Embed Size (px)

Citation preview

RISK MANAGEMENT AND FINANCIAL CRISISParis, March 19 & 20, 2009

2nd InternationalFINANCIAL RESEARCH FORUM

with the support of:

LARGE RISK in INSURANCE

Research Chair AXA/FdR

INSTITUT LOUIS BACHELIERCENTRE D'INNOVATION FINANCIERE

Risk & Liquidityin the Industrial EconomyResearch Initiative

Risk & Liquidityin the Industrial EconomyResearch Initiative

Chairman: Lorenzo BERGOMI, Société Générale CIB

“ Hedging Interest Rate Margins on Demand Deposits”

Jean-Paul LAURENT, IFSA, Lyon University Alexandre ADAM, BNP Paribas Mohamed HOUKARI, ISFA

“ The Price of Protection: Derivatives, Default Risk, and Margining”

Rajna GIBSON, University of Geneva Carsten MURAWSKI, University of Melbourne

Discussant: Patrice PONCET, Paris I University and ESSEC Business School

Chairman: Olivier TOUTAIN, MOODY’S

“ Accounting for Guarantees within the Granulatory Adjustment for Basel II”

Eva LÜTKEBOHMERT, Sebastian EBERT, University of Bonn

“ Comparison Results for Exchangeable Credit Risk Portfolios”

Areski COUSIN, Lyon University, ISFA Actuarial School, Jean-Paul LAURENT, ISFA, Lyon University

Discussant: Christian GOURIEROUX, CREST and University of Toronto

08 h 00 / 08 h 30

08 h 30 / 08 h 45

08 h 45 / 10 h 15

10 h 15 / 10 h 30

10 h 30 / 11 h 30

11 h 30 / 12 h 30

12 h 30 / 14 h 00

Thursday - March 19, 2009

REGISTRATION

COFFEE BREAK

PARALLEL SESSIONS

PARALLEL SESSIONS

LUNCH hosted by Danièle NOUY, Secretary General, French Central Bank

Parallel session I : Risk Management

Parallel session 3: Large Portfolio

Parallel session 2 : Backtesting

Parallel session 4: Fund Performance

WELCOME ADDRESS by Jean LAURENT, Chairman, FINANCE INNOVATION & Europlace Institute of Finance (EIF)

PLENARY SESSION I Guest speaker: Til SCHUERMANN, Federal Reserve Bank of New York

“The 7 Deadly Frictions of Subprime Mortgage Credit Securitization”

Chairman: Alain MONFORT, CNAM and CREST

“ Robust Backtesting Tests for Value-at-Risk Models” José OLMO, University of London, J. Carlos ESCANCIANO, Indiana University

“ Backtesting Value-at-Risk: A GMM Duration-Based Test”

Sessi TOKPAVI, Gilbert COLLETAZ, and Bertrand CANDELON University of Orléans, Christophe HURLIN, Maastricht University

Discussant: Jean-Michel ZAKOIAN, CREST and Lille III University

Chairman: Raphaël DOUADY, Riskdata

“ Performance with an Application to Hedge Funds” Serge DAROLLES, L-Performance with an Application to Hedge Funds, Christian GOURIEROUX, CREST and University of Toronto, Joann JASIAK, York University, Canada

“ Does Team Management Reduce Operational Risk? Evidence from the Financial Services Industry”

Stefan RUENZI, University of Texas at Austin, Michaela BÄR, University of Cologne, Conrad S. CIOCCOTELLO, Georgia State University

Discussant: Olivier COHEN*, Société Générale CIB

Panel Session: “New Challenges in Risk Management”

Chairman : Michel CROUHY, NATIXIS

Valérie RABAULT, BNP Paribas

Tarik SMIRES, KPMG

Chairman: Stéphane GREGOIR*, EDHEC

“ Jump and Cojump Risk in Subprime Home Equity Derivatives”

Bruce MIZRACH, Rutgers University

“ Parameter Stability and the Valuation of Mortgages and Mortgage-Backed Securities”

Michael LACOUR-LITTLE, California State University, Yun W. PARK, California State University, Richard K. GREEN, University of Southern California

