Embed Size (px)

DESCRIPTION

Thesis discussing the impact of risk on household behaviour, discussing various coping strategies including marriage.

Citation preview

Risk and Insurance in Rural Zimbabwe

Hans Hoogeveen

Cover design: Crasborn Graphic Designers bno, Valkenburg a.d. Geul Copyright: © 2001 by J.G.M. Hoogeveen ISBN 90.517.0819.x This book is no. 247 of the Tinbergen Institute Research Series, established through cooperation between Thela Thesis and the Tinbergen Institute. A list of books which already appeared in the series can be found in the back.

VRIJE UNIVERSITEIT

Risk and Insurance in Rural Zimbabwe

ACADEMISCH PROEFSCHRIFT

ter verkrijging van de graad van doctor aan de Vrije Universiteit te Amsterdam, op gezag van de rector magnificus

prof.dr. T. Sminia, in het openbaar te verdedigen

ten overstaan van de promotiecommissie van de faculteit der Economische Wetenschappen en Bedrijfskunde

op donderdag 26 april 2001 om 13.45 uur in het hoofdgebouw van de universiteit,

De Boelelaan 1105

door

Johannes Gerardus Maria Hoogeveen

geboren te Arnhem

Promotoren: prof.dr. J.W. Gunning

prof.dr. P. F. Lanjouw

Preface

After a bit more than four years, �project thesis� has come to closure. I put behind me a period I enjoyed tremendously. This project would not have been brought to fruition however, if it were not for the support of many. Rightfully first to put in the limelight are Jan-Willem Gunning and Peter Lanjouw, the best kind of supervisors one can wish. Not only was I able to learn much from them, working with Jan-Willem and Peter was characterised by flexibility, speediness, and a contagious enthusiasm for development economics and many issues beyond that narrow focus. Jan-Willem�s supportive trust in me deserves mentioning. After failing my oral exam he did not give up on me, even though I tried hard through a continued messing up of my maths. And Peter�s keen eye for reality helped me to look for the relevance in what I was doing. I�m glad to have discovered that Peter does have one nasty habit. He never allowed me to boost my morale by beating him at a game of squash. Obviously, I haven�t given up yet. I am also indebted to Kees Burger, Chris Elbers, Michiel Keizer and Jenny Lanjouw for their useful comments and suggestions on various occasions. This thesis would not have been written for Bill Kinsey, who provided the data for it. His efforts to go out in the field year after year to compile a longitudinal data set are worth praising. Especially in the field of economics where primary data collection is grossly undervalued the importance of his efforts cannot be stressed sufficiently. I hope many others will be allowed the opportunity to benefit from the fruits of his work. My ultimate gratitude is for the farmers in Mpfurudzi, Sengezi and Mutanda who received us with heart-warming hospitality and who willingly spend their valuable time with the survey teams. Most of my time as Ph.D. student I spent at the Tinbergen Institute and at the Department of Development Economics. I feel indebted to many individuals in both

places: Bas, Luc, Udo, Elfie, Marian, Henri, Trudy, Rob, Bert, Arno, Henk and Marleen Dekker, who became such a good friend. Yet my time as Ph.D. student would not have been so nice, if it were not for those that helped to change the mindset every now and then. Out of many, Pieter occupies a special place. Our frequent lunches in the mensa do not capture what we shared. Kickboxing and a cold beer afterward on Roebijn�s balcony in Washington does so much better. Squash with Joudi, Paul and Xander broke the dread of yet another revision just like a bit of jogging with Bert and Rutger and not to forget tennis (and lots of beer) with Dennis. Life was very sweet while doing fieldwork in Zimbabwe where I enjoyed the collaboration with some remarkable individuals. Belinda from the nose brigade, Michael who joined me in climbing a spirit inhabited mountain, Trudy, who taught me how to prepare a British cup of tea and Pedzisayi with whom I spent some cosy nights outside, sharing a mosquito net and listening to the crickets. Though we knew each other long before I embarked on �project thesis� Takawira Mumvuma cannot go without mentioning as such a great friendship has grown between us over the years. Other people, not involved in any research activities and often not even interested in it, I like to thank as well. For the time well spent, over dinner, in a cafe, having discussions or while skating or playing volleyball. Worth mentioning most in this respect are the �ecoboys�, and the other Pandje members. I still believe in our project and would like to paraphrase Karen Blixen to express my hopes: We�ll have a farm in Europe. Very much I feel indebted to my parents. You instilled in me that the least you can do is to try and put in a bit of effort, an attitude that helped me proceed on various occasions. There is one thing I can safely admit to you now: studying economics was not such a bad choice after all. Eventually, and most importantly, I want to mention Ariënne, my love. For providing moral support and accepting, especially during the past year, my monomaniacal focus on economics. On many occasions you helped me regain my balance and were you able to put life back into perspective. But now, �project thesis� is over. It�s been enough. The time to move on has come. Hans Amsterdam, 8 February 2001

Contents

1. Introduction 1 1.1 Risk in Rural Zimbabwe 1 1.2 Thesis Outline 5

2. Risk, Insurance and the Poor: A Review of the Literature 9 2.1 Introduction 9 2.2 Assuring Smooth Consumption 10 2.3 Self-Insurance Options 18 2.4 Insurance and Credit Transactions 25 2.5 Conclusion 30

