Embed Size (px)

Citation preview

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 1/40

Enabling Service Tax Practice - Level I

Presentation

onCharge Reverse Charge in Service Tax

Organized By ByIndirect Tax Committee of ICAI &Vijayawada Branch of ICAI Dr. Sanjiv Agarwal@ Vijayawada FCA, FCS,8th Nov, 2013, Friday Jaipur / Delhi

© Dr. Sanjiv Agarwal

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 2/40

This Presentation Covers –

Charge of Service TaxPayment of Service TaxPerson liable to pay TaxRegistration under Service TaxReverse charge provisions

Concept

Conditions

Rates

Full / partial (joint) reverse charge

Abatements & reverse charge

3

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 3/40

Section 66 (up to 30.6.2012)

There shall be levied a tax @ 12 percent of the value of

taxable services as referred to in section 65(105), i.e.,taxable services

Not to apply w.e.f. 1.07.2012

3

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 4/40

Section 66B (W.e.f 1.7.2012)

There shall be levied a tax at the rate of twelve per cent

on the value of all services, other than those servicesspecified in the negative list, provided or agreed to beprovided in the taxable territory by one person toanother and collected in such manner as may be

prescribed

4

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 5/40

Essential ingredients for charge of Service Tax (Section 66B) There should be a service involved

Such service should not be one included in the negative listas defined in section 66D.

Services should be provided or agreed to be provided. Services should be provided in the taxable territory only.

Services should be provided by one person to anotherperson.

Tax shall be levied on value of services so provided oragreed to be provided.

Collection shall be in prescribed manner.

5

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 6/40

Provided or to be provided v. provided or agreed to be provided Before actual provision of service is made, all relevant

information on chargeable event must be known

On account advance payment without any identification ofservices or activities may not be liable to service tax

Services which have only been agreed to be provided butare yet to be provided are taxable

Receipt of advances for services agreed to be providedbecome taxable before the actual provision of service

Advances that are retained by the service provider in theevent of cancellation of contract of service by the servicereceiver become taxable as these represent considerationfor a service that was agreed to be provided.

6

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 7/40

Section 68 deals with payment of service tax

Every person providing taxable service (service provider)

shall pay tax @ 12.36% , to be collected in prescribed

manner. [section 68(1)]

Service recipient is a person liable to pay service tax in

certain cases [section 68 (2)]

Person liable to pay service tax – defined in rule 2(1)(d) of

Service Tax Rules, 1994

7

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 8/40

Defined in rule 2(1)(d) of Service Tax Rules, 1994 and

2(m) of POP Rules, 2012

Person liable to pay service tax u/s 68 or rule 2(1)(d) of

ST Rules, 1994

Persons liable

Service provider

Specified service receivers [Rule 2(1)(d)(i)(A to G)]

Importer of service

8

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 9/40

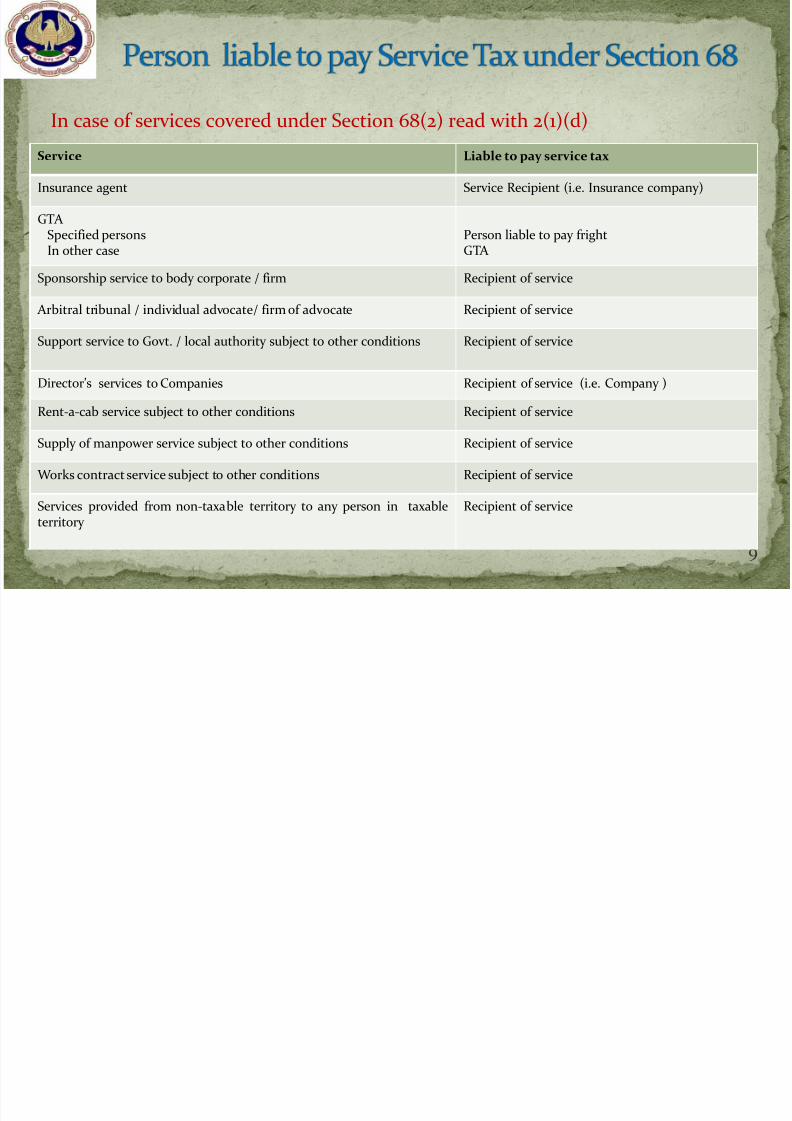

In case of services covered under Section 68(2) read with 2(1)(d)

9

Service Liable to pay service tax

Insurance agent Service Recipient (i.e. Insurance company)

GTASpecified personsIn other case

Person liable to pay frightGTA

Sponsorship service to body corporate / firm Recipient of service

Arbitral tribunal / individual advocate/ firm of advocate Recipient of service

Support service to Govt. / local authority subject to other conditions Recipient of service

Director’s services to Companies Recipient of service (i.e. Company )

Rent-a-cab service subject to other conditions Recipient of service

Supply of manpower service subject to other conditions Recipient of service

Works contract service subject to other conditions Recipient of service

Services provided from non-taxable territory to any person in taxableterritory

Recipient of service

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 10/40

Every person who is liable to pay service tax shall take registration

under service tax as per section 69 of Finance Act, 1994

Service recipient shall obtain registration under service tax as recipient

of service, pay service tax and file return

Assessees who have to take registration

Service provider who has provided a taxable services of valueexceeding Rs. 9 lakhs in the preceding financial year