Discussant: Jean-Paul LAURENT*, ISFA, Lyon University

Chairman: Xavier FREIXAS*, Universitat Pompeu Fabra, Barcelona

“ The Same Bond at Different Prices : Identifying Search Frictions and Demand Pressures”

Peter FELDHÜTTER, Copenhagen Business School

“ Return and Volume: Between Information and Liquidity”

Gaëlle LE FOL, Evry University and CREST, Serge DAROLLES, SGAM AI and CREST, Gulten MERO, Rennes University and CREST

Discussant: Laurence LESCOURRET*, ESSEC and CREST

** To be confirmed** Poster sessions are effective means of conveying information. Poster’s visual aspects are combined with presenter’s verbal explanations.

Parallel session 6 : Modelling Defaults

Parallel session 8 : Credit Derivatives

PLENARY SESSION II :

PARALLEL SESSIONS

18 h 00 / 19 h 00

14 h 00 / 15 h 30

15 h30 / 16 h 30

16 h 30 / 17 h 00

17 h 00 / 18 h 00

Parallel session 5 : Mortgage Backed Securities

Parallel session 7 : Trading Liquidity

Guest speaker : Christian de BOISSIEU, Centre d’Observation Economique (COE)

Chairman : Marek MUSIELA, BNP Paribas

Jean-Michel LASRY, Calyon

Pierre-Louis LIONS, Collège de France

PARALLEL SESSIONS

ROUND TABLE

POSTER SESSION** 1 (see last page)

“Crisis and Risk Management : The View Point of Market Professionals”

Pierre CAILLETEAU, Moody’s Michel CROUHY, NATIXIS Jean-François DANDE, KPMG

Farhoud MOADDEL, Fitch SolutionsMarek MUSIELA, BNP ParibasFrench Central Bank*

Panel Session : “Financial Markets and Science - New Challenges”

Chairman: Nizar TOUZI, Polytechnic School

“ Pricing of Defaultable Securities in a Multi-Factor Quadratic Gaussian Model”

Samson ASSEFA, University of Technology, Sydney

“Modelling of Successive Defaults” Ying JIAO, Paris VII University, Nicole EL-KAROUI, Paris VI University and Polytechnic School, Monique JEANBLANC, Evry University

Discussant: Caroline HILLAIRET, Polytechnic School

Chairman: Boris LEBLANC, BNP Paribas

“ Credit Risk Discovery in the Stock and CDS Market: Who, When and Why Leads? ”

Lidija LOVRETA, Santiago FORTE, Ramon Llull University

“ Modeling Default and Prepayment using Lévy Processes: an Application to Asset Backed Securities”

Henrik JÖNSSON, Technical University Eindhoven, Wim SCHOUTENS, Geert Van Damme, K.U.Leuven University

Discussant: Vivien BRUNEL, Société Générale

LARGE RISK in INSURANCE

Research Chair AXA/FdR

REGISTRATION

COFFEE BREAK

PARALLEL SESSIONS

PARALLEL SESSIONS

Parallel session 11 : Systematic Risk Parallel session12 : Liquidity and Security Design

