Embed Size (px)

Citation preview

Retirement income strategies:What have we learned?

John Ameriks

Principal

Vanguard

May 19, 2009

> 2

Agenda

• An old problem on a new scale• Products old and new• Consequences of volatility • Implications for planners

> 3

The changing retirement landscape

Key forces in the United States• The baby boomers are retiring• DC (or DB) lump sums are more prevalent• People are living longer• Health care burden is rising—even with Medicare

> Many retirees face an “asset/income” challenge.

> 4

15%

35% 36%

44%

28%

57%53%

44% 46%49% 49%

53%

60% 61%

0%

10%

20%

30%

40%

50%

60%

70%

Cuts in socialsecurity

Outliving savings Interest ratechanges

Health carecosts

Guaranteedincome

Marketfluctuations

Inflation, taxes

2004 2006

The changing consumer landscape

Growing consumer anxiety in the United StatesPre-retirees who are “very concerned” about:

Source: McKinsey & Company, 2006.

> 5

Spending is more complicated than saving

Accumulators:

How should I invest?

How much should I save?

> 6

Spending is more complicated than saving

Retirees:

How much can I spend to –

• Avoid running out of money?

• Avoid undue frugality?

• Leave something for heirs?

When can I afford

to retire?

How should I invest?

How do I estimate

my income needs?

How much will healthcare

cost?

Can I stomach income

volatility?

How can I

minimize taxes?

> 7

Retirement income planning

Constraints

• Regular income

• Flexible spending

• Survivors/bequests

Income goals

• Investment risk

• Inflation risk

• Longevity risk

Risk mitigation

• Investment costs

• Guarantee costs

• Taxes

Trading off conflicting goals and risks

> 8

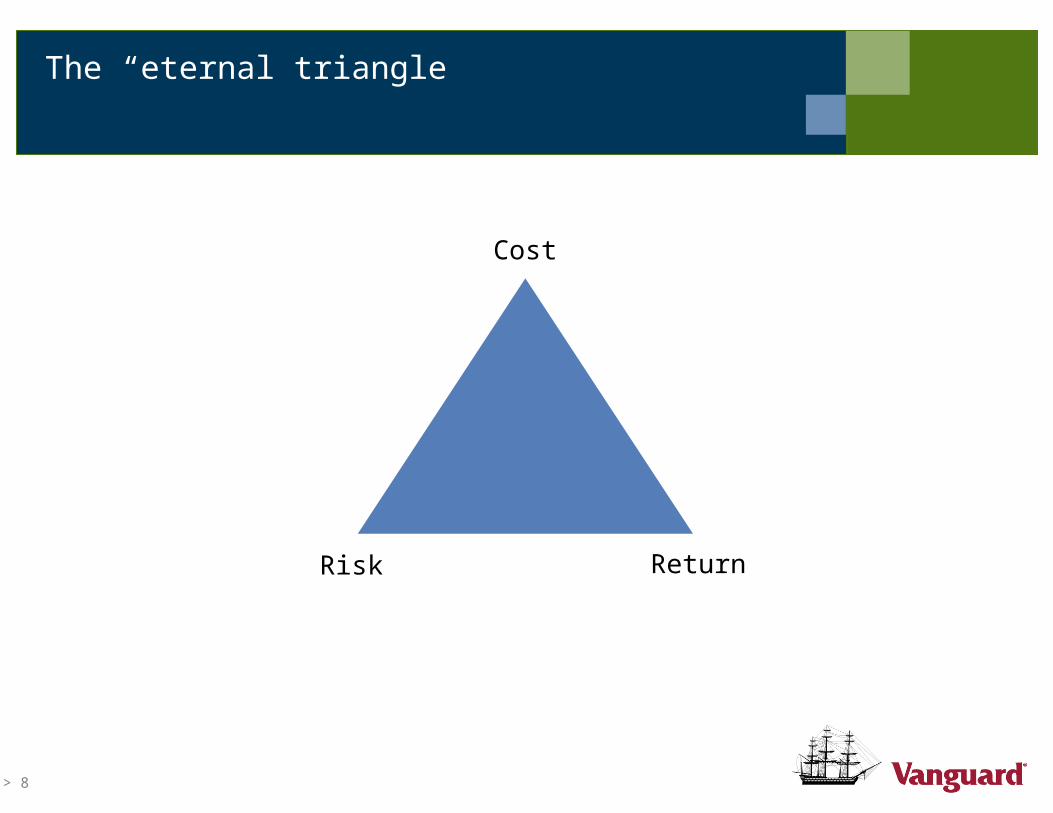

The “eternal triangle”