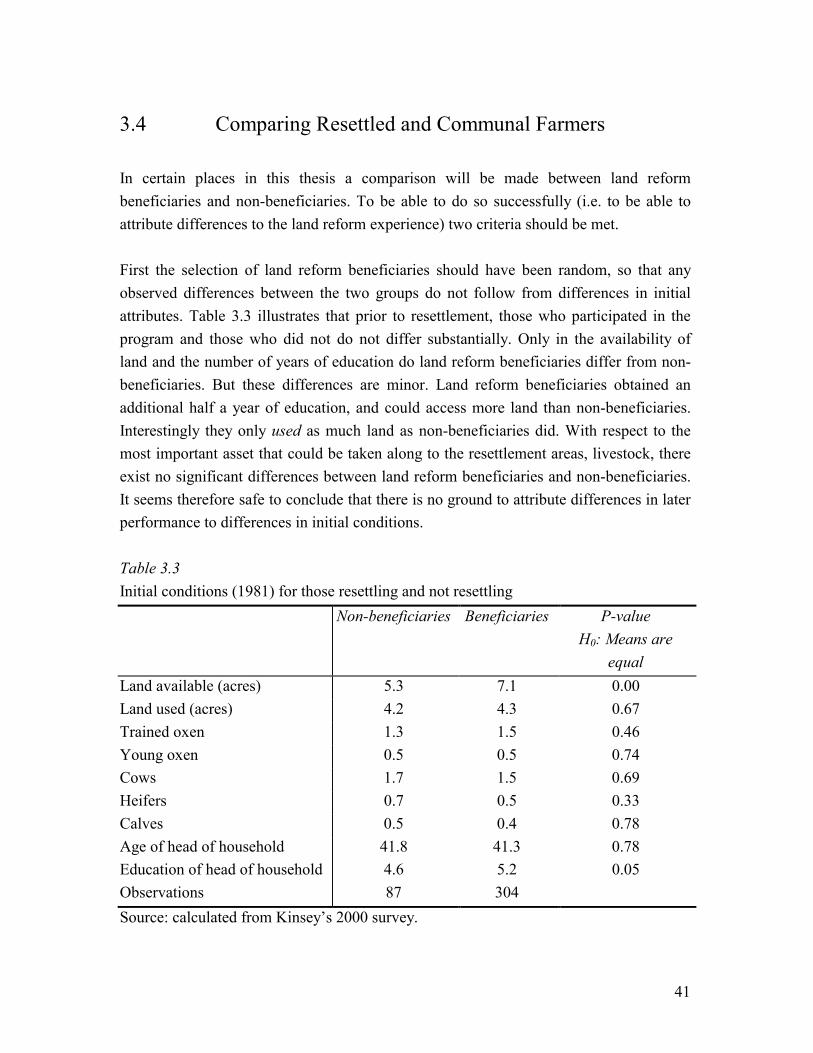

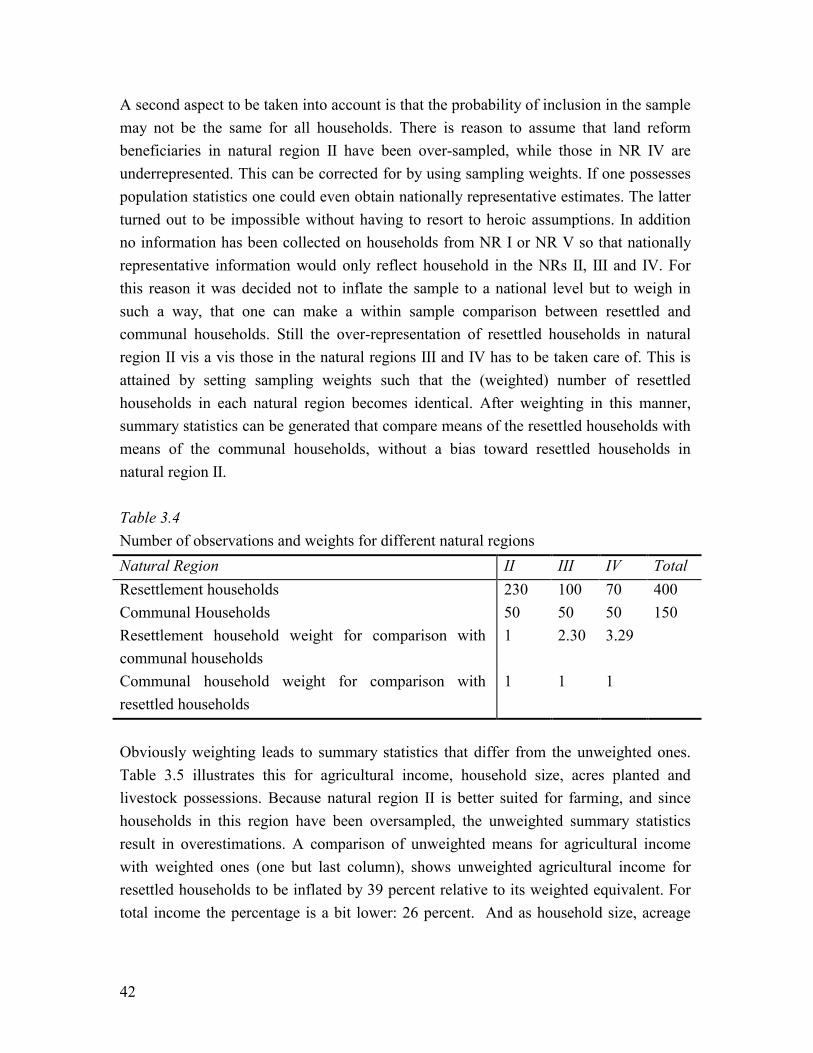

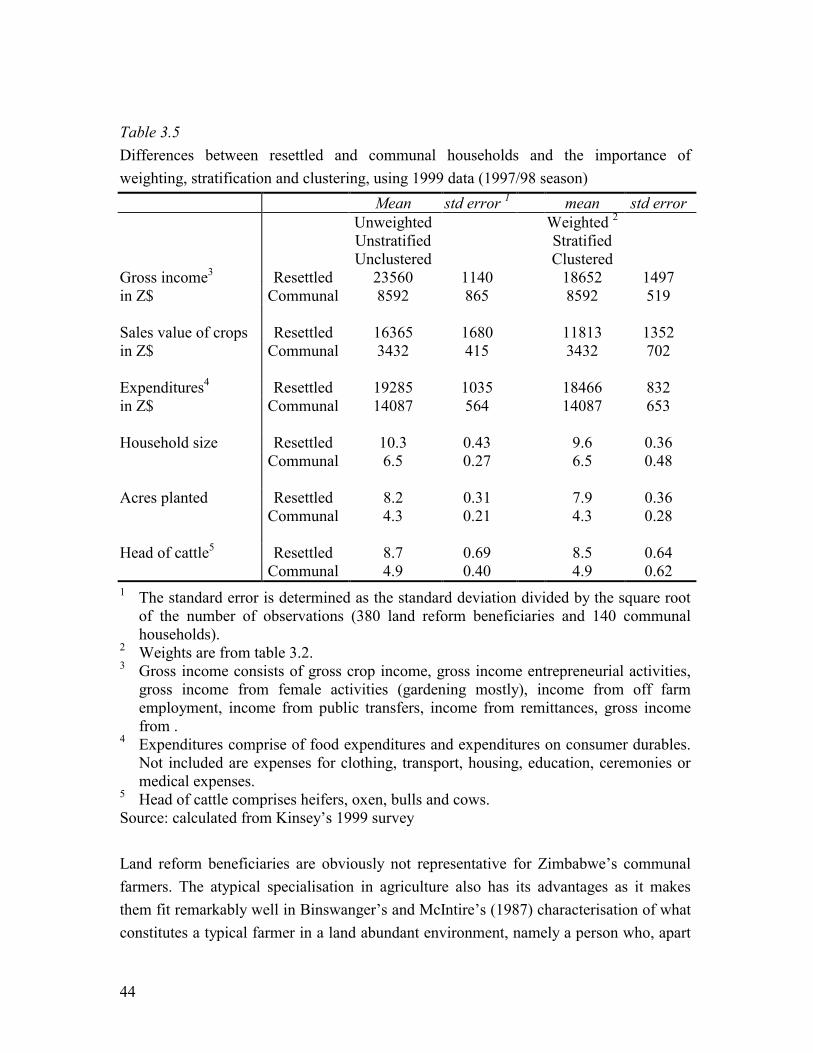

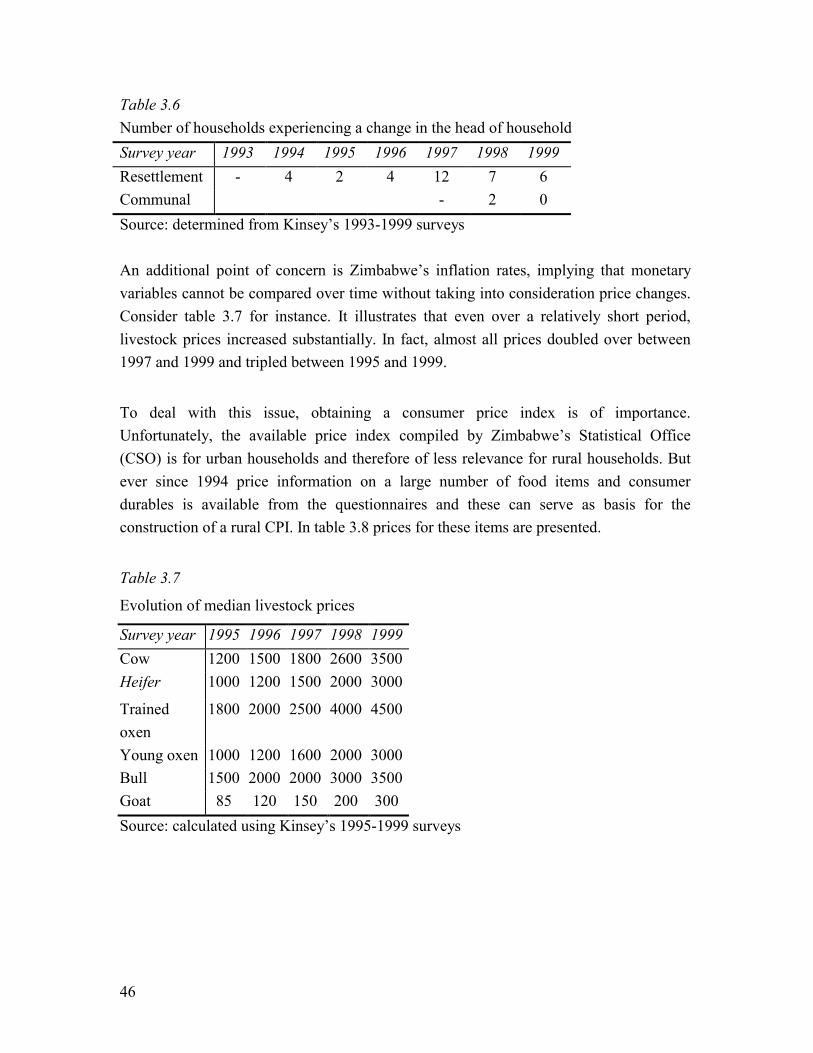

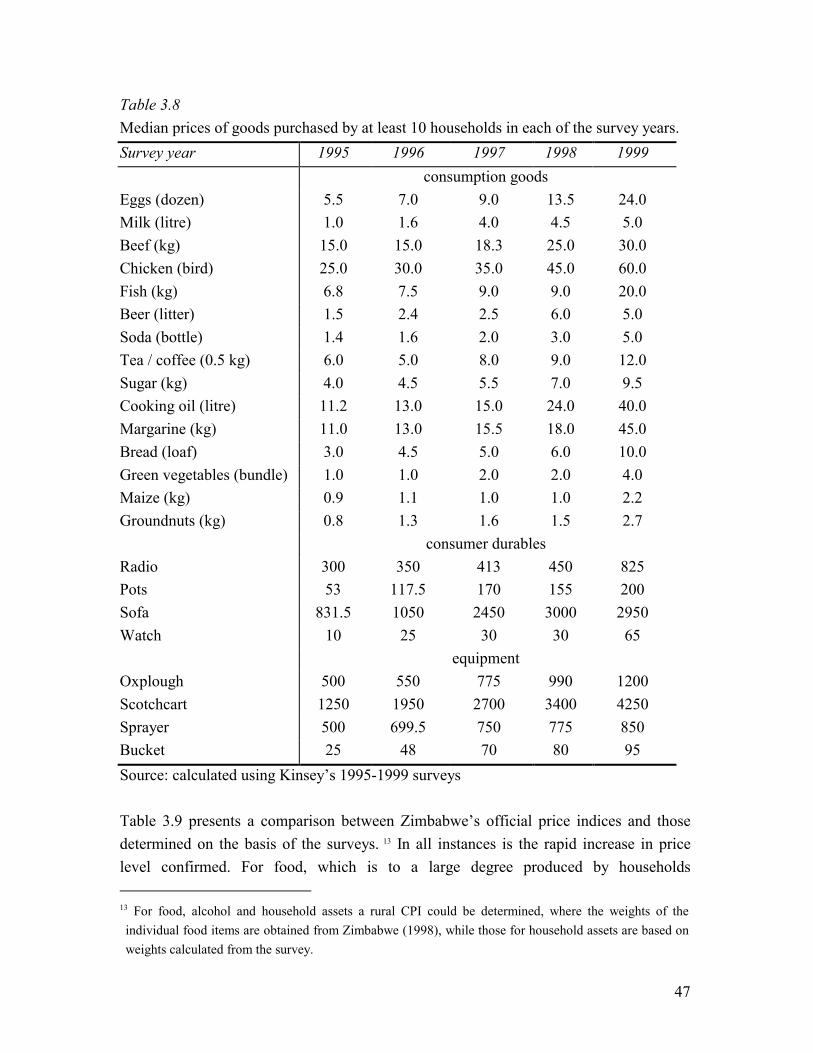

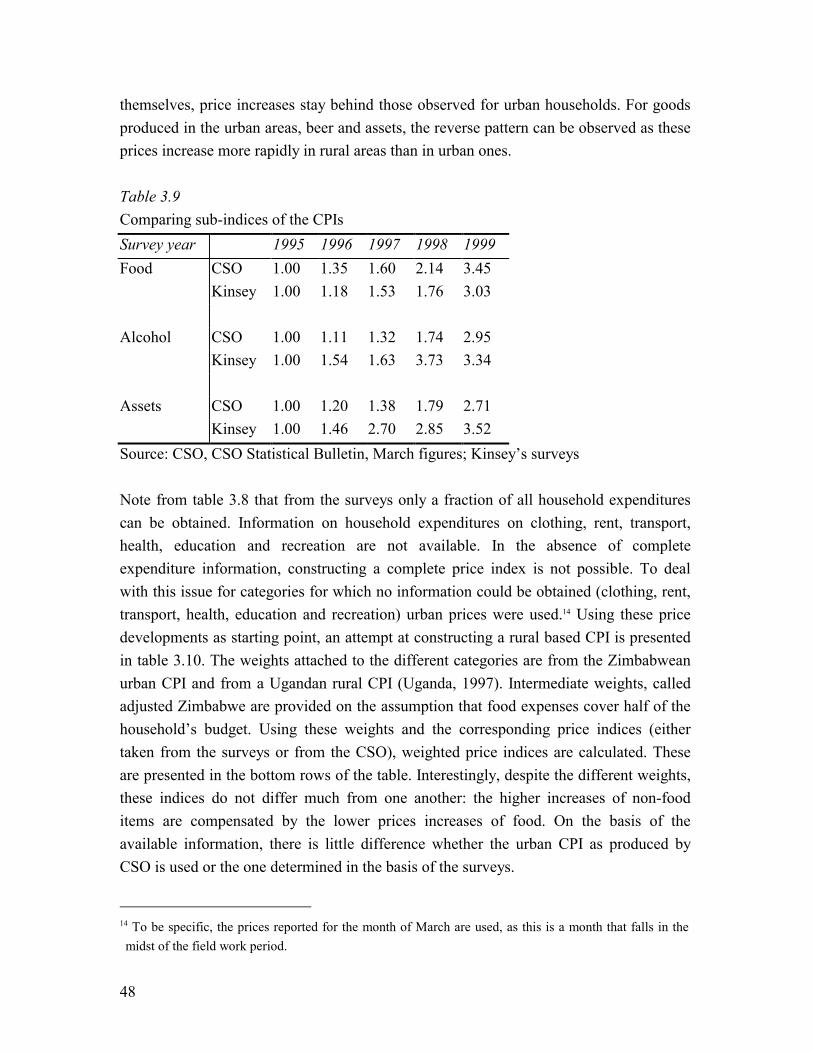

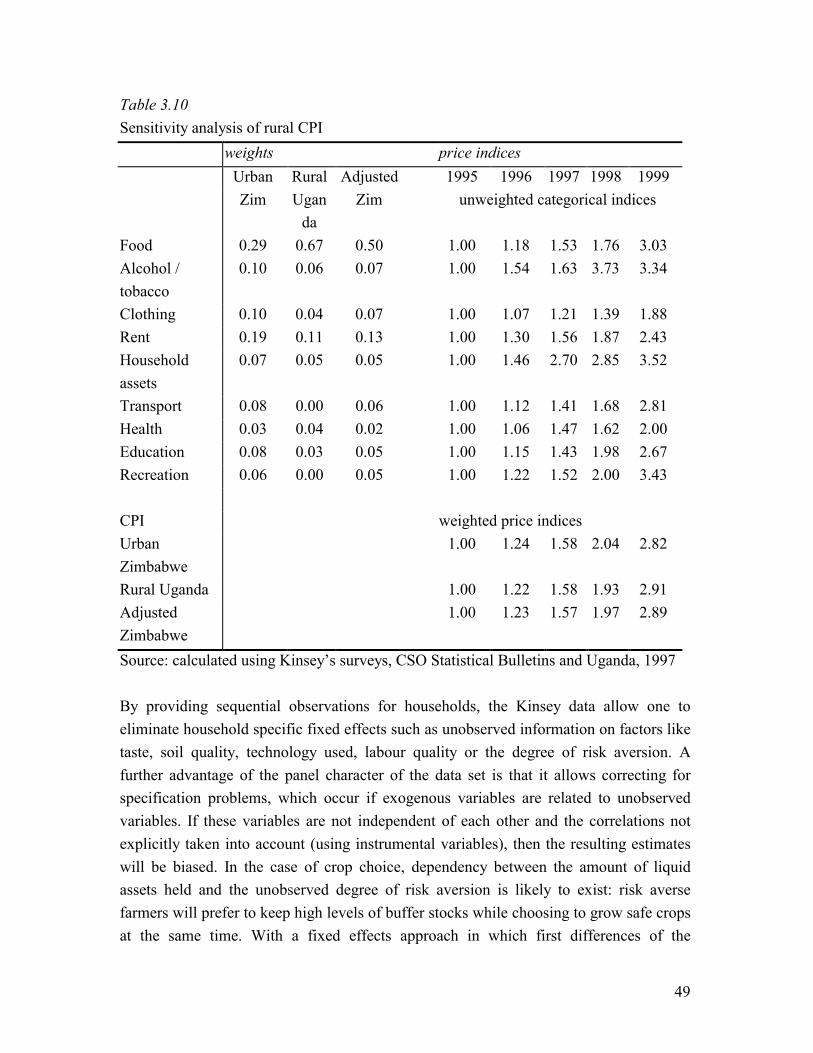

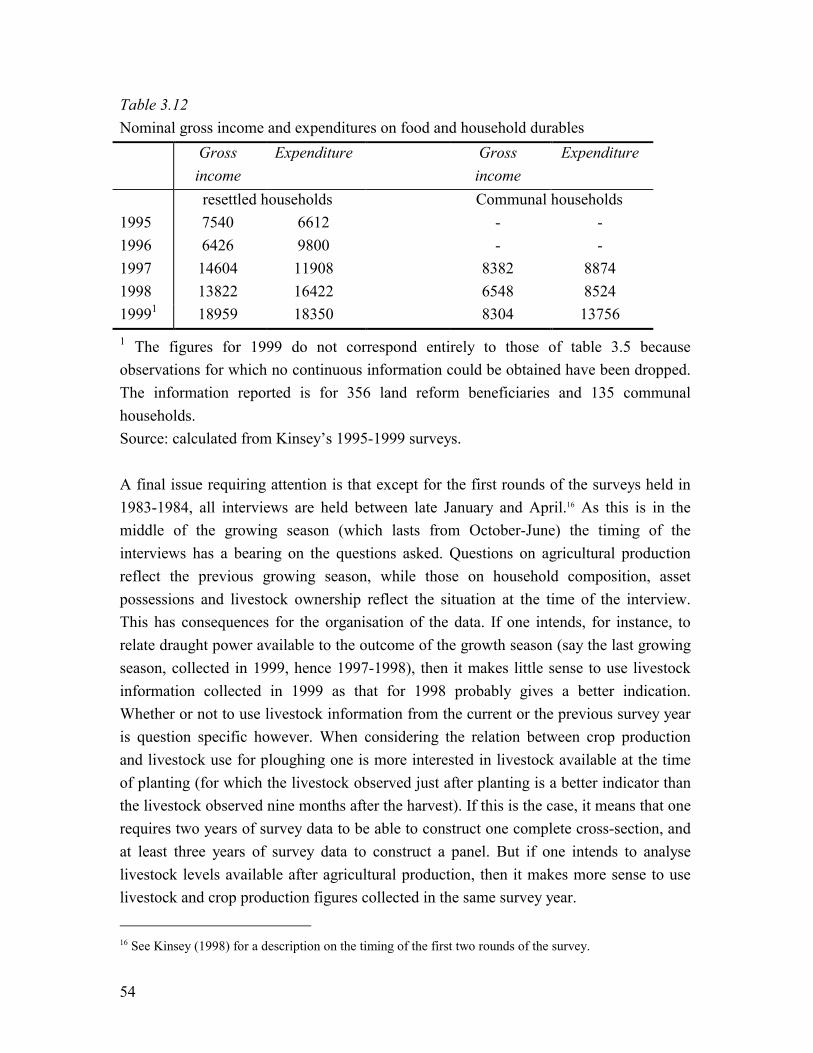

3. The Data Set 33 3.1 Introduction 33 3.2 Land Reform in the Early 1980s 34 3.3 Sampling Issues 38 3.4 Comparing Resettled and Communal Farmers 41 3.5 Making Comparisons over Time 45 3.6 Data Reliability 51 3.7 Conclusion 55

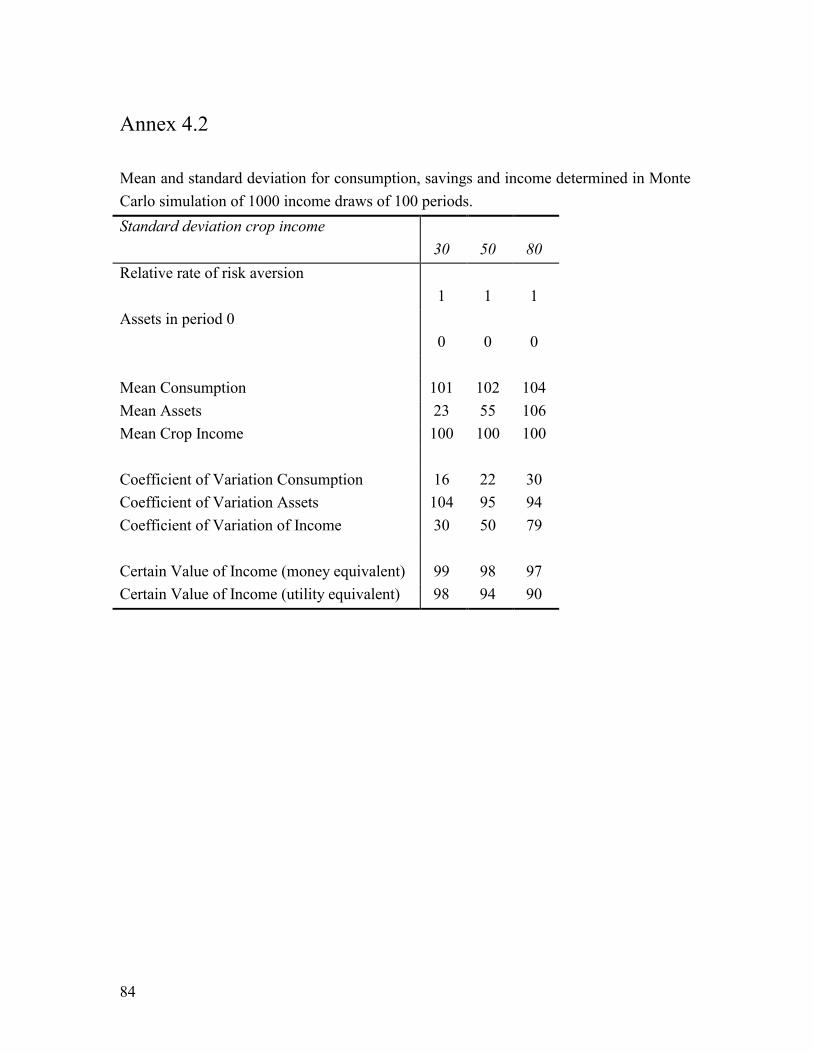

4. The Puzzle of the Absent Formal Insurance Services 57 4.1 Introduction 57 4.2 Income Variability, Buffer Stocks and Consumption Fluctuations 59 4.3 Deriving a Consumption Rule 66 4.4 Determining Optimal Consumption Variability 72 4.5 Benefits from Introducing Formal Financial Institutions 78 4.6 Discussion 81 Annex 4.1 83 Annex 4.2 84

