Embed Size (px)

Citation preview

Review

Review Item

An firm has a project with NPV>0 that costs a lot of money.

It pays off after the owner dies. Should she invest? In the project? In

financial assets? How?

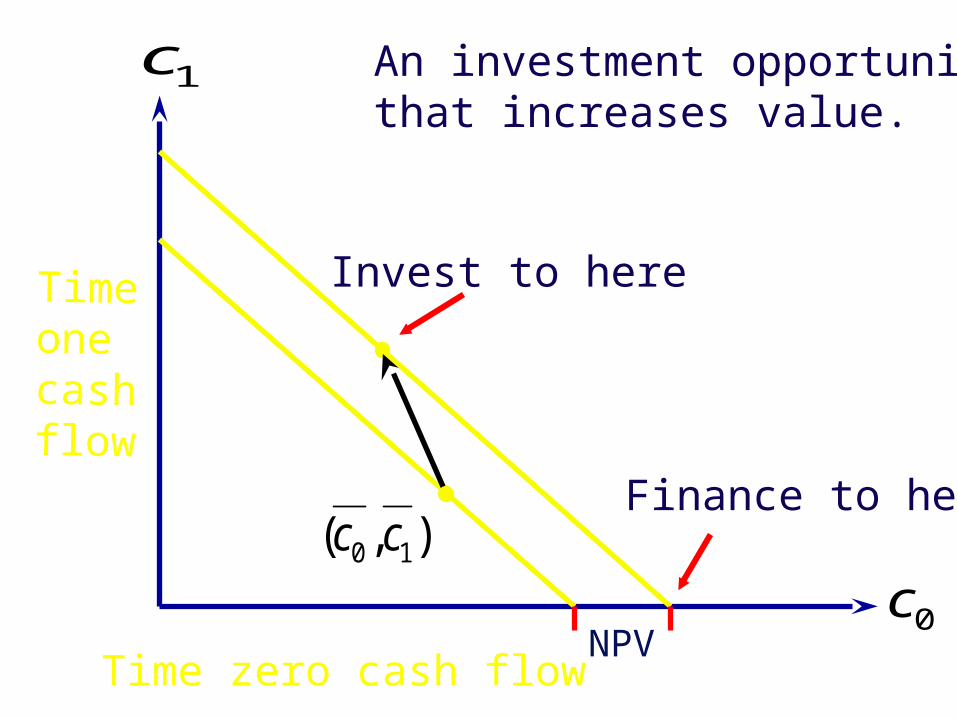

0c

1c

),( 10 cc

Time zero cash flow

Timeonecashflow

An investment opportunity that increases value.

NPV

Invest to here

Finance to here

Review item

What is the interest rate?

Don’t write

The interest rate is the time value of money.

Do write:

The interest rate is the premium for current delivery of money.

P0 is the price of current money in current money, namely 1.

P1 is the price of time-one money in terms of current money, something <1.