Risk Return

Cost

> 9

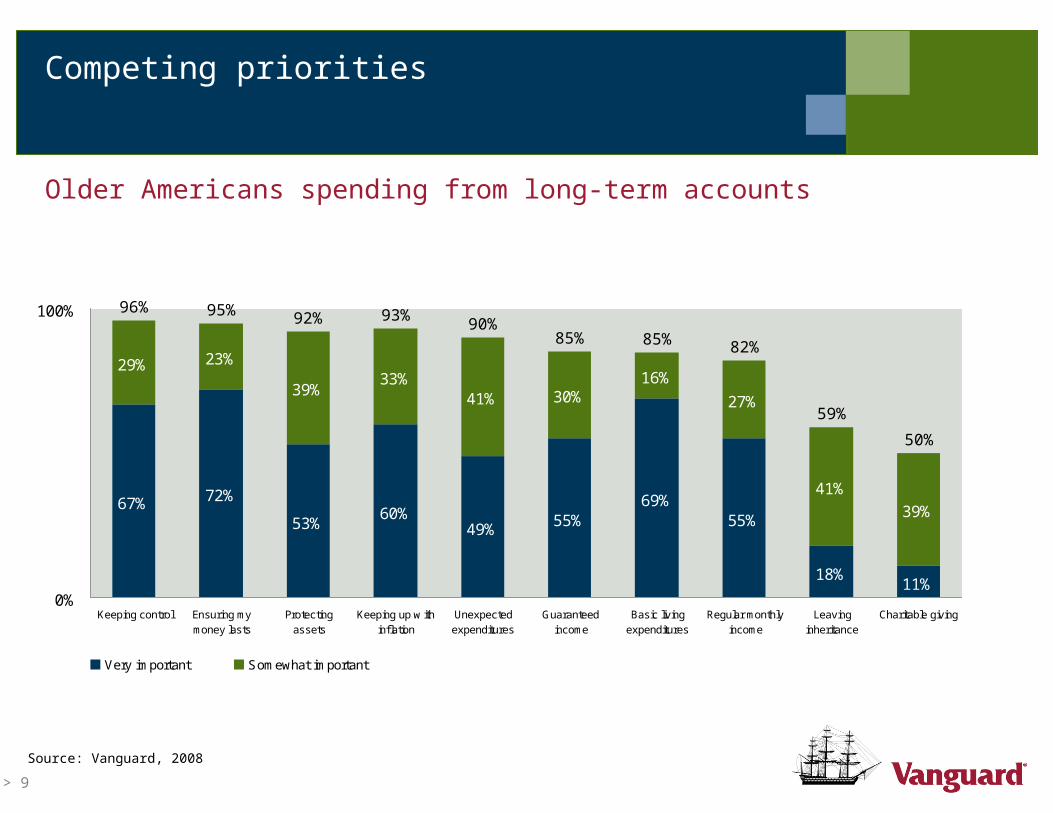

Competing priorities

67% 72%

53%60%

49%55%

69%55%

18%11%

29% 23%

39%33%

41% 30%16%

27%

41%

39%

0%

100%

Keeping control Ensuring mymoney lasts

Protectingassets

Keeping up w ithinf lation

Unexpectedexpenditures

Guaranteedincome

Basic livingexpenditures

Regular monthlyincome

Leavinginheritance

Charitable giving

Very important Somewhat important

96% 95% 92% 93%90%

85% 85% 82%

59%

50%

Source: Vanguard, 2008