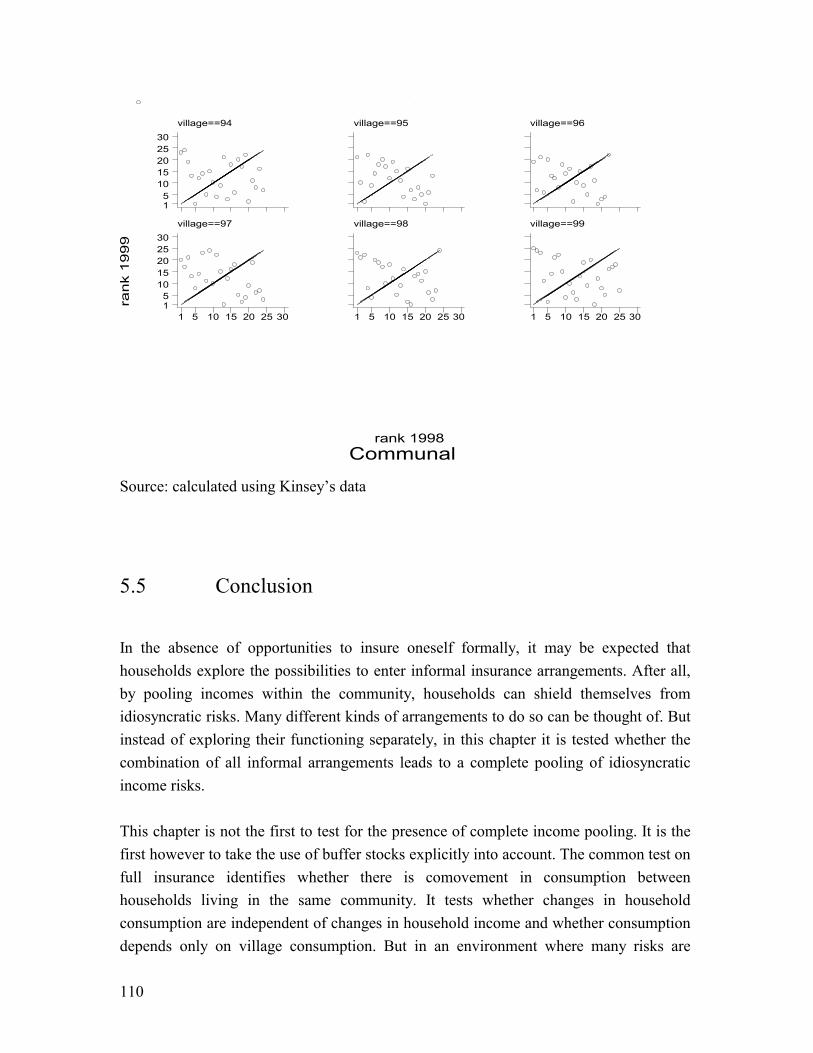

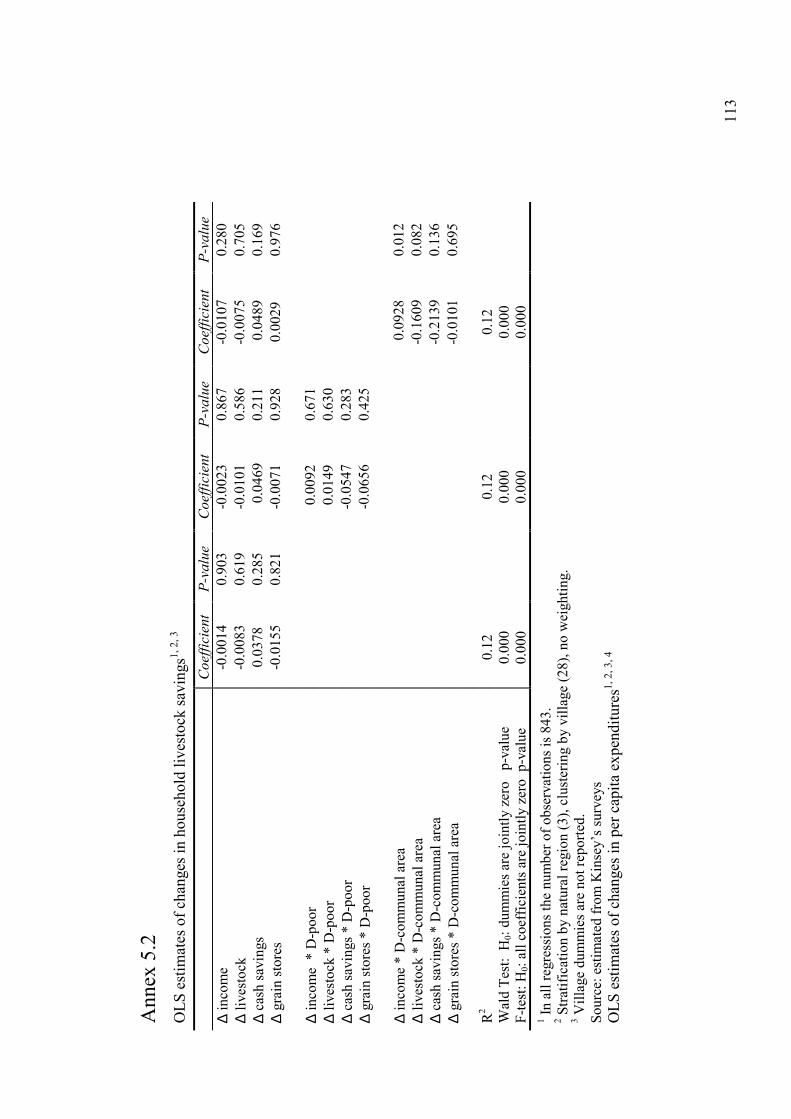

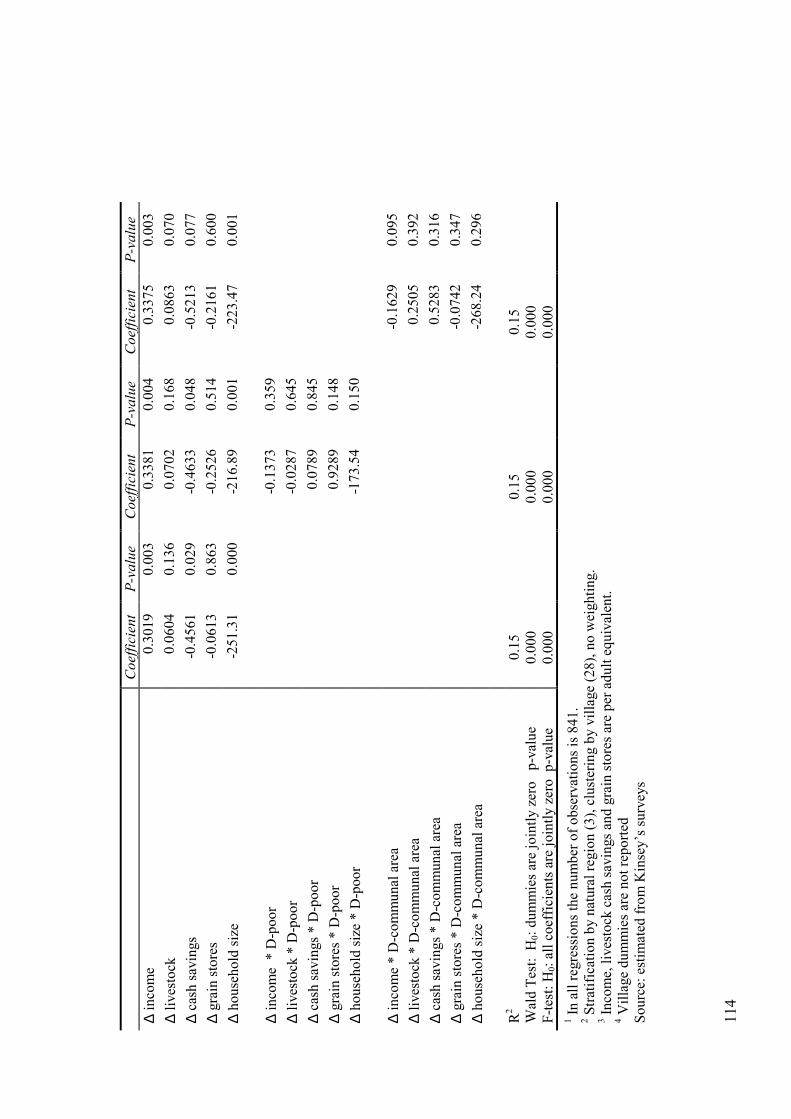

5. Evidence on Informal Insurance in the Community 85 5.1 Introduction 85 5.2 Income Pooling in the Presence of Buffer Stocks 89 5.3 Identifying Community Level Effects 97 5.4 Estimation Results 102 5.5 Conclusion 110 Annex 5.1 112 Annex 5.2 113

