Embed Size (px)

Citation preview

Revenue Cycle Impacts of Disruption

WE WON’T BE BORED

1

“Signs of Disruption in the Revenue Cycle”

• What are three C’s that keep CFO’s up at night? Compliance? Cash flow? Customer service? Cybersecurity? Complaints? Competition? HINT: How about Cash flow, Customer service and CRAP… yep, just CRAP!!

• Or Claims Requiring Additional Processing/CRAP!

• Instead of ‘without margin there is no mission.’ How about re-thinking the new world of revenue cycle.

MISSION DRIVES MARGIN

DEMONSTRATING MISSION WILL ENSURE MARGIN

“I am worried about the cost of my healthcare; not the cost ofhealthcare.” It is always personal.

2

What is Disruption?

• Maybe new catch phrase

• Maybe just change. But with more significant impact.

• Maybe complete re-thinking of healthcare delivery

• Maybe the patients are confused with all the new words we use

• Maybe the payers are implementing their own form of disruption

• Maybe anyone throws out the word to cover up for something else

• Or maybe it is a dynamic opportunity to reach out – to our patients, our communities, our payers and be the LEADER.

3

Patient – New Medicare Cards- no longer SS#

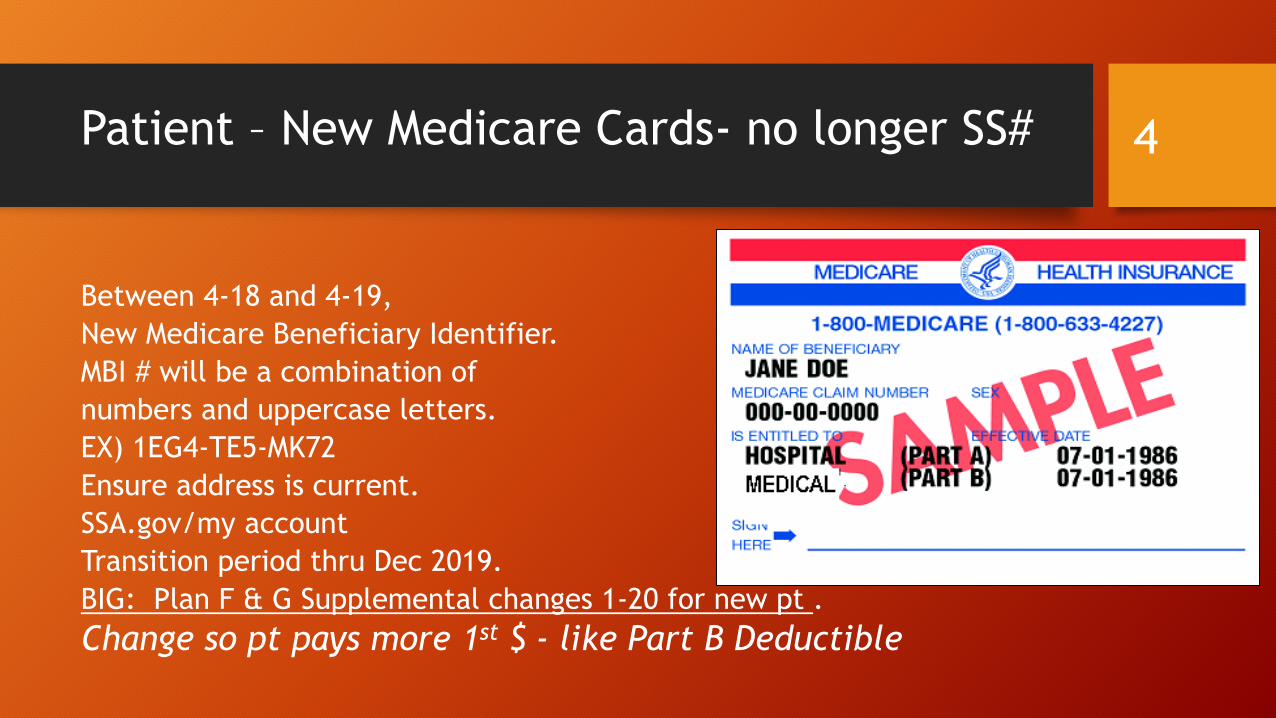

Between 4-18 and 4-19,

New Medicare Beneficiary Identifier.

MBI # will be a combination of

numbers and uppercase letters.

EX) 1EG4-TE5-MK72

Ensure address is current.

SSA.gov/my account

Transition period thru Dec 2019.

BIG: Plan F & G Supplemental changes 1-20 for new pt .

Change so pt pays more 1st $ - like Part B Deductible

4

Patient Impact- Convenient Care Movement & Contracts impacting patients

• Access ‘healthcare’ thru social media

• Research their own healthcare needs – internet

• Insurance directed care vs physician directed care..

• EX) Physician orders care. Payer denies as ‘not medically necessary.’ Catch phrase for multiple denials – broad and difficult to challenge. No payment from the payer.

• Closed Networks – payer/provider specific services

• Out of Network/OON= significant financial impact

• EX) Penalty: Two distinct deductibles due, plus full billed charges. (No contract between payer and provider = no reduction in charges.)

• 20% of all inpts had to deal with out of network – ER providers, reference labs, etc. 8-18

• Congress urges Federal Trade Commission to investigate anti-competitive provisions in payer/hospital contracts. Such as anti-steering restrictions to keep from going to lower cost providers. 10-18

5

More ‘hot off the press- CDI”(Clinical documentation integrity)

Integra filed a False Claims Act lawsuit Aug 10th in the US District Court of

Central CA against Providence Health & Services. The lawsuit allege

Providence routinely used unwarranted major complications and comorbidity

secondary codes on Medicare claims to inflate reimbursement.

According to the 100-pg lawsuit, Integra discovered the unwarranted

secondary codes during an analysis of Medicare claims dated back to 2011.

Integra said an investigation of the business practices of Providence and its

consultant, clinical documentation improvement company, JA Thomas &

Associates, confirmed that Providence’s false Medicare claims were not only

intentional but were part of a systematic effort to boost its Medicare revenue.

Pushed doctors to make unwarranted dx and used leading queries.