Service receiver liable to pay service tax under reverse charge

mechanism u/s 68(2) / rule 2(1)(d) Input service distributor

Importer of service being person liable u/s 68(2)

10

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 11/40

Service tax is an indirect tax levied by service provider on

the service recipient

Service provider collects service tax from service receiver

and pays to Govt. itself / himself

Under reverse charge, the position becomes reverse

Instead of tax being paid by service provider, service

receiver has to deposit tax in Govt. account

11

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 12/40

12

Service provider pays servicetax

Service receiver pays service tax

oth service provider and servicereceiver pay service tax

Service tax payment - differentscenarios

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 13/40

Normally, service tax is payable by person who provides the service

Section 68(2) makes provision for reverse charge i.e. making personreceiving the service liable to pay tax

Authority for reverse charge u/s 68(2) of Finance Act, 1994

Person liable to pay tax – Rule 2(1)(d) of Service Tax Rules, 1994

W.e.f. 1.7.2012, a new scheme of taxation is applicable whereby the

liability of payment of service tax shall be both on the service providerand the service recipient (Notification No. 30/2012-ST, dated 20.6.2012 )

The extent to which tax liability has to be discharged by the servicereceiver is specified in Notification No. 30/2012-ST dated 20.6.2012.

13

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 14/40

Under Partial Reverse Charge (Proportional / Joint)

Renting of motor vehicles Manpower supply & security services Works contracts

Under Full Reverse Charge (100%) Insurance related services by agents goods transportation by road sponsorship arbitral tribunals

legal services company director's services services provided by Government / local authority excluding

specified services services provided by persons located in non-taxable territory to

persons located in taxable territory.

14

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 15/40

Governed by Notification No. 30/2012-ST dated 20.06.2012 w.e.f. 1.7.2012

Liabilities of both the service provider and service receiverare statutory and independent of each other

Liability cannot be shifted by mutual agreement

Reverse charge will not apply where the service receiver islocated in non-taxable territory

Reverse charge shall not be applicable if provider of service was liable before 1.7.2012

Service Tax will not be payable by service receiver underreverse charge, if service was provided prior to 1.7.2012,even if payment is made after 30.06.2012

15

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 16/40

Credit of tax paid can be availed by service recipient if it isinput service for him

The credit of tax paid by the service recipient under partial

reverse charge would be available on the basis on the taxpayment challan (but invoice required)

Service provider under RCM may claim refund of tax paid

under rule 5(b) of CCR, 2004

Service Tax under reverse charge to be paid within 6 monthson actual payment (Rule 7 of POT Rules, 2011)

16

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 17/40

Small scale benefit is available only to service provider (not to service receiver), if entitled

Service receiver under reverse charge cannot avail exemption of Rs. 10 lakh under

Notification No. 33/2012-ST dated 20.06.2012

Valuation of services by services provider and service receiver can be on different principles,

if permitted by law (e.g. works contract - Refer Notification No. 30/2012-ST, explanation II)

Invoice to be prepared as per Rule 4A of Service Tax Rules, 1994

It is a statutory obligation (not contractual) on the service recipient to pay Service Tax,

whether under full or proportional reverse charge

Service Tax under reverse charge has to be paid only by cash vide GAR Challan No. 7 and it

cannot be paid by way of utilization of Cenvat Credit.

Once paid, Cenvat credit can be taken for paying eligible input service

17

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 18/40

In case of proportional reverse charge (manpower supply &security, works contract and motor vehicle hire to carrypassengers), it is advisable that service provider should chargeService Tax only on his portion of service in the invoice andmention that Service Tax on balance amount is payable by

service receiver. Service receiver liable only for his portion

For three specified services provided by business entities beingcompany, society, co-operative society, trust etc, reverse charge

will not apply.

Reverse charge will also not apply where the service recipient isany person or business entity not being a body corporate in caseof three specified services

18

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 19/40

“Business Entity” means any person ordinarily carryingout any activity relating to industry, commerce or anyother business or profession

“Body Corporate” means the meaning assigned to inclause (7) of Section 2 of the Companies Act, 1956 andsection 2(11) of 2013 Act.

•

Company , corporation and LLP are‘body

corporate’

• Firm, HUF, Trust are not ‘body corporate’

• Co-operative society is legally not ‘body corporate’

19

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 20/40

In respect of manpower supply and security services, workscontract services and renting of motor vehicles to carrypassenger, reverse charge shall be applicable only when followingtwo conditions are satisfied –

service receiver is a business entity registered as a body corporate,and service provider is any one of the following entities –

Individual Hindu undivided family (HUF) Firm (including limited liability partnerships) Association of persons

If both the above conditions are not satisfied in respect of thesethree services, Service Tax shall be payable by the serviceprovider in ordinary course.

