Embed Size (px)

Citation preview

Revised Current Cost Financial Statements 2015 including Openreach Undertakings

Ofcom Statement on BT’s Current Cost Financial Statements 2015

Introduction

BT published the 2014/15 regulatory financial statements (RFS) on 31 July 2015. Our review

of the RFS identified a number of errors. To address these and other errors, BT has issued

revised 2014/15 RFS.

On 6 November we opened an investigation into BT’s apparent non-compliance with SMP

conditions 13A.8 and 8A.8, which require BT to publish reconciliation reports and

corresponding audit opinions (the “Reconciliation Report”) in relation to its RFS. On 30

November we confirmed our decision that BT had contravened, and was continuing to

contravene these conditions.

BT’s reporting obligations

BT’s reporting obligations arise out of market reviews conducted by Ofcom and SMP

Conditions and Directions related to regulatory reporting1 Under such SMP Conditions BT

is required to publish with the audited RFS any written statement made by Ofcom and

provided to BT commenting on the data in the notes to or the presentation of any or all of

the RFS, the Reconciliation Report and/or the Accounting Methodology Document.

While responsibility for the preparation of the RFS rests with BT, Ofcom believes that such

a statement can be helpful to users of the RFS by drawing attention to important aspects

of BT’s 2014/15 RFS and the outcomes of our review of BT’s regulatory reporting concluded

in May 2014 (the “Regulatory Reporting Review”) . We required BT to include a statement

with the RFS published on 31 July (our “July Statement”) and have required BT to include

this updated statement from Ofcom with the revised RFS.

Revised 2014/15 Regulatory Financial Statements

In our July Statement, we noted that as a result of issues that we and BT had identified, BT

issued a list of errata and corrections to its 2013/14 RFS. We said that we hoped this would

not be necessary for 2014/15.

However, we subsequently identified some errors in the 2014/15 RFS and BT discovered

some further issues during the preparation of its Reconciliation Report.

1 Some obligations also arise from the Undertakings given by BT under the Enterprise Act

2002. 2 Further information about our investigation is available at Further information about

our investigation is available at

In our July Statement, we explained that BT must now publish and notify Ofcom in advance

of any changes that it intends to make to its allocation methodologies (the “Change Control

Notification”). We noted that one of the changes in the Change Control Notification related

to BT’s proposed treatment of Excess Construction Charges (ECCs). We explained that we

had raised some concerns with BT regarding the appropriateness of this treatment, but

explained that BT considered that its proposed treatment was appropriate and had

adopted it in its 2014/15 RFS. This statement was based on information provided to us by

BT. However, it later became apparent that BT had not reflected the proposed treatment

in the 2014/15 RFS as £1.5m of costs had not been attributed to connection services. The

description in our July Statement was therefore incorrect.

We also identified several errors in the accounts as originally published. BT describes these

in Section 2.1.7 below. The largest error relates to the disclosure of eliminations of EOI

charges within residual markets.

Following discussions with Ofcom, BT decided to reissue the 2014/15 RFS to address these

errors.

The Reconciliation Report

Under SMP conditions 13A.8(vi) and 8A.8(vi), BT is required to publish the Reconciliation

Report setting out the changes it has made to its regulatory accounting methodology and

material errors it has corrected, and the impact of those changes and errors on the RFS.

The Reconciliation Report must be published within four months of the end of the financial

year to which it relates i.e. by 31 July. In our July Statement we noted that BT had said that

it would not meet this deadline for financial year 2014/15.

On 6 November we opened an investigation into BT’s apparent non-compliance with SMP

conditions 13A.8(vi) and 8A.8(vi). On 30 November we issued a ‘confirmation decision’ to

BT under section 96C of the Communications Act 2003, stating that we were satisfied that

BT had contravened and was continuing to contravene those SMP conditions and requiring

BT to publish the Reconciliation Report by 4 December 20152.

http://stakeholders.ofcom.org.uk/enforcement/competition-bulletins/open-cases/all-open-cases/cw_01171/

Ofcom Statement on BT’s Current Cost Financial Statements 2015

Update to our July Statement

The remainder of this statement contains the points raised in our July Statement which we

have updated where necessary.

The Regulatory Reporting Review

In the Regulatory Reporting Review, Ofcom made a number of changes to BT’s regulatory

reporting requirements. These were intended to give Ofcom a greater role in determining

the way that BT prepares its RFS, to improve the presentation of the RFS and supporting

documentation and to ensure that Ofcom and other stakeholders have the information

that they need.

Changes to the basis of preparation

Changes to the basis of preparation introduced for 2014/15 include new Regulatory

Accounting Principles (including the requirement for consistency with regulatory decisions)

and the requirement for BT to prepare its RFS on a regulatory asset value adjusted current

cost basis.

The RFS are produced by BT on the basis described in its new Accounting Methodology

Document3, which sets out amongst other things BT’s Attribution Methods and Accounting

Policies.

Additional Reporting Requirements in 2014/15

The 2014/15 RFS reflect the directions we made in our March 2015 Statement (Directions

for Regulatory Financial Reporting)4. These include revised formats for several of the

3 http://www.btplc.com/Thegroup/RegulatoryandPublicaffairs/Financialstatements/2015/AccountingMethodologyDocument201415.pdf 4 http://stakeholders.ofcom.org.uk/binaries/consultations/financial-

reporting/statement/statement.pdf 5 http://www.btplc.com/Thegroup/RegulatoryandPublicaffairs/Financialstatements/2015/ChangeControlNotification-31March2015.pdf

schedules and the requirement for BT to prepare its RFS on a regulatory asset value

adjusted current cost basis.

It is important that BT retains responsibility for its RFS and can respond to changes in

circumstances when deciding how best to prepare them. However, as noted above, for the

first time in 2014/15, BT must now publish a Change Control Notification. The Change

Control Notification must be accompanied by a description of each of the changes, the

reason for making the changes and their impact on the RFS (based on the prior year RFS).

Where in Ofcom’s opinion a proposed change does not comply with any SMP Conditions

or the Regulatory Accounting Principles, Ofcom can direct BT not to make such change.

BT published its 2014/15 Change Control Notification on 31 March 2015.5 This set out the

changes that BT considered to be necessary to reflect the new reporting requirements that

followed the Fixed Access Market Review6 and the Wholesale Broadband Access Market

Review7, and other changes to reflect changes in circumstances identified by BT.

We discussed the Change Control Notification with BT. Following these discussions, BT

decided not to implement one of its proposed changes (described in the Change Control

Notification as “BT TSO Electricity”) and amended some other changes. These changes

should be reflected in BT’s Reconciliation Report.

As explained above, one of the changes in the Change Control Notification related to BT’s

proposed treatment of ECCs. BT considers that its proposed treatment is appropriate and

has now adopted it in the revised 2014/15 RFS. We have made a proposal for reporting of

ECCs in the Leased Lines Charge Control consultation issued on 12 June 20158. Depending

on stakeholder comments we may direct BT to change the way that it reports ECCs in future

RFS.

6 http://stakeholders.ofcom.org.uk/telecoms/ga-scheme/specific-conditions-entitlement/market-power/fixed-access-market-reviews-2014/statement/ 7 http://stakeholders.ofcom.org.uk/binaries/consultations/review-wba-

markets/statement/WBA-Statement.pdf 8 http://stakeholders.ofcom.org.uk/binaries/consultations/llcc-dark-fibre/summary/llcc-

dark-fibre.pdf

Ofcom Statement on BT’s Current Cost Financial Statements 2015

Cost Attribution Review

In the Regulatory Reporting Review, we explained that we would review BT’s existing

attribution rules against the new Regulatory Accounting Principles and that we would

consult on the findings from this review alongside the Business Connectivity Market Review

consultation, with the intention that any proposed changes to the attribution rules would

be reflected in any consequent price control.

In June 2015, we published the initial findings from that review and invited stakeholders’

views on if and how BT’s existing attribution rules need to change (the “Cost Attribution

Review”). We explained that we had identified some errors in spreadsheets and supporting

calculations and costs that have been allocated incorrectly. BT has explained that it has

corrected these errors in the 2014/15 RFS.

We also identified some attribution methodologies used by BT to prepare the 2013/14 RFS

that we consider are inappropriate because we do not consider that they appropriately

reflect the activities that cause the costs to be incurred. Where we consider that current

rules are not appropriate, we proposed what we consider to be appropriate cost

attribution methodologies.

In November, we published a second consultation on the Cost Attribution Review updating

the proposals made in June and making proposals for further changes to BT’s attribution

methodologies. We included further proposals for changes to the way BT attributes some

of its costs in our update on the proposed Leased Lines Charge Controls.9

We expect to make our decision on if and how BT should change its attribution rules in spring 2016. BT has not reflected the proposed changes in the 2014/15 RFS.

9 http://stakeholders.ofcom.org.uk/binaries/consultations/bcmr-update-proposed-

leased-lines-charge-controls/summary/BCMR_LLCC_Consultation.pdf

Contents

Page 1

Revised Current Cost Financial Statements

1.1 Introduction: Regulation in the UK .............................................................................. 5

1.2 Regulatory Financial Reporting Obligations ................................................................ 7

1.3 Revisions to the Current Cost Financial Statements .................................................... 8

2.1 Basis of Preparation .................................................................................................. 11

2.1.1 Regulatory Accounting Framework ...................................................................... 11

2.1.2 Regulatory Accounting Principles ........................................................................ 11

2.1.3 Documentation and Application of the Regulatory Accounting Framework ....... 11

2.1.4 Changes to BT’s Financial Reporting Obligations ................................................. 12

2.1.5 Comparability of current and prior year results .................................................. 12

2.1.6 Change Control Notification – amendments and additional methodologies ....... 15

2.1.7 Revision of the 2014/15 RFS including comparative information ........................ 16

3.1 Statement of Responsibility ...................................................................................... 20

4.1 Report of Independent Auditors ............................................................................... 22

5.1 Performance Summary by Market 2015 ................................................................... 27

5.2 Performance Summary by Market 2014 ................................................................... 28

6.1 Wholesale sector costs .............................................................................................. 30

6.1.1 Attribution of Wholesale Current Costs 2015 ........................................................ 31

6.1.2 Attribution of Wholesale Current Costs 2014 ........................................................ 32

6.2 Wholesale MCE sector costs...................................................................................... 33

6.2.1 Attribution of Wholesale Current Cost Mean Capital Employed 2015 ................... 34

6.2.2 Attribution of Wholesale Current Cost Mean Capital Employed 2014 ................... 35

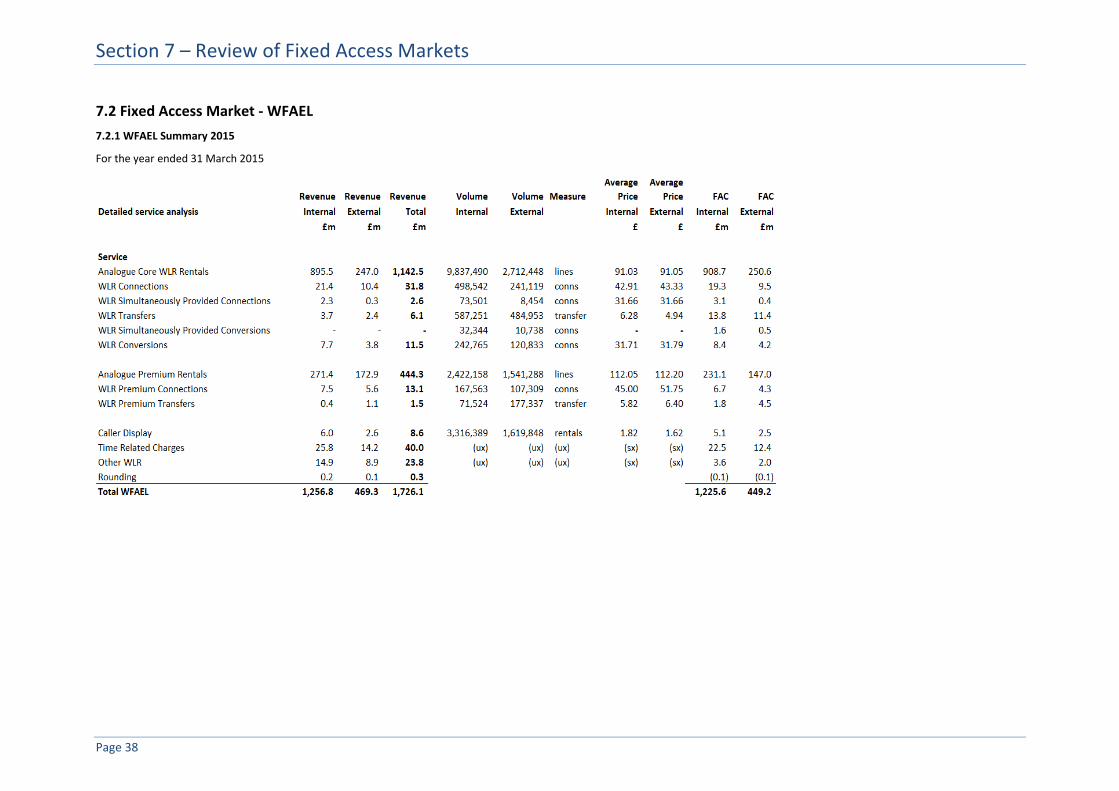

7.1 Fixed Access Markets Review .................................................................................... 37

7.2 Fixed Access Market - WFAEL .................................................................................... 38

7.2.1 WFAEL Summary 2015 ......................................................................................... 38

7.2.2 WFAEL calculation of FAC based on component costs and usage factors 2015 .. 39

7.2.3 WFAEL Summary 2014 ......................................................................................... 40

7.2.4 WFAEL calculation of FAC based on component costs and usage factors 2014 .. 41

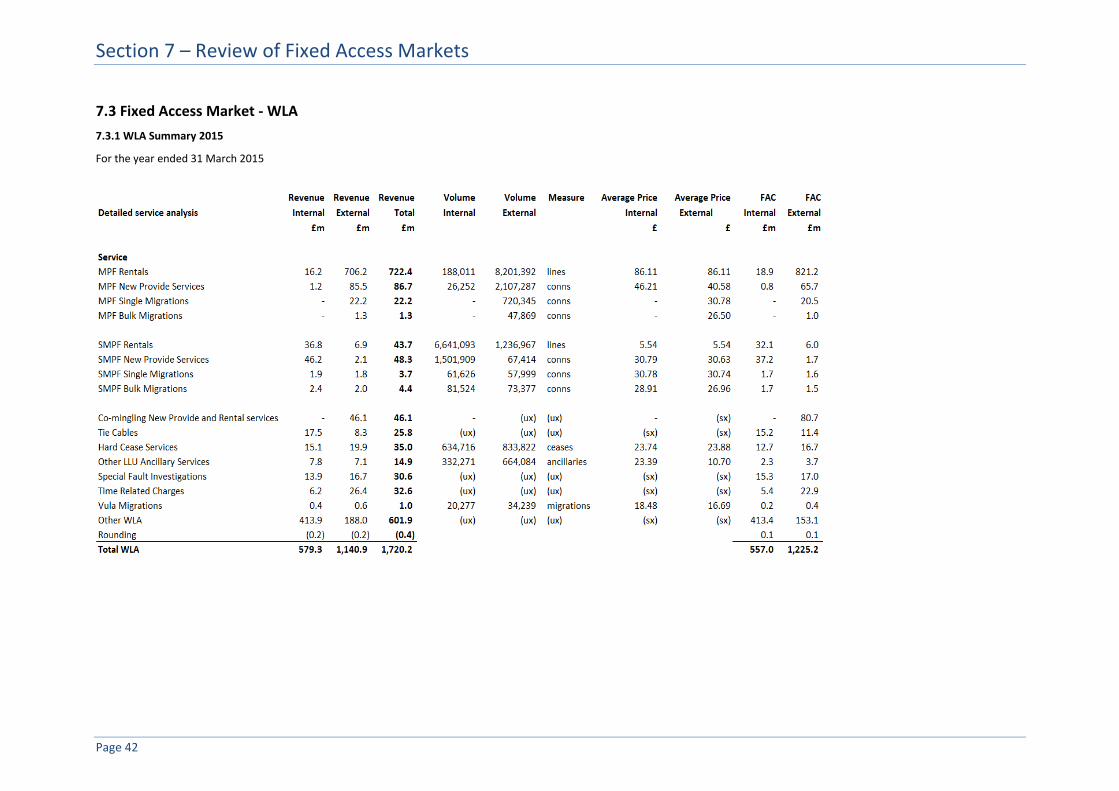

7.3 Fixed Access Market - WLA ........................................................................................ 42

7.3.1 WLA Summary 2015 ............................................................................................. 42

7.3.2 WLA calculation of FAC based on component costs and usage factors 2015 ...... 43

7.3.3 WLA Summary 2014 ............................................................................................. 45

7.3.4 WLA calculation of FAC based on component costs and usage factors 2014 ...... 46

7.4 Fixed Access Market – ISDN2..................................................................................... 48

7.4.1 ISDN2 Summary 2015 .......................................................................................... 48

7.4.2 ISDN2 Summary 2014 .......................................................................................... 49

7.5 Fixed Access Market – ISDN30................................................................................... 50

7.5.1 ISDN30 Summary 2015 ........................................................................................ 50

7.5.2 ISDN30 Summary 2014 ........................................................................................ 51

8.1 Review of Business Connectivity Markets ................................................................. 53

8.2 Business Connectivity Market – Low Bandwidth TISBO ............................................ 55

8.2.1 Low Bandwidth TISBO Summary 2015 ................................................................. 55

8.2.2 Low Bandwidth TISBO calculation of FAC based on component costs and usage factors 2015 .................................................................................................................. 56

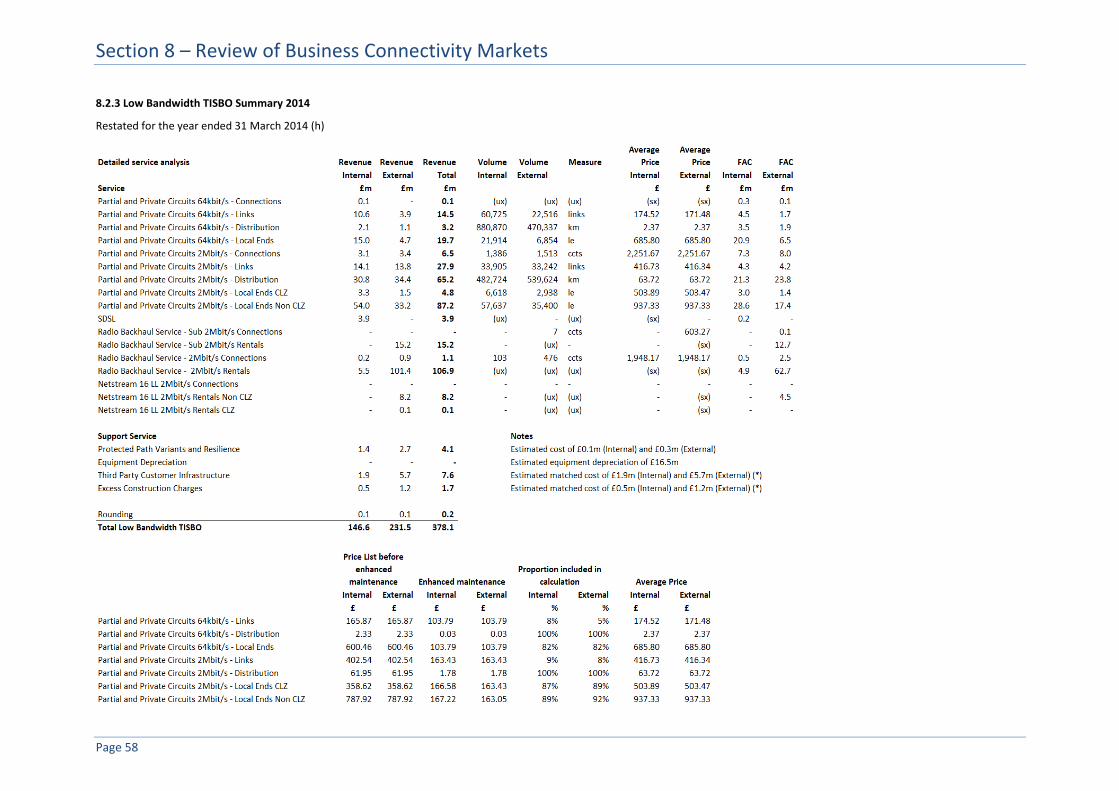

8.2.3 Low Bandwidth TISBO Summary 2014 ................................................................. 58

8.2.4 Low Bandwidth calculation of FAC based on component costs and usage factors 2014 .............................................................................................................................. 59

8.3 Business Connectivity Market – Medium Bandwidth TISBO ..................................... 61

8.3.1 Medium Bandwidth TISBO Summary 2015 .......................................................... 61

8.3.2 Medium Bandwidth TISBO calculation of FAC based on component costs and usage factors 2015 .................................................................................................................. 62

8.3.3 Medium Bandwidth TISBO Summary 2014 .......................................................... 63

8.3.4 Medium Bandwidth TISBO calculation of FAC based on component costs and usage factors 2014 .................................................................................................................. 64

8.4 Business Connectivity Market – High Bandwidth TISBO ............................................ 65

8.4.1 High Bandwidth TISBO Summary 2015 ................................................................ 65

Contents

Page 2

8.4.2 High Bandwidth TISBO calculation of FAC based on component costs and usage factors 2015 .................................................................................................................. 66

8.4.3 High Bandwidth TISBO Summary 2014 ................................................................ 67

8.4.4 High Bandwidth TISBO calculation of FAC based on component costs and usage factors 2014 .................................................................................................................. 68

8.5 Business Connectivity Market – TI Regional Trunk .................................................... 69

8.5.1 TI Regional Trunk Summary 2015 ........................................................................ 69

8.5.2 TI Regional Trunk calculation of FAC based on component costs and usage factors 2015 .............................................................................................................................. 70

8.5.3 TI Regional Trunk Summary 2014 ........................................................................ 71

8.5.4 TI Regional Trunk calculation of FAC based on component costs and usage factors 2014 .............................................................................................................................. 72

8.6 Business Connectivity Market – Technical Areas (Point of Handover) ...................... 73

8.6.1 Technical Areas (Point of Handover) Summary 2015........................................... 73

8.6.2 Technical Areas (Point of Handover) calculation of FAC based on component costs and usage factors 2015 ................................................................................................. 74

8.6.3 Technical Areas (Point of Handover) Summary 2014........................................... 75

8.6.4 Technical Areas (Point of Handover) calculation of FAC based on component costs and usage factors 2014 ................................................................................................. 76

8.7 Business Connectivity Market – AISBO Non WECLA .................................................. 77

8.7.1 AISBO Non WECLA Summary 2015 ...................................................................... 77

8.7.2 AISBO Non WECLA calculation of FAC based on component costs and usage factors 2015 .............................................................................................................................. 78

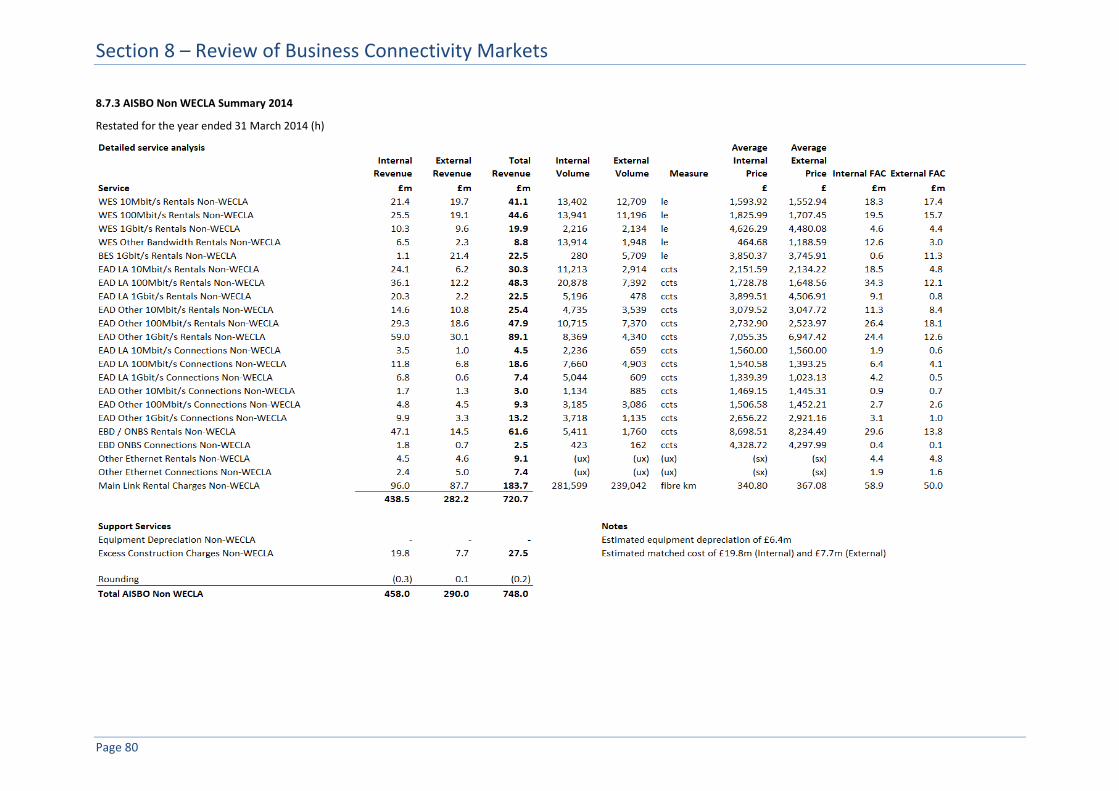

8.7.3 AISBO Non WECLA Summary 2014 ...................................................................... 80

8.7.4 AISBO Non WECLA calculation of FAC based on component costs and usage factors 2014 .............................................................................................................................. 81

8.8 Business Connectivity Market – AISBO WECLA ......................................................... 83

8.8.1 AISBO WECLA Summary 2015 .............................................................................. 83

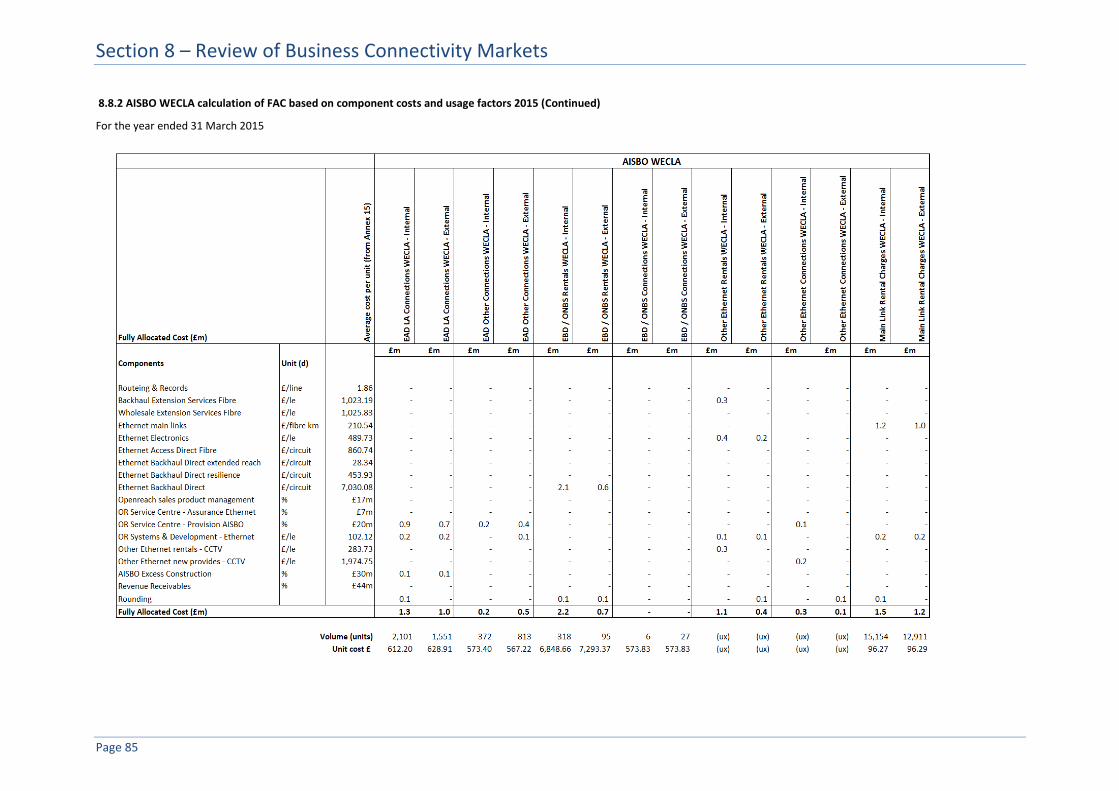

8.8.2 AISBO WECLA calculation of FAC based on component costs and usage factors 2015 .............................................................................................................................. 84

8.8.3 AISBO WECLA Summary 2014 .............................................................................. 86

8.8.4 AISBO WECLA calculation of FAC based on component costs and usage factors 2014 .............................................................................................................................. 87

8.9 Business Connectivity Market – MISBO Non WECLA ................................................. 89

8.9.1 MISBO Non WECLA Summary 2015 ..................................................................... 89

8.9.2 MISBO Non WECLA calculation of FAC based on component costs and usage factors 2015 .................................................................................................................. 90

8.9.3 MISBO Non WECLA Summary 2014 ..................................................................... 91

8.9.4 MISBO Non WECLA calculation of FAC based on component costs and usage factors 2014 .................................................................................................................. 92

9.1 Review of Narrowband Markets ................................................................................ 94

9.2 Narrowband Market – Fixed Call Origination ............................................................ 95

9.2.1 Fixed Call Origination Summary 2015 .................................................................. 95

9.2.2 Fixed Call Origination Summary 2014 .................................................................. 95

9.3 Narrowband Market – Fixed Geographic Call Termination ....................................... 96

9.3.1 Fixed Geographic Call Termination Summary 2015 ............................................. 96

9.3.2 Fixed Geographic Call Termination Summary 2014 ............................................. 96

9.4 Narrowband Market – Technical areas (Interconnect Circuits) ................................. 97

9.4.1 Technical areas (Interconnect Circuits) Summary 2015 ....................................... 97

9.4.2 Technical areas (Interconnect Circuits) calculation of FAC based on component costs and usage factors 2015 ........................................................................................ 98

9.4.3 Technical areas (Interconnect Circuits) Summary 2014 ....................................... 99

9.4.4 Technical areas (Interconnect Circuits) calculation of FAC based on component costs and usage factors 2014 ...................................................................................... 100

10.1 Wholesale Broadband Access (“WBA”) Markets Review ....................................... 102

10.2 WBA - Market A ..................................................................................................... 103

10.2.1 WBA (Market A) Summary 2015 ...................................................................... 103

10.2.2 WBA (Market A) calculation of FAC based on component costs and usage factors 2015 ............................................................................................................................ 104

10.2.3 WBA (Market A) EOI 2015 ................................................................................ 106

10.2.4 WBA (Market A) Summary 2014 ...................................................................... 107

Contents

Page 3

10.2.5 WBA (Market A) calculation of FAC based on component costs and usage factors 2014 ............................................................................................................................ 108

10.2.6 WBA (Market A) EOI 2014 ................................................................................ 110

11.1 BT Reconciliation Statement 2015 ........................................................................ 112

11.2 BT Reconciliation Statement 2014 ........................................................................ 112

11.3 BT Reconciliation Statement MCE 2015 ................................................................ 113

12.1 Revised Openreach Information ............................................................................ 115

12.2 Revised Openreach Income Statement 2015 ........................................................ 116

12.3 Revised Openreach Income Statement 2014 ........................................................ 117

12.4 Revised Openreach MCE Statement 2015 ............................................................. 118

12.5 Revised Openreach MCE Statement 2014 ............................................................. 119

12.6 Reconciliation of Revised Openreach Income Statements .................................... 120

Appendix 1.1 Network Activity Statements Consolidated 2015 .................................... 122

Appendix 1.2 Network Activity Statements Consolidated 2014 .................................... 125

Appendix 2.1 Price Controls in Regulated Markets ....................................................... 129

Appendix 3.1 Adjusted Financial Performance Schedule .............................................. 131

Appendix 3.2 Adjusted Financial Performance Schedule 2015 ..................................... 132

Appendix 3.3 Adjusted Financial Performance Schedule 2014 ..................................... 133

Appendix 4 Revised Time Related Charges and Special Fault Investigation Costs ........ 135

Glossary ......................................................................................................................... 137

Footnotes ...................................................................................................................... 140

Additional Information .................................................................................................. 142

Section 1 – Introduction to the Current Cost Financial Statements

Page 4

Section 1 Introduction to the Current Cost Financial Statements

Section 1 – Introduction to the Current Cost Financial Statements

Page 5

1.1 Introduction: Regulation in the UK

European Union (“EU”) regulation

In EU countries, electronic communications networks and services are governed by directives and regulations set by the European Commission (“EC”). These create a Europe-wide framework covering services such as fixed and mobile voice, broadband, cable and satellite TV.

The directives include rules covering access and interconnection, universal service obligations and a requirement for national regulators to review markets for Significant Market Power (“SMP”) every three years.

Companies with SMP typically have a market share of 40% or more and are able to do things such as increase prices without losing business to competitors (as would happen in a fully competitive market).

The directives also cover how regulators set price controls which can have a major impact on the companies subject to them. The rules require national regulators to consult with the EC on any price control decisions before they are finalised to make sure they are consistent with European regulations.

The EC announced its strategy for the Digital Single Market on 6 May 2015 which included a plan to review the EU Telecommunications Framework. As part of this review, the EC aims to assess how to encourage investment in infrastructure and how to make current telecoms and media rules fit for new challenges and new providers. The EC will also consider a European approach to spectrum management.

UK regulation

The telecoms and broadcasting industries are regulated primarily by Ofcom (the UK’s independent regulator) within the framework set by the various European directives, the Communications Act and other UK and EU regulations and recommendations. The telecoms sector is subject to an extensive ex-ante regulatory framework set out under the European Common Regulatory Framework.

The Communications Act and Ofcom

The Communications Act gives Ofcom legal powers and sets out how electronic communication and broadcasting services should be regulated in the UK. It includes the conditions set by the European directives.

Ofcom’s main duties are:

to further the interests of citizens in relation to communications matters.

to further the interests of consumers in relevant markets, where appropriate by promoting competition.

Under the powers of the Communications Act, Ofcom sets conditions that Communication Providers (“CPs”) must comply with. Some conditions, known as General Conditions, apply to all CPs. These mainly deal with protecting consumers’ general access and interconnection, planning for emergencies, providing information to Ofcom and allocating and transferring phone numbers. Other conditions apply to certain companies that are universal service providers or that Ofcom has decided have SMP in a particular market.

We are the designated universal service provider for the UK (except for the Hull area where it is KCOM Group) and so we have certain obligations. The main one is to make sure that basic fixed-line services are available at an affordable price to all consumers in the UK. We are also obliged to provide public payphones.

We have SMP in a number of markets. Ofcom’s market reviews are therefore very important for us. Following a market review, if Ofcom decides that a CP has SMP, it can put controls in place, typically on the prices which the CP can charge. Ofcom will generally try to set charges that are reasonably based on costs and an appropriate return on the capital invested.

Anyone can appeal against Ofcom’s decisions through a number of routes, including to the Competition Appeal Tribunal (“CAT”) or to the High Court.

In March 2015, Ofcom announced a major review of the digital communications market. The Strategic Review of Digital Communications will examine competition, investment, innovation and the availability of products in the fixed-line, broadband and mobile markets. It will focus on three areas in particular:

ensuring the right incentives for private-sector investment, which can help deliver availability and quality of service.

maintaining strong competition and tackling obstacles or bottlenecks that might be holding the sector back.

identifying whether there is scope for deregulation in some areas.

The first phase of the review examined current and future market factors that may affect digital communications services, and current regulatory approaches. To inform this work, Ofcom engaged with a wide range of stakeholders - including industry, consumer groups, the UK Government and devolved administrations - through meetings and workshops. This phase of the review has concluded with a discussion document issued in July 2015.

Section 1 – Introduction to the Current Cost Financial Statements

Page 6

BT’s Undertakings

In response to Ofcom’s 2005 Strategic Review of Telecommunications, we gave some legally-binding undertakings under the Enterprise Act 2002. These Undertakings (which included the creation of Openreach) began in September 2005. They aim to give clarity and certainty to the UK telecoms industry about the way we provide ‘upstream’ regulated products. This in turn supports effective and fair competition in related ‘downstream’ markets.

Impact of Regulation

There were a number of regulatory decisions and outcomes of appeals that affected us during the year and will impact us in the future.

Fixed Access and Wholesale Broadband Access Market Reviews

In June 2014, Ofcom completed its reviews of both the Fixed Access market (covering WLR, LLU, GEA, ISDN2 and ISDN30 products) and the Wholesale Broadband Access (WBA) market (covering IPstream, Datastream and WBC).

Ofcom continued to impose charge controls on the markets where we have SMP. These controls cover the three years to March 2017.

During this period, the artificially low price of full LLU will be phased out to better reflect the actual costs of providing the service of CPs.

Ofcom did not impose price regulation of wholesale fibre broadband (GEA)

For WBA, Ofcom enlarged the size of the area where the competition is greater and where we are free to set prices as we wish.

Business Connectivity Market Review

During the year Ofcom began its pre-consultation process ahead of reviewing the business connectivity markets and the associated leased line charge control.

Consultation documents were issued in May and June 2015 with the new regulations applying from April 2016

Ofcom’s review will consider, amongst other things, the merits of introducing a new passive dark fibre remedy as well as scope for further deregulation, reflecting an increasingly competitive market.

Wholesale Narrowband

In April 2015, Ofcom issued a ‘call for inputs’, being the first stage in its review of the wholesale fixed call origination, termination and interconnection markets.

Market Review

The review will consider whether regulation of call origination is still appropriate and whether further charge controls are required when the current controls end in September 2016.

Cost accounting and Accounting Separation

Where a provider has SMP, the Communications Act enables Ofcom to impose one or more obligations in relation to each market, including the implementation of cost accounting and/or accounting separation.

The purpose of imposing an obligation to implement a cost accounting system is to ensure that fair, objective and transparent criteria are followed in allocating our costs to services in situations where we are subject to obligations for charge controls or cost-oriented prices.

The purpose of imposing an obligation regarding accounting separation is to provide a higher level of detail of information than that derived from statutory financial statements, to reflect as closely as possible the performance of parts of our business as if they had operated as separate businesses, to prevent discrimination in favour of our own activities and to prevent unfair cross-subsidy.

The Company’s cost accounting and accounting separation systems need to be capable of reporting regulatory financial information to demonstrate full compliance with our regulatory obligations.

Section 1 – Introduction to the Current Cost Financial Statements

Page 7

1.2 Regulatory Financial Reporting Obligations

The form and content of these Current Cost Financial Statements is based on the reporting obligations set out by Ofcom. We refer to these obligations as “the Final Statements and Notifications”.

(a) Fixed Access and WBA markets regulatory market obligations are:

“Regulatory Financial Reporting” Statement issued 20 May 2014.

“Directions for Regulatory Financial Reporting” issued on 30 March 2015.

(b) Narrowband/BCMR market regulatory obligations consists of:

“The Regulatory Financial Reporting Obligations on BT and Kingston Communications” issued 22 July 2004.

“Changes to BT’s Regulatory Financial Reporting Framework” issued 31 August 2005.

“Changes to BT’s Regulatory Financial Reporting and Audit Requirements” issued 16 August 2006.

“Changes to BT’s Regulatory Financial Reporting and Audit Requirements” issued 30 May 2007.

“Changes to BT’s 2007/08 Regulatory Financial Statements” issued 26 June 2008.

“Changes to BT and KCOM’s Regulatory Financial Reporting – 2008/09 update” issued 15 June 2009.

“Changes to BT and KCOM’s regulatory and financial reporting 2009/10 update” issued 4 June 2010.

“Changes to BT and KCOM’s regulatory and financial reporting 2010/11 update” issued 2 June 2011.

“Changes to BT and KCOM’s regulatory and financial reporting 2011/12 update” issued 17 April 2012.

“Changes to BT and KCOM’s regulatory and financial reporting 2012/13 update” issued 25 April 2013.

“Changes to BT and KCOM’s regulatory and financial reporting 2013/14 update” issued 3 April 2014.

“Regulatory Financial Reporting” Statement published 20 May 2014.

The Initial Statement and Notification on our regulatory financial reporting requirements imposed 34 SMP Services Conditions (OA1-OA34) to the relevant markets where we are deemed to have SMP and to the relevant technical areas associated with the identified markets. Full details of these conditions can be found in the Final Statement and Notification “The regulatory financial reporting obligations on BT and Kingston Communications”, which was issued on 22 July 2004.

Ofcom published six Directions under SMP Services Condition OA2 to impose further requirements on us in respect of our regulatory financial reporting obligations. The original Directions and amendments to these Directions can be found in the Final Statements and Notifications.

Direction 1 sets out a list of network components that we must report on under the regulatory financial reporting obligation and in its reference offers.

Direction 2 imposes a transparency principle on us in relation to the accounting documentation.

Direction 3 sets out the Regulatory Financial Statements that should be prepared, delivered to Ofcom and published, and the level of audit opinion that should be secured for each statement.

Direction 4 sets out the required form and content of the different types of Regulatory Financial Statements required under Direction 3.

Direction 5 sets out the detailed form of the Fairly Presents in Accordance with (FPIA) audit opinion required under Direction 3.

Direction 6 sets out the detailed form of the Properly Prepared in Accordance with (PPIA) audit opinion required under Direction 3.

We are also required by Ofcom to provide additional detailed information to enable Ofcom to regulate effectively and efficiently. This additional information is not subject to any independent examination.

In the Current Cost Financial Statements for 2015, we are obliged to report on the following SMP markets (in the UK excluding the Hull area, modified where stated below):

Fixed Access markets

Wholesale analogue exchange line services.

Wholesale local access services.

Wholesale ISDN2 exchange line services.

Wholesale business ISDN30 exchange line services.

Business Connectivity markets

Traditional interface symmetric broadband origination (TISBO) (up to and including 8Mbit/s).

TISBO excluding the WECLA (above 8Mbit/s up to and including 45Mbit/s).

TISBO excluding the WECLA (above 45Mbit/s up to and including 155Mbit/s).

Technical areas (Point of Handover).

Alternative interface symmetric broadband origination (AISBO) excluding the WECLA (up to and including 1Gbit/s).

Section 1 – Introduction to the Current Cost Financial Statements

Page 8

AISBO in the WECLA (up to and including 1Gbit/s).

Multiple interface symmetric broadband origination (MISBO) excluding the WECLA (above 1Gbit/s).

Wholesale regional trunk segments.

Narrowband markets

Call origination on fixed public narrowband networks.

Fixed geographic call termination.

Technical areas (Interconnect Circuits).

Broadband markets

Wholesale Broadband Access (Market A).

For the purpose of the Statements we have chosen to use abbreviated names to the markets which can be seen in Table 1. All the markets have Accounting Separation (AS) and Cost Accounting (CA) obligations. Other abbreviated names, acronyms and footnotes used through the document are defined in the Glossary and Footnotes on pages 137 and 140 respectively.

Openreach

We are also required by the Undertakings (section 5.31) to disclose the financial results of Openreach separately and to reconcile the financial results to the Openreach segmental information shown in BT Group plc’s Annual Report. We have included this information in section 12.

Regulatory Financial Review

To help a user of the Current Cost Financial Statements understand the changes in the performance of products and services in each market, we are required to prepare “Regulatory Financial Reviews”. These are included in section 7 to 10 at the grouped market level, as defined by Ofcom, to explain:

The main factors and influences that drive each market or groups of markets.

New products and services.

Further detail is provided in Section 2 as to methodology and other changes in comparatives affecting the prior year results, and changes in methodology for the current year.

New Reporting Obligations

In Ofcom’s Statement of 20 May 2014 on “Regulatory Financial Reporting”, Ofcom set out additional obligations for BT to produce a reconciliation report that:

Discloses the impact of the prior year methodologies upon the current year results.

Discloses the impact of material errors on the prior year results, where material error is one that exceeds the higher of 5% or £1 million on any figure in the prior year Current Cost Financial Statements.

BT is also required to obtain external assurance upon those reports. This reconciliation report “Reconciliation Report 2015” will be published during November 2015.

1.3 Revisions to the Current Cost Financial Statements

Subsequent to the original publication of the Current Cost Financial Statements on 31 July 2015 (the “31 July 2015 RFS”), certain errors in the 31 July 2015 RFS have been discovered. Following discussions with Ofcom we have corrected for these errors in this document, the “Revised Current Cost Financial Statements 2015” (the “Revised RFS”). A description of these errors is given in section 2.1.7 below.

In June 2015 and November 2015 Ofcom published consultation documents arising from its Cost Attribution Review. In these consultations Ofcom identified some attribution methodologies we have used to prepare the RFS that it considered are inappropriate and proposed what it considers to be appropriate alternatives. Ofcom included further proposals for changes to the way we attribute some of our costs in its update on the proposed leased lines charge controls issued in November 2015.

As these proposals are currently still under consultation, we have not reflected any of the proposed changes to attribution methodologies in the Revised RFS. This should not be construed as indicating either our agreement or our disagreement with them.

For example, although we have not adjusted the Revised RFS we do agree with Ofcom that transaction costs incurred in respect of our proposed acquisition of EE should be excluded from the costs of regulated products. None of the purchase price of EE (£12.5bn) or the related transaction costs will be allocated to our regulated products in 2016 or future years. These costs were less than 0.2% of the costs reported in the RFS in 2015.

Section 1 – Introduction to the Current Cost Financial Statements

Page 9

Table 1 – Market Review Name Abbreviations

Market Review Name Abbreviated Name

Wholesale fixed analogue exchange line services WFAEL

Wholesale local access services WLA

Wholesale ISDN2 exchange line services ISDN2

Wholesale business ISDN30 exchange line services ISDN30

Traditional interface symmetric broadband origination (TISBO) (up to and including 8Mbit/s)

Low Bandwidth TISBO

TISBO excluding the WECLA (above 8Mbit/s up to and including 45Mbit/s)

Medium Bandwidth TISBO

TISBO excluding the WECLA (above 45Mbit/s up to and including 155Mbit/s)

High Bandwidth TISBO

Technical areas (Point of Handover) Technical areas (Point of Handover)

Alternative interface symmetric broadband origination (AISBO) excluding the WECLA (up to and including 1Gbit/s)

AISBO Non WECLA

AISBO in the WECLA (up to and including 1Gbit/s) AISBO WECLA

Multiple interface symmetric broadband origination (MISBO) excluding the WECLA (above 1Gbit/s)

MISBO Non WECLA

Market Review Name Abbreviated Name

Wholesale regional trunk segments TI Regional Trunk

Call origination on fixed public narrowband networks

Fixed call origination

Fixed call termination Fixed geographic call termination

Technical areas (Interconnect Circuits) Technical areas (Interconnect Circuits)

Wholesale Broadband Access (Market A) WBA – Market A

Section 2 – Basis of Preparation

Page 10

Section 2 Basis of Preparation

Section 2 – Basis of Preparation

Page 11

2.1 Basis of Preparation

2.1.1 Regulatory Accounting Framework

The ultimate holding company of British Telecommunications plc (the “Company”) is BT Group plc (referred to together with its subsidiary and associated undertakings and joint ventures as the “Group” or “BT”). Substantially all the businesses and activities of the Group are carried out by British Telecommunications plc, its subsidiaries, associated undertakings and joint ventures.

BT Group plc’s Annual Report dated 6 May 2015 details the basis of preparation and explains the accounting policies adopted by the Group. BT’s Annual Report for 2014/15, on which the independent external auditors issued an unqualified report, did not contain a statement under Section 498(2) or 498(3) of the Companies Act 2006 and has been delivered to the Registrar of Companies.

The Company has, by agreement with BT Group plc, prepared the Current Cost Financial Statements in accordance with the Accounting Methodology Document (as described in Section 2.1.3 below) and the Regulatory Accounting Principles (as described in Section 2.1.2 below), by disaggregating balances recorded in the general ledgers and other accounting records of the Group.

The Accounting Methodology Document and the Regulatory Accounting Principles set out the framework under which the Current Cost Financial Statements are prepared.

2.1.2 Regulatory Accounting Principles

Regulatory Accounting Principles are the principles we apply or use in the preparation of the Current Cost Financial Statements, for example, that all costs should be fully attributed to the relevant cost centre.

Ofcom directed the Regulatory Accounting Principles in its Regulatory Financial Reporting Final Statement dated 20 May 2014 including the requirement for consistency with regulatory decisions, and that these changes would be applicable for the Current Cost Financial Statements 2015.

2.1.3 Documentation and Application of the Regulatory Accounting Framework

In adhering to the Regulatory Accounting Principles, we prepare and update annually our methodology documentation. For 2014/15 we have combined our methodology documentation into the Accounting Methodology Document. This document covers:

Attribution Methods – we explain how we attribute revenue, transfer charges, costs,

assets and liabilities to activities.

Transfer Charge System Methodology – we explain our approach within our regulatory

costing system (“REFINE”) on transfer charges.

Non-discrimination - we demonstrate how we ensure an equivalent treatment for

internal and external CPs. For each reported market, we disclose the average price of

services sold to external CPs and the average price sold to internal CPs. Where a reported

market is required to buy input services from an upstream reported market, the cost is

shown in Current Cost Financial Statements as an Equivalence of Input (“EOI”) charge.

This applies for WBA (Market A).

Accounting Policies - the way we apply the requirements of the Companies Act 2006,

Article 4 of the International Accounting Standards (“IAS”) Regulation, and our

accounting policies, whenever not superseded by the Regulatory Accounting Principles,

in each of the Current Cost Financial Statements. The Accounting Methodology

Document (“AMD”) details the accounting policies adopted in preparing the underlying

financial information.

Long Run Incremental Cost (“LRIC”) Methodology - the long run incremental cost

principles, procedures and processes form the framework we use to calculate long run

incremental costs and stand alone costs.

Current Cost Accounting (“CCA”) - we prepare the Current Cost Financial Statements

under the Financial Capital Maintenance (“FCM”) convention in accordance with the

principles set out in the handbook “Accounting for the Effects of Changing Prices”,

published in 1986 by the Accounting Standards Committee. Under the FCM convention

we include changes in asset values in our income statement as unrealised holding gains

or losses. The CCA section also includes the Regulatory Asset Valuation (RAV) where

Ofcom has directed an alternative methodology for valuing parts of the local access

network.

Usage Factors - we use usage factors in our costing methodology to reflect when the

services have a different relative usage of network components.

In addition to this Accounting Methodology Document, we also publish a Wholesale Catalogue, which separately identifies and describes services which are internally, externally, or internally and externally supplied, and those which are used in the course of supplying other wholesale services.

The economic markets defined by Ofcom’s Final Statements and Notifications do not correspond to how the Group is organised for management and accounting purposes. The Current Cost Financial Statements are therefore produced by overlaying the requirements of the regulatory reporting framework on the management and accounting structure of the Group.

Section 2 – Basis of Preparation

Page 12

We reconcile the Current Cost Financial Statements to BT’s statutory accounts and we explain any differences.

Due to the complex nature of the RFS, figures in this report are individually rounded to the nearest relevant unit (e.g. £m). Totals and sub-totals are calculated based on these rounded figures. Where required by the Directions and Notifications rounding differences are shown on each individual schedule. Where rounding differences are not shown minor summation inconsistencies may arise between schedules.

2.1.4 Changes to BT’s Financial Reporting Obligations

Ofcom’s “Directions for Regulatory Financial Reporting” dated 30 March 2015 has had an impact on the disclosure requirements and regulatory accounting methodologies within the Current Cost Financial Statements for the year ended 31 March 2015. This Direction gives effect to recommendations from market reviews.

These do not represent all changes directed by Ofcom, only those which have required us to change the definitions of various markets and restate the Regulatory Financial Statements.

(a) Implementation of the Fixed Access Market Review (FAMR) published 26 June 2014

Ofcom imposed SMP services conditions with respect to regulatory accounting in relation to the following markets:

o The supply of copper loop-based, cable-based and fibre-based wholesale local access at a fixed location in the United Kingdom excluding the Hull Area.

o Wholesale fixed analogue exchange line services in the United Kingdom excluding the Hull Area.

o Wholesale ISDN30 exchange line services in the United Kingdom excluding the Hull Area.

o Wholesale ISDN2 exchange line services in the United Kingdom excluding the Hull Area.

We are required to separately identify in the Regulatory Financial Statements:

o Each of the internal and external Network Services used in the Wholesale Local Access Market and separately attribute the costs, revenues and volumes of each of the internal and external Network Services used in the Wholesale Local Access Market.

o Each of WLR + SMPF Simultaneous Connections and WLR + SMPF Simultaneous Migrations; and separately attribute the costs of each of WLR + SMPF Simultaneous Connections and WLR + SMPF Simultaneous Migrations.

We are required to disclose the revenue, volume, average price and FAC of VULA Migrations.

We are required to disclose all network components and FAC of VULA Migrations (calculation of FAC based on component costs and usage factors for the WLA market in the Regulatory Financial Statements).

We are required to prepare the Regulatory Financial Statements, explanations and other required information on a Regulatory Asset Value adjusted current costs basis. We are required to value the Access Ducts capitalised prior to 1 August 1997 on the basis of the closing historical cost on 31 March 2005 which is indexed by the Retail Price Index from 31 March 2005.

(b) Implementation of the Wholesale Broadband Access Market Review (“WBAMR”) published 26 June 2014

Ofcom imposed SMP services conditions with respect to regulatory accounting in relation to the following market:

o WBA (Market A).

We are required to not attribute the costs of 21CN in accordance with the Future Benefits Principle to the Network Services considered in the WBA Statement. This principle attributed 21CN costs to services that could use 21CN in the future but do not currently use this platform.

The changes described have been made in accordance with Ofcom’s direction. Where the changes impact the methodology in the Current Cost Financial Statements we have disclosed them in section 2.1.5. There are several changes which impact the structure of the regulated markets. These are not included in the list in section 2.1.5 but have been made to reflect the above changes. A list of these changes is available in our “Change Control Notification” Report published on 31 March 2015 (“Change Control Notification in accordance with SMP Condition 21 of Ofcom’s Regulatory Financial Reporting Final Statement published on 20 May 2014”) and are identifiable as ‘Changes to Market Definitions’.

2.1.5 Comparability of current and prior year results

Ofcom’s Regulatory Financial Reporting Final Statement published 20 May 2014 directed BT to make certain additional disclosures. BT has a new obligation under SMP Condition 21 to publish by 31 March 2015 all methodology changes that were implemented between the 2014 Current Cost Financial Statements and the 2015 Current Cost Financial Statements. This obligation was met by the publication of the “Change Control Notification” on 31 March 2015.

There were a number of changes to our methodologies made after 31 March 2015:

Section 2 – Basis of Preparation

Page 13

It was not possible to update our methodologies by 31 March 2015 to reflect the final Ofcom decisions on regulatory accounting methodologies in “Directions for Regulatory Financial Reporting” issued on 30 March 2015. We had made changes in line with Ofcom’s consultation on changes to our methodologies but these were not exactly in line with Ofcom’s final requirements. In these circumstances, we are required to make certain methodology changes to ensure compliance with the Final Statements and Notifications.

We have notified Ofcom, via an exchange of letters, of certain methodology changes made after 31 March 2015 which are to be considered as if they were included in the Change Control Notification of 31 March 2015.

Further changes to our methodologies were made as a result of notifications from our auditors to make sure that errors would not be introduced into the Current Cost Financial Statements.

Each of these post 31 March 2015 methodology changes is described in Section 2.1.6 below.

Certain of these methodology changes have had an impact on the comparability of the current and prior year results and the comparatives for the year ended 31 March 2014 has been restated accordingly. The impacts quoted below are based upon our estimates of the impact of the changes on 2013/14 costs:

(a) Changes to BT’s financial reporting obligations as set out in the Current Cost Financial Statements and Notifications which is explained in section 2.1.4.

(b) The prior year comparatives have been restated to reflect the following methodology changes implemented in the current year. Changes identified with an asterisk (*) are those methodology changes implemented as a result of Ofcom’s Directions for Regulatory Financial Reporting dated 30 March 2015 which have a material market impact. Changes required under this Direction are discussed in section 2.1.4.

(i) Cumulo rebate attribution*

We have changed the data we use to calculate the Profit Weighted Net Replacement Costs (“PWNRCs”) used in applying our Cumulo rebate methodology, to use the most up to date available information for Profit Weights (the market regulatory costs of capital) and Net Replacement Costs (“NRC”). Our previous methodology had been to use the NRCs and profit weightings that were agreed with the Valuation Office for the current rateable asset valuation. This change moves costs from WFAEL (£39m) and WLA (£16m), to the Business Connectivity (£22m), Narrowband (£11m), WBA (£6m) and Residual markets (£16m).

(ii) Regulatory Asset Valuation (RAV)*

We now use RAV for the access duct network instead of CCA in the Current Cost Financial Statements. We apply this only to ‘access duct’. We value the Access Ducts capitalised prior to 1 August 1997 on the basis of the closing historical cost on 31 March 2005 which is indexed by the Retail Price Index from 31 March 2005. This change decreases costs across all markets, most significantly WFAEL (£46m), WLA (£20m) and AISBO non WECLA (£11m).

(iii) 21CN Future Benefits attribution*

We had attributed 21CN platform costs to services that could use 21CN in the future but do not currently use this platform. We had called this the “future benefits” principle. Ofcom has directed us not to use this approach. Accordingly, 21CN costs previously attributed to IPstream and Datastream on a “future benefits” basis are instead attributed to Wholesale Broadband Connect (“WBC”) and Residual WBA services such as Superfast Broadband and TV Connect. Similarly, the 21CN costs attributed to Wholesale Extension Services (“WES”), Backhaul Extension Services (“BES”) and Ethernet Access Direct (“EAD”) services on a “future benefits” basis are now attributed to Wholesale Residual Ethernet services. The most significant impact of this change is to moves cost from WBA (Market A) (£40m) and AISBO non WECLA (£30m) into Residual markets.

(iv) Classification of 64kbit/s Trunk from Low Bandwidth TISBO into TI Regional Trunk

We now apportion costs between distribution, regional trunk and national trunk services based on billing data to align with Ofcom’s Business Connectivity Market Review. Historically we have reported 64kbit/s circuits in the TISBO low bandwidth market because these circuits are carried over a network of pre-provided 2Mbit/s circuits so there is no physical distinction between distribution and trunk. This change moves costs from Low Bandwidth TISBO (£3m) and into TI Regional Trunk (£2m) and Residual markets (£1m).

(v) Allocation of DSLAM costs between Markets A & B*

We had apportioned DSLAM costs between WBA markets based on an analysis of which costs are driven by the number of DSLAMs at each site and which costs are driven by the number of broadband subscribers connected at each site. We now apportion the costs only by the number of DSLAMs at each site. This change moves costs from WBA (Market A) (£6m) to Residual markets.

(vi) Classification of Featurenet from Low Bandwidth TISBO into Network Residual

We have reclassified circuits used by our Featurenet products so that they are reported in Network Residual instead of being treated as a downstream user of Low Bandwidth

Section 2 – Basis of Preparation

Page 14

TISBO circuits. This change moves costs from Low Bandwidth TISBO (£7m) and TI Regional Trunk (£1m) into Residual markets.

(vii) Renaming of sectors and F8 code repointing

We have made several changes to the mapping of the regulatory chart of accounts in order to improve the cost category descriptions in the Current Cost Financial Statements. The changes impact the calculation for the apportionment of BT TSO Managed Assets to other activity groups, plant groups and Residual markets in proportion to core assets (see AG102 in the Accounting Methodology Document). The largest impacts of this change are to move costs from Residual markets (£4m),WFAEL (£1m) and WLA(£1m) to Low Bandwidth TISBO (£3m) and WBA (Market A) (£3m).

(viii) Duct and Fibre allocations to 21CN

We have improved our attribution process so that costs for duct are apportioned to 21CN fibre plant groups (previously they were not) and so that backhaul fibre is allocated wholly to backhaul fibre plant groups and core fibre is allocated wholly to core fibre plant groups (previously backhaul and core cable plant groups were apportioned as a single cost category to all 21CN fibre plant groups). The most significant impact of this change is to move Mean Capital Employed (“MCE”) from AISBO Non WECLA (£16m), Low Bandwidth TISBO (£12m) and WBA (Market A) (£7m) into Residual markets.

(ix) Current Cost Financial Statements goodwill

We have changed our reporting of goodwill so that it is within the Retail Residual market MCE, and not in the MCE reconciliation to the statutory accounts section of the RFS. The change is presentational and does not impact market costs.

(c) The prior year comparatives have been restated to reflect the correction of the following errors identified in the Current Cost Financial Statements 2014:

(i) Classification of Non-geographic call termination

We have removed non-geographic fixed call terminations from the Fixed geographic call termination market and reallocated the costs, assets and volumes to Residual markets in line with Ofcom’s Narrowband Market Review (September 2013). The change moves costs from Fixed geographic call termination (£4m) into Residual markets.

(ii) Classification of Siteconnect

Siteconnect 155Mbit will be reported in the High Bandwidth TISBO market, not Wholesale Residual. The most significant impact of this change is to move revenue from the Wholesale residual market (£1m) into High Bandwidth TISBO. As Siteconnect is now separately disclosed, we have ensured that the prices reflect the BT Wholesale Carrier

Price List (“CPL”) and the volume of circuits reflect the updated 2013/14 data taken from PCNBS (billing data).

(iii) Access fibre – fibres per bearer

As noted in the 2013/14 Current Cost Financial Statements, access fibre is apportioned to Ethernet products as well as older Time Division Multiplexing (“TDM”) products that consume it. The number of fibres is derived from the number of TDM bearers from Core Transmission Costing System (“CTCS”) and the number of fibres per bearer which is obtained from Integrated Network System (“INS”). We identified that the way we retrieved data from INS was incorrect and instead retrieved this data using CTCS. This change mainly moves costs from AISBO Non WECLA (£3m) into ISDN30 services.

(iv) Excess Construction Charge (“ECC”) cost component rationalisation

We have reduced the number of specific components used for ECCs. This change maps ECC credits to all services using fibre and duct whereas the previous approach did not. This change primarily moves MCE from Wholesale Residual (£8m), MISBO Non WECLA (£4m), Point of Handover (£3m) into AISBO WECLA (£10m) and AISBO Non WECLA (£4m).

(v) SDH plant group to component mapping

We corrected a formula error in our SDH plant group to component model. This change moves costs from Low Bandwidth TISBO (£2m) and other bandwidth TISBO markets (£1m) into AISBO Non WECLA (£4m).

(vi) Call Origination volumes

Non-geographic call origination volumes were, in 2013/14, sourced from a system called Powerhouse (a system which sources data from our Call Statistics Centralisation System (CSCS)). The Powerhouse system volumes for 2013/14 have been found to be overstated due to an error in a Powerhouse query used to extract data from CSCS. This change moves costs from the Call origination market (£5m) into Residual markets.

(vii) BT Wholesale cost of sales transfer charges

Costs relating to BT Wholesale cost of sale transfer charges were in 2013/14 treated as an overhead of BT Wholesale activities. These costs of sale are incurred by BT Wholesale in providing non-regulated services. This change moves costs from Low Bandwidth TISBO (£6m), WBA Market A (£2m), Fixed geographic call termination (£2m) and Call origination (£2m) into Residual markets.

(viii) PPC volumes

In 2013/14 certain formula errors were made and some assumptions (e.g. we assume that Megastream internal circuits have two local ends, not one) were not applied when collating the volumes for Low, Medium and High TISBO, Regional Trunk and Point of

Section 2 – Basis of Preparation

Page 15

Handover (POH) markets. This change primarily moves costs from Wholesale Residual (£1m) and into the High Bandwidth TISBO and Regional Trunk Segments markets.

(ix) WBC internal and external volumes

The volumes of Wholesale Broadband Connect (WBC) that are used as in input to Wholesale Broadband Managed Connect (WBMC) should be reported as internal WBC volumes, however in 2013/14 they were reported as internal or external depending on the final user of the WBMC service. The WBC volumes that are used within WBMC are themselves not sold externally as WBC therefore they should always be reported as internal. This impact changes the presentation of WBC internal and external volumes in Wholesale Broadband Market A but has no overall impact on the market.

(d) The prior year comparatives were also restated for minor errata that were corrected and published on our website in “Errata Report 2014”. We restated for ISDN2 Transfer Price and Access Cards component usage factor from our published “Errata report“.

(e) Ofcom requested a further change to correct an insignificant error. This was to correct an error in relation to the attribution of electronic costs to EBD services in the MISBO Non WECLA market. The impact of this change upon the market was less than £1m.

There were no other restatements or re-presentations. However our ongoing review of cost attribution and valuation methodologies resulted in a number of additional improvements and updates to reflect changes in Group structure. In these instances the restatement of comparative information for the year ended 31 March 2014 was either not practicable or was not required as the impact was not material. These methodology changes are described in the Change Control Notification report and in Section 2.1.6.

As required by Ofcom’s Regulatory Financial Reporting: Final Statement dated 20 May 2014 we will be providing a separate audited report which sets out changes made to our Regulatory Accounting Methodology and the impact of such changes on the Regulatory Financial Statements, and Material Errors (using Ofcom’s definition of material) corrected in the Regulatory Financial Statements and the impact of such Material Errors on the Regulatory Financial Statements. This report will be published during August 2015.

2.1.6 Change Control Notification – amendments and additional methodologies

Our Change Control Notification report contained all the methodology changes we had made up to 31 March 2015. We have made certain changes to our methodologies after 31 March 2015 which we have grouped into three categories:

Changes made to comply with Ofcom’s 30 March 2015 Direction:

Regulatory Asset Valuation (RAV): We proposed in the Change Control Notification to apply RAV in full to copper cables. We have changed this to comply with Ofcom’s

Direction, which set out that the RAV adjustment should not be applied to Copper and only to Access Duct. [Change Control Notification – section 3.7].

Cumulo rebate allocation: We proposed in the Change Control Notification to use data from the 2013/14 RFS to derive the weighting element of the Profit Weighted Net Replacement Costs for Cumulo. We have changed this to use component weighted average cost of capital for the profit weighting element, as set out in Ofcom’s Direction. [Change Control Notification – section 3.12].

BDUK: We made a minor change to create a new plant group and component which covers all government grants and not BDUK areas only. This plant group and component only includes the grants received. [Change Control Notification – Section 3.23].

Time Related Charges, ISDN30, PSTN Transfers, BES 1000MB Rentals Internal WECLA, splitting co-mingling rentals between basket and non-basket services (and implementing associated revenue changes to the WLA/WAELS markets): Ofcom directed in its Directions for Regulatory Reporting (30 March 2015) that these services be reported in the WAELS/WLA market. We had not made this change but in order to comply with the direction are doing so in the 2014/15 RFS.

Changes notified to Ofcom to be considered as within the 31 March 2015 Change Control Notification report:

NGA tie cables: We have changed how we attribute duct costs to NGA tie cables so that it is attributed on the basis of the cumulative capital expenditure on duct associated with NGA. It was previously attributed to NGA tie cables based upon the depreciation on the NGA capital expenditure on duct in the year.

NGA Development: We have changed how we attribute development spend for NGA between Fibre to the Cabinet (FTTC) and Fibre to the Premises (FTTP) so that it is on the basis of NGA development spend (it was previously based on volumes). There is no impact upon figures reported in the RFS.

We have decided to withdraw the proposed change BT Technology, Service & Operations Electricity – new methodology for Public Switched Telephone Network. [Change Control Notification – section 3.20]. In the Change Control Notification we identified that we would implement a new methodology for Public Switched Telephone Network power cost attribution.

Following notification from our auditors to avoid the introduction of errors into the RFS:

PPC volumes: Internal and external Partial and Private Circuit volumes are sourced from the Core Transmission costing system (CTCS). We have identified that in 2014/15 local end and main link volumes are overstated in CTCS due to a number of circuits recorded as live in the system which are actually ceased and hence not

Section 2 – Basis of Preparation

Page 16

billable. We have therefore used Geneva Genius (billing system) data to produce the 2014/15 RFS.

Call origination volumes: Non-geographic call origination volumes have historically been retrieved via a system called Powerhouse which queries an underlying call data system called CSCS. We have identified that Call origination volumes, sourced directly from CSCS, which we submit to Ofcom on a quarterly basis are more accurate and lower than those from Powerhouse. We have therefore used CSCS data to populate the 2014/15 RFS.

2.1.7 Revision of the 2014/15 RFS including comparative information

Subsequent to the original publication of the RFS on 31 July 2015 (the “31 July 2015 RFS”), certain errors in the 31 July 2015 RFS have been identified. Following discussions with Ofcom we have corrected for these errors within this Revised RFS. A description of these errors and revisions is given below:

1. 2015 RFS Presentation of Residual Market Results and Eliminations

In the 31 July 2015 RFS on page 25 and page 26, we correctly presented the results for all individual SMP Markets, Total SMP markets and Total Markets. However, the treatment of the eliminations of inter-market charges incorrectly reported the results for residual markets as we did not present the elimination of trading between wholesale markets within the results for Total Wholesale Markets. We have corrected for this in this Revised RFS. We show the impact of the change on the 2014/15 results in Table 1 (Extract from Section 5.1 Performance Summary by Market 2015 of the 31 July 2015 RFS (page 25)) and Table 2 (Amended Presentation of Residual Market results and eliminations included in the Revised RFS) below.

The 31 July 2015 RFS treats inter-market charges as follows in Table 1 below:

Charges between all markets of £5,347m are eliminated against total operating costs

as shown on the “Eliminations” row.

Charges of £49.7m to WBA Market A from other markets (as disclosed in section

10.2.1 on page 101 of the 31 July RFS) are balanced by an equal credit within

Wholesale Residual (as disclosed in section 6.1.1 on page 29 of the 31 July RFS).

As the “Eliminations” figure includes charges from other Markets of £909m that

relate to inputs in services provided in WBA Market A and Wholesale Residual, the

operating costs of Retail Residual have been increased by this amount to ensure that

the total markets figure is correct.

We adopted the above treatment of inter-market charges in the 31 July 2015 RFS following the changes to market reporting (as described in section 2.1.4 (a) on page 12 of the 31 July

RFS). Whilst the treatment appropriately presents the results for all individual SMP Markets, Total SMP markets and Total Markets, it is not an appropriate presentation of the results for Wholesale Residual, Total Wholesale Markets and Retail Residual.

Accordingly, we have amended the presentation of the results of those residual and aggregated disclosures and of the eliminations, which we consider more appropriately present the results of these residual markets.

In this amended presentation in Table 2 below:

Charges from other Markets of £909m that relate to inputs in services provided by

WBA Market A and Wholesale Residual are eliminated before the “Total Wholesale

Markets”. The “Eliminations” line relates only to charges from Wholesale Markets to

Retail Residual.

Charges of £49.7m to WBA Market A from other markets (as disclosed in section

10.2.1 on page 101 of the 31 July 2015 RFS) are shown within the £148m operating

costs below and charges of £859m to Wholesale Residual from other Markets are

shown within the £2,253m operating cost below.

The operating costs of Retail Residual include the charges from Wholesale Markets

to Retail Residual.

In this amended presentation, the reported results of all individual SMP markets (including all supplementary schedules), Total SMP Markets and Total Markets are unchanged from those shown in the RFS. This amended presentation affects certain schedules in the RFS which are listed below:

Section 5.1 and 5.2 – Performance Summary by Market for 2015 and 2014 (restated).

Section 6.1.1 and 6.1.2 – Attribution of Wholesale Current Costs 2015 and 2014

(restated). In the amended schedules a new “EOI eliminations” column has been

added.

Separately to this, since publication of the 31 July 2015 RFS, Ofcom has clarified that the “Adjustment for EOI and Internal” line included in the pro-forma financial statements for WBA Market A (Sections 10.2.1 and 10.2.4) was intended to show the impact of removing internal EOI based charges from the fully allocated costs of this market and also the impact of reducing both internal and external revenues by the same amount. We have also made this change within the Revised RFS.

Section 2 – Basis of Preparation

Page 17

Table 1 - Extract from Section 5.1 Performance Summary by Market 2015 of the 31 July 2015 RFS (page 25)

Total SMP Markets 3,192 2,506 5,698 2,453 1,383 (54) 177 (24) (2) 3,933 1,765 12,485 14.2 %

Wholesale Residual 2,154 784 2,938 1,344 454 (14) (34) (29) 1 1,722 1,216 2,140 56.8 %

Total Wholesale Markets 5,346 3,290 8,636 3,797 1,837 (68) 143 (53) (1) 5,655 2,981 14,625 20.4 %

Retail Residual - 14,691 14,691 13,437 794 - - - 1 14,232 459 4,377 10.5 %

Eliminations (5,347) - (5,347) (5,347) - - - - - (5,347) - -

Roundings 1 (2) (1) - (1)

Total Markets - 17,979 17,979 11,887 2,631 (68) 143 (53) - 14,540 3,439 19,002 18.1 %

Table 2 - Amended Presentation of Residual Market results and eliminations included in the Revised RFS

Total SMP Markets 3,192 2,506 5,698 2,453 1,383 (54) 177 (24) (2) 3,933 1,765 12,485 14.2%

Wholesale Residual 2,154 784 2,938 2,253 454 (14) (34) (29) 1 2,631 307 2,140 14.3%

EOI Eliminations (909) - (909) (909) - - - - - (909) - -

Total Wholesale Markets 4,437 3,290 7,727 3,797 1,837 (68) 143 (53) (1) 5,655 2,072 14,625 14.2%

Retail Residual - 14,691 14,691 12,528 794 - - - 1 13,323 1,368 4,377 31.3 %

Eliminations (4,438) - (4,438) (4,438) - - - - - (4,438) - -

Roundings 1 (2) (1) - - - - - - - (1) -

Total Markets - 17,979 17,979 11,887 2,631 (68) 143 (53) - 14,540 3,439 19,002 18.1 %

Internal

Revenue

External

Revenue

Total

Revenue Operating Costs Depreciation

Holding

(gain)/loss

Supp.

Dep.

Other CCA

Adjs. Roundings

Total CCA

Operating

Costs Return

Mean Capital

Employed

Return on

MCE

Section 2 – Basis of Preparation

Page 18

2. Ethernet Electronics component attribution in 2013/14 comparatives