Embed Size (px)

Citation preview

Risk Management in a Negative Interest Rate Environment

Martijn de Groot

Associate Director

Zanders

April 2015

2

The views expressed in the following material are the

author’s and do not necessarily represent the views of

the Global Association of Risk Professionals (GARP),

its Membership or its Management.

2

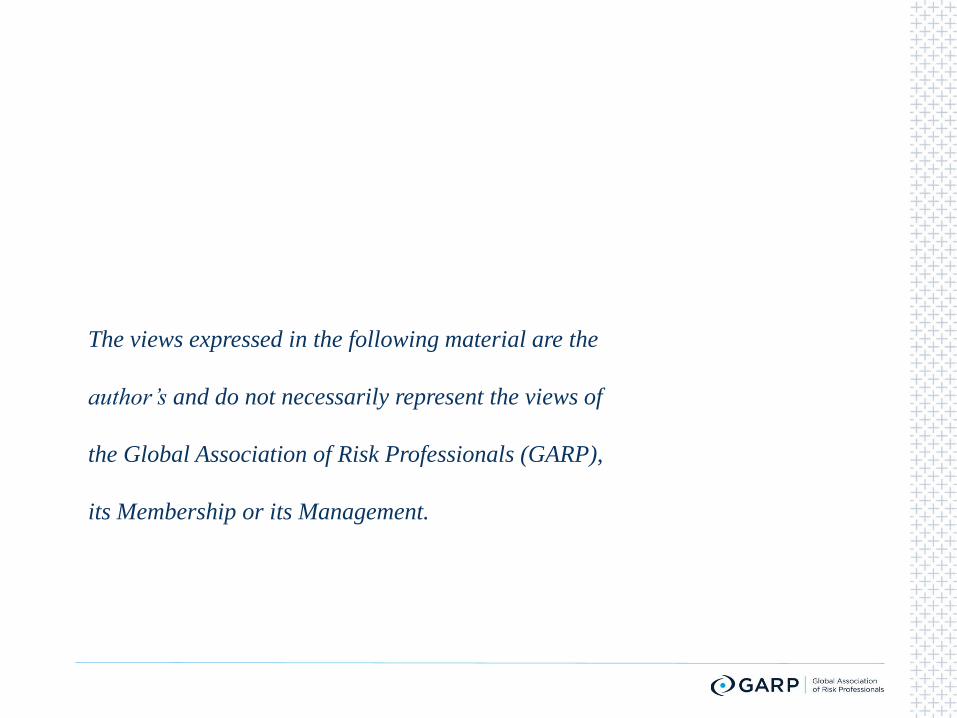

Conventional wisdom is that interest rate earned on investments are never less than zero because investors could alternatively hold cash.