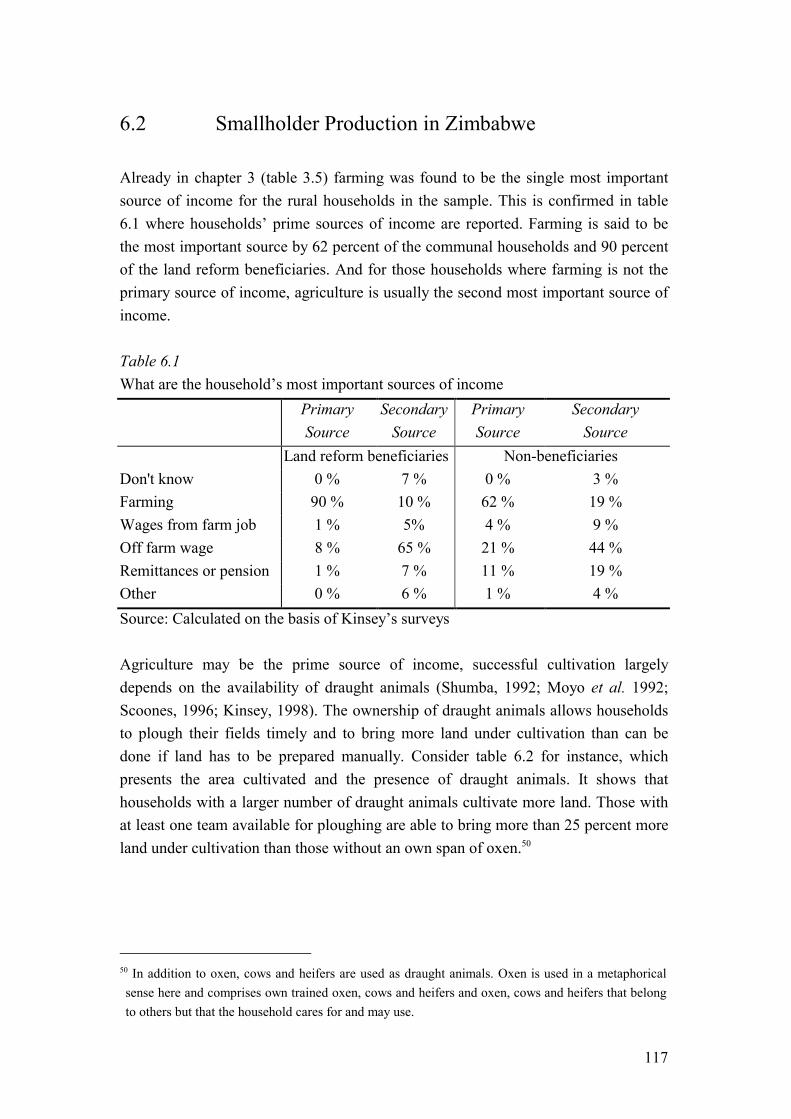

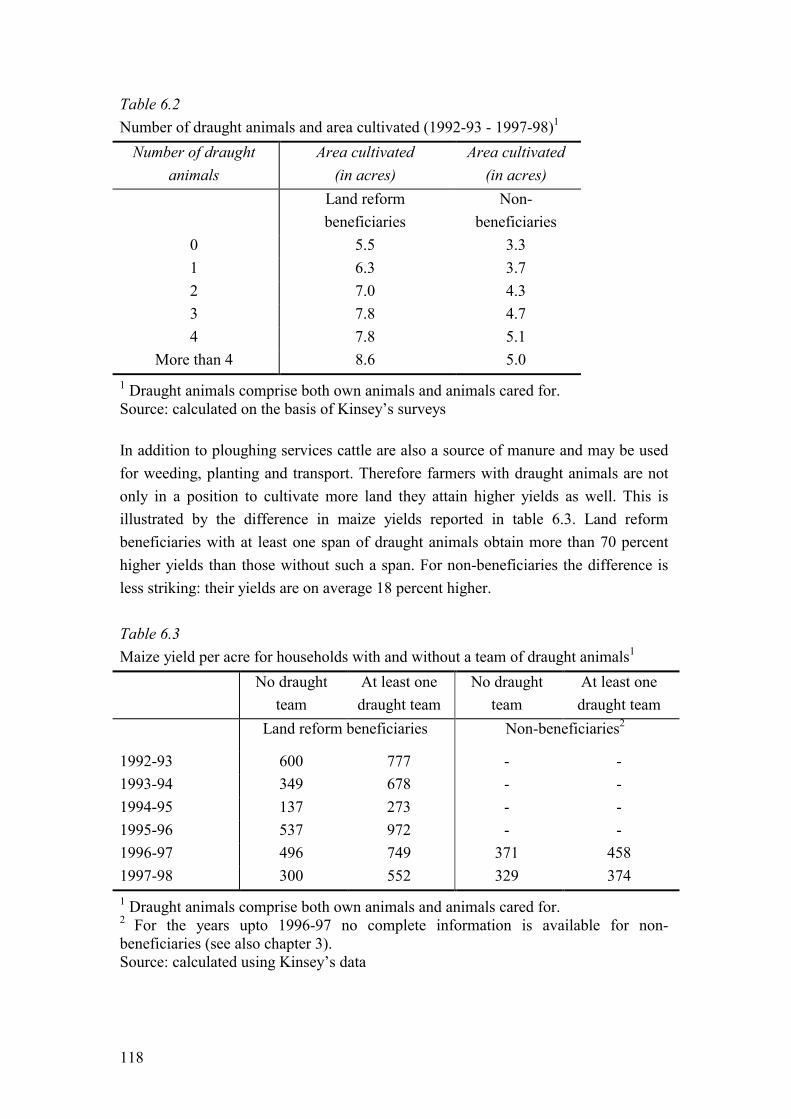

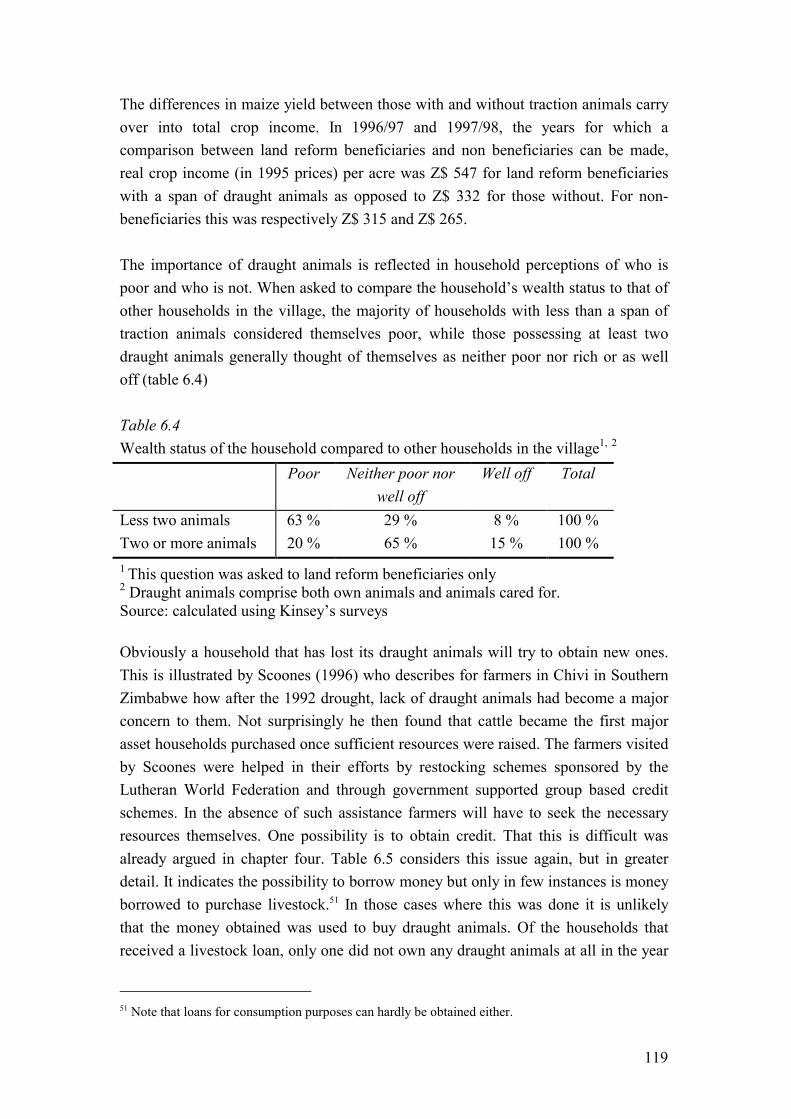

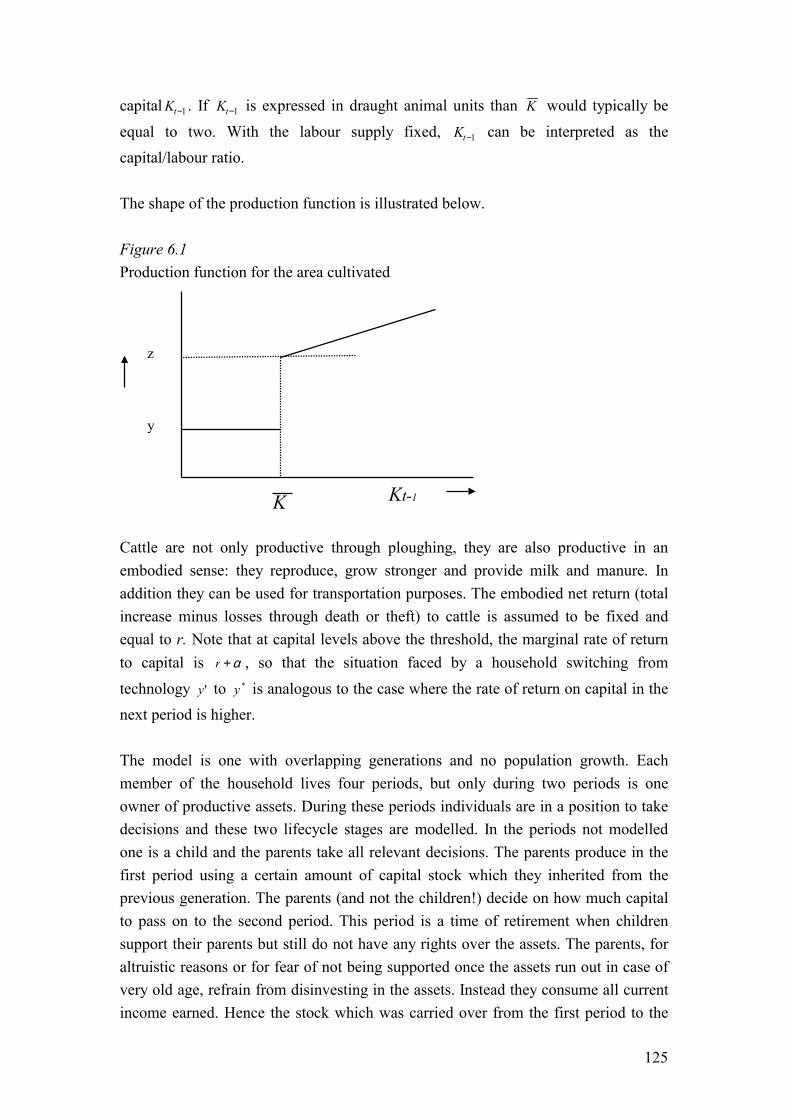

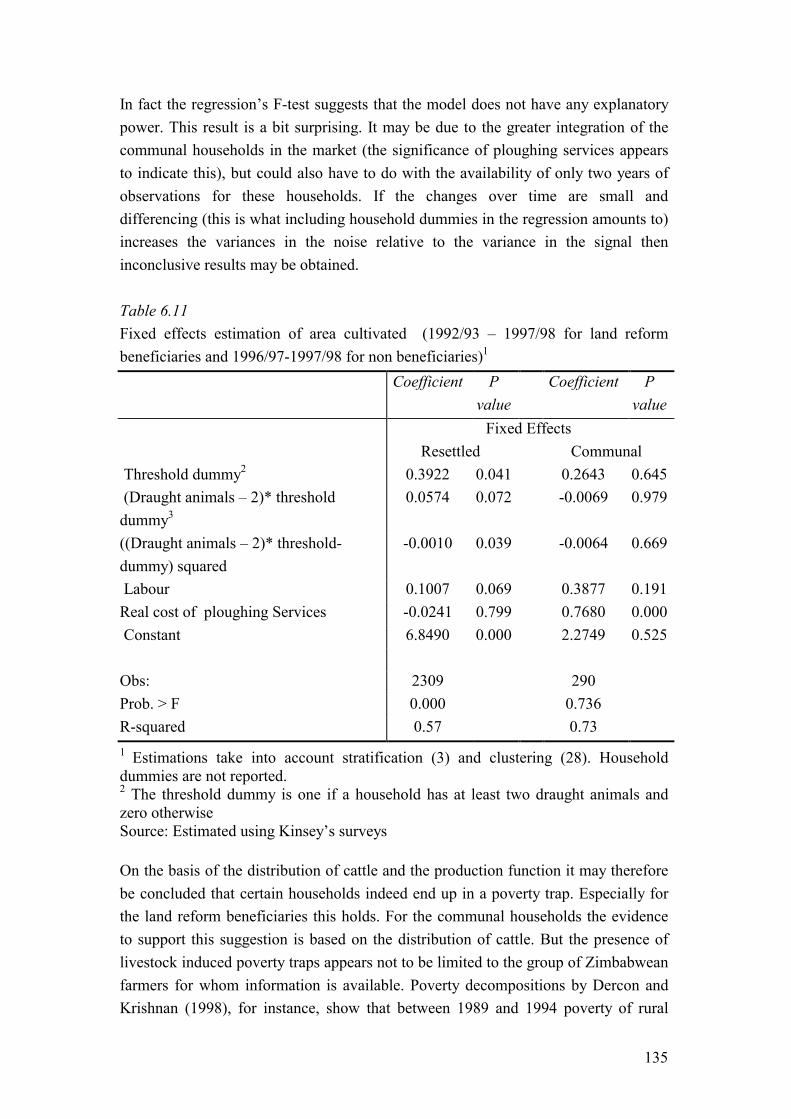

6. Cattle as Source of Risk 115 6.1 Introduction 115 6.2 Smallholder Production in Zimbabwe 117 6.3 Deriving a Livestock Induced Poverty Trap 123 6.4 The Distribution of Draught Animals 131 6.5 The Production Technology 133 6.6 Conclusion 136

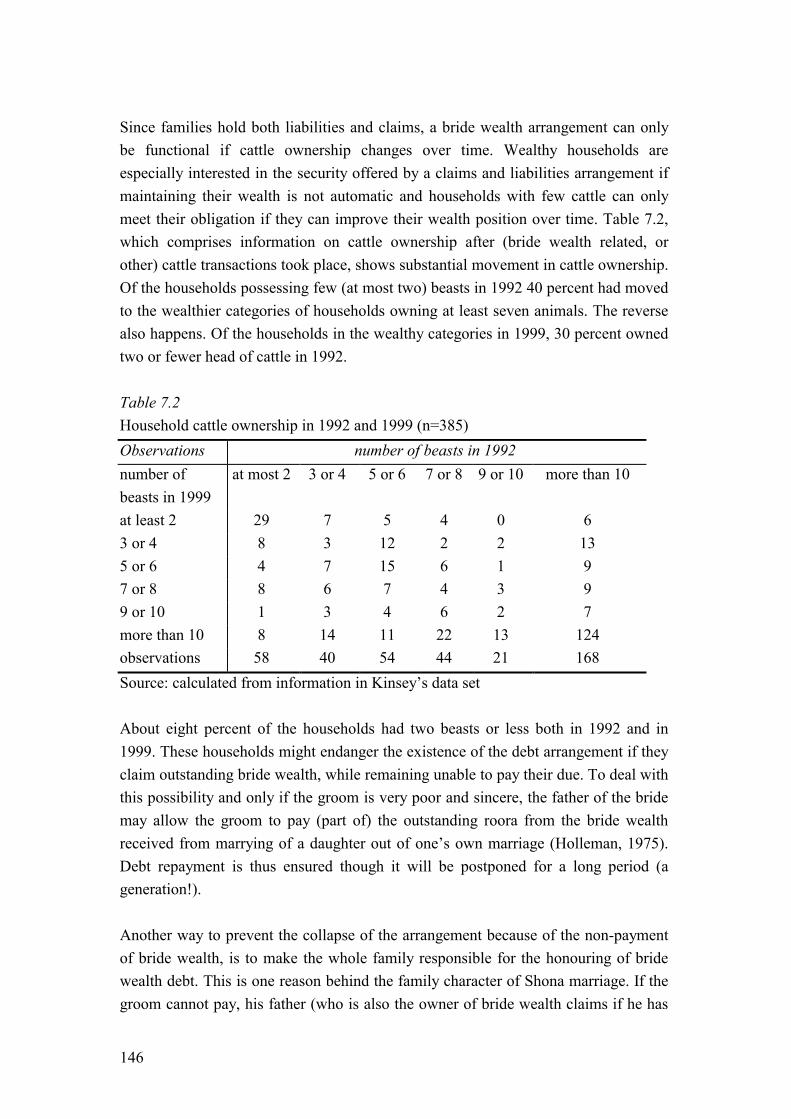

7. Bride Wealth as Informal Insurance 137 7.1 Introduction 137 7.2 Conditional Claims and Liabilities 139 7.3 Shona Marriage as Informal Insurance Mechanism 141 7.4 Implications of Insurance Interpretation of Bride Wealth 151 7.5 Conclusion 159

8. Enhancing Household Security 161 8.1 Introduction 161 8.2 Risk and Insurance in Rural Zimbabwe: Summary 162 8.3 Improving Household Security 169

9. Summary in Dutch - Samenvatting 177 9.1 Inleiding 177 9.2 Uit het Leven van een Zimbabwaanse Boer 178 9.3 Risico en Verzekeren op het Platteland van Zimbabwe: Samenvatting 181

References 189

Introduction

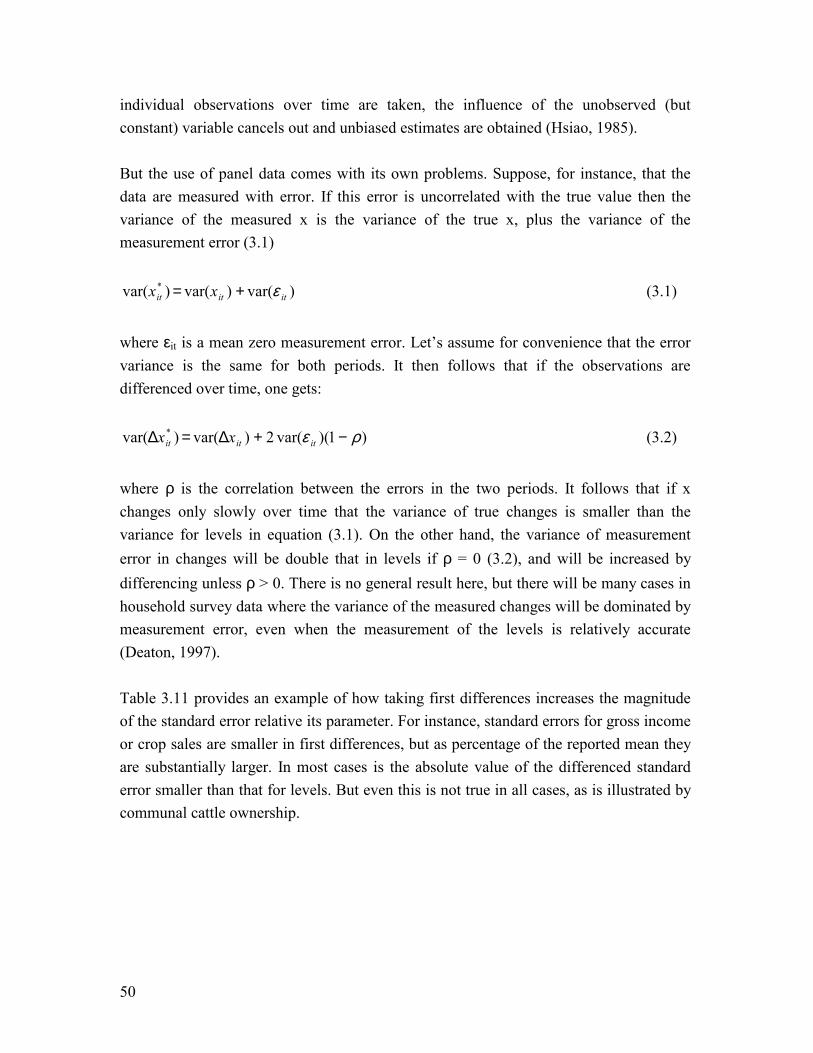

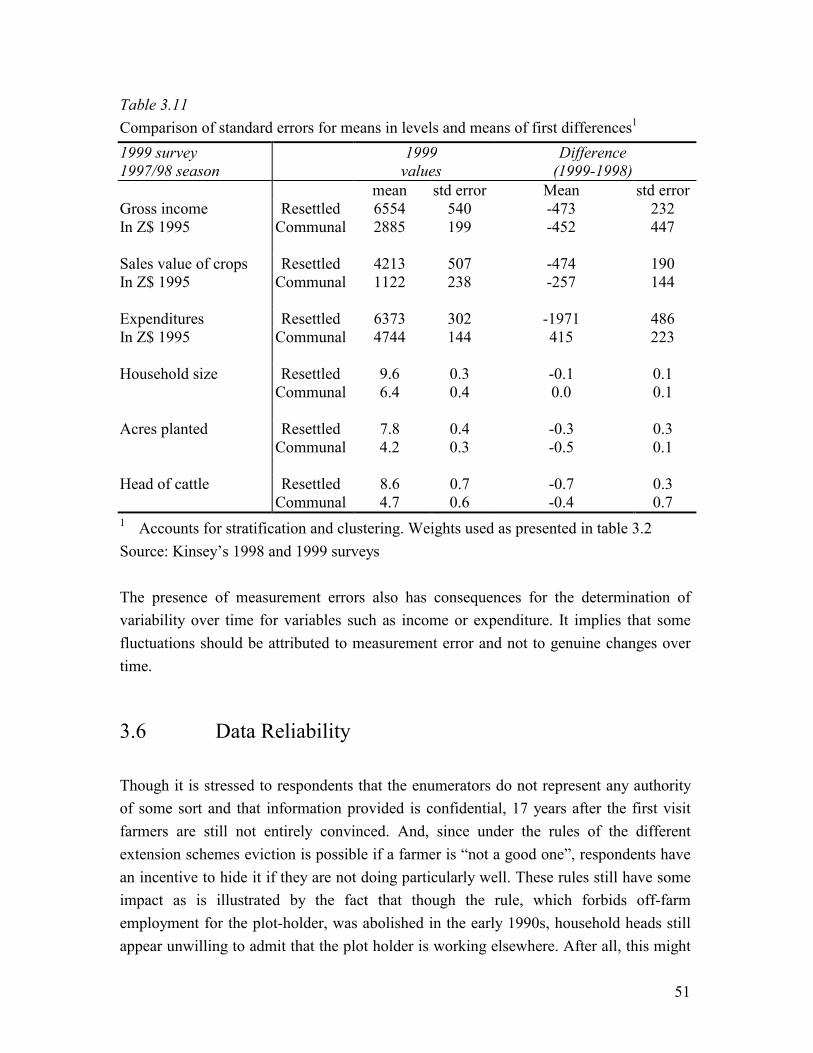

1.1 Risk in Rural Zimbabwe A distinctive feature of life in a developing country is the importance of risk. This is immediately apparent for those who for the generation of their income depend upon dryland farming. Differences in timing, intensity and quantity of rainfall and other weather phenomena like storms, evaporation and cloud cover, the incidence of disease, pests, fire or attacks by wild animals cause yields to fluctuate unpredictably. Variations in the price of inputs and marketed output cause farm profits to vary, and illness at the moment of planting may, through its effect on labour, seriously affect the household�s income for that year. Risk not only affects income. Medical bills, the introduction of cost recovery schemes leading to the demand of school fees or payments and contributions to funerals go at the expense of outlays for food and other necessities. In an economy with a comprehensive social security system and various options to insure one�s health, wealth and life, risk continues to have a great influence on people�s lives. Even when the material consequences of illness, unemployment or inability to work are insured, risk has enormous consequences for well being in a broader sense. This stretches well beyond the individual and their families. The introduction of state

2

pensions in the Netherlands for instance, effectively solved the risk of old age. But this solution also appears to have changed family composition and the norms and values with which the elderly are regarded. If the (non)-insurance of old age risk has such a profound influence on the way people live in an economy with mature financial markets, then one might well appreciate how serious the consequences of risk can be for a Zimbabwean farmer who does not have access to any formal insurance services. To explore this in somewhat greater detail, consider the following illustration of a stylised farm household in Zimbabwe�s rural areas. A young couple in rural Zimbabwe starts to till the soil using two head of cattle, which the husband managed to obtain in the years previous to their marriage. The household grows maize, which is mostly used for own consumption, and cotton. Though the couple lives in an isolated rural area, it is not entirely closed off from the rest of the economy. Once a year it sells its maize surplus and its cotton to the relevant marketing boards or to traders. In return the household buys fertiliser, seed and other goods it requires. What is left of the money from crop sales is set aside to deal with unexpected expenses such as medical bills, to pay for transport, for funeral contributions and to pay school fees. Because banks are absent in the area in which they live, savings are mostly kept in the form of food stores, as cash and as livestock. Cattle especially are a preferred store of wealth, because they breed, because their labour power is a valuable input in agricultural production and because the animals can be sold relatively quickly when money is needed. Agriculture is rain-fed and yields not only vary from one year to the next, but between different households in the village as well. The couple does not want variability in income to affect its consumption. To attain this objective it relies on its savings and on its neighbours. Those with good harvests provide the household with gifts in years it has been unlucky. In years in which the couple obtained a good harvest the favours are returned. In doing so the spouses participate in a village level reciprocal insurance arrangement. Through hard work, moderate consumption and breeding the couple manages to increase its herd from two to five animals, to send its children to school and to deal with adverse circumstances such as the occasional illness or unsatisfactory rainfall. So far, the husband paid only part of his bride wealth dues. As the family is doing relatively well now, his father in law demands repayment of part of the outstanding bride wealth

3

obligation which he intends to use this as instalment for the bride wealth of his own son who is about to get married. To meet this request, the husband repays two animals. In the following year a cow dies of old age, a calf is born and sold again to foot medical bills incurred for their daughter who had fallen seriously ill. Now the couple is left with one trained oxen and one cow, just sufficient to pull a plough. To avoid that the hard work at the yoke affects the cow�s ability to breed the couple decides to spare her and to only use their ox for ploughing. It follows that they need to collaborate with other villagers, mostly those in a situation similar to theirs, and to pool their animals to form a team of two animals suited for ploughing. This strategy is costly because it implies that less land can be brought under cultivation than would have been the case otherwise and that not all land can be planted timely. Income from cultivation is therefore expected to drop. The choice pays off however and the cow falls pregnant. Then, through a bout of bad luck, the animal gets stolen before she has giving birth. After harvesting and because less land was brought under cultivation than normally would have been the case, the couple does not have the resources to purchase an additional beast, unless it takes its children out of school. Instead they decide to continue to prepare land with the one ox they have. The couple remains actively involved in gift exchanges within the village so as to be considered a reliable neighbour and in the expectation that this helps them obtain draught power at planting times. Additionally, the son asks his father for assistance. After all, the latter has outstanding bride wealth claims on his sons-in-law that he can still reclaim. Then a drought strikes, reducing aggregate village income to close to zero. In their struggle to deal with the adverse circumstances better off villagers sell livestock to buy food. The couple could do this as well, but then it would lose its last draught animal. It tries to avoid this by depending on the solidarity of better-endowed villagers. But while the drought lasts and resources get very scarce, the better off prefer to continue their reciprocal relations exclusively amongst themselves. Selling livestock to safeguard their poor neighbour at the expense of future income generating possibilities embedded in their cattle, is considered too costly. Under these circumstances the couple has no choice but to sell its ox (at a very low price), to take its children from school and to wait for public assistance.