6

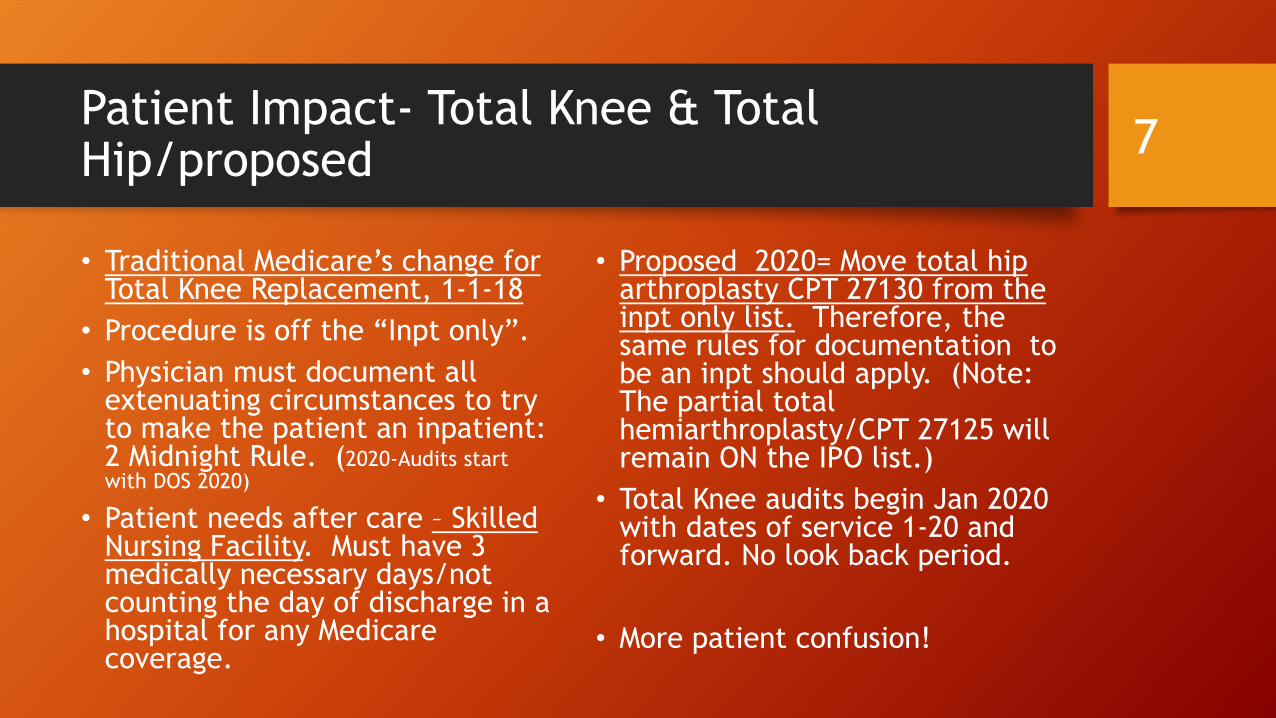

Patient Impact- Total Knee & Total Hip/proposed

• Traditional Medicare’s change for Total Knee Replacement, 1-1-18

• Procedure is off the “Inpt only”.

• Physician must document all extenuating circumstances to try to make the patient an inpatient: 2 Midnight Rule. (2020-Audits start with DOS 2020)

• Patient needs after care – Skilled Nursing Facility. Must have 3 medically necessary days/not counting the day of discharge in a hospital for any Medicare coverage.

• Proposed 2020= Move total hip arthroplasty CPT 27130 from the inpt only list. Therefore, the same rules for documentation to be an inpt should apply. (Note: The partial total hemiarthroplasty/CPT 27125 will remain ON the IPO list.)

• Total Knee audits begin Jan 2020 with dates of service 1-20 and forward. No look back period.

• More patient confusion!

7

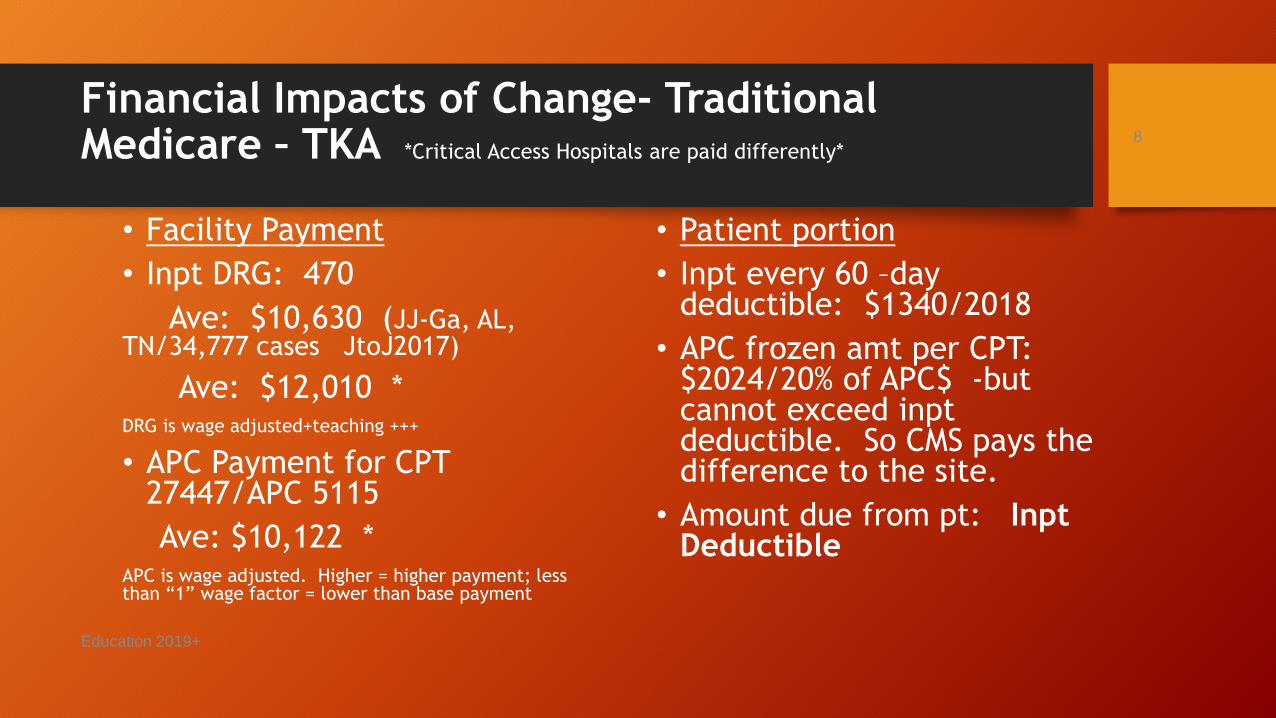

Financial Impacts of Change- Traditional Medicare – TKA *Critical Access Hospitals are paid differently*

• Facility Payment

• Inpt DRG: 470

Ave: $10,630 (JJ-Ga, AL, TN/34,777 cases JtoJ2017)

Ave: $12,010 *DRG is wage adjusted+teaching +++

• APC Payment for CPT 27447/APC 5115

Ave: $10,122 *APC is wage adjusted. Higher = higher payment; less than “1” wage factor = lower than base payment

• Patient portion

• Inpt every 60 –day deductible: $1340/2018

• APC frozen amt per CPT: $2024/20% of APC$ -but cannot exceed inptdeductible. So CMS pays the difference to the site.

• Amount due from pt: InptDeductible

Education 2019+

8

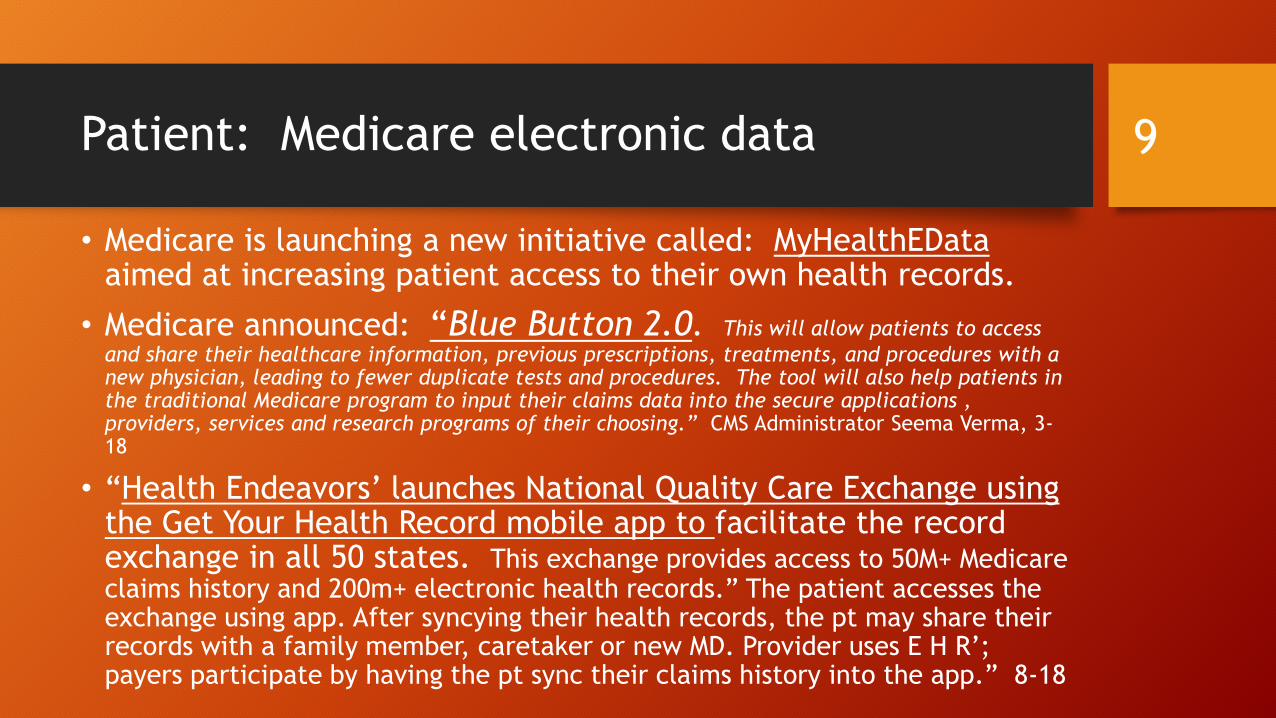

Patient: Medicare electronic data

• Medicare is launching a new initiative called: MyHealthEDataaimed at increasing patient access to their own health records.

