Embed Size (px)

Citation preview

Rice farming in the Philippines: some facts and opportunities

V. Bruce J. Tolentino, Ph.D. Deputy Director-General International Rice Research Institute September 2015

Yes! But how?

R. Mendoza (June 2015)

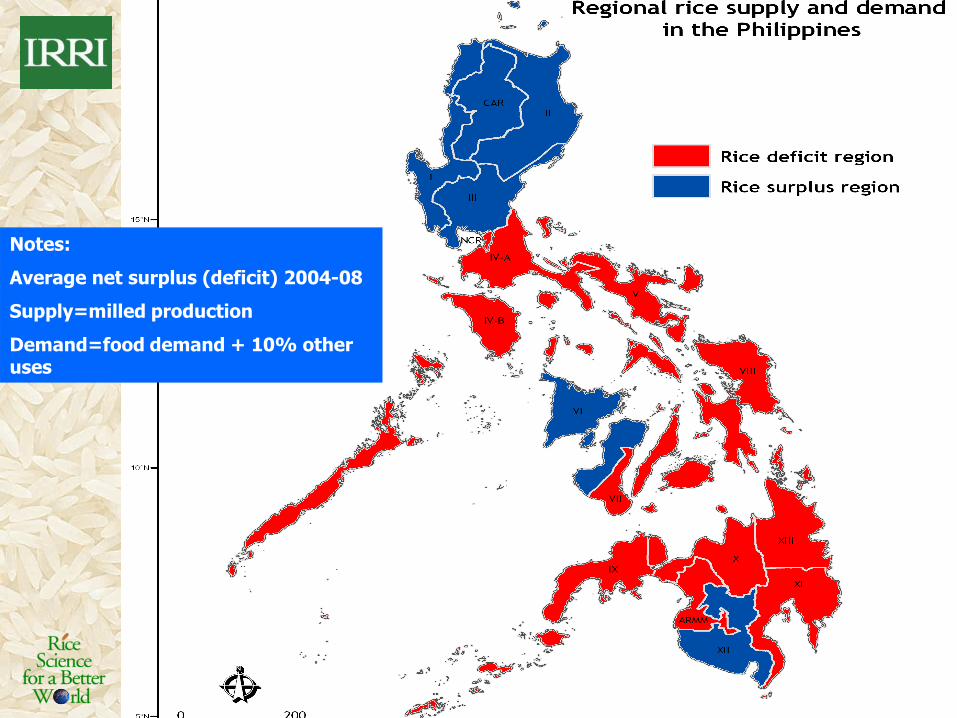

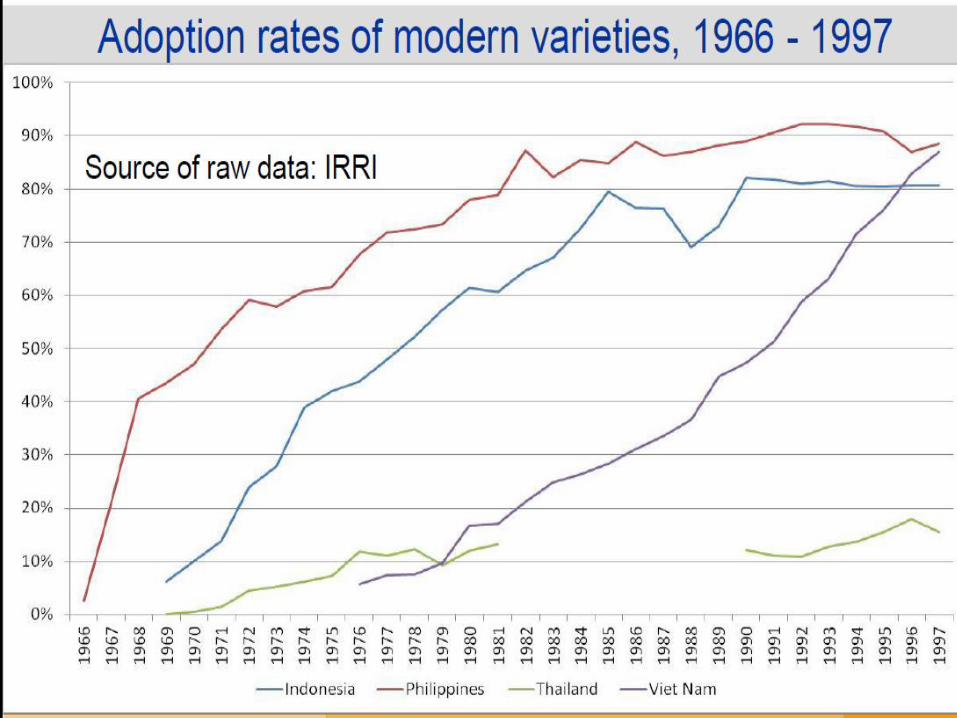

Areas planted to rice

Notes:

Average net surplus (deficit) 2004-08

Supply=milled production

Demand=food demand + 10% other uses

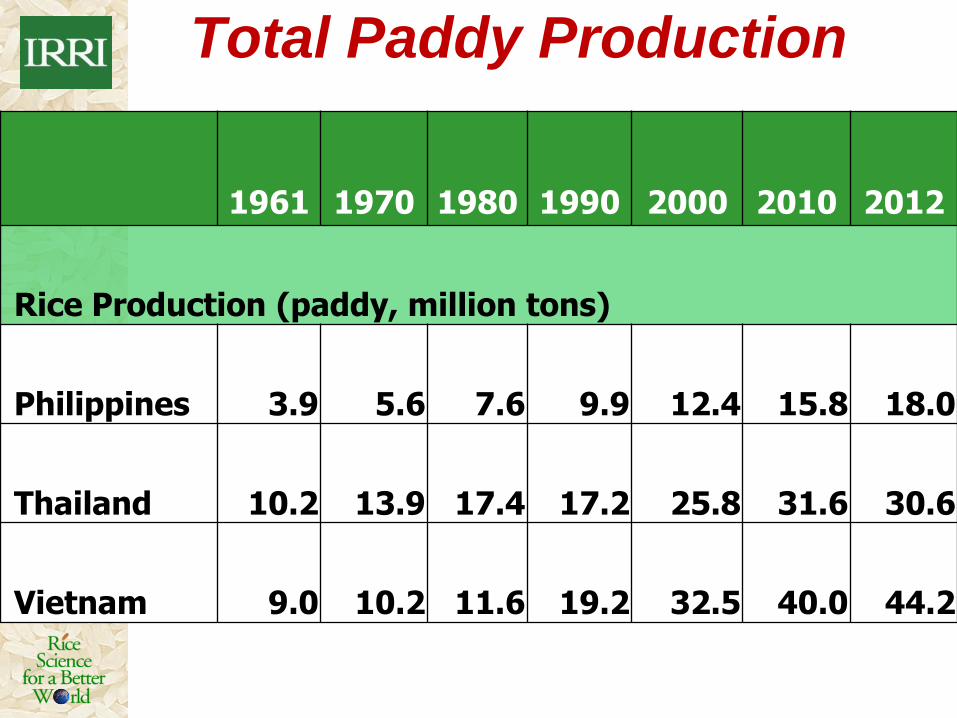

Total Paddy Production

1961 1970 1980 1990 2000 2010 2012

Rice Production (paddy, million tons)

Philippines 3.9 5.6 7.6 9.9 12.4 15.8 18.0

Thailand 10.2 13.9 17.4 17.2 25.8 31.6 30.6

Vietnam 9.0 10.2 11.6 19.2 32.5 40.0 44.2

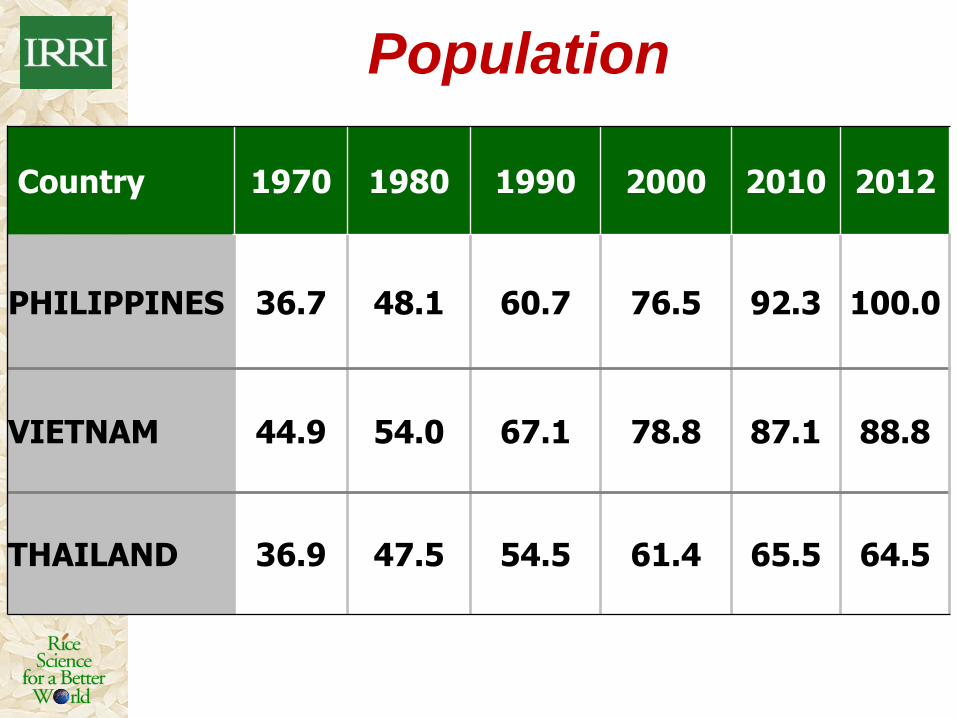

Population

Country 1970 1980 1990 2000 2010 2012

PHILIPPINES 36.7 48.1 60.7 76.5 92.3 100.0

VIETNAM 44.9 54.0 67.1 78.8 87.1 88.8

THAILAND 36.9 47.5 54.5 61.4 65.5 64.5

45

50

55

60

65

70

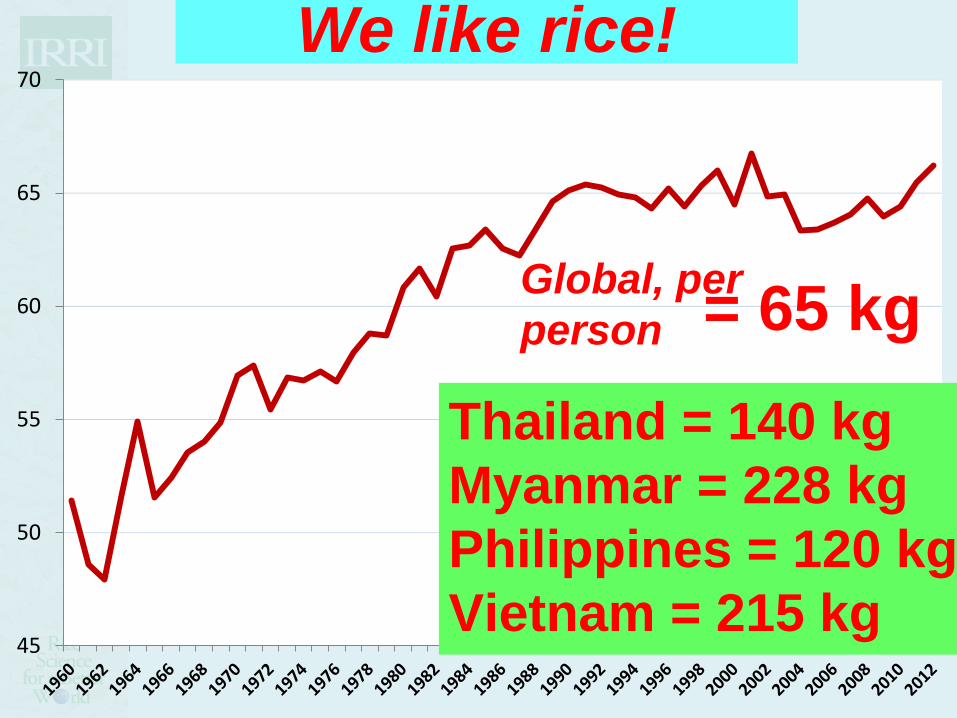

Consumption per capita in kg/person

Thailand = 140 kg

Myanmar = 228 kg

Philippines = 120 kg

Vietnam = 215 kg

We like rice!