‘Earning’ interest

-1

0

1

2

3

4

5

6

1-1

-20

07

1-6

-20

07

1-1

1-2

00

7

1-4

-20

08

1-9

-20

08

1-2

-20

09

1-7

-20

09

1-1

2-2

00

9

1-5

-20

10

1-1

0-2

01

0

1-3

-20

11

1-8

-20

11

1-1

-20

12

1-6

-20

12

1-1

1-2

01

2

1-4

-20

13

1-9

-20

13

1-2

-20

14

1-7

-20

14

1-1

2-2

01

4

EUR 1 month rate

3

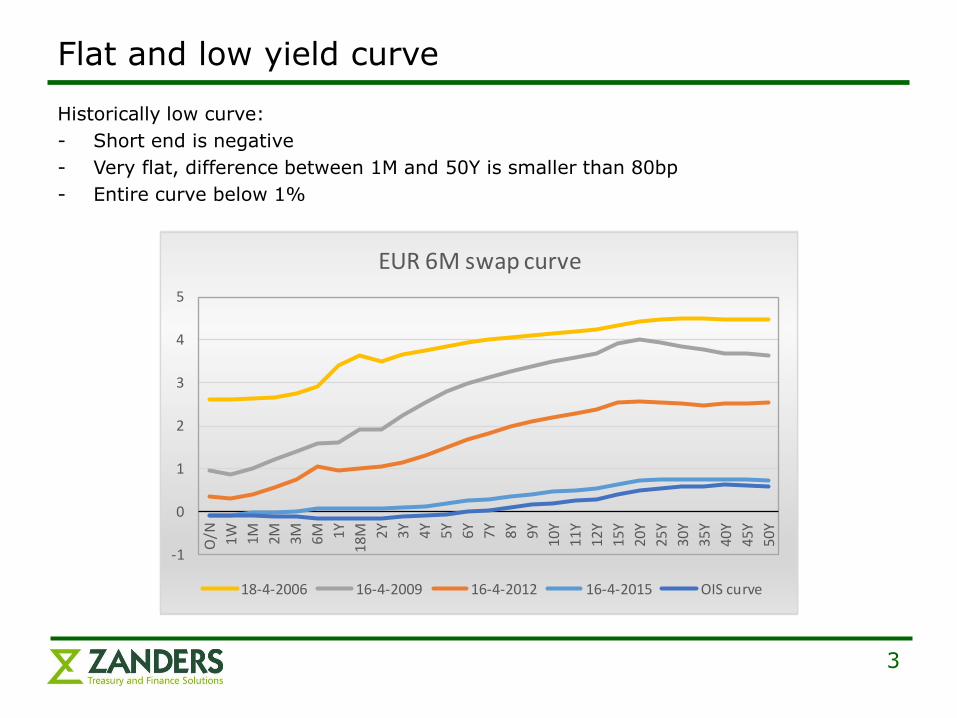

Historically low curve:

- Short end is negative

- Very flat, difference between 1M and 50Y is smaller than 80bp

- Entire curve below 1%

Flat and low yield curve

-1

0

1

2

3

4

5

O/N 1W 1M 2M 3M 6M 1Y

18M 2Y 3Y 4Y 5Y 6Y 7Y 8Y 9Y

10

Y

11

Y

12

Y

15

Y

20

Y

25

Y

30

Y

35

Y

40

Y

45

Y

50

Y

EUR 6M swap curve

18-4-2006 16-4-2009 16-4-2012 16-4-2015

-1

0

1

2

3

4

5

O/N 1W 1M 2M 3M 6M 1Y

18M 2Y 3Y 4Y 5Y 6Y 7Y 8Y 9Y

10Y

11Y

12Y

15Y

20Y

25Y

30Y

35Y

40Y

45Y

50Y

EUR 6M swap curve

18-4-2006 16-4-2009 16-4-2012 16-4-2015 OIS curve

4

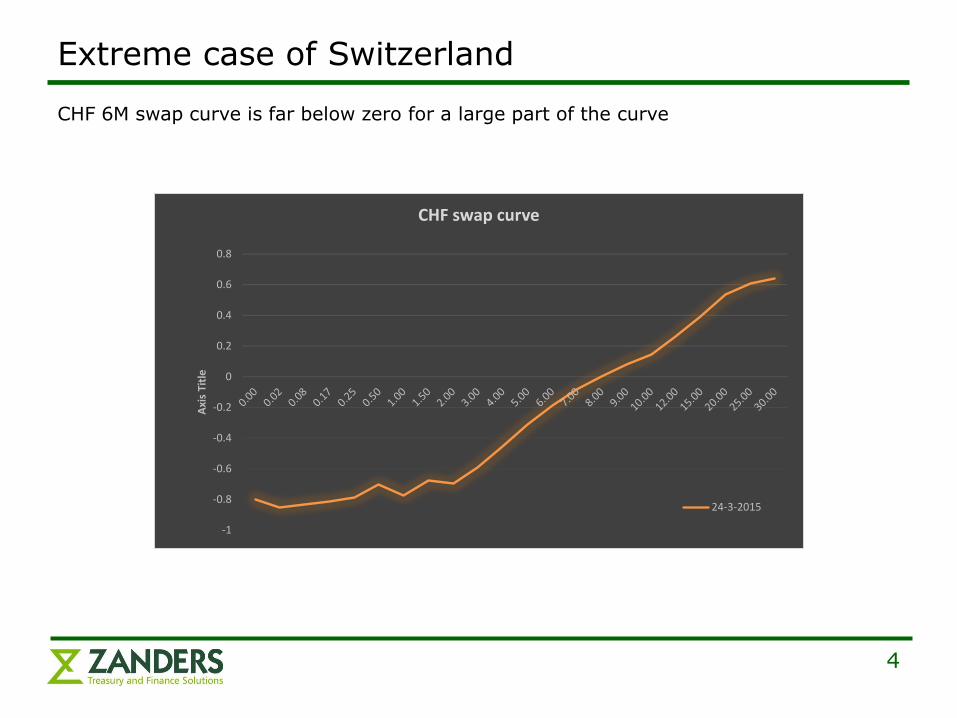

CHF 6M swap curve is far below zero for a large part of the curve

Extreme case of Switzerland

-1

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

Axi

s Ti

tle

CHF swap curve

24-3-2015

5

Question

Are negative interest rates bad for financial institutions?

