Embed Size (px)

Citation preview

TAX ISSUES

17 September 2014

Titre de la présentation1

A focus on ownership

structures

Date2 Titre de la présentation

AGENDA

Tax and other considerations

1. South Africa

- (Re)structuring the SA Group

-Exit strategy

2. Cross-border

-Tax considerations for cross-border investments

- Funding

- Exchange control

- Transfer pricing

Date3 Titre de la présentation

TAX AND OTHER CONSIDERATIONS

SOUTH AFRICA

Date4 Titre de la présentation

01

Date5 Titre de la présentation

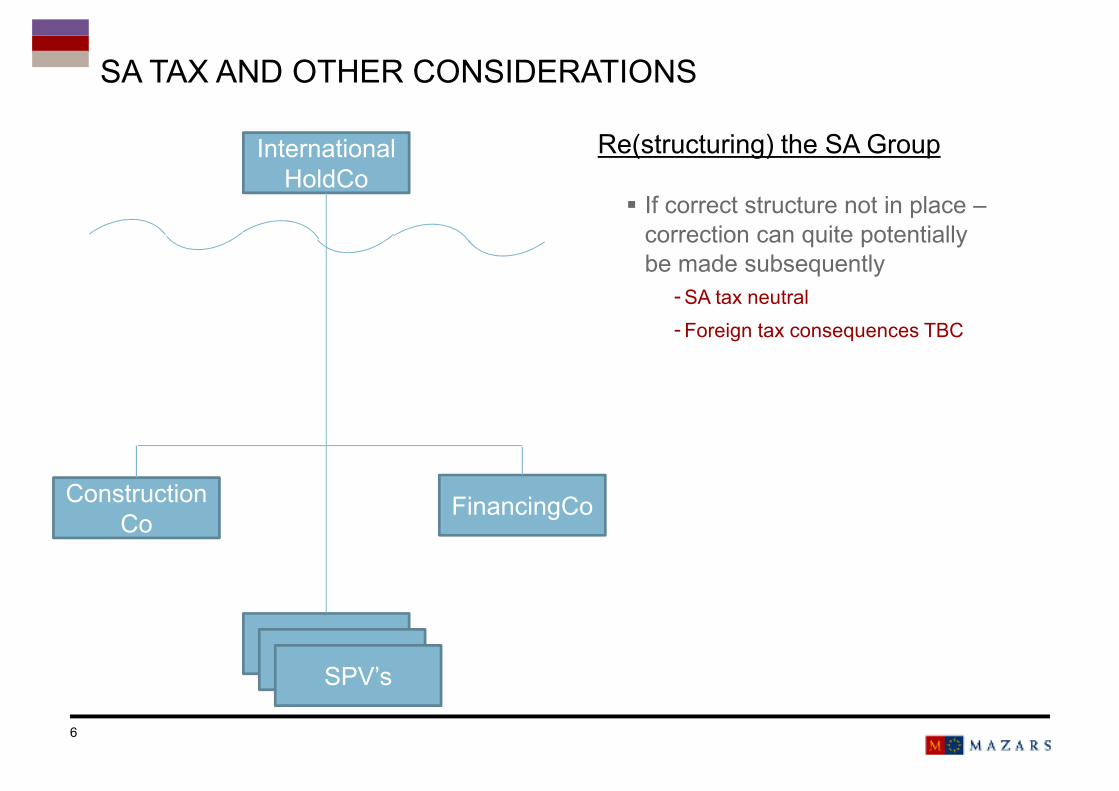

SA TAX AND OTHER CONSIDERATIONS

Re(structuring) the SA Group

� Advisable to have a single SA

Holdco

-Single point of entry (and exit)

-Offshore funding structure

simplified to one entity

� Organise other companies as

sub’s

-SPV HoldCo

-Construction Co (local content

requirement)

-Financing Co (?)