• Medicare announced: “Blue Button 2.0. This will allow patients to access

and share their healthcare information, previous prescriptions, treatments, and procedures with a new physician, leading to fewer duplicate tests and procedures. The tool will also help patients in the traditional Medicare program to input their claims data into the secure applications , providers, services and research programs of their choosing.” CMS Administrator Seema Verma, 3-18

• “Health Endeavors’ launches National Quality Care Exchange using the Get Your Health Record mobile app to facilitate the record exchange in all 50 states. This exchange provides access to 50M+ Medicare claims history and 200m+ electronic health records.” The patient accesses the exchange using app. After syncying their health records, the pt may share their records with a family member, caretaker or new MD. Provider uses E H R’; payers participate by having the pt sync their claims history into the app.” 8-18

9

More on MyHealthEData & Interoperability (means?) 2019 Final PPS rule

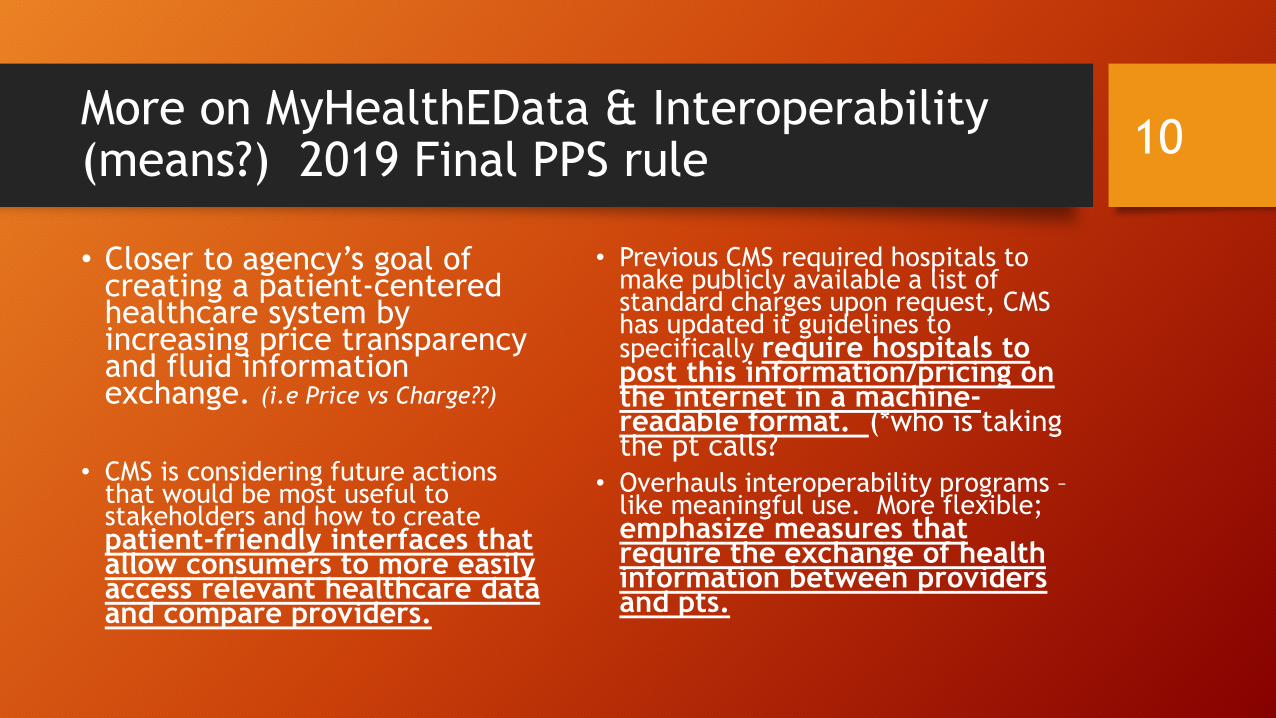

• Closer to agency’s goal of creating a patient-centered healthcare system by increasing price transparency and fluid information exchange. (i.e Price vs Charge??)

• CMS is considering future actions that would be most useful to stakeholders and how to create patient-friendly interfaces that allow consumers to more easily access relevant healthcare data and compare providers.

• Previous CMS required hospitals to make publicly available a list of standard charges upon request, CMS has updated it guidelines to specifically require hospitals to post this information/pricing on the internet in a machine-readable format. (*who is taking the pt calls?

• Overhauls interoperability programs –like meaningful use. More flexible; emphasize measures that require the exchange of health information between providers and pts.

10

Patient Impact Potential Changes

• HHS Sec Azar ‘mulls ‘ change to HIPAA privacy that impedes the ability of doctors, hospitals and payers to coordinate better delivery at lower costs. Exploring changes to the Federal Privacy act that protects privacy of substance abuse and mental health who seek treatment in federal assisted programs. 8-18

• “American Patients First” – Gag clauses would no longer be acceptable. Congress passed legislation banning the clauses and signed into law 10-18. Pharmacist can show difference in pricing between using insurance and cash payment.

• Hey, United is creating their own Individual Health Records/IHR 11-18 Accessible by 50 M patients. Create their own data base. States it will interface with hospitals E HR. Cost to make this happen? Using/sampling with ACOs.

Stats on Privacy concerns:

• 49% of adults are very concerned about health information security.

• 36% currently use online portal to access health information

• Those aged 35+ are more likely to use a portal than those aged 18-34. (39% to 28%)

• 31% of adults are most concerned about diagnosis diseases being shared. (SCOUT survey, Cision, 7-25-18)

• “Hackers demand more than $1M in bitcoin from Washington Hospital. Grays Harbor Hospital and 8 clinics. Older system in hospital; newer in clinics. 8-19

11

Patients – Healthcare perceptions – the challenges of the healthcare community to ‘meet the need.”New ‘words’ in healthcare but means what to the community? Population health, Volume vs Value, etc.

• EBRI March 2018• More likely to have a Primary care provider:

• 85% Baby boomers• 78% Gen Xers • 67% Millennials *Think CVS, Walgreens,

Walmart, Apple, Amazon, employers*

Much more likely to use walk-in clinics:• 14 % Baby boomers• 18% GenX• 30% Millennials

• Much more interested in Telemedicine: Not the Jetsons but…• 19% Baby boomers• 27% GenX• 40% Millennials

Much more likely to research healthcare options:• 31% Baby boomers• 34% GenX• 51% Millennials

Generational Different Approaches to Healthcare - CHALLENGE

12

“Virtual Care moves to the frontline of provider-patient relationships.” Healthcare Dive 5-18

• Kaiser Permanente and United Healthcare are using telehealth for primary care visits and quick patient consultations.

• Using for primary care appts and quick consultations. Ease-no time off work. (Think diabetes. Also pts reach out to the provider with results, etc.)

• Hold potential to improve quality, cut costs and improve accessibility to specialty services. Recent Accenture report = 70% of consumers are interested in virtual healthcare. Only 20% have actually received it.