20

8/12/2019 Reverse Charge on Service Tax - India

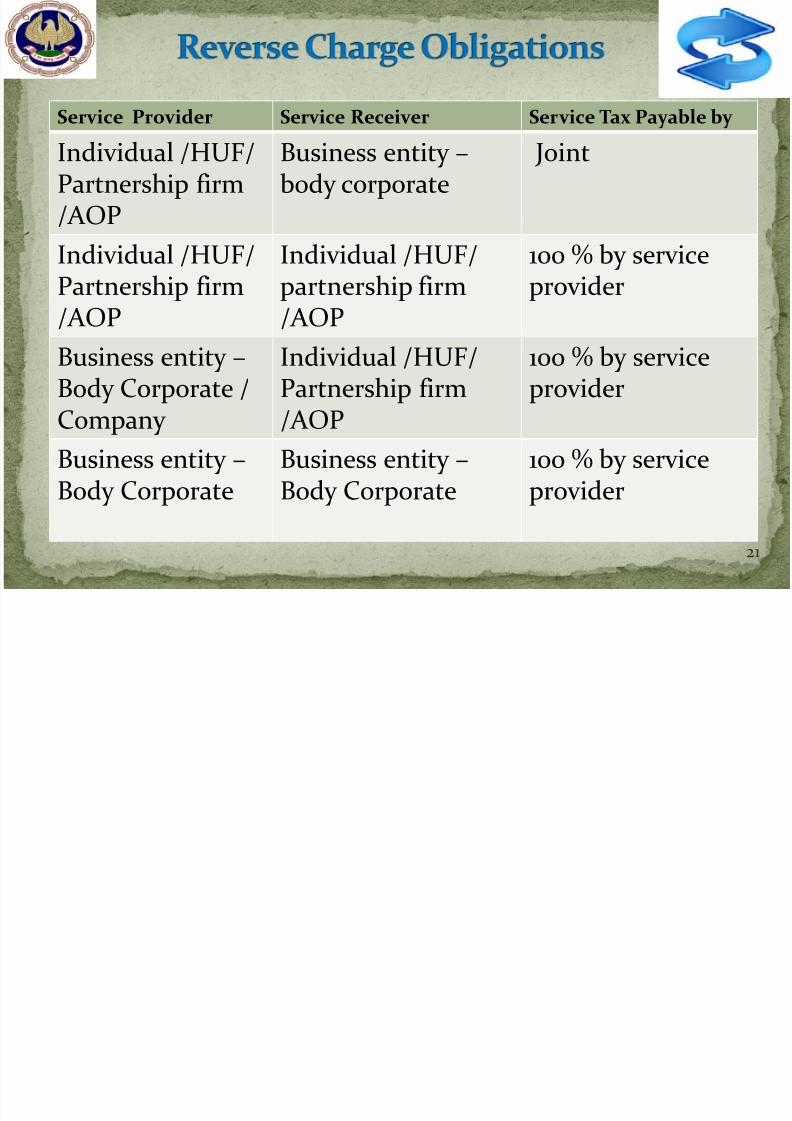

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 21/40

Service Provider Service Receiver Service Tax Payable by

Individual /HUF/Partnership firm/AOP

Business entity – body corporate

Joint

Individual /HUF/

Partnership firm/AOP

Individual /HUF/

partnership firm/AOP

100 % by service

provider

Business entity –Body Corporate /

Company

Individual /HUF/Partnership firm

/AOP

100 % by serviceprovider

Business entity –Body Corporate

Business entity – Body Corporate

100 % by serviceprovider

21

8/12/2019 Reverse Charge on Service Tax - India

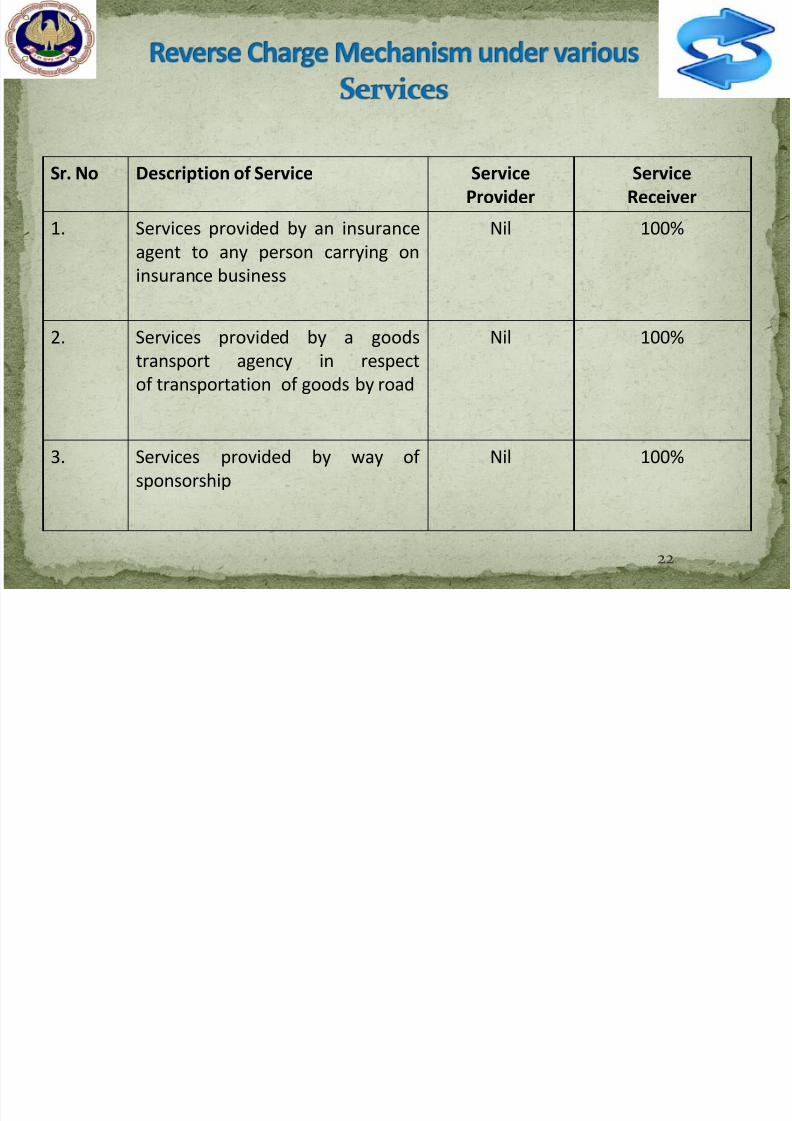

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 22/40

Sr. No Description of Service Service

Provider

Service

Receiver

1. Services provided by an insurance

agent to any person carrying on

insurance business

Nil 100%

2. Services provided by a goods

transport agency in respect

of transportation of goods by road

Nil 100%

3. Services provided by way of

sponsorship

Nil 100%

22

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 23/40

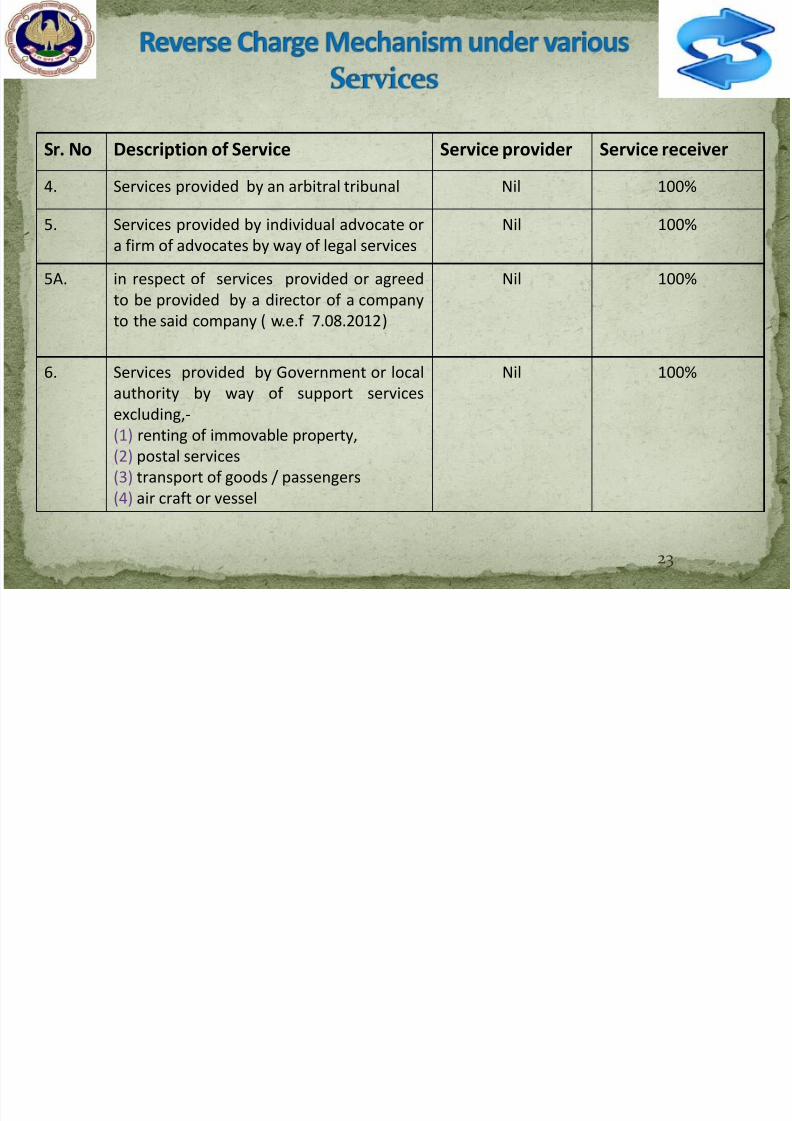