Older Americans spending from long-term accounts

> 10

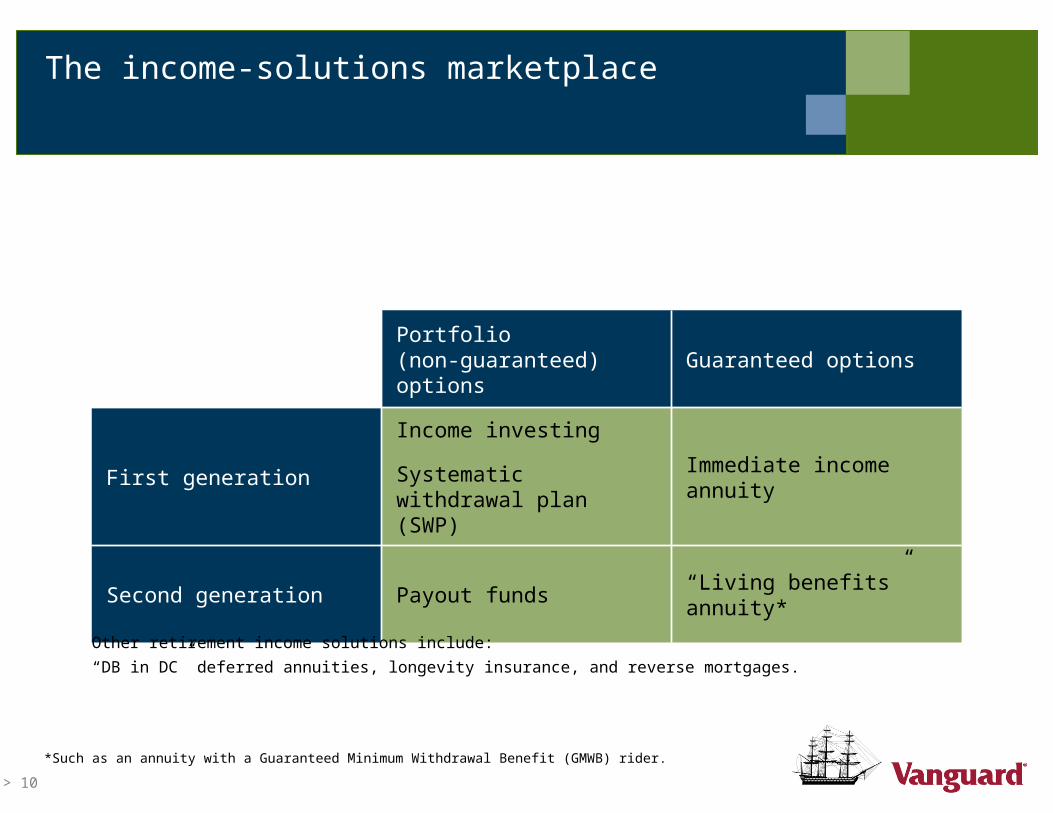

*Such as an annuity with a Guaranteed Minimum Withdrawal Benefit (GMWB) rider.

Portfolio (non-guaranteed) options

Guaranteed options

First generation

Income investing

Systematic withdrawal plan (SWP)

Immediate income annuity

Second generation Payout funds “Living benefits” annuity*

The income-solutions marketplace

Other retirement income solutions include:

“DB in DC” deferred annuities, longevity insurance, and reverse mortgages.

