Embed Size (px)

Citation preview

Retirement Plan Update

September 24, 2015

Patrick McKie, CPA, RPA

• Audit Manager, CBIZ MHM, LLC and Mayer Hoffman McCann P.C.

• Significant experience in a variety of retirement plan audits, including 401(k), 403(b), defined benefit, and 11-K engagements

• Completed the Retirement Plan Associate program sponsored by the International Foundation of Employee Benefit Plans and the Wharton School of Business

• AICPA and PICPA Member

Agenda

• Regulatory Changes– New IRS Revenue Procedures– DOL Audit Quality Study and Proposal to

Congress• New Accounting Pronouncements

– ASU 2015-04: DB Plan Reporting– ASU 2015-07: Investments that Calculate NAV

per Share– ASU 2015-12: Reporting Simplifications

• Other Industry Developments

Regulatory Changes

• US Dept. of the Treasury implements myRA program to encourage retirement savings for workers with no retirement plans offered by employers

• Roth IRA program with no fees investing in variable-rate government securities (avg. return of 3.19%)

• Annual contributions up to $5,500 (+$1k catch-up)• Maximum balance of $15,000; funds then rolled into

a private-sector Roth IRA• Potential lack of interest from employers /

employees

Regulatory Changes – New IRS Rev. Procs.

• RP 2015-6: IRS Determination Letters• RP 2015-27: EPCRS Impovements• RP 2015-28: New EPCRS Correction Methods• RP 2015-36: IRS Opinion and Advisory Letters

– Deadline for application for updated opinion letters extended through October 30, 2015

IRS Revenue Procedure 2015-28

• In 2013, the IRS issued Rev. Proc. 2013-12, which published a comprehensive system of correction programs for operational failures occurring in tax-qualified retirement plans

• IRS received significant feedback that certain correction methods were overly costly and discouraging employers from instituting automatic enrollment features in retirement plans

• In order to increase average participation rates in retirement savings plans, the IRS elected to implement modified correction methods in specific circumstances

IRS Revenue Procedure 2015-28 (continued)

• If a plan sponsor does not properly implement an initial deferral election made by a plan participant, the plan sponsor can avoid paying a QNEC if the election is properly implemented prior to the plan year’s Form 5500 extended due date (or within a month of the participant informing the plan sponsor).

• Plan sponsors have three months to implement changes of other deferral elections without incurring a QNEC

• Failures to implement proper deferral elections within these time periods but under two years qualify for reduced QNEC calculations

IRS Rev. Proc. 2015-28 - Example

• New employee becomes eligible for his employer’s 401(k) plan on January 1, 20X1, and makes a 5% deferral election.

• If this deferral election is not implemented, the plan sponsor has until October 15, 20X2 to implement this election– If the participant informs the plan sponsor, the

election must be implemented by the end of the following month

IRS Rev. Proc. 2015-28 – Example (continued)

• If the 5% deferral election was not implemented timely but discovered within two years, the plan sponsor may correct by paying 25% of any contributions this employee would have made to the plan had the election been implemented timely.

• Corrections outside a two-year window require 50% of missed employee contributions to be paid into the impacted participant’s account.

• The plan sponsor is responsible for paying any missed matching contributions and lost earnings for this period.

• Notice of these corrections is required to be made to the impacted participant.

Department of Labor Audit Quality Study

• The DOL’s Employee Benefits Security Administration (EBSA) conducted a study on the audit quality of 400 employee benefit plan audits for the 2011 plan year.

• 39% of these 400 plan audits were considered to have major deficiencies which failed to meet regulatory standards.

• Failure rate has increased significantly over the past three decades– 1988: 23%; 1997: 19%; 2004: 33%)

• CPA firms that perform less than 25 plan audits annually had a 76% deficiency rate