4

After the drought the better off households, and especially those who are still able to plough, recover relatively quickly. This does not hold for the couple. They are without draught animals and have no choice but to prepare their land manually. The income they earn from farming is low and to supplement it their children herd cattle for wealthy villagers. Obviously the couple tries to save in order to buy the required two head of cattle. But the amount needed is so large that it is next to impossible to save a sufficiently large fraction from the reduced income to do so. The couple also tries to borrow cattle from others at planting time, but without an own beast to share they are served last. By the time animals are available for use, the optimal time for planting has long gone while the beasts obtained are tired from their previous efforts. All this contributes to the couple being stuck in poverty for a prolonged period. Only when the husband�s father manages to obtain a cow from one of his sons in law (after he recovered from the drought) which he passes on to his son, does there appear scope for improvement. By that time, the children have been out of school for several years. The example underscores the multi-facetedness of risk (drought, illness, theft, livestock survival, and social exclusion) and the important bearing it has on the lives of rural households in Zimbabwe. It can also serve as illustration as to how the presence of a formal insurance mechanism might have allowed avoiding such a bad episode. The prolonged period of poverty could have been avoided if the couple could have effectuated an insurance claim after the drought, or if such a claim could have been made after the cow was stolen. In that case the household would have been less destitute when the drought arrived and therefore less likely to become excluded from the solidarity arrangement so that the ox would not have to be sold. The example also illuminates the importance of cattle, in production and as buffer stock. Furthermore it illustrates that of the many causes of poverty, chance or risk is one of them, and that risk at the individual level contributes to inequality (in the village in this case). Obviously the latter two aspects are worth avoiding: because poverty is cause for grave concern in itself, and because more and more empirical evidence shows that greater inequality leads to reduced growth and hence to relatively less means for poverty alleviation. In the illustration several informal insurance arrangements exist that try to do so: reciprocal gift exchanges, pooling cattle and assistance within the family. Still these mechanisms were unable to prevent the outcomes during the drought and for the educational attainment of the couple�s children.

5

1.2 Thesis Outline The different aspects highlighted by the example are considered in greater detail in this thesis. In chapter two a review of the literature on risk and insurance by the poor is provided. It is shown that formal insurance in which a large number of households pool their risks is efficient, and also that such an optimal situation cannot exist in practice because of information and enforcement problems. Dealing with these problems is costly as it requires intensive monitoring. This contributes to the absence of insurance arrangements in rural areas. It follows that households have to mitigate income risks themselves (though this goes at the expense of their already meagre income), rely on self-insurance or participate in informal insurance arrangements. Chapter three is an intermediary chapter in which the data set is introduced. The data have been collected in Zimbabwe amongst land reform beneficiaries and non-beneficiaries who live in three different agro-ecological zones. The first year of information used in this thesis was collected in 1992 and covers the agricultural season 1990/91. Ever since the information has been updated annually for the same group of households. The thus created panel data set is unique for Africa because of the length of the period covered and because of the wide range of topics on which questions have been asked. Furthermore it is well suited for a study on risk and insurance. Chapter four presents a puzzle. What is the reason for the absence of formal insurance arrangements in rural areas when income risks are so large that households would be prepared to spend a substantial fraction of their income to deal with these? One explanation is that income risk is not that large, either because households are able to diversify most risks or because they participate in informal insurance arrangements. The empirical evidence presented does not support this suggestion. Another possibility is that reliance on buffer stocks is such an efficient means to deal with income risk that it greatly reduces demand for formal insurance. This option is explored empirically, by considering the variability in consumption, and by using a simulation model. The conclusion that arises is that reliance on buffer stocks does not offer a sufficient explanation either. This leaves the original puzzle unanswered. Therefore a third suggestion is offered: insurance is absent not because of market failures but because of institutional failures. It is absent because of the uncertainty of the potential insurees as to whether an insurance company will meet its future liabilities.

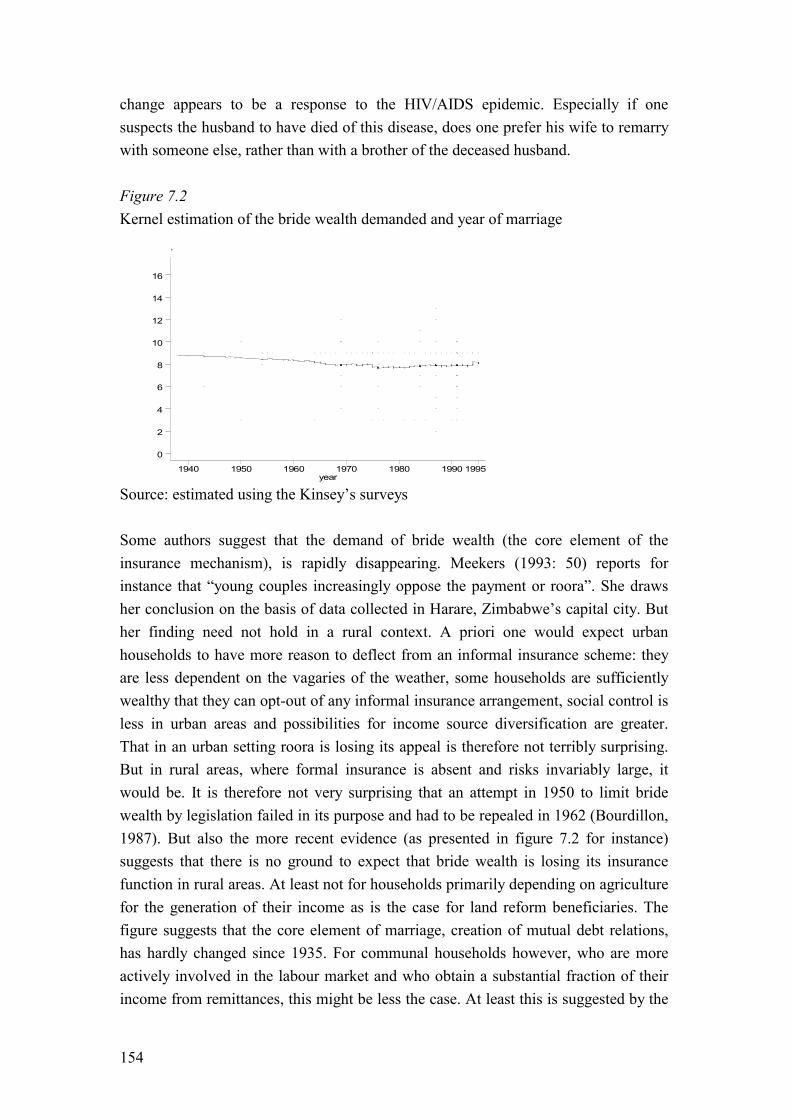

6

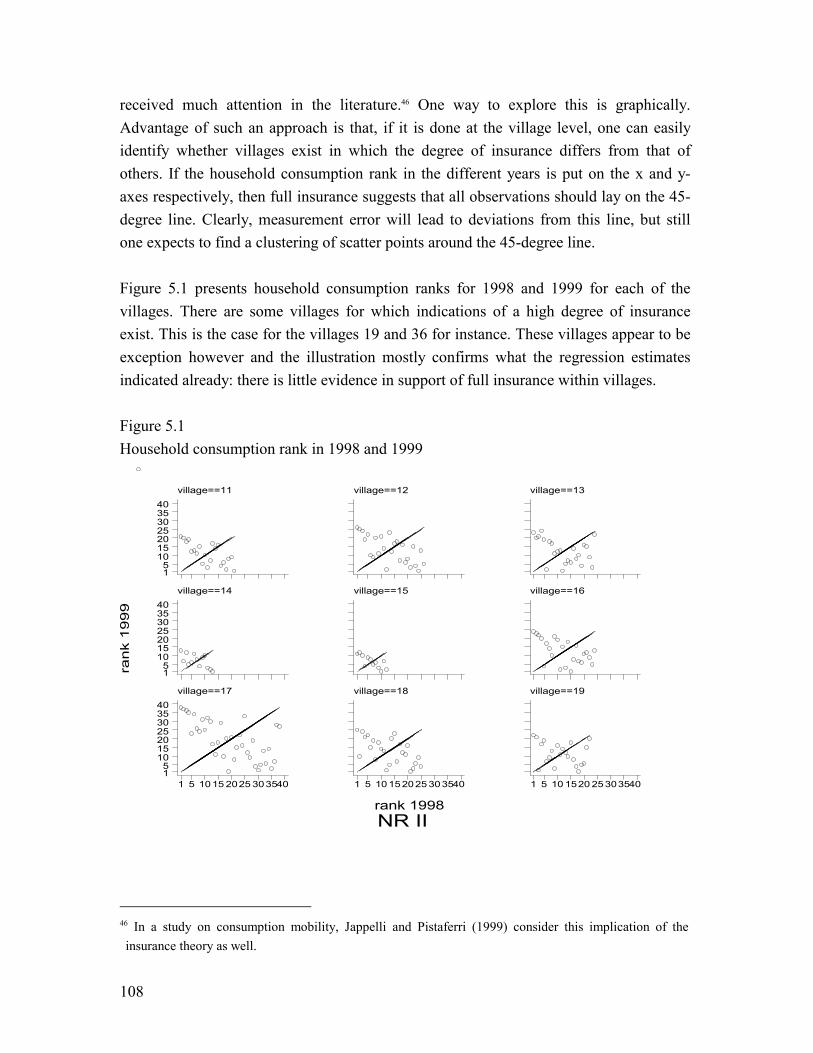

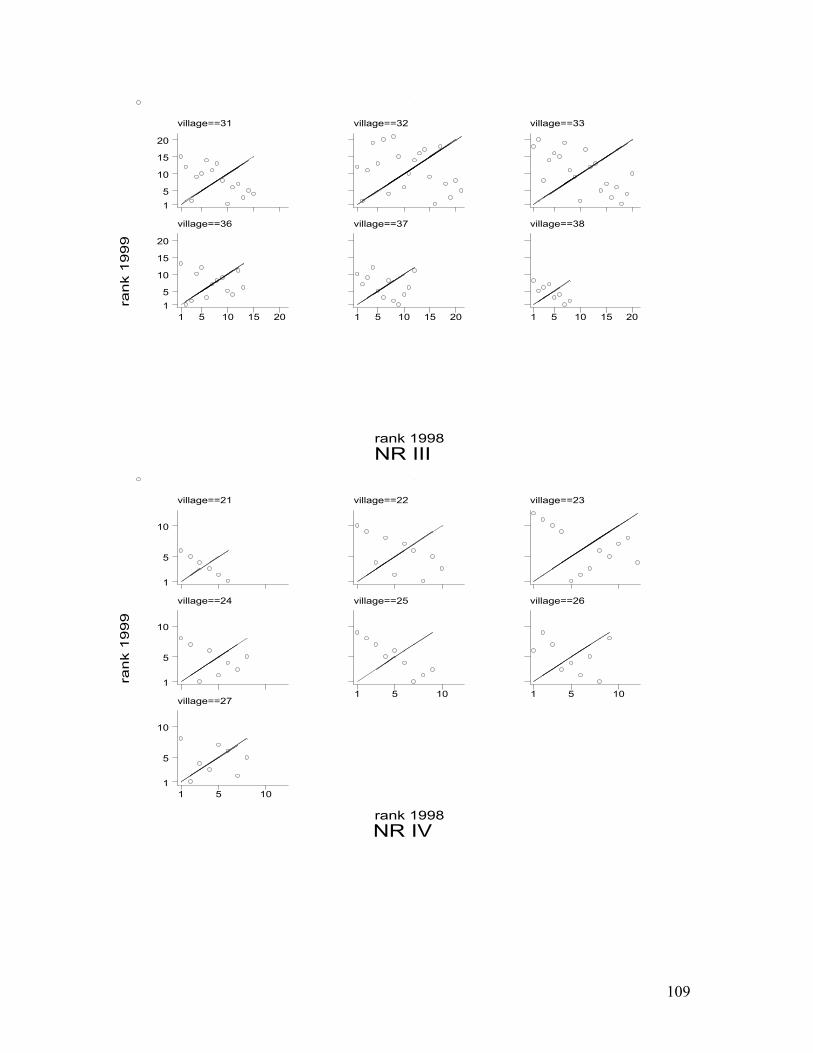

Given the absence of formal insurance and the existence of considerable variation in consumption at the household level, one may wonder whether informal insurance arrangements exist that allow households to deal with income variability. To this end in chapter five it is explored whether informal insurance is partial or complete. The latter would be the case if all household specific variations in income were pooled, implying that household consumption would only be dependent on what is available in the aggregate. The common test for complete insurance is therefore whether household consumption is explained by aggregate consumption alone and independent of household income. It is shown theoretically however, for an environment where buffer stocks are used to smooth consumption, that the appropriate empirical test is whether household consumption is independent of income and the change in savings. This test is then used in the empirical part of this chapter. An additional issue is what is the relevant insurance community. Close knit communities have an advantage in creating an insurance pool in that they are able to reduce monitoring costs. But it generally also means that the pool is confined to small geographic areas. If the main risk is geographically correlated, as is the case in Zimbabwe, then benefits from income pooling may be limited. To discover whether the village defines an insurance community or whether a wider geographic setting should be considered it is explored at which geographic level, survey site or village, evidence for insurance is strongest. The example presented in the previous section also showed that once poor, one might become excluded from the informal insurance arrangement, especially if a covariate shock occurs. Whether the poor are worse insured than the better off is therefore also explored empirically. The main result of chapter five is that informal insurance arrangements exist but that the security offered is partial. Insurance is not found to be confined to villages alone, but to cover greater distances as well. And the poor are shown to be just as well protected as the better off. In the chapters four and five rainfall is identified as a major source of income risk and cattle as an important buffer stock. As such they can be sold at times of adverse circumstances, and assist households in surviving shocks. But cattle are not the main store of savings they are also a major source of draught power. Therefore the great appreciation of cattle in rural Zimbabwe should not come as a surprise. The special position of cattle in rural Zimbabwe is illustrated by the common belief of the Shona, the dominant ethnic group in Zimbabwe amongst whom the data have been collected, that

7

should a man drink water from a container used by animals he would be in danger of incurring sickness and even death. But no such danger exists when sharing a container of water with cattle because �they are like people� (Bourdillon, 1987: 78). Nevertheless, as major source of draught power, cattle are also a source of risk. The chapters six and seven look into this issue. In chapter six the importance of cattle for income generation is explored in greater detail and the question is posed what are the consequences for income generation if a household loses its draught animals. It is argued theoretically that because at least two animals are required to pull a plough (i.e. there is a non-convexity in the production function), a poverty trap potentially exists. This follows from the fact that in an environment with absent credit markets where farmers without draught animals earn little, it may become very difficult to set aside sufficient resources to purchase a new set of draught animals. Evidence in support of a poverty trap is provided. The distribution of wealth is in accordance with the theoretical predictions. Support for the existence of a non-convex production technology is also provided. Cattle, by being a buffer stock are not only a source of security, given the reality of a livestock induced poverty trap they are also a source of risk. In chapter five, evidence for the existence of informal insurance arrangements was already found and in chapter seven it is considered whether there exists an informal insurance arrangement allowing households to avoid a livestock induced poverty trap. It presents an informal insurance arrangement that evolves around the demand of bride wealth. The arrangement is a typical mixture of credit and insurance elements. In this case bride wealth liabilities are paid at times of fortune, while claims are called in when the household is going through a difficult period. The claims are mostly in the form of cattle so that the bride wealth arrangement provides protection against shocks in livestock ownership (and hence in income). But as cattle are also a buffer stock, the arrangement can also be used to smooth consumption. What makes the mechanism unique is that it combines close monitoring (after all those involved in bride wealth arrangements are family members) with a large pool of risk (because many households are connected in a network of claims and liabilities). In chapter eight a summary of main findings is provided. With this as point of departure it is demanded whether new formal financial instruments can be designed that would be appropriate for rural Zimbabwe. Two types of insurance are proposed. One allows to better deal with covariate risks. This is a rainfall-based insurance. It deals with

8

enforcement problems by relying on advance payments and is able to reduce monitoring costs by making use of the fact that most risk faced by these rural households is quantity risk and that there exists a high correlation between income outcomes and rainfall. The other broadens a household�s possibilities to deal with idiosyncratic risks. This is a claims and liabilities arrangement. It makes use of the fact that claims and liabilities can provide security if they are conditional. The arrangement deals with information and enforcement problems by combining personal relations with peer pressure. By building a network of bilateral relations the arrangement is also able to pool risks over many households.