Global, per

person = 65 kg

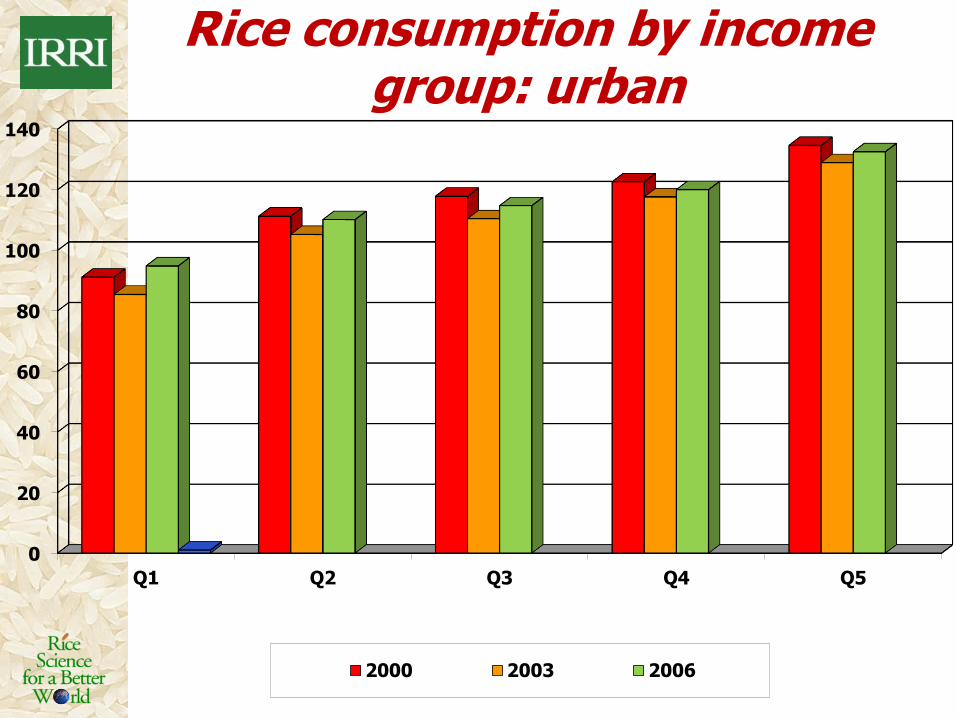

Rice consumption by income group: urban

0

20

40

60

80

100

120

140

Q1 Q2 Q3 Q4 Q5

2000 2003 2006

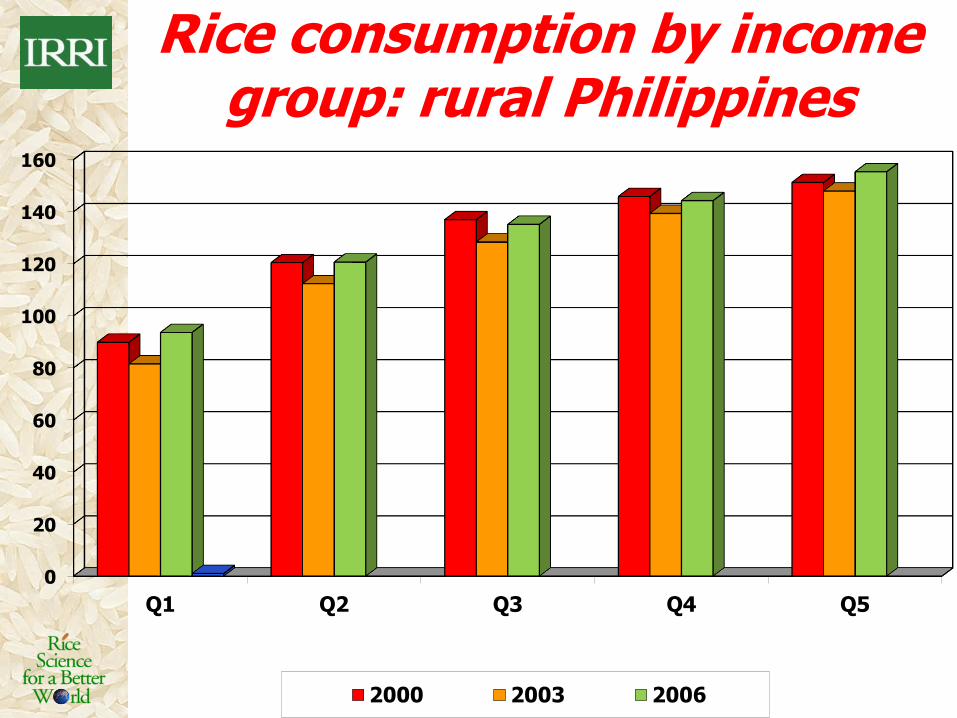

Rice consumption by income group: rural Philippines

0

20

40

60

80

100

120

140

160

Q1 Q2 Q3 Q4 Q5

2000 2003 2006

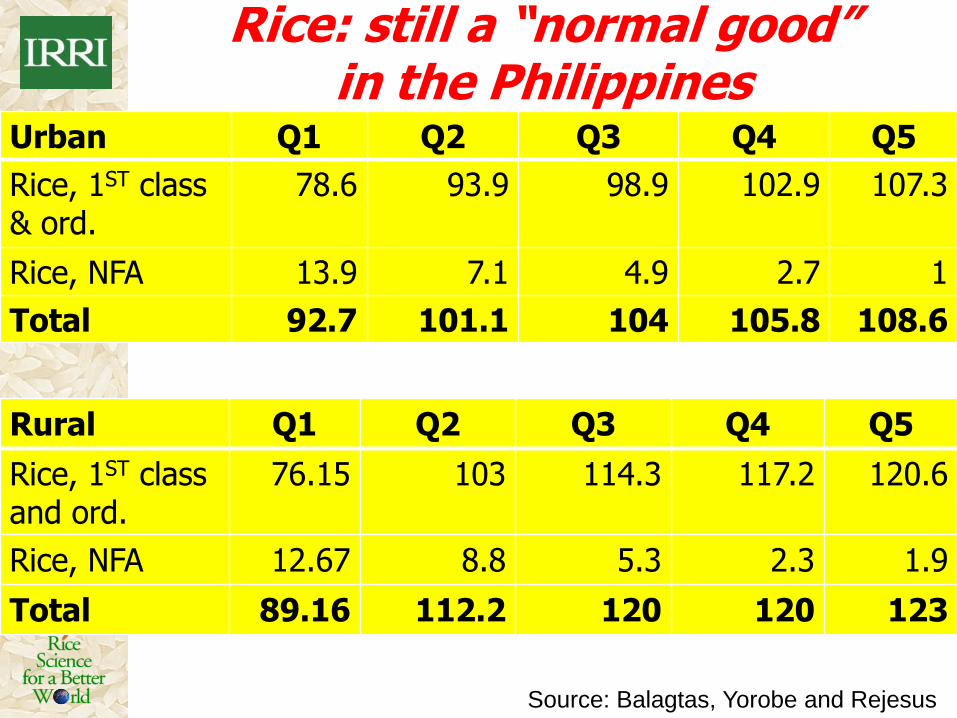

Rice: still a “normal good” in the Philippines

Urban Q1 Q2 Q3 Q4 Q5

Rice, 1ST class & ord.

78.6 93.9 98.9 102.9 107.3

Rice, NFA 13.9 7.1 4.9 2.7 1

Total 92.7 101.1 104 105.8 108.6

Rural Q1 Q2 Q3 Q4 Q5

Rice, 1ST class and ord.

76.15 103 114.3 117.2 120.6

Rice, NFA 12.67 8.8 5.3 2.3 1.9

Total 89.16 112.2 120 120 123

Source: Balagtas, Yorobe and Rejesus

2.4 M Filipino rice farmers

Average farm size of

1.14 ha.

Changes in rice farming in the

Philippines: Insights from five

decades of IRRI Loop Survey

Kei Kajisa September 3, 2015

IRRI Loop Survey

•Initiated in 1966, every 4-5 years until 2011-12, 23 rounds;

•Detailed records on rice production in both wet and dry seasons.

•The world’s longest survey series of rice farming and rice farm families.

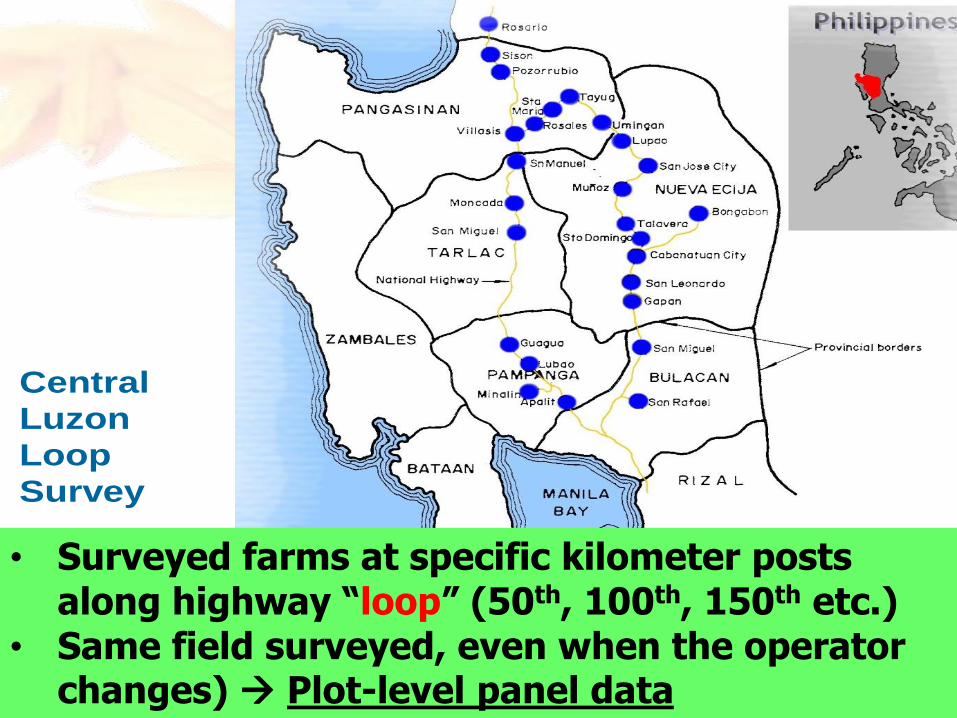

Central

Luzon

Loop

Survey

• Surveyed farms at specific kilometer posts along highway “loop” (50th, 100th, 150th etc.)