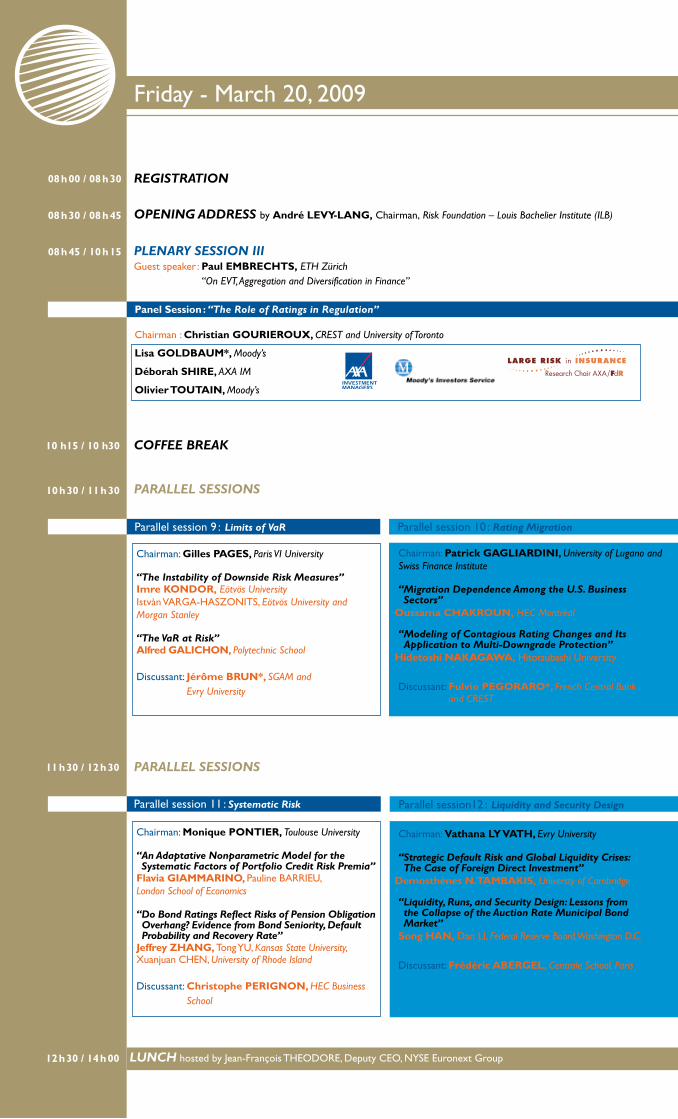

OPENING ADDRESS by André LEVY-LANG, Chairman, Risk Foundation – Louis Bachelier Institute (ILB)

PLENARY SESSION III Guest speaker : Paul EMBRECHTS, ETH Zürich

“On EVT, Aggregation and Diversification in Finance”

Panel Session : “The Role of Ratings in Regulation”

Chairman : Christian GOURIEROUX, CREST and University of Toronto

Lisa GOLDBAUM*, Moody’s

Déborah SHIRE, AXA IM

Olivier TOUTAIN, Moody’s

Friday - March 20, 2009

Parallel session 9 : Limits of VaR Parallel session 10 : Rating Migration

08 h 45 / 10 h 15

08 h 00 / 08 h 30

08 h 30 / 08 h 45

10 h15 / 10 h30

10 h 30 / 11 h 30

11 h 30 / 12 h 30

12 h 30 / 14 h 00 LUNCH hosted by Jean-François THEODORE, Deputy CEO, NYSE Euronext Group

Chairman: Gilles PAGES, Paris VI University

“ The Instability of Downside Risk Measures” Imre KONDOR, Eötvös University Istvàn VARGA-HASZONITS, Eötvös University and Morgan Stanley

“The VaR at Risk” Alfred GALICHON, Polytechnic School

Discussant: Jérôme BRUN*, SGAM and Evry University

Chairman: Monique PONTIER, Toulouse University

“ An Adaptative Nonparametric Model for the Systematic Factors of Portfolio Credit Risk Premia”

Flavia GIAMMARINO, Pauline BARRIEU, London School of Economics

“ Do Bond Ratings Reflect Risks of Pension Obligation Overhang? Evidence from Bond Seniority, Default Probability and Recovery Rate”

Jeffrey ZHANG, Tong YU, Kansas State University, Xuanjuan CHEN, University of Rhode Island

Discussant: Christophe PERIGNON, HEC Business School

Chairman: Patrick GAGLIARDINI, University of Lugano and Swiss Finance Institute

“ Migration Dependence Among the U.S. Business Sectors”

Oussama CHAKROUN, HEC Montréal

“ Modeling of Contagious Rating Changes and Its Application to Multi-Downgrade Protection”

Hidetoshi NAKAGAWA, Hitotsubashi University

Discussant: Fulvio PEGORARO*, French Central Bank and CREST

Chairman: Vathana LY VATH, Evry University

“ Strategic Default Risk and Global Liquidity Crises: The Case of Foreign Direct Investment”

Demosthènes N. TAMBAKIS, Universty of Cambridge

“ Liquidity, Runs, and Security Design: Lessons from the Collapse of the Auction Rate Municipal Bond Market”

Song HAN, Dan LI, Federal Reserve Board, Washington D.C.