Sr. No Description of Service Service provider Service receiver

4. Services provided by an arbitral tribunal Nil 100%

5. Services provided by individual advocate or

a firm of advocates by way of legal services

Nil 100%

5A. in respect of services provided or agreedto be provided by a director of a company

to the said company ( w.e.f 7.08.2012)

Nil 100%

6. Services provided by Government or local

authority by way of support services

excluding,-(1) renting of immovable property,

(2) postal services

(3) transport of goods / passengers

(4) air craft or vessel

Nil 100%

23

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 24/40

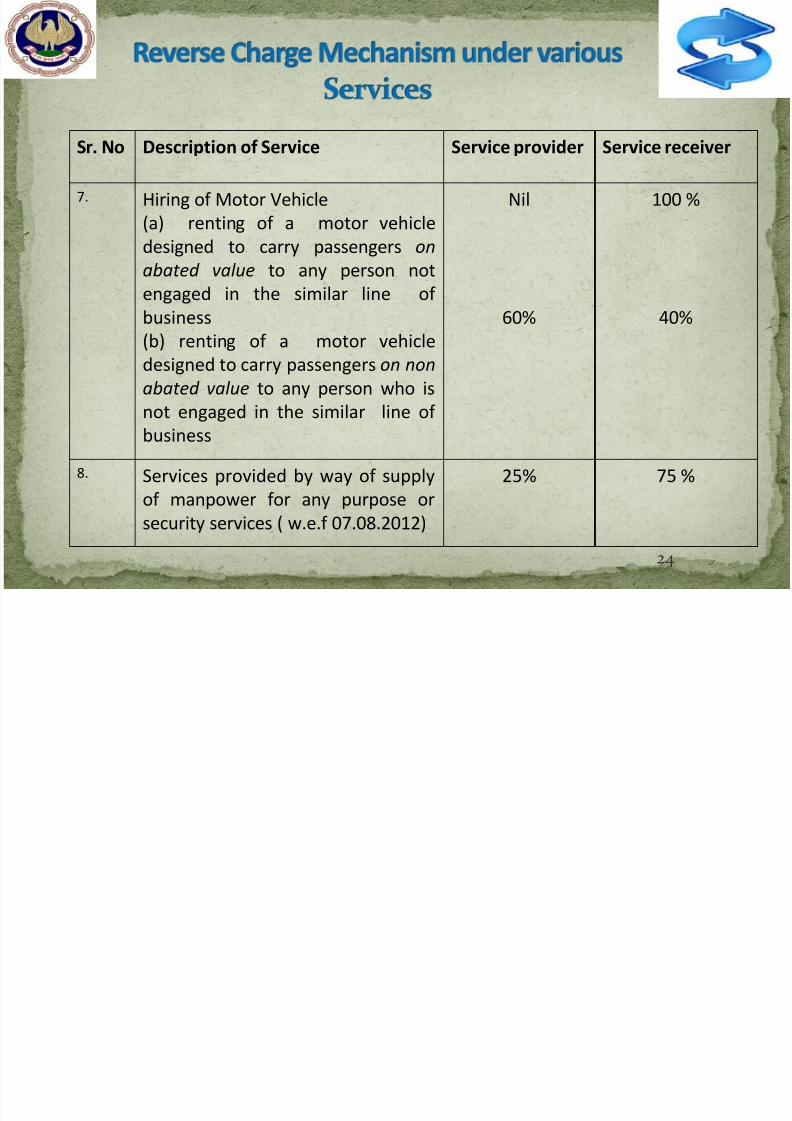

Sr. No Description of Service Service provider Service receiver

7. Hiring of Motor Vehicle

(a) renting of a motor vehicle

designed to carry passengers on

abated value

to any person notengaged in the similar line of

business

(b) renting of a motor vehicle

designed to carry passengers on non

abated value to any person who is

not engaged in the similar line ofbusiness

Nil

60%

100 %

40%

8. Services provided by way of supply

of manpower for any purpose or

security services ( w.e.f 07.08.2012)