• Same field surveyed, even when the operator changes) Plot-level panel data

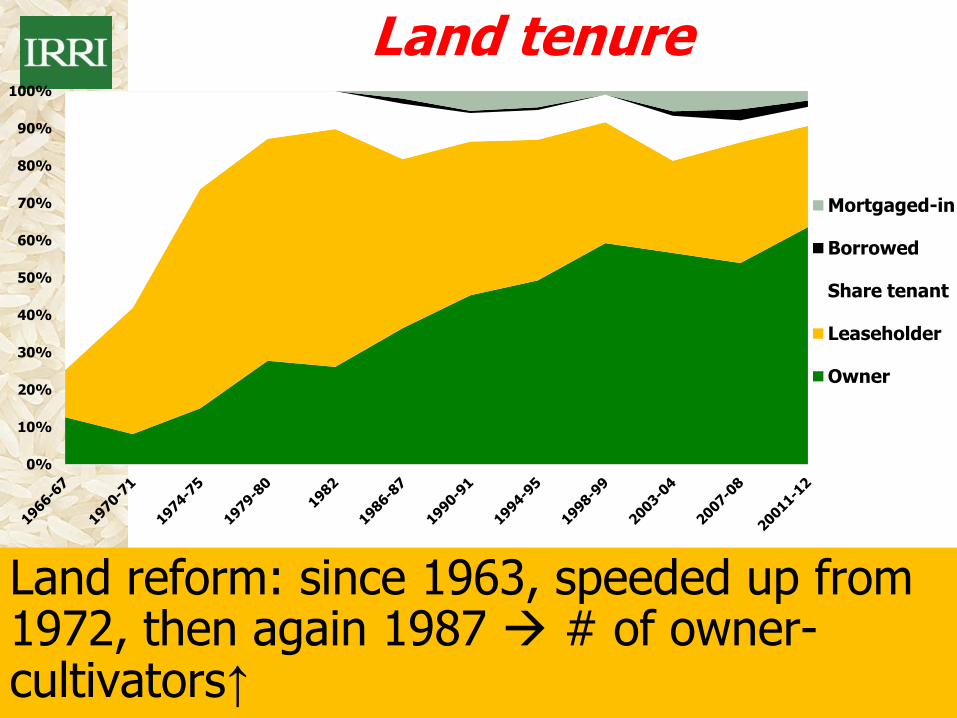

Land reform: since 1963, speeded up from 1972, then again 1987 # of owner-cultivators↑

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Land tenure

Mortgaged-in

Borrowed

Share tenant

Leaseholder

Owner

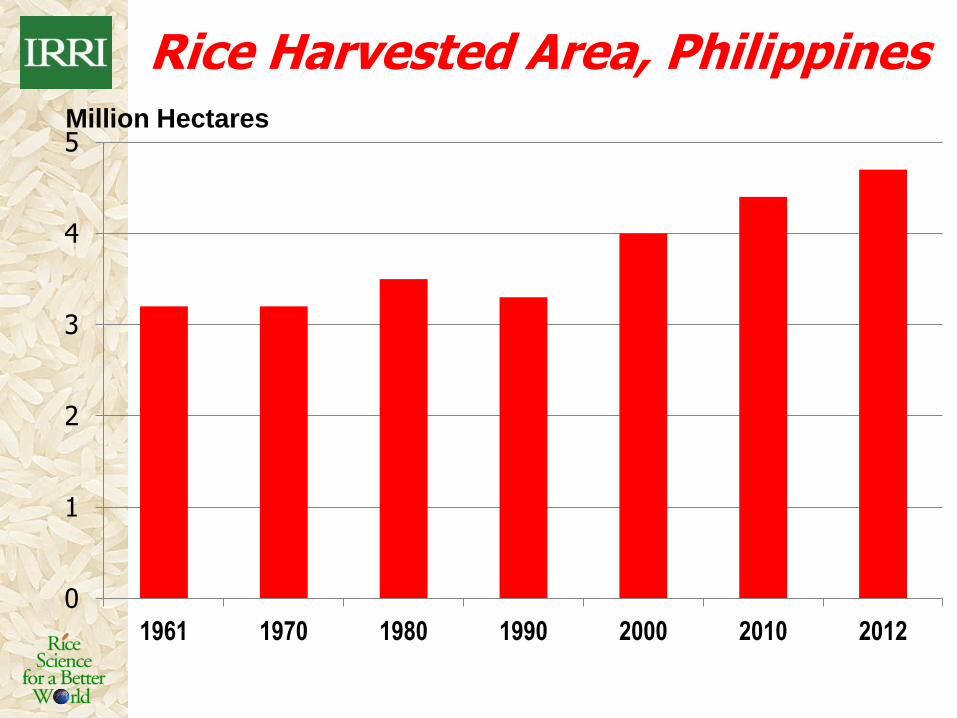

Rice Harvested Area, Philippines

0

1

2

3

4

5

1961 1970 1980 1990 2000 2010 2012

Million Hectares

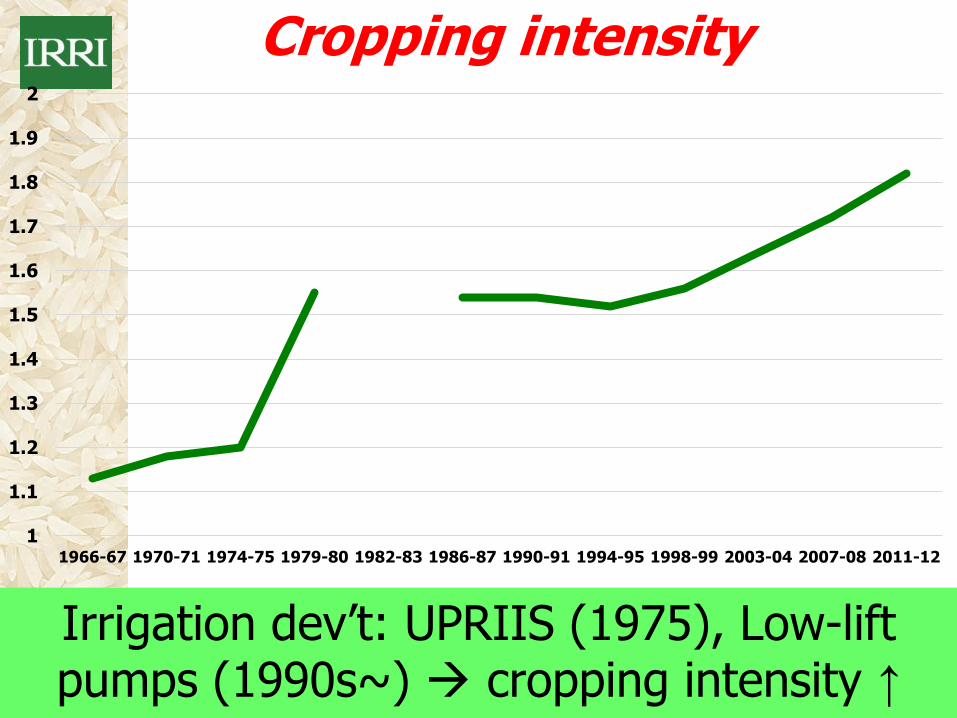

Irrigation dev’t: UPRIIS (1975), Low-lift pumps (1990s~) cropping intensity ↑

1

1.1

1.2

1.3

1.4

1.5

1.6

1.7

1.8

1.9

2

1966-67 1970-71 1974-75 1979-80 1982-83 1986-87 1990-91 1994-95 1998-99 2003-04 2007-08 2011-12

Cropping intensity

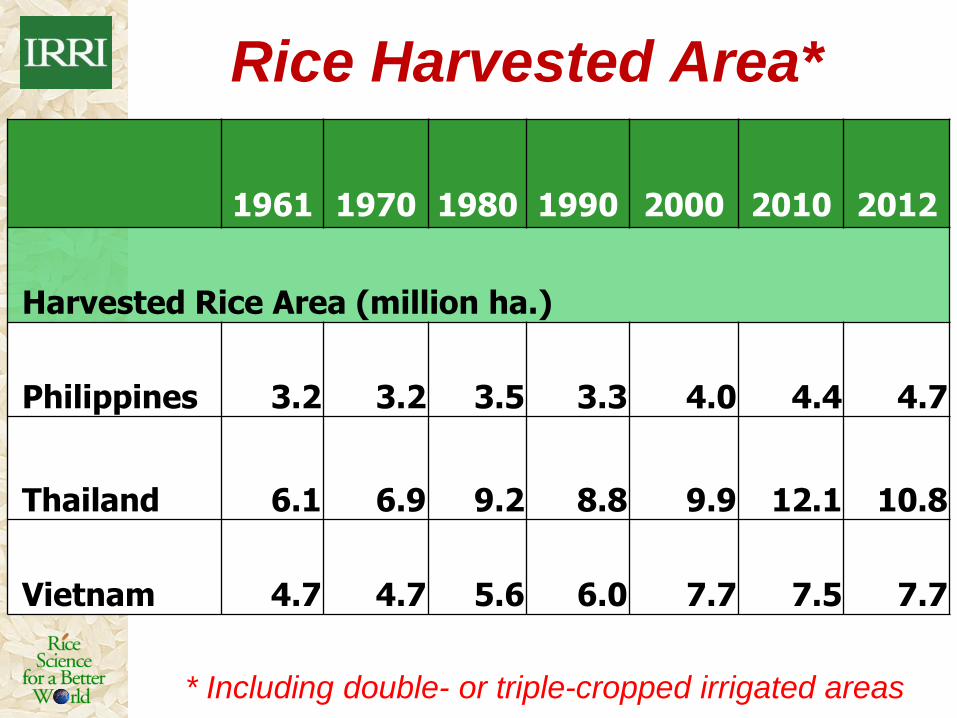

Rice Harvested Area*

1961 1970 1980 1990 2000 2010 2012

Harvested Rice Area (million ha.)

Philippines 3.2 3.2 3.5 3.3 4.0 4.4 4.7

Thailand 6.1 6.9 9.2 8.8 9.9 12.1 10.8

Vietnam 4.7 4.7 5.6 6.0 7.7 7.5 7.7

* Including double- or triple-cropped irrigated areas

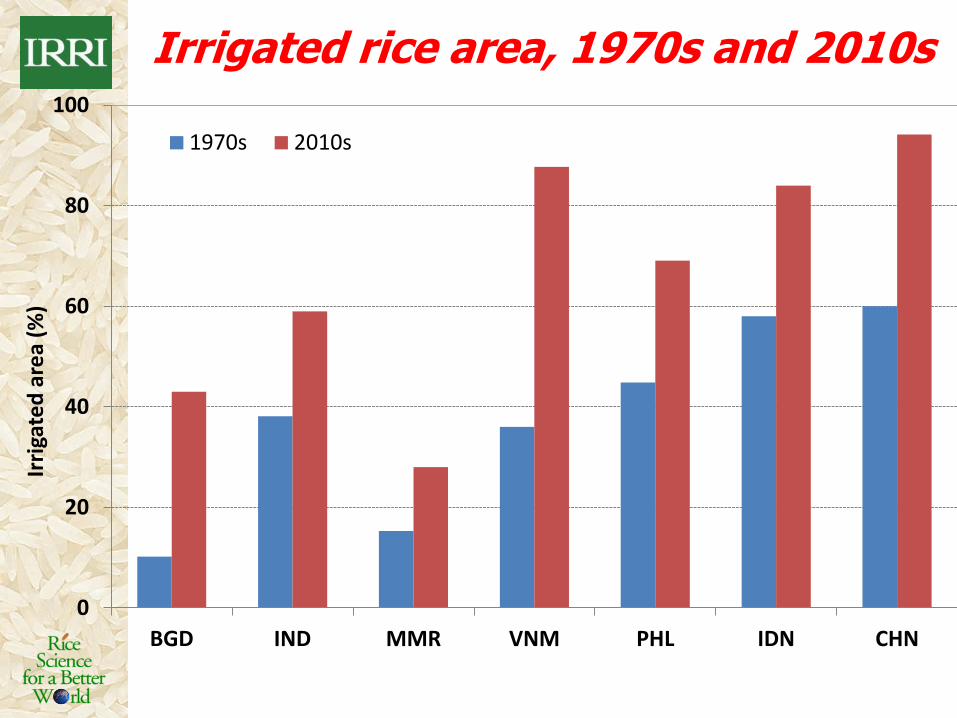

Irrigated rice area, 1970s and 2010s

0

20

40

60

80

100

BGD IND MMR VNM PHL IDN CHN

Irri

gate

d a

rea

(%)

1970s 2010s

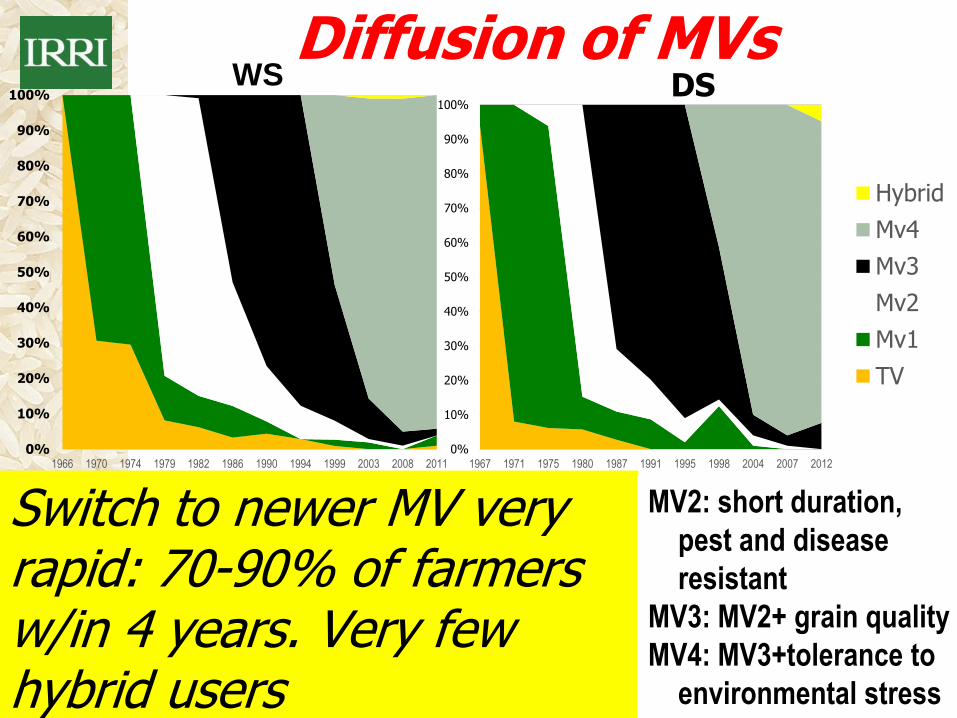

Diffusion of MVs

Switch to newer MV very rapid: 70-90% of farmers w/in 4 years. Very few hybrid users