Discussant: Frédéric ABERGEL, Centrale School, Paris

** To be confirmed** Poster sessions are effective means of conveying information. Poster’s visual aspects are combined with presenter’s verbal explanations.

Risk & Liquidityin the Industrial EconomyResearch Initiative

Risk & Liquidityin the Industrial EconomyResearch Initiative

PARALLEL SESSIONS

PARALLEL SESSIONS

POSTER SESSION** II (see last page)

Parallel session 13 : Interbank Market

Parallel session 15 : Bankruptcy and Regulatory Capital

Parallel session 14 : Equilibrium Models

Parallel session 16 : Monetary Policy

PLENARY SESSION IV Guest speaker : Roger GUESNERIE, Collège de France

Panel Session : “New Markets for Post-Crisis” Chairman : Jean-Michel LASRY, Calyon

Christophe BOURDILLON, Caisse des Dépôts et Consignations (CDC)

Philippe CHALMIN, Dauphine University

Vincent REMAY, NYSE Euronext

Hamid TAWFIKI, Avenir Global Investment Advisors

CLOSING ADDRESS by Arnaud de BRESSON, Managing Director, Europlace Institute of Finance (EIF)

COCKTAIL18 h 15 / 19 h 00

14 h 00 / 15 h 30

15 h 30 / 16 h 30

16 h 30 / 17 h 00

17 h 00 / 18 h 00

18 h 00 / 18 h 15

Chairman: Bruno BIAIS*, Toulouse University

“ Liquidity, Moral Hazard and Inter-Bank Market Collapse”

Enisse KHARROUBI, Edouard VIDON, French Central Bank

“Liquidity, Hoarding and Interbank Market Spreads: The Role of Counterparty Risk” Florian HEIDER, Marie HOEROVA, Cornelia HOLTHAUSEN, European Central Bank

Discussant: Nathalie PISTRE*, NATIXIS Asset Management

Chairman: Jean-Charles ROCHET*, Toulouse University

“ Financial Crises and Portfolio Allocation of Credit Risk Capital for Buy and Hold Investors”

Simone VAROTTO, Henley Business School, University of Reading

“Resolution of Financial Distress under Chapter 11” Amira ANNABI, Michèle BRETON, Pascal FRANCOIS, HEC Montréal

Discussant: Philippe PRIAULET, NATIXIS and Evry University

Chairman: Michel GUILLARD*, Evry University

“ Fear of Default and Volatility in a Dynamic Financial-Market Equilibrium”

Emilio OSAMBELA, Swiss Finance Institute and University of Lausanne

“ Heterogeneous Beliefs and the Vulnerability of Financial Innovation”

Hong YAN, University of South Carolina Weidong TIAN, University of North Carolina

Discussant: Bertrand VILLENEUVE, Tours University and CREST

Chairman: Sanvi AVOUYI-DOVI, French Central Bank

“ Systematic Risk, Banking Regulation and Optimal Monetary Policy”

Enrique MARTINEZ-GARCIA, Federal Reserve Bank of Dallas, Ethan COHEN-COLE, Federal Reserve Bank of Boston

“ Application of Stochastic Optimal Control to Financial Market Debt Crises”

Jérôme L. STEIN, Brown University

Discussant: Olivier de BANDT*, French Central Bank

16 h30 / 17 h 00

Poster Sessions 1 Thursday - March 19, 2009

Constant Proportion Portfolio Insurance Strategies for Credit Portfolios, Meng-Lan YUEH, Chenghi University

A Precursor of Market Crashes, Taisei KAIZOJI, International Christian University

Credit Spread Changes under Switching Regimes, Olfa MAALAOUI, Georges DIONNE, Pascal FRANCOIS, HEC Montréal

Real Effects of the 200-08 Financial Crisis around the World, Hui TONG, IMF, Shang-Jin WEI, Columbia University