6

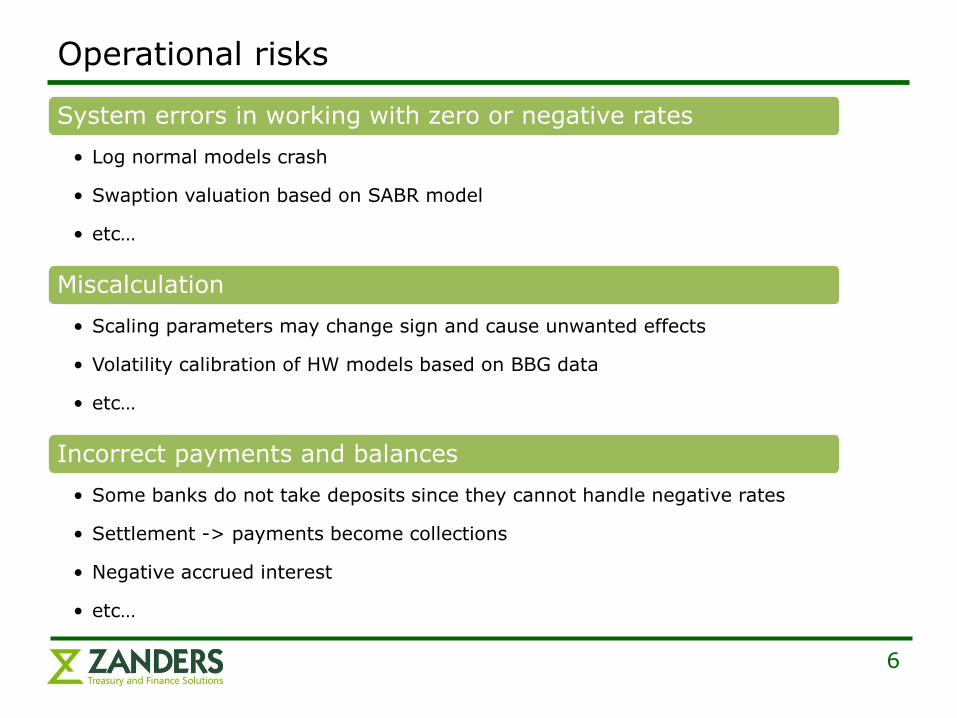

Operational risks

System errors in working with zero or negative rates

• Log normal models crash

• Swaption valuation based on SABR model

• etc…

Miscalculation

• Scaling parameters may change sign and cause unwanted effects

• Volatility calibration of HW models based on BBG data

• etc…

Incorrect payments and balances

• Some banks do not take deposits since they cannot handle negative rates

• Settlement -> payments become collections

• Negative accrued interest

• etc…

7

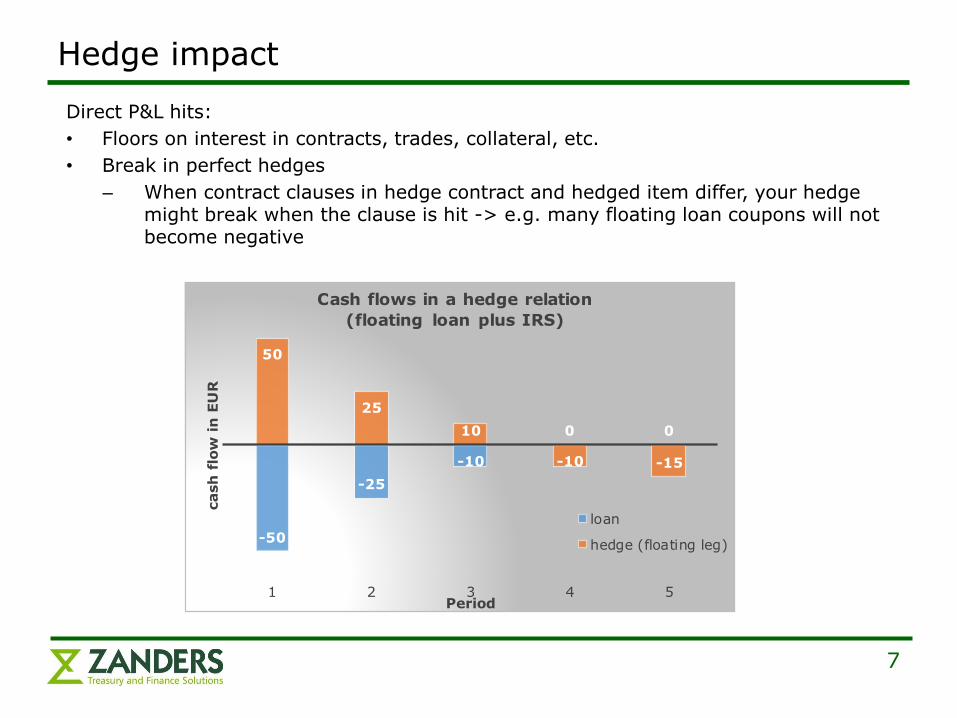

Direct P&L hits:

• Floors on interest in contracts, trades, collateral, etc.

• Break in perfect hedges

– When contract clauses in hedge contract and hedged item differ, your hedgemight break when the clause is hit -> e.g. many floating loan coupons will notbecome negative

Hedge impact

-50

-25

-10

0 0

50

25

10

-10 -15

1 2 3 4 5

cash f

low

in E

UR

Period

Cash flows in a hedge relation

(floating loan plus IRS)

loan

hedge (floating leg)

8

