Embed Size (px)

Citation preview

INVESTMENTS, LLCKEATING

Reverse Merger ServicesThe Turnkey Solution for Private Companies

Seeking a Rational Alternative to an IPO

January 2006

5251 DTC Parkway, Suite 1090Greenwood Village, Colorado 80111-2739(720) 889-0139 ✦ Fax: (720) 889-0135

150 California Street, Suite 610San Francisco, California 94111

(415) 433-1800 ✦ Fax: (415) 399-9709

www.keatinginvestments.com

©2006 Keating Investments, LLC

Keating Investments, LLC and Keating Securities, LLC operate under the generic name of Keating Investments or Keating. KeatingInvestments is a registered investment advisor and the parent of Keating Securities, LLC. All securities transaction-related services,including underwriting, distribution and placement of securities, market-making and trading activities are conducted through KeatingSecurities, LLC, a registered broker-dealer and a member of the NASD.

ounded in 1997 by Timothy J. Keating,Keating Investments is a Denver-based

broker-dealer, registered investment advisor, andNASD member committed to helping private firmssignificantly increase their stockholder value bygoing public. For the past five years, we have beentaking qualified private companies public throughour reverse merger program. We provide a turnkeygoing public solution as a rational alternative forcompanies that would find it difficult or untimelyto launch a traditional initial public offering (IPO).

Turnkey Solution

Our business goes well beyond simply providingpublicly traded shells from our inventory. Instead,we offer our clients a turnkey package of value-addedservices to help smooth their transition from privateentity to public firm. We provide support at everystep of the going public process.

✦ Origination: We screen private companies toensure that they have the financial characteristics,management talent and growth potential to attractinterest on Wall Street and to develop a liquidtrading market.

✦ Transaction Execution: We oversee the entire

staff attorneys generate all required transactiondocumentation for review by the client’s counsel,including the preliminary proposal, letter ofintent, share exchange agreement and financialadvisory agreement.

About Keating Investments

✦ Distribution: We work closely with portfolioclients to develop a realistic capital marketsstrategy and then raise capital, as needed.

✦ Market-Making: We help clients apply for listingon the AMEX or NASDAQ exchange, and helpcreate and maintain an active market for thecompany’s stock.

✦ After Market Support: We provide our clientswith a comprehensive, thorough after market support package as an aggregator and consolidatorof services, customizing a solution unique to eachclient’s needs. Our 24-month program representsa strategic and highly structured approach to creating actively traded, widely held and fully

Some Facts about Keating Investments

✦ 4 reverse merger transactions completed in thepast 12 months

✦ Authorized by NASD to conduct a general securities business, arrange private placementsand act as un underwriter and market-maker

✦ 20 employees, 15 licensed professionals

✦ Principal office in Denver

✦ Branch office in San Francisco focusing on ourinternational business

✦ Market-maker on NASDAQ and the Pink Sheets(trading ID: KTNG)

F

1

valued stocks.

going public transaction from end-to-end. Our

There are SignificantBenefits to Being aPublicly Traded StockInvestors place a high premium on liquidity,or having the ability to sell stock quickly. As aresult, public companies trade at significantlyhigher valuations than private firms withsimilar financial characteristics. By goingpublic, the value of a company is immediatelyvalued at a higher level — resulting in thecreation of new value for existing stockholders(See Table 1).

In addition to higher valua-tions, public companiesalso enjoy other significantbenefits, including:

✦ Lower cost of capital andsuperior access to thecapital markets

✦ Creation of a stock currency to fund acquisitions

✦ Equity-based compensa-tion for management andemployees

✦ Liquidity for investors and minority share-holders

✦ A foundation for future financing activities

✦ Improved corporate visibility and prestige

Of course, public companies also incurobligations, such as the cost of periodicfinancial reporting, compliance with Sarbanes-Oxley, full disclosure of company information,and restrictions on stock sales by major orcontrolling shareholders. For rapidly growingcompanies, the capital-raising opportunitiesand other benefits of being public substan-tially outweigh these disadvantages.

Most companies consider going publicthrough the traditional IPO process. Whilean IPO offers many advantages, it is anavenue mainly open to only a few largefirms, not to smaller, emerging companies.Furthermore, there is no certainty that anIPO will be successfully completed – anadditional cause for concern. Indeed, asinvestors and underwriters have becomemore cautious in their approach to newpublic offerings, the IPO market for issuerswith capitalizations under $100 million hasall but disappeared (See Table 2).

