Embed Size (px)

Citation preview

Risk Management Report Pillar 3 - 1Q15

1

Risk Management Report - Pillar 3 – 1Q15

RISK MANAGEMENT REPORT PILLAR 3

BANCO DO BRASIL S.A.

1st Quarter 2015

2

Risk Management Report- Pillar 3 – 1Q15

Summary

1. OBJECTIVE ......................................................................................................................... 7 2. INTRODUCTION ................................................................................................................. 8 3. GOVERNANCE ................................................................................................................... 9

3.1 Relevant Risks ................................................................................................................ 9 3.2 Corporate Risk Governance ......................................................................................... 10 3.3 Risk Management Process ........................................................................................... 12 3.4 Reports .......................................................................................................................... 12

4. REGULATION ................................................................................................................... 13 4.1 Basel II .......................................................................................................................... 13

4.1.1 Pillar l - Minimum Capital Requirements .............................................................. 14 4.1.2 Pillar ll - Risk and Capital Supervisory Process ................................................... 14 4.1.3 Pillar lll – Transparency and Market Discipline .................................................... 15

4.2 Basel III ......................................................................................................................... 16 4.3 Basel I in Banco do Brasil ............................................................................................. 17

4.3.1 Market Risk ................................................................................................................... 17 4.3.2 Credit Risk ..................................................................................................................... 17 4.3.3 Operational Risk............................................................................................................ 18

5. PRUDENTIAL CONGLOMERATE .................................................................................... 19 5.1 BALANCE SHEETS .......................................................................................................... 19

5.2 Composition of the Prudential Conglomerate ............................................................... 23 5.3 Composition of the Economic and Financial Consolidation .......................................... 23

6. RISK MANAGEMENT ....................................................................................................... 25 6.1 Credit Risk ..................................................................................................................... 25

6.1.1 Management Objectives ............................................................................................... 25 6.1.2 Credit Policy .................................................................................................................. 27 6.1.3 Management Strategies ................................................................................................ 27 6.1.4 Management Processes ............................................................................................... 28 6.1.5 Communication and Information Processes ................................................................. 29 6.1.5.1 Communication process for internal clients ......................................................... 29 6.1.5.2 Communication process for external clients ........................................................ 30 6.1.6 Measurement Systems ................................................................................................. 30 6.1.6.1 Concentration ....................................................................................................... 30 6.1.6.2 Regulatory Capital Requirement .......................................................................... 30 6.1.7 Mitigation Policy ............................................................................................................ 31 6.1.8 Processes for Monitoring the Effectiveness of Mitigators ............................................. 31 6.1.9 Exposure to Credit Risk ................................................................................................ 31 6.1.10 Acquisition, Sale or Transfer of Financial Assets ................................................. 44 6.1.11 Securities (TVM) operations derived from securitization processes .................... 44 6.1.12 Exposure to counterparty credit risks ................................................................... 45 6.1.13 Mitigating instruments .......................................................................................... 48

6.2 Market and Liquidity Risks ............................................................................................ 50 6.2.1 Management Objectives ............................................................................................... 50 6.2.2 Management Policies and Strategies ........................................................................... 50 6.2.3 Hedge Policies .............................................................................................................. 53 6.2.4 Risk measuring systems and communication and information processes ................... 53 6.2.5 Market Risk Management Structure ............................................................................. 55 6.2.6 Market Risk Management Process ............................................................................... 57 6.2.7 Negotiable Portfolios ..................................................................................................... 59 6.2.8 Non-negotiable Portfolios .............................................................................................. 61 6.2.9 Liquidity Risk Management Structure ........................................................................... 63 6.2.10 Liquidity Risk Management Process .................................................................... 65

6.3 Operational Risk............................................................................................................ 67 6.3.1 Management Objectives ............................................................................................... 67 6.3.2 Operational Risk Policy ................................................................................................. 68 6.3.3 Management Processes and Strategies ....................................................................... 68 6.3.4 Communication and Information Processes ................................................................. 69 6.3.5 Measurement Systems ................................................................................................. 69

3

Risk Management Report- Pillar 3 – 1Q15

6.3.6 Operational Risk Mitigation ........................................................................................... 70 6.3.7 Control of Operational Risk ........................................................................................... 70 6.3.8 Banco do Brasil Related Entities ................................................................................... 71

6.4 Strategy Risk ................................................................................................................. 71 6.4.1 Management Objectives ............................................................................................... 71 6.4.2 Management Model ...................................................................................................... 72 6.4.3 Management Structure ................................................................................................. 72 6.4.4 Management Processes ............................................................................................... 73 6.4.5 Information and Communication Processes ................................................................. 74

6.5 Reputational Risk .......................................................................................................... 74 6.5.1 Management Objectives ............................................................................................... 74 6.5.2 Management Model ...................................................................................................... 74 6.5.3 Management Structure ................................................................................................. 75 6.5.4 Management Processes ............................................................................................... 76 6.5.5 Information and Communication Processes ................................................................. 76

6.6 Environmental Risk ....................................................................................................... 76 6.6.1 Management Objectives ............................................................................................... 76 6.6.2 Management Model ...................................................................................................... 77 6.6.3 Management Structure ................................................................................................. 77 6.6.4 Management Processes ............................................................................................... 78 6.6.5 Environmental Responsibility Policy ............................................................................. 78 6.6.6 Information and Communication Processes ................................................................. 78 6.6.7 Shareholdings ............................................................................................................... 78

7 CAPITAL ............................................................................................................................ 81 7.1 Capital Management ..................................................................................................... 81 7.2 Referential Equity (RE) Details ..................................................................................... 83 7.3 Prudential Adjustments deducted from CET1: .............................................................. 84 7.4 Minimum Reference Equity Required (MRER) ............................................................. 85 7.5 Capital Adequacy Ratio ................................................................................................ 87 7.6 Assessment of Sufficiency and Adequacy of Reference Equity (PR)........................... 87

4

Risk Management Report- Pillar 3 – 1Q15

List of Tables

Table 1 – Capital Minimum Requirement in relation to RWA: ........................................................ 17 Table 2 - Prudential Balance Sheet x Consolidated Balance Sheet: ............................................. 20 Table 3 - Composition of the Prudential Conglomerate ................................................................. 23 Table 4 - Composition of the Economic and Financial Consolidation: ........................................... 24 Table 5 - Concentration of the ten and of the hundred largest customers in relation to the total of transactions with credit granting feature ........................................................................................ 32 Table 6 - Credit risk average exposure .......................................................................................... 32 Table 7 - PJ credit risk exposure by geographic regions ............................................................... 33 Table 8 - PF credit risk exposure by geographic regions ............................................................... 34 Table 9 - Credit risk exposure of the financial conglomerate, by economic sector ........................ 35 Table 10 - Credit risk exposure of the agribusiness portfolio, segregated by economic sector and businesses portfolio (PJ) – 1Q15 ................................................................................................... 36 Table 11 - Credit risk exposure of the agribusiness portfolio, segregated by economic sector and businesses portfolio (PJ) – 4Q14 ................................................................................................... 36 Table 12 - Credit risk exposure of the agribusiness portfolio, segregated by economic sector and businesses portfolio (PJ) – 3Q14 ................................................................................................... 37 Table 13 - Credit risk exposure of PF and PJ portfolios by maturity of the transactions – 1Q15 .. 37 Table 14 - Credit risk exposure of PF and PJ portfolios by maturity of the transactions – 4Q14 .. 38 Table 15 - Credit risk exposure of PF and PJ portfolios by maturity of the transactions – 3Q14 .. 38 Table 16 - Amount of overdue transactions by geographical regions. ........................................... 39 Table 17 - Amount of overdue transactions, segregated by economic sector – 1Q15 .................. 40 Table 18 - Amount of overdue transactions, segregated by economic sector – 4Q14 .................. 41 Table 19 - Amount of overdue transactions, segregated by economic sector – 3Q14 .................. 41 Table 20 – Write-off transactions by economic sector. .................................................................. 42 Table 21 - Total allowances for loan and lease losses in the quarter and variations .................... 43 Table 22 - Credit risk exposure by FPR ......................................................................................... 43 Table 23 - Loss operations assigned, with substantial transfer of risks and benefits .................... 44 Table 24 - Value of the portfolio granted with co-obligation, recorded in the off balance sheet .... 44 Table 25 - Value of the exposures derived from acquiring FIDC and CRI ..................................... 45 Table 26 - Notional value of contracts to be liquidated in clearing house liquidation systems, in which the clearing house acts as central counterparty .................................................................. 47 Table 27 - Notional value of contracts subject to counterparty credit risk in which clearing houses do not act as central counterparty, Segmented in uncollateralized agreements and collateralized agreements. ............................................................................................................. 47 Table 28 - Positive gross value of the respective contracts, including derivatives, loans to settle, assets loans and repurchase agreements, disregarded the positive values related to compensation agreements defined in CMN Resolution 3,263/05. ................................................. 47 Table 29 - The value of collaterals that cumulatively meet the requirements of paragraph VII, Art.9, of Bacen Circular 3,678/13 ................................................................................................... 48 Table 30 - The value of collaterals that cumulatively meet the requirements of paragraph VII, Art.9, of Bacen Circular 3,678/13: .................................................................................................. 48 Table 31 - Collateral coverage. ...................................................................................................... 49 Table 32 - Mitigated value of exposure, weighted by the respective weighting factor ................... 50 Table 33 - Derivative financial instruments in the country and abroad, by market risk factor, with and without a central counterpart – 1Q15 ...................................................................................... 51 Table 34 - Derivative financial instruments in the country and abroad, by market risk factor, with and without a central counterpart – 4Q14 ...................................................................................... 52