P 11

0 P

Pr

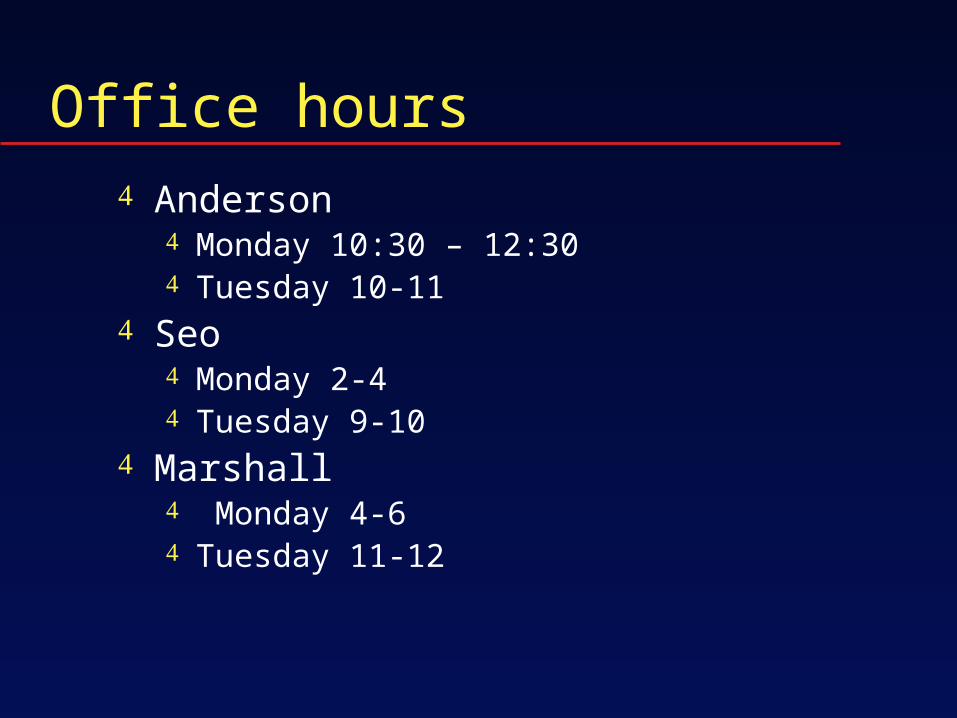

Office hours Anderson

Monday 10:30 – 12:30 Tuesday 10-11

Seo Monday 2-4 Tuesday 9-10

Marshall Monday 4-6 Tuesday 11-12

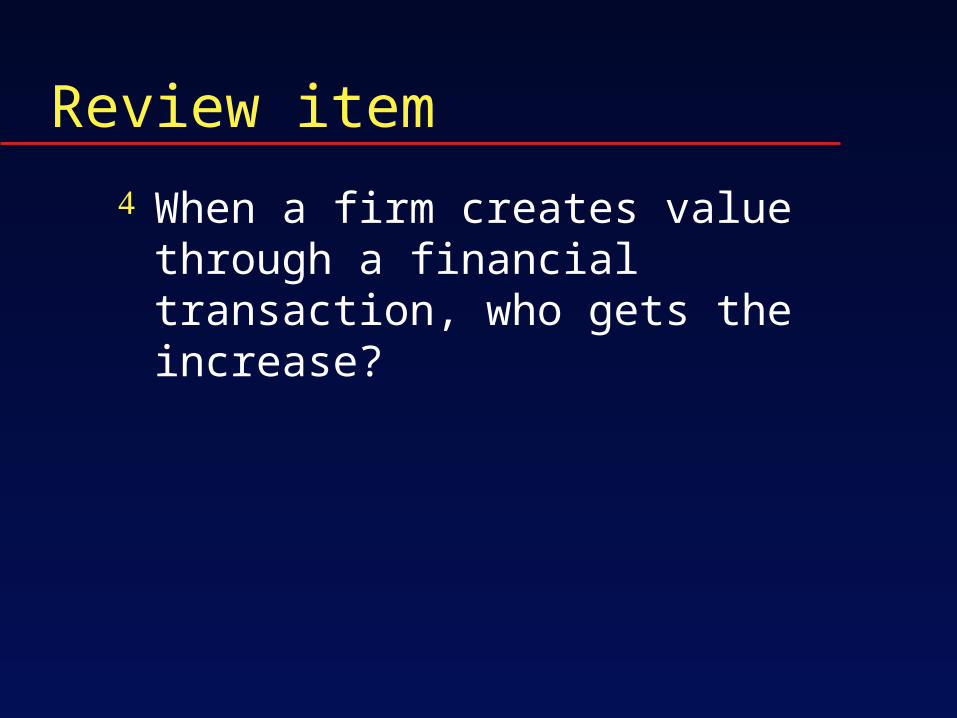

Review item

When a firm creates value through a financial transaction, who gets the increase?

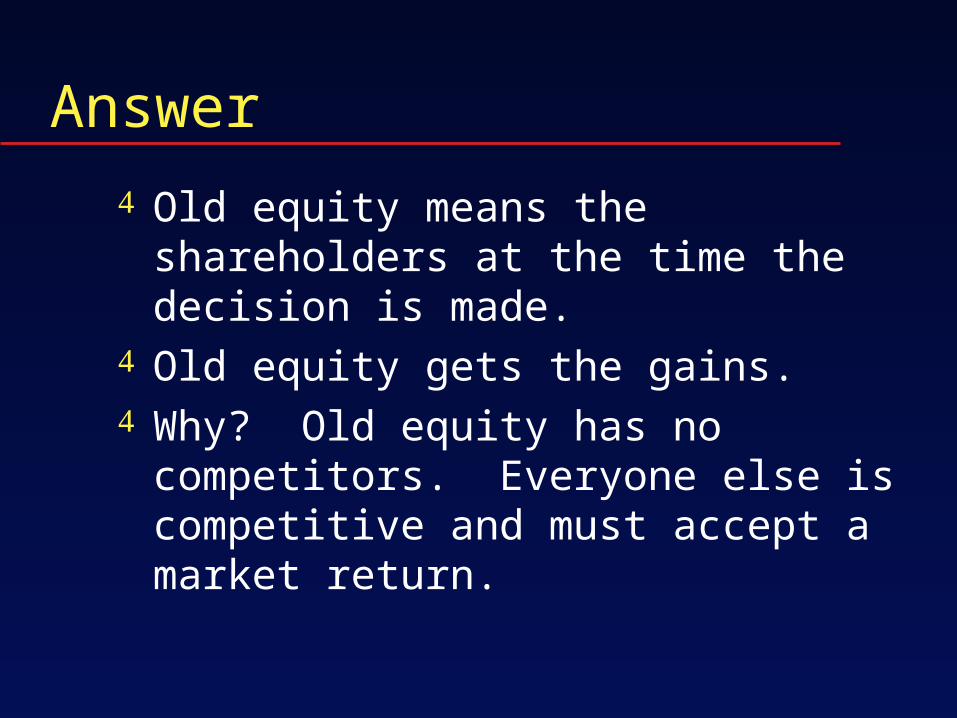

Answer

Old equity means the shareholders at the time the decision is made.

