt powder category increased in volume from 2014 to 2015. It is believed that the category

took some share from beer powder. The beer powder lost share as the maize price, which is the

main ingredient of the product, increased.

4 / Feedback Report

Market Trends Cont.

Sorghum beer is mainly sold in the wholesale channel, although selected brands are also available

in retail sector, but in lower volumes and smaller pack sizes. The on-consumption channel

experienced the greatest decline, possibly as consumers shifted their purchasing to the retail sector.

The retail market is generally characterised by more promotional and marketing activities than other

channels.

The sorghum beer demand remained focused in non-metropolitan regions where it is still considered

a traditional drink during family gatherings. Most regions experienced overall volume decline in

2015. The Western Cape region experienced the greatest decline and it is hypothesised that

consumers substituted sorghum beer with cheaper wine and other alcoholic beverages.

The category is expected to continue declining in volume in the short to medium term as less

sorghum is planted in the country and the manufacturers are forced to source the product from other

countries.

5 / Feedback Report

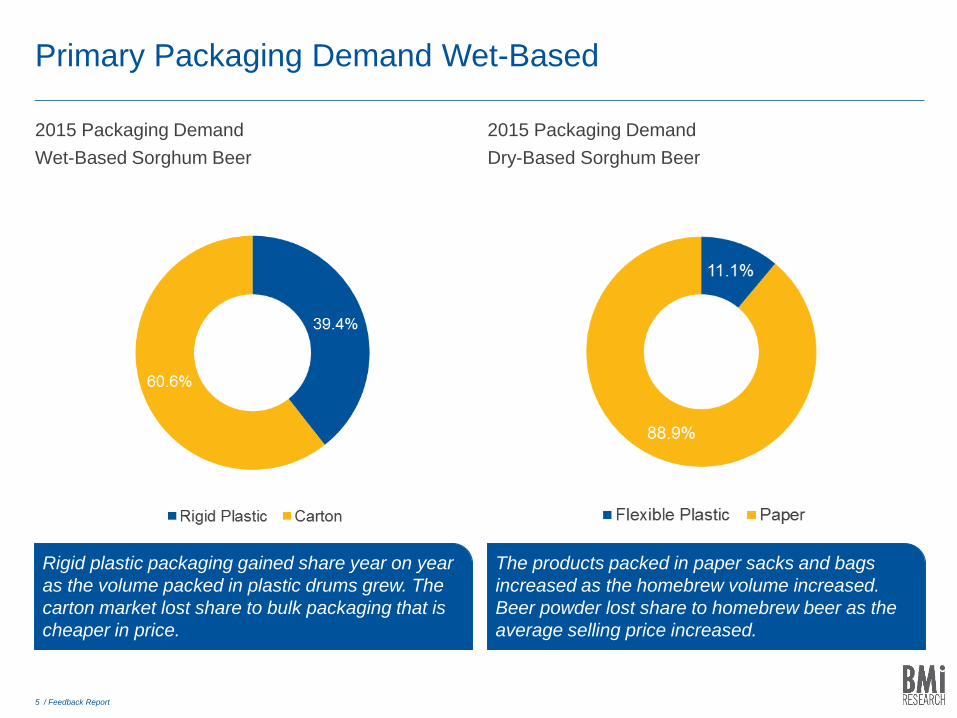

Primary Packaging Demand Wet-Based

2015 Packaging Demand

Wet-Based Sorghum Beer

Rigid plastic packaging gained share year on year

as the volume packed in plastic drums grew. The

carton market lost share to bulk packaging that is

cheaper in price.

The products packed in paper sacks and bags

increased as the homebrew volume increased.

Beer powder lost share to homebrew beer as the

average selling price increased.