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1966 1970 1974 1979 1982 1986 1990 1994 1999 2003 2008 2011

WS

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1967 1971 1975 1980 1987 1991 1995 1998 2004 2007 2012

DS

Hybrid

Mv4

Mv3

Mv2

Mv1

TV

MV2: short duration,

pest and disease

resistant

MV3: MV2+ grain quality

MV4: MV3+tolerance to

environmental stress

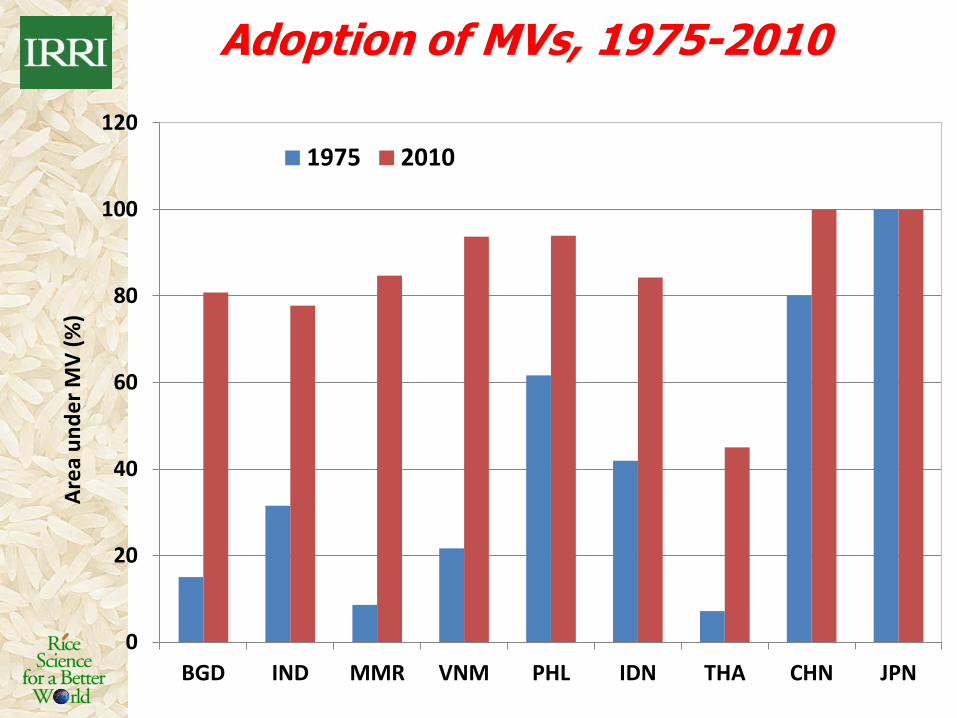

Adoption of MVs, 1975-2010

0

20

40

60

80

100

120

BGD IND MMR VNM PHL IDN THA CHN JPN

Are

a u

nd

er

MV

(%

)

1975 2010

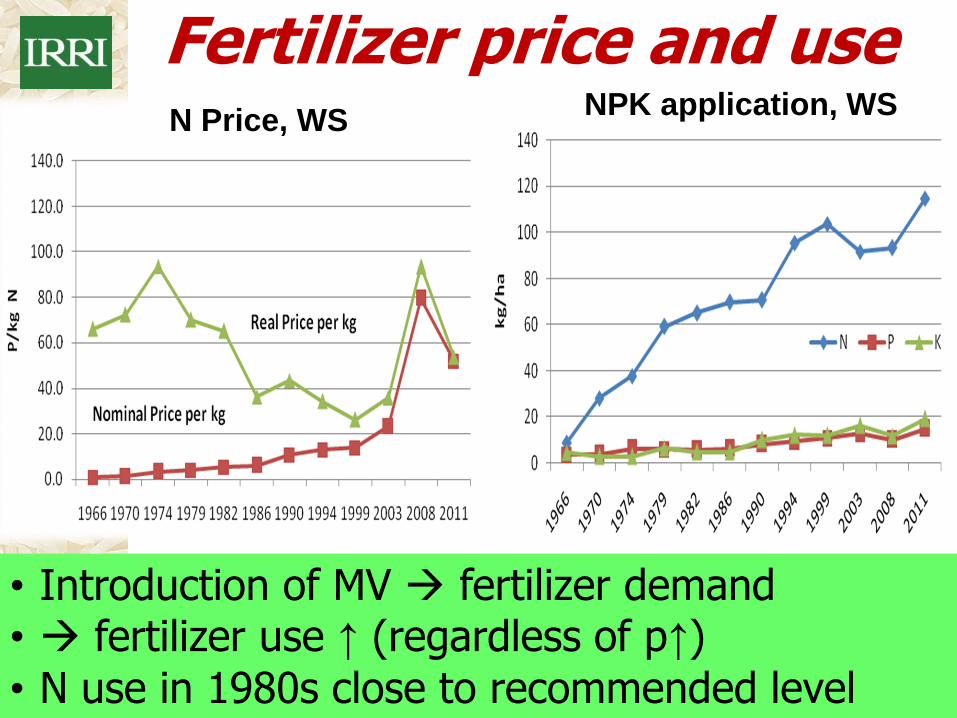

Fertilizer price and use

• Introduction of MV fertilizer demand • fertilizer use ↑ (regardless of p↑)

• N use in 1980s close to recommended level

N Price, WS NPK application, WS

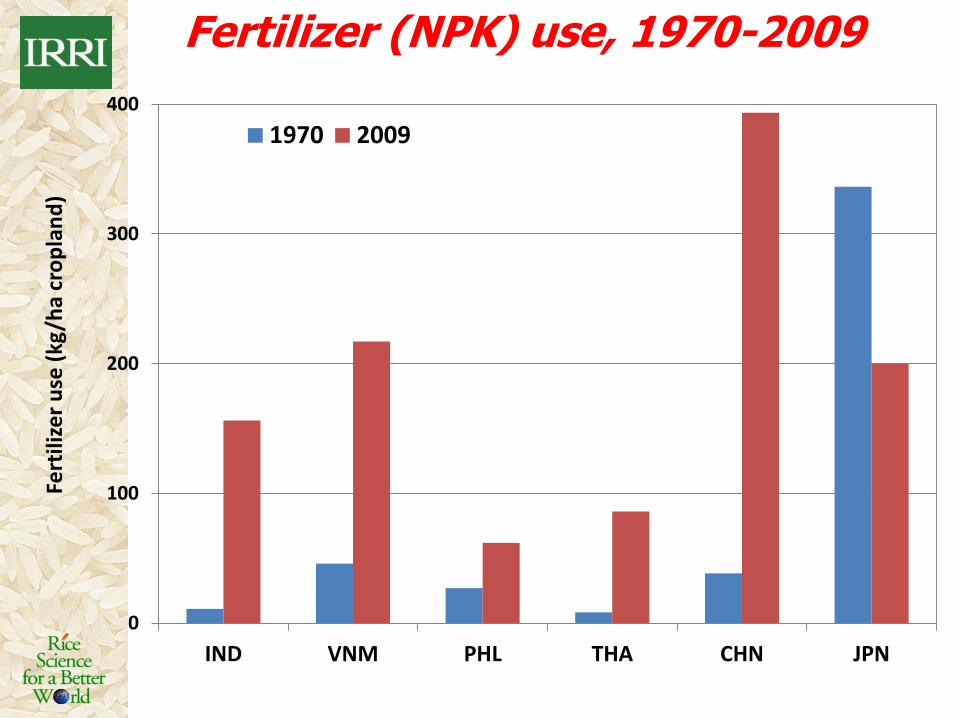

Fertilizer (NPK) use, 1970-2009

0

100

200

300

400

IND VNM PHL THA CHN JPN

Fert

ilize

r u

se (

kg/h

a cr

op

lan

d)

1970 2009

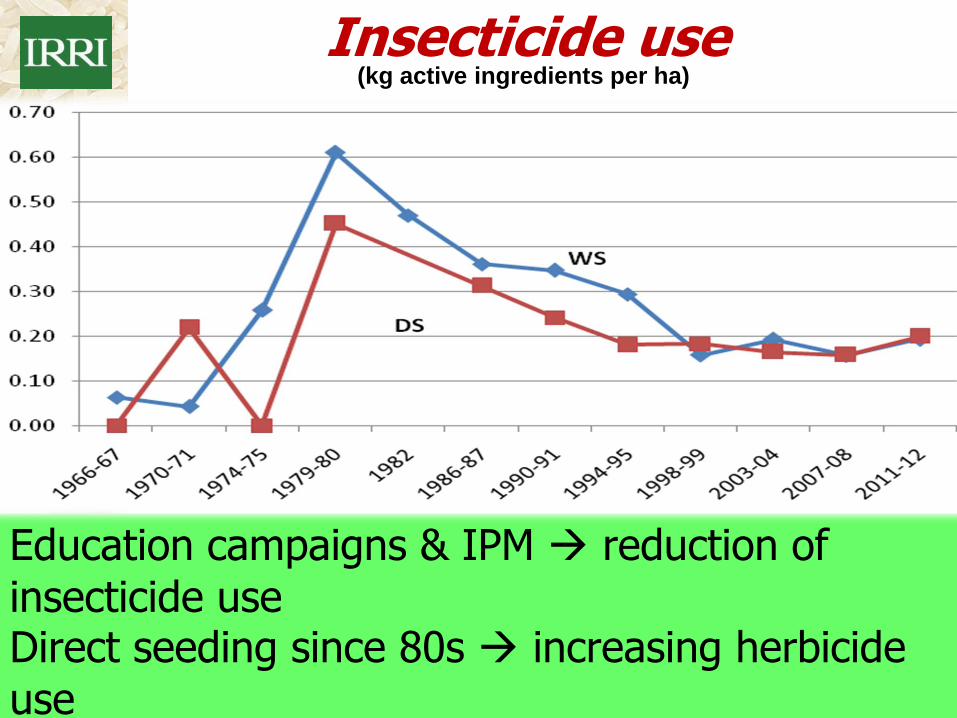

Insecticide use

Education campaigns & IPM reduction of

insecticide use Direct seeding since 80s increasing herbicide

use

(kg active ingredients per ha)

Maintaining low insecticide use

• Philippines farms use the lowest amount than other countries: Thai, Vietnam, Indonesia, and China;

• New varieties released since 1997 have less resistance to pests and diseases (Laborte et. al, 2015);

• Should resistance traits again be added to future varieties? Are there alternative approaches to pest management?