5

Risk Management Report- Pillar 3 – 1Q15

Table 35 - Derivative financial instruments in the country and abroad, by market risk factor, with and without a central counterpart – 3Q14 ...................................................................................... 52 Table 36 - Derivative financial instruments in the country and abroad, by market risk factor, with and without a central counterpart – 2Q14 ...................................................................................... 52 Table 37 - Derivative financial instruments in the country and abroad, by market risk factor, with and without a central counterpart – 1Q14 ...................................................................................... 53 Table 38 - Negotiable Portfolio by relevant market risk factor, divided into positions purchased and positions sold. .......................................................................................................................... 61 Table 39 - Impact on the result or on the assessment of the value of the institution due to shocks in interest rates segmented by risk factor – Value at Risk methodology ....................................... 63 Table 40 – Impact on the result or on the assessment of the institution value due to the shocks in interest rates, segmented by risk factor – Economic Value of Equity methodology ...................... 63 Table 41 - Phases of the operational risk management process ................................................... 68 Table 42 - Operational losses monitoring by loss events category................................................ 71 Table 43 - Strategy risk management activities ............................................................................. 71 Table 44 - Reputational Risk management activities ..................................................................... 74 Table 45 – Equity Interests – Non Negotiable Portfolio ................................................................. 80 Table 46 - Reference Equity (RE) Details ...................................................................................... 84 Table 47 – Prudential Adjustments ................................................................................................ 85 Table 48 – Required Minimum Reference Equity .......................................................................... 86 Table 49 – Basel Ratio (Total Capital Ratio) and PR margin ......................................................... 87 Table 50 - Criteria and parameters for classification of the capital condition ................................ 88

6

Risk Management Report- Pillar 3 – 1Q15

List of Figures Figure 1 – Risk Management Governance Structure .................................................................. 11

Figure 2 - Risk Management Structure and Process .................................................................. 12

Figure 3 - Basel II Pillars ............................................................................................................. 13

Figure 4 - Capital allocation Models ............................................................................................ 14

Figure 5 - Pillar III Structure ........................................................................................................ 16

Figure 6 – Credit risk management ............................................................................................. 25

Figure 7 - Credit risk management structure ............................................................................... 29

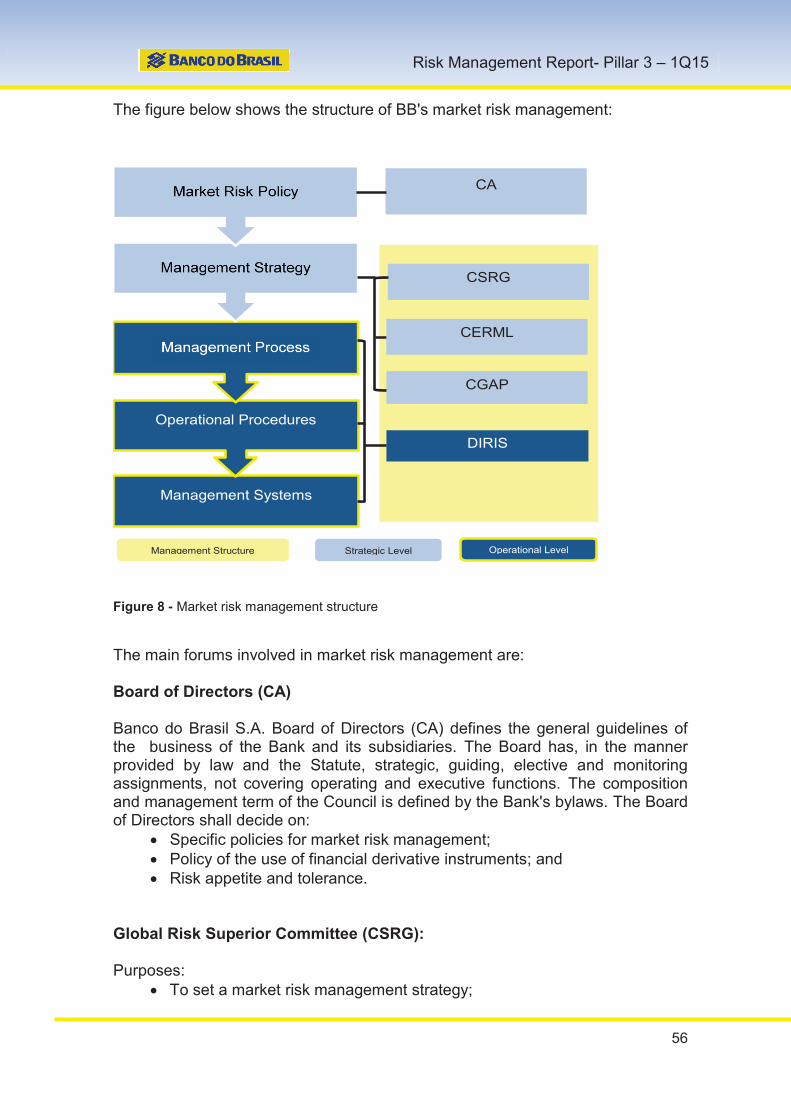

Figure 8 - Market risk management structure ............................................................................. 56

Figure 9 - Management Process ................................................................................................. 59

Figure 10 - Liquidity Risk Management ....................................................................................... 64

Figure 11 – Strategy Risk Management ...................................................................................... 73

Figure 12 – Reputational Risk Management ............................................................................... 76

Figure 13 – Organizational Structure involved in the capital and risk management ................... 81

7

Risk Management Report- Pillar 3 – 1Q15

1. Objective

The purpose of this report is to inform the interested public about Banco do Brasil`s risk management structures, processes and policies, aligned with Basel ll Pillar lll guidelines, including information related to risk and capital management, the calculation of the amount of Risk Weighted Assets (RWA) and the Reference Equity (PR). The calculation of PR and RWA considers the consolidation scope of the Financial Conglomerate until 12.31.2014, and, as of 01.01.2015, according to the CMN Resolutions 4,192/13 and 4,193/13, of the Prudential Conglomerate1, in accordance with the Financial Institutions Chart of Accounts (Cosif), which covers not only financial institutions, but also consortium managing companies, payment institutions, companies that acquire operations or that direct or indirectly have credit risk and investment funds in which the conglomerate considerably holds risks and benefits.

1 Prudential Regulation Details on the link: http://www.bcb.gov.br/?REGPRUDENCIAL

8

Risk Management Report- Pillar 3 – 1Q15

2. Introduction

Banking system sustainability is indissolubly linked to risk-management and capital policies and mechanisms. The methods of identifying, assessing, controlling, mitigating and monitoring risk safeguard financial institutions in adverse situations and provide support for positive, recurring earnings over time. BB considers essential risk and capital management to the process of decision-making, providing greater stability, better capital allocation and optimization of risk-return ratio. Brazil’s participation in the Basel Committee on Banking Supervision encourages broader, timelier adoption of international prudential standards. Changes in the global financial environment, such as market integration through globalization, the emergence of new transactions and products, increasing technological sophistication, and new regulations, have made financial activities and processes - and their risks – more and more complex. Additionally, the lessons learned from financial disasters reinforce the main need for risk management in the banking industry. Those factors have influenced regulatory agencies and financial institutions to invest in risk management, seeking to strengthen their financial health. In concert with that outlook, BB has invested in the continual improvement of its risk-management process and practices, in line with international market benchmarks, Basel ll Accord and adjustments made by Basel lll Accord. Banco do Brasil remains continuously aligned with the best management practices, among which, the risk management architecture with multidimensional scope whose specificities are described in this report.

9

Risk Management Report- Pillar 3 – 1Q15

3. Governance

3.1 Relevant Risks

Banco do Brasil has a process of identification of risks that will be part of the risks inventory and for the definition of relevant risks. That process is quite important for the risks and capital management, as well as for the business management, since it seeks to identify which risks should be managed by the Institution. The identification of the risks incurred by the Institution is made through the analysis of the business segments that are explored, direct and indirectly, considering the Entities Related to Banco do Brasil.

After the definition of the risks inventory and its corresponding concepts, comes the classification of risks according to their relevance, which is made through a quantitative or qualitative assessment. The quantitative assessment is used for the risks that can be measured. The qualitative assessment is applied for those risks that can`t be measured due to the absence of a methodology or data base. The risks below are part of Banco do Brasil`s Financial Conglomerate Relevant Risks Corporate Range:

Market Risk – defined as a possibility of losses resulting from the the fluctuation of market values of positions held by a financial institution. It includes the risks of the operations that are subject to the variations of exchange, interest rates, share prices and the price of commodities. Liquidity Risk – possibility of imbalances between tradable assets and liabilities - "mismatches" between payments and receipts - which can affect the institution’s payment ability, taking into account the different currencies and settlement terms of its rights and obligations. Banking Book Interest Rate Risk – defined as the risk related to the exposure subject to the variation of the interest rates of the exposures that are not classified in the trading portfolio (Trading Book). Credit Risk – possibility of losses associated with the non-fulfillment by a borrower or a counterparty of their respective financial obligations according to negotiated terms, the devaluation of a loan agreement due to a drop in the borrower’s risk rating, a decline in gains or earnings, benefits granted in renegotiation, and recovery costs. Counterparty Credit Risk – it is a subcategory of credit risk that is understood as a possibility of a certain counterparty not fulfilling its obligations related to settlement of transactions that involve trading financial assets, including those related to the settlement of financial derivatives.

10

Risk Management Report- Pillar 3 – 1Q15

Credit Concentration Risk – it is also a subcategory of credit risk and it is defined as a possibility of credit losses arising from significant exposure to counterparty, a risk factor or groups of counterparties related by common characteristics. Operational Risk – possibility of losses due to failures, deficiencies, or improper internal processes, people and systems or external events. This includes the possibility of losses arising from legal risk. Strategy Risk – possibility of losses arising from adverse changes in the business environment, or use of inappropriate assumptions in decision making. Reputational Risk – possibility of negative perception about the Institution on the part of customers, counterparties, shareholders, investors, government agencies, community or supervisors that can adversely affect the sustainability of the business. Environmental Risk – possibility of losses arising directly or indirectly from: i) social and environmental impacts resulting from administrative and business practices of BB, or people related to its operation; and ii) adverse impacts on the Bank’s operations resulting from conjectural aspects related to social and environmental unsustainability of the modes of production and the existing consumption patterns. Legal Risk - possibility of losses associated with improper or deficient contracts signed by the Institution, as well as sanctions resulting from noncompliance with legal provisions and compensation for damages to third parties resulting from activities engaged in by the institution. Participations Risk – possibility of losses resulting from exposures in the societal participations. Complementary Pension Fund Entities and Private Health Insurance Plan Operators for Employees Risk – possibility of negative impacts derived from exposures registered in the entities sponsored by complementary pension fund and private health insurance plan operators for employees. Model Risk – possibility of losses derived from the inadequate development or use of models, as a result of the inaccuracy or insufficiency of data or the incorrect formulation in its construction.

3.2 Corporate Risk Governance

The risk-governance model adopted by BB involves a superior committee and executive committee structure, with the participation of many units at the Bank, addressing the following issues:

a) separation of duties: business versus risk; b) specific structure for risk management; c) defined management process;

11

Risk Management Report- Pillar 3 – 1Q15

d) decisions in several hierarchical levels; e) clear rules and authority structure; and f) reference to best management practices.