Old equity gets the gains. Why? Old equity has no competitors.

Everyone else is competitive and must accept a market return.

Review item

Two assets have the same expected return.

Each has a standard deviation of 2%. The correlation coefficient is .5. What is the standard deviation of an

equally weighted portfolio?

Answer

Var P = .5x.5x4+.5x.5x4+2x.5x.5x.5x2x2

= 3 Standard deviation = sq. root of 3 =1.732

Review item

A firm has a project with positive NPV. The project costs 100M to start. The firm has only 50M. What should it do?

Answer

Raise the money in the capital market. It can because NPV is market

valuation.

EPS and ROE under Proposed Capital Structure

Shares Outstanding = 240

Recession Expected Expansion

EBIT $1,000 $2,000 $3,000

Interest 640 640 640

Net income $360 $1,360 $2,360

EPS $1.50 $5.67 $9.83

ROA 5% 10% 15%

ROE 3% 11% 20%

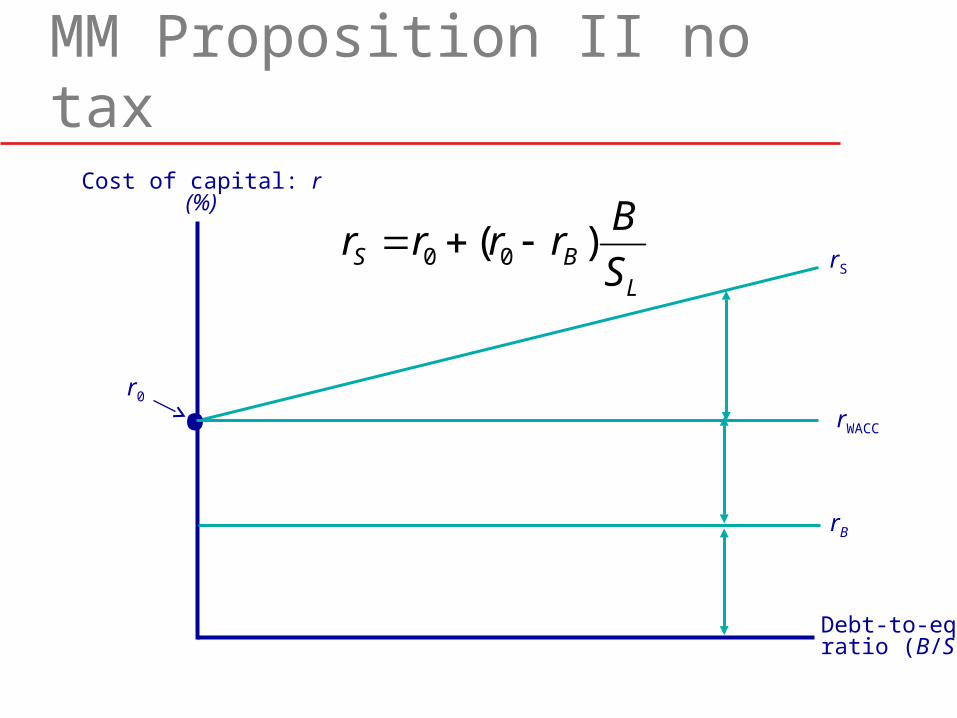

Proposition II of M-M

rB is the interest rate

rs is the return on (levered) equity r0 is the return on unlevered equity

B is value of debt SL is value of levered equity

rs = r0 + (B / SL) (r0 - rB)

MM Proposition II no tax

Debt-to-equityratio (B/S)

Cost of capital: r(%)

.r0

rS

rWACC

rB

LBS S

Brrrr )( 00

MM II (with taxes)

Corporate taxes, not personal rB = interest rate rS = return on equity r0 = return on unlevered equity B = value of debt SL = value of levered equity Previously, without taxes

rS = r0 + (B/SL)(r0 - rB)

Effect of tax shield

Increase of equity risk is partly offset by the tax shield

rS = r0 + (1-TC)(r0 - rB)(B/SL) Leverage raises the required return less

because of the tax shield.