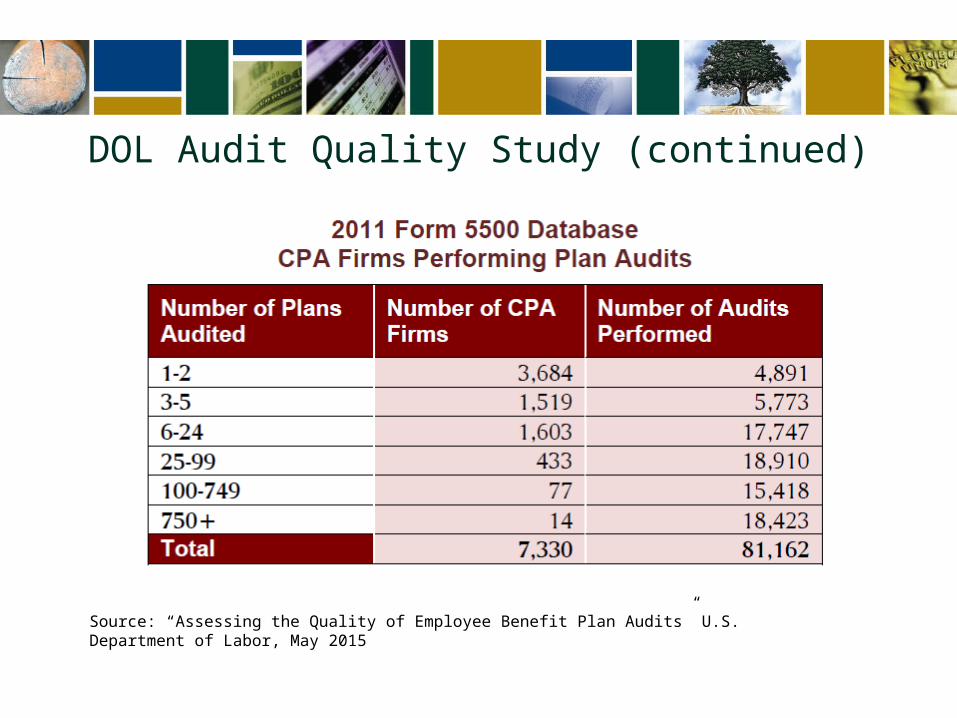

DOL Audit Quality Study (continued)

Source: “Assessing the Quality of Employee Benefit Plan Audits” U.S. Department of Labor, May 2015

DOL Audit Quality Study (continued)

Source: “Assessing the Quality of Employee Benefit Plan Audits” U.S. Department of Labor, May 2015

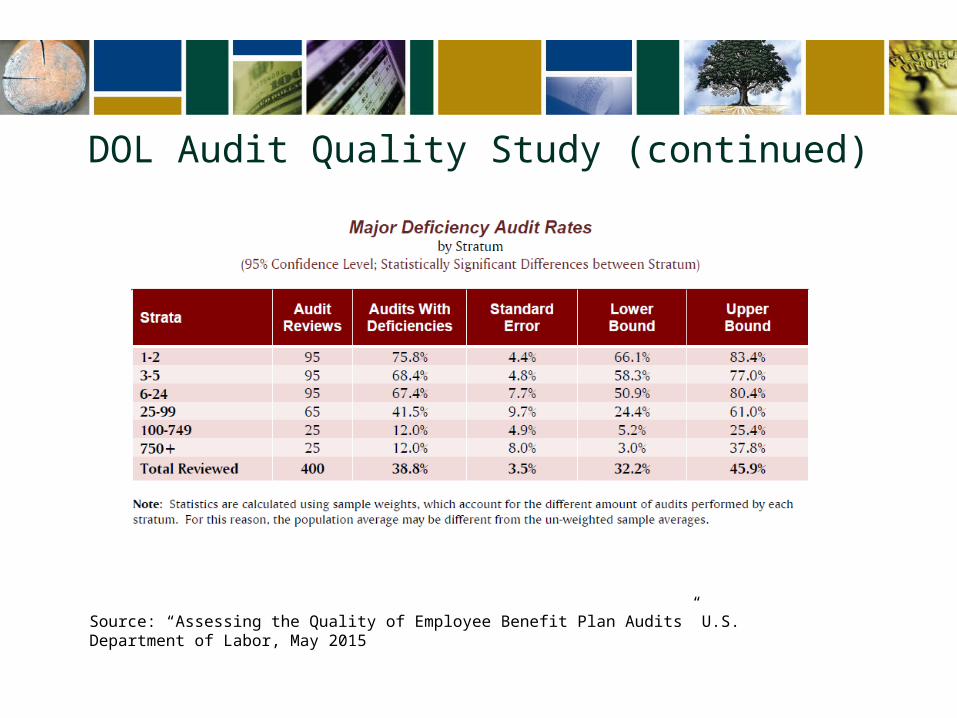

DOL Audit Quality Study (continued)