Dynamic Correlation Hedging in Copula Models for Portfolio Selection, Denitsa STEFANOVA, Amsterdam University, Redouane ELKAMHI, University of Iowa

Competition Among Rating Agencies and Information Disclosure, Anastasia KARTASHEVA, Wharton School, Neil A. DOHERTY, University Of Pennsylvania, Richard D. PHILLIPS, Georgia State University

The Effect of CEO Stock Options on Bank Investment Choice, Borrowing, and Capital, Hamid MEHRAN, Joshua ROSENBERG, Federal Reserve Bank of New York

Sovereign Credit Risk with Endogenous Default, Alexandre JEANNERET, UCLA

A Closer Look at Credit Ratings for CDOs, Amal MOUSSA, Columbia University, Rama CONT, Paris VI University and CNRS

Bank Competition and Economic Stability: The Role of Monetary Policy, Sylvain CHAMPONNOIS, UCSD Rady School of Management

Explaining What Leads Up to Stock Market Crashes, Rossitsa YALAMOVA, University of Lethbridge, Bill McKELVEY, UCLA Anderson School of Management

Herd Induced By Uninformed Traders in Efficient Financial Markets, Gongyu CHEN, University of Cambridge, Gilles-Edouard ESPINOSA, Polytechnic School

Financial Liberalization and Banking Crises, Choudhry Tanveer SHEHZAD, Jakob de HAAN, University of Groningen

Credit Rating Agencies’Function on Bond Markets, Philippe RAIMBOURG, University Paris I, Jean-Noël ORY, Metz University

Sensitivity Analysis of Credit Risk Measures in the Beta Binomial Framework, Franck MORAUX, University of Rennes

Optimal Investment for Property-Liability Insurance Firms with an Actively Managed Economic Capital, Selim MANKAI, Catherine BRUNEAU, University Paris VIII

The Paris Financial Market in the 19th Century: An Efficient Multi-Polar Organization?, Pierre-Cyrille HAUTCOEUR, EHESS, Angelo RIVA, European Business School

Extracting Implied Correlation Matrices from Index Option Prices: A Statistical Approach, Romain DEGUEST, Columbia University, Rama CONT, Paris VI University and CNRS

A Microfounded Decomposition of Emerging Markets Sovereign Bond Spreads, Paula MARGARETIC, Toulouse University

Financial Integration, Liquidity and the Depth of Systematic Crises, Fabio FERIOZZI, Fabio CASTIGLIONESI, Guido LORENZONI, Tilburg University

How to Pay Incentives at A Bank?: The RAROC Approach, Dan GALAI, The Hebrew University

An Application to Credit Risk of Optimal Quantization Methods for Nonlinear Filtering, Callegaro GIORGIA, Evry University & Scuola Normale of Pisa

Jump Risk, Stock Returns, and Slope of Implied Volatility Smile, Shu YAN, University of South Carolina, Abass SAGNA, Paris VI University

Chairman : Bertrand VILLENEUVE, Tours University and CREST

Poster Session 1 Thursday - March 19, 2009

Common Versus Individual Pecularities of CEE Exchange Rate Volatility. Analytical Approach on the CEE Macroeconomic Volatility Drivers in the Context of the Actual Financial Crisis, Cristina-Maria TRIANDAFIL, National Bank of Romania, Peter BREZEANU, Academy of Economic Studies, Bucharest

Performance Analysis of Credit-Linked CPPI Portfolios, Meng-Lan YUEH, Chenghi University

Bid-Ask Spread Modelling: A Perturbation Approach, Simone SCOTTI, Turino University, Vathana LY VATH, Evry University

Threshold Copulas and Financial Contagion, Piotr JAWORSKI, Fabrizio DURANTE, University of Warsaw Institute of Mathematics

Counterparty Risk in Financial Contracts: Should the Insured Worry about the Insurer?, James THOMPSON, University of Waterloo

Market Discipline and Banking Supervision: The Role of Subordinated Debt, Isabelle DISTINGUIN, University of Limoges

Optimal Prepayment and Default Rules for Mortgage-Backed Securities, Tiziano VARGIOLU, Giulia de ROSSI, University of Padua