Risk, Insurance and the Poor

A Review of the Literature 2.1 Introduction1 Many people in developing countries are poor, face fluctuating incomes and can not make use of the services of formal financial institutions. This does not imply that they accept their situation passively and allow consumption to fluctuate along with income. On the contrary. Most families actively explore various ways to cope with income fluctuations and are innovative in doing so. This chapter presents a literature review of the different means the poor exploit to insure themselves against income risk. In dealing with income variability the interest is not only in avoiding the worst possible outcomes. Of course avoiding that consumption falls below the survival threshold is a first priority, but it may be considered part of a broader strategy of consumption smoothing. In doing so families make use of arrangements that reduce uncertainty over

1 Part of the material for this chapter was published in A. Kreimer and M. Arnold (eds.) 2000. Managing Disaster Risk in Emerging Economies. Disaster Risk Management Series no. 2. (Washington D.C.: The World Bank).

10

income realisations, like diversification. They also make adjustments after the realisation of income outcomes, such as borrowing and lending or the drawing down of buffer stocks. And they collaborate with others and pool risks in informal insurance arrangements. Advantage of the latter way of coping is that if insurance is complete, households do not have to undertake additional smoothing activities. Full insurance allows a household to specialise in the activity in which it has a comparative advantage and that brings the highest expected returns, irrespective of fluctuations therein. Unfortunately partial insurance is the rule, and even poor households can therefore not focus on the most profitable activity. In addition they often have to implement, often costly, measures to cope with any remaining income fluctuations. The organisation of this chapter is as follows. Section 2.2 discusses why fully efficient risk pooling is rarely achieved and examines possibilities for intertemporal consumption smoothing through savings and credit markets. Section 2.3 provides a review of mechanisms poor households make use of to smooth consumption when formal and informal insurance arrangements are absent. To this end a distinction is made between ex ante adjustments affecting the distribution of income realisations and ex post mechanisms allowing the stabilisation of household consumption contingent on a realised state. Section 2.4 contains an overview of the empirical literature on the role and scope of informal mechanisms in protecting the poor by pooling risks with others. Section 2.5 concludes.

2.2 Assuring Smooth Consumption To explore the methods rural households use to stabilise their consumption, imagine a village where each household earns an income that fluctuates over time. Village in this context does not literally mean village. It is a metaphor for any group, ranging from fellow villagers, the family or the international capital market, within which incomes can be pooled. For a start a storage technology is assumed to be absent. If collaboration between community members is absent, it follows that each household consumes the income it generates. If income is high, there is plenty to consume; when income is low, consumption shortages are experienced. Depending on income realisations, households go through a cycle of famines and feasts. Clearly this is not desirable and a household with a mild

11

aversion to risk earning an income with a coefficient of variation of 50 percent, would be prepared to give up between 12.5 and 25 percent of its average income to attain stable consumption (see chapter four). This is an enormous amount, especially if one realises that households that are poor to start with, are willing to sacrifice it. But for households in rain-fed agriculture a coefficient of variation of 50 percent is a realistic level of income variation. Dercon (1992a) for instance reports a coefficient of variation of crop income of 67 percent for households in Africa�s Sahellian zone, and one of 52 percent for those in the Sudanian zone. For South Indian villages estimates of the coefficient of variation of annual income from the main crops range between 37 and 101 percent (Townsend, 1994). In chapter four that the average coefficient of variation of household income for rural households in Zimbabwe is shown to lie between 40 and 60 percent.

If incomes earned by villagers are independent of each other, a situation might occur in which one household is on the brink of survival while its neighbour has so much that it spends its resources on only marginally appreciated items. Obviously if this were to happen, the advantages of income sharing would quickly be recognised. And if the number of households with whom income is pooled is large, aggregate income would even show little variation because of the law of large numbers. If, for ease of exposition, each household in the village is equally important2 and if each household has an identical utility function, then the optimal solution would be to pool all income and then redistribute it in such a way that each household attains the same marginal utility from each additional unit of consumption. In other words, each household obtains the same amount from the pool. It follows that with complete insurance household consumption does not depend on individual income, but only on aggregate income. This observation has served as basis for many tests on the presence of full insurance (see section 2.4 and chapter five). But in rural Africa, like in many places in the world, risks are not uncorrelated. Rainfall for instance usually affects all households in the village simultaneously. If in the presence of such covariate risk villagers would pool their incomes, then they would discover that the income aggregate is not stable. Cross sectional pooling does not insulate against community wide shocks and mutual insurance is only effective in dealing with idiosyncratic risk. To avoid aggregate income fluctuations, one has to ensure that the pool is large and comprises of uncorrelated risks, for instance by including villagers living in different agro-ecological zones. For households in rural

2 More specifically, if each household is assigned the same Pareto weight by the central planner (see also chapter 5).

12

Africa this is difficult to attain, if only because of communication and transport difficulties. But governments and private companies are often in a position to deal with these issues, explaining why formal insurance by these institutions is attractive. Now let the main source of risk not be rainfall, but illness. If illness is transient and recovery complete, then its consequences are temporary. But what if the disease affects someone�s capacity to work permanently so that the person becomes a lasting recipient of resources from the pool? Ideally, the members of the insurance pool will continue to transfer resources to the unlucky person even if it is unclear whether he will ever recover. The reason for this is that insurance is based on an ex ante agreement. Before the occurrence of an event with unknown consequences the insurance participants promise to share unexpected benefits and losses. Everybody is better off under this arrangement because the gain in utility from obtaining more than one expects, is less than the loss in utility from getting less than one expects so that obtaining the expected amount (in the aggregate all unexpected surpluses and deficits cancel) is preferred. But, after the occurrence of the event lucky households will have a great incentive to renege on their promise to support the unlucky ones. This is the enforcement problem. Enforcement problems occur because under certain conditions it is more attractive to opt out of an insurance arrangement than it is to make a contribution to the pool. The presence of this problem explains why informal insurance breaks down in extremely adverse circumstances like famines. In those situations the marginal utility from consumption is so huge that relatively lucky members in the insurance arrangement are no longer prepared to make net contribution to the pool. It also explains why the elderly risk exclusion from insurance pools. Their contributions to the pool are structurally less than what they obtain from it so that other participants in the insurance have an incentive to collude against them. If risk aversion decreases with wealth, enforcement problems also explain why the wealthy have less of an incentive to participate in mutual insurance networks. Their gains in terms of increased security are of relatively little value to them so that they opt out more easily if the contribution they have to make is too large. Another reason for wealthy households to opt out of informal insurance arrangements is that they have other options to smooth their consumption: the sale of buffer stocks for instance. There are three ways to deal with enforcement problems. The first is through advance payment. Enforcement problems do not occur if villagers set aside an amount (the insurance premium) before the event takes place. Formal insurance arrangements

13

typically make use of ex ante payments. But before ex ante payments can be a functional solution to the enforcement problem two conditions have to be met. First the institution offering the insurance has to be reliable so that insurees can be assured that the institution will meet its liabilities. Additionally a savings instrument has to be available which allows storage of resources over time, and which can be liquidated at short notice to make indemnity payments. In an agricultural society these conditions are often not met and contributions to the pool are usually made after the risk has manifested itself. Another way to deal with enforcement problems is by relying on punishment. Punishment reduces the benefits of opting out of an insurance arrangement. If the penalty is sufficiently serious opting out can be prevented entirely (the Mafia applies this principle successfully to prevent former members from revealing its secrets). Punishment may take various forms, it may be through a legal forum, through (threats with) violence or evil spells or it may be by feeling guilty. Guilt may be the reason why the young support the elderly. Another reason might be that the elderly have sufficient political leverage (i.e. sufficient possibilities for retribution) to ensure that their support is guaranteed. A third solution to enforcement problems lies in repeated interaction between participants. Repeated interaction contributes to the establishment of a self-enforcing insurance scheme as long as it remains attractive to participate. This happens if the benefits from continued participation exceed the cost of having to make a transfer in the current period. In such an insurance scheme those reneging on their promise are excluded from the future benefits of the insurance. Exclusion from future benefits is an implicit punishment. It is often relied upon, but to be effective it requires that members of the insurance group know each other well and that information on non-compliance is reliable. Exclusion as punishment is less suited if people are impatient (so that they do not care about the future) or if the frequency of shocks is low and intervals between different events long. So far risk has been exogenous in the sense that households could not affect it. Only rarely can risks not be influenced by behaviour (rainfall is an exception). If households can affect their level of risk then those fully insured might take risks they would not be prepared to take otherwise. This is the moral hazard problem. Another manifestation of the same problem is that, once insured, households have less of an incentive to put in the level of effort they would have put in had the insurance been absent. Consider for instance a household that can choose between two levels of activity. One requires a high

14

level of effort and the expected return from it is high. Another requires less effort and its expected return is low. Assume that the expected utility from additional expected income is sufficient to provide compensation for the disutility of extra effort so that in the absence of insurance the household puts in the high level of effort. Next some insurance is introduced. Now the household�s income is put into a common pool, which is distributed among the participants. In this case it is very well possible that the extra income the household obtains after pooling as a result of the high effort it has put in, is insufficient to compensate it for the disutility of doing so. After all, most benefits of the high level of effort are taxed away by the insurance pool and benefit other members in the pool. The optimal response to such a situation of high implicit taxation is to work less. But all households think along the same lines and each of them concludes it is not sensible to put in the high level of effort. This leads to a situation where no-one works hard, where aggregated income is low and where everybody would have been better off in the absence of insurance. The consequences of moral hazard are less if villagers feel a certain altruism or responsibility toward each other. In that instance each household internalises the undesirable implications of its own shirking behaviour. Intense monitoring in combination with punishment also allows one to deal with moral hazard. This kind of monitoring is possible in close knit communities (like our village) and offers an explanation why privacy is a scarce commodity in village economies. The need for monitoring also clarifies why many informal insurance arrangements are between members of (extended) families, between those with the same (ethnic) background, between people collaborating closely or those living in the same community. In close monitoring, village members are likely to have an advantage over formal institutions, which explains why non-market institutions may function in environments where formal institutions fail. The flip side of this argument is that risks faced by members of these close-knit groups are often correlated. And as was argued before, in those cases mutual insurance is less effective so that the benefits of a large pool have to be traded off against the cost of monitoring. Even in villages with little privacy there is a limit to what close monitoring can do especially if it is not clear whether a bad outcome is due to external circumstances or the result of insufficient effort and care. A solution employed in practice it to offer incomplete insurance so that part of the shock has to be covered by the household itself. This contributes to an in-build incentive to maintain effort at the desired level or to avoid unnecessary risks. Insurance is thus partial, a finding consistent with most empirical

15

research into mutual insurance at the village level. Partial insurance can explain why few farmers specialise completely, and why many prefer to diversify by cultivating plots that are scattered around and of different physical characteristics. Until now the focus has been on insurance. Next the attention is shifted to the use of credit and savings in dealing with income variability. The presence of a credit market allows households to smooth consumption by permitting them to borrow money when they face bad income draws and to repay their debts later. An important difference between insurance and credit or savings is the time dimension of the latter instruments. Where the principle behind mutual insurance is the cross-sectional sharing of incomes, implying that households have to decide on an optimal sharing rule, the use of credit (the same holds for savings) implies that households have to decide on the optimal intertemporal allocation. The underlying rule for an optimum is not unlike the rule that described the optimum for a mutual insurance however. It states (for the case where the rate of time preference equals the rate of return on assets) that the household should be indifferent between consuming its last unit of consumption in the current period and saving it and consuming it the next period. An important difference between relying on mutual insurance and using credit is that credit leads to permanent differences in consumption between otherwise identical households. Consider for instance a village with two households of equal wealth, of comparable composition and with identical time preferences and expectations about the level and variation of their income. The households do not insure each other but a household with a good income draw will lend money to the household with a bad income draw. This helps both to smooth their consumption. In this respect a credit agreement contributes to improved consumption security. But consider what happens after the realisation of the first period�s income outcomes, when one of both households obtains a higher income. The unlucky household borrows money and knows it will have to pay interest in the future. Since the expectations for the generation of income remain identical for both households, it means that the expected income that can be used for consumption by the unfortunate household has to be lower (it pays interest) than that for the household which was lucky (it receives interest). This has a bearing on current consumption as the intertemporal smoothing rule tells the unlucky household to bring its current consumption in line with the reduced expected future consumption level. For the lucky household the reverse holds. Relying on a credit arrangement therefore leads to inequality between households of different fortune, something which would not have

16

occurred had the households relied on a mutual insurance arrangement. For this reason, insurance contracts are to be preferred. There are also advantages to relying on credit. For instance it prevents wealthy households that are not interested in participating in an insurance pool, from withdrawing completely from the provision of security. And there is an in-built incentive in credit provision that helps to avoid moral hazard. After all, borrowers have to repay their loans so that they bear the full consequences of bad outcomes and are therefore suitably motivated to avoid risks and to put in the optimal level of effort. In many other respects the provision of credit is subject to similar problems as is the provision of insurance. There is an enforcement problem contributing to the absence of formal credit in poor areas. After all, how can a lender be assured that his borrower will repay? The enforcement problem may be solved not by relying on punishment but by demanding collateral. Unfortunately collateral is something the poor usually cannot provide. Another way to deal with enforcement problems is to rely on close monitoring. But monitoring is costly and comprises a large fixed cost element. This makes small loans, in which the poor would be mostly interested, unattractive especially as raising interest rates on small loans does not overcome this problem. It eventually leads to a situation in which only lenders with very risky projects are prepared to borrow (adverse selection). Like insurance, credit providers also fail to provide much security after the occurrence during covariate shocks. One reason is that many households will seek credit at the same time, leading to increases in local interest rates. Another is that credit providers are likely to stop providing credit if they consider the conditions of borrowers so bad that they feel no longer assured of loan repayment. Especially for the poor, the fact that loan repayments have to be made at fixed dates makes reliance on credit for consumption smoothing unattractive. After all, at the date of repayment household income may be low. In that case loan repayments would drain the already limited resources available for consumption. To avoid such a situation household might decide not to take loans in the first place. The ground for such a precautionary motive disappears if repayment is conditional on the situation of the borrower. In this case some of the (repayment) risk is passed on to the lender so that the loan instrument and risk pooling become intertwined. The possibilities for consumption smoothing through intertemporal decisions are not exhausted in the absence of credit markets. Household can also make use of buffer

17

stocks. In a way accumulating buffer stocks is the mirror image of relying on credit. Where making use of credit implies repaying after the event, accumulating buffer stocks requires resources to be set aside before the event. Clearly it is possible to run out of buffer stocks, especially after a particularly bad shock or after a series of bad income realisations. In that case, consumption can no longer be shielded from fluctuations in income. But generally a high degree of consumption stability can be achieved through the use of buffer stocks. Like relying on credit, following a buffer stock strategy is not an optimal strategy. It leads to differences between lucky and unlucky households and uncorrelated risks are not pooled. But to deal with covariate shocks (against which mutual insurance is helpless) a buffer stock strategy is very appropriate. For buffer stocks to properly fulfil their function, they have to meet a number of criteria. Buffer stocks should yield a sufficiently high return to encourage households to take them up. In many situations this is not the case. Food stocks decay for instance. The value of the buffer stock should also be uncorrelated or negatively correlated with income realisations. A buffer stock whose value drops if incomes are bad as is the case with cattle for instance is of less use than a buffer stock whose value is independent of income outcomes (gold) or increases with them (food stocks). Buffer stocks should not be lumpy, i.e. one should be able to keep them in small amounts. One does not kill a cow to feed a family for one day. In that case a chicken or goat would suffice. A buffer stock should also be liquid, meaning that it can be used for consumption purposes easily, either because there is an active market on which the buffer stock can be sold and where food can be bought in return or because it can be used for consumption directly. Finally, a buffer stock should be safe to keep, implying that it has to be around when it is needed and not easily get stolen or disappear otherwise (by being subject to survival risk for instance). It will be clear that the ideal buffer stock does not exist. But by keeping combinations of different assets households are able to circumvent the greatest obstacles. Food stocks for instance (safe, relatively liquid, not lumpy, negatively correlated with income outcomes but with a negative return) can be combined with cattle (relatively safe and liquid, with a positive return but negatively correlated with income outcomes and lumpy) and cash (liquid, not lumpy, relatively safe, uncorrelated income outcomes, but with negative returns (inflation)). Recapitulating, to shield consumption from fluctuations in income households have three options, each of which can be explored but which even in combination are unlikely to

18

lead to complete consumption smoothing. Risks may be pooled in a mutual insurance. If the mutual only offers partial insurance or if risks are covariate consumption may be smoothed through credit markets by borrowing resources in times of income shortfall and repaying them in more favourable times. Additionally liquid assets can be accumulated in good seasons and disposed off in adverse times. Dealing with income risk entices costs. If consumption cannot be shielded from income variability, then income decisions will not be based on a profit-maximising basis alone. Risk mitigating considerations start playing a role and through diversification the variability of income might be reduced at the expense of lower mean income. If households rely on informal insurance, they have to rely on costly measures to deal with the information and enforcement problems. An additional disadvantage of informal insurance arrangements is that poor households might become excluded, especially during covariate shocks. And accumulating buffer stocks in the form of livestock may lead to overgrazing and low returns on savings which could be used more productively elsewhere in the economy.