• Kaiser: grown to more than ½ of their 100M encounters. Big: paid a per member per month for their 11.7M members. 95% are covered thru a capitated program. Makes engaging physicians easier - no payment for volume.

• ++1 in 4 organization –remote pt monitoring improved patient satisfaction.

• ++38% say it reduced hospital admissions.

• ++1 in 4 say – decreased ER visits. (Becker Review/KLAS research 10-19)

13

CMS advocating Comparisons of charges. 11-18

• JAMA Internal Medicine Study/9-18 = Only 21% of hospitals had the ability to provide a complete hospital price estimate for a common procedure.

• CMS has created an online pricing comparison tool for outpt procedures. Part of Exec Order to Increase Choice and Reduce Cost.

• Medicare.gov. It compares average prices for a procedure in BOTH ambulatory surgery centers and outpt hospital departments.

• EX) Input name= Release and/or relocation of median nerve of hand.

Pt pays: $157 ASC or $322 in hospital Medicare pays: $628 ASC vs $1289 in outpt hospital.

• Disclaimers: no physician fees are included, treatment may include additional procedures, ask your doctor.

14

More Patient Engagement- Protecting Patients from Surprise Billing (Arbitration 7-19)

• CMS – Proposed legislation: “No More Surprise Medical Bills Act” The bill would create a ‘binding arbitration’ process to determine the appropriate provider payment rate in surprise OUT –OF-NETWORK scenarios. ( survey: 39% surprise bill, 1 in 6 ER visits)

• Defined as: when seeking care from IN- NETWORK but providers who provided services where the pt would not know were out of network. Limit pt’s cost sharing to the amt the pt would owe to an in-network provider and prohibit providers from engaging in balance billing…

• EX) Pt went to in-network hospital. But the ER providers nor the consultant cardiologist were in their network. Most plans – pt ends up paying full billed charges. (No discounting as no contract)

• Debated: Who pays up to the in-network amount? Payer? Provider? All about protecting the patient –but no consensus. (7-19)

15

Unfortunately, more on surprise billing

• “Frequency and price tags on surprise medical bills for emergency and inpt services at in-network hospitals is on the rise”, according to a published study in JAMA. 8-19

• Percentage of ER visits resulting in surprise bills jumped to 32.3% in 2010 to 42.8% in 2016 while the increase for inpt admissions went from 26.3% to 42%. (Think specialists/consultants. Think radiology interps. Think reference lab send outs. Are they all in the same networks as the hospital? Why not?)

• Kaiser Family Foundation has found about 40% have reported receiving an expected out of network bill.

• Congress has multiple ideas to deal with - none are acceptable to the insurance payers, providers /doctors and hospitals and yes – where is the pt in all these decision-making lobbies? What is the plan forward for the unknowing patients?

16

Patient’s Getting the Contracted/Allowable per CPT - Major challenge

• Pricing Transparency – means?

• “Interoperability and pricing transparency could move us closer to true value-based care.” Anne Phelps, Deloitte & Touche, LLP

• Patients out of pocket has continued to be a high stress factor due to the high deductibles. (50% now have one. $3500 per person)

• Can your patients get both an estimated of billed charges and the allowable/contracted amount from the in-network payer? Not possible in most cases. How can you be an engaged shopper?

• Pres Trump’s Executive Order – force all providers to publish their contracted terms. WOW! But is this a reaction to the above?

17

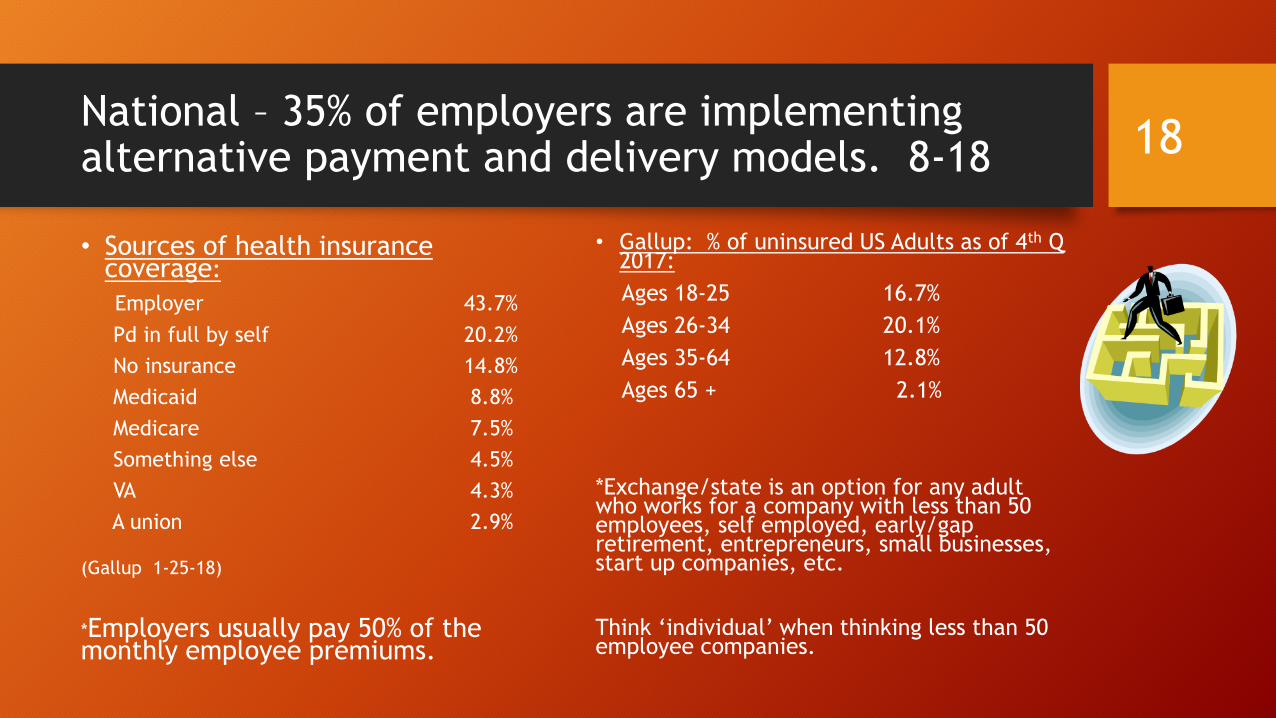

National – 35% of employers are implementing alternative payment and delivery models. 8-18

• Sources of health insurance coverage:

Employer 43.7%

Pd in full by self 20.2%

No insurance 14.8%

Medicaid 8.8%

Medicare 7.5%

Something else 4.5%

VA 4.3%

A union 2.9%

(Gallup 1-25-18)

*Employers usually pay 50% of the monthly employee premiums.

• Gallup: % of uninsured US Adults as of 4th Q 2017:

Ages 18-25 16.7%

Ages 26-34 20.1%

Ages 35-64 12.8%

Ages 65 + 2.1%

*Exchange/state is an option for any adult who works for a company with less than 50 employees, self employed, early/gap retirement, entrepreneurs, small businesses, start up companies, etc.

Think ‘individual’ when thinking less than 50 employee companies.

18

Trustee report on Social Security and Medicare ‘financial health.’ 6-19

• Social Security/SS– Becomes insolvent in 2034. Same as last year.

• By 2035, 77% of benefits payable then.

• 62 M retirees, disabled workers, spouses and surviving children.

• Ave payment is $1294

• By 2030, 1 in 5 over 65.

• Medicare –Becomes insolvent in 2026- 3 yrs earlier than previously forecast. Inpt/Part A care won’t be able to cover projected bills. (Tax based)

• Part B and Part D are solvent for 10 years and beyond. (Premium)

• SS drain has begun: higher expenditures than revenue collected for the first time since 1982. By 2034, the excess will be completely gone. Resulting in 21% cut to benefits.