• Appears that the number of limited-scope audits being performed is contributing to decreased quality

• Plans with deficient audits represented $653 billion of assets at risk

• EBSA concludes that the quality of employee benefit plan audits has not improved, and that the smaller a CPA firm’s benefit plan audit practice, the greater the incidence of audit deficiencies

DOL Audit Quality Study (continued)

• EBSA made the following recommendations (among others) for changes to ERISA:

1. Allow the Secretary of Labor to issue civil penalties of up to $1,100 per day against the accountants performing deficient audits

2. Amend the definition of “qualified public accountant” to include additional requirements and qualifications

3. Allow the Secretary of Labor to establish accounting principles and audit standards specifically for EBP audits

4. Repeal the limited-scope audit exemption

Recent Accounting Pronouncements

• ASU 2015-04: Practical Expedient for the Measurement Date of an Employer’s Defined Benefit Obligation and Plan Assets

• ASU 2015-07: Disclosure for Investments in Certain Entities That Calculate Net Asset Value per Share

• ASU 2015-12: (Part I) Fully Benefit-Responsive Investment Contracts, (Part II) Plan Investment Disclosures, (Part III) Measurement Date Practical Expedient– a/k/a EBP Simplification Rules

Recent Accounting Pronouncements (continued)

• ASU 2015-04 was issued to remediate situations where fiscal-year entities sponsor defined benefit plans which follow calendar-year reporting

• The plan sponsor may use a practical expedient that permits the entity to measure defined benefit plan assets and obligations using the month-end that is closest to the entity’s fiscal year-end

• Practical expedient should be applied consistently year-to-year and for all such plans sponsored by the entity

Recent Accounting Pronouncements (continued)

• ASU 2015-07 removes the requirement to categorize within the fair value hierarchy investments measured using the net asset value (NAV) per share practical expedient

• Also removes the requirement to make certain disclosures for investments measured using the NAV per share practical expedient

• No changes to the basic financial statements• Effective for calendar-year 12/31/16 (public entities) or

12/31/17 (nonpublic entities)

Recent Acc. Pron. – ASU 2015-12• FASB issued a three-part ASU to simplify financial reporting for

benefit plans – Part I: Fully Benefit-Responsive Investment Contracts – Part II: Plan Investment Disclosures – Part III: Measurement Date Practical Expedient

• Developed by the Emerging Issues Task Force (EITF) – Responded to advocacy efforts by the AICPA’s Employee Benefit

Plans Expert Panel – Identified the issues affecting a large number of plans with the

goal of completing a project within a short period of time • Effective for fiscal years beginning after December 15, 2015

– Early application is permitted – Plans can early adopt any of the ASU’s three parts without early