Moreover, the IPO market is very sensitiveto market fluctuations and investmenttrends, as well as to the corporate financingcalendar. As investors and underwriters chase“hot” deals, it is difficult for solid companiesin less popular industries to go public throughan IPO. And, as conditions change, it isnot uncommon for deals to be delayed orcancelled late into a very expensive process.

The Reverse MergerAlternative to an IPOFor companies that should be public butcannot do so through a traditional IPO, a well-structured, well-supported reverse

2

TABLE 1

Public Companies Trade at a Premium

Private Public PublicValuation Ratio Company Company Company

Median Median Premium

Price/Net Sales 0.6 3.2 433%

Price/Gross Cash Flow 7.3 17.3 137%

Price/Net Income 7.0 23.9 241%

Source: Pratt’s Stats™ and Public Stats™ at www.BVMarketData.comValuation data based on 7,503 private company transactions and 1,233 public company transactions between 1/90 and 11/05. Universe restricted to transactions under $100 million.

added services that we provide is the worstof all worlds — a company has all the costsand obligations of a reporting public companywithout any of the benefits.

The shells that we acquire as principals andultimately provide to our clients are the firststep in our end-to-end value chain of services.We then link our capital raising, market-making, merger & acquisition and aftermarket support services to complete thechain. The end result is a highly valued and actively traded stock.

We don’t lay any claim to the stockholdervalue that has already been created by ourclient companies. Instead, we measure thevalue of our services by the differencebetween the market capitalization of thepublic company and the private market valueof the same company. As a rule of thumb, webelieve that we are able to increase existingstockholder value by 100% or more.

Like the shares owned by the management ofour portfolio companies, all the shares of thecompany’s stock that we own as principalsare restricted. This simple but powerful factensures that our interests are completely alignedwith the interests of our clients at all times. 3

merger can be a rational alternative. This isparticularly true for emerging firms withsolid financial qualifications and stronggrowth prospects.

A reverse merger takes far less time tocomplete than an IPO. A typical reversemerger into an already-trading public shelltypically takes 60 to 90 days to complete, andis not dependent on market conditions orprevailing investor sentiment. In contrast, anIPO can easily take a year or longer, involvinga significant diversion of management energyand corporate focus at a time when companiesneed to concentrate on maximizing theirbusiness potential and marketplace influence.

Our Mission: CreatingStockholder ValueOur business mission is to create substantial,incremental stockholder value for emerginggrowth companies by taking them publicthrough reverse mergers.

We are not in the business of buying andselling public company shells as commodities.Merging into a shell without all of the value-

TABLE 2

0

100

200

300

1997 1998 1999 2000 2001 2002 2003 2004 2005

IPO Activity

Total IPOsIPOs < $100 MMIPOs < $25 MM

Source: Hoover’s IPO Central. YTD information as of December 31, 2005.

4

Keating’s RigorousSuitability Criteria

inquiries from companies interested inlearning more about our turnkey reversemerger services. Because not every companyis equally suited for success in the publicmarkets, we have developed a proprietaryrisk analysis process for identifying privatecompanies that have the potential tobecome highly successful publicly tradedcorporations.

In evaluating potential clients, we weigh anumber of factors, such as a company’scompetitive position within its industry, itsintellectual property advantages, and theexperience and talents of its managementteam. Other considerations include itsgrowth potential and projected capitalrequirements.

On a qualitative basis, we seek two types ofcompanies — emerging firms in businesssectors that are positioned for dynamicgrowth and proven market leaders in stable industries. Additionally, we look formanagement teams that have demonstratedsuccess managing companies in the publicequity markets. We also focus on companieswith a large group of customers or affiliatesthat may want to participate in their successas a public stock.

But proven business plans and excitinggrowth stories are only parts of the equation.Candidate companies must clear a series ofquantitative hurdles. In particular, we wantto make certain that client companies will

qualify to trade on the AMEX or NASDAQwithin 12 months of going public. Thisensures that virtually any investor in theU.S. is eligible to purchase the stock.