2015 Packaging Demand

Dry-Based Sorghum Beer

6 / Feedback Report

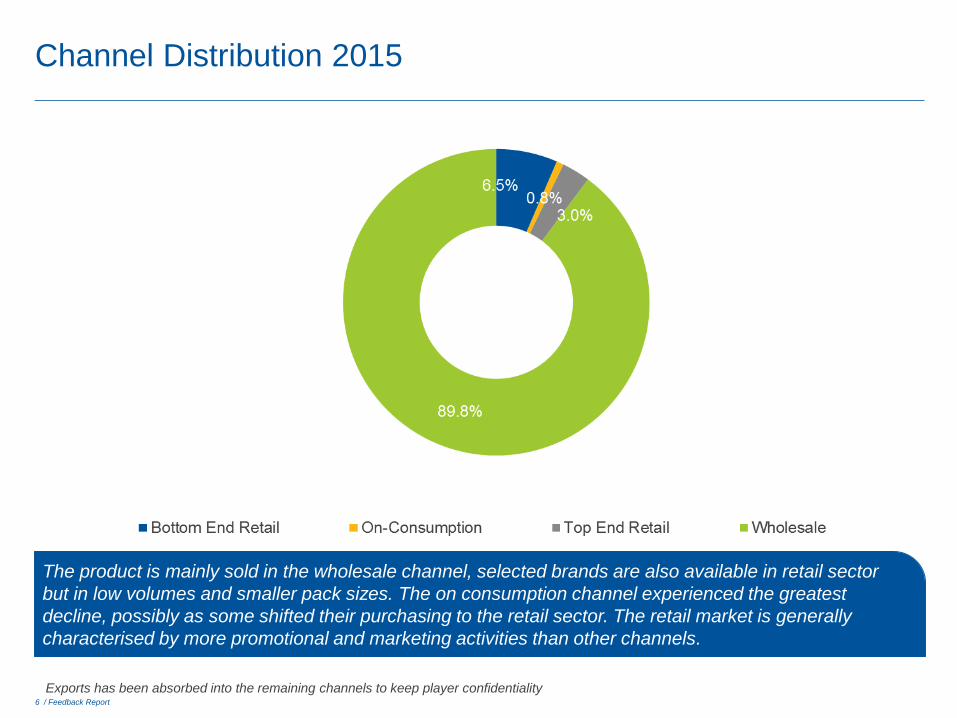

Channel Distribution 2015

Exports has been absorbed into the remaining channels to keep player confidentiality

The product is mainly sold in the wholesale channel, selected brands are also available in retail sector

but in low volumes and smaller pack sizes. The on consumption channel experienced the greatest

decline, possibly as some shifted their purchasing to the retail sector. The retail market is generally

characterised by more promotional and marketing activities than other channels.

7 / Feedback Report

Local Regional Distribution 2015

Excludes exports

The sorghum beer demand remained focused in non-metropolitan regions where it is still considered a

traditional drink during family gatherings. Most regions experienced overall volume decline in 2015. The

Western Cape region experienced the greatest decline and it is hypothesised that consumers substituted

sorghum beer with cheaper wine and other alcoholic beverages.

BMi Solutions

9 / Feedback Report

Packaging Annual Beverage Publications

All reports Full Report (All reports below)

• Packaging overview

• Paper & Board

• QPM

• Quarterly Import

Alcoholic Beverages

• Flavoured Alcoholic

Beverages

• Malt Beer

• Sorghum Beer

• Spirits

• Wine

Non Alcoholic Beverages

• Bottled Water

• Carbonated Soft

Drinks

• Cordials and Squash

• Energy Drinks

• Fruit Juice

• Iced Tea

• Mageu

• Sports Drinks

Dairy Beverages

• Dairy Juice Blends

• Drinking Yoghurt

• Flavoured Milk

• Maas

• Milk

BMi Tracking Report Schedule 2016

Annual Food Publications Confectionery & Snacks On Request

• Canned Protein

• Dairy

• Desserts

• F&C Beverages

• Pasta

• Rice

• Wheat and Grain

• Ice Cream

• Packaging of Snack

Foods

• South African

Confectionery Market

• The Impulse Market

in South Africa

• Biscuits and Rusks

• Breakfast Foods

• Baked Products

• Baking Aids

• Eggs

• Fats and Oils

• Frozen and Par-

Baked Products

• Premixes

• Pre-prepared Meals

• Processed Meat

Products

• Protein

• Sauces

• Soup and

Condiments

• Sweet and Savoury

Spreads

• Value Added Meals

10 / Feedback Report

Commissioned

Instore

Category

Ranging

Mystery

Shopping

Shopper

Insights

Promotional

Effectiveness

Instore

Compliance

Shelf &

Promotional

Price Surveys

Solutions Consumer

Insights

Shopper

Insights

Business

Insights

Advertising &

Campaign Testing

Omni

Channel

Competitive

Advertising

Tracking

Advertising

Category Quantification

Beverages Food Packaging

Advanced Analytics

Competitive

Pricing Simulation

Statistical

Optimisation

Model60%

Price

Sensitivity

Promotional

Effectiveness

Predictive Analytics

Copyright & Disclaimer

All rights reserved. No part of this publication may be reproduced,

photocopied or transmitted in any form, nor may any part of this

report be distributed to any person not a full-time employee of the

subscriber, without the prior written consent of the consultants.

The subscriber agrees to take all reasonable measures to

safeguard this confidentiality.

Note:

Although great care has been taken to ensure accuracy and

completeness in this project, no legal responsibility can be

accepted by BMi for the information and opinions expressed in

this report.

Copyright © 2016

BMi Research (Pty) Ltd

Reg No. 2008/004751/07

Thank youbmi.co.za

Contact

BMi Research

Telephone: +27 11 615 7000

Fax: +27 11 615 4999

Email: [email protected]