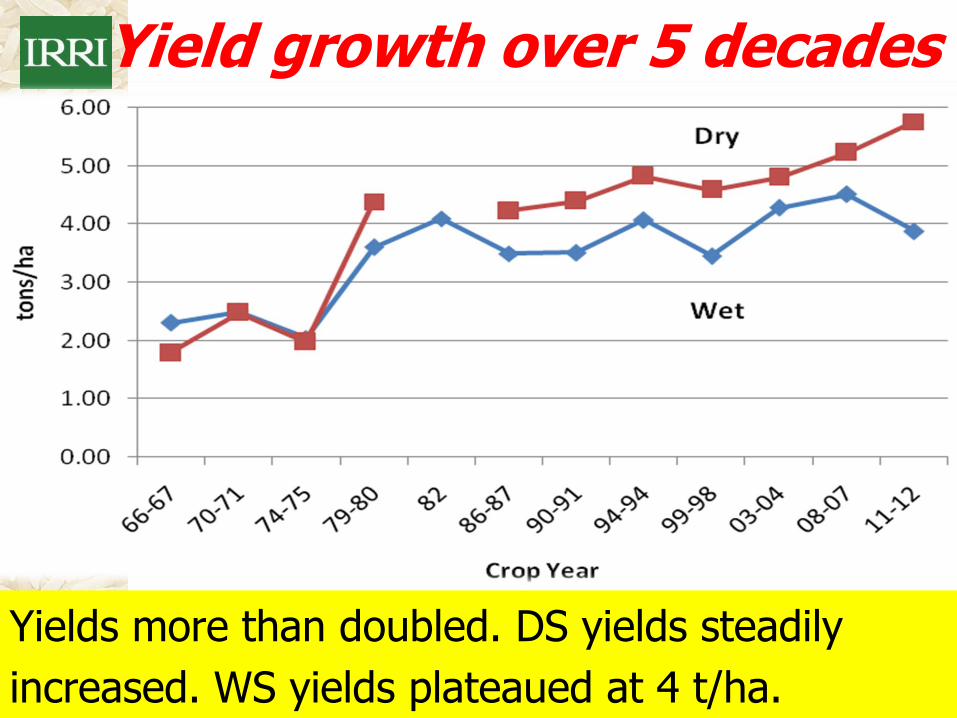

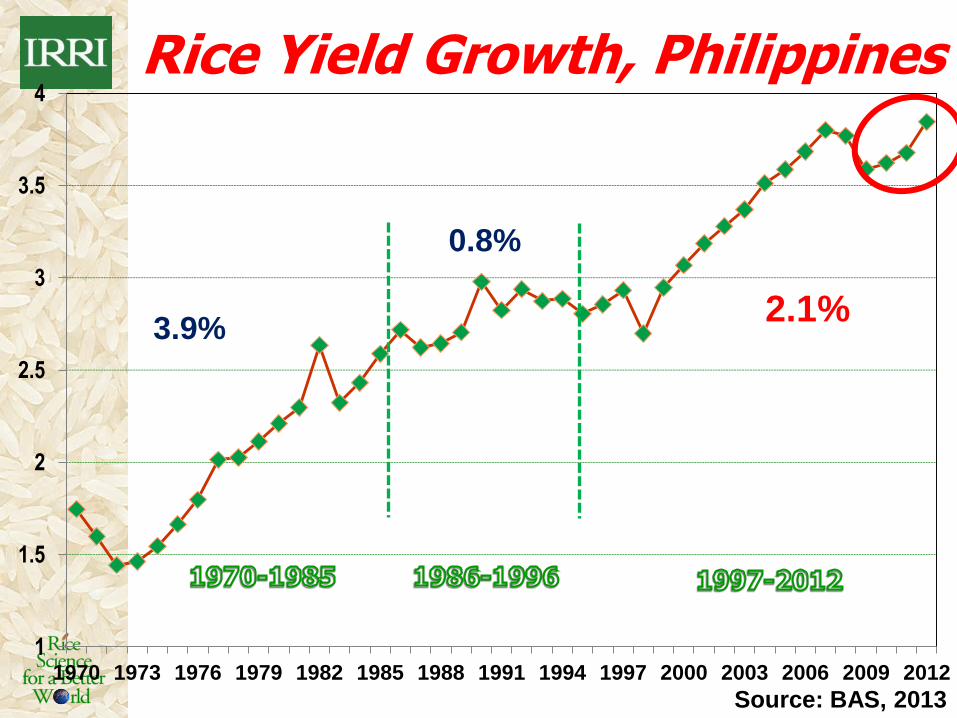

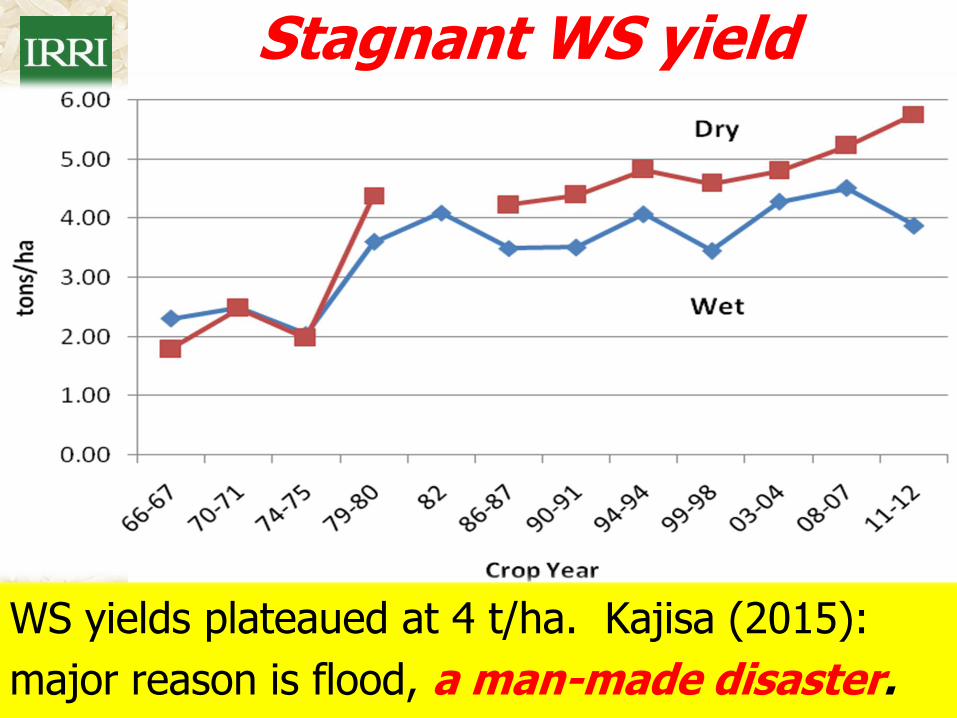

Yield growth over 5 decades

Yields more than doubled. DS yields steadily

increased. WS yields plateaued at 4 t/ha.

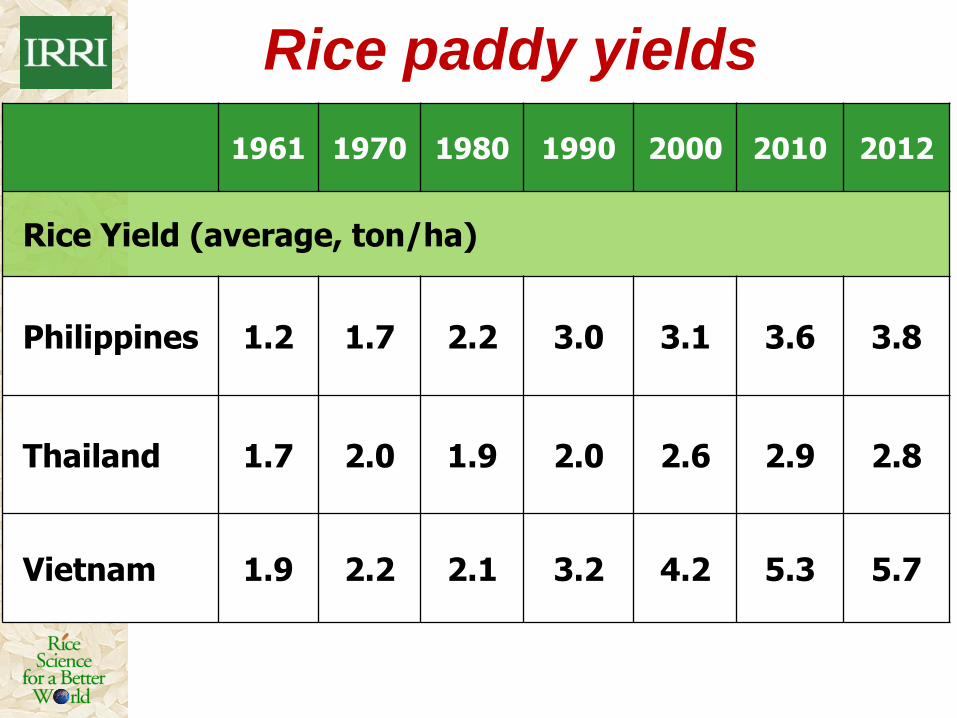

Rice paddy yields

1961 1970 1980 1990 2000 2010 2012

Rice Yield (average, ton/ha)

Philippines 1.2 1.7 2.2 3.0 3.1 3.6 3.8

Thailand 1.7 2.0 1.9 2.0 2.6 2.9 2.8

Vietnam 1.9 2.2 2.1 3.2 4.2 5.3 5.7

1

1.5

2

2.5

3

3.5

4

1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 2012

3.9% 2.1%

0.8%

Source: BAS, 2013

Rice Yield Growth, Philippines

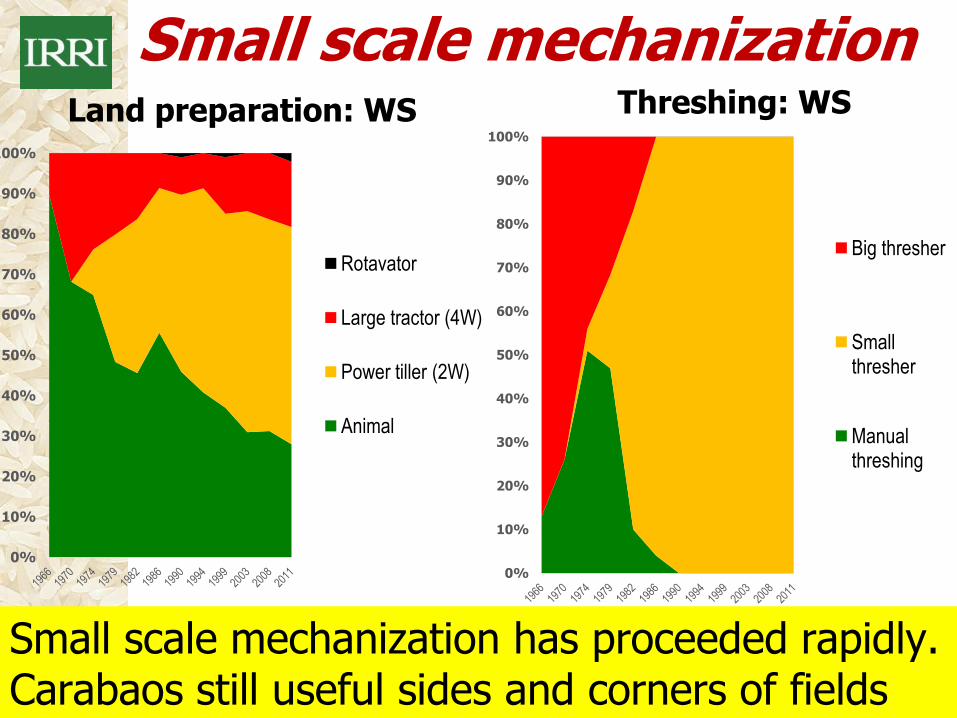

Small scale mechanization

Small scale mechanization has proceeded rapidly. Carabaos still useful sides and corners of fields

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Land preparation: WS

Rotavator

Large tractor (4W)

Power tiller (2W)