Question

Are negative interest rates bad for financial institutions?

Are negative interest rates bad for risk management?

9

Pension and life insurance

• Present value of future liabilities

• Coverage ratios are under pressure despite good recent asset returns

• Yield as high as the ultimate forward rate will probably not be made on high rated

bonds for many years ahead.

Client behaviour

• Cheap lending

• Mortgage redemptions

• Savings

Modelling interest rate scenarios

• Originally insignificant assumptions may have crucial impact in current market

situation

We are in uncharted waters

10

Rethink crucial assumptions

Suddenly risk managers should revisit some crucialassumptions:

1) Is there a floor in interest rates and2) do we model this in our risk management?

11

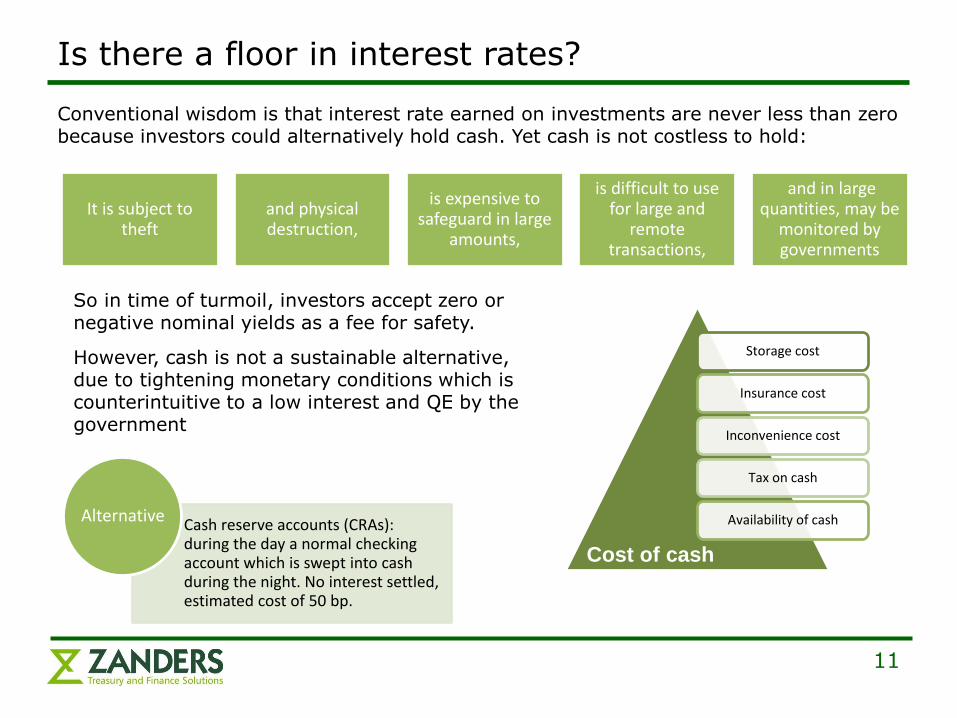

Conventional wisdom is that interest rate earned on investments are never less than zero because investors could alternatively hold cash. Yet cash is not costless to hold:

Is there a floor in interest rates?