MM II and WACC

Debt-to-equityratio (B/S)

Cost of capital: r(%)

.r0

rS

rB.0.200=

0.100

. rWACC

.0.2351

200370

Optimal Debt and Value

Debt (B)

Value of firm (V)

0

Present value of taxshield on debt

Present value offinancial distress costs

Value of firm underMM with corporatetaxes and debt

VL=VU+TCB=

V=Actual value of firm

VU=Value of firm with no debt

B*

Maximumfirm value

Optimal amount of debt

ChannelsOperating CashFlows = $1

Debtchannel

Equitychannel

TC

(1-TC)(1-TS)

TB

1 - TB

TS

Value asequity

Value asdebt

Operating C.F.’s ofthe whole economy

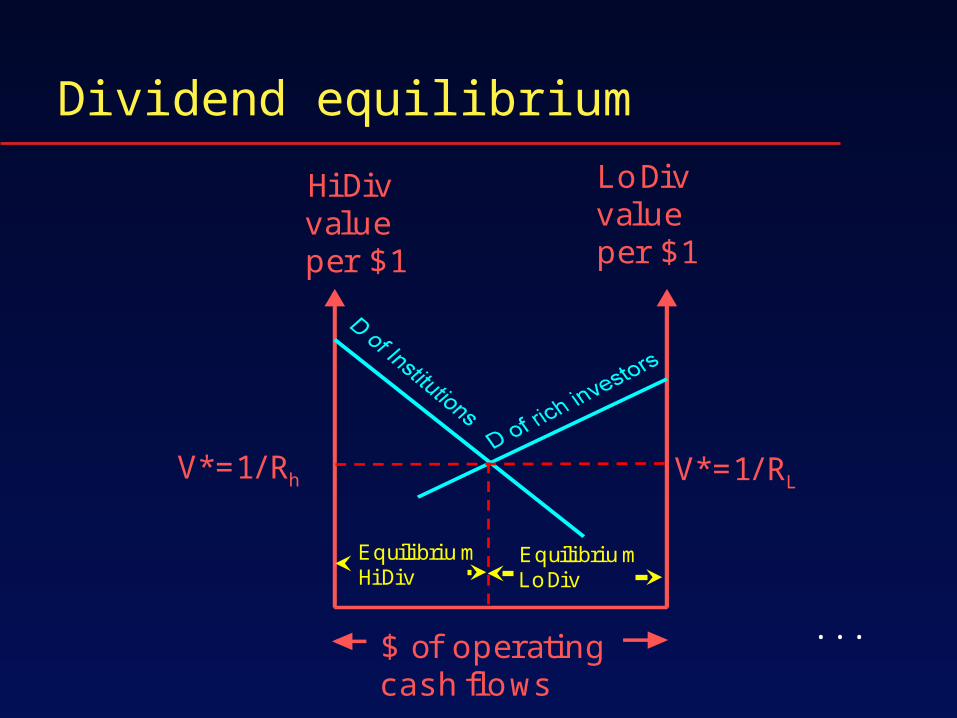

D of Institutions D of rich investors

V* = 1/RB V* = 1/RS

asdebt

as equity

Miller: Tax-class clienteles

Value asequity

Value asdebt

Operating C.F.’s ofthe whole economy

tax reform

increaseddebt

...

Separation theorem interpreted for dividends (Figure 18.4)

C1

C0

s lo p e = - (1 + r)

L o w -d iv id e n d firm

H ig h -d iv id e n dfirm

w

F u tu rere tu rno r

d iv id e n d n o

Dividend equilibrium

$ of operatingcash flows

HiDivvalueper $1

LoDivvalueper $1

mq ili riuo iv

EL

mEquilibriuHiD iv

u bD

V*=1/Rh V*=1/RL

...

Review item

What is the weighted average cost of capital?

Answer

Give the definitions and the formula. rB = bond rate

rS = expected return on shares

B = market value of bonds S = market value of shares TC = corporate tax rate

Pay-off pitch

rWACC =(S/(S+B))rS + (B/(S+B))(1-TC)rB

Now say that it applies when (1) the physical project has the same

risk as the firm (2) it is financed like the firm.

Review item

Does a good project have IRR greater than the hurdle rate, or less?

Answer

IRR is the discount rate that makes NPV(IRR) = 0.

The hurdle rate is the market rate for the risk-class.

Investing means cash flows are first negative, then positive.

Financing (in this context) means cash flows are first positive, then negative.

More answer

Other sign patterns, IRR is not useful. Investing, a good project has IRR >

hurdle rate. Financing, a good project has hurdle

rate > IRR.

![Chinese Oilfield Review Winter 2000 - Schlumberger 2000/p2_9.pdf · 2000/2001 3 [1] NPV [2] 6 [3] NPV [4] 1. Newendorp PD: Decision Analysis for Petroleum Exploration Aurora Planning](https://img.pdfslide.net/doc/110x75/5b4a31eb7f8b9a5c278c05a5/chinese-oilfield-review-winter-2000-2000p29pdf-20002001-3-1-npv-2.jpg)