25% 75 %

24

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 25/40

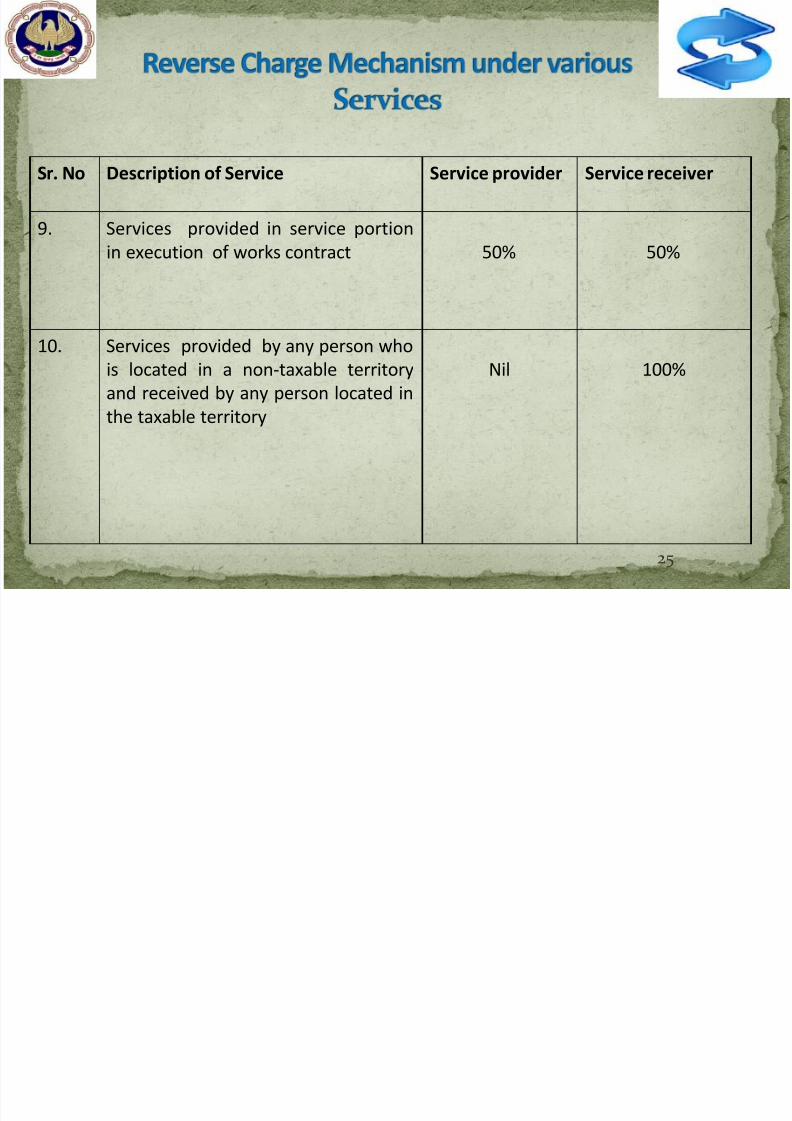

Sr. No Description of Service Service provider Service receiver

9. Services provided in service portion

in execution of works contract 50% 50%

10. Services provided by any person who

is located in a non-taxable territory

and received by any person located in

the taxable territory

Nil 100%

25

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 26/40

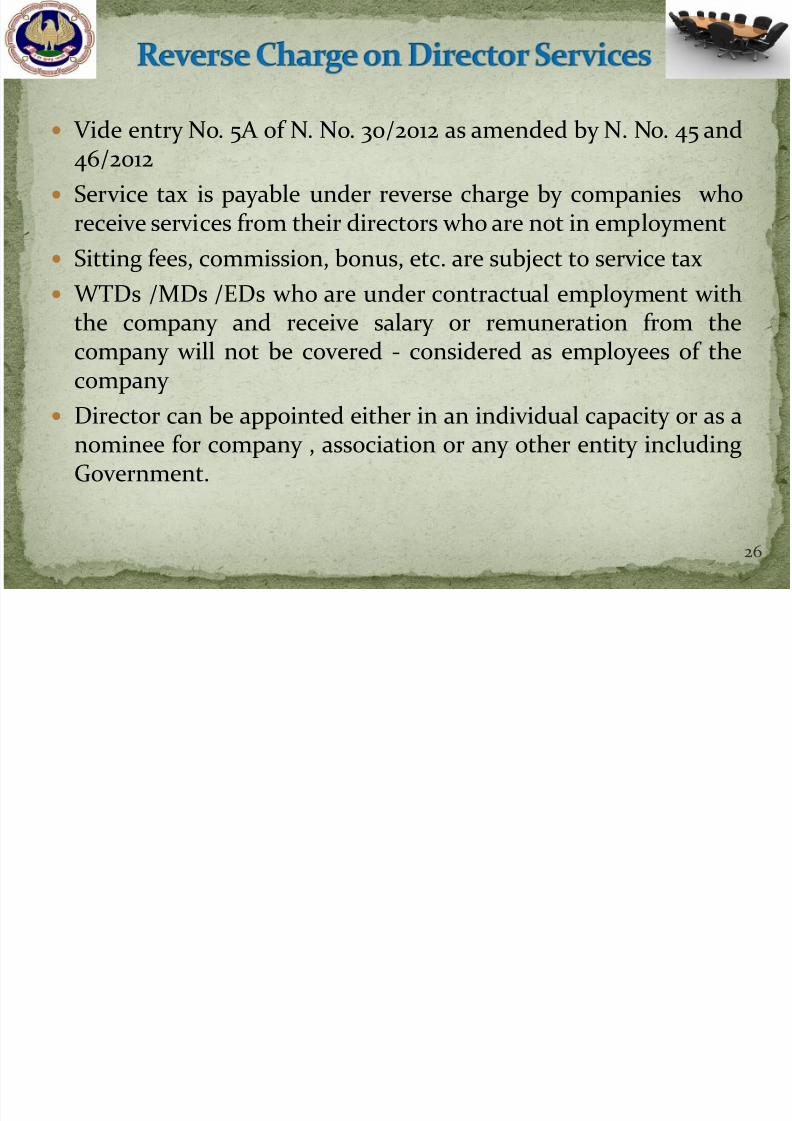

Vide entry No. 5A of N. No. 30/2012 as amended by N. No. 45 and46/2012

Service tax is payable under reverse charge by companies whoreceive services from their directors who are not in employment

Sitting fees, commission, bonus, etc. are subject to service tax

WTDs /MDs /EDs who are under contractual employment withthe company and receive salary or remuneration from thecompany will not be covered - considered as employees of thecompany

Director can be appointed either in an individual capacity or as anominee for company , association or any other entity includingGovernment.