It is subject to theft

and physical destruction,

is expensive to safeguard in large

amounts,

is difficult to use for large and

remote transactions,

and in large quantities, may be

monitored by governments

Storage cost

Insurance cost

Inconvenience cost

Tax on cash

Availability of cash

Cost of cash

So in time of turmoil, investors accept zero or negative nominal yields as a fee for safety.

However, cash is not a sustainable alternative, due to tightening monetary conditions which is counterintuitive to a low interest and QE by the government

Cash reserve accounts (CRAs): during the day a normal checking account which is swept into cash during the night. No interest settled, estimated cost of 50 bp.

Alternative

12

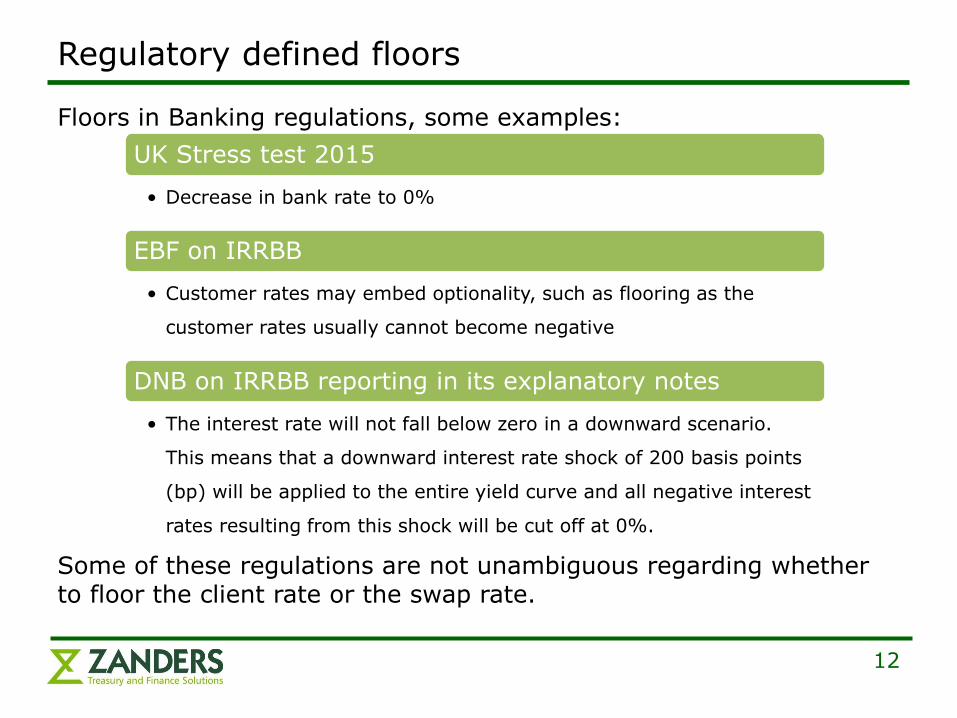

Floors in Banking regulations, some examples:

Some of these regulations are not unambiguous regarding whetherto floor the client rate or the swap rate.

Regulatory defined floors

UK Stress test 2015

• Decrease in bank rate to 0%

EBF on IRRBB

• Customer rates may embed optionality, such as flooring as the

customer rates usually cannot become negative

DNB on IRRBB reporting in its explanatory notes

• The interest rate will not fall below zero in a downward scenario.

This means that a downward interest rate shock of 200 basis points

(bp) will be applied to the entire yield curve and all negative interest

rates resulting from this shock will be cut off at 0%.