> 11

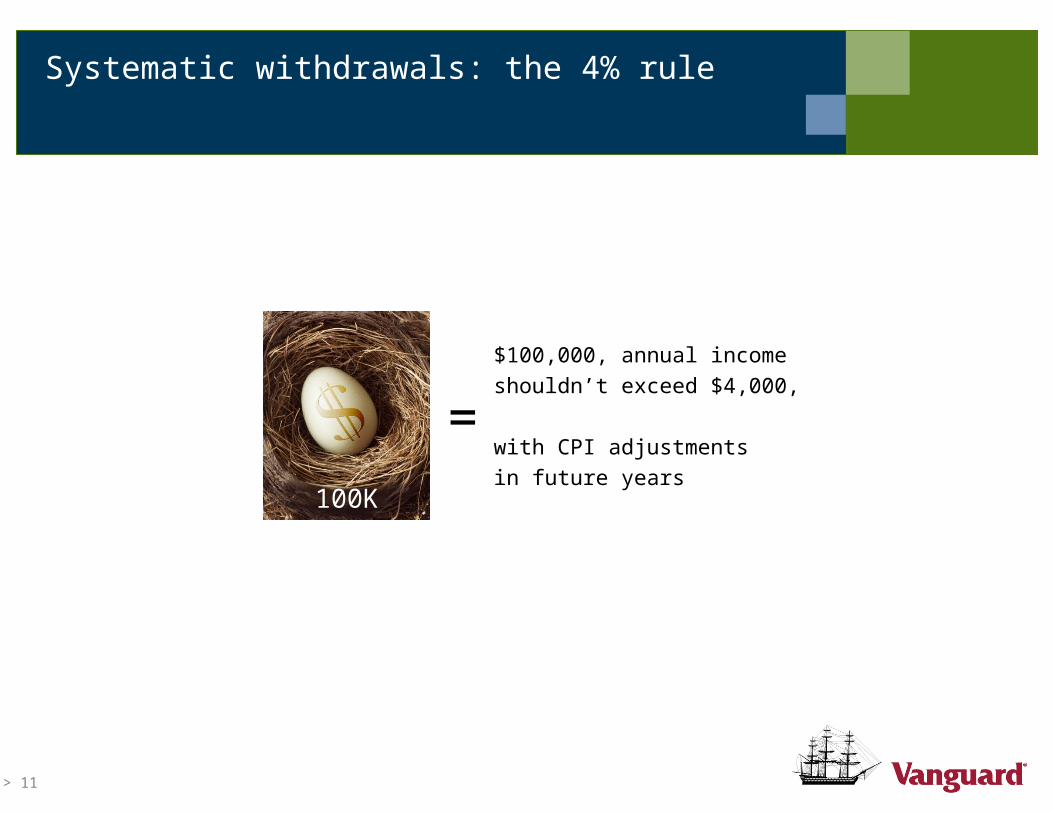

Systematic withdrawals: the 4% rule

$100,000, annual income

shouldn’t exceed $4,000,

with CPI adjustments

in future years

=100K

> 12

Systematic withdrawals and longevity risk

Historic probability of going broke in 30 years

0%

13%

29%

44%

$4,000 $5,000 $6,000 $7,000Initial annual withdraw (plus inflation thereafter)

Source: Vanguard Investment Strategy GroupIMPORTANT: The projections or other information generated by this analysis regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results. Note: This analysis does not consider taxes. Annual returns and inflation for a given asset allocation are based on historic data from 1926 through 2007. Past performance is not a guarantee or a prediction of future results. Stock market returns are for Standard & Poor’s 500 Index from1926 to 1970, the Dow Jones Wilshire 5000 Index from 1971 through April 22, 2005, and the MSCI U.S. Broad Market Index thereafter; bond market returns are based on the Standard & Poor’s High Grade Corporate Index from 1926 to 1968, the Citigroup High Grade Index from 1969 to 1972, the Lehman Long-Term AA Corporate Index from 1973 to 1975, and the Lehman Aggregate Bond Index thereafter. Results may vary with each use and over time.

> 13

Payout funds: A new approach to systematic withdrawals

The investor’s problem• How much from my lump sum should I withdraw? • How do I manage my portfolio in light of my spending? • What are the mechanics of taking out money?

Payout funds: a “do it for me” income program• “SWP in a box”– fund manager oversees payouts • Embedded portfolio strategy – integrated with payout strategy• Monthly distribution payments using distribution mechanics of mutual funds

Two types in United States marketplace• Liquidating – goal is liquidation of account over fixed period (e.g.,10 years)• Endowment – goal is perpetual stream of payments with residual balance