adopting the other parts

Source: Accounting Standards Update (ASU) 2015-12, AICPA, 8/25/15

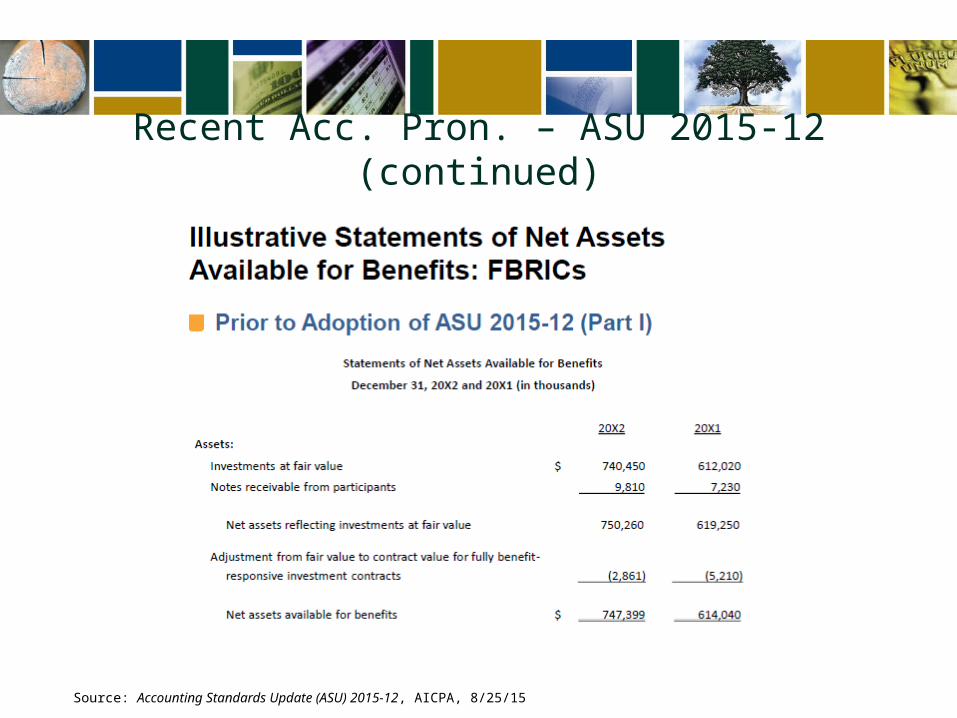

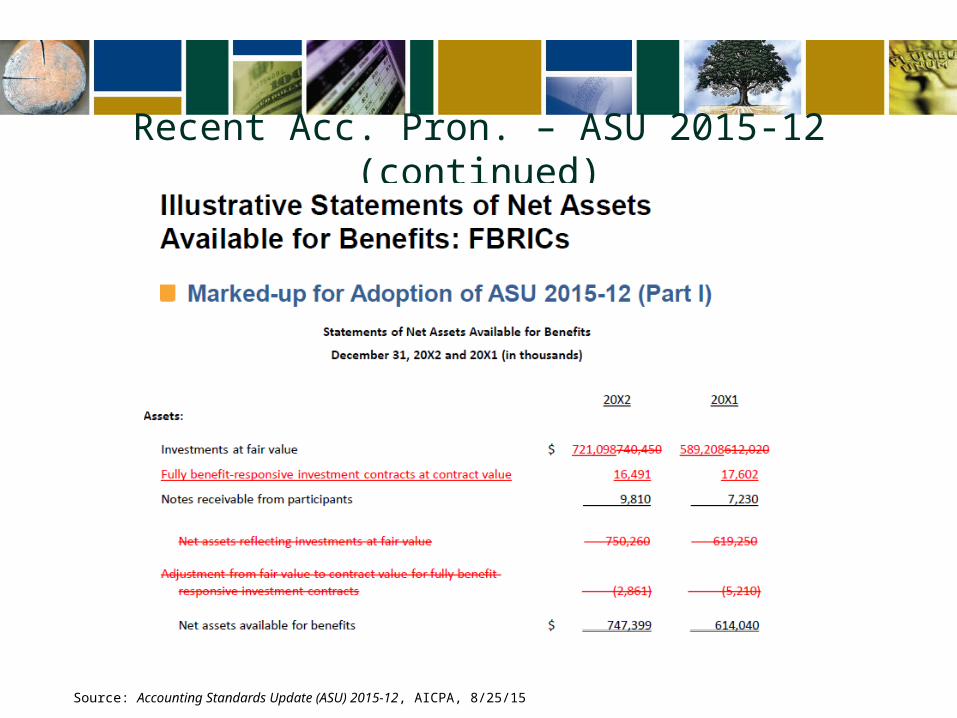

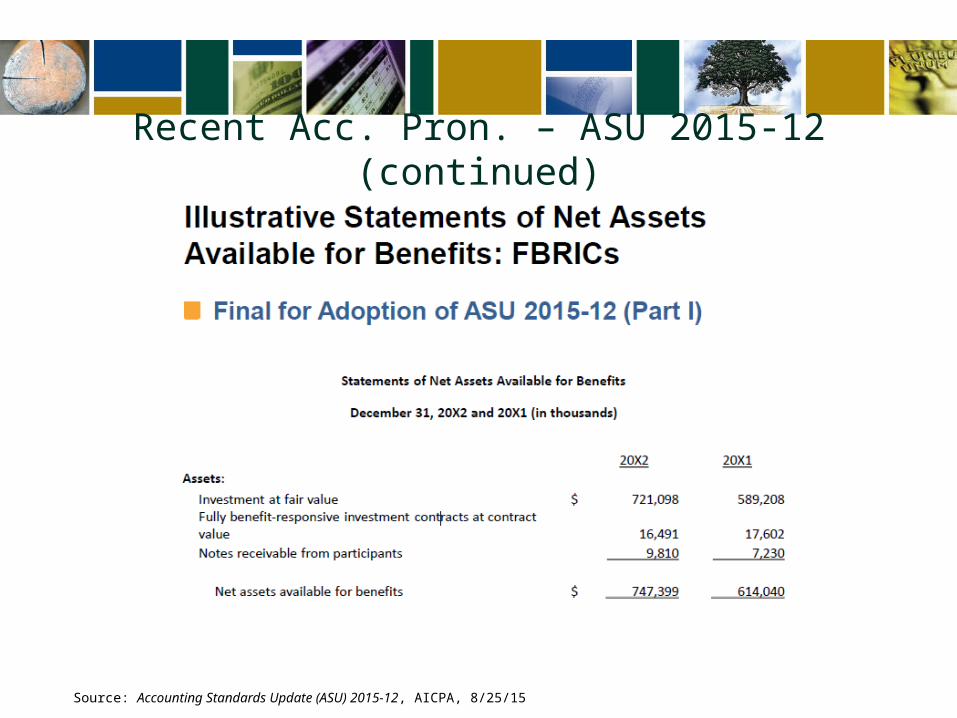

Recent Acc. Pron. – ASU 2015-12 (continued)

• Eliminates requirements to measure fair value and present related fair value measurement disclosures– Responds to concerns about the cost and effort required to

measure the fair value of FBRICs when fair value is not the relevant measure

• Instead, plans will present FBRICs at contract value in the statement of net assets available for benefits, either as – Investments at contract value – Fully benefit-responsive investment contracts at contract value

• Responds to concerns about the cost and effort required to measure the fair value of FBRICs when fair value is not the relevant measure

Source: Accounting Standards Update (ASU) 2015-12, AICPA, 8/25/15

Recent Acc. Pron. – ASU 2015-12 (continued)

Source: Accounting Standards Update (ASU) 2015-12, AICPA, 8/25/15

Recent Acc. Pron. – ASU 2015-12 (continued)

Source: Accounting Standards Update (ASU) 2015-12, AICPA, 8/25/15

Recent Acc. Pron. – ASU 2015-12 (continued)

Source: Accounting Standards Update (ASU) 2015-12, AICPA, 8/25/15

Recent Acc. Pron. – ASU 2015-12 (continued)

Source: Accounting Standards Update (ASU) 2015-12, AICPA, 8/25/15