2.3 Self-Insurance Options In the previous section four ways to shield consumption from income variability were distinguished: insurance and credit transactions, accumulation and decumulation of buffer stocks and adaptations to the income process. A common element of the first two mechanisms is their susceptibility to information and enforcement problems. The latter two mechanisms are not affected by these problems as they are carried out by the household itself and not in interaction with others. In this section the focus is on these mechanisms, which are labelled self-insurance. Self-insurance comprises those options for dealing with income risk which are carried out by the household itself and which are, for that reason, not affected by information and enforcement problems. In seeking self-insurance, households may explore (1) risk management or (2) risk coping strategies or a combination of the two. Alderman and Paxson (1992) introduced this terminology and classify the former as aiming to reduce income variability and the latter as aiming to cushion the effect of income risk on consumption. They include under risk coping, saving behaviour as well as credit and insurance transactions. The treatment of these latter two transactions is postponed till the next section. In this section the focus is first on the use of risk management and then on buffer stocks.

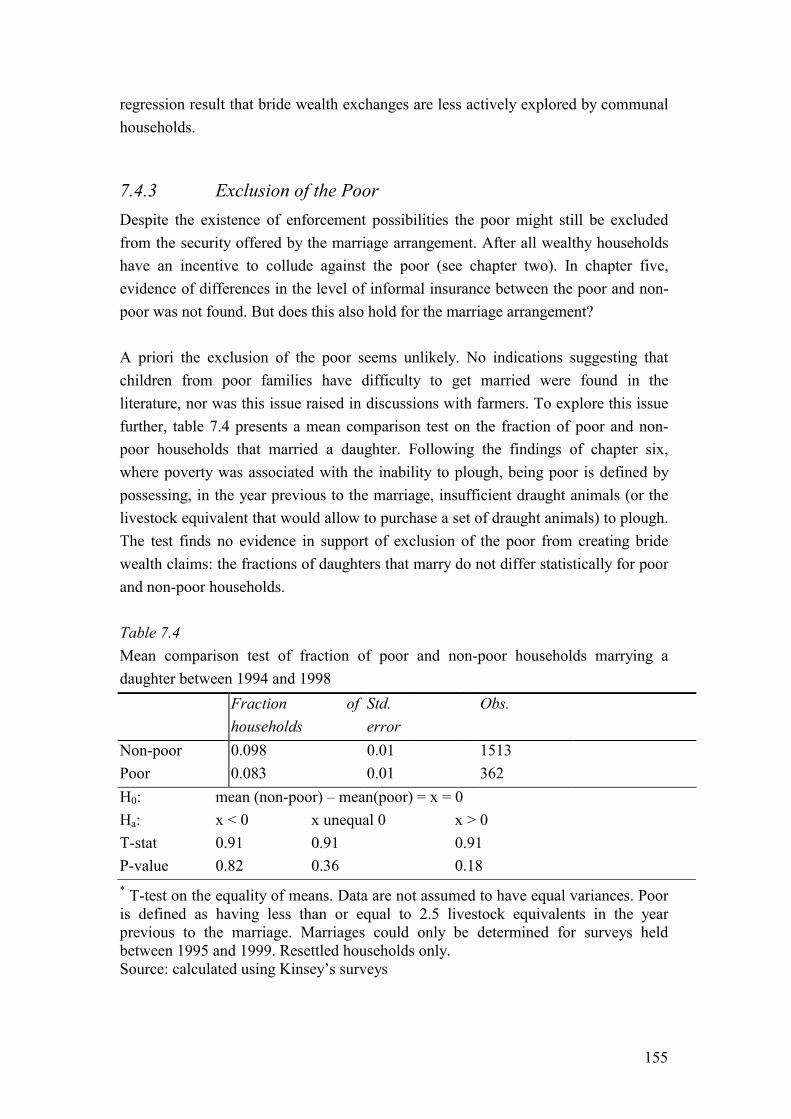

19

One way to reduce variability in total income is through diversification. Diversification brings a reduction in income risk if the sources from which income is generated have a correlation coefficient below one. Various suggestions exist on how income sources can be diversified.3 For farmers, if rains or soil type are heterogeneous, spatial spreading of plots may help to ensure a stable yield. If the length and pattern of the rainy season are variable, differences in planting dates may reduce income risk. In homogenous areas diversification can be attained by growing crops of different characteristics. And agricultural outcomes may be complemented with off farm incomes. Rosenzweig and Stark (1989) find for instance for a group of Indian households that those facing greater volatility in farm profits are also more likely to have a household member employed in steady wage employment. Diversification of income sources is especially attractive if a reduction in income variability is not associated with a reduction in mean income. Empirical evidence that a combination of activities does not have to be at the expense of mean income is provided by Blarel et al. (1992). They report that cropping systems such as mixed cropping and field fragmentation take advantage of complementarities between crops, variations in soil types and differences in micro climate so that risk spreading is possible with little loss in total income. The same can also be attained if a household conducts several activities because of timing differences, as is the case with seasonal activities, or when it undertakes additional income generating activities to deal with low income. Kochar (1997) shows that households in India cope with negative idiosyncratic shocks by working longer hours or taking an extra job. Dekker and Hoppenbrouwer (1993) illustrate for Zimbabwe that households took up gold panning, an activity usually not undertaken, to earn income during the 1992 drought. Whenever diversification goes at the expense of specialisation it will be costly. Still households will be prepared to explore the risk reducing opportunities of diversification. To understand why, realise that most households accumulate assets which yield no or a negative return to protect consumption from (uninsured) variability in income. Since asset accumulation goes at the expense of current consumption, households sacrifice consumption now for greater safety later. Suppose the same level of safety can be attained by skewing the income process in such a way that both its variability and mean are reduced. The household will then be indifferent between both options if the net present value of the utility cost of a reduction in expected income which accompanies the choice for a safer income process is equal to the net present value of the reduction in utility that follows from the postponement of consumption required to accumulate assets.

3 For a recent review of the literature on diversification, see Ellis (1998).

20

In that sense risk management and the accumulation of buffer stocks are substitutes.4 Just and Candler (1985) illustrate that there is room for income skewing. They show for Nigeria how crop diversification can reduce the variability of agricultural income but also that the reduction of income variability comes at a cost: the safest outcomes have the lowest returns. Since diversification is not costless combining different income sources can be interpreted as a risk management strategy. This does not imply that a household, which undertakes few different activities, does not try to reduce its income risk: a household may also have specialised in a low return - low risk activity. A little diversified household is therefore not necessarily one taking its income decisions independent of the risk associated to it. Specialisation in a low income - low risk activity is more likely in the presence of entry barriers, for instance if the most profitable activities require substantial investments. In that case it will be difficult for poor households to accumulate sufficient savings to overcome the entry barrier to the activity. Dercon (1998) illustrates this for Tanzania. He argues that cattle are a profitable investment, but one that requires a large sum of money. Dercon shows that this leads to a situation where richer households own substantial cattle herds, while poorer households specialise in low return - low risk activities. Entry barriers may not only confine poorer households to low return-low risk activities, they may also prevent the poor from entering the high return-low risk activity. A study by Reardon, Delgado and Matlon (1992) for the Sahel region associates for instance higher and more stable incomes and food consumption with diversification. Dercon and Krishnan (1996) provide an illustration for this phenomenon. They use survey data from rural Ethiopia and rural Tanzania to analyse different income portfolios of households and find that the most attractive off farm employment opportunities (in terms of risk and return) have the highest entry barriers. Entry is determined by investment in particular skills or by access to capital, something only the wealthy can afford. It has been suggested in the previous section that buffer stocks and risk management may be considered substitutes. If wealth is associated with accumulation of buffer stocks (which in turn can be associated with better access to credit because of the presence of collateral) then wealthier households may be prepared to bear more risk than poorer households. Evidence to support that the wealthier are less affected by income risk is 4 This is only true from a household utility perspective. At the aggregate level, where through the law of big numbers idiosyncratic risks cancel out, buffer stocks are to be preferred to risk management as the latter leads to lower expected aggregate income.

21

presented by Rosenzweig and Binswanger (1994). They show for certain villages in India that wealthier households allocate their productive assets to riskier activity portfolios than poorer households and find that increasing the coefficient of variation of rainfall timing by one standard deviation would, for a household in the bottom wealth quartile, reduce farm profits by 35 percent. For a household of median wealth this would be 15 percent, while the increased riskiness would have a negligible effect on the profitability of the richest farmers. Dercon (1996) presents comparable results. He argues for Tanzania that sweet potatoes are a low risk crop yielding a low return. Dercon shows that this crop is favoured by the non-wealthy. Households in the wealthiest quintile devote on average a little less than two percent of their land to sweet potatoes as opposed to nine percent for households in the lowest quintile. The implication is that the poor who have fewer buffer stocks, less possibilities to access credit and a greater interest in risk management strategies are often not able to access the safest and most rewarding income opportunities because of entry barriers and are consequently confined to safe but low return income generating possibilities. Let us now turn to the use of buffer stocks. Implicit in studying their use is the suggestion that households have a long run perspective. After all, to accumulate buffer stocks one has to be prepared to forego current consumption in exchange for benefits at an unspecified time in the future when income may be temporarily low. The notion that farmers have a long run perspective has not always been accepted. Bauer and Paish for instance wrote in 1952 that �small producers are unlikely to have the self-restraint and foresight to set aside in good times sufficient reserves to cushion the effect of worse ones, or, even if they have, they may be debarred from doing so by social custom and obligations� (p.766). But since Schultz (1964) launched his thesis about the rational but inefficient peasant farmer, and in view of the abundant empirical evidence in defence of Schulz�s thesis, this notion has been left. If farmers have a long term perspective and they smooth their consumption then it follows that temporary shocks should not affect their consumption. In response to a positive temporary shock households should accumulate assets, and following a temporary and negative shock they should be depleted. Only if changes in permanent income occur (i.e. changes in the net present value of lifetime income) should consumption be adjusted. So a possible test as to whether rural households smooth their consumption is to test whether consumption is unaffected by temporary shocks and whether it adjusts following permanent shocks. To be able to do so, one has to distinguish between permanent and transitory shocks. In practice this is difficult but Paxson (1992) in her study on Thai rice farmers found a way to do so. She identifies rainfall variation as an exogenous temporary component of