> 14

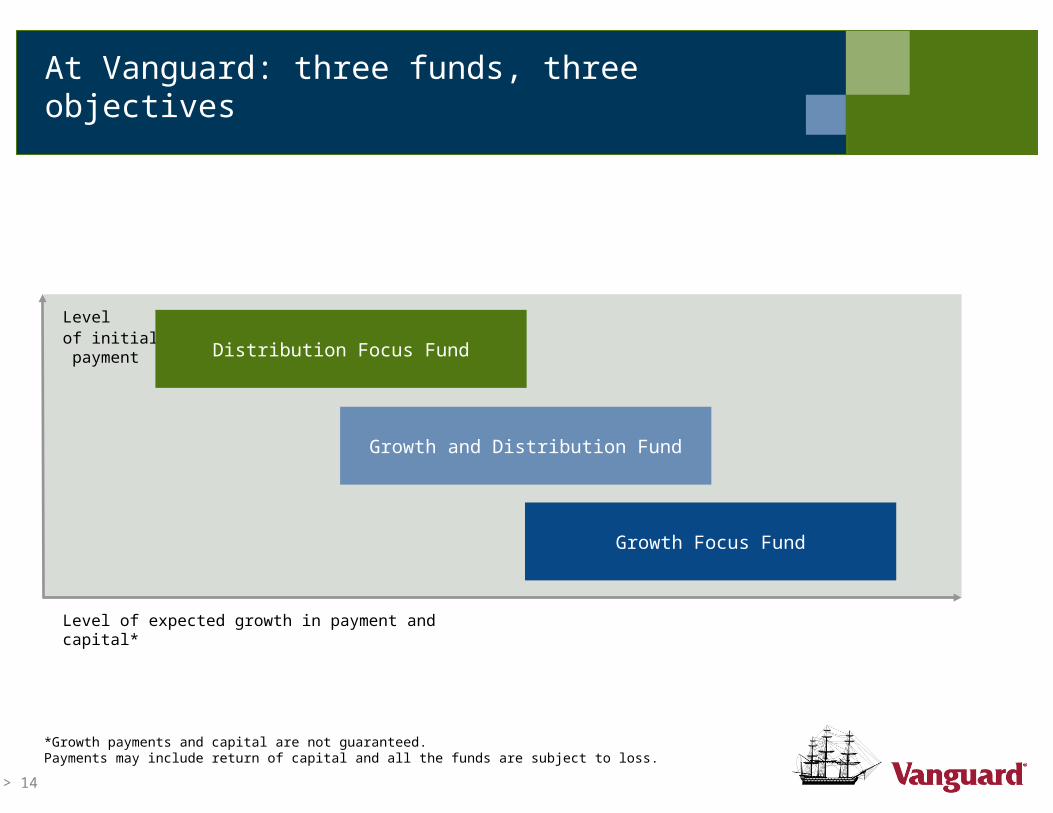

At Vanguard: three funds, three objectives

Level of initial payment

Level of expected growth in payment and capital*

Growth and Distribution Fund

*Growth payments and capital are not guaranteed.Payments may include return of capital and all the funds are subject to loss.