The minimum qualifications we look for inclient companies can be summarized in ourCAPITAL qualification criteria checklist:

✦ Current shareholders’ equity of $2 million or more

✦ Annual growth in revenue and earnings of 20% or more during thepast two years

✦ People and management with solidexperience and track records of success in managing companies in the public markets

✦ Income of at least $1 million in thepast 12 months

✦ Trailing 12-month revenue of $10 million or more

✦ Audited balance sheets for the two

income and cash flow statements for

NASDAQ within 12 months of thetransaction (See Tables 3.1 and 3.2)

CAPITAL CHECKLIST

The CAPITAL qualification criteriachecklist above should be viewed as generalguidelines only. We are flexible and willingto consider private companies that do notmeet all of the CAPITAL checklistrequirements.

Every month we receive hundreds of

most recent fiscal years and audited

the three most recent fiscal years

✦ Listing eligibility for either AMEX or

5

TABLE 3.1 AMEX LISTING STANDARDS

Standard 1 Standard 2 Standard 3 Standard 4

Operating History N/A 2 years N/A N/A

Stockholders’ Equity $4 million $4 million $4 million N/A

Pre-tax Net Income* $750,000 N/A N/A N/A

Total Market Capitalization N/A N/A $50 million $75 million or

Total Assets N/A N/A N/A $75 million and

Total Revenues N/A N/A N/A $75 million

Minimum Price $3.00 $3.00 N/A $3.00

Market Value of Public Float $3 million $15 million $15 million $20 million

Distribution Alternatives 800 public stockholders and 500,000 shares publicly held or400 public stockholders and 1 million shares publicly held or400 public stockholders, 500,000 shares publicly held andaverage trading volume of 2,000 shares for last 6 months

*Net income requirement applies to previous year, or 2 out of the 3 most recent years.

TABLE 3.2 NASDAQ LISTING STANDARDS

Capital Market National Market System

Operating History 1 year and N/A 2 years and N/A

Stockholders’ Equity $5 million or $15 million $30 million N/A

Net Income* $750,000 or $1 million N/A N/A

Total Market Capitalization** $50 million N/A N/A $75 million or

Total Assets N/A N/A N/A $75 million and

Total Revenue N/A N/A N/A $75 million

Minimum Price $4.00 $5.00 $5.00 $5.00

Market Value of Public Float $5 million $8 million $18 million $20 million

Number of Stockholders 300 400 400 400

Number of Publicly-held Shares 1.0 million 1.1 million 1.1 million 1.1 million

Number of Market Makers 3 3 3 4

*Net income requirement applies to previous year, or 2 out of the 3 most recent years.

**If $50 million market capitalization requirement is satisfied for SmallCap, then there are no operating history, stockholders’ equity or netincome requirements.

Listing Standards

Domestic:Margie Blackwell

International:Luca Toscani

Rick Schweiger

Turnkey Solution

plan and financial statements todetermine whether the companyfits Keating’s suitability criteria

✦ Provide preliminary valuation advice✦ Provide capital structure advice✦ Identify Public Shells in Keating

inventory that are available forreverse merger

✦ Provide introductions to qualifiedand experienced small cap securitiesattorneys and accounting firms

✦ Provide preliminary information ontransaction overview and timeline

✦ Negotiate and finalize terms andpricing

(after signing LOI and payment of non-refundable commitment fee)

✦ Exchange and review due diligence information, includingbackground checks

✦ Provide Definitive Share ExchangeAgreement for exchange of public shell shares for privatecompany shares

✦ Manage the entire transaction and close the reverse merger

with review of required post-closing SEC filings

0

PHASE 11 22Transaction ExecutionOrigination

SERVICES

PEOPLE

TIME LINE(DAYS)

✦

✦

✦

✦

✦

✦

(Contemporaneous Step

✦ Review private company business

✦ Assist private company counsel

✦ Provide letter of intent (LOI) and/or FAA✦ Provide project plan and timeline

Jeff AndrewsRandy Haag

Steve HenricksReed MadisonSteve OsselloChris Wrolstad

Mike Keating

Justin DavisSong He

Tim KeatingPamela Solly

n

✦ Develop and launch company’s financial brand identity

✦ Create all online and offline content✦ Provide independent research guidance✦ Develop investor Web tool✦ Manage all facets of media relations✦ Launch comprehensive stock

promotion campaign✦ Prepare thorough investor kits✦ Provide all response to public inquiry