19

How many Srs are still working past retirement age?

• Only about ½/50% of all employees are covered by a retirement plan.

• Recent study by Bankrate.com:• 70 % of non-retired Americans plan to work as long as possible during

retirement.

• 2% say they have NO plans to work during retirement.

• Of those who plan to work as long as possible, 38% say its because they like to work, 35% need the money, and 27% say it’s a mix.

• Largest # of working after retirement since 1965.

• Medicare as Secondary payer – after age 65 – but still working and covered by major commercial insurance. (Baby boomers = major $ hit. Move from Commercial to Medicare.)

20

Patients - Cost

• Affordable Care Act – mandated 10 essential benefits, no allowance to limit coverage due to pre-existing conditions, no rating a patient based on health history, no lifetime limits, coverage of children thru age 26, insurance required for employers with over 50 employees.

• Allowed for Subsidies for lower income adults who could not afford premiums in the healthcare exchanges/individual and gap coverage.

• Continued problematic conversations regarding funding of the Cost Sharing Subsidies/CSR. Tax funds paid to insurance companies to be made ‘whole’ as premiums are reduced for the subscriber. Unclear of path forward.

• Premiums continue to be a primary area of concern! ***92% businesses under 20 employees. How are they getting insurance?

• 2019 Budget – ‘Trumps budget calls for ACA repeal , cuts to Medicare and Medicaid”

21

Copyright © 2011-2019 Appeal Academy – All Rights Reserved 22

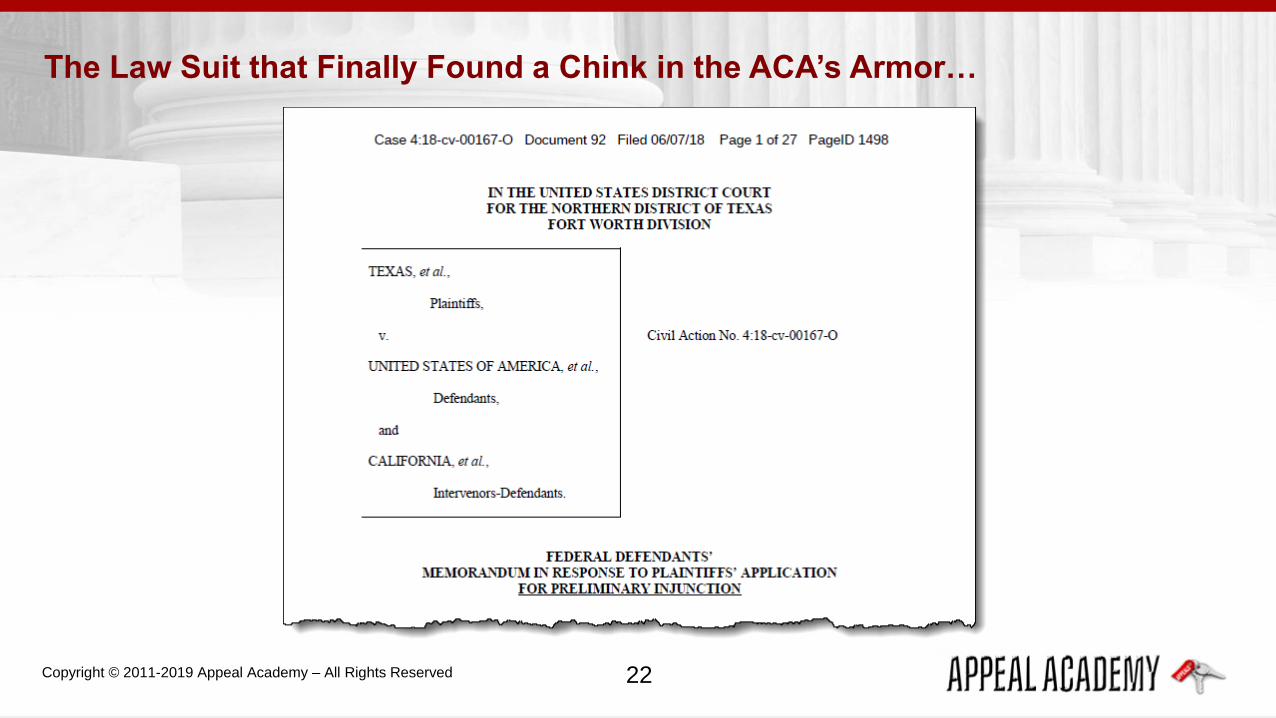

The Law Suit that Finally Found a Chink in the ACA’s Armor…

Copyright © 2011-2019 Appeal Academy – All Rights Reserved 23

…The Judge allowed for the ACA to stay in effect… for who knows how long

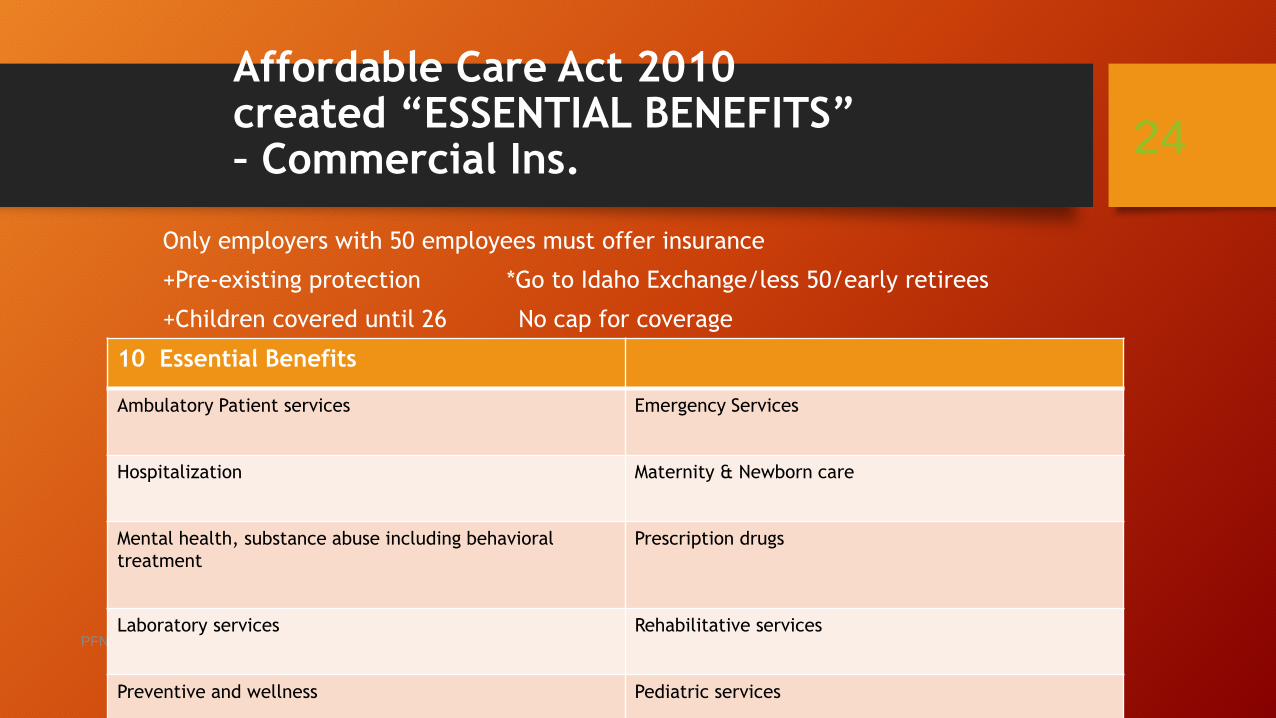

Affordable Care Act 2010created “ESSENTIAL BENEFITS” – Commercial Ins.