In December/14, the Executive Board approved the reconfiguration of strategic governance bodies. The new setting for the committees related to risk management shall be:

· Credit Risk Executive Committee (CERC); · Market and Liquidity Executive Committee (CERML); · Internal Controls and Operational Risk Executive Committee (CERO); · Global Risk Superior Committee (CSRG).

The figure below represents the governance structure of the Bank’s risk management:

Figure 1 – Risk Management Governance Structure

All decisions related to risk management are made jointly and in accordance with BB’s guidelines and rules. Banco do Brasil’s risk governance is centralized in the Global Risk Superior Committee (CSRG), composed by members of the Executive Board of Directors, whose main purpose is to establish strategies for risk management, appropriate overall risk-exposure limits to capital allocation in light of risks. The Risk Management Board (DIRIS) is responsible for managing credit, market and liquidity risks and the Operational Risk Unit (URO) is responsible for managing the operational risk. These structures are linked to the Office of the Vice-President for Internal Controls and Risk Management, which foster synergy among processes and contribute to a better capital allocation.

12

Risk Management Report- Pillar 3 – 1Q15

The figure below demonstrates the decision-making flow of topics related to risk management:

Figure 2 - Risk Management Structure and Process

Decisions are reported to participating units through documents that objectively express the position taken by the Senior Management, guaranteeing application throughout the Bank. 3.3 Risk Management Process The risk-management process involves a continuous flow of information, abiding by the following phases:

a) Planning: data gathering and analysis phase and preparation of proposals; b) Decision: proposals are assessed and debated in a collegiate way, in

competent levels and communicated to participating areas; c) Execution: the participating units implement the decisions made; and d) Monitoring: checking on the implementation of the resolutions and report to

Executive Committees and CSRG. 3.4 Reports

Risk-management reports support decision-making processes about risk in the Executive Committees, the Global Risk Superior Committee (CSRG), the Executive Board of Directors (CD), and the Board of Directors (CA). The reports produced periodically have managerial qualitative and quantitative information and subsidize the dissemination of information to the market, as the Management Report and the Performance Analysis Report.

13

Risk Management Report- Pillar 3 – 1Q15

4. Regulation

4.1 Basel II

In June 2004, the Basel Committee on Banking Supervision published a document, commonly known as Basel II, with the following objectives:

a) promote financial stability; b) strengthen the capital structure of institutions; c) favor the adoption of best risk-management practices; and d) encourage greater transparency and market discipline.

Basel II proposes a more comprehensive approach in terms of strengthening banking supervision and stimulating greater transparency in disclosing information to the market, based on three major premises:

a) Pillar I - capital requirement for the coverage of credit, market and operational risks;

b) Pillar II - risks and capital supervision; and c) Pillar III - information transparency and market discipline.

The figure 3 represents the Pillars of Basel II:

Figure 3 - Basel II Pillars

14

Risk Management Report- Pillar 3 – 1Q15

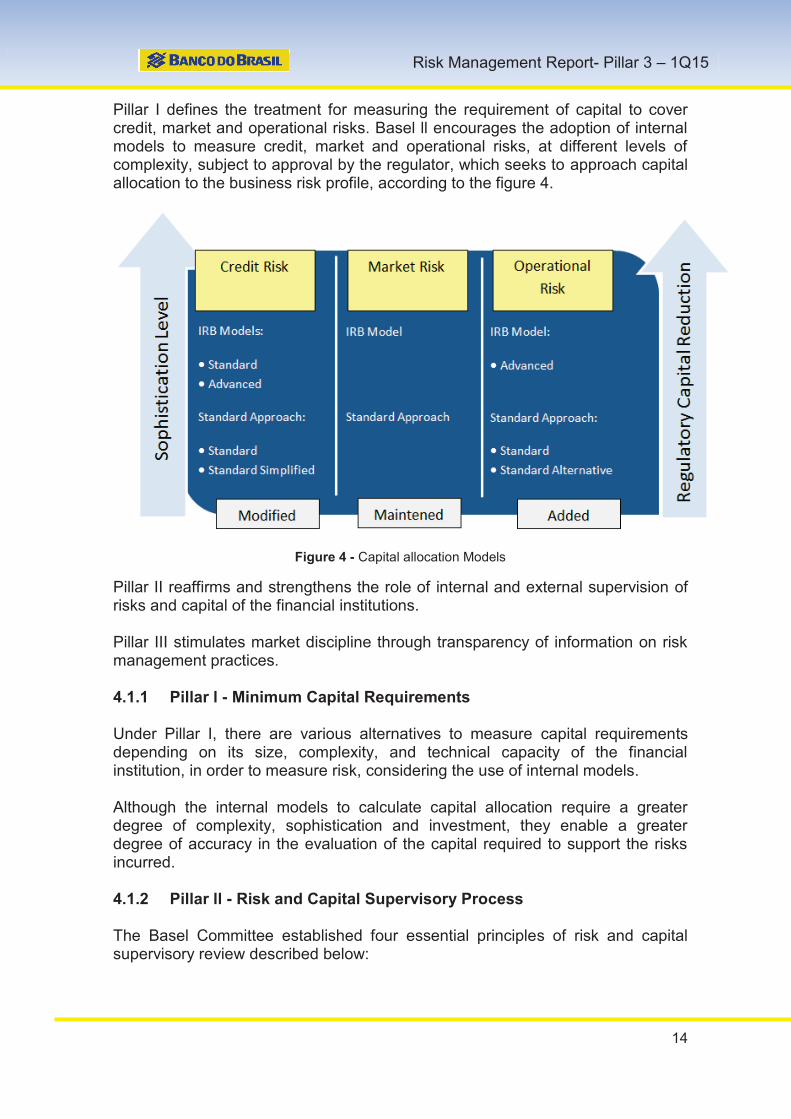

Pillar I defines the treatment for measuring the requirement of capital to cover credit, market and operational risks. Basel ll encourages the adoption of internal models to measure credit, market and operational risks, at different levels of complexity, subject to approval by the regulator, which seeks to approach capital allocation to the business risk profile, according to the figure 4.

Figure 4 - Capital allocation Models

Pillar II reaffirms and strengthens the role of internal and external supervision of risks and capital of the financial institutions. Pillar III stimulates market discipline through transparency of information on risk management practices.

4.1.1 Pillar l - Minimum Capital Requirements Under Pillar I, there are various alternatives to measure capital requirements depending on its size, complexity, and technical capacity of the financial institution, in order to measure risk, considering the use of internal models. Although the internal models to calculate capital allocation require a greater degree of complexity, sophistication and investment, they enable a greater degree of accuracy in the evaluation of the capital required to support the risks incurred. 4.1.2 Pillar ll - Risk and Capital Supervisory Process The Basel Committee established four essential principles of risk and capital supervisory review described below:

15

Risk Management Report- Pillar 3 – 1Q15

1) First Principle: banks must have a process to assess their capital adequacy in relation to their risk profile and have a strategy to maintain adequate levels of capital to cover risks;

2) Second Principle: supervisors should evaluate the banks’ strategies, the

estimates of capital, and the ability of banks to monitor and to guarantee their compliance with minimum capital requirements. The supervisors must take adequate measures just in case they are not satisfied with the result of the process;

3) Third Principle: supervisors expect, and may require, banks to operate

above the minimum capital requirements; and 4) Fourth Principle: supervisors may intervene in advance and require

banks to take prompt actions if their capital level falls below the minimum level.

The main features that reflect a rigorous process to assess capital adequacy should involve:

a) supervision of the Bank’s Senior Management; b) solid assessment of capital needs to tolerate business risks; c) comprehensive assessment of risks; d) monitoring and reporting; and e) review of internal controls.

Pillar II emphasizes the need for a bank to have an adequate volume of capital to tolerate all risks involved in the business. Besides the capital, the regulator also assesses internal controls and capital and risk management processes, which must be sufficient and adequate.

4.1.3 Pillar lll – Transparency and Market Discipline By encouraging information disclosure, Basel II seeks to increase market players’ power of evaluation and action. The purpose of Pillar lll is to complement minimum capital requirements (Pillar I) and the supervisory review process (Pillar II), encouraging participants to exercise market discipline. To guarantee compliance with Pillar lll, Basel II requires supervisors to have a greater number of persuasive instruments, ranging from dialogue with the bank’s management to financial fines, depending on the disclosure deficiency that is shown. It represents the set of information-disclosure requirements which will allow market players to evaluate the essential information in the institution’s structure, capital measurements, risk exposure, risk-management processes, and capital adequacy.

16

Risk Management Report- Pillar 3 – 1Q15

Pillar III is based on four categories/divisions:

a) scope of application - represents the relationship between recommendations and the bank’s structure;

b) capital - demonstrates the bank’s ability to absorb eventual losses; c) risk exposure - displays forms and the risk assessment itself; and d) capital adequacy - enables the judgment of capital adequacy in light of risks

incurred. Figure 5 represents the structure of Pillar III:

Figure 5 - Pillar III Structure

4.2 Basel III On 1st March 2013, the Central Bank of Brazil (Bacen) published the Basel III rules related to the definition of capital and capital requirements. Some of the measures included in the Brazilian regulatory framework stand out:

a) definition of a new methodology for calculating regulatory capital, which increases the capacity to absorb losses and continues to be divided into Tiers I and II, being Tier I composed by the Core Capital and Additional Tier I Capital;

b) definition of a new methodology for calculating the capital requirement maintenance, adopting minimum requirements for Referential Equity, Tier I and Core Capital, and the introduction of the Additional Core Capital;

A gradual implementation of the capital requirement that extends from October 2013 to January 2019 was established, so the transition is made gradually and