To Creating Stockholder Value Through A Keating Reverse Merger

✦ Assist with NASDAQ or AMEX listing application

✦ Assist with selection of AMEX

✦ File Form 211 with NASD, as necessary ✦ Make market for NASDAQ, OTC

➤150+

After Market Support

33 44 55Distribution Market-Making

Develop capital markets

Identify and evaluate variousfinancing alternativesArrange bridge loan financing,as required

placement memorandum (for PIPE) or prospectus (for registered public follow-onoffering)Assist with coordination of road showClose PIPE or follow-on offering

ps)

strategy with private company

Review private company private Bulletin Board or Pink Sheet stocks

specialist firm, if applicable

8

Costs The costs of going public include more than just the one-time fees associated with the reverse merger transaction. Companies also must consider the costs of raising capital and the ongoing expenses associatedwith being a public company.

*Excludes typical equity dilution cost of 7-10%. **Legal and audit fees are paid directly to those professional advisors.

Table 4.1 One Time Reverse Merger Transaction Fees (Cash)

Service Cost Comments/Assumptions

Investment Banking* $350,000 Includes cash “cost” of shell; excludes equity dilution

Legal** $50,000 Review of Letter of Intent & review/negotiation of Share Exchange Agreement

Audit** $50,000 Preparation of pro forma financials

Total $450,000 Add additional $100,000 in legal & audit fees for non-U.S. company

Table 4.2 Capital Raising Fees

Service Cost Comments/Assumptions

Placement Fee 10% Placement fee for PIPEs; discount for underwritings

Expense Allowance 3% Non-accountable expense allowance

Total 13%

Placement Warrants 10% Warrants equal to 10% of the number of securities placed

Table 4.3 Annual Ongoing Costs of Being a Public Company

Service Cost Comments/Assumptions

Legal $75,000 3 10-Q’s; 10-K; 8-K’s; review of press releases (add 50% for non-U.S.)

Audit $100,000 Assumes large regional firm; add 50% for Big 4 (add 50% for non-U.S.)

Directors’ Fees $45,000 $15,000 per director x 3 non-executive directors

Independent Research $30,000 Upfront payment for initial report + 3 follow-up reports

D&O Insurance $70,000 $5 million of coverage

After Market Support $600,000 See Table 4.4 for details

Total $920,000

Table 4.4 After Market Support Annual Costs

Service Cost Comments/Assumptions

Keating AMS $120,000 Management and administration of after market support program

Financial Marketing Initiatives $480,000 Partner marketing services, Website development and news distribution