13

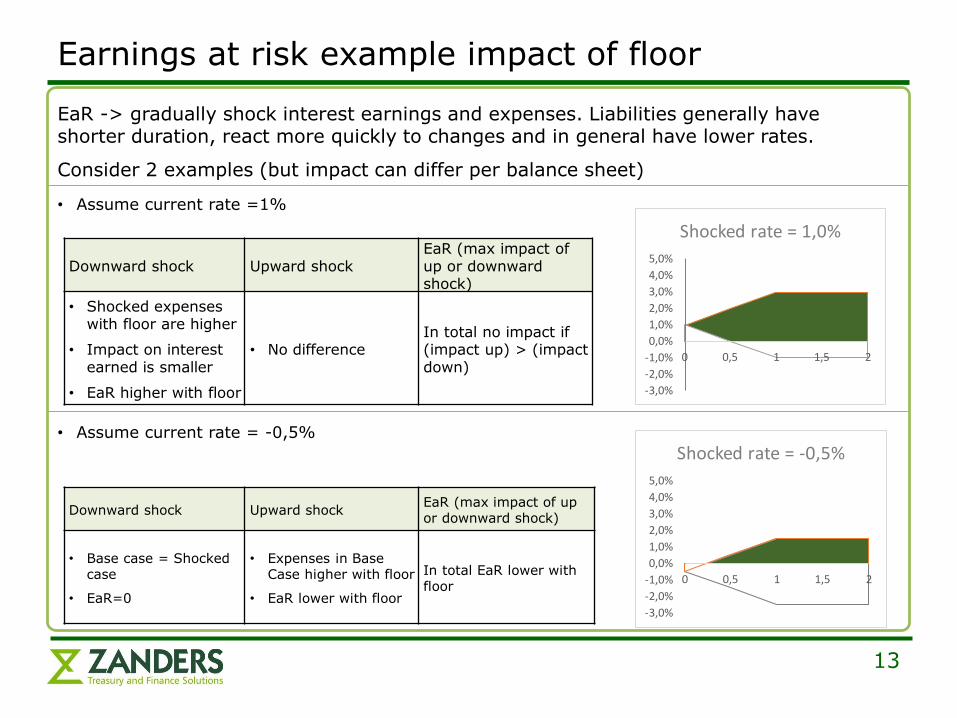

EaR -> gradually shock interest earnings and expenses. Liabilities generally have shorter duration, react more quickly to changes and in general have lower rates.

Consider 2 examples (but impact can differ per balance sheet)

• Assume current rate =1%

• Assume current rate = -0,5%

Downward shock Upward shockEaR (max impact of up or downward shock)

• Shocked expenses with floor are higher

• Impact on interest earned is smaller

• EaR higher with floor

• No differenceIn total no impact if (impact up) > (impact down)

Earnings at risk example impact of floor

Downward shock Upward shockEaR (max impact of up or downward shock)