17

Risk Management Report- Pillar 3 – 1Q15

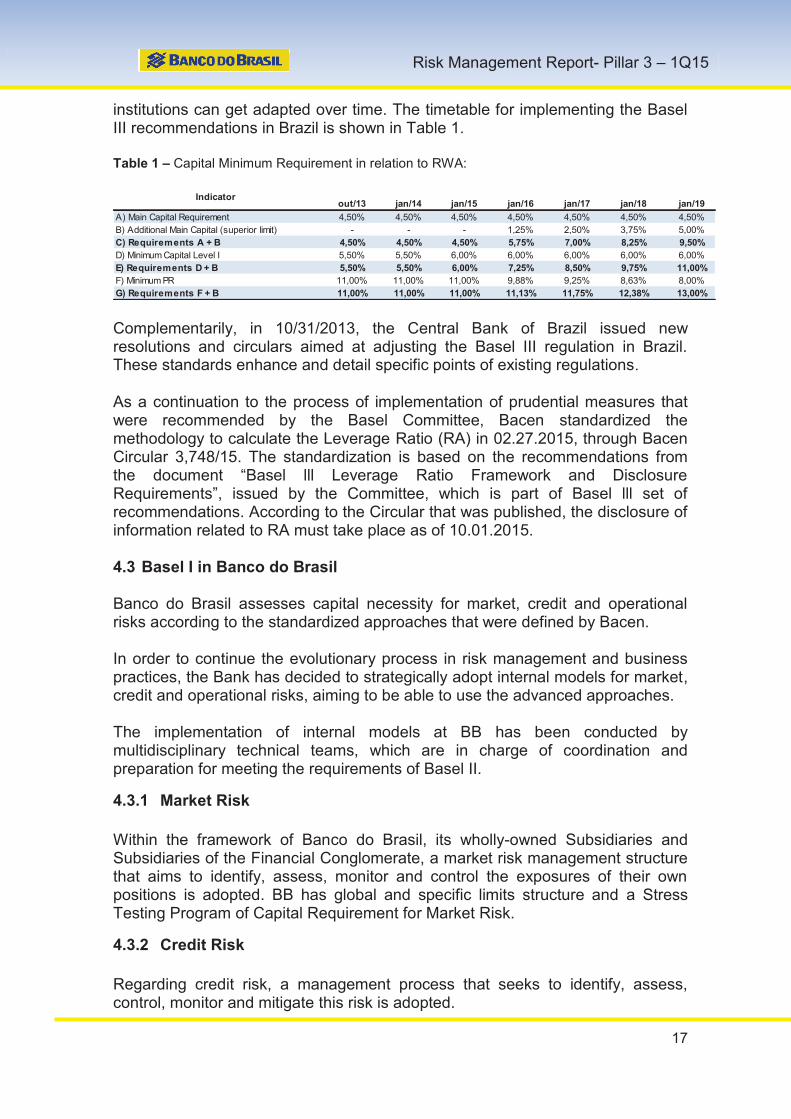

institutions can get adapted over time. The timetable for implementing the Basel III recommendations in Brazil is shown in Table 1.

Table 1 – Capital Minimum Requirement in relation to RWA:

Complementarily, in 10/31/2013, the Central Bank of Brazil issued new resolutions and circulars aimed at adjusting the Basel III regulation in Brazil. These standards enhance and detail specific points of existing regulations.

As a continuation to the process of implementation of prudential measures that were recommended by the Basel Committee, Bacen standardized the methodology to calculate the Leverage Ratio (RA) in 02.27.2015, through Bacen Circular 3,748/15. The standardization is based on the recommendations from the document “Basel lll Leverage Ratio Framework and Disclosure Requirements”, issued by the Committee, which is part of Basel lll set of recommendations. According to the Circular that was published, the disclosure of information related to RA must take place as of 10.01.2015. 4.3 Basel I in Banco do Brasil

Banco do Brasil assesses capital necessity for market, credit and operational risks according to the standardized approaches that were defined by Bacen. In order to continue the evolutionary process in risk management and business practices, the Bank has decided to strategically adopt internal models for market, credit and operational risks, aiming to be able to use the advanced approaches. The implementation of internal models at BB has been conducted by multidisciplinary technical teams, which are in charge of coordination and preparation for meeting the requirements of Basel II.

4.3.1 Market Risk

Within the framework of Banco do Brasil, its wholly-owned Subsidiaries and Subsidiaries of the Financial Conglomerate, a market risk management structure that aims to identify, assess, monitor and control the exposures of their own positions is adopted. BB has global and specific limits structure and a Stress Testing Program of Capital Requirement for Market Risk.

4.3.2 Credit Risk

Regarding credit risk, a management process that seeks to identify, assess, control, monitor and mitigate this risk is adopted.

out/13 jan/14 jan/15 jan/16 jan/17 jan/18 jan/19

A) Main Capital Requirement 4,50% 4,50% 4,50% 4,50% 4,50% 4,50% 4,50%B) Additional Main Capital (superior limit) - - - 1,25% 2,50% 3,75% 5,00%C) Requirements A + B 4,50% 4,50% 4,50% 5,75% 7,00% 8,25% 9,50%

D) Minimum Capital Level I 5,50% 5,50% 6,00% 6,00% 6,00% 6,00% 6,00%E) Requirements D + B 5,50% 5,50% 6,00% 7,25% 8,50% 9,75% 11,00%

F) Minimum PR 11,00% 11,00% 11,00% 9,88% 9,25% 8,63% 8,00%G) Requirements F + B 11,00% 11,00% 11,00% 11,13% 11,75% 12,38% 13,00%

Indicator

18

Risk Management Report- Pillar 3 – 1Q15

BB uses proprietary methodologies to rate clients` risks. Developed according to best market practices, these models (credit score and behavior score) consider both aspects, as registration and historical use of banking products and customer credit with the Bank and the market. Bacen Circular 3,648/13, which dates back to 03.04.2013, establishes minimum requirements for the use of internal ratings based on Basel II approach for credit risk. At the Bank, implementation of the approach is driven by strategic project with the responsibility to build databases, develop models of risk parameters and validation processes, ensuring integration with the management and documentation. The Bank is carrying out the construction of models of risk parameters (probability of default, exposure at the time of default, loss given default and effective maturity) and review of risk mitigators provided in Basel ll.

In order to support the process of managing credit risk, BB has also made significant investments in solutions for information technology (TI), and the new tools have already been installed.

4.3.3 Operational Risk

The Bank has an operational risk management structure that is responsible for prospecting and developing the operational risk management policies and strategies. The management process aims to identify, assess, control, monitor and mitigate the operational risk, which promotes a more effective management and the culture dissemination.

The Bank has a methodology that allows managers to identify operational risks associated to processes under his responsibility, including the identification of the occurrence of faults/inadequacies, assessing the possibility of loss, identification of risk factors, identification of operational risks and their classification. The development of strategies and management instruments are also highlighted, aiming to mitigate the operational risk, which contributes for the continuity and solidity of the organization, among which the operational risk assessment in the Entities Linked to Banco do Brasil S/A is considered; the definition of operational loss limits binding the processes managers, products and services; the verification of the products managerial result considering the operational loss; the implantation of improvements for mitigating external thefts; and the improvement of actions for mitigating electronic fraud losses. Those measures are intended mainly to reduce and prevent events that generate operating loss, besides strengthening the operational risk structure of the Bank.

19

Risk Management Report- Pillar 3 – 1Q15

5. Prudential Conglomerate

The CMN Resolution 4,192, published on 03.01.2013, in its 3rd article, item ll, establishes that, as of 01.01.2014, the calculation of Reference Equity must be made in consolidated bases for institutions that are part of the Prudential Conglomerate. In addition, on 03.01.2013, the CMN Resolution 4,195 was published and it is about the elaboration of Analytical Balance Sheet - Prudential Conglomerate. According to the 1st article of the CMN Resolution 4,195, the financial institutions and other institutions authorized to work by Bacen, except for credit cooperatives, must elaborate the Analytical Balance Sheet in a consolidated way, including data relevant to the entities described as follows, located in Brazil and abroad, on which the Bank has a direct or indirect control:

I. Financial institutions; II. Other institutions authorized to work by Bacen;

III. Consortium managing Companies; IV. Payment institutions that issue or accredit credit cards; V. Societies that acquire credit operations, including real estate loan, or

credit rights like leasing companies, securities companies and corporations of an exclusive object;

VI. Securities, capitalization and reinsurance societies, as well as complementary pension fund entities;

VII. Investment funds in which the entities that are part of the conglomerate, under any form, undertake or substantially have risks and benefits, such as exclusive investment funds, credit rights investment funds and financial investment funds, and

VIII. Other corporate bodies located in Brazil that have a societal participation in the entities quoted in the items I through VI.

The shareholding in which there is a shared control must also be consolidated (proportionally to the participation held by the institution), according to the 3rd article of the CMN Resolution 4,195. 5.1 Balance Sheets

As follows, there is the composition of the Prudential Balance Sheet compared to the Balance Sheet disclosed in the Consolidated Financial Statements, as well as the reference values in the "Attachment 1 - Composition of the Reference Equity".

20

Risk Management Report- Pillar 3 – 1Q15

Table 2 - Prudential Balance Sheet x Consolidated Balance Sheet:

In tho usands o f R eaisR eference in R E P rudential

Eco no mic and

F inancial

A SSET S

C urrent assets and lo ng-term receivables 1,334,170,745 1,501,811,020

C ash and C ash Equivalents 16,158,473 16,536,604

Sho rt- term Interbank Investments 349,471,489 351,658,176

Open market investments 309,058,044 310,652,775

Interbank deposits 40,413,445 41,005,401

Securit ies and D erivat ive F inancial Instruments 113,020,231 235,999,192

Own portfo lio 81,516,310 198,596,900

Funding instruments issued by institution authorized by Banco Central do Brasil ( t ) 18,020 --

Other 81,498,290 --

Subject to repurchase agreements 14,148,545 17,291,266

P ledged in guarantee 14,672,255 16,404,689

Derivative financial instruments 2,683,121 3,754,490

(A llowance for securities losses) -- (48,153)

Interbank acco unts 64,452,659 64,485,914

Payments and receipts pending settlement 3,719,204 3,719,278

Restricted deposits 59,245,252 59,266,005

Banco Central do Brasil deposits 56,612,772 56,633,525

National Treasury - rural credits resources 268,651 268,651

National Housing Finance System 2,363,829 2,363,829

Interbank onlendings 283,403 295,544

Correspondent banks 1,204,800 1,205,087

Interdepartmental A cco unts 196,501 196,501

Internal transfers of funds 196,501 196,501

Lo an Operat io ns 606,367,071 630,530,018

Public sector 39,262,782 66,992,715

Private sector 592,844,412 590,955,810

Loan operations linked to assignment 306,873 306,873

(A llowance for loan pperations) (26,046,996) (27,725,380)

Lease T ransact io ns 336,044 1,012,162

Private sector 647,241 1,054,153

(Unearned income on leasinf transactions) (282,986) --

(A llowance for leasing transactions losses) (28,211) (41,991)