Total $600,000

9

After Market Support

0

0%

25%

6 12 18 24

Months

Prog

ram

Foc

us

50%

75%

100%

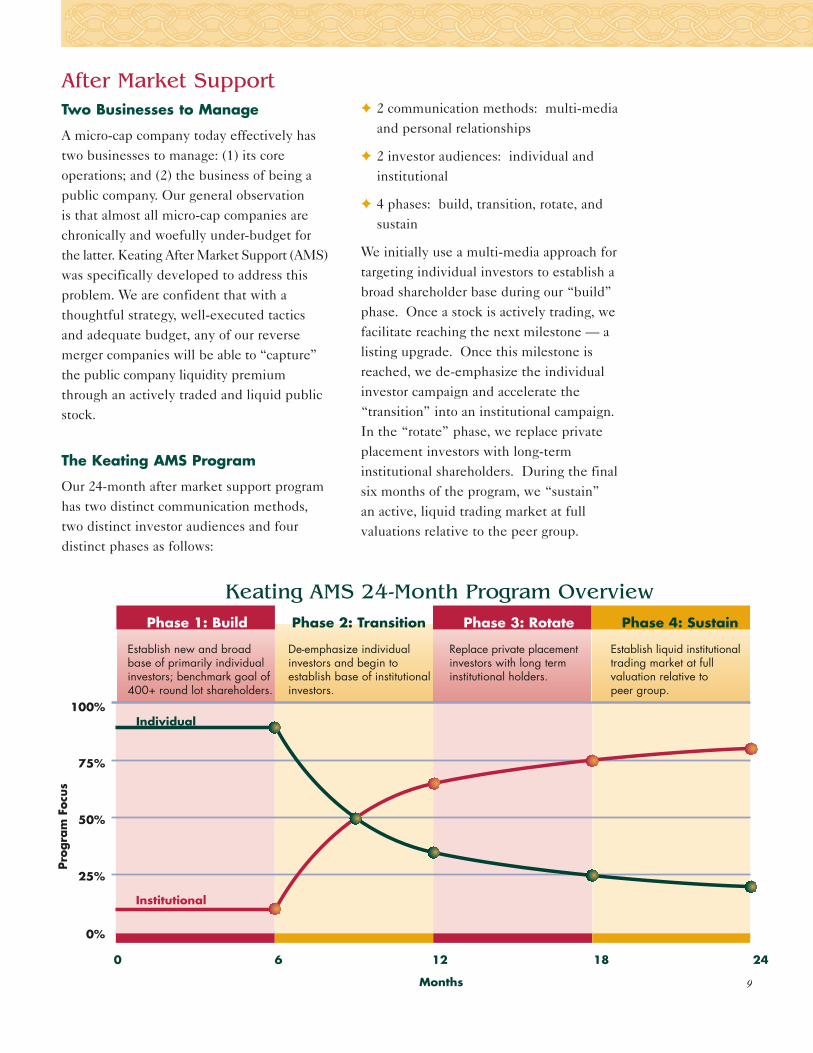

Keating AMS 24-Month Program OverviewPhase 1: Build Phase 2: Transition Phase 3: Rotate Phase 4: Sustain

Establish new and broadbase of primarily individual investors; benchmark goal of 400+ round lot shareholders.

De-emphasize individual investors and begin to establish base of institutional investors.

Replace private placementinvestors with long term institutional holders.

Establish liquid institutional trading market at full valuation relative to peer group.

Individual

Institutional

✦ 2 communication methods: multi-mediaand personal relationships

✦ 2 investor audiences: individual and institutional

✦ 4 phases: build, transition, rotate, and sustain

We initially use a multi-media approach fortargeting individual investors to establish abroad shareholder base during our “build”phase. Once a stock is actively trading, wefacilitate reaching the next milestone — alisting upgrade. Once this milestone isreached, we de-emphasize the individualinvestor campaign and accelerate the

In the “rotate” phase, we replace privateplacement investors with long-term institutional shareholders. During the final

an active, liquid trading market at full valuations relative to the peer group.

Two Businesses to Manage

The Keating AMS Program

Our 24-month after market support programhas two distinct communication methods,two distinct investor audiences and four distinct phases as follows:

A micro-cap company today effectively hastwo businesses to manage: (1) its core operations; and (2) the business of being apublic company. Our general observation is that almost all micro-cap companies arechronically and woefully under-budget for

was specifically developed to address this problem. We are confident that with a thoughtful strategy, well-executed tactics and adequate budget, any of our reverse

the public company liquidity premium through an actively traded and liquid public stock. “transition” into an institutional campaign.

six months of the program, we “sustain”

merger companies will be able to “capture ”

the latter. Keating After Market Support (AMS)

10

Keating’s Team of Registered Professionals

Series 5, 7, 24, 27, 55, 63, 66

Timothy J. Keating, President

Before founding KeatingInvestments in 1997, Tim Keatingheld senior management positionsin the equity and equity derivativedepartments of Bear Stearns,Nomura and Kidder, Peabody in both London and New York.He is a 1985 cum laude graduateof Harvard College with an A.B. in economics.

Founder and President

Series 7, 24, 55,63, 66

Kyle L. Rogers, Partner

Formerly a senior analyst forGoldman Sachs & Co.’s PrivateWealth Management Division,Kyle began his career in institutional sales with that firm’s Fixed Income, Currency & Commodities Division. Heearned a B.A. in governmentfrom Dartmouth College, where he was captain of the varsity football team.

Kelley N. Boland, Associate

Kelley Boland began her career asa private attorney with Dieterichand Associates in Los Angeles,specializing in securities law andcorporate litigation. She earned aB.A. in political science from theUniversity of Michigan, and a J.D.from the University of San DiegoSchool of Law. She is a memberof the State Bar of California andthe State Bar of Colorado.