26

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 27/40

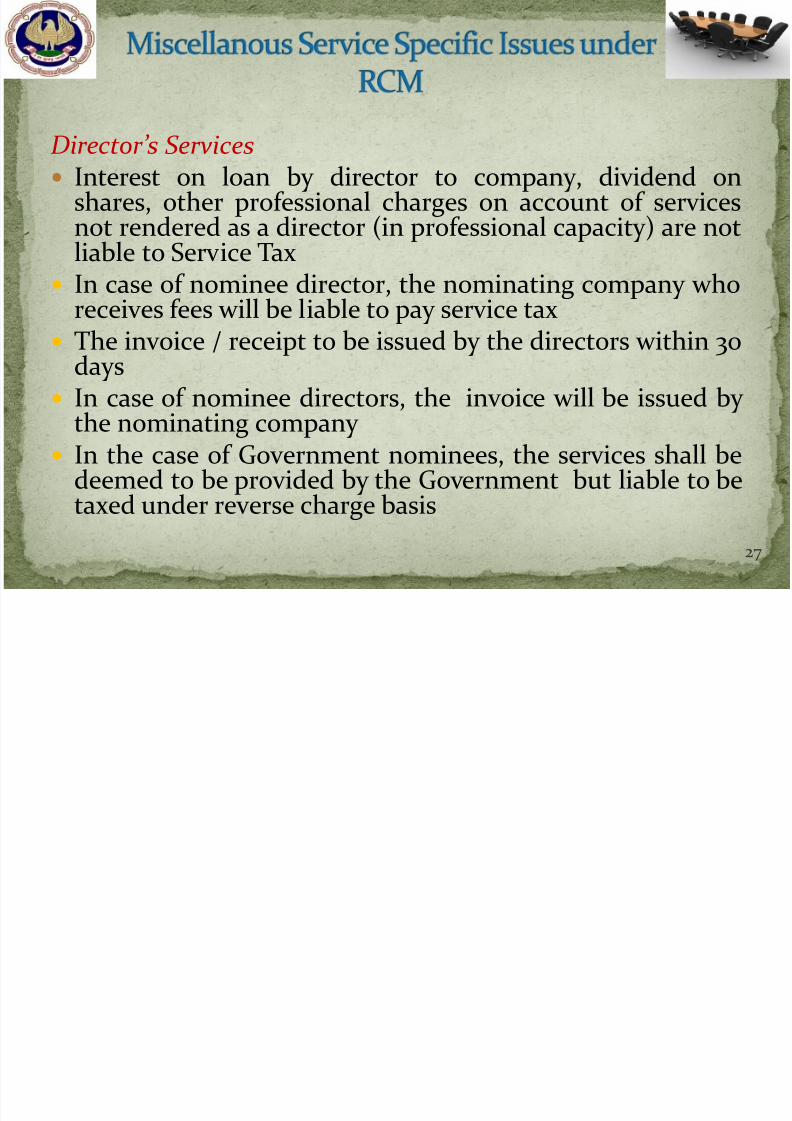

Director’s Services Interest on loan by director to company, dividend on

shares, other professional charges on account of servicesnot rendered as a director (in professional capacity) are notliable to Service Tax

In case of nominee director, the nominating company whoreceives fees will be liable to pay service tax

The invoice / receipt to be issued by the directors within 30days

In case of nominee directors, the invoice will be issued bythe nominating company

In the case of Government nominees, the services shall bedeemed to be provided by the Government but liable to betaxed under reverse charge basis

27

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 28/40

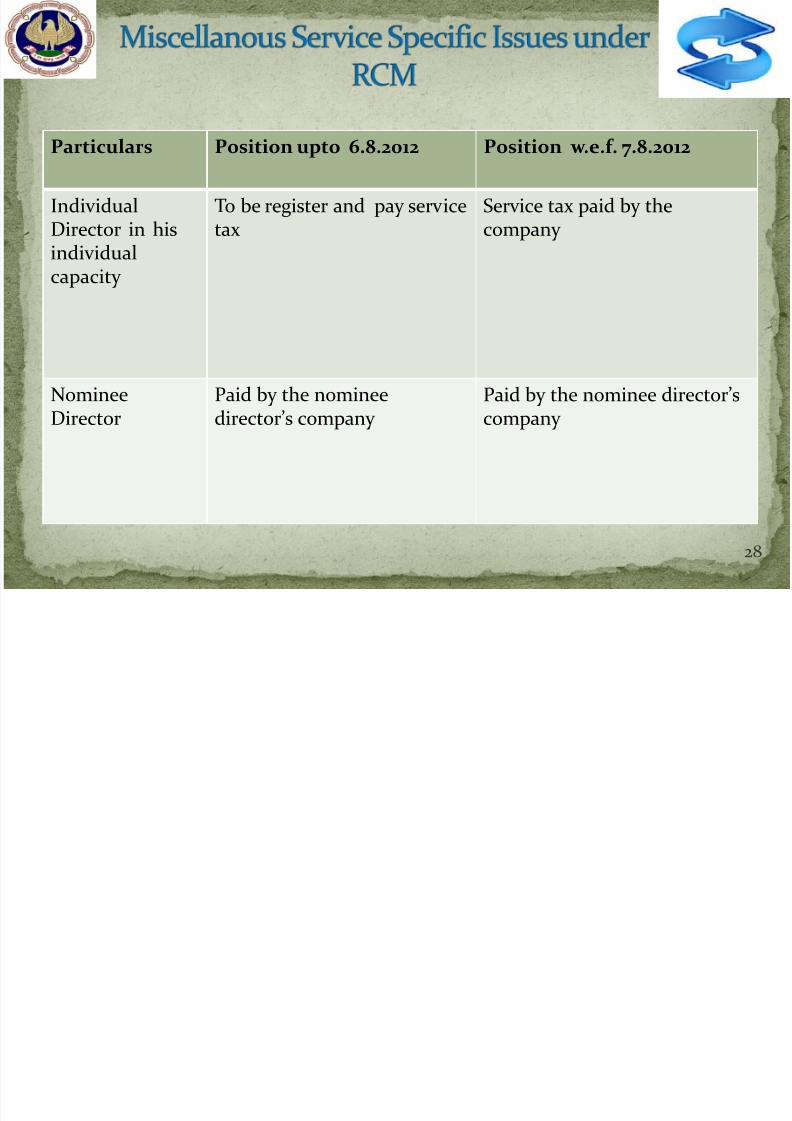

Particulars Position upto 6.8.2012 Position w.e.f. 7.8.2012

IndividualDirector in hisindividual

capacity

To be register and pay servicetax

Service tax paid by thecompany

Nominee

Director

Paid by the nominee

director’s company

Paid by the nominee director’s

company

28

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 29/40

Manpower Supply Services

Service is manpower supply service if under commandof principal employer

•

Cleaning service, piece basis / job basis contract is notmanpower supply service

Service tax will be applicable on salary plus PF, ESI,commission of labour contractor and other charges