Animal

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Threshing: WS

Big thresher

Small thresher

Manual threshing

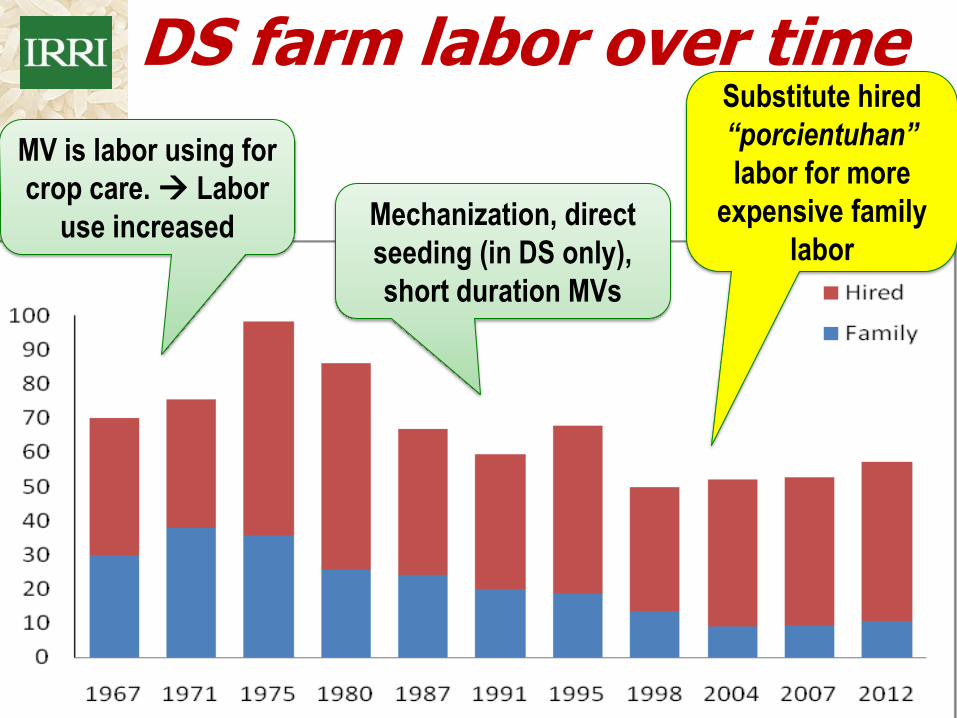

DS farm labor over time

MV is labor using for

crop care. Labor

use increased Mechanization, direct

seeding (in DS only),

short duration MVs

Substitute hired

“porcientuhan”

labor for more

expensive family

labor

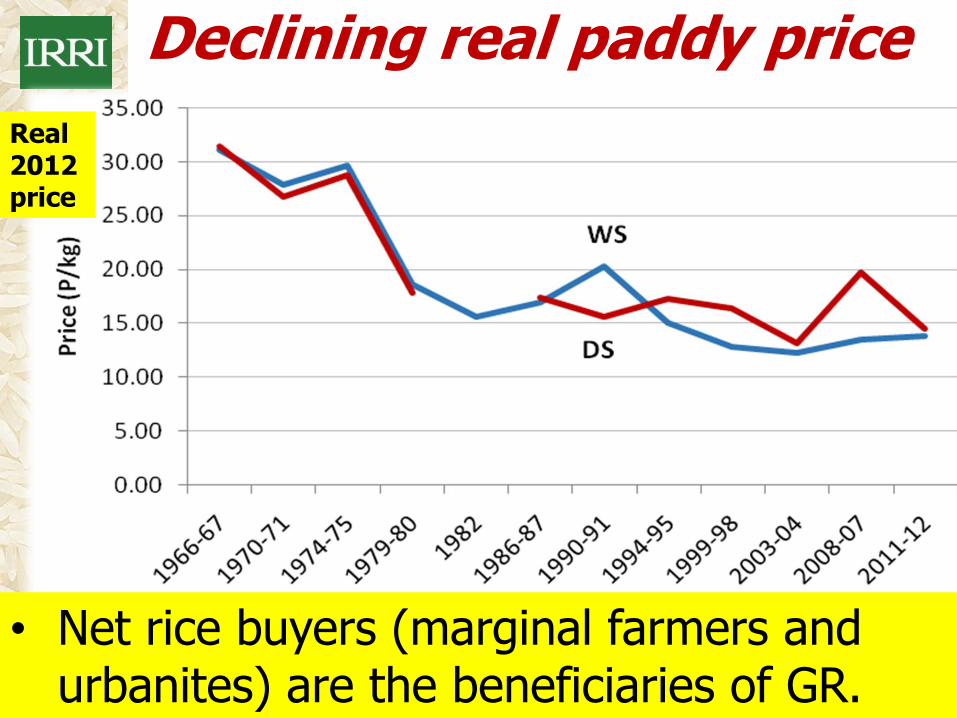

Declining real paddy price

• Net rice buyers (marginal farmers and urbanites) are the beneficiaries of GR.

Real 2012 price

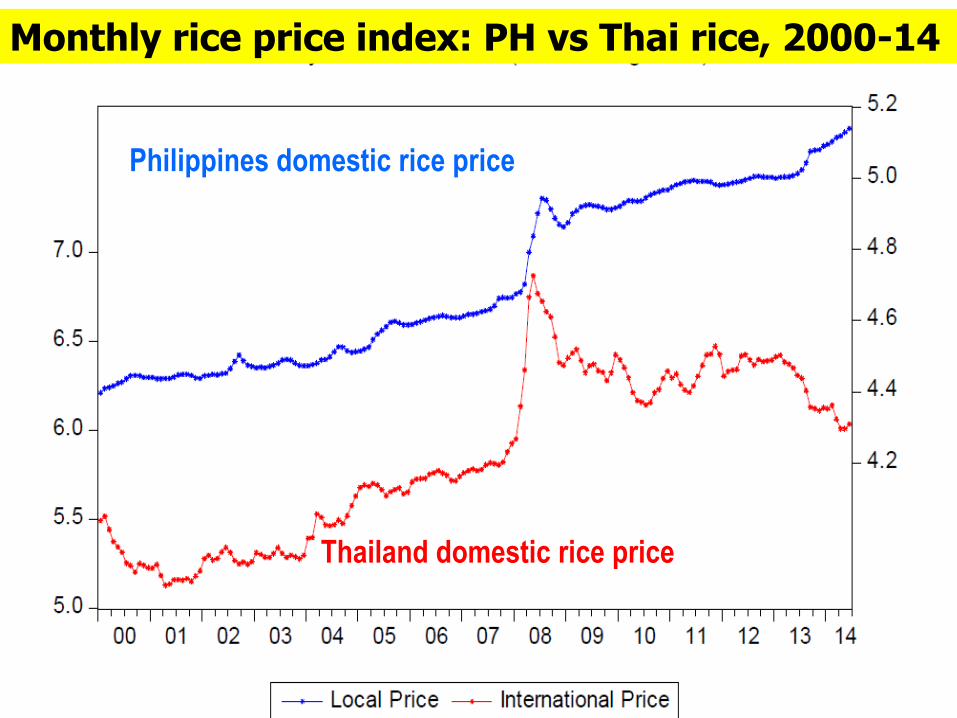

SWS

Philippines domestic rice price

Thailand domestic rice price

Monthly rice price index: PH vs Thai rice, 2000-14

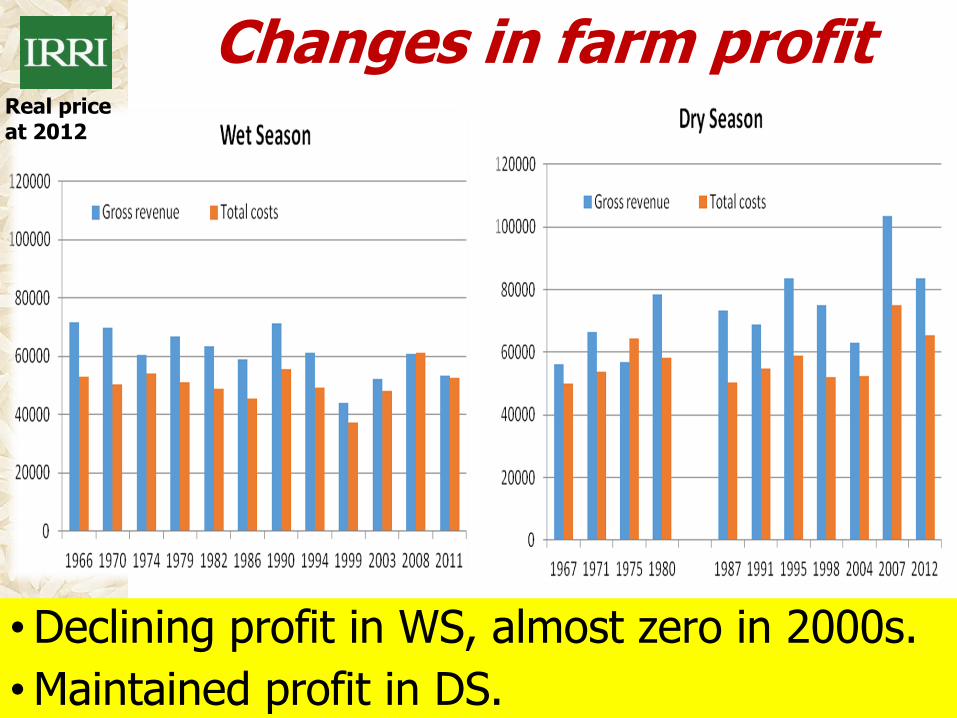

Changes in farm profit

•Declining profit in WS, almost zero in 2000s.

•Maintained profit in DS.

Real price at 2012

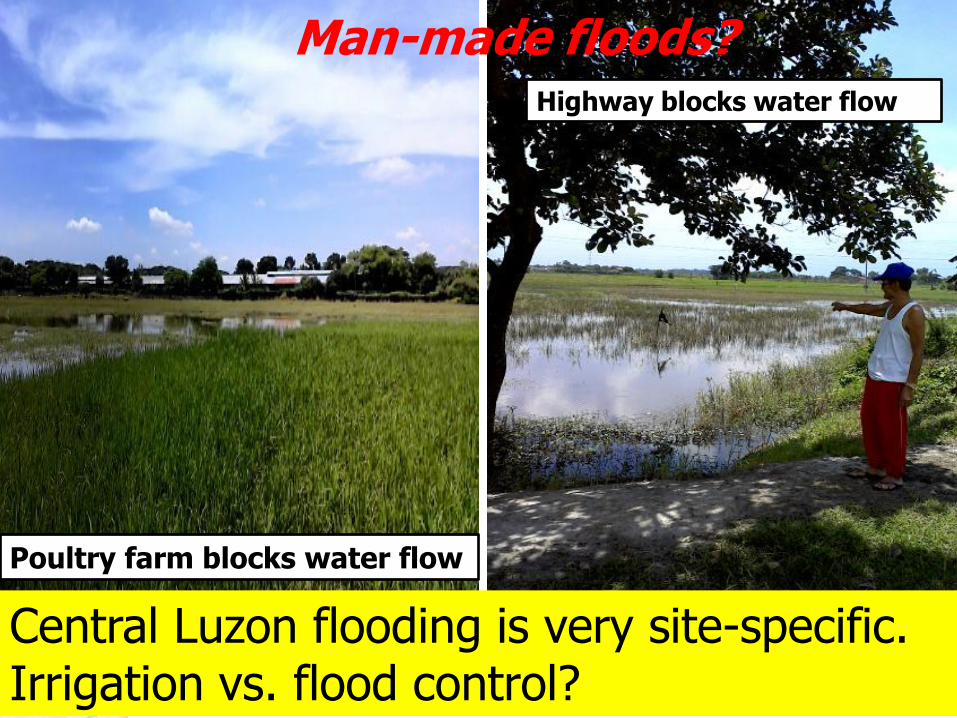

Stagnant WS yield

WS yields plateaued at 4 t/ha. Kajisa (2015):

major reason is flood, a man-made disaster.

Poultry farm blocks water flow

Highway blocks water flow

Man-made floods?

Central Luzon flooding is very site-specific. Irrigation vs. flood control?

Reducing losses due to floods

WS flooding is worsening:

•A man-made disaster? Flooded areas in patches, seriousness varies by location.

•What is best approach? Breeding or engineering?