Series 7, 66

Luca Toscani, Partner

Luca was formerly a hedge fundmanager with Medici CapitalManagement and an arbitragetrader at Bear Stearns in London.He graduated summa cum laudefrom Venice University in Italy,with a degree in economics andbusiness. He also has two yearsof study at Warwick Universityand University College London.

Operations Origination

Series 7, 24, 63

Margie L. Blackwell, Partner

Formerly with Tele-Communications, Inc. for eleven years, Margie hasnegotiated and structured 23reverse merger transactions andpublic shell acquisitions sincejoining Keating Investments in 2000. She is also a member of the National InvestmentBanking Association.

Series 7, 63

Laney Meyer, Compliance Officer

Laney formerly served asAssociate General Counsel atCentrix Financial, LLC handlinglitigation and compliance. Shebegan her legal career as anAssociate at Wolf & Slatkin, P.C. She holds a J.D. from theUniversity of Denver School ofLaw, a B.A. from Colorado StateUniversity and is currently workingtowards her MS in TechnicalCommunication.

Pending

11

Series 7, 66

Jeff L. Andrews,Senior Vice President

Jeff Andrews joined Keating in 2003 after three years as afinancial advisor with UBS. He is currently a board member ofKUSA-TV’s 9Kids Who Care and the University of Denver’sBridge Project. He earned a B.A.in English and political sciencefrom Tufts University and wascaptain of the ski team.

Series 7, 63

Steven J. Ossello

Steve was formerly principal for W&O Enterprises, LLC. In addition to other roles, he was president of Children’sTechnology Group, Inc. and co-founded and held executivepositions at Golden Capital andAlpine Gaming, Inc. He beganhis career at PaineWebber, Inc.after earning a B.B.A. fromGonzaga University.

Series 7, 63

Randy J. Haag

Before joining Keating, Randywas founder and CEO ofWebAccommodate Systems. Hewas previously president andCEO of Spark Online, boardmember of Double EagleSystems and in 1992 foundedHaag & Associates. He began his career with E.F. Hutton afterreceiving a B.S. in BusinessFinance from San Diego StateUniversity.

Series 7, 63

Steven J. Henricks

Steve Henricks was formerlypresident of Equity FundingGroup, a corporate finance firmproviding capital raising and M & A consulting services.Previously, he held investmentsales positions with L.F.Rothschild and Drexel Burnham.He earned an M.B.A. fromSuffolk University and a B.S. inbusiness administration fromState University of New York.

Series 7, 63

Christopher S. Wrolstad

Chris Wrolstad has 16 yearsexperience in entrepreneurialfinance and operations includingprincipal roles in startup companies and a corporate VP role with Century Casinos,Inc. He began his career as an investment executive withPaineWebber and holds a B.S.degree from Gonzaga University.

Series 7, 24, 63, 65

H. Reed Madison

Reed Madison recently served aspresident of Madison Financial,LLC, advising early stagegrowth companies. He began his investment career withShearson/American Express in1984. He earned a B.S. from theUniversity of Montana where he was also an Academic All-American football player.

Distribution

12

Series 7, 24, 55, 63

Series 7, 63

Song He, Vice President

Song was formerly a regionalmarketing manager for a telecomprovider in China and a businessanalyst for a Chinese public company. A CPA, Song has anM.S. in Accountancy and anM.B.A. from the University ofIllinois at Urbana-Champaign,and an electrical engineeringdegree from Wuhan Universityof Technology in China.

Series 7, 63

Pamela A. Solly, Vice President

Pamela Solly joined KeatingInvestments in 2004 after 15 years of legal and financeexperience with Cyprus AmaxMinerals Company. She is a 1996 graduate of the Universityof Denver, Masters ofInternational Managementdegree and a 1988 graduate of Regis University, B.S. degreein business administration.

Market-Making

Justin K. Davis, Vice President

Justin joined Keating in 2005after managing financial servicesfor the National Park Service.He was formerly marketing manager for ServiceMagic.comand a philanthropic programdirector. He holds an M.B.A.from the University of Virginia(Darden) and a B.A. in economicsfrom Vanderbilt University.

Michael J. Keating, Senior Vice President

Mike was formerly a financialadvisor with Financial NetworkInvestment Corp. in Virginia,and with Westport ResourcesInvestment Services inConnecticut. He began hiscareer as an institutional currency broker. He graduatedfrom Boston College’s CarrollSchool of Management with aB.S. in finance.