Only employers with 50 employees must offer insurance

+Pre-existing protection *Go to Idaho Exchange/less 50/early retirees

+Children covered until 26 No cap for coverage

PFNF Education 2017

24

10 Essential Benefits

Ambulatory Patient services Emergency Services

Hospitalization Maternity & Newborn care

Mental health, substance abuse including behavioral

treatment

Prescription drugs

Laboratory services Rehabilitative services

Preventive and wellness Pediatric services

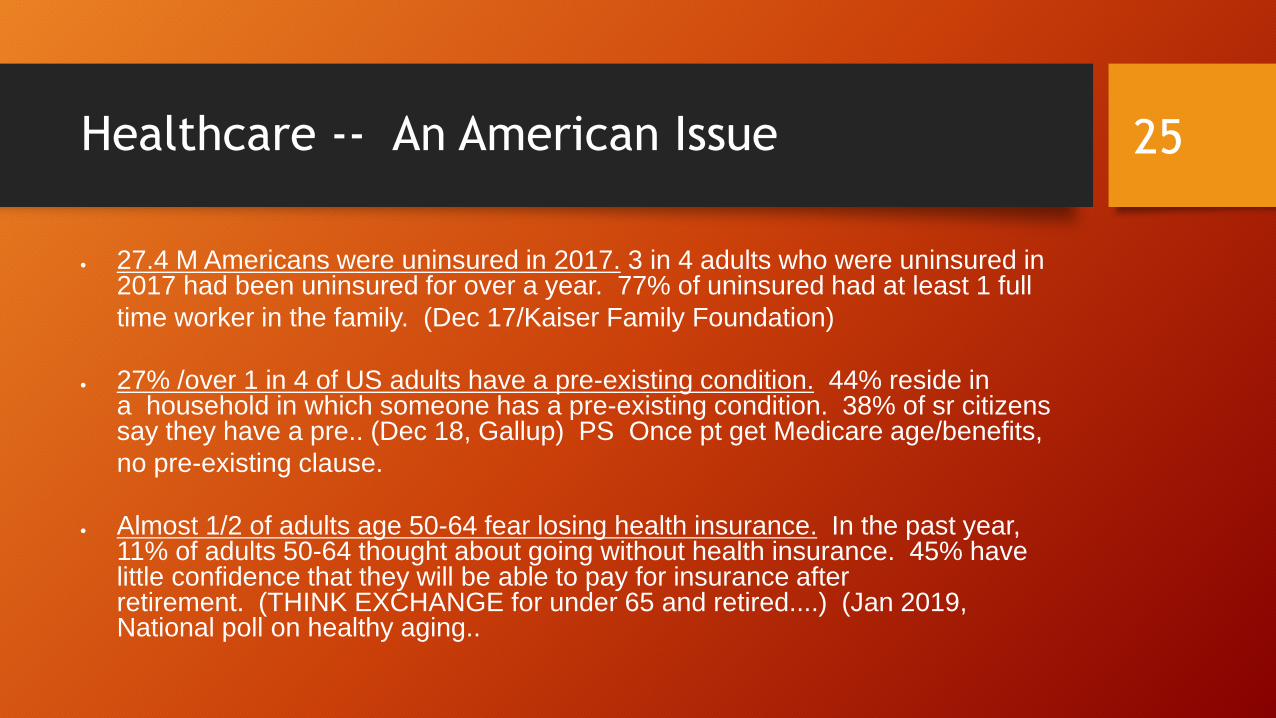

Healthcare -- An American Issue

27.4 M Americans were uninsured in 2017. 3 in 4 adults who were uninsured in 2017 had been uninsured for over a year. 77% of uninsured had at least 1 full

time worker in the family. (Dec 17/Kaiser Family Foundation)

27% /over 1 in 4 of US adults have a pre-existing condition. 44% reside in a household in which someone has a pre-existing condition. 38% of sr citizens say they have a pre.. (Dec 18, Gallup) PS Once pt get Medicare age/benefits,

no pre-existing clause.

Almost 1/2 of adults age 50-64 fear losing health insurance. In the past year, 11% of adults 50-64 thought about going without health insurance. 45% have little confidence that they will be able to pay for insurance after retirement. (THINK EXCHANGE for under 65 and retired....) (Jan 2019, National poll on healthy aging..

25

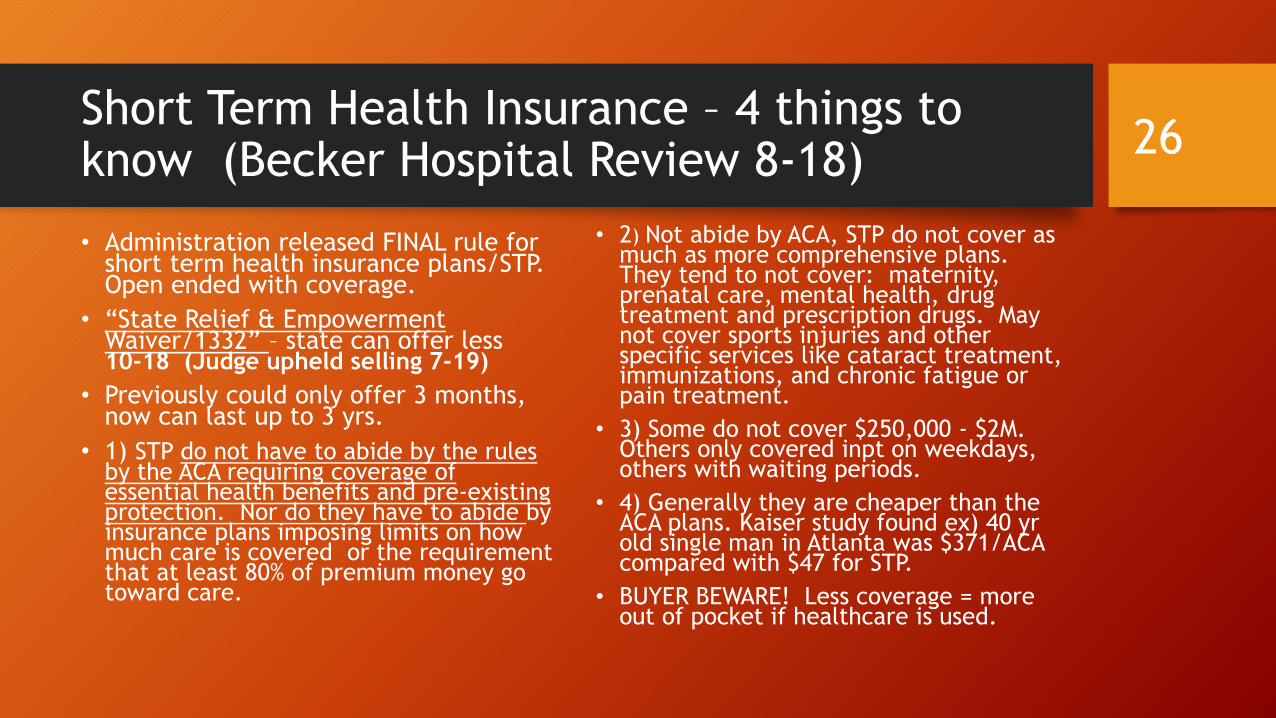

Short Term Health Insurance – 4 things to know (Becker Hospital Review 8-18)

• Administration released FINAL rule for short term health insurance plans/STP. Open ended with coverage.

• “State Relief & Empowerment Waiver/1332” – state can offer less 10-18 (Judge upheld selling 7-19)

• Previously could only offer 3 months, now can last up to 3 yrs.

• 1) STP do not have to abide by the rules by the ACA requiring coverage of essential health benefits and pre-existing protection. Nor do they have to abide by insurance plans imposing limits on how much care is covered or the requirement that at least 80% of premium money go toward care.

• 2) Not abide by ACA, STP do not cover as much as more comprehensive plans. They tend to not cover: maternity, prenatal care, mental health, drug treatment and prescription drugs. May not cover sports injuries and other specific services like cataract treatment, immunizations, and chronic fatigue or pain treatment.