• Base case = Shocked case

• EaR=0

• Expenses in Base Case higher with floor

• EaR lower with floor

In total EaR lower with floor

-3,0%

-2,0%

-1,0%

0,0%

1,0%

2,0%

3,0%

4,0%

5,0%

0 0,5 1 1,5 2

Shocked rate = 1,0%

-3,0%

-2,0%

-1,0%

0,0%

1,0%

2,0%

3,0%

4,0%

5,0%

0 0,5 1 1,5 2

Shocked rate = -0,5%

14

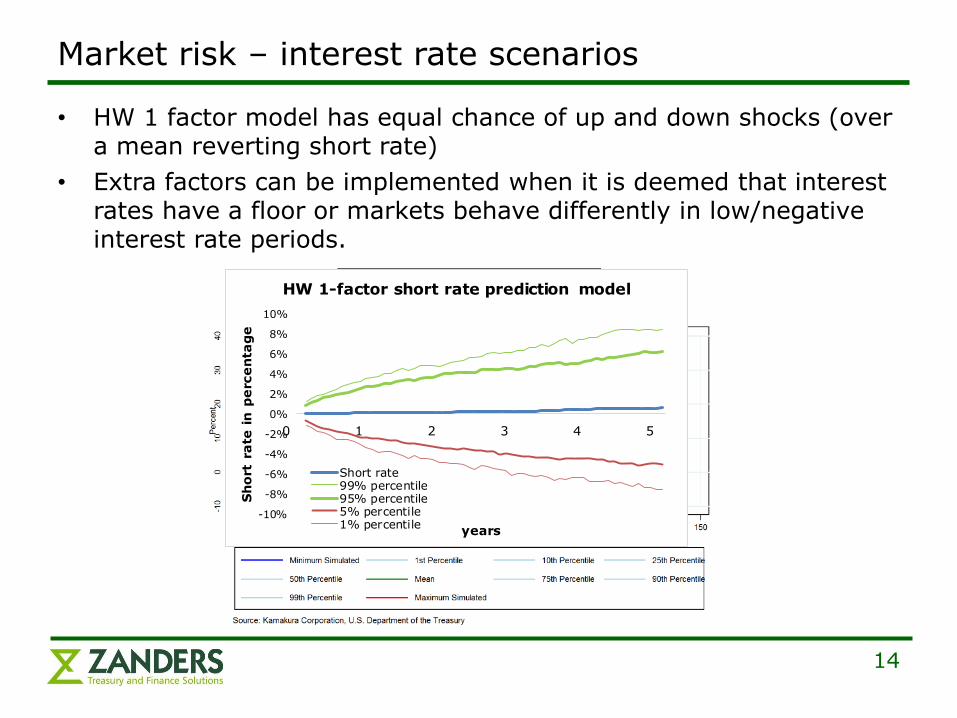

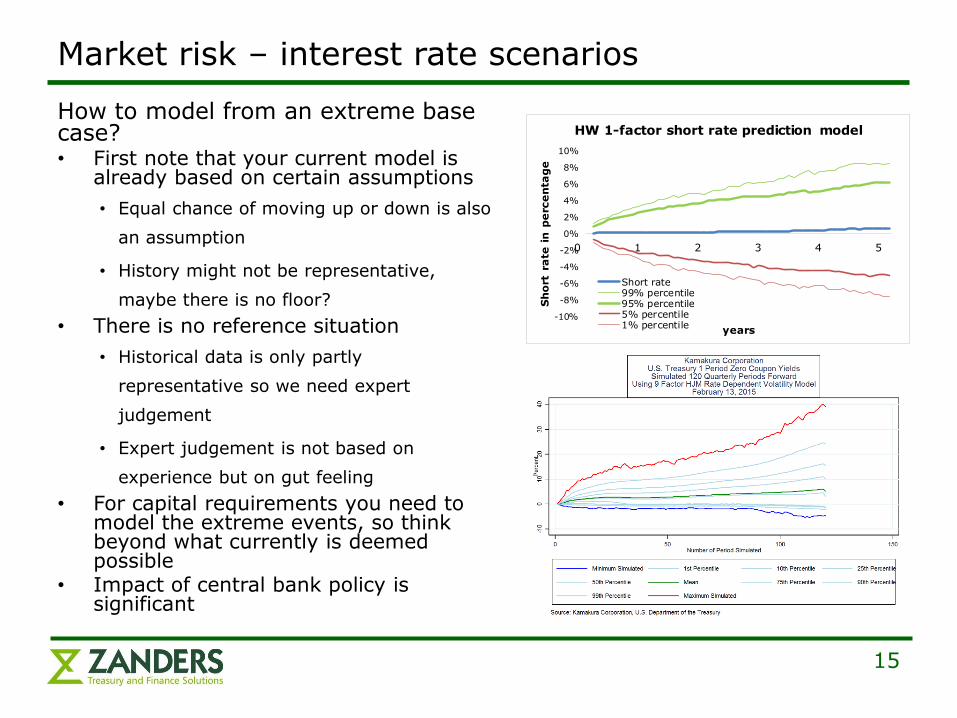

• Extra factors can be implemented when it is deemed that interest rates have a floor or markets behave differently in low/negative interest rate periods.

• HW 1 factor model has equal chance of up and down shocks (over a mean reverting short rate)

Market risk – interest rate scenarios

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

0 1 2 3 4 5

Sh

ort

ra

te i

n p

erc

en

tag

e

years

HW 1-factor short rate prediction model

Short rate99% percentile95% percentile5% percentile1% percentile

15

How to model from an extreme base case?• First note that your current model is

already based on certain assumptions

• Equal chance of moving up or down is also

an assumption

• History might not be representative,

maybe there is no floor?

• There is no reference situation

• Historical data is only partly

representative so we need expert

judgement

• Expert judgement is not based on

experience but on gut feeling

• For capital requirements you need tomodel the extreme events, so thinkbeyond what currently is deemedpossible

• Impact of central bank policy is significant

Market risk – interest rate scenarios

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

0 1 2 3 4 5

Sh

ort

ra

te i

n p

erc

en

tag

e

years

HW 1-factor short rate prediction model

Short rate99% percentile95% percentile5% percentile1% percentile

16

Conclusion

• We are in uncharted waters

• Market is currently pushing the ‘former’ floor in interest rates

• Maybe negative rates are not sustainable,

• But current interest rates are further decreasing

• No consensus on risk modelling, but:

– Be aware of possible operational risks

– Critically look at all floors implemented in your calculations

– Revisit crucial assumptions e.g. in client behaviour and interest rate scenarios