• Guidance clarifies that indirect investments in FBRICs through investment companies (e.g., stable value CCTs) are not in the scope of the FBRIC guidance – Plans should report these investments at fair value – These funds typically qualify for measuring fair value using the

net asset value (NAV) practical expedient – The amount previously presented as contract value is now

presented as fair value

Recent Acc. Pron. – ASU 2015-12 (continued)

Source: Accounting Standards Update (ASU) 2015-12, AICPA, 8/25/15

• ASU 2015-07 Disclosures for Investments in Certain Entities That Calculate Net Asset Value per Share (or Its Equivalent) – Eliminates the requirement to categorize investments measured

at fair value using the NAV practical expedient in a hierarchy level

• Investments presented at contract value (e.g., FBRICs) are not included in the hierarchy table

• Underlying securities of a synthetic investment contract are not included in the hierarchy table

Recent Acc. Pron. – ASU 2015-12 (continued)

Source: Accounting Standards Update (ASU) 2015-12, AICPA, 8/25/15

• Part II: Plan Investment Disclosures – Affects all types of plans – Simplifies the level of disaggregation for investments

measured using fair value • Disaggregate by general type of investment (e.g., common stocks, corporate

bonds, mutual funds) • Plans are exempt from the requirements of ASC 820-10-50-2B to

disaggregate assets by class (e.g., nature, characteristics, risks) • Disclosure of fair value information required by ASC 820 shall be provided

by general type rather than class (e.g., valuation techniques, inputs, level 3 reconciliation)