Other R eceivables 183,586,425 197,641,607

Receivables from guarantees honored 202,339 522,197

Foreign exchange portfo lio 20,273,324 21,195,789

Receivables 1,940,048 3,008,124

Securities trading 1,298,541 1,415,617

Specific credits 1,591,775 1,591,775

Insurance, pension plans and capitalization -- 5,389,705

Sundry 160,049,845 166,723,444

Tax credits 28,396,867 --

Resulting from tax losses and negative basis of social contribution on net income (g) 1,427,850 --

Resulting from temporary differences 26,969,017 --

Excess of 10% from Core Capital ( j 1 ) 3,280,709 --

Excess of 15% from Core Capital ( l) 558,709 --

Tax credits resulting from temporary differences not deducted from RE (v) 6,513,057 --

Tax credits resulting from temporary differences for loan losses 16,616,542 --

Actuarial assets related to defined benefit pension funds (h 1 ) 6,499,810 --

Other 125,153,168 --

(A llowance for o ther losses) (1,769,447) (2,205,044)

Other A ssets 581,852 3 ,750,846

Assets not for own use and stock materials 323,776 662,827

(A llowance for impairment) (127,047) (147,038)

Prepaid expenses 385,123 3,235,057

1Q15

21

Risk Management Report- Pillar 3 – 1Q15

P ER M A N EN T A SSET S 35,728,904 21,854,684

Investments 17,435,643 3 ,584,912

Investments in subsidiaries and associated companies 17,226,756 1,807,311

Domestic 16,718,464 1,138,384

Goodwill (e 1 ) 784,708 --

Investments 15,933,756 --

Investments in insurance companies 4,286,469 --

Excess of 15% from Core Capital (k) 338,654 --

Investments not deducted from RE (u) 3,947,815 --

Other Investments 11,647,287 --

Funding instruments issued by institution authorized for Banco Central do Brasil (n) 3,804,661 --

Other 7,842,626 --

Abroad 508,292 668,927

Goodwill (e 2 ) 60,500 --

Other 447,792 --

Other investments 263,182 1,873,349

(Accumulated impairment) (54,295) (95,748)

P ro perty, plant and equipment 7,208,795 7 ,504,117

Land and buildings 6,252,619 6,476,557

Revaluation of land and buildings 144,716 --

Other property, plant and equipment 9,277,341 9,915,844

(Accumulated depreciation) (8,465,881) (8,888,284)

Leased assets ( 1 ) 819,559 - -

Leased assets 931,200 --

(Accumulated depreciation) (111,641) --

Intangible 10,239,221 10,728,629

Intangible assets 17,156,363 17,826,391

Goodwill (e 3 ) 4,961,028 --

Other Intangible assets 12,195,335 --

Constituded from October 1, 2013 ( f 1 ) 6,051,268 --

Constituded before October 1, 2013 ( f 2 ) (o 1 ) 6,144,067 --

(Accumulated amortization) (6,917,142) (7,097,762)

Goodwill Amortization (e 4 ) (2,447,597) --

Other Amortization (4,469,545) --

Intangible assets amortization constituded from October 1, 2013 ( f 3 ) (930,682) --

Intangible assets amortization constituded before October 1, 2013 ( f 4 ) (o 2 ) (3,538,863) --

D eferred 25,686 37,026

Organization and expansion costs (m 1 ) 1,605,810 1,630,006

(Accumulated amortization) (m 2 ) (1,580,124) (1,592,980)

T OT A L A SSET S 1,369,899,649 1,523,665,704 (1) Leasing transact ions were considered based on the f inancial method, and the amounts were reclassif ied from the heading of leased assets to the heading of leasing transact ions, after deduct ion of residual amounts received inadvance.

22

Risk Management Report- Pillar 3 – 1Q15

In tho usands o f R eaisR eference in R E P rudential

Eco no mic and

F inancial

LIA B ILIT IES

C urrent liabilit ies and lo ng-term liabilit ies 1,288,063,367 1,439,633,857

D epo sits 466,404,678 468,005,995

Demand deposits 73,685,265 73,712,090

Savings deposits 144,089,086 144,089,086

Interbank deposits 36,736,128 37,554,005

Time deposits 211,894,199 212,650,814

Securit ies so ld under repurchase agreements 331,549,202 338,906,729

Own portfo lio 46,605,230 54,503,543

Third-party portfo lio 284,943,972 284,059,645

Free movement portfo lio -- 343,541

F unds fro m A cceptance and Issuance o f Securit ies 170,172,264 183,328,583

Funds from real state, mortgage, credit and similar bonds 139,952,996 148,531,086

Funds from debentures 970,022 99

Foreign securities 29,241,111 34,773,173

Certificates of structured operations 8,135 24,225

Interbank acco unts 2,774,239 2 ,774,586

Receipts and payments pending settlement 2,753,421 2,753,768

Correspondent banks 20,818 20,818

Interdepartmental A cco unts 4,118,051 4 ,206,078

Thrid-party funds in transit 4,111,162 4,197,215

Internal transfers of funds 6,889 8,863

B o rro wings 27,791,273 29,156,933

Domestic loans - o ther institutions 1,413,180 1,872,457

Foreign borrowing 26,378,093 27,284,476

D o mestic Onlending - Off ic ial Inst itut io ns 90,686,029 92,614,783

National Treasury 296,690 344,720

BNDES 42,263,854 43,247,174

Caixa Econômica Federal 14,232,878 14,232,878

Finame 33,175,438 34,072,842

Other institutions 717,169 717,169

F o reign Onlending 477 477

Foreign Onlending 477 477

D erivat ive F inancial Instruments 4,301,519 5 ,632,137

Derivative Financial Instruments 4,301,519 5,632,137

Other Liabilit ies 190,265,635 315,007,556

Billing and co llection of taxes and contributions 4,412,615 4,508,918

Foreign exchange portfo lio 17,244,226 17,785,981

Shareholders and statutory distributions 2,137,341 2,159,810

Taxes and social security 18,605,150 24,819,821

Provision for deferred tax liabilities ansing from positive adjustments of benefit pension funds (h 2 ) 324,021 --

Provision for deferred tax liabilities ansing from tax credits ( j 2 ) 1,731,772 --

Other 16,549,357 --

Securities trading 1,038,613 940,540

Technical provisions for insurance, pension plans and capitalization -- 108,981,702

Financial and development funds 12,264,779 12,264,779

Special operations 2,158 2,158

Subordinated debts 49,664,241 52,809,400

In accordance with the CM N Resolution No.4,192/2013 as Tier II 21,075,691 --

In accordance with regulations preceding the CM N Resolution No.4,192/2013 as Tier II (s) (x) 22,600,521 --

Other Subordinated debts 5,988,029 --

Equity and debt hybrid securities 6,268,723 6,268,723

In accordance with regulations preceding the CM N Resolution No.4,192/2013 as Capital M anagement (q) (w) 4,650,730 --

Other 1,617,993 --

Debt instruments eligible as capital 24,776,310 25,001,325

Instruments eligible as capital M anagement (p) 19,484,955 --

Instruments eligible as Tier II ( r) 5,291,355 --

Other liabilities 53,851,479 59,464,399

D EF ER R ED IN C OM E 420,635 433,808

Shareho lder's Equity 81,415,647 83,598,039

C apital (a 1 ) 54,000,000 54,000,000

Local residents 42,971,511 42,971,511

Domiciled abroad 11,028,489 11,028,489

Instrument Qualifying as C ET 1 (a 2 ) 8 ,100,000 8 ,100,000

C apital R eserves (c 1 ) 13,992 13,992

R evaluat io n R eserves (c 2 ) 2 ,788 2 ,788

P ro f it R eserves (b 1 ) 30,015,198 25,393,416

A ccumulated Other C o mprehensive Inco me (c 3 ) (10,174,852) (10,174,852)

R etained earnings/ accumulated lo sses (b 2 ) 2 ,054 4 ,623,836

(T reasury Shares) ( i) (1,629,765) (1,629,765)

N o nco ntro lling Interests (d) 1,086,232 3 ,268,624

T OT A L LIA B ILIT IES 1,369,899,649 1,523,665,704

1Q15

23

Risk Management Report- Pillar 3 – 1Q15

5.2 Composition of the Prudential Conglomerate

The institutions included in the prudential balance sheet consolidation scope are in the table as follows, segregated by business segments:

Table 3 - Composition of the Prudential Conglomerate

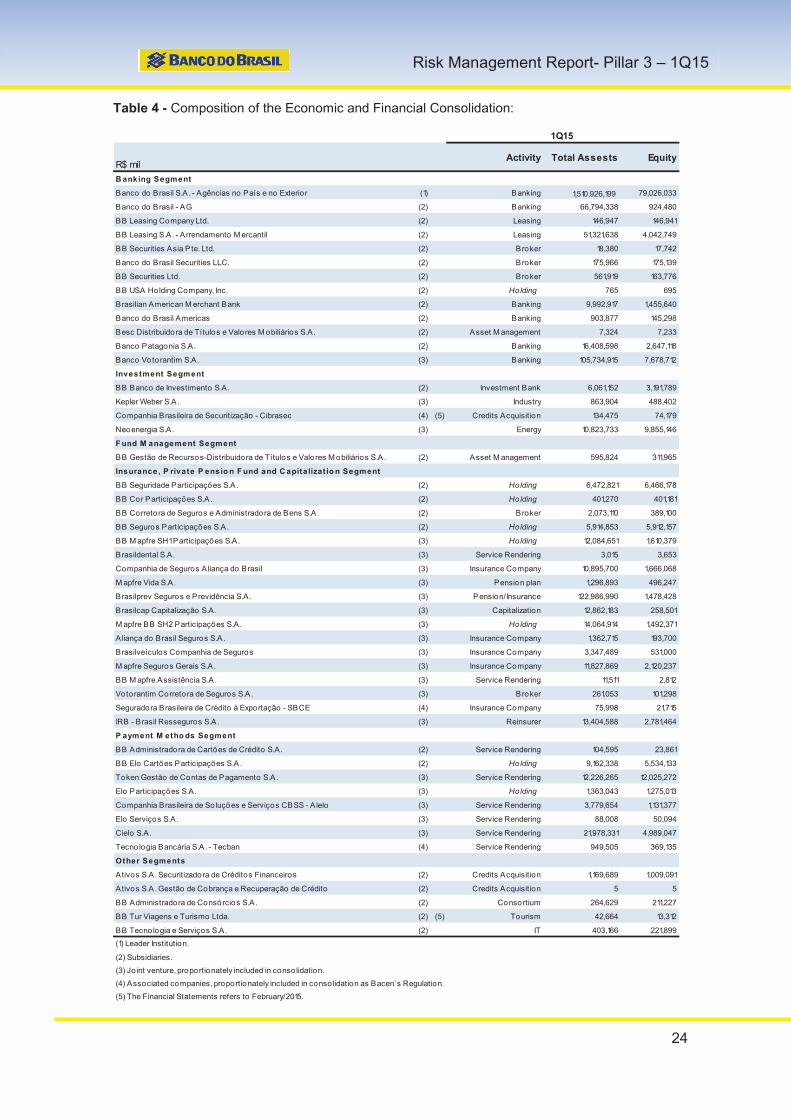

5.3 Composition of the Economic and Financial Consolidation As follows, the institutions included in the scope of consolidation of the economic financial consolidation, segregated by business segments, are shown:

R$ milActivity Total Assests Equity

F inancial Inst itut io ns

Banco do Brasil S.A. - Agências no País e no Exterior (1) Banking 1,510,926,199 79,026,033

Banco do Brasil - AG (2) Banking 66,794,338 924,480

BB Leasing Company Ltd. (2) Leasing 146,947 146,941

BB Leasing S.A. - Arrendamento M ercantil (2) Leasing 51,321,638 4,042,749

BB Securities Asia Pte. Ltd. (2) Broker 18,380 17,742

Banco do Brasil Securities LLC. (2) Broker 175,966 175,139

BB Securities Ltd. (2) Broker 561,919 163,776

BB USA Holding Company, Inc. (2) Holding 765 695

Brasilian American M erchant Bank (2) Banking 9,992,917 1,455,640

Banco do Brasil Americas (2) Banking 903,877 145,298

Besc Distribuidora de Títulos e Valores M obiliários S.A. (2) Asset M anagement 7,324 7,233

Banco Patagonia S.A. (2) Banking 16,408,598 2,647,118

BB Banco de Investimento S.A. (2) Investment Bank 6,061,152 3,191,789 BB Gestão de Recursos-Distribuidora de Títulos e Valores M obiliários S.A.

(2) Asset M anagement 595,824 311,965

C o nso rt ium M anager

BB Administradora de Consórcios S.A. (2) Consortium 264,629 211,227

P ayment Inst itut io ns

BB Administradora de Cartões de Crédito S.A. (2) Service Rendering 104,595 23,861

Companhia Brasileira de Soluções e Serviços CBSS - Alelo (3) Service Rendering 3,779,654 1,131,377

Cielo S.A. (3) Service Rendering 21,978,331 4,989,047

Securit izat io n C o mpanies

Ativos S.A. Securitizadora de Créditos Financeiros (2) Credits Acquisition 1,169,689 1,009,091

Companhia Brasileira de Securitização - Cibrasec (4) Credits Acquisition 134,475 74,179

(4) Associated company proportionately included in consolidation, as Bacen’s Regulation.

1Q15

(1) Leader Institution.

(2) Subsidiaries.

(3) Jo int ventures, proportionately included in consolidation.

24

Risk Management Report- Pillar 3 – 1Q15

Table 4 - Composition of the Economic and Financial Consolidation:

R$ milActivity Total Assests Equity

B anking Segment

Banco do Brasil S.A. - Agências no País e no Exterior (1) Banking 1,510,926,199 79,026,033

Banco do Brasil - AG (2) Banking 66,794,338 924,480

BB Leasing Company Ltd. (2) Leasing 146,947 146,941

BB Leasing S.A. - Arrendamento M ercantil (2) Leasing 51,321,638 4,042,749

BB Securities Asia Pte. Ltd. (2) Broker 18,380 17,742

Banco do Brasil Securities LLC. (2) Broker 175,966 175,139

BB Securities Ltd. (2) Broker 561,919 163,776

BB USA Holding Company, Inc. (2) Holding 765 695

Brasilian American M erchant Bank (2) Banking 9,992,917 1,455,640

Banco do Brasil Americas (2) Banking 903,877 145,298

Besc Distribuidora de Títulos e Valores M obiliários S.A. (2) Asset M anagement 7,324 7,233

Banco Patagonia S.A. (2) Banking 16,408,598 2,647,118

Banco Votorantim S.A. (3) Banking 105,734,915 7,678,712

Investment Segment

BB Banco de Investimento S.A. (2) Investment Bank 6,061,152 3,191,789

Kepler Weber S.A. (3) Industry 863,904 488,402

Companhia Brasileira de Securitização - Cibrasec (4) (5) Credits Acquisition 134,475 74,179

Neoenergia S.A. (3) Energy 10,823,733 9,855,146

F und M anagement Segment

BB Gestão de Recursos-Distribuidora de Títulos e Valores M obiliários S.A. (2) Asset M anagement 595,824 311,965

Insurance, P rivate P ensio n F und and C apitalizat io n Segment

BB Seguridade Participações S.A. (2) Holding 6,472,821 6,466,178

BB Cor Participações S.A. (2) Holding 401,270 401,181

BB Corretora de Seguros e Administradora de Bens S.A. (2) Broker 2,073,110 389,100

BB Seguros Participações S.A. (2) Holding 5,914,853 5,912,157

BB M apfre SH1 Participações S.A. (3) Holding 12,084,651 1,610,379

Brasildental S.A. (3) Service Rendering 3,015 3,653

Companhia de Seguros Aliança do Brasil (3) Insurance Company 10,895,700 1,666,068

M apfre Vida S.A. (3) Pension plan 1,296,893 496,247

Brasilprev Seguros e Previdência S.A. (3) Pension/Insurance 122,986,990 1,478,428

Brasilcap Capitalização S.A. (3) Capitalization 12,862,183 258,501

M apfre BB SH2 Participações S.A. (3) Holding 14,064,914 1,492,371

Aliança do Brasil Seguros S.A. (3) Insurance Company 1,362,715 193,700

Brasilveículos Companhia de Seguros (3) Insurance Company 3,347,489 531,000

M apfre Seguros Gerais S.A. (3) Insurance Company 11,827,869 2,120,237

BB M apfre Assistência S.A. (3) Service Rendering 11,511 2,812

Votorantim Corretora de Seguros S.A. (3) Broker 261,053 101,298

Seguradora Brasileira de Crédito à Exportação - SBCE (4) Insurance Company 75,998 21,715

IRB - Brasil Resseguros S.A. (3) Reinsurer 13,404,588 2,781,464

P ayment M etho ds Segment

BB Administradora de Cartões de Crédito S.A. (2) Service Rendering 104,595 23,861

BB Elo Cartões Participações S.A. (2) Holding 9,162,338 5,534,133

Token Gestão de Contas de Pagamento S.A. (3) Service Rendering 12,226,265 12,025,272

Elo Participações S.A. (3) Holding 1,363,043 1,275,013

Companhia Brasileira de Soluções e Serviços CBSS - A lelo (3) Service Rendering 3,779,654 1,131,377

Elo Serviços S.A. (3) Service Rendering 88,008 50,094

Cielo S.A. (3) Service Rendering 21,978,331 4,989,047

Tecnologia Bancária S.A. - Tecban (4) Service Rendering 949,505 369,135

Other Segments

Ativos S.A. Securitizadora de Créditos Financeiros (2) Credits Acquisition 1,169,689 1,009,091

Ativos S.A. Gestão de Cobrança e Recuperação de Crédito (2) Credits Acquisition 5 5

BB Administradora de Consórcios S.A. (2) Consortium 264,629 211,227

BB Tur Viagens e Turismo Ltda. (2) (5) Tourism 42,664 13,312

BB Tecnologia e Serviços S.A. (2) IT 403,166 221,899

(2) Subsidiaries.

(3) Jo int venture, proportionately included in consolidation.

(4) Associated companies, proportionately included in consolidation as Bacen’s Regulation.

(5) The Financial Statements refers to February/2015.

(1) Leader Institution.

1Q15

25

Risk Management Report- Pillar 3 – 1Q15

6. Risk Management

6.1 Credit Risk

6.1.1 Management Objectives

Banco do Brasil’s Prudential Conglomerate credit risk is managed according to best market practices and follows the banking supervision and regulatory rules. It seeks to identify, assess, control, and mitigate the risk exposures, monitor the management process, contribute to maintain the bank’s health and solvency, and ensure the interests of the shareholders. Credit risk management in the Conglomerate involves Credit Policy, risk appetite and tolerance, strategies, processes, procedures and credit risk management systems, as the figure below:

Figure 6 – Credit risk management

Note: CA = Board of Directors; CSRG = Global Risk Superior Committee; CERC = Credit Risk Executive Committee; DICRE = Credit Board; DIRAO = Asset Restructuring Board; DIRIS = Risk Management Board, URO = Operational Risk Unit.

Management Structure

Operational Procedures

Management Systems

CA

CSRG

CERC

Strategic Level

DICRE

DIRAO

DIRIS

Operational Level

26

Risk Management Report- Pillar 3 – 1Q15

Board of Directors (CA) Banco do Brasil S.A Board of Directors (CA) defines the Bank and its subsidiaries general business. The Board has, in the manner provided by law and the Statute, strategic, guiding, elective and monitoring assignments, not covering operating and executive functions. The composition and management term of the Council is defined by the Bank's bylaws. The Board of Directors shall decide on policies, corporate strategy, investment plan, master plan and the Bank’s general budget. Global Risk Superior Committee – CSRG

Purposes: · to set credit risk management strategy; · to determine global limits to credit risk exposure; · to approve the risk factors that will make up the documents and reports

to be submitted to regulatory agencies and other institutions; · to approve methodologies, criteria and parameters for calculation of

provisions for contingent claims;

Credit Risk Executive Committee– CERC Purposes: To approve:

· the implementation of actions that enable the loan portfolio management; · the loans portfolio risk mitigatory actions and instruments; · contingency plans regarding credit and social and environmental risk

management; · specific limits to credit risk exposures; · models, methodologies, criteria and parameters for credit risk

management; the process of collecting and recovering debts; · to assess the internal validations result and define, whenever necessary,

corrective measures for models of credit risk management;

To analyse and propose to CSRG the:

· credit risk management strategy; · global limits to credit risk exposures;

To monitor the:

· measures implemented to mitigate the risk in the loan portfolio management;

· development of Allowance for Loan and Lease Losses (ALLL), submitting it to the attention of CSRG;

· recommendations and guidelines resolved by the Committee.