• 3) Some do not cover $250,000 - $2M. Others only covered inpt on weekdays, others with waiting periods.

• 4) Generally they are cheaper than the ACA plans. Kaiser study found ex) 40 yrold single man in Atlanta was $371/ACA compared with $47 for STP.

• BUYER BEWARE! Less coverage = more out of pocket if healthcare is used.

26

Hospitals and Physicians= Change

• Healthcare deals announced/Merger Mania: 115 done in 2017

• Providers must be able to adapt to the changing payer environment – federal, state and local. Potential loss of personal financial ‘touch.”

• Federal rules implemented. Then after $ expended, discontinued and/or changed.

• EX) New payment model for physicians. “MedPAC votes to kill MIPS, recommends alternative/VVP voluntary value program. 1-12-18”

• Transition from ‘volume ‘ to value. “Outcome based payments.” “Accountable care. Pop Health”

• What does this mean to the pt?

• (EX) What if the payer does not pay for a service as the outcome was not within the payer-specific guidelines?

• (EX) Physician believes a course of treatment will help the pt. The payer denies as not medically necessary or experimental. Now what happens to the patient?

“Healthcare Experts Unable to Define “value based care” or “population health.” Humana convened a group of healthcare experts to build consensus on definitions.. They found common ground on value based –PAYMENT – they couldn’t agree on Value-based care or population health. Fierce Healthcare 7-19

27

About 1 in 5 healthcare payments are tied to value-based model. (Healthcare dive 1-11-19)

• Value-based payments make up about 22% of all care delivery payments, up from 18% for 2018

• Intermtn Healthcare/Utah =new company – Castell – will build on lessons learned from its primary care model which reduced admission and costs along with improved pt ratings and physician satisfaction. 8-19

Patients: Do patients understand Value Based? How does it impact them?

• “5 Health Systems sign landmark deal with BCBS NC.”

• Under the model, called Blue Premier, payments to physicians and hospitals are tied to the value of services provided. Total payments to the health systems will be based on their collective ability to manage cost and quality performance.

• BCBS NC wants to shift all within 5 yrs

• Cone Health, Duke University Health System, UNC Healthcare, Wake Forest Baptist Health, WakeMedHealth & Hospitals.

28

Payers – Traditional vs. Medicare Advantage/Part C challenges

*By 2035, all baby boomers will be 65. 2 workers to pay for 1 Medicare pt and 1 SSA $*

Traditional Medicare – Began in 1965• 65 year olds or disabled

• Part A = out of pocket -$1340 each 60 days. No monthly premium.

• Part B = $134 monthly premium (adjusted for income)

• Part B = $183 1x yearly deductible; coinsurance due with each outpt service

• Part D= prescription. “Tiered drugs’. Average $50 monthly premium

• 19% of Americans will work past 65. Working Aged = Commercial primary.

• Medicare Advantage/Part C:1-17 Privately run health plans have enrolled more than 17 M elderly and disabled people –about 1/3 of those eligible for Medicare –at a cost to tax payers of more than $150B a year. *

• Each insurance company who sells Part C insurance creates their own ‘rules’ – must offer same benefits as Traditional –but can establish own out of pocket costs, maximum amt of pocket yearly, and additional benefits.

• Part C insurance plans are paid yearly bonuses regarding low complaints. Insurance plans are paid a per member, per month, to manage the patient’s care.

29

Medicare Advantage/Part C/MA –increase enrollments

• By 2020, it is forecast that Medicare Advantage/MA will constitute 50% of the Medicare market.

• Significant changes were made to allow revision/expansion supplemental benefits –like hearing aides, health club memberships, in home visits, home delivered meals, glasses, and others ‘patient specific needs.”

• 2019 – allow negotiation with pharmacy pricing

• 2019- more ‘enticing’ payments for providers

• Significant payments to plans for “Star Rating’’(4&5) rated by pts.

• Limiting out of pocket yearly expense .

• But not all plans are sold in all counties of the country.

• No out of country benefit, no out of community benefit (Emergency/exception)

• No ability to have a Medicare Supplemental – pt pays all out of pocket plus monthly premium.

30

Change of payer/provider relationships

• Walmart buys Humana/discussion

Same impact of where pharmacy can be purchased

Walmart lost Pill Pack to Amazon/purchased… 9-18

Walmart ‘taps’ HUMANA executive to head up health unit. *Put more focus on its wellness business* 7-18

Joining with Anthem’s MA plans to pay for over the counter items –braces, etc.

• Rise of “Convergence” in healthcare. Means?

• Cigna Corp agrees to buy Express Scripts, the nation’s largest pharmacy benefit manager.

• Convergence: Where a company merges its capabilities with another organization in an adjacent industry. Only works if the industry’s solutions are not comprehensive, compelling or able to satisfy customer needs.

• Expand group purchasing efforts.

• Deloitte : Convergence is innovation for healthcare, but converge to what? 4-10-18; Newsroom 2-18

31

Payers – Changing Climate

• ‘CVS agrees to buy Aetna in $69 B deal that could shake up healthcare industry.”

• “We want to get closer to the community as all healthcare is local. “ CVS would provide a broad range of health services to Aetna’s 22 M member at its nationwide network of pharmacies and walk-in clinics.

• Think out of network for other pharmacies.

• Payer audits – each payer defines ‘coverage’ rules. Each provider has to try to stay aware of payer ‘interpretations.’ *Using External Companies*

• EX) VA hires a 3rd party audit company-CGI. Went back 3 yrs-like Medicare.

• EX) Medicare pays external audit companies to Audit all providers/service. Paid a % of what is denied/upheld/RAC.

• EX) Medicaid audits and pays an outside company to audit providers for compliance.

• EX) All payers do post-payment audits.

• EX) Payers do not guarantee payment when doing ‘authorizations.”

32

More Convergence ---Walgreens & Microsoft

• Walgreens: Consumer Facing Care.

• In-store visual clinics, lab services, retail clinics. Telehealth services. Using ‘smart technology”.

• Partnering with payers/Humana and local providers/Seattle area.

• “Walgreens partners with Microsoft to develop new Healthcare delivery models.” 1-15-19

• Walgreens Boots Alliance and Microsoft signed a seven year deal ‘ to develop new healthcare delivery models, technology, and retail innovations to advance and improve the future of healthcare.”

• Walgreens will test ‘digital health centers’ in some of its stores, which are aimed at merchandising and sale of select healthcare-related hardware devices. They will also collaborate on software research.

• “WBA will work with Microsoft to harness the information that exists between payers and healthcare providers to leverage, in the interest of patients and with consent, our extraordinary network of accessible and convenient locations to deliver new innovations, greater value and better health outcomes in healthcare systems across the world.”

33

More Payer Challenges- Anthem and Imaging*Anthem is the largest for-profit organization of BXBS*

• Anthem BC – Discontinuing coverage of outpt imaging at hospital. “Imaging Clinical Site of Care.”

• Directing patients to Free Standing Imaging Center for CT and MRI.

• 2017- Ky, Ind, MO, WI. Added CO, GA, NV, NY, OH, CA. March 2018-added CT, Maine and VA. 13 states impacted

• Pt steerage, limiting pt choice and labor cost to do prior authorization for CT and MRI. Some exceptions – Rural, tied to pre-op services.

• Quality of care, availability of the reports, interoperability limitations, Rad provider interpreting = all listed as concerns.

• United is very interested. But looking at a different approach??

34

Payers- United – largest payer –It is all in the contract. Mid –year changes?**United revenues will hit $243B-$245B in 2019**

• United Healthcare

• Continues to buy companies that work directly with hospitals. Advisory Group, Optum, physician groups.

• NEW: Site of Service determinations for outpt procedures. URG-11.03 eff 5-18.

“Certain elective procedures should be performed in an ambulatory surgical center/ASC vs outpt hospital.”