Employees sent on deputation is also covered undermanpower supply services

29

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 30/40

Security Services

Security services means services relating to the security of

any property, whether movable or immovable, or of any

person, in any manner and includes the services of

investigation, detection or verification, of any fact or

activity

CA services are not security services

Distinction between manpower supply & security services

30

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 31/40

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 32/40

Rent-a-cab Service

Reverse charge will be applicable when renting to aperson who is not in similar line of business

Service receiver will pay on 40% in every case whetherabatement is claimed or not

No Cenvat credit (not an input service)

Cost to company

32

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 33/40

Goods Transport Service

Service tax liability arise when consignment note is

issued

GTA will be liable for pay tax only when both service

provider and service receiver are individuals

Tax on 25% (abated value), if GTA does not avail

Cenvat Credit otherwise tax on 100% value

33

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 34/40

Service Provider Service Receiver

Individual Advocate / Firm / LLP Business entity with turnover > Rs 10

lakhs in preceding financial year

Arbitral Tribunal Business entity with turnover > Rs 10

lakh in previous financial year

34

Legal Services

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 35/40

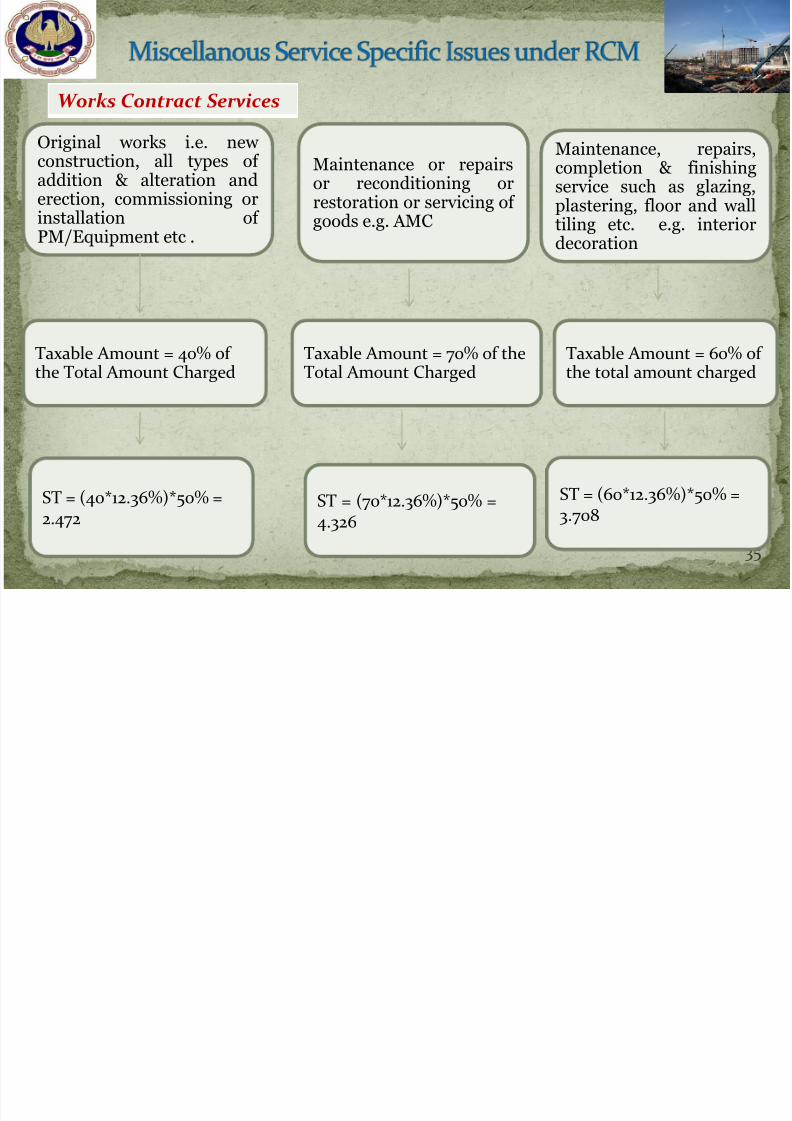

35

Original works i.e. newconstruction, all types ofaddition & alteration anderection, commissioning orinstallation ofPM/Equipment etc .

Taxable Amount = 40% ofthe Total Amount Charged

ST = (40*12.36%)*50% =2.472

Maintenance or repairsor reconditioning orrestoration or servicing ofgoods e.g. AMC

Maintenance, repairs,completion & finishingservice such as glazing,plastering, floor and walltiling etc. e.g. interiordecoration