27

Risk Management Report- Pillar 3 – 1Q15

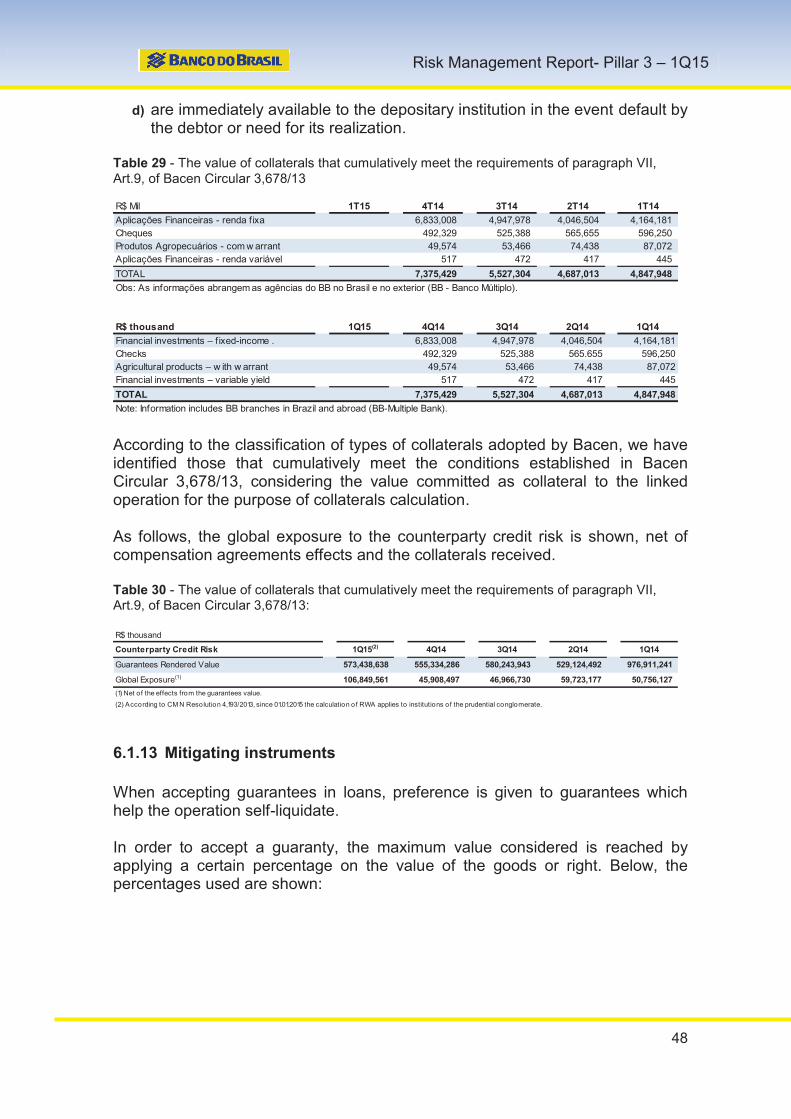

In accordance with CMN Decision 3,721/09, the credit risk management structure of Banco do Brasil was approed, composed by Global Risk Superior Committee (CSRG), Credit Risk Executive Committee (CERC), Credit Board (DICRE), Operational Asset Restructuring Board (DIRAO), Risk Management Board (DIRIS) and Operational Risk Unit (URO). That credit risk management structure is compatible with the nature of transactions, the complexity of products and services, and in proportion to the size of the credit-risk exposure incurred by Banco do Brasil. As Diris is the unit of the Bank that is in charge of overall risk management and does not have any ties with the management of third-party resources administration or with the fulfillment of transactions subject to credit risk, the CA pointed out the Director of the Risk Management Board as responsible for BB’s credit risk management before Bacen. 6.1.2 Credit Policy

Banco do Brasil’s credit policy contains strategic guidelines to direct credit-risk management actions in the financial conglomerate. It is approved by the Board of Directors and reviewed every year. It applies to all businesses that involve credit risk and is available to all employees. It is expected that the Subsidiaries, Affiliates and Investment companies define their paths from these guidelines, taking into account the specific needs and legal and regulatory issues to which they are subject. The credit policy is divided into four blocks: General Aspects, Credit Risk taking, Collections and Credit Recovery, and Credit Risk Management. Each block contains a comprehensive set of statements which encompasses all stages of credit-risk management at Banco do Brasil. Some topics addressed in Banco do Brasil’s credit policy are listed below:

· concept of credit risk; · conditions for risk taking;

· separation of duties; · guidelines for collections and credit recovery;

· joint decisions; · capital planning · risk appetite; · allowance and capital levels; · risk limits; · stress tests. · client rating;

6.1.3 Management Strategies

Aligned with the objectives of credit risk management, the Board of Directors (CA) establishes the credit policy and the risk appetite of Banco do Brasil and approves management strategies, which are defined by the Global Risk Superior Committee (CSRG) and operationalized by the Credit Risk Executive Committee (CERC).

28

Risk Management Report- Pillar 3 – 1Q15

The credit-risk management strategies, described below, aim to guide the actions in the operational level, comprising: · approving credit risk management models; · setting goals for timely payment, recovery, maximum loss, and quality of the

loan portfolio; · setting risk and concentration limits; and · keeping appropriate levels of allowances and capital.

6.1.4 Management Processes

According to Banco do Brasil’s credit risk management structure, the Credit (DICRE), Operational Asset Restructuring (DIRAO) and Risk Management (DIRIS) Boards are responsible for implementing strategic decisions approved by the CA, CSRG and CERC, keeping exposure in the risk levels set by the Executive Management. DICRE focuses on clients and operations, whose main products are: registration, marketing studies and information on economic sectors, methodologies (risk, risk components, and credit limits), risk analysis (clients, operations, projects, economic sectors, countries, and projects), validation and monitoring of risk methodology and credit-risk components, study of investment and leasing transactions, economic/financial evaluation and diagnosis of businesses/corporate groups, monitoring the credit portfolio, and producing inputs for pricing credit risk. DIRAO operates in collecting, and recovering troublesome credits, whose main products are: models to rate clients under collections and recovery, collection and recovery strategies, recovery quality indicators, management of collections and recovery channels, debt rescheduling, restructuring transactions, setting negotiating floors and methodologies for dealing with troublesome credits or defaults. DIRIS focuses on managing the credit risk of aggregate positions, whose main products are: policies, risk limits, credit risk models, information on credit risk, indicators of credit portfolio quality, capital allocation as a function of risk, management of the credit portfolio’s risk, controlling of credit risk exposure and stress testing.

29

Risk Management Report- Pillar 3 – 1Q15

Figure 7 summarizes the responsibilities of the Boards:

Figure 7 - Credit risk management structure

The processes and procedures of the credit risk management structure are validated and performed by two internal units at different points in time, a fact that ensures the adequate separation of duties and the independence of work. The Internal Control Board (DICOI) is responsible for validating the financial conglomerate’s risk determination and measurement models and the bank’s internal control system. Internal Audit (AUDIT) periodically evaluates credit risk management processes to verify whether they are consistent with the strategic guidelines, credit policy, and regulatory and internal rules. 6.1.5 Communication and Information Processes

The disclosure of credit risk information is a continual and ongoing process whose premises considered when selecting and disclosing information include best practices, banking laws, users` needs, the bank’s interests, confidentiality, and the relevance of the information. The communication and information on credit risk management is provided to internal and external clients, according to the following processes: 6.1.5.1 Communication process for internal clients

The operational units of the credit risk management structure permanently communicate risk exposure to upper management in order to monitor management actions and decision-making by the Senior Management.

30

Risk Management Report- Pillar 3 – 1Q15

The communication process involves several reports on credit risk management, which are produced periodically and are the result of analysis conducted by professionals from the units. They demonstrate the credit risk of all exposures or in certain portfolios, such as:

a) Presentation of the Bank’s credit portfolio X National Financial System; b) Comparative BB credit portfolio x main competitors; c) Credit Risk Panel; and d) Stress testing.

6.1.5.2 Communication process for external clients

The operational units of the credit risk management structure produce information for external users and send it to the Investor Relations Unit (URI) that, as a practice of transparency, discloses the information to the market, as a transparent governance practice. That allows investors and interested parties to monitor risk-management actions and the evolution of credit risk, and to prove the Bank’s capital adequacy to cover all risks taken. Information for external users is provided on a publicly accessible location, easily found on the bank’s website. The information is published in the following documents: · Performance Analysis Report; · Explanatory Notes to Financial Statements; and · Annual Report.

6.1.6 Measurement Systems

Credit risk is measured in many ways: by default, arrears, portfolio quality, and allowance for doubtful accounts, concentration, and regulatory capital requirements, among others. The quantity and nature of the operations, the diversity and complexity of our products and services, and the volume exposed to credit risk require systematic measurement of credit risk at Banco do Brasil. The Bank has enough databases and corporate system infrastructure to ensure comprehensive measurement of credit risk. Some of these risk measures are highlighted below. 6.1.6.1 Concentration

The Bank has developed and implemented a system to measure and monitor credit risk concentration in businesses. The model is based on the Herfindahl Index. It evaluates concentration based on borrowers` credit risk, and it considers the interrelationship among the various economic sectors that comprise the businesses credit portfolio. 6.1.6.2 Regulatory Capital Requirement

The Bank measures the Regulatory Capital requirement for credit risk through Regulatory Simplified Standardized Approach, whose procedures for calculating

31

Risk Management Report- Pillar 3 – 1Q15

the potion of risk-weighted assets (RWA) regarding exposure to credit risk (RWACPAD) were released by the Bacen through Circular 3,644/13. Those procedures were implemented in a proprietary system that determines the capital requirements quickly and securely, allowing timely verification of the bank’s solvency under the regulator’s rules. The Bank uses Regulatory Capital information to assess the efficiency of capital allocation and planning. 6.1.7 Mitigation Policy