Distribution Focus Fund

Growth Focus Fund

> 15

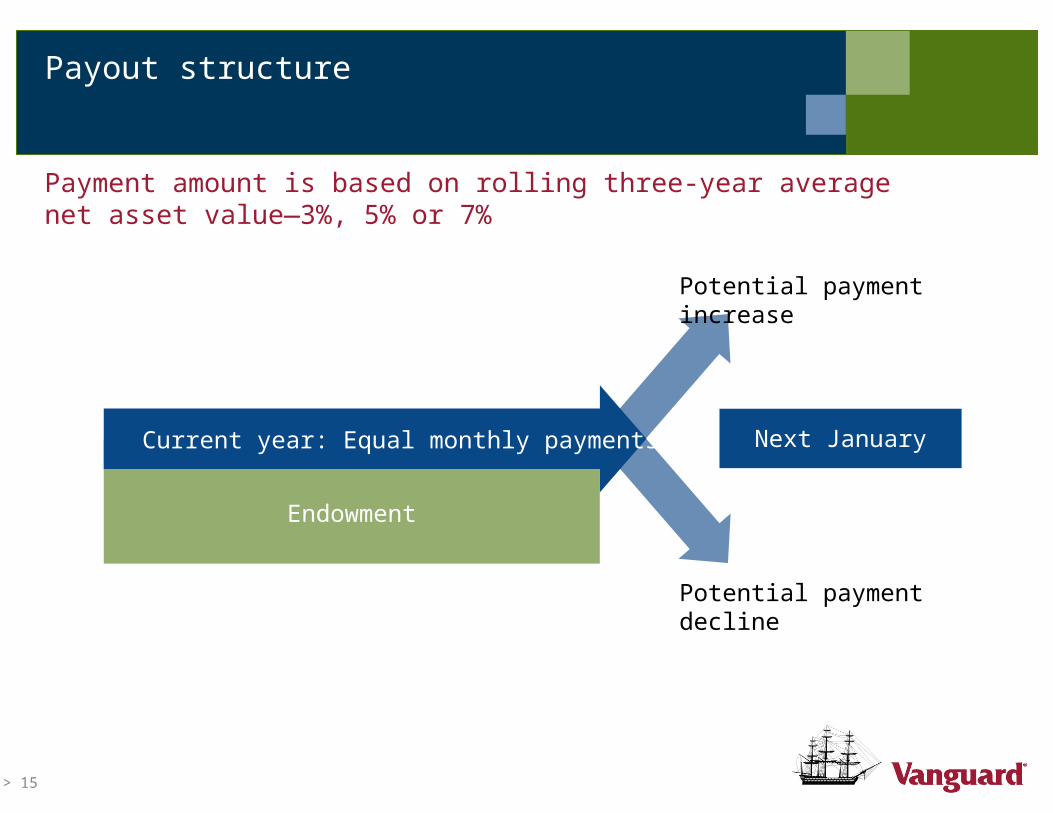

Payout structure

Payment amount is based on rolling three-year average net asset value—3%, 5% or 7%

Next JanuaryCurrent year: Equal monthly payments

Potential payment decline

Endowment

Potential payment increase

> 16

Income annuities

The traditional solution to longevity risk

Annuitypool

Investor B $

Investor A $

Investor C $

$$$ 76

$$$$$$$ 86

$$$$$$$$$$ 96

Pooling benefits • Near-zero longevity risk• Near-zero income risk• Less required savings