• Self-directed brokerage accounts are one general type • Applies to investments held in a master trust • Provides consistency with the level of disaggregation provided by most

trustees, custodians and insurance companies and with the information required in Form 5500

Recent Acc. Pron. – ASU 2015-12 (continued)

Source: Accounting Standards Update (ASU) 2015-12, AICPA, 8/25/15

• Disclosure simplifications – No longer required: the significant investment strategies for an

investment in a fund that files an annual report on Form 5500 as a direct filing entity when the plan measures that investment using the NAV practical expedient

– Eliminates the requirement to disclose the net appreciation or depreciation in fair value of investments by general type • Instead, plans only need to disclose this amount in the

aggregate – Plans are no longer required to disclose individual investments

with a value equal to or greater than 5% of net assets available for benefits

– Applies to investments held in a master trust • ASU is to be applied retrospectively

Recent Acc. Pron. – ASU 2015-12 (continued)

Source: Accounting Standards Update (ASU) 2015-12, AICPA, 8/25/15

• Part III: Measurement Date Practical Expedient – Simplifies accounting for a plan with a fiscal year end (FYE) that doesn’t

coincide with a calendar month end – Added to the project as a result of a similar practical expedient that the

FASB recently issued for employers with FYEs that don’t end at the end of a calendar month (ASU 2015-04)

– Allows a plan to measure its investments and investment-related accounts using the month end closest to its FYE (i.e., an alternative measurement date)

• Disclose as an accounting policy • Disclose financial effects of contributions, distributions and/or significant

events that occur between the alternative measurement date and the plan’s fiscal year end

• Apply consistently year to year – ASU to be applied prospectively

Other Industry Developments

• The retirement plan marketplace has seen numerous court cases stemming from the market risk of investments, fee structures, and other plan governance issues.

• ERISA attorneys are scrutinizing public information on retirement plans to determine if governance responsibilities are being performed appropriately

• Various companies mine the information uploaded to the Department of Labor’s EFAST system and publish statistics for comparison to other plans / industry standards (Brightscope.com)

Other Industry Developments - Litigation

• Tibble v. Edison International Inc.– Class-action suit that the 401(k) plan paid excess fees

compared to those charged to other plans of similar size, industries, etc., and that investment monitoring responsibilities were not performed

– Supreme Court allowed charges outside a six-year statute of limitations from when the investments were purchased

– Conclusion pending– New suit being filed over common stock valuation and

lack of public disclosures

Other Industry Developments – Litigation (continued)

• Abbott v. Lockheed (Martin)– $62 million settlement on behalf of plan participants– Breach of fiduciary duties under ERISA; imprudent

management of retirement savings due to excessively high investment and record keeping fees

– Lockheed has also agreed to perform monthly evaluations on investments and must receive bids from three third-party record keeping services

• Haddock v. Nationwide– $140 million settlement on behalf of trustees of five

employer-sponsored defined contribution plans– Alleged:

• Revenue-sharing agreements with third-party mutual fund companies results in losses to the plans and breaches of fiduciary duties under ERISA

• Investments in outside mutual funds with high management fees to maximize “undisclosed kickbacks”

– 13 years of litigation before settlement was reached

Other Industry Developments – Litigation (continued)

Other Industry Developments - HTFA

• On August 8, 2014, the Highway and Transportation Funding Act of 2014 (HTFA) was signed into law.

• Extends pension funding relief originally provided under MAP-21, a transportation funding bill from 2012

• Allows use of higher interest rates when calculating plan liabilities, which translates into reduced funding requirements from plan sponsors

• Allowable interest rates will continue to increase through 2020 when these provisions will expire

• Commonly referred to as “pension smoothing”

QUESTIONS & ANSWERS

Patrick McKie, CPA, RPA

p: 610-862-2329

![Attracts and holds heavy objects with 1000 · 16 MHM-A1612 25 MHM-A2512 32 MHM-A3212 50 MHM-A5012 Pad Bore size [mm] Part number 16 MHM-A1613 25 MHM-A2513 32 MHM-A3213 50 MHM-A5013](https://img.pdfslide.net/doc/110x75/5f0548b87e708231d4123317/attracts-and-holds-heavy-objects-with-1000-16-mhm-a1612-25-mhm-a2512-32-mhm-a3212.jpg)