Securitization and the Intensity of Competition, Jung-Hyun AHN, Paris X University, Régis BRETON, University of Orléans

The Formation of Financial Networks, Ana BABUS, CFAP – University of Cambridge

The Age of Turbulence – Credit Derivatives Style, Hans BYSTRÖM, Lund University

From Default Rates to Default Matrices: An Application to Brazilian Consumer Credit, Ricardo SCHECHTMAN, Central Bank of Brazil

CDO Tranches: Measuring Impact on Economic Capital and Capital Allocation in Credit Portfolios, Yim LEE, Unicredit

Danger on the Exchange: Counterparty Risk on the Paris Exchange in the Nineteenth Century, Angelo RIVA, European Business School, Eugène N. WHITE, Rutgers University

Instability of Portfolio Optimization under Coherent Risk Measures, Istvan VARGA-HASZONITS, Morgan Stanley, Imre KONDOR, Collegium Budapest

Representation of Coherent Risk-Evaluating Processes, Eisele KARL-THEODOR, Strasbourg University

Where’s the Smoking Gun? A Study of Underwriting Standards for US Subprime Mortgages, Rajdeep SENGUPTA, Geetesh BHARDWAJ, Federal Reserve Bank of Saint-Louis

Modeling of CDO Options with Multi-Period Spread Dynamics, Jochen DORN, Paris I University, Yacine SADOUNI, Euro-VL / SGSS

A Tale of Two Platforms: Dealer Intermediation in the European Sovereign Bond Market, Michaël MOORE, Harvard, Peter DUNNE, Queens University, Belfast, Harald HAU, INSEAD and CEPR

Extension of Random Matrix Theory to the L-Moments for Robust Portfolio Allocation, Ghislain YANOU, Paris I University

Stock Market Integration in Emerging Countries: Further Evidence from the Philippines and Mexico, Fred JAWADI, Amiens School of Management, Mohamed El Hedi AROURI, University of Orléans and EDHEC

Poster Session 2 Friday - March 20, 2009

Chairman : Monique JEANBLANC, Evry University08 h 00 / 08 h 30

with the support of:

SPONSORS

Conc

ept &

Des

ign

: ww

w.p

aulm

orga

n.fr

- C

rédi

t pho

to :

Corb

is

PAVILLON ROYAL Route de Suresnes 75116 PARIS

On linePlease register by March 13, 2009

on the web site: www.finance-innovation.org/risk09/

Click on “Registration”

By faxPlease use the enclosed registration form and fax it to:

+33 (0)1 49 27 56 28

For further information:

By telephone+33 (0)1 49 27 56 49 / 13 71

contact : Rachel Curbinon

Registration

M

RER

RER

Rue Dufrénoy Rue

Spo

ntin

i

Route de Suresnes

Aven

ue Lo

uis B

arth

ouBo

ulev

ard

Lan

nes

Boul

evar

d F

land

rin

Rue

de

la F

aisa

nder

ie

Henri Martin

Avenue Foch

Université ParisDauphine

Avenue Victor Hugo

Rue de la Tour

Rue de Longchamp

Rue de la Muette à N

euilly

Avenue

AvenueFoch

PorteDauphine

AvenueHenri Martin

BOUL

EVAR

D

PÉRI

PHÉR

IQUE

Boul

evar

d L

anne

s

2nd InternationalFINANCIAL RESEARCH FORUM

INSTITUT LOUIS BACHELIERCENTRE D'INNOVATION FINANCIERE

LARGE RISK in INSURANCE

Research Chair AXA/FdR

Risk & Liquidityin the Industrial EconomyResearch Initiative

Risk & Liquidityin the Industrial EconomyResearch Initiative

![Risk Management (3C05/D22) Unit 3: Risk Management · 2004. 4. 29. · Risk-management planning Risk resolution [Boehm 1991] Risk monitoring Software risk management steps & techniques](https://img.pdfslide.net/doc/110x75/6122993708b35f7a264d6759/risk-management-3c05d22-unit-3-risk-2004-4-29-risk-management-planning.jpg)