Series 7, 63

Frederic M. Schweiger

Rick was most recently CFO andgeneral counsel for Old WorldIndustries, Inc. He was also director for Boucher Auto Groupand an attorney with Mulcahy &Wherry. He graduated magna cumlaude from the University of NotreDame (Accounting), MarquetteUniversity Law School and New York University Law School (LLM Taxation).

Transaction Execution

Pending

After Market Support

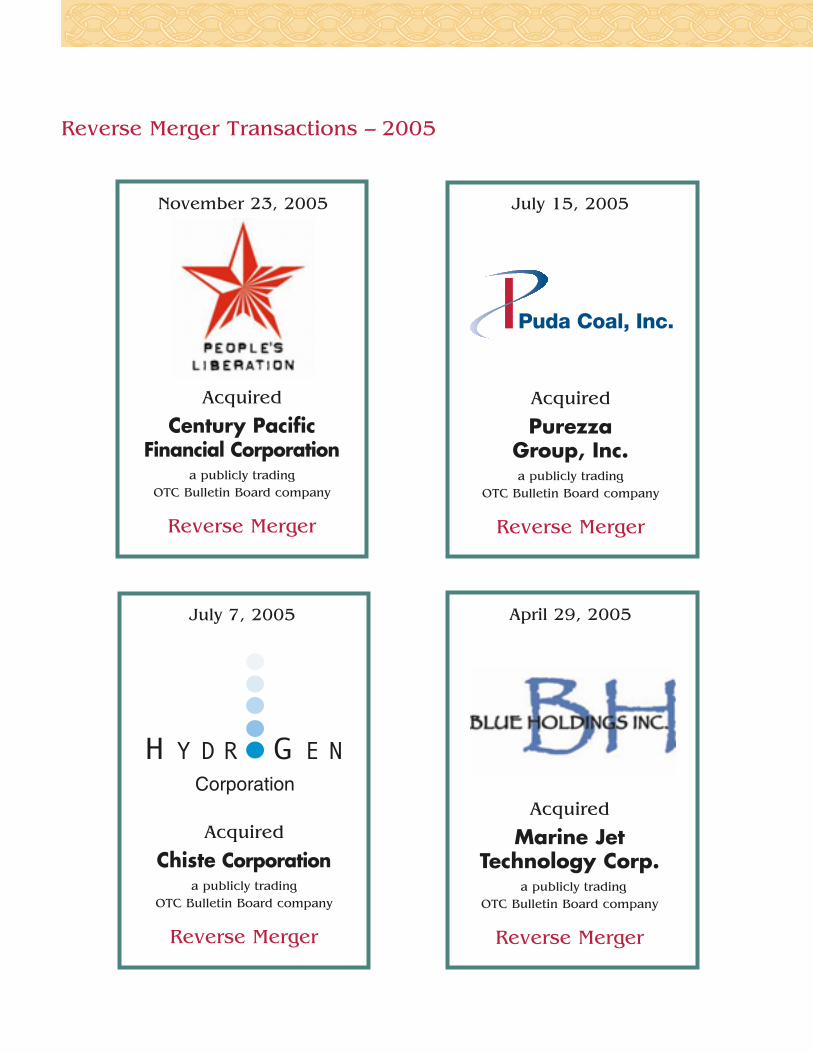

Reverse Merger Transactions – 2005

April 29, 2005

Acquired

Marine Jet Technology Corp.

a publicly trading OTC Bulletin Board company

Reverse Merger

July 15, 2005

Acquired

Purezza Group, Inc.a publicly trading

OTC Bulletin Board company

Reverse Merger

July 7, 2005

Acquired

Chiste Corporationa publicly trading

OTC Bulletin Board company

Reverse Merger

November 23, 2005

Acquired

Century Pacific Financial Corporation

a publicly trading OTC Bulletin Board company

Reverse Merger

Corporation

5251 DTC Parkway, Suite 1090Greenwood Village, Colorado 80111-2739(720) 889-0139 ✦ Fax: (720) 889-0135

150 California Street, Suite 610San Francisco, California 94111

(415) 433-1800 ✦ Fax: (415) 399-9709

www.keatinginvestments.com