Taxable Amount = 70% of theTotal Amount Charged

Taxable Amount = 60% ofthe total amount charged

ST = (70*12.36%)*50% =4.326

ST = (60*12.36%)*50% =3.708

Works Contract Services

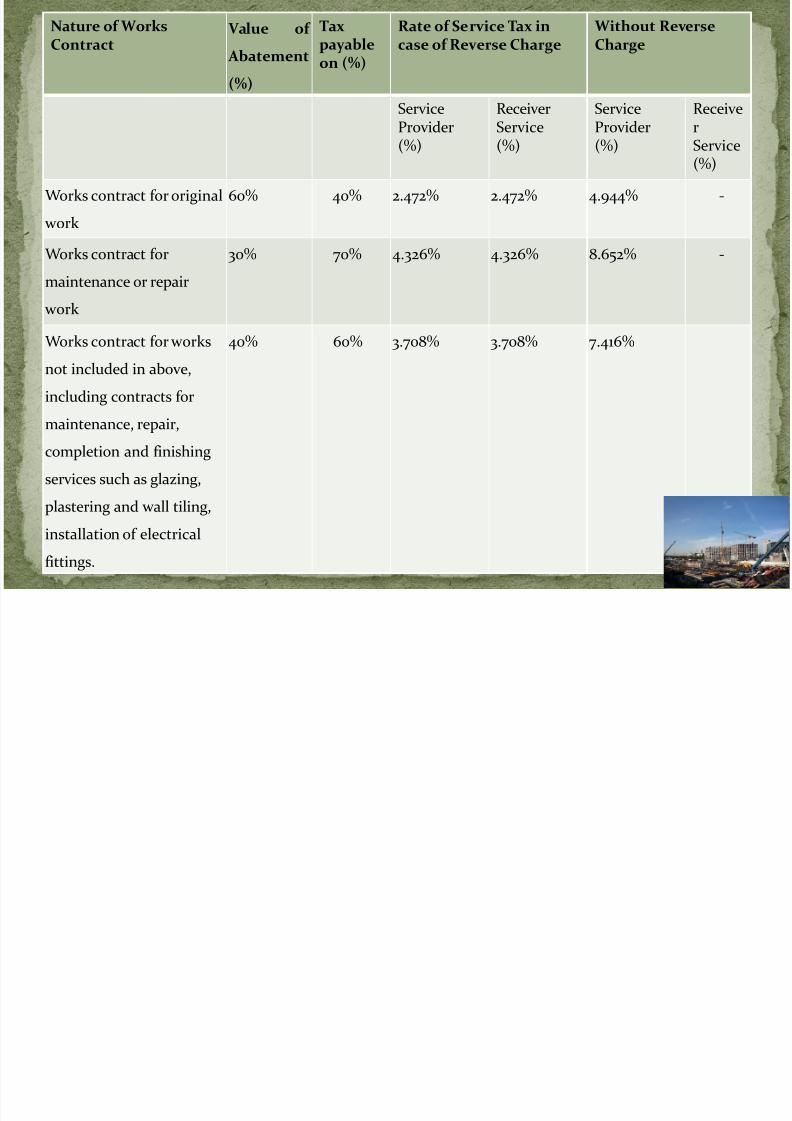

Nature of Works V l f Tax Rate of Service Tax in Without Reverse

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 36/40

Nature of WorksContract Value of

Abatement

(%)

Taxpayableon (%)

Rate of Service Tax incase of Reverse Charge Without Reverse

Charge

ServiceProvider

(%)

ReceiverService

(%)

ServiceProvider

(%)

Receiver

Service(%)

Works contract for original

work

60% 40% 2.472% 2.472% 4.944% -

Works contract for

maintenance or repair

work

30% 70% 4.326% 4.326% 8.652% -

Works contract for works

not included in above,

including contracts for

maintenance, repair,

completion and finishing

services such as glazing,

plastering and wall tiling,

installation of electrical

fittings.

40% 60% 3.708% 3.708% 7.416%

36

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 37/40

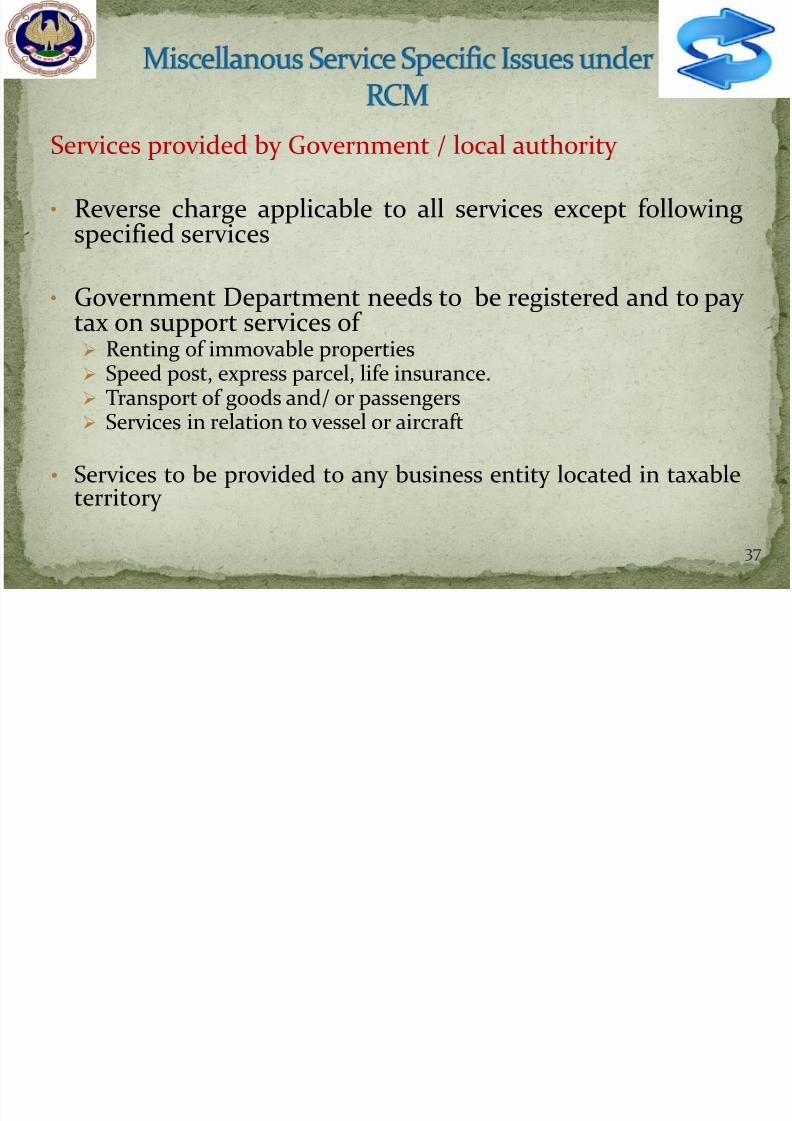

Services provided by Government / local authority

• Reverse charge applicable to all services except followingspecified services

• Government Department needs to be registered and to paytax on support services of Renting of immovable properties Speed post, express parcel, life insurance. Transport of goods and/ or passengers

Services in relation to vessel or aircraft

• Services to be provided to any business entity located in taxableterritory

37

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 38/40

Reverse Charge Mechanism

Additional information suggested on the invoice –

Amount of Service Tax based on his share of Service Tax liability, if any, (which service

recipient is required to pay to the service provider) - in case of joint or proportionate reverse

charge liability. Fact that entire amount of Service Tax on the invoice is payable by the service recipient under

reverse charge (if so).

Invoice amount is inclusive / exclusive of applicable Service Tax.

Alternatively, in case of proportionate reverse charge, service provider should charge Service

Tax only on that part of the invoice for which he is liable to pay and wants to recover from the

service recipient and mention that balance amount is payable by the service recipient.

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 39/40

Sl. No Description of taxable service Taxable

value(%) Conditions

7 Transport of goods by road by Goods

Transport Agency

25 CENVAT credit on inputs, capital

goods and input services, used

for providing the taxable service,

has not been taken under the

provisions of the CENVAT Credit

Rules, 2004.

9 Renting of any motor vehicle designed

to carry passengers

40 Same as above

39

8/12/2019 Reverse Charge on Service Tax - India

http://slidepdf.com/reader/full/reverse-charge-on-service-tax-india 40/40

THANK YOU

FOR

YOUR

PRECIOUS TIME

AND

ATTENTION

Dr. Sanjiv Agarwal

FCA, FCS, Jaipur