Submarino rice survives

17 to 21 days of flooding

Samba-Sub1

Samba

Samba-Sub1

IR64-Sub1

IR49830 (Sub1)

IR64

IR42

IR64

IR64-Sub1

Samba-Sub1

IR49830 (Sub1)

Samba

IR64

IR64-Sub1

IR49830 (Sub1)

IR42

IR64-Sub1

IR64

IR49830 (Sub1)

IR49830 (Sub1)

IR42

Samba

IR42

Samba

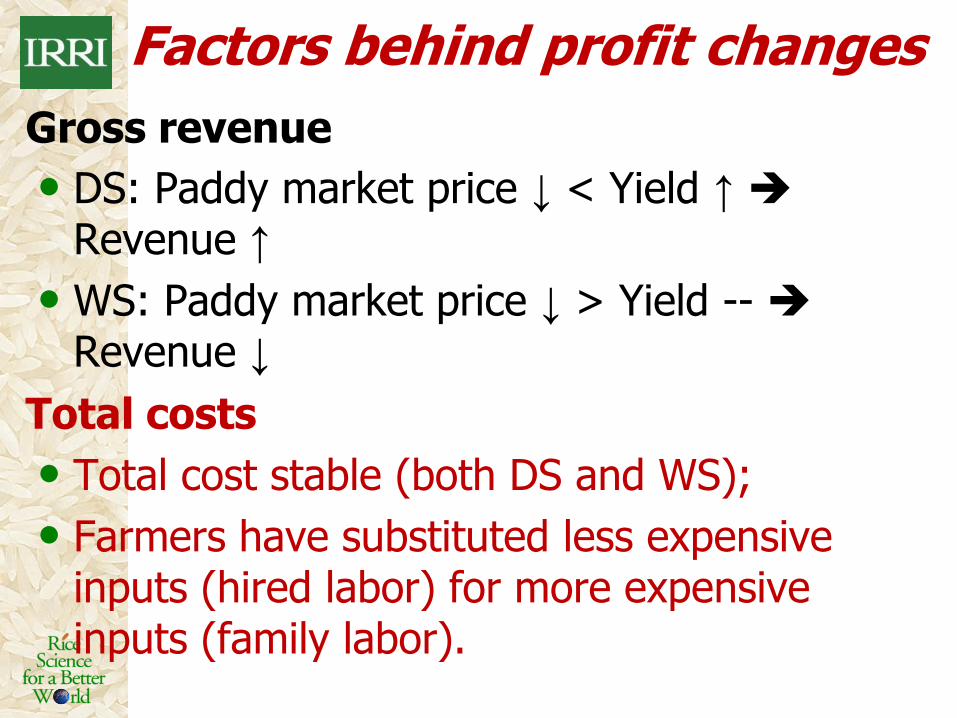

Factors behind profit changes

Gross revenue

• DS: Paddy market price ↓ < Yield ↑ Revenue ↑

• WS: Paddy market price ↓ > Yield -- Revenue ↓

Total costs

• Total cost stable (both DS and WS);

• Farmers have substituted less expensive inputs (hired labor) for more expensive inputs (family labor).

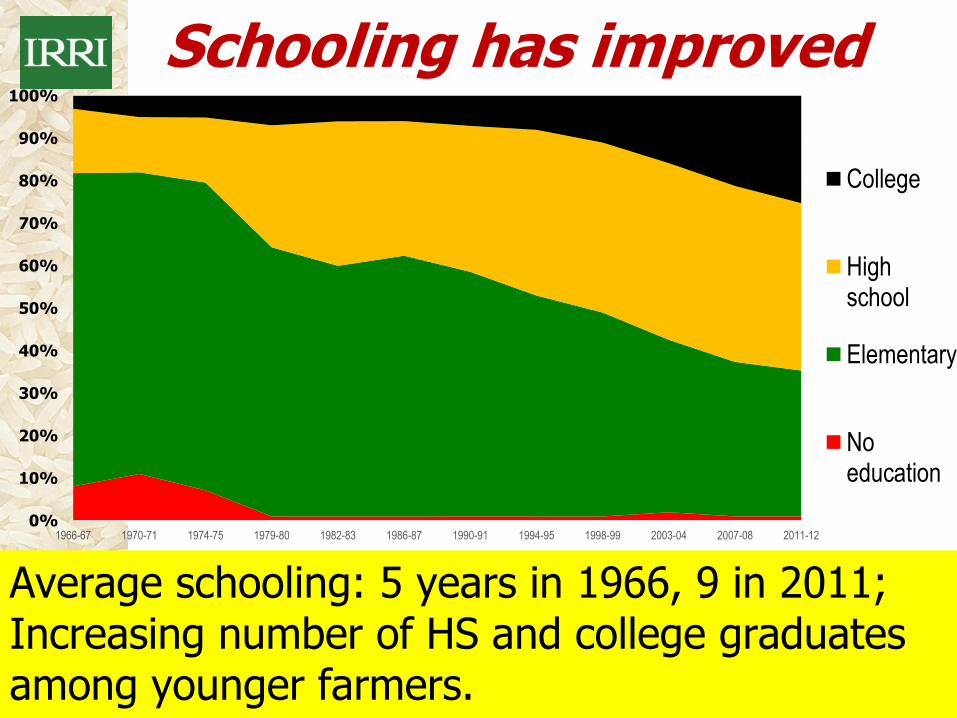

Schooling has improved

Average schooling: 5 years in 1966, 9 in 2011; Increasing number of HS and college graduates among younger farmers.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1966-67 1970-71 1974-75 1979-80 1982-83 1986-87 1990-91 1994-95 1998-99 2003-04 2007-08 2011-12

College

High school

Elementary

No education

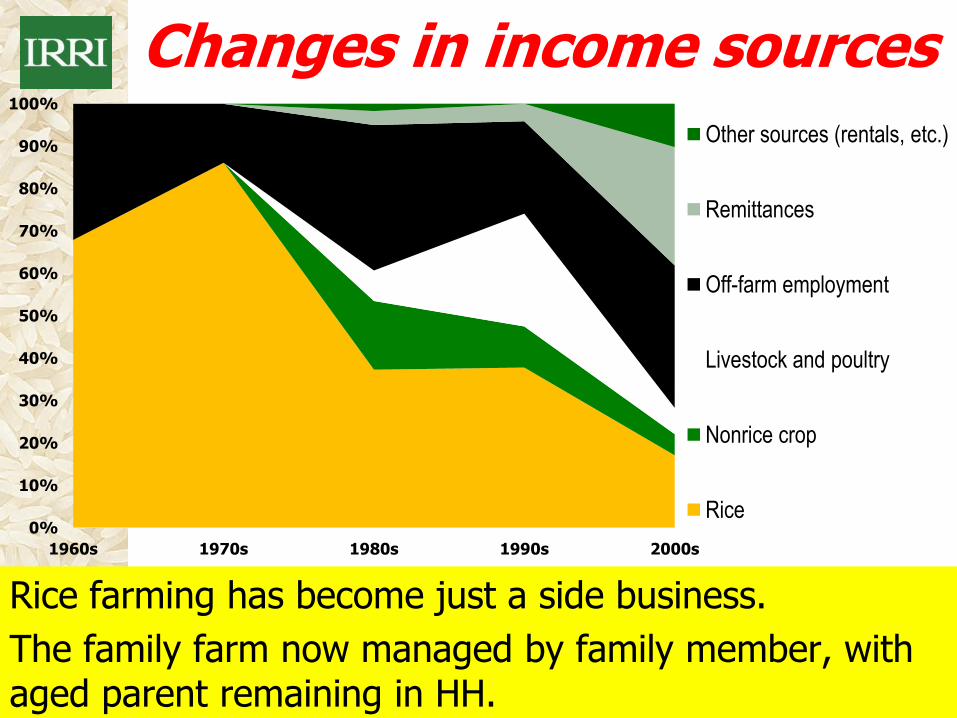

Changes in income sources

Rice farming has become just a side business.

The family farm now managed by family member, with aged parent remaining in HH.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1960s 1970s 1980s 1990s 2000s

Other sources (rentals, etc.)

Remittances

Off-farm employment

Livestock and poultry

Nonrice crop

Rice

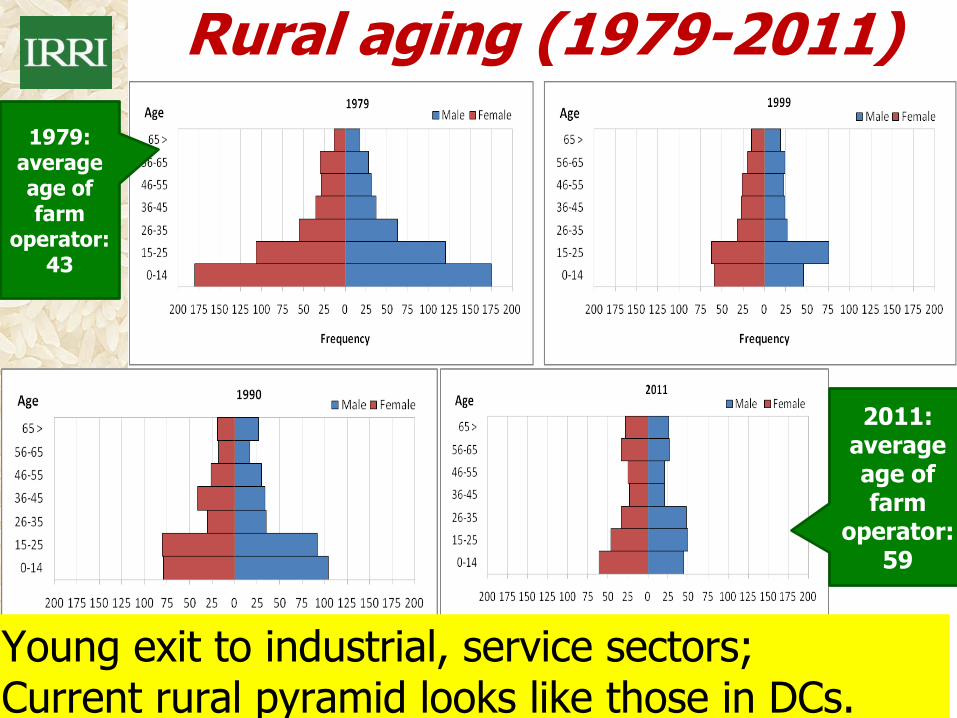

Rural aging (1979-2011)

1979: average age of farm

operator: 43

Young exit to industrial, service sectors; Current rural pyramid looks like those in DCs.

2011: average age of farm

operator: 59

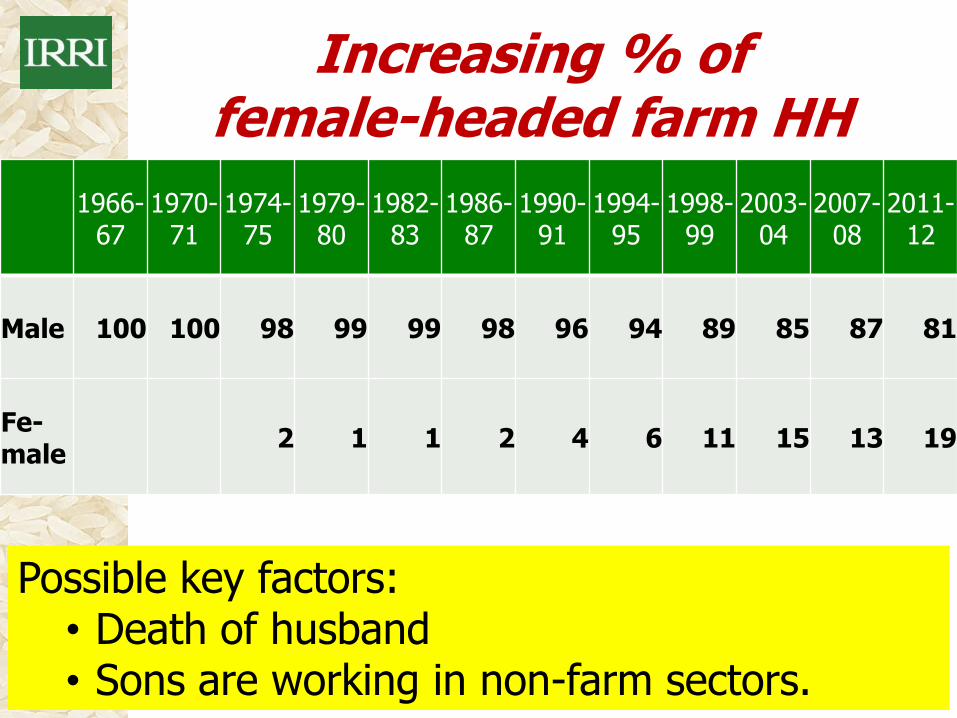

Increasing % of female-headed farm HH

1966-

67 1970-

71 1974-

75 1979-

80 1982-

83 1986-

87 1990-

91 1994-

95 1998-

99 2003-

04 2007-

08 2011-

12

Male 100 100 98 99 99 98 96 94 89 85 87 81

Fe-male

2 1 1 2 4 6 11 15 13 19

Possible key factors: • Death of husband • Sons are working in non-farm sectors.