� Structure allows for

BEE/Community Trust at any

given level required

International

HoldCo

SA HoldCo

SPV HoldCoConstruction

CoFinancingCo

SPVSPVSPV’s

Trust

Bidding

rights

Capital/loan/

prefs

Date6 Titre de la présentation

SA TAX AND OTHER CONSIDERATIONS

Re(structuring) the SA Group

� If correct structure not in place –

correction can quite potentially

be made subsequently

-SA tax neutral

-Foreign tax consequences TBC

International

HoldCo

Construction

CoFinancingCo

SPVSPVSPV’s

Date7 Titre de la présentation

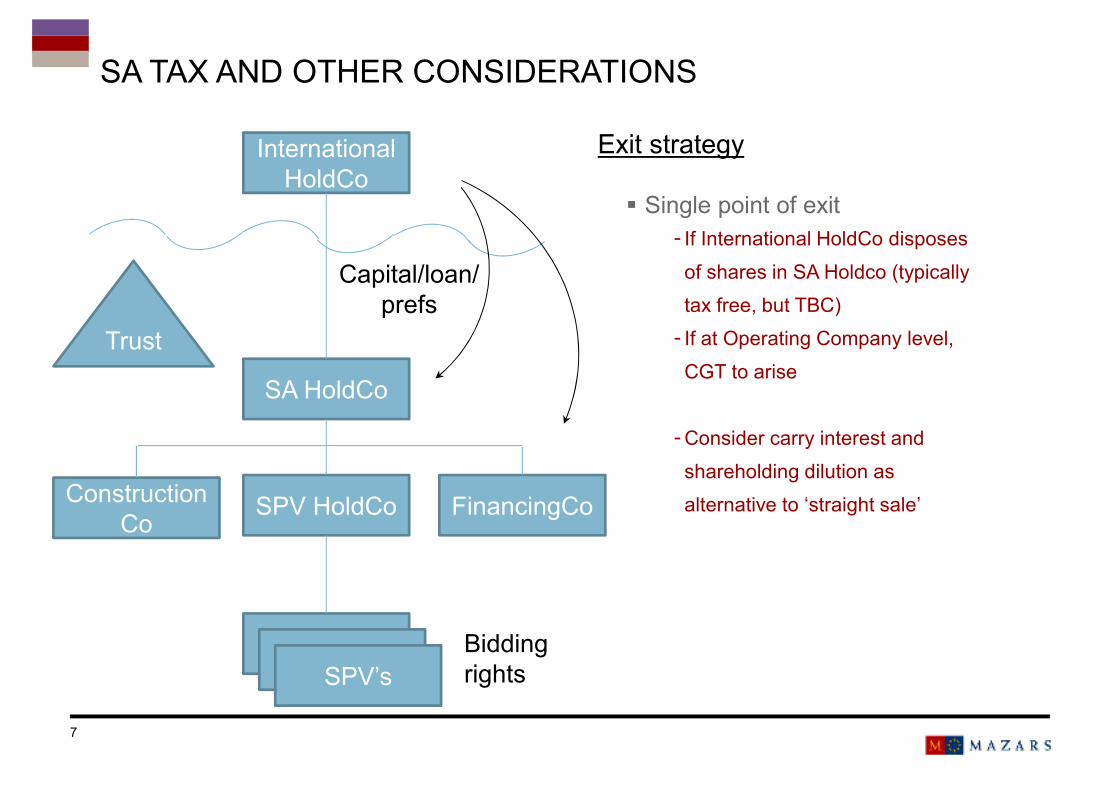

SA TAX AND OTHER CONSIDERATIONS

Exit strategy

� Single point of exit

- If International HoldCo disposes

of shares in SA Holdco (typically

tax free, but TBC)

- If at Operating Company level,

CGT to arise

-Consider carry interest and

shareholding dilution as

alternative to ‘straight sale’