• United Healthcare-owns Optum

• Effective 3-18, ER Facility E&M Coding Revision for commercial and Medicare Advantage plans.

• Polices focus on ED level 4/99284 and level 5/99285 – whether the provider is contracted or not.

• Using Optum ED Claim (EDC) Analyzer tool which uses presenting problems, dx services provided, and associated pt’s co-morbidities.

35

More Payer Anguish- “If the plan approved the furnishing of a service thru an

advance determination of coverage, it may not deny coverage later on the basis of a lack of

medical necessity.” Medicare Mgd Care Manual. YAHOO! (PI Manual, Chp 6, Section 6.1.3)

• United MA – doing pre-audits/pre payment and then having another company doing post audits for the same accounts.

• Challenge them – Medicare Managed Care Manual, Cpt 4, Section 10:16.

• NJ Medicaid- NJ legislature passed bill 6-21 to limit any non-emergent ER visit $ to $140. AHA: “Hospitals should not be penalized for doing the right thing by providing quality care to patients who show up at our doors because insurance companies have failed to provide a network of providers available to these pts.”

• United- NYC Health and Hospital (largest public health system) sued UnitedHealth for $11M. Medicare Advantage and Medicaid mgt. Inpatient denials. Non coverage. (5-18)

• BCBS of Texas- for ER out of network claims after 6-4, the members will be on the hook for the entire out of network ED bill if they use it for what the insurer deems not serious or life threatening. (Updating)

36

Payer + Provider: ‘Long road from Contention to Cooperation.”

• ‘Anthem/BC (Indianapolis-based) determines ER visits are not covered for 300+ diagnosis. *Non-emergent*

• Impacts Kentucky, GA, Ohio, Indiana and Missouri. 40M+ BC members.

• Exceptions: under 14, on IV/new, no other care weekends, physician referrals to the ER, a lack of urgent care available.

• American College of ER Physicians:

“The changes do not address the underlying problem..pts have to decide if their symptoms are medical emergencies or not BEFORE they seek treatment. “

Anthem believes 10% reviewed/4% denied

• If the diagnosis does not warrant ‘emergent’ under the payer-specific guidelines, there is on payment to the hospital and providers.

• EX) Pt in Frankfort, KY –after experiencing increasing pain on her right side of her stomach, thought appendix had ruptured. ER tested, diagnosed with ovarian cysts.

• Patient owed full $12,000

• Denials are based on FINAL diagnosis; with little ‘weight’ for presenting diagnosis.

• BCBS TX physicians: “This will create deaths. This will make the pt think twice before going to the ER.”

37

More Payer-Provider Challenges -CignaNo longer paying drug administration

• Effective 5-19: Reimbursement policy for infusion and injection.

• “We routinely review our coverages, reimbursement and administrative policies… In that review, we take into consideration one or more of the following: evidence-based medicine, professional society recommendations, CMS guidance, industry standards and our other existing policies.”

• ‘As a result of this review, we want to make you aware that we will NO LONGER SEPARATELY REIMBURSE infusion and injection administration services billed by facilities because infusion and injections administration services are considered INCIDENTAL TO THE PRIMARY SERVICE and are not separately reimbursable.”

• “The affected CPT codes: 96360-96379 and 96521 thru 96523. This aligns with our current reimbursement poslicies for facility routine supplies. (EXCLUDES: Chemo 96400-530 and sub-inj 96372)

• NOTE:” In Nov, 2018, we began applying this update to claims from the ER DEPARTMENTS. This updates expands to all areas within a facility.” (No observation or ER. What if have chemo and non-chemo drugs at the same treatment time?)

• WOW! A) What is the primary service that is being paid? B) If it is drugs, are you getting full billed charges as it must now cover all visit and all infusion costs C) What about the ER visit or HBC visit?

38

Payer + Provider = New payment relationships

• AHA, AHIP and 4 other associations (AMA, BC/BS and MGMA) join to improve prior authorizationprocesses.1-18

• Six healthcare groups agreed to take steps to make prior authorization processes more effective and efficient.

• Decrease the # of providers required to comply with prior authorization based on their ‘performance, adherence to evidence-based medical practices or participation in a value-based agreement with the health insurance provider.”

• Disney partners with 2 Florida health systems to offer HMO. 2-18

• Directly contracted with Orlando Health/6 acute hospitals and Florida hospital, Orlando/20 campuses to roll out two insurance plans for Disney employees.

• Goal: lower healthcare costs, higher outcomes

• Using Cigna/Allegiance to administer the program.

• NOTE: Remember employer-owned insurance is still looking for ways to reduce their costs..

• 11% of employers are looking at Direct to health system./ National Bus Group 8-18

39

Payers /Physicians– “Really really hate Prior Authorizations/PA” - AMA survey 3-18• New survey of American Medical Association –examined the attitudes of 1,000 physicians

regarding prior authorization.

• Insurance companies: As an effort to deliver the best possible therapy to the patient and to avoid unnecessary care.

• Physicians: Simply a tactic to make expensive care more onerous, driving down the costs to the insurance companies.

• Q: How would you describe the burden: 84% very high.

• 86% report that the burden has increased over the past 5 yrs.

• 79% reported having to repeat prior auths even for pts previously approved.

• Ins requests prior auths 29.1 x per week.

• 78% reported that PA can at lead to treatment abandonment.

• Dedicate an average of 14.6 hrs per week for Prescription and medical services per practice = 2 business days

• IDEA SUGGESTED: If ins really cares about appropriate tx, tie to the electronic medical record; make it fast and give results before the pt leaves our office.

40

National

• ‘Fed Up With Drug Companies, Hospitals Decide to Start Their Own.” 1-18

• Intermountain Healthcare, Trinity Health, Ascension, SSL Health/SSM and the US Dept of Veterans Affairs. ++

• “There is a dangerous gap between the demand and supply of affordable prescription drugs. “ CIVICA-RX

• Formation of a new not-for-profit generic drug company will work with 1000+ hospitals.

• About a year to get rolling/expect 1st Q of 2019. ‘Healthcare systems are in the best position to fix the problems.”

• “Amazon, JP Morgan, Berkshire form new company to tackle healthcare costs.” 1-18 (Now called Haven)

• Forming indpt company to address healthcare needs of their US employees/500,000 ‘free from profit-making incentives and constraints.”

• Focus will be technology solutions first.

• New CEO: Dr Atul Gawande. 3 focus areas: Data tracking/treatments; continuing pre-existing coverage; end of life care. 6-18

• 2-18 35% would use Amazon ins plan

• 8-18 Setting up own employee clinics/Seattle.

41

The Healthcare Nation at a Glance

• Apple opening its iPhone-based health records feature to developers and researchers to they can create apps that use health record data to help users better manage medications, nutrition plans and dx.

• Google is developing its own prescription for US healthcare costs: Smarter Artificial Intelligence.

• HealthPopuli: US Worker’s say Healthcare is the most critical issue facing the nation.

• Geisinger, Dignity Health among first hospitals to pilot Apple’s medical records system. 1-18• Apple announced its intent to

integrate patient health records into its Health app to make it easier for consumers to review their medical data. While providers offer ‘portals’ for access, Apple aims to embed patient data from multiple providers into the iPhone main system. Download 11.3Beta version.

• Others in pilot: Rush University Medical Center, LA Cedars-Sinai, Philly Penn Medicine.

42

Thanks for Joining Us in this Educational Journey…

Day Egusquiza, President

AR Systems, Inc

Patient Financial Navigator Foundation, Inc.

PO Box 2521

Twin Falls, Idaho [email protected]

Http://arsystemsdayegusquiza.com

Pfnfinc.com Not-for-profit Foundation

Patient Financial Navigator Foundation, Inc –

A family owned, Idaho-based foundation.

Transforming the hassle factor in healthcare thru

Education.

43

SAVE THE DATES!

44

September 20-23, 2020AHIA 39th

Annual ConferenceSheraton Seattle Hotel