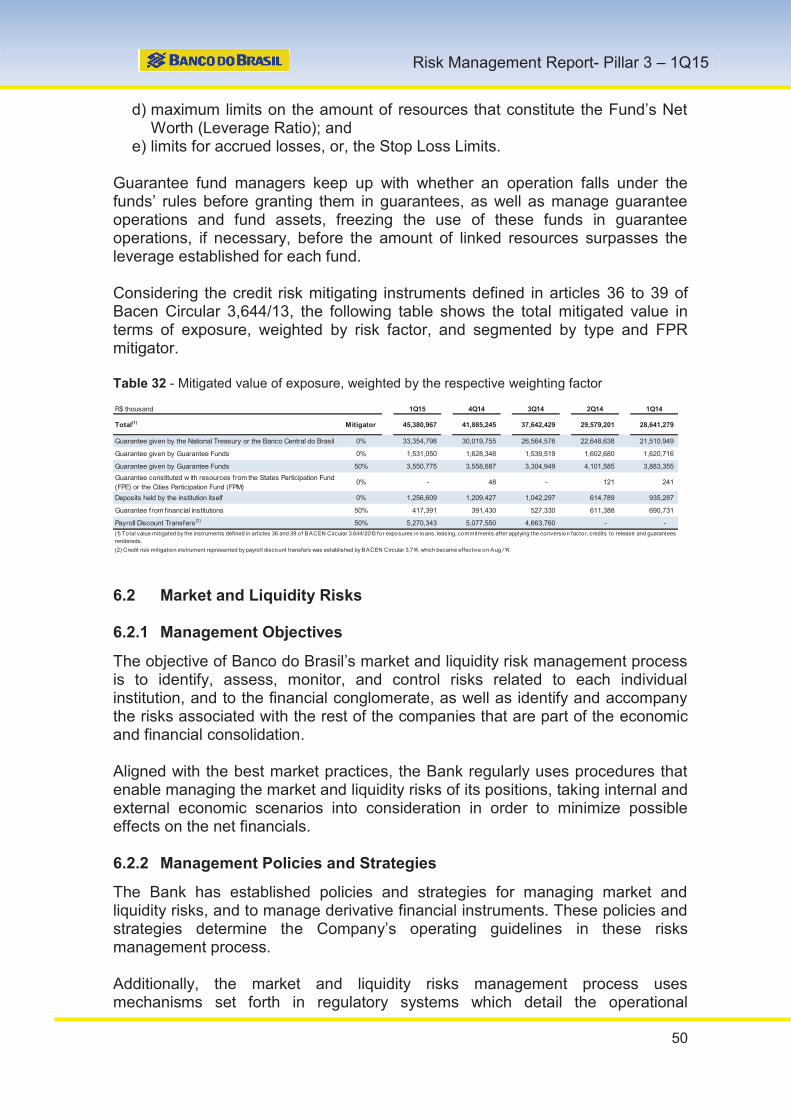

Banco do Brasil adopts a conservative attitude towards credit risk. In conducting any business subject to credit risk, the bank’s general rule is to tie it to a mechanism that provides partial or complete hedging of risk incurred. In managing credit risk on the aggregate level, to keep exposure within the risk levels established by the Senior Management, the Bank has the prerogative to transfer or to share credit risk. The use of credit risk mitigating instruments is stated in the Credit Policy, present in strategic decisions, and formalized in credit rules, reaching all levels of the organization and covering all stages of credit risk management. Credit rules provide clear, comprehensive guidelines for the operational units. Among other aspects, the rules address ratings, requirements, choices, assessments, formalization, control, and reinforcement of guarantees, ensuring the adequacy and sufficiency of the mitigator throughout the transaction cycle.

6.1.8 Processes for Monitoring the Effectiveness of Mitigators

Monitoring the effectiveness of mitigators is part of the Bank’s credit risk management processes. We quote, as an example, monitoring exposures subject to credit risk, the risk ratings of loans, capital management, and credit collection and recovery. The processes of monitoring credit risk exposure and rating loans risks produce important information for verifying the effectiveness of mitigating instruments. The low default ratio in certain segments of the credit portfolio and the lowest level of allowances in certain transactions may mean that the existence of guarantees tied to exposure reducing credit risk and capital requirements for its coverage. 6.1.9 Exposure to Credit Risk

The table below shows the concentration levels of the ten largest customers in relation to total transactions with credit granting feature.

32

Risk Management Report- Pillar 3 – 1Q15

Table 5 - Concentration of the ten and of the hundred largest customers in relation to the total of transactions with credit granting feature

The following table shows credit risk average exposure of individual portfolios (PF) and businesses (PJ):

Table 6 - Credit risk average exposure

The next table presents the credit risk exposure of the businesses portfolio (PJ), segregated by geographic regions in Brazil:

1st to 10th 1st ao 100th

1Q15 11.4% 25.7%

4Q14 10.2% 24.2%

3Q14 10.4% 24.3%

2Q14 9.6% 23.2%

1Q14 10.6% 23.8%

4Q13 10.7% 23.8%

3Q13 10.4% 23.4%

R$ million

Exposure Balance * Average Balance Balance * Average Balance Balance * Average Balance

Individuals

Agribusiness 119,912 39,971 119,414 39,805 112,543 37,514

Mortgage 30,539 10,180 28,645 9,548 25,863 8,621

Payroll Loan 59,863 19,954 58,843 19,614 61,364 20,455

Auto Loans 10,164 3,388 10,608 3,536 23,548 7,849

Credit Cards 67,624 22,541 67,311 22,437 65,504 21,835

Others 49,571 16,524 48,603 16,201 49,792 16,597

Total Individuals 337,674 112,558 333,424 111,141 338,614 112,871

Companies - -

Agribusiness 45,815 15,272 48,038 16,013 48,137 16,046

Investments 93,115 31,038 90,552 30,184 74,201 24,734

Import/Export. 16,530 5,510 16,505 5,502 15,531 5,177

Working Capital 234,454 78,151 229,541 76,514 222,814 74,271

Others 173,047 57,682 165,889 55,296 159,230 53,077

Total Companies 562,960 187,653 550,526 183,509 519,913 173,304

Total 900,634 300,211 883,950 294,650 858,526 286,175

* Includes BB internal portfolio and loans to concede

1Q15 4Q14 3Q14

33

Risk Management Report- Pillar 3 – 1Q15

Table 7 - PJ credit risk exposure by geographic regions

The table below presents the credit risk exposure of the individuals portfolio (PF), segregated by geographic regions in Brazil:

R$ million 1Q15

Region Agribusiness Investments Import/Export. Working Capital Others

Midw est 1,256 23,237 229 17,931 7,161 Northeast 296 4,849 231 17,846 10,465 North 139 3,913 56 6,883 2,555 Southeast 36,932 41,902 13,674 145,677 96,847 South 7,010 13,460 2,332 29,927 13,464 Foreign - 5,936 9 16,190 42,556 Total 45,633 93,297 16,530 234,454 173,047

R$ million 4Q14

Region Agribusiness Investments Import/Export. Working Capital Others

Midw est 1,559 22,600 257 17,960 7,050 Northeast 368 4,735 532 17,965 10,202 North 142 3,989 45 6,877 2,464 Southeast 38,349 40,707 13,249 142,074 96,339 South 7,600 13,376 2,413 30,873 12,992 Foreign - 5,166 9 13,792 36,843 Total 48,018 90,572 16,505 229,541 165,889

3Q14

Region Agribusiness Investments Import/Export. Working Capital Others

Midw est 1,507 9,368 274 13,791 6,472 Northeast 341 4,645 545 17,309 9,648 North 120 3,928 61 6,752 2,245 Southeast 39,381 38,802 12,293 140,750 92,936 South 7,635 13,016 2,357 30,829 12,696 Foreign - 4,443 1 13,383 34,386 Total 48,984 74,201 15,531 222,814 158,383

34

Risk Management Report- Pillar 3 – 1Q15

Table 8 - PF credit risk exposure by geographic regions

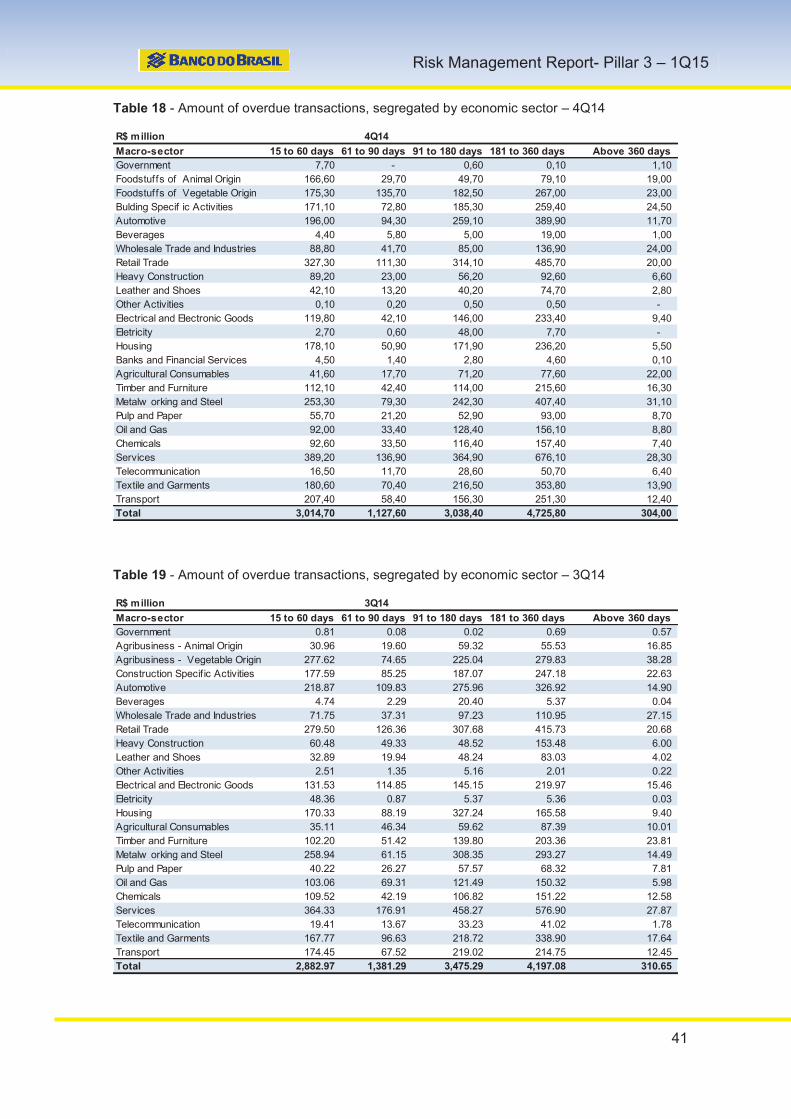

The next table shows the behavior of the total credit risk exposure, segregated by economic sector:

R$ million 1Q15

Region Agribusiness Mortgage Payroll Loans Auto Loans Credit Cards Others