22

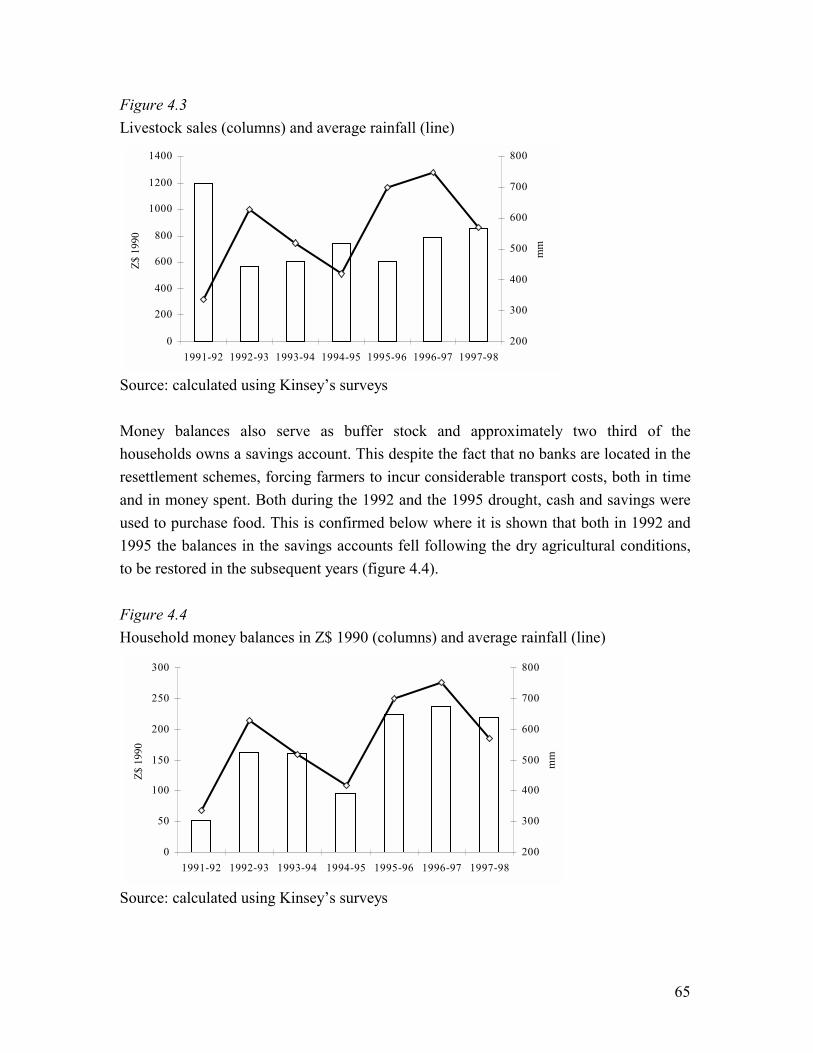

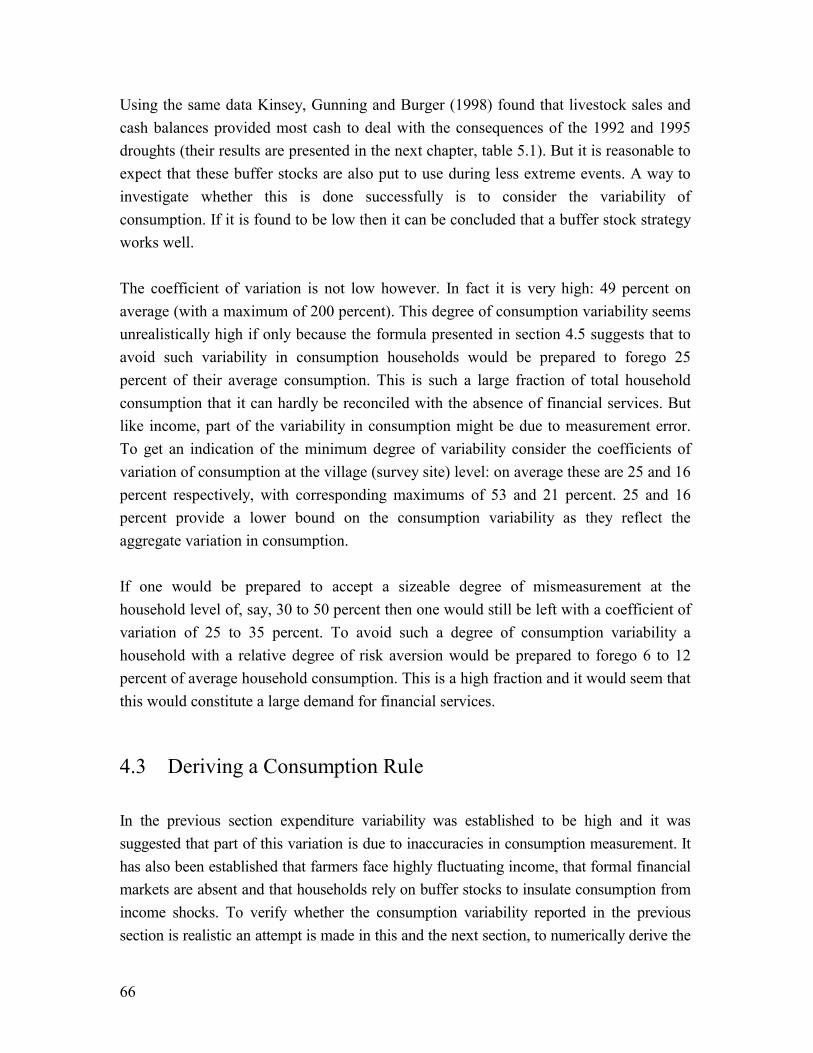

income and confronts this with household savings. Her results show farmers to save three quarters to four fifths of transitory income changes, which is not significantly different from one, which is what the coefficient should be in the case of complete consumption smoothing. She concludes that the marginal propensity to save transitory income is high and that farmers therefore smooth consumption. Paxson is not the only one to find evidence in support of this. For Kenya, Bevan, Collier and Gunning (1989), show that farmers invested most of their windfall income during the coffee boom of the 1975-79 in profitable investments and spent only a fraction of it on additional consumption. Musgrove (1979), Bhalla (1979 and 1980), and Wolpin (1982) also find consumption smoothing to be real and significant. Rosenzweig and Wolpin (1993) illustrate for India how smoothing is carried out in practice. They find bullock sales to increase significantly when weather outcomes are poor and incomes low, and purchases of bullocks to increase when rainfall is ample and incomes above average. For beneficiaries of Zimbabwe�s land reform program Kinsey, Burger and Gunning (1998) show that they accumulated considerable numbers of livestock, financial assets and food stocks and that these were used to smooth consumption during the droughts of 1992 and 1995. A buffer stock strategy can be quite successful. Walker and Jodha (1982) for instance report the responses of drought hit households in rural India. They show that in some areas assets were depleted by up to 60 percent, that debts were increased by up to 192 percent but that total consumption expenditure per household fell only 8-12 percent. Buffer stocks, accumulated in more prosperous times, were instrumental in ensuring a fall in consumption, which was small relative to the fall in income. Simulation exercises by Deaton (1989 and 1991) confirm the ability of a buffer stock strategy to secure household consumption. Only when a series of shocks occurs may households run out of buffer stock and become vulnerable to low income realisations. The latter finding is consistent with Webb and Reardon�s (cited in Alderman and Paxson, 1992) observation that famine conditions were observed in Burkina Faso and Ethiopia only after two successive droughts. Apparently consumption levels could be maintained during the first year of the drought, but when buffer stocks started to get depleted, consumption had to be adjusted downward. Deaton�s analysis is based on the presence of a safe savings instrument. In a developing country context good savings instruments are scarce. Simulation exercises along the lines of Deaton by Dercon (1992b) show that if there is a large positive covariance between asset values and income an asset strategy to smooth consumption becomes less effective. Households then tend to

23

restrict the sale of assets during crises because they gain so little extra consumption in return. Unfortunately a positive association between asset values and (real) income is common, especially in places where markets are less well integrated. The scarcity of food during a shock drives up its price while the large amount of buffer stocks for sale reduces the price of assets. Fafchamps and Gavian (1996) show for instance that in Niger the price of livestock is plummeted during the 1984 drought. The same occurred in Zimbabwe during the 1992 drought. But not only under drought conditions do prices collapse. In Zimbabwe it is not uncommon for livestock to be sold at a huge discount, simply because the buyer knows that the seller is facing an urgent situation and will have difficulty to find another willing buyer. In the face of such price fluctuations a buffer stock strategy may very well fail in its objective to maintain consumption at its original level. Nonetheless a household that reduces its consumption still behaves rationally. It responds to the change in the food - buffer stock price ratio and substitutes current consumption (which is expensive) for future consumption (which is relatively cheap). Fafchamps, Udry and Czukas (1998) illustrate for West Africa the consequences of buffer stocks whose values are positively correlated with income outcomes. They find that livestock is a buffer stock as it is accumulated when there is windfall income while disinvestment takes place in years with adverse weather shocks. They also find that livestock sales compensate only a surprisingly low, twenty to at most thirty percent of (drought related) income shortfalls due to village level shocks during the Sahellian drought of the 1980s. For Zimbabwe Kinsey, Burger and Gunning (1998) found that households had sufficient assets left after the 1992 drought. Since the households also sharply reduced the frequency and the quantity of meals during the drought it suggests that buffer stocks were not able to compensate the reduction in income. Again there is evidence of sharply reduced prices for the main buffer stock: cattle. In 1992 the real producer price index for beef in Z$/mt was 807. In 1993 it was 552 (Zimbabwe, 1997).5 In this context it should not come as a surprise that so many households turned to gold panning during this drought. Not only was this one of the few opportunities left to earn some additional income, gold, being an internationally traded commodity, is an example of a good whose value is typically little affected by local income variations. Another reason to cut back current consumption following an income shock may be to avoid a reduction in permanent income following the sale of productive assets. Udry

5 The high correlation between rainfall and livestock prices is confirmed for the households incorporated in Kinsey�s data set (introduced in chapter three). For the period 1991/2-1997/98 the correlations between real livestock prices and national rainfall were 0.33, 0.22 and 0.27 for respectively cows, trained oxen and heifers. Each of these is significant at the 1 percent level.

24

(1995) shows for instance for Nigerian farmers who faced a crisis, which was less serious than the ones in Burkina Faso and Zimbabwe, that grain stocks and cash savings were used to buffer consumption from income, but that livestock savings were unaffected. He concludes that livestock are primarily held for productive purposes because livestock are subject to diminishing returns while the return to grain storage is constant, so that households prefer to buffer through grain stocks as selling livestock become increasingly expensive in terms of foregone return. The fact that the crises in Zimbabwe and Burkina Faso were worse than the one in Nigeria then not only explains why livestock was used as buffer stock in these instances, but also why households might have been reluctant to rely too much on the sale of livestock: it could have reduced permanent income too much. Johda (1978) even suggests that ensuring that the opportunities for future income generation are preserved during a crisis is a primary concern of rural families. When faced with extreme food shortages rural households do not seek the protection of current consumption but the protection of productive assets, which are disposed of as a last resort, since their loss is likely to affect the household�s long-term prospects of recovery from a crisis. Based on their experiences during the droughts in the 1980s in Sudan, Pyle and Gabbar (1990) arrive at a similar conclusion. They distinguish three stages of household coping. Initially, households pursue strategies that do not endanger future production but which are directed at conserving the assets they possess, including the collection of wild foods, consumption of food stores, recalling of loans etc. If the bad conditions prevail, less favoured measures have to be followed which affect the household�s potential for future income generation. This includes a severe rationing of consumption, sale of productive assets and, in farming, consumption of seeds. When all these strategies are insufficient and the bad conditions prevail, households may starve, or survive without much to fall back on, leaving them in an extremely vulnerable position. Whether it is due to changes in relative prices or for fear of depleting one�s productive assets, household consumption is generally adapted downward following temporary income shortfalls. Agarwal (1990) describes how drought conditions reduce consumption and lead to shifts in the types of foods eaten from fine to coarse grains to animal feed. As scarcity worsens there is a decline in foods such as milk, meat, fruits and vegetables, food is made to last longer and a reduction in the quantity eaten by cooking fewer meals a day is followed going hungry for several days. The decline in food consumption is accompanied by the decline in other consumption: clothing, religious ceremonies and the postponement of marriages. Education expenses also fall. Jacoby and

25

Skoufias (1997) report for India for instance decreases in investment in children�s education in response to income shocks.

The available evidence therefore suggests that the availability of buffer stocks is no guarantee for a smooth consumption pattern. Buffer stocks go a long way to avoid unwanted variations in consumption. But in the face of a series of shocks, when the prices of buffer stocks collapse or if the buffer stocks have a productive use a well, then households may prefer to reduce consumption rather than deplete their buffer. The consequences of this choice vary. A temporary reduction in consumption may a devastating experience, it need not have long-term implications for health. Still, Behrman (1988) finds that because households in rural South India are not able to smooth consumption, the health of children, and especially that of girls, suffers during seasons before the major harvest. A prolonged reduction, or cutting back of education expenditures can easily lead to a permanent reduction in the ability to generate income in the future. Hoddinott and Kinsey (1999) find for Zimbabwe that child growth was not only reduced by the 1995 drought but also that the reduction was permanent: no catch up growth was recorded after the drought.

2.4 Insurance and Credit Transactions The efficiency gains to be attained by pooling income risk between households, opens scope to explore ways to smooth consumption through insurance transactions. In section 2.2 it was concluded that if idiosyncratic risks are fully pooled then household consumption should track village income and nothing else. Townsend (1994) tests this hypothesis in three of the Indian ICRISAT villages. He finds comovement in consumption between households living in the same village but rejects the strongest form of complete risk sharing. Nonetheless he finds that consumption is not much influenced by own income, sickness, unemployment, or other idiosyncratic shocks, controlling for village level risk, leading him to the conclusion that risk pooling is less than perfect, but nonetheless considerable. Ravallion and Chaudhuri (1997) confirm the comovement in consumption between households in Townsend�s villages, but show that Townsend�s econometric test is biased toward the acceptance of the full insurance model. They redo his estimates and where Townsend finds that the marginal propensity to consume out of a household�s own income is nowhere greater than 0.14, Ravallion�s and Chaudhuri�s put it between 0.12 and 0.46. Deaton (1997) examines the presence of complete risk pooling within villages in Côte d�Ivoire. He finds little evidence for it.

26

Grimard (1997) considers whether the ethnic group is a more appropriate basis to delimit the membership of an insurance pool than is living in the same village. He uses the same data as Deaton and finds somewhat stronger evidence in support of insurance. Jalan and Ravallion (1999) finally, find evidence of partial insurance for a panel of households in rural China. Interestingly they distinguish the degree of insurance by wealth group and find that the poorest decile is much less insured than the wealthiest. For the poorest wealth decile, 40 percent of an income shock is passed on to current consumption as opposed to approximately ten percent for the richest third.

So though most insurance tests reject the presence of complete insurance, they are in support of the presence of some, partial, insurance. It is therefore interesting to know how this insurance is arrived at. One way is through self-insurance. Though this is not what most authors who test for full insurance have in mind, a test on the independence of consumption from household income is also accepted if households protect their consumption against income shocks through the sale of buffer stocks (chapter five provides a more elaborate treatment of this issue). But security is also sought in interaction with others. There are many manifestations of this. Labour invitations and other forms of manpower assistance are a way to help the sick and the old (Scott, 1976). Livestock loans allow access to productive assets by those who cannot afford them (chapter six). Children that parents cannot support are sometimes adopted by better off households. For Zimbabwe Deininger, Hoogeveen and Kinsey (2001) report that land reform beneficiaries who are generally wealthier than ordinary farmers take care of substantially more children and adults members. Food and other gifts are provided to those hit by illness of productive family members or crop damage. Most of these forms of assistance must be returned at some time in the future. Platteau (1997) introduces a separate term to describe these mutual gift relations: balanced reciprocity. He illustrates it with the functioning of informal sea rescue organisations, which exist in small scale fishermen communities in Senegal. In these organisations captains commit themselves to helping to rescue fishermen in trouble at sea and to contributing towards repairing or replacing damaged equipment. Such contributions are made in the expectation of future reciprocity. Another way to obtain security is through interlinked transactions. Interlinking is the simultaneous fixing of transactions between two parties over several markets, with the terms of one transaction contingent on the terms of another. Sharecropping is an example. In sharecropping contracts, the lessee pays the lessor a predetermined share of the harvest instead of a fixed sum. These institutions contribute to risk sharing because

27

rents are low when outcomes are bad while they are high when the lessee can afford it: at high outcomes. Another form of interlinkage is between credit and marketing in which a borrower uses the lender as exclusive wholesaler for his output. Often it takes several periods before a significant loan is made thus allowing the borrower to assess the lender�s capacity and willingness to repay. This strategy reduces information problems and improves the farmer�s opportunities to borrow. Interlinkage may thus induce Pareto improving changes in the allocation of resources (Hoff et al. 1993). Nonetheless, in many instances interlinkage is associated with large costs and distortions. The miserable employment conditions many farm workers on Zimbabwe�s commercial farms have to put up with in exchange for some security of employment are a telling example of this. And the distortions associated with a 50 percent share are similar to those associated with a 50 percent marginal tax rate. This illustrates that informal insurance arrangements may provide solutions to the problem of risk in areas where formal insurance and credit markets are absent. It also shows that these solutions may be costly. Nevertheless certain groups are prepared to bear these costs. Obtaining transfers are another means to secure a more stable household income. Private transfers are large and frequent in some countries. Cox and Jimenez (1997) show that 40 percent of black South Africans either receive or give transfers that, on average, amount to 37 percent of income for net recipients.6 These same authors find for the Philippines (Cox and Jimenez, 1998) that 82 percent of urban households and 89 percent of rural households report receiving transfers. Migrants play an important role in the provision of these transfers. Again in the Philippines, 26 percent of urban households and 13 percent of rural households received remittances from abroad. These are sent by spouses to support their family back home and by migrant children living in urban areas who sent money and goods to support their parents in rural areas. But not in all cases are transfers this important. Rosenzweig (1988) finds that transfers respond to risk but that they amount to less than 10 percent of the size of typical income shortfalls. Especially in economies where the consequences of a natural disaster spill over from the agriculture to other economic sectors the role of transfers in income smoothing is limited. Czukas, Fafchamps and Udry (1998), for instance, find little evidence for transfers to offset income shocks in the droughts in Burkina Faso between 1981 and 1985. Reardon, Matlon and Delgado (1992) confirm this as they report transfers to comprise less than three percent of the losses for the poorest households after the 1984 drought in the Sahel. 6 Many of these transactions may also be considered income source diversification instead of informal insurance, depending on whether the outmigrated family member is thought to have formed a different household or whether he is still considered part of the original household.

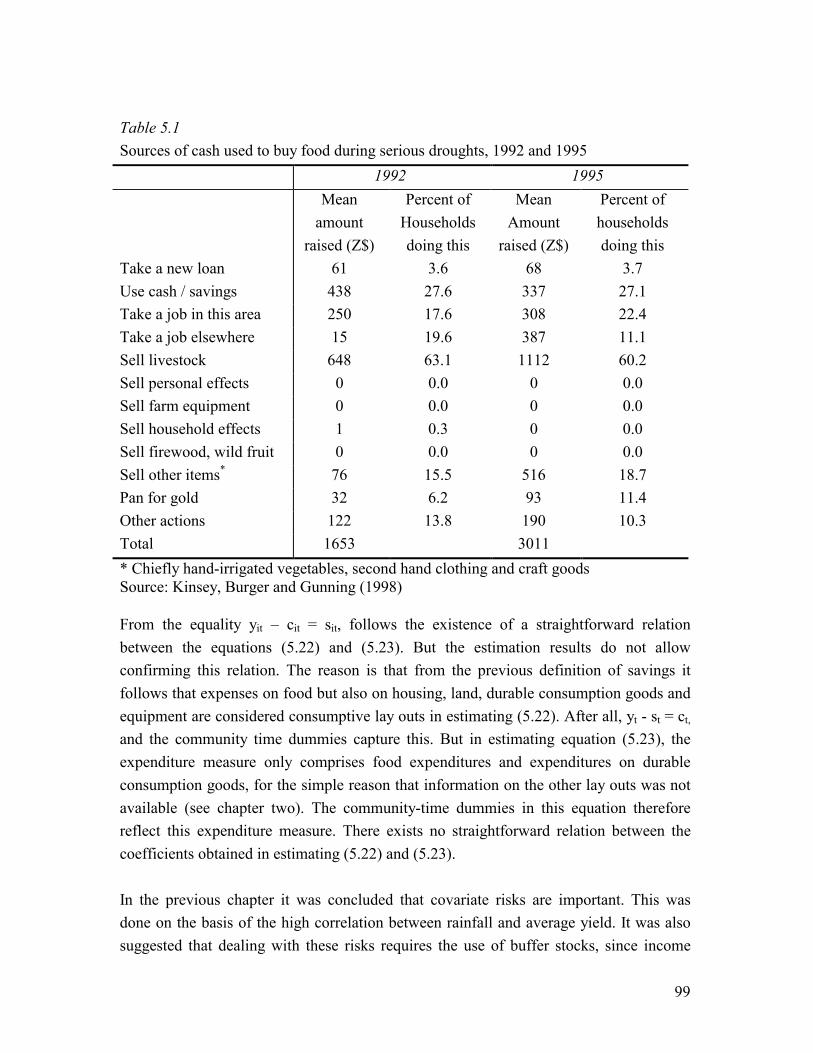

28