…yet negligible adoption

> 17

The living benefit annuity

Age 65 investor $

• 5% for life

• “Ratchets up” in good markets; no downside

• Liquidity at FMV

Balanced fund

VA wrapper

But

• Fees, surrender charges

• Insurer’s hedging skills

> 18

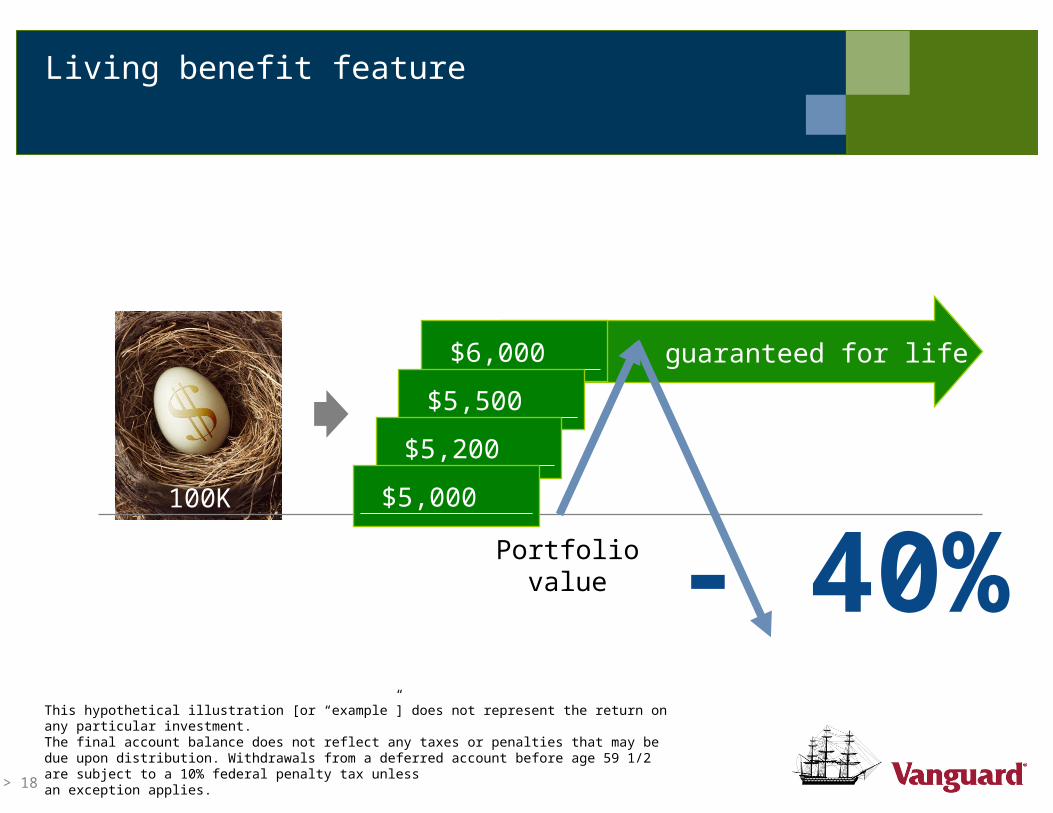

Living benefit feature

guaranteed for life$6,000

$5,500

$5,200

100K

Portfolio value

$5,000

- 40%This hypothetical illustration [or “example”] does not represent the return on any particular investment. The final account balance does not reflect any taxes or penalties that may be due upon distribution. Withdrawals from a deferred account before age 59 1/2 are subject to a 10% federal penalty tax unless an exception applies.

> 19

Perhaps too good to be true?

• Hedging programs were apparently weaker than generally believed

• Providers on the retail side exiting this market–Fidelity, Mass Mutual announcements–Others financially stressed, prices rising

• How do you properly price this product?–Long-term put options not widely available–Dynamic hedges subject to dramatic price swings–Behavioral elements highly uncertain

• Clients will need to be aware that the terms of the deal could change...

> 20

Other income solutions

• Reverse mortgage market – continues at low level of usage

– Is it the right solution only for the house-rich and cash-rich?

• Longevity insurance – still novel product

– Will investors be this far-sighted?

• “DB in DC” – the return of the deferred annuity

– Should participants incur higher costs for a retirement income

“option” they typically don’t exercise?

> 21

Vanguard’s perspective

• Despite all the product development – – No “killer app” – Hybrid solutions may flourish if hedging successful, costs fall– Individual “income allocation” decisions, no universals or defaults

• The in-plan vs. beyond-the-plan dilemma – – Fiduciary decisions– Regulatory constraints– Participant vulnerability

• Education and advice will be key

> 22

Complexity – how many accounts do retirees own?

0%

5%

10%

15%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 ormore

Pe

rce

nta

ge

of r

etir

ee

s

Number of accounts

Source: Vanguard, 2008

Median = 6.0Mean = 6.7

Including both transaction and long-term accounts

> 23

The planner’s perspective

• Not a lack of strategies, but a lack of a framework for decision-making – Need for methodology and process – Need for client communication tools

• Having a robust retirement income plan – more than Social Security and a SWP– Strategic use of annuities?– Payout funds for discretionary income?– New guaranteed options: what role will/should they play?

• The key questions:– How will nonguaranteed investors react in times of volatility?– Will the guarantors be successful with their hedging?

Bottom-line: Striking the right balance between risk, return and cost

> 24

Disclaimers

For more information about Vanguard funds and variable annuity products, visit www.vanguard.com, or call 800-523-1030, to obtain fund and variable annuity contract prospectuses. Investment objectives, risks, charges, expenses, and other important information about the product are contained in the prospectuses; read and consider them carefully before investing.

Annuity guarantees are based on the claims-paying ability of the underlying insurance companies that issue the annuity.

The Managed Payout Funds are not guaranteed to achieve their investment objectives, are subject to loss, and some of their distributions may be treated in part as a return of capital. The dollar amount of a fund’s monthly cash distributions could go up or down substantially from one year to the next and over time. It is also possible for a fund to suffer substantial investment losses and simultaneously experience additional asset reductions as a result of its distributions to shareholders under its managed distribution policy.

An investment in a fund could lose money over short, intermediate, or even long periods of time because each fund allocates its assets worldwide across different asset classes and investments with specific risk and return characteristics. Diversification does not necessarily ensure a profit or protect against a loss in a declining market. The funds are proportionately subject to the risks associated with their underlying funds, which may invest in stocks (including stocks issued by REITs), bonds, cash, inflation-linked investments, commodity-linked investments, long/short market neutral investments, and leveraged absolute return investments.

© 2009 The Vanguard Group, Inc. All rights reserved. Vanguard Marketing Corporation, Distributor.