International

HoldCo

SA HoldCo

SPV HoldCoConstruction

CoFinancingCo

SPVSPVSPV’s

Trust

Bidding

rights

Capital/loan/

prefs

Date8 Titre de la présentation

02

TAX AND OTHER CONSIDERATIONS

CROSS-BORDER

Date9 Titre de la présentation

Tax considerations for cross-border investments

� Funding

-Thin capitalisation

- Draft IN and EBITDA

- No safe harbour

-Hybrids

-WHTs and DTAs

-Limitation on excessive interest

� Exchange control

� Transfer pricing

-Debt

-Other related party fees

International

HoldCo

SA HoldCo

SPV HoldCoConstruction

CoFinancingCo

SPVSPVSPV’s

Trust

Bidding

rights

Capital/loan/

prefs

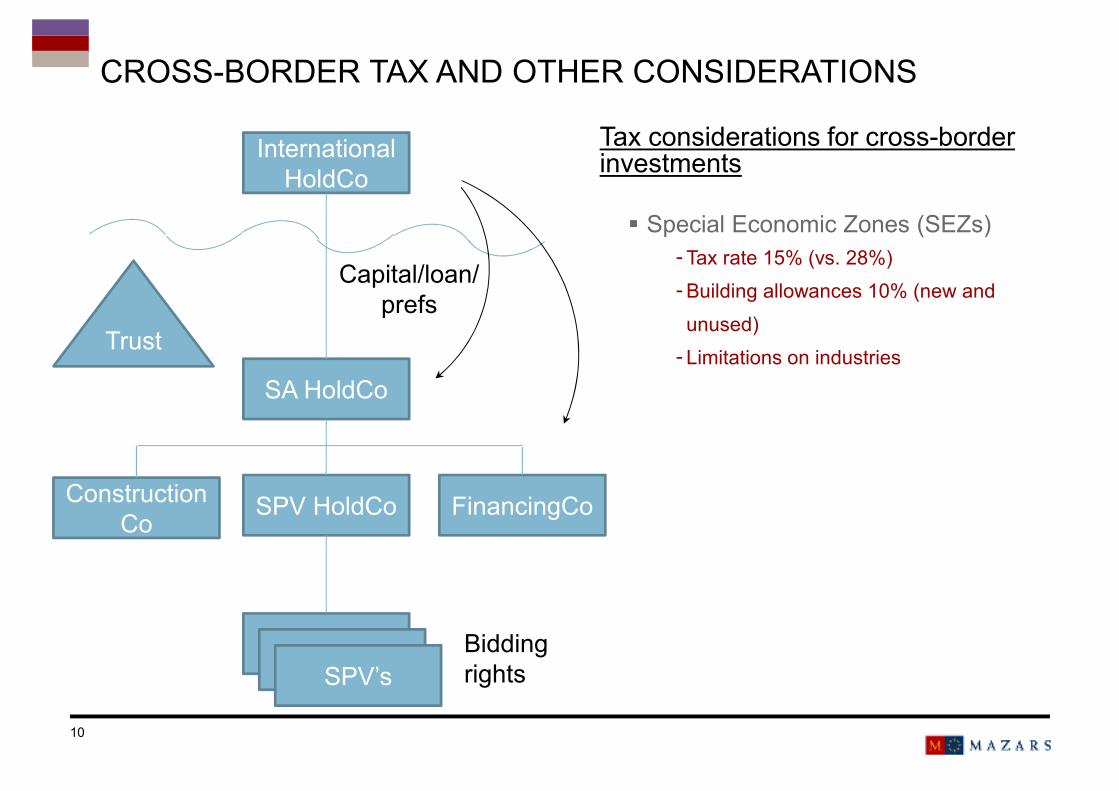

CROSS-BORDER TAX AND OTHER CONSIDERATIONS

Date10 Titre de la présentation

Tax considerations for cross-border investments

� Special Economic Zones (SEZs)

-Tax rate 15% (vs. 28%)

-Building allowances 10% (new and

unused)

-Limitations on industries

International

HoldCo

SA HoldCo

SPV HoldCoConstruction

CoFinancingCo

SPVSPVSPV’s

Trust

Bidding

rights

Capital/loan/

prefs

CROSS-BORDER TAX AND OTHER CONSIDERATIONS

Date11 Titre de la présentation

Date12 Titre de la présentation

Questions

DateTitre de la présentation13

Mazars is present in 5 continents.

CONTACT

Mazars South Africa

Mazars House

Rialto Road

Grand Moorings Precinct

Century City

7441

Tel. +27 (0) 21 818 5000

Fax +27 (0) 21 818 5001