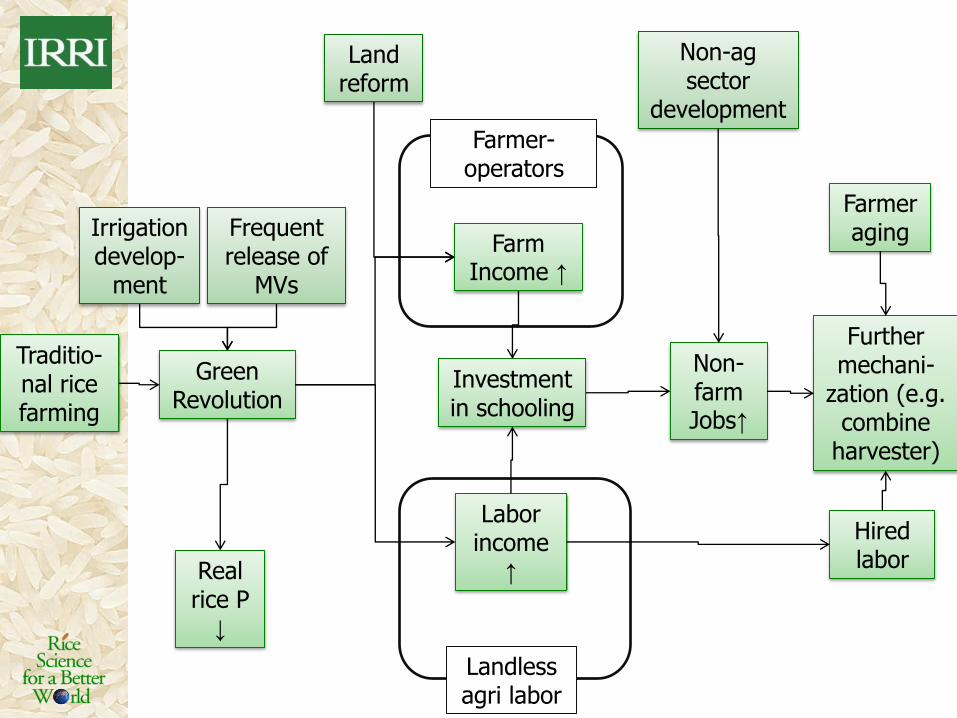

Traditio-nal rice farming

Green Revolution

Irrigation develop-

ment

Farm Income ↑

Investment in schooling

Non-farm Jobs↑

Farmer aging

Hired labor

Further mechani-

zation (e.g. combine

harvester)

Land reform

Non-ag sector

development

Frequent release of

MVs

Farmer-operators

Landless agri labor

Labor income

↑ Real rice P

↓

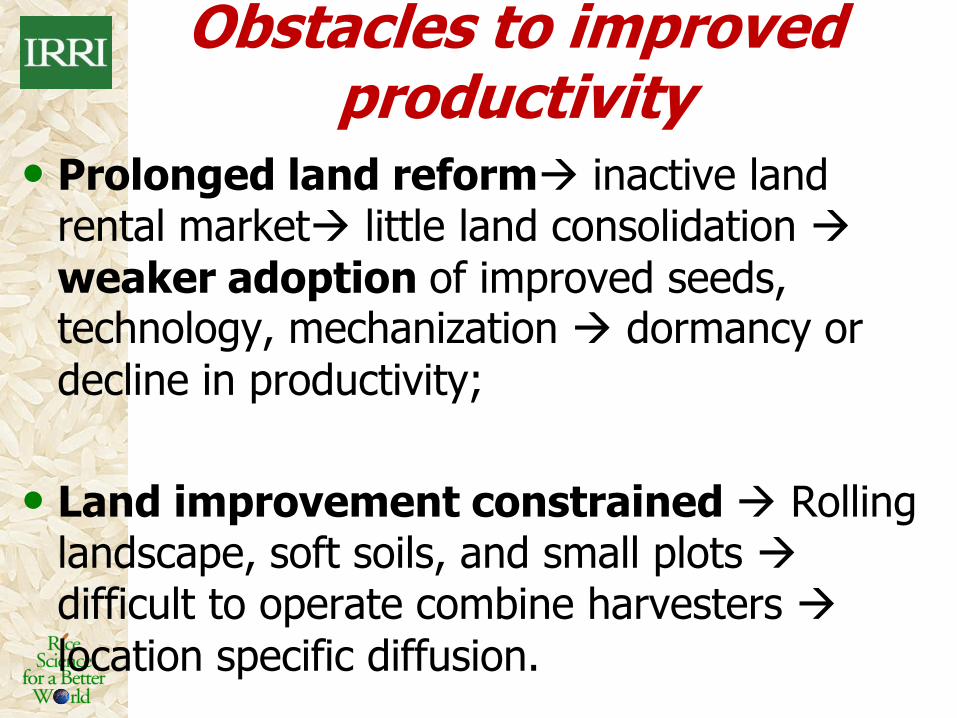

Obstacles to improved productivity

• Prolonged land reform inactive land rental market little land consolidation

weaker adoption of improved seeds, technology, mechanization dormancy or

decline in productivity;

• Land improvement constrained Rolling landscape, soft soils, and small plots difficult to operate combine harvesters

location specific diffusion.

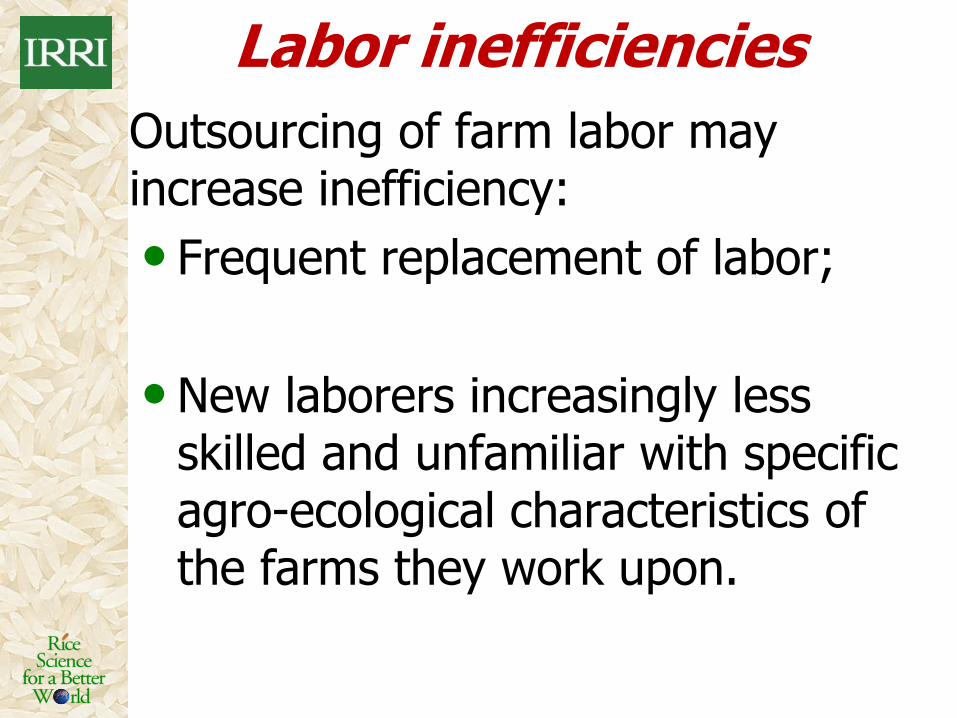

Labor inefficiencies

Outsourcing of farm labor may increase inefficiency:

• Frequent replacement of labor;

• New laborers increasingly less skilled and unfamiliar with specific agro-ecological characteristics of the farms they work upon.

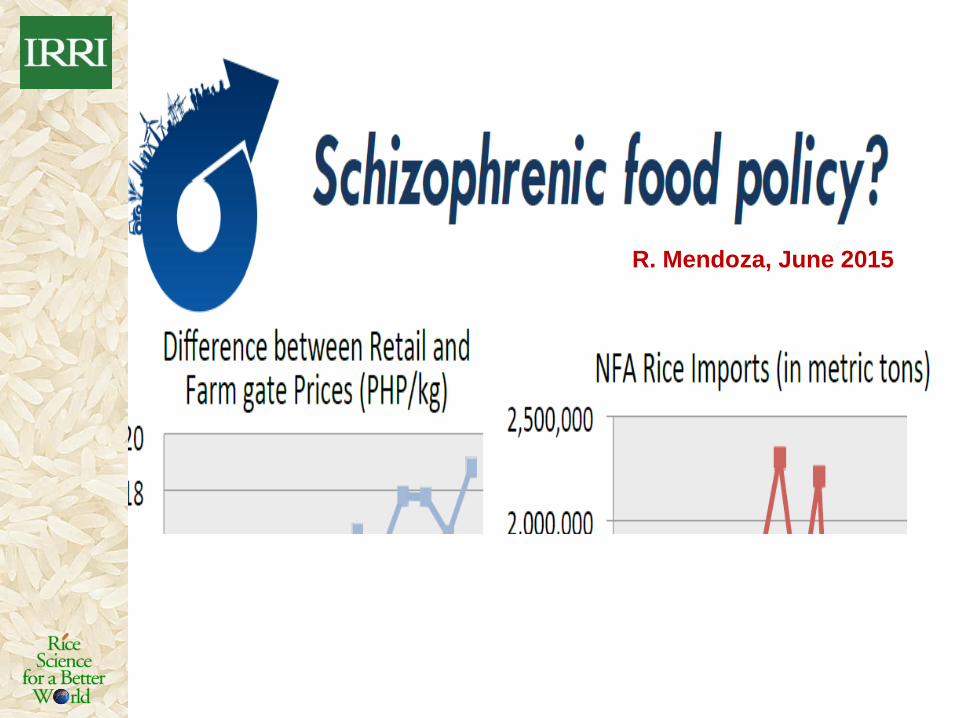

R. Mendoza, June 2015

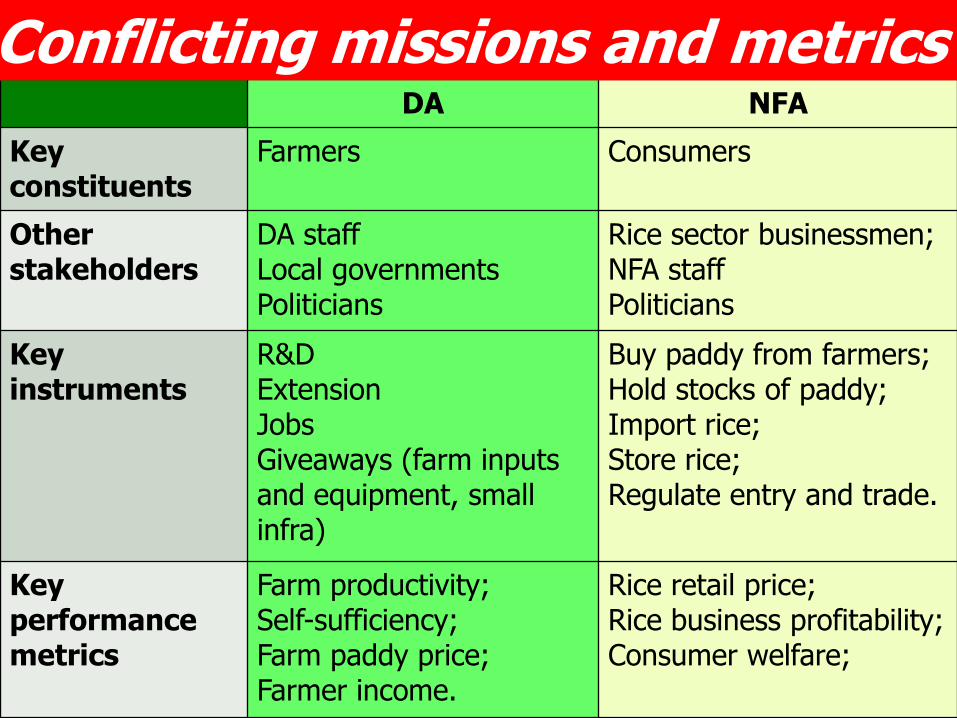

DA NFA

Key constituents

Farmers Consumers

Other stakeholders

DA staff Local governments Politicians

Rice sector businessmen; NFA staff Politicians

Key instruments

R&D Extension Jobs Giveaways (farm inputs and equipment, small infra)

Buy paddy from farmers; Hold stocks of paddy; Import rice; Store rice; Regulate entry and trade.

Key performance metrics

Farm productivity; Self-sufficiency; Farm paddy price; Farmer income.

Rice retail price; Rice business profitability; Consumer welfare;